reserved alternative investment funds (raif) · 2020. 7. 29. · the ultimate tool to achieve...

TRANSCRIPT

Reserved Alternative Investment Funds (RAIF)The missing link

© 201 . Deloitte Touche Tohmatsu Limited 2

The ultimate tool to achieve alternative investment industry needsRAIF

• Overlapping regulatory framework atproduct/manager level

• Reduction in the time to market

• Significant costs incurred

• SCS/SCSp/Soparfi regime does not allow segregationof risks and variable capital

• Following strong lobbying from industry specialists tocreate a more flexible mechanism that is based on allcurrently available regimes, on 13 July 2016 theLuxembourg Parliament voted on a new law for thepurpose of creating a new type of alternativeinvestment fund in Luxembourg, the RAIF

• The law offers a mechanism “directly inspired” by thecurrently available fund regime

Why a new vehicle?

What was proposed?

© 201 . Deloitte Touche Tohmatsu Limited 3

As from now on, projects can be launched…RAIF

Day

1

Day

1

+10

/12

busi

ness

day

sIncorporation Registration with

RCS + RAIF list

Marketing & road-shows

• The vehicle will be an AIF that is not subject to the CSSF supervision, hence less time is requiredfor setting-up

• The RAIF has to be managed by an authorised AIFM located in Lux/EU/3rd country (whereAIFMD passport available)

© 201 . Deloitte Touche Tohmatsu Limited 4

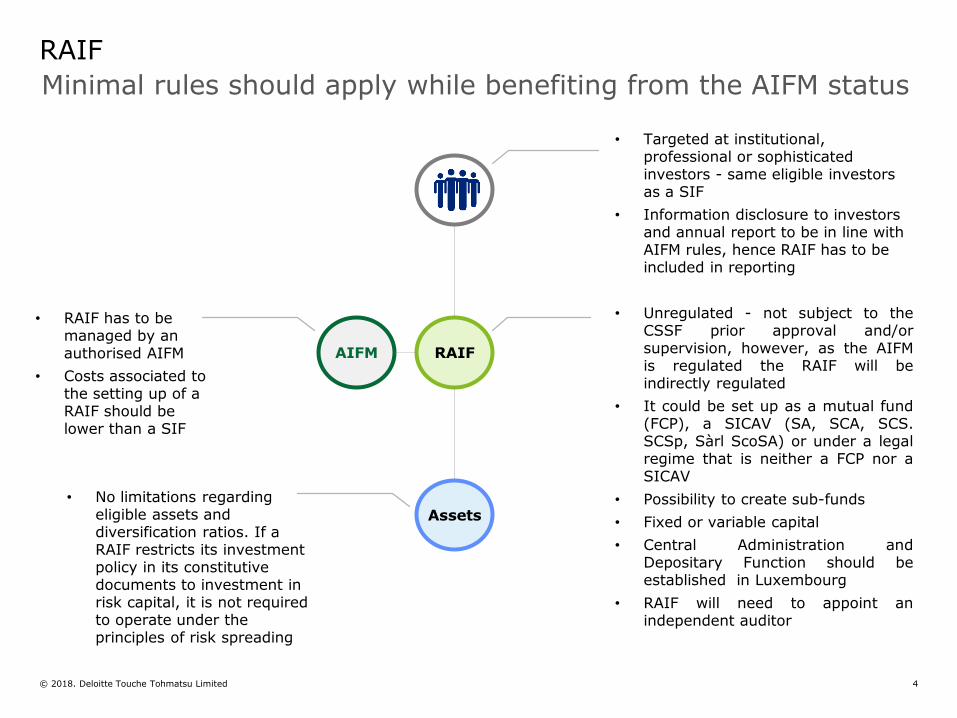

Minimal rules should apply while benefiting from the AIFM statusRAIF

RAIF

Assets

AIFM

• Unregulated - not subject to theCSSF prior approval and/orsupervision, however, as the AIFMis regulated the RAIF will beindirectly regulated

• It could be set up as a mutual fund(FCP), a SICAV (SA, SCA, SCS.SCSp, Sàrl ScoSA) or under a legalregime that is neither a FCP nor aSICAV

• Possibility to create sub-funds• Fixed or variable capital• Central Administration and

Depositary Function should beestablished in Luxembourg

• RAIF will need to appoint anindependent auditor

• Targeted at institutional,professional or sophisticatedinvestors - same eligible investorsas a SIF

• Information disclosure to investorsand annual report to be in line withAIFM rules, hence RAIF has to beincluded in reporting

• RAIF has to bemanaged by anauthorised AIFM

• Costs associated tothe setting up of aRAIF should belower than a SIF

• No limitations regardingeligible assets anddiversification ratios. If aRAIF restricts its investmentpolicy in its constitutivedocuments to investment inrisk capital, it is not requiredto operate under theprinciples of risk spreading

© 201 . Deloitte Touche Tohmatsu Limited 5

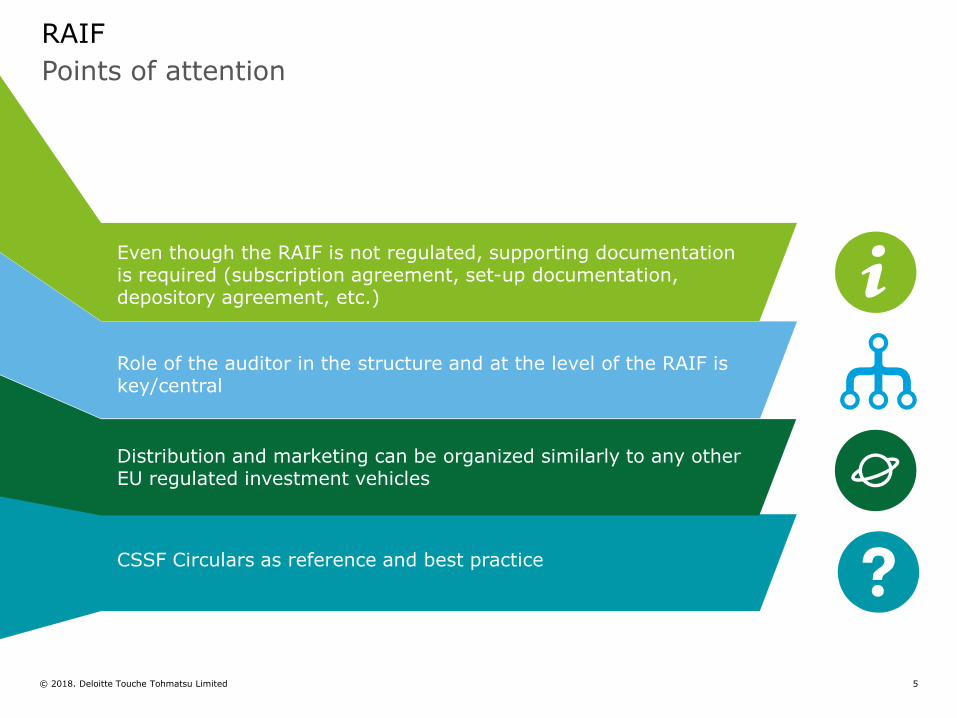

Points of attentionRAIF

Even though the RAIF is not regulated, supporting documentation is required (subscription agreement, set-up documentation, depository agreement, etc.)

Role of the auditor in the structure and at the level of the RAIF is key/central

Distribution and marketing can be organized similarly to any other EU regulated investment vehicles

CSSF Circulars as reference and best practice

© 201 . Deloitte Touche Tohmatsu Limited 6

A tax neutral fund vehicle relying on the existing SIF or SICAR regimes

RAIF

SIF regime

SICAR regime

VAT

By default:Full CIT/MBT/NWT exemption or full tax transparency for FIARFCP/SCS/SCSpNo WHT on any distributions1bps subscription tax is applicable (with exemptions availablesimilarly to SIFs)No tax on speculative capital gains for investors

Alternatively, when investing in risk capital assets: Subject to CIT/MBT but any income from transferable securities andincome from temporary investments (<12 months) is exempt; or alternatively full tax transparency for RAIFs set-up as partnershipsNo subscription taxNo WHT on any distributionsNo tax on speculative capital gains for investors

No Luxembourg VAT on fees paid in consideration for the management of the AIF whether the RAIF is applying the SIF or the SICAR tax regime

© 201 . Deloitte Touche Tohmatsu Limited 7

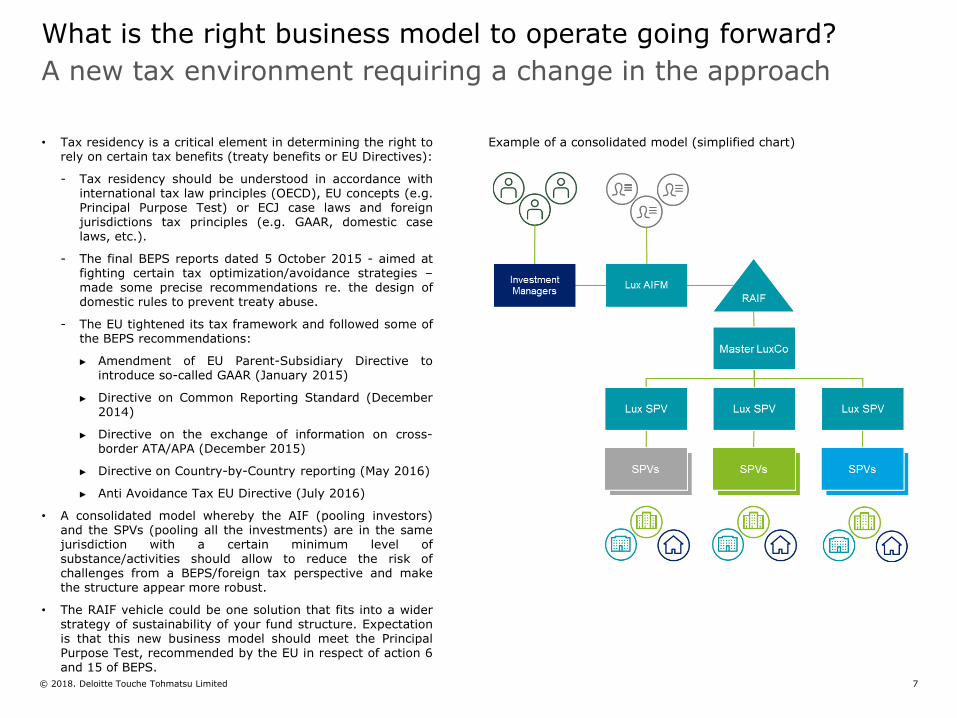

A new tax environment requiring a change in the approachWhat is the right business model to operate going forward?

• Tax residency is a critical element in determining the right torely on certain tax benefits (treaty benefits or EU Directives):

- Tax residency should be understood in accordance withinternational tax law principles (OECD), EU concepts (e.g.Principal Purpose Test) or ECJ case laws and foreignjurisdictions tax principles (e.g. GAAR, domestic caselaws, etc.).

- The final BEPS reports dated 5 October 2015 - aimed atfighting certain tax optimization/avoidance strategies –made some precise recommendations re. the design ofdomestic rules to prevent treaty abuse.

- The EU tightened its tax framework and followed some ofthe BEPS recommendations:

Amendment of EU Parent-Subsidiary Directive tointroduce so-called GAAR (January 2015)

Directive on Common Reporting Standard (December2014)

Directive on the exchange of information on cross-border ATA/APA (December 2015)

Directive on Country-by-Country reporting (May 2016)

Anti Avoidance Tax EU Directive (July 2016)

• A consolidated model whereby the AIF (pooling investors)and the SPVs (pooling all the investments) are in the samejurisdiction with a certain minimum level ofsubstance/activities should allow to reduce the risk ofchallenges from a BEPS/foreign tax perspective and makethe structure appear more robust.

• The RAIF vehicle could be one solution that fits into a widerstrategy of sustainability of your fund structure. Expectationis that this new business model should meet the PrincipalPurpose Test, recommended by the EU in respect of action 6and 15 of BEPS.

Example of a consolidated model (simplified chart)

© 201 . Deloitte Touche Tohmatsu Limited 8

Key Contacts

Partner

Partner

Raymond Krawczykowski Partner+352 451 452 [email protected]

Partner

99

Key Contacts

Simon RamosPartner+352 451 452 [email protected]

Francisco da CunhaPartner+352 451 452 [email protected]

Yves KnelPartner+352 451 452 [email protected]

© 201 . Deloitte Touche Tohmatsu Limited

© 2018. Deloitte Touche Tohmatsu Limited 10

Key Contacts

Tax – Private EquityRaphaël LouagePartner+352 451 452 898 [email protected]

Tax – Private EquityDany TeillantPartner+352 451 452 [email protected]