regulation and investment in telecommunications: chile

TRANSCRIPT

W D R D i a l o g u e T h e m e 3 r d c y c l e

D i s c u s s i o n P a p e r W D R 0 6 0 8

Regulation and Investment in Telecommunications: Chile Case Study

M a r c h 2 0 0 6

L e o n a r d o M e n a C o r o n e l Comments invited, please post them to the author or online at: http://www.regulateonline.org/content/view/680/31/

2

The World Dialogue on Regulation for Network Economies (WDR) The WDR project was initiated by infoDev, which provides foundation funding. Additional foundation support is provided by the International Development Research Centre (IDRC – Canada), and the LIRNE.NET universities: the Center for Information and Communication Technologies (CICT), Technical University of Denmark; the Economics of Infrastructures Section (EI), Delft University of Technology, The Netherlands; the LINK Centre at the University of Witwatersrand, South Africa; and the Media@LSE Programme at the London School of Economics, United Kingdom.

The WDR Project is managed by the Learning Initiatives on Reforms for Network Economies (LIRNE.NET), an international consortium of research and training centres, administered at the Center for Information and Communication Technologies (CICT), Technical University of Denmark. Members include the Technical University of Denmark; the Delft University of Technology, the Netherlands; the London School of Economics, UK; the University of Witwatersrand, South Africa; LIRNEasia, Sri Lanka; and Comunica, Uruguay.

The World Dialogue on Regulation for Network Economies (WDR) facilitates an international dialogue to generate and disseminate new knowledge on frontier issues in regulation and governance to support the development of network economies.

Contact: WDR Project, LIRNE.NET Center for Information and Communication Technologies Technical University of Denmark, Building 371 DK 2800 Lyngby, DENMARK Phone: +45 4525 5178

Fax: +45 4596 3171 Email: [email protected]

WDR Project Coordinator Merete Aagaard Henriksen: [email protected]. WDR <www.regulateonline.org> LIRNE.NET <www.lirne.net> © 2006 The World Dialogue on Regulation for Network Economies (WDR)

3

Table Contents

Acronyms.......................................................................................................................... 4 Executive Summary .......................................................................................................... 5 About the Author ............................................................................................................... 4

1 Introduction ....................................................................................................................... 7 2 Measuring the Telecommunications Regulatory Environment (TRE)................................. 7 3 The Chilean Telecommunications Sector .......................................................................... 9

3.1 Competition Defence Bodies.................................................................................... 13 3.2 Investment in Telecoms ........................................................................................... 14

4 Fixed Telephony Regulatory Environment....................................................................... 18 4.1 Market Entry ............................................................................................................ 18 4.2 Scarce Resources ................................................................................................... 20 4.3 Interconnection ........................................................................................................ 20 4.4 Rate Regulation ....................................................................................................... 21 4.5 Regulation of Anti-Competition Practices ................................................................. 24 4.6 Evaluation of the Regulatory Environment ............................................................... 24

5 Mobile Telephony Regulatory Environment..................................................................... 24 5.1 Market Entry ............................................................................................................ 24 5.2 Scarce Resources ................................................................................................... 27 5.3 Interconnection ........................................................................................................ 28 5.4 Rate Regulation ....................................................................................................... 28 5.5 Regulation of Anti Competition Practices ................................................................. 28 5.6 Evaluation of the Regulatory Environment ............................................................... 29

6 Conclusions .................................................................................................................... 30 6.1 Lessons Learnt ........................................................................................................ 32

7 Bibliography .................................................................................................................... 33

4

Acronyms

ADSL asymmetric digital subscriberlLine CMET Complejo Manufacturero de Equipos Telefónicos

CTC Compañía Telefónica de Chile ENTEL Empresa Nacional de Telecomunicaciones LMDS local multipoint distribution system

SUBTEL Subsecretaría de Telecomunicaciones (telecom regulator) TelSur Telefónica del Sur TelCoy Compañía de Teléfonos de Coyhaique VTR Vía Transradio Chilena WLL wireless local loop

About the Author Leonardo Mena Coronel – graduated as an Electric Civil Engineer from the University of Chile and obtained a Master of Arts in Economics at Georgetown University. He is a telecom expert and has broad experience in the fields of technical-economics and regulation. He has participated in high level telecom regulatory processes in Chile, and from 1996-2004, and has worked closely with the authorities on the evaluation of studies for regulating local, wireless and rural network public and access tariffs. From 1998-2000, he was in charge of the Telecommunication Development Department, which provides more than 6000 areas with pay phones. In 2004, he was part of the group of experts in charge of evaluating the access tariffs divergences reported in cost studies by the regulatory authority and the main local and mobile companies. His current focus is telecom and information technology public policy fields, specifically with regards to technological convergence, network unbundling, Internet consumption patterns, electronic payment services and electronic document standards for the public sector.

5

Executive Summary Although investment trends are influenced by many national and international factors, during last decade, investment flow behaviour in the Chilean telecom sector has been affected in particular by regulatory actions. Reforms have stimulated investment, creating openings for new business as well as improving observed trends in the already more dynamics ones. This case study assesses the telecom regulatory environment (TRE) in Chile to examine the different factors impacting on perceptions and mitigation of investment risk. The evaluation considers five dimensions: (1) entrance to the market, (2) access to scarce resources, (3) interconnection, (4) tariff regulation, and (5) regulation of anti-competitive practices. The selected evaluation periods (1994-1998 and 1999-2004) coincide with key regulatory events in the sector, as well as with important changes in investment flows. In particular, in 1994 the telecom law was reformed in anticipation of the opening of the market, particularly for long distance. Further key events for these periods of analysis include the establishing of regulated prices for the dominant operator from May 1994 to May 1999; PCS mobile phone concessions beginning to offer services between 1998 and 1999; implementation of “Calling Party Pays”; and tariffs for the dominant operator established for the period from May 1999 to May 2004. Telecom investment flows were on the increase until 1997, with more than USD 1,000 million for that year. From 1997 to 1999, a slight reversion in the trend was observed due to an overall decrease in economic activity. However, for 2000 there was again an improvement resulting in a higher investment level than for any other year during the 1990s. During 2000, investment in the sector reached about USD 1,120 millions, with 40% allocated to mobile infrastructure improvements. During 1994-1998, increases in fixed local lines took place during a period of uncertainty produced by a new legal framework involving technical and tariff aspects of interconnection that restrained new entrants. This situation resulted in an unsatisfactory evaluation of four out of the five dimensions of examination. Despite legal changes, interconnection between local companies was subject to imbalanced negotiations between operators and only dominant operator investments benefited. The former monopoly of long distance communications, especially international calls, was weakened by competition and the end of cross-subsides. The first period of assessment for mobile telephony (1994-1998) can be understood as the beginning of competition due to the development of regulations to introduce new competitors and to generate cost based pricing conditions for interconnection with local operators. The precarious level of regulations is evident in the results of the evaluation of the regulatory environment, with the exception of free public tariffs, which was evaluated in a positive way. During this period, mobile incumbents made investments to protect their position from new entrants; in fact, they digitalized their networks and introduced alternative market forms – in particular, prepaid – in order to attain better conditions before the granting of new PCS concessions in 1998.

The period 1999-2004 was especially complex for local telephony, because despite an improved TRE, in particular pertaining to market entrance and interconnection, this period was marked by an international contraction of the sector. However, the higher efficiency imposed by the regulator on the dominant operator in 1999 tariff regulation, and which was strongly resisted, allowed the cable operator to take advantage of economies of scope and capitalize on the new regulatory environment. This resulted in growth during the 1999-2004 period and demonstrated clear leadership in introducing new technologies. By the end of the period, competition was characterized by the deeper maturity of the market and a slower expansion.

For mobile telephony, the environment improved in a significant way, stimulating investment. Between the two periods assessed, there was a qualitative leap in regulation. The entrants had effective regulations and both sector and anti-monopoly regulatory activity allowed

6

development and growth to the extent that investment in the mobile segment reached and quickly exceeded that of the local segment. Interconnection and tariff conditions improved significantly, as well as the entrance to market with the new licenses and the additional aspects imposed by the authority. In short, between the two periods of assessment there was an important change in the composition of investments due to a beneficial environment and conditions of higher certainty around interconnection and pricing. Moving beyond twisted pairs, the mobile and cable networks became more relevant towards the end of period. In this context, participation of the dominant local operator suffered an important decline. Cable and mobile phone competition were consolidated. The TRE methodology used in this case study provides a broader understanding of the impact produced by the new regulatory measures.

7

1 Introduction Although investment is influenced by several national and international factors, including sectoral regulation, since early in the last decade trends in investment flows for the Chilean telecom sector have been affected by regulatory actions. Reforms in the sector have stimulated investment, directly opening new spaces to investors and/or reinforcing the positive trends observed in the more dynamic segments. Between 1988 and 1989, public companies, Compañía de Teléfonos de Chile (CTC), now Telefónica CTC-Chile, and Empresa Nacional de Telecomunicaciones (ENTEL) were privatized, consequent to the telecom law which had previously been amended in 1987, incorporating a rate-fixing methodology based the average costs of an efficient company, with rates based on incremental development costs.1 While Chilean telecommunications opened up early to competition with the enactment in 1982 of General Telecommunications Law eliminating the legal monopoly and encouraging the entry of competitors into local telephony, the weaknesses of the law, particularly regarding interconnection rules, inhibited competition until 1994, when it was amended.2

The period from 1994-2004 was marked by intense competitive activity driven by the opening of national and international long distance markets, and the generation of technical pro-competitive regulations during the first half of the period, and by mobile telephony and cable during the second, coupled with the consolidation of sectoral regulations. These competitive spaces were opened via actions undertaken by the sectoral and anti-monopoly regulators. The methodology employed in this study assesses the telecom regulatory environment (TRE) across five dimensions: (1) entrance to the market, (2) access to scarce resources, (3) interconnection, (4) tariff regulation, and (5) regulation of anti-competitive practices. The results obtained reflect the opinion of the author3 exclusively, and as a preliminary investigation are intended to be used as input for subsequent in-depth assessments to canvass perceptions of a broader cross-section of stakeholders. This paper is organised as follows. The next section provides an overview of the methodology. Section three introduces the Chilean telecom sector, including key regulatory events and investment trends. The next sections assess the TRE in terms of fixed line regulation (section 4) and mobile telephony (section 5), followed by conclusions (section 6). Additionally, the study includes four annexes: a timeline of the main regulatory and business landmarks for the sector, background information on the regulatory institution, ownership of the main operators in the sector, and further details of the assessment undertaken.

2 Assessing the Telecom Regulatory Environment (TRE) It is possible to identify three main sources of investment risk, namely sectoral, macro or country, and regulatory and business sources. Macro-level risk includes factors that affect the economy as a whole, such as inflation, rates of exchange or the country’s political stability. Regulatory risk refers to the uncertainty associated with government actions, including the sectoral regulator and other authorities (such as health, environmental or other authorities) intervening in the corresponding industry. Business risk is associated with factors

1 Long-term Incremental Cost 2 Fisher and Serra (2002). 3 The author was assisted by economist Silvana Sánchez, whom he thanks for her work.

8

such as demand, substitutes and performance of competitors.4 The methodology used in this study focuses on the regulatory environment facing existing and/or potential telecom operators, that is to say, it corresponds to a subset of the regulatory risk, described as the telecommunications regulatory environment, which includes specific aspects of the telecom sector.

The TRE methodology seeks to measure the perception of significant stakeholders, so the specific regulatory environment, negative or positive, is not based, at least directly, on quantitative information, but on the subjective appreciation of the agents regarding several factors. In particular these factors correspond to the context of investment (new or incremental) and the nature of the subsector in which investment is made (fixed or mobile networks). Furthermore, the way in which investors perceive the TRE changes depending on their situation regarding their investments at a particular point in time. Indeed, once the investment has been made, investors will be particularly sensitive to changes in factors that mitigate anticipated profits. Conversely, they will react negatively to elements favouring the opening of the market to new stakeholders. Stakeholders’ diverse situations, as a result of their particular investments, whether in dominant, minority or new operator’s projects, as well as the status of these investments (effective or potential), illustrate the usefulness of TRE assessment methods that traverse a range of opinions, and take them into account. Diversity of perspective can be garnered through mechanisms such as surveys to solicit subjective views of investors, and/or others coming from academia or experts – thus reflecting a general point of view summarising the environment conditions prior to the entry of an investor. In the case of mechanisms based consulting stakeholders, such as surveys, focus groups and panels, the complexity is associated with the way of achieving an adequate level of representation. It is necessary to identify the range of stakeholders, that is to say, the active individuals within the regulatory sphere, and to achieve representation when considering their perceptions. As noted above, the purpose of this study is to represent the perceptions of existing and potential operators, and other stakeholders. Regarding the former, a survey would be enough to obtain all the information, although in the case of the latter, opinions are founded on the perceptions of stakeholders outside the sector, largely foreign operators and institutional investors who may be willing to fund certain projects. These investors form their opinions on the basis of a much broader setting than the operators in the sector and the sectoral regulator, encompassing financial analysts, study centres, sectoral consultancy groups, mass media, providers, and other financial institutions, among other entities. As a result, measuring the environment in this manner requires the mixture of direct and indirect opinions capable of shaping the opinion of potential investors.

The case study undertaken for Sri Lanka, upon which this document is based, chose to conduct a pilot survey based on the opinion of a sectoral expert, and then extend the study to include ther perspectives of a number of informed stakeholders. The second step, which involves obtaining a cross-section of stakeholders, was not undertaken for this current preliminary assessment for Chile.

It is fair to note that investment may be affected by companies’ internal factors alien to the regulatory environment and even the overall investment environment. An operator’s global strategy may affect the rest of the stakeholders’ investments, as might have been the case of the investment policies followed in Chile by Telefónica, when it decided to invest in Brazil, and Telecom Italia, when it pulled out of the region. As a result, these factors will have an indirect effect through the impact these decisions make on the perception of the other stakeholders, who, faced with the same regulatory conditions, can react by evaluating the TRE more pessimistically or optimistically.

4 Samarajiva and Dokeniya (2005).

9

In another respect, the study focuses on the relation between gross capital formation and sectoral regulatory environment in Chile. This, despite the maturation process of the sector, has also been associated with a change in ownership and its concentration, resulting from mergers and acquisitions. This process, inherent in developing markets, may correspond to several factors, such as cost-cutting measures, the withdrawal of investors whose opportunity costs no longer justify participating in a certain market, or other situations that are reflected in the business environment but are neutral to gross capital formation.

This case study corresponds to the first stage of the methodology employed for the Sri Lanka case, which involves obtaining the author’s independent opinion as a starting point to move forward in its application to the Chilean case in particular, and Latin-American in general. This first study makes it possible to access the necessary inputs to deal with a second panel stage and, in the future, have the use of accurate periodic measurements representative of the regulatory environment in the sector. As regards the inputs provided by the study, the periods relevant to the evaluation, a chronology that will allow stakeholders to adopt a position in the context of each evaluation period, and a first evaluation that will motivate a discussion and generate a common context for the interpretation of the factors contained in the methodology are identified. Although the availability of this first motivating, informative vision seems positive, caution must be used to prevent its dissemination among those consulted from causing a starting-point bias in their answers. For this purpose, it may be wise to subject the paper to discussion and obtain opinions that support or challenge the author’s perceptions in the first place. Joint dissemination of the paper and opinions about it may correct the bias. The evaluation periods chosen allow the stakeholders to easily adopt a position in each of them, through the identification of relevant regulatory landmarks that have changed the conditions of competition in the sector, coinciding with changes in the magnitude and composition of investment flows. In 1994 the General Telecommunications Law was amended, with the opening of the market, especially the long-distance market, and the dominant operator’s rates were fixed for the period May1994-May1999. In 1999 the Calling-Party-Pays system was incorporated into mobile telephony and the dominant operator’s rates were fixed for the period May 1999- May 2004. In this study, the evaluation of the regulatory environment is undertaken in terms of five dimensions: entry into the market, access to scarce resources, interconnection, rate regulation, and regulation of anti-competition practices. The evaluation of each period is undertaken mainly with regard to the other period considered, which hinders comparison among countries. The final evaluation of each dimension is undertaken on a five-point scale: poor (1), unsatisfactory (2), neutral (3), satisfactory (4), and excellent (5).

The data used come from public sources, available on the Internet, mainly on the sectoral5, and anti-monopoly6 regulator’s sites and those of the companies in the sector.

3 The Chilean Telecommunications Sector The Chilean telecommunications sector is structured around 24 primary zones corresponding to local service delivery, within which long-distance telephone communications also occur. Historically, Telefónica CTC-Chile was a monopoly covering 21 primary zones, with the other three, in the south of the country, accounting for 5% of the lines offered by the local monopoly Telefónica del Sur (TelSur) and its subsidiary Telefónica de Coyhaique. For mobile telephony, all granted concessions are countrywide.

5 Subsecretaría de Telecomunicaciones (www.subtel.cl). 6 Fiscalía Nacional Económica (www.fne.cl) and Tribunal de Defensa de la Libre Competencia

(www.tdlc.cl).

10

However, for local telephony during 1994-1998, stagnation in coverage coincided with a systematic reduction in the main operator’s (CTC) share, alongside the emergence of VTR –(the main cable TV operator), as a telephony provider. Teledensity7 shows growth during the period, despite stagnation in fixed lines, a trend which was reversed in 20048 (see figure 1). Fixed telephony coverage for 1994 was 11.6 lines per 100 inhabitants, increasing to 20.4 in 1998, and reaching 20.7 in 2004. Stagnation in fixed line took place during a global contraction of the sector following the financial collapse of dot-com companies, and in the wake of strict rate fixing for the majority operator in the local segment and its entry into the Brazilian market. On the other hand, development of applications and services complementary to the local network - especially switched Internet access - was stimulated as a result of access charges fixed at long-term marginal costs. During this period, the regulatory authority fixed asymmetric access charges for the main entrant. Consequently, fixed telephony penetration expanded on average by 15.1% during 1994- 1998, reaching a plateau during 1999- 2004, and rising to 20.7%, i.e. just over 3.3 million fixed lines. Mobile telephony was a virtually insignificant segment of the market during 1994-1998, followed by annual increases in penetration of 49%, reaching a 59.6% penetration in late 2004, when the number of mobile phones rose to over 9.5 million. Since its commercial launch in mid-1997, prepaid has been the most significant form of subscribership, accounting for 82.6% of total of mobile subscribers in 2004, and 93% of -new subscribers for this segment in the previous year.

Figure 1 – Telecom Coverage Indicators

Source: Subsecretaría de Telecomunicaciones.

7 The standard indicator for telecommunications coverage is teledensity, measuring the number of lines per 100 inhabitants, for fixed telephony, and the number of subscribers per 100 inhabitants for mobile telephony. 8 Although there was a decrease in local penetration between 2002 and 2003, this in part could be due to changes in the accounting methodology to achieve greater efficiency in tariff and and restrictive-growth context.

0

10

20

30

40

50

60

70

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Years

Fixedtelepho

(lines/inh)

Mobiltelepho

(subscrib

/100 i h )

MobilTelephon/Fixe

dTelepho

Subs

crib

ers/

lines

/100

inh.

Fixed line (lines / 100 inhab.

Mobile telephony (subscribers / 100 inhab.

Mobile telephone / filxed line

11

Between 1994-1998, the most intensive competition within the telecom market was in the long-distance segment, which until the start of the period was in the hands of Entel Chile. The sector was opened to competition with introduction of the dial-up multicarrier system, which, during the period, enabled 80% price reductions and increases in international outgoing traffic from 63.5 million minutes in 1994 to 215 for 1998, amounting to 35.6 % growth. During the same period, fixed line coverage was sustained by Compañía de Telecomunicaciones de Chile, now Telefónica CTC-Chile, which reached an 87% share in fixed telephone lines in 1998. Towards the end of the first assessment period, based on resolutions of the anti-monopoly bodies, the regulator tried to advance in the regulation of the disaggregated supply of network facilities, managing to establish rates for them and have public supply from the majority operator in 1999. However, this supply was never noticed by the authority, which, at the end of the period, chose to prepare rules and regulations which were not completed,9 still keeping an insignificant share in the services provided by this company.

As far as results are concerned, a considerable availability of service delivery, measured in a 3-year period, is noticeable at the national level between 2001 and 2003. The proportion of households with a fixed and/or mobile telephone expanded from 67.2% to 82.6%. In that same period, there was a significant improvement in the situation of the first two income quintiles, since the ratio between the coverage in the last quintile and first quintile went from 2.6 in 2000 to 1.6 in 2003. Mobile telephony has had high growth rates: 134.5% in 1999, 55% in 2001, and in 2004 the trend in the growth rate slowed, rising by 27.2%. These growth rates far exceeded the mobile market growth expectations existing when PCS and the calling-party-pays systems were introduced during 1998. Despite the increase in 2004, the less significant growth of the last period would be indicative of the greater maturity reached by this segment. The following figure summarises the evolution of the growth rate in number of fixed lines and number of mobile subscribers.

Figure 2: Growth Rates in the Telecommunications Sector

9 As stated in the public reference document issued by Subtel, regarding the terms of reference of the

Regulations of the supply of switching and/or transmission facilities provided as intermediate services or private circuits.

12

Source: Subsecretaría de Telecomunicaciones.

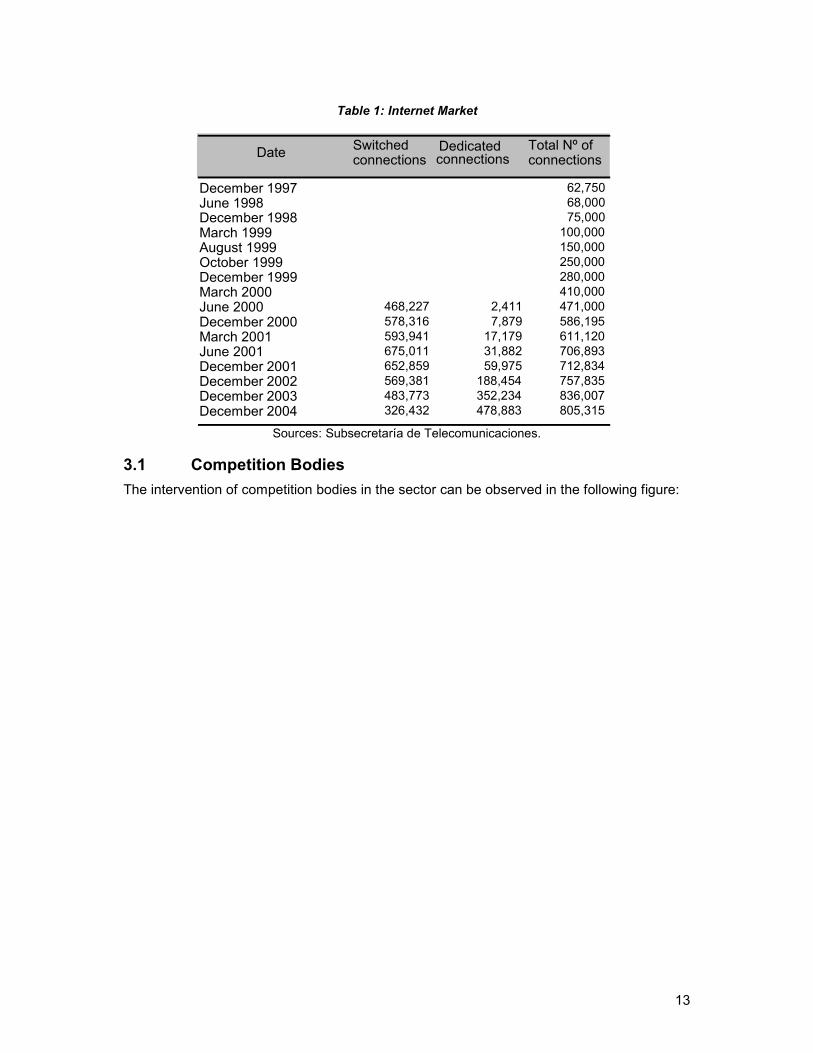

The evolution experienced by the Internet market (see table 1) is also remarkable, particularly in the case of dedicated connections. The overall number of customers is divided into customers with switched connections and customers with dedicated connections, involving ADSL, Cable Modem and WLL technologies. In 2004 dedicated connections by households outnumbered switched connections due to the increasing incorporation of broadband Internet access. In December 2004, according to Subtel, 40.5% of customers corresponded to the switched form of subscribership and 59.5% to dedicated.

0

1,000,000 2,000,000 3,000,000 4,000,000 5,000,000 6,000,000 7,000,000 8,000,000 9,000,000 10,000,000

Years

20.0 0.0 20.0 40. 60.0 80.0 100. 120.0 140.0 160.0

Number of fixed telephone lines Number of mobile subscribers Growth rate fixed numbers Growth rate mobile numbers

Num

ber o

f fix

ed li

nes

and

mob

ile s

ubsc

riber

s

2000

1994

1995

1996

1997

1998

1999

2001

2002

2003

2004

Gro

wth

rate

fixe

d &

mob

ile n

umbe

rs, %

13

Table 1: Internet Market

Sources: Subsecretaría de Telecomunicaciones.

3.1 Competition Bodies The intervention of competition bodies in the sector can be observed in the following figure:

Date Switched connections

Dedicated connections

Total Nº of connections

December 1997 62,750 June 1998 68,000 December 1998 75,000 March 1999 100,000 August 1999 150,000 October 1999 250,000 December 1999 280,000 March 2000 410,000 June 2000 468,227 2,411 471,000 December 2000 578,316 7,879 586,195 March 2001 593,941 17,179 611,120 June 2001 675,011 31,882 706,893 December 2001 652,859 59,975 712,834 December 2002 569,381 188,454 757,835 December 2003 483,773 352,234 836,007

December 2004 326,432 478,883 805,315

14

Figure 8: Regulatory and Competition Processes

This diagram is the result of the interaction of the participating institutions, each within their competences, coupled with a permanent adjustment process in those areas where there is overlap and a need for increased coordination. Thus, as of 1999, the participation of the anti-monopoly body has consolidated - in a traumatic fashion at first - the determination of the final bidding terms for granting radio electric services. Moreover, in the assessment of final services liable to rate fixing, the regulator produces a proposal, which acts as a basis for assessment. Finally, in the case of complaints and enquiries made by companies in the sector, the practice of consulting the sectoral regulator has prevailed.

3.2 Investment in Telecoms The growth of the Telecommunications sector is closely linked with the evolution of the country’s Gross Domestic Product. For most of the period 1994-2004, the growth of the communications GDP was greater than the growth of the aggregate activity level. However, the difference between both rates decreased systematically. This trend is illustrated in figure 3:

Regulador Antimonopolio

Regulador Sectorial Responde consulta

Analiza propuesta de FusiónResuelve, rechaza o aprueba (fija

condiciones para la fusión)

Regulador Antimonopolio

Regulador Sectorial Propone servicios finales

afectos a regulación tarifaria

Resuelve servicios finales y operadoresafectos a fijación de tarifas

Fija tarifas

Regulador Antimonopolio

Regulador Sectorial Dicta norma técnica y fijamodalidad de asignación

Analiza efectos de modalidad seleccionada

Fija bases de concurso Licita y adjudica

Resolution of complaints and regulation of mergers and/or acquisitions

De facto link Legal link

Antimonopoly Regulator

Sectoral Regulator Deals with enquiries

Analyses merger proposalResolves, rejects or approves (sets

merger terms)

Antimonopoly Regulator

Sectoral Regulator Proposes final servicesliable to rate regulation

Establishes final services and operatorsliable to rate fixing

Fixes rates

Antimonopoly Regulator

Sectoral Regulator Issues technical rule and

sets allocation modality

Analyses effects of selected modality

Sets bidding terms Invites bids & grants concessions

Regulation of new technologies

Rate Regulation

15

Figure 3: Country’s GDP Growth Rate and Telecommunications Sector GDP Growth Rate

Source: Subtel, based on Central Bank information: years 1995 and 1996 sector includes Transport; year 2003 provisional figures, year 2004 preliminary figures; year 1995 basis pesos 1986; 1996 onwards, basis pesos 1996.

Investment flow by the collection of companies in the telecommunications sector grew till 1997, driven largely by Telefónica CTC-Chile investments, reaching over US$ 1 billion that year. Between 1997-1999, the trend was slightly reversed as a result of decreased business activity. However, in the year 2000 that decline was interrupted and a recovery occurred, the level of investment being higher than any year in the 1990s. During the year 2000, the sector’s investment reached about USD 1.12 billion, accounting for nearly 8% of the country’s aggregate investment, with 40% allocated to the development of mobile telephony infrastructure.10 These figures are particularly interesting since they occurred within the framework of a significant cutback in investments by Telefónica CTC-Chile. Until the mid 90s, investment in telecommunications tended to concentrate on fixed and long-distance telephony networks, while in the late 90s and early this century, it was split mainly between fixed and mobile networks.

This large volume of investment allocated to mobile networks accounts for the substantial increase from 1997 to 2001. Investment in mobile telephony reached almost 35% of all telecommunications investment in late 2001 (see figure 5). Since 2002 the performance of investments has been affected by the crisis that hit the telecommunications industry globally, as well as by the global slowdown in local and long-distance segments. In particular, the level of investment in the telecommunications industry in 2002 fell by 38% with regard to the previous year, as observed in figure 4. Since that date, the level of investment has remained relatively stable.

10 Source: Subsecretaría de Telecomunicaciones.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Years

CommunicatioGDP

thrat

Country’s G PGrowth

Cou

ntry

’s &

com

mun

icat

ions

GD

P

16

Figure 4: Evolution of Investment - Telecommunications Sector (in million dollars)

Source: Subtel, based on information from the companies.

2003 and 2004 estimates, 2004 Telefónica CTC-Chile report.

734

200

400

600

800

1,000

1,200

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Investment (Million d ll )

17

Figure 5: Composition of Telecommunications Investment. In percentages

Source: Subsecretaría de Telecomunicaciones.

The maturity of the sector, the stakeholder consolidation process, and the international investment environment could account for the trend in investment in the second half of the period 1999-2004. It is worth observing that after a decade, a more mature market has returned to the investment levels of privatised monopolies, but in a technological setting that encompasses mobile and cable networks, alongside traditional copper pairs.

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

Fixed Telephony

Mobile Telephony

LongDistane

Internet

Others

2001

2002

18

4 Fixed Telephony Regulatory Environment

4.1 Market Entry In 1994, following the legal change that established the regulation of interconnection rates, new fixed telephony operators entered areas overlapping CTC areas, CTC having a 94.5% share of the total amount of operational telephone lines. These new operators were linked to long-distance carriers such as EntelPhone and Télex Chile, other networks such as Teleductos, a supplier of copper pairs in the downtown area of the capital. Two competitors, Manquehue and CMET, both with a traditional copper pair infrastructure, had joined in during the 1980s. Entel soon lost its monopolistic power in long distance, reaching just 41% of the international long-distance traffic in 1995, while in December 1998, Telefónica CTC-Chile still held on to 87% of operational telephone lines. No new competitors entered the local telephony market during the period 1999-2004 - after the rates decree was issued in 1999 - but market share by Telefónica CTC fell to 73.2% in 2004. However, competition manifested itself in the business customer niche. The company VTR, by making use of its packaging advantages with cable television, managed to make significant headway, reaching a 10% share in 2004. A special case is that of the third local company, Telefónica del Sur, which had to face the competition of Telefónica CTC-Chile in the Tenth and Eleventh Regions of Chile. With regards to reducing barriers to entry, the 1999 rate fixing established service prices in a disaggregated manner. In principle, any competitor of Telefónica-CTC could gain access to the outside plant necessary to provide its services using the dominant company’s network, without incurring these sunken costs. In March 2000, Telefónica CTC made the Supply of Network Disaggregation Facilities available to interested parties, indicating conditions for competitors interested in renting its network and starting negotiations. In late 2004, Telefónica CTC was offering a little over 583,000 copper pairs for disaggregation, about 14,000 lines for retail and over 4,300 square metres for housing services in the First to Ninth Regions. However, late that year, fewer than 3,000 lines had been opened for disaggregation. Chile was the first country in Latin America with a supply in network disaggregation (AHCIET, 2001), but in practice, this policy did not mean any significant advantages for entry. Thus, the deployment of new networks, especially HFC, became the main form of competitive entry. In late 1999, the authority sought to bring competition into local telephony and Internet service providers by inviting respective bids for the provision of wireless services. Only one of the first two bidding processes – WLL and LMDS – was completed successfully in an eventful process. Some potential interested parties resorted to the Court of Defence of Free Competition (Tribunal de Defensa de la Libre Competencia) to secure its postponement for almost two years. Paradoxically, once the bidding was allowed to go ahead with restrictions imposed by the anti-monopoly body, the Project funding sources had closed down after the collapse of dot com companies. None of the original claimants competed for a licence, and only one company, Entel, managed to secure 100MHz on the 3400MHz band. Furthermore, Subtel decided to postpone the call for public bids for the granting of LMDS service concessions indefinitely.

19

Figure 6: Evolution of the main Local Telephony Companies’ share

Source: author’s own devising based on data from the Finance Ministry, Subtel and reports.

Evolution of fixed telephony competitors

0

50000

100000

150000

200000

250000

300000

350000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Years

Ope

ratio

nal l

ines

VTR CNT, Telsur Entelphone TELCOY OTHERS

Source: author’s own devising based on data from the Finance Ministry, Subtel and reports.

The effect of competition was more noticeable in the case of long distance service providers. Until 1993, there was a legal monopoly in long-distance telephony when the Anti-monopoly Resolution Commission finally authorized the participation of local telephony companies to provide long distance services, and requested that the government implement a multcarrier

Country’s G P

Growth t

30% 40% 50% 60% 70% 80% 90%

100%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Years

Mar

ket S

hare CTC

Others TelSur

20

system within 18 months, which required the amendment of the General Telecommunications Law. This system became operational in October 1994. Nine companies, including CTC-Mundo, a subsidiary of Telefónica-CTC, entered this market immediately. The decentralisation of the service was quick. In 1995, Entel, a quasi monopolistic company in early 1994, as noted above, managed only 41% of international calls. In national long distance, concentration was somewhat greater, due to the fact that only three companies (Telefónica-CTC Mundo, Entel and Télex Chile) have fibre optic networks covering the entire country, and the other carriers use their networks to provide these services. In December 2004, 41 companies were operating under a concession to provide national and international long-distance telephone services. Only three of the latter carriers (Telefónica, Entel, and Chilesat, now Telmex) have their own nationwide networks.

4.2 Scarce Resources In general terms, the mechanisms in force establish rights of use to be awarded without any restrictions, except when there is a technical rule which allows for only a limited number of providers. In these cases, public bids must be invited. In the event of equal claims among different interested parties, the law favours the right of the party that applied for the use of the bands before the rule governing it had been issued, and inviting new bids if the draw persists.

A significant case in point is the allocation of spectrum for wireless telephony (WLL). On October 29th, 1999, the Subsecretaría de Telecomunicaciones published in the Official Gazette, exempted resolution N° 1498 – which set the technical standard for wireless public telephone service on the 3.400-3.700 MHz frequency band. The bidding process began in December 1999 (which was later postponed for two years). In the same geographical area, service could be provided by as many as three concessionaires. The service area of each concession was to cover all the national territory.

In December 1999, the terms for the bidding process designed to grant three national 100MHz concessions on the 3.4MHz-3.7MHz band were made available to 30 companies. In May 2000, in the face of company claims, the Anti-monopoly Resolution Commission took a precautionary measure and put the bidding on hold. The claimants asked for smaller concessions at the regional level and for monetary guarantees to be reduced. Finally, after being advised by the anti-monopoly body, Subtel set new conditions, halving band width (50MHz) per concession, increasing licences per geographical area to four, and splitting half the band into regional-level concessions.11 Paradoxically, two years after the first call for bids, the final result coincided with the authority’s original proposal. None of the competing companies bid for the regional-level bands, except Entel, which did so all over the country, actually securing a nationwide concession, with the qualification that in most of the country, half the band width up for bids was not awarded.

4.3 Interconnection During the period 1994-1998, the access price policy was conservative with regard to the possible impact of keener competition on the dominant operator in local telephony. Access charges were set at an average long-term cost (USD 2cents/min) - to the benefit of fixed charges in their long-term marginal cost - thus stimulating an increase in the number of Telefónica CTC users and the income of this company, as a result of increased traffic brought about by competition in the long-distance segment. It is important to note the subsidy imposed in 1994 on international long-distance communications, which applied access

11 The Chilean territory is divided into 13 administrative regions.

21

charges 14 times higher than those for national communications. This subsidy was maintained throughout the period, even after competition caused a sharp fall in shared rates applied to international communications. Amendments to the General Telecommunications Law, enacted in 1994, established the regulation of all charges and rates provided by utility companies through interconnections, depending on the costs of such services. However, loopholes in the law allowed the dominant operator’s access charges fixed in 1994 to be applied only to long-distance communications. This left the access charges applied by fixed telephony companies to free negotiation between the parties. During the period 1994-1998, companies had to apply access charges symmetrical to those fixed for the dominant operator, and/or refrain from signing the respective interconnection agreements. The mandate of the law, which provides for the regulation of access rates between telephone companies, was not applied during the first half of the period studied. The provisions of this law introduced detailed procedures and rules regarding internetworking. These provisions substantially improved the negotiating position of entrant companies and reduced disputes and lawsuits related to interconnection. The right of every company to interconnect was established, as well as the obligation to accept these interconnections. Furthermore, authorities were given the power to set Network Termination Points on telephone networks, where companies can converge to interconnect. It was also established that the services provided through interconnections and the services, including administrative facilities, that telephone companies provide to others and to carriers are subject to rate regulation. Likewise, all the services that fixed telephony companies provided to long-distance carriers were also subject to regulation. In September 1995, SUBTEL established a detailed procedure and deadlines of three months for the acceptance of interconnections between telephone companies.12

4.4 Rate Regulation According to the regulatory framework, prices and other characteristics of services are established freely13 by companies, with the exception of those that are an input for other providers and in situations in which competitive conditions in telephony are not in place. Within the previous framework, local telephony provided by Telefónica is liable to retail rate fixing, with the exception of companies in the south of the country, where TelSur’s and its subsidiary Telcoy’s retail rates are fixed, while mobile and long-distance telephony fall into the free-rate regime due to the high degree of competition. Likewise, the prices of services provided through interconnections must be fixed for all companies. In general terms, the main characteristic of rate regulation for services liable to price fixing is that they be calculated on the basis of the long-term marginal costs of an efficient company, adjusted to minimum distortion so as to finance the average long-term costs of that efficient company.14 The structure, level and indexing mechanism of the rates for liable services are fixed every five years.

The following table shows the evolution of residential rates during the period 1994 -2004.

12 At present, these rules make it difficult for existing owners of networks to deny, delay, or overcharge

for interconnections. Díaz and Soto (2000). 13 When competitive conditions do not guarantee a regime of rate freedom, as the Resolution

Commission may establish, the prices or rates of the service assessed will be fixed in accordance with the conditions and procedures indicated in the Telecommunications Law.

14 That is to say, that which considers investment and exploitation costs, including capital costs, of each service in that efficient company. Costs to be considered are limited to those indispensable for the efficient company to be able to provide telecommunications services subject to rate regulation, according to available technology and maintaining the quality established for such services.

22

Table 2: Evolution of Residential Rates. Telecommunications (USD Dec. 2004*, VAT included)15

Source: Public Regulation Indicators, Public Utility Services 2004. Finance Ministry *Average dollar rate in December 2004: 576.17. Central Bank

Figure 7: Evolution of Residential Rates

15 Author’s own devising on the basis of the calculation made at Public Regulation Indicators, Public

Utility Services 2004. Finance Ministry. The service that was considered for this purpose corresponds to local calls. An average bill with 478 minutes’ local calls a month plus fixed charge was considered: 30% of the calls correspond to reduced time till the year 2003, then 6% is transferred to night time, the result being 24% reduced time and 70% normal time.

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

1992

1994

1996

1998

2000

2002

2004

2006

Years

USD

Dec

. 200

4

Santiago Antofagasta Concepción

Date Santiago Antofagasta Concepción1994 25.67 31.13 27.68 1995 25.33 30.71 27.31 1996 25.21 30.57 27.18 1997 24.54 29.76 26.47 1998 24.64 29.88 26.57 1999 24.80 29.40 29.07 2000 25.85 30.60 30.27 2001 26.04 30.81 30.47 2002 27.00 32.01 31.66 2003 26.62 31.66 31.32 2004 24.98 30.55 32.99

23

Despite structural changes in the different retail rates, the real value of phone bills have remained stable throughout the period,16 which shows that differences occur only with regard to the policies followed in the matter of access charges. As regards to rate fixing, in 1998, through Resolution 515 of April 1998, the Resolution Commission established that only the dominant operator in a certain geographical area had to be subjected to rate fixing of its services to the public. It also imposed rate fixing in a disaggregated manner for switching and transmission facilities provided by that operator to its competitors. In addition, in January 2001, Telefónica CTC Chile presented a request to the Resolution Commission for the liberalisation of local telephony retail rates. In July of 2001, the Resolution Commission, through Resolution 611, rejected the request, stating that existing market conditions did not yet justify such freedom all over the country. Furthermore, it decided that Telefónica CTC Chile could present alternative rate schemes and ask the authority for administrative acts complementary to Rates Decree N° 187 of 1999 that would allow rate differentiations based on costs, within each rate area, for volume-based customer categories. In March 2002, Telefónica CTC Chile sued the State for damages, in an attempt to receive compensation for rates reportedly fixed below their costs of operation. Of special interest is the declaration that the efficient company, which, according to the law, starts “from scratch”,17 should regard the network structure of the real company as efficient, as regards the optimal setting of exchanges and other matters in contention. In that regard, the authority decided to impose higher efficiency levels for rate purposes, through the theoretical redesign of network structure. In August 2002, the Ministries of Transport and Telecommunications, and Finance, Development and Reconstruction issued Decree N° 455, which sanctioned the flexibility of rates through schemes of High Consumption (geared to residential customers) and Very High Consumption (geared to companies, based on monthly flat income). Moreover, Subtel authorised Telefónica CTC Chile to market the pre-paid telephone service to lower-income segments.

Between 1994 and 2002 the authority refrained from fixing the access charges of fixed telephony companies which overlapped with Telefónica.18 In January 2002 it fixed the access charges of VTR, the main competitor in fixed telephony, and between 2003 and 2005, coinciding with Telefónica’s rate process, it fixed the access rates for the rest of the non-dominant companies for the first time. As a result of that process, and noted by the authority itself,19, access charges reached figures even higher than, but closer to, those fixed for the dominant operator.

16 Rate differences in relation to the primary zones of Concepción would seem to be due to changes in

the criteria for the design of the efficient company for that area. 17 Title V, General Telecommunications Act. 18 The exception corresponds to those four primary zones where Telefónica acted as an entrant and

rates were fixed for TelSur and TelCoy. Furthermore, during that period, Subtel fixed rates for rural companies, concessionaires of the Fondo de Desarrollo de las Telecomunicaciones (FDT), whose coverage mainly spanned areas underserved by Telefónica, and even extended these rates to concessions that Telefónica itself had obtained through FDT.

19 During that period, the Finance Ministry told the press that symmetry in access charges was necessary.

24

4.5 Regulation of Anti-Competition Practices After triggering the amendment to the 2004 Law through resolution Nº 389 of 1993, and following the opening of the long-distance market, between 1994 and 1998 the competition defence bodies remained relatively distant from the market until early 1998, when they proceeded, at the request of the regulator, to assess services liable to rate fixing. Direct intervention was to appear in a concentrated manner at the end of the second period, associated with the review of the performance of the sectoral regulator in the processes of radioelectric spectrum allocation, and specific cases such as the setting of conditions for Telefónica CTC-Chile’s entry as a competitor into the south of the country, where the monopoly had been exercised by TelSur and its subsidiary Telcoy.

4.6 Evaluation of the Regulatory Environment In general terms, an improvement between periods is noticeable, which has produced interesting results as far as the increased number of entrants is concerned, especially the local cable TV operators. The early resolution of interconnection problems, the increased activity of anti-monopoly bodies, the effective bidding for wireless network bands, plus the reduction in cross-subsidies in the regulated rate structure stand out among the specific aspects of this improvement. Factors that worked against further improvement include a lack of coordination between the sectoral and anti-monopoly regulator in the bids for bands, as well as the strong regulatory asymmetries introduced when establishing the dominant operator’s and its main competitor’s access charges. This latter aspect hindered interconnection agreements and payment of the access charges fixed. The opposite occurred in mobile telephony.

Evaluation of the Telecommunications Regulatory Environment

Fixed Telephony Component 1994-1998 1999-2004

Entry into the market Unsatisfactory Satisfactory

Allocation of scarce resources Unsatisfactory Neutral

Interconnection Unsatisfactory Satisfactory Rate regulation Unsatisfactory Neutral

Regulation of anti competition practices Neutral Neutral

5 Mobile Telephony Regulatory Environment

5.1 Market Entry Until 1996, mobile telephony was divided into two areas: the Santiago and Valparaíso area, which concentrated about 70% of subscribers, and the rest of the country. Two concessionaires operated in each of these areas. Bellsouth and CTC operated in the Santiago and Valparaíso area, while Entel and VTR operated in the rest of the country.20 In early 1996, VTR and CTC merged their mobile telephony operations, creating the company Startel, with nationwide coverage. In December 1997, VTR sold its 45% share in the condominial mobile telephony company CTC, which was then renamed Telefónica- Móvil.

20 Strictly speaking, the concession was granted to Telecom, owned by Motorola (67%) and ENTEL

(33%). In 1996, Entel increased its share to 59%, and Telecom was renamed ENTEL Telefonía Personal. In 1997, Entel increased its share to 75%.(Fisher-Serra 2001)

25

In March 1997, following a public bidding process, Subtel granted two PCS mobile telephony (1.900 MHz band) concessions to Entel21 and a third one to ChilesatPCS, a subsidiary of Télex-Chile. BellSouth, which had only one concession in the Metropolitan Area and the Fifth Region, was the only company without nationwide coverage. In March 1999, Entel sold its third concession to Bellsouth. The anti-monopoly authority studied a complaint filed against Bellsouth for anti-competition practices regarding the provision of roaming in its service area. Entel PCS started service in March 1998, while ChilesatPCS began operating in August of that year. In April 1999, Télex – Chile sold its mobile telephony subsidiary, which was then renamed SmartcomPCS. In February 1999, the “Calling-party-pays” system came into force. This system forced fixed telephony users calling a mobile telephone to pay the mobile network an access charge established by the authorities, while mobile telephony users only pay for outgoing calls. In mid 1998, there were 650 thousand mobile telephony subscribers, 61% of which were Telefónica Móvil customers, 20% Entel customers, 16.5% BellSouth customers, and the rest were Télex Chile customers. By December 2001, market shares had changed substantially; Telefónica-Móvil’s share had reached 31.5%, while Entel PCS outperformed it with 38.9% of the market share. BellSouth and SmartcomPCS lagged behind with 17.4% and 12.2%, respectively.22 A development that became the focus of the sector’s attention was the granting of a licence for Nextel Chile to provide digital radio trunking services.23 Incumbent mobile operators (Entel, Bellsouth, Smartcom and Telefónica Móvil) resorted to SUBTEL, the Anti-monopoly Commission, the Office of the Comptroller General of the Republic24 and the law courts against the authorisation granted by the authority to this company for interconnection with the public telephone network. The companies argued that the rules were being changed by authorising Nextel to become another mobile operator, without having competed for a licence to provide the service. In October 2003, the Court of Appeal ruled in favour of Nextel, within the framework of the appeal lodged by mobile companies, overruling the initial sentence passed by the Transport and Telecommunications minister.

Table 3: Mobile Companies’ share (as a % of total subscribers)

21 Subtel did not consider Comisión Preventiva’s recommendation that rules should be set to prevent

one company from having more than one concession in the same geographical area, so Entel obtained two national concessions and kept its original concession in an area inhabited by about 30% of mobile telephony users.

22 The boom in the number of mobile telephony subscribers resulted in CTC and VTR having capacity problems with their networks. Subtel had 30 MHz which had been set aside for a potential additional entrant, but decided to give them to these two companies on two 15 MHz bands.

Smartcom appealed, since this concession was granted without any previous bidding, and as it was the company with the fewest subscribers, it had ample room to accommodate customers, since the other companies had capacity problems. After several years in court, bids were invited but in the end the only bidders were the two original participants, which were granted the 30 MHz, with 20 MHz for Telefónica Móvil and the rest for BellSouth. Initially, the bidding process was by beauty contest, but due to a draw in the score, the companies ended up competing for the frequencies on the basis of payment to the State.

23 Wireless communications services within companies. 24The office of the Comptroller General of the Republic is an independent body of the executive,

charged with controlling the legality of the Administration’s actions.

26

Source: Public Regulation Indicators, Public Utility Services 2004. Indicadores de Regulación Pública, Servicios de Utilidad Pública 2004. Finance Ministry.25

25 The merger of Telefónica Móvil and Bellsouth came into effect in the first half of 2005.

Nº of

subscribers

Nº of

subscribers

Nº of

subscribers

Nº of

subscribers

Nº of

subscribers

Nº of

subscribers

Nº of

subscribers

Entel PCS 185,274 18.61 656,000 28.8 1,274,000 36.8 1,938,846 38.9 2,300,000 37.5 2,684,214 36.6 3,556,495 36.7

Telefónica Móvil 554,225 55.67 1,153,794 50.7 1,224,520 35.4 1,570,087 31.5 1,849,283 30.2 2,269,757 31 3,300,000 34.1

Bellsouth 200,000 20.09 390,000 17.1 691,000 20 866,269 17.4 1,032,000 16.8 1,200,000 16.4 1,400,000 14.4

Smartcom PCS 56,061 5.63 78,000 3.4 270,000 7.8 610,000 12.2 946,000 15.5 1,170,000 16 1,434,227 14.8

TOTAL 995,560 100 2,277,794 100 3,459,520 100 4,985,202 100 6,127,283 100 7,323,971 100 9,690,722 100

2002 2003 2004 1998 1999 2000 2001

27

Figure 9: Evolution of the main Mobile Telephony Companies’ share26

0.00

10.00

20.00

30.00

40.00

50.00

60.00

1998 1999 2000 2001 2002 2003 2004 2005

Years

%

Entel PCS

TelefónicaMóvil

Bellsouth

Source: Finance Ministry.

5.2 Scarce Resources In mobile telephony, restrictions in the management of scarce resources are reflected in the Subtel-driven process of inviting bids for mobile telephony concessions on the 1900MHz band. While the process was initiated through the call for bids in November 1995, resistance in court from the existing operators, Telefónica Móvil and Bellsouth, delayed the process for years. Eventually, in January 1998, three concessions - two of them granted to Entel subsidiaries and the third to the Télex-Chile group – were allowed to become operational. During this period, the incumbent companies digitalised their networks and introduced aggressive prepaid schemes. Early in the period 1999-2004, the authority deployed great activity regarding mobile telephony. It began a process intended to make an additional 30MHz of radioelectric spectrum on 1900MHz available to the mobile market. In early 2000, intense competition existed in mobile telephony, with four competitors and penetration much higher than preliminary estimates. The asymmetry in costs between companies, caused by the allocation of twice the spectrum (60MHz) to a group of companies,27 was particularly aggressive for pre-existing companies, which had to use 25MHz to serve a mixture of analogue and digital customers on 800MHz. Subtel established a procedure aimed at directly distributing 30MHz of radioelectric spectrum on the 1900MHz band among the companies, in accordance with technical and economic efficiency criteria. These rules were halted by the anti-monopoly authority, which ordered the awarding of these bands by tender, establishing a

26 Telefónica Móvil and Bellsouth merged in 2005, giving rise to the dominant operator Movistar. 27 Entel obtained two concessions, each through two different subsidiaries, with 30MHz for each, but

in practice it started operating under the name of only one of them, EntelPCS.

0 00

50.00

10 00

20 00

40 00

30 00

60 00

28

60MHz limit per concessionaire, thereby preventing Entel’s participation. The result of the bid was the granting of the 30Mhz to the 800MHz band operators. The paradox repeated itself, since the result was analogous to that sought by the regulator, but several years later.28

5.3 Interconnection Mass consumption in the mobile industry in Chile was prompted by the passing of the rates decrees issued by the authority in 1999, which fixed mobile network interconnection rates and implemented the ‘calling-party-pays’ system.2930 Following this decree, the rates that mobile companies could apply for communications coming from other networks were fixed. In this regard, it is important to stress that only access charges are regulated in mobile telephony, that is to say, the interconnection cost paid by third parties for using a mobile company’s network. This value, close to USD 13cents/min in the first fixing, favoured the growth of mobile phone services, especially among lower-income segments of the population through the use of prepaid cards. In February 2003, the Technical Economic Terms, meaning the new rates decrees for mobile companies for the period 2004-2009, were set. These came into force in February 2004. This new decree involved a 26.7% reduction in access charges for the 5 years the regulated rates would be in force.

5.4 Rate Regulation Mobile telephony is purposely excluded from the rate fixing regime.31 This does not mean that fixing will not be applicable through the mere rule of law. While there is regulation in access charges, the rates that the different companies apply to their customers for the service is a free process. This rate freedom applied to retail prices has led to the development of a complex supply of schemes.32

5.5 Regulation of Anti Competition Practices As noted above, since 1999, the anti-monopoly body’s participation in the determination of the final bidding terms for the granting of radioelectric spectrum has consolidated. In mobile telephony, intervention as a result of complaints and enquiries made by companies in the sector became frequent at the end of the first half of the assessment period. The most outstanding case was the complaint filed by mobile telephony companies against Telefónica Móvil, called Startel at the time. The accusation was that Startel had implemented the Calling-Party-Pays-Plus (CPPP) system, whereby the mobile user did not have to pay for incoming mobile phone calls, with no rise in the income from mobile access charges. The anti-monopoly body ordered a halt to the scheme, and ruled it a challenge to competition, since Startel did not cover the costs incurred by the scheme. Also, the Commission ordered consultations before the company decided to make any changes to its rate schemes, in the

28 As a result of the sealed tender in the wake of the draw in coverage and opportunity between both

bidders, the second mechanism meant additional returns for the Executive, without any sectoral impact, since the income occurs in the Nation’s general budget.

29 This decree allowed operators to subsidise mobile equipment and extend the service. 30 According to this rate structure, local telephony companies pay an access charge to mobile

telephony companies for calls made from fixed to mobile networks. Local telephony companies responded to this charge to their subscribers with the same structure.

31 Article 29, General Telecommunications Law –18168- 32 See Technical Economic Terms (Bases Técnico Económicas) of the Study for the Rate Fixing of

services liable to rate fixing provided by Utility Concessionaire Telefónica Móvil. Period 2004-2009 (February 2003)

29

same way it marketed its services, and retail rates. This situation was maintained until the regulator implemented the Calling-Party-Pays system.

5.6 Evaluation of the Regulatory Environment In general terms, a significant improvement in the regulatory environment between periods is noticeable. Of special importance is the introduction of the ‘Calling-Party-Pays’ system, which allowed the successful incorporation of PCS operators by enabling them to charge for the costs associated with access service, thus putting an end to uncertainty in the collection of access charges from fixed operators, especially the dominant operator. In addition, intervention from the anti-monopoly body set a major legal precedent regarding anti-competitive supply in this market. The main failures stem from the eventful process of allocation of new frequencies on the 1900MHz band, in which the lack of coordination between the anti-monopoly authority and the regulator have led to delays and a general loss of reputation for the latter.

Evaluation of the Telecommunications Regulatory Environment

Mobile Telephony Components 1994-1998 1999-2004

Entry into the market Unsatisfactory Satisfactory

Allocation of scarce resources Unsatisfactory Neutral

Interconnection Unsatisfactory Satisfactory

Rate regulation Neutral Excellent

Regulation of anti competition practice Unsatisfactory Neutral

30

6 Conclusions The assessment provides the inputs necessary to tackle the panel phase proposed in Samarajiva and associates’ methodology (2005) for the Sri Lanka case study. The periods relevant to the evaluation were identified, plus a chronology that will allow stakeholders to adopt a position in the context of each evaluation period, and a first evaluation has been drafted that motivates discussion and generates a common context for the interpretation of the factors contained in the methodology. Although the availability of this first vision seems positive for the motivation and information of the stakeholders, caution must be used in the event of its dissemination among those consulted so as not to cause a preliminary bias in their answers. For this purpose, it may be wise to subject the paper to some kind of discussion and obtain opinions that support or challenge the author’s perceptions. Joint dissemination of the paper and opinions about it may correct this bias. For the correct determination of the TRE, it is extremely important to discuss both the universe of stakeholders to be represented and to ponder each group identified. However, the difficulty in resolving both issues makes it advisable to proceed with the option taken in the Sri Lanka case study, gathering information from a broad panel. In the Chilean case, a point must be made of incorporating both controlling and institutional investors, especially pension funds. In addition, academia, specialised media and regulators must be regarded as environment-forming agents. A review of the factors making up the proposed components of the TRE reveals elements which hinder differentiation between the two periods, as is the case of timely information on facilities or access to interconnections (see annex for details). Furthermore, the quality of service provision can hardly allow a differentiation between periods – least of all between countries – since it is mostly precarious. For instance, interconnections involve digital frames under conditions of non-discrimination between interconnected companies. In the case of timely information, its adequate availability would make it necessary for dominant companies to acquire information systems, which, in some cases, would mean dropping complex legacy systems. In addition, among the factors making up a certain component, dissimilar impacts on the TRE are noticeable, for which there are no ponderations proposed. A case in point is the retail rate component, in which the focus of regulation – desirable but not having a great impact – contrasts with the existence of cross-subsidies – which have a major impact on regulatory perception. It is suggested that the solution proposed in the methodology should be used, which involves starting the panel discussion by dealing with a proposal of weights. A special mention to the evaluation in the regulation-of-anti-competition-practices component is due, since the anti-monopoly rule was not modified between the two periods. However, a shift in stress is apparent in the conduct of the institutions. These shifts in stress can only be noticed in the light of enquiry or complaint processes, so, in this regard, the TRE will judge the intensity of activity of the competition defence bodies in the country, regardless of the strengths or weaknesses of the regulatory framework. As far as the chosen evaluation periods are concerned, the identification of relevant regulatory landmarks that have changed the conditions of competition in the sector will allow the stakeholders to easily adopt a position in each of them. These landmarks coincide with changes in the magnitude and composition of investment flows. In particular, in 1994 the General Telecommunications Law was amended, with the opening of the market, especially the long-distance market, and the dominant operator’s rates were fixed for the period between May 1994 and May 1999. In addition, between 1998 and 1999, PCS mobile telephony concessions came into force, the Calling-Party-Pays system was incorporated into the segment and the dominant operator’s rates were fixed for the period between May 1999

31

and May 2004. Nevertheless, for an adequate understanding one must bear in mind that investors go by expectations, and perception, and therefore investment may anticipate regulatory actions, as is the case of investment in digitalization of mobile networks before the entry of PCS companies. The comparison of the TRE between countries does not seem easy, since the methodology places evaluators in the position of having to compare the performance of each factor in a period with regard to the other, generating relative evaluations. Comparison between countries requires an absolute reference evaluation, external to the country, to facilitate the conduct of the task. In order to achieve this, it is proposed that a methodology of standardisation should be incorporated to at least correct the bias that might be introduced from the other determinants of the business environment, such as macro and business risk. Cultural bias, whether more or less optimistic, is unimportant due to the similarity among the countries. As regards to the results obtained for a first overview, these account reasonably for the trend in sectoral investment in both periods: In fixed telephony, for the period 1994-1998, as is evident from the TRE evaluation, expansion occurred amid uncertainty over the implementation of a new legal framework, with technical and rate aspects of interconnection that inhibited the entrants. In particular, despite the legal change, in practice interconnection between local companies was subjected only to asymmetric negotiations between the parties, favouring the investments of the dominant operator, whose investment flow may also have acted as a deterrent, reducing competitors to acting in market niches. As a result, the dominant operator concentrated most of the investment, and thus strengthened its position. In contrast, the old long-distance monopoly was diluted with competition and with the subsidies established in long-distance – especially international – communications to local telephony users. In mobile telephony, the first period, from 1994 to late 1998, can be regarded as one of incipient competition, since in this period, regulations to new competitors and to generating conditions for interconnection at a wholesale price were prepared. Investments were stimulated beforehand, precisely for the defence of competitors existing to date, which digitalised their networks and introduced new forms of marketing, in particular prepaid schemes, in order to take more advantageous positions at the moment of entry of PCS concessions.

The period 1999-2004 in fixed telephony is particularly complex, since although the TRE incorporated improvements in all areas, these improvements occurred in a climate of international slowdown in the sector. Minor operators were finally confined to the corporate sector and some high-income residential areas. However, this, and the increased efficiency imposed by the regulator on the dominant operator in the strongly opposed 1999 rate fixing, made room for the cable operator, which took advantage of its economies of scale and managed to capitalise on the new regulatory environment, growing successfully throughout the period 1999-2004. Cable TV operators demonstrated clear leadership regarding the introduction of new technologies. However, at the end of the period, this competition was marked by greater maturity of the market, with slower expansion. During this period there was a significant change in the composition of investments, with technologies different from the copper pairs of traditional networks, such as mobile and cable networks, becoming more noticeable. Within the previous framework, the dominant operator’s market share had suffered a sharp fall, as the challenger came into its own, prompting the merger of the two main cable companies. In mobile telephony, the TRE reasonably reflects the reality of investment, since there is a major qualitative upsurge in the regulation of the segment. The entrants had the regulations and the regulatory, sectoral and anti-monopoly activity necessary to develop and grow, to the extent that at the start of the period, investments in this segment drew level with and soon topped those in the local segment. At the end of the period, this TRE, together with the

32

increasing maturity of the market, encouraged the consolidation and merger of stakeholders in the segment.

6.1 Lessons Learned Some of the specific lessons include:

The TRE is not neutral to the description of its five components, and no elements of differing value which might lead to those factors being pondered in the same way can be mixed into any of them.