registration document...registration document 2010this document is a full translation of the...

TRANSCRIPT

2010REGISTRATIONDOCUMENT

REGISTRATION DOCUMENT 2010

This document is a full translation of the original French text.

The original document was filed with the AMF (French Securities Regulator) on March 4, 2010,in accordance with article 212-13 of the General Regulation of the AMF. As such, it may beused to support a financial transaction if accompanied by a prospectus duly approved by theAMF. Only the French version is legally binding.

This document contains corrected information included in the first update of the RegistrationDocument filed with the AMF on May 6, 2010.

This Registration Document is available online at www.societegenerale.com

Page

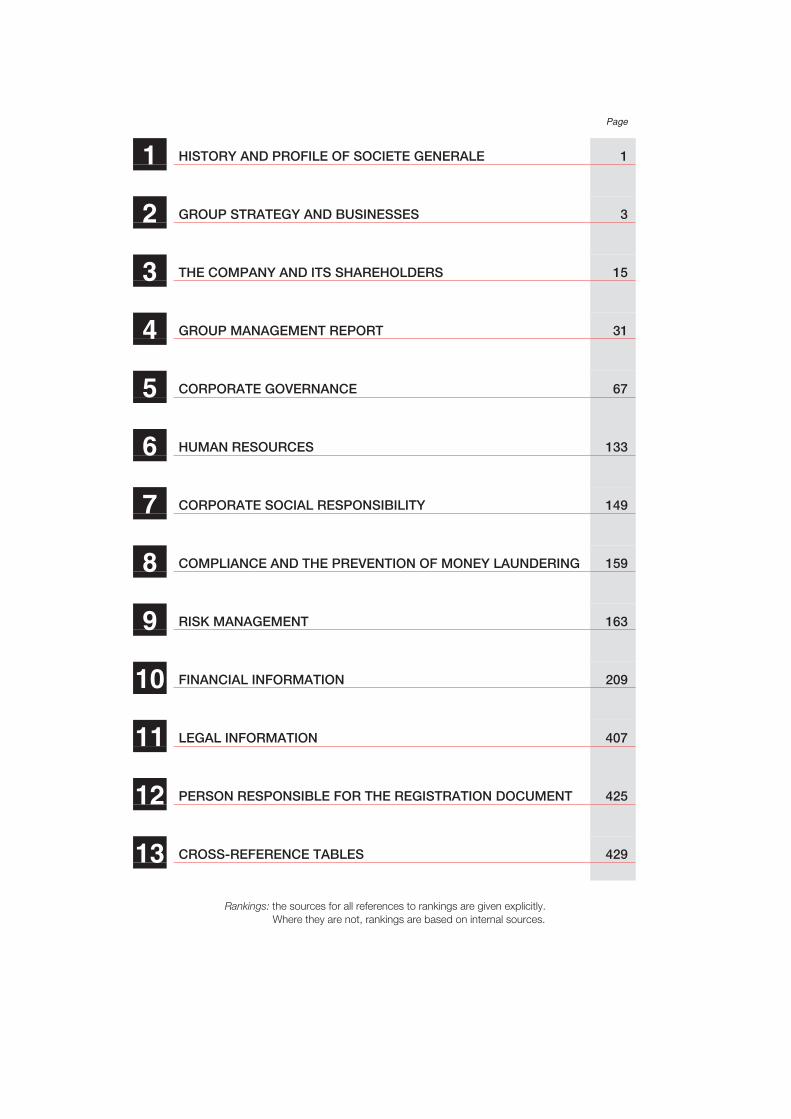

1 HISTORY AND PROFILE OF SOCIETE GENERALE 1

2 GROUP STRATEGY AND BUSINESSES 3

3 THE COMPANY AND ITS SHAREHOLDERS 15

4 GROUP MANAGEMENT REPORT 31

5 CORPORATE GOVERNANCE 67

6 HUMAN RESOURCES 133

7 CORPORATE SOCIAL RESPONSIBILITY 149

8 COMPLIANCE AND THE PREVENTION OF MONEY LAUNDERING 159

9 RISK MANAGEMENT 163

10 FINANCIAL INFORMATION 209

11 LEGAL INFORMATION 407

12 PERSON RESPONSIBLE FOR THE REGISTRATION DOCUMENT 425

13 CROSS-REFERENCE TABLES 429

Rankings: the sources for all references to rankings are given explicitly.Where they are not, rankings are based on internal sources.

1 HISTORY AND PROFILE OFSOCIETE GENERALE

Page

History 2

Profile of Societe Generale 2

SOCIETE GENERALE GROUP - 2010 Registration Document 1

HISTORY AND PROFILE OF SOCIETE GENERALE1

� HISTORY

Societe Generale was founded in 1864 by public subscription,with the aim of financing industrial investments andinfrastructure projects.

During the Third Republic, the company progressively built up anationwide network, and by 1940 had opened a total of 1,500branches compared with just 32 in 1870.

Following the Franco-Prussian war in 1870, the Alsace-Mosellebranches were transferred to a German law subsidiary, SocieteGenerale Alsacienne de Banque (Sogénal).

After opening its first foreign office in London in 1871, SocieteGenerale rapidly developed an international network byextending Sogénal’s activities into Central Europe (Germany,Austria, Switzerland, Luxembourg), and by establishingbranches in North Africa in 1909-1911 and later in the UnitedStates (1940).

Societe Generale was nationalised in 1945, and played anactive role in financing post-war construction. It helped to

spread new financing techniques (such as medium-termdiscountable credit, off-balance sheet operations and leasefinance).

Following the liberalisation of the French banking system in1966, Societe Generale diversified its activities and expandedits individual customer base.

It once more became a private banking group following itsprivatisation in July 1987.

Societe Generale has considerably grown since 1997, thanks tothe development of its franchises and also through acquisitionsin its businesses in Europe and worldwide. With the takeover ofCrédit du Nord (by acquiring a majority stake in 1997 thenbuying out its minority shareholders in 2009), the Groupexpanded its Retail Banking activity on its domestic market, witha network of regional banks. In 2001, Societe Generaleabsorbed Sogénal.

� PROFILE OF SOCIETE GENERALE

Societe Generale, a public limited company (société anonyme),is the parent Company of the Societe Generale Group.

Societe Generale is one of the leading financial services groupsin Europe, operating in 83 countries and employing 156,681staff from 128 different nationalities. Its largest overseas entitiesin terms of their payroll are in Russia, the Czech Republic,Romania, Egypt, Morocco and the United States.

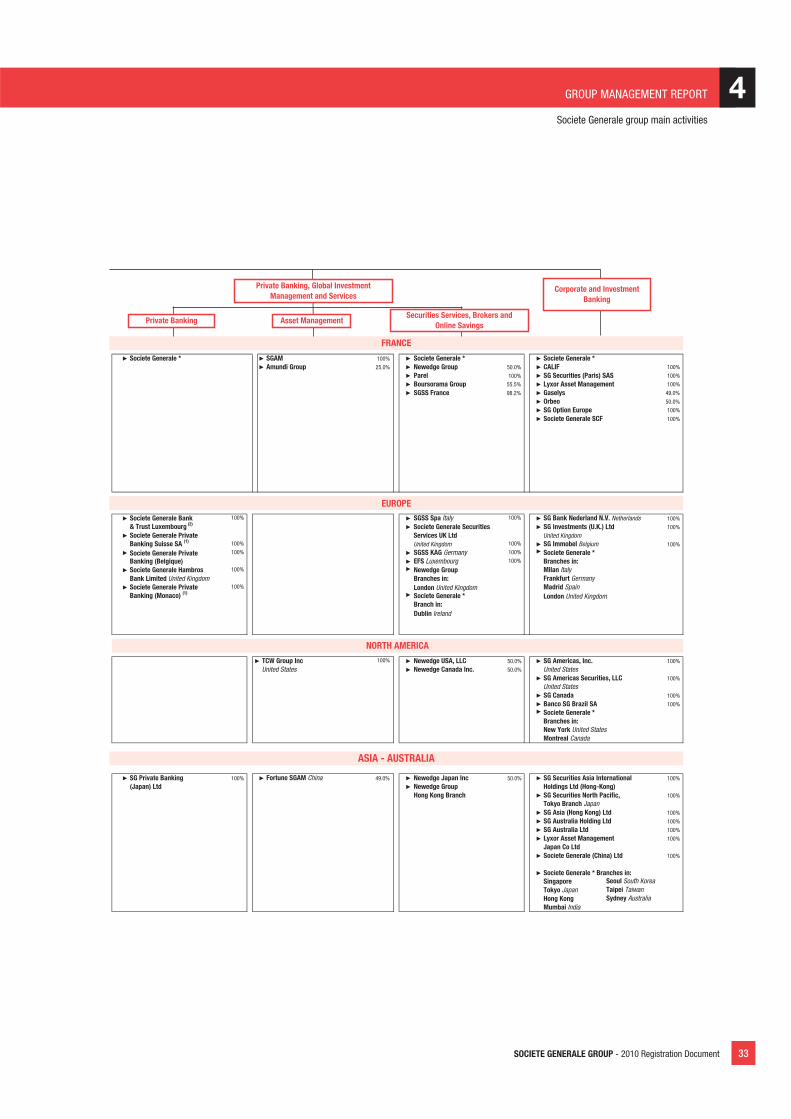

The Group is organised around five core businesses: FrenchNetworks / International Retail Banking / Specialised Financingand Assurances / Private Banking, Global InvestmentManagement and Services / Corporate and InvestmentBanking.

On March 3, 2010, Societe Generale’s long-term rating wasAa2 at Moody’s, A+ at Fitch and A+ at Standard & Poor’s.

2 2010 Registration Document - SOCIETE GENERALE GROUP

2 GROUP STRATEGY AND BUSINESSES

Page

A profitable and balanced growth strategy 4

The Group’s core businesses 6

SOCIETE GENERALE GROUP - 2010 Registration Document 3

GROUP STRATEGY AND BUSINESSES2

� A PROFITABLE AND BALANCED GROWTH STRATEGY, BASEDON A ROBUST UNIVERSAL BANKING MODEL

Although 2009 continued to be difficult, the Societe GeneralGroup was able to capitalise on its robust universal bankingmodel to achieve solid results that have enabled it to absorb thenegative impacts of the crisis.

2009 saw the appearance of the first encouraging signs ofeconomic recovery. The global environment has remainedparticularly fragile and uncertain, however: the financial marketsare still volatile and some have not yet normalised, while thecost of bank liquidity and credit spreads are still far from theirpre-crisis levels. Given this environment, the public authoritieshave massively intervened, taking unprecedented measures tostimulate the economy (fiscal stimulus programmes andaccommodating monetary policies), guaranteeing the liquidityand solvency of certain market players while laying thefoundations for a new regulatory framework. For instance, theguidelines defined during the G20 summit in Pittsburgh notablyprovide for an increase in the capital requirements for marketactivities, the standardisation of accounting and prudential rulesand the introduction of a minimum liquidity standard. The worksdirected by the Financial Stability Board and the BaselCommittee should lead to the definition of the new regulations’outlines and implementation conditions.

In these challenging conditions, the Group has demonstratedthe resilience of its universal banking model, based on aportfolio of diversified businesses, and produced Group netincome of EUR 0.68 billion in 2009. This model has alsoundergone adjustments to take the new environment intoaccount, as shown, for example, by the creation of Amundi,which combines the asset management activities of the Groupand Crédit Agricole SA. Finally, the Group has strengthened itsfinancial structure (Core Tier 1 ratio of 8.4% and Tier 1 ratio of10.7%), particularly thanks to the EUR 4.8 billion capitalincrease completed in October.

The Societe Generale Group therefore appears to be wellpositioned to fully benefit from the end of the crisis, by pursuingits profitable and balanced growth strategy and continuing toadapt its model to the new environment through its “AmbitionSG 2015” project.

The French Networks form the first pillar of the Group’suniversal banking strategy. They experienced sustained growthin 2009, testifying to the strength of the franchise. Theacquisition of the 20% of Crédit du Nord held by Dexia willenable the Group to increase its exposure to these resilientactivities and create synergies. More generally speaking, in

2010 the Group will reassert its multi-brand strategy, based onthree competing and complementary brand companies:

� the multi-channel relationship bank Societe Generale(8.4 million individual customers and 2,282 branches);

� the Network of Crédit du Nord and its regional banks,characterised by a strong culture of local customer relations;

� the leading French on-line bank Boursorama, which relies onan innovative model and attractive price positioning.

The Group intends to continue this growth trend on thesebases, through more effective leveraging of its franchise, byreinforcing remote channels, developing the business customersegment and assisting companies with their financing needs. Inaddition, after a phase of high investment in recent years, theGroup will continue to generate productivity gains by reshapingits processes and through pooling between the variousnetworks.

International Retail Banking’s performance in a turbulentenvironment reflects the strong resilience of the franchises,which have maintained high recurring profitability with arelatively limited cost of risk except for Russia. The Groupremains confident about the medium-term prospects of itsactivities in this country. More generally, Societe Generale willbe very well positioned to benefit from the economic recovery,particularly thanks to very solid positions in certain highpotential markets:

� in Russia, with three brand companies (Rosbank, DeltaCreditand BSGV);

� in Central and Eastern Europe excluding Russia, where theGroup has nearly 6.8 million customers and leadingfranchises (No. 2 bank in Romania and No. 3 bank in theCzech Republic in terms of balance sheet size);

� in the Mediterranean Basin and Sub-Saharan Africa,particularly through its positions in Morocco (No. 3 privatebank) and in Egypt (No. 2 private bank).

Specialised Financing saw its activity slow down in 2009, witha fall in origination affecting most of the businesses and anincrease in the cost of risk in an unfavourable environment. In2010, these activities will still be subject to liquidity constraints,with ongoing vigilance in terms of risk management. Efforts tocontrol operating expenses will be continued, as will theoptimisation of operations. To achieve this, the Group intends topursue its geographic streamlining in synergy with International

4 2010 Registration Document - SOCIETE GENERALE GROUP

GROUP STRATEGY AND BUSINESSES

A profitable and balanced growth strategy, based on a robust universal banking model

2

Retail Banking, particularly for consumer finance, and toconsolidate its leadership in Europe in business financing andservices. With regard to Insurance activities, the Group willcontinue with its policy of catering for Group network customersin France and abroad and its strategy of developing personalprotection insurance in France.

For the Private Banking, Global Investment Managementand Services businesses, the combination of the assetmanagement operations of Crédit Agricole SA and SocieteGenerale was completed on December 31, 2009, creatingAmundi, Europe’s 3rd largest asset manager. This new entity, inwhich Societe Generale holds a 25% stake, will benefit from theresources of the two groups’ distribution networks and majorsynergies from the pooling of production facilities. 2010 will alsosee the operational implementation of the merger between TCWand Metwest, whose expertise in the US fixed incomeinvestment management market is particularly complementary.

Given its good financial results and the recognised quality of itsfranchise (Best Global Private Bank for its range of structuredproducts according to Euromoney, and one of the top 3 privatebanks in Europe according to Private Banker International),Private Banking will continue its development in 2010,particularly capitalising on partnerships with the SocieteGenerale Network and targeted development projects,especially in the Middle East.

As for Securities Services and Newedge, in 2010 the Groupintends to maintain the business growth reported over the year(growth of assets under custody and under administrationmanaged by SGSS, confirmation of the leading positions heldby Newedge in derivative brokerage) while continuing with theproductivity measures already begun.

Corporate and Investment Banking, which recorded anexcellent operational performance in 2009, has solidcommercial franchises for 2010. Equity derivative activitiesconfirmed their leadership, while fixed income, currencies andcommodities activities increased their market share. TheFinancing and Advisory businesses were also widelyrecognised by the market (Best Export Finance Arranger for the8th year running according to Trade Finance, ranked 4th for Eurobond issues and No. 4 for announced M&A deals in France)and Lyxor confirmed its position as a major player in alternativeinvestment management.

In addition, Corporate and Investment Banking’s risk profile wasreduced (significant fall in the VaR and disposal of EUR 8 billionof illiquid assets in 2009) and legacy assets, which producedEUR 4.3 billion of losses over the year, were unified at the endof 2009 within a dedicated structure with a specific governancesystem.

In 2010, SG Corporate & Investment Banking will continue tostrengthen its client-driven activities, particularly by optimisingthe strategic coverage of its largest clients. The Group will alsocontinue with its targeted development, particularly in theadvisory, fixed income and commodities businesses. At thesame time, SG CIB will move ahead with its operationalefficiency optimisation programme through the “Resolution”project, and will maintain strict risk control.

On a more general, cross-business level, with “Ambition SG2015” the Group has initiated a vast company-wide project,which will enable it to capitalise on the post-crisis bankingenvironment, along three main lines:

� strengthening its comparative relationship bankingadvantages, as a bank with strong customer relations. Thisparticularly depends on optimising the product and servicerange and its adaptation to the needs of the Group’s variouscustomer segments, which is vital for sustainable andprofitable growth;

� thoroughly transforming its operational model and increasingprocess industrialisation, to become even more efficient andleverage to our relationship strategy;

� inspiring the long-term commitment of employees to thisambitious company-wide project. To this end, the Group willimplement a series of measures to more effectively developand reward talent and strengthen its positioning as anexemplary employer.

Overall, thanks to the Group’s intrinsic strengths, its growthdrivers and its development projects, Societe Generale is wellpositioned to gain full benefit from the end of the crisis andanticipates a rebound in its financial results as from 2010.Furthermore, Societe Generale intends to pursue its mission offinancing the French economy and to continue supporting itscustomers’ development, while maintaining a high solvencyratio.

SOCIETE GENERALE GROUP - 2010 Registration Document 5

GROUP STRATEGY AND BUSINESSES2

� THE GROUP’S CORE BUSINESSES

The Societe Generale Group’s activities are organised into 5divisions: French Networks / International Retail Banking /Specialised Financing and Insurance / Private Banking, GlobalInvestment Management and Services / Corporate andInvestment Banking.

French Networks

The French Networks are organised around the two structuresand brands Societe Generale and Crédit du Nord with its sixregional banks. They offer a large range of products andservices covering the needs of a diversified customer base,composed of more than 9.8 million individual customers andmore than 500,000 businesses and professionals.

Thanks to its professional and dynamic teams and its multi-channel structure, with a network of more than 3,000 branches,including 16 net openings in 2009, the French Networks led thenon-mutual players with a market share of 9.1% for depositsand 8.6% for loans for resident and non-resident customers.

In 2009, the deposit component of the business saw significantgrowth in average outstandings (+5.3% vs. 2008), mainly drivenby business customers (+15.2% vs. 2008). A +1.8% rise wasreported for individual customer outstandings compared to 2008.

In terms of financing the economy, average loan outstandingsamounted to EUR 153.1 billion, representing +2.8% growthyear-on-year (for the Group as a whole in France, loanoutstandings increased by +3.1% in 2009).

Loan demand, particularly for housing loans, was initially heldback by the wait-and-see attitude of households, but picked upin the 2nd half of 2009, stimulating renewed growth inoutstandings.

On the business market, average loan outstandings reported a+2.8% rise compared to 2008. The fiscal measures taken by theGovernment to help relieve cash flow tensions resulted in acontraction of operating loans, while investment loans increasedby 7.5% in a depressed environment. However, the FrenchNetworks remained true to their policy of supporting theeconomy by financing major projects in many sectors (SAFT,MANUTAN, ORPEA, AUSY, INGENICO, etc.) and for localauthorities.

The financial performance of the French Networks issatisfactory, with net banking income of EUR 7,253 million in2009, up +2.0% compared to 2008 (excluding the PEL/CELeffect and the Visa capital gain of EUR 72 million in 2008), inline with the target set.

2009 also saw the acquisition of the additional 20% of Crédit duNord’s capital by Societe Generale, bringing its stake to 100%.This transaction is aimed at strengthening the Group’spositioning in French Retail Banking and optimising theeffectiveness of its domestic coverage, particularly by poolingresources, while pursuing a multi-brand strategy.

Since January 1, 2010, Retail Banking activity in France hasbeen organised around three structures: the Societe GeneraleNetwork, the Crédit du Nord Network and Boursorama (whichwas previously part of the Private Banking Global InvestmentManagement and Services division).

� Societe Generale Network

Despite a morose economic environment and ongoing strongcompetition, the Societe Generale Network is continuing todistinguish itself through its strong commercial performances.

The Group has continued to develop its franchise thanks to itsnetwork of 2,282 permanent branches (+9 net openings vs.end-2008), mainly located in urban regions where a large shareof the national wealth can be found, and high performanceremote channels. With its extensive and innovative product andservice range and its effective organisation, based on thedeployment of customer advisors, the Group has been able tocreate a true partnership with its customers. The implementationof synergies between individual and business customers andbusiness lines has also helped to create business opportunitiesand consolidate customer relations.

With 5.3 million sight accounts, individual customers are a majorcomponent of the portfolio. The proactive sales initiatives andattractive ranges led to the opening of 67,000 new accountsin 2009, notably by young customers. Regulated SavingsAccounts found renewed favour with the marketing of the LivretA in early 2009 (1.4 million Livret A pass book accounts withoutstandings of EUR 3.8 billion in Q4 09), but also thanks to thesuccess of the Housing Savings Plan (PEL) promotionalcampaign. The success of certain products, such aspersonalised cards (charity cards and affinity cards, lifeinsurance for young people, etc.), testifies to the Group’scontinuous innovation, in line with customer expectations.

6 2010 Registration Document - SOCIETE GENERALE GROUP

GROUP STRATEGY AND BUSINESSES

The Group’s core businesses

2

Societe Generale has also enhanced its sales operationsdedicated to asset management clients, through a joint ventureconcluded with Societe Generale Private Banking, with theopening of a new regional centre in Lille, after the centres inBordeaux, Lyons and Marseille in 2008.

The average loan oustandings driven by individual customerstotalled EUR 65.2 billion, 88% of which are composed ofhousing loans. Deposits came out at EUR 59.4 billion.

The business customer structure and organisation have beenreshaped in recent years. The soundness of this process isreflected in the growth of the franchise: with the acquisition ofmore than 6,000 new SMEs in the last three years, the portfolioincluded 123,000 businesses at the end of 2009. Theprofessionalism and proactive attitude of the 600 dedicatedcustomer advisors have helped to create a close relationshipwith customers. To promote the personalisation of relations,which is one of the key expectations of customers, the SocieteGenerale Network has assisted them with their developmentprojects and given them advice and solutions suited to theirneeds.

There has been proven success for the joint ventures withCorporate and Investment Banking covering interest rate andforeign exchange hedging transactions, advisory services toSMEs and financing for local authorities. These partnershipshave strengthened the Network’s expertise and thereforehelped to improve the net banking income.

At the end of 2009, the average outstandings driven bybusiness customers amounted to EUR 20.7 billion in terms ofdeposits and EUR 60.0 billion in terms of loans.

� Crédit du Nord Network

Crédit du Nord and its six regional banks: Courtois, Kolb,Laydernier, Nuger, Rhône-Alpes and Tarneaud are able todevelop a relationship with customers based on a localapproach, professionalism and innovation. The Group offers itscustomers the benefits of a regional bank on a human scalecombined with the advantages of a country-wide group. This isparticularly thanks to its innovative range, but also to itsorganisation, which promotes local, personalised customerrelations. The Group’s entities are run like real SMEs and enjoyconsiderable decision-making autonomy, meaning that they canrespond quickly to their customers’ requests.

Crédit du Nord’s operating structure, composed of 785branches (7 net openings in 2009) and 8,600 employees,serves 1.4 million individual customers, 150,000 professionalsand associations and more than 33,000 businesses andinstitutional clients.

Professional customers are a priority for the Group, which hastherefore introduced a structure catering for their needs. This isorganised around dedicated advisors, responsible both for thebusiness and private aspect of customer relations, a range ofspecifically developed services and counter services within thebranches.

For the 5th year running, the Crédit du Nord Group led the mainFrench banks in terms of customer satisfaction on the individualand professional customer markets in 2009. It was rankedsecond on the business market. These rankings are a testamentto the Group’s model that positions it as a group of regionalbanks focused on service quality and customer relations.

International Retail Banking

Over the last ten years, the Group has worked to extend anddiversify the regions where it operates, with the aim particularlyof expanding its audience and increasing its businessopportunities. The implementation of a universal bankingstrategy, which largely draws on the French model but isadapted to local circumstances and needs, has enabled it toconfirm its leading positions in Central and Eastern Europe, theMediterranean Basin, Sub-Saharan Africa and the Frenchterritories. At the same time, the Group, through a well-chosenproduct and service range and the partnerships that it hascreated with its customers, has contributed to the economicdevelopment of the various markets where it operates.

The soundness of the strategic decisions and the investmentsaccompanying them is shown by the indicators. At the end of2009, International Retail Banking’s loan outstandings equalledEUR 60.4 billion, in other words x8 compared to 1999, and itsdeposits EUR 64.0 billion, x7 compared to 1999. The network,composed of 652 points of sale through 21 entities in 1999, nowhas 3,767 branches in 37 countries and 41 entities. InternationalRetail Banking’s employees (nearly 61,300), representingnumerous nationalities, offer a wealth of experience for thebenefit of customers. With revenues of EUR 4,724 million in2009, the division accounted for 22% of the Group’s revenues.

In Central and Eastern Europe, the acquisition of BRD inRomania in 1999, then Komercni Banka in 2001, were key stepsin the Group’s international expansion. Its interest in the Russianmarket has been demonstrated since 1993 with the obtaining ofa banking licence in Russia for BSGV and the development of auniversal banking entity as from 2003. This interest was thenconfirmed with the acquisition of DeltaCredit in 2005 and aboveall the acquisition in 2006 of a 20% stake in Rosbank, theleading private network, which the Group now controls, owning

SOCIETE GENERALE GROUP - 2010 Registration Document 7

GROUP STRATEGY AND BUSINESSES2

65.3% of its capital. The Group is currently transforming itsoperations in Russia, drawing on the expertise of specialisedentities (consumer finance, real estate loans, leasing andCorporate and Investment Banking). All of the activities in thiscountry will now be supervised by a legal entity, created for thispurpose, 81.5%-owned by Societe Generale and 18.5%-ownedby Interros & others.

The other transactions completed in Central and EasternEurope in the last three years reflect the Group’s determinationto ensure good geographic coverage of the region, withacquisitions in Croatia and Georgia in 2006, then in Moldavia,Albania and Macedonia in 2007.

Overall, the Group’s operations in the region consist of 2,781points of sale belonging to 17 entities. Its deposit outstandingstotalled EUR 44.5 billion and its loan outstandingsEUR 42.4 billion. In the Czech Republic, Komercni Banka hasthe 3rd largest balance sheet with deposit market shares of18.4% and loan market shares of 18.0%. BRD in Romania,which operates the leading private network with 930 points ofsale, holds loan market shares of 15.6% and deposit marketshares of 16.4%.

In the Mediterranean Basin, the long-standing entities inMorocco (1962) then Lebanon (1969), were joined by those inAlgeria (1999) and Tunisia in 2002. In Egypt, the merger ofNational Societe Generale Bank, acquired in 1978, and ofMIBank (2005), created a major local banking player. TheGroup now operates in 6 countries through 678 points of sale.Its EUR 12.4 billion of deposit outstandings and EUR 11.0 billionof loan outstandings have been largely driven by itssubsidiaries in Morocco and Egypt, where the Group hasleading positions: in Morocco, Societe Generale Maroc is theNo. 3 private bank and in Egypt NSGB is the No. 2 private bank.

In Sub-Saharan Africa and the French territories, the Group’sstructure first of all organised itself around the entities inSenegal and Côte d’Ivoire (1962), then New Caledonia andPolynesia (1971-1973). In 1998, it was extended to BurkinaFaso, Equatorial Guinea and Madagascar, then Chad (1999),Benin (2002) and Ghana (2003), followed by Mauritania in 2007after the acquisition of a majority stake in the BanqueInternationale d’Investissement. Deposit outstandings amountedto EUR 6.7 billion and loan outstandings to EUR 6.2 billion,driven by a portfolio of 1.2 million customers, dominated byindividual customers, but also including the country’s largestcompanies. In line with its policy of investing in regions withhigh potential, since 2008 the Group has turned its attention toAsia. After acquiring 15% of the capital of the Vietnamese bankSeabank in August 2008, which was increased to 20% inDecember 2008, it obtained the status of a local player on theChinese market. More recently, the International Retail BankingNetworks extended their operations in India, following theupturn in Corporate and Investment Banking activities.

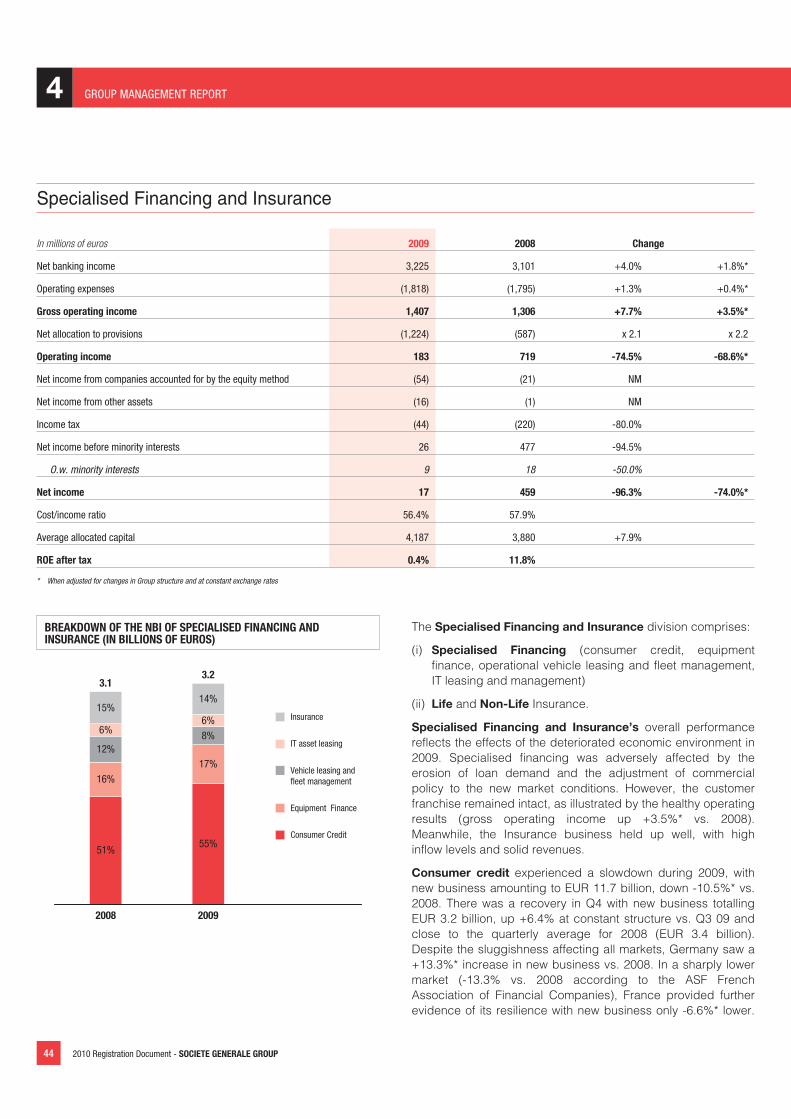

Specialised Financing and Insurance

This division covers:

- Specialised Financing: consumer finance, equipmentfinance, operational vehicle leasing and fleet managementand IT leasing and management

- life and non-life insurance

The Specialised Financing and Insurance division manages anddevelops a portfolio of financing activities in France and abroadfor individual customers and businesses. It operates in 46countries with more than 30,000 employees. Europe is its mainbase of activity (93% of loan outstandings in 2009) where itholds strong positions. These specialised businessescomplement universal banking, with which they implementnumerous synergies while diversifying their distributionnetworks, particularly through partnerships and businessintroducers.

After a period of very sustained internal and external growthfrom 2001 to mid-2008, 2009 was a year of consolidation in amorose economic environment.

Specialised Financing and Insurance revenues equalledEUR 3,225m in 2009, up +1.8% (when adjusted for changes inGroup structure and at constant exchange rates) compared to2008, indicating good resilience to a more difficult environment.

� Consumer finance (SGCF)

The Societe Generale Consumer Finance business linemanages the Group’s international consumer finance activities.Its activity consists of offering multi-product financing solutionsto its individual customers and partners:

- vendor, equipment and vehicle finance for distributors andmanufacturers;

- direct financial solutions for individual customers;

- management services for partner banking networks.

Societe Generale Consumer Finance now operates in 25countries with total outstandings of EUR 23.1 billion. It is rankedNo. 3 in France thanks to its long-standing subsidiaries CGI andFranfinance, No. 4 in Germany and the No. 2 vehicle financingspecialist in Russia with Rusfinance Bank. The business line hasprioritised a strategy of creating specific entities appropriate toeach of their markets and in 2009 it continued thetransformation of its operations while taking the economicenvironment into account. 2009 also saw the operational launchof the consumer finance joint venture with La Banque Postale.

8 2010 Registration Document - SOCIETE GENERALE GROUP

GROUP STRATEGY AND BUSINESSES

The Group’s core businesses

2

� Vendor and equipment finance (SGEF)

SG Equipment Finance, which is the European leader in vendorand equipment finance for businesses, specialises in threesectors of activity: hi-tech products, industrial equipment andtransport. SG Equipment Finance offers businesses tailor-madefinancing solutions (leasing, conventional loans, etc.), throughits business introducer (equipment manufacturers anddistributors) and banking partnerships, and directly to Groupcustomers. At the end of 2009, SG Equipment Finance hadoperations in 25 countries and its outstandings totalledEUR 18.9 billion, excluding factoring.

� Operational vehicle leasing and fleetmanagement

The ALD Automotive business line provides operational vehicleleasing and fleet management. It enables its businesscustomers, whether they are SMEs, Large Corporates orMultinationals, to concentrate on their core activities withoutworrying about the management and maintenance of theirvehicle fleet. This management method, which is expanding,meets companies’ wishes to outsource service management.

ALD Automotive operates in 39 countries on four continents. Forseveral years, ALD Automotive has been the European No. 2and the global No. 3. At the end of 2009, it managed a fleet of793,800 vehicles, including 600,500 under lease.

In 2009, ALD Automotive expanded its network in the USthrough a global partnership with Wheels Inc., a specialist andleader in vehicle fleet management for large corporates in NorthAmerica, and China through a joint venture with Baosteel, theChinese industry leader.

Thanks to these partnerships, ALD Automotive has increased itscapacity to meet the strategic needs of multinationalcompanies.

� IT asset leasing and management (ECS)

ECS is the European leader in IT asset leasing andmanagement and is committed to providing companies withgreater availability, adaptability and control of their informationsystems. ECS operates in 16 countries.

� Insurance

Societe Generale’s Insurance business line combines theSogecap Group’s personal insurance business and the generalinsurance activities of the company Sogessur.

The Sogecap Group (under the international brand name“Societe Generale Insurance”) operates in four areas: lifeinsurance, pension policies, borrower’s insurance andindividual and collective protection. It now has branches in 15countries.

In France, Sogecap, which is the No. 7 life insurer and the No. 4bankassurer, relies mainly on the Societe Generale Network tomarket its range, while its subsidiary Oradea Vie distributes itsproducts through external partners (independent brokers andasset management advisors). The quality of its services and theperformance of its policies receive regular praise from thefinancial press, particularly the Erable Evolution range.

Internationally, Sogecap’s subsidiaries and branches aredeveloping their activities mainly by relying on SocieteGenerale’s Retail Banking Networks and the Group’sSpecialised Financing and Insurance subsidiaries.

In 2009, the Sogecap Group produced a turnover of EUR 8.8 billion,increasing its insurance outstandings (mathematical reserves) toEUR 68.6 billion.

Sogessur is the main partner of the Societe Generale Network inFrance for equipment and personal protection insurance. Thesubsidiary designs, develops and manages a complete rangeof auto, home, accident and legal protection insurance forindividual clients. At the end of 2009, Sogessur managed nearly1,200,000 policies.

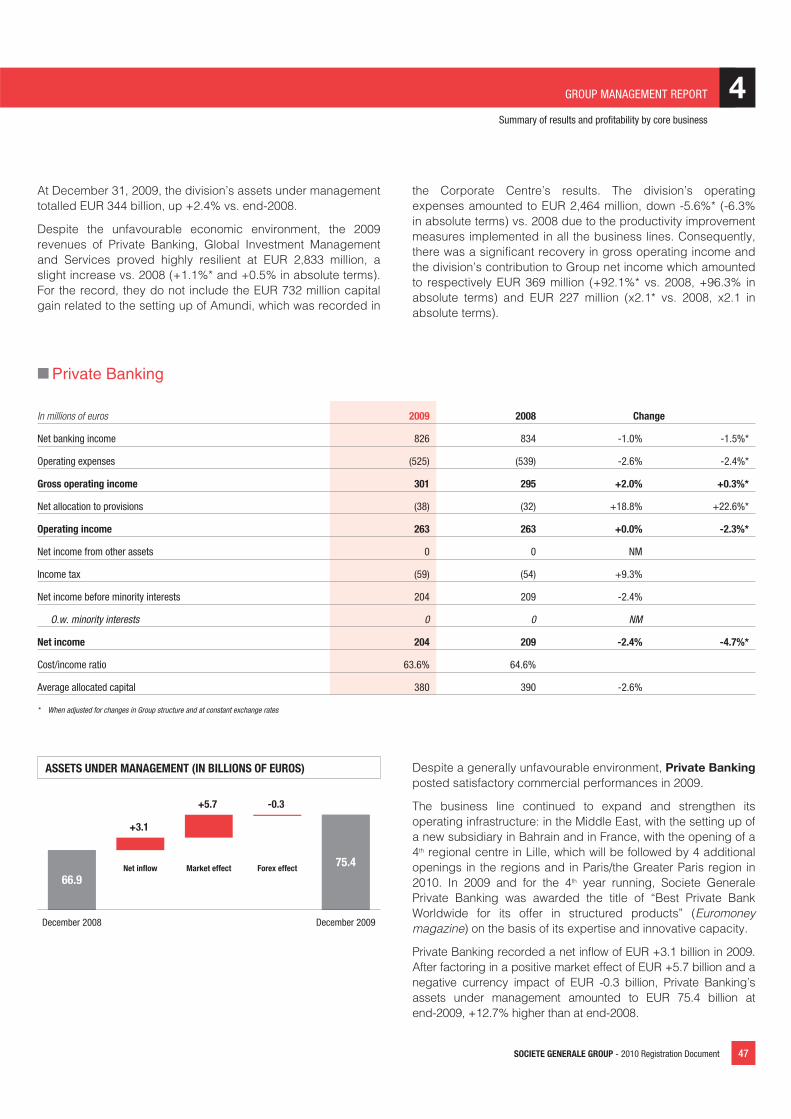

Private Banking, Global InvestmentManagement and Services

The Private Banking, Global Investment Management andServices division consists of Asset Management, with SocieteGenerale Asset Management and Amundi, the partnership withCrédit Agricole Asset Management in operation sinceJanuary 1, 2010; Private Banking with Societe Generale PrivateBanking; the Securities business with Societe GeneraleSecurities Services; derivative brokerage with Newedge andonline banking with Boursorama.

At end-2009, the division’s assets under managementamounted to EUR 344 billion. This figure does not include theassets managed by Lyxor Asset Management, (a consolidatedsubsidiary of the Global Markets business line of Corporate andInvestment Banking), nor does it include the assets of clientsmanaged directly by the French Networks. Assets undercustody continued to grow, reaching EUR 3,073 billion, shoringup the Group’s position as the No. 2 European custodian. Thedivision reported revenues of EUR 2,833 million for 2009.

SOCIETE GENERALE GROUP - 2010 Registration Document 9

GROUP STRATEGY AND BUSINESSES2

� Private Banking

Societe Generale Private Banking’s 2,800 employees, workingin 26 countries, offer a comprehensive range of financialservices suited to the specific needs of business people andindividual clients with a financial net worth of over EUR 1 million.The partnership created in 2008 with Rockefeller & Co has alsoenabled Societe Generale Private Banking to extend itsexpertise to cater for high net worth individuals and familyoffices.

The private bankers rely on an integrated business modelfavouring the design of international solutions to define tailor-made financial and asset management solutions (tax advice,trust advice, and so on) for each client. The strategies regularlyestablished by the international product centres of expertisealso offer a wide choice of investment solutions from anextensive range of markets and asset classes. This includesinvestment funds, hedge funds, structured products, privateequity and real estate. This client range is regularly enhanced tokeep pace with changes in the expectations of SocieteGenerale Private Banking’s clients. For instance, a newinternational centre of expertise dedicated to real estateproducts and services was created at the start of 2009. Thiscapitalises on the real estate expertise of the entire SocieteGenerale Group allowing more diverse real estate investmentopportunities to be offered.

The wealth management structure has also been reinforced. InFrance, a new regional centre was opened in Lille, after thecentres opened in Bordeaux, Marseille and Lyons in 2008.Societe Generale Private Banking already has a strongpresence in Europe and Asia and has continued thedeployment of its activities in the Middle East. After setting upoperations in Abu Dhabi and Dubai under the brand nameSociete Generale Private Banking, the Group has created a newsubsidiary in Bahrain under the brand name Societe GeneraleWealth Management.

The teams’ knowhow and expertise make Societe GeneralePrivate Banking a major, globally recognised wealth manager,as shown by the titles “Best Private Bank Worldwide for its offerin structured products” awarded to Societe Generale PrivateBanking for the 4th year running in 2009 by Euromoneymagazine, and “Outstanding Wealth Manager for Family Officeservices” awarded in 2009 by the magazine Private BankerInternational to the global alliance Societe Generale PrivateBanking / Rockefeller & Co.

At December 31, 2009, the Private Banking business linemanaged EUR 75 billion of assets and reported revenues ofEUR 826 million for 2009.

� Asset Management

Societe Generale Asset Management (SGAM) operates in theworld’s principal investment pools:

� In the US, through its subsidiary TCW. As a recognisedplayer on the US fixed income market, TCW has continued itsdevelopment and increased its capacity to meet clients’needs with the concluding, in December 2009, of a finalagreement to acquire 100% of MetWest, a well-regardedCalifornian asset manager managing nearly EUR 21 billion ofassets. At the end of December 2009, prior to the integrationof MetWest’s assets, TCW managed more than 25% of theassets entrusted to the Group.

� In Europe and Asia, particularly through Amundi’s extensiveoperations.

Through cross-selling and a continuous quality and innovationapproach, SGAM offers a broad client base (institutionals,distributors, businesses, family offices and individuals) primeaccess to an international range of investment products andsolutions covering all the fundamental asset classes andalternative management. SGAM is rated M2 by Fitch Ratingsand, since 2000, has kept the best rating given to an assetmanagement company for its organisation as a whole.

At December 31, 2009, the business line managed EUR 269 billionof assets and reported revenues of EUR 765 million for 2009.

The measures to realign the business line’s range andorganisation, initiated at the end of 2008 and continued in 2009,will be operational from 2010.

SGAM Alternative Investments’ structured, index-fund andalternative management activities will be incorporated with theirequivalents at Lyxor Asset Management, and therefore attachedto Corporate and Investment Banking’s businesses, in the firstquarter of 2010. Lyxor Asset Management will become abroader and more powerful specialised and unique SocieteGenerale Group player, managing a total of EUR 86 billion ofassets and combining the capital market and AssetManagement cultures of these global areas of expertise.

Amundi, the shared asset management division 25%-owned bySociete Generale and 75%-owned by Crédit Agricole, hasexisted as from December 31, 2009. This entity solelycomprises the CAAM Group’s activities, to which SocieteGenerale is contributing its fundamental investmentmanagement activities, 20% of TCW and its joint venture inIndia. At January 1, 2010 it had EUR 670 billion of assets undermanagement, ranking it 3rd in Europe and in the top 8 globally.

10 2010 Registration Document - SOCIETE GENERALE GROUP

GROUP STRATEGY AND BUSINESSES

The Group’s core businesses

2

Amundi enjoys the support of two powerful banking groups,which it will use to develop its strategy along two lines:

� providing savings solutions for the Retail Banking Networks ofthe Societe Generale and Crédit Agricole groups. With50 million individual customers worldwide, Amundi will be amarket leader in Europe and may consider otherpartnerships;

� acting as a multi-expertise asset manager offering a highperformance management range suited to the needs ofinstitutional clients and relying on an extensive internationalnetwork on five continents.

� Securities Services and Online SavingsSECURITIES BUSINESS

Societe Generale Securities Services (SGSS) operates in 25countries and relies on major pan-European platforms to offer acomprehensive, integrated and adaptable range of services,which includes:

� the clearing services activity, combining the sophisticated andflexible management of securities back-office sub-contractingsolutions with a clearing service range that leads the marketand is adapted to the latest changes in the sector;

� the custody and depositary bank activity, which providesfinancial intermediaries and institutional investors with localand international custody services, covering all assetclasses;

� fund administration services on behalf of mutual funds,asset management and investment companies, banks andinstitutional investors, consisting of valuation and middleoffice operations for their complex derivative products (OTCand structured) and the calculation of their portfolios’performance and risk;

� issuer services, notably including the management of stockoption plans, employee share ownership plans and freeshare plans;

� liquidity management (cash and securities) servicesproviding flow optimisation solutions ranging from securitieslending/borrowing to the hedging of forex risk;

� transfer agent activities.

With EUR 3,073 billion of assets under custody at the end ofDecember 2009, SGSS is the 6th global custodian and is ranked2nd in Europe. It also offers its depositary services to 3,062mutual funds and provides the valuation of 4,663 mutual funds,accounting for EUR 450 billion of assets under administration.

In recognition of the expertise of its teams and its ability todevelop innovative technical solutions, SGSS was named“Regional Sub-custodian of the Year: South Europe” by themagazine ICFA (International Custody & Fund Administration).This prestigious title has also been confirmed by the manyawards given by the magazine Global Custodian for the qualityof its range, particularly in Greece, Spain and South Africa.

DERIVATIVE BROKERAGE

Newedge, which was created in 2008 from the merger of thebrokerage activities of Fimat and Calyon Financial (subsidiary ofCrédit Agricole), offers its clients a very extensive andinnovative range of clearing and execution services for listedderivative contracts (on financial instruments and commodities)and OTC contracts (OTC interest rate, foreign exchange, equity,index and commodity derivatives).

Through its operations in around 15 countries on 3 continents,Newedge also offers its clients a single point of entry for accessto more than 85 financial markets worldwide. This largeinternational presence allows Newedge to handle very largevolumes. For instance, in 2009, 1.5 billion deals were executedand 1.6 billion contracts were cleared.

With a market share of 12.5%(1) at the end of November 2009,Newedge is one of the largest players on the global derivativeclearing and execution market. It is also the leading FuturesCommission Merchant in the US.

ONLINE BANKING

Boursorama has operations in four European countries in threedifferent areas:

� Boursorama is the leading online bank in France. Through itswebsite www.boursorama-banque.com the company offers acomprehensive, innovative and high performance solutioncombining conventional banking products with savingsproducts such as mutual funds and life insurance policies.These services are also available in Germany, under thebrand name Onvista Bank, and in Spain, since 2009, underthe brand name SelfBank. In 2009, Boursorama confirmed itsstatus as a leading online bank in France and received anumber of awards from the banking profession. BoursoramaBanque received the “Top Prize for the Best Online Bank2009” (“Le Revenu” magazine, September 2009) and the title“Customer Service Provider of the Year” (BVA-Video Conseilsurvey, July 2009) and also remains the “Least ExpensiveBank” (“Mieux Vivre Votre Argent” magazine, May 2009) forthe 2nd year running. With more than 34,000 accounts openedover the year, Boursorama had more than 107,000 sightaccounts at the end of 2009.

(1) Global Listed Derivatives Exchanges

SOCIETE GENERALE GROUP - 2010 Registration Document 11

GROUP STRATEGY AND BUSINESSES2

� Boursorama is a major European brokerage and onlinesavings player, offering private investors the chance tomanage their savings independently online through acomprehensive range of savings products and services andaccess to the main international financial markets. Theseservices can be accessed in France on the websitewww.boursorama.com, as well as in Germany on www.onvista-bank.de, in Spain on www.selftrade.es, and in the UK onwww.selftrade.co.uk. In 2009, Boursorama executed 6.3 millionstock market orders. Its savings outstandings (mutual fundsand life insurance) in France totalled EUR 2.9 billion at the endof 2009.

� Boursorama is also the leading provider of online financialinformation in France and Germany, through the siteswww.boursorama.com and www.onvista.de.

Boursorama was transferred to the French Networks division onJanuary 1, 2010.

Corporate and Investment Banking

SG CIB is Societe Generale’s Corporate and Investment Bankingarm. With nearly 11,000 employees in 33 countries, SG CIB ispresent on the main financial markets in the regions where theGroup operates, with extensive European coverage andoperations in the Central and Eastern Europe, Middle East andAfrica, Americas and Asia-Pacific zones. It offers its clientsbespoke financial solutions combining innovation, advice and highexecution quality in three areas of expertise: investment banking,financing and market activities.

� SG CIB offers its issuer clients (businesses, financialinstitutions and the public sector) a strategic advisoryapproach, as well as debt or equity fund-raising solutions,optimised financing and answers to their hedging needs;

� SG CIB offers investors, which include asset managers,pension funds, family offices, hedge funds, sovereign funds,banks, insurance companies, distributors and individualcustomers, global access to the equity, fixed income, credit,forex and commodity markets and a unique range of cross-asset tailor-made solutions and advice, based on top marketexpertise.

Given the changes in the economic and financial environmentand in order to come out of the crisis as one of the leadingcorporate and investment banks, SG CIB has changed theorganisation of its activities, taking into account three priorities:developing its client-driven approach, increasing operationalefficiency and transaction security and improving its risk profile.

To strengthen its positions, facilitate cross-selling and thereforebetter serve its clients, SG CIB has therefore reorganised theformer “Equities”, “Fixed Income, Currencies and Commodities”and “Financing and Advisory” divisions around two divisions:

� Global Markets now unites the “Equities” and “FixedIncome, Currencies and Commodities” market activitieswithin a single Markets platform, to offer a multi-productvision and optimised cross-asset solutions;

� Financing and Advisory which, aside from the coverage andcorporate banking activities that it already incorporated, nowincludes some activities that previously belonged to the“Equities” and “Fixed Income, Currencies and Commodities”divisions.

SG CIB has also launched a project to optimise the Resourcemanagement structure, notably based on processindustrialisation and increased coordination between the frontand back offices. This project will be gradually introduced fromthe first quarter of 2010 to improve operational efficiency(reduced operational risks, supporting of the activity’sdevelopment and enhanced customer service).

� Global Markets

To assist its clients in an environment where the financialmarkets are increasingly interconnected, SG CIB has united itsexperts within an integrated platform, providing global accessto the equity, fixed income, credit, forex, commodities andalternative management markets. SG CIB’s financial engineers,salespeople, traders and specialist advisors use all of theseunderlyings to offer bespoke solutions suited to the specificneeds and risks of each client. These solutions take the form ofsimple transactions, or structured deals for more complexarrangements.

EQUITIES

SG CIB’s historic presence on all the world’s major primary andsecondary equity markets and its long-standing tradition ofinnovation give it a leading position in a comprehensive rangeof varied solutions, covering every cash, derivative and equityresearch activity.

� Equity derivatives are one of SG CIB’s areas of excellence,for which it has received regular awards from the bankingprofession, which once again this year gave it the title “EquityDerivatives House of the Year” (Risk Magazine, January2010) and “Global Provider in Equity Derivatives” (RiskMagazine, September 2009). SG CIB’s leadership in this fieldis also illustrated by its top ranking in flow activities: with amarket share that is continuing to grow, amounting to 13.9%at the end of 2009, the bank is global No. 1 for warrants. Ithas also maintained its No. 2 ranking on the European ETF(Exchange Traded Funds) market, with a market share of20.8%.

12 2010 Registration Document - SOCIETE GENERALE GROUP

GROUP STRATEGY AND BUSINESSES

The Group’s core businesses

2

� Thanks to its large range of innovative and effectiveinvestment solutions, Lyxor Asset Management, a 100%subsidiary of Societe Generale that offers structured, index-fund and alternative management solutions, was awarded thetitles “Institutional Manager of the Year” (AlternativeInvestment News, Institutional Investor, July 2009) and “BestFund-linked House and Best Fund-linked Structured Product:Asia” (Finance Asia, for the 2nd year running) in 2009. As partof the reorganisation of Private Banking, Global InvestmentManagement and Services’ asset management activities,SGAM Alternative Investments’ structured, index-fund andalternative management activities will be transferred to Lyxorin early 2010. At December 31, 2009, the assets managed byLyxor amounted to EUR 73 billion.

FIXED INCOME, CREDIT, CURRENCIES ANDCOMMODITIES

Fixed income activities cover an exhaustive range of productsand services ensuring the liquidity, pricing and hedging of risksrelating to the fixed income, credit, forex and commodityactivities of SG CIB’s clients.

� Fixed income, credit and currencies: the fixed income,credit and currencies teams, based in London, Paris, Madridand Milan, as well as the US and the Asia-Pacific region, offera large range of flow and derivative products. They provideSociete Generale’s clients with personalised solutions to meetasset and liability management, risk management andrevenue optimisation needs. SG CIB’s expertise has alsobeen regularly recognised in this field. For instance, in 2009,SG CIB was ranked No. 1 for European credit research(Euromoney Survey, European Fixed Income Research, May2009).

� Commodities: for nearly 20 years, SG CIB has been a majorplayer on the commodities market, both for energy (oil,natural gas, coal, Liquefied Natural Gas, etc.) and metals(base and precious metals). The alliances created withindustrial partners – Gaselys with GDF Suez and Orbeo withRhodia – have also enabled SG CIB to become a majorplayer on the European natural gas, electricity and CO2

emissions market. Finally, as a 1st category member of theLondon Metal Exchange, SG CIB provides clearing andexecution services for futures and options contracts. In 2009,SG CIB was named “Commodity Derivatives House of theYear” by Energy Risk magazine.

Aside from providing market access for all of these underlyings,SG CIB’s Cross Asset research team, made up of analysts allover the world, produces many themed and multi-productanalyses covering all asset classes. These analyses, which helpto interpret market trends and translate them into strategies, arean excellent decision-making tool for investors, and as suchreceive regular awards. In 2009, for example, the division’smacro-economic research and strategic research teams were

ranked No. 1 by the Extel survey. SG CIB’s research was alsoranked No. 1 for French equities (Thomson Extel Europe survey)in 11 out of the 14 categories defined by Euromoney, for FixedIncome, and for oil (Risk Commodity Rankings).

� Financing and AdvisoryThe “Financing and Advisory” division unites the “Coverage &Investment Banking” and “Global Finance” activities.

COVERAGE & INVESTMENT BANKING

The “Coverage & Investment Banking” teams offer theirclients, which include businesses, financial institutions and thepublic sector, an integrated, global, tailor-made approachbased on:

- extensive strategy advisory services, covering mergers andacquisitions and IPO structuring, as well as debt and capitalrestructuring and ALM; and

- access to optimised fund-raising solutions, notably throughthe creation of joint ventures with Global Finance and MarketActivities.

In 2009, SG CIB was ranked the 4th “Financial Advisor in Francebased on M&A deals announced” (Thomson Reuters,December 2009) and was bookrunner for the Arcelor Mittalconvertible bond issue, which received the award “EMEAStructured Equity Issue of the Year” (IFR magazine).

GLOBAL FINANCE

The “Global Finance” teams rely on global expertise and broadsector knowledge to provide issuer clients with an exhaustiverange and integrated solutions in three key areas: fund-raising,structured financing and hedging of interest rate, foreignexchange and inflation risks.

The debt and equity fund-raising solutions provided by SG CIBare made possible by its capacity to offer issuers access to allof the global markets and to create innovative strategicfinancing and acquisition or LBO financing solutions. Thereorganisation of SG CIB also included uniting part of thecapital market financial engineering activities (balance sheetand debt optimisation and securitisation), which previouslybelonged to the “Fixed Income, Currencies and Commodities”divisions, within Global Finance, so as to enhance the coverageof issuer clients within a single division.

SG CIB’s capital market expertise has given it a leading positionon the Euro-denominated debt capital markets (No. 4 at the endof 2009 according to IFR magazine and No. 3 for Euro corporateissues).

SG CIB offers its clients the benefit of its structured financingexpertise, which is globally recognised in many sectors: export,real estate and the hotel industry, infrastructures and assets,and natural and energy resources.

SOCIETE GENERALE GROUP - 2010 Registration Document 13

GROUP STRATEGY AND BUSINESSES2

In 2009, SG CIB was voted “Best Global Export FinanceArranger” for the 8th year running by Trade Finance magazine.Its achievements on the commodity markets also won it the title“Best Commodity Finance Bank”, awarded by Trade Financemagazine. Furthermore, it was named “Best Arranger of ProjectFinance Loans” for the 2nd year running by Euroweek magazine.

� Legacy assetsSome assets made illiquid as a result of the credit crisis,because of their nature (CDOs of RMBS’, RMBS’, CMBS’ andother European, US or Australian ABS’) or their structure (assetshedged by monolines, exotic credit derivatives, etc.) are nolonger in line with the bank’s strategic objectives and riskprofile. They were identified in 2008 and have been graduallygrouped together and entrusted to a dedicated team,responsible for managing them until they are extinguished. Thisteam implements diversified strategies (selling, portfolio

restructuring, setting up of hedges, etc.) to optimise exitconditions, in accordance with the risk reduction target and theobjective of reallocating resources to Corporate and InvestmentBanking’s strategic activities. It is subject to a specificgovernance approach optimising interactions between theMarket, Risk and Finance Divisions. The centralisation of theseassets was completed in 2009. To facilitate the reading andunderstanding of Corporate and Investment Banking’sperformances, the revenues produced by these legacy assetsare now disclosed separately from the revenues of coreactivities.

In 2009, SG CIB generated revenues of EUR 6,867 million,including EUR 9,693 million produced by core activities(EUR 7,200 million from market activities and EUR 2,493 millionfrom Financing and Advisory activities), while legacy assetsgenerated negative revenues of EUR -2,826 million.

14 2010 Registration Document - SOCIETE GENERALE GROUP

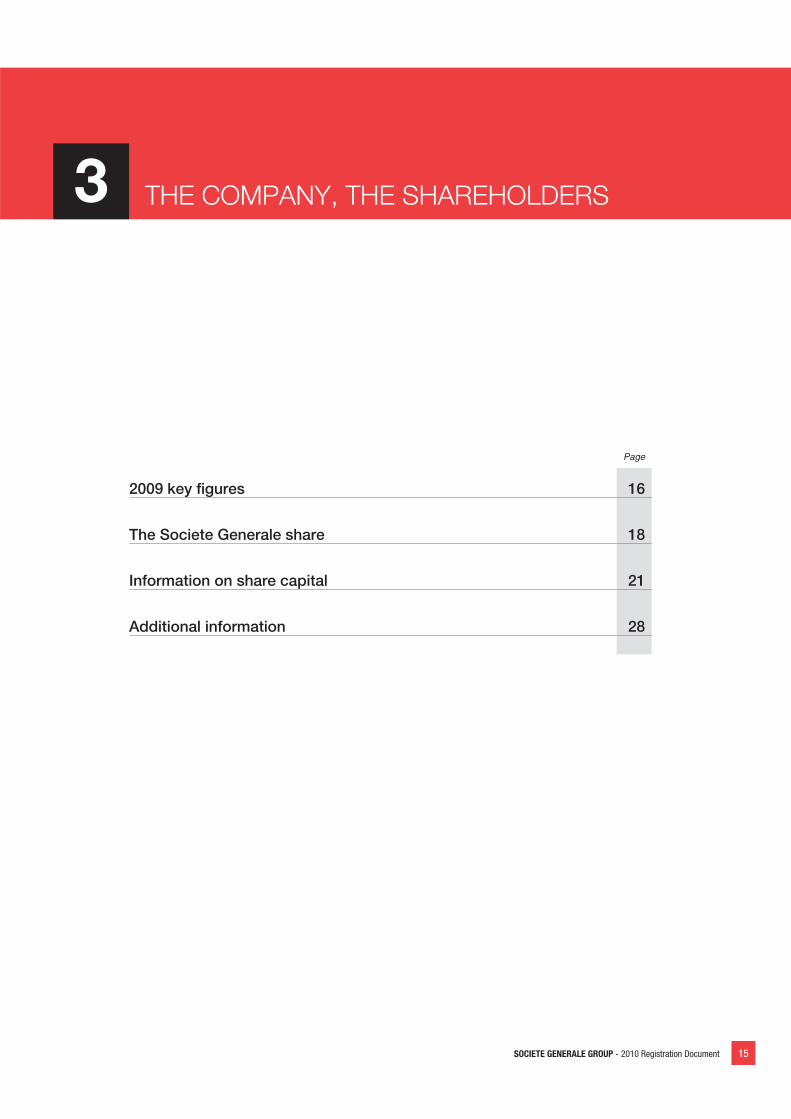

3 THE COMPANY, THE SHAREHOLDERS

Page

2009 key figures 16

The Societe Generale share 18

Information on share capital 21

Additional information 28

SOCIETE GENERALE GROUP - 2010 Registration Document 15

THE COMPANY, THE SHAREHOLDERS3

� 2009 KEY FIGURES2009 2008 (1) 2007 2006 2005

Results (in millions of euros)Net Banking Income 21,730 21,866 21,923 22,417 19,166

Operating income excluding net loss on unauthorised andconcealed trading activities 116 3,683 6,713 8,035 6,562

Operating income including net loss on unauthorised andconcealed trading activities 1,802

Net income before minority interests 1,108 2,773 1,604 5,785 4,916

Net income 678 2,010 947 5,221 4,402

French Networks 971 1,251 1,375 1,344 1,059

International Retail Banking 445 618 686 471 386

Specialised Financing and Insurance 17 459 600 521 453

Private Banking, Global Investment Management and Services 227 110 652 577 460

Corporate and Investment Banking 623 (1,870) (2,221) 2,340 1,841

Corporate Centre and other (1,605) 1,442 (145) (32) 203

Activity (in billions of euros)Total assets and liabilities 1,023.7 1,130.0 1,071.8 956.8 835.1

Customer loans 344.5 354.6 305.2 263.5 227.2

Customer deposits 300.1 282.5 270.7 267.4 222.5

Assets under management 344 336 435 422 386

Equity (in billions of euros)Group shareholders' equity 42.2 36.1 27.2 29.1 23.0

Total consolidated equity 46.8 40.9 31.3 33.4 27.2

Average headcount (2) 160,144 160,430 130,100 115,134 100,186

2005-2007: Basel I2008-2009: Basel II(1) Changes in 2008

– The Corporate Centre includes the accounting effects related to the revaluation of debts linked specifically to own credit risk and credit derivative instruments used to hedge the loans and receivables portfolios previously included inCorporate and Investment Banking’s results;– All of the real estate subsidiaries (GENEFIM, SOGEPROM and GENEFIMMO and their respective subsidiaries), which were previously affiliated with Corporate and Investment Banking, except for ODIPROM, have been affiliated with theFrench Networks.

(2) Including temporary staff.

CONTRIBUTION OF THE CORE BUSINESSESTO THE GROUP’S NET BANKING INCOMEEUR 21.7 billion

Net banking income

EUR 0.68 billionNet income

Globallysatisfactorycommercialperformancein France and abroad

Reduction of therisk profile

Realignment withthe newenvironment

6.3

2.3

2.0

2.6

5.7

7.0 4.5 1.5

6.9

2.8

3.2

4.7

7.3

2.8

3.1

5.0

7.2

3.7

2.8

3.4

7.1

3.2

2.4

2.8

6.8

24.919.621.622.218.9

2005 2006 2007 2008 2009

French Networks

International Retail Banking

Specialised Financing andInsurance

Corporate and InvestmentBanking

Private Banking, GlobalInvestment Management andServices

(In billions of euros)

Core businesses

16 2010 Registration Document - SOCIETE GENERALE GROUP

THE COMPANY, THE SHAREHOLDERS

2009 key figures

3

NET BANKING INCOME

(In billions of euros)

2005 2006 2007 2008 2009

19.2

22.4 21.9 21.925

20

15

10

5

0

21.7

GROSS OPERATING INCOME

7.0

8.7

0

1

2

3

4

5

6

7

8

9

(In billions of euros)

2005 2006 2007 2008

7.6

6.3

2009

6.0

NET INCOME

4.4

5.2

0

1

2

3

4

5

6

(In billions of euros)

2005 2006 2007 2008

0.9

2.0

2009

0.7

SHAREHOLDERS’ EQUITY

23.0

29.127.2

36.1

42.2

2005

(In billions of euros)

2006 2007 2008 2009

25

45

40

30

35

20

15

10

5

0

ROE AFTER TAX (1)

26.1 25.8

(In %)

2005 2006 2007 2008

25

30

20

15

10

5

0

3.6

6.4

2009

0.9

B.I.S. RATIO (2)

31.12.2008 31.12.2009

Core Tier 1*

Tier 2

*Tier 1 = Hybrid capital + Core tier 1

Hybridcapital*

(In %)

14

12

10

2

4

6

8

0

13.0

11.6

8.4

2.3

2.3

6.7

2.1

2.8

2005-2007: Basel I

2008-2009: Basel II

(1) Group ROE calculated on the basis of average Group shareholders’ equity under IFRS (including IAS 32 & 39 and IFRS 4), excluding unrealised capital losses and gains except fortranslation reserves, deeply subordinated notes, undated subordinated notes and after deduction of interest to be paid to holders of these notes.

(2) Does not reflect additional minimum capital requirements (in 2008, the Basel II requirement cannot be lower than 90% of CAD requirements).

SOCIETE GENERALE GROUP - 2010 Registration Document 17

THE COMPANY, THE SHAREHOLDERS3

� THE SOCIETE GENERALE SHARE

Stock market performance

Societe Generale's share price increased by 43.5% in 2009,closing at EUR 48.95 on December 31. In comparison, the CAC40 index gained 22.3% and the DJ EURO STOXX BANK index48.9%.

At December 31, 2009, the Societe Generale Group’s marketcapitalisation stood at EUR 36.2 billion, ranking it 11th amongCAC 40 stocks (7th largest stock in terms of free float) and 6th

among euro zone banks (6th at December 31, 2008).

The market for the Group’s shares remained highly liquid in2009, with an average daily trading volume on the CAC 40 ofEUR 151.43 million, representing a daily capital rotation ratio of0.61% (versus 1.18% in 2008). In value terms, SocieteGenerale's shares were the 6th most actively traded on the CAC40 index.

Stock exchange listing

Societe Generale’s shares are listed on the Paris StockExchange (deferred settlement market, continuous tradinggroup A, ISIN code FR0000130809) and are also traded in theUnited States under an American Depository Receipt (ADR)programme.

Stock market indices

The Societe Generale share is a component stock of theCAC 40, STOXX 50, EURO STOXX 50, Euronext 100, MSCIEURO, FTSE4 Good and ASPI Eurozone indices.

Total return* for shareholders

The following table shows the cumulative and annualised average total return on investment for Societe Generale shareholders overdifferent time periods ending December 31, 2009.

Duration of shareholding DateCumulative total

return*Annualised average

total return*

Since privatisation Jul. 8, 1987 747.6% 10.0%

15 years Dec. 31, 1994 360.1% 10.7%

10 years Dec. 31, 1999 42.9% 3.6%

5 years Dec. 31, 2004 -12.7% -2.7%

4 years Dec. 31, 2005 -39.9% -12.0%

3 years Dec. 31, 2006 -53.6% -22.6%

2 years Dec. 31, 2007 -41.8% -23.7%

1 year Dec. 31, 2008 47.7% 47.7%Source: Datastream.

* Total return = capital gain + net dividend reinvested in shares.

18 2010 Registration Document - SOCIETE GENERALE GROUP

THE COMPANY, THE SHAREHOLDERS

The Societe Generale share

3

Dividend history

2009 2008 2007 2006 2005

Net dividend (in EUR) * 0.25 (1) 1.20 (2) 0.90 5.20 4.50

Payout ratio (%) (3) 55.6 35.5 45.8 42.2 41.8

Net yield (%) (4) 0.5 3.3 0.9 4.0 4.3

* In accordance with standard IAS 33, per share data relating to periods preceding the capital increases that occurred in Q4 2006, Q1 2008 and Q4 2009 have been adjusted for the ratios published by Euronext. The adjusted dividendsamounted to EUR 1.14 in 2008, EUR 0.80 in 2007, EUR 4.61 in 2006 and EUR 3.97 in 2005.

(1) Amount and option of payment in new shares will be submitted to the General Meeting.

(2) Dividend with option of payment in new shares

(3) Net dividend/earnings per share.

(4) Net dividend/closing price at end-December.

Stock market data Dec. 31, 2009 Dec. 31, 2008 Dec. 31, 2007 Dec. 31, 2006 Dec. 31, 2005

Share capital (number of outstanding shares) 739,806,265 580,727,244 466,582,593 461,424,562 434,288,181

Market capitalisation (in EUR billion) 36.2 20.9 46.2 59.3 45.1

Earnings per share (in euros) * 0.45 3.20 1.75 10.94 9.50

Book value per share at year-end (in euros) * 48.9 49.6 50.0 56.5 47.1

Share price (in euros) * high 53.8 87.8 140.6 119.9 93.3

low 18.0 26.1 83.3 89.5 65.6

closing 49.0 34.1 87.8 114.1 91.6* In accordance with standard IAS 33, per share data relating to periods preceding the capital increases that occurred in Q4 2006, Q1 2008 and Q4 2009 have been adjusted for the ratios published by Euronext.

SHARE PERFORMANCE *

10

20

30

40

50

60

70

80

90

Dec

- 07

Dec

- 08

Feb

- 09

Jan

- 09

Mar

- 09

Apr -

09

May

- 09

Jun

- 09

Jul -

09

Sep

- 09

Oct -

09

Nov

- 09

Dec

- 09

Feb

- 08

Jan

- 08

Mar

- 08

Apr -

08

May

- 08

Jun

- 08

Jul -

08

Aug-

08

Aug-

09

Sep

- 08

Oct -

08

Nov

- 08

Societe GeneraleDJ Euro Stoxx BanksCAC 40

Source : Datastream

* Historical series adjusted for the impact of the capital increases carried out in Q1 2008 and Q4 2009.

SOCIETE GENERALE GROUP - 2010 Registration Document 19

THE COMPANY, THE SHAREHOLDERS3

MONTHLY CHANGE IN SHARE PRICE *

0

10

20

30

60

70

90

Jan. Feb. March April May June July August Sept. Oct. Nov. Dec. Jan. Feb. March April May June July August Sept. Oct. Nov. Dec.

40

50

80

2008 2009

63.0 61.258.1

62.5 62.2

52.248.0

56.4

51.5

31.6

26.129.0

23.4 21.318.0

28.233.0

36.3 35.2

43.7

47.0

43.6 43.7

46.3

87.0

77.9

67.472.5 74.4

62.558.8

66.3 64.9 65.1

45.7

37.535.4

30.5 30.3

37.441.5 42.2 42.7

53.8 53.450.9 50.7 49.3

Source: Datastream

* Historical series adjusted for the impact of the capital increases carried out in Q1 2008 and Q4 2009.

TRADING VOLUMES (AVERAGE DAILY TRADED VOLUME AS % OF CAPITAL**)

2008 2009

0.0

0.5

1.0

1.5

2.0

2.5

Jan. Feb. March April May June July August Sept. Oct. Nov. Dec. Jan. Feb. March April May June July August Sept. Oct. Nov. Dec.

1.821.97

1.43

0.89

0.69

0.94 0.94

0.75

1.23 1.33

0.85

0.62 0.680.78

0.95

0.67 0.70

0.45 0.42 0.46 0.52

0.94

0.49

0.34

Source: Datastream

** Share capital excluding preference shares

20 2010 Registration Document - SOCIETE GENERALE GROUP

THE COMPANY, THE SHAREHOLDERS

Information on share capital

3

� INFORMATION ON SHARE CAPITAL

Changes in share capital

OperationsDate of record or

completion ChangeTotal number of shares

after operationsShare capital

(in euros)

Change in share capitalresulting from operation

(%)

Exercise of stock optionsfrom October 27 to December 31, 2006

Dec. 31, 2006recorded on Jan. 11, 2007 395,846 461,424,562 576,780,702.50 0.08

Exercise of stock options(1st half 2007) andincrease through 2007 Company Savings Plan Jul. 11, 2007

261,4144,578,835 466,264,811 582,831,013.75 1.05

Exercise of stock options (2nd half 2007)Dec. 31, 2007

recorded on Jan. 11, 2008 317,782 466,582,593 583,228,241.25 0.07

Exercise of stock options from January 1 to 11,2008 recorded on Feb. 5, 2007 34,080 466,616,673 583,270,841.25 0.01

Capital increase with pre-emptive subscription rightsdecided on February 8, 2008 recorded on Mar. 14, 2008 116,654,168 583,270,841 729,088,551.25 25.00

Increase through 2008 Company Savings Plan recorded on Jun. 24, 2008 7,456,403 590,727,244 738,409,055.00 1.28

Cancellation of shares Nov. 2, 2008 10,000,000 580,727,244 725,909,055.00 (1.69)

Issue of preference shares (B shares) recorded on May 28, 2009 45,045,045 B shares

622,772,289 divided into582,727,244A shares and

45,045,045 B shares 782,215,361.25 7.76

Increase through the exercise of the option for thepayment of dividends in shares recorded on Jun. 17, 2009 13,810,504 A shares

639,582,793 divided into594,537,748A shares and

45,045,045 B shares 799,478,491.25 2.21

Increase through 2009 Company Savings Plan recorded on Jul. 10, 2009 10,757,876 A shares

650,340,669 divided into605,295,624A shares and

45,045,045 B shares 812,925,836.25 1.68

Exercise of stock options in 2009 recorded on Oct. 15, 2009 411 A shares

650,341,080 divided into605,296,035A shares and

45,045,045 B shares 812,926,350.00

Capital increase with pre-emptive subscription rightsdecided on October 5, 2009 recorded on Nov. 2, 2009 134,510,230 A shares

784,851,310 divided into739,806,265A shares and

45,045,045 B shares 981,064,137.50 20.68

Cancellation of preference shares decided onNovember 3, 2009 recorded on Dec. 23, 2009 45,045,045 B shares 739,806,265 A shares 924,757,831.25 (5.74)

SOCIETE GENERALE GROUP - 2010 Registration Document 21

THE COMPANY, THE SHAREHOLDERS3

Share capital

At December 31, 2009, Societe Generale's paid up sharecapital amounted to EUR 924,757,831.25 and comprised739,806,265 shares with a nominal value of EUR 1.25 per share,all eligible for dividends paid out of income earned fromJanuary 1, 2009.

As part of the Group's capital market activities, transactionsmay be carried out involving indices or underlying assets with aSociete General share component. These transactions do nothave an impact on the Group's future capital.

The increase by 159,079,021 shares in 2009 includes:

� the issue of 134,510,230 shares through the capital increasewith pre-emptive subscription rights performed in October2009;

� the issue of 13,810,504 shares following the distribution ofdividends in shares in June 2009;

� the issue of 10,757,876 million shares subscribed by theGroup’s employees in July under the Global Employee ShareOwnership Plan;

� the exercising of share subscription options, issued by theCompany, on 411 shares.

In accordance with article 19 of its By-laws, on May 28, 2009,Societe Generale issued 45,045,045 preference shares to theSociété de Prise de Participations de l’Etat (SPPE). These shareswere bought back by Societe Generale on November 4, 2009before being cancelled on December 23, 2009.

Share buybacks

The Joint General Meeting of May 19, 2009 authorised theCompany to buy or sell its own shares with a view to cancellingbought-back shares, granting, honouring or covering stockoptions, otherwise allocating shares or making any other form ofallocation to employees and Chief Executive Officers of theGroup, granting shares when rights attached to convertiblesecurities are exercised, holding and subsequently usingshares in exchange or as payment for acquisitions andcontinuing the liquidity contract set up in November 2004. Theliquidity contract was terminated on December 31, 2009.

Under the agreement concluded on December 9, 2008between the French government and the Societe GeneraleGroup relating to the subscription by the government ofsubordinated notes issued by Societe Generale, the Groupundertook not to buy back its own shares throughout theholding period of the notes subscribed by the government,except for redemptions to honour or cover the Group'semployee share ownership plans and day-to-day managementoperations.

Since it launched its share buyback programme in September1999, Societe Generale has bought back 108.4 million of its

own shares, for a total net amount of EUR 8.4 billion. In 2002,Societe Generale cancelled 7.2 million shares representing atotal of EUR 438 million, followed by a further 18.1 million in2005, representing a total of EUR 1,352 million, and 10.0 millionshares in 2008 totalling EUR 1,217 million.

Overall, Societe Generale bought back 2,111,262 ordinaryshares in 2009 worth EUR 57,401,425.88 and sold ortransferred 1,138,227 shares with a total disposal value ofEUR 13,827,409.12.

� 275,732 shares were used for the payment of acquisitions in2009;

� 1,835,530 shares were allocated to employees to cover freeshare plans.

During the capital increase with pre-emptive subscription rightsin Q4 2009, Societe Generale sold 12,024,864 rights attachedto treasury shares worth EUR 31,729,236.29.

The total transaction cost of the buybacks was EUR 28,700.71.

22 2010 Registration Document - SOCIETE GENERALE GROUP

THE COMPANY, THE SHAREHOLDERS

Information on share capital

3

From January 1, 2009 to December 31, 2009

Purchases Disposals / Exercise of stock options

Number Purchase price Number Purchase price Disposal / strike price

Cancellation 0 - 0.00

Acquisitions 275,732 25.12 6,925,796.18 275,732 25.12 6,925,796.18 27.91 7,695,680.12

Allocation to employees 1,835,530 27.50 50,475,629.70 862,495 94.26 81,299,845.44 7.11 6,131,729.00

Total 2,111,262 27.19 57,401,425.88 1,138,227 77.51 88,225,641.62 12.15 13,827,409.12

Between January 1, 2010 and February 17, 2010, Societe Generale purchased 2,000,000 of its own shares for a purchase price ofEUR 85,970,000. These shares were immediately earmarked for allocation to employees.

Share buybacks and treasury shares

At December 31, 2009, the Societe Generale Group held11,976,621 shares under its share buyback programme,representing 1.62% of its capital, and 8,987,016 treasuryshares, representing 1.21% of its capital. In total, the Groupholds 20,963,637 of its own shares either directly or indirectly

(excluding shares held under trading operations), with a netbook value of EUR 940,555,421.95 and a nominal value ofEUR 26,204,546.25. Of this total, 11,976,621 shares, with amarket value of EUR 808,078,421.95, have been allocated tocover stock options and free shares granted to employees.

VALUE OF TREASURY SHARES AND BUYBACKS AT DECEMBER 31, 2009

Percentage of capital held directly or indirectly 2.83% *

Number of shares cancelled over the last 24 months 10,000,000

Number of shares held directly 11,976,621

Net book value of shares held directly EUR 808,078,421.95

Market value of shares held directly EUR 582,082,270.86* 3.85% including stock set aside for the coverage of 2005, 2006 and 2007 stock option plans.

At December 31, 2009 Number of shares Nominal value (in euros) Book value (in euros)

Societe Generale 11,976,621 14,970,776 808,078,422

Subsidiaries 8,987,016 11,233,770 132,477,000

Finareg 4,944,720 6,180,900 80,180,000

Gene-act1 2,210,112 2,762,640 19,385,000

Vouric 1,832,184 2,290,230 32,912,000

Total 20,963,63 26,204,546 940,555,422

SOCIETE GENERALE GROUP - 2010 Registration Document 23

THE COMPANY, THE SHAREHOLDERS3

Breakdown of capital and voting rights (1) over 3 years

At December 31, 2009 (2) At December 31, 2008 At December 31, 2007

Number ofshares

% of capital% of voting

rights*Number of

shares% of capital

% of votingrights*

Number ofshares

% of capital% of voting

rights*

Group Employee ShareOwnership Plan 52,775,654 7.13% 10.46% 41,219,452 7.10% 10.91% 33,458,863 7.17% 11.56%

Major shareholders with morethan 1% of the capital andvoting rights

67,824,045 9.17% 12.32% 62,303,884 10.73% 14.71% 47,737,086 10.23% 15.63%

Groupama 31,338,265 4.24% 5.55% 23,831,529 4.10% 5.78% 16,336,391 3.50% 5.48%CDC 16,754,025 2.26% 2.78% 14,253,665 2.45% 3.09% 10,778,058 2.31% 3.10%

Meiji Yasuda LifeInsurance Cy 11,069,312 1.50% 2.74% 11,069,312 1.91% 3.43% 11,069,312 2.37% 4.16%

CNP 8,662,443 1.17% 1.25% 6,805,811 1.17% 1.28% 5,188,089 1.11% 1.25%

Fondazione CRT (3) (3) (3) 6,343,567 1.09% 1.12% 4,365,236 0.94% 1.64%

Free float 598,242,929 80.87% 74.63% 457,213,306 78.73% 71.27% 355,074,822 76.10% 67.11%

Buybacks 11,976,621 1.62% 1.48% 11,003,586 1.89% 1.71% 21,324,806 4.57% 4.01%

Treasury stock 8,987,016 1.21% 1.11% 8,987,016 1.55% 1.39% 8,987,016 1.93% 1.69%

Total 100.00% 100.00% 100.00% 100.00% 100.00%

Number of outstanding shares 739,806,265 807,180,185 580,727,244 644,824,914 466,582,593 531,812,177

(1) Including double voting rights (article 14 of Societe Generale’s by-laws).

(2) At December 31, 2009, the share of European Economic Area shareholders in the capital is estimated at 45.9%.

(3) Shareholder with less than 1% of the capital and voting rights

As % of capital

9.17%Major shareholderswith more than 1%of capital and votingrights

7.13%Group employeeshare ownershipplan

1.21%Treasury stock

1.62%Buybacks

80.87%Other

As % of voting rights*

12.32%

10.46%Group employee shareownership plan

1.11%Treasury stock

1.48%Buybacks

74.63%Other

Major shareholders withmore than 1% of capital

and voting rights

* As of 2006 and in accordance with article 223-11 of the AMF’s General Regulations, the total number of voting rights is calculated on the basis of all shares with voting rights attached.

24 2010 Registration Document - SOCIETE GENERALE GROUP

THE COMPANY, THE SHAREHOLDERS

Information on share capital

3

Shareholder agreements

On July 24, 2000, Societe Generale signed an agreement withSantander Central Hispano concerning the management of thetwo parties' cross-holdings. Under the terms of this agreement,Societe Generale and Santander Central Hispano each grantthe other party a pre-emptive right to the shares held directly orvia a subsidiary by each of the parties in the capital of the other,although this right does not apply in the event of a public offermade by a third-party for the shares of one or other of theparties.

The agreement was signed initially for a period of three yearsand is subsequently renewable for two-year periods.

This pre-emptive clause was published by the French FinancialMarkets Council in Decision No. 201C1417 datedNovember 30, 2001. This agreement was still in place atDecember 31, 2009. However, at this date, Santander CentralHispano no longer held any shares in Societe Generale.

Information about article L. 225-100-3 ofthe French Commercial Code