refineries in canada - squarespace · current status of refineries in canada ... mismatch between...

TRANSCRIPT

Relevant • Independent • Objectivewww.ceri.ca1

Refineries in Canada

Canadian Energy Research Institute

Dinara MillingtonCanadian Energy Research Institute

November 23-24, 2015Grand Challenge Forum: “Responsible Development of Low Permeability Hydrocarbon Resources”

Relevant • Independent • Objectivewww.ceri.ca2

Canadian Energy Research Institute

Founded in 1975, the Canadian Energy Research Institute (CERI) is an independent, not-for-profit research institute specializing in the analysis of energy economics and relatedenvironmental policy issues in the energy production, transportation, and consumptionsectors.

Our mission is to provide relevant, independent, and objective economic research ofenergy and environmental issues to benefit business, government, academia and thepublic.

Our core supporters include the Government of Canada (Natural Resources Canada), theGovernment of Alberta (Alberta Energy), the Canadian Association of PetroleumProducers (CAPP), and the University of Calgary. In-kind support is also provided by theAlberta Energy Regulator (AER) and the Petroleum Services Association of Canada(PSAC).

All of CERI’s research is placed in the public domain and can be accessed via our websiteat www.ceri.ca .

Celebrating 40 Years of Quality Research

Relevant • Independent • Objectivewww.ceri.ca3

Canadian Energy Research InstituteAgenda

• Current Status of Refineries in Canada

• Economics of Refining Business

• CERI’s Analysis of building a refinery in Alberta

• Conclusions

Relevant • Independent • Objectivewww.ceri.ca4

Current Status of Canadian Refineries

Relevant • Independent • Objectivewww.ceri.ca5

Other Plants with Crude Processing CapacityLocation Province Plant Capacity (b/d)

Asphalt Plants

Lloydminster SK Husky Energy 29,000

Moose Jaw SK Moose Jaw Refinery 15,000

Petrochemical Plants (currently using crude oil as feedstock)

Sarnia ON Nova Chemicals 80,000

Mississauga ON Suncor Lubricants 16,000

Upgraders*

Fort McMurray AB Syncrude 474,000

Fort McMurray AB Suncor Base U1/U2 267,000

Fort McMurray AB Suncor Millenium 90,000

Fort Sask AB Shell Scotford 255,000

Fort McKay AB CNRL Horizon 114,000

Wood Buffalo AB Nexen-CNOOC 72,000

Lloydminster SK Husky Energy 82,000

Relevant • Independent • Objectivewww.ceri.ca6

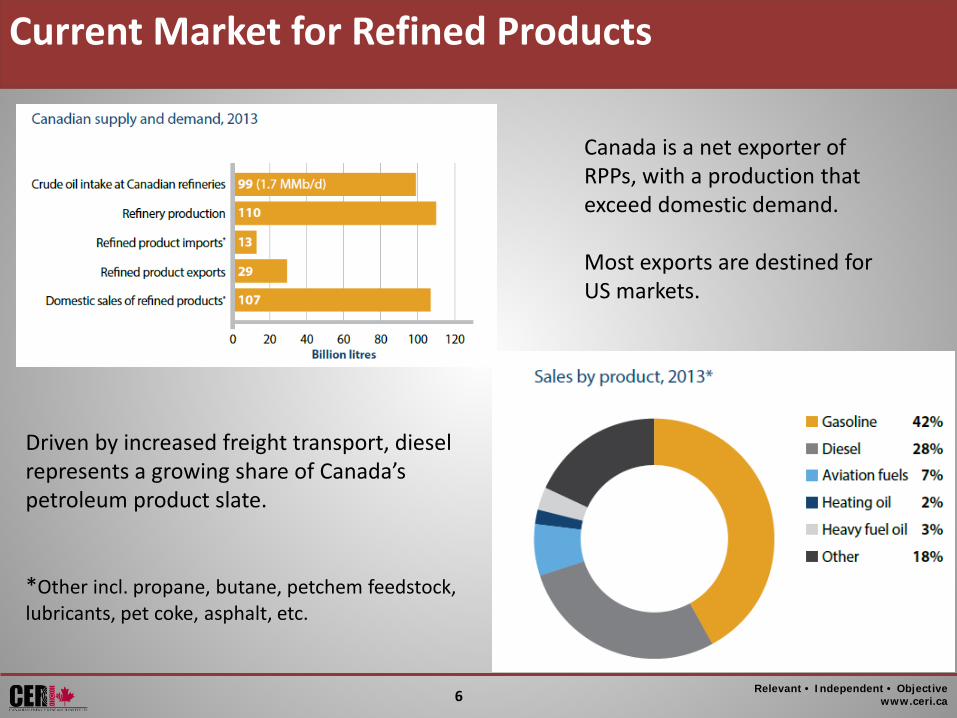

Current Market for Refined Products

Canada is a net exporter of RPPs, with a production that exceed domestic demand.

Most exports are destined for US markets.

Driven by increased freight transport, diesel represents a growing share of Canada’s petroleum product slate.

*Other incl. propane, butane, petchem feedstock, lubricants, pet coke, asphalt, etc.

Relevant • Independent • Objectivewww.ceri.ca7

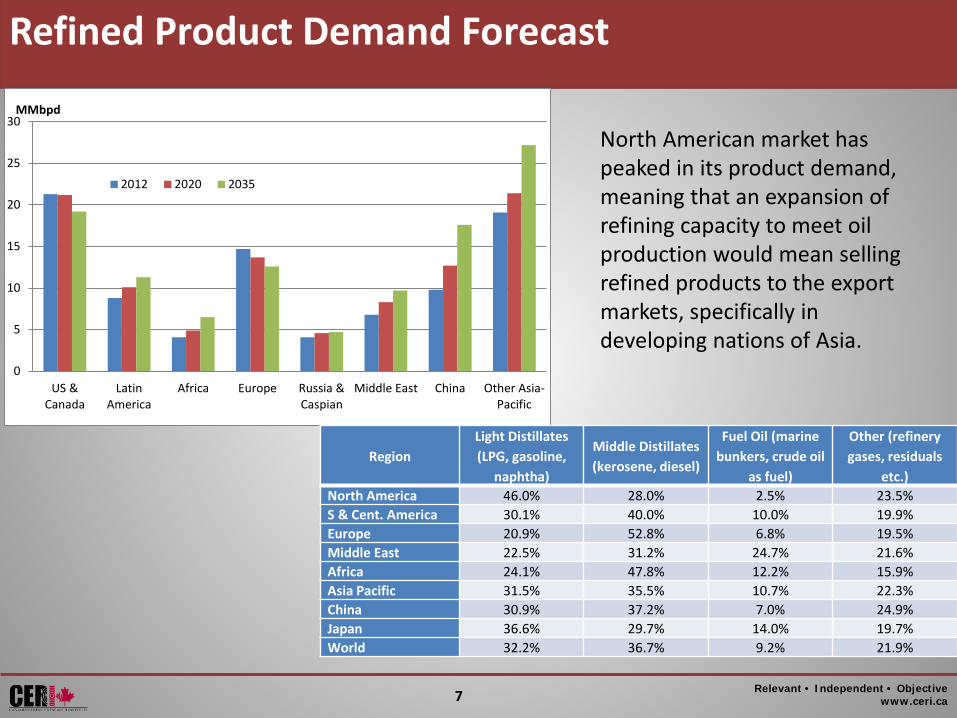

Refined Product Demand Forecast

0

5

10

15

20

25

30

US &Canada

LatinAmerica

Africa Europe Russia &Caspian

Middle East China Other Asia-Pacific

MMbpd

2012 2020 2035

RegionLight Distillates (LPG, gasoline,

naphtha)

Middle Distillates (kerosene, diesel)

Fuel Oil (marine bunkers, crude oil

as fuel)

Other (refinery gases, residuals

etc.)North America 46.0% 28.0% 2.5% 23.5%S & Cent. America 30.1% 40.0% 10.0% 19.9%Europe 20.9% 52.8% 6.8% 19.5%Middle East 22.5% 31.2% 24.7% 21.6%Africa 24.1% 47.8% 12.2% 15.9%Asia Pacific 31.5% 35.5% 10.7% 22.3%China 30.9% 37.2% 7.0% 24.9%Japan 36.6% 29.7% 14.0% 19.7%World 32.2% 36.7% 9.2% 21.9%

North American market has peaked in its product demand, meaning that an expansion of refining capacity to meet oil production would mean selling refined products to the export markets, specifically in developing nations of Asia.

Relevant • Independent • Objectivewww.ceri.ca8

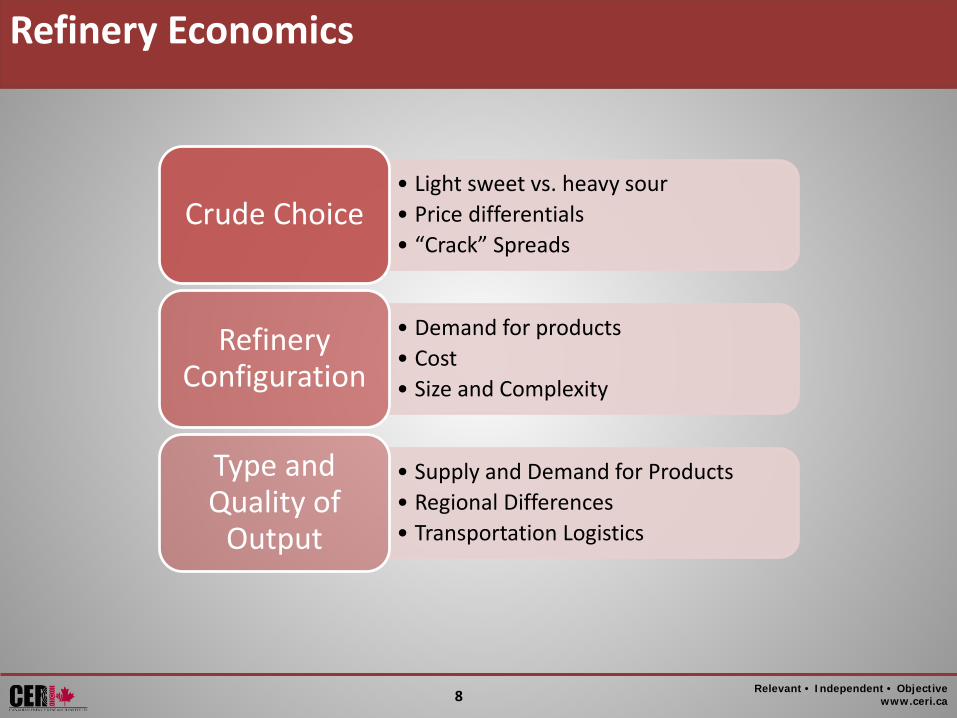

Refinery Economics

• Light sweet vs. heavy sour• Price differentials• “Crack” Spreads

Crude Choice

• Demand for products• Cost• Size and Complexity

Refinery Configuration

• Supply and Demand for Products• Regional Differences• Transportation Logistics

Type and Quality of

Output

Relevant • Independent • Objectivewww.ceri.ca9

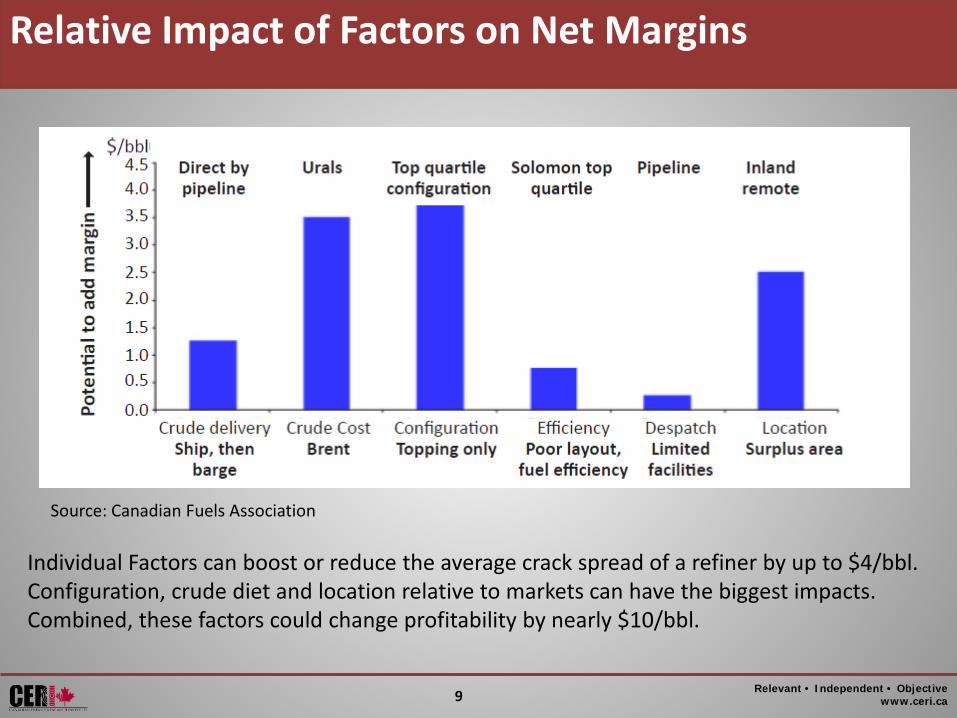

Relative Impact of Factors on Net Margins

Source: Canadian Fuels Association

Individual Factors can boost or reduce the average crack spread of a refiner by up to $4/bbl. Configuration, crude diet and location relative to markets can have the biggest impacts. Combined, these factors could change profitability by nearly $10/bbl.

Relevant • Independent • Objectivewww.ceri.ca10

Canadian Refinery Business

• Three distinct geographical regions:

Western Canada – land-locked, local production abundant Ontario – access to both domestic and foreign crudes Quebec and Atlantic Canada – importing foreign crudes is more economic than

cost of transporting crude from Western provinces

Mismatch between available domestic feedstock and domestic refinery configuration

Transportation Distances

Complexity of Canadian Refineries

Global RPP Market Dynamics

Refining Capacity in North America

Relevant • Independent • Objectivewww.ceri.ca11

CERI Study 145: “Refining Bitumen”

In this study CERI conducted a preliminary cost-benefit analysis (CBA) of building and operating a greenfield refinery

The CBA results suggest that a greenfield commercial refinery project is net socially beneficial across a typical discount rate range (13-15 percent) for the refinery business but:

If the average WTI price drops below $85/bbl over the life of the project – the project would be a net cost to society.

With current and expected level of crude prices in near-term (2016-2018), it is uneconomic to build new greenfield refineries, although….

Expansions/re-configurations to existing facilities to meet the changing demand and process other crude slates are possible.

Relevant • Independent • Objectivewww.ceri.ca12

CERI Study 145: Sensitivity Analysis

-3,000 -2,000 -1,000 0 1,000 2,000 3,000 4,000

Disc.Rate for Emissions Social Costs (0%)

Disc.Rate for Emissions Social Costs (1%)

Operating Costs (25% change)

Financing Debt (10% change)

Oil Prices (20% change)

Diesel Prices (20% change)

CCS Unit (No)

Capital Costs (25% change)

Discount Rate (2% change)

NPV (2013 Mln CDN$)

Decrease in NPV

Baseline NPV

Increase in NPV

NPV Sensitivity Analysis:

Relevant • Independent • Objectivewww.ceri.ca13

Conclusions

The economics of the refining business are complex. As a capital intensive manufacturing industry operating between the two related but independent markets for crude oil and finished petroleum products, refining is a challenging business.

Profitable operations that deliver adequate returns on investment are a function of a complex set of variables underpinned by basic supply and demand dynamics, and shaped by competition that is increasingly global in nature.

Refiners must strive to maximize their margins by optimizing a number of variables. They operate in a business environment that is dynamic, and that comes with varying levels of commercial, technical, regulatory and economic risks.

Declining demand and excess refining capacity create challenging market conditions for refiners in North America, and especially Canada.

Fuel demand is growing in Asia, and represents a potential new market for Canada – a market that theoretically could be supplied by refining Canadian bitumen.

Relevant • Independent • Objectivewww.ceri.ca14

Thank you!

www.ceri.ca