refit forum 2 february 2018 slides - ey.com · avon cosmetics cjeu judgment in avon cosmetics ltd...

TRANSCRIPT

ReFIT Forum

2nd February 2018

WelcomeSimon Baxter – Indirect Tax Retail Sector Leader

2nd October 2018

Agenda

10.30 Welcome and introduction Simon Baxter

Caselaw update Emma Hughes

IFRS accounting update Kevin Paterson & JohnO’Connell

Boehringer Ingelheim – cashback opportunity Simon Baxter

11.30 Coffee

11.45 Hot topics Ethan Ding

Brexit update including people aspects Rosemarie McGuire andSimon Baxter

Global VAT update Saleena Beedassy

13:00 Open Forum/Close/Buffet Lunch

ReFIT Forum - 2nd February 2018

Emma Hughes

2nd February 2018

Caselaw update

Agenda – case law update

Case law reviewØ Phoenix Foods Limited – First-tier Tribunal (‘FTT’) Judgment

Ø Avon Cosmetics – Court of Justice of the European Union (‘CJEU’) Judgment

Ø DPAS – referral to the CJEU

Noteworthy casesØ United Biscuits (Pensions Trustees) Limited and United Biscuits Pension

Investments LimitedØ Di MauraØ Littlewoods Limited and Others

ReFIT Forum - 2nd February 2018

Phoenix Foods Limited (‘Phoenix’)

First-tier Tribunal (‘FTT’) decision

Summary: Bicarbonate of Soda is zero rated as a supply of food of a kind used for humanconsumption

The case considers whether bicarbonate of soda (BoS), sold as a baking ingredient, is ‘food of akind used for human consumption’ and so zero-rated for VAT purposes under VATA94, Schedule 8,Group 1, Item 1.

Facts: Phoenix supplies dried powdered and granular products to food retailers. Phoenixpurchased supplies of BoS in bulk and packaged it for sale to supermarkets.

The packaging referred to BoS as:

‘a versatile raising agent for soda bread, cookies and gingerbread’ (Tesco own-brand)

‘a gentle raising agent for use in sticky toffee pudding, cookies, gingerbread, soda bread and a widerange of recipes’ and ‘can also be used around the house as a cleaner, deodoriser and mildabrasive’. (Lidl under the brand ‘Belbake’)

At the time, the packaging also referred to the fact that BoS ‘can also be used around the houseas a cleaner, deodoriser and mild abrasive’.

Phoenix treated all of its supplies of BoS to Tesco and to Lidl as zero rated for VAT purposes.HMRC advised Phoenix that BoS should be treated as standard rated regardless of its usage.HMRC considered BoS to be a generic item with multiple uses.

ReFIT Forum - 2nd February 2018

Phoenix Foods Limited (‘Phoenix’)

First-tier Tribunal decision

The question of whether or not it should be regarded as ‘food of a kind used for humanconsumption’ should be determined by the nature of the product and not how it is marketed.The FTT highlighted that the supplies made by Phoenix, which are the subject of this appeal, wereintended to be used primarily as a baking ingredient. The sales were made to leadingsupermarkets; although the packaging of the Belbake product sold to Lidl did suggest that theremay be other uses for the product, the packaging was consistent with the primary intended use ofthe BoS being that of a culinary ingredient.

In allowing the appeal, the FTT considered that:• BoS is an essential ingredient in some bread and cakes• It is critical to the texture of such foods and texture, alongside taste, is an important attribute

of food• When it is used as a baking ingredient, it is added purely as a leavening agent, however its

addition is not purely cosmetic.• The supplies in this case were clearly intended to be used primarily as a baking ingredient

ReFIT Forum - 2nd February 2018

Phoenix Foods Limited (‘Phoenix’)

First-tier Tribunal decision

• The FTT held that in a case where a product might have various uses, the intended use of theproduct, as determined from the form of the packaging and the manner in which it is to besold, is part of the facts and circumstances surrounding the supply that should be taken intoaccount in determining its classification.

Comment:

• This case raises a number of issues as to what should be considered as ‘food’ and HMRC'sapproach in classifying products differently according to their intended use.

• Although the case concerned bicarbonate of soda it applies equally to all other products(whether ingredients or foods in their own right) which are properly classed, on a commonsense test, as being food of a kind used for human consumption. A second non-food use for aproduct need not deny it zero-rating if use as a food was the primary purpose.

ReFIT Forum - 2nd February 2018

Avon Cosmetics

CJEU Judgment

In Avon Cosmetics Ltd C-306/16, the CJEU has rejected a claim that a derogation from EU law whichauthorised the UK to charge VAT on sales by direct selling companies based on their open marketvalue, was unlawful.Background• To re-cap - Avon sells beauty products in the UK to representatives, known as “Avon ladies”, who in

turn make the retail sale to their customers. Avon sells its goods to the Avon ladies at a discount fromthe “brochure prices” of either 20% or 25%, so that unless they pass on some of that discount to theircustomers, the 20% or 25% represents gross profit.

• The majority of the Avon ladies have modest turnover and are not therefore registered for VAT.• The consequence of this ordinarily would be that VAT would be charged on Avon only on the

consideration received by it on the sales to the representatives and no VAT would be charged inrespect of the retail sales.

• In order to ensure that this direct selling model does not result in profits on retail sales escaping VAT,HMRC obtained a derogation allowing it to direct companies like Avon to account for VAT on the retailprice: the company might sell goods for £75, but had to account for VAT on a final selling price of£100.

• Avon challenged the lawfulness of the derogation on the basis that it was charged output tax asthough its sales force was VAT-registered but no allowance was made for sales of samples, etc to theAvon ladies on which no input tax was recoverable, putting Avon in a worse position than itscompetitors.

ReFIT Forum - 2nd February 2018

Avon Cosmetics

CJEU Judgment

Judgments:

• The FTT agreed with Avon but said that it did not have jurisdiction to amend the derogation or declare it invalid.The FTT therefore decided to refer the matter to the CJEU.

• Advocate General Bobek released his opinion on 7 September 2017, in which he considered that the derogationfor direct selling could not be applied with modifications so as to enable the Avon ladies to recover input tax.

• CJEU’s judgment -The CJEU followed Advocate General Bobek’s earlier opinion and concluded that thederogation did not infringe the principle of fiscal neutrality and could not be modified for the Avon ladies.

• The CJEU has held that the UK acted lawfully in its failure to provide for VAT deduction in respect of costs borneby sales representatives, whilst holding the taxpayer (on selling to those representatives) liable to VAT on theretail open market selling price received by the representatives.

• Further, as the derogation is an anti-avoidance measure concerning the value of the taxable amount of the supply,the CJEU considered that the resulting input tax implications were not fundamental to the derogation. On thisbasis, the CJEU held that the European Commission did not need to be notified specifically about the failure ofthe derogation to provide for VAT deduction in respect of costs borne by sales representatives when the UKsought authorisation to use the derogation.

Comment

• Businesses which have implemented this type of operating model will be disappointed with the CJEU's judgment,which results in ‘sticking tax’ at the business level. Affected businesses may wish to consider whether to use analternative operating model going forward.

ReFIT Forum - 2nd February 2018

DPAS – referral to the CJEU

ReFIT Forum - 2nd February 2018

Background - DPAS administered dental plans, whereby a patient paid DPAS a fixed sum each month by direct debit tocover the costs of their dental maintenance and insurance cover for emergency treatment. After deducting its fee and theinsurance premium, DPAS paid the rest of the money collected over to the dentists. A £10 registration fee was added tothe first payment.As a result of the CJEU decision in Axa UK (C-175/09), DPAS’s supplies would have been wholly standard rated witheffect from 1 January 2012 as debt collection services supplied to the dentists. To avoid this VAT treatment, DPASrestructured its supplies.It changed the contracts in January 2012 to create two supplies: A taxable contract with the dentist, and an exemptpayment handling contract with the patient. The original FTT found for the taxpayer. HMRC appealed to the UT.The UT’s first decision:• The new arrangements and corresponding VAT treatment could not apply to existing customers that failed to return an

acceptance form (taxpayer loss);• The £10 registration fee paid by customers could not be ancillary to an exempt supply but was a separate standard

rated supply (taxpayer loss); and• The arrangements could apply to existing customers that returned the acceptance form and to new customers and the

arrangements were not abusive (taxpayer win).

The questions concerning whether the supply to customers fell within the payments exemption or whether the serviceswere excluded from exemption as supplies of debt collection were stayed awaiting the CJEU judgments in Bookit andNEC. Ultimately the UT concluded that a reference to the CJEU is required.Comment: The decision clearly sets out the difficulty of determining the scope of the exemption and even refers to thetension between Axa, NEC & Bookit. Clear guidance on the meaning of debt collection and the scope of the paymentexception is welcomed.

Questions referred

In the light of Article 135(1)(d) of Council Directive 2006/112/EC1 (the Principal VAT Directive) and the interpretations of thatprovision given by the Court of Justice in AXA, Bookit II and NEC, the Upper Tribunal (Tax and Chancery Chamber) respectfullyrefers the following questions to the Court of Justice of the European Union for a preliminary ruling:

1. Is a service, such as that performed by the taxpayer in the present case, consisting of directing, pursuant to a direct debitmandate, that money is taken by direct debit from a patient’s bank account and passed by the taxpayer, after deduction of thetaxpayer’s remuneration, to the patient’s dentist and insurance provider, an exempt supply of transfer or payment services withinArticle 135(1)(d) of the Principal VAT Directive?

2. In particular, do the decisions in Bookit II and NEC lead to the conclusion that the exemption from VAT in Article 135(1)(d) is notapplicable to a service, such as that performed by the taxpayer in the present case, which does not involve the taxpayer itselfdebiting or crediting any accounts over which it has control but which, where a transfer of funds results, is essential to thattransfer? Or does the decision in AXA lead to the contrary conclusion?

3. What are the relevant principles to be applied for determining whether or not a service such as that performed by the taxpayer inthe present case falls within the scope of ‘debt collection’ within Article 135(1)(d)? In particular, if (as the Court decided in AXA inrelation to the same or a very similar service) such a service would constitute debt collection if provided to the person to whomthe payment is due (i.e. the dentists in the present case and in AXA), does that service also constitute debt collection if such aservice is provided to the person from whom the payment is due (i.e. the patients in the present case)?

DPAS – referral to the CJEU

ReFIT Forum - 2nd February 2018

Case lawNoteworthy cases

United Biscuits (Pensions Trustees) Limited and United Biscuits Pension Investments Limited► In a loss for the taxpayer, the High Court’s key finding is that non-insurer’s fund management supplies to defined

benefit schemes are subject to VAT.

C-246/16 Di Maura► The CJEU held that the VAT Directive does not permit a disproportionate restriction of the possibility of adjusting VAT

via a claim for BDR. It does, however, permit Member States to take into account the uncertainties surrounding non-payment by requiring the taxable person to take certain reasonable measures. However, the requirement thatinsolvency proceedings be concluded in relation to the customer represents a disproportionate restriction. This is notan issue in the UK but is in many other EU jurisdictions.

Littlewoods Limited and Others► The Supreme Court has disagreed with the Court of Appeal and held that the Littlewoods claimants are not entitled to

compound interest. The Supreme Court considered that the payment of simple interest in this case cannotrealistically be regarded as having deprived Littlewoods of an adequate indemnity.

ReFIT Forum - 2nd February 2018

Contacts

ReFIT Forum - 2nd February 2018

Questions?

Kevin Paterson and John O’Connell

2nd February 2018

IFRS Lease Accounting Update

Introductions

Emily BrowneAssociate PartnerFinancial Accounting Advisory ServicesTel: +44 (0) 207 951 6500Email: [email protected]

Kevin PatersonPartnerInternational Tax ServicesTel: +44 (0) 207 951 1347Email: [email protected]

ReFIT Forum - 2nd February 2018

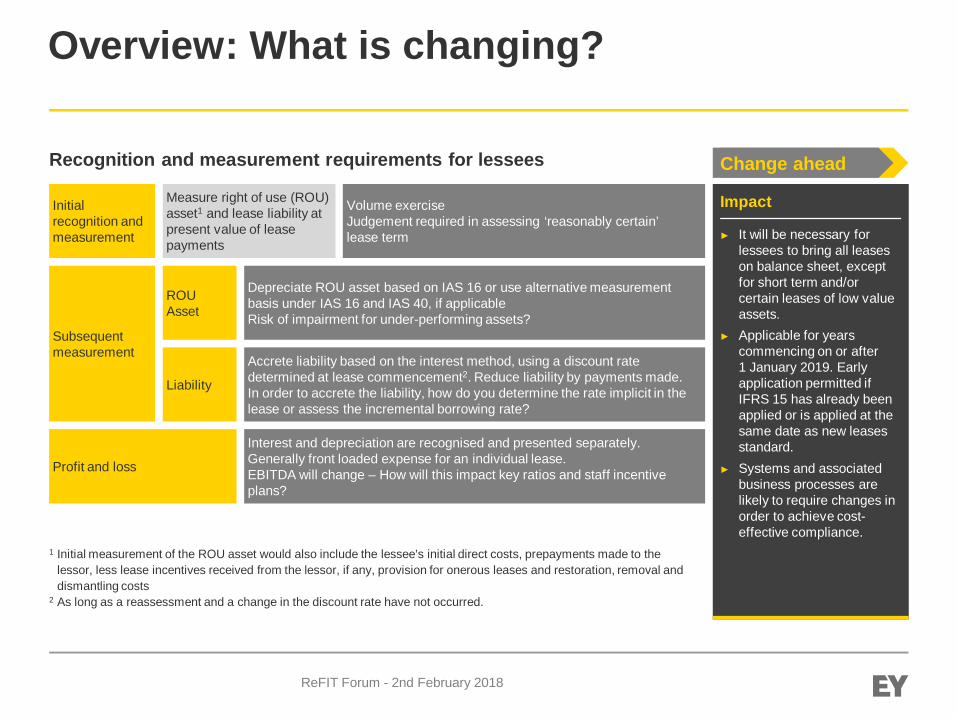

Overview: What is changing?

Change ahead

Impact

► It will be necessary forlessees to bring all leaseson balance sheet, exceptfor short term and/orcertain leases of low valueassets.

► Applicable for yearscommencing on or after1 January 2019. Earlyapplication permitted ifIFRS 15 has already beenapplied or is applied at thesame date as new leasesstandard.

► Systems and associatedbusiness processes arelikely to require changes inorder to achieve cost-effective compliance.

Recognition and measurement requirements for lessees

Initialrecognition andmeasurement

Measure right of use (ROU)asset1 and lease liability atpresent value of leasepayments

Subsequentmeasurement

ROUAsset

Liability

Depreciate ROU asset based on IAS 16 or use alternative measurementbasis under IAS 16 and IAS 40, if applicableRisk of impairment for under-performing assets?

Accrete liability based on the interest method, using a discount ratedetermined at lease commencement2. Reduce liability by payments made.In order to accrete the liability, how do you determine the rate implicit in thelease or assess the incremental borrowing rate?

Profit and loss

Interest and depreciation are recognised and presented separately.Generally front loaded expense for an individual lease.EBITDA will change – How will this impact key ratios and staff incentiveplans?

Volume exerciseJudgement required in assessing ‘reasonably certain’lease term

1 Initial measurement of the ROU asset would also include the lessee’s initial direct costs, prepayments made to thelessor, less lease incentives received from the lessor, if any, provision for onerous leases and restoration, removal anddismantling costs

2 As long as a reassessment and a change in the discount rate have not occurred.

ReFIT Forum - 2nd February 2018

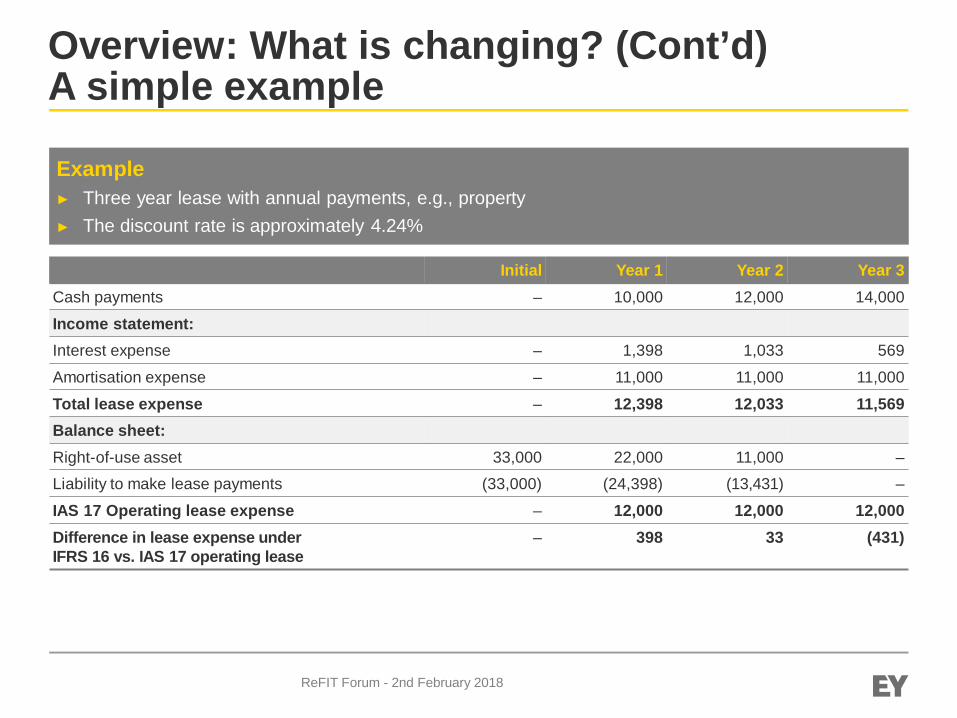

Overview: What is changing? (Cont’d)A simple example

Example► Three year lease with annual payments, e.g., property► The discount rate is approximately 4.24%

Initial Year 1 Year 2 Year 3Cash payments – 10,000 12,000 14,000Income statement:Interest expense – 1,398 1,033 569Amortisation expense – 11,000 11,000 11,000Total lease expense – 12,398 12,033 11,569Balance sheet:Right-of-use asset 33,000 22,000 11,000 –Liability to make lease payments (33,000) (24,398) (13,431) –IAS 17 Operating lease expense – 12,000 12,000 12,000Difference in lease expense underIFRS 16 vs. IAS 17 operating lease

– 398 33 (431)

ReFIT Forum - 2nd February 2018

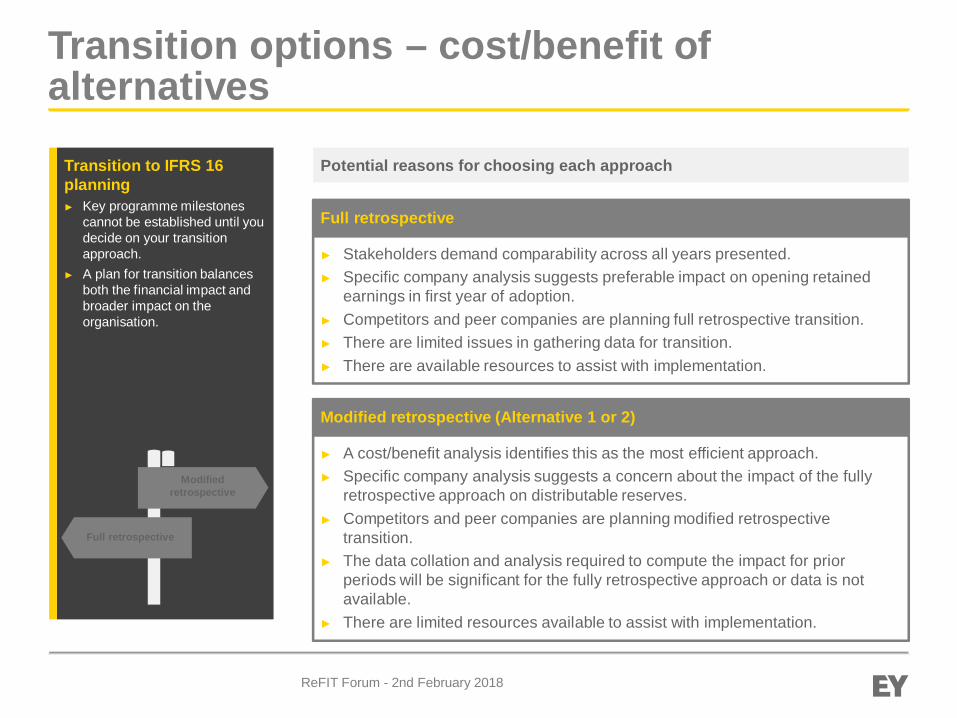

Transition options – cost/benefit ofalternatives

Transition to IFRS 16planning► Key programme milestones

cannot be established until youdecide on your transitionapproach.

► A plan for transition balancesboth the financial impact andbroader impact on theorganisation.

► Stakeholders demand comparability across all years presented.► Specific company analysis suggests preferable impact on opening retained

earnings in first year of adoption.► Competitors and peer companies are planning full retrospective transition.► There are limited issues in gathering data for transition.► There are available resources to assist with implementation.

Full retrospective

Potential reasons for choosing each approach

► A cost/benefit analysis identifies this as the most efficient approach.► Specific company analysis suggests a concern about the impact of the fully

retrospective approach on distributable reserves.► Competitors and peer companies are planning modified retrospective

transition.► The data collation and analysis required to compute the impact for prior

periods will be significant for the fully retrospective approach or data is notavailable.

► There are limited resources available to assist with implementation.

Modified retrospective (Alternative 1 or 2)

Modifiedretrospective

Full retrospective

ReFIT Forum - 2nd February 2018

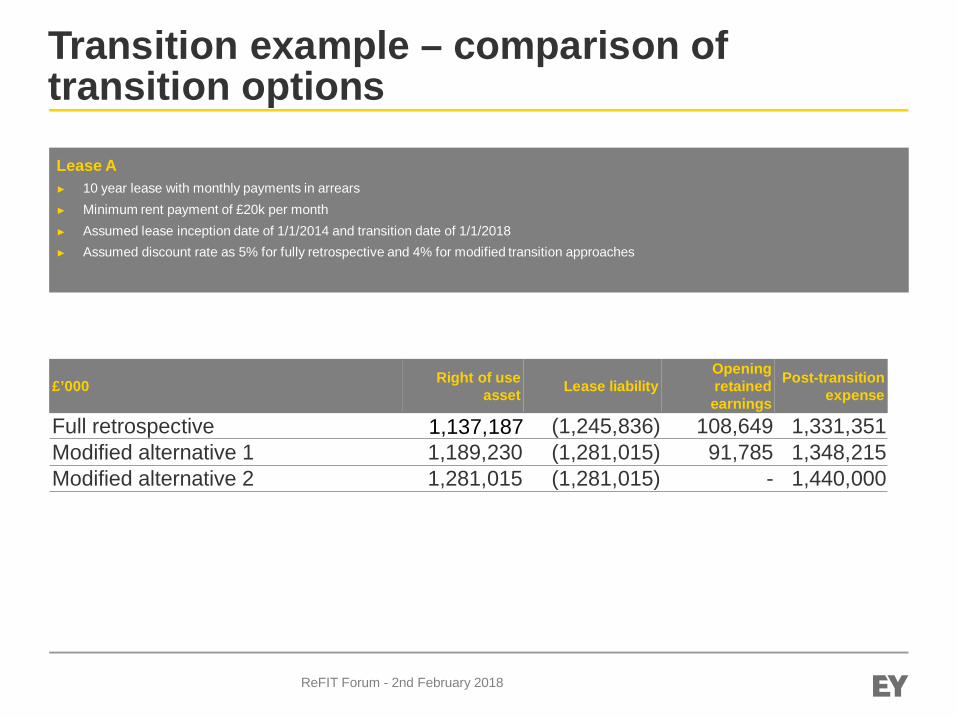

Transition example – comparison oftransition options

£’000 Right of useasset Lease liability

Openingretainedearnings

Post-transitionexpense

Full retrospective 1,137,187 (1,245,836) 108,649 1,331,351Modified alternative 1 1,189,230 (1,281,015) 91,785 1,348,215Modified alternative 2 1,281,015 (1,281,015) - 1,440,000

Lease A► 10 year lease with monthly payments in arrears► Minimum rent payment of £20k per month► Assumed lease inception date of 1/1/2014 and transition date of 1/1/2018► Assumed discount rate as 5% for fully retrospective and 4% for modified transition approaches

ReFIT Forum - 2nd February 2018

Leasing Tax – That Was Then

Current tax position complicated but well established

Section 53 Finance Act 2011 – “Frozen GAAP”

Lease Discussion Document August 2016Focussed on P&M leases and largely aimed at lessorsPut forward 4 options; 3 of which removed capital allowances entitlement

Spring Budget 2017 – Intention to maintain the current system of lease taxation

ReFIT Forum - 2nd February 2018

Leasing Tax – This is Now

December 1st Consultative Document – Comments by 28 February 2018

Section 53 Finance Act 2011 to be repealed with effect from 1 January 2019

Leases divided between P&M long funding leases and non long funding leases(including property)

For long funding leases lessee continues to have choice of capital allowances ordeductions under basic principles.

Non long funding leases (including property) - existing position retained BUTlessee can claim amortisation of right to use asset and finance cost as areasonable alternative (extending sp3/91)Some modification of long funding lease rules proposed.

ReFIT Forum - 2nd February 2018

Leasing Tax – This is Now – SomeComplexitiesNormal rule is that transitional adjustments should be tax effected

Proposal is to exclude any difference between the right to use asset and leaseobligation and allow relief for the amortisation of the lease obligation

Produces a deferred tax effect that will need to be considered

2nd consultative document on leasing as part of corporate interest deductibility -3 options – responses due by 28th February 2018

ReFIT Forum - 2nd February 2018

Leasing Tax – Some practical considerations& next stepsAre your tax teams aware of the consultation and considering possibleimplications for future tax position and processes/controls?Share finance team project status on IFRS 16 and any transition optionpreference/decision

Consider responding to the Consultation Document

Any tax preference to use current rules or amortisation/interest expense for taxdeductions for non long funding leases?

Determination of future books and records required for non long funding leases,in particular in light of possible corporate interest deductibility implications

New processes/controls to assess deferred tax balances and manage unwind oftransition adjustments

ReFIT Forum - 2nd February 2018

Appendix

ReFIT Forum - 2nd February 2018

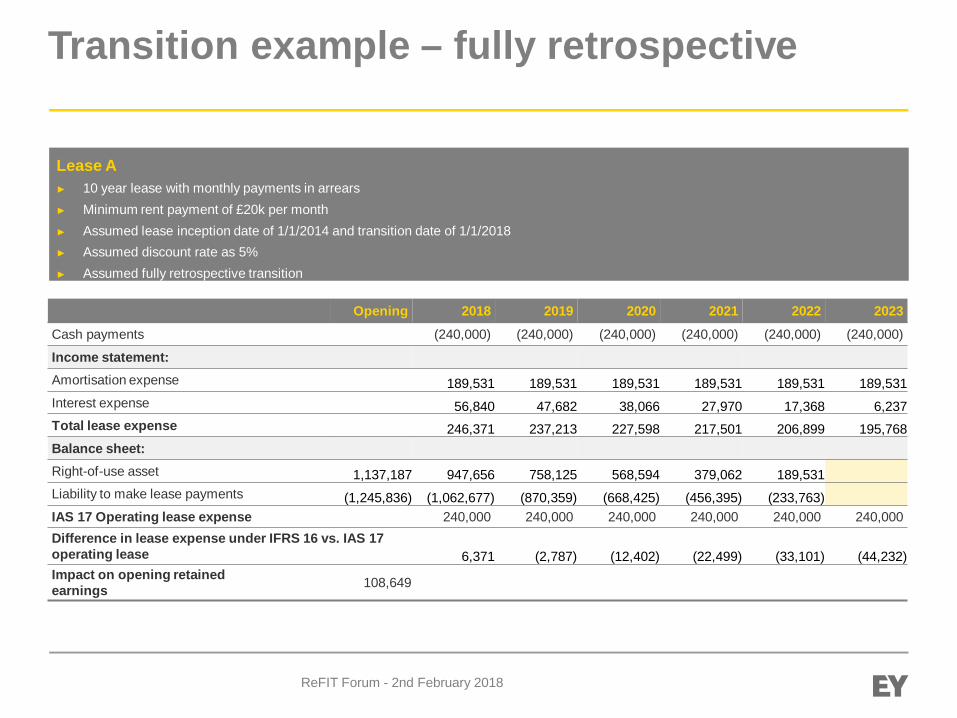

Transition example – fully retrospective

Lease A► 10 year lease with monthly payments in arrears► Minimum rent payment of £20k per month► Assumed lease inception date of 1/1/2014 and transition date of 1/1/2018► Assumed discount rate as 5%► Assumed fully retrospective transition

Opening 2018 2019 2020 2021 2022 2023Cash payments (240,000) (240,000) (240,000) (240,000) (240,000) (240,000)

Income statement:Amortisation expense 189,531 189,531 189,531 189,531 189,531 189,531Interest expense 56,840 47,682 38,066 27,970 17,368 6,237Total lease expense 246,371 237,213 227,598 217,501 206,899 195,768Balance sheet:Right-of-use asset 1,137,187 947,656 758,125 568,594 379,062 189,531Liability to make lease payments (1,245,836) (1,062,677) (870,359) (668,425) (456,395) (233,763)IAS 17 Operating lease expense 240,000 240,000 240,000 240,000 240,000 240,000Difference in lease expense under IFRS 16 vs. IAS 17operating lease 6,371 (2,787) (12,402) (22,499) (33,101) (44,232)Impact on opening retainedearnings 108,649

ReFIT Forum - 2nd February 2018

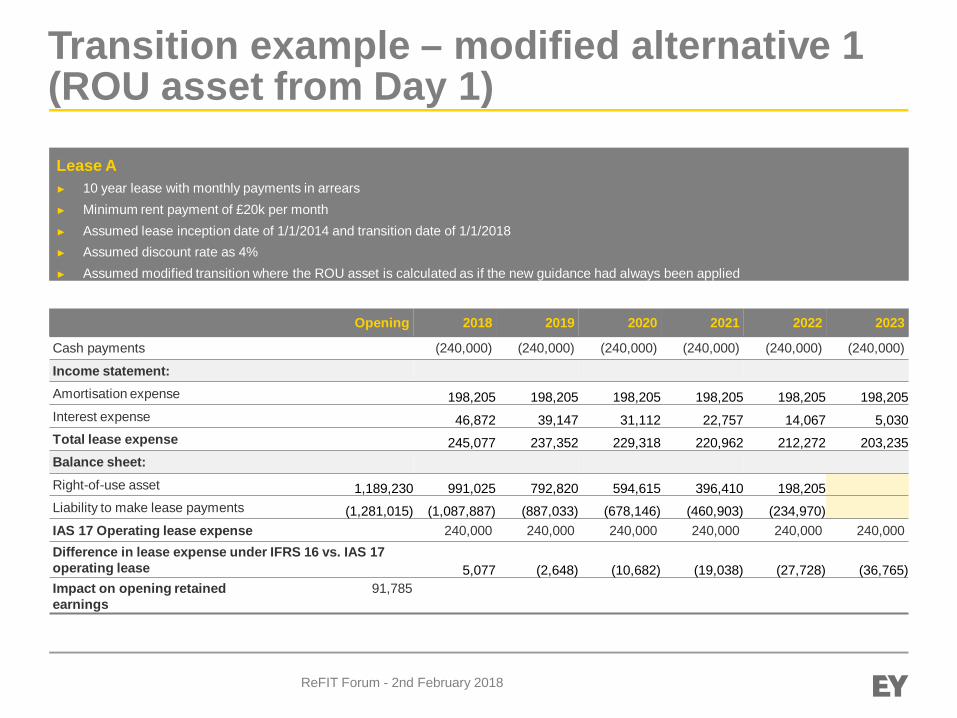

Transition example – modified alternative 1(ROU asset from Day 1)Lease A► 10 year lease with monthly payments in arrears► Minimum rent payment of £20k per month► Assumed lease inception date of 1/1/2014 and transition date of 1/1/2018► Assumed discount rate as 4%► Assumed modified transition where the ROU asset is calculated as if the new guidance had always been applied

Opening 2018 2019 2020 2021 2022 2023

Cash payments (240,000) (240,000) (240,000) (240,000) (240,000) (240,000)

Income statement:Amortisation expense 198,205 198,205 198,205 198,205 198,205 198,205Interest expense 46,872 39,147 31,112 22,757 14,067 5,030Total lease expense 245,077 237,352 229,318 220,962 212,272 203,235Balance sheet:Right-of-use asset 1,189,230 991,025 792,820 594,615 396,410 198,205Liability to make lease payments (1,281,015) (1,087,887) (887,033) (678,146) (460,903) (234,970)IAS 17 Operating lease expense 240,000 240,000 240,000 240,000 240,000 240,000Difference in lease expense under IFRS 16 vs. IAS 17operating lease 5,077 (2,648) (10,682) (19,038) (27,728) (36,765)Impact on opening retainedearnings

91,785

ReFIT Forum - 2nd February 2018

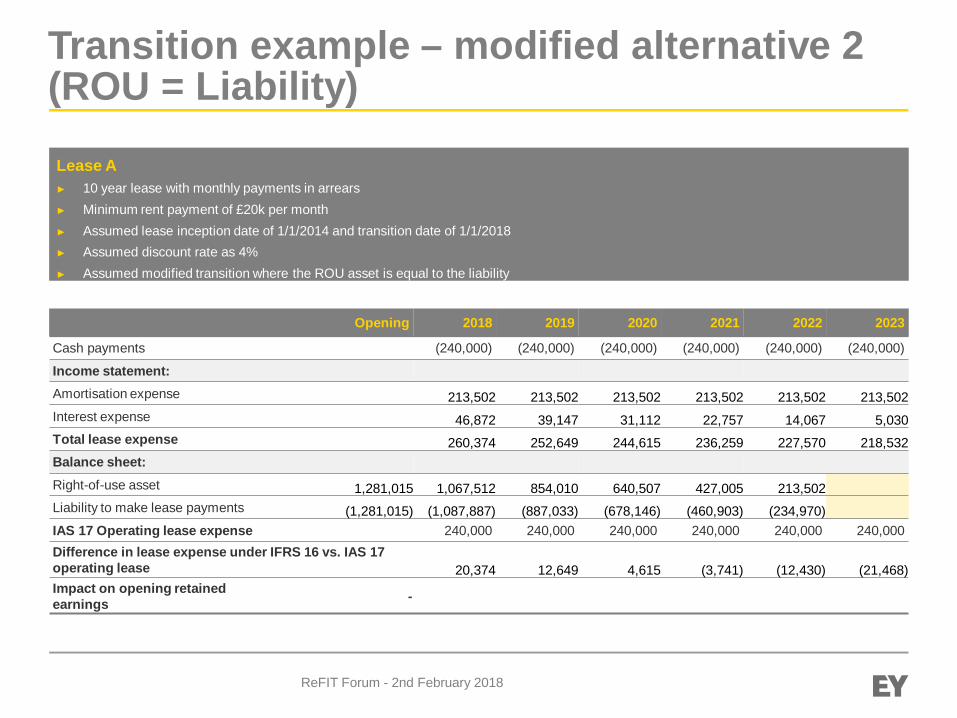

Transition example – modified alternative 2(ROU = Liability)Lease A► 10 year lease with monthly payments in arrears► Minimum rent payment of £20k per month► Assumed lease inception date of 1/1/2014 and transition date of 1/1/2018► Assumed discount rate as 4%► Assumed modified transition where the ROU asset is equal to the liability

Opening 2018 2019 2020 2021 2022 2023

Cash payments (240,000) (240,000) (240,000) (240,000) (240,000) (240,000)

Income statement:Amortisation expense 213,502 213,502 213,502 213,502 213,502 213,502Interest expense 46,872 39,147 31,112 22,757 14,067 5,030Total lease expense 260,374 252,649 244,615 236,259 227,570 218,532Balance sheet:Right-of-use asset 1,281,015 1,067,512 854,010 640,507 427,005 213,502Liability to make lease payments (1,281,015) (1,087,887) (887,033) (678,146) (460,903) (234,970)IAS 17 Operating lease expense 240,000 240,000 240,000 240,000 240,000 240,000Difference in lease expense under IFRS 16 vs. IAS 17operating lease 20,374 12,649 4,615 (3,741) (12,430) (21,468)Impact on opening retainedearnings -

ReFIT Forum - 2nd February 2018

Questions?

Simon Baxter

2nd February 2018

Boehringer Ingelheim CashbackOpportunity

Boehringer Ingelheim Cashback Opportunity

► Boehringer Ingelheim Pharma GmbH & Co. KG [C2017:1006]► Manufacturer of pharmaceutical products for supply to wholesalers

and retail pharmacies► Principles of Elida Gibbs ECJ decision – application of Article 90(1) –

VAT Directive 2006/112/EC► Under the German system of statutory (public) health insurance,

pharmacies supply medicines to health insurance funds, which in turnmake them available to persons insured by them

► Pharmacies are required to discount the price of products and recoupthis from the pharma manufacturer (or from wholesaler)

► German Tax Authority regards this rebate as a reduction in the valueof supplies made through the supply chain so pharma manufactureraccounts for VAT on the initial consideration charged less the rebatepaid – all good so far

ReFIT Forum - 2nd February 2018

Boehringer Ingelheim Cashback Opportunity

► Where a product is for a person with private health insurance,medicines are supplied by pharmacies to the individual

► Individual then seeks reimbursement from their insurer► Insurer claims a rebate from the pharma manufacturer to subsidise

the cost► German Tax Authority challenged the adjustment to the value of

supplies by Boehringer by virtue of payments made to insurers► GTA argued that the insurers were not part of the original supply chain

which fixed the considerations payable► In a short judgement, the CJEU determined that the was no difference

between the two circumstances for the purposes of Article 90(1) as inboth instances, the value of supply made by Boehringer had beenreduced to the extent of the rebates

ReFIT Forum - 2nd February 2018

Is this anything new?

► Debateable, but it does reinforce the principle that supply chains arecomplex and may involve rebates/discounts being paid to parties notpart of the original supply chain at all – this was the differentiator inBoehringer

► Review of how cashback arrangements operate e.g. TopCashBackand Quidco and where intermediaries may be involved

► What are the contractual arrangements in place?► Clearly retailer knows the amount of cashback on offer as would

expect to control this, not the cashback site► Previous attempts at making adjustments refused by HMRC► Was the correct approach made/reasons given and does Boehringer

help?► Opportunity value?► Next steps

ReFIT Forum - 2nd February 2018

Questions?

Coffee

Ethan Ding

2nd February 2018

Hot Topics

Agenda

Ø European Commission proposal on EU’s VAT AreaØ Office of Tax Simplification – Review of VATØ Making Tax DigitalØ Disclosure of Tax Avoidance Schemes – VAT and Other Indirect TaxesØ UK Voucher ConsultationØ Online marketplaces – extension of joint and several liabilityØ Other topics

ReFIT Forum - 2nd February 2018

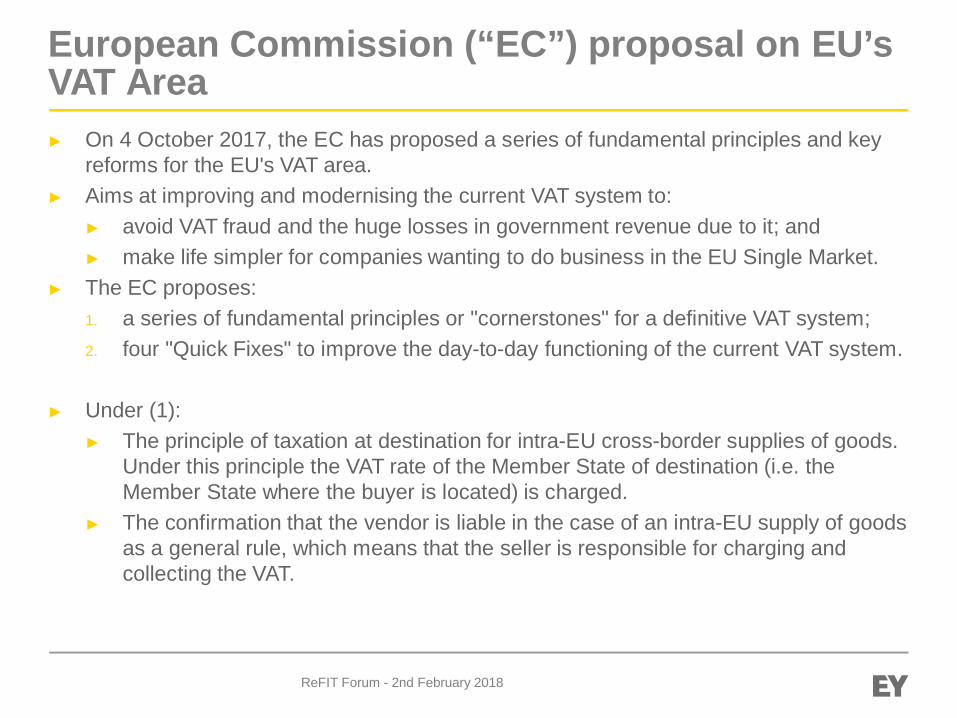

European Commission (“EC”) proposal on EU’sVAT Area► On 4 October 2017, the EC has proposed a series of fundamental principles and key

reforms for the EU's VAT area.► Aims at improving and modernising the current VAT system to:

► avoid VAT fraud and the huge losses in government revenue due to it; and► make life simpler for companies wanting to do business in the EU Single Market.

► The EC proposes:1. a series of fundamental principles or "cornerstones" for a definitive VAT system;2. four "Quick Fixes" to improve the day-to-day functioning of the current VAT system.

► Under (1):► The principle of taxation at destination for intra-EU cross-border supplies of goods.

Under this principle the VAT rate of the Member State of destination (i.e. theMember State where the buyer is located) is charged.

► The confirmation that the vendor is liable in the case of an intra-EU supply of goodsas a general rule, which means that the seller is responsible for charging andcollecting the VAT.

ReFIT Forum - 2nd February 2018

European Commission (“EC”) proposal on EU’sVAT Area

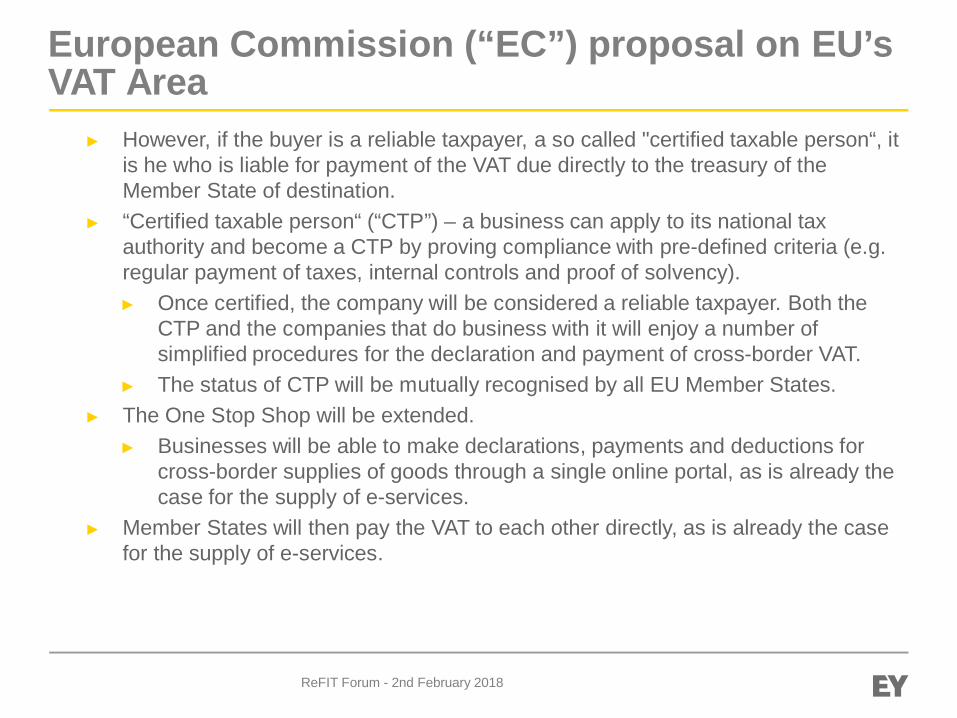

► However, if the buyer is a reliable taxpayer, a so called "certified taxable person“, itis he who is liable for payment of the VAT due directly to the treasury of theMember State of destination.

► “Certified taxable person“ (“CTP”) – a business can apply to its national taxauthority and become a CTP by proving compliance with pre-defined criteria (e.g.regular payment of taxes, internal controls and proof of solvency).► Once certified, the company will be considered a reliable taxpayer. Both the

CTP and the companies that do business with it will enjoy a number ofsimplified procedures for the declaration and payment of cross-border VAT.

► The status of CTP will be mutually recognised by all EU Member States.► The One Stop Shop will be extended.

► Businesses will be able to make declarations, payments and deductions forcross-border supplies of goods through a single online portal, as is already thecase for the supply of e-services.

► Member States will then pay the VAT to each other directly, as is already the casefor the supply of e-services.

ReFIT Forum - 2nd February 2018

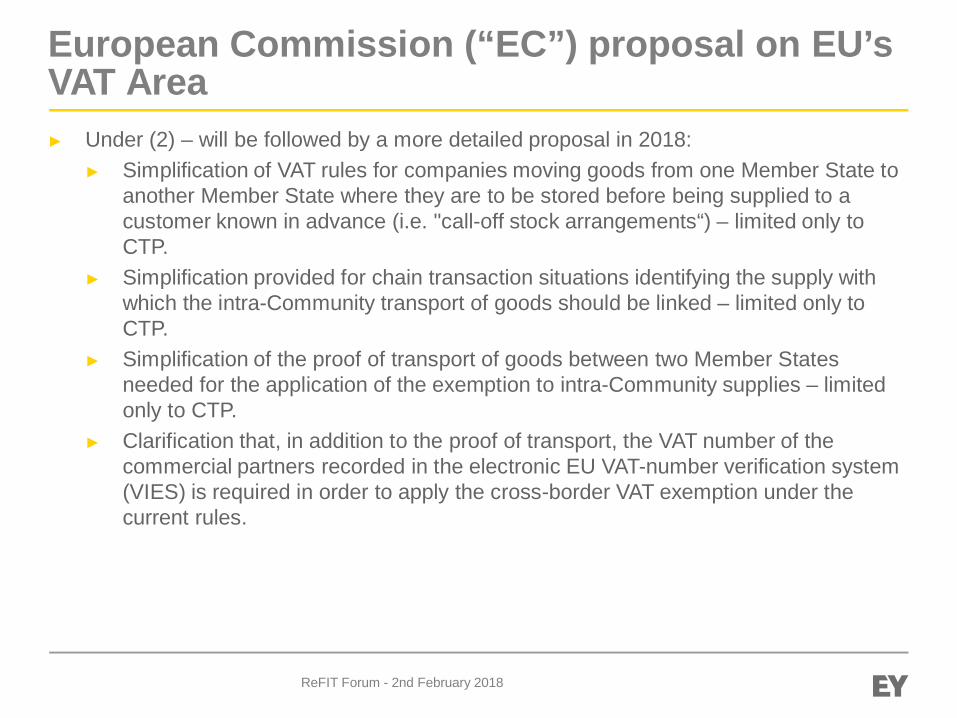

European Commission (“EC”) proposal on EU’sVAT Area► Under (2) – will be followed by a more detailed proposal in 2018:

► Simplification of VAT rules for companies moving goods from one Member State toanother Member State where they are to be stored before being supplied to acustomer known in advance (i.e. "call-off stock arrangements“) – limited only toCTP.

► Simplification provided for chain transaction situations identifying the supply withwhich the intra-Community transport of goods should be linked – limited only toCTP.

► Simplification of the proof of transport of goods between two Member Statesneeded for the application of the exemption to intra-Community supplies – limitedonly to CTP.

► Clarification that, in addition to the proof of transport, the VAT number of thecommercial partners recorded in the electronic EU VAT-number verification system(VIES) is required in order to apply the cross-border VAT exemption under thecurrent rules.

ReFIT Forum - 2nd February 2018

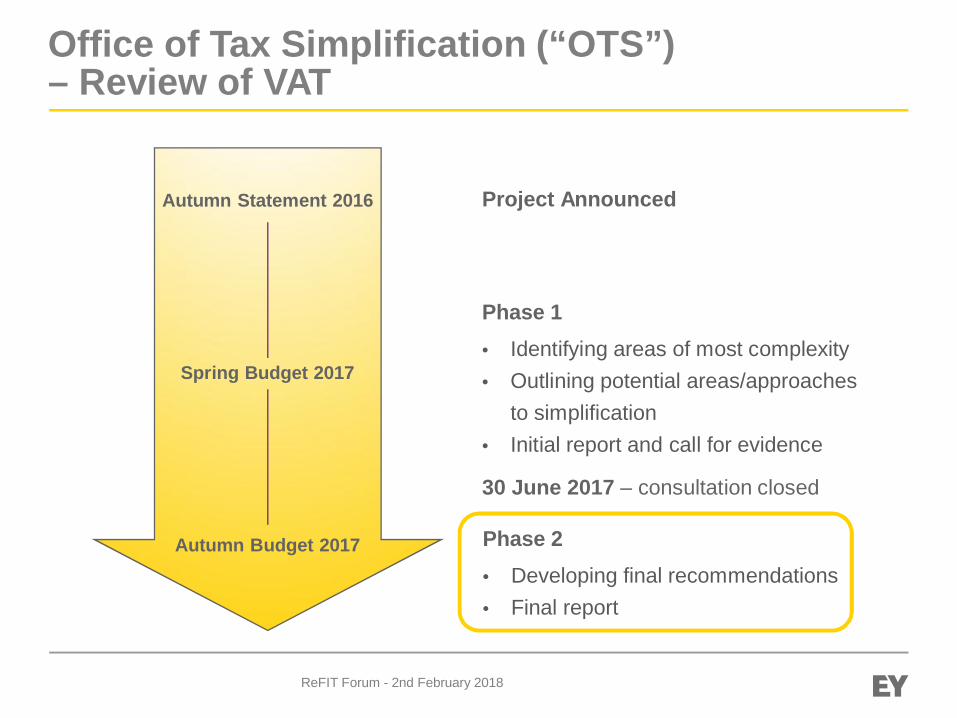

Office of Tax Simplification (“OTS”)– Review of VAT

Autumn Statement 2016

Spring Budget 2017

Autumn Budget 2017

Project Announced

Phase 1• Identifying areas of most complexity• Outlining potential areas/approaches

to simplification• Initial report and call for evidence

Phase 2• Developing final recommendations• Final report

30 June 2017 – consultation closed

ReFIT Forum - 2nd February 2018

Office of Tax Simplification (“OTS”)– Review of VAT8 areas under review:1.Identifying the implications of a high registration threshold

2.Multiple rates: Causes of complexity

3.Partial exemption, option to tax and capital goods scheme

4.Special Accounting Schemes

5.VAT administration, penalty and appeals processes

6.Formal ruling system

7.VAT and Making Tax Digital (MTD)

8.Further areas for investigation

ReFIT Forum - 2nd February 2018

Office of Tax Simplification (“OTS”)– Review of VAT► OTS Report published in November 2017.

► Contains 23 recommendations for simplifying the tax, with its lead recommendationrelating to the future level and design of the VAT registration threshold.

► Chancellor responded to the OTS’ recommendations:► Examine VAT threshold, but maintain at its current level in the meantime.► Appreciation of administrative issues faced by business.► Review of VAT rates and relief.► Continue to engage with OTS in relation to the Capital Goods Scheme and Partial

Exemption regulations.► Online handling of option to tax to be considered as part of Making Tax Digital.

► Next step – Government will engage with business, the public and the OTS on some ofthe areas, and consider any future legislative changes as part of the normal Budgetprocess.

ReFIT Forum - 2nd February 2018

Making Tax Digital (“MTD”)

► All VAT registered businesses above the VAT registration threshold will be compulsorilyrequired to meet the MTD requirements with reference to their VAT obligations fromApril 2019.

► Need to ensure that they can:1. store VAT records digitally,2. submit VAT returns electronically via an interface (“API”) with HMRC software, and3. demonstrate a clear electronic audit trail (or “digital journey”) from source systems

to VAT return submission.

► For (1), businesses will need to keep digital records for VAT purposes from April 2019at the earliest, and for other taxes from a date to be appointed (but not before April2020 at the earliest).

ReFIT Forum - 2nd February 2018

Making Tax Digital (“MTD”)

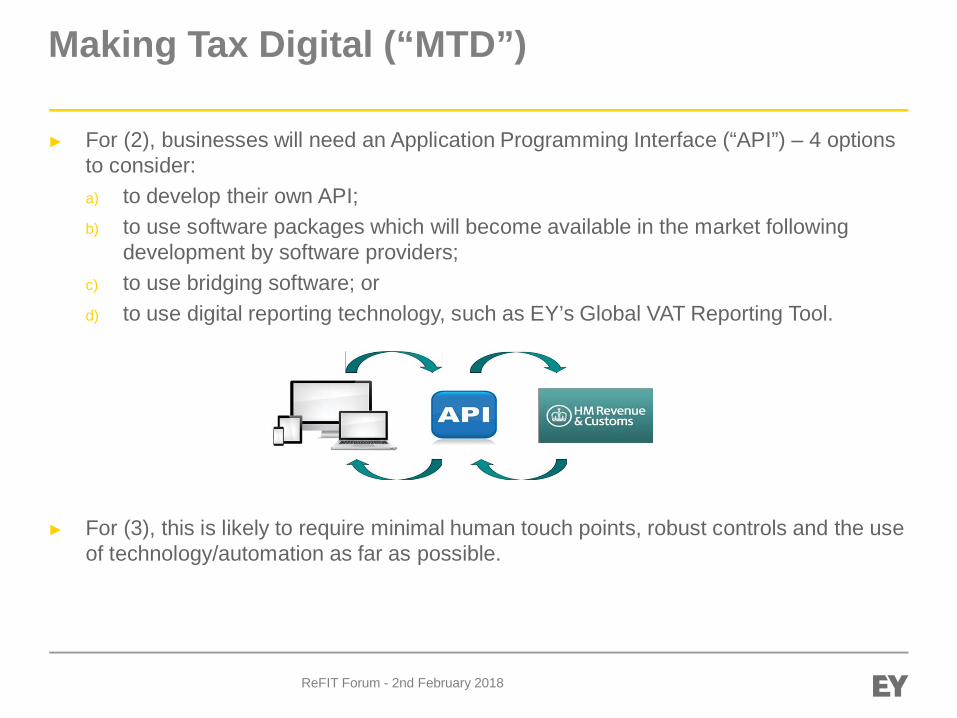

► For (2), businesses will need an Application Programming Interface (“API”) – 4 optionsto consider:a) to develop their own API;b) to use software packages which will become available in the market following

development by software providers;c) to use bridging software; ord) to use digital reporting technology, such as EY’s Global VAT Reporting Tool.

► For (3), this is likely to require minimal human touch points, robust controls and the useof technology/automation as far as possible.

ReFIT Forum - 2nd February 2018

Making Tax Digital (“MTD”)

► How is HMRC delivering this?► Currently working with software developers, who will develop MTD-ready software

that can link securely to HMRC systems using the APIs provided by HMRC.► Enables businesses to send data to and receive data from HMRC securely.

► Income Tax pilot has been launched.► VAT pilot will be launched in April 2018.

► Campaign to raise awareness of the MTD obligation for businesses.► Partner with agents & developers to promote the benefits of digital.► User research to better understand business models and VAT processes.► Launch VAT pilot and on-board volunteers ahead of the “go live” date.

► VAT API public beta testing will go “live” in April 2018.► Currently seeking “early adopters” who will voluntarily submit their data, their

electronic return, etc. via the MTDfB website or APIs before the official “go live”date.► An opportunity for businesses to be involved and influence the process.► HMRC is keen to hear from businesses regarding becoming ‘early adopters’

under the VAT pilot.

ReFIT Forum - 2nd February 2018

Making Tax Digital (“MTD”)

► Areas to consider:► HMRC published draft MTD regulations, explanatory memorandum and VAT

Notice, for consultation – consider providing your feedback. Closing date is 9February 2018.

► Consider whether or not to take part in the HMRC pilot MTD scheme later this year.► Assess whether current processes will meet the ‘digital journey’ concept (e.g.

analysing the current processes, controls, data and use of technology and develop(and implement) required changes to be in line with the MTD requirements).

ReFIT Forum - 2nd February 2018

Disclosure of Tax Avoidance Schemes- VAT and Other Indirect Taxes (“DASVOIT”)► The new UK VAT disclosure rules came into force on 1 January 2018.► The rules are aimed at promoters of VAT and other indirect tax ‘avoidance’

arrangements.► However, they also place reporting obligations on businesses, which have implemented

arrangements in-house without an external promoter.► In December 2017, HMRC released its final guidance on DASVOIT as well as updating

Notice 700/8 (Disclosure of VAT avoidance schemes).

► Broadly, a promoter (including an in-house promoter) will have to make a disclosure ifthe following conditions are met:► there is an ‘arrangement’ – which includes a transaction or series of transactions;► the arrangement will, or might be expected to, create a tax advantage (very broadly

defined);► that tax advantage is, or might be expected to be, one of the main benefits of the

arrangements; and► one of the prescribed ‘hallmarks’ is present.

► Does not matter what the motive of the arrangement is (i.e. having a commercialpurpose is no defence against having to make a disclosure).

ReFIT Forum - 2nd February 2018

Disclosure of Tax Avoidance Schemes- VAT and Other Indirect Taxes (“DASVOIT”)► In practice, any sort of VAT (or other indirect tax) planning is likely to involve an

‘arrangement’ for these purposes and is also likely to give rise to a tax advantage,which would be one of the main benefits of the arrangement.

► Therefore, for any UK indirect tax planning, a disclosure is likely to be required if one ofthe hallmarks is present. The general hallmarks for all indirect taxes are:1. Confidentiality from either HMRC or another promoter2. Premium fee3. Standardised documentation

► For in-house arrangements, where there is no promoter, only items 1 and 2 apply.► For these two hallmarks, it is not relevant whether there actually is a confidentiality

obligation or a premium fee – the question is whether a hypothetical promoter mightreasonably be expected to require confidentiality, or be able to agree a premium fee.

► In addition to these, there are four specific hallmarks which apply only to VAT:1. Retail splitting and value shifting2. Offshore supplies – insurance and finance3. Offshore supplies – relevant business person4. Disapplication of the option to tax

ReFIT Forum - 2nd February 2018

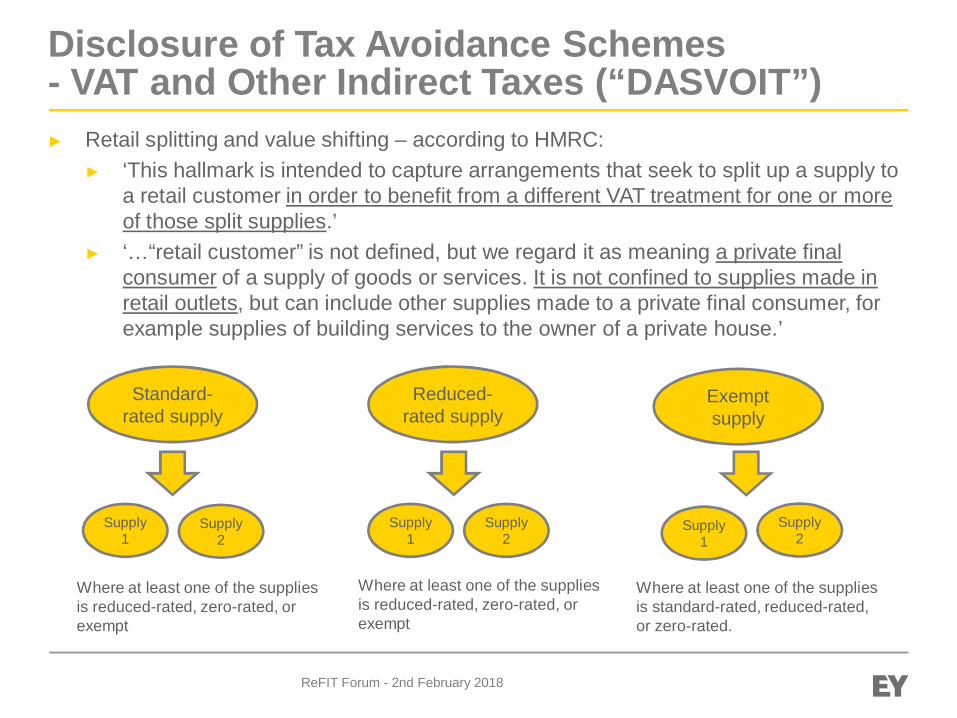

Disclosure of Tax Avoidance Schemes- VAT and Other Indirect Taxes (“DASVOIT”)► Retail splitting and value shifting – according to HMRC:

► ‘This hallmark is intended to capture arrangements that seek to split up a supply toa retail customer in order to benefit from a different VAT treatment for one or moreof those split supplies.’

► ‘…“retail customer” is not defined, but we regard it as meaning a private finalconsumer of a supply of goods or services. It is not confined to supplies made inretail outlets, but can include other supplies made to a private final consumer, forexample supplies of building services to the owner of a private house.’

Standard-rated supply

Reduced-rated supply

Exemptsupply

Supply1

Supply2

Supply1

Supply2

Supply2

Supply1

Where at least one of the suppliesis reduced-rated, zero-rated, orexempt

Where at least one of the suppliesis reduced-rated, zero-rated, orexempt

Where at least one of the suppliesis standard-rated, reduced-rated,or zero-rated.

ReFIT Forum - 2nd February 2018

Disclosure of Tax Avoidance Schemes- VAT and Other Indirect Taxes (“DASVOIT”)► In situations where there is no promoter (i.e. the arrangements are put in place by an

in-house team), then the business itself has the obligation to make any disclosure toHMRC.

► Failure to do so can result in significant financial penalties and potentially being namedand shamed.

► It should be noted that there are grandfathering provisions – mean that anyarrangements which are in place before 1 January 2018 are not required to bedisclosed under the new regime.► On the face of it, this means that existing structures which are in place should not

need to be disclosed.► However, this protection only applies where arrangements which are put in place

on or after 1 January 2018 are ‘the same or substantially the same’ as thegrandfathered arrangements.

► Therefore, care should be taken when making any changes to the existingarrangements - if this means that the arrangements are no longer ‘the same orsubstantially the same’ as they are now, a disclosure could potentially be required.

ReFIT Forum - 2nd February 2018

UK Voucher Consultation

► A consultation document on “VAT and Vouchers” – released on 1 December 2017 alongwith the Winter Finance Bill.

► May be relevant to those buying, selling and redeeming vouchers and gift cards.► Relates to the EU Vouchers Directive (Council Directive (EU) 2016/1065) – agreed on

27 June 2016.► Amends the VAT Directive and legislates for a common VAT treatment of vouchers

across the EU.► Applies to any vouchers for which a payment has been made and which will be

redeemed against goods or services.► Changes do not extend to discount vouchers or money-off tokens and will apply to

vouchers issued on, or after, 1 January 2019.► Consultation closes on 23 February 2018.

► Although the new rules have been decided in principle, it explains the rules and thefuture VAT treatment for vouchers in circulation which were issued before the new rulesstart.

► It invites comments in certain areas in order to identify any issues that businesses canforesee and aims to provide enough detail for businesses to plan for the changes.

ReFIT Forum - 2nd February 2018

UK Voucher Consultation

► Example issues that may impact retailers:► Definition of SPV/MPV between UK rules and EU Vouchers Directive;► UK VAT accounting under the “Argos” principle;► Distribution of MPV’s under the EU Vouchers Directive;► Breakage.

► Also a great opportunity:► To review current voucher arrangements.► To discuss the claim opportunity presented by the Court of Appeal decision in the

Associated Newspapers case.► To consider submitting claims in respect of businesses which operate external

promotion schemes or internal staff incentive arrangements involving vouchers orother services (e.g. tickets to concerts or sporting events).

ReFIT Forum - 2nd February 2018

Online marketplaces – extension of joint andseveral liability► In the Winter Finance Bill, the Government legislated to hold online marketplaces jointly

and severally liable (JSL) for the UK VAT liabilities of businesses selling goods throughtheir platforms.

► Bill extends the existing JSL liability provisions for online marketplaces from the date ofRoyal Assent.

► The new JSL provisions extend the scope of existing JSL provisions – an onlinemarketplace can now be held JSL for VAT payable by any person selling goods throughthe online marketplace who fails to comply with any requirement imposed by UK VATlaw.

► There is a new JSL provision, whereby any online marketplace which allows anunregistered non-UK business to continue to sell goods through its marketplace 60days after it ‘knew or should have known’ that the non-UK business is required to beregistered for VAT, will be JSL for any unpaid VAT.

► Finally a penalty can be levied in circumstances where the online marketplace fails todisplay valid VAT numbers in certain situations.

ReFIT Forum - 2nd February 2018

Other topics

► Postponed accounting for VAT following Brexit► Recognition that businesses currently benefit from postponed accounting for VAT

when importing goods from the EU.► The Government will take this into account when considering potential changes

following Brexit, and will look at options to mitigate any cash flow impacts forbusinesses that a border between the UK and EU might create.

► VAT split payment for online payments► This is a measure to tackle the non-payment of VAT by some overseas businesses

trading online with UK customers. A split payment mechanism allows VAT to beextracted from online payments in real time.

► VAT grouping► HMRC reviewed eligibility for membership, the VAT treatment of cross border

supplies involving branches, and the interaction between VAT grouping and thecost sharing exemption.

► It is clear that UK VAT grouping is valuable to businesses, and HMRC will continueto review the scope of VAT grouping.

ReFIT Forum - 2nd February 2018

Questions?

Rosemarie McGuire & Simon Baxter

2nd February 2018

Brexit Update

The People impacts ofBrexit

2nd February 2018

Rosemarie McGuire

ReFit forum

The People impacts ofBrexit

2nd February 2018

Rosemarie McGuire

Background

Ø The UK’s decision to leave the EU has introduced new people challenges and opportunities.Ø Immigration regulations and visa requirements will change, making access to the right talent

more restrictive.Ø Throughout this period, organisations will need to consider how talent is sourced, structured

and retained, along with the Tax, Social Security and Compliance implications.

ReFIT Forum - 2nd February 2018

Today we will cover the following:

Ø Recap on the likely people impacts ofBrexit

Ø Retail sector insights and webcast results

Ø Common pitfalls and how Retail can avoidthem

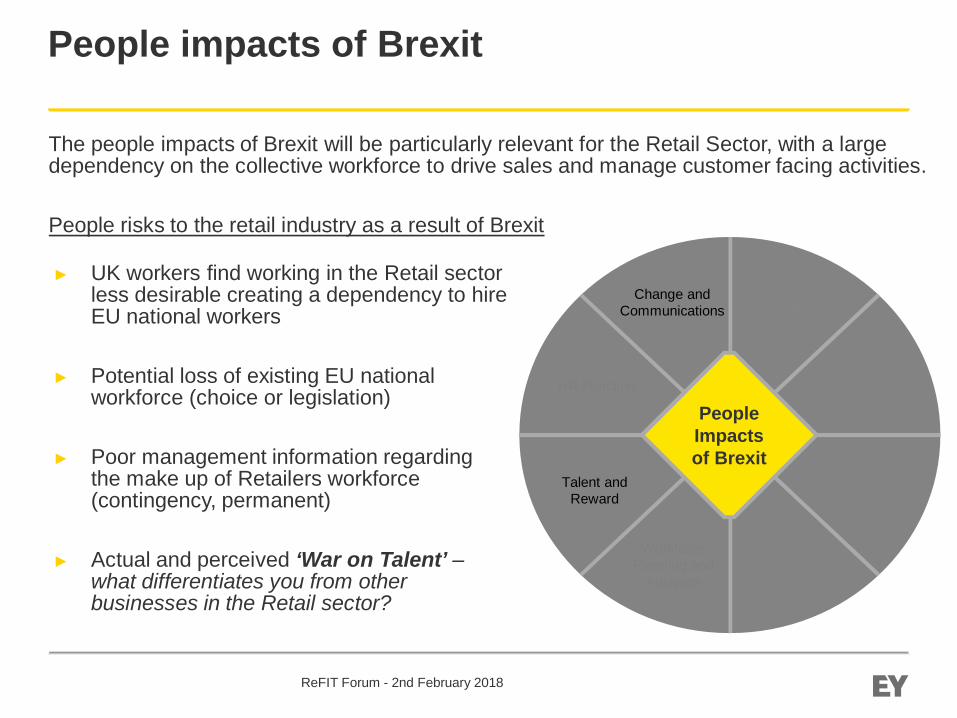

People impacts of Brexit

► UK workers find working in the Retail sectorless desirable creating a dependency to hireEU national workers

► Potential loss of existing EU nationalworkforce (choice or legislation)

► Poor management information regardingthe make up of Retailers workforce(contingency, permanent)

► Actual and perceived ‘War on Talent’ –what differentiates you from otherbusinesses in the Retail sector?

The people impacts of Brexit will be particularly relevant for the Retail Sector, with a largedependency on the collective workforce to drive sales and manage customer facing activities.

People risks to the retail industry as a result of Brexit

ReFIT Forum - 2nd February 2018

Mobility

Immigration

Tax and SocialSecurity

EmploymentLaw

WorkforcePlanning and

Analytics

Talent andReward

HR Function

Change andCommunications

PeopleImpactsof Brexit

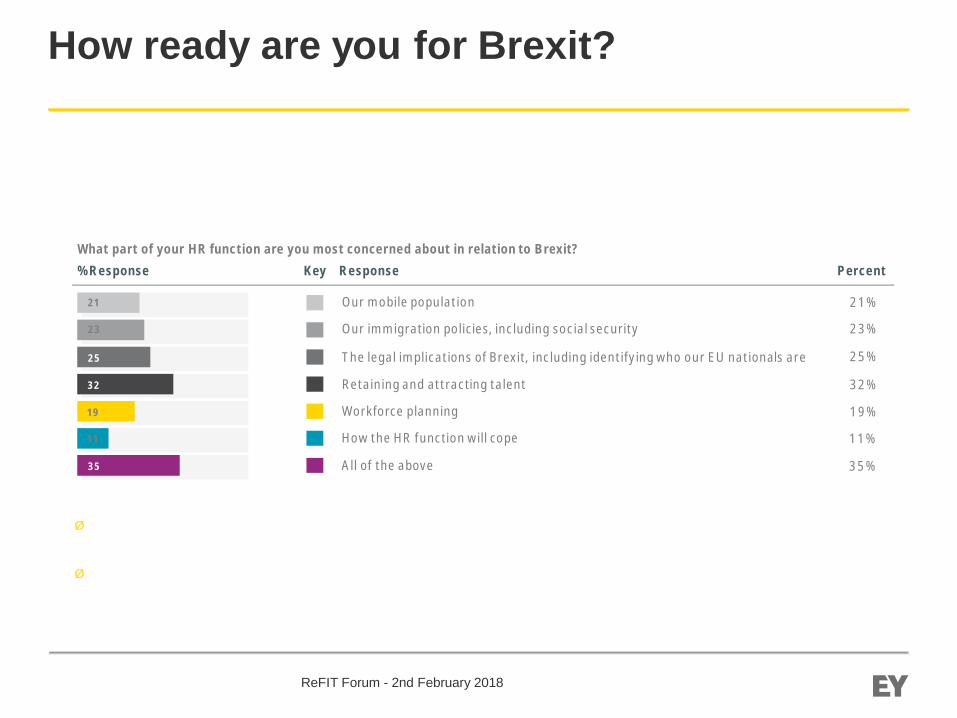

How ready are you for Brexit?

ReFIT Forum - 2nd February 2018

Ø HR has the opportunity to have a leading role in the shaping and management of Brexit changesgoing forward.

Ø Understanding your current workforce and the “War on Talent” is essential for businesses in theRetail sector, as retaining a competitive advantage will become increasingly challenging.

What part of your HR function are you most concerned about in relation to Brexit?Key Response Percent

Our mobile population

Retaining and attracting talent

All of the above

Our immigration policies, including social security

The legal implications of Brexit, including identifying who our EU nationals are

21

23

25

32

19

11

35

% Response

Workforce planning

How the HR function will cope

25%

23%

21%

32%

19%

11%

35%

On 19th October, People Advisory Services delivered a webcast to 1,111 organisations highlightingkey actions to take to mitigate against the impacts of Brexit.As part of that webcast a series of polling questions were asked and some of the results arehighlighted below:

What can Retail learn from the market?

For any business, being proactive and ready for the challenges of Brexit will be key to differentiatingyour brand and being able to mitigate against these impacts.

With this in mind, what are the common pitfalls you should be looking to avoid?

ReFIT Forum - 2nd February 2018

Ø Having a reactive HR function – How can your HR function lead by example?

Ø Incomplete workforce planning – How accurate is the data you have stored on your

employees?

Ø Delivering stand alone communications and support – Has the overall communication

strategy been considered?

Ø Underestimating what talent means for you - How confident are you that you have

identified where your critical roles lie and how talent will be sourced in the future?

Ø Lack of investment in your employee morale – How has Brexit impacted your

employee experience?

People Impacts of Brexit Webcast

ReFIT Forum - 2nd February 2018

Rosemarie McGuireDirectorPeople Advisory Services+44 20 778 30726

Ø Date: 20th February 2018Ø Time: 13.00-14.00 GMTØ Register: [email protected]

Agenda

Ø Relocation: Insight into sectors thathave already moved, or are planning to

Ø Reorganisation: How businesses areplanning to reorganise as a result ofBrexit

Ø Reality: our recommendations now thatthe Brexit deadline is in sight

Brexit updateSimon Baxter

2nd February 2018

Page 66

Brexit update

► On 31st January 2018, the European Commission published a Noticeto Stakeholders regarding the Customs, Excise Duties and VATconsequences of the UK’s withdrawal from the EU

► Highlights, subject to any transitional arrangements, that as of thedate of withdrawal, EU rules relating to all indirect taxes will no longerapply in the UK

► Notice includes information relating to:► Goods moving from and to the UK to and from the EU, will be subject to Customs

supervision including Customs Duties► Authorisations from the UK granting AEO status and other customs simplifications

will no longer be valid in the EU► Suppliers of telecoms, broadcasting or e-services to non-taxable persons in the EU

and wishing to use the Mini One-Stop Shop (MOSS), will have to be VAT registeredin an EU (and not UK) territory

► A company established in the UK carrying on taxable transactions in a MemberState may be required to designate a tax representative

ReFIT Forum - 2nd February 2018

Page 67

Brexit update – what are retailers doingnow?

► Thorough analysis of the impact of withdrawal, including:

► Mapping existing EU-UK supply chains► Understanding fragile supply chains► What would hard Brexit mean re levels of Customs Duty and administration?► Which ports are most used for future imports from the EU?► Discussions with EU customers?► Discussions with key UK suppliers who themselves import from the UK – what are

their plans to keep supplying you?► Ireland – stock consolidation in the UK and then shipping to Ireland? Needs careful

consideration► Distance selling► Customs reliefs

► Transitional period? Everyone wants one, but political posturing could mean thereisn’t one

ReFIT Forum - 2nd February 2018

Questions?

Global VAT updateSaleena Beedassy

2nd February 2018

Page 70

Global Indirect Tax Updates – Key Trends

► Introduction of VAT► Gulf Co-Operation Council (GCC) update

► VAT on electronic commerce: New rules adopted by the Council

► Real time reporting and making tax digital

► VAT compliance changes

► Introduction of rules to tax supplies of digital services – still high onthe agenda

ReFIT Forum - 2nd February 2018

Page 71

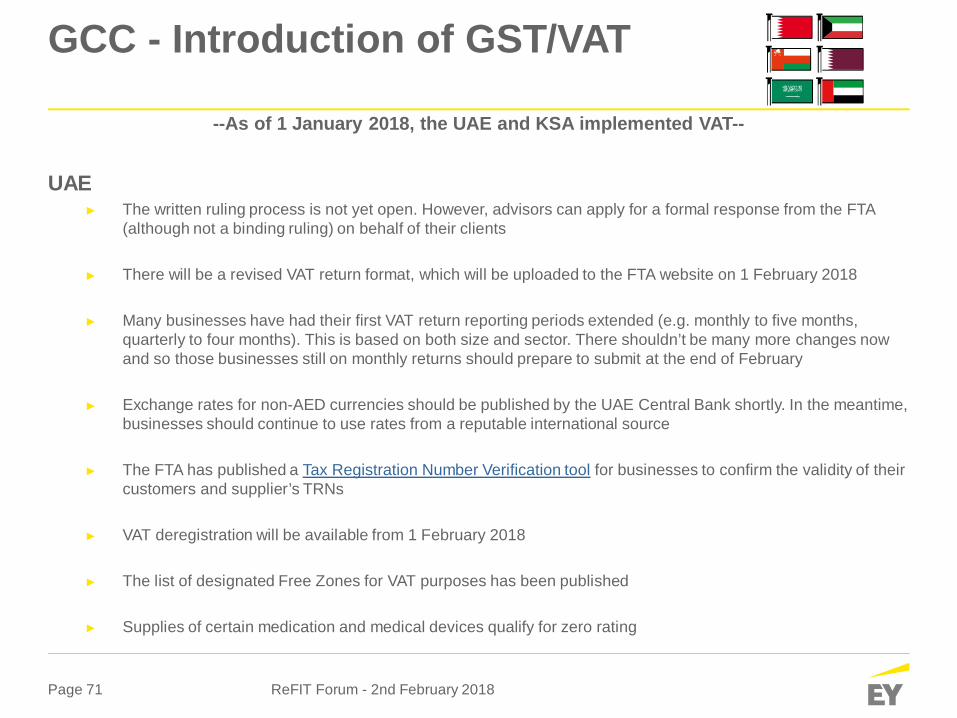

GCC - Introduction of GST/VAT

--As of 1 January 2018, the UAE and KSA implemented VAT--

UAE► The written ruling process is not yet open. However, advisors can apply for a formal response from the FTA

(although not a binding ruling) on behalf of their clients

► There will be a revised VAT return format, which will be uploaded to the FTA website on 1 February 2018

► Many businesses have had their first VAT return reporting periods extended (e.g. monthly to five months,quarterly to four months). This is based on both size and sector. There shouldn’t be many more changes nowand so those businesses still on monthly returns should prepare to submit at the end of February

► Exchange rates for non-AED currencies should be published by the UAE Central Bank shortly. In the meantime,businesses should continue to use rates from a reputable international source

► The FTA has published a Tax Registration Number Verification tool for businesses to confirm the validity of theircustomers and supplier’s TRNs

► VAT deregistration will be available from 1 February 2018

► The list of designated Free Zones for VAT purposes has been published

► Supplies of certain medication and medical devices qualify for zero rating

ReFIT Forum - 2nd February 2018

Page 72

GCC - Introduction of GST/VAT

KSA

► The FTA has published a Tax Registration Number Verification tool for businesses to confirm the validity ofcustomer and supplier TRNs

► On 21 January 2018, the KSA tax authority released further information relating to the VAT implementingregulations

► Article 66 specifies that data should be entered into the system in Arabic “whenever and to the extentpracticably possible” (previously Arabic was required in all cases)

In addition:

► The requirement for tax invoices and all records to be issued in Arabic remains as previously stated

► The VAT registration certificate of a business or a branch should be displayed and visible to the general public

► All registered businesses need to issue a simplified VAT invoice for all transactions not otherwise coveredspecifically by the remaining paragraphs in the Article – this will generally affect transactions with the endconsumers

► If the understatement of Net Tax by the Taxable Person is less than SR 50,000, the taxable Person may correctthe error by adjusting the Net Tax in its next Tax Return

ReFIT Forum - 2nd February 2018

Page 73

VAT on Electronic Commerce: New RulesAdopted

► On 5 December 2017 the Council of the European Union adopted new rules making it easier foronline businesses to comply with VAT obligations

► Part of the EU's 'digital single market' strategy, the proposals are aimed at facilitating thecollection of VAT when consumers buy goods and services online

► The new rules extend an existing EU-wide portal (mini 'one-stop shop') for the VAT registration ofdistance sales

► They establish a new portal for distance sales from third countries with a value below €150. This willreduce the costs of complying with VAT requirements for business-to-consumer transactions

► For start-ups and SMEs, the new rules introduce an important simplification. Below €10 000 inyearly cross-border online sales, a business will be able to continue applying VAT rules used in itshome country

► The new rules set out the following timeline:► Extension by 2021 of the one-stop shop to distance sales of goods

ReFIT Forum - 2nd February 2018

Page 74

Real Time Reporting - Update and the MoveTowards Digital

► Standard Audit File for Tax purposes (SAF-T) is an international standard for theelectronic submission of accounting data from organisations to tax authorities.

► The standard is defined by the Organisation for Economic Co-operation andDevelopment (OECD).

► Follows the general global trend of making tax digital in an effort to close the VAT Gap

Challenges

► Practically speaking, identifying the specific SAF-T records that are required ischallenging as each country implements the OECD's standard slightly differently

► Business required to contend with different SAF-T filing deadlines and file formats

► There is an impact on technology, data, processes and people/resources.

ReFIT Forum - 2nd February 2018

Page 75

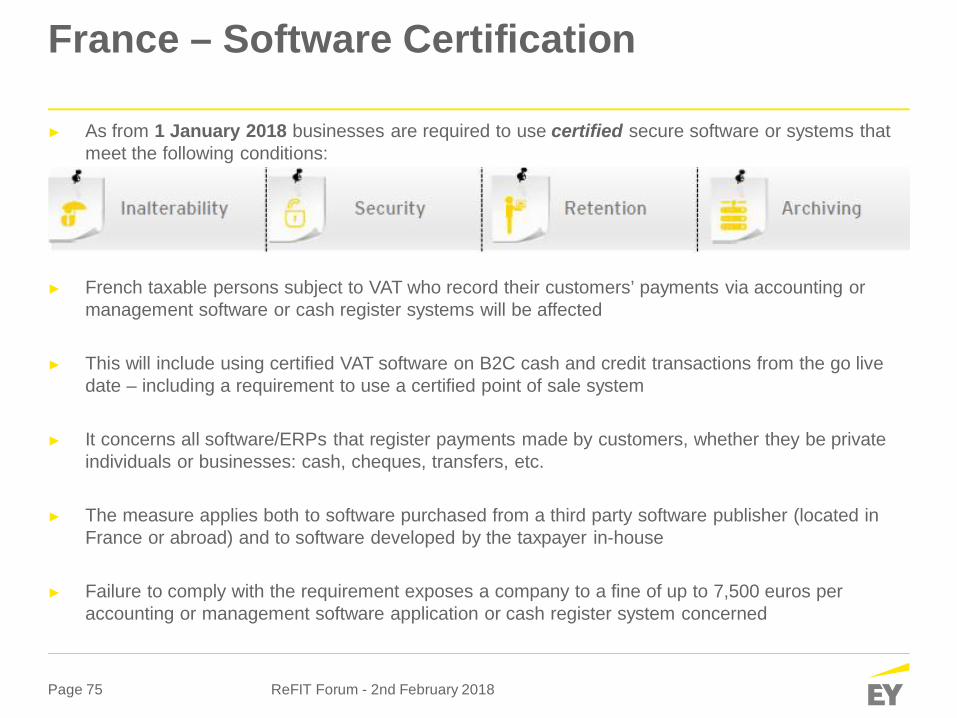

France – Software Certification

► As from 1 January 2018 businesses are required to use certified secure software or systems thatmeet the following conditions:

► French taxable persons subject to VAT who record their customers’ payments via accounting ormanagement software or cash register systems will be affected

► This will include using certified VAT software on B2C cash and credit transactions from the go livedate – including a requirement to use a certified point of sale system

► It concerns all software/ERPs that register payments made by customers, whether they be privateindividuals or businesses: cash, cheques, transfers, etc.

► The measure applies both to software purchased from a third party software publisher (located inFrance or abroad) and to software developed by the taxpayer in-house

► Failure to comply with the requirement exposes a company to a fine of up to 7,500 euros peraccounting or management software application or cash register system concerned

ReFIT Forum - 2nd February 2018

Page 76

Global Indirect Tax Updates - Italy

► VAT rates► The standard VAT rate set to increase from 22% to 25% by 2021► The reduces VAT rate will also increase from 10% to 13% by 2021► The increase will happen in phases starting from 1 January 2019

► Electronic invoicing► From 1 January 2019 an e-invoicing obligation will apply to all B2B and B2C transactions► This will impact Italian established entities as well as non established taxable persons VAT

registered in Italy► Potential penalties for non compliance will range between 90% to 180% of the applicable VAT

► Intrastat► Move to monthly intrastat reporting for purchases over the reporting threshold► Quarterly filings remain for supplies below a certain threshold

► New permanent establishment (“PE”) definition► A significant and continuous economic presence in the territory of the State, set up in a way that

it does not result in a substantial physical presence in the same territory, may constitute a PE.► This implies the possibility of a PE presence, even in the case where a company does not have

a physical presence in the Italian territory to the extent other factors may indicate a significantpresence (e.g. revenues, number of customers etc.)

ReFIT Forum - 2nd February 2018

Page 77

Global Indirect Tax Updates - Russia

Introduction of a tax-free system

► Citizens of countries outside the Eurasian Economic Union (EAEU) may be entitled to claim back the VAT paid ongoods purchased in Russian retail stores

► Provided the purchased goods are then moved outside of the EAEU customs territory

► How will it work► Stores will be obliged to issue foreign purchasers with special receipts that may be used► The store will refund the VAT to the customer minus a refund fee

► Conditions include► The VAT refund is claimed within 1 year of the date of purchase► The goods must have crossed the Russian border within 3 months of purchase► The purchase must be for at least RUB 10,000 (inclusive of tax)► The goods are not excise goods

► Timeline – 1 January 2018

► Opportunities/Challenges► Potential for increased sales► Cost of compliance and establishing business processes

ReFIT Forum - 2nd February 2018

Page 78

Global Indirect Tax Updates

► Hungary► VAT rates for various goods and services has changed as of 1 Jan 2018► Supply of meals and non-alcoholic beverages prepared on site in restaurants is now subject to

a reduced rate of 5% (previously 18%)► As of 1 July 2018, taxpayers issuing invoices using invoicing software will be required to

provide real-time data to the tax authority► This applies initially to invoices issued where the VAT amount exceeds HUF 10,000 (approx.

EUR 320)

► Latvia► Reduced VAT rate (5%) introduced from 1 January 2018► Applicable to certain fresh fruits and vegetables► VAT return form has been amended, as of 1 January 2018 the new return will included

amended and additional boxes

► Belgium► With effect from 1 Jan 2018 Belgium is expected to introduce a new measure which will allow

landlords to opt to apply VAT on the lease of ‘new’ commercial buildings► A building will only be considered “new” if no VAT has become due on costs directly relating to

the building prior to 1 January 2018

ReFIT Forum - 2nd February 2018

Page 79

Global Indirect Tax Updates

► Poland► Obligation to file daily SAF-T bank statements has been withdrawn► Introduction of a retail sales tax on suppliers of goods has been postponed to 1 January

2019

► Serbia► As of 1 January 2018 the VAT calculation overview must be submitted with the VAT

return► Provides the tax authority with a more detailed overview of how the VAT return was

populated

► Croatia► 1 January 2018 a single reduced rate of VAT has been introduced► 12% will replace the former 13% and 5% VAT rates

► Norway► The lower rate of VAT has been increased from 10% to 12%► The Norwegian Ministry of Finance has adopted an administrative regulation confirming

that SAF-T will be introduced in Norway with effect from 1 January 2020

ReFIT Forum - 2nd February 2018

Page 80

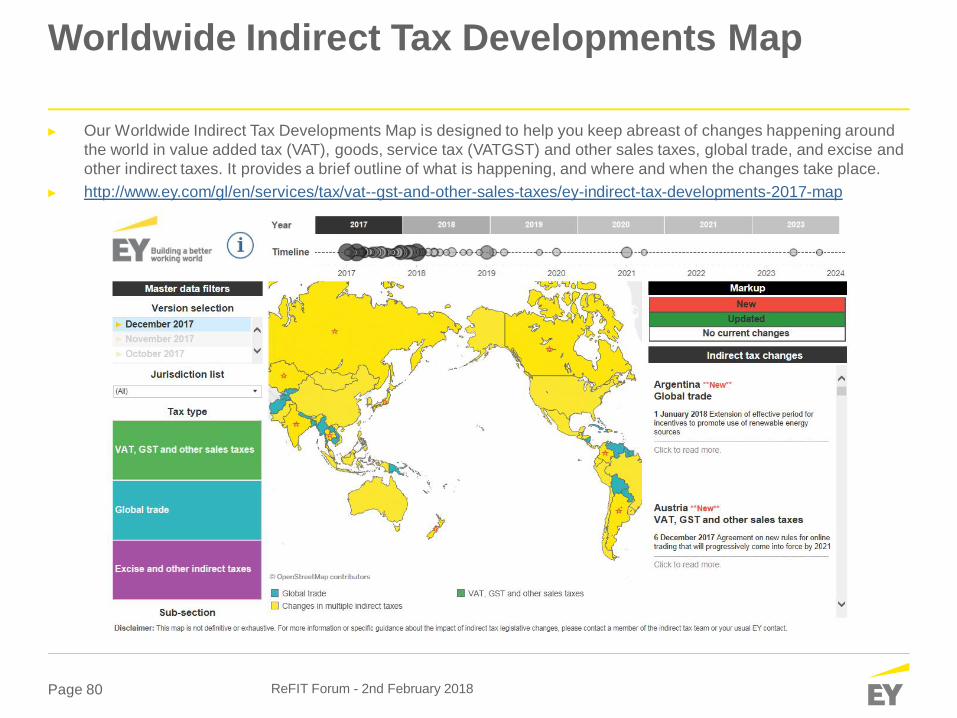

Worldwide Indirect Tax Developments Map

ReFIT Forum - 2nd February 2018

► Our Worldwide Indirect Tax Developments Map is designed to help you keep abreast of changes happening aroundthe world in value added tax (VAT), goods, service tax (VATGST) and other sales taxes, global trade, and excise andother indirect taxes. It provides a brief outline of what is happening, and where and when the changes take place.

► http://www.ey.com/gl/en/services/tax/vat--gst-and-other-sales-taxes/ey-indirect-tax-developments-2017-map

Questions?

Open Forum

Thank youNext ReFIT – Tuesday 17th April 2018

www.ey.com/uk/refit

EY | Assurance | Tax | Transactions | Advisory

Ernst & Young LLP

© Ernst & Young LLP. Published in the UK.All Rights Reserved.

The UK firm Ernst & Young LLP is a limited liability partnership registered in England and Waleswith registered number OC300001 and is a member firm of Ernst & Young Global Limited.

Ernst & Young LLP, 1 More London Place, London, SE1 2AF.

ey.com