residential business briefing - cushman & wakefield .../media/reports/india/residential...

TRANSCRIPT

RESIDENTIAL MARKET INCREASING AFFORDABILITY OF NEW RESIDENTIAL LAUNCHES IN INDIA

"A correction of the launch prices will improve attractiveness and relevance of these locations to the end-users. The economic confidence slowly creeping back into end-user sentiments aided by a corrected Base Price as well as lowered ticket size is likely to provide the needed boost to improve sales.”

Shveta JainManaging Director – Residential Services, India Cushman & Wakefield

OVERVIEWIn an end of the year report for residential market for metropolitan cities of National Capital Region (NCR), Mumbai and Bengaluru, Cushman & Wakefield research records a drop in launch prices in high development activity markets of these cities. The analysis records that new residential projects in select micro markets are cheaper by 4% - 20% on weighted average Basic Sale Price (BSP) over the last two years. This report tracks the development activities in locations of Dwarka Expressway, New Gurgaon, Southern Peripheral Road, Sohna, Noida Expressway and Noida Extension in NCR; Thane, Goregaon and Malad in Greater Mumbai and South-West and Southern submarkets in Bengaluru.

The suburban location of Goregaon in Mumbai registered the biggest decline in Average Weighted Basic Sale Price at 20% where the per square feet (psf) rate averages at INR 10,500 psf in 2015 followed by Thane which saw 18% decline. Southern Peripheral Road in Gurgaon also saw a decline of 10% in weighted average base selling price of new launch projects compared to 2013.

In contrast, most of the submarkets in Bengaluru witnessed steady launch prices except in Far South* and Western** submarkets where average new launch prices in 2015 declined by 2-7% compared to 2013. South East*** micro market of Bengaluru was an exception to the rule where both the Average Weighted Basic Sale Price (19%) and the Average Ticket Size (18%) of apartment saw an increase.

# Weighted average Basic Sale Price of mid segment projects in new launches.## Average ticket size for newly launched 2BHK unit in mid segment in apartment projects. Ticket price is inclusive of BSP only.

MARKET SNAPSHOT

City Location Average new % change in % change in launch BSP 2015 Weighted Average Average Ticket

# # ## (INR/sf) BSP Size (compared to 2013) (compared to 2013)

Bengaluru Far South 3,850 -7% 3%Bengaluru South East 5,111 19% 18%

Delhi-NCR Noida Expressway 4,600 -4% 6%Delhi-NCR Noida Extension 3,700 -5% 11%Delhi-NCR New Gurgaon 5,800 -9% -9%Delhi-NCR Southern Peripheral Road 6,300 -10% -14%

Mumbai Mulund 12,250 7% -4%Mumbai Malad 10,750 -8% -15%Mumbai Thane 8,300 -18% -18%Mumbai Goregaon 10,500 -20% -17%

* Electronic City** Mysore Road, Uttarahalli Main Road, Magadi Road*** Sarjapur Road, Outer Ring Road (Marathahalli-Sarjapur), HSR Layout, Hosur Road

Source: Cushman & Wakefield Research

DELHI-NATIONAL CAPITAL REGIONWith declining number of new launches amidst a slump in buyer's interest, Delhi-NCR witnessed new unit launches aggregating approximately 23,000 in 2015, a 14% decline from the previous year. 79% of the units were launched in the locations of Dwarka Expressway, New Gurgaon, Southern Peripheral Road, Sohna, Noida Expressway and Noida Extension. At approximately 12,400 units,mid segment accounted for nearly half of the total new launches in 2015 in Delhi-NCR.

With a view to attract buyers, developers have tried to bring down the ticket size of their offerings by either

Submarkets 2013 2015 % Change

Dwarka Expressway 6,100 5,500 -10%New Gurgaon 6,400 5,800 -9%Southern Peripheral Road 7,000 6,300 -10%Noida Expressway 4,800 4,600 -4%Noida Extension 3,900 3,700 -5%

Note: Computation on Weighted Average Base Selling Price of Mid segment projects in new launches.

2013 2014 2015

No. of Projects 77 41 40No. of Units 38,400 26,802 22,979

reducing unit sizes or reducing capital values or both. Such efforts from developers have been witnessed across submarkets especially in Southern Peripheral Road, New Gurgaon and Noida. Dwarka Expressway and Southern Peripheral Road saw the largest decline of 10% in launch prices in Delhi-NCR as against 2013 in Base Selling Price.

Southern Peripheral Road*Primary prices in the submarket has softened by 10% compared to 2013, while the apartment size offered by developers in recent projects also trimmed to around 1,200 sf from earlier 1,400 sf making it slightly affordable for end-users. However, prices in the secondary market ranges from INR 5,500 – 6,300 psf for projects indicating a variation of 5-8%. The reduction in base price and average size of the apartments has led to a 14% decline in overall ticket price in the submarket to INR 72 lakhs in Q4 2015 compared with INR 84 lakhs in 2013.

New Gurgaon**Although, the average size of a 2BHK unit remained similar in the range of 1,400-1,500 sf, the BSP has reduced from INR 6,400 psf in 2013 to INR 5,800 psf in Q4 2015, registering a decline of approximately 9% over the last two years. The submarket of New Gurgaon witnessed average ticket price of 2BHK reducing from INR 95 lakh in 2013 to INR 88 lakh in Q4 2015. Owing to huge under-construction

inventory of 38,000 – 40,000 units in this submarket. However, considering the fact that ready to move projects are available in the range of INR 4,000 – 5,000 per sf, the price of new launches are at a premium of 20-22%.

NoidaThe submarkets of Noida witnessed softening of capital values of new launches, while registering a marginal increase in the average size of a 2BHK. The capital values of new launches have softened by 4-5% since 2013, however the average size of a 2BHK has increased marginally leading to stable or increased ticket sizes. While Noida Expressway is fast emerging as a mid-segment residential destination with presence of basic infrastructure which attracts end-users, Noida Extension has established itself as the affordable residential region in Delhi-NCR with one of the lowest capital values. Infrastructure initiatives and continuous demand from end-users are the major reasons for stable ticket sizes in Noida.

NEW LAUNCH DATA

NEW LAUNCH DATA: WEIGHTED AVERAGE BSP (INR/SF)

Source: Cushman & Wakefield Research

*Southern Peripheral Road: Sector 68, 69, 70, 70A, 71, 72, 73**New Gurgaon: Sector 81, 81A, 82, 82A, 83, 84, 85, 86, 88A, 88B, 89, 89A, 90, 91, 92, 93, 95, 95A, 95B

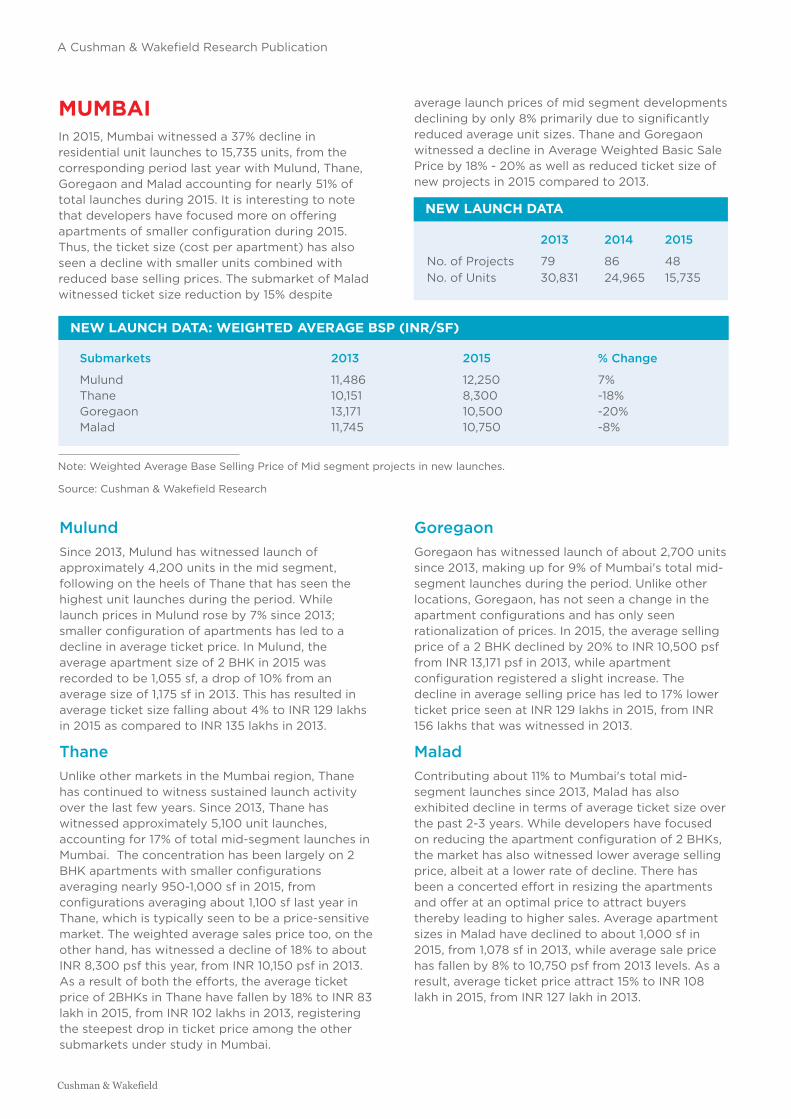

MUMBAIIn 2015, Mumbai witnessed a 37% decline in residential unit launches to 15,735 units, from the corresponding period last year with Mulund, Thane, Goregaon and Malad accounting for nearly 51% of total launches during 2015. It is interesting to note that developers have focused more on offering apartments of smaller configuration during 2015. Thus, the ticket size (cost per apartment) has also seen a decline with smaller units combined with reduced base selling prices. The submarket of Malad witnessed ticket size reduction by 15% despite

Submarkets 2013 2015 % Change

Mulund 11,486 12,250 7%Thane 10,151 8,300 -18%Goregaon 13,171 10,500 -20%Malad 11,745 10,750 -8%

2013 2014 2015

No. of Projects 79 86 48No. of Units 30,831 24,965 15,735

average launch prices of mid segment developments declining by only 8% primarily due to significantly reduced average unit sizes. Thane and Goregaon witnessed a decline in Average Weighted Basic Sale Price by 18% - 20% as well as reduced ticket size of new projects in 2015 compared to 2013.

Note: Weighted Average Base Selling Price of Mid segment projects in new launches.

MulundSince 2013, Mulund has witnessed launch of approximately 4,200 units in the mid segment, following on the heels of Thane that has seen the highest unit launches during the period. While launch prices in Mulund rose by 7% since 2013; smaller configuration of apartments has led to a decline in average ticket price. In Mulund, the average apartment size of 2 BHK in 2015 was recorded to be 1,055 sf, a drop of 10% from an average size of 1,175 sf in 2013. This has resulted in average ticket size falling about 4% to INR 129 lakhs in 2015 as compared to INR 135 lakhs in 2013.

ThaneUnlike other markets in the Mumbai region, Thane has continued to witness sustained launch activity over the last few years. Since 2013, Thane has witnessed approximately 5,100 unit launches, accounting for 17% of total mid-segment launches in Mumbai. The concentration has been largely on 2 BHK apartments with smaller configurations averaging nearly 950-1,000 sf in 2015, from configurations averaging about 1,100 sf last year in Thane, which is typically seen to be a price-sensitive market. The weighted average sales price too, on the other hand, has witnessed a decline of 18% to about INR 8,300 psf this year, from INR 10,150 psf in 2013. As a result of both the efforts, the average ticket price of 2BHKs in Thane have fallen by 18% to INR 83 lakh in 2015, from INR 102 lakhs in 2013, registering the steepest drop in ticket price among the other submarkets under study in Mumbai.

GoregaonGoregaon has witnessed launch of about 2,700 units since 2013, making up for 9% of Mumbai's total mid-segment launches during the period. Unlike other locations, Goregaon, has not seen a change in the apartment configurations and has only seen rationalization of prices. In 2015, the average selling price of a 2 BHK declined by 20% to INR 10,500 psf from INR 13,171 psf in 2013, while apartment configuration registered a slight increase. The decline in average selling price has led to 17% lower ticket price seen at INR 129 lakhs in 2015, from INR 156 lakhs that was witnessed in 2013.

MaladContributing about 11% to Mumbai's total mid-segment launches since 2013, Malad has also exhibited decline in terms of average ticket size over the past 2-3 years. While developers have focused on reducing the apartment configuration of 2 BHKs, the market has also witnessed lower average selling price, albeit at a lower rate of decline. There has been a concerted effort in resizing the apartments and offer at an optimal price to attract buyers thereby leading to higher sales. Average apartment sizes in Malad have declined to about 1,000 sf in 2015, from 1,078 sf in 2013, while average sale price has fallen by 8% to 10,750 psf from 2013 levels. As a result, average ticket price attract 15% to INR 108 lakh in 2015, from INR 127 lakh in 2013.

NEW LAUNCH DATA: WEIGHTED AVERAGE BSP (INR/SF)

NEW LAUNCH DATA

Source: Cushman & Wakefield Research

BENGALURUThe unit launches in Bengaluru in 2015 have substantially declined by 62% to approximately 15,600 in comparison to 2014. However, in comparison to the other cities, Bengaluru has shown an exceptionally stable market trend. While the new unit launches have not seen a reduction in the unit sizes or ticket sizes, the focus segment has changed over the last two years. In 2015, a majority of the new launches (83%) were concentrated in the mid-segment. While new launch prices have remained stable across most submarkets, Far South saw developers reducing the Average Weighted Basic Sale Price in mid segment by 7%, to remain competitive. South East submarket was an exception where both the Average Weighted Basic Sale Price (19%) and the Average Ticket Size (18%) of apartments saw an increase.

Submarkets 2013 2015 % Change

Far South 4,125 3,850 -7%South East 4,277 5,111 19 %West 3,557 3,500 -2%

Note: Weighted Average Base Selling Price of Mid segment projects in new launches.

2013 2014 2015

No. of Projects 157 125 44No. of Units 49,279 40,927 15,603

New launches in 2015 were concentrated mainly in few submarkets including Far South and South-East submarkets. Approximately 47% of the new unit launches in 2015 were witnessed in Far South, South east and West submarkets in Bengaluru. A closer examination of the ticket prices and base selling prices in these submarkets reveals that Bengaluru continues to be a stable market in terms of ticket prices, with developers not having to resort to lowering of selling prices or reducing apartment size to make them more affordable.

Far South: Electronic CityThe weighted average base selling price declined by 7% to INR 3,850 psf in 2015, from INR 4,125 psf in 2013. This is mainly due to the fact that the new launches were fewer in 2015 and were quoted at a comparatively lower prices than the previous two years, resulting in a dip in the weighted average prices. While unit launches in the years 2013 and 2014 were split between Affordable (33% - 49%) and Mid-segment (51%-65%), the unit launches in 2015 were only focused on Mid-segment. Overall, the demand has been subdued in this submarket as developers focussed on launches in submarkets in proximity to upcoming commercial hubs in the city.

South - East:Sarjapur Road, Outer Ring Road (Marathahalli - Sarjapur), HSR Layout, Hosur Road In 2015, South-east submarket witnessed launches pre-dominantly in the mid segment. This is primarily attributed to the commercial real estate sector growth along the Outer Ring Road submarket area, which has presented an opportunity for residential development. The submarket has presence of approximately 44 msf of Grade A office space. This has helped generate strong demand for residential space in the submarket and is leading to increase in capital values. Between the years 2013 and 2015, the weighted average base prices increased by 19% to INR 5,111 psf with an average unit size of 2BHK at 1,190 sf.

NEW LAUNCH DATA

NEW LAUNCH DATA: WEIGHTED AVERAGE BSP (INR/SF)

Source: Cushman & Wakefield Research

SHVETA JAIN

For more information on Residential Services offered byCushman & Wakefield India, contact:

KAMAL AGARWALAssociate - [email protected]

Managing Director - Residential