regulation in the south african port system

TRANSCRIPT

The Ports Regulator

Regulation in the South African

Port System Coal Transportation Africa Summit

Mahesh Fakir

CEO

19 May 2015

National Ports Act Background

• Sea transport is an essential vehicle of international trade. • With approximately 80% of SA’s trade being by sea, efficient ports are catalysts for

trade growth • The Act was established with the purpose of ensuring affordable, internationally

competitive, efficient and safe port services based on a transparent and cost-effective nature that is economically and environmentally sustainable.

• The Act contains mandates and functions of Ports Regulator and National Ports Authority

• Sets out powers of Ministers of Transport and Public Enterprises • Sets overall governance framework for ports system • Enacted on the 26th November 2006 • Structure

– Act – Parliament – Regulations – Minister of Transport – Directives – Ports Regulator – Rules - NPA

www.portsregulator.org 2

Objectives of the National Ports Act

• Development of an effective and productive ports industry for economic growth and development

• Promote and improve efficiency and performance in the management and operations of ports

• Promote the development of an integrated regional production and distribution system in support of government policies

www.portsregulator.org 3

The role of the Ports Regulator (In terms of the Ports Act)

• Exercise economic regulation of the port system in line with government’s strategic objectives

• Promote equity of access to ports, facilities and services provided in ports

• Monitor the activities of the National Ports Authority to ensure compliance with the Act

• Adjudicate complaints and appeals against the Authority

• Approve or reject the Authority tariffs

• Promote regulated competition

• Regulate the provision of adequate, affordable and efficient port services and facilities

www.portsregulator.org 4

Who is the Ports Regulator?

• It consists of 9 Members (currently 6) that constitute the economic regulatory authority for the ports system in South Africa

• They are independent in the performance of their mandate from Government Departments

• They are one of the key institutions envisaged by the Ports Policy

• The Secretariat assists the Regulator in carrying out its mandate

www.portsregulator.org 5

What is the Regulator’s role in NPA tariffs?

• To ensure that NPA tariffs are utilised in ensuring that the port system is efficient

• To ensure that the tariffs are affordable to port users

• To ensure that the tariffs are predictable and non-discriminatory

• To prevent the utilisation of tariffs for cross-subsidisation unless in the public interest

www.portsregulator.org 6

Economic Impact of the Regulator • Since inception of the Regulator in 2009 to date:

– There has been a smoothing of the NPAs tariffs – Tariff decision has translated into a saving to users of more than

R5.2 b over the period

• Rationalised Tariffs – R1 bn rebate – Significantly lower approved tariffs – Continued sustainability of NPA

• Proactive and risk mitigating – Excessive Tariff Increase Margin Credit – R2.5 bn available to offset future increases

• Looking forward – Fair tariff incidence – More accurate investment signals through a multi-year tariff

methodology

www.portsregulator.org 7

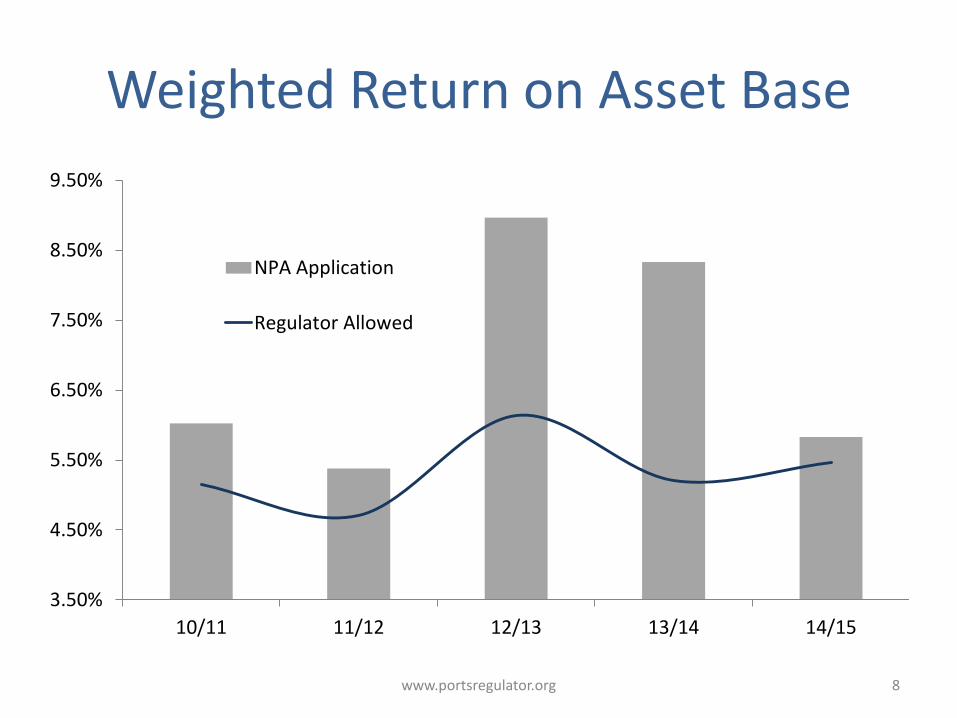

Weighted Return on Asset Base

www.portsregulator.org 8

3.50%

4.50%

5.50%

6.50%

7.50%

8.50%

9.50%

10/11 11/12 12/13 13/14 14/15

NPA Application

Regulator Allowed

Revenue Determinations and Stabilisation of Tariffs

www.portsregulator.org 9

4

5

6

7

8

9

10

11

12

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

An

nu

al r

eve

nu

e R

(b

illio

n)

NPA Revenue Applied for NPA Revenue Allowed

Purpose of NPA tariffs

• To enable the NPA to-

– Recover its investment in owning, controlling and administering ports and its investment in port services and facilities

– Recover its costs in maintaining, operating, controlling and administering ports and its costs in providing port services and facilities

– Make a profit commensurate with the risk involved in ports services and facilities

www.portsregulator.org 10

The Regulatory Manual

• Outlines the mandate of the Ports Regulator of South Africa (the Regulator), the regulatory framework governing the National Ports Authority’s (the Authority/NPA) tariff setting process and matters relating to compliance of the NPA with the Regulatory Framework.

• 2nd version of the manual – 2014/15 Interim Tariff manual (one year)

– 2015/16-2017/18 Tariff manual (multi-year)

11 www.portsregulator.org

Multi-Year Methodology • Previously an interim 1 year methodology • Now fixed for 3 years with annual review and an annual

adjustment of tariffs • No fixing of tariffs for the 3 year period to protect users

from possible large step changes in the tariff. • Large variations in the users and usage of port

infrastructure and services over time • Annual review allows adjustments in prices to be more

efficiently and appropriately allocated to users • Lower regulatory uncertainty

– Will narrow the difference between what is requested by the NPA and subsequently granted by the Regulator.

– Assists stakeholders in formulating responses to the NPA tariff application in a manner that will assist the Regulator in its decision making.

12 www.portsregulator.org

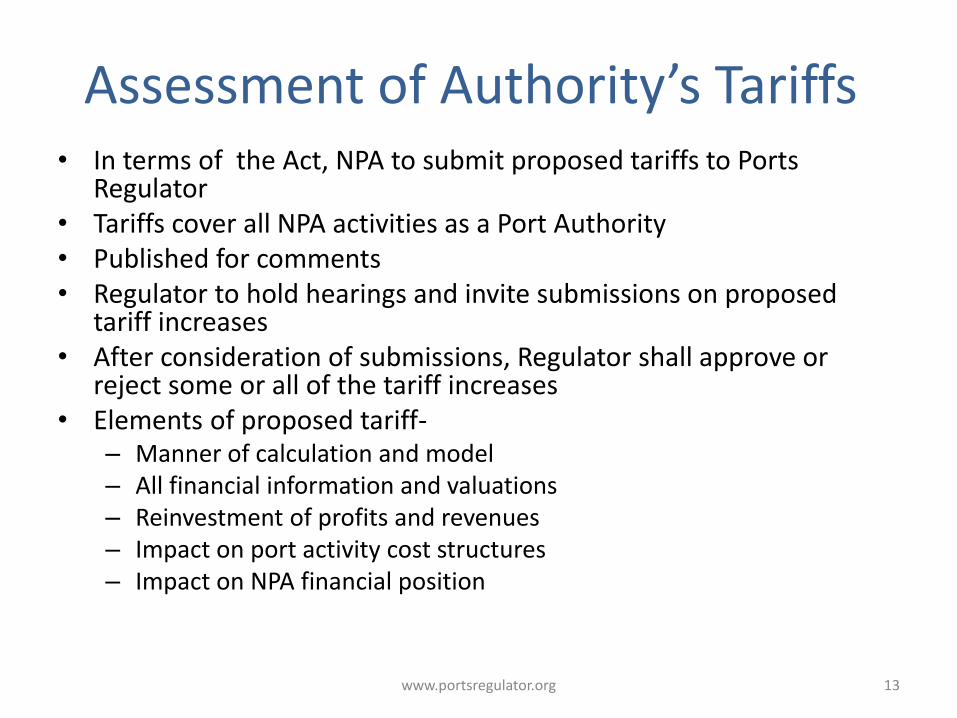

Assessment of Authority’s Tariffs • In terms of the Act, NPA to submit proposed tariffs to Ports

Regulator • Tariffs cover all NPA activities as a Port Authority • Published for comments • Regulator to hold hearings and invite submissions on proposed

tariff increases • After consideration of submissions, Regulator shall approve or

reject some or all of the tariff increases • Elements of proposed tariff-

– Manner of calculation and model – All financial information and valuations – Reinvestment of profits and revenues – Impact on port activity cost structures – Impact on NPA financial position

www.portsregulator.org 13

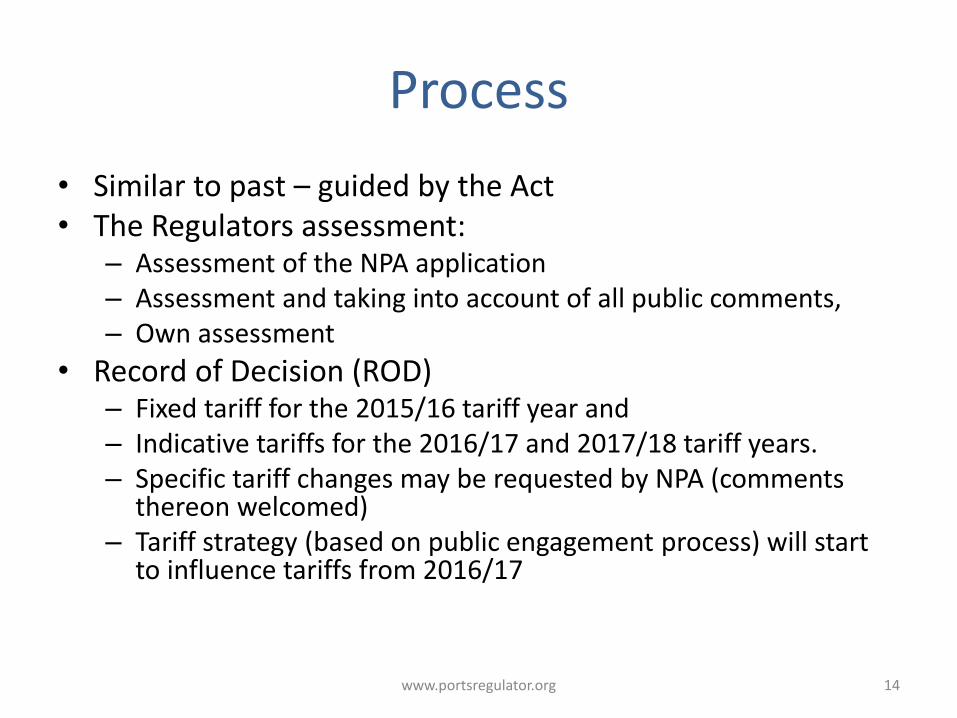

Process

• Similar to past – guided by the Act • The Regulators assessment:

– Assessment of the NPA application – Assessment and taking into account of all public comments, – Own assessment

• Record of Decision (ROD) – Fixed tariff for the 2015/16 tariff year and – Indicative tariffs for the 2016/17 and 2017/18 tariff years. – Specific tariff changes may be requested by NPA (comments

thereon welcomed) – Tariff strategy (based on public engagement process) will start

to influence tariffs from 2016/17

14 www.portsregulator.org

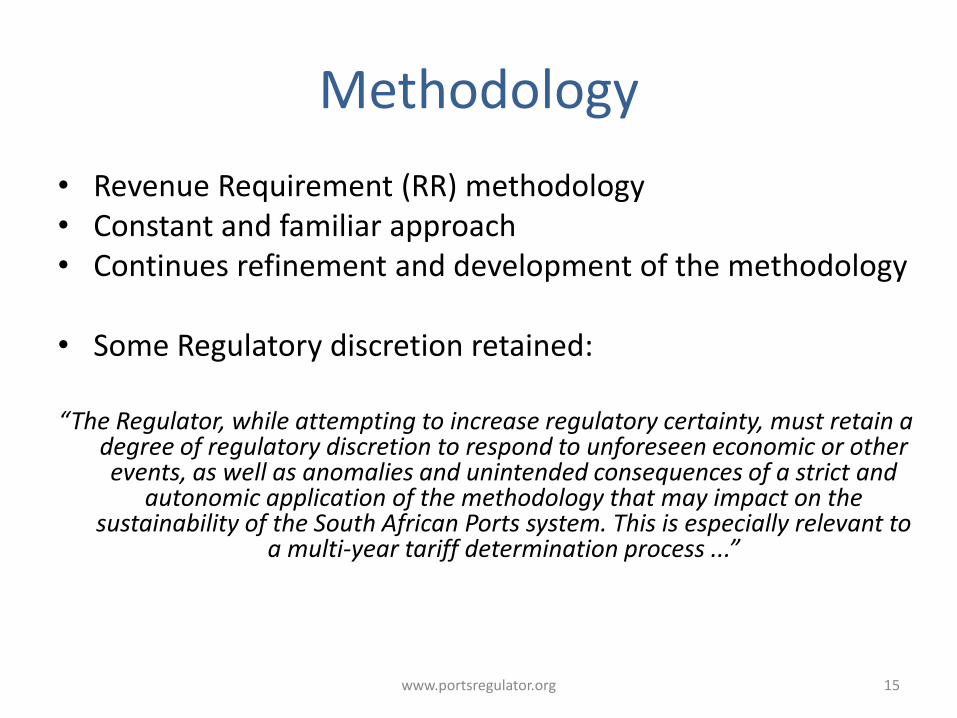

Methodology

• Revenue Requirement (RR) methodology • Constant and familiar approach • Continues refinement and development of the methodology

• Some Regulatory discretion retained:

“The Regulator, while attempting to increase regulatory certainty, must retain a

degree of regulatory discretion to respond to unforeseen economic or other events, as well as anomalies and unintended consequences of a strict and

autonomic application of the methodology that may impact on the sustainability of the South African Ports system. This is especially relevant to

a multi-year tariff determination process ...”

15 www.portsregulator.org

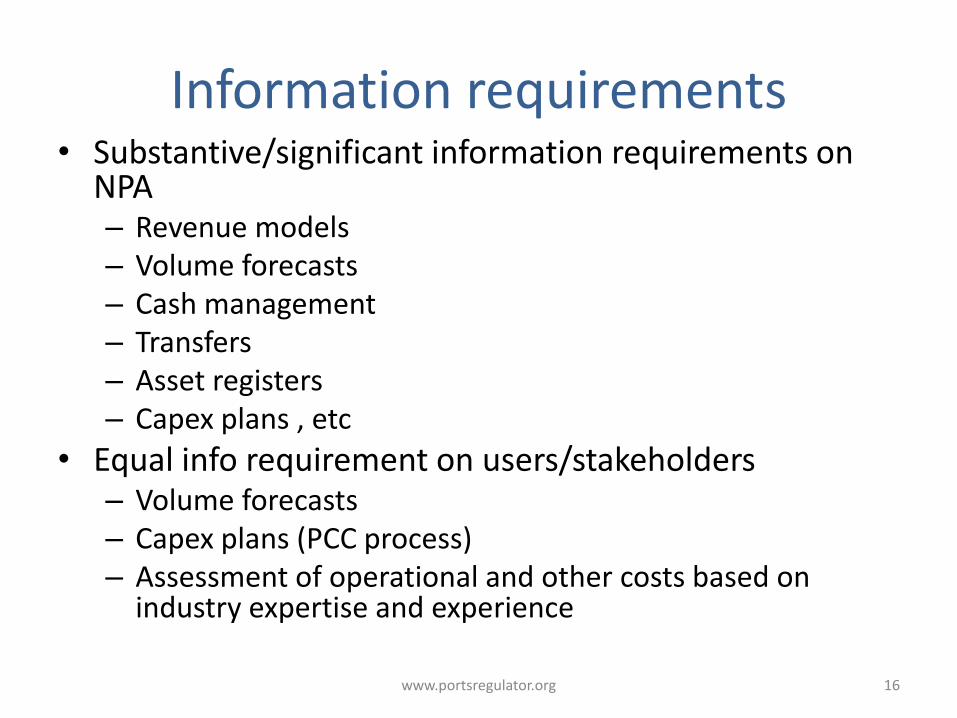

Information requirements • Substantive/significant information requirements on

NPA – Revenue models – Volume forecasts – Cash management – Transfers – Asset registers – Capex plans , etc

• Equal info requirement on users/stakeholders – Volume forecasts – Capex plans (PCC process) – Assessment of operational and other costs based on

industry expertise and experience

16 www.portsregulator.org

Components of the Revenue Required Tariff Methodology

• Regulatory Asset Base (RAB) – Depreciation – Working Capital – Asset Valuation

• Weighted Average Cost of Capital (WACC) (CAPM model) • Taxation • Operating Expense • Depreciation • Claw Back • Excessive Tariff Increase Margin Credit (ETIMC) • Volume forecast

17 www.portsregulator.org

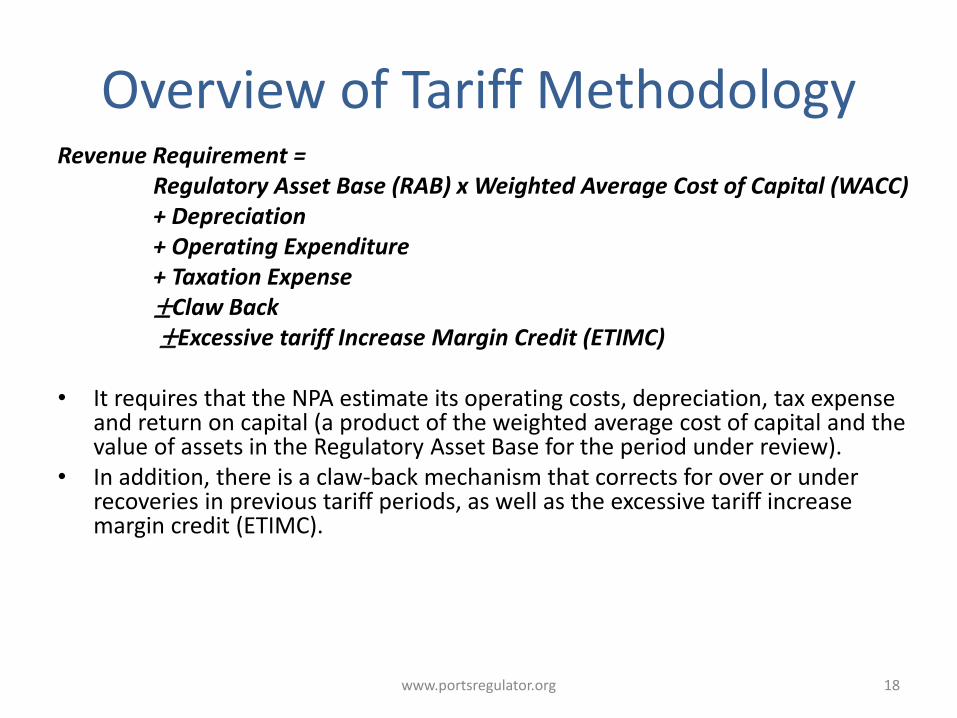

Overview of Tariff Methodology

Revenue Requirement = Regulatory Asset Base (RAB) x Weighted Average Cost of Capital (WACC) + Depreciation + Operating Expenditure + Taxation Expense ±Claw Back ±Excessive tariff Increase Margin Credit (ETIMC) • It requires that the NPA estimate its operating costs, depreciation, tax expense

and return on capital (a product of the weighted average cost of capital and the value of assets in the Regulatory Asset Base for the period under review).

• In addition, there is a claw-back mechanism that corrects for over or under recoveries in previous tariff periods, as well as the excessive tariff increase margin credit (ETIMC).

18 www.portsregulator.org

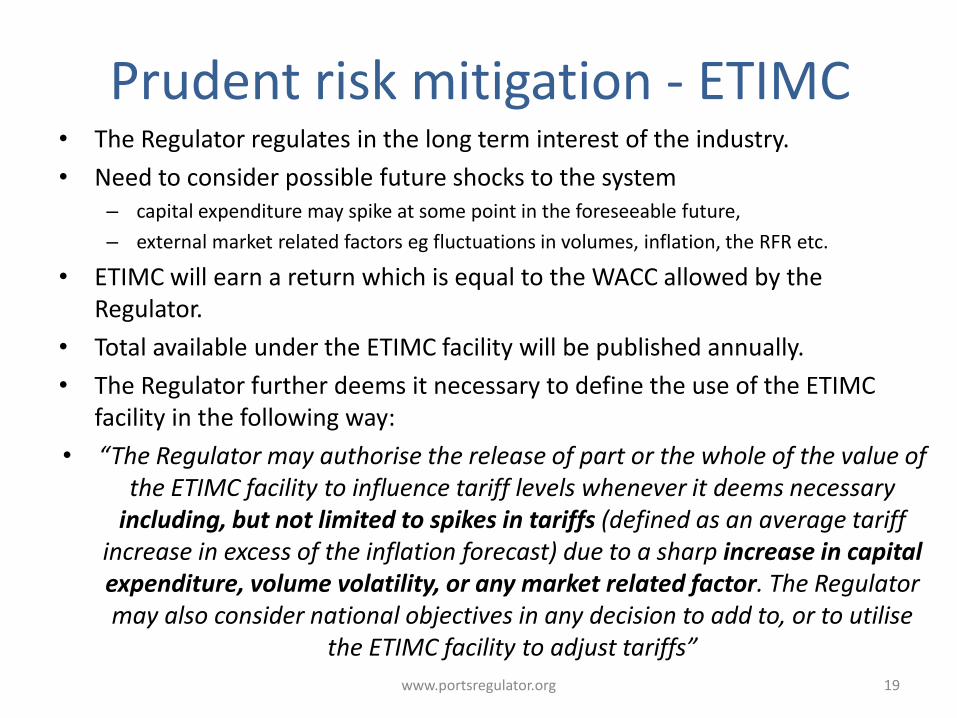

Prudent risk mitigation - ETIMC • The Regulator regulates in the long term interest of the industry.

• Need to consider possible future shocks to the system – capital expenditure may spike at some point in the foreseeable future,

– external market related factors eg fluctuations in volumes, inflation, the RFR etc.

• ETIMC will earn a return which is equal to the WACC allowed by the Regulator.

• Total available under the ETIMC facility will be published annually.

• The Regulator further deems it necessary to define the use of the ETIMC facility in the following way:

• “The Regulator may authorise the release of part or the whole of the value of the ETIMC facility to influence tariff levels whenever it deems necessary

including, but not limited to spikes in tariffs (defined as an average tariff increase in excess of the inflation forecast) due to a sharp increase in capital expenditure, volume volatility, or any market related factor. The Regulator may also consider national objectives in any decision to add to, or to utilise

the ETIMC facility to adjust tariffs”

19 www.portsregulator.org

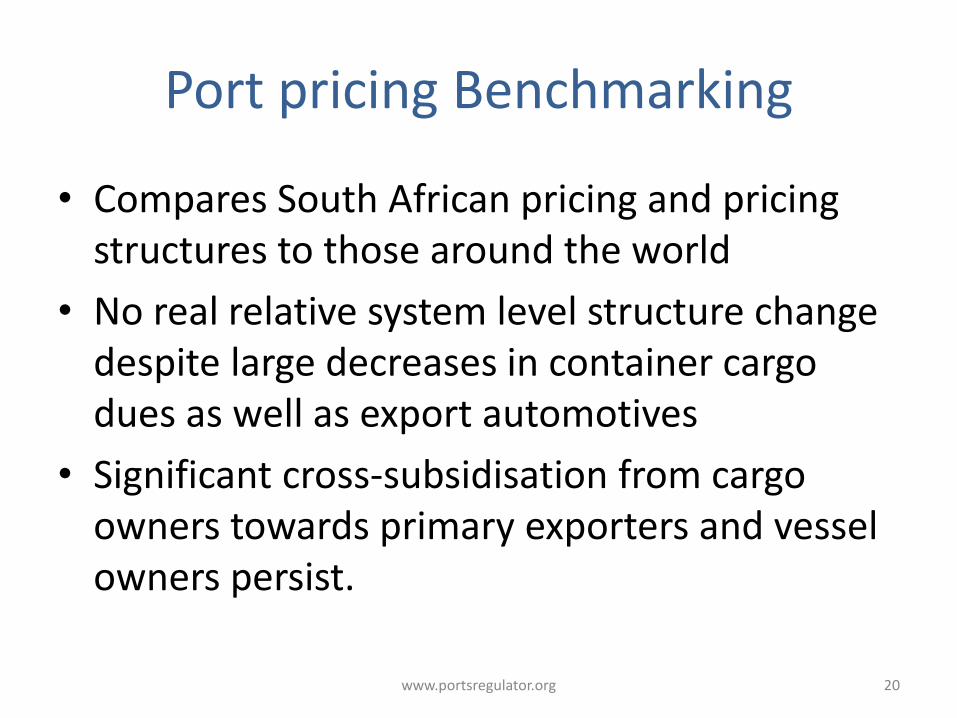

Port pricing Benchmarking

• Compares South African pricing and pricing structures to those around the world

• No real relative system level structure change despite large decreases in container cargo dues as well as export automotives

• Significant cross-subsidisation from cargo owners towards primary exporters and vessel owners persist.

20 www.portsregulator.org

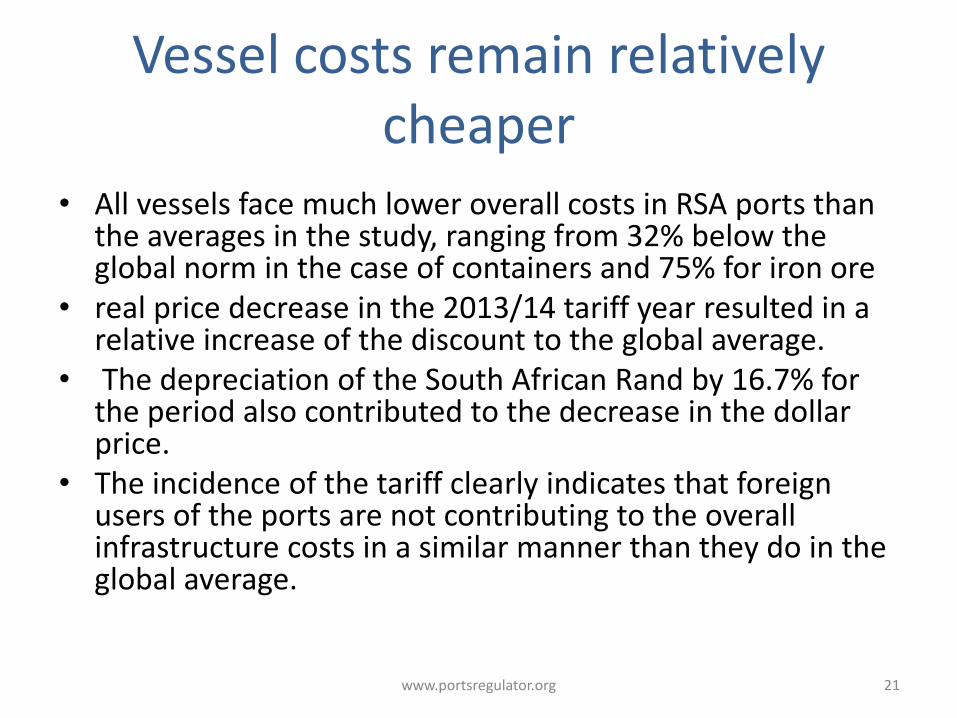

Vessel costs remain relatively cheaper

• All vessels face much lower overall costs in RSA ports than the averages in the study, ranging from 32% below the global norm in the case of containers and 75% for iron ore

• real price decrease in the 2013/14 tariff year resulted in a relative increase of the discount to the global average.

• The depreciation of the South African Rand by 16.7% for the period also contributed to the decrease in the dollar price.

• The incidence of the tariff clearly indicates that foreign users of the ports are not contributing to the overall infrastructure costs in a similar manner than they do in the global average.

21 www.portsregulator.org

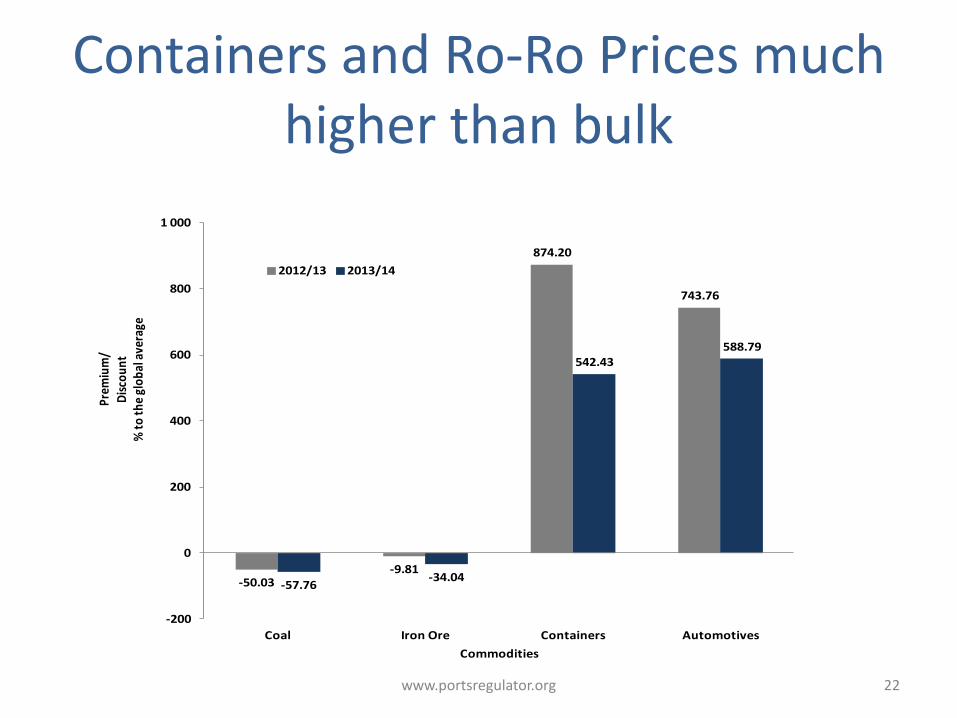

Containers and Ro-Ro Prices much higher than bulk

-50.03-9.81

874.20

743.76

-57.76-34.04

542.43588.79

-200

0

200

400

600

800

1 000

Coal Iron Ore Containers Automotives

Pre

miu

m/

Dis

cou

nt

% t

o t

he

glo

bal

ave

rage

Commodities

2012/13 2013/14

22 www.portsregulator.org

Transhipment below global average

$14.31

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

Tariffs(US$)

Port

Cargo Dues per TEU Transhipped (export, full)

23 www.portsregulator.org

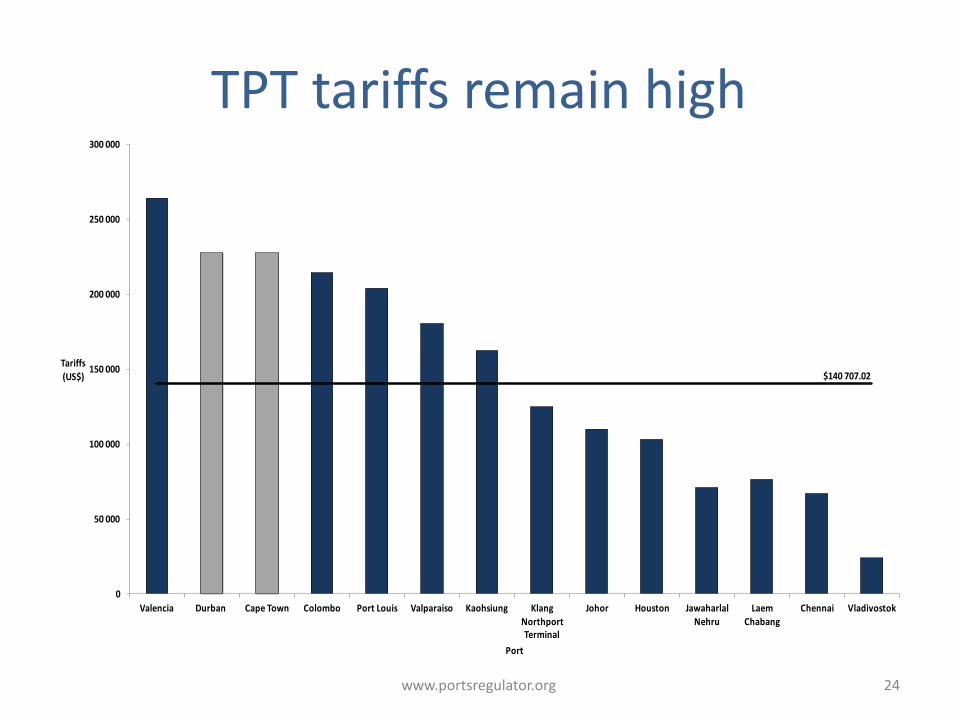

TPT tariffs remain high

$140 707.02

0

50 000

100 000

150 000

200 000

250 000

300 000

Valencia Durban Cape Town Colombo Port Louis Valparaiso Kaohsiung Klang

Northport Terminal

Johor Houston Jawaharlal

NehruLaem

ChabangChennai Vladivostok

Tariffs

(US$)

Port

24 www.portsregulator.org

What can we conclude from this? • High levels of cross-subsidisation in the port system remain a

concern.

• The Regulator has started to adjust the tariff book within the parameters of the Revenue Required methodology applied in the tariff setting process.

• This has started to bring about some normalisation- much more is required and current Tariff Strategy process will take it further.

• South African “Free on Board” (FOB) export and “Cost, Insurance and Freight” (CIF) import predominance in concluding international trade contracts ensuring that the bulk of the port charges liability lies with the South African party, South African container cargo owners continue to carry the greatest burden of the transaction.

25 www.portsregulator.org

Tariff Strategy

• Must address the anomalies and imbalances in the tariff book.

• Establish a more equitable and fair allocation of costs

• Determines the slicing of the cake-not the size

• Close cooperation with the NPA

• Will include comprehensive public consultative process

• May start to take effect from 2016/17

www.portsregulator.org 26

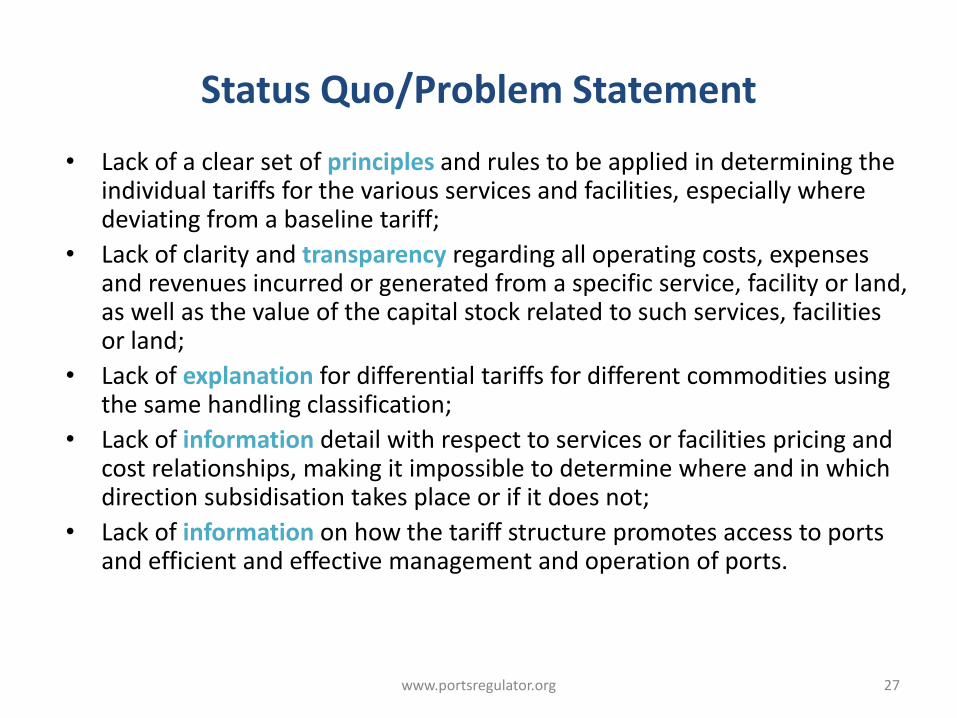

Status Quo/Problem Statement

• Lack of a clear set of principles and rules to be applied in determining the individual tariffs for the various services and facilities, especially where deviating from a baseline tariff;

• Lack of clarity and transparency regarding all operating costs, expenses and revenues incurred or generated from a specific service, facility or land, as well as the value of the capital stock related to such services, facilities or land;

• Lack of explanation for differential tariffs for different commodities using the same handling classification;

• Lack of information detail with respect to services or facilities pricing and cost relationships, making it impossible to determine where and in which direction subsidisation takes place or if it does not;

• Lack of information on how the tariff structure promotes access to ports and efficient and effective management and operation of ports.

www.portsregulator.org 27

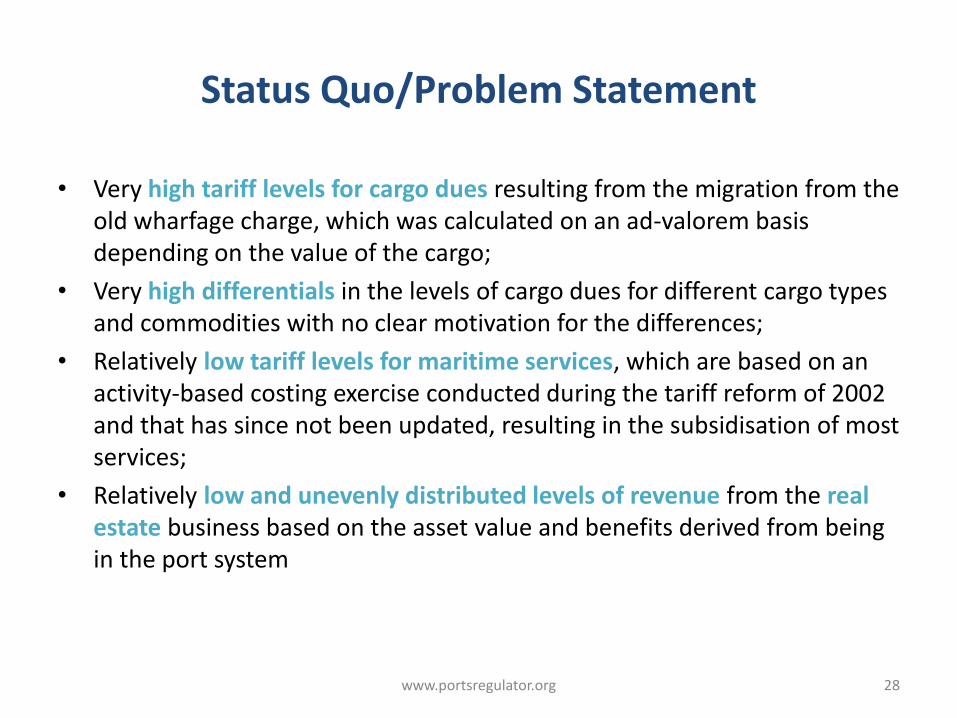

Status Quo/Problem Statement

• Very high tariff levels for cargo dues resulting from the migration from the old wharfage charge, which was calculated on an ad-valorem basis depending on the value of the cargo;

• Very high differentials in the levels of cargo dues for different cargo types and commodities with no clear motivation for the differences;

• Relatively low tariff levels for maritime services, which are based on an activity-based costing exercise conducted during the tariff reform of 2002 and that has since not been updated, resulting in the subsidisation of most services;

• Relatively low and unevenly distributed levels of revenue from the real estate business based on the asset value and benefits derived from being in the port system

www.portsregulator.org 28

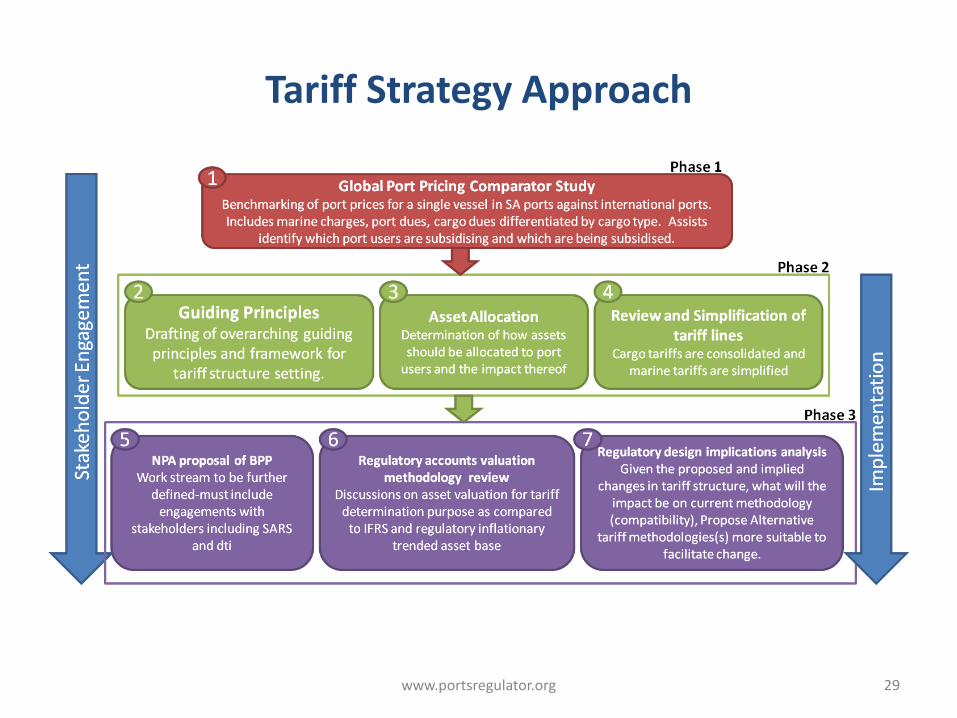

Tariff Strategy Approach

www.portsregulator.org 29

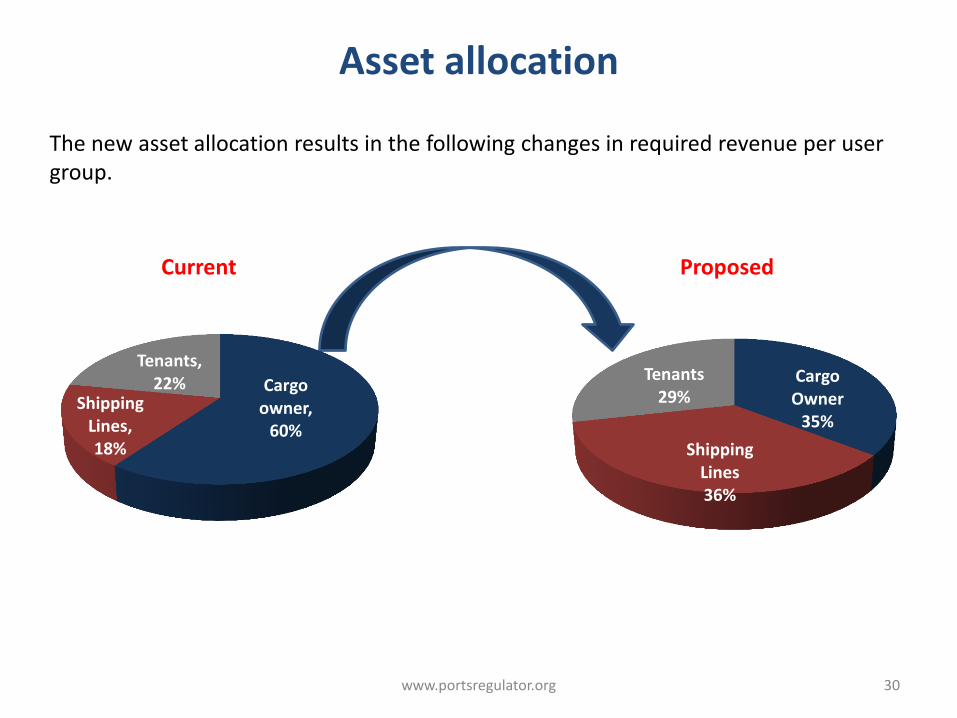

Asset allocation

www.portsregulator.org 30

Cargo owner,

60%

Shipping Lines, 18%

Tenants, 22% Cargo

Owner 35%

Shipping Lines 36%

Tenants 29%

The new asset allocation results in the following changes in required revenue per user group.

Current Proposed

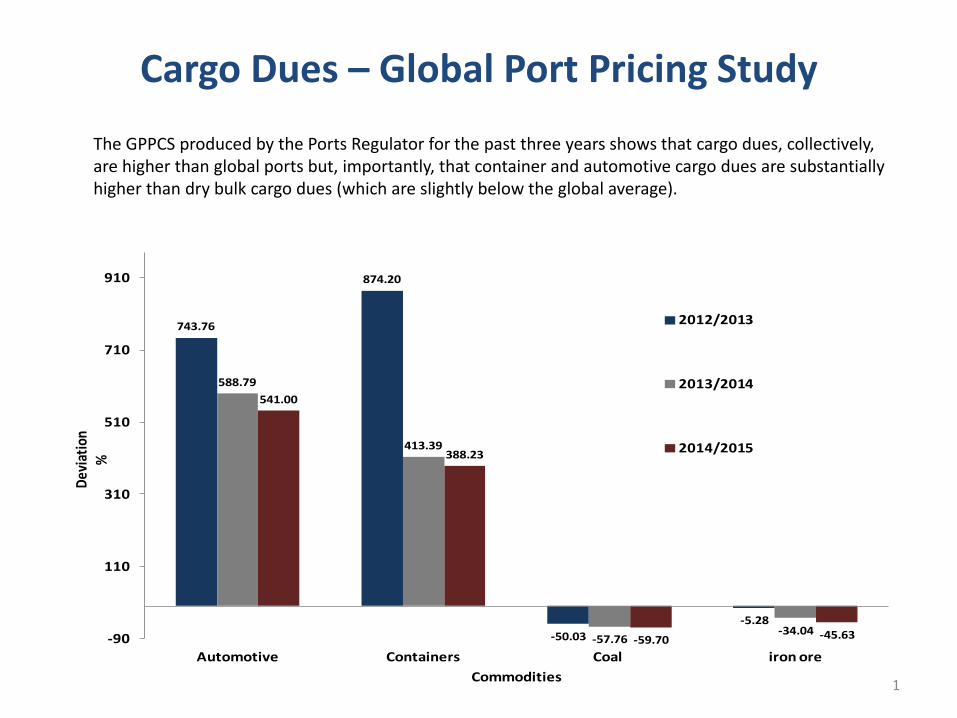

Cargo Dues – Global Port Pricing Study

The GPPCS produced by the Ports Regulator for the past three years shows that cargo dues, collectively, are higher than global ports but, importantly, that container and automotive cargo dues are substantially higher than dry bulk cargo dues (which are slightly below the global average).

www.portsregulator.org 31

743.76

874.20

-50.03

-5.28

588.79

413.39

-57.76-34.04

541.00

388.23

-59.70 -45.63-90

110

310

510

710

910

Automotive Containers Coal iron ore

Dev

iati

on%

Commodities

2012/2013

2013/2014

2014/2015

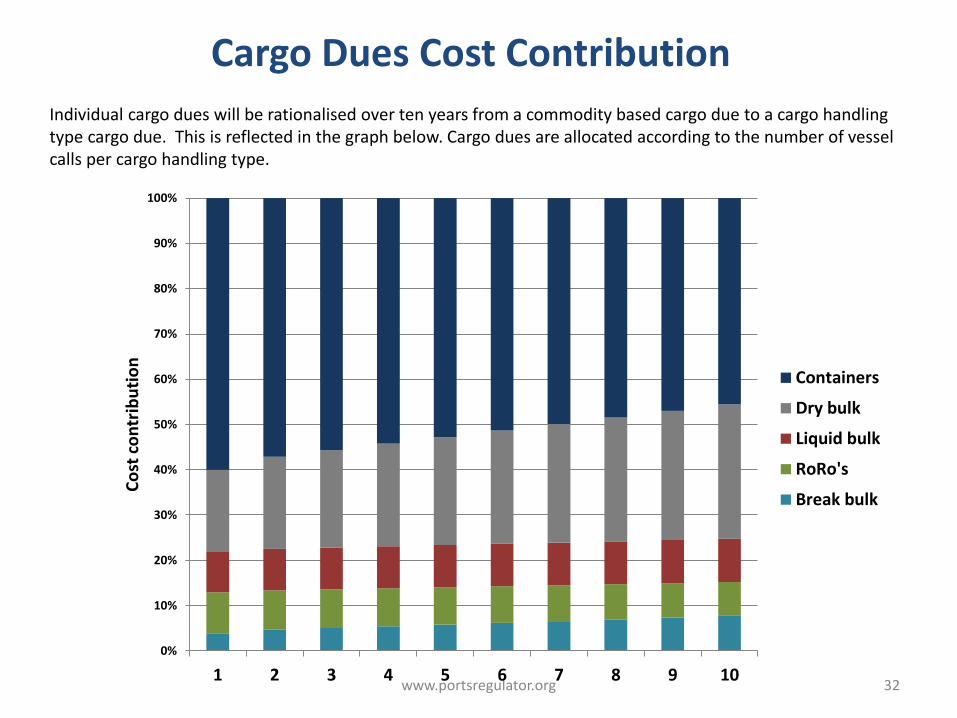

Cargo Dues Cost Contribution

www.portsregulator.org 32

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5 6 7 8 9 10

Co

st c

on

trib

uti

on

Containers

Dry bulk

Liquid bulk

RoRo's

Break bulk

Individual cargo dues will be rationalised over ten years from a commodity based cargo due to a cargo handling type cargo due. This is reflected in the graph below. Cargo dues are allocated according to the number of vessel calls per cargo handling type.

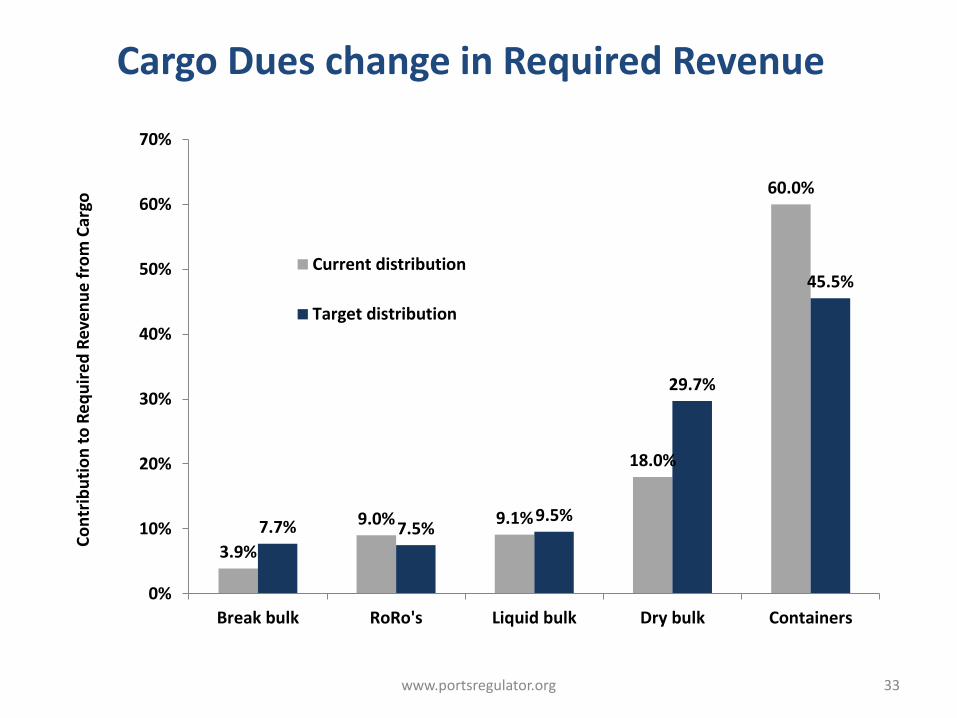

Cargo Dues change in Required Revenue

www.portsregulator.org 33

3.9%

9.0% 9.1%

18.0%

60.0%

7.7% 7.5% 9.5%

29.7%

45.5%

0%

10%

20%

30%

40%

50%

60%

70%

Break bulk RoRo's Liquid bulk Dry bulk Containers

Co

ntr

ibu

tio

n t

o R

eq

uir

ed

Rev

en

ue

fro

m C

argo

Current distribution

Target distribution

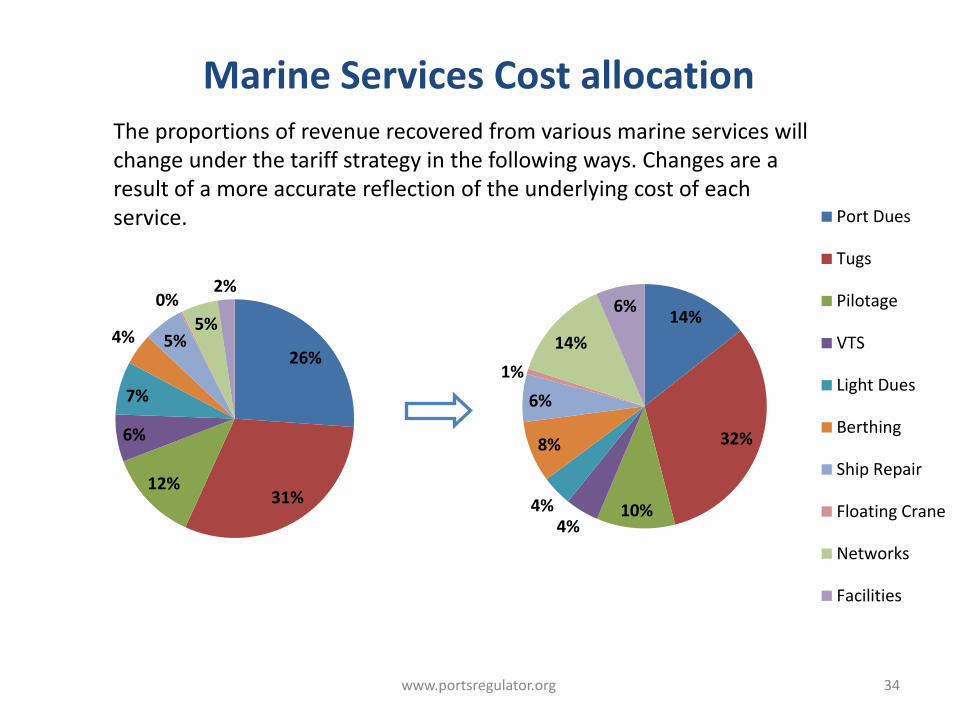

Marine Services Cost allocation

www.portsregulator.org 34

26%

31% 12%

6%

7%

4% 5%

0%

5%

2%

14%

32%

10% 4%

4%

8%

6%

1%

14%

6%

Port Dues

Tugs

Pilotage

VTS

Light Dues

Berthing

Ship Repair

Floating Crane

Networks

Facilities

The proportions of revenue recovered from various marine services will change under the tariff strategy in the following ways. Changes are a result of a more accurate reflection of the underlying cost of each service.

Strategic approach to cross-subsidies

www.portsregulator.org 35

Potential Cross-subsidies arising from historical

pricing

Tariff strategy approach

Cargo owners are subsidising other user groups

such as vessel owners, and tenants.

A new asset allocation that results in an infrastructure cost reflective tariff

proportional to the benefit each user group derives from the infrastructure or

service provision. See sections 2 and 3.

Container and automotive cargo owners pay

more than dry bulk cargo owners on a global

comparator basis

Similarly, infrastructure is costed according to benefit derived from each cargo

handling type – this is calculated by weighting total revenue required from cargo

owners according to the number of vessel calls per cargo type and is then

divided by total volume to get a per unit cost. See section 4.1.

It is still to be determined whether lessees are

being subsidised (i.e. paying less than market

value for their land) and whether some lessees are

subsidising others (i.e. paying unequal or unfair

tariffs).

The Regulator will start to actively monitor rental prices to ensure that two

pieces of land with similar characteristics are not being charged radically

different rentals. Furthermore, the Regulator will endeavour to determine the

market value of port land as part of its asset valuation exercise. See section 4.3.

Port users of a particular port subsidising users in

other ports, through a system wide tariff book

approach.

System-wide pricing will remain in order to reduce the risk placed on any single

port user; however, the tariff book is to be rebalanced and direct user charges in

certain instances may be introduced. See section 2.3.

Port users subsidise fledgling port-related

industries and other national policy

initiatives/government objectives.

Discounting certain infrastructure for identified port users in order to achieve

national objectives of economic growth and inclusion will remain. See section

5.

Use of port revenue/profits for non-port

purposes.

This is outside the scope of the tariff strategy

Port users of the same category or user group

paying lower tariffs than similar users through

differentiated tariffs or discount structures.

All discount structures are to be removed from the tariff book. Tariff

rationalisation will result in a gradual move towards consolidated tariffs that will

include the removal of any discount structure currently in place. Certain built-in

incentives and discounts will remain, mainly related to coastwise shipping and

transhipment etc. See section 5.2 for further information.

Port users’ role critical in considering and supporting the following...

• NPA Port Development Framework Plan (medium to long term planning)

• Annual Capex plan and expenditure trends (projects)

• Volume: Trade and vessel traffic

• Port productivity and performance (infrastructure and marine performance)

• Operators Performance Standards

www.portsregulator.org 36

Operationalised just over 3 years ago, PCCs maturing and gradually improving in:

• Advising Minister of Transport

– Varying levels of success in changing sequencing/scheduling of Capex by NPA

• Assessing and/or supporting Capex programme/infrastructure

– Improved engagement with Capex programme, though there is room for

improvement

• Defining efficient terminal and marine operations indicators and

holding NPA to account on these

– KPI subcommittees being established and/or operationalised to define terminal and

marine operating standards against which NPAs performance will be measured at

port level.

• Submissions on NPAs tariff application

– Through NPCC, port users’ collective submission on the NPAs tariff application are

processed. Have to date been instrumental in interrogating components/ elements

of the NPAs application

www.portsregulator.org 37

38

Ke ya leboga Ke a leboha

Ke a leboga Ngiyabonga Ndiyabulela

Ngiyathokoza Ngiyabonga

Inkomu Ndi khou livhuha

Thank you Dankie

Go to http://www.portsregulator.org for documents

including Records of Decision, Regulatory Manual,

consultation submissions and reports, Draft Tariff Strategy

and other useful documents

www.portsregulator.org