regional analysis methods benchmarking, location quotients, shift-share

Post on 21-Dec-2015

239 views

TRANSCRIPT

Regional Analysis Methods

Benchmarking, Location Quotients, Shift-share

Agenda

• Review

• Shift-Share– What is it?– How do you do it?– What does it mean?

• Tools for interpreting

– Cautions and limits

• Multipliers

• Policy Map?

First Assignment – Q1

• What was the population of Allegheny County in 2000 and 2004 (Census or BEA)? – 2000: 1,279,817 (BEA - REIS or Census July

1est.)– or 2000: 1,281,666 (Census 2000 (SF1) -

April 1 estimate)– 2004: 1,247,512 (BEA-REIS)

First Assignment Q2-4

• How many total jobs were available in Allegheny County in 2004?– 861,868 (BEA total employment)

• How many Allegheny County residents were employed in 2004?– 604,203 (BLS, CPS/LAUS)

• What was the total "covered" employment in 2004?– 685,878 (BLS, QCEW)

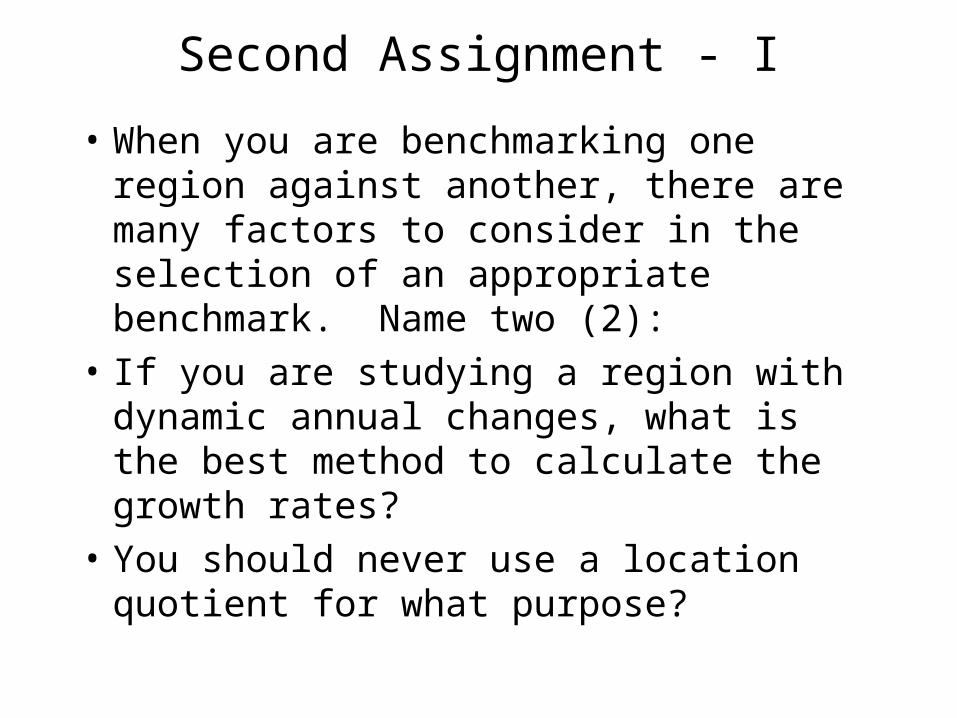

Second Assignment - I

• When you are benchmarking one region against another, there are many factors to consider in the selection of an appropriate benchmark. Name two (2):

• If you are studying a region with dynamic annual changes, what is the best method to calculate the growth rates?

• You should never use a location quotient for what purpose?

Second Assignment Part 2

• There a several considerations for interpreting a location quotient. Name two (2):

• What is the difference between a firm and an establishment?

How do we interpret Pgh’s Growth?

Pittsburgh, 1969-2000

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

19

69

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

State and local

Military

Federal, civilian

Services

Finance, insurance, and real estate

Retail trade

Wholesale trade

Transportation and public utilities

Manufacturing

Construction

Mining

Agricultural services

Pittsburgh, 1969-2000

-

100,000

200,000

300,000

400,000

500,000

600,000

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

Manufacturing

Services

We can look at a basic view

Or a little more complexityPittsburgh, 1969-2000

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

Resource based

FederalGovernmentLocal Serving

Mfg & Trade

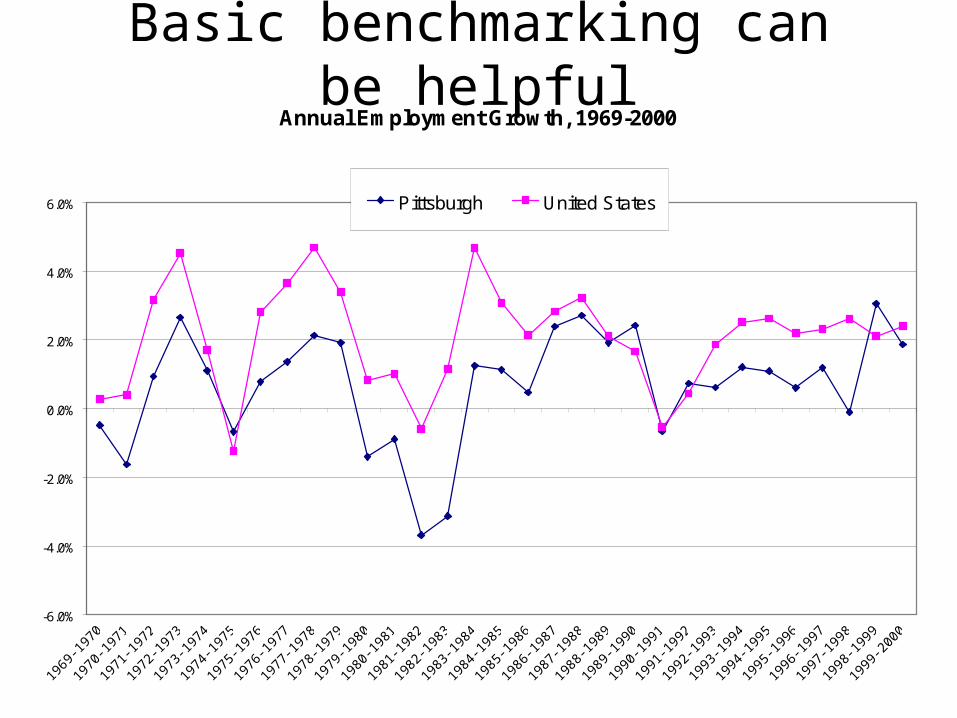

Basic benchmarking can be helpfulAnnual Employment Growth, 1969-2000

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

1969

-197

0

1970

-197

1

1971

-197

2

1972

-197

3

1973

-197

4

1974

-197

5

1975

-197

6

1976

-197

7

1977

-197

8

1978

-197

9

1979

-198

0

1980

-198

1

1981

-198

2

1982

-198

3

1983

-198

4

1984

-198

5

1985

-198

6

1986

-198

7

1987

-198

8

1988

-198

9

1989

-199

0

1990

-199

1

1991

-199

2

1992

-199

3

1993

-199

4

1994

-199

5

1995

-199

6

1996

-199

7

1997

-199

8

1998

-199

9

1999

-200

0

Pittsburgh United States

Basic benchmarking can be helpfulEmployment Change, 1970-1993

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

San Diego Boise Tucson Fresno Memphis New Orleans Toledo Pittsburgh

But these descriptions still haven’t explained much

Location Quotients

Loc

atio

n Q

uot

ien

t

Employment Growth

Important industries that may require attention

High

High

Low

Low

Important growth industries

Industries of little promise to local economy

Potential emerging industries

Total

Total

Industry

Industry

Region

Natio

n

Formula Interpretation

Shift-Share

• What are the 3 components of a shift-share analysis?

• A competitive industry is defined as WHAT?

• Explain– National share– Industry Mix– Regional Shift

• What are the limits of shift-share?

Albuquerque, 1970-1990

Albuquerque 1970 1990 Absolute

Region Total 150,901 342,529 191,628

Target Region Year 1 Year 2 Ri

AGSVC 552 2,268 1,716CON 9,028 18,634 9,606FARM 1,165 1,729 564FED 11,193 14,599 3,406FIRE 12,471 26,569 14,098MFG 10,453 26,240 15,787MIL 7,600 8,134 534MIN 1,388 1,313 -75RETAIL 25,424 59,987 34,563STLGOV 19,322 44,475 25,153SVC 36,971 107,068 70,097TRAN 8,253 14,904 6,651WHSALE 7,081 16,609 9,528

• 127 % total employment growth

• +190,000 Jobs

• What explains this growth?

Three factors…

• Growth of the national economy

• Presence of growth industries (or declining ones)

• Local competitive factors

Albuquerque 1970 1990 Absolute PercentRegion Total 150,901 342,529 191,628 127%

Projected at National Ave.

Projected Mix

Regional Shares

83,770 107,858 14,595 93,263

ChangeEmployment

Diff btw US & actual ch.

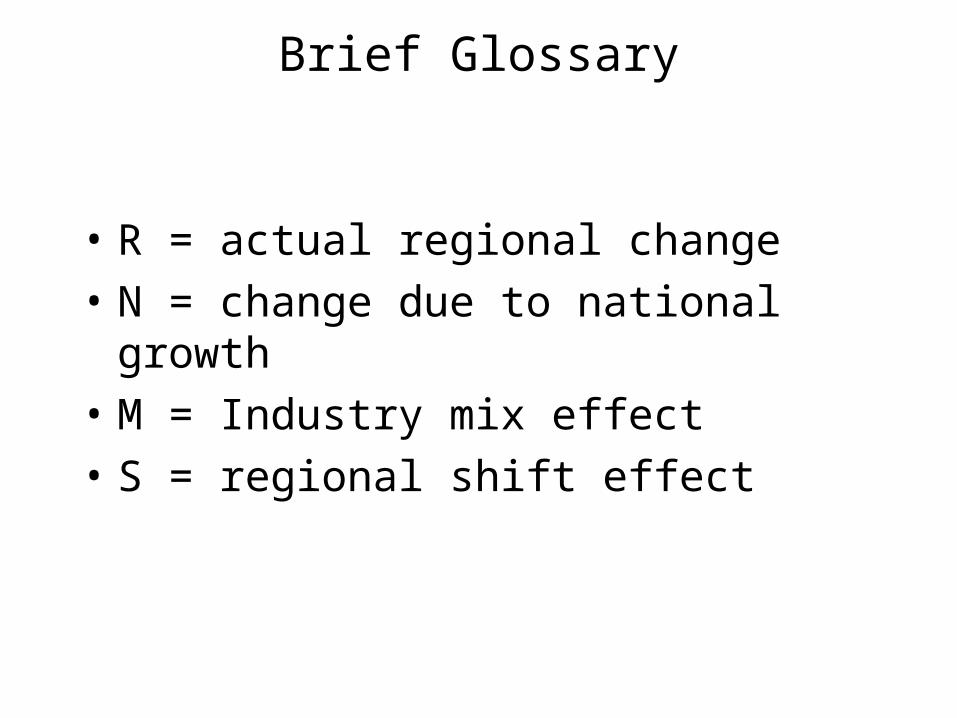

Brief Glossary

• R = actual regional change

• N = change due to national growth

• M = Industry mix effect

• S = regional shift effect

Growth of the U.S. Economy

• If Alb had grown at the U.S. rate, it would have added 83,770 jobs.

• The growth of the U.S. economy accounted for 83,770, or 44% of the actual change.

• Alb in fact added more than 191,000 jobs – so something else must explain the region’s growth

The mix of industries in the region

• The presence of growth industries were not a major factor in the region’s performance. Growth industries on the whole accounted for 8% of the actual change, which equaled 14,595 jobs.

• Must add jobs faster than the nation as a whole to have a positive Mix effect

Local competitive factors

• The shift-share analysis estimates that 49% of the growth in employment is the result of local competitive conditions.

• 93, 263 of the jobs created in Albuquerque were due to these local advantages

• These advantages were spread across every industry but one – Mining.

Albuquerque Industry Data

Target Region Year 2 Ri Ri pct Mi Si

AGSVC 2,268 1,716 311% 668 742CON 18,634 9,606 106% 504 4,090FARM 1,729 564 48% -748 665FED 14,599 3,406 30% -5,037 2,229FIRE 26,569 14,098 113% 2,548 4,627MFG 26,240 15,787 151% -6,287 16,271MIL 8,134 534 7% -5,503 1,818MIN 1,313 -75 -5% 135 -981RETAIL 59,987 34,563 136% 2,266 18,183STLGOV 44,475 25,153 130% -1,527 15,953SVC 107,068 70,097 190% 29,770 19,803TRAN 14,904 6,651 81% -1,884 3,954WHSALE 16,609 9,528 135% -312 5,909

What are the key industries?

We can combine statistics on economic growth, the shift-share, and

specialization (LQs) to highlight leading and lagging industries.

Finding Key Industries

Identify the non-competitive

factors

Fix them if possible

Sustain

Innovate

Develop the value chain - Buyers & Supplier

Prepare for transition

Manage decline

Do nothing

Watch the market

Minimize investment

Not Competitive Competitive

Lag

gin

gL

ead

ing

State and Local Gov

• It is a large industry in the region with considerable growth.

• It is not a growth industry nationally – but this industry does not move on strictly national dynamics.

• It is a desirable goal to growth this industry?

Manufacturing

• Still somewhat small – only 7% of regional employment, less then 27,000 employees.

• Potential emerging sector in the region, but the sector is declining nationally– Can Alb capture more of this industry and for

how long?– Are there subsectors in which the region has a

concentration and an advantage that are growing?

Services

• Employment in Services accounts for 25% of the region’s employment (comparable to the US share).

• The industry grew by 70,000 jobs in the region (190%), well above national and industry growth

• Local factors were positive, but contributed less to the growth than national and industry factors.

Shift-share + benchmarkingShift-Share Comparison, 1970-1993

-600,000

-400,000

-200,000

0

200,000

400,000

600,000

San Diego Boise Tucson Fresno Memphis NewOrleans

Toledo Pittsburgh

Regional Shift

Industry Mix

You may need to normalize the dataRegional Shift as a Proportion of Total Change

(3.50)

(3.00)

(2.50)

(2.00)

(1.50)

(1.00)

(0.50)

-

0.50

1.00

San Diego Boise Tucson Fresno Memphis New Orleans Toledo Pittsburgh

The level of industry detail impacts the shift-share analysis

2digit 4 digitAbsolute Change -10132 -10132National Effect -9450 -9450Industry Mix 690.71 -2759Local Shift -1373 2075.2

• More detail increases the accuracy of the industry mix effect and the local shift.

The time frame impacts the shift-share

1969 2000 R N M S1969-2000 1,128,141 1,384,664 256,523 991,947 -4,278 -731,146

1969 1988 R N M S1969-1988 1,128,141 1,205,775 77,634 571,936 -6,419 -487,883

1988 2000 R N M S1989-2000 1,205,775 1,384,664 178,889 297,892 29,909 -148,912

Aggregated 256,523 869,827 23,491 -636,795

• If the industry structure changes dramatically then a longer time frame distorts the industry mix effect.

Strategies for missing data

• Ignore it• Find an alternative source• Estimate missing midpoint data with an average or

linear projection• Use the proportion of the industry from a higher

level of geography • Project the missing data based on regional growth• Project the missing data based on national industry

growth

Comparing the 3 "Solutions" to missing data

R N M SComplete Data 106,225 67,610 5,990 32,625Incomplete Data 71,221 67,610 5,990 -2,379Partial Data 99,926 61,972 11,259 26,695

For Construction R N M SComplete Data 10,973 3,694 1,963 5,316Incomplete Data 10,973 3,694 1,963 5,316Partial Data 10,973 3,694 1,963 5,316

1 – estimate nondisclosed data

2 – ignore nondisclosed data or assume = 0

3 – exclude missing sectors entirely

Multipliers

• What is a multiplier?– Based on industry input-output

• How do you use them correctly– Change in final demand

– Substitution

– Total vs. direct vs. indirect jobs

• Sources– RIMS II

– IMPLAN

– REMI