regulation of trust or company service providers - cr… · 11 disciplinary sanctions by hkicpa...

TRANSCRIPT

START PRESENTATION

30.4.2018

2

The Financial Action Task Force (“FATF”), which is

an inter-governmental body established in 1989, sets

international standards on combating money

laundering and terrorist-financing.

Introduction

The FATF has made 40 Recommendations.

Hong Kong has been a member of the FATF since 1991.

1

The FATF Recommendations (1)

Recommendations 22, 28 and 35 are relevant to designated non-financial businesses and professions (“DNFBPs”). DNFBPs includes legal professionals, accounting professionals, estate agents and trust or company service providers (“TCSPs”).

Recommendation 22

DNFBPs should be subject to customer due diligence (“CDD”) and record-keeping requirements when they engage in specified transactions.

3

The FATF Recommendations (2)

Recommendation 28

DNFBPs should be subject to effective systems for monitoring and ensuring compliance with anti-money laundering and countering the financing of terrorism (AML/CFT) requirements.

Recommendation 35

There should be a range of effective, proportionate and dissuasive sanctions, whether criminal, civil or administrative, to deal with any non-compliance with AML/CTF requirements by DNFBPs.

4

2

5

The Anti-Money Laundering and Counter-Terrorist

Financing (Financial Institutions) (Amendment) Bill

2017 ("the AML Bill") received its First Reading at

the Legislative Council meeting of 28 June 2017.

The AML Bill was passed on 24 January 2018.

《 Anti-Money Laundering and Counter-Terrorist Financing Ordinance (“AMLO”)》 (1)

《Professional Accountants Ordinance》 (Chapter 50)

The Law Society of Hong Kong

Hong Kong Institute of

Certified Public Accountants

Estate Agents

Authority Companies

Registry

《 Legal Practitioners Ordinance》 (Chapter 159)

《Estate Agents Ordinance》

(Chapter 511)

《 Anti-Money Laundering and Counter-Terrorist Financing Ordinance》 (Chapter 615 )

6

Legal Professionals

Accounting

Professionals Estate Agents

Trust or Company Service Providers

• To prescribe statutory CDD and record-keeping requirements to DNFBPs when these professionals engage in specified transactions.

《 Anti-Money Laundering and Counter-Terrorist Financing Ordinance》 (2)

3

《 Anti-Money Laundering and Counter-Terrorist Financing Ordinance》 (3)

• The licensing regime for TCSPs came into operation on 1 March 2018

• Introduce a licensing regime for TCSPs to require them to apply for a licence from the Registrar of Companies (“the Registrar”) and satisfy a “fit-and-proper” test before they can provide trust or company services as a business in Hong Kong. (AMLO sections 53F, 53G and 53H)

• The Registrar keeps a register of all TCSP licensees, which is open for public inspection. (AMLO section 53D)

7

“Fit and Proper” Test (1)

Applicants, and their directors / partners / ultimate

owners (where applicable), will be subject to a “fit and proper” test.

In determining whether a person is fit and proper to

carry on, or be associated with, a TCSP business,

the Registrar will have regard to any matter that the

Registrar considers relevant.

8

4

“Fit and Proper” Test (2)

Other matters to be taken into account include :-

• whether the person has any criminal conviction, in particular, those relating to money laundering or terrorist financing or involving fraud or dishonesty

• whether the person is an undischarged

bankrupt/ in liquidation or receivership

(AMLO sections 53H and 53I)

9

Licensing Regime for TCSPs

The TCSP licensing requirement (including the fit and

proper test) does not apply to:

• an authorized institution;

• a licensed corporation that operates a TCSP business that is ancillary to the corporation’s principal business;

• an accounting professional;

• a legal professional.

(AMLO section 53B)

10

5

HKICPA’s Guidelines on Anti-Money Laundering and

Counter-Terrorist Financing for Professional Accountants

HKICPA has issued AML / CTF guidelines, which form

part of the Code of Ethics for Professional Accountants,

and non-compliance with them may result in disciplinary

proceedings against the members and / or CPA practices

concerned.

Under the Ordinance, there is no criminal penalty for the

statutory CDD and record-keeping requirements, and

breaches by accountants will continue to be subject to the

disciplinary regime of HKICPA.

11

Disciplinary sanctions

by HKICPA

Disciplinary sanctions

by HKICPA

12

6

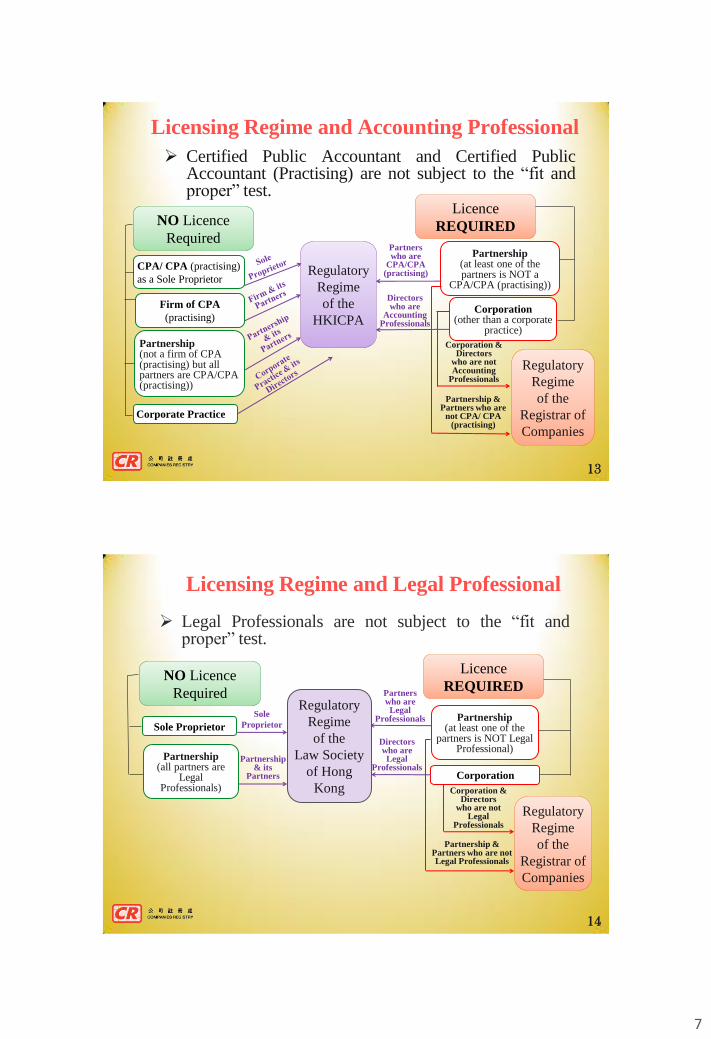

Licensing Regime and Accounting Professional

Certified Public Accountant and Certified Public Accountant (Practising) are not subject to the “fit and proper” test.

NO Licence

Required

CPA/ CPA (practising)

as a Sole Proprietor

Firm of CPA

(practising)

Partnership (not a firm of CPA (practising) but all partners are CPA/CPA (practising))

Corporate Practice

Regulatory

Regime

of the

HKICPA

Licence

REQUIRED

Partnership (at least one of the partners is NOT a

CPA/CPA (practising))

Partners who are

CPA/CPA (practising)

Corporation (other than a corporate

practice)

Regulatory

Regime

of the

Registrar of

Companies

Partnership & Partners who are

not CPA/ CPA (practising)

Directors who are

Accounting Professionals

Corporation & Directors

who are not Accounting

Professionals

13

Licensing Regime and Legal Professional

Legal Professionals are not subject to the “fit and proper” test.

Sole Proprietor

Regulatory

Regime

of the

Law Society

of Hong

Kong

Sole

Proprietor

NO Licence

Required

Partnership (all partners are

Legal Professionals)

Partnership & its

Partners

Licence

REQUIRED

Partnership (at least one of the

partners is NOT Legal Professional)

Partners who are Legal

Professionals

Partnership & Partners who are not Legal Professionals

Regulatory

Regime

of the

Registrar of

Companies

Corporation

Corporation & Directors

who are not Legal

Professionals

Directors who are

Legal Professionals

14

7

15

Validity Period and Renewal of Licence

In usual circumstances, a licence, once

granted, will last for 3 years.

(AMLO sections 53K and 53O)

A licensee may apply to the Registrar for a

renewal of the licence.

Applicants for renewal of a licence will be

subject to the same “fit and proper” test

applicable to an application for a new

licence.

(AMLO section 53R)

16

Revocation or Suspension of Licence

The Registrar may revoke a licence or suspend a licence for a specified period if the Registrar considers that an individual licensee, any partner, director or ultimate owner of a licensee is no longer a fit and proper person to carry on, or be associated with, a trust or company service business.

The revocation or suspension of licence takes effect at the time specified in the notice.

The Registrar must inform the licensee of the revocation or suspension by notice in writing.

(AMLO section 53Q)

8

17

Any person proposing to become a partner, director

or an ultimate owner of a licensee is required to

obtain the Registrar’s prior written approval.

Registrar’s Approval to Become a Partner/

Director/ Ultimate Owner of a TCSP Licensee

(AMLO sections 53S, 53T & 53U)

The application for the approval is to be made by

the licensee.

The Registrar will apply the same “fit and proper” test.

18

Licensee’s Duty to Give Notifications

A licensee has the duty to notify the Registrar if :-

• There is any change in the particulars previously

provided in connection with the licensee’s application for the grant or renewal of a licence;

• The licensee intends to cease to carry on the trust

or company service business.

(AMLO sections 53W and 53X)

9

19

Power of Inspection and Discipline

Site inspections will be carried out to ensure

compliance with the CDD and record-keeping

requirements.

• Public reprimand;

• Remedial order to remedy the contravention;

• Payment of a pecuniary penalty not

exceeding $500,000.

(AMLO section 53Z)

Licensees will be subject to disciplinary sanctions to

be imposed by the Registrar as follows:-

Application for TCSP Licence (1)

Sole proprietor

Partnership Corporation

Apply for TCSP Licence

20

10

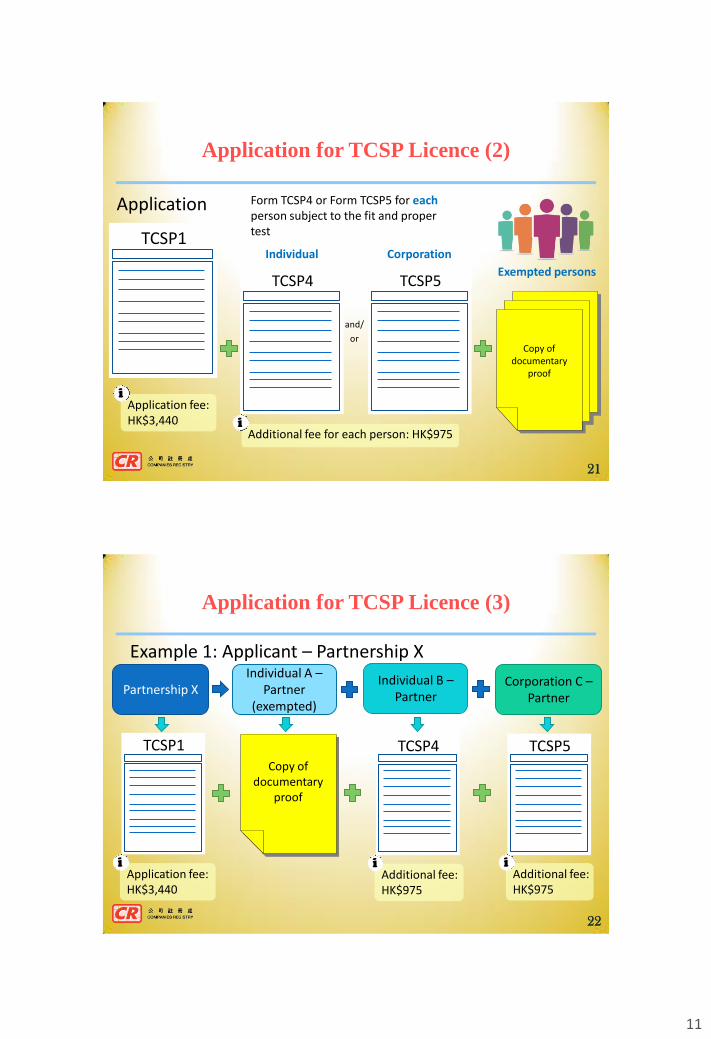

Application for TCSP Licence (2)

Copy of documentary

proof

Exempted persons

Form TCSP4 or Form TCSP5 for each person subject to the fit and proper test TCSP1

TCSP4 TCSP5

Additional fee for each person: HK$975 i

Individual Corporation

Application fee: HK$3,440

i

Application

and/

or

21

Application for TCSP Licence (3)

Example 1: Applicant – Partnership X Individual A –

Partner (exempted)

Individual B – Partner

Corporation C – Partner

Copy of documentary

proof

TCSP1 TCSP4 TCSP5

Partnership X

Application fee: HK$3,440

i Additional fee: HK$975

i Additional fee: HK$975

i

22

11

TCSP4

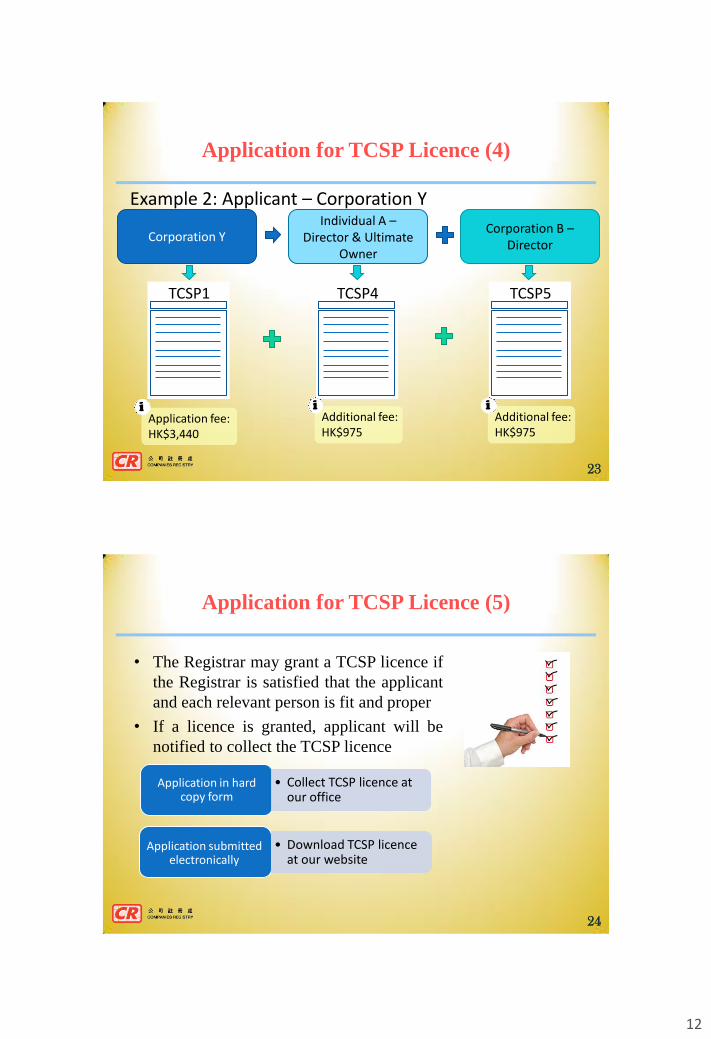

Application for TCSP Licence (4)

Individual A – Director & Ultimate

Owner

Corporation B – Director

Example 2: Applicant – Corporation Y

TCSP1 TCSP5

Corporation Y

Application fee: HK$3,440

i Additional fee: HK$975

i Additional fee: HK$975

i

23

Application for TCSP Licence (5)

• The Registrar may grant a TCSP licence if

the Registrar is satisfied that the applicant

and each relevant person is fit and proper

• If a licence is granted, applicant will be

notified to collect the TCSP licence

Application in hard copy form

• Collect TCSP licence at our office

Application submitted electronically

• Download TCSP licence at our website

24

12

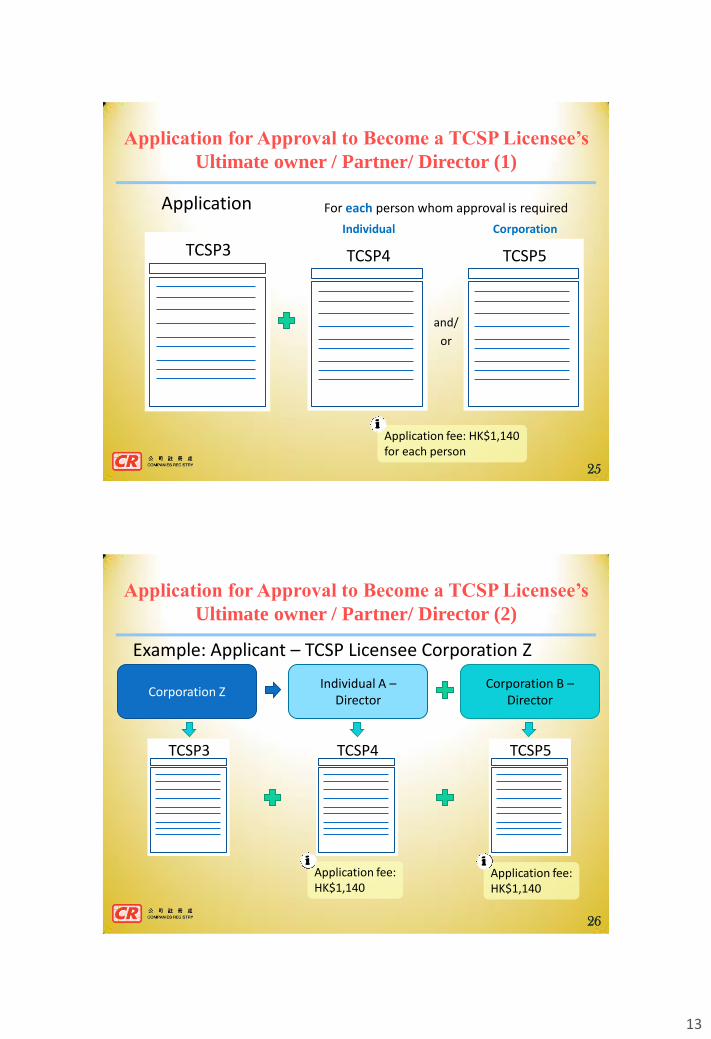

Application for Approval to Become a TCSP Licensee’s Ultimate owner / Partner/ Director (1)

For each person whom approval is required

and/

or

TCSP3 TCSP4 TCSP5

Application

Application fee: HK$1,140 for each person

i

Individual Corporation

25

Example: Applicant – TCSP Licensee Corporation Z

Application for Approval to Become a TCSP Licensee’s Ultimate owner / Partner/ Director (2)

TCSP4

Individual A – Director

Corporation B – Director

TCSP3 TCSP5

Corporation Z

Application fee: HK$1,140

i Application fee: HK$1,140

i

26

13

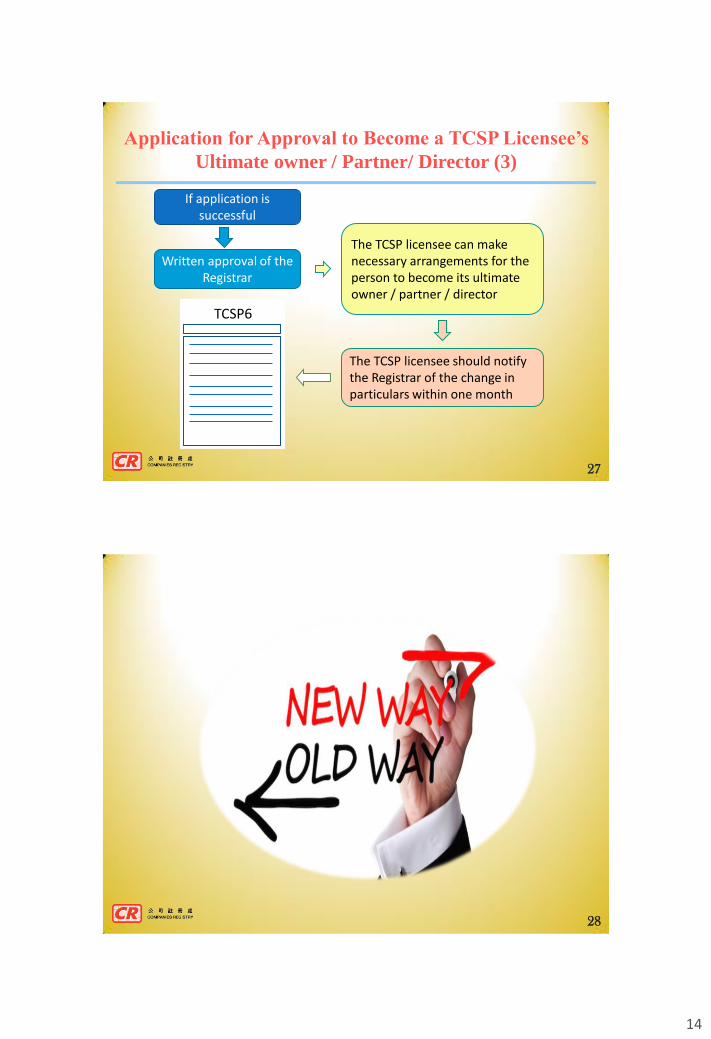

Application for Approval to Become a TCSP Licensee’s Ultimate owner / Partner/ Director (3)

The TCSP licensee should notify the Registrar of the change in particulars within one month

TCSP6

Written approval of the Registrar

If application is successful

The TCSP licensee can make necessary arrangements for the person to become its ultimate owner / partner / director

27

28

14

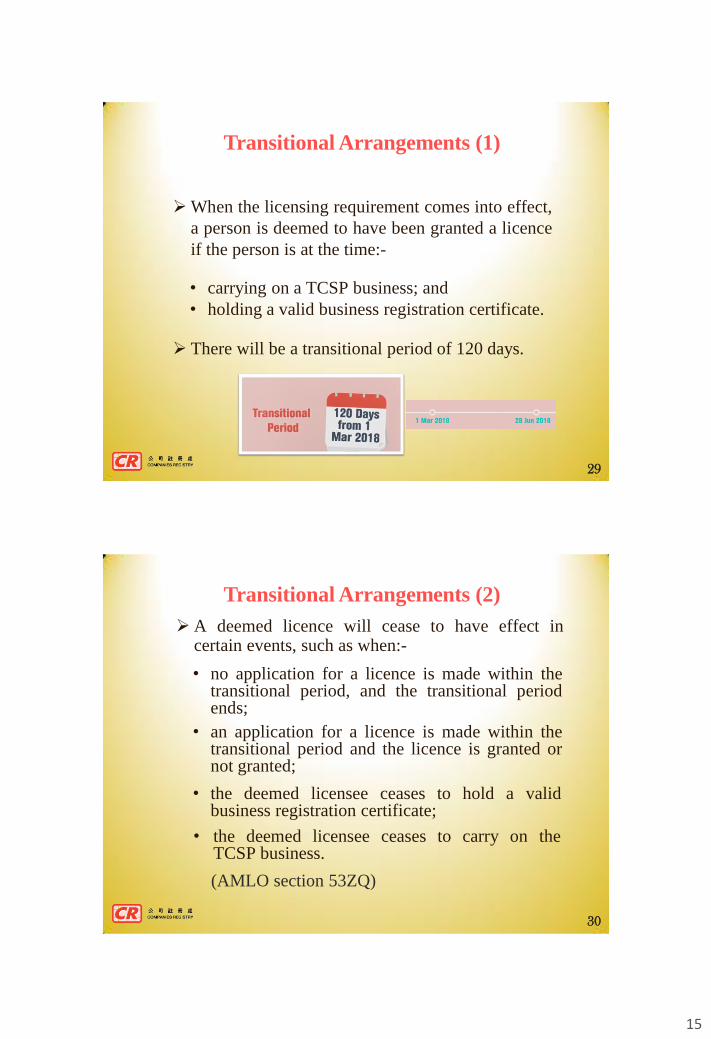

Transitional Arrangements (1)

When the licensing requirement comes into effect,

a person is deemed to have been granted a licence

if the person is at the time:-

• carrying on a TCSP business; and

• holding a valid business registration certificate.

There will be a transitional period of 120 days.

29

Transitional Arrangements (2)

A deemed licence will cease to have effect in certain events, such as when:-

• no application for a licence is made within the transitional period, and the transitional period ends;

• an application for a licence is made within the transitional period and the licence is granted or not granted;

• the deemed licensee ceases to hold a valid business registration certificate;

• the deemed licensee ceases to carry on the TCSP business.

(AMLO section 53ZQ)

30

15

Applications for TCSPs licences

Up to 31 March 2018

Number of applications

> 1,700

Number of enquiries

> 6,000

Number of visits on TCSP website

31

> 78,000

Guidelines and Reference Materials

The Registrar has published the following

guidelines:-

• Guideline on Licensing of Trust or Company Service Providers;

• Guideline on Compliance of Anti-Money Laundering and Counter-Terrorist Financing Requirements for Trust or Company Service Providers;

• Guideline for Imposition of Pecuniary Penalty.

External circulars, pamphlets, demonstration

videos, hotline, FAQs, etc.

32

16

17