release of the global competitiveness report 2012-13 …cpd.org.bd/downloads/gcr2012.pdf · the...

TRANSCRIPT

Release of The Global Competitiveness Report 2012-13

and The Bangladesh Business Environment Study 2012

CENTRE FOR POLICY DIALOGUE (CPD)

B A N G L A D E S H

a c i v i l s o c i e t y t h i n k – t a n k

Press Advisory Dhaka: September 05, 2012

1

2

Study Advisors Professor Mustafizur Rahman

Dr Debapriya Bhattacharya

Team Leader Dr Khondaker Golam Moazzem

Analysis and Research Kishore Kumer Basak

Saifa Raz

Survey Team Urmee Dasgupta

Data Collection and Data Entry Operation Shanker Chandra Saha

Harunur Rashid

GCR Study Team

3

I. Introduction and Objectives

II. Methodology

• Survey Design

• Assessment of Global Competitiveness Index

• Assessment of Bangladesh’s Business Environment

III. Global Competitiveness Report (GCR) 2012-2013: Major Findings

• Global Competitiveness Index (GCI)

• Performance of Selected Economies in GCI

• Bangladesh in GCI Ranking and Changes in GCI Scores

IV. Identification of Problematic Factors for Bangladesh Economy

V. Bangladesh’s Business Environment in 2012

VI. Findings from Rapid Perception Survey

VII. Concluding Remarks

VIII. Annex

Content

• The Centre for Policy Dialogue (CPD) in collaboration with the World Economic Forum (WEF) has been carrying out the Executive Opinion Survey (EOS) since 2001.

• CPD has conducted the 12th survey this year

• EOS is based on the questionnaires developed by the WEF

• CPD also conducted the 9th Rapid Assessment Survey on the prevailing economic issues and concerns

• Major objectives of the press briefing are

• To release WEF’s Global Competitiveness Report 2012-13 in Bangladesh. The report is launching globally today, 5 September 2012

• To report the state of competitiveness of Bangladesh during 2011

• To state the recent concerns on business environment in Bangladesh

4

I. Introduction and Objectives

5

Survey Design

• WEF-CPD survey covers the large and medium companies

• Total assets should be no less than Tk.10 crores (US$1.25 million)

• Number of respondents: 87 in 2012 (70 in 2011)

• Both manufacturing and service related firms and related trade bodies were

covered in the EOS survey

• Domestic companies held the overwhelming share of total responses (85%)

• 86% companies are located in the Dhaka region • Survey conducted: February to April, 2012

• Reference period: January to December 2011

• Rapid Assessment Survey (RAS) was carried out along with the Executive Opinion Survey (EOS)

• This presentation is based on findings of both the surveys

Table: Sectoral Distribution of Survey Respondents

Sectors 2011 2012

Total 70 (100%) 87 (100%)

Manufacturing 33(47.1%) 33(38.1%)

RMG 15(21.4%) 11(13.6%)

Pharmaceuticals 3(4.3%) 4(4.5%)

Power generation/Leather 6(8.6%) 5(5.4%)

Others 9(12.9%) 13(14.6%)

Financial Institution 5(7.1%) 9(10%)

Real Estates & Construction 5(7.1%) 6(6.4%)

ICT 6(8.6%) 11(12.7%)

Other Services 21(30%) 28(32.7%)

II. Methodology

Stage of development Factor driven Stage 1

Transition from stage 1 - 2

Efficiency driven stage 2

Transition from stage 2 - 3

Innovation driven stage 3

GDP per-capita (US$) <2,000 2,000 - 2,999 3,000 - 8,999 9,000 - 17,000 > 17,000

Basic requirements 60% 40-60% 40% 20-40% 20%

Efficiency enhancers 35% 35-50% 50% 50% 50%

Innovation and sophistication

5% 5-10% 10% 10-30% 30%

6

• Assessment of Bangladesh's Business Environment

• Global Competitiveness Index (GCI) is an index of weighted average of 12 different pillars

• Basic requirements sub-index :(4 pillars)factor-driven stage

• Efficiency enhancers sub-index:(6 pillars)efficiency-driven stage

• Innovation and sophistication factors sub-index:(2 pillars)innovation-driven stage

• GCI is estimated on the basis of moving averages of two years

• Each sub-index has different weights considering country’s stages of development

• Bangladesh is considered at factor-driven stage

Table: Subindex weights and income thresholds for stages of development

II. Methodology

•Assessment of Bangladesh's Business Environment

• Analysis has been performed by employing three statistical techniques

• Frequency analysis (% of respondents)

• Weighted index (average weighted response)

• Chi-square test (level of significance)

• Executive Opinion Survey and Rapid Perception Survey use qualitative data (7-point Likert scale)

• Negative responses (scale: -3 ~ -1)

• Indifferent responses (scale: 0)

• Positive responses (scale:1~ 3)

• Various weighted responses are clustered into six groups:

a) Worst: (-3.0 to -2.01) b) Worse: (-2.0 to -1.01) c) Bad: (-1.0 to -0.01)

d) Good: (+0.01 to +1.0) e) Better: (+1.01 to +2.0) f) Best: (+2.01 to +3.0)

7

Response Levels

Responses Completely Disagree

Largely Disagree

Somewhat Disagree

Indifferent

Somewhat Agree

Largely Agree

Completely Agree

Weight -3 -2 -1 0 +1 +2 +3

Group Worst

(-3.0 to -2.01) Worse

(-2.0 to -1.01) Bad

(-1.0 to -0.01) Neutral Good

(+0.01 to +1.0) Better

(+1.01 to +2.0) Best

(+2.01 to +3.0)

II. Methodology

8

III. Global Competitiveness Report 2012-13: Major Findings

9

III. Global Competitiveness Report 2012-13: GCI Economies 2011-12 2012-13 Change

Switzerland 1 1 Singapore 2 2 Finland 4 3 Sweden 3 4 Netherlands 7 5 Germany 6 6 USA 5 7 UK 10 8 Hong Kong SAR 11 9 Japan 9 10

• Global Competitiveness Index: Rankings

•A total of 144 countries have been assessed in 2012 (142 in 2011)

• New inclusions: Gabon, Guinea, Liberia, Seychelles and Sierra Leone

• Libya was re-included after one year of absence

• Belize, Angola, Syria and Tunisia had to exclude from this year’s Report

• Six of top ten countries are European and three from Asia and rest is the USA

•Switzerland has been maintaining the top position in the table for the last four years: innovation and labour market efficiency, best scientific research institutions; and high productivity.

•Singapore remains the top Asian country by retaining the 2nd position: best public and private institutions; efficiency of its goods and labor markets; strong financial market; world-class infrastructure.

•Finland moves up one place to reach 3rd position: a well functioning and highly transparent public institution.

•USA continues to decline, falling two more positions to take 7th place this year.

10

III. Global Competitiveness Report 2012-13: GCI Countries 2011-12 2012-13 Change

Malaysia 21 25

China 26 29

Thailand 39 38

Brazil 53 48

Indonesia 46 50

India 56 59

Philippines 75 65

Russian Federation 66 67

Sri Lanka 52 68

Colombia 68 69

Vietnam 65 75

Bangladesh 108 118

Pakistan 118 124

Nepal 125 125

•Performance of Selected Economies

•Among the BRIC countries, only Brazil managed to gain five positions, standing at 48th

•China remains top (29) followed by India (59) and Russia (67)

• In South Asia, all the countries slipped from their earlier ranks.

• Sri Lanka dropped by 16 ranks (68), Pakistan 6 ranks (124), Nepal remained at their last year’s position (125)

•Bangladesh experienced a steep fall this year

• Standing at 118th, slipped by 10 positions

•GCI score also came down

•Among other Asian countries, Philippines gained 10 positions (65) switching place with Vietnam (75), Thailand ranked 38th, Malaysia at 25th and Indonesia at 50th.

11

III. Global Competitiveness Report 2012-13: GCI

Indices Rank Score (out of 7) % Change

in Score 2011-12 2012-13 2011-12 2012-13

GCI 108 118 3.73 3.65 -2.14

Basic Requirements (BR) 112 119 3.81 3.72 -2.36

Institutions 112 127 3.31 3.2 -3.32

Infrastructure 134 134 2.24 2.22 -0.89

Macroeconomic Stability 75 100 4.70 4.24 -9.79

Health and Primary Education 108 103 5.01 5.2 3.79

Efficiency Enhancers (EE) 99 107 3.69 3.62 -1.90

Higher Education and Training 126 126 2.81 2.88 2.49

Goods Market Efficiency 81 95 4.09 4.10 0.24

Labour Market Efficiency 100 117 4.02 3.91 -2.74

Financial Market Sophistication 67 95 4.07 3.74 -8.11

Technological Readiness 122 125 2.82 2.74 -2.84

Market Size 49 47 4.32 4.36 0.93

Innovation and Sophistication (IS) 113 122 3.04 2.98 -1.97

Business Sophistication 98 108 3.51 3.5 -0.28

Innovation 124 130 2.57 2.47 -3.89

Bangladesh in GCI Rankings and Changes in GCI Scores

• In the GCI 2012-13, Bangladesh ranked 118th , slipped 10 positions (108th in 2011-12)

• Among the same sample of 2011-12, position would stand at 114th . Countries advanced from behind are: Dominican Rep., Nicaragua, Guyana, Cameroon, Nigeria, Senegal and Paraguay

• GCI score also declined by 2.1% (from 3.73 in 2011 to 3.65 in 2012-13)

• Ranks in the three main pillars dropped sharply

• Basic requirement: 119th (112th) and score: 3.72 (3.81), -2.4%

• Efficiency enhancer: 107th (99th), score: 3.62 (3.69), -1.9%

• Innovation and sophistication: 122nd (113th), score: 2.98 (3.04), -2.0%

• Ranks in sub-pillars where Bangladesh’s position has declined

• Institutions: 127th (112th)

• Macroeconomic stability: 100th (75th)

• Goods market efficiency: 95th (81st)

• Labour market efficiency: 117th (100th)

• Financial market sophistication: 95th (67th)

• Ranks in sub-pillars where Bangladesh’s position has improved

• Human capital (health and primary education): 103rd (108th)

• Market size: 47th (49th) 12

III. Global Competitiveness Report 2012-13: GCI

13

IV. Identification of Problematic Factors for Bangladesh’s Economy

Rank 2011 2012 1 Inadequate supply of infrastructure (22.56) Inadequate supply of infrastructure (20.39) 2 Corruption (18.45) Corruption (17.43) 3 Inefficient government bureaucracy (17.40) Access to financing (9.88) 4 Policy instability (6.98) Inefficient government bureaucracy (9.34) 5 Inadequately educated workforce (6.02) Policy instability (8.40) 6 Access to financing (5.16) Inflation (8.33) 7 Inflation (4.97) Government instability/coups (5.68) 8 Foreign currency regulations (4.02) Foreign currency regulations (4.12) 9 Tax regulations (3.92) Tax rates (3.97) 10 Crime and theft (3.15) Inadequately educated workforce (3.81) 11 Tax rates (2.39) Complexity of tax regulations (2.26) 12 Government instability/coups (2.20) Poor work ethic in national labour force (1.71) 13 Poor work ethic in national labour force (1.63) Crime and theft (1.63) 14 Restrictive labour regulations (0.86) Insufficient capacity to innovate (1.17) 15 Poor public health (0.29) Restrictive labour regulations (1.09) 16 Poor Public Health (0.78)

• Inadequate supply of infrastructure (20.4%), corruption (17.4%) and lack of access to finance (9.9) are top three problematic factors.

• For the first time, lack of access to finance for businesses perceived as a major constrain: ‘Crowd out’ effect due to excess government borrowing.

•Another growing important problematic factor for businesses is government instability

• Jumped up to rank 7th from 12th in 2011.

•Positive changes were discerned in case of inadequate educated workforce, inefficient government bureaucracy, policy instability, lax tax regulation and crime and theft. 14

Identification of Problematic Factors for Doing Business

2011 2012

1 Identifying potential markets and buyers (17.83) Identifying potential markets and buyers (15.99)

2 Inappropriate production technology and skills (13.78) Access to imported inputs at competitive prices (11.40)

3 Access to imported inputs at competitive prices (13.40) Inappropriate production technology and skills(11.03)

4 High cost or delays caused by domestic transportation (11.13) Difficulties in meeting quality requirements of buyers (10.75)

5 Difficulties in meeting quality requirements of buyers (10.87) Access to trade finance(10.57)

6 Technical requirements and standards abroad (10.37) Tariff barriers abroad(10.57)

7 Access to trade finance (8.22) High cost or delays caused by domestic transportation(9.10)

8 High cost of delays caused by foreign transportation (5.56) Technical requirements and standards abroad(8.09)

9 Rules of origin requirements abroad (5.44) Rules of origin requirements abroad(4.60)

10 Burdensome procedures/corruption at foreign borders (3.41) High cost or delays caused by foreign transportation(4.41)

Burdensome procedures/corruption at foreign borders(3.49)

•Top three problematic factors for exporting are - Lack of identification of potential markets and buyers, insufficient access of imported inputs at competitive prices and use of inappropriate production technology.

•These factors affect the cost-competitiveness in the global market

•Concerns raised for a number of other factors: difficulty in meeting buyer’s standard, inadequate access to trade finance and high cost or delays caused by domestic transportation

•Positive changes were observed: technical standards, international transportation and business processes at international borders

15

Identification of Problematic Factors when Exporting

Rank 2011 2012

1 Burdensome import procedures (23.19) Burdensome import procedures(23.23)

2 Tariffs and non-tariff barriers (20.77) Tariffs and non-tariffs barriers (21.9)

3 Corruption at the border (17.14) Corruption at the border(18)

4 High cost or delays caused by domestic transportation (11.32) High cost or delays caused by domestic transportation (12.95)

5 High cost or delays caused by foreign transportation (10.33) Crime and theft (7.42)

6 Crime and theft (8.13) Domestic technical requirements and standards (7.33)

7 Domestic technical requirements and standards (7.47) High cost or delays caused by foreign transportation (6.85)

8 Inappropriate telecommunications infrastructure (1.65) Inappropriate telecommunications infrastructure (2.28)

•Top three most problematic factors for importing are: burdensome import procedures; tariff and non-tariff barriers; corruption at border points

•Positions are remained the same

•Two other major concerning factors were: crime and theft, domestic technical requirements and standards

16

Identification of Problematic Factors when Importing

17

V. Bangladesh’s Business Environment 2012

18

104

62

48 44

87

103

2

6

7

12

Perceptions on

Economy

2

9

9

16

0

12

2

4

5 5

4

9 9

6 2

10

1

4

1

3

4

7

Government and

Institutions Infrastructure

Innovation and

Technology

Financial Environment Foreign Trade and

Investment

Domestic

Competition

Company Operations and

Strategy

Education and

Human Capital

Corruption and Ethics Travel and Tourism Environment Health

Numbers of Positively Shifted Indicators Numbers of Negatively Shifted Indicators

Total Number of Questions 2010: 148 2011 : 149 2012 : 151

43

106

37

114

Optimistic Pessimistic

2010

2012

2011

2012

2011

2010

2011 2012

Comparison of Responses Between 2011 and 2012

Performance at a Glance

Factors Indicators Level of Improvement

Overall Perception on Economy

The threat of terrorism did not impose significant costs on business

Good > Better

Organized crime did not impose marginal costs on businesses

Bad > Good

Governance & Public Institutions

Level of taxes has somewhat no impact on incentives to work or invest

Bad > Good

Domestic Competition

High-quality, specialized training services are to some extent not available

Worse > Bad

Standards on product/service quality, safety and other regulations do not hinder competition in the country

Bad > Good

Travel and Tourism Foreign visitors are usually welcome in the country Better > Best

19

Improvements in Business Environment

Factors Indicators Level of decline

Governance & Public Institutions

Public trust in the ethical standards of politicians is very low (88%) Worse > Worst

Police services can not relied upon at all to enforce law and order (71%) Bad > Worse

Government subsidies and tax breaks is insignificantly distort competition (43%)

Good > Bad

Government’s efforts are moderately weak to address income inequality (68%)

Bad > Worse

Infrastructure Roads are underdeveloped Bad > Worse

Innovation & Technology

Businesses use a small scale internet for selling their goods and services for consumers (64%)

Good > Bad

Foreign direct investment (FDI) bring very few new technology in the country (45%)

Good > Bad

Financial Environment

It is difficult for entrepreneurs to find venture capital (90%) Worse > Worst

The regulation and supervision of securities exchanges are ineffective in the country ( 74%)

Bad > Worse

The level of sophistication of financial markets in the country is poor by international standards (68%)

Bad > Worse

The financial sector do not provide a wide variety of services (42%) Good > Bad

It is difficult to raise money by issuing shares on the stock market (44%) Good > Bad

20

Declines in Business Environment

Factors Indicators Level of Decline

Foreign Trade and Investment

It is to a certain extent difficult to obtain trade finance at affordable cost (42%)

Good > Bad

Domestic Competition

State-owned enterprises are favored over private companies in the country (47%)

Good > Bad

Company Operation and Strategy

The willingness to delegate authority to subordinates is low- top management controls all important decisions (74%)

Bad > Worse

Corporate governance management has little accountability to investors and boards of directors (40%)

Good > Bad

Production process mostly use labor-intensive methods or previous generations of process technology prevail (73%)

Bad > Worse

Corruption, Ethics and Social Responsibility

The judiciary is perhaps influenced by members of government, citizens or firms (75%)

Bad > Worse

Undocumented extra payments or bribes from one private firm to another to secure business is common (67%)

Bad > Worse

The corporate ethics of firms is not good in the country (70%) Bad > Worse

Undocumented extra payments or bribes made by firms for favorable judicial decisions are to some extent common (67%)

Bad > Worse

Health Cancer is a concern for company’s next five years profile (42%) Good > Bad

21

Declines in Business Environment

22

Level 2011 2012

Bad (-1.00 to -0.01)

1.Economic activity is to some extent undeclared or unregistered (43%).

2.Organized crime does not impose much significant costs on businesses (71%).

1. Economic activity is to some extent undeclared or unregistered (57%). National government is quite ineffective in managing major global risks (70%).

Good (0.00 to 1.00)

3. The economy will experience moderate growth in next 12 months (62%). 4. The incidence of common crime and violence imposes slight significant costs on businesses (53%). 5. The threat of terrorism does not impose much

significant costs on business (72%).

3. The economy will experience moderate growth in next 12 months (36%). 4. The incidence of common crime and violence does not impose much costs on businesses (56%) . Business-government relations is generally cooperative in the country (49%). 2. Organized crime impose slight significant costs on businesses (59%)

Better (1.01 to 2.0)

5. The threat of terrorism does not impose much significant costs on business (75%)

Overall Perception on the Economy

Improved positive remarks •There is a strong perception regarding marginal scope and minimum cost of the

threat of terrorism (1.23, 75% in 2012 vis-à-vis 0.33, 72% in 2011) • 59% businessmen mentioned that organised crime was to some extent less and did

not impose significant cost on businesses. Positive remarks •Perception on economic growth in 2012 has been weakened compared to that in 2011

(0.06, 36% in 2012 vis-à-vis 0.65, 64% in 2011) Negative remarks • 70% respondents mentioned that government’s initiative was somewhat less effective

in managing global risks during 2011 • 57% respondents criticized the undeclared/unregistered nature of major economic

activities

Level 2011 2012

Worst (-3.00 to -2.01)

2. Public trust in the ethical standards of politicians is very low (88%).

Worse (-2.00 to -1.01)

1.Economic policy-making is centralized - government controls almost all important decisions (84%)

2.Public trust in the financial honesty of politicians is low (90%)

3. When deciding upon policies and contracts, government officials favour well-connected firms and individuals (90%)

4.Intellectual property protection and anti-counterfeiting measures are moderately weak and not properly enforc(82%)

3. Government officials highly favoritism show to well connected firms and individuals when deciding upon policies and contracts(84%) .

The ability of politicians is very week to govern effectively (79%). 4. Intellectual property protection and anti-counterfeiting measures are

weak and properly enforced (77%) . 13. Government’s efforts are week to address income inequality(68%)

. 6. Police services can not relied upon at all to enforce law and

order(71%)

Government and Public Institution

Improved/Positively Remarked (see the following Table)

•Perception improved: 40% of respondents perceived that level of taxes to some extent has no adverse impact on incentives to work or invest (0.16 in 2012 vis-à-vis -0.33 in 2011)

•Possible impact of newly enacted tax laws needs to be assessed before starting their operation in 2015

•Positive but unchanged remarks: Agriculture policy somewhat balanced the interests of different stakeholders in 2012 (0.70 in 2011 and 0.74 in 2012): Preparation of the “National Agriculture Policy 2011” is well appreciated

• 75% respondents mentioned that press was relatively free though perception level has slightly decelerated (1.16, 75% in 2012 vs. 1.27, 79% in 2011)

• 83% perceived that access to online is somewhat free (last year: 75%) 23

2010-11: 115th 2011-12: 112th 2012-13: 127th

Level 2011 2012

Bad (-1.00 to -0.01)

5. The national Parliament is ineffective as a law-making institution (68%)

6. Police services cannot be relied upon to enforce law and order (59%)

7. The legal framework for private businesses to settle disputes and challenge the legality of government actions and regulations is moderately inefficient and subject to manipulation (58%)

8. The composition of public spending is wasteful (62%) 9. The level of taxes limits the incentives to work or invest (41%) 10. Complying with administrative requirements for business

required by the government is often burdensome (65%) 11. Obtaining information about changes in government policies and

regulations are impossible (64%) 12. Property rights, including over financial assets, are poorly defined

and not well-protected by law (51%) 13. The government's efforts to reduce poverty and address income

inequality are ineffective (50%) 14. The legal framework for private business in settling disputes is

moderately inefficient (61%).

Government reform are somewhat never implemented efficiently (68%).

5. The national Parliament is ineffective to some extent as a law-making

institution( 60%) . 8. The composition of public spending is quite wasteful (67%) . 14. The legal framework for private business in settling disputes is

moderately inefficient (63%). 10. Complying with administrative requirements for business by the

government is somewhat burdensome (63%) . 7. The legal framework for private business in challenging the

legality of government actions and regulations is moderately inefficient (56%) .

12. Property rights, including financial assets are not well-protected (52%) .

11. For business obtaining information about changes in government polices and regulations affecting their activities are quite impossible (49%) .

15. Government subsidies and tax breaks is insignificantly distort competition (43%) .

Good (0.00 to 1.00)

15. Government subsidies & tax breaks do not distort competition (62%)

16. Agricultural policy balances the interests of taxpayers, consumers and producers (56%)

9. The level of taxes relatively have no impact on incentives to work or invest (40%).

16. The agriculture policy to some extent balances the interests of taxpayers, consumers and producers.(63%)

Better (1.01 to 2.0)

17. The press is relatively free (79%) • Access to online information including press is free (75%)

17. The press is relatively free (75%) . 18. The access to online content is entirely free (83%) .

24

Government and Public Institution

2010-11: 115th 2011-12: 112th 2012-13: 127th

Negative but unchanged situation (see the Table in the previous page)

There was no improvement in the negative perception on the following issues:

•Government officials favoritism to well connected firms (-1.52, 84%) and wasteful public spending (-0.83, 63%)

• Ineffectiveness of national parliament as a law making institution (-0.91, 60%)

• Inefficient legal framework for government actions and regulations (56%) and weak protection of property rights (52%)

Negative perception deteriorated

•Public distrust over the politicians has increased significantly (-2.01, 88%),

•Government subsidies was perceived to be somewhat distortive for competition and perception level was declined from positive to negative (0.02 in 2011 vis-à-vis -0.05 in 2012 )

•Huge amount of petroleum supply at subsidised rate in the rental power plants has a major disconcerting factor in the subsidy management

•68% respondents mentioned that income inequality was not adequately addressed in Government’s initiatives during 2012 (-1.16 in 2012 vis-à-vis -0.37 in 2011)

•71% perceived that police service can not be relied upon to enforce law and order, and the perception has further declined in 2012 (-1.11 vis-à-vis –0.75 in 2011)

25

Government and Public Institution

2010-11: 115th 2011-12: 112th 2012-13: 127th

Level 2011 2012

Worst (-3.00 to -2.01)

1. The quality of electricity supply (lack of interruptions and voltage fluctuations) is poor (100%)

1. The quality of electricity supply ( lack of interruptions and lack of voltage fluctuations) is insufficient and suffers frequent interruptions (94%) .

Worse (-2.00 to -1.01)

2. General infrastructure of the country is underdeveloped (79%)

3. Railroads are underdeveloped (83%)

3. The railroad system is underdeveloped (78%) . 2. General infrastructure (e.g. transport, telephony and energy) is

underdeveloped (80%) . 4. Roads are underdeveloped (74%) .

Positive but unchanged remarks (see Table in the following page) •Air transport network in case of providing connections to overseas markets and for offering new businesses was positively remarked by 42% respondents (0.05 in 2012 vis-à-vis 0.21in 2011)

Negative but unchanged remarks •Quality of electricity supply was perceived to be worst (94%) though marginal

improvement in the perception level was observed (-2.07 in 2012 vis-à-vis -2.39 in 2011)

•Marginal rise in the electricity supply despite huge investment with upward revision of electricity tariff for several times; allowing to set up rental power plant to supply electricity at high cost caused huge burden of ‘excess subsidy’ and ‘crowd out’ effect to the private sector

•Over 70% respondents have ‘worse’ remarks as regards condition of the infrastructure including railroads (78%) and ground transport network (71%)

• ‘Bad’ remarks by 50% respondents regarding port facilities and air transport infrastructure.

26

Infrastructure

2010-11: 133rd

2011-12: 134th 2012-13: 134th

Level 2011 2012

Bad (-1.00 to -0.01)

4. Roads are underdeveloped (69%) 5. Port facilities & inland waterways are underdeveloped (70%)

6. Passenger air transport is underdeveloped (50%) 7. National ground transport network (buses, trains, taxis, etc.)

offer transportation to a wide range of travellers to key business centres and tourist attractions within the country which is somewhat inefficient (54%)

8. The country's postal system cannot often be sufficiently trusted to have a friend mail a small package worth US$100 (54%)

7. National ground transport network (buses, trains, trucks, taxis, etc. ) offer somewhat inefficient transportation within country (71%) .

The changes between different modes of transport (e.g. from port to rail or airport to roads) are quite inefficient (55%).

8. The country’s postal system can not often be sufficiently trusted to have a friend mail a small package worth US$100 (56%) .

5. Port facilities are underdeveloped and inefficient by international standards (54%) .

6. Air transport infrastructure is not developed enough (50%) .

Good (0.00 to 1.00)

9. The air transport network does offer good connections to some key business markets (56%)

10. New telephone lines for business are available and quite reliable (61%)

9. The air transport network provide quite well connections to the overseas markets offering the greatest potential to the country’s business (42%) .

Deteriorated negative remarks

• 74% respondents perceived that quality of roads and highways has gone down to “worse” level (-1.28 in 2012 vis-à-vis -0.93 in 2011).

• Slow progress in the implementation of major large scale highway projects, poor maintenance and delayed repair works of highways and district level roads caused less smooth traffic.

27

Infrastructure

2010-11: 133rd

2011-12: 134th 2012-13: 134th

Positive remarks

•Bank’s balance sheets although remarked as good but the perception was relatively weak compared to the last year (0.57, 59% in 2012 vis-à-vis 0.90, 71% in 2011).

Unchanged negative remarks

•Weak financial governance caused adverse consequences in both money and capital markets.

•Money market: access to credit (-1.65, 77%) perceived to be difficult: ‘Crowd-out’ effect and collapse of the stock market in December, 2010

Level 2011 2012

Worst (-3.00 to -2.01)

2. It is difficult for entrepreneurs with innovative but risky projects to find venture capital (90%)

Worse (-2.00 to -1.01)

1. It is often impossible to obtain a bank loan with only a good business plan and no collateral (72%) 2. Entrepreneurs with innovative but risky projects do

not often find venture capital (82%)

1. It is difficult to obtain bank loan with only a good business plan and no collateral (77%) .

5. The regulation and supervision of securities exchanges are ineffective in the country( 74%).

There are significant price bubbles: assets are overvalued (71%). 3. The level of sophistication of financial markets in the country is poor by

international standards (68%) .

28

Financial Environment 2010-11: 66th

2011-12: 67th 2012-13: 95th

Level 2011 2012

Bad (-1.00 to -0.01)

3. The level of sophistication of financial markets is somewhat poor by international standards (50%)

4. During the past year, obtaining credit for company has become difficult (41%)

5. Regulations of securities exchanges is not transparent, effective and independent of undue influence from industry and government (67%)

6. Financial auditing and reporting standards regarding company financial performance are weak (40%)

7. Interests of minority shareholders in the country are not protected by law (52%)

8. Competition among providers of financial services is not ensure the provisions of financial services at affordable prices(37%).

7. The interests of minority shareholders are somewhat not protected by the legal system(70%) .

To obtain financing for business development is difficult in the country( 60%).

8. Competition among providers of financial services is not ensure the provisions of financial services at affordable prices(54%).

6. Financial auditing and reporting standards regarding company financial performance is relatively week (48%) .

9. The financial sector do not provide a wide variety of financial products and services to business(42%) .

11. It is quite difficult to raise money by issuing shares on the stock market (44%) .

Good (0.00 to 1.00)

9. The financial sector provides a number of financial products and services to business. (43%)

10. Banks are somewhat healthy with sound balance sheets (71%) 11. Raising money by issuing shares on the stock market is sometimes

possible for a good company (50%)

10. Banks in the country is to some extent healthy with sound balance sheets( 59%) .

Deteriorated negative perception

•Capital market: main consequences are related to weak interests in protecting minority shareholders (-1.00, 70%), poor financial auditing and reporting( -0.40, 48%), overvalued assets and significant price bubbles (-1.05, 71%)

• Overhauling of the capital market is urgently required

• ADB project for strengthening the capital market should be properly implemented

29

Financial Environment 2010-11: 66th

2011-12: 67th 2012-13: 95th

Deteriorated negative perception

• Finding venture capital for entrepreneurs with innovative but risky projects became harder than before (-2.06 in 2012 vis-à-vis -1.64 in 2011)

• Perception regarding the sophistication of the financial market has declined due to weak performance on number of accounts.

• Sophistication in financial markets was remarked as poor and the perception on it was deteriorating (-1.01, 68% in 2012 vis-à-vis -0.44, 50%)

• Regulation and supervision of securities were perceived to be ineffective and deteriorating (-1.29, 74% in 2012 vis-à-vis -0.97, 67% in 2011)

• Financial products and services are few and is remarked as in adequate for businesses (-0.17, 42% in 2012 vis-à-vis 0.10, 43% in 2011)

• Weak financial governance, poor monitoring and supervision of the regulatory authority and lack of adequate political commitment towards addressing the anomalies in the financial sector have become persistent challenges for efficient operation of the financial sector.

30

Financial Environment 2010-11: 66th

2011-12: 67th 2012-13: 95th

Unchanged negative remarks

•Government initiatives towards enforcement of environmental regulation are quite inadequate

• Both environmental regulations and their enforcement were perceived to be lax (-0.88, 63%) and (-1.24, 77%) in 2012

• 67% respondents mentioned that development environment is not friendly and perception on it has declined (-0.93 in 2012 vis-à-vis -0.32 in 2011).

• Quality of natural environment is quite poor (-0.37, 51%).

•An in-depth analysis is required with regard to understanding poor environmental standard and improvement of environmental compliance in the country.

•This may related with understanding the reasons for unwillingness of the private sector to be compliant with environmental rules, requirement of support for implementing the rules and regulatons, institutional weakness for enforcement of environmental rules and possible alternate mechanism to ensure environmental standards.

Level 2011 2012

Worse (-2.00 to -1.01)

1. Enforcement of environmental regulation is lax (75%) 1. Enforcement of environmental regulation is lax (77%) .

Bad (-1.00 to -0.01)

2. Environmental regulation is lax (57%) 3. Environmental challenges have negative impact on business

operations or local business expansion (52%) 4. The natural environment is polluted (50%) 5. Country’s development is not sustainable (49%)

5. Country’s development is not environmentally sustainable (67%) 2. Environmental regulation is lax (63%) . 4. The quality of natural environment is poor (51%) .

31

Environment

Other Issues

• For details on other issues please see the annex.

• The annex include following issues with elaborate :

• Innovation and Technology

• Foreign Trade and Investment

• Domestic Competition

• Company Operations and Strategy

• Human Capital and education

• Health

• Corruption, Ethics and Social Responsibility

• Travel and Tourism

32

33

VI. Findings from Rapid Assessment Survey

Level 2011 2012

Worse (-2.00 to -1.01)

1. Inflation is one of the top most challenges for Bangladesh in 2011 (83%)

2. Supply of gas will not increase significantly in 2010 (82%) 3. Government’s initiatives to enhance generation of electricity/gas are

not adequate (75%) 4Government’s efforts to combat the rising of food prices are ineffective

(74%) 5Monitoring and supervision system of the SEC is inefficient (76%) 6Inflation is one of the a top most challenges in 2011 (83%) ’ 7Government has not properly flagged the climate change issues both at

home and abroad (38%) 8. Insider trading in stock market is pervasive (80%)

5. The monitoring & supervision system of the SEC to regulate the market is inefficient (88%) . 8. Insider trading in Bangladesh's stock market is pervasive (80%) . Government's macro economic management during 2011 is not good (75%). 2. The supply of gas was not increase significantly in 2011 (70%) 4. Governments efforts to combat against the rising food prices are ineffective (72%) . Availability of bank credit in 2011 compared to the previous years is difficult to get (72%). The impact of current devolution of Taka against US dollar on business is bad (67%).

Bad (-1.00 to -0.01)

9. Supply of electricity will not increase significantly in 2011 (61%) 10. Investment environment in 2011 to some extent will deteriorate ( 36%) 11. Development of ‘Industrial relations’ is mainly related with reducing labour unrest in the industrial sector (43%) 12. Government’s initiatives in the last two years were inadequate to

build Digital Bangladesh by 2021 (62%) 13. Corporate tax structure is somewhat not so conducive for higher level

of investment (48%) 14. Rules and regulation regarding capital market is inadequate (59%) 15. Money laundering through the formal banking system is somewhat

pervasive (45%)

The government's effort to reduce industrial pollution is ineffective (67%). 10. The investment environment in Bangladesh in 2012 will deteriorate

further. (57%) 9. Electricity supply for industrial activities is not improved (54%) . Bangladesh tax system is complex. (56%) 12. Governments initiatives in the last three years were inadequate to build

digital Bangladesh by 2021. (57%) The draft value Added Tax Act 2011 is unfriendly to business (45%). The proposed Direct taxes Code bill 2012 will not reduce the practice of

tax evasion (40%) Indian's recent measure to provide duty free market access is insignificant

(46%).

Good (0.00 to 1.00)

16. PPP would be one of the major ways of investment in the infrastructure sector (52%)

15. Money laundering through the formal banking system in Bangladesh is somewhat rare (43%). Impact of changes in the EU-GSP scheme on Bangladesh's economy will be

positive (38%).

34

Rapid Assessment Survey 2012

• 43% respondents perceived that money laundering through banking system has declined (0.028) : This is happened due to various initiatives undertaken by the government.

• Lack of improvement in infrastructure facilities has remained a major concern.

• 70% mentioned about no improvement in gas supply (-1.22); 54% opined about scarcity in the supply of electricity (-0.65)

• 57% perceived that investment environment in the country has deteriorated (-0.71)

More than 75% respondents expressed their concerns about weak macroeconomic management in 2011 (-1.22)

• 72% expressed their concerns with regard to difficulty in getting credit (-1.11)

• Fluctuation of Taka against US dollar was a concern to 67% respondents

• 72% respondents mentioned that government could not handle the inflation situation properly (-1.19)

• Most of the problems in the capital market was unresolved. This is evident in:

• Inefficient supervision to regulate the capital market (88%, -1.86 )

• Pervasive insider trading in stock market (80%, -1.39)

• Entrepreneurs expressed mixed reaction regarding a number of issues

• Draft VAT Act is perceived to be somewhat unfriendly to business (45%,-0.31)

• 40% thought that proposed Direct Taxes Code Bill 2012 may not reduce the practice of tax evasion (-0.27)

• 46% respondents mentioned that duty free access to Indian market may not significantly contribute to rise Bangladesh’s export (-0.20)

• The new rules of origin under the EU-GSP scheme would positively contribute to Bangladesh economy (50%, 0.42)

35

Rapid Assessment Survey 2012

• Entrepreneurs mentioned that production cost has significantly increased in

July 2011 to December 2011 compared to July 2010 to December 2010

(High: 57% vs. 26%) mainly because of high inflation.

• High interest rate for borrowing bank loan has escalated production cost of

firms during July 2011-December 2011 compared to the same period of the

last year ( High: 47.6% vs. 17.6%) . 36

Rapid Assessment Survey 2012

Effect of Inflation and Bank Lending Rates on Production of Surveyed Firms

0

10

20

30

40

50

60

Jul 2010 - Dec 2010 Jul 2011 - Dec 2011 Jul 2010 - Decr 2010 Jul 2011 - Dec 2011

Inflation Lending Rate

pe

rce

nt

High medium low none

• Adverse business environment has affected businesses in other ways

• Rise of employment in the firms was slower in 2011 compared to that in 2010 (High: 2% in 2012 vs. 5% in 2011)

• About 20% of businessmen mentioned that employment in their firms has decreased in 2011

• Similarly, production in the surveyed firms has slowed down in 2012 (high: 4.5% in 2012 vs. 9.1% in 2011)

• More than 10% respondents mentioned that production in their firms has declined in 2011

37

0

10

20

30

40

50

60

70

July 2010 - December 2010 July 2011 - December 2011

Pe

rce

nt

Increased Decreased Unchanged

0

10

20

30

40

50

60

70

80

90

July 2010 - December 2010 July 2011 - December 2011

Pe

rce

nt

Increased Decreased Unchanged

Rapid Assessment Survey 2012

Changes in Number of Employees

Changes in Production

38

VII. Concluding Remarks

• Major fall in the rankings were in case of: financial market sophistication (28 ranks), macroeconomic stability (25 ranks), labour market efficiency (17 ranks), institutions (15 ranks) and business sophistication (10 ranks)

• Weaknesses observed in every accounts: basic requirements, efficiency enhancers and innovation and sophistication

• Bangladesh’s exceptionally better performance in financial market and labour market in the earlier years has been gradually eroded.

• Performance was found relatively better in case of market size (among the mid-level economies)

39

3.3

3.35

3.4

3.45

3.5

3.55

3.6

3.65

3.7

3.75

3.8 90

95

100

105

110

115

120

2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

Sco

re

Ran

k

GCI Rank GCI Score • Bangladesh’s largest fall in the global ranking in a single year

• From 108 to 118 (10 ranks and loss of 2.14% points)

• Some South Asian countries have similar experiences (Sri Lanka)

• It indicates that Bangladesh is loosing its competitiveness and it has started to move in reverse direction from a slow and steady improvement over the last several years.

Concluding Remarks

40

• Top three problematic factors for doing business included lack of access to finance for the first time along with the problems of poor infrastructure and prevalence of corruption.

• The weakness of public institutions has been further exposed in 2012: weak subsidy management, unreliable police services and failure to address income inequality issues

• Financial market was at a disastrous state in 2011: deterioration in the sophistication in bank’s performance, weak monitoring and supervision of banking and security markets, difficulty in getting loan

• Development of human resources has made marginal progress

• Corruption has been more widespread in 2011 • Undocumented payment was prevalent which ranked Bangladesh at the last

position

• Lax environmental rules and its enforcement of rules and regulations • An in-depth analysis is required to understand the major constraints for

ensuring better environmental compliances in the industrial sector

Concluding Remarks

• Government should take proper measures to regain its competitive strengths particularly in macroeconomic management and efficiency in financial market.

• A number of specific measures need to be taken up:

• Macroeconomic policy for long term stability

• Restore discipline in the financial sector

• Improve efficiency of public institutions

• Take bold political steps against corruption

• Timely implementation of infrastructure related projects and try to ensure maximum return from those projects

41

Concluding Remarks

Thank you!

42

43

VIII. Annex

Level 2011 2012

Worse (-2.00 to -1.01)

1. Internet access in schools is very limited (77%) 2. Scientific research institutions are minimal (81%) 3. In the area of R&D, collaboration between the business community

and local universities is minimal (90%) 4. A failed entrepreneurial project is considered an embarrassment

(69%) 5. Government procurement decisions do not result in technological

innovation (78%)

2. The quality of scientific research institutions are minimal (79%) . 5. Government procurement decisions don not foster innovation.(75%) 1. The level of access to the Internet in schools is very limited (74%) . 4. A failed entrepreneurial project is considered an embarrassment

.(75%) 3. On research and development (R&D), business and universities do not collaborate.(71%) The government do not continuously improve its provision of services to help business in the country boost their economic performance. (70%)

Positive Remarks (see Table after the next slide):

•Respondents shared positive remarks on some issues as like in the last year

Considerable use of virtual social networks for professional & personal communication (0.41 in 2012 vis-à-vis 0.49 in 2011) ; similarly, use of ICTs for communicating and carrying out transactions (0.15)

Positive remarks on use of new (0.21) and available latest technologies ( 0.18)

Over 50% respondents perceived that government is to some extent successful in promoting the use of ICT (0.31)

44

Innovation and Technology

2010-11: 119th

2011-12: 122nd 2012-13: 130th

Level 2011 2012

Bad (-1.00 to -0.01)

6. ICT poorly improving access for all citizens to basic services (50%) 7. Online government services such as personal tax, car registrations,

passport applications, business permits and e-procurement are unavailable (70%)

8. ICT creating very few new business models, services and products in the country (38%)

9. ICT creating very few organizational models within businesses in the country (52%)

10. The government does not have a very clear implementation plan for utilizing information and communication technologies for improving the country's overall competitiveness (44%)

11. The use of ICT by the government has not improved the efficiency of government services (47%)

12. Laws relating to the use of information technology (e-commerce, digital signatures, consumer protection) are non existent (68%)

13. Digital content in the country is not accessible via multiple platforms (39%)

14. Collaboration among firms, suppliers, partners and associated institutions within clusters is non-existent (52%)

12. Laws relating to the use of ICT (e.g. electronic commerce, digital signatures, consumer protection) is quite underdeveloped. (51%)

14. Collaboration among firms (e.g. suppliers, competitors, clients) in order to promote knowledge flows and innovation is non-existent. (52%)

The existing internet bandwidth capacity limits businesses to perform their activities or embark on new business opportunities. (67%)

18. Businesses use a small scale internet for selling their goods and services for consumers (64%) .

The licensing of foreign technology is not common enough (51%). 9. ICT do not create new organizational models (e.g. virtual teams,

remote working, telecommuting) within businesses (52%) . 11. ICTs by the government do not improve the quality of government

services to citizens sufficiently (49%) . 13. Digital content to some extent is not accessible (50%) . The internet do moderately increase the sales of business and

allowing to access new customers (52%). 6. ICTs poorly improving access for all citizens to basic services (48%) .

8. ICT creating very few new business models, services and products in the country (47%) .

16. Foreign direct investment (FDI) bring very few new technology in the country (45%) .

New companies with new ideas do not grow significantly (41%). 10. The government do not have a clear implementation plan for

utilizing ICTs to improve country’s overall competitiveness (40%) .

45

Innovation and Technology

2010-11: 119th

2011-12: 122nd 2012-13: 130th

Level 2011 2012

Good (0.00 to 1.00)

14. The latest technologies are largely available and used (47%) 15. Companies are able to absorb new technology (57%) 16. FDI in the country is an important source for new technology (46%)

17. ICT are an overall priority for the government (60%) 18. Companies use the internet extensively for buying and selling

goods, and for interacting with customers and suppliers (57%) 19. Virtual social networks (Facebook, Twitter, Linkedin etc.) for

professional & personal communication are used. (56%)

ICTs use for communicating and carrying out transactions with other business is good in the country (48%) .

14. The latest technologies in the country is quite available (50%) . 15. Businesses absorb new technology largely (50%) . In promoting the use of ICTs government is quite successful (53%). 19. The use of virtual social networks (e.g. Facebook, Twitter, Linkedln

) is used for professional and personal communication (56%) .

Unchanged Negative Remarks (see the last Table):

• No change in the negative remarks about institutional, governance and infrastructure related issues for ICT development.

• Less progress in case of development of ICT related laws in 2012 (-0.93, 51%) vis-a-vis in 2011(-0.94, 68%)

• Minor utilisation of ICT in government services in 2012 (-0.44,49%) vis-a-vis in 2011 (-0.37, 47%)

• Marginal changes in case of access to ICT for all citizens to basic services (-0.20, 48%) .

• Insufficient public spending for ICT development: Difficult to achieve the goal of ‘Digital Bangladesh’ by 2021

• Less spending on R&D, brain drain of talented people and neglecting the issues regarding science and technology halted the progress of innovation and technology:

• Poor quality of research institution (-1.41, 79%)

• Unfavourable and uncompetitive procurement decisions to foster innovation (-1.35, 75%)

• Lack of collaboration among private sector and universities on R&D related issues (-1.32,71%)

Deteriorated Negative Remarks

• Limited use of internet for selling goods and services (-0.47, 64%): Replicate the ‘good’ examples

• Less evidence of bringing new technology through FDI (-0.07, 45%) 46

Innovation and Technology

2010-11: 119th

2011-12: 122nd 2012-13: 130th

Level 2011 2012

Bad (-1.00 to -0.01

1. Foreign ownership of companies is rare (50%) 2. Customs procedures are often slow and cumbersome (89%)

1. Foreign ownership of companies is rare (63%) 2. The level of efficiency of customs procedures are

moderately inefficient in the country (67%) . The predictability and clarity of import regulations is

quite opaque and uncertain (51%). 4. It is to a certain extent difficult to obtain trade finance

at affordable cost (42%).

Good (0.00 to 1.00)

3. Tariff and non-tariff barriers sometimes does not significantly reduce the ability of imported goods to compete in the domestic market (42%)

4. To obtain trade finance at affordable cost is not much difficult. (41%)

3. Non-tariff barriers do not limit the ability of imported goods to complete in the domestic market (44%)

Better (1.01 to 2.0)

5. Rules governing foreign direct investment are moderately beneficial and encourage foreign direct investment (62%)

5. Rules governing foreign direct investment are moderately encourage foreign direct investment (FDI) (64%)

Positive Remarks

• 64% respondents mentioned that rules regarding FDI are favourable for encouraging new investment (1.04 in 2012 vis-à-vis 1.01 in 2011).

• 44% respondents commented that tariff and NTBs do not limit the ability of imported goods to complete in the domestic market (0.14 in 2012 vis-à-vis 0.15 in 2011)

• Rising supplementary duties and other taxes at import stage in recent years could be a concern for the imported products. Application of supplimentary duties and taxes should be justified on logical grounds and should be time bound.

Unchanged Negative Remarks

• Exporters and importers face various kinds of constraints due to poor logistical support and high cost associated with it.

• 67% respondents mentioned the existing customs procedures as inefficient (-0.66 vis-à-vis -0.46 in 2011)

• 51% respondents maintained that import regulations are remarked as unclear and unpredictable (-0.33 ).

Deteriorated Negative Remarks

• Trade finance at affordable cost was considered to be difficult to 42% respondents (-0.11 vis-à-vis -0.12 in 2011 )

47

Foreign Trade and Investment

Level 2011 2012

Worse (-2.00 to -1.01)

1. Process equipment and machinery are mostly imported (87%) 2. Specialized research and training services are not available in the

country (82%)

Bad (-1.00 to -0.01)

3. Buyers make purchasing decisions mainly based on the lowest price (69%)

4. Standards on product/ service quality, energy & other regulations are lax (61%)

5. Anti-monopoly policy is lax and ineffective at promoting competition (56%)

6. Corporate activity is dominated by a few business groups (70%) 7. Well developed and deep clusters in the economy are rare or absent

(37%) 8. Formal policies to support cluster development are non-existent

(53%)

6. Corporate activity is dominated by a few business groups (71%) . 2. High-quality, specialized training services are not available enough

(67%) . 3. Buyers make purchasing decisions based on the lowest price (65%) .

5. Anti-monopoly policy to some extent does not promote competition in the country (46%) .

7. Well-developed and deep clusters is quite non-existent (41%) . 13. State-owned enterprises are favored over private companies in the

country (47%) .

48

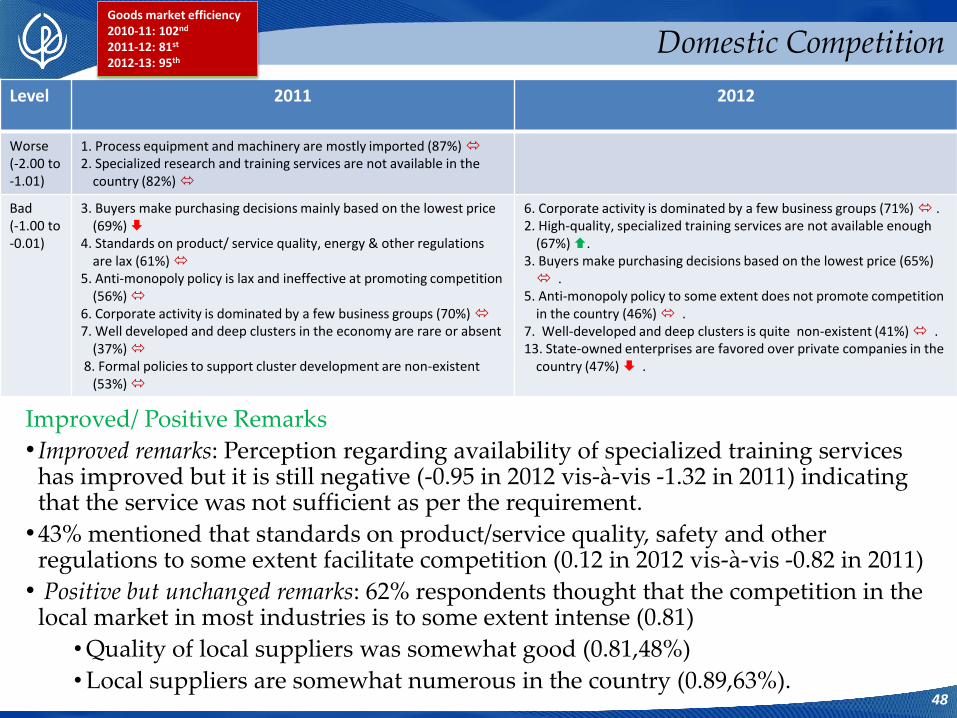

Goods market efficiency 2010-11: 102nd 2011-12: 81st 2012-13: 95th

Domestic Competition

Improved/ Positive Remarks

• Improved remarks: Perception regarding availability of specialized training services has improved but it is still negative (-0.95 in 2012 vis-à-vis -1.32 in 2011) indicating that the service was not sufficient as per the requirement.

•43% mentioned that standards on product/service quality, safety and other regulations to some extent facilitate competition (0.12 in 2012 vis-à-vis -0.82 in 2011)

• Positive but unchanged remarks: 62% respondents thought that the competition in the local market in most industries is to some extent intense (0.81)

•Quality of local suppliers was somewhat good (0.81,48%)

•Local suppliers are somewhat numerous in the country (0.89,63%).

Level 2011 2012

Good (0.00 to 1.00)

9. Competition in the local market is intense in most industries (51%)

10. Local suppliers are numerous and include the most important materials, components, equipment and services (51%)

11. The quality of local suppliers is good (42%) 12. State-owned enterprises have little role in the economy (54%) 13. State-owned enterprises are not favored over private sector

competitors (39%) 14. Starting a new business is easy (41%)

4. Standards on product/service quality, safety and other regulations do not hinder competition in the country (43%) .

11. The quality of local suppliers is quite good (48%) . 9. The competitions in the local market is intense in most industries

(62%) . 10. Local suppliers are numerous in the country (63%) .

49

Domestic Competition Goods market efficiency 2010-11: 102nd 2011-12: 81st 2012-13: 95th

Unchanged negative remarks

• A large number of respondents however considered the domestic competition at an early stage.

• 71% respondents mentioned about dominance of few business groups in the corporate activity (-0.98)

• 65% respondents noted that buyers’ purchasing decision was led by lowest price of the product (-0.91)

• 41% commented about lack of well-developed and deep clusters in the country (-0.13)

• Anti-monopoly policy has yet to promote competition though perception regarding the issue has improved this year( -0.44 in 2012 vis-à-vis -0.66 in 2011): Establishment of the Competition Commission is immediately needed

• Government’s stance regarding the state owned enterprises over private enterprises has been negatively remarked by 47% respondents (-0.01 in 2012 vis-à-vis 0.09 in 2011).

• Performance of most of the state-owned enterprises was not satisfactory despite various kinds of support for improving their competitiveness.

Level 2011 2012

Worse (-2.00 to -1.01)

1. Competitiveness of companies in international markets is primarily due to low cost or local natural resources (82%)

2. Exports to neighboring countries are limited (85%) 3. Companies do not spend money on R&D (88%) 4. Companies often technology exclusively from licensing or imitating

foreign companies (85%) 5. Management compensation is based on fixed salaries (78%)

1. Competitive advantage of companies in international market is based upon low-cost or natural resources (81%) .

4. Companies obtain technology from licensing or imitating foreign companies (83%) .

3. Companies do not spend money on R&D (79%) . 11.The willingness to delegate authority to subordinates is low- top

management controls all important decisions (74%) . 5. Management compensation do not based on performance rather

than fixed salaries (75%) . 8. Production process mostly use labor-intensive methods or previous

generations of process technology prevail (73%) .

Unchanged negative remarks

• Company operations were adversely affected due to weaknesses in the management and marketing related issues, lack of skilled manpower and underdevelopment of value chain etc.

• 81% respondents referred to resource or labour-based competitiveness as weak and unsustainable (-1.51)

• 83% respondents remarked about imitating or licensing foreign technologies as the source for obtaining technologies (-1.48)

• 56% criticised insufficient use of marketing tools and techniques for sales( -0.69)

• 60% stated companies’ limited involvement in the value chain as their weakness (-0.56)

• More than half of the respondents expressed their concerns regarding very few introduction of models, structures and designs (-0.69, 56%)

• 75% respondents maintained that employee’s performance is less appreciated while fixing compensation (-1.11) 50

2010-11: 105th 2011-12: 98th 2012-13: 108th

Company Operations and Strategy

Level 2011 2012

Bad (-1.00 to -0.01)

6. Exporting companies are primarily involved in individual steps of the value chain (56%)

7. Exporting companies sell primarily in a small number of foreign markets (61%)

8. Production processes mostly use labour-intensive methods or previous generations of process technology (71%)

9. The extent of marketing is limited and primitive (59%) 10. International distribution & marketing takes place through foreign

companies (48%) 11. Willingness to delegate authority to subordinates is low - top

management controls all important decisions (69%) 12. Senior management positions are held by usually relatives without

regard to merit (46%)

9. Companies use a little sophisticated marketing tools and techniques (56%) .

Companies do not introduce new business models, organizational structures or designs that allow them to differentiate their goods in the market (60%).

6. Exporting companies have a narrow, primarily involved in individual steps of the value chain (60%) .

12. Senior management positions are held by usually relatives or friends without regard to merit (54%) .

10. International distribution and marketing not at all owned and controlled by domestic companies (48%) .

14. Corporate governance management has little accountability to investors and boards of directors (40%) .

Good (0.00 to 1.00)

13. Firms are responsive to customers and customer retention (53%) 14. Corporate governance by investors & boards directors is

characterized to some extent by management with little accountability (47%)

13. Companies are responsive to customers and seek customer retention (46%) .

Deteriorated negative remarks • 74% respondents mentioned about excessive control of the top management in the

decision making process and it was increasing (-1.21) •Use of outdated technologies in the operation was high and perception level has declined

in 2012 as perceived by 73% respondents ( -1.03) • 40% mentioned that accountability between investors and boards was marginal and it has

declined in 2012 (-0.11) Positive remarks • 46% respondents thought that companies are responsive to customers and seek customer

retention though the level of perception decreased this year (0.16 in 2012 vis-à-vis 0.59 in 2011).

51

Company Operations and Strategy 2010-11: 105th 2011-12: 98th 2012-13: 108th

Level 2011 2012

Worse (-2.00 to -1.01)

1. Formal social safety net not at all provide protection from economic insecurity in the event of job loss or disability (91%).

2. Primary schools are of poor quality (80%) 3. Talented people leave to pursue opportunities in other countries

(75%)

1. Formal social safety net not at all provide protection from economic insecurity in the event of job loss or disability (82%).

3. Talented people leave to pursue opportunities in other countries (70%) .

2. Primary schools are of poor quality (73%) .

Bad (-1.00 to -0.01)

3. The educational system often does not meet the needs of a competitive economy (62%)

4. Math & science education in the schools lags far behind many other countries in the world (74%)

5. Management or business schools are limited or of poor quality (43%)

6. Scientists & engineers are not widely available (46%) 7. Pay is not related to worker productivity (51%) 8. Labour regulation prevents the companies from employing foreign

labour (55%) 9. The general approach of companies to human resources is to invest

little in training and employee development (71%) 10. For similar work, wages for women are below those of men (43%)

9. Companies invest a little in training and employee development (68%) .

4. The quality of math and science education is relatively poor in the country’s school (62%) .

3.The educational system not well enough in meet the needs of a competitive economy (61%) .

8. Labour regulation to some extent limits the ability to hire foreign labour (52%) .

7. Pay is somewhat unrelated to worker productivity (45%) . 6. Scientists and engineers are rather unavailable in the country (52%) .

10.For similar work, wages for women are not equal always those of men (52%) .

5. The quality of management or business schools is relatively poor in the country (44%) .

Positive remarks (in the next table)

•Respondents maintained their positive views with a number of issues: employer-worker relations (0.40,51%), opportunities for women in business leadership (0.04, 40%), wages determination by individual companies (0.72,64%) and flexibility in hiring and firing of workers ( 0.69,63%).

52

2010-11: 106th

2011-12: 108th 2012-13: 103rd Human Capital and Education

Level 2011 2012

Good (0.00 to 1.00)

11. The hiring and firing of workers is flexibly determined by employers (63%)

12. Labor-employer relations are generally cooperative(43%) 13. Wages are fixed by each individual company (75%) 14. Businesses provide women with the same opportunities as men to

rise to positions of leadership (43%)

14. Business provide women equal opportunities for positions of leadership (40%) .

12. Labor-employer relations is generally cooperative (51%) . 11. The hiring and firing of workers is flexibly determined by employers

(63%) . 13. Wages are set up to each individual company (64%) .

Unchanged negative remarks (see the table of the last page) •The development of education system requires significant changes on a number of

accounts: • 61% respondents mentioned about backward education system with regard to meeting

the need of competitive economy (-0.69) • About two-third respondents mentioned about poor quality of primary schools

(-1.16,73%); similar view as regards below the average quality of math and science education (-0.74, 62%)

• Scarcity of scientists and engineers (-0.24, 52%) and low quality of management or business schools (-0.16, 44%) suffered businesses to get adequate supply of skilled professionals

•Companies faced constraints due to lack of development of human resources in the country • Marginal investment in training and employee development (-0.94, 68%) • Weak link between wage and productivity (-0.31, 45%) • Somewhat unequal wages for female against male workers (-0.18, 52%) • Talented people left the country to pursue opportunities in other countries (-1.21,73%)

• Social safety net yet to provide protection to all from economic insecurity (-1.79, 82%)

53

Human Capital and Education 2010-11: 106th

2011-12: 108th 2012-13: 103rd

Level 2011 2012

Worse (-2.00 to -1.01)

1. Quality of healthcare provided for ordinary citizens is poor(83%)

2. Healthcare is mostly accessible among elites (69%)

Bad (-1.00 to -0.01)

3. Healthcare delivery is largely fragmented among physicians, clinics and hospitals (81%)

4. Heart disease and related cardio vascular problems are minor problems (53%)

5. Employees do not take advantage of the policies and/or programmes implemented (37%)

6. Diabetes does not impact seriously (49%)

6. A serious impact of the Diabetes will have on company’s in the next five years (55%) .

4. A serious impact of the Heart disease and related cardiovascular problems will have on company’s in the next five years (60%) .

5. A typical employee health care needs are not met by company (43%) . A serious impact of the Chronic respiratory will have on company’s in the

next five years (51%). 8. A serious impact of Cancer will have on company’s in the next five years

(42%) .

Good (0.00 to 1.00)

7. Mental illness does not impact seriously (61%) 8. Cancer does not impact seriously (50%)

7. A less impact of mental illness will have on company’s in the next five years (64%)

Better (1.01 to 2.0)

9. Tuberculosis does not impact seriously (61%) 10. HIV/AIDS is not affecting business operations (77%)

11. Malaria does not impact seriously (70%)

9. A smaller impact of the tuberculosis will have on company’s in the next five years (66%) .

11. A minor impact of the malaria will have on company’s in the next five years (68%) .

10. A negotiable impact of the HIV/AIDS will have on company’s in the next five years (74%) .

Unchanged negative remarks

Respondents have expressed their concerns about a number of health related issues.

• Prevalence of diabetes (-0.68, 55%), heart diseases (-0.65,60%) and chronic respiratory diseases (-0.15,51%) would have adverse impact on company’s performance in the next five years.

Deteriorated negative remarks

• 42% respondents expressed their concerns with regard to cancer among employees in 2012 (-0.11). 54

Health

Level 2011 2012

Worst (-3.00 to -2.01)

1. Undocumented extra payments or bribes made by firms for annual tax payments are common (94%)

1.Undocumented extra payments or bribes made by firms connected with annual tax payments are very common (88%) .

Worse (-2.00 to -1.01)

2. Domestic firms paying bribes to public servants or public officials are common (87%)

3. The government‘s effort combat corruption is unsuccessful (76%)

4. Diversion of public funds to companies, individuals or groups due to corruption is common (85%)

5. Undocumented extra payments or bribes made by firms for import and export permits are common (88%)

6. Undocumented extra payments or bribes made by firms for public utilities are common (80%)

7. Undocumented extra payments or bribes made by firms for awarding of public contracts and licenses are common (91%)

5. Undocumented extra payments or bribes made by firms connected with imports and exports are quite common (90%) . 7. Undocumented extra payments or bribes made by firms connected with awarding of public contracts and licenses to some extent are common (90%) . 3. The government’s effort to combat corruption and bribery is ineffective fully (87%) 6. Undocumented extra payments or bribes made by firms connected with public utilities (e.g. telephone, electricity) are common (82%) . 4. Diversion of public funds to companies, individuals or groups due to corruption is not uncommon (80%) . 14. The judiciary to some extent is influenced of members of government, citizens or firms (75%) . 12. Undocumented extra payments or bribes from one private firm to another to secure business is common (67%) . 11. The corporate ethics of firms is not good enough in the country (70%) . 9. Undocumented extra payments or bribes made by firms connected with obtaining favorable judicial decisions are sometime common (67%) .

55

Corruption, Ethics and Social Responsibility

• There is not a single positive perception found in case of corruption and ethics. Deteriorated negative perception • Perception about rise in corruption at public sector, judiciary and at private sector was getting stronger.

• 75% respondents perceived that judiciary is largely influenced by MPs, influential firms and citizens (-1.22 in 2012 vs. -1.00 in 2011).

• 67% mentioned that use of undocumented extra payments or bribes has further increased for favorable judicial decisions ( -1.06 in 2012 vis-à-vis -0.94 in 2011).

• Undocumented payments by firms to secure business has increased which is mentioned by 67% respondents in 2012(-1.20 in 2012 vis-à-vis -0.67 in 2011)

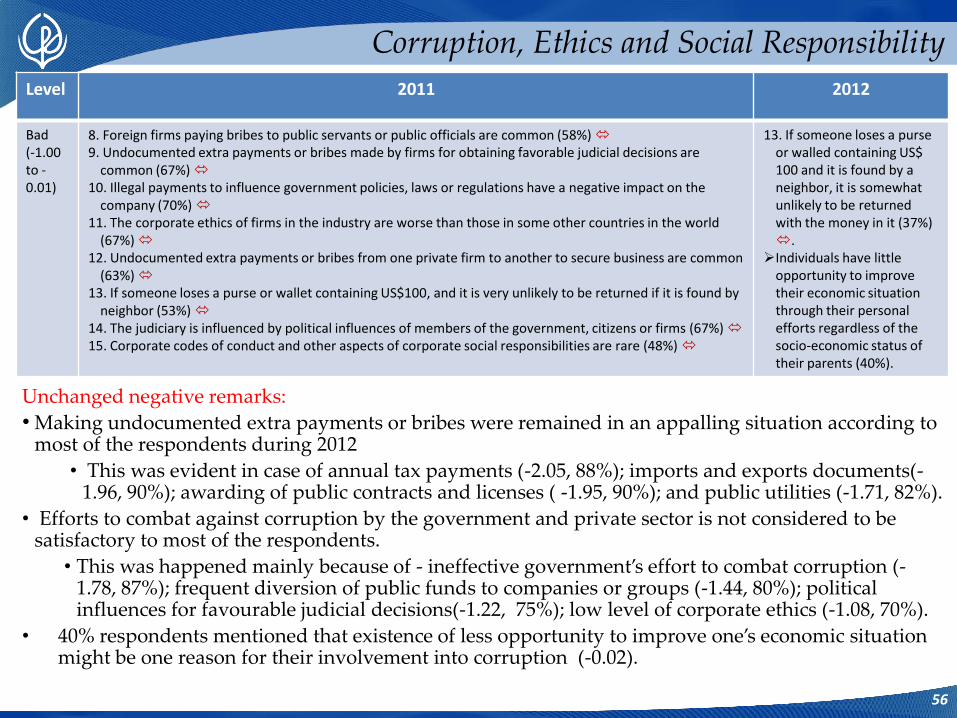

Unchanged negative remarks:

• Making undocumented extra payments or bribes were remained in an appalling situation according to most of the respondents during 2012

• This was evident in case of annual tax payments (-2.05, 88%); imports and exports documents(-1.96, 90%); awarding of public contracts and licenses ( -1.95, 90%); and public utilities (-1.71, 82%).

• Efforts to combat against corruption by the government and private sector is not considered to be satisfactory to most of the respondents.

• This was happened mainly because of - ineffective government’s effort to combat corruption (-1.78, 87%); frequent diversion of public funds to companies or groups (-1.44, 80%); political influences for favourable judicial decisions(-1.22, 75%); low level of corporate ethics (-1.08, 70%).

• 40% respondents mentioned that existence of less opportunity to improve one’s economic situation might be one reason for their involvement into corruption (-0.02).

56

Corruption, Ethics and Social Responsibility

Level 2011 2012

Bad (-1.00 to -0.01)

8. Foreign firms paying bribes to public servants or public officials are common (58%) 9. Undocumented extra payments or bribes made by firms for obtaining favorable judicial decisions are

common (67%) 10. Illegal payments to influence government policies, laws or regulations have a negative impact on the

company (70%) 11. The corporate ethics of firms in the industry are worse than those in some other countries in the world

(67%) 12. Undocumented extra payments or bribes from one private firm to another to secure business are common

(63%) 13. If someone loses a purse or wallet containing US$100, and it is very unlikely to be returned if it is found by

neighbor (53%) 14. The judiciary is influenced by political influences of members of the government, citizens or firms (67%) 15. Corporate codes of conduct and other aspects of corporate social responsibilities are rare (48%)

13. If someone loses a purse or walled containing US$ 100 and it is found by a neighbor, it is somewhat unlikely to be returned with the money in it (37%) .

Individuals have little opportunity to improve their economic situation through their personal efforts regardless of the socio-economic status of their parents (40%).

Level 2011 2012

Bad (-1.00 to -0.01)

1. Development of the Travel and Tourism sector does not take into account issues related to environmental protection and sustainable development (63%)

2. Tourism marketing is non-existent or ineffective in attracting tourists (57%)

1. The government’s effort is quite ineffective to ensure that the Travel and Tourism sector is being developed in sustainable way (65%) .

2. Country’s marketing and branding campaigns to attract tourists is relatively ineffective (61%) .

Good (0.00 to 1.00)

3. The development of the Travel and Tourism industry is a priority for the government to some extent (52%)

4. Senior executives are quite likely to be recommended to extend their first business trip in the country for leisure purposes (50%)

3. The development of the Travel & Tourism industry is a priority for the government of the country (46%) .

4. Senior executives are quite likely to be recommended to extend their first business trip in the country for leisure purposes (46%) .

Better (1.01 to 2.0)

5. Foreign visitors are usually welcome in the country (89%)

Best 2.0 1 to 3.0)

5. Foreign visitors are usually welcome in the country(98%)

Improved/positive remarks • About half of the respondents perceived that government gives marginal priority to

develop travel and tourism industry (0.08) • Almost all respondents mentioned that foreign visitors are usually welcome (2.06,

98%) in the country • Leveled up to the ‘Best’ in welcoming foreign visitors, (2.05, 98%) Unchanged negative remarks • Development of the tourism sector is constrained by lack of policy support by the

government. • Lack of marketing and branding campaigns (-0.90, 61%).

•Tourism related ADP projects particularly building infrastructure in traditional and emerging tourist spots should be implemented on a priority basis.

57

Travel and Tourism