report.docx

DESCRIPTION

indo techTRANSCRIPT

INDUSTRY OVERVIEW

The information in this section has been extracted from various government

publications and industry sources. Neither we, the Selling Shareholders, the

BRLMs nor any other person connected with the Issue have verified this

information. Industry sources and publications generally state that the information

contained therein has been obtained from sources generally believed to be reliable,

but that their accuracy, completeness and underlying assumptions are not

guaranteed and their reliability cannot be assured and, accordingly, investment

decisions should not be based on such information.

CRISIL has used due care and caution in preparing this report. Information has

been obtained by CRISIL from sources which it considers reliable. However,

CRISIL does not guarantee the accuracy, adequacy or completeness of any

information and is not responsible for any errors or omissions or for the results

obtained from the use of such information. No part of this report may be

published/reproduced in any form without CRISIL's prior written approval.

CRISIL is not liable for investment decisions which may be based on the views

expressed in this report. CRISIL Research operates independently of, and does not

have access to information obtained by CRISIL's Rating Division, which may, in

its regular operations, obtain information of a confidential nature that is not

available to CRISIL Research.

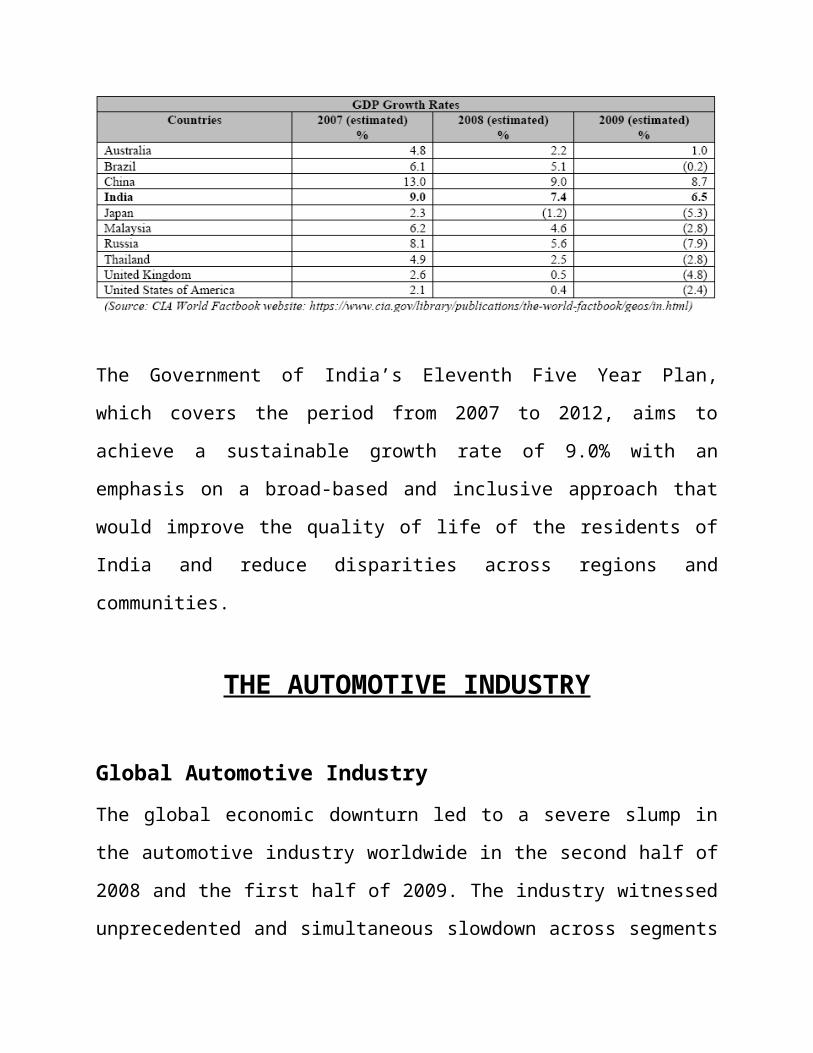

THE INDIAN ECONOMY

The Indian economy has demonstrated a sustained growth rate of more than 6.0%

per annum since 1997, which has made it one of the world’s fastest growing

economies. According to the CIA World Factbook, India’s economy grew by

9.0%, 7.4% and 6.5% in 2007, 2008 and 2009, respectively. India’s population is

approximately 1.16 billion, second only to China. India had an estimated GDP of

approximately US$ 3.57 trillion in 2009, which makes it the fourth largest national

economy in the world after the United States of America, China and Japan, in

purchasing power parity terms (Source: CIA World Factbook). The GDP growth

rates for certain developed and developing economies are set out below:

The Government of India’s Eleventh Five Year Plan, which covers the period from

2007 to 2012, aims to achieve a sustainable growth rate of 9.0% with an emphasis

on a broad-based and inclusive approach that would improve the quality of life of

the residents of India and reduce disparities across regions and communities.

THE AUTOMOTIVE INDUSTRY

Global Automotive Industry

The global economic downturn led to a severe slump in the automotive industry

worldwide in the second half of 2008 and the first half of 2009. The industry

witnessed unprecedented and simultaneous slowdown across segments and

geographies. During the last quarter of 2008, most of the world’s markets,

regardless of region, experienced a 40.0% to 60.0% decline in volume, as

compared to the same period in the previous year. The overall decline in volume

resulted in significant overcapacity among many manufacturers, causing OEMs to

implement a series of

cost-cutting measures such as plant closures, renewed pricing pressure on

automotive components and raw materials suppliers, and maintenance of lower

inventory levels to lower operating expenses. However, the global automotive

markets showed signs of revival during the second half of 2009. (Source:

Association of German Auto Industry/Verband der Automobilindustrie.

Global automotive production showed a decline of 12.8%, from 70.78 Million

vehicles in 2008 to 61.73 Million vehicles in 2009. (Source: Association of

German Auto Industry/Verband der Automobilindustrie. Almost all countries

(with the exception of Italy and China) that were considered by the Association of

German Auto Industry, showed a decline of approximately 10.0% to 30.0% in

passenger vehicle production.

In 2008 and 2009 (2009 figures are estimates or partially interim), Europe

produced 18.36 and 15.11 Million passenger vehicles, respectively. The United

States produced 8.45 and 5.58 Million passenger vehicles, respectively. China, on

the other hand, showed a 47.6% jump in production, from 5.68 Million passenger

vehicles in 2008 to 8.38 Million passenger vehicles in 2009.

(Source: Association of German Auto Industry/Verband der Automobilindustrie)

Similarly, almost all countries considered, with the exception of China, showed a

drop of approximately 30.0% to 50.0% in commercial vehicle production. In 2008

and 2009 (2009 figures are estimates, or partially interim), Europe produced 3.43

and 1.82 Million commercial vehicles and the United States produced 224,648 and

132,283 commercial vehicles, respectively. (Source: Association of German Auto

Industry. In this segment, China demonstrated an increase of 49.4%, from 3.62

Million commercial vehicles in 2008 to 5.41 Million commercial vehicles in 2009

which was against the global trend. (Source: Association of German Auto

Industry/Verband der Automobilindustrie.

INDIAN AUTOMOTIVE COMPONENT INDUSTRY

The automotive components industry in India has been growing steadily, with

turnover increasing at a rate of 298.8% between the fiscal years 2004 and 2009.

Export sales have also gradually become more important over the past six years.

As a percentage of turnover, exports increased to 19.9% in the fiscal year 2009

from 18.9% in the fiscal year 2004. (Source: Auto Component Industry in India,

Automotive Component Manufacturers Association of India)

The chart below sets forth the turnover and export figures for the automotive

components industry in India for the periods stated:

Automotive Components Industry by Segments

Aluminium Die-Casting and Machining

Aluminium die-casting is the process of producing engineered

metal parts by forcing molten aluminium into reusable steel

moulds. These moulds, which are also referred to as dies, can be

used to produce complex shapes with a high degree of accuracy

and repeatability.

Die-casting methods vary as a result of the various methods employed in injecting

the molten aluminium into the mould. The oldest form of die-casting is gravity die-

casting. In gravity die-casting, molten aluminium is inserted under normal

atmospheric pressure. This method is utilised less frequently than low pressure and

high pressure diecasting. Typically, for most products, high pressure die-casting is

more desirable. Under this process, the aluminium is injected at high speed and

high pressure, so the entire cavity may be filled before any portion of the casting

solidifies, resulting in fewer discontinuities in the casting. (Source: North

American Die Casting Association; website: http://diecasting.org/faq) However,

high pressure die-casting moulds and machines are very expensive and are only

economical when utilised on a large scale to produce a large number of products.

(Source: European Aluminium Association; website: http://www.eaa.net/en/about-

aluminium/production-process/castings/) Low pressure die-casting is an alternative

to high pressure die-casting. In this process, the die is placed over the furnace and

the cavity is filled by forcing the molten metal upwards, through the use of

pressurised gas. Once the cavity is filled, the pressure is released and the metal

flows back towards the furnace. The various filled dies are removed and the

castings are extracted. Low pressure die-casting is particularly suited for use in the

production of automotive wheels or other components that are symmetrical across

an axis of rotation.

BRAKES

The brakes segment is relatively less concentrated as compared to other segments

of the automotive components industry, with a large number of producers.

Producers may produce a number of products of varying complexity, from smaller

products for the replacement market to fully functional brakes systems. CRISIL

estimates the size of the brakes industry to be Rs. 9,400.00 Million during the

fiscal year 2010, and expects a CAGR of 12.0% until the fiscal year 2015, when

CRISIL expects that the total market size to be Rs. 16,100.00 Million. For the

fiscal year 2010, OEMs contributed 69.0% of the overall demand of the brakes

segment, the replacement market accounted for 20.0% and exports accounted for

the balance of 11.0%. (Source: CRISIL Research) Other characteristics of the

market include barriers to entry in respect of the relatively large distribution

networks that are required of producers that wish to enter the replacement market.

Relationships with OEMs are the other viable alternative to the replacement

market, however OEMs typically wish to deal with only a small number of

suppliers, to reduce their own costs. Although raw materials are relatively

expensive for the brakes industry, such costs are lessened by the lower wage costs

of India and the fact that most costs are passed on to consumers. (Source:CRISIL

Research)

SUSPENSIONS

Shock absorbers play an important role in the suspensions segment of the

automotive components industry due to their pervasiveness as a suspension

solution. Globally, shock absorber manufacturing is dominated by Japanese

companies, although most shock absorbers are generally sold on a regional basis.

Increasingly, international shock absorber manufacturers are developing

manufacturing capabilities in developing countries such as India and China.Shock

absorber manufacturing in India mostly takes place in the unorganised sector.

(Source: Cygnus business Consulting & Research, Industry Monitor – Automotive

Components, September 2008)

TRANSMISSIONS

Clutches are a major component of any transmission system. Globally, Europe is

the largest producer of clutches, followed by the United States and Asia, excluding

Japan. Asia is the fastest growing regional market. In India, the easing of the excise

duty regime to help promote the steel industry has also had a knock-on effect in

benefiting clutch manufacturers and the automobile industry as a whole. (Source:

Cygnus Business Consulting & Research, Industry Monitor – Automotive

Components, June 2010)

OUR BUSINESS

Overview

we are a leading automotive component manufacturing company in India. We

manufacture and supply a diverse range of components for two-wheelers, three-

wheelers, passenger vehicles, light commercial vehicles (“LCVs”) and heavy

commercial vehicles (“HCVs”).

Our products include:

• aluminium die-casting products, such as high-pressure, low-pressure and gravity

die-castings and twowheeler aluminium alloy wheels;

• suspension products, such as shock absorbers for two-wheelers and three-

wheelers, front forks for motorcycles and hydraulic and gas-charged dampers,

struts and gas springs for passenger vehicles, LCVs and HCVs;

• transmission products, such as clutches, friction plates and continuous variable

transmissions; and

• brake products, such as hydraulic disc brakes for two-wheelers, rotary brake discs

for two-wheelers and hydraulic drum brakes and tandem master cylinders for

three-wheelers.

We have 16 manufacturing plants in India, all of which are located in the major

automotive manufacturing belts of the country, comprising seven in Aurangabad,

Maharashtra, five in Pune, Maharashtra, two in Pantnagar, Uttarakhand, and one

each in Manesar, Haryana and Chennai, Tamil Nadu. We also have two

manufacturing plants in Massenbachhausen, Germany, which are owned by our

subsidiary Amann Druckguss GmbH (“Amann Druckguss”), and one in Torino,

Italy, which is owned by our indirect subsidiary Endurance Fondalmec SpA,

(“Endurance Fondalmec”). The following table sets forth the production capacities

and volumes for the fiscal year 2010 at our various manufacturing

locations:hydraulic drum brakes and tandem master cylinders for three-wheelers.

We are promoted by Mr. Anurang Jain, who commenced aluminium die-casting

operations in 1985 through Anurang Engineering Company Private Limited, which

subsequently merged with and into our Company. Since then, several brake,

suspension and transmission businesses promoted by Mr. Anurang Jain in India

were consolidated with our Company. Our Company also owns an 85.0% equity

interest in High Technology Transmission Systems (India) Private Limited

(“HTTS India”), our subsidiary, and the balance equity interest is held by Adler

SpA (“Adler”). HTTS India manufactures and sells clutches, friction plates and

CVTs for two-wheelers and three-wheelers. We also have a joint venture in India

with Magneti Marelli SpA (“Magneti Marelli”), Endurance Magneti Marelli Shock

Absorbers (India) Private Limited (“EMM JV”), a company in which we own a

50.0% equity interest. EMM JV manufactures struts, shock absorbers and gas

springs for passenger vehicles and LCVs.

Our customers include global OEMs such as various subsidiaries of Fiat Group

Automobiles SpA and associated brands including Lancia and Alfa Romeo,

Daimler AG, Audi AG, Porsche AG, Magyar Suzuki ZRT and two leading French

automobile manufacturers, as well as leading Indian OEMs such as Bajaj Auto

Limited, the two leading HCV manufacturers in India, a leading Indian MUV and

SUV manufacturer, India Yamaha Motor Private Limited, Royal Enfield Motors

Limited, a Korean automobile manufacturer that currently operates in India, Maruti

Suzuki India Limited and Honda Motorcycle & Scooter India Private Limited. We

have a long-standing relationship with Bajaj Auto Limited, which is our largest

customer. We have been supplying components to Bajaj Auto Limited since our

inception.

We have won several industry awards including the ‘Component Manufacturer of

the Year - 2008’ at the NDTV Profit, Car India and Bike India Awards in 2008 and

‘Auto Component Manufacturer of Year’ at the Auto Monitor Awards in 2008. We

have also received several awards and recognitions for quality, cost, delivery and

vendor performance from our customers such as Bajaj Auto Limited, Fiat India

Automobiles Private Limited, Honda Motorcycle & Scooter India Private Limited

and a leading Indian HCV manufacturer.

HISTORY

Our casting and machining division is the oldest business line at our Company.

Anurang Engineering Company Private Limited, which merged with and into our

Company in August 2006, established a high-pressure die-casting facility in

Aurangabad in 1985. In 1996, we opened our second high-pressure die-casting

plant in Takve, Pune. We have since opened several more plants at various

locations in India, specialising in high and low-pressure diecasting, as well as the

production of alloy wheels. We opened our alloy wheel die-casting plant in

Chakan, Pune in

2006.

Key Products

The five major product lines of our aluminium alloy casting and machining

division are:

• high-pressure die-casting products;

• low-pressure die-casting products;

• gravity die-casting products;

• alloy wheels; and

• machined products.

High-pressure die-casting products

We commenced high-pressure die-casting in 1985 in Aurangabad. We manufacture

a number of high-pressure diecasting products for a variety of vehicles. Our major

high-pressure die-casting products include crank cases for Bajaj motorcycles and

Honda scooters and front and rear transmission housings for a leading Indian HCV

manufacturer’s passenger vehicles.

Alloy wheels

We commenced the production of alloy wheels in 2006 at our manufacturing

facility in Chakan. We produce aluminium alloy wheels for Yamaha motorcycles

such as the Fazer, FZ16, FZS, Libero, Alba, YBR and Gladiator, and for Bajaj

motorcycles such as the Pulsar, Platina and Discover.

Two-wheeler hydraulic disc brake assemblies

We manufacture two-wheeler hydraulic disc brake assemblies, including front and

rear discs, for front or rear-only applications for motorcycles ranging from 125 cc

motorcycles, such as the Bajaj Discover, to 500 cc motorcycles, such as the Royal

Enfield Electra. Our major hydraulic disc brake products include brake discs,

master cylinders and callipers.

Three-wheeler drum brake assemblies

We produce drum brakes for use in three-wheelers such as the Bajaj RE, RE Max

and RE Diesel. Our major drum brake products include brake panel assemblies,

disc brake calliper assemblies and wheel cylinder assemblies.

Suspensions

The major products of our suspension division include:

• two-wheeler and three-wheeler shock absorbers

• passenger vehicle, LCV and HCV struts and gas springs, which

are manufactured by EMM JV.

Transmissions

Key Products

The major products of our transmissions division include:

• clutch assemblies;

• continuous variable transmissions (“CVTs”); and

• friction plates.

Raw Materials

The principal raw materials we use in our production are

aluminium alloys, steel sheets, steel tubes and customized

mechanical components, produced according to our

specifications, such as springs, pistons, canisters, under-brackets

and gears. For the fiscal year 2010, our total raw materials costs

accounted for 55.1% of our total income.

Aluminium

In our domestic operations, we primarily purchase most of our

aluminium at prices that are directly negotiated with our

customers on a regular basis. Thus, we believe that our purchases

of aluminium alloy are relatively unexposed to the risk of market

price fluctuations as such price fluctuations are often directly

passed through to our customers at the negotiated price. The

prices that we agree with our raw materials suppliers are fixed on

a quarterly basis, which is the same timeframe for which we enter

into price agreements with our customers. Our alloy suppliers for

our domestic operators are typically based in India and Southeast

Asia. For our German and Italian operations, we purchase our

aluminium at spot market prices.

Utilities

Electricity

To power our operations, we need a substantial amount of

electricity. For the fiscal year 2010, our total electricity costs

comprised 4.9% of our total income. Our operations in India,

Germany and Italy purchase utilities from their respective local

utility companies. In India, we have also set up three wind power

plants aggregating 7.1 MW in Rajasthan and Maharashtra.

Transportation

Our domestic operations use a number of different modes of

transportation including road, air and rail to supply our customers

with adequate amounts of finished goods and within their

required deadlines. The mode of transportation for a particular

shipment is dependent on the urgency, size and value of the

order. Typically, we ship finished goods to our OEM clients by

road. In a few cases, our customers may directly pick up the

goods at our own facilities, and

these arrangements are handled by our customers.

RESEARCH AND DEVELOPMENT

We believe that continued research and development activities

are critical to maintaining our leadership position in the industry

and will provide us with a competitive advantage as we seek

additional business with new and existing customers. We own four

dedicated research and development centres, three in

Aurangabad (one each for twowheeler and three-wheeler

suspensions, transmissions and brake systems) and one in Pune

(for casting). We also own an additional research and

development centre in Pune through EMM JV, for research in

passenger vehicle suspension systems. All of these centres are

approved by DSIR. Consequently, all of our product divisions are

supported by DSIR-approved R&D centres that allow the divisions

to design, develop and produce new products. As of July 31, 2010,

we employed 95 research and development engineers, designers,

technicians and support staff.

Our research and development activities and initiatives include:

• materials engineering and metallurgical research, including

defect and failure analysis of die-casting components;

• process and tool engineering;

• product design and reverse engineering, such as the design of a

new disc brake system for a newlylaunched 150 cc motorcycle;

• product simulation using sophisticated computer aided design

and computer-based simulations such as nonlinear simulation of

alloy wheel designs;

• a comprehensive prototyping program including mock-ups and

real-world testing; and

• quality assurance and testing, such as radial fatigue and

cornering fatigue tests in respect of our alloy wheel designs.

Technical Collaborations

We have entered into joint ventures and technical collaborations

with a number of partners across vehicle segments that are

typically valid for three to seven years.

Joint Venture with Magneti Marelli

Our Company entered into a joint venture agreement with

Magneti Marelli on June 11, 2008, pursuant to which a joint

venture company, Endurance Magneti Marelli Shock Absorbers

(India) Private Limited (“EMM JV”), was formed for the design,

manufacture, assembly and marketing of struts and shock

absorbers for use in passenger vehicles, LCVs and HCVs.

Agreement with WP Suspension Austria GmbH

Our Company entered into an agreement with WP Suspension

Austria GmbH on July 6, 2008. Under the terms of the agreement,

WP Suspension has agreed to provide technical assistance with

regard to developing, manufacturing and distributing high

performance suspension components for use in motorcycles. The

agreement requires that our Company will not sell similar

products made under the agreement outside of the designated

manufacturing and sales

territory of India. Further, sales by our Company are to be made

only to Bajaj Auto Limited or an Austrian motorcycle company, on

an OEM basis, and exclusively within India. The agreement

provides that should Bajaj Auto Limited or the Austrian

motorcycle company require these products outside of India, our

Company and WP Suspension will meet with the objective of

acceding to such request.

License and Technical Assistance Agreement with Akebono Brake

Industry Company Limited

Our Company entered into an agreement with Akebono Brake

Industry Company Limited on March 30, 2007. Under the terms of

the agreement, Akebono has agreed to provide technical

assistance and licensing arrangements to our Company to

develop and produce drum brake shoes and linings for use in two-

wheelers and three-wheelers in India, through the use of non-

asbestos adhesive and grinding technology. Akebono has also

agreed to provide training for our engineers at our Company sites

or at Akebono’s site. The terms of the agreement prevent the sale

of licensed products made under the agreement outside of India

unless a royalty has been paid on such products, and the license

itself is non-exclusive and non-transferable. Exports are permitted

in the form of original equipment installed on vehicles made in

India, replacements for such original equipment or as

replacement parts in 15 Asian countries, Turkey and Italy.

Technical Assistance Agreement with Teksid

Our Company entered into an agreement with Teksid Aluminium

Srl on July 4, 2008. Under the terms of the agreement, Teksid will

provide technical assistance and licensing arrangement to allow

our Company to develop and produce aluminium cylinder heads

for use in passenger vehicles. The terms of the agreement

prevent the manufacture of licensed products outside India. The

license is non-transferable. We are yet to initiate any transfer of

technology under this agreement.

Competition

The automotive component industry is extremely competitive. We

face both domestic and international competition. Typically, large

suppliers work with only a limited number of OEMs. Consequently,

we do not have a single competitor across all our product ranges.

The leading competitive players within the various product ranges

in which we operate include:

Aluminium Die-casting: Sunbeam, Rico Auto (Gurgaon, Haryana,

India), Sundaram Clayton (Chennai, Tamil Nadu, India), Jay Hind

Industries (Pune, Maharashtra, India)

Aluminium Alloy Wheels (Two-Wheelers): Enkei (Pune,

Maharashtra, India) as well as international competitors from

China

Brakes (Two-Wheelers and Three-Wheelers): Brembo (Pune,

Maharashtra, India), Bosch Chassis Systems (Jalgaon,

Maharashtra, India and Pune, Maharashtra, India)

Struts/Shock Absorbers/Gas Springs (Passenger Vehicles, LCVs

and HCVs):Gabriel, Tennaco, Munjal Showa (Gurgaon, Haryana,

India)

Clutch Assemblies (Two-Wheelers and Three-wheelers): FCC Rico

(Gurgaon, Haryana, India), Makino (Delhi, India)

CVTs (Two-Wheelers): FCC Rico (Gurgaon, Haryana, India)

Awards

The following lists some of the awards that we have received in

recognition of our achievements, products or services for the last

three calendar years:

Overall

• Greentech Foundation, HR Excellence for Best Innovative

Retention Strategies, Silver Award, 2010

• NIPM, Best HR Practices Award, 2009

• Auto Monitor Awards, Auto Component Manufacturer of the

Year, 2008

• NDTV Profit, Car India and Bike India, 2008

REGULATIONS AND POLICIESREGULATIONS AND

POLICIES

Regulation of the automotive components

manufacturing industry

The National Auto Policy

The National Auto Policy, 2002, as amended (“National Auto

Policy”) was introduced by the Department of Heavy Industries,

Ministry of Heavy Industries and Public Enterprises, GoI in March

2002, with the aim, among others, to promote a globally

competitive automotive industry and emerge as a global source

for auto components, ensure a balanced transition to open trade

at a minimal risk to the Indian economy and local industry, to

encourage modernisation of the industry and facilitate indigenous

design, research and development and to develop domestic

safety and environmental standards at par with international

standards.

The Automotive Mission Plan, 2006-2016

The Automotive Mission Plan, 2006-2016 (“Automotive Mission

Plan”) was released by the Ministry of Heavy Industries and Public

Enterprises, GoI in December 2006, containing recommendations

of the Task Force of the Development Council on Automobile and

Allied Industries constituted by the Government of India, in

relation to the preparation of the Tenth Five Year Mission Plan for

the Indian Automotive Industry. For the promotion of exports in

the auto component sector, among other things, it recommends

the creation of Special Automotive Component Parks and virtual

Special Economic Zones, which would enjoy certain exemptions

on sales tax, excise and customs duty, as well as certain tax

exemptions and concessions in relation to promotion of research

and development (“R&D”) in the automotive sector

OTHER INFORMATION

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION

A. Material Contracts for the Issue

1. Engagement Letter dated September 15, 2010 between our

Company, the Selling Shareholder and the BRLMs.

2. Issue Agreement dated September 27, 2010 between our

Company, the Selling Shareholder and the BRLMs.

3. Memorandum of Understanding dated September 20, 2010

between our Company, the Selling

Shareholder and the Registrar to the Issue.

4. Escrow Agreement dated [●] between our Company, the

Selling Shareholder, the BRLMs, Escrow Collection Bank and the

Registrar to the Issue.

5. Syndicate Agreement dated [●] between our Company, the

Selling Shareholder, BRLMs and the Syndicate Members.

6. Underwriting Agreement dated [●] between our Company, the

Selling Shareholder, the BRLMs and the Syndicate Members.

DECLARATION

We, hereby declare and certify that all relevant provisions of the

Companies Act and the guidelines and regulations issued by the

Government or the regulations or guidelines issued by SEBI

established under Section 3 of the SEBI Act as the case may be,

have been complied with and no statement made in this Draft

Red Herring Prospectus is contrary to the provisions of the

Companies Act or the SEBI Act or rules or regulations or

guidelines, as the case may be. We further certify that all

statements in this Draft Red Herring Prospectus are true and

correct.