redefining the carrier cloud: a market forecast view

TRANSCRIPT

TBR

T EC H N O LO G Y B U S I N ES S R ES EAR C H , I N C .

Redefining the Carrier Cloud: A Market Forecast View

Technology Business Research Webinar Series

July 13, 2015

TBR

2 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

Your presenter

Michael Sullivan-Trainor

Executive Analyst, Telecom

Email: [email protected]

Twitter: @mikest

Carrier Cloud Webinar

TBR

3 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

Agenda

• Key Trends

• Revenue Forecast

• Market Leaders

• NFV-SDN Impact

• Leading Operators

• Leading Suppliers

• Supplier Opportunity

Carrier Cloud Webinar

TBR

4 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

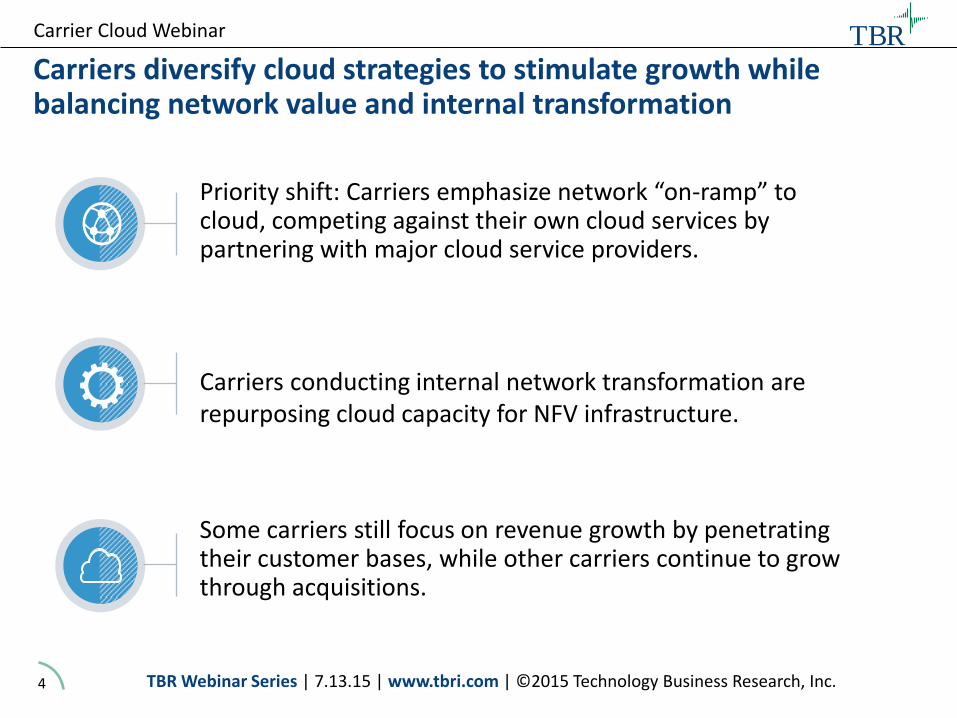

Carriers diversify cloud strategies to stimulate growth while balancing network value and internal transformation

Priority shift: Carriers emphasize network “on-ramp” to cloud, competing against their own cloud services by partnering with major cloud service providers.

Carriers conducting internal network transformation are repurposing cloud capacity for NFV infrastructure.

Some carriers still focus on revenue growth by penetrating their customer bases, while other carriers continue to grow through acquisitions.

Carrier Cloud Webinar

TBR

5 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

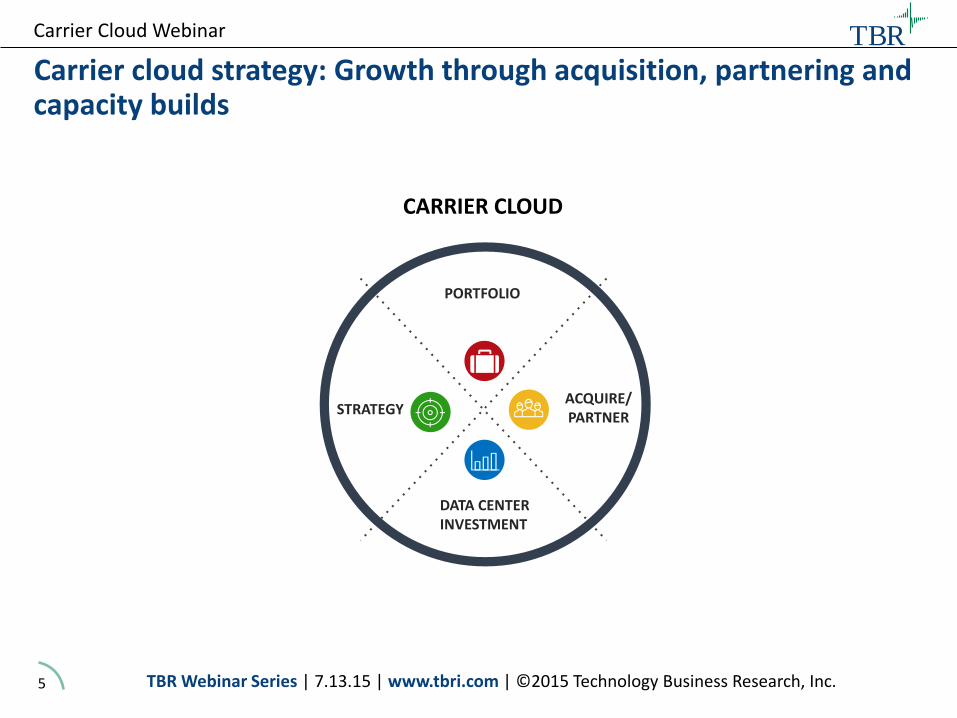

Carrier cloud strategy: Growth through acquisition, partnering and capacity builds

CARRIER CLOUD

STRATEGY

PORTFOLIO

DATA CENTER INVESTMENT

ACQUIRE/ PARTNER

Carrier Cloud Webinar

TBR

6 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

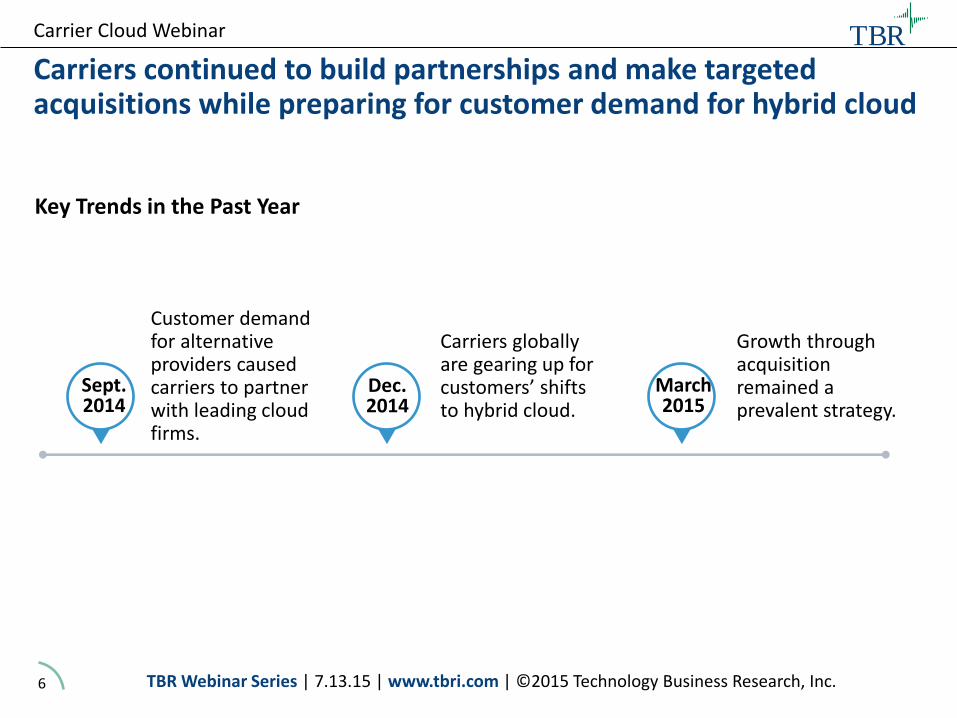

Carriers continued to build partnerships and make targeted acquisitions while preparing for customer demand for hybrid cloud

Customer demand for alternative providers caused carriers to partner with leading cloud firms.

Growth through acquisition remained a prevalent strategy.

Dec. 2014

March 2015

Sept. 2014

Carriers globally are gearing up for customers’ shifts to hybrid cloud.

Key Trends in the Past Year

Carrier Cloud Webinar

TBR

7 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

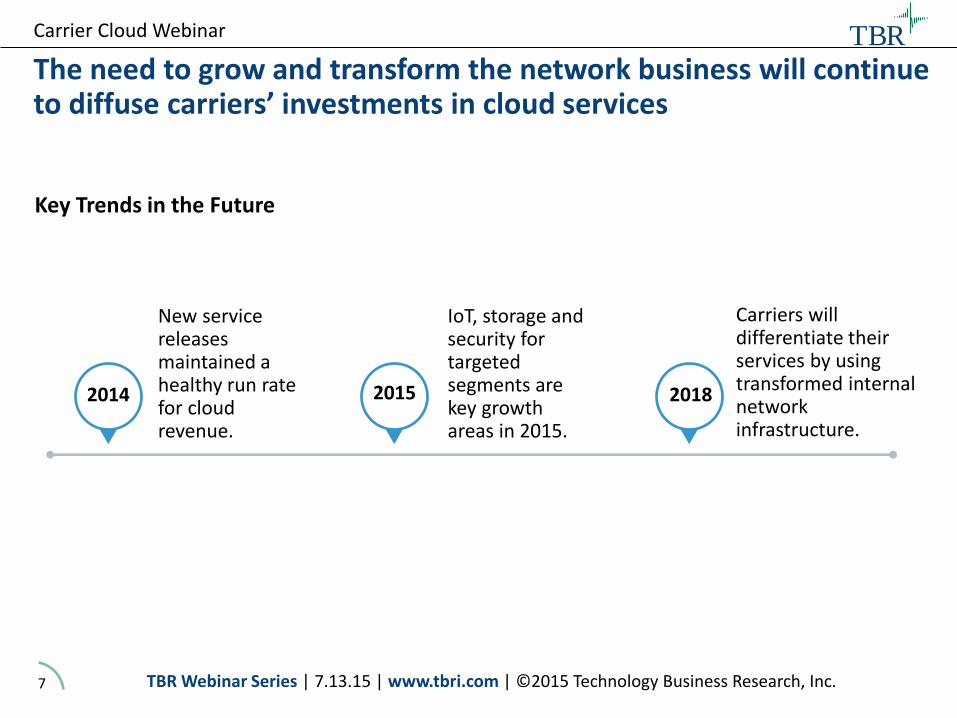

The need to grow and transform the network business will continue to diffuse carriers’ investments in cloud services

New service releases maintained a healthy run rate for cloud revenue.

Carriers will differentiate their services by using transformed internal network infrastructure.

2015 2018 2014

IoT, storage and security for targeted segments are key growth areas in 2015.

Key Trends in the Future

Carrier Cloud Webinar

TBR

8 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

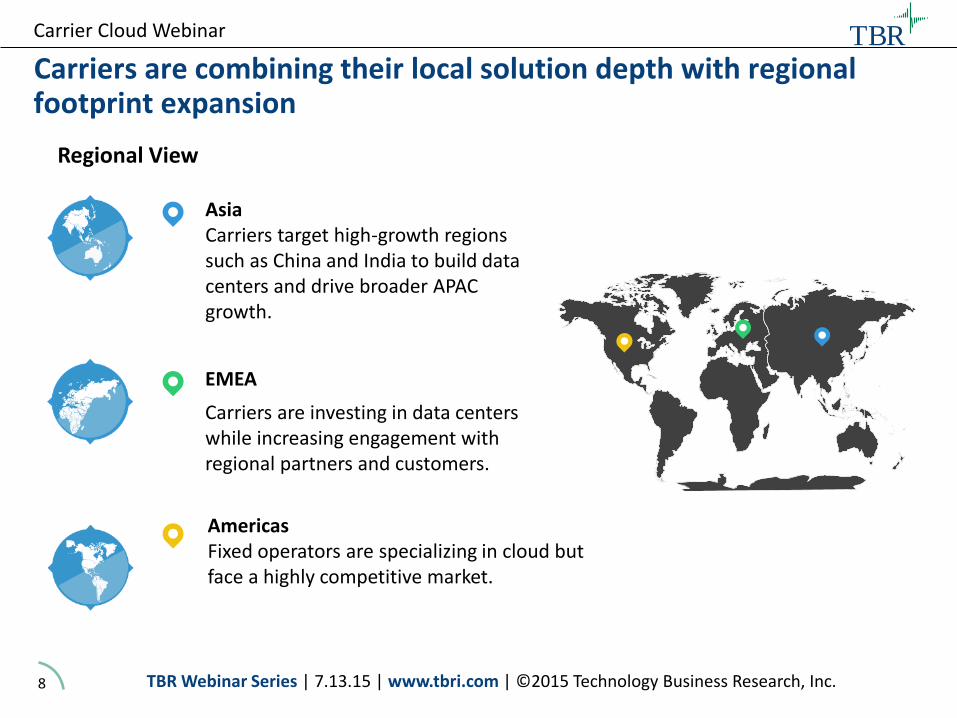

Carriers are combining their local solution depth with regional footprint expansion

Asia Carriers target high-growth regions such as China and India to build data centers and drive broader APAC growth.

EMEA

Carriers are investing in data centers while increasing engagement with regional partners and customers.

Americas Fixed operators are specializing in cloud but face a highly competitive market.

Regional View

Carrier Cloud Webinar

TBR

9 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

Cloud Service: Forecast

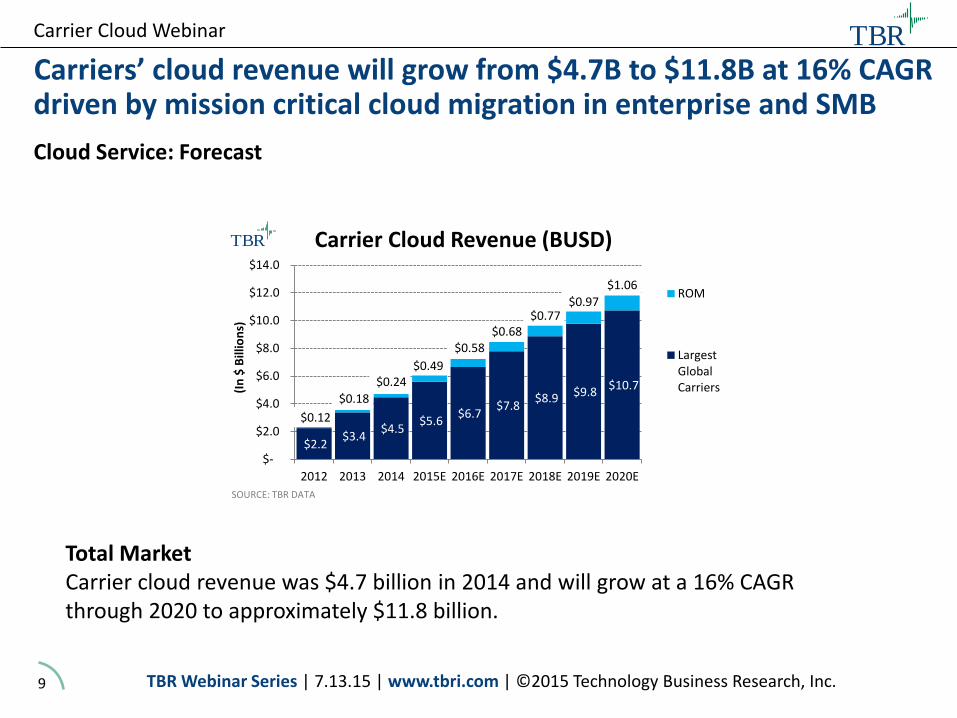

Carriers’ cloud revenue will grow from $4.7B to $11.8B at 16% CAGR driven by mission critical cloud migration in enterprise and SMB

Carrier Cloud Webinar

Total Market Carrier cloud revenue was $4.7 billion in 2014 and will grow at a 16% CAGR through 2020 to approximately $11.8 billion.

$2.2 $3.4

$4.5 $5.6

$6.7 $7.8

$8.9 $9.8 $10.7

$0.12

$0.18

$0.24 $0.49

$0.58 $0.68

$0.77 $0.97

$1.06

$-

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

2012 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E

(In

$ B

illio

ns)

Carrier Cloud Revenue (BUSD)

ROM

LargestGlobalCarriers

TBR

SOURCE: TBR DATA

TBR

10 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

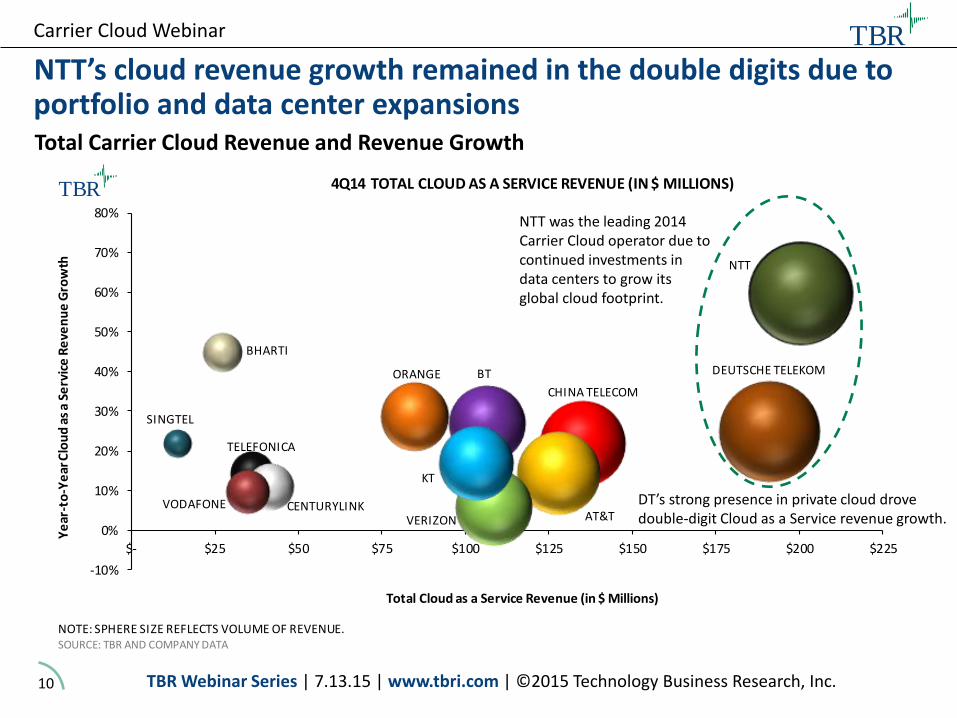

NTT

DEUTSCHE TELEKOM

CHINA TELECOM

AT&TVERIZON

BT

KT

ORANGE

TELEFONICA

CENTURYLINKVODAFONE

BHARTI

SINGTEL

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

$- $25 $50 $75 $100 $125 $150 $175 $200 $225

Ye

ar-t

o-Y

ear

Clo

ud

as

a Se

rvic

e R

eve

nu

e G

row

th

Total Cloud as a Service Revenue (in $ Millions)

4Q14 TOTAL CLOUD AS A SERVICE REVENUE (IN $ MILLIONS) TBR

NOTE: SPHERE SIZE REFLECTS VOLUME OF REVENUE.SOURCE: TBR AND COMPANY DATA

Total Carrier Cloud Revenue and Revenue Growth

NTT’s cloud revenue growth remained in the double digits due to portfolio and data center expansions

DT’s strong presence in private cloud drove double-digit Cloud as a Service revenue growth.

NTT was the leading 2014 Carrier Cloud operator due to continued investments in data centers to grow its global cloud footprint.

Carrier Cloud Webinar

TBR

11 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

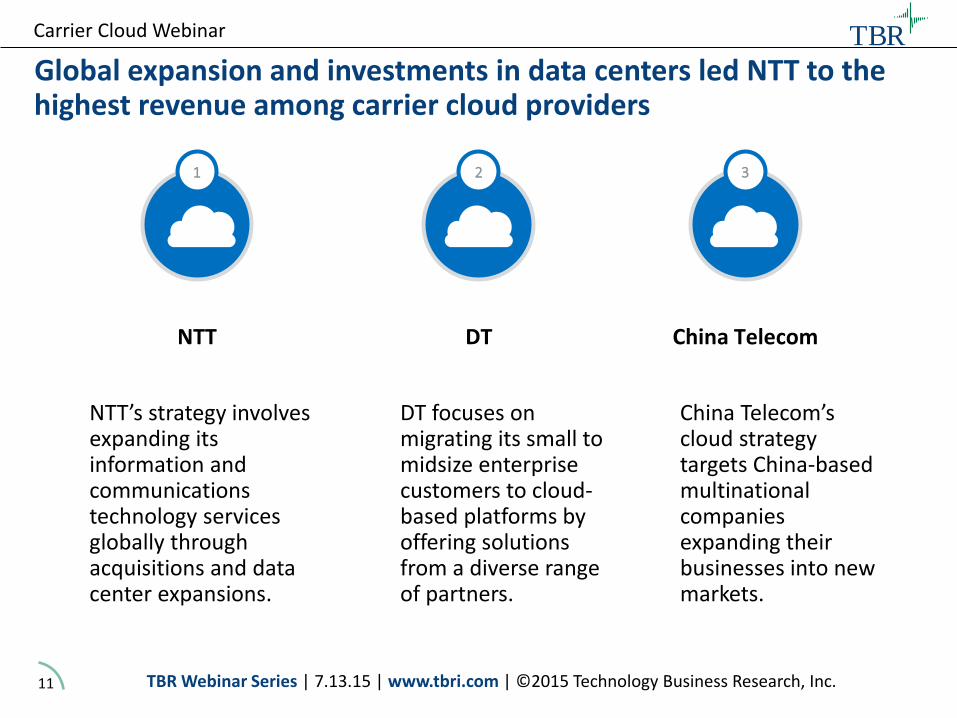

China Telecom

1

NTT

NTT’s strategy involves expanding its information and communications technology services globally through acquisitions and data center expansions.

China Telecom’s cloud strategy targets China-based multinational companies expanding their businesses into new markets.

2

DT

DT focuses on migrating its small to midsize enterprise customers to cloud-based platforms by offering solutions from a diverse range of partners.

Global expansion and investments in data centers led NTT to the highest revenue among carrier cloud providers

3

Carrier Cloud Webinar

TBR

12 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

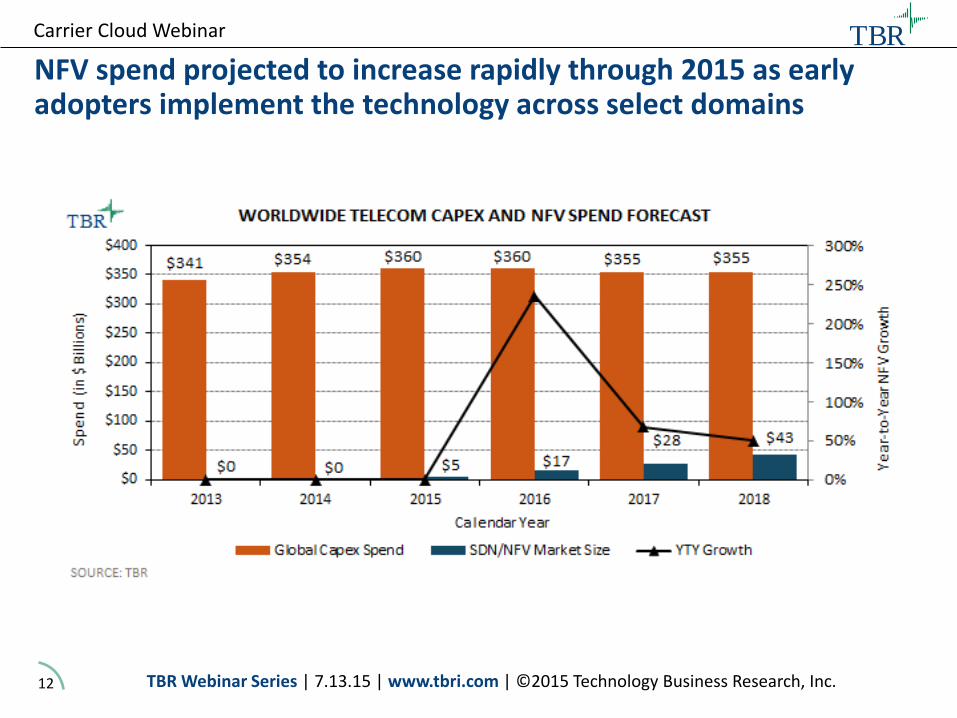

NFV spend projected to increase rapidly through 2015 as early adopters implement the technology across select domains

Carrier Cloud Webinar

TBR

13 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

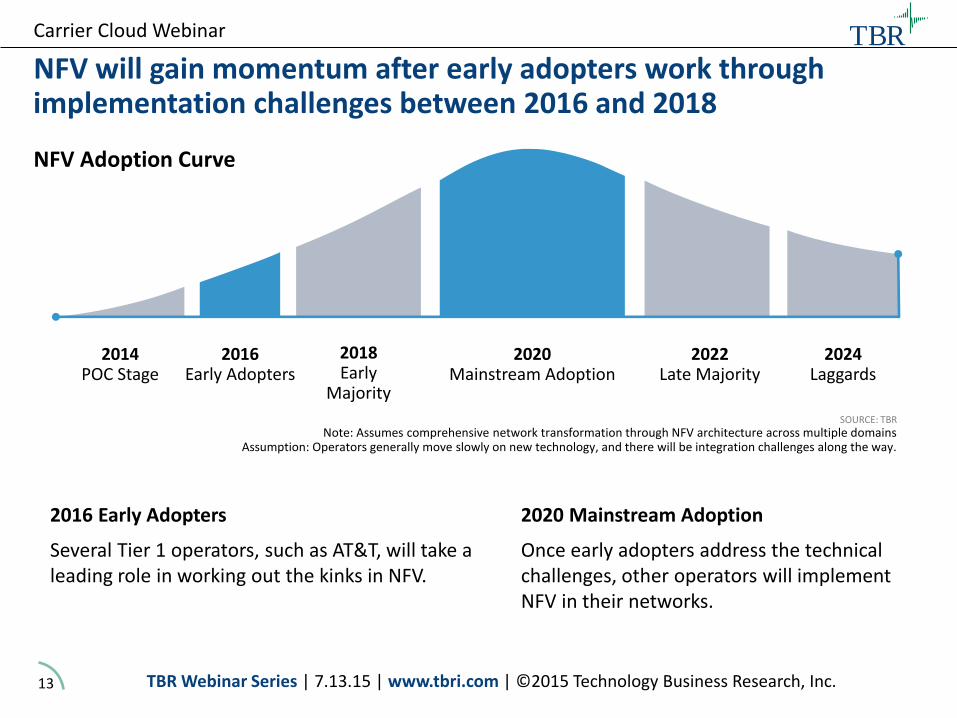

NFV will gain momentum after early adopters work through implementation challenges between 2016 and 2018

2014 POC Stage

2016 Early Adopters

2022 Late Majority

2024 Laggards

2018 Early

Majority

2020 Mainstream Adoption

SOURCE: TBR

Note: Assumes comprehensive network transformation through NFV architecture across multiple domains Assumption: Operators generally move slowly on new technology, and there will be integration challenges along the way.

NFV Adoption Curve

2016 Early Adopters 2020 Mainstream Adoption

Several Tier 1 operators, such as AT&T, will take a leading role in working out the kinks in NFV.

Once early adopters address the technical challenges, other operators will implement NFV in their networks.

Carrier Cloud Webinar

TBR

14 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

HIGH

HIGH LOW

Stra

tegi

c Im

po

rtan

ce

Rate of Adoption

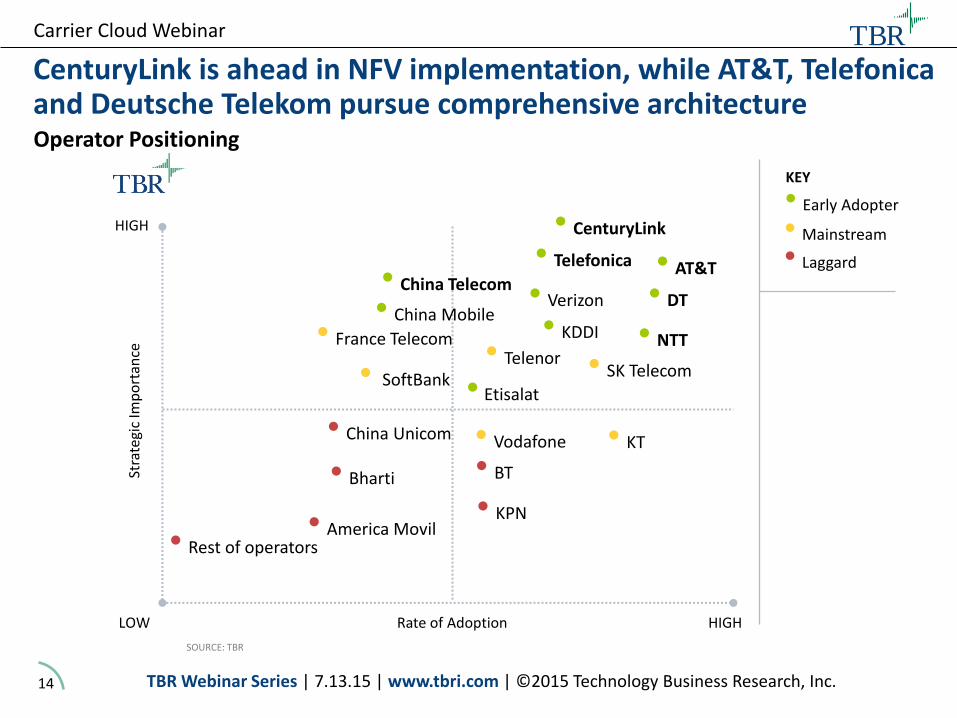

CenturyLink is ahead in NFV implementation, while AT&T, Telefonica and Deutsche Telekom pursue comprehensive architecture

• AT&T

• DT

• Telefonica

• NTT

• Vodafone

• China Telecom

• China Unicom

• Bharti • BT

• Rest of operators

• KPN

• Verizon

• KT

• Telenor

• KDDI

• SK Telecom • SoftBank

• America Movil

Operator Positioning

• CenturyLink

• France Telecom

• Early Adopter

• Mainstream

• Laggard

KEY

SOURCE: TBR

• Etisalat

• China Mobile

Carrier Cloud Webinar

TBR

15 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

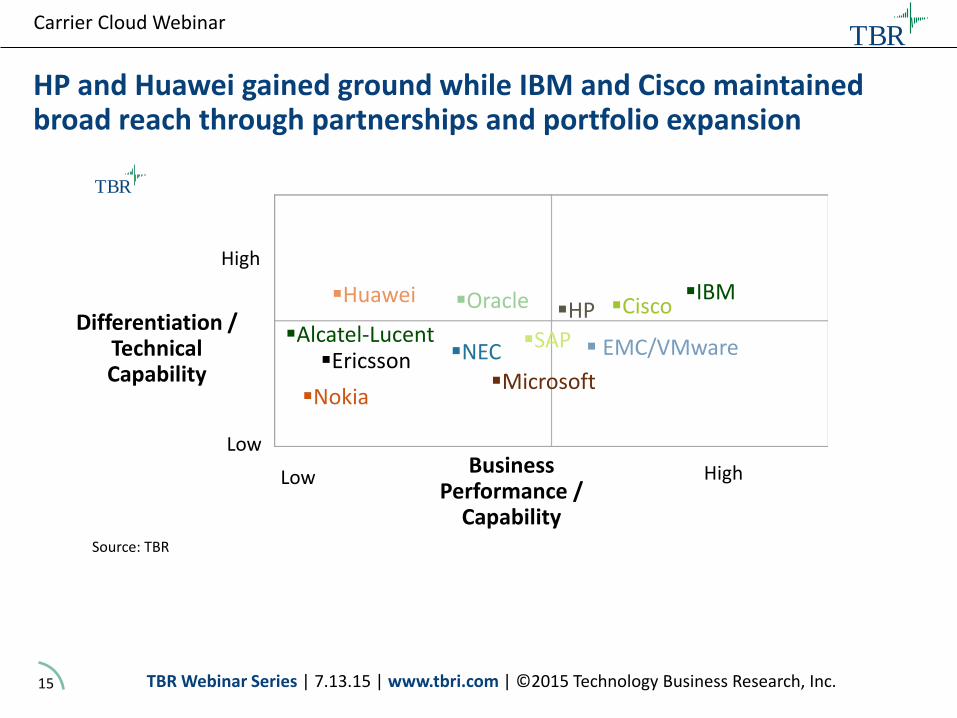

HP and Huawei gained ground while IBM and Cisco maintained broad reach through partnerships and portfolio expansion

Carrier Cloud Webinar

Differentiation / Technical Capability

Business Performance /

Capability

High

Low

High Low

Cisco

EMC/VMware

Microsoft

SAP

Oracle HP

IBM

Nokia

Huawei

Ericsson Alcatel-Lucent

NEC

TBR

Source: TBR

TBR

16 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

Vendor Revenue from Cloud Solutions

Vendor revenue from cloud solutions

Carrier Cloud Webinar

Total Market The market for cloud-related hardware and software was nearly $21.7 billion in 2014 and will grow at a 12% CAGR through 2019 to approximately $38.3 billion.

Key Segments

Hardware (servers, storage and data center networking) accounted for more than two-thirds of cloud components revenue in 2014 and will rise slowly as a percentage of revenue through 2019.

Fastest Growth Operations management and security software will post a leading CAGR of 15.1% from 2014 to 2019, reaching nearly $5.2 billion.

TBR

17 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

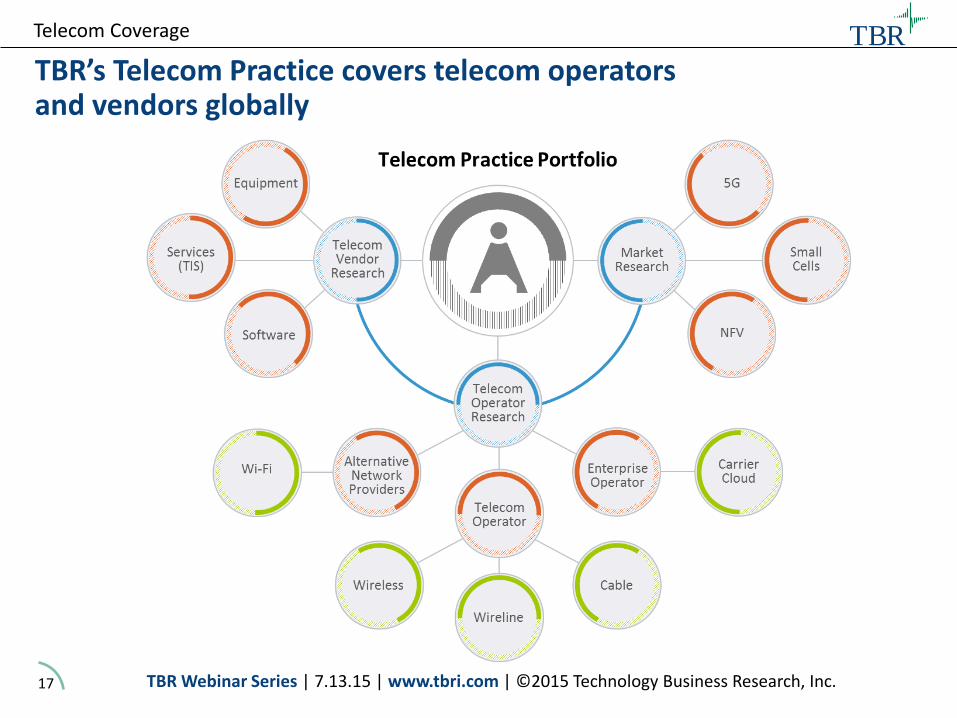

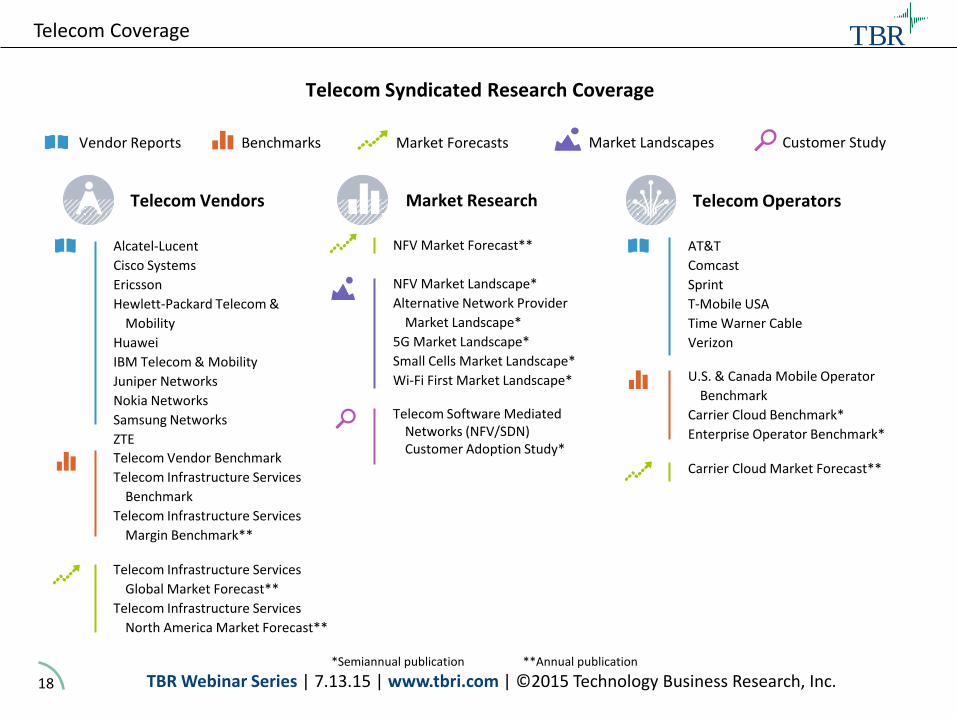

TBR’s Telecom Practice covers telecom operators and vendors globally

Telecom Coverage

TBR

18 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

Telecom Vendors

Telecom Syndicated Research Coverage

Market Research Telecom Operators

Alcatel-Lucent

Cisco Systems

Ericsson

Hewlett-Packard Telecom &

Mobility

Huawei

IBM Telecom & Mobility

Juniper Networks

Nokia Networks

Samsung Networks

ZTE

Telecom Infrastructure Services

Global Market Forecast**

Telecom Infrastructure Services

North America Market Forecast**

Telecom Vendor Benchmark

Telecom Infrastructure Services

Benchmark

Telecom Infrastructure Services

Margin Benchmark**

NFV Market Forecast** AT&T

Comcast

Sprint

T-Mobile USA

Time Warner Cable

Verizon

U.S. & Canada Mobile Operator

Benchmark

Carrier Cloud Benchmark*

Enterprise Operator Benchmark*

Carrier Cloud Market Forecast**

NFV Market Landscape*

Alternative Network Provider

Market Landscape*

5G Market Landscape*

Small Cells Market Landscape*

Wi-Fi First Market Landscape*

Telecom Software Mediated Networks (NFV/SDN) Customer Adoption Study*

*Semiannual publication **Annual publication

Vendor Reports Benchmarks Market Landscapes Market Forecasts Customer Study

Telecom Coverage

TBR

19 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

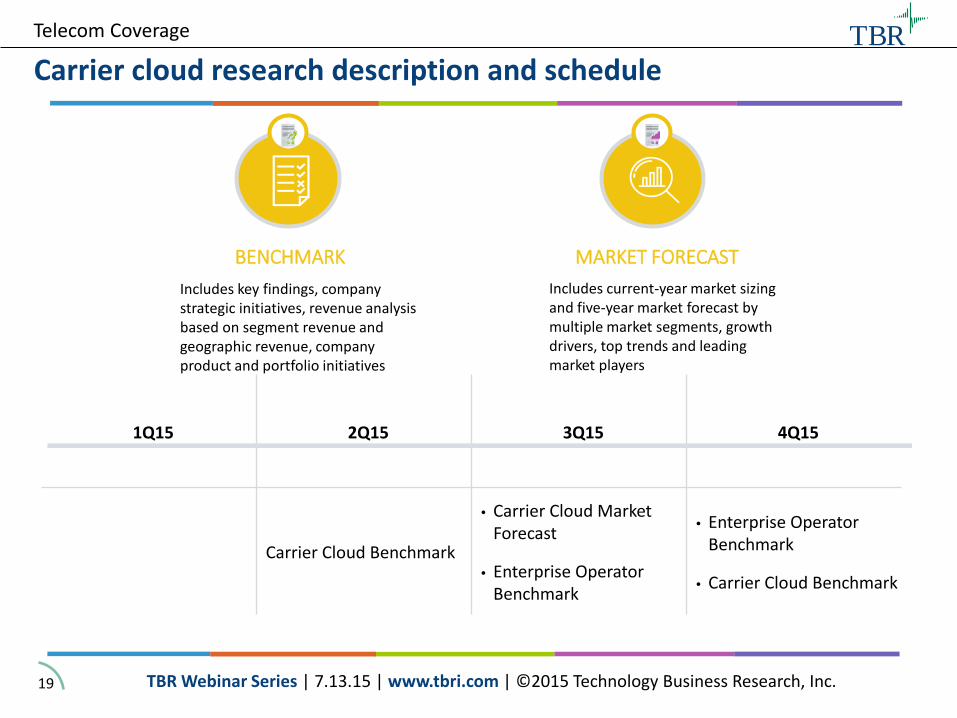

Carrier cloud research description and schedule

1Q15 2Q15 3Q15 4Q15

Carrier Cloud Benchmark

• Carrier Cloud Market Forecast

• Enterprise Operator Benchmark

• Enterprise Operator Benchmark

• Carrier Cloud Benchmark

BENCHMARK

Includes key findings, company strategic initiatives, revenue analysis based on segment revenue and geographic revenue, company product and portfolio initiatives

MARKET FORECAST

Includes current-year market sizing and five-year market forecast by multiple market segments, growth drivers, top trends and leading market players

Telecom Coverage

TBR

20 TBR Webinar Series | 7.13.15 | www.tbri.com | ©2015 Technology Business Research, Inc.

Questions?

Twitter: @TBRinc SlideShare: www.slideshare.net/TBR_Market_Insight YouTube: www.youtube.com/user/TBRIChannel LinkedIn: www.linkedin.com/company/technology-business-research

James McIlroy Vice President of Sales Email: [email protected] Telephone: 603.929.1166

Q&A

Michael Sullivan-Trainor

Executive Analyst, Telecom

Email: [email protected]

Twitter: @mikest

TBR

T EC H N O LO G Y B U S I N ES S R ES EAR C H , I N C .

About TBR Technology Business Research, Inc. is a leading independent technology market research and consulting firm specializing in the business and financial analyses of hardware, software, professional services, telecom and enterprise network vendors, and operators. Serving a global clientele, TBR provides timely and actionable market research and business intelligence in formats that are tailored to clients’ needs. Our analysts are available to further address client-specific issues or information needs on an inquiry or proprietary consulting basis. TBR has been empowering corporate decision makers since 1996. To learn how our analysts can address your unique business needs, please visit our website or contact us today.

Contact Us

1.603.929.1166 [email protected] www.tbri.com 11 Merrill Drive Hampton, NH 03842 USA

This report is based on information made available to the public by the vendor and other public sources. No representation is made that this information is accurate or complete. Technology Business Research will not be held liable or responsible for any decisions that are made based on this information. The information contained in this report and all other TBR products is not and should not be construed to be investment advice. TBR does not make any recommendations or provide any advice regarding the value, purchase, sale or retention of securities. This report is copyright-protected and supplied for the sole use of the recipient. Contact ©Technology Business Research, Inc. for permission to reproduce.