recommendation on possible need for amendments … · recommendation on possible need for...

TRANSCRIPT

Recommendation on possible need for Amendments to the Insurance Groups Directive

1

CEIOPS-DOC-04/05

RReeccoommmmeennddaattiioonn

oonn ppoossssiibbllee nneeeedd ffoorr

AAmmeennddmmeennttss

ttoo tthhee IInnssuurraannccee GGrroouuppss DDiirreeccttiivvee

October 2005

CEIOPS e.V. - Sebastian-Kneipp-Str. 41 - 60439 Frankfurt – Germany – Tel. + 49 69-951119-20 – Fax. + 49 69-951119-19

email: [email protected]; Website: www.ceiops.org

Recommendation on possible need for Amendments to the Insurance Groups Directive

2

Content 1. Background .......................................................................................... 4 2. Executive Summary............................................................................... 4 3. Introduction ......................................................................................... 7 4. Current conduct of supplementary supervision .......................................... 9 5. Role of the Lead Supervisor .................................................................. 10

5.1 EU Directive provision ..................................................................... 10 5.2 Current Practices ............................................................................ 10 5.3 Problematic issues .......................................................................... 11 5.4 Possible solutions ........................................................................... 11

5.4.1 Reporting to CEIOPS on appointment of Lead Supervisors .............. 11 5.4.2 Aligning the approach with that of the FCD................................... 11

5.5 Recommendation of CEIOPS............................................................. 13 6. One holding company in the EEA in insurance groups whose head offices are located outside the EEA ........................................................................... 13

6.1 EU Directive provision ..................................................................... 13 6.2 Current practices............................................................................ 13 6.3 Problematic issues .......................................................................... 13 6.4 Possible solutions ........................................................................... 14 6.5 Recommendation of CEIOPS............................................................. 15

7. Solvency calculations at group level ....................................................... 15 7.1 Introduction................................................................................... 15 7.2 The scope of the calculation: current practices, problematic issues, possible solutions and recommendation of CEIOPS................................................ 19

7.2.1 Definition of the scope of the adjusted solvency calculation............. 19 7.2.2 Identification of the undertaking required to perform and submit the PUSC .............................................................................................. 21 7.2.3 Identification of the parent undertaking in relation to which the PUSC has to be performed.......................................................................... 23 7.2.4 Calculation of the PUSC for groups whose holding company is located outside EEA ..................................................................................... 25

7.3 Calculation methods in force throughout the EEA: current practices, problematic issues, possible solutions and recommendation of CEIOPS ........ 27

7.3.1 Possible deletion of Requirement Deduction Method from the IGD.... 27 7.3.2 Consistency of the Requirement Deduction Method under the IGD and the FCD........................................................................................... 28 7.3.3 Possibility to use all the calculation methods................................. 29

7.4 Possible sources of differences between calculation methods: current practices, problematic issues, possible solutions and recommendation of CEIOPS .............................................................................................. 30

7.4.1 Differences stemming from different national implementation of the IGD options...................................................................................... 31 7.4.2 Different national interpretations of the IGD ................................. 33

8. Intra group transactions (IGT) and exposures ......................................... 34 8.1 EU Directive provision ..................................................................... 34 8.2 Current practices............................................................................ 34 8.3 Problematic issues, possible solutions and recommendation of CEIOPS... 35

8.3.1 Art. 8 IGD................................................................................ 35 8.3.2 Definition of IGT (items to be reported, exposures) ....................... 36 8.3.3 Criteria for “significance” ........................................................... 37 8.3.4 Frequency for reporting/schedule for reporting.............................. 37

Recommendation on possible need for Amendments to the Insurance Groups Directive

3

8.3.5 Format for reporting.................................................................. 38 8.3.6 Extension of parties for reporting transactions between other parties within the group ............................................................................... 38

9. Internal Control, Risk Management and Corporate Governance .................. 39 9.1 EU Directive provision ..................................................................... 39 9.2 Current practices............................................................................ 40 9.3 Problematic issues .......................................................................... 40 9.4 Possible solutions ........................................................................... 41 9.5 Recommendation of CEIOPS............................................................. 41

10. Avoiding and preparing for crisis situations............................................ 42 10.1 EU Directive provision ................................................................... 42 10.2 Current practices .......................................................................... 42 10.3 Problematic issues ........................................................................ 42 10.4 Possible solutions.......................................................................... 43 10.5 Recommendation of CEIOPS........................................................... 43

11. Enforcement measures....................................................................... 44 11.1 Recommendation of CEIOPS........................................................... 44

Annex I Implementation of the calculation methods...................................45

Recommendation on possible need for Amendments to the Insurance Groups Directive

4

1. Background

On 27 October 1998 Directive 98/78/EC on the Supplementary Supervision of Insurance Undertakings in an Insurance Group (Insurance Groups Directive-IGD) was adopted.

Art. 11 of the Directive states that not later than 1 January 2006 the Commission shall submit to the European Insurance and Occupational Pensions Committee (EIOPC) a report on the application of this Directive and, if necessary, on the need for further harmonisation.

In this perspective CEIOPS gave a mandate to its Insurance Group Supervision Committee (IGSC)1 to prepare the present paper.

The recommended amendments to IGD mentioned in this paper must be seen as a first step only. Some of the recommendations outlined in this paper will touch upon issues we expect to be covered within the Solvency II project. The recommendations given in this paper are therefore either outside the scope of Solvency II, or they are paramount requirements deemed necessary for supplementary supervision but not expected to be reversed after Solvency II implementation. Furthermore, we acknowledge that the IGD is expected to be revised following a future Solvency II Directive, with possibly a larger focus on risk based methods of supervision.

2. Executive Summary

When assessing the Directive and the potential need for changes in order to reach further harmonisation, the convergence in supervisory methods that is achieved in practice through the Helsinki Protocol and the Guidelines for Coordination Committees2 (Co-Co Guidelines), adopted by CEIOPS on 24 February 2005, should be taken into account. If convergence has been reached through supervisory practice, the need for amendments to the Directive will be reduced.

1 The IGSC is chaired by Ole-Jørgen Karlsen from Norway. The Members of the IGSC are Alfred Parnis (Malta); Ana Cristina dos Santos (Portugal); Anna Lundberg (Sweden); André Schroeder (Luxembourg); Anna Wawrzeniecka (Poland); Anne Pirn (Estonia); Brendan Smith (Ireland); Carlos Montalvo (Spain); Dina Mikelsone (Latvia); Fausto Parente (Italy); Jan Geert Schouwstra (Netherlands); John Wilkinson (United Kingdom); Jozef Fujda (Slovakia); Juha Sasi (Finland); Liga Gange (Latvia); Lisbeth Strand (Norway); Lucilla Caterini (Italy); Maria Koronaiou (Greece); Mojca Berkovie Simeonov (Slovenia); Monika Jurasova (Czech Republic); Noel Guibert (France); Nora Kiss (Hungary); Ole Laustsen (Denmark); Ole-Jørgen Karlsen (Chairman, Norway); Pierre Lemoine (Belgium); Sibylle Schulz (Germany); Teresa Bum (Austria) and Werner Furrer (Liechtenstein). 2 See www.ceiops.org.

Recommendation on possible need for Amendments to the Insurance Groups Directive

5

In a survey conducted among the coordination committees (Co-Cos) involved in supervising insurance groups operating in more than one EEA country it appears that more efficiency in the exercise of the supplementary supervision is needed (e.g. in the majority of groups, no Lead Supervisor has been appointed). One suggestion to promote Co-Cos to appoint a Lead Supervisor would be to make the process more transparent, e.g. by introducing a yearly reporting to CEIOPS by those Co-Cos that have not yet appointed such a Lead Supervisor and requiring them to state the reasons why no such Lead Supervisor has been appointed. The majority of the CEIOPS members believes that no change in the IGD is currently necessary, since the Protocol already provides supervisors with the means of organising the most adequate and efficient structure for group-wide supervision. However, some members do support aligning the IGD with the Financial Conglomerates Directive (Directive 2002/87/EC - FCD) with regard to the introduction of a coordinator responsible for most aspects of supplementary supervision.

CEIOPS recommends that the IGD introduces an option for supervisors involved in a Co-Co to ask for a reorganisation of third country groups, e.g. by introducing a holding company situated within the EEA. The further details on the decision-making process should be dealt with at Level 3.

Supervisors have already made efforts in order to avoid an excessive burden on insurance groups while preserving effectiveness and efficiency of supplementary supervision. Further improvements in this field might be related to the possibility to increase flexibility for supervisors and allow them to tailor the structure of supervision to the structure of the group to the maximum possible extent. To achieve this aim amendments to the IGD might be envisaged in order:

- to shift from Member States to supervisors the power to grant waivers for performing Adjusted Solvency Margin (ASM) and Parent Undertaking Solvency Calculation (PUSC): this would imply more flexibility for supervisors who could grant waivers taking into account case-by-case situations, without being bound by general choices made by each Member State when implementing the IGD (see Chapter 7.2.3); and

- concerning groups whose head office is located outside EEA, to provide supervisors with the power to require the constitution of an EEA holding company so that they can assess the capital adequacy of the group at EEA level (Chapter 7.2.4). A similar provision is envisaged by the FCD.

The IGD provides some general principles for the adjusted solvency calculation and allows Member States to choose from three calculation methods one of which insurance undertakings in their jurisdiction might/have to apply:

1. Deduction and Aggregation Method;

2. Requirement Deduction Method; and

3. Accounting Consolidation Based Method.

Recommendation on possible need for Amendments to the Insurance Groups Directive

6

To cater for a more practical application of the IGD as well as the comparison with similar FCD provisions CEIOPS recommends that some amendments are made to the IGD in order to improve cooperation among supervisors and to promote level playing field:

- the Requirement Deduction Method might be deleted from the IGD since its use is not common throughout EU (see Chapter 7.3.1). If not deleted, it should anyway be amended in order to make it consistent with the similar calculation method envisaged under the FCD (see Chapter 7.3.2);

- supervisors should be enabled to use all the calculation methods in force, even though their use is not envisaged under the national implementation of the IGD (see Chapter 7.3.3). A similar provision is envisaged by the FCD.

The IGD clearly states that the three calculation methods are prudentially equivalent and that they effectively cope with the elimination of capital multiple gearing. However, some different quantitative results might be achieved in the calculation if different methods are applied or even if the same method is applied under different assumptions. Those differences might hinder comparability of the results performed according to the different methods/assumptions in force in each Member State and might be a threat to the aim of a level playing field.

Art. 8 IGD stipulates that Member States shall provide that supervisors exercise general supervision over transactions between an insurance undertaking and participants of the insurance group. The Directive requires at least annual reporting by the insurance undertakings to the competent authorities of significant transactions. If it appears that the solvency of the insurance undertaking is, or may be, jeopardised, the supervisor shall take appropriate measures at the level of the insurance undertaking.

However many differences have been observed between implementation in national laws by Member States, each Member State being satisfied with their own interpretation and implementation of the IGD regarding Intra Group Transactions (IGT). To seek level playing field, to seek convergence to the FCD, and to ease the burden of insurance groups operating in more than one Member State, CEIOPS has outlined issues that may call for amendments of the current IGD.

The conclusion is that it is not necessary to change the IGD with respect to IGT. The IGD has recently been changed by introducing requirements on adequate risk management and internal controls in order to identify, measure, monitor and control intra-group transactions. This should give a positive impulse to this subject, both for the group/company and for the supervisor. What really matters is that methods will be developed for identifying the sort of transactions that might pose risks and that supervisors understand why they might pose a risk. Further, it is important that those risks are discussed, understood, and if necessary an action plan agreed, between all supervisory authorities who might be affected by them. The role the Co-Cos have to play becomes more important

Recommendation on possible need for Amendments to the Insurance Groups Directive

7

by discussing the relevant group transactions of the individual companies within the group.

CEIOPS therefore recommends that guidance should be developed at EU level, and supervisory authorities should seek to improve the efficiency of supervision of IGT at group level.

CEIOPS therefore recommends that the Directive should not be changed with respect to the kind of transactions that have to be reported. Each Co-Co must supplement the Member States’ reporting requirements if necessary by for example requiring more frequent or more extensive reporting. Such Co-Co decisions will depend upon the group structure, internal control procedures and the risk assessment. Furthermore, CEIOPS recommends the development of further guidance at EU-level (level 3), with the aim of converging EEA-Members supervisory practice.

The FCD has a more comprehensive approach to internal control and risk management. Art. 9 outlines more specific requirements with regard to internal control mechanisms and risk management processes. CEIOPS recommends that the IGD should be revised in 2006 to harmonise with the principal, general requirements to internal control mechanisms and risk management processes as given in the Art. 9 FCD, even if they are not fully comprehensive, and link such first stage harmonization with a second stage, in line with the specific insurance Solvency II decisions concerning internal controls and risk management.

CEIOPS considers that, even though it would probably be complex, a general guideline for crisis situations, taking into account the potential specific risks of the individual insurance group, should be worked out within each Co-Co (on a case-by-case basis). One solution could be to consider restricting an amendment of the IGD to add a general obligation for supervisors to inform other relevant supervisors of a crisis or an emerging crisis in a group or in a company belonging to a group. It could then be left to CEIOPS to develop a more comprehensive definition of what or which cases represent a crisis, and how and when notification to other supervisors is needed.

3. Introduction

The supplementary supervision of insurance undertakings in an insurance group enables the supervisors involved to form a more soundly based judgement on the financial situation of insurance undertakings within that group, thus providing additional safety to policyholders. Furthermore, the IGD aims to prevent distortion of competition, and to contribute to the stability of financial markets. Essential elements addressed by the IGD in this regard, are group solvency (the elimination of multiple gearing of own funds instruments), the extent and validity of IGT and the strength of the group's internal control mechanisms.

Recommendation on possible need for Amendments to the Insurance Groups Directive

8

The need for cooperation between competent authorities is recognised by Art. 7 IGD. To facilitate the close cooperation between supervisory authorities from different Member States the Helsinki Protocol was agreed between supervisors from all Member States in 2000. CEIOPS (and its predecessor The Conference of the Insurance Supervisory Services) has been working since then to identify and resolve the issues arising from supplementary supervision of groups operating across EEA borders with the aim of establishing a more common approach to group or supplementary supervision and thus to create a more level playing field for insurance groups operating throughout the EEA.

The overview of the suggested amendments to the Directive presented in this paper is in particular based on the practical experiences of Member States in seeking compliance with the IGD across Member States’ borders. CEIOPS has also taken into account relevant parts of the FCD, adopted in 2003, while preparing this paper.

The principle of solo-supervision remains untouched, which leaves the final responsibility of supervisory action to the supervisory authority in the Member State in which the insurance undertaking is authorised (acknowledging International Association of Insurance Supervisors’ (IAIS) Insurance Core Principle (ICP) 15 which states that the supervisory authority should have the powers to protect one or more insurers within its jurisdiction that belong(s) to a group against financial difficulties which may occur in other parts of the group).

When assessing the Directive and the potential need for changes in order to reach further harmonisation, the convergence in supervisory methods that is achieved in practice through the Helsinki Protocol and the Co-Co Guidelines, should be taken into account. If convergence may be reached through supervisory practice, the need for amendments to the Directive will be limited.

For some recommendations it has also been considered relevant to refer to the ICPs adopted by the IAIS.

The issues considered in this paper are dealt with by:

- describing how the issue is addressed by EU legislation today;

- describing how the issue is addressed by supervisory authorities and through supervisory practice, including how it is addressed in the Helsinki Protocol and in the Co-Co Guidelines;

- describing the challenges with current legislation and/or current supervisory practice;

- presenting alternative solutions to overcome current challenges, including pro & contra arguments; and

- recommending CEIOPS’ preferred solution.

Recommendation on possible need for Amendments to the Insurance Groups Directive

9

4. Current conduct of supplementary supervision

Within the framework of the IGD, insurance supervisory authorities of EEA Member States identified early-on the need to agree on a common supervisory approach aiming towards a more level playing field for those insurance groups with undertakings in more than one EEA Member State, reducing the scope for regulatory arbitrage and to reduce the burden of both insurance groups and supervisory authorities. Thus, the Helsinki Protocol was signed by all the insurance supervisory authorities of Member States in 2000. The Helsinki Protocol was extended to the new EEA Member States in 2004.

The Helsinki Protocol foresees the establishment of Co-Cos to handle the supplementary supervision of a given insurance group. The Co-Co will consist of one supervisor from every Member State involved. The Co-Co will agree on the organisational form of supplementary supervision, and will also agree on how and when information requested from the insurance group by the Co-Co shall be collected. Furthermore, without prejudice to the responsibilities of the supervisors involved under their national legislation, the Co-Co will, in light of the IGD, discuss and coordinate any measures, if necessary, to be taken by the relevant competent authority against any insurance undertaking being part of a group, both in regular and crisis situations. The Co-Co will meet as often as the members deem necessary3.

It follows from the Helsinki Protocol that supervisors represented in the Co-Cos share a mutual responsibility to cooperate regarding supplementary supervision.

Without prejudice to the options allowed for in the IGD, CEIOPS has developed the Co-Co Guidelines in order to minimise, to the extent possible, other practical obstacles to efficient and comparable supplementary supervision across Member States. These Guidelines encourage the mutual exchange of information regarding relevant national legislation and supervisory methods. Furthermore they encourage, where possible and appropriate, the Co-Co to seek efficient ways of information collection and analysis. However, there will still be obstacles to harmonised supplementary supervision across EEA, following Member States’ different implementation of options given in the IGD.

3 Typically, the Co-Cos of the major insurance groups meet face-to-face once every year, and exchange

information by telephone or email during the year. Co-Cos of smaller insurance groups may have had one initial meeting, and have since exchanged information by telephone or email.

Recommendation on possible need for Amendments to the Insurance Groups Directive

10

5. Role of the Lead Supervisor

5.1 EU Directive provision

Art. 7 IGD lays down requirements on cooperation between Member States regarding the exchange of information between competent authorities. Art. 4.2 IGD regards the option of appointing one (or more) competent authority(ies) to assume responsibility for exercising supplementary supervision. Other Articles of the IGD assume cooperation between supervisory authorities regarding insurance groups operating in more than one EEA Member State.

The FCD goes further in confirming the role of the coordinator to assume responsibility for exercising supplementary supervision. It also specifies the extent of information to be exchanged between relevant supervisors (Art. 12).

5.2 Current Practices

CEIOPS has agreed, through the Helsinki Protocol, that within the framework of the IGD, Member States' insurance supervisory authorities should strive to cooperate via a Co-Co. The Co-Co should consist of members of EEA supervisory authorities involved with the supervision of insurance undertakings within the insurance group.

The supervisors concerned should strive for forms of cooperation in the exercise of the supplementary supervision which are sufficiently flexible.

The Co-Co of an insurance group may decide to appoint either a Key Coordinator and/or a Lead Supervisor.

The Helsinki Protocol describes the role of a Key Coordinator as a supervisor arranging and managing the coordination of the activities necessary to carry out the supplementary supervision. The Key Coordinator does not assume any of the responsibilities for supplementary supervision from other supervisors, as allowed for in Art. 4.2 IGD.

The Helsinki Protocol describes the role of a Lead Supervisor as a supervisor responsible for carrying out most or all of the supplementary supervision and assuming the responsibility to do so, whenever the IGD leaves a choice in that respect (in line with Art. 4.2 IGD). The Lead Supervisors should share its findings with the other supervisors of the Co-Co. A Lead Supervisor may only be appointed if there is unanimity within the Co-Co. In practice, it was expected that the Lead Supervisor would also be chosen to chair the Co-Co, and act as a Key Coordinator.

CEIOPS approved the Co-Co Guidelines on 24 February 2005. These Guidelines address this issue and encourage the appointment of a Lead Supervisor.

Recommendation on possible need for Amendments to the Insurance Groups Directive

11

The Co-Co Guidelines point out that the Co-Co should have a Lead Supervisor/Key Coordinator, whose tasks should include planning and coordination of supervisory activities in cooperation with the relevant competent authorities. It is suggested that the Co-Co may entrust additional tasks to this Lead Supervisor/Key Coordinator.

5.3 Problematic issues

In a survey conducted among the Co-Cos involved in supervising insurance groups operating in more than one EEA country it appears that more efficiency in the exercise of the supplementary supervision is needed (e.g. in the majority of groups, no Lead Supervisor has been appointed). More efficiency may be achieved through the adoption of the Guidelines approved by CEIOPS. Furthermore, one may also assume that the supervisory burden connected with Lead Supervisor’s duties can actually discourage appointing one. Nonetheless, even without appointing one member of the Co-Co as Lead Supervisor, the flow of information, information gathering etc. runs smoothly.

5.4 Possible solutions

5.4.1 Reporting to CEIOPS on appointment of Lead Supervisors

If further harmonisation between Member States is expected it will be necessary to find means of enhancing convergence in the way supervisory coordination is organised. One suggestion to promote Co-Cos to appoint a Lead Supervisor would be to make the process more transparent, e.g. by introducing a yearly reporting to CEIOPS by those Co-Cos that have not yet appointed such a Lead Supervisor and requiring them to state the reasons why no such Lead Supervisor has been appointed. (It may be that there are situations in which there are acceptable arguments against such an appointment).

Pro: Introducing such reporting, and keeping the option not to appoint a Lead Supervisor open, would mean allowing some flexibility for those situations in which a Lead Supervisor would not represent any added value to the supervisory processes whilst still introducing discipline towards reducing the number of groups where supervision is conducted independently.

Contra: To the extent it is seen as a disadvantage, a number of authorities may still want to keep the flexibility to not appointing a Lead Supervisor, allowing for more ad-hoc supervisory action to be taken without seeking unanimous decisions or the agreement of the Lead Supervisor.

5.4.2 Aligning the approach with that of the FCD

The main differences observed between the IGD and the FCD, in this regard, are directly related with the different supervisory perspectives in the banking and insurance sectors. In fact, whereas in the banking sector a top down supervision

Recommendation on possible need for Amendments to the Insurance Groups Directive

12

approach has been implemented (meaning that the supervisors mainly address the ultimate parent of the financial group), in the insurance sector the EU Directives are based on a bottom up approach (the supervisors’ approach is mainly that of the individual insurance undertaking according to the solo-plus principle). Consequently, the development of a more harmonized approach between the two methods of supplementary supervision, at the level of the insurance group and at the level of the financial conglomerate, must take these different perspectives into account.

In view of the need for increased collaboration between supervisors, and considering the involvement of supervisors from different sectors and different Member States, the FCD foresees the appointment of a coordinator among them, and identifies which competent authorities involved should be considered relevant for the purpose of supplementary supervision at the level of the financial conglomerate.

Pro: Introducing a mandatory system with a coordinator given powers to decide the detail of the supplementary supervision as well as to conduct most aspects of the supplementary supervision (after consultation with relevant supervisor) would reduce the regulatory burden for insurance entities and supervisors. For instance, reporting would be centralised to one supervisory authority.

There are insurance companies which are members of several IGD/FCD groups. This may lead - at least partly - to multiple, overlapping reporting and unnecessary regulatory and supervisory burden. Any IGD/FCD harmonisation would reduce this burden. Currently different group structures are quite flexible and can change fast. These structural changes may lead to abrupt and repeated shifts between the IGD and FCD supervision. Some supervisors also predict, that IGD/FCD harmonisation will be a necessity in the near future.

Contra: The current regime, with the solo-plus approach of the IGD, provides Member States' supervisors with enough flexibility to allocate tasks and powers within the Co-Co (by appointing one (or more) Lead Supervisor(s), by delegating tasks or by granting waivers).

The Co-Co can, in fact, already decide to distribute tasks within the Co-Co, in order to define a form of supplementary supervision tailored to the structure of each group which avoids any unnecessary or bureaucratic burden.

Those supervisors, who support this view, believe that the enhancement of cooperation is the essential means to increase the efficiency of group supervision. They believe that the Helsinki Protocol already covers any possible organisation of this cooperation, so that no change to the IGD is necessary.

The FCD also requires a high level of cooperation, even though under a slightly different format between the Coordinator (mandatory appointed under certain fixed criteria), the Relevant Competent Authorities and the other Competent Authorities.

Recommendation on possible need for Amendments to the Insurance Groups Directive

13

5.5 Recommendation of CEIOPS

The majority of the CEIOPS members believes that no change in the IGD is currently necessary, since the Protocol already provides supervisors with the means of organising the adequate and efficient structure for group-wide supervision. However, some supervisors do support aligning the IGD with the FCD with regard to the introduction of a coordinator responsible for most aspects of supplementary supervision, as this is expected to ease the performance of supervisory tasks.

CEIOPS is aware that the role of the Lead Supervisor is an important issue that will have to be considered at a later stage and in detail, probably within the context of the Solvency II project.

Whichever of the solutions is chosen, CEIOPS believes that an option should be retained which allows for the conduct of sub-group supervision for those sub-groups that represent either specific risks to the group or which have a particularly high impact on their national markets.

6. One holding company in the EEA in insurance groups whose head offices are located outside the EEA

6.1 EU Directive provision

The IGD does not address the possibility that competent authorities may, for groups whose head offices are located outside the EEA, require the establishment of a holding company which has its head office within the EEA.

The FCD has introduced the right to ask groups with their head office outside the EEA to organise their operations under the umbrella of a separate holding company in Europe (Art. 18 (3) FCD).

6.2 Current practices

As the Helsinki Protocol has been drafted within the limits of the IGD, no possibility was foreseen to ask for the establishment of such a holding company.

The IAIS’ ICP 17 indicates that supervisors should not allow group structures that hinder effective supervision.

6.3 Problematic issues

In the event that it is impossible for a particular third country to achieve an adequate level of supervisory cooperation, to receive the necessary information and/or if there are no equivalent regimes for supervising the groups on a group-wide or consolidated basis (correspondent to the EU standards), it will not

Recommendation on possible need for Amendments to the Insurance Groups Directive

14

be possible to carry out supplementary supervision of the insurance group in a satisfactory manner.

Particularly with respect to the US, but also in the case of Swiss insurance groups, it has proven difficult to achieve a cooperation agreement securing access to the relevant information necessary to conduct supplementary supervision, including information necessary for the calculation of the adjusted solvency requirement. Furthermore the variety of regimes of the US-led groups makes it difficult to assess properly whether the local regimes can be considered equivalent with that in the EEA.

Also in respect of other third countries the decision as to whether or not the supervisory regime outside EEA can be considered equivalent to that provided for by the EU regime, may represent a difficult challenge. The process of deciding which third countries’ supervisory regimes are equivalent, both for purely insurance groups as well as for financial conglomerates, should be coordinated at EEA level. There may, however, be discrepancies both in the supervisory regimes for insurance groups and conglomerates in a particular third country, and there may also be differences between the needs of European supervisors involved in insurance group supervision and those involved in conglomerate supervision.

6.4 Possible solutions

A requirement for establishing one overall holding company for European activities of an insurance group having its head office outside the EEA would facilitate a more streamlined supervision of these groups.

The introduction of a single holding company in Europe, under which all insurance companies throughout the EEA are organised, could reduce the need for extending the scope of supervision outside the EEA. The possibility to ask for establishment of one EEA holding company would be relevant for insurance groups where several different supervisory authorities are responsible for different insurance undertakings within EEA, when the overall holding company has its head office outside the EEA, and when the third country supervisor does not have adequate supervisory focus on group-related issues. It may also be used for those cases where no supervisor responsible for group supervision can be identified.

Pro: With the introduction of such a power, one would first of all give incentives to third country groups to organise their operation in a transparent way, allowing supervisors to conduct proper supplementary supervision on the group’s activities. It would also facilitate the supervisory process for those supervisors responsible for supervision in the home country of the particular group. These elements should indicate that the enforcement of the “supervisory tool” of reorganisation of a third country group into a structure under the umbrella of a holding company domiciled and supervised in the EEA would be minimised.

Recommendation on possible need for Amendments to the Insurance Groups Directive

15

To require a reorganisation of the group structure if current structure of the group hinders the effective supervision, is an essential power for supervisory authorities (avoid moral hazard, i.e. the establishment of difficult structures in order to hinder effective supervision).

The establishment of one EEA holding company for third country insurance groups may reduce the regulatory burden for the insurance companies, as they would no longer have to supply the (EEA) supervisors with information concerning the parent company/ies).

Even though an option for the supervisors to ask the group to establish a holding company within Europe may seem dramatic, e.g. it may be seen as taking an active part in the decision-making processes of a particular group, and may not be practicable in many circumstances, the very existence of such a feature may lead to some sort of discipline among market participants. This, in itself, may force the groups with the most complex structures to become more transparent. (see also Chapter 10)

Contra: Some supervisory authorities are of the opinion that requiring changes in group structures interferes with the management of the group, and that by doing so supervisors may be taking on a too strong a responsibility for managing the operations of the group.

6.5 Recommendation of CEIOPS

CEIOPS recommends that the IGD is amended to introduce an option for supervisors involved in a Co-Co to ask for a reorganisation of third country groups e.g. by introducing a holding company situated within the EEA4. A requirement from the supervisory authorities to establish one holding company situated within the EEA should only be required after other possible ways of addressing the challenges of supervising the group have been exhausted. The further details on the decision-making process should be dealt with at Level 35.

7. Solvency calculations at group level

7.1 Introduction

The IGD requires a calculation of capital adequacy at the insurance group level, and the Directive sets out the general principles the insurance undertaking must follow in performing such an adjusted solvency calculation. The Directive also provides supervisory authorities with the necessary information and verification powers to assess such capital adequacy.

The use of these common general principles for the adjusted solvency calculation has made a positive contribution to the functioning of the European insurance

4 See Art. 18 FCD. 5 Please see also Chapter 7.2.4, where this issue is also dealt with.

Recommendation on possible need for Amendments to the Insurance Groups Directive

16

market as well as facilitating the comparison of capital adequacy of insurance groups located in different Member States which enhances a level playing field within the EEA.

However, the practical application of the Directive provisions relating to the solvency calculation has outlined some difficulties and has created a general need to streamline supervision in order to further enhance comparability and the level of harmonisation between the Member States.

The cooperation between the supervisors of different Member States aims at ensuring an efficient and effective group-wide supervision, even seeking for a further convergence in its practical application.

The following chapters aim at underlining the main areas where further harmonisation may be needed in order to ensure a level playing field and a fair competition among both national and cross-border insurance groups. Moreover, these chapters could be useful in the light of the application of the FCD.

The IGD considers conditions under which an insurance undertaking subject to supplementary supervision has to:

- calculate its own ASM; and

- perform a PUSC following a “bottom-up approach”, provided that the parent undertaking of an insurance company is an insurance holding company and/or a reinsurance company and/or a third country insurance company.

The Directive envisages that:

- each insurance undertaking in the group must perform the ASM as well as the PUSC, with the possibility for the Member States to grant waivers for some undertakings under certain circumstances6;

- the PUSC must be performed in relation to all the parent companies at each level of the group participation chain, with the possibility for the Member States to give some waivers in order to perform the calculation with reference to the ultimate parent company only7.

6 See IGD, Annex I and Annex II. 7 See IGD, Annex II.

Recommendation on possible need for Amendments to the Insurance Groups Directive

17

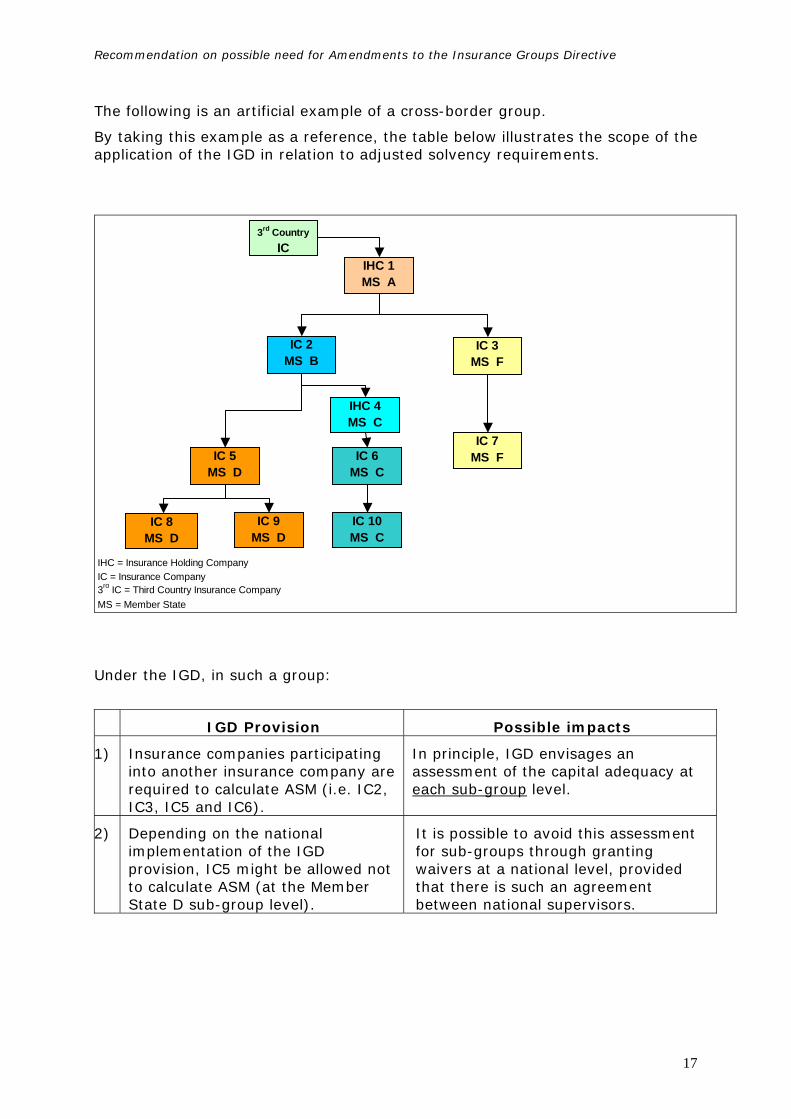

The following is an artificial example of a cross-border group.

By taking this example as a reference, the table below illustrates the scope of the application of the IGD in relation to adjusted solvency requirements.

IHC = Insurance Holding CompanyIC = Insurance Company3rd IC = Third Country Insurance CompanyMS = Member State

IC 2MS B

IC 5MS D

IC 8MS D

IC 9MS D

3rd Country IC

IC 6MS C

IC 10MS C

IHC 4 MS C

IC 3MS F

IC 7MS F

IHC 1MS A

Under the IGD, in such a group:

IGD Provision Possible impacts

1) Insurance companies participating into another insurance company are required to calculate ASM (i.e. IC2, IC3, IC5 and IC6).

In principle, IGD envisages an assessment of the capital adequacy at each sub-group level.

2) Depending on the national implementation of the IGD provision, IC5 might be allowed not to calculate ASM (at the Member State D sub-group level).

It is possible to avoid this assessment for sub-groups through granting waivers at a national level, provided that there is such an agreement between national supervisors.

Recommendation on possible need for Amendments to the Insurance Groups Directive

18

3) IC2 and IC3 are also required to perform a PUSC. They are required to perform it on IHC1 and/or on 3rdIC, depending on national implementation.

a) More insurance undertakings (IC2 and IC3) might be required to perform the same PUSC at the top level of the group.

b) More than one PUSC might be performed (in relation to IHC1 and/or 3rd IC).

4) Depending on the national implementations of IGD, IC2 or IC3 might be granted a waiver to perform PUSC on IHC1 and/or on 3rdIC.

The multiple burden under previous Art. 3 might be avoided through the granting of a waiver, in agreement with other involved supervisors.

5) Depending on the national implementations, IC6 might be also required to perform a PUSC on IHC4.

More PUSC might be required within the same group with reference to different intermediate holding company (parent company for the national sub-group).

6) Depending on the national implementation of IGD, IC6 might be granted a waiver to perform PUSC (at the Member State C sub-group level).

The multiple burden under previous Art. 5 might be avoided through granting waivers.

The table above outlines that the solo-plus approach followed by the IGD may imply rather a complex scope of its application and a possibly unnecessary burden on insurance companies. The IGD, however, provides supervisors with some powers to tailor the adjusted solvency calculation requirement to the structure of each supervised insurance group, through the granting of waivers and through cooperation amongst the involved supervisors.

By signing the Helsinki Protocol, insurance supervisors agreed to make best efforts to streamline supervision and to avoid an excessive burden on insurance groups. Taking advantage of the flexibility of the IGD provision, the work of CEIOPS by means of its IGSC and the establishment of Co-Cos for each cross-border group has avoided an excessive multiplication of the calculations. Furthermore the Co-Cos tried to have checked the solvency calculation of the group by a single supervisor in those situations where the solvency calculations at sub-group level are not relevant. Further streamlining of the supervision might be achieved by ensuring to supervisors the necessary powers to grant waivers and therefore to avoid excessive burden on insurance groups8.

Despite supervisors’ efforts for streamlining supervision, some problems have arisen in the practical application of the Directive provisions. The main critical areas concern:

8 See also Chapter 7.2.4.

Recommendation on possible need for Amendments to the Insurance Groups Directive

19

- the scope of the adjusted solvency calculation;

- the calculation methods; and

- the possible sources of differences between methods.

These areas are listed below, together with some suggestions for possible actions that could be taken to mitigate them.

7.2 The scope of the calculation: current practices, problematic issues, possible solutions and recommendation of CEIOPS

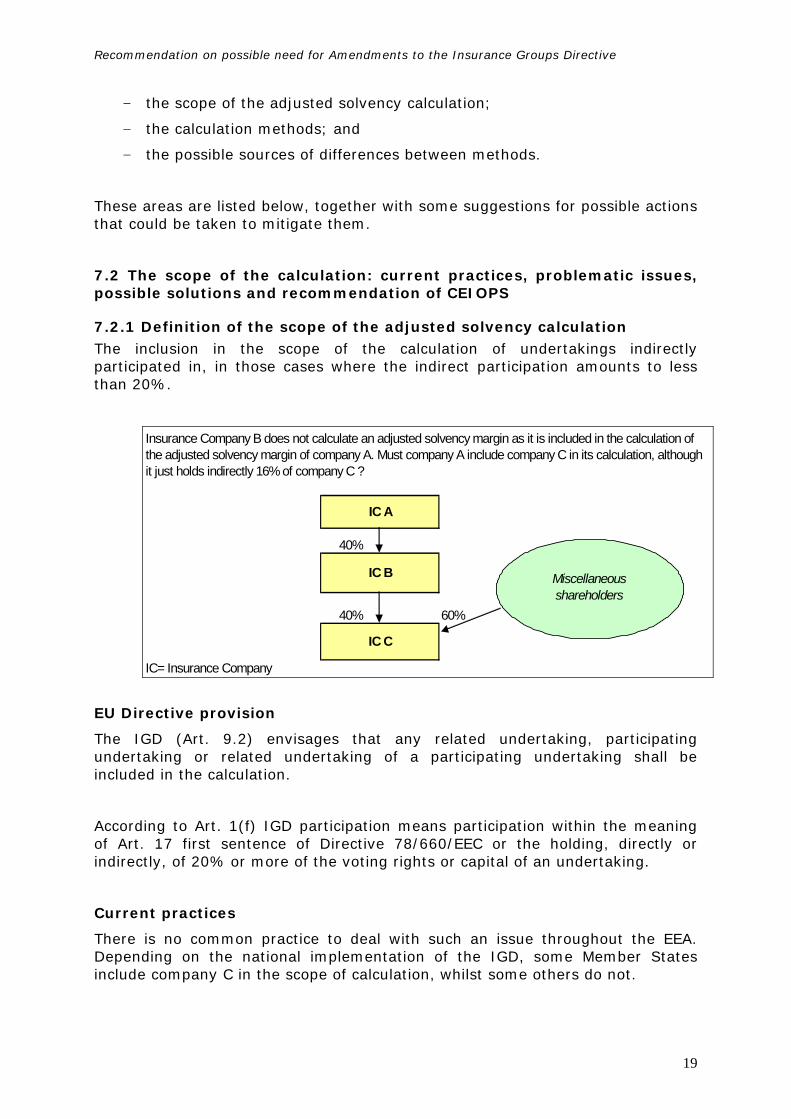

7.2.1 Definition of the scope of the adjusted solvency calculation The inclusion in the scope of the calculation of undertakings indirectly participated in, in those cases where the indirect participation amounts to less than 20%.

40%

40% 60%

IC= Insurance Company

Insurance Company B does not calculate an adjusted solvency margin as it is included in the calculation of the adjusted solvency margin of company A. Must company A include company C in its calculation, although it just holds indirectly 16% of company C ?

IC B

IC A

IC C

Miscellaneous shareholders

EU Directive provision

The IGD (Art. 9.2) envisages that any related undertaking, participating undertaking or related undertaking of a participating undertaking shall be included in the calculation.

According to Art. 1(f) IGD participation means participation within the meaning of Art. 17 first sentence of Directive 78/660/EEC or the holding, directly or indirectly, of 20% or more of the voting rights or capital of an undertaking.

Current practices

There is no common practice to deal with such an issue throughout the EEA. Depending on the national implementation of the IGD, some Member States include company C in the scope of calculation, whilst some others do not.

Recommendation on possible need for Amendments to the Insurance Groups Directive

20

Problematic issues

Different national interpretations on the IGD provisions may affect both, cross-border groups and national groups (i.e. groups whose entities are all located in the same country), undermining possible comparisons with similar groups located in other Member States.

Possible solutions

- Changes to the Directive

This issue might be coped with by introducing a more specific definition of participation, with reference to the inclusion in the adjusted solvency calculation.

Pro: comparability, clarity and therefore level playing field

Contra: lack of flexibility (supervisors may need the power to tailor the scope to the different group structures)

- Changes in the supervisory approach

Another possibility is to issue detailed supervisory guidance at EEA level (level 3).

Pro: flexibility

Contra: no cases specified

Recommendation of CEIOPS

CEIOPS recommends the issuance of supervisory guidance at EEA level (level 3) as CEIOPS does not foresee a need for changing the Directive.

Recommendation on possible need for Amendments to the Insurance Groups Directive

21

7.2.2 Identification of the undertaking required to perform and submit the PUSC

Which insurance company is going to perform the PUSC?

IC 2MS B

IC 3MS F

IHC 1MA A

EU Directive provision

The IGD (Annex II) envisages that Member States may waive the calculation of the PUSC if more than one insurance undertaking has the same parent undertaking. If the insurance undertakings are authorised in different Member States (as it is in the example above), an agreement granting exercise of the supplementary supervision must be concluded with the supervisory authority of the other Member States.

Current practices

Reference is made to the Helsinki Protocol and to the Co-Cos that have been established for each multinational group.

Problematic issues

Practical application showed that:

- it is necessary that supervisors cooperate within each Co-Co in order to avoid a double burden for those different undertakings in the same insurance group;

- according to the IGD provisions and to their national implementations throughout EU, insurance undertakings might be required to perform the PUSC in relation to their parent company without, in practice, having sufficient information to do so.

Possible solutions

- Changes to the Directive

These issues might be addressed by amending the IGD in order to require the parent company to directly perform its own adjusted solvency calculation, in a sort of “top-down approach”.

Recommendation on possible need for Amendments to the Insurance Groups Directive

22

In this hypothesis, some related details should be also clarified, i.e. the definition of the supervisory regime envisaged for insurance holding companies, the identification of the supervisory authority with responsibility for this supervision (especially if the insurance holding company is not located in the same Member State as the insurance sub-group) and the identification of the methods to measure an adequate distribution of capital within the group. To this aim, provisions similar to those within the FCD might be envisaged.

Pro: avoidance of a double burden for the supervised group, availability of the information, consistency with similar provision of the FCD and no need to grant waivers

Contra: loss of flexibility compared to the current situation

- Changes in the supervisory approach

Another possibility is to deal with these issues at the Co-Co level in relation to the specific structure of the group, so that the Co-Co should be asked to take case-by-case decisions. Supervisory guidance could also be issued at EEA level by CEIOPS.

Pro: flexibility

Contra: If no supervisory guidance at the EEA level is issued, coordination among different Co-Cos should be pursued in order to ensure a level playing field among the different multinational groups.

Recommendation of CEIOPS

CEIOPS recommends case-by-case solutions at the Co-Co level. The issuance of guidance at EEA level (level 3) might assist this as CEIOPS does not foresee a need for changing the Directive.

Recommendation on possible need for Amendments to the Insurance Groups Directive

23

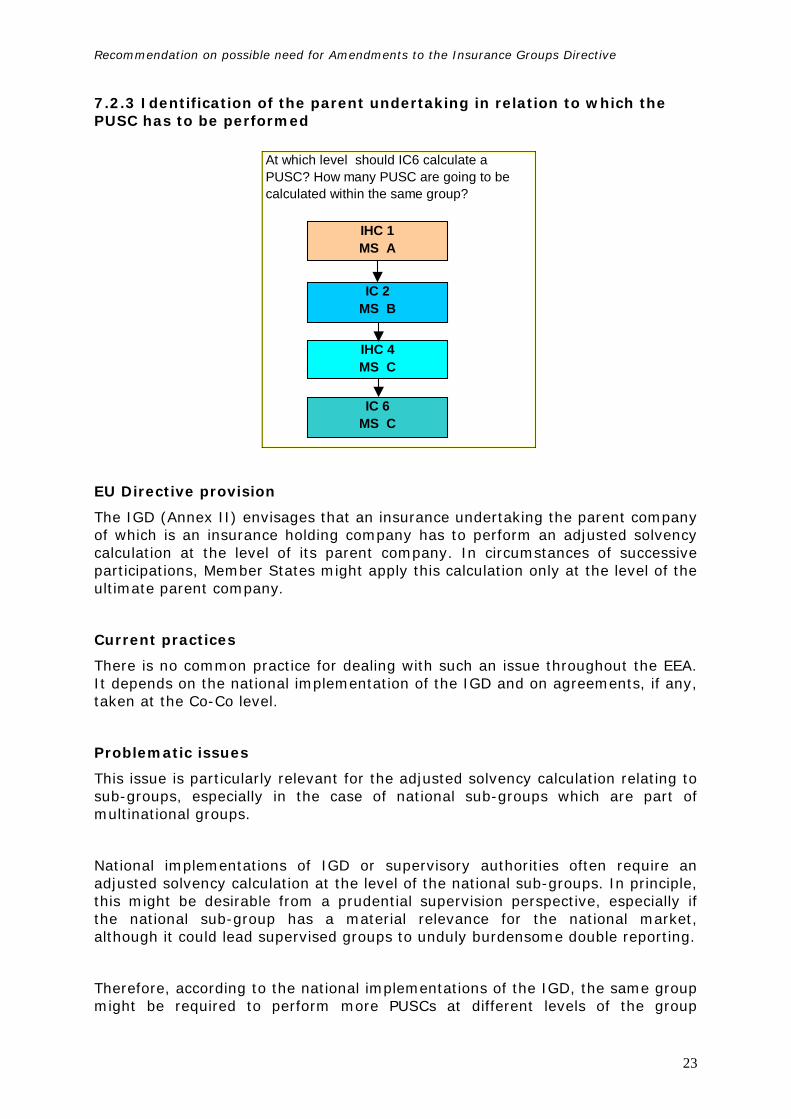

7.2.3 Identification of the parent undertaking in relation to which the PUSC has to be performed

At which level should IC6 calculate a PUSC? How many PUSC are going to be calculated within the same group?

IC 2MS B

IC 6MS C

IHC 4 MS C

IHC 1MS A

EU Directive provision

The IGD (Annex II) envisages that an insurance undertaking the parent company of which is an insurance holding company has to perform an adjusted solvency calculation at the level of its parent company. In circumstances of successive participations, Member States might apply this calculation only at the level of the ultimate parent company.

Current practices

There is no common practice for dealing with such an issue throughout the EEA. It depends on the national implementation of the IGD and on agreements, if any, taken at the Co-Co level.

Problematic issues

This issue is particularly relevant for the adjusted solvency calculation relating to sub-groups, especially in the case of national sub-groups which are part of multinational groups.

National implementations of IGD or supervisory authorities often require an adjusted solvency calculation at the level of the national sub-groups. In principle, this might be desirable from a prudential supervision perspective, especially if the national sub-group has a material relevance for the national market, although it could lead supervised groups to unduly burdensome double reporting.

Therefore, according to the national implementations of the IGD, the same group might be required to perform more PUSCs at different levels of the group

Recommendation on possible need for Amendments to the Insurance Groups Directive

24

participation chain which are submitted to different supervisors. In the example above, IC6 might be required to perform the PUSC with reference to IHC4 and IC2 might be required to perform another PUSC with reference to IHC1.

Further difficulties were outlined if the head offices of the multinational parent group are located outside the EEA (see Chapter 7.2.4).

Possible solutions

- Changes to the Directive

A possibility would be to amend the IGD in order to shift from Member States to supervisors the power to grant waivers for performing ASM and PUSC. The IGD (Annexes I and II) currently provides Member States with the power to waive calculation under certain circumstances. Therefore, the general choices made in the national implementation of the IGD might bind supervisors by not allowing them to grant waivers even though they deem them appropriate for specific cases.

Annexes I and II of the IGD could consequently be amended so that they could envisage that “Member States shall allow supervisors to waive...” instead of “Member States may waive...”.9

Pro: avoidance of the potential double burden reporting for supervised groups, more flexibility for supervisors that could grant waivers taking into account case-by-case situations, without being bound by the general choice made by the Member State when implementing the IGD.

Contra: no specific cases outlined

- Changes in the supervisory approach

Improving cooperation among supervisory authorities, in order to achieve a structure of supervision tailored for each group structure. Cooperation among supervisors will also mitigate the effects of possible differences in the national implementations and reduce potential burden reporting for supervised groups.

Pro: flexibility, supervision tailored to the structure of the supervised group

Contra: potential burdensome double reporting for the group

9 A similar provision is envisaged in FCD, Annex 1 with reference to the choice of the calculation method to be

applied.

Recommendation on possible need for Amendments to the Insurance Groups Directive

25

Recommendation of CEIOPS

The amendments to the IGD can enhance improvements of the cooperation at Co-Co level, in order to define a structure of the supervision tailored for the group structure.

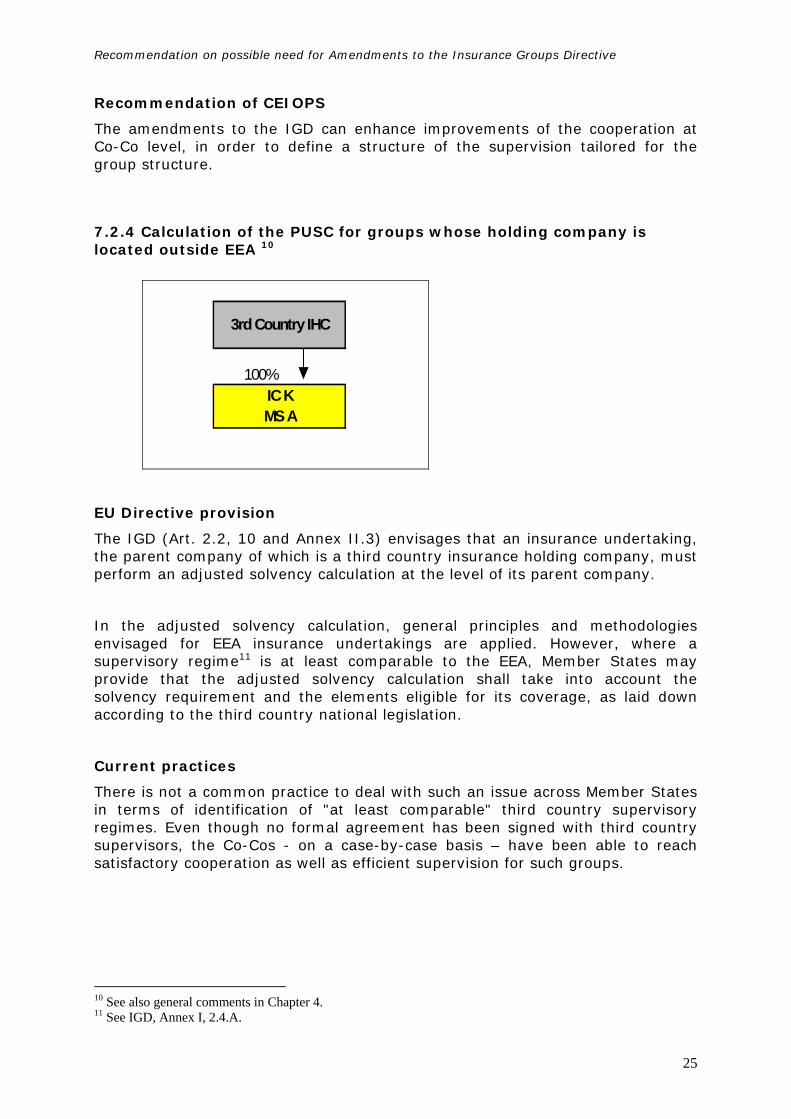

7.2.4 Calculation of the PUSC for groups whose holding company is located outside EEA 10

100%

3rd Country IHC

IC K MS A

EU Directive provision

The IGD (Art. 2.2, 10 and Annex II.3) envisages that an insurance undertaking, the parent company of which is a third country insurance holding company, must perform an adjusted solvency calculation at the level of its parent company.

In the adjusted solvency calculation, general principles and methodologies envisaged for EEA insurance undertakings are applied. However, where a supervisory regime11 is at least comparable to the EEA, Member States may provide that the adjusted solvency calculation shall take into account the solvency requirement and the elements eligible for its coverage, as laid down according to the third country national legislation.

Current practices

There is not a common practice to deal with such an issue across Member States in terms of identification of "at least comparable" third country supervisory regimes. Even though no formal agreement has been signed with third country supervisors, the Co-Cos - on a case-by-case basis – have been able to reach satisfactory cooperation as well as efficient supervision for such groups.

10 See also general comments in Chapter 4. 11 See IGD, Annex I, 2.4.A.

Recommendation on possible need for Amendments to the Insurance Groups Directive

26

Problematic issues

Practical application showed that:

- it is difficult to assess the comparability of a third country supervisory regime; and

- insurance undertakings at a low level of the group participation chain had difficulties performing the PUSC for this kind of group (see also Chapter 7.2.3).

Consequently, there is a strong need for Member States' supervisory authorities to cooperate with the home country supervisors in order to assess the group capital adequacy.

Possible solutions

- Changes to the Directive

It would be possible to adopt a solution similar to that envisaged by the FCD, i.e. to amend the IGD in order to have the power, if necessary (please refer to chapter 6.5), to require the constitution of a holding company located in EEA for calculating the PUSC - and therefore for assessing the capital adequacy of the sub-group – at the EEA level.

Some related details should also be clarified, such as the definition of cases where the constitution of such a holding company would be considered necessary, the identification of the supervisory authority in charge of requiring this constitution. To this aim, provisions similar to those contained within the FCD might be envisaged.

Pro: facilitating supplementary supervision of this kind of group, consistency between the IGD and the FCD

Contra: no specific cases outlined

- Changes in the supervisory approach

It would be possible to issue supervisory guidance at the EEA level regarding which third countries are considered to have an equivalent solvency regime.

Pro: flexibility, level playing field

Contra: no specific cases outlined

Recommendation on possible need for Amendments to the Insurance Groups Directive

27

Recommendation of CEIOPS

Some CEIOPS members favour the amendment of the IGD, others the issuance of supervisory guidance at the EEA level. Both of these solutions could be adopted at the same time.

7.3 Calculation methods in force throughout the EEA: current practices, problematic issues, possible solutions and recommendation of CEIOPS

The IGD provides general principles for the adjusted solvency calculation and allows Member States to choose from three calculation methods which one/s insurance undertakings in their jurisdiction might/have to apply:

- Deduction and Aggregation Method;

- Requirement Deduction Method;

- Accounting Consolidation Based Method.

The national implementation of the calculation methods is illustrated in Annex 1. The table shows that the Accounting Consolidation Based Method is the most used method in 7 Member States (it is the only one allowed in 2 Member States), the Deduction and Aggregation Method is the main method in 5 countries (in 4 Member States it is the only one allowed) whilst the Requirement Deduction Method is hardly used.

7.3.1 Possible deletion of Requirement Deduction Method from the IGD

EU Directive provision

The Requirement Deduction Method is one of the calculation methods allowed under the IGD (Annex 1).

Current practices

According to the results of the above-mentioned survey reported in Annex 1, the use of the Requirement Deduction Method is not the preferred method in any Member State. 8 Member States will allow its use under certain conditions.

Problematic issues

The Requirement Deduction Method might not be necessary for IGD purposes.

Possible solutions

- Changes to the Directive

It might be possible to amend the IGD in order to delete the Requirement Deduction Method.

Recommendation on possible need for Amendments to the Insurance Groups Directive

28

Pro: simplicity and level playing field, facilitation of calculations and therefore of the exercise of supervision.

Contra: inconsistency with the FCD (However, under the FCD in some jurisdictions method 4 is being used and this relies upon the availability of methods 1-3 in FCD).

- Changes in the supervisory approach

Not applicable

Recommendation of CEIOPS

CEIOPS recommends the deletion of the option of the Requirement Deduction Method.

7.3.2 Consistency of the Requirement Deduction Method under the IGD and the FCD

EU Directive provision

The FCD envisages that the calculation of the capital adequacy of the conglomerate is carried out according to methods that are very similar to those used under the IGD.

However, it is worth underlining a difference between the IGD Requirement Deduction Method and the FCD Book Value/Requirement Deduction Method. This difference is related to the item to be added to the solvency requirement of the parent undertaking for determining the amount to be deducted from the eligible elements (own funds according to the FCD) of the parent undertaking12:

- the IGD makes reference to the proportional share of the solvency requirement of the related insurance undertaking;

- the FCD makes reference to the higher of the book value of the parent undertaking’s participation in other entities of the group and these entities’ solvency requirements; the solvency requirements of the latter shall be taken into account for their proportional share.

Current practices

Not applicable

Problematic issues

The use of the method is not consistent under the IGD and the FCD. This lack of consistency might be relevant in the context of possible inter-relationships

12 See IGD, Annex I Section 3 and FCD, Annex I Section 2.

Recommendation on possible need for Amendments to the Insurance Groups Directive

29

between the IGD and the FCD, especially in case of an insurance sub-group being part of a financial conglomerate.

Possible solutions

- Changes to the Directive

It might be appropriate to amend the Requirement Deduction Method under the IGD in coherence with the FCD Book Value/Requirement Deduction Method.

Pro: consistency between the FCD and the IGD

Contra: no specific cases outlined

- Changes in the supervisory approach

Not applicable.

Recommendation of CEIOPS

CEIOPS recommends the amendment to the IGD, if the method is not deleted.

7.3.3 Possibility to use all the calculation methods

EU Directive provision

Under Art. 7 IGD, Member States should ensure that the adjusted solvency calculation is carried out according to one of the three calculation methods; however, a Member State may provide for the competent authorities to authorise or impose the application of a method other than that/those chosen by the Member State.

Current practices

Reference is made to the results of the above-mentioned survey, reported in Annex 1.

Problematic issues

Different national implementations of the options envisaged by the IGD might cause difficulties in the cooperation between supervisory authorities in the case of multinational groups.

If the national implementation does not allow the use of a specific calculation method and does not allow the supervisor to authorise or impose the application of a method other than that/those chosen by the Member State:

Recommendation on possible need for Amendments to the Insurance Groups Directive

30

- it could be difficult to reach an agreement between the supervisors involved upon the use of the same calculation method throughout a group (i.e. for the group as a whole and for national sub-groups, if required). This could potentially lead the insurance group to burdensome double reporting; and

- a supervisor may not be legally able to rely on the PUSC submitted by another Member State’s supervisor, if it is performed under a calculation method which is not allowed in its own country.

Possible solutions

- Changes to the Directive

It might be appropriate to amend the IGD in order to enable supervisors to allow the use of all the three calculation methods throughout the EEA. This would also be in line with similar provisions envisaged by the FCD (Annex I).

Pro: facilitation of cooperation among supervisors, avoidance of potential double burden for multinational insurance groups, consistency with the FCD

Contra: no specific cases outlined

- Changes in the supervisory approach

Not applicable

Recommendation of CEIOPS

CEIOPS recommends the amendment of the IGD in line with the FCD provision (Annex I, para. 3).

7.4 Possible sources of differences between calculation methods: current practices, problematic issues, possible solutions and recommendation of CEIOPS

The IGD (8th preamble) clearly states that the three calculation methods are prudentially equivalent and that they effectively cope with the elimination of capital multiple gearing.

However, some different quantitative results might be achieved in the calculation if different methods are applied or even if the same method is applied under different assumptions.

Awareness of the differences that might arise in the calculation is particularly important for supervisory purposes as it helps the assessment of the solvency

Recommendation on possible need for Amendments to the Insurance Groups Directive

31

position of the whole group. Nevertheless, those differences might hinder comparability of the results performed according to the different methods/assumptions in force in each Member State and might be a threat to the aim of a level playing field. The main differences13,14 outlined relate to:

- different national implementation of the IGD options; and

- different national interpretations of the IGD.

7.4.1 Differences stemming from different national implementation of the IGD options

EU Directive provisions

The IGD (Art. 9 and Annex I) envisages that Member States shall provide that the adjusted solvency calculation is carried out according to one of three possible methods. Since the three methods may not give the same quantitative results, although they are prudentially equivalent, the option for Member States to choose one of the three methods gives rise, itself, to the possibility of differences in the results.

Current practices

Reference is made to the results of the above-mentioned survey, reported in Annex 1.

Problematic issues

The use of one method instead of another one might lead to different results in relation to, e.g.:

- intangible assets held by subsidiaries: the Accounting Consolidation Based Method as well as the Deduction/Aggregation Method provide for an automatic exclusion of the intangible assets held by participated undertakings from the eligible elements; whilst the Requirement Deduction Method does not. The latter, in fact, takes into account the participated undertakings for the value at which they are recognised in the participating undertaking’s balance-sheet (i.e. at equity, without any deduction for the intangible assets owned).

- IGT results: the Accounting Consolidation and the Requirement Deduction Methods provide for a systematic elimination of the effects of IGT from

13 Some outlined differences stem from different national implementation of the EU Solo Solvency Directives.

The comparability of the results of different groups could not profitably be enhanced without a more harmonised solo solvency regime throughout the EEA. So that it seems only possible – waiting for the ending of the EEA Solvency II project – to increase the comprehensibility of the different national systems among supervisors. This could assist with the work undertaken within the Co-Cos.

14 It is worth underlining that the application of different national accounting principles might also affect quantitative results of the adjusted solvency calculation. Regarding this, the forthcoming introduction of the IASB accounting standards is likely to reduce these differences in the long run. Nonetheless, it is not going to eliminate all the possible sources of differences listed above, to the extent they stem from different national implementation of the EU solo solvency Directives. In addition, especially in the first phase of its application, accounting harmonisation still leaves room for a number of options, open to Member States (i.e. extent of the adoption) and to insurers.

Recommendation on possible need for Amendments to the Insurance Groups Directive

32

the eligible elements; while the Deduction/Aggregation Method does not. The former methods, in fact, are applied under accounting rules which explicitly foresee the elimination of the effects of any IGT. For the Deduction/Aggregation Method, such elimination is governed by the general rule (Annex I, 1.D) which only mentions the elimination of the eligible elements arising out of reciprocal financing.

- minority interests: the Deduction/Aggregation Method as well as the Requirement Deduction Method provide for a systematic exclusion of any minority interests, whilst the Accounting Consolidation Based Method does not. The latter actually includes, to a certain extent, the minority shares of a subsidiary’s equity.

Possible solutions

- Changes to the Directive

An amendment to the IGD aimed at introducing the adoption of a single calculation method might be a solution to improve the comparability of the results.

Pro: comparability of the results, simplicity

Contra: The use of a single method would be a partial solution, since some differences would still be unsolved (i.e. different national implementations of the EU Solo-Solvency Directives). Moreover, it would be difficult to select a single “best method” due to the fact that there is not only one best method but – according to some circumstances and to the structure of the group – one method can be preferred to another one.

- Changes in the supervisory approach

The comparability of the results of different groups could profitably be enhanced by issuing at EEA level a detailed application supervisory guidance with specific reference to the main sources of differences between the methods.

Pro: flexibility of the approach which enables Member States' supervisors to consider different solutions for different practical cases/structures as well as any further source of difference which might arise in the future

Contra: no specific cases outlined

Recommendation of CEIOPS

CEIOPS recommends the issuance of supervisory guidance at EEA level (level 3), as CEIOPS does not foresee a need for changing the Directive.

Recommendation on possible need for Amendments to the Insurance Groups Directive

33

7.4.2 Different national interpretations of the IGD

EU Directive provisions

The IGD provides for some general principles to be applied under certain circumstances. As is the case for all the Directives, the practical application has given rise to a number of cases which can be dealt with in different ways depending on the interpretation of such general principles in the implementation process.

Current practices

No common practice

Problematic issues

Different national implementations due to diverse interpretations of the IGD might cause differences in the adjusted solvency calculation’s quantitative results in relation to, for instance:

- transferability: the IGD envisages that elements are eligible towards covering the ASM provided that their transferability within the group is effective. However, no specific definition of “transferability” is provided so there is room for different interpretations by different supervisors;

- limits of admissibility of subordinated loans issued by holding companies: these elements are eligible towards covering the ASM, although the limits are not specified. Reference to similar provisions relating to subordinated loans issued by insurance undertaking is useless since in this case reference is made to a percentage of the required solvency margin (that is 0 for insurance holding companies); and

- limits of admissibility of minority interests in the use of the Accounting Consolidation Based Method: Art. 10 IGD envisages the general principle of proportionality in the application of the three methods; for the Accounting Consolidation Based Method this implies the use of the percentages used for preparing the consolidated accounts. However, in the practical application of the calculation, there is no common opinion among Member States of the percentage that should be taken into account and therefore on the limit of admissibility of these kind of elements towards covering the ASM.

These differences might hinder the comparability of the adjusted solvency calculations among different multinational groups and therefore might distort the attempt to create a level playing field.

Possible solutions

- Changes to the Directive

It would be possible to amend the IGD to further clarify some of these limits and therefore avoid different interpretations of the same rule (e.g.

Recommendation on possible need for Amendments to the Insurance Groups Directive

34

how to fix an eligibility limit for the subordinated debt issued by a holding company, how to define transferability, etc.).

Pro: clarity, level playing field

Contra: lack of flexibility

- Changes in the supervisory approach

It would be possible to issue a detailed supervisory guidance at EEA level with specific reference to the treatment of the outlined elements/items. Further cooperation among supervisory authorities could be sought in order to follow common approaches. A wide and as much as possible homogeneous application within the Co-Cos concerning the adjusted solvency calculations15 should also be pursued.

Pro: flexibility

Contra: no specific cases outlined

Recommendation of CEIOPS

Both solutions could be adopted at the same time.

8. Intra group transactions (IGT) and exposures

8.1 EU Directive provision

Art. 8 of the IGD stipulates that Member States shall provide that supervisors exercise general supervision over transactions between an insurance undertaking and participants of the insurance group. The Directive requires at least annual reporting by the insurance undertakings to the competent authorities of significant transactions. The Directive furthermore requires the Member States to ensure adequate risk management processes and internal control mechanisms regarding IGT. If it appears that the solvency of the insurance undertaking is, or may be, jeopardised, the supervisor shall take appropriate measures at the level of the insurance undertaking.

8.2 Current practices

The IGD was implemented in national laws and other regulations. The Conference of the Insurance Supervisory Services investigated in 2002 the way

15 See Co-Co Guidelines, § 4.6 Solvency.

Recommendation on possible need for Amendments to the Insurance Groups Directive

35

the Directive was implemented in Member States (on the objectives, significance criteria and the frequency of reporting of IGT). Many differences between implementation by Member States have been observed. Each Member State is satisfied with its own interpretation and implementation of the IGD regarding IGT. However, to seek level playing field, to seek convergence to the FCD, and to ease the burden of insurance groups operating in more than one Member State, CEIOPS has outlined below-mentioned issues that may call for amendments of the current IGD.

8.3 Problematic issues, possible solutions and recommendation of CEIOPS

8.3.1 Art. 8 IGD

Does Art. 8 IGD meet its objectives for cross border groups or can it be deleted from the IGD?

Pro: IGT are an important source of information on the companies´ intra group activities and give good information as to potential risk that may jeopardise the solvency of the insurance undertaking and the group.

Insurance companies and groups have, for two years, been reporting these transactions and the importance of these reports is still growing. Insurance groups that are also (part of) a financial conglomerate must also report to the requirements of the FCD, so convergence should be sought.

Contra: IGT are only one way of gaining a more detailed understanding of the group: other risk assessments may be more important. Transactions have to be reported by the individual insurance companies and not by the group.

The frequent reporting of significant transactions and exposures is an administrative burden to both insurance companies and the supervisory authorities.

Annual reporting of IGT may not, contain relevant information to enhance good supervision (e.g. because of time-lag).

Recommendation of CEIOPS