request for proposal (rfp) for solution to … for ewirm solution_10... · request for proposal...

TRANSCRIPT

REQUEST FOR PROPOSAL (RFP)

FOR

SOLUTION TO IMPLEMENT ENTERPRISE-WIDE INTEGRATED RISK MANAGEMENT

ARCHITECTURE UNDER BASEL II & BASEL III

(FOR THE BANK AND ITS GROUP ENTITIES)

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 2 of 250

Definitions of major terms/ abbreviations used on the document

Sl. No. Acronym/ Term Used Definition

1 AFS Available for Sale

2 AIC Akaike Information Criterion

3 AIRB Advanced Internal Ratings Based

4 ALCO Asset Liability Management Committee

5 ALM Asset and Liability Management

6 AMA Advanced Measurement Approach

7 AMFI Association of Mutual Funds in India

8 AMS Annual Maintenance Service

9 ASCII American Standard Code for Information Interchange

10 ATS Annual Technical Support

11 Bank Canara Bank

12 Basel II Guidelines

Framework for Capital Measurement and Capital Standards issued

by Basel Committee on Banking Supervision

13

14

15

16

Basel II RBI Guidelines

• Master Circular - Prudential Guidelines on Capital Adequacy and

Market Discipline- New Capital Adequacy Framework (NCAF)

• Implementation of the Advanced Measurement Approach

(AMA) for Calculation of Capital Charge for Operational Risk -

Guidelines

• Capital Adequacy - The Internal Ratings Based (IRB) Approach to

Calculate Capital Requirement for Credit Risk

• Prudential Guidelines on Capital Adequacy - Implementation of

Internal Models Approach for Market Risk

17

Basel III Guidelines

A global regulatory framework for more resilient banks and banking

systems and International framework for liquidity risk

measurement, standard and monitoring

18

19

Basel III RBI Guidelines

• Guidelines on Implementation of Basel III Capital Regulations in

India

• Guidelines on Liquidity Risk Management and Basel III Framework

on Liquidity Standards

• Capital Requirements for Bank’s Exposures to Central

Counterparties

20 BEEL Best Estimate Expected Loss

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 3 of 250

21 BEICF Business Environment and Internal Control Factors

22 BIC Bayesian information criterion

23 BIS Bank for International Settlements

24 BLM Business Line Mapping

25 BRS Business Requirement Specifications

26 CBS Core Banking Solutions

27 CDSL Central Depository Services Limited

28 CO Commercial Offer/ Commercial Bid/ Price Bid

29 CORDEx Credit & Operational Risk Loss Data Exchange

30 CRMD Credit Risk Management Department

31 CRMS Credit Risk Management System

32 CSV Comma-Separated Value

33 CVA Credit Valuation adjustment

34 DGA Duration Gap Analysis

35 DIT Department of Information Technology

36 EAD Exposure at Default

37 ECGC Export Credit Guarantee Corporation

38 ECS Electronic Clearing Service

39 EDA Exploratory Data Analysis

40 EDW Enterprise Data Warehouse

41 EEPE Effective Expected Positive Exposure

42 EFT/ SEFT Electronic Funds Transfer/ Special Electronics Fund Transfer

43 EMD Earnest Money Deposit

44 EOD End of Day

45 EPE Expected Positive Exposure

46 ETL Extract, Transform, Load

47 EVT Extreme Value Theory

48 EWIRM Enterprise Wide Integrated Risk Management

49 FEDAI Foreign Exchange Dealers’ Association of India

50 FIFO First In First Out

51 FIMMDA Fixed Income Money Market and Derivatives Association of India

52 FIRB Foundation Internal Ratings Based

53 Flexcube Core Banking Application software used in bank

54 FM&S Financial Management and Subsidiaries

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 4 of 250

55 FX Foreign Exchange

56 GUI Graphical User Interface

57 HFT Held for Trade

58 HTM Held to Maturity

59 IMA Internal Model Approach

60 IMF International Monetary Fund

61 IPR Intellectual Property Right

62 IRB Internal Ratings Based

63 IRC Incremental Risk Charge

64 IRMD Integrated Risk Management Department

65 IT Information Technology

66 KRI Key Risk Indicators

67 LGD Loss Given Default

68 LIFO Last In First Out

69 M Effective Maturity

70 MBS Mortgage backed Securities

71 MDB Multilateral Development Bank

72 MIS Management Information System

73 MLE Maximum-Likelihood Estimation

74 MPE Maximum Peak Exposure

75 MRMS Market Risk Management System

76 MTM Marked to Market

77 MVA/E Market Value of Asset/ Equity

78 MVS Market Value Sensitivity

79 NAS Network Attached Storage

80 NCAF New Capital Adequacy Framework

81 NEFT National Electronic Funds Transfer

82 NPA Non-Performing Asset

83 NPV Net Present value

84 NSDL National Securities Depository Limited

85 OBD Overseas Banking Division

86 OEM Original Equipment Manufacturer/ Product Vendor

87 ORC Operational Risk Category

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 5 of 250

88 ORCC Operational Risk Capital Charge

89 ORM Operational Risk Management

90 ORMD Operational Risk Management Department

91 ORMF Operational Risk Management Framework

92 ORMS Operational Risk Management System

93 OSD Original Software Developer

94 PD Probability of Default

95 PFE Potential Future Exposure

96 QRRE Qualified Revolving Retail Exposures

97 RAPM Risk Adjusted Performance Measurement

98 RAROC Risk Adjusted Return on Capital

99 RBI Reserve Bank of India

100 RCA Root Cause Analysis

101 RCSA Risk and Controls Self-Assessment

102 RFP Request for Proposal

103 RTGS Real Time Gross Settlement

104 RWA Risk Weighted Assets

105 SI System Integrator/ Bidder

106 SL Specialized Lending

107 SLA Service Level Agreement

108 SLS Structural Liquidity Statement

109 SVaR Stressed Value at Risk

110 SWIFT Society for Worldwide Interbank Financial Telecommunication

111 TGA Traditional Gap Analysis

112 TO Technical Offer

113 UAT User Acceptance Test

114 VaR Value at risk

115 XML Extensible Mark-up Language

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 6 of 250

TABLE OF CONTENTS

1 INTRODUCTION 10

1.1 OVERVIEW 10

1.2 BROAD SCOPE OF WORK 11

1.3 INVITATION FOR BIDS 23

2 INSTRUCTIONS FOR BID SUBMISSION 25

2.1 GENERAL INSTRUCTIONS 25

2.2 DOCUMENTS COMPRISING THE BID 29

2.3 KEY GUIDELINES FOR PREPARING RFP RESPONSE 34

3 ADDITIONAL INSTRUCTIONS FOR BIDDERS 34

3.1 GENERAL INSTRUCTIONS 34

3.2 PAYMENT TERMS 45

3.3 WARRANTY & ANNUAL MAINTENANCE 47

3.4 TERMINATION 50

4 EVALUATION METHODOLOGY 55

4.1 NORMALIZATION OF BIDS 56

4.2 OPENING OF BIDS BY THE BANK 56

4.3 ELIGIBILITY CRITERIA 58

4.4 EVALUATION CRITERIA 63

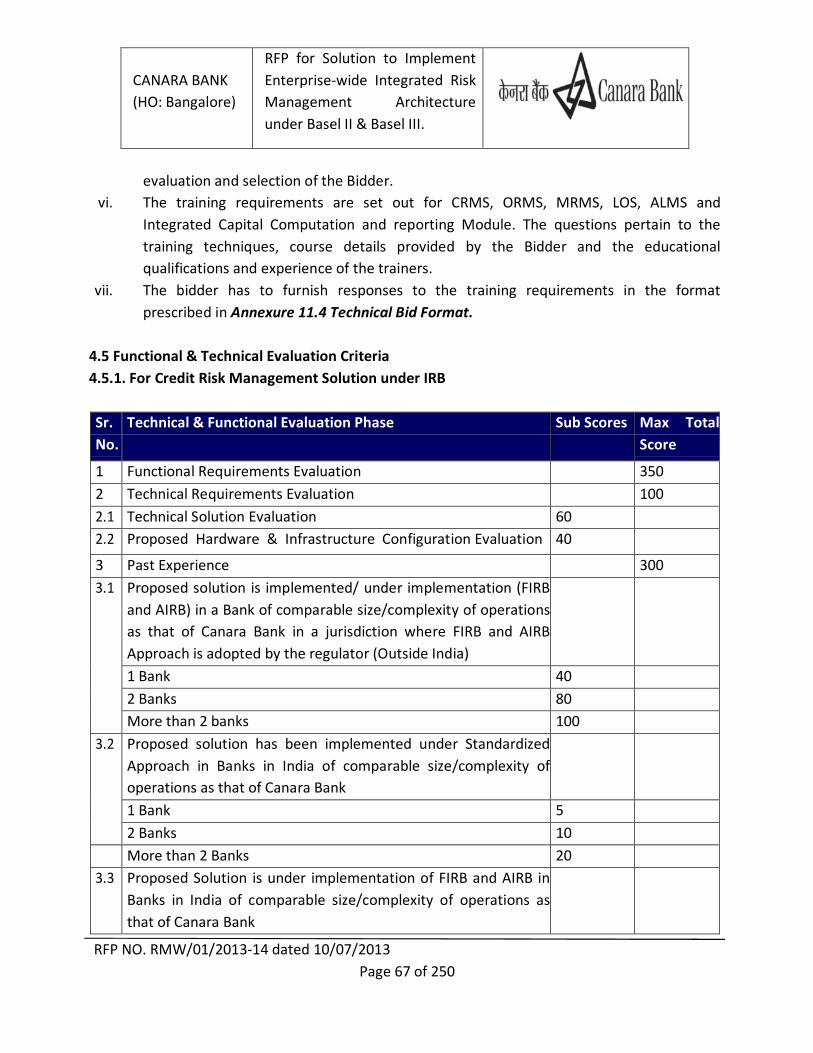

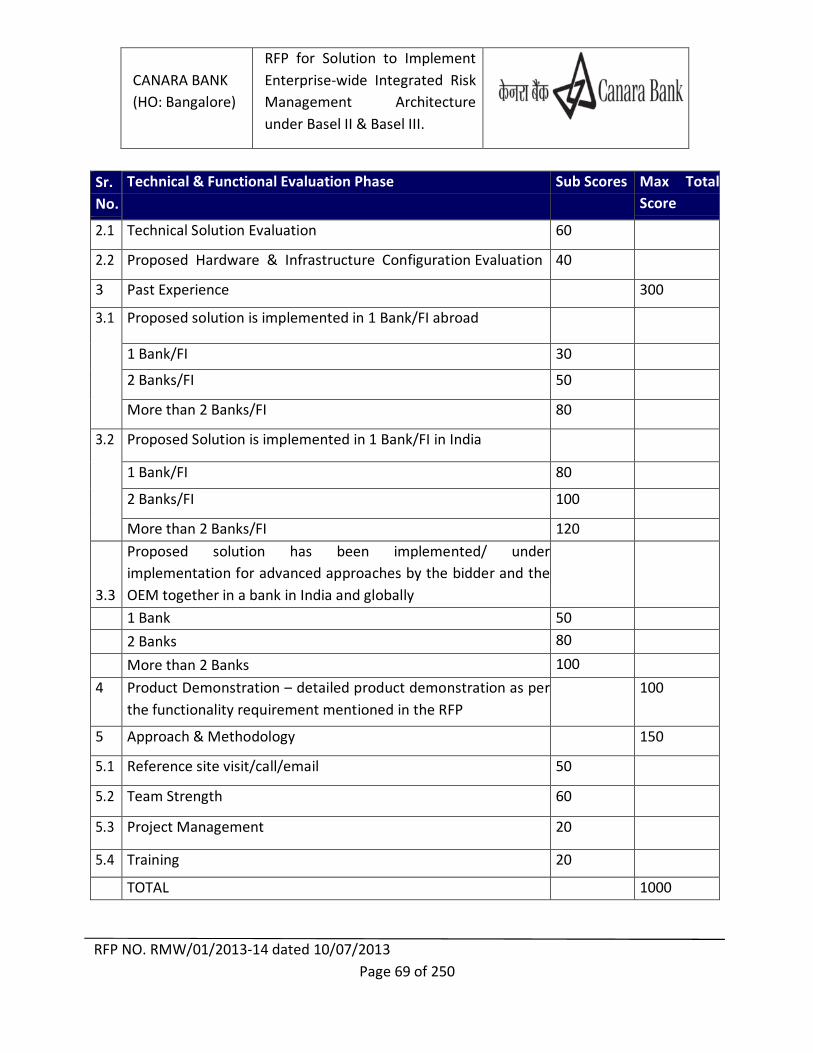

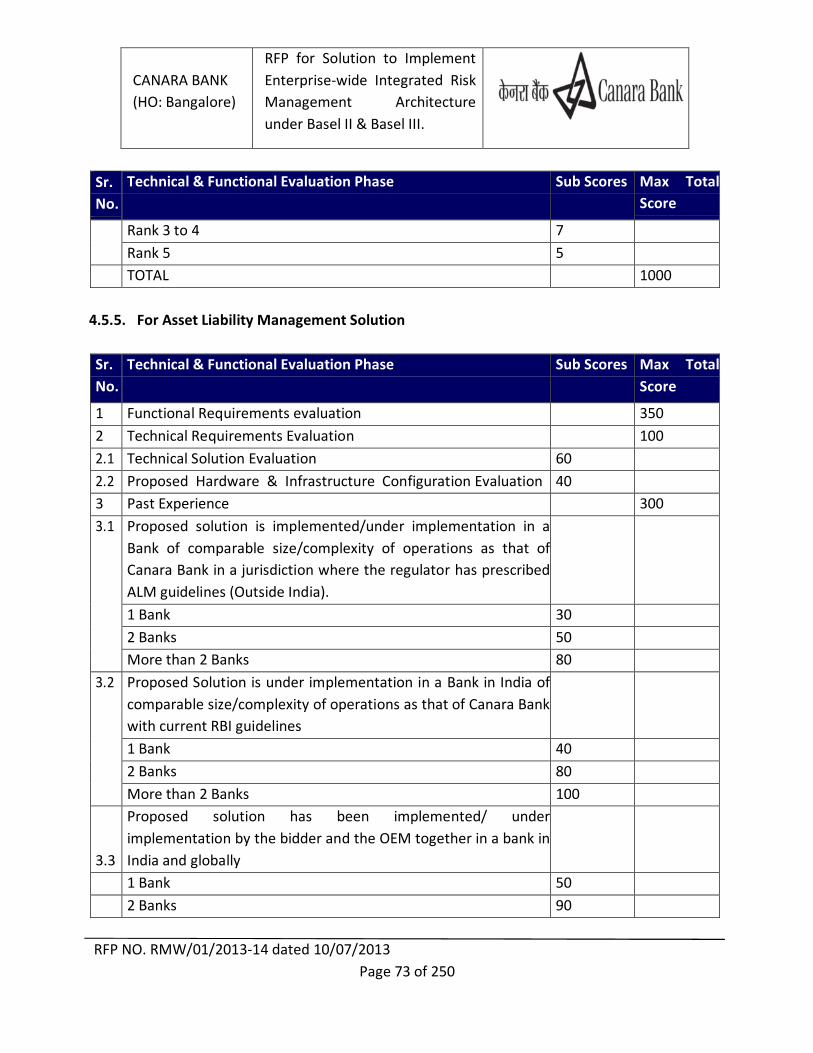

4.5 FUNCTIONAL AND TECHNICAL EVALUATION CRITERIA 67

4.6 SHORTLISTING OF TECHNICALLY QUALIFIED BIDDER 75

4.7 COMMERCIAL EVLUATION PROCESS 77

4.8 TECHNO-COMMERCIAL EVALUATION PROCESS 77

4.9 DISQUALIFICATION PARAMTERS IN TECHNICAL BID EVALUATION 78

5 OTHER TERMS & CONDITIONS 79

6 FUNCTIONAL REQUIREMENTS FOR CREDIT RISK 84

6.1 FUNCTIONAL REQUIREMENTS 84

6.2 HARDWARE REQUIREMENTS 115

6.3 TRAINING REQUIREMENTS 115

6.4 PROJECT MANAGEMENT METHODOLOGY 116

7 FUNCTIONAL REQUIREMENTS FOR OPERATIONAL RISK 118

7.1 FUNCTIONAL REQUIREMENTS 118

7.2 HARDWARE REQUIREMENTS 137

7.3 TRAINING REQUIREMENTS 137

7.4 PROJECT MANAGEMENT METHODOLOGY 138

8 FUNCTIONAL REQUIREMENTS FOR MARKET RISK 139

8.1 FUNCTIONAL REQUIREMENTS FOR MARKET RISK UNDER IMA 139

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 7 of 250

8.2 FUNCTIONAL REQUIREMENTS FOR ALM SYSTEM 166

8.3 HARDWARE REQUIREMENTS 183

8.4 TRAINING REQUIREMENTS 183

8.5 PROJECT MANAGEMENT METHODOLOGY 184

8.6 ADDITIONAL INFORMATION FOR MARKET RISK 186

9 INTEGRATED CAPITAL COMPUTATION & REPORTING MODULE 188

9.1 FUNCTIONAL REQUIREMENTS 188

9.2 HARDWARE REQUIREMENTS 189

9.3 TRAINING REQUIREMENTS 189

9.4 PROJECT MANAGEMENT METHODOLOGY 191

10 TECHNICAL SPECIFICATIONSACROSS ALL SYSTEMS/ RISK SOLUTIONS 192

11 ANNEXURE 201

11.1 UNDERTAKING FROM BIDDER 201

11.2 ELIGIBILITY CRITERIA FORMAT 202

11.3 COVER LETTER FOR TECHNICAL BID 203

11.4 TECHNICAL BID FORMAT 205

11.5 COVER LETTER FOR COMMERCIAL BID 213

11.6 COMMERCIAL BID (BILL OF MATERIAL) FORMAT 215

11.7 BID OFFER COVERING LETTER 224

11.8 REFERENCE SITE DETAILS 226

11.9 PARTICULARS OF BIDDER 227

11.1 PAST EXPERIENCE DETAILS 231

11.11 PERFORMANCE GUARANTEE FORMAT 233

11.12 MANUFACTURERS’ / PRODUCERS’/ AUTHORIZATION FORM 237

11.13 IMPLEMENTATION TEAM PROFILE 239

11.14 IMPORTANT PROJECT TIMELINES 242

11.15 LIST OF EXISTING APPLICATIONS 243

11.16 DATA CENTER AND DISASTER RECOVERY SITE OF GROUP ENTITIES 250

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 8 of 250

SCHEDULE OF ACTIVITIES AND EVENTS

RFP Reference RMW/01/2013-14

Date of issue of the RFP 10.07.2013

Last date and time for submission of

Queries by the Bidder

17.07.2013 - 3.00 PM

Date and time for Pre-Bid Meeting 25.07. 2013 - 3.00 PM

Date for publishing clarifications on

website

29.07.2013

Last date & time for submission of Bids:

Eligibility Criteria, Technical and

Commercial Proposals.

14.08.2013 - 3.00 PM

Place for submission of bids GM Secretariat

Risk Management Wing

2nd

Floor

Canara Bank Head Office

112 – J.C Road

Bangalore – 560002

Date and Time of Opening of Eligibility

Criteria and Technical Proposals

14.08.2013 - 4.00 PM

Bid document price (nonrefundable) Rs 1,00,000

Earnest Money Deposit Rs 50,00,000

Address for Communication GM Secretariat

Risk Management Wing

2nd

Floor

Canara Bank Head Office

112 – J.C Road

Bangalore – 560002

Email – [email protected]

Date for Technical Presentation Will be informed after 21.08.2013

Date and Time of Opening of Commercial

Proposals

Will be notified to the shortlisted

bidders.

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 9 of 250

Note:

a. Bids will be opened in the presence of bidders’ representatives who choose to attend on the

bid opening date.

b. The schedule is subject to change and notice of changes shall be published on the website of

the Bank. The Bank reserves the right to cancel the RFP at any time without incurring any

obligation to any bidder.

c. Any queries regarding RFP may be sent to Canara Bank GM’s Secretariat, Risk Management

Wing, 2nd

Floor, Head Office, 112 J.C Road, Bangalore - 560002 or via email to

d. The bidders may note that no further notice will be given in this regard. Further, in case the

Bank does not function on the aforesaid date due to unforeseen circumstances or holiday

then the bid will be accepted up to 03:00 PM on the next working day and bids will be

opened at 04:00 PM at the same venue on that day.

e. The RFP document can be downloaded from Bank’s website

http://www.canarabank.com/English/Scripts/Tenders.aspx.

f. Any bid without payment of bid document price and EMD will be rejected.

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 10 of 250

1. Introduction

1.1 Overview

Risk Management especially in the post financial crisis has become a significant function in

banks across the world. In the context of ongoing changes in financial landscape banks are

required to be ever more nimble and at the same time ensure that all the risks are managed

and/or mitigated effectively.

Canara Bank (herein after referred to as the ‘Bank’) views the current market dynamics and

resulting regulatory requirements as an opportunity to create an Integrated Risk Management

Framework that will create shareholder value by aligning the Bank’s business strategy to its risk

management policies, processes and systems. Over a period of time, Canara Bank has taken

various initiatives for strengthening risk management practices. Bank has an integrated

approach for management of risk and in tune with this, formulated policy documents taking into

account the Business requirements / best international practices and the supervisory guidelines.

These policies address different risk classes viz., Credit Risk, Operational Risk and Market Risk.

Over the years, Bank has earned the reputation of being technology savvy and one of the

Frontrunners among public sector banks in modern‐day banking trends. Having implemented its

Core Banking Solution in 2010, Bank is one of the first Public Sector Banks in the country to have

all domestic branches on a single Core Banking platform. Under this solution umbrella, all

branches and ATMs of BANK have been networked, with online Tele banking, net banking and

mobile banking facility made available to both its Core Banking Customers – individual as well as

Corporate. Regular banking services apart, the customer can also avail of a variety of other

value‐added services like Cash Management Service, Insurance, Mutual Funds and Demat.

Bank has a strong network of over 3600 domestic branches, 34 Circle Offices and 5 overseas

Branches, which are.

1. Canara Bank, London Branch

2. Canara Bank, Hong Kong Branch

3. Canara Bank, Leicester Branch

4. Canara Bank, Shanghai branch

5. Canara Bank, Manama, Bahrain

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 11 of 250

Bank is having plans to open more domestic and overseas branches in other jurisdictions.

The Bank has the following subsidiaries and group entities:

i. Canbank Venture Capital Fund Limited (CVCFL)

ii. Canbank Financial Services Limited (CANFINA)

iii. Canara Bank Securities Limited

iv. Canbank Factors Limited

v. Canbank Computer Services Limited (CCSL)

vi. Canara Robeco Asset Management Company Limited

vii. Canara HSBC Oriental Bank of Commerce Life Insurance Company Limited

viii. Can Fin Homes Limited

ix. Commercial Bank of India LLC, Moscow

x. Pragathi Gramin Bank (Regional Rural Bank)

xi. Kerala Gramin Bank (Regional Rural Bank)

1.2 Broad Scope of Work

The scope of project envisages a complete turnkey solution which includes design, sizing,

procurement, installation, customization, configuration, maintenance of the hardware, software

and other components required for an Enterprise Wide Integrated Risk Management (EWIRM)

Solution. This would also envisage parameterization, historical data management, verifying data

quality, migrating data, user acceptance testing, documentation, trainings, knowledge transfer

and support. The solution/s offered should be web based, open platform and support data

transfer and consolidation from both the networked and standalone systems either online or

dial up. The EWIRM Solution shall be implemented at the Bank and its group entities except

Canara HSBC Oriental Bank of Commerce Life Insurance Company Limited and Commercial Bank

of India LLC, Moscow.

Credit Risk Management is an important part of bank’s operations. This would help the bank in

keeping a check on the asset quality at appraisal level as well as on an ongoing basis. For moving

to advanced Approaches for credit risk, Banks have to classify exposures into specified

categories viz. Corporate, Sovereign, Bank, Retail, Equity and Others estimate various Risk

components viz. Probability of Default (PD), Loss Given Default (LGD), Exposure At Default (EAD)

and Effective Maturity (M) and comply with minimum standards as per the Basel II Internal

Ratings Based (IRB) Approach guidelines.

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 12 of 250

Bank has currently adopted Standardised Approach for Credit Risk under Basel II. Bank has put in

place four Credit risk rating models namely, RAM model, Manual model, Small Value model &

Portfolio model for assignment of Internal Ratings to the borrowers. In this regard, the Bank has

collated the required data for RAM Model validation since 2004 to 2012.Bank now intends to

adopt Advanced Internal Rating Based Approach (AIRB) for calculating capital charge for Credit

Risk.

Operational Risk, which is intrinsic to the bank in all its material products, activities, processes

and systems, is emerging as an important component of the enterprise‐wide risk management

system. Recognizing the importance of Operational Risk Management (ORM), the Bank has

adopted a Comprehensive Operational Risk Management Policy. This would entail the bank to

move towards enhanced level of sophistication in the years ahead and to capture qualitative

and quantitative aspects of operational risks in measurement and management of operational

risk.

Bank is presently under the Basic Indicator approach for Operational Risk Regulatory Capital

Calculation. Further the Bank has taken initiatives to progress towards adopting advanced

approaches. To achieve this objective, the Bank has planned to implement an Operational Risk

Management Solution (ORMS). Bank is also gearing up its risk management process for

migrating to advanced approach under Basel II operational risk estimation ‐ Advanced

Measurement Approach (AMA).

Market Risk Management is also an important part of overall risk management in Bank and it

covers both domestic and forex treasury operations. Bank is presently under Standardized

Modified Duration Approach for calculation of capital charge for Market Risk. Bank intends to

move to Advanced Approach under Basel II by adopting Internal Models Approach.

The Bank has a comprehensive system of internal controls, systems and procedures to monitor

and mitigate risk. The Bank has also institutionalized new product approval process to identify

the risks inherent in the new product and activities. The Bank has carried out a comprehensive

Self‐Assessment exercise spanning all the risk areas and evolved a road map to move towards

implementation of Basel II norms as per RBI’s guidelines. The program of Risk Management,

Organizational Structure, Risk measures, risk data compilation and reporting is getting

implemented for a period of time in the Bank with the strategic aim of migration to advanced

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 13 of 250

approaches which would help achieve long term benefits. The Bank has appointed a consultant

for assistance in the Bank’s initiative to migrate to advanced risk management approaches and

for the implementation of an Enterprise Wide Integrated Risk Management Architecture.

Bank recognizes the need for an enterprise wide risk management architecture where in

advanced risk management approaches are implemented within its subsidiaries and group

entities. All the subsidiaries and group entities of the Bank has a risk management function

including risk management policies and is guided by the Group Risk Management policy of the

Bank. The implementation of the enterprise wide integrated risk management architecture at

the Bank envisages roll out of advanced risk management approaches to all the subsidiaries and

group entities of the Bank.

The Bank has already taken steps in this direction and this Request For Proposal (RFP) is

intended to invite Techno‐Commercial bids from eligible Bidders to provide end‐to‐end

solutions for implementation of Credit Risk Management System (CRMS), Operational Risk

Management System (ORMS), Market Risk Management System (MRMS) and an Integrated

Capital Computation and Reporting Module for the advanced approaches under RBI Guidelines

on Basel II and Basel III to have an integrated risk management frame work, herein after

referred to as EWIRM Solution. The requirements under CRMS has been split into two sections

one for a CRMS in compliance with IRB requirements and second a Loan Origination System

(LOS). Similarly the requirements for MRMS have been defined for MRMS under IMA

Compliance and Asset Liability Management System (ALMS) including Fund Transfer Pricing

(FTP).

Within this RFP the terms bidder and system integrator (SI) have been used interchangeably.

Responsibilities of Bidder

Successful bidder based on this RFP terms and conditions should

(i) Implement the solution at all branches including overseas branches, and its subsidiaries

and group entities as decided by the Bank and should support multilingual requirements.

The system should:

a. Support estimation of all risk components and capital calculations (regulatory &

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 14 of 250

economic) as per the guidelines issued by RBI and Basel under the Standardized and

IRB approaches. The solution should be able to meet the Pillar I, II, III and stress

testing requirements as per RBI and Basel guidelines on Basel II and Basel III. The

solution should be capable of supporting all the required statistical, analytical, risk

modeling, pricing and reporting requirements as per regulatory and Bank’s internal

requirements.

b. Support operational risk measurement and modeling as per RBI and Basel II

requirements under AMA. ORMS should be available to the bank at Enterprise-wide

Level.

c. Be able to perform back testing, stress testing, calculate specific risk VaR and

Incremental risk VaR requirements as per Basel II, Basel III and RBI guidelines.

d. strengthen bank’s ALM system processes by complying with all ALM DGA

requirements by RBI.

e. Support home host country requirements for overseas operations and also

requirements of the subsidiaries and group entities of the Bank.

(ii) Provide data repository such as but not limited to list of KRI’s, Risk and Control, UAT

scenarios, Scenarios for scenario analysis with their due mapping, reporting templates

(iii) Set up, installation and testing of the required hardware and software within the Bank

including its data centers at Bangalore and Disaster Recovery Site in Mumbai. Ensure in

coordination with the Bank that the solution is accessible from all across the Bank

including overseas branches, its subsidiaries and group entities. Details of data center

and disaster recovery site of the subsidiaries and group entities are furnished in

Annexure no. 11.16.

(iv) Offer Facilities Management support for EWIRM solution and associated IT Infrastructure

proposed by the bidder for the entire project duration.

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 15 of 250

(v) Impart training on EWIRM solution to designated personnel of the Bank and its

subsidiaries and group entities including users, technical personnel handling the system

and trainers.

(vi) Provide Hand-over of the solution at the end of the agreed period post UAT signoff.

(vii) Ensure system is in compliance with RBI requirements for all Basel II advanced

approaches and Basel III and other relevant regulatory guidelines. Any instances of non-

compliance observed will need to be rectified at no additional cost and well within

timelines stipulated by the regulator

(viii) Incorporate changes in system arising on impact of amendment to regulations/bank’s

policy at no additional cost and well within timelines stipulated by the regulator

(ix) Assist the bank in conducting the User Acceptance tests

(x) Provide complete documentation including logic used, empirical analysis done,

methodology etc. as per regulatory and audit requirements

(xi) Provide all statutory, regulatory Management Information System (MIS), adhoc MIS

(including development if needed) and Executive Information System (EIS) reports as

required by the Bank and its subsidiaries and group entities in the desired format as per

regulatory and Bank’s requirements

(xii) Meet all requirements specified in this RFP

The Bidder should implement the EWIRM Solution compliant with Basel II advanced approaches

and Basel III at the Central Processing Center (CPC), Head Office, all the Circle Offices, domestic

branches, overseas branches, subsidiaries and group entities and demonstrate their capability as

per agreed number of site demonstrations at group entities. The solution will be implemented in

branches/Administrative offices/subsidiaries/group entities as decided by the Bank.

In case the product/ solution/ vendor/ OEM is taken over/ amalgamated/ dissolved the impact

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 16 of 250

of such an event should not have any adverse implication on the service level/ time line/cost

that have been proposed for implementation of the solution.

1.2.1 Solution Design, size and procurement

(i) Selected bidder is required to design, size, procure and implement the EWIRM Solution

with the functionalities identified in the Functional Requirements and Technical Solution

Requirements for Credit Risk Management, Operational Risk Management, Market Risk

Management and Integrated Capital Computation and Reporting as detailed across this

RFP.

(ii) Automated Interfaces required of the solution with other internal system solution and

outside system solution has to be provided by the selected bidder to ensure satisfaction

of the functional and technical requirements. Bidder will be responsible for the

procurement of any tool required to develop the interface. Bidder will document the

entire interface logic and process with change management procedures in compliance

with Bank’s policies and procedures.

(iii) The selected bidder is expected to leverage the bank’s existing datacenter services, EDW

infrastructure (as and when operational), SAN storage, backup tape libraries, archival,

legacy data etc. With the endeavor to reduce the overall cost of procurement to the

Bank, the bidder shall also continuously explore avenues to reduce the cost and act in

the best interest of the Bank.

1.2.2 Gap identification & Resolution

The selected bidder will be responsible for conducting the gap assessment of the EWIRM solution

with bank’s framework, policy, procedures, governance, methodology, approach, existing

system, tools, models, reports, Basel II, Basel III and other regulatory guidelines issued by RBI etc.

pertaining to Credit Risk Management, Operational Risk Management, Market Risk Management

and Integrated Capital Computation and Reporting, in order to implement EWIRM solution as per

this RFP requirements and to:

1. Provide the Bank with the gap identification report along with the recommendations and

estimated time frames to implement the same

2. Determine the customization requirements, in case a particular functionality / requirement is

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 17 of 250

not supported by the existing version of the EWRIM solution;

3. Resolve gaps by customizing the proposed solution by way of modifications / enhancements,

as necessary

1.2.3 Parameterization, Configuration and Customization of software

1. The Bidder shall be responsible for accuracy of the parameters set in the system according

to business needs of the Bank.

2. The cost of all customizations is required to be included in the Commercial Bid and the Bank

will not make any additional costs for this throughout the term of the contract if the same

has been specified as a requirement of Canara Bank in this RFP. Thus, this is a fixed bid and

all necessary customizations based on the functional requirements specified in the RFP will

need to be conducted by the Bidder.

3. Bidder needs to give detailed plan for customization. All customization has to be completed

within the project timelines.

4. The Bidder should ensure that the quality assurance and development standards outlined in

the development methodology are adhered to and required functionalities/reports related

to same are generated and shared with the Bank team on a regular basis

5. Enhancements provided by the Bidder would include changes in the software due to

Statutory and Regulatory changes and those required due to changes in industry practices in

India and/or abroad or any other requirements of the Bank related to the above, which will

need to be provided at no extra cost to the Bank for the entire period of the contract. It will

include, but not limited to, all the functionalities mentioned in the Functional Requirements

and at no additional costs.

1.2.4 Testing

1. The Bidder will be responsible for conducting system integration testing to verify that all

system elements have been properly integrated and that the system performs all its

functions.

2. Bidder will conduct a “User Acceptance Test” (“UAT”) under guidance, review and

supervision of the bank to ensure that all the functionality required by the Bank is available

and is functioning accurately as per the expectations of the Bank.

3. Bidder will be responsible for setting and maintaining the test environment during the entire

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 18 of 250

period of project implementation and will ensure its configuration and parameterization for

conducting the UAT as per bank's risk management framework and in compliance with this

RFP’s requirements. The bidder shall ensure that the test environment has the same

configuration and functionalities as that of the production environment.

4. The Bidder will provide the scenarios for UAT and assist in preparing test cases including the

test data to support all the Business scenarios. The Bidder should dedicate resources (from

Bidder as well as OEM team) to work with the Bank’s project team for this purpose.

5. The Bidder will assist the Bank in analyzing / comparing the results of testing.

6. Bidder shall provide adequate resources for trouble-shooting during the entire UAT process

of the Bank.

7. The Bidder will be responsible for maintaining appropriate program change control and

version control of the system as well as documentation of UAT and change of configuration

and parameterization after making changes in the system.

8. All errors, bugs enhancements/ modifications required during and after testing will be

resolved within the overall timelines for implementation. Sign – off for the same will be

obtained from the Bank prior to implementing the work around, in respect of errors and

bugs affecting the functioning of the Bank.

9. The Bidder will be responsible for using appropriate tools for logging, managing, resolving

and tracking issues and its progress, arising out of testing and ensuring that all issues are

addressed in a timely manner to the satisfaction of the Bank and as per requirements

mentioned in this RFP.

1.2.5 Training

The Bidder shall be responsible for training the employees of the Bank including overseas

branches and its subsidiaries and group entities in the areas of system administration,

implementation, use / operations, management, database management, error handling /

troubleshooting, etc. of the EWIRM Solution.

Structure of the training program covering number of trainings, locations and number of

participants etc. is to be advised by the bidder.

Bidder will also be responsible to develop training and reference materials for all the

functionality of the software. Training / reference materials should be designed separately for

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 19 of 250

operational staff / user, IT department and senior management. Training material should

comprehensively cover all the functionality of the proposed EWIRM solution and be written in a

user friendly manner with use of graphs, processes flows, screen-shots of the actual system

functionality etc.

Bidder should provide Bank specific training material designed considering its requirements in

this RFP. Training material so provided will be subject to review and sing-off by the bank as a

project deliverable.

The training should at least cover the following areas:

• Functionality available in the solution including logic and methodology of the same;

• Customization / Parameterization;

• Techniques for Slicing and dicing of data, information, and output

• Auditing techniques including generation of audit trail reports;

• Advanced trouble shooting techniques;

• Techniques for generation, view and reporting of intermittent results;

• Deployment of various processes, risk reporting and identification procedures,

application of controls, analysis procedures provided as part of the solution;

• Techniques of Customization, development and configuration of required reports

including ad-hoc reports from the solution provided;

• Development and deployment of new functionalities using the proposed solution;

• System & Application Administration such as creation of user, user groups, assigning

rights, System Information Security Settings etc.

• Perform Impact Analysis using the solution;

• Business use of the solution

As per the requirements defined in this RFP, bank may increase more areas of trainings which

bidder would be liable to provide.

1.2.6 Implementation

The proposed solution should cover all the existing branches/units/administrative offices as

decided by the Bank and have the capability to scale up for meeting future requirements.

The solution should be scalable and capable to handle increased volumes. In the event the bank

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 20 of 250

adds/changes/updates source/core banking systems in the future the solution should be flexible

to handle such new source systems.

The Bidder will have to provide the necessary interface to all the applications as required. The

list of Bank’s existing applications in the Bank and its Group Entities is detailed later in Annexure

11.15.

At present, the Bank’s Core Banking Solution is in Oracle Database. The database for EWIRM

Solution should be compatible to CBS (Oracle). The successful bidder shall be responsible for

taking up with the system integrator of CBS for the required data. Ultimately, the EWIRM Risk

Solutions shall be linked to Enterprise Data Warehouse (as and when operational). The

successful bidder shall coordinate with EDW integrators for the requirements. The proposed

solution should be compatible both the platforms i.e. Intel & AIX.

By means of diagrammatic / pictorial representations, the Bidder should provide complete

details of the hardware, software and network architecture of the EWIRM Solution (module and

sub‐module wise), including source / method of Data capture and transfer, validation, updation

and database maintenance for networked and non‐networked branches.

The Bidder should assist for implementation in 100 branches/units /administrative offices and

subsidiaries and group entities spread across the country (along with all the Circle Offices) on

pilot basis. The Bidder should install and commission the solution and integrate with the Bank’s

applications at domestic branches, overseas branches, subsidiaries and group entities. The

branches for pilot implementation would be decided by the Bank.

The system should be implemented in all the remaining units after its satisfactory working in

100 branches/units/administrative offices and implementation in all the units should be

completed within 12 months from the date of signing of contract.

Details of functional and technical requirements are provided in Section 6, Section7, Section 8,

Section 9 & Section 10: Functional Requirements & Technical Requirements of this document.

The Bidder should provide hardware systems, operating system, database, for EWIRM solution

including CRMS application software, ORMS application software, MRMS application software,

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 21 of 250

Integrated Capital Computation and Reporting module application software and other necessary

software & hardware required for the successful implementation of the proposed solution

including DR site of equal capacity as live including data replication requirements (at the end

of day) along with data replication solution and a required Test server (Application &

Database Server).Firewall & Network Security will be provided by the Bank. The Bidder has to

ensure that vulnerabilities at application level in case of any breach shall be handled by the

offered application software.

The Bidder has to upgrade servers/ storage at no extra cost to the Bank, in case the offered

configuration does not meet the requirements, for 7 years from the implementation start date.

The total storage provided/ proposed by the bidder shall take into account incremental growth

of the Bank over the next 7 years and should be in RAID 5 or RAID 1+0. The Bidder may propose

a Network Attached Storage (NAS) / Storage Area Network (SAN) to meet the requirements as

found suitable. The proposed hardware at the data center must be in active‐passive cluster with

external SAN storage with back up tape library and support RAID 0 to 5 with no single point of

failure.

A complete Bill of Material for the hardware required for the successful operation of the

solution should also be provided by the Bidder, with full particulars like make, model, part

numbers, proposed configuration, including all details like memory type proposed with future

expandability, processor type, number of processors, processor speed, future expandability, bus

speed, etc. and clearly show no single point of failure. Please refer Annexure 11.4 Technical Bid

Format (sub sections on hardware requirements) and Annexure 11.6: Commercial Bid (Bill of

Material) Format.

The Bidder should specify the hardware requirement taking into consideration the efficiency

level, response time, data processing requirement, number of users, and all other parameters to

ensure that the efficiency of software system is not affected because of hardware. Bidder should

provide details for DR site such as network and security requirements, switches, routers etc. The

Bidder will certify that the hardware specified is adequate for meeting performance standards

set by the Bank, and it takes full responsibility of upgrading hardware without any extra cost to

the Bank, if at the time of implementation or any time subsequently it is found that the

hardware specified requires upgrade. At any point in time during the contract period, the CPU

utilization should neither exceed 60% nor should the Hard Disk utilization exceed 60% at the

Primary Data Centre. In case the hard disk utilization exceeds 60%, the additional hardware has

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 22 of 250

to be provided by the Bidder at no further cost.

The Bidder must ensure no hardware equipment or software, for which ‘End‐‐‐‐of‐‐‐‐Sale’ has been

declared, is offered as part of this bid. None of the hardware or software should have an ‘End‐‐‐‐

of‐‐‐‐Support’ mandated by the respective OEM within seven years from date of completion of

the project and the bidder should ensure continuity at all times without disruption of

operations.

The Bidder should also provide the Bank with the number of racks required for the servers /

equipment and associated infrastructure, as well as power requirements (average, peak and

rated power) and any other specific requirements for the servers / equipment (Network and

security requirements, switches, routers etc.) and associated infrastructure for both DC (Data

Centre) & DR (Disaster Recovery) sites.

Sizing of equipment, hardware etc. as required, depending on the functionalities required by the

bank as mentioned in the RFP, should be provided by the Bidder for processing of existing

portfolio of the Bank/Group with increase in volumes at approximately 20% p.a. and addition of

new products/instruments and data maintenance for a minimum period of 7 years as per RBI

guidelines.

The Bidder has to give an undertaking to implement the solution at any location / branch

identified by Bank at no extra cost.

As part of implementation all data migration (as and when required) from the existing systems

to the system proposed will be done by the Bidder. The Bidder shall demonstrate to the

satisfaction of the Bank regarding accuracy and comprehensiveness of the data migrated to the

proposed system.

During the period of contract, if any of the subsidiaries or group entities of Canara Bank get

merged, the data of the merged entity needs to be migrated and integrated to the central

database which needs to be provided at no extra cost. Similarly if any of the subsidiary and

group entity goes out of Canara Bank, the data relating to such entity needs to be extracted and

stored separately at no additional cost. During the period of contract if any entity gets merged,

the bidder shall facilitate such mergers of databases and if necessary provide suitable solution

on mutually agreed terms.

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 23 of 250

1.2.7 Facilities Management Services (FMS) and Helpdesk

The Bidder is required to provide Helpdesk services till the completion of the implementation

across Bank and its group entities. Facility Management services will be provided by the bidder

till the end of the project. The bidder is required to indicate the resource requirements for FMS

in the Bill of Material.

Facilities Management: Facilities Management would include support for all hardware,

application software, etc. which would be provided by the Bidder. Bidder should elaborate on

FMS like number of resources to be deployed post implementation and detail it accordingly in

Bill of Material. FMS services should be provided for entire project duration (1 year

implementation and 6 years maintenance)

Helpdesk: Helpdesk refers to availability of resources to record and respond to events and

incidents related to the application, hardware & software implemented as per the scope of this

RFP. Helpdesk services should be provided till implementation is completed. At any point of time

during the day a minimum of two resources shall be available.

Uninterrupted services of helpdesk shall be available to all the domestic and overseas branches

situated in different time zones all through their respective working hours.

During AMC period the requirements are specified in section 3.3: Warranty and Annual

Maintenance.

1.2.8 Information Security

System should have standard input, communication, processing and output validations and

controls. System hardening should be done by bidder. Access controls at DB, OS, and Application

levels should be ensured in compliance to the Information Security Policy of the Bank.

1.3 Invitation for Bids

The Bank invites RFP for a turnkey project for implementation of EWIRM Solution for advanced

approaches under Basel II, Basel III and RBI guidelines. The broad scope of the project envisages

installation, customization, parameterization, implementation, and maintenance of application

software, system software, database, interfaces etc. as well as supply, installation &

maintenance of related hardware at primary and disaster recovery data centers of the Bank,

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 24 of 250

with training to designated personnel of the Bank and its subsidiaries and group entities.

Each Bidder should notify the Bank of any error, fault, or discrepancy found in this RFP

document but not later than 12.07.2013. The Bank’s responses to the queries raised by

proposed bidders will be put on the Bank’s website.

The Bidders shall, by responding to the Bank’s RFP document, be deemed to have accepted the

terms as stated in this RFP document.

The bidder shall ensure compliance of Central Vigilance Commission guidelines (CVC) issued/ to

be issued from time to time pertaining to works covered under this RFP.

1.3.1 Disclaimer

The information contained in this Request for Proposal (RFP) document for implementation of

EWIRM Solution under Basel II and Basel III or information provided subsequently to Bidder(s) or

applicants whether verbally or in documentary form by or on behalf of the Bank, is provided to

the Bidder(s) on the terms and conditions set out in this RFP document and all other terms and

conditions subject to which such information is provided. The RFP document contains

statements derived from information that is believed to be true and reliable at the date

obtained but does not purport to provide all of the information that may be necessary or

desirable to enable an intending contracting party to determine whether or not to enter into a

contract or arrangement with Bank in relation to the provision of services.

The RFP document is not a recommendation, offer or invitation to enter into a contract,

agreement or any other arrangement, in respect of the services. The provision of the services is

subject to observance of selection process and appropriate documentation being agreed

between the Bank and any successful Bidder as identified by the Bank, after completion of the

selection process as detailed in this document. No contractual obligation whatsoever shall arise

from the RFP process unless and until a formal contract is signed and executed by duly

authorized officers of Canara Bank with the Bidder. Each Bidder should conduct their own

investigations and analysis and should check the accuracy, reliability and completeness of the

information in this RFP and where necessary obtain independent advice. The Bank makes no

representation or warranty and shall incur no liability under any law, statute, rules or

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 25 of 250

regulations as to the accuracy, reliability or completeness of this RFP. The Bank may, at its

absolute discretion, but without being under any obligation to do so, update, amend or

supplement the information in this RFP.

2. Instructions for Bid Submission

2.1 General Instructions

2.1.1 Cost of Application/ Bid Document

Application Money of `1,00,000/‐ (Rupees One Lakh only) by way of Demand Draft/ Banker’s

Cheque/ Pay Order issued by a Scheduled Commercial Bank favoring Canara Bank, payable in

Bangalore, which is non‐refundable, must be submitted separately along with RFP response.

The RFP documents can be downloaded from Bank’s Website and Govt. Web site (National

Information Center Website). The cost of application/bid document should be deposited at the

time of submitting the response.

All costs and expenses (whether in terms of time or material or money) incurred by the

Recipient/ Bidder in any way associated with the development, preparation and submission of

responses, including but not limited to attendance at meetings, discussions, demonstrations,

site visits, etc. and providing any additional information required by the Bank, will be borne

entirely and exclusively by the Bidder.

2.1.2 Bid Security (E.M.D)

The Bidder shall furnish, as part of their Bid, a Bid security in the form of Demand Draft/Banker’s

Cheque/ Pay order only. The Bid security is required to protect the Bank against the risk of

Bidder’s conduct, which would warrant the security’s forfeiture.

The Bid security shall be denominated in Indian Rupees and shall be in the following form:

• Demand Draft/Banker’s Cheque/ Pay Order, issued by a Scheduled Commercial Bank in

India, drawn in favor of Canara Bank payable at Bangalore for a sum of `50,00,000/‐(Rupees

Fifty Lakhs Only).

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 26 of 250

Any Bid not secured as detailed above, will be rejected by the Bank, as non-responsive.

Unsuccessful Bidders’ Bid security will be refunded within 30 days after signing the agreement

with the successful bidder without any interest.

The successful Bidder’s Bid security will be discharged upon the Bidder signing the Contract and

furnishing the performance guarantee as per the format mentioned in Annexure 11.11:

Performance Bank Guarantee. No interest will be paid on the bid security

Bank reserves the right to forfeit the Bid security for any of the following reasons:

• If a Bidder withdraws their Bid after the due date of submission and during the period of Bid

validity specified by the Bidder on the Bid Form; or

• If a Bidder makes any statement or encloses any form which turns out to be false / incorrect

at any time prior to signing of Contract; or

• In the case of a successful Bidder, if the Bidder fails:

- To sign the Contract within a period of 21 days from the date of communication of the

results to the bidder by the Bank; OR

- To furnish Performance Guarantee as mentioned in Section 3.1.7: Performance Bank

Guarantee herein.

2.1.3 Registration of RFP Response

Registration of RFP response will be effected by the Bank by making an entry in a separate

register kept for the purpose upon Bank receiving the RFP response in the above manner. The

registration must contain all documents, information, and details required by this RFP. The

submission should be in the format outlined in this RFP and should be submitted only through

hand delivery.

If the submission to this RFP does not include all the documents and information required or is

incomplete or submission is through Fax mode, the RFP response is liable to be summarily

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 27 of 250

rejected. All submissions, including any accompanying documents, will become the property of

Bank. The Bidder shall be deemed to have licensed, and granted all rights to the Bank to

reproduce the whole or any portion of their submission for the purpose of evaluation, to

disclose the contents of the submission to other Bidders who have registered a submission and

to disclose and/or use the contents of the submission as the basis for any resulting RFP process,

notwithstanding any copyright or other intellectual property right of the Bidder that may subsist

in the submission or accompanying documents.

2.1.4 Request for Additional Information

Bidders are required to direct all communications for any clarification related to this RFP, to the

designated Bank officials and must communicate the same in writing (address for

communication as given in table of schedule of activities and events). All queries relating to the

RFP, technical or otherwise, must be in writing only i.e. either via physical or electronic mail. The

Bank will try to reply, without any obligation in respect thereof, every reasonable query raised

by the Bidder in the manner specified. All responses posted in the website shall be part of the

RFP.

However, the Bank will not answer any communication reaching the bank later than 3.00 PM on

17.07.2013 this being the last date to receive clarifications.

The Bank may in its absolute discretion seek, but will be under no obligation to seek, additional

information or material from any Bidders after the RFP closes. Such information sought by the

Bank and material provided by the Bidder will be taken to form part of that Bidder’s response.

The Bank may in its sole and absolute discretion engage in discussion with any Bidder (or

simultaneously with more than one Bidder) after the RFP closes to clarify any response.

2.1.5 Pre‐‐‐‐Bid Meeting

The Bank plans to hold a pre‐bid meeting on 25.07.2013 at 3.00 p.m. at the address specified in

Bid details under introduction note in order to bring greater clarity on the scope of work and

terms of the RFP being floated. The Bidders are expected to use the platform to have all their

queries answered. Bidders are requested to send their queries relating to RFP to our office by e‐

mail, well in advance (latest by 17.07.2013 3.00 pm), so that the same could be discussed during

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 28 of 250

the Pre‐Bid meeting with interested Bidders. All queries along with bank responses will be

uploaded on the bank website on 29.07.2013.

Interested Bidders will be allowed to participate in the Pre‐Bid meeting. Also, bank will allow a

maximum of 2 representatives from each Bidder to participate in the pre‐bid meeting.

Non‐attendance at the Pre‐bid Meeting will not be a cause for disqualification of a Bidder.

The Bank will have liberty to invite its project/technical consultant or any outside agency,

wherever necessary, to be present in the pre‐bid meeting to reply to the queries of the Bidders

in the meeting.

2.1.6 Disqualification

Any form of canvassing/ lobbying/ influencing/ query regarding short listing, status etc. will

result in a disqualification of the Bidder. The Bank reserves the sole right to disqualify any

prospective bidder and no obligation to discuss regarding the same with the concerned bidder

being disqualified.

2.1.7 Language of Bid

The language of the bid response and any communication with the Bank must be in written

English only. Supporting documents provided with the RFP response can be in another language

so long as it is accompanied by an attested translation in English, from a recognized translator,

in which case, for purpose of evaluation of the bids, the English translation will govern. The Bank

reserves the right to accept or reject the translated scripts after performing reasonable due

diligence. The Bidder shall submit a fresh translation from another translator in case Bank is not

satisfied with the current one.

2.1.8 Period of Validity of Bids

Bids should remain valid for the period of at least six (6) months from the last date for

submission of bid prescribed by the Bank. A bid valid for a shorter period shall be rejected by the

Bank as non‐responsive. In case the last date of submission of bids is extended, the Bidder shall

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 29 of 250

ensure that validity of bid is reckoned from modified date for submission.

2.1.9 Amendment of RFP and Bidding Documents

At least 7 days prior to the last date for bid‐submission, the Bank may, for any reason, whether

at its own initiative or in response to clarification(s) sought from the prospective Bidders, modify

the RFP contents/ covenants by amendment. Clarification /amendment, if any, will be notified

on Bank’s website. No individual communication would be made in this respect. In case any

bidder has submitted the bid prior to the amendment has the right to resubmit the bid by

modifying or withdraw the bid. The bid last submitted or bid modified by the bidder will be

considered for evaluation.

2.1.10 Authorization to Bid

The proposal/ bid shall be signed by authorized representative backed by proper authority

/authorization/ resolution of the bidder and the bid submitted by the said authorized person

shall be binding on bidder.

• All pages of the bid shall be initialed by the person or persons signing the bid.

• Bid form shall be signed in full only in blue ink & official seal of the bidder affixed.

• Any inter-lineation, erasure or overwriting shall be valid only if they are initialed by the

person or persons signing the Bid.

• All such initials shall be supported by an official seal of the Bidder’s firm.

The proposal/bid must be accompanied with an undertaking letter duly signed by the

designated personnel as provided in Annexure 11.1 Undertaking From Bidder. The letter should

also indicate the complete name and designation of the designated personnel.

2.2 Documents Comprising the Bid

The Bidder has to submit 2 copies of the response and a soft copy of the complete technical Bid

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 30 of 250

in Microsoft Office 2007 / Open Office format on a Compact Disc (CD) super‐scribing “Soft Copy

of Technical Bid against RFP– RMW/01/2013-14 dated 10.07.2013” along with the technical bid.

The Bidder will not furnish the softcopy of the commercial bid.

The Bid prepared by the Bidder should comprise the following components:

1. ENVELOPE – I: Eligibility Criteria:

Separate envelopes with superscriptions as “Eligibility Criteria” should be included within the

overall Envelope. The Bidder should submit the following:

a. The sheet mentioning compliance/ non‐compliance to all the eligibility criteria

specifications with remarks and other requirements given in Annexure 11.2: Eligibility

Criteria Format.

b. All the proofs required for eligibility criteria as mentioned in Section 4.3: Eligibility Criteria

Format

Bid Document Cost and Bid Security: Separate envelopes with superscriptions as “Bid

document cost” and “Bid Security” should be included within the overall Envelope. The Bidder

should submit the following:

c. Cost of Application/ Bid Document – a Demand draft/Bankers Cheque/Pay Order of

`1,00,000 and Bid Document

d. Bid Security (Earnest Money Deposit) – a Demand draft/Bankers Cheque/Pay Order of

`50,00,000

2. ENVELOPE – II: Technical Bid :

Technical Bid: Separate envelopes with superscriptions as “Technical Bid and Masked

Commercial Bid” should be included within the Envelope II.

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 31 of 250

a. Technical Bid

b. Masked Commercial Bid

The Bidder should submit compliance / non‐compliance to all the specifications with remarks

and other requirements given in the Bid Document and Scope of Work.

The Technical Bid should be complete in all respects and contain all information asked for,

except commercial prices. The Technical Bid should include all items asked for in bid document.

The technical offer should not contain any price information. The Technical Offer should be

complete and indicate that all products and services asked for are quoted. For example, the

Technical Bid should mention that Annual Maintenance Charges (AMC) etc. are included in the

Commercial Bid, without mentioning the actual amounts in the Technical Bid and terms of

Payment, Delivery and any other conditions, which may appear in the Commercial Bid. The

Bidder should enclose a copy of the Masked Commercial Bid (as per the format provided in

Annexure 11.6.2) as per price schedule without the prices (please put ‘X’ mark wherever prices

are quoted) along with other bid documents for evaluation purpose.

3. ENVELOPE – III: Commercial Bid:

The Commercial Bid should give all relevant price information and should not contradict the

Technical Offer in any manner. Please note that if any envelope is found to contain both

technical and commercial bid together, that bid will be rejected.

The details required under Annexures as mentioned in section 2.2.1 below shall also be

enclosed. The Bank may reject any proposal not containing all the requirements called for in

Annexures.

The Technical Bid of the eligible Bidders will be opened first for evaluation. Final bidder would

be decided by Techno – Commercial Evaluation.

Prices quoted by the Bidder shall be fixed during the Bidder’s performance of the Contract and

shall not be subject to variation on any account, including exchange rate fluctuations, changes in

taxes, duties, levies, charges etc. A Bid submitted with an adjustable price quotation will be

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 32 of 250

treated as nonresponsive and will be rejected. All costs proposed by the Bidder will have to be

rational. Details of total costs provided will have to be in line with the itemized costs.

2.2.1 List of Documents

Envelope Documents Reference

ENVELOPE –I

Eligibility Criteria

Eligibility Criteria Annexure 11.2: Eligibility Criteria

Cost of Application/

Document

Section 2.1.1: Cost of Application/ Bid

Document

Bid Security (Earnest Money

Deposit)

Section 2.1.2: Cost of Application/ Bid

Document

ENVELOPE – II

Technical Bid

Technical Bid

Undertaking from Bidder Annexure 11.1: Undertaking from Bidder

Bid Offer Covering Letter Annexure 11.7: Bid Offer Covering Letter

Cover Letter for Technical Offer Annexure 11.3: Cover Letter for

Technical Bid

Technical Bid Format Annexure 11.4: Technical Bid Format

Reference Site Details Annexure 11.8: Reference Site Details

Particulars of Bidder Annexure 11.9: Particulars of Bidder

Past Experience Details Annexure 11.10: Past Experience Details

Manufacturers’/ Producers’

Authorization Form

Annexure 11.12: Manufacturers’/

Producers’ Authorization Form

Implementation Team Profile Annexure 11.13: Implementation Team

Profile

Project Timelines Annexure 11.14: Important Project

Timelines

Masked Commercial Bid Annexure 11.6.2: Masked Commercial

Bid (Bill of Material) Format

Compact Disc Section 2.2. Documents comprising the

Bid

ENVELOPE – III:

Commercial Bid

Commercial Bid

Cover Letter for Commercial

Bid

Annexure 11.5: Cover Letter for

Commercial Bid

Commercial Bid (Bill of Annexure 11.6: Commercial Bid (Bill of

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 33 of 250

Envelope Documents Reference

Material) Format Material) Format

2.2.2 Sealing and Marking of Bids

1. The Bidder has to submit 2 copies of the response and a soft copy of the complete technical

Bid in Microsoft Office 2007 / Open Office format on a Compact Disc (CD) super‐scribing

“Soft Copy of Technical Bid against RFP–RMW/01/2013-14 dated 10.07.2013” along with

the technical bid. The Bidder will not furnish the softcopy of the commercial bid.

2. The Bidder shall seal the envelopes containing “Envelope – I: (a) Eligibility Criteria, (b) Cost

of application and Bid security”, “Envelope – II: Technical Bid” and “Envelope – III:

Commercial Bid” separately and the three envelopes shall be enclosed and sealed in a

SINGLE OUTER ENVELOPE marked as

“ORIGINAL: Solution to Implement Enterprise Wide Integrated Risk Management

Architecture under Basel II and Basel III Guidelines‐‐‐‐FINAL BID”

3. The inner and outer envelopes shall:

a. be addressed to the Bank at the address given; and

b. bear the following in separate envelopes

i. “Solution to Implement Enterprise Wide Integrated Risk Management Architecture

under Basel II and Basel III –Eligibility Criteria”

ii. “Solution to Implement Enterprise Wide Integrated Risk Management Architecture

under Basel II and Basel III – Non‐Price Bid (Technical Bid)”,

iii. “Solution to Implement Enterprise Wide Integrated Risk Management Architecture

under Basel II and Basel III – Price Bid (Commercial Bid)”,

c. All envelopes should indicate on the cover the name and address of the Bidder.

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 34 of 250

4. If the outer envelope is not sealed and marked, the Bank will assume no responsibility for

the bid’s misplacement or premature opening.

2.3. Key Guidelines for preparing RFP response:

Bidder’s proposal should strictly conform to the specifications mentioned here in the RFP.

Proposals not conforming to the specifications will be rejected subject to the Bank’s discretion.

Any incomplete or ambiguous terms / conditions / quotes may result in disqualification of the

offer at Bank’s discretion. The Bidder has to offer specific remarks for technical requirements

and clearly confirm compliance. Any deviations on technical requirements should be clearly

informed in Remarks column.

Deviation/ comments on other terms prescribed by the Bank are to be provided in a separate

section in Technical Bid. The Bank is not bound to evaluate the deviations mentioned at any

other section of the bid.

For supplementary information a separate sheet should be used.

All pages should be numbered (like 1/xxx, 2/xxx where xxx is last page number of Bid document)

and initialed under the company seal.

Technical Bid documents are to be properly filed in a box‐ file and should not contain any loose

papers.

Canara Bank reserves the right to reject any or all proposals. Similarly, it reserves the right not to

include any Bidder in the final short‐list.

3. Additional Instructions for Bidders

3.1 General Instructions

3.1.1 Nature of Bid

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 35 of 250

a. The bid shall be submitted by an SI, thus the SI will be the bidder.

b. One SI cannot submit more than one bid.

c. The OEMs joining SI will be the product vendors.

d. One OEM can bid only with one Bidder (SI).

e. The SI is responsible to carry out the process and accomplish the assigned task.

f. Any third party (For e.g.: in the nature of a consultant) apart from the SI and the OEM

cannot be part of the bid.

g. A bidder to this RFP acting as the SI cannot participate in the bid submitted by another

bidder (SI) as the OEM of that bid.

h. One bidder can bid along with multiple OEMs (but only one OEM for one risk solution) to

provide EWRIM Solution through this bid subject to point g above.

i. Any subcontracting and assignments by the Bidder, of the work stated within this RFP is not

permissible

j. The bank intends to procure only Perpetual Licenses. The bank should have the entitlement

/ right to use these licenses without any restriction. The bidder (SI) should also share the

official & authentic license definition of all the proposed OEM's.

k. All the new software release/version / upgrades or otherwise for any reason should be

made available to the Bank and the bank is not liable to pay / oblige SI or any OEM any

additional charges / fees pertaining to third party royalty charges etc. And also this should

not be the reason to restrict the bank from upgrading to the new release / new version of

the software.

l. The OEM should endorse the hardware & related software sizing, stating that technically

their software can be deployed on the proposed sizing. This can be through declaration or

sharing authentic / official benchmark reports.

3.1.1.1 Participation Methodology

In this bid, either the Indian Agent on behalf of the OEM or OEM itself can act as the product

vendor but both cannot participate simultaneously for the same product in the bid.

If an agent participates on behalf of the OEM, the same agent shall not participate on behalf of

another OEM in this bid for the same item/product.

In the event of Agent/Representative being not able to perform the obligations as per the

provisions of the contract/warranty, the prime Bidder (SI) should assume complete

responsibility on behalf of the OEM/Agent for providing end-to-end solution i.e., technology,

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 36 of 250

personnel, financial and any other infrastructure that would be required to meet intent of this

RFP.

3.1.2 Source Code

a. Bidder has to keep source code of proposed solution with approved / recognized escrow

agency under escrow arrangements mutually acceptable to the bank and Bidder but at

Bidder’s cost.

b. The application software should mitigate Application Security Risks, at a minimum, those

discussed in OWASP top 10 (Open Web Application Security Project)

c. The Bank reserves the right to Audit the Application / Source Code by suitable Security

Auditor.

d. The Bidder shall provide complete and legal documentation of all subsystems, licensed

operating systems, licensed system software, and licensed utility software and other

licensed software. The Bidder shall also provide licensed software for all software products

whether developed by it or acquired from others as part of the project. The Bidder shall also

indemnify the Bank against any levies / penalties on account of any default in this regard.

e. In case the Bidder is coming with software or hardware which is not its proprietary software

or hardware, then the Bidder must submit evidence in the form of agreement it has entered

into with the software vendor or hardware vendor which includes support from the software

vendor or hardware vendor for the proposed software and hardware for the full period

required by the Bank.

3.1.3 Information Ownership

All information processed, stored, or transmitted by successful Bidder’s equipment belongs to

the Bank. By having the responsibility to maintain the equipment, the Bidder does not acquire

implicit access rights to the information or rights to redistribute the information. The Bidder

understands that civil, criminal, or administrative penalties may apply for failure to protect

information appropriately.

CANARA BANK

(HO: Bangalore)

RFP for Solution to Implement

Enterprise-wide Integrated Risk

Management Architecture

under Basel II & Basel III.

RFP NO. RMW/01/2013-14 dated 10/07/2013

Page 37 of 250

Any information considered sensitive by the Bank must be protected by the successful Bidder

from unauthorized disclosure, modification or access. The bank’s decision will be final.

Types of sensitive information that will be found on Bank system’s which the Bidder plans to

support or have access to include, but are not limited to: Information subject to special

statutory protection, legal actions, disciplinary actions, complaints, IT security, pending cases,

civil and criminal investigations, etc. The successful bidder shall exercise adequate judgment to