report on the actuarial investigation as at 30 june 2015 -...

TRANSCRIPT

REPORT ON THE ACTUARIAL INVESTIGATION AS AT 30 JUNE 2015

BHP Bil l i ton Superannuation Fund

3 0 M AR C H 2 0 1 6

Issued by Russell Employee Benefits Pty Ltd ABN 70 099 865 013, AFSL 220705 (REB).This document has been prepared for the trustee for the

BHP Billiton Superannuation Fund and has not been prepared for use as financial product advice to any third party, such as an employer or a

member of the superannuation fund. It is important to note that there has been no consideration of any third party’s objectives, financial situation or

needs taken into account when preparing this document. The information has been compiled from sources considered to be reliable, but is not

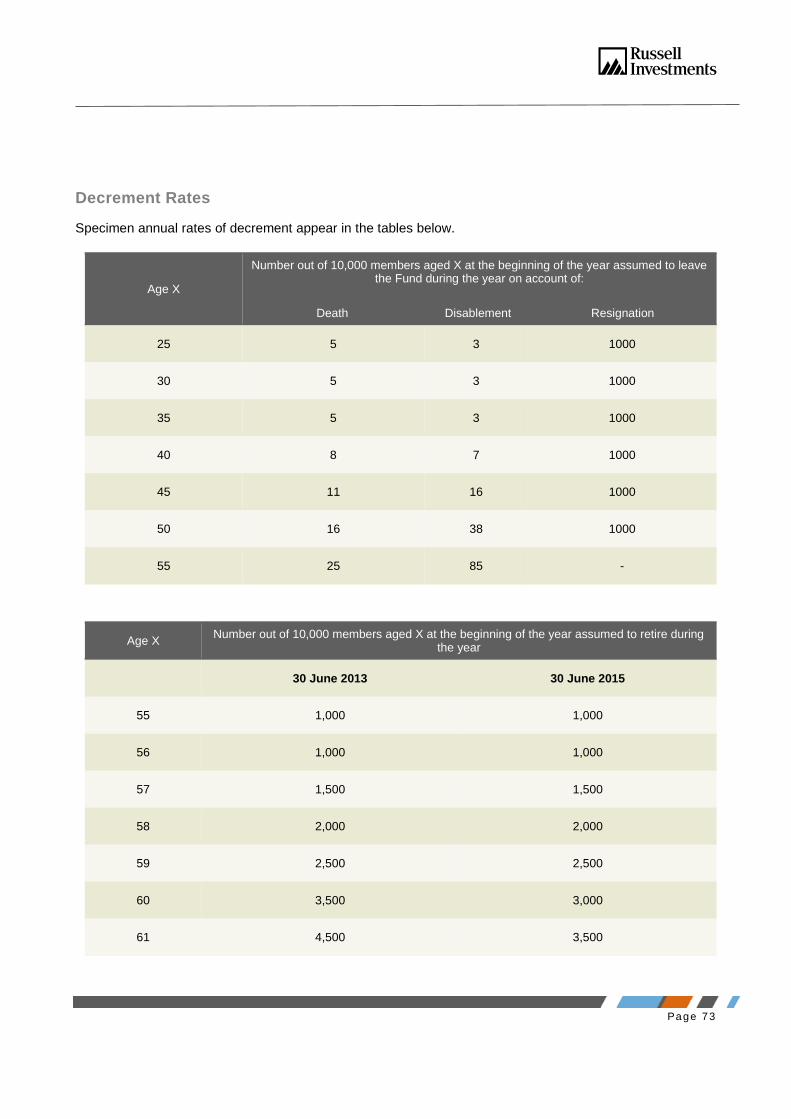

guaranteed. Past performance is not a reliable indicator of future performance. REB is paid on a fee for service basis. REB is part of Russell

Investments which provides investment management and consulting services to institutions, superannuation funds, employers and

individuals. REB’s Financial Services Guide is available from www.russellinvestments.com.au or by calling (02) 9229 5111.

T i t l e P a g e

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY ---------------------------------------------------------------------------------------------------------------------------------------------------------- 1

2 INTRODUCTION -------------------------------------------------------------------------------------------------------------------------------------------------------------------- 5

3 OVERVIEW OF THE FUND ------------------------------------------------------------------------------------------------------------------------------------------------------ 8

4 MEMBERSHIP ----------------------------------------------------------------------------------------------------------------------------------------------------------------------- 9

5 ASSETS AND INVESTMENTS ------------------------------------------------------------------------------------------------------------------------------------------------ 12

6 FUNDING METHOD ------------------------------------------------------------------------------------------------------------------------------------------------------------- 19

7 EXPERIENCE AND ASSUMPTIONS ---------------------------------------------------------------------------------------------------------------------------------------- 21

8 EXPERIENCE AND ASSUMPTIONS - FINANCIAL --------------------------------------------------------------------------------------------------------------------- 22

9 EXPERIENCE AND ASSUMPTIONS - DEMOGRAPHIC -------------------------------------------------------------------------------------------------------------- 27

10 SOLVENCY AND OTHER MEASURES OF FINANCIAL POSITION ----------------------------------------------------------------------------------------------- 32

11 DETERMININATION OF COSTS UNDER THE AGGREGATE FUNDING METHOD -------------------------------------------------------------------------- 37

12 VALUATION RESULTS --------------------------------------------------------------------------------------------------------------------------------------------------------- 41

13 SENSITIVITY OF ASSUMPTIONS ------------------------------------------------------------------------------------------------------------------------------------------- 45

14 CONSIDERATION OF PENSION LIABILITIES --------------------------------------------------------------------------------------------------------------------------- 50

15 INSURANCE ----------------------------------------------------------------------------------------------------------------------------------------------------------------------- 51

16 MATERIAL RISKS ---------------------------------------------------------------------------------------------------------------------------------------------------------------- 56

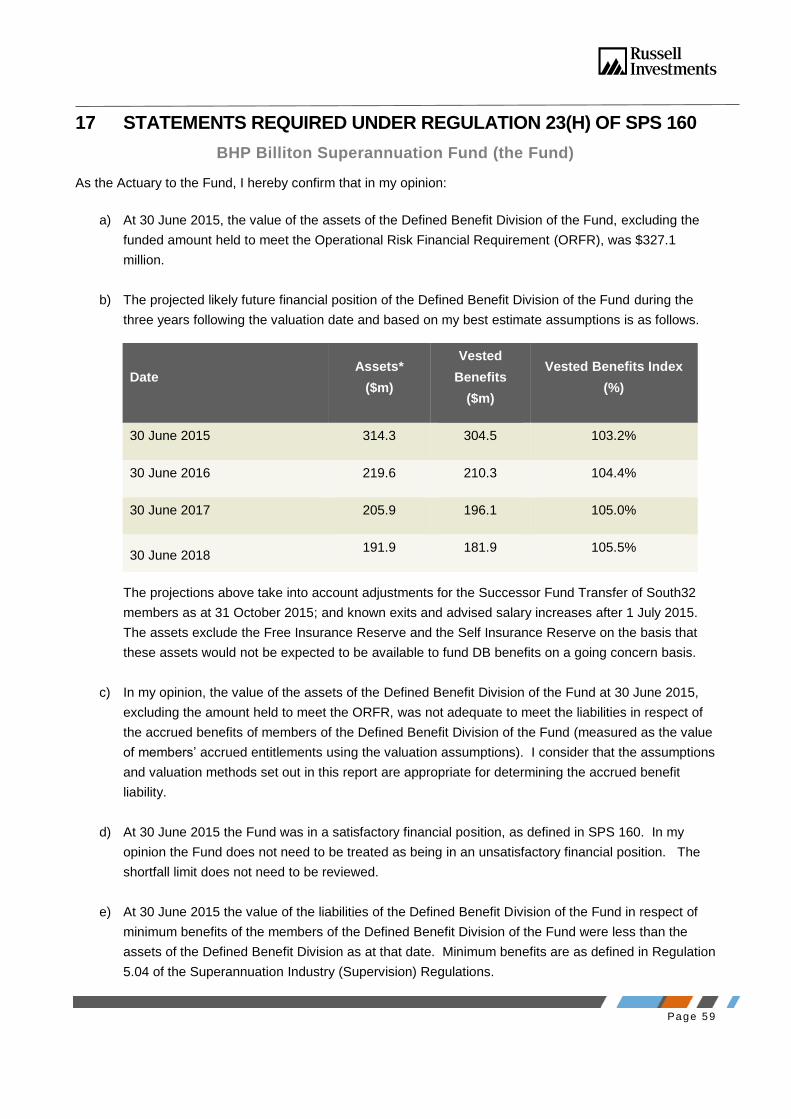

17 STATEMENTS REQUIRED UNDER REGULATION 23(H) OF SPS 160 ------------------------------------------------------------------------------------------ 59

APPENDIX A - APPENDIX ASUMMARY OF BENEFITS AND CONDITIONS -------------------------------------------------------------------------------------------- 62

APPENDIX B - SUMMARY OF ACTUARIAL ASSUMPTIONS ---------------------------------------------------------------------------------------------------------------- 72

APPENDIX C - STATEMENT OF CHANGES IN NET ASSETS FOR THE FUND FOR THE PERIOD 1 JULY 2013 TO 30 JUNE 2015----------------- 76

Page 1

1 EXECUTIVE SUMMARY

1.1 I am pleased to present my report to the Trustee of the BHP Billiton Superannuation Fund (the

Trustee), PFS Nominees Pty Ltd, on the actuarial investigation into the BHP Billiton Superannuation

Fund (the Fund) as at 30 June 2015.

1.2 I, Tony Miller, carried out the previous triennial actuarial investigation of the Fund as at 30 June

2013. The results of the investigation were presented in my report dated 25 June 2014. I also

carried out an annual investigation as at 30 June 2014 (in my report dated 30 April 2015) which was

undertaken to meet the legislative requirements for funds providing defined benefit pensions, (i.e. to

provide an opinion in relation to the payment of defined benefit pensions from the Fund).

Investigation of Defined Benefit Liabilities Only

1.3 The Fund provides benefits in respect of both defined benefit and defined contribution liabilities. The

purpose of this valuation is to investigate the financial condition of the Fund with respect to defined

benefit liabilities only.

1.4 I note that as at 30 June 2015, based on asset information from the Fund financial statements at that

date, the amount of Fund assets directly attributable to defined contribution liabilities, exceeded the

corresponding liabilities. It may therefore be seen that the defined contribution liabilities are more

than fully funded. I am therefore satisfied that there is currently no feature of the defined contribution

section of the Fund which would adversely affect the recommendations of this investigation with

respect to the defined benefit liabilities.

Defined Benefit Membership

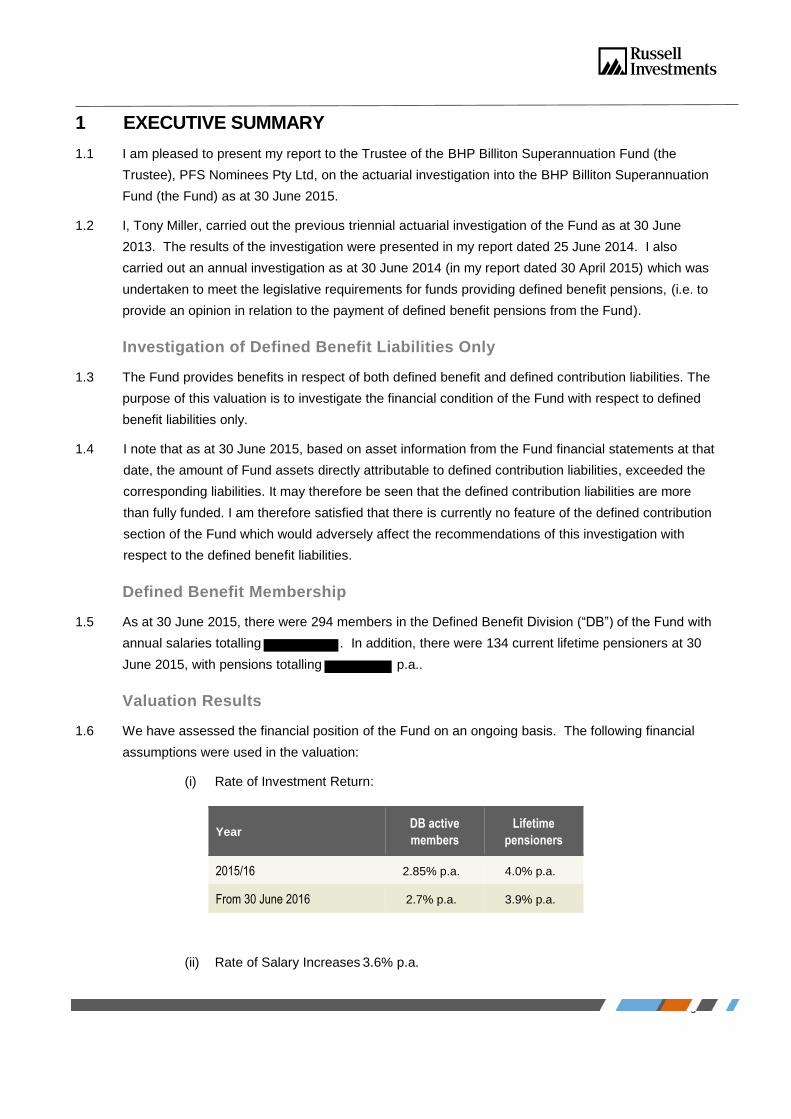

1.5 As at 30 June 2015, there were 294 members in the Defined Benefit Division (“DB”) of the Fund with

annual salaries totalling . In addition, there were 134 current lifetime pensioners at 30

June 2015, with pensions totalling p.a..

Valuation Results

1.6 We have assessed the financial position of the Fund on an ongoing basis. The following financial

assumptions were used in the valuation:

(i) Rate of Investment Return:

Year DB active

members

Lifetime

pensioners

2015/16 2.85% p.a. 4.0% p.a.

From 30 June 2016 2.7% p.a. 3.9% p.a.

(ii) Rate of Salary Increases 3.6% p.a.

Page 2

1.7 The corresponding effective gap between the net investment earning rate and the salary inflation

rate is -0.75% p.a. for the year to 30 June 2016 and -0.90% p.a. thereafter. In the previous triennial

investigation as at 30 June 2013, an effective gap of 0% p.a. was assumed (from 1 July 2015).

1.8 As at 30 June 2015, the ratio of the value of assets to vested benefits for DB members including the

lifetime pensioners (the “DB VBI”) was 107.4%.

1.9 Deducting the value of the South32 notional reserve from the assets and the value of the vested

benefits of South32 DB members from the total DB vested benefits as at 30 June 2015, the value of

the DB VBI (excluding South32) was 108.0% as at that date.

1.10 Based on the asset information in the financial statements of the Fund as at 30 June 2015, the VBI

for the entire Fund was 100.9% as at 30 June 2015.

1.11 Under SIS Regulation 9.04, a defined benefit fund is defined to be in an ‘unsatisfactory financial

position’ if the value of the assets of the fund is inadequate to cover the value of the liabilities of the

fund in respect of benefits vested in the members of the Fund. The actuarial investigation of the

Fund at 30 June 2015 revealed that the Fund was not in an unsatisfactory financial position at that

date and the Fund remained technically solvent.

1.12 For the purposes of projecting the Fund’s financial position after 1 July 2015, we took into account

the successor fund transfer of the South32 employees as at 31 October 2015, known exits post

30 June 2015 and 1 September 2015 salary increases that had been advised to us. On this basis,

our projection of the Fund’s financial position from 1 July 2015 for a period of 10 years shows that,

the DB VBI is expected to continue to be over 100%, assuming that the employer continues to

contribute at the current rate of 31.6% of salaries. This indicates that, on an ongoing basis and on

the basis of the actuarial assumptions, it is expected that the assets of the Fund should be more than

sufficient to continue to cover the benefits of active members and the required pension payments.

1.13 Under Rule A.11.5 of the Trust Deed, I recommend that BHP Billiton contributes the following in

respect of active members of the Fund:

At the rate of 31.6% of superannuation salaries in respect of members of Parts 1, 2 and 9;

Accumulation members

In accordance with Rule 2.2 of Section A and Rule 3 of Section B of Part 10 in respect of Part 10

members;

In accordance with Rule B.17A.2.2 of Section A and Rule B.17B.3 of Section B of Part 17 in

respect of Part 17 members;

In accordance with Rule B.19.3 of Section B of Part 19 in respect of Part 19 members; and

In accordance with Rule A.11.1A in respect of members who are receiving deemed member

contributions.

1.14 I understand that the Company, at its discretion, may wish to make additional top-up contributions by

respective Reporting Entities following the end of each financial year if the salary increases

Page 3

experienced by members of the Reporting Entity during the year exceed the assumed rate used for

Company accounting reporting purposes. The additional contributions would be the amount advised

by the Fund’s actuary as the increase in Fund liabilities arising in respect of the higher than assumed

rates of salary increase, adjusted for contribution tax.

1.15 I also understand that the Company, at its discretion, may wish to make additional top up

contributions if it is determined that there is a financial strain in respect of the pensioner liabilities.

1.16 I recommend that the Trustee continues to monitor the financial position of the Fund on a quarterly

basis in line with the reporting requirements to APRA. If the Fund’s experience is significantly

different from our assumptions, it may be necessary to review the recommended level of

contributions. The Trustee or Employer can initiate an interim actuarial review and new contribution

recommendation at any time if there is concern that the Fund is approaching a level where the VBI is

less than 100%. Should the VBI fall below 99% (the current shortfall limit) an interim investigation

may be required under the superannuation legislation requirements as set out in Superannuation

Prudential Standard SPS 160.

1.17 I also recommend the Minimum Requisite Benefit (MRB) as coded in the administration system be

reviewed to avoid any risk of the members receiving a benefit payment that is lower than the MRB

and to facilitate required reporting to APRA.

1.18 In respect of the Fund’s insurance arrangements, I advise that having regard to the preference of the

Trustee, the retention of the reserves which have been established within the Fund to cover the

potential benefits payable to those members who are not fully covered by the appointed insurer (but

not topped up in the event of a claim payment against these reserves) is recommended unless

otherwise advised by the Actuary.

1.19 In respect of the investment arrangements, I recommend that the Trustee satisfy itself that the tax

treatment of the investment vehicles used satisfactorily provides for the opportunity for the assets

backing the pensioner liabilities to be tax free.

1.20 The Fund has received from APRA an exemption from the requirement for plans paying pension

benefits to have an annual valuation until 30 June 2016, the then scheduled date for the next

triennial valuation. With this current valuation being conducted with an effective date of 30 June

2015, it is recommended that the Trustee now seek exemption from the 30 June 2016 and 30 June

2017 valuations.

1.21 I note that there are sufficient assets in the DB Operation Reserve (#184) and the Cash Reserve

(attributable to DC) as at 30 June 2015 to repay the loan from DB to DC. I recommend that the

Trustee should ensure that they are satisfied that these assets are available to repay the loan when

required and are not set aside for any other purpose.

1.22 In undertaking the analysis required for the preparation of the recommendations of this review we

have assumed that those members who are eligible to receive a pension on retirement would be

able to select the pension option upon retirement after the early retirement age of 55. However with

Page 4

the scheduled program of increases in the preservation age from 55 to 60 there is doubt as to

whether a member would be able to select the pension offered by the Fund unless they had attained

the applicable preservation age. We have selected the more conservative financial assumption that a

member would continue to be able to take a pension on retirement at or after age 55 for the purpose

of this actuarial investigation pending final resolution of this matter.

1.23 I am not aware of any other event since 30 June 2015 that warrants review of the recommendations

in this report.

Tony Miller

Fellow of the Institute of Actuaries of Australia

30 March 2016

I confirm that this actuarial investigation report satisfies Russell Investment Group’s Quality Assurance

standards and meets the requirements of Professional Standard 400 of The Institute of Actuaries of

Australia.

Gabrielle Baron

Fellow of the Institute of Actuaries of Australia

30 March 2016

Russell Investments Level 13 8 Exhibition Street MELBOURNE VIC 3000

Page 5

2 INTRODUCTION

Background

2.1 The Trust Deed of the BHP Billiton Superannuation Fund (the Fund) requires the Trustee to request

that the actuary undertakes an actuarial investigation of the Fund at least every three years, or more

frequently if required by Superannuation Law. The actuary is required to report on the results of the

investigation within such periods and in such manner as required by Superannuation Law having

regard to the state and sufficiency of the Fund with respect to the present and future liabilities and to

make any recommendations as the actuary sees fit. The report of the actuary is provided to the

Trustee who in turn is required to provide a copy to the Company.

2.2 The most recent triennial investigation of the Fund was undertaken as at 30 June 2013 and,

accordingly, the next triennial investigation was due as at 30 June 2016. This triennial investigation

has been undertaken as at the earlier date of 30 June 2015 at the request of BHP Billiton, the

Principal Employer of the Fund, with the approval of the Trustee following the successor fund

transfer of South32 members.

2.3 As part of this investigation, BHP Billiton has requested that we consider the impact of the South32

demerger, the large number of recent exits of DB members (including the post 30 June 2015 exits)

and post 30 June 2015 salary increases.

Purpose of the Investigation

2.4 This investigation is made as at 30 June 2015 and is presented to PFS Nominees Pty Ltd, the

Trustee of the Fund, by the Actuary to the Fund, Tony Miller, FIAA.

2.5 Under the provisions of the Superannuation Industry (Supervision) Act 1993 (“SIS”):

an actuarial investigation and report are due every three years; and

the investigation must consider the solvency and financial position of the Fund both as at the

investigation date and during the ensuing three years.

2.6 The main aims of the investigation are:

to examine the current financial position of the Fund;

to provide advice to the Trustee on the contribution rate at which the employer should

contribute under Rule A11.5 and comment on the appropriateness of the Funding Plan

adopted by the Trustee;

to meet the requirements of the Trust Deed and the relevant superannuation legislation with

respect to the conduct of actuarial investigations;

to meet the reporting requirements of Superannuation Industry Supervision Regulation 9.31

and SPS160; and

to provide advice on any other matters the actuary considers relevant.

Page 6

2.7 This report also satisfies the requirements of the Professional Standard 400 and Guidance Note 465

of the Actuaries Institute regarding the investigation of the financial condition of defined benefit

superannuation funds.

2.8 The Fund provides benefits in respect of both defined benefit and defined contribution liabilities. The

purpose of this valuation is to investigate the financial condition of the Fund with respect to defined

benefit liabilities only.

2.9 It is noted that APRA Prudential Standard applicable to the management of defined benefit funds,

SPS 160, requires annual actuarial valuations of superannuation funds which pay defined benefit

pensions, such as the Fund. The Trustee has received an exemption from this requirement from

APRA for an annual valuation as at 30 June 2015 with the next valuation being due as at 30 June

2016. I recommend that the Trustee now consider seeking an exemption for the 30 June 2016 and

30 June 2017 annual valuations.

Previous Actuarial Investigation

2.10 I carried out the previous triennial actuarial investigation of the Fund on behalf of Russell Employee

Benefits as at 30 June 2013 (“the 2013 report”) and the results were presented in a report dated

25 June 2014.

2.11 The 2013 report recommended that the Employer contributes the following to the Fund:

At the rate of 31.6% of superannuation salaries in respect of members of Parts 1, 2 and 9 until

30 June 2017;

Accumulation members

In accordance with Rule 2.2 of Section A and Rule 3 of Section B of Part 10 in respect of Part 10

members;

In accordance with Rule B.17A2.2 of Section A and Rule B.17B.3 of Section B of Part 17 in

respect of Part 17 members;

In accordance with Rule B.19.3 of Section B of Part 19 in respect of Part 19 members; and

In accordance with Rule A.11.1A in respect of members who are receiving deemed member

contributions.

2.12 I understand that the Company, at its discretion, may wish to make additional top-up contributions by

respective Reporting Entities following the end of each financial year if the salary increases

experienced by members of the Reporting Entity during the year exceed the assumed rate used for

Company accounting reporting purposes. The additional contributions would be the amount advised

by the Fund’s actuary as the increase in Fund liabilities arising in respect of the higher than assumed

rates of salary increase, adjusted for contribution tax.

2.13 I confirmed these funding recommendations in my actuarial investigation of the Fund as at 30 June

2014 which was primarily undertaken to meet the legislative requirements for funds providing defined

Page 7

benefit pensions, (i.e. to provide an opinion in relation to the payment of defined benefit pensions

from the Fund).

2.14 I understand that the Company has been making contributions on this basis.

South32 Demerger

2.15 As at 25 May 2015, as a result of the demerger of South32 from BHP Billiton, several employing

entities which were legal entities of South32 became Temporary Participating Employers (TPEs) of

the Fund. There were 53 DB members of the Fund employed by the TPEs at that date.

2.16 In accordance with the Deeds of Temporary Adherence (DTAs) which set out the terms of the

temporary participation of the TPEs, a DB Transfer Amount was determined as at 25 May 2015

reflecting “the amount of DB Assets calculated as at the Effective Date, for the purposes of this

deed, by the Trustee on the advice of the Actuary, which would be applicable to the DB TPE

Members if the TPE had ceased participation in the Fund on the Effective Date”.

2.17 From that date, the Trustee recorded the DB Transfer Amount as a notional reserve of the Fund for

tracking purposes only.

2.18 As at 1 November 2015, the DB members employed by the TPEs transferred to the Plum

Superannuation Fund by means of a successor fund transfer. This transaction involved the transfer

of the member liabilities and the DB Transfer Amount (and other assets in accordance with the

DTAs) as at that date to the new arrangement.

Other Key events since 30 June 2015

2.19 The investment return on the Fund assets since 30 June 2015 has been 0.2% to 29 February 2016.

This rate may be compared with the assumed investment return of 1.9% for the same period.

2.20 We note that there have been 78 exits (and notified exits) of DB members since 30 June 2015

(including the South32 employees), and one of these members elected to become a lifetime

pensioner. We have considered these exits as part of this investigation.

Page 8

3 OVERVIEW OF THE FUND

3.1 The operations of the BHP Billiton Superannuation Fund (“the Fund”) are governed by a Trust Deed

dated 1 July 1926, as amended.

3.2 The Fund is a “regulated” fund under the Superannuation Industry (Supervision) Act and therefore

qualifies for concessional tax treatment.

3.3 There are seven categories of active membership of the Fund. Parts 1, 2 and 9 provide lump sum

and pension defined benefits i.e. benefits related to members’ period of membership and salary over

the last few years of membership. Parts 1, 2 and 9 are known as the Defined Benefit Division

(“DB”). In addition the Fund provides lump sum defined contribution benefits for Parts 10, 17, 18 and

19 (i.e. lump sum benefits related to net contributions and investment earnings thereon). Parts 10,

17, 18 and 19 are known as the Defined Contribution Division (“DCD”).

3.4 Parts 1, 2, 9, 10 and 18 are closed to new members. A detailed description of the benefits valued in

this investigation is included in Appendix A to this report.

Investment Arrangements

3.5 The Trustee has determined the strategic asset allocation for the DB assets in accordance with the

Dynamic Investment Strategy (DIS) reflecting BHP Billiton’s Global De-Risking Strategy. As at

30 June 2015, 20% of the DB assets were invested in “growth” assets (such as shares and property)

and the 80% balance was invested in “defensive” assets (such as fixed interest and cash).

3.6 The Fund’s assets in respect of Accumulation members and the additional accumulation accounts of

DB members are invested in accordance with the investment choices made by members with

accumulation balances.

Insurance Arrangements

3.7 The Fund currently provides death and disablement benefits for both DB and Accumulation

members of the Fund. The death and TPD benefits of each DB member are insured by TAL with the

amount of insured cover based on the estimated benefit less the member’s vested benefit.

3.8 The Fund retains a small amount of self-insured risk which is discussed further in Section 15 of this

report.

Page 9

4 MEMBERSHIP

Membership Data

4.1 The Fund administrator (Plum) is responsible for maintaining member records, payment of benefits

and other administrative tasks as at 30 June 2015. Membership data was provided by Plum in

respect of members of the Fund as at 30 June 2015.

4.2 I have done reasonableness checks on the membership data to ensure that all dates, salaries and

other amounts were reasonable. Overall I am satisfied that the data provided is sufficiently accurate

for the purposes of this investigation. Although I have no reason to doubt the quality of the data, the

results of this investigation are dependent on the quality of the data provided.

4.3 I note that while the salary data supplied by Plum was the most up-to-date as provided to them by

the Company when conducting this investigation, some salary data remains to be reviewed which

may affect the results presented in this report.

Membership Summary

4.4 Since the previous triennial actuarial investigation, the number of DB members has decreased from

434 as at 30 June 2013 to 294 as at 30 June 2015 (including 53 members employed by South32).

This represents a decrease of 32% in the number of DB members. Details of the change in

membership are summarised below:

Number of DB Members

Page 10

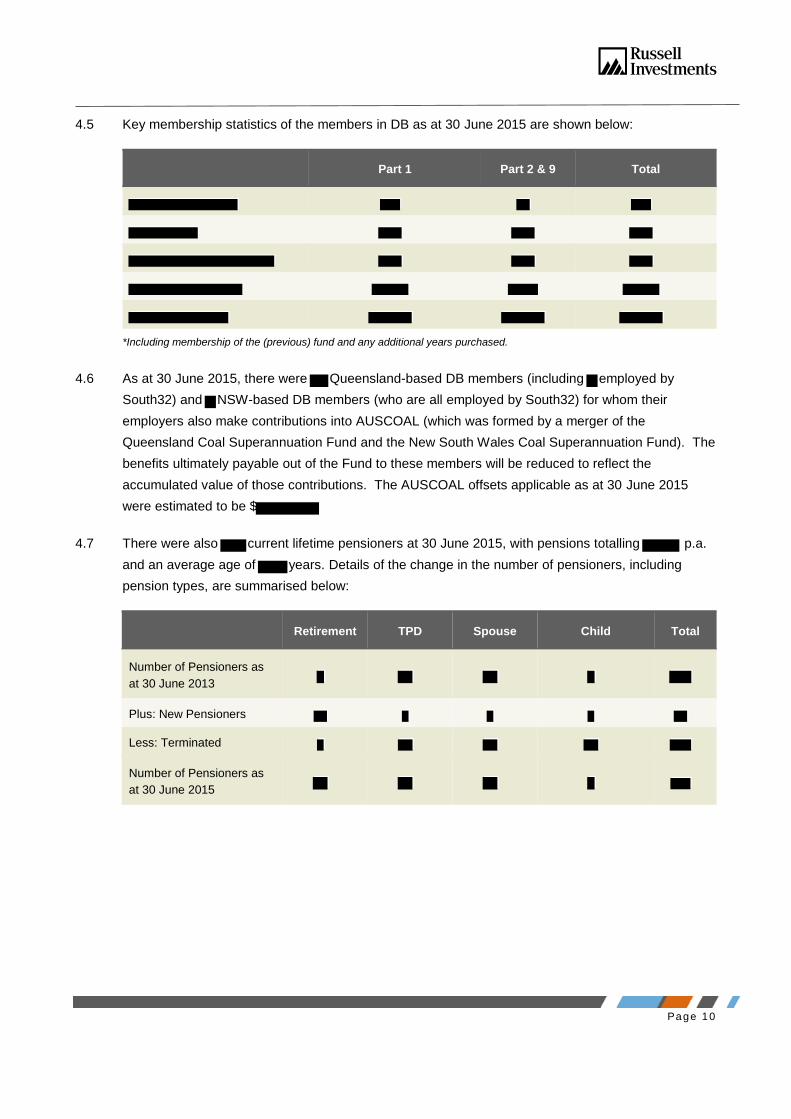

4.5 Key membership statistics of the members in DB as at 30 June 2015 are shown below:

Part 1 Part 2 & 9 Total

*Including membership of the (previous) fund and any additional years purchased.

4.6 As at 30 June 2015, there were Queensland-based DB members (including employed by

South32) and NSW-based DB members (who are all employed by South32) for whom their

employers also make contributions into AUSCOAL (which was formed by a merger of the

Queensland Coal Superannuation Fund and the New South Wales Coal Superannuation Fund). The

benefits ultimately payable out of the Fund to these members will be reduced to reflect the

accumulated value of those contributions. The AUSCOAL offsets applicable as at 30 June 2015

were estimated to be $

4.7 There were also current lifetime pensioners at 30 June 2015, with pensions totalling p.a.

and an average age of years. Details of the change in the number of pensioners, including

pension types, are summarised below:

Retirement TPD Spouse Child Total

Number of Pensioners as

at 30 June 2013

Plus: New Pensioners

Less: Terminated

Pensioners

Number of Pensioners as

at 30 June 2015

Page 11

4.8 In addition, the Fund contained other membership groups (and account balances) as shown in the

following table:

Fund Part Number of

members

Total Account

Balances ($m)

Defined Contribution Division (Parts 10, 17, 18 & 19)

Spouse Account (Part 15)

Retained Benefits Division (Part 14)

Allocated Pensioners (Part 16)

Voluntary Account Balances (Parts 1, 2 & 9)

Totals for non DB liabilities

4.9 The value of these accounts were provided by Plum. They are consistent with the value of the

accounts shown in the Financial Statements as at 30 June 2015 of $3,411,282,000.

Page 12

5 ASSETS AND INVESTMENTS

5.1 Financial information was obtained in the first instance from the audited financial statements of the

Fund as at 30 June 2015 and further information from Plum. The Fund’s Financial Statements as at

30 June 2015 were audited and signed on 23 October 2015 by Graeme McKenzie of Ernst & Young.

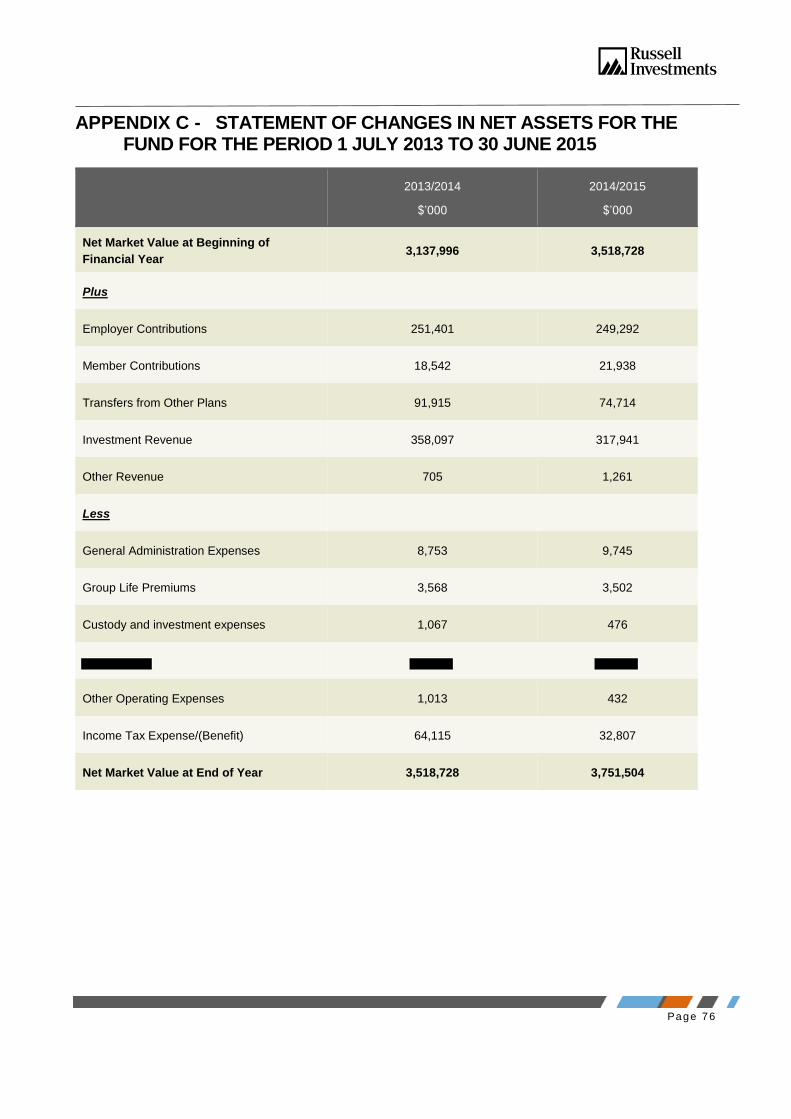

5.2 The statement of changes in net assets for the period 1 July 2013 to 30 June 2015 is shown in

Appendix C of the report.

Value of Assets

5.3 As at 30 June 2015, the total net market value of assets of the Fund available to pay benefits and

reserves, as stated in the audited financial statements was $3,751,504,000. This value includes the

Operational Risk Reserve (ORR) of $2,272,000 and the Litigation Reserve of $608,281 as at that

date. The value of total fund assets as at that date (excluding those reserves) is $3,748,624,000.

5.4 The value of the invested assets (excluding the assets directly attributable to defined contribution

accounts which includes additional voluntary accounts for defined benefit members) can be

summarised below:

Reserve Amount at

30 June 2015

Where the Reserve is held as at

30 June 2015

DB Reserve $268,099,476 DB Reserve Account #182

Self-Insurance Reserve $1,029,258 DB Reserve Account #183

DB Operation Reserve $7,961,633 DB Reserve Account #184

Free Insurance Reserve $11,881,853 DB Reserve Account #185

BHP litigation DB reserve $608,281 DB Reserve Account #186

Operation Risk Reserve $2,271,965 DB Reserve Account #275

South32 DB Reserve $44,882,881 DB Reserve Account #293

Cash Reserve $4,592,479

Value of the DB assets to be used for the DB VBI and DB ABI as at 30 June 2015

5.5 The composition of the value of the assets attributable to DB is as shown on the following page.

Page 13

Value at 30 June 2015 ($)

DB Reserve Account Balance (#182) $268,099,476

South32 DB Reserve (#293)* $44,865,422

Plus DB to DC loan $11,319,307

Plus Free Insurance Reserve (#185) $11,881,853

Plus Cash Reserve (attributable to DB) $536,702

Plus Self-insurance reserve (#183)** $826,750

Less DB contribution tax payable ($747,476)

Net Value of assets supporting DB liabilities

*The ORR funding for 2014/2015 in respect of South32 members has been deducted from the South32 Reserve

for the purpose of these calculations.**We have taken into account the value of the self-insurance reserve as at

31 October 2015 as discussed in 5.7 below.

5.6 One of the DB assets is a loan of originally $8.0 million from DB to DC to establish an operating

reserve in 2011. The value of this loan has accrued at the rate of the investment return on Account

#182 to $11,319,307 at 30 June 2015 (which takes into account the DB share (excluding South32) of

the funding of the ORR in June 2015). On the basis of advice received from the administrator, I

understand that the DB Operation Reserve (#184) and the Cash Reserve (attributable to DC) are

designated to provide the funding to cover this loan. I note that as at 30 June 2015, the total value of

these reserves exceed the value of the loan. I believe that the Trustee should ensure that they are

satisfied that these assets are available to repay the loan when required and are not set aside for

any other purpose.

5.7 If the Fund was to be wound up and the vested benefits paid out to all members immediately, the

Free Insurance Reserve would remain part of the DB assets but would no longer be a liability of the

Fund. We have also considered the Self-Insurance Reserve a DB asset for VBI purposes as

recommended in my 30 June 2013 report. However, in determining the amount of the Self

Insurance reserve which may be counted as an asset, I have deducted any known liabilities

(excluding the South32 share of this reserve).

5.8 Note that these amounts of the Free Insurance Reserve and the Self Insurance Reserve are

included in both the DB assets and the DB liabilities for the purpose of calculating the DB ABI as

they represent an ongoing liability of the Fund.

5.9 Further details on the Free Insurance Reserve and the Self Insurance Reserves are provided in

section 12 of this report.

Page 14

Value of the DB assets to be used for funding purposes as at 30 June 2015

5.10 For the purpose of determining assets for funding purposes (for the Aggregate funding method and

the projections of DB VBI and DB ABI), I have excluded the amount of the Free Insurance Reserve

and the Self Insurance Reserve from the DB assets as while they represent an ongoing, self-funded

liability of the Fund they are not included explicitly in the funding program determinations. We have

also adjusted the value of assets to take into account the expected ORR funding of 0.05% of DB

assets as at 30 June 2016 for funding purposes. The net value of assets supporting DB liabilities for

this purpose is set out below:

Value at 30 June 2015 ($)

DB Reserve Account Balance (#182) $268,099,476

South32 DB Reserve (#293)* $44,865,422

Plus DB to DC loan $11,319,307

Plus Cash Reserve (attributable to DB) $536,702

Less DB contribution tax payable ($747,476)

Less estimated ORR funding as at 30 June 2016 ($157,218)

Net Value of assets supporting DB liabilities for funding

purposes

*The ORR funding for 2014/2015 in respect of South32 members has been deducted from the South32 Reserve

for the purpose of these calculations.

5.11 I have used these adjusted net market values of the DB assets for the purpose of assessing the

financial position of the DB. It should be noted that these values do not include the voluntary account

balances of DB members.

5.12 The results of this investigation are dependent on the quality of the asset information. Any changes

to the asset values above will have an impact on the outcome of the investigation and any resulting

recommendations.

Page 15

Operational Risk Financial Requirement

5.13 Under APRA’s Prudential Standard 114 “Operational Risk Financial Requirement”, superannuation

plans are required to establish and maintain financial resources to address losses arising from

operational risks. This is referred to as the Operational Risk Financial Requirement (ORFR). These

requirements apply with effect from 1 July 2013. Under transitional arrangements, the Fund may

build the resources to meet the ORFR target amount immediately, or over a period of no more than

three years.

5.14 A plan must also have a documented strategy to determining, implementing, managing and

maintaining an ORFR target amount and suitable policies to manage the financial resources held to

meet the ORFR target, including a tolerance limit below which the ORFR requires replenishment.

5.15 We note that the Trustee has decided to adopt an ORFR of 0.11% for this fund. For the year ending

30 June 2014, a transfer of 0.02% of Fund assets was made from the Operation DB Reserve (#184)

to the ORR and for the year ending 30 June 2015, a transfer of 0.04% of Fund assets was made

from the Operation DB Reserve (#184) to the ORR. Adjustments were made to the loan amount

between DB and DC and from the South32 DB Reserve to reflect the appropriate share of this

funding. It is expected that the final tranche of funding (of 0.05% of assets) will occur in the year to

30 June 2016 (which has been reflected in the funding calculations in this investigation).

Investment Objectives

5.16 The Trustee has set investment objectives for each of the Fund’s five investment options available to

members and for the defined benefit assets of the Fund.

5.17 The DB investment objective is to maximise the return on investment, subject to reducing the

investment risk of the defined benefit portfolio over time and as the funding level improves. The

funding level used for this purpose is the financial position under International Accounting Standard

19 (IAS 19).

Investment Strategy

5.18 The Trustee has determined the DB strategic asset allocation, including the assets representing the

Free Insurance Cover Reserve, after consultation with the Fund’s investment consultant. The

Dynamic Investment Strategy (DIS) for the DB assets reflects BHP Billiton’s Global Risk

Management Framework and involves the progressive reduction in growth assets and consequent

increase in defensive assets to reduce investment risk as the Fund approaches a 100% funding level

on the IAS 19 basis. The asset allocation will change either when the Accrued Benefit Index (ABI) of

the defined benefits reaches specified threshold levels or on specific set dates, whichever comes

first. Specifically, when the ABI level reaches a “trigger point” or the target date is reached, the

proportion of defensive/growth assets will increase/decrease by 5%. The maximum level of

defensive assets under the DIS is 85% of the total assets which is expected to be met by 31 January

2016 (in accordance with the strategy).

Page 16

5.19 The Fund’s assets in respect of DC liabilities are invested in accordance with the investment choices

made by members. Therefore, there is no mismatch between the actual returns earned by the

Fund’s DC assets and the returns credited to members’ DC accounts.

5.20 The target and actual allocations of the Fund’s DB investments to the various investment classes at

30 June 2015 are shown in the following table. The table shows the asset allocation at

30 June 2015 which is in line with the Dynamic Investment Strategy and the Company’s Global Risk

Management Framework:

Investment Sector Target allocation (%) Actual allocation (%)

Australian Shares 11.0% 10.9%

Global Shares Unhedged 4.0% 3.9%

Global Shares Hedged 4.0% 3.7%

Private Markets 0.0% 0.1%

Australian Property 0.0% 0.0%

Global Property Securities 1.0% 0.9%

Australian Fixed interest 0.0% 0.0%

Inflation Linked Securities 80.0% 80.4%

Cash 0.0% 0.0%

Total 100.0% 100.0%

*Note: Actual Asset Allocation may not equal 100% due to rounding

5.21 As at 30 June 2015, 20% of the DB assets were invested in “growth” assets (such as shares and

property) and the 80% balance was invested in “defensive” assets (such as index-linked bonds and

cash). It is expected that the DB assets will be invested in 15% “growth” assets and 85% “defensive

assets by 31 January 2016 in accordance with the DIS strategy.

5.22 It should be noted that these assets are currently held predominantly in the MLC Life No.2 Statutory

Fund. Investment income in respect of assets supporting pension liabilities are not subject to

taxation, provided appropriate certification is undertaken. This valuation has been conducted on the

basis that investment income in respect of pensioner assets is tax free. We are currently working

with the administrator to confirm that the tax treatment of the investment vehicles used for pensioner

assets are able to access this tax free status.

Page 17

5.23 The Fund only has a small proportion of assets invested in illiquid assets and the likelihood of having

to sell the illiquid assets in the Fund on a forced sale basis is immaterial.

5.24 Subject to being satisfied with respect to the tax free status of the pensioner assets as noted above, I

believe that the investment objectives and strategy adopted by the Trustee continues to be

appropriate for a fund of this size and with the benefit design of the Fund, having regard to the risk

objectives of the sponsoring employer.

Crediting Rate Policy

5.25 The crediting rate policy relates to the crediting of investment earnings to accumulation accounts for

defined benefit members and defined contribution members.

Crediting Rates for Accumulation accounts – DC members and DB voluntary accounts

5.26 The Fund uses the movement in daily unit prices to credit investment earnings to members’

accounts. We consider this crediting rate policy adopted by the Trustee to be appropriate as it

minimises cross subsidies between different sections of the Fund and between different members.

We have not conducted an analysis of the application of this policy.

Crediting Rates for DB Members Only

5.27 The Trustee’s standard approach to determining Crediting Rates applied in respect of DB members

for MAC Accounts, Late Payment Interest or for Surcharge Accounts is as follows:

set Crediting Rates in arrears after the end of each month, determined by the actuary to

the Fund;

the Crediting Rate will be based on the actual “money weighted” investment return of

the assets supporting the particular liabilities, after investment fees and taxes; and

Crediting Rate information provided by the actuary will include the monthly rate and an

annualised rate on a simple basis (using days).

For the purpose of applying Late Payment Interest the rate is subject to a minimum of

zero.

Interim Crediting Rates

5.28 An ‘interim earning rate’ is required to allocate investment earnings to exiting members’ accounts for

the period from when the last Crediting Rate was effective to the date of exit. It is also used to

provide quote information to current members. As a principle, the Interim Rate should be a

reasonable proxy for the expected Crediting Rate over the next period and a simple measure to

calculate.

Page 18

5.29 The standard Trustee Interim Rate:

is the 90 day bank bill rate (on the last working day of the prior month) adjusted for 15%

tax;

will be retrospectively overridden by the Crediting Rate;

is determined by the actuary to the sub-plan or fund; and

is an annualised rate.

5.30 I consider that the crediting rate policy currently adopted by the Trustee is appropriate.

DCD Assets

5.31 As part of undertaking this actuarial investigation, we compared the vested benefits of Accumulation

members with the estimated value of the assets deemed to be attributable to Accumulation

members. For the purpose of this determination, asset values were taken from the Fund financial

statements at 30 June 2015 and our calculations are as follows:

Value at 30 June 2015($ million)

Total net market value of assets of the Fund 3,751.5

Less: Estimated Defined Benefit Assets (excluding Self Insurance

Reserve and Free Insurance Reserve) (314.4)

Less: Operation Risk Reserve (2.3)

Less: Litigation Reserve (0.6)

Less: Free Insurance Reserve (11.9)

Less: Self Insurance Reserve (1.0)

Estimated value of assets available for Accumulation members* 3,421.3

Vested benefits for Accumulation members* 3,411.3

*It should be noted that the vested benefits and assets for Accumulation members includes the voluntary account balances

for DB members.

5.32 As can be seen from the table, the amount of assets attributable to Accumulation members exceeds

the comparable vested benefits by $10.0 m or 0.3% of assets available for Accumulation members.

Having regard to the operation of this Fund we would expect the surplus assets in respect of

Accumulation members to be of this magnitude.

Page 19

6 FUNDING METHOD

General

6.1 Over the life of the Fund, the total income (mainly contributions and investment income) must be

sufficient to meet the total expenditure (mainly benefits and expenses). The funding method is the

method by which the actuary considers the long-term financial position of the Fund with a view to

ensuring the Fund’s assets will be sufficient over the long term to meet its liabilities as they arise.

6.2 In a defined benefit fund such as this, a pool of assets is built up over time that is available to meet

benefit and expense payments as they arise. The pool of assets is built up by member and

employer contributions and positive investment income on assets already accumulated. The pool is

reduced by benefit payments, tax, expenses and negative investment income.

6.3 The amount of benefits which the Fund will be liable to pay from the pool in future cannot be known

in advance since benefits depend on members’ salaries near their date of leaving, their completed

membership at that date, and their reason for leaving. The amount of future tax and expenses also

cannot be known in advance. It is therefore necessary to estimate these future liabilities and hence

the amount that will be required in the pool of assets. The estimate is based on a set of assumptions

about future experience. More details on the individual assumptions used are included in Sections 7,

8 and 9 of this report.

6.4 The amount in the pool of assets at any time is determined primarily by the level of contributions,

benefit outflows and investment income. The rate at which the employer contributes to the Fund is

usually the only variable inflow over which the employer can exercise significant control and is the

main determinant of the speed with which benefits are funded, i.e. the pace of funding of benefits.

The actuarial funding method is the basis for determining this contribution rate.

Funding Objective

6.5 The Superannuation Industry (Supervision) Act 1993 (SIS) and associated Regulations contain a

number of funding and solvency requirements.

6.6 SIS solvency standards consider the funding of Minimum Requisite Benefits, as well as the funding

of vested benefits. A failure to cover Minimum Requisite Benefits with the net realisable value of

assets results in “technical insolvency” and a requirement for a rigorous five year plan to restore

solvency.

6.7 In addition, Superannuation Prudential Standard (SPS 160), focuses strongly on having plans aim to

have assets in excess of vested benefits. This implies having a vested benefit index for defined

benefits (DB VBI) that is in excess of 100%. The DB VBI is the ratio of the market value of assets to

the corresponding total of vested benefits of members.

Page 20

6.8 On this basis, the Fund has a funding objective which focuses on building assets to a level which

covers the vested benefits by a margin considered sufficient to provide security of member benefits

and stability of employer contribution.

6.9 For this valuation, we have adopted the actuarial financing objective of achieving and maintaining a

DB VBI of at least 105% over the period to the next actuarial investigation.

Funding Method

6.10 The Projected Benefit Funding Method will be used to assess the capability of the recommended

employer contributions to achieve the funding objective on the basis of the selected assumptions by:

Projecting members’ expected future Vested Benefits;

Projecting the expected future values of assets, and then

Assessing the ability of the Employer Contributions to achieve the funding objective, and if

necessary;

Determining alternative Employer Contributions considered necessary to achieve the funding

objective.

6.11 I would suggest that as the Fund is closed to new members and with consideration given to the

regulatory requirements, it is appropriate to use the Projected Benefit Funding method for this

valuation.

6.12 I have also determined the long term contribution rate under the “Aggregate Funding Method” as a

guide to the underlying contribution rate based on the selected assumptions.

6.13 The effect of the Aggregate Funding method is to spread the expected future cost of the Fund’s

defined benefits over the average future working lifetime of the current members to produce a level

of contribution as a percentage of these members’ salaries. This method makes no specific

allowance for new members to replace current members who leave, which is appropriate for the

Fund as the defined benefit division is closed to new entrants.

6.14 The results of these analyses are discussed in more detail in sections 10, 11 and 12.

Page 21

7 EXPERIENCE AND ASSUMPTIONS

7.1 The valuation of the Fund’s projected future liabilities is an essential part of determining the

employer’s contribution rate, as described in Section 5. In order to value the projected liabilities, it is

necessary to make assumptions regarding the timing and amount of future benefit payments,

expenses and contributions since these cannot be known in advance. These assumptions are

divided into two categories:

financial assumptions relating to the rates of salary growth and investment income; and

demographic assumptions relating to the rates of retirement, resignation, death and

disablement.

7.2 While each of the assumptions used is normally the actuary’s best estimate of future experience, in

practice, the Fund’s actual experience in any period can be expected to differ from the assumptions

to some extent. However, it is intended that over longer periods, and when all of the assumptions

are combined, they will provide a reasonable estimate of the likely future experience and financial

position of the Fund.

7.3 In setting the assumptions to be used in this investigation, I have taken into account assumptions

adopted for the last actuarial investigations of the Fund, my general experience of superannuation

plans similar to this one and the particular views of the Employer regarding future superannuation

salary growth.

7.4 A summary of the assumptions used in this investigation is included in Appendix B.

Page 22

8 EXPERIENCE AND ASSUMPTIONS - FINANCIAL

Investment Returns

8.1 While short term differences between actual investment return experience and the actuarial

assumption can affect the long-term financial position of the Fund as measured by the actuarial

investigation, the assumption used in the investigation must be based on long-term expectations

since the investigation potentially involves valuing payments for many years into the future.

8.2 The actual net investment return earned on the Fund’s DB assets were 9.3% in 2013/14 and 5.5% in

2014/15 (an average rate of 7.4% p.a. over the two years). These rates were higher than the short

term rates of 4.4% p.a. and 4.2% p.a. for 2013/14 and 2014/15 respectively assumed in the 2013

actuarial investigation. These returns have therefore had a positive impact on the financial position of

the Fund.

8.3 In February 2006, the Trustee of the Fund and BHP Billiton agreed to adopt a Dynamic Investment

Strategy (DIS) which sets the DB asset allocation according to the level of Accrued Benefits Reserve

Index (ABI). The asset allocation changes either when the ABI of the defined benefits reaches

specified threshold levels or on specific set dates, whichever comes first. Specifically, when the ABI

level reaches a “trigger point” or the target date is reached, the proportion of defensive/growth assets

will increase/decrease by 5%. The maximum level of defensive assets under the DIS is 85% of the

total DB assets which is expected to be implemented as at 31 January 2016. As at 30 June 2015,

20% of the DB assets were invested in growth assets and the 80% balance was invested in

defensive assets.

8.4 This investment strategy aims to reduce the investment risk as the funding level improves, thus

reducing the risk of future deterioration of the funding position.

8.5 Due to the Dynamic Investment Strategy of the Fund, estimated earning rates are expected to

decrease over time as the asset allocation progressively changes to a more defensive allocation.

The earning rates I have used in this valuation are based on the DIS investment strategy and our

current expectations of investment returns (net of taxation and investment management expenses)

taking into account the expected duration of 5 years for DB active members and 10 years for lifetime

pensioners. The assumed rates are set out below:

Year DB active

members

Lifetime

pensioners

2015/16 2.85% p.a. 4.00% p.a.

From 30 June 2016 2.70% p.a. 3.90% p.a.

8.6 The investment returns for lifetime pensions also take into account the fact that no tax applies to the

investment income on assets covering superannuation pensions. As noted in 5.22, we are currently

Page 23

working with the administrator to confirm that the tax treatment of these vehicles takes into account

the tax-free nature of the assets backing the pensioner liabilities.

Salary Increases

8.7 For the purpose of an actuarial investigation, salary increases are generally split into two

components, namely inflationary increases and promotional increases. Inflationary increases are

generally assumed to be in line with increases in Average Weekly Earnings over time while

promotional increases are often related to age and to the industry in which members are employed.

8.8 The salary increases (inflationary increases and promotional increases) of DB members averaged

around 2.6% p.a. over the two years to 30 June 2015, which was lower than the expected combined

rate of 4.0% p.a. assumed in the 2013 actuarial investigation. This had a positive impact on the

financial position of the Fund.

8.9 From our discussions with the Company, and taking into account current long-term expectations for

wage inflation and expectations for Fund members based on their type of employment, I consider an

inflationary salary increase assumption of 3.6% p.a. to be appropriate for this actuarial investigation

of the Fund. This compares with an assumption of 4.0% p.a. adopted for the actuarial investigation

of the Fund as at 30 June 2013.

8.10 This assumption, which has been developed having regard to advice from the Company, assumes

inflationary salary increases will be 1.5% per annum in excess of expected general price inflation of

2.1% per annum (based on bond yields as at 30 June 2015).

8.11 In the triennial investigation as at 30 June 2013, we assumed that promotional salary increases

applied to age 41 in line with an age-based scale. As the youngest member was aged 39 as at 30

June 2015, we have removed the promotional salary scale assumption in this investigation.

'Gap' Between Investment Returns and Salary Growth

8.12 The assumption of major significance in the valuation of the Fund's future defined benefit liabilities

and contributions is the difference (or ‘gap’) between the assumed future rate of investment earnings

and the assumed rate of future growth in salaries, i.e. the real rate of return on invested assets.

These factors are offset against each other in their financial effect - hence the difference between the

rates is more important than the absolute values ascribed to them. The higher the real rate of return

assumed, the lower the value placed on the liabilities and the lower the estimated contribution rate

required and vice versa.

Page 24

Year

Investment

earnings

(p.a.)

Salary growth

(p.a.)

Effective “gap”

(p.a.)

2015/16 2.85% 3.60% - 0.75%

From 30 June 2016 2.70% 3.60% - 0.90%

8.13 In the previous triennial investigation of the Fund as at 30 June 2013, an initial effective gap of 0.4%

p.a., decreasing gradually to a long term effective gap of 0% p.a. was assumed. The actual effective

gap over the two years to 30 June 2015 was 4.8% p.a. (investment returns of 7.4% p.a. minus salary

growth of 2.6% p.a.).

8.14 As can be seen from the table above, for this investigation, I have adopted an initial effective gap of

minus 0.75% for one year, decreasing to a long term effective gap of minus 0.90% p.a.. The reasons

for the reduction in the gap is the lower expected returns on the Fund assets overall and the increase

in the proportion of assets invested in defensive asset classes such as inflation-linked bonds. The

reduction in the gap typically increases the long-term Employer contribution rate unless offset by

other compensating factors.

Expenses

8.15 Under the structure of the underlying fee basis of the Fund, unless the Company approves

otherwise, there is effectively no cross subsidisation of costs and fees between the DB and other

divisions.

8.16 The administration expenses payable from the Fund in respect of non-active members (those in the

RBD, Spouse Account and Allocated Pension Division) are precisely equal to the fees deducted from

these members’ accounts.

8.17 The fees deducted from DC members’ accounts are considered to adequately cover the

administration costs payable from the Fund in respect of DC members.

8.18 As the actual deductions from all divisions of the Fund, other than the DB, fully cover the

corresponding administration costs, the contributions made by BHP Billiton in respect of DB

members only need to cover the administration costs in respect of DB members.

8.19 I have analysed the fees paid in the two years to 30 June 2015. The total administration expenses in

respect of DB members were approximately 0.11% and 0.13% of the average DB assets in

2013/2014 and 2014/2015 respectively.

8.20 I have also analysed the structure of administration costs (those under the current agreement

between the Trustee and Plum (including APRA fees), and between Russell and the Trustee)

expected to be paid in the future. These costs also amount to 0.12% of current DB assets.

Page 25

8.21 Taking into account the known benefits payable subsequent to 30 June 2015 (including South32

transfers), the expected known expenses are 0.14% of adjusted DB assets (bearing in mind that

some of the fees are fixed costs).

8.22 In the previous actuarial investigation, I assumed that the expenses in respect of DB members were

0.2% of the DB assets.

8.23 For the purposes of this investigation I have assumed that future annual DB expenses payable are

likely to total 0.15% p.a. of DB assets (which incorporates a small margin for unexpected expenses).

Insurance

8.24 The Trustee has appointed TAL to underwrite most of the death and disablement benefits in respect

of DB and DC members. Based on premium rates in the current insurance policy, I have estimated

the cost of insurance in respect of DB members to be approximately 0.7% of the DB members’

salaries (which is the same as the cost assumed in the last triennial investigation). Details of the

Fund’s group insurance arrangements in respect of death and disablement benefits are included in

Section 15.

8.25 The insurance premiums for the 2 free units of cover provided to DC members are paid from the

Free Insurance Reserve (FIR).

Taxation

8.26 Future changes in the taxation regime applying to superannuation plans in Australia may have an

impact on the financial status of the Fund. Ongoing discussions at Federal Government level have

considered changing aspects of the superannuation tax structure without reaching any conclusions.

Some increases in taxation may arise in future. I have however assumed that the current regime will

continue and that the tax rate presently applying to the Fund will be maintained in future, i.e. that the

Fund will remain a regulated and complying fund under SIS and the Tax Act respectively and that a

concessional tax rate of 15% will apply to net deductible contributions and investment earnings. If

additional taxes are levied on superannuation plans in Australia, it would be appropriate to review the

contribution recommendations.

8.27 As the liability for any excess contributions tax and the Division 293 tax will rest with Fund members,

I have not allowed for any of these taxes in this investigation.

8.28 As any outstanding superannuation surcharge amounts are deducted from members’ benefits, they

do not represent a cost to the Employer and I have not allowed for these in this investigation

Member Contributions

8.29 DB member contributions, of 4% of salary, are currently capped at per annum (the

contribution for a DB member with a salary of or more). This maximum contribution is set

by BHP Billiton and can be varied. For the purpose of this investigation it has been assumed that the

Page 26

maximum member contribution will not be varied. Over time, as salaries increase, this means that

the proportion of the cost of funding benefits which is met by the Employer will increase.

Page 27

9 EXPERIENCE AND ASSUMPTIONS - DEMOGRAPHIC

9.1 I have compared the Fund’s experience over the past six years against the assumptions that were

adopted in the previous triennial actuarial investigation.

Retirement

9.2 During the six year investigation period, a total of 227 defined benefit members retired (including

retrenchments over age 55) from the Fund compared to 322 expected retirements based on the

assumptions used in the previous investigation. A comparison between actual and expected

retirements over the 6 year period is shown in the chart below.

9.3 We note that the experience for ages 60 to 65 in the graph above is different to the assumptions as

shown in the table below.

Age Actual Expected Actual vs Expected (%)

60 30 38.9 77%

61 22 39.5 56%

62 18 39.0 46%

63 15 32.7 46%

64 14 26.9 52%

65 6 24.9 24%

-

5

10

15

20

25

30

35

40

45

55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70

Retirement

Actual

Expected

Page 28

9.4 Accordingly, we have reduced the retirement rates over this period to be more consistent with

experience (and taking into account increasing preservation ages in the future) as set out below:

Age X Number out of 10,000 members aged X at the beginning of the year assumed to retire during

the year

30 June 2013 30 June 2015

55 1,000 1,000

56 1,000 1,000

57 1,500 1,500

58 2,000 2,000

59 2,500 2,500

60 3,500 3,000

61 4,500 3,500

62 5,500 4,000

63 6,500 4,500

64 7,500 5,000

65 10,000 10,000

9.5 In the actuarial investigation as at 30 June 2013, we assumed that future eligible retirees did not

elect a benefit in pension form. To determine if this assumption is still appropriate, we have analysed

the pension elections as set out below:

Two years to 30 June 2015 Six years to 30 June 2015

No. retirees eligible for a pension 90 224

No. retirees electing a pension 16 18

% of retirees electing a pension 17.8% 8.0%

9.6 It is noted that in the last two years, there has been a material increase in the number of eligible

retirees electing a pension benefit. Plum has advised that anecdotally the possible reasons for these

increases are:

Page 29

Plum has included a paragraph on benefit statements and exit statements quantifying

the pension benefit;

Financial planners being more aware of this option and of the value of the benefit in a

low interest rate environment; and

DB members being more cautious with their benefits due to investment market volatility

in recent times.

9.7 On this basis, I suggest that it is reasonable to assume that there will be a pension take-up of the

order of 15% of eligible retirees going forward.

9.8 A related issue to consider is the proportion of benefits that are taken as a pension when the pension

option is chosen. I note that the average proportion of the lump sum benefit taken as a pension over

that period was 77% (with the majority taking 100% of their lump sum in pension form). I suggest

that a reasonable assumption for the proportion of the benefit taken as a pension is 75% (for those

members that elect the pension option.

9.9 On the basis of the above I have therefore assumed for the purpose of this valuation, that 15% of

eligible retirees will take a pension and will take 75% of their benefit in pension form.

9.10 Historically, those members eligible to elect to have all or a portion of their benefit taken as a pension

were able to do so on retiring after age 55. However the legislative process by which the

preservation age is being progressively increased from 55 to 60 has implications which may mean

that a pension is unable to be taken unless the member had attained at least their preservation age

at retirement. Until this matter is resolved by the Trustee we have adopted the more conservative

financial assumption that a member would continue to be able to take a pension on retirement at or

after age 55.

Resignation and retrenchment

9.11 The number of resignations and retrenchments (under age 55) totalled 169 during the six year

investigation period, which was about 83% of the number expected on the assumptions adopted at

the 30 June 2013 investigation. This shows that the observed number of resignations was broadly

consistent with that expected on the basis of the assumptions adopted in the 30 June 2013

investigation.

Page 30

9.12 The chart below compares the actual number of resignations (including retrenchments and transfers)

and the expected number of resignations based on the rates used in the previous actuarial

investigation over the 6 year period to 30 June 2015.

9.13 The experience over the last six years has generally been consistent with that expected. I have

therefore retained the assumed resignation rates used in the previous investigation. The resignation

rates are set out in Appendix B.

Deaths and Disablements

9.14 The bulk of the future service portion of the death and disablement benefits is insured. However,

there are circumstances where some or all of the benefit in excess of the vested benefit may not be

covered by the TAL insurance policy. In these situations, the Fund may still be liable for the benefit.

9.15 During the six year investigation period, there were no disablements, and one death resulting in 1

new Spouse pensioner and 3 new child pensioners. As there is insufficient data in respect of the

Fund’s deaths and disablements to produce statistically reliable demographic assumptions, I have

adopted the same death and disability assumptions adopted for the previous actuarial investigation.

Sample death and disability rates are set out in Appendix B/

-

10

20

30

40

50

60

70

80

90

100

25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65+

Withdrawal

Actual

Expected

Page 31

9.16 Based on the more recent experience of the Fund, which indicates no members taking a pension on

disability, I have retained the assumption that no members will elect to take a pension on disability.

Other Assumptions

9.17 I have assumed that pensioner mortality (the rates at which pensioners die) will be in accordance

with ALT 2010-2012 with a 1% p.a. mortality improvement for all pensioners from 1 July 2011. In the

previous triennial investigation, I assumed that the mortality rates set out in the table a(90) produced

by the British Institute of Actuaries in 1977, rated down three years, would apply. The new mortality

assumptions will result in an increase in the value of pensioner liabilities as this mortality table

reflects the lighter mortality experienced in the community compared to the past.

9.18 Based on the underlying experience I have continued to assume that the disability pensioner

mortality will continue to be based the mortality rates set out in the table a(90) produced by the

British Institute of Actuaries in 1977 (rated down three years but with a further age adjustment).

Disability pensioners under the age of 55 will have an adjusted age of 75, while those who are over

55 will receive an adjustment of 20 years added onto their age. This adjustment is reduced gradually

from 20 years to 0 years by the age of 85. These adjustments were also assumed in the previous

investigation.

9.19 In valuing pensioner liabilities, child pensions are assumed to be paid until the age of 25.

9.20 No explicit assumptions are made regarding the incidence of new spouse or child pensions as this

risk is covered by insurance in the first instance. I have assumed that 90% of future pensioners are

married, with male pensioners three years older than their spouses (if spouse’s date of birth is not

provided). In the previous investigation, we assumed that all pensioners were married.

Page 32

10 SOLVENCY AND OTHER MEASURES OF FINANCIAL POSITION

10.1 When assessing the adequacy of the assets and future contribution rates, both the long-term funding

and short-term solvency positions should be considered. I have calculated two measures of the

Fund’s financial position at the investigation date: the Vested Benefits Index and the Accrued

Benefits Reserve Index for the DB and the Fund as a whole. I have also considered the Fund’s

position with respect to the minimum benefits required to be paid to satisfy Superannuation

Guarantee legislation, and the position on termination of the Fund.

10.2 The indices allow for the offsets (totalling applied to future benefits to be paid from the

Fund to reflect the Company’s accumulated contributions made to the Queensland Coal

Superannuation Fund, now AUSCOAL, on behalf of DB members and to the New South Wales

Coal Superannuation Fund, now AUSCOAL, on behalf of DB members.

Vested Benefits Index

10.3 The Vested Benefits Index (VBI) represents the ratio of the assets at market value to the vested

benefits. The value of vested benefits represents the total amount which the Fund would be required

to pay if all members were to voluntarily leave service on the valuation date. This is the key measure

used under applicable legislation in assessing the financial condition of a Fund.

10.4 The vested benefits have been determined as the amount of the member resignation benefit, or the

early retirement benefit for those members who are eligible to retire (including an allowance for the

assumed pension take-up). In the case of lifetime pensioners, the present value of the expected

future pension payments is used to determine the vested benefit.

10.5 We have determined that the VBI for the entire Fund as at 30 June 2015 was 100.9% compared to

100.5% at 30 June 2013. A VBI above 100% indicates that the Fund was not in an “Unsatisfactory

Financial Position” as at 30 June 2015 as defined in section 9.04 of the Superannuation Industry

Supervision (SIS) Regulations.

Page 33

10.6 The following table shows the calculation of the VBI for the DB (the DB VBI) as at 30 June 2015

along with the corresponding figure as at the date of the previous triennial investigation. This

calculation excludes the voluntary account balances of DB members and includes the vested

benefits in respect of the lifetime pensioners.

Date

Market value of assets covering DB members

($ M)

Vested benefits of DB members

($ M)

DB VBI (%)

30 June 2015 327.1 304.5 107.4%

30 June 2013 349.2 337.5 103.5%

10.7 Accordingly, there was a surplus of assets relative to vested benefits.

10.8 In light of the subsequent successor fund transfer of South32 in October I have also tested the DB

VBI excluding South32. Deducting the value of the notional South32 Reserve as at 30 June 2015 (as

determined in 11.7) and South32’s share of the self-insurance reserve from the DB assets and the

vested benefits of the South32 DB members as at 30 June 2015 from the DB vested benefits, I have

determined that the DB VBI (excluding South32) was 108.0% as at 30 June 2015 indicating a slight

strengthening of the Fund’s financial condition would arise from the transfer out of South32.

Accrued Benefits Reserve Index

10.9 While the VBI is a measure of the immediate ability of the Fund to meet the resignation or retirement

benefits of members at the investigation date, the Accrued Benefits Reserve Index is a simple

measure of a Fund’s strength on a continuing or “going concern” basis over the longer term. This

index compares the market value of assets to the present value of the accrued benefits of members

in respect of service to the valuation date. The method of calculating the accrued benefits reserve is

the same as that used to determine the present value of accrued benefits for the purposes of AAS25

disclosure and uses the actuarial assumptions set in Appendix B of this report.

10.10 We have determined that the Accrued Benefit Reserve Index for the entire Fund as at 30 June 2015

was 99.9% compared to 99.0% at 30 June 2013.

10.11 The following table shows the calculation of the Accrued Benefit Reserve Index for the DB liabilities

only as at 30 June 2015 along with the corresponding figure as at the date of the previous triennial

investigation. This calculation excludes the voluntary account balances of DB members and includes

the vested benefits in respect of the lifetime pensioners.

Page 34

Date

Market value of assets covering DB

members

($ M)

Accrued benefits of DB members

($ M)

Accrued Benefits Reserve Index

(%)

30 June 2015 327.1 341.8 95.7%

30 June 2013 349.2 375.0 93.1%

The above table shows that the Accrued Benefits Reserve Index has increased since the

determination at 30 June 2013.

Minimum Requisite Benefit Index

10.12 Minimum Requisite Benefits (MRBs) are the minimum benefits required to be paid in respect of a

member to satisfy Superannuation Guarantee legislation. Regulation 9.06(3) of the Superannuation

Industry (Supervision) Regulations defines a superannuation plan to be “technically insolvent” if its

market value of assets is not sufficient to cover its accrued MRBs.

10.13 The MRB Index compares the market value of assets to the MRBs of members at the valuation date.

10.14 We understand that the MRBs may not have been fully and accurately coded at the time of this

actuarial investigation. Given that for most DB members, the leaving service benefit is significantly

higher than their MRB, in aggregate, total MRBs are expected to be much less than the total leaving

service benefits for DB members as at 30 June 2015.

10.15 With a DB VBI of 107.4% at 30 June 2015, in my opinion it is extremely likely that the net market

value of DB assets exceeds the DB MRBs as at that date.

10.16 As also recommended in the 30 June 2013 valuation report, I recommend that the configuration of

the MRB should be reviewed for all Defined Benefit members of the Fund as quickly as possible to

allow for confirmation of the above result and to allow for ongoing testing of technical insolvency,

particularly given that the SG rate is legislated to progressively increase in the future. In addition, the

Fund will be required to report values of the MRB to APRA on a regular basis and hence it will be

necessary to be able to make these calculations.

Termination of the Fund

10.17 The Trust Deed states that, on termination of employer contributions, the Fund must be closed to

new members. Benefits are to be allocated to members and either transferred into another

superannuation fund, approved deposit fund or eligible rollover fund or retained in the Fund and paid

to the member on their cessation of service with the employer.

10.18 As total allocations are limited to the assets held in the Fund, the Fund is never technically unable to

cover benefits payable on termination of the Fund. However, if the Fund was to be wound up at a

Page 35

time when its VBI was less than 100%, DB members’ vested benefits would likely be reduced unless

the employer made up any shortfall.

10.19 In the event of winding up, lifetime pensioners would be paid prior to the payment of active members’

benefits (in excess of Minimum Requisite Benefits) as required by legislation.

10.20 On wind up, the Trustee would need to consider whether to:

continue to provide lifetime pensions in a superannuation fund similar to the Fund; or

outsource lifetime pensions to a life insurance company (i.e. purchase lifetime annuities for

the pensioners).

10.21 The calculations of the VBI, Accrued Benefit Reserve Index and MRBI all assume that the first of

these scenarios applies. Life insurance companies have strict capital adequacy requirements that

would require significantly higher assets to be held in respect of lifetime pensioners than held by the

Fund. In practice, the amount of assets required to outsource lifetime pensioners would depend upon

commercial considerations at the time. I have estimated the order of magnitude of the assets

required by calculating the amount that would be required to be held in a bond portfolio to meet the

pension liabilities. This is likely to understate the required amount because it makes no allowance for

the insurer’s profit margin, expenses and any reserves required.

10.22 Based on a fixed interest portfolio (with a 10 year duration) of government bonds, the estimated

pension liability is This is higher than the liability of m included in the VBI

calculation based on the “funding” assumptions.

10.23 On wind up, the Trustee also would need to consider the impact of not having the ability to realise

any future income tax benefit and having to sell illiquid assets on a forced sale basis.

10.24 For the purpose of this investigation, the Deferred Tax Asset (DTA) in respect of the assets attributed

to the DBD was assumed to be zero.