resource guide for indian business: low carbon investment ... · resource guide for indian...

TRANSCRIPT

Resource Guide for

Indian Business:

Low Carbon Investment

in India

March 2010

Resource Guide for Indian Business: Low Carbon Investment in India I

Contents

Foreword

About this guide

Executive summary

Glossary and monetary terms

1. Introduction

2. An enabling environment for low carbon development

3. Drivers for private sector engagement

4. Finance for low carbon development

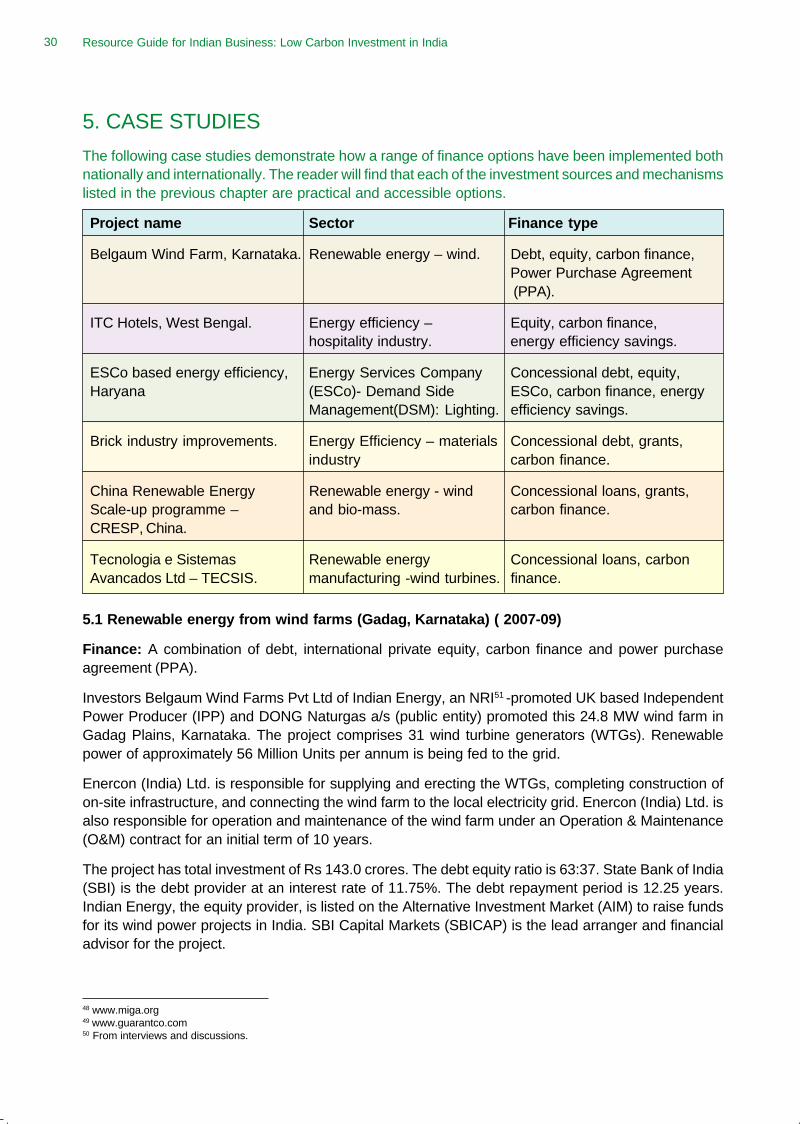

5. Case studies

Annexes

Annex 1. Annotated list of information sources

Annex 2. Bibliography and suggested reading

Resource Guide for Indian Business: Low Carbon Investment in IndiaII

Resource Guide for Indian Business: Low Carbon Investment in India III

Foreword

I am delighted to present this Resource Guide for Indian Business: Low Carbon Investment in India.

The challenge of climate change and the need for a low carbon development model are wellunderstood by policy makers and business leaders across the globe. It is essential that policymakers reach the necessary agreements and ultimately a consensus on how the world shouldtackle global warming at an inter-governmental level. But the necessary commitment of policy makersis only half the story - I believe that it is only by leveraging private sector capital and unleashing thepower of the markets to boost investment in green technology and pollution reducing projects thatthe challenges of climate change can be met.

India is very well placed to be at the forefront of this drive to harness private sector expertise and buildthe world’s post-carbon economy. It has great potential for technological developments which willenable India’s citizens to leap-frog the wasteful development model of the West. There are a widerange of choices for the future and these choices could bring huge opportunities for businesses.

In order to exploit the potential role of the private sector in fuelling low carbon growth, policy makersmust establish a clear and consistent regulatory environment around all aspects of climate changemitigation. Before investors part with funds for clean technologies such as renewable energy, theymust be confident they are basing investment decisions within a secure regulatory framework. Thecost of capital is related to risk and politicians must make it a priority to minimise risk for investors bycreating policy stability. It is also necessary to examine how expertise in the financial markets can beused to develop innovative financing techniques. This is an area where I believe the City of Londoncan work closely in partnership with India by linking India’s drive and entrepreneurial flair with theCity’s expertise as a financial innovator and as a centre for carbon financing.

This Resource Guide has been produced following the recommendation of the City of LondonAdvisory Council for India that low carbon investment become one of the City of London’s priorityareas of focus in India. It is targeted at Indian businesses, with the aim of providing an overview oflow carbon development in the Indian context; the mechanisms available to harness investmentdomestically and from abroad in the low carbon area; and an overview of the role that the nationaland state governments are playing in enabling an investment-friendly environment. It providesinformation and succinct introductions and references to sources of assistance in financing projectsand services for Indian businesses.

I hope that you find this Resource Guide useful and informative.

Stuart FraserPolicy ChairmanCity of London

Resource Guide for Indian Business: Low Carbon Investment in IndiaIV

About this Guide

Responding to the challenges of climate change, such as managing greenhouse gas (GHG)emissions, water consumption and waste, are national priorities that present major investmentopportunities in the coming years. India’s path to further growth and prosperity and a low carboneconomy will require the active involvement of business and financial institutions.

This Resource Guide stems from a City of London roundtable discussion, ‘Financing a Low CarbonEconomy for India’, moderated by Naina Lal Kidwai, Group Chairperson, HSBC India on 30 September2009. The roundtable brought together Indian academic and business leaders with UK carbon marketexperts to discuss opportunities and existing roadblocks to low carbon investment in India (includingcarbon financing for industrial projects and carbon neutral infrastructure projects).

At the roundtable, participants discussed the issue that Indian companies are not seeking orreceiving investment to reduce their carbon emissions to the extent of their counterparts in Chinaor South East Asia. In 2008, clean tech investments into India decreased due to the shortinvestment horizons. The lack of low carbon investment from domestic Indian banks in the SMEsector was also noted. Participants agreed that getting to a stage where investors can invest inlarger projects would be a very valuable.

This resource guide is targeted at Indian corporates and aims to provide detail of the mechanismsavailable to harness investment domestically and from abroad in the low carbon area. It aims toprovide:

• An understanding of low carbon development in the Indian context, explaining strategic andregulatory developments such as the National Action Plan for Climate Change (NAPCC).

• Useful information and links for businesses in India who aspire to be part of this clean revolutionand require a quick reference to relevant issues.

• Succinct introductions and links to assistance in financing projects and services (particularlyrenewable energy and energy efficiency).

• An overview of the role that the national and state governments are playing in enabling aninvestment-friendly environment.

• Case-studies of national and international projects.

Resource Guide for Indian Business: Low Carbon Investment in India V

About the City of London

The City of London has long recognised the critical importance of India to the UK based financialservices industry, and is committed to making the best possible use of existing cultural, linguistic,political and trade relationships. In order to strengthen direct links with India, the City of Londonestablished the City Office in Mumbai in 2007. The City Office in Mumbai works to further strengthentrading and investment links in both directions between India and the UK through the provision ofworld class financial services and products.

Guidance to the City Office is provided by the City of London India Advisory Council. The Council ischaired by Mrs. Naina Lal Kidwai (Group Chairperson, HSBC India). Other members of the Councilare: Mr. Mukesh Ambani (Chairman of Reliance), Ms. Zia Mody (Senior Partner of AZB & Partners),Mr. Nasser Munjee (Chairman of Development Credit Bank), Mr. Deepak Parekh (Chairman of theHDFC Group), Dr. Ajay Shah (Senior Fellow, NIPFP), Mr. Jairaj Purandare (Executive Director, PWC),Mr. Jamshyd Godrej (Chairman of Godrej & Boyce Mfg. Co. Ltd), Mr. Neeraj Swaroop (CEO of StandardChartered Bank, India), Mr. Ajay Srinivasan (CEO-Financial Services, Aditya Birla Group) andMr. Shardul Shroff (Managing Partner of Amarchand & Mangaldas & Suresh A Shroff & Co.)

In 2009, climate change and low carbon development were adopted by the City of London AdvisoryCouncil for India as one of the priority areas for engagement by the City Office in Mumbai and the Cityof London. The City of London has been at the forefront of action on climate change for the last fifteenyears - championing the uptake of renewable energy, pioneering the development of carbon emissionsmarkets and becoming the first public body to develop a climate adaptation strategy. The City is theworld’s leading international financial and business centre and the leading international centre forcarbon finance, capable of providing the necessary finance for that investment and of managing thenew risks that go with it.

Contacts:

Eva George Anita NandiChina and India Business Development Manager City RepresentativeEconomic Development Office, City of London City Office in MumbaiPO Box 270, Guildhall, DBS House, Prescott Road,London, EC2P 2EJ Fort, Mumbai, 400 001UK IndiaTel +44 (0)20 7332 1565 Tel +91 22 664527244Email: [email protected] Email: [email protected]

Resource Guide for Indian Business: Low Carbon Investment in IndiaVI

Acknowledgements & Consultations

We thank the following persons for their contributions:

Dr. Anvita Arora (CEO, iTrans Pvt. Ltd, Indian Institute of Technology, New Delhi),Ms. Seema Arora (Principal Councillor & Head, CII-ITC Centre for Excellence in SustainableDevelopment), Dr. Bharat Bhargava (Director, Ministry of New and Renewable Technology - MNRE),Ms. Vandana Bhansali (Associate Vice President - Corporate Sustainability, HSBC India), Mr. UnmeshBrahme (Senior Vice President, HSBC India), Mr. Gavin English (Managing Director, WSPimc),Mr. Richard Folland (Managing Director, Climate Strategies), Mr. Vinod Kala (Founder Director,Emergent Ventures India), Mr. S Kanchan (Vice President - Finance & Accounting, Kalpan Hydro),Dr. V K Kaul (General Manager, Solar Photovoltaic team, Central Electronics Limited),Ms. Ritu Kumar (Senior Advisor – Environment, Social & Governance, Actis), Dr. Sameer Maithel(Director, Greentech), Mr. R Miglani (Regional Climate Change Specialist, International FinanceCorporation), Mr. Shishir Athale, (Director, Sudnya Industrial Services Pvt. Ltd.), Mr. M Parshad(Director, Agriculture Insurance of India Ltd.), Mr. K S Popli (Director-Technical, Indian RenewableEnergy Development Agency Ltd. - IREDA), Mr. Andrew Reicher (Programme Manager – PrivateInfrastructure Development Group), Mr. Nick Robins (Head of Climate Change Centre, HSBC),Dr. Shruti Shil (Business Resources Associate, Jain Irrigation Systems ltd.), Ms. Richa Shukla(Project Manager, Willis); Mr. Ajay Srinivasan (CEO-Financial Services, Aditya Birla Group) andMr. Chris Vermont (GuarantCo).

Disclaimer: This guide is for information purposes only and does not offer financial advice. Theinformation herein has been obtained from sources, which the authors and publishers believe to bereliable. But the authors and publishers do not guarantee its accuracy or completeness. Readers areadvised to verify the information from independent sources. The authors and publishers make norepresentation or warranty, express or implied, concerning the fairness, accuracy or completeness ofthe information and opinions contained herein. All opinions expressed herein are based on thejudgement at the time of this report and are subject to change without notice due to economic, political,industry and firm-specific factors. The authors, publishers and anyone associated with this report arenot liable for any unintended errors or omissions and any opinions expressed hereon. The authorsand publishers are not liable for the consequences of the use of information in this guide.

The guide has been researched and written by Ripin Kalra (lead author), Ashutosh Pandey,Jeremy Doyle, Aloke Barnwal and Gaurav Sarup.

WSP international management consulting ltd.

WSP House,70, Chancery Lane,London,WC2A [email protected]

Resource Guide for Indian Business: Low Carbon Investment in India VII

Executive Summary

Low carbon development and business opportunities

Climate change is a major global systemic risk, and the response to this issue has the potential to beone of the greatest business opportunities of this century. The scientific evidence on the causes andfuture impacts of climate change is strengthening all the time. Human activity is increasing the stocksof greenhouse gases in the atmosphere, which is warming the planet.

“Low carbon development” or “climate change mitigation”1 are terms used to describe the transitiontowards options that reduce human interference with the climate system. This means reducing therelease of greenhouse gases into the atmosphere from chemicals or fossil fuel use. It also involvesreducing emissions from changes in land use such as deforestation. In addition to low carbondevelopment, “adaptation” to climate change is also required; this means adjusting to the widespreadimplications of future climate change, including changes in seasonal weather patterns and the frequencyor intensity of natural disasters.

The Indian business environment is changing quickly

Primary energy demand in India is expected to more than double by 2030, and coal and oil currentlyaccount for over 90% of India’s energy consumption. At a national level, the Government of India isimplementing increasingly wide- reaching regulations and incentives to reduce emissions and ispreparing adaptation plans. Such measures, including the far-reaching National Action Plan on ClimateChange (NAPCC), are a part of India’s international commitments on climate change. They alsoreflect India’s need to secure the ability to create increased economic activity to deliver prosperity andgrowth. Regulations and incentives to promote renewable energy and energy efficiency are wellunderway in tandem with the Jawaharlal Nehru National Solar Mission (JNNSM) and National Missionfor Enhanced Energy Efficiency (NMEEE).

The resulting business opportunities are considerable. India aims to increase the share of gridconnected renewable energy to 10% by 2012. 20GW of solar power generation is planned by 2022 aspart of the JNNSM. There is also a substantial effort for off-grid energy solutions for India’s rural andremote areas. The NMEEE aims to improve energy efficiency in priority industries such as power,cement, fertiliser, aluminium, iron & steel, railways, pulp & paper and textiles. The ‘energy conservationbuilding code’ (ECBC) has been developed for commercial buildings. New measures in the IndiaUnion Budget 2010-11 include a new National Clean Energy Fund to support clean energy. This willbe funded by a coal levy, raising 2500 crores/annum (USD500m/annum). The government has plannedRenewable Energy Certificates (RECs) and Energy Saving Certificates (ESCerts) to sustain marketbased mechanisms.

Such measures can be expected to be maintained or strengthened in coming years and will presentgrowth potential for many sectors, particularly energy, transport, industry, agriculture and forestry.Companies that manage climate change risks and exploit new opportunities will generate a competitiveadvantage over rivals.

Indian industry has already developed ways to help bypass the resource intensive growth path ofdeveloped nations. There is now good evidence that Indian companies are reducing emissions andadapting to the impacts of climate change. More Indian companies are undertaking focused efforts tomanage their carbon footprints, with top management support. Such information is increasinglyimportant in influencing the decision-making of financial institutions.

Resource Guide for Indian Business: Low Carbon Investment in IndiaVIII

National and international financing is increasingly focussing on low carbon energy

Now that clean technology is an investment category in its own right, public financial institutions andbanks, private equity and venture capital funds are emerging as significant investors in Indian cleantechnology companies. The International Financial Institutions such as International FinanceCorporation (IFC) and the Asian Development Bank (ADB) are also shifting their investment policiestowards low carbon solutions, bringing added interest and resources to the sector. Carbon financealso provides a way to monetise the greenhouse gas benefits of clean projects and this has been asignificant catalyst in India. Clarity is needed around the rules for an international carbon marketbeyond the Kyoto commitment period (2012). This is under negotiation at UN level, with discussionsin Mexico in November 2010.

The private sector in India has implemented low carbon projects using a range of investment sources:self-financing, private equity investment, venture capital and where available, carbon finance. Thenew impetus from the public sector reflects the considerable success to date and sets a high level ofambition for further accelerating low carbon investment in India.

1 Terms used interchangeably for the purposes of this document.

Resource Guide for Indian Business: Low Carbon Investment in India IX

Glossary & Monetary Terms

BEE – Bureau of Energy Efficiency

CDM – Clean Development Mechanism

CEA – Central Electricity Authority

CER – Certified Emission Reduction

CERC – Central Electricity Regulatory Commission

ESCerts – Energy Saving Certificates

ESCo – Energy Services Company

GHG – Greenhouse Gases

IEX – Indian Energy Exchange

Rs – Indian National Rupee

IREDA – Indian Renewable Energy Development Agency

IRR – Internal Rate of Return

MNRE – Ministry of New & Renewable Energy

NAPCC – National Action Plan on Climate Change

NBFC – Non-banking Financial Companies

NMEEE – National Mission on Enhanced Energy Efficiency

JNNSM – Jawaharlal Nehru National Solar Mission

REC – Renewable Energy Certificates

SEB – State Electricity Board

SERC – State Electricity Regulatory Commission

USD – United States Dollar

tCO2e – Tons of carbon dioxide equivalents

Exchange Rates and Monetary terms

Rs = Indian National Rupee

USD = US Dollar

Commonly used monetary terms in India are:

Crore = 100,00,000

Lakh = 1,00,000

Million = 1,000,000

1 crore = 10 Million

1 lakh = 0.1 Million

The following exchange rate has been used for this guide

1USD = Rs 45Rs 1 crore = 0.2 Million USD

Rs 10 crores = 2 Million USD

Rs 100 crores = 20 Million USD

Resource Guide for Indian Business: Low Carbon Investment in India 1

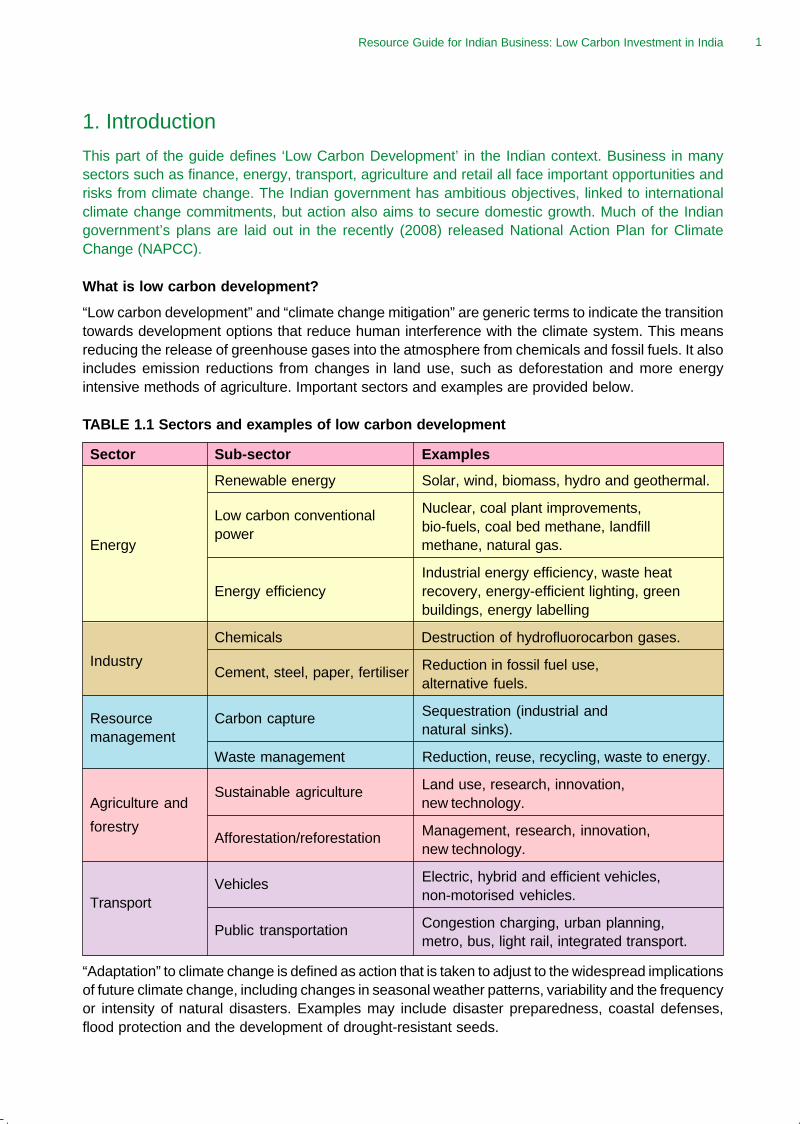

1. Introduction

This part of the guide defines ‘Low Carbon Development’ in the Indian context. Business in manysectors such as finance, energy, transport, agriculture and retail all face important opportunities andrisks from climate change. The Indian government has ambitious objectives, linked to internationalclimate change commitments, but action also aims to secure domestic growth. Much of the Indiangovernment’s plans are laid out in the recently (2008) released National Action Plan for ClimateChange (NAPCC).

What is low carbon development?

“Low carbon development” and “climate change mitigation” are generic terms to indicate the transitiontowards development options that reduce human interference with the climate system. This meansreducing the release of greenhouse gases into the atmosphere from chemicals and fossil fuels. It alsoincludes emission reductions from changes in land use, such as deforestation and more energyintensive methods of agriculture. Important sectors and examples are provided below.

TABLE 1.1 Sectors and examples of low carbon development

Sector Sub-sector Examples

Renewable energy Solar, wind, biomass, hydro and geothermal.

Low carbon conventional Nuclear, coal plant improvements,

power bio-fuels, coal bed methane, landfillEnergy methane, natural gas.

Industrial energy efficiency, waste heatEnergy efficiency recovery, energy-efficient lighting, green

buildings, energy labelling

Chemicals Destruction of hydrofluorocarbon gases.

IndustryCement, steel, paper, fertiliser Reduction in fossil fuel use,

alternative fuels.

Resource Carbon capture Sequestration (industrial and

management natural sinks).

Waste management Reduction, reuse, recycling, waste to energy.

Sustainable agriculture Land use, research, innovation,Agriculture and new technology.

forestryAfforestation/reforestation Management, research, innovation,

new technology.

Vehicles Electric, hybrid and efficient vehicles,

Transport non-motorised vehicles.

Public transportation Congestion charging, urban planning,metro, bus, light rail, integrated transport.

“Adaptation” to climate change is defined as action that is taken to adjust to the widespread implicationsof future climate change, including changes in seasonal weather patterns, variability and the frequencyor intensity of natural disasters. Examples may include disaster preparedness, coastal defenses,flood protection and the development of drought-resistant seeds.

Resource Guide for Indian Business: Low Carbon Investment in India2

Climate change overview

The recent UN Framework Convention on Climate Change meeting at Copenhagen in December 2009resulted in the ‘Copenhagen Accord.’ This reemphasised that ‘climate change is one of the greatestchallenges of our time.’ It agreed that it is necessary to prevent dangerous interference with the climatesystem through deep reductions in global emissions of greenhouse gases (GHGs), with the aim ofkeeping the rise in global temperature to below 20C. It also called for urgent action to adapt to the climatechange which is already occurring. Importantly, developed countries committed jointly to mobiliseUSD 100 billion [Rs 450,000 crores] a year by 2020 to address the needs of developing countries.

In some cases there may be a fundamental link for businesses such as those in the energy, forestmanagement, food and agricultural sectors. Others may feel the impact indirectly, such as the financialservices and engineering sectors. It is important for institutions of all types to be aware of possibleimpacts on their operations.

Figure 1.1: Impacts of temperature rises

Source: Stern N (2007) ‘The economics of climate change: The Stern Review’.

India is one of the countries predicted to be most exposed to climate change impacts. Temperature risesof 20C and beyond will have major consequences for human health, food production, water availabilityand ecosystems. Human settlements and economic activity in coastal regions are at the highest risk.

Surface air temperatures in India have been increasing at the rate of 0.40C per hundred years,particularly during the post-monsoon and winter seasons. Due to climate change, winter temperaturesare forecasted to increase by as much as 3.20C by 2050, and 4.50C by 2080. Summer temperatureswill increase by 2.20C by 2050, and 3.20C by 2080. It is estimated that in India up to 3% of GDP isalready spent annually responding to the adverse impacts of a changing climate.

Delay in current cropping schedule

Increasing population under water stress

Increased water runoffDecreasing quality of xxxxxxand ground water resources

Tropical forest gradually replacedby tropical savannas and shrub lands

Blodiversity loss

Loss of small slands

Coral bleaching

50C40C30C20C10C

Agriculture

WaterResources

ForestryandEcosystem

Health

ExtremeWeatherEvents

Falling crop yields

Loss of agricultural landsdue to seal level rise

Increasing potential of cropyields in selected countries

Increased respiratory and cardiovasculardiseases due to thermal stress

Outbreak of ventro born diseases (malaria and dengue)

Increased frequency and intensity of extreme weather events(heat waves and drought, flooding and tropical cyclones)

Resource Guide for Indian Business: Low Carbon Investment in India 3

As the consensus regarding a low carbon future is emerging globally, including the “green recovery”economic stimulus packages introduced to combat the global financial crisis, there has been a significantfocus on economic activity that reduces greenhouse gas emissions, manages water resources carefullyand eliminates waste. The maturing of clean technologies means that many projects are becomingfinancially attractive for investors. Across the globe businesses are utilising their creativity and expertiseto address the challenge ahead to become a part of the solution.

Low carbon development in the Indian context

India is the world’s fifth largest greenhouse gas emitter. However, per capita emissions are a quarterof the global average. Much of the carbon emissions in India come from energy consumption in thebuildings, transport, industry and agriculture sectors, as around 90% of Indian primary energy supplycomes from coal and oil. The above sectors are growing rapidly and demand could more than doubleby 2030. Renewable and or clean energy tend to be the focus areas of many investment funds operatingin India, but opportunities in water and waste management companies are also emerging. Carbonfinance (see box below) has also played its role in progressing low carbon development particularly inrenewable energy, waste management, fuel-switching and energy efficiency.

Carbon Finance: Kyoto Protocol And Mexico (Cop16, 2010)

Carbon finance refers to investments in projects that reduce emissions of greenhousegases and creation (or origination) of financial instruments that can be traded in carbonmarkets globally.

The Clean Development Mechanism (CDM), the most active carbon financemechanism for India, was established under the Kyoto Protocol2 in 1997. Essentially,it allows developing nations to sell “Certified Emissions Reductions” (CER) creditsto developed countries. This is done through projects where cleaner technologies(for example electricity from a wind farm) replace higher emissions options (forexample electricity from a coal-fired power station). The price of credits is determinedthrough trading in the international market. India is the second most active of all theeligible countries with the market in India worth an estimated at 5 billion USD3 [Rs22,500 crores].

Market based mechanisms (such as CDM) that emerged from the Kyoto Protocol aredue to expire in 2012 unless further agreement is reached on their future. This isdependent on the outcome of ongoing talks that will culminate in 2010 at the 16th

Conference of Parties - COP16 (Mexico November 2010).

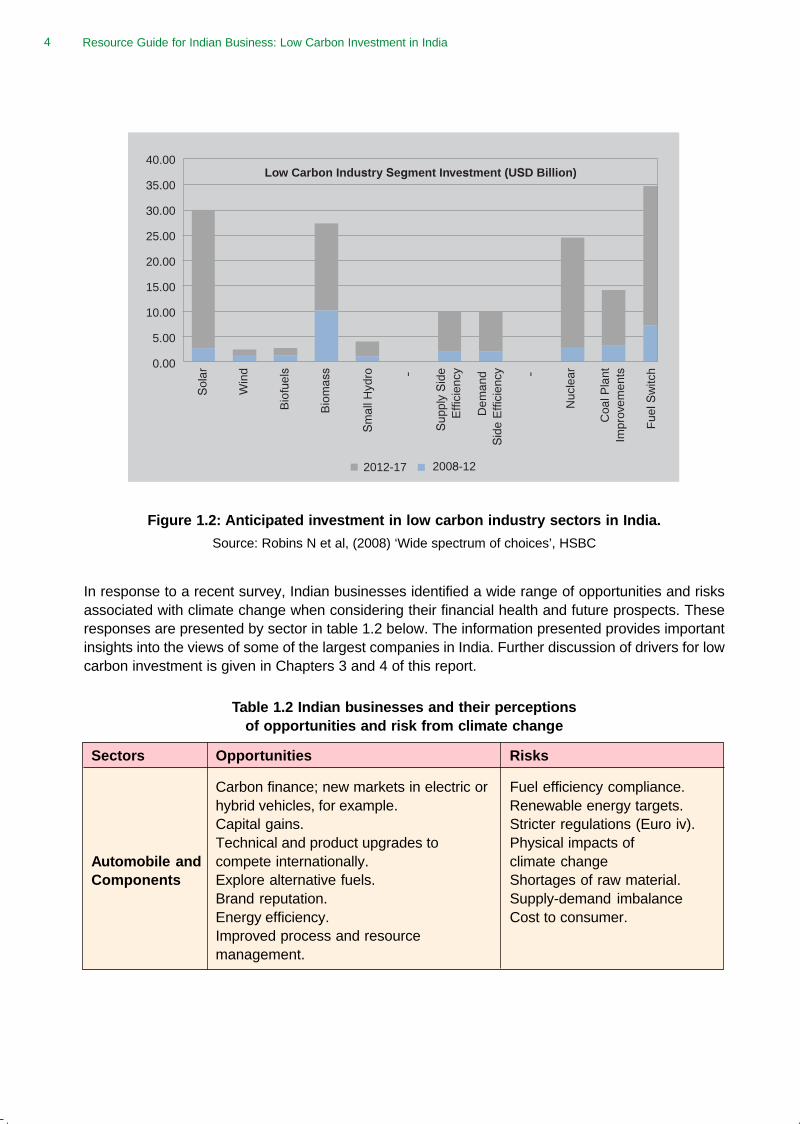

Renewable energy and energy efficiency are already emerging as mature sectors in India3 .Industry segments are shown in figure 1.2 below, including future markets beyond 2012. Thewider low carbon industry in India, inclusive of all core environmental services, supply chaincomponents and the reclassified conventional sectors is pegged4 at aroundUSD 294.2 billion [Rs 1,323,900 crores].

2 Kyoto Protocol: An agreement negotiated in 1997 that commits developed countries to binding greenhouse gas emissions targets butprovides flexible market based mechanisms such as Clean Development Mechanism (CDM) to minimise the cost to participants to meettheir targets. 39 countries within European Union, Economies in Transition and OECD (known as Annexe B countries) agreed to bindingcommitments on the emissions from 1990 to 2008-2012.

3 Renewable energy industry turnover in India was Rs 2,250 crore in 2009. UN (2009), ‘World economic and social survey’.4 Sharp J (2009), Low Carbon environmental goods and services: an industry analysis’, BERR, UK.

Resource Guide for Indian Business: Low Carbon Investment in India4

Figure 1.2: Anticipated investment in low carbon industry sectors in India.

Source: Robins N et al, (2008) ‘Wide spectrum of choices’, HSBC

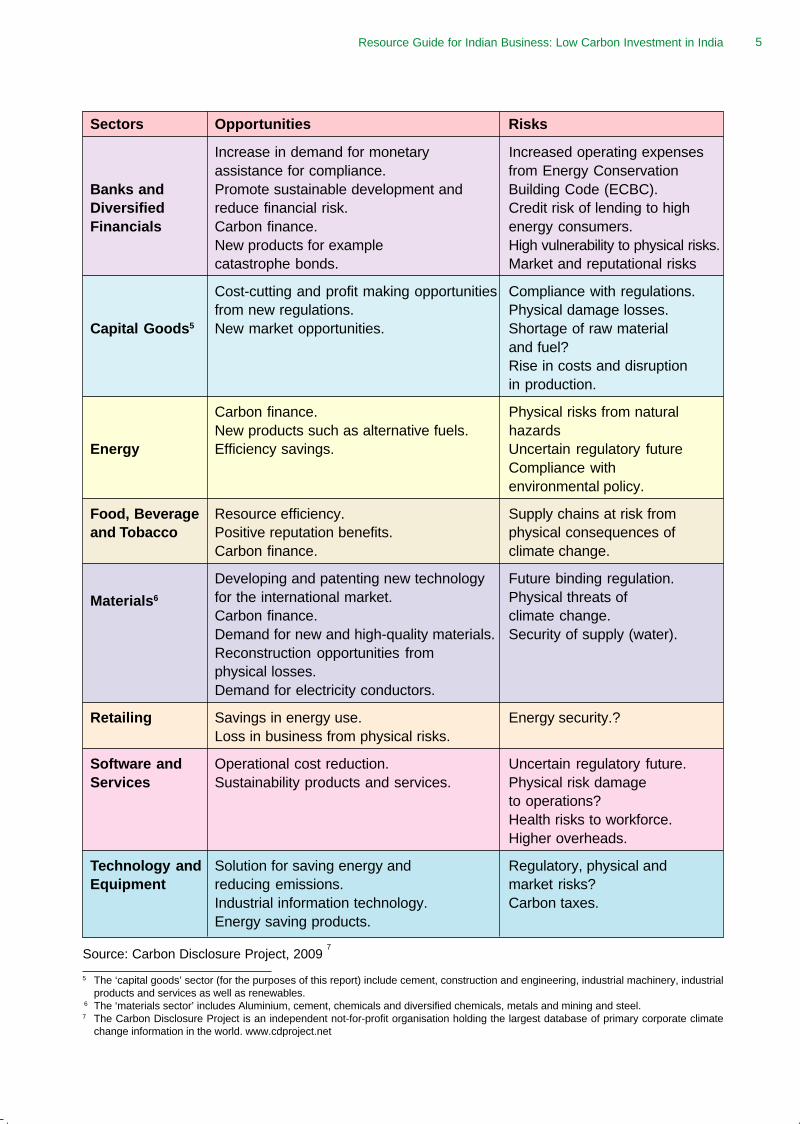

In response to a recent survey, Indian businesses identified a wide range of opportunities and risksassociated with climate change when considering their financial health and future prospects. Theseresponses are presented by sector in table 1.2 below. The information presented provides importantinsights into the views of some of the largest companies in India. Further discussion of drivers for lowcarbon investment is given in Chapters 3 and 4 of this report.

Table 1.2 Indian businesses and their perceptionsof opportunities and risk from climate change

Sectors Opportunities Risks

Carbon finance; new markets in electric or Fuel efficiency compliance.hybrid vehicles, for example. Renewable energy targets.Capital gains. Stricter regulations (Euro iv).Technical and product upgrades to Physical impacts of

Automobile and compete internationally. climate changeComponents Explore alternative fuels. Shortages of raw material.

Brand reputation. Supply-demand imbalanceEnergy efficiency. Cost to consumer.Improved process and resourcemanagement.

Low Carbon Industry Segment Investment (USD Billion)40.00

35.00

30.00

25.00

20.00

15.00

10.00

5.00

0.00

2012-17 2008-12

Sol

ar

Win

d

Dem

and

Sid

e E

ffici

ency

Nuc

lear

Coa

l Pla

ntIm

prov

emen

ts

Fue

l Sw

itch

Sup

ply

Sid

eE

ffici

ency- -

Sm

all H

ydro

Bio

mas

s

Bio

fuel

s

Resource Guide for Indian Business: Low Carbon Investment in India 5

Increase in demand for monetary Increased operating expensesassistance for compliance. from Energy Conservation

Banks and Promote sustainable development and Building Code (ECBC).Diversified reduce financial risk. Credit risk of lending to highFinancials Carbon finance. energy consumers.

New products for example High vulnerability to physical risks.catastrophe bonds. Market and reputational risks

Cost-cutting and profit making opportunities Compliance with regulations.from new regulations. Physical damage losses.

Capital Goods5 New market opportunities. Shortage of raw materialand fuel?Rise in costs and disruptionin production.

Carbon finance. Physical risks from naturalNew products such as alternative fuels. hazards

Energy Efficiency savings. Uncertain regulatory futureCompliance withenvironmental policy.

Food, Beverage Resource efficiency. Supply chains at risk fromand Tobacco Positive reputation benefits. physical consequences of

Carbon finance. climate change.

Developing and patenting new technology Future binding regulation.

Materials6 for the international market. Physical threats ofCarbon finance. climate change.Demand for new and high-quality materials. Security of supply (water).Reconstruction opportunities fromphysical losses.Demand for electricity conductors.

Retailing Savings in energy use. Energy security.?Loss in business from physical risks.

Software and Operational cost reduction. Uncertain regulatory future.Services Sustainability products and services. Physical risk damage

to operations?Health risks to workforce.Higher overheads.

Technology and Solution for saving energy and Regulatory, physical andEquipment reducing emissions. market risks?

Industrial information technology. Carbon taxes.Energy saving products.

Source: Carbon Disclosure Project, 2009 7

Sectors Opportunities Risks

5 The ‘capital goods’ sector (for the purposes of this report) include cement, construction and engineering, industrial machinery, industrialproducts and services as well as renewables.

6 The ‘materials sector’ includes Aluminium, cement, chemicals and diversified chemicals, metals and mining and steel.7 The Carbon Disclosure Project is an independent not-for-profit organisation holding the largest database of primary corporate climate

change information in the world. www.cdproject.net

Resource Guide for Indian Business: Low Carbon Investment in India6

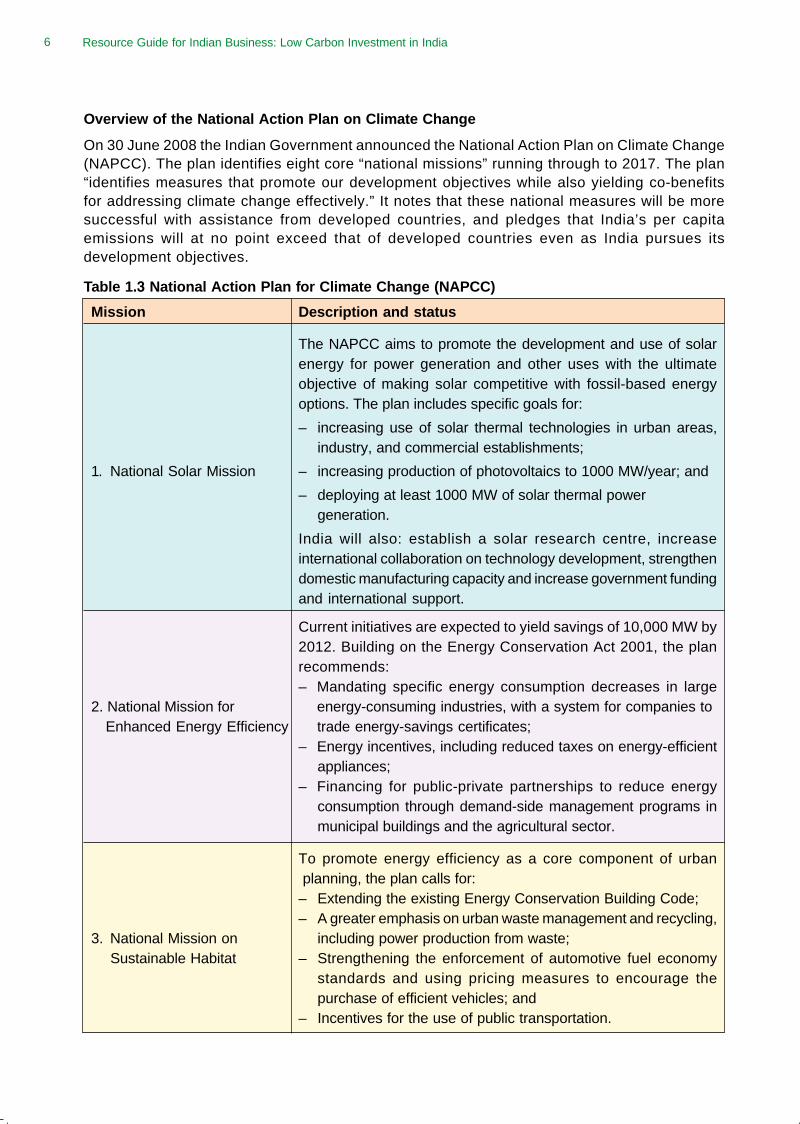

Overview of the National Action Plan on Climate Change

On 30 June 2008 the Indian Government announced the National Action Plan on Climate Change(NAPCC). The plan identifies eight core “national missions” running through to 2017. The plan“identifies measures that promote our development objectives while also yielding co-benefitsfor addressing climate change effectively.” It notes that these national measures will be moresuccessful with assistance from developed countries, and pledges that India’s per capitaemissions will at no point exceed that of developed countries even as India pursues itsdevelopment objectives.

Table 1.3 National Action Plan for Climate Change (NAPCC)

Mission Description and status

The NAPCC aims to promote the development and use of solarenergy for power generation and other uses with the ultimateobjective of making solar competitive with fossil-based energyoptions. The plan includes specific goals for:

– increasing use of solar thermal technologies in urban areas,industry, and commercial establishments;

1. National Solar Mission – increasing production of photovoltaics to 1000 MW/year; and

– deploying at least 1000 MW of solar thermal powergeneration.

India will also: establish a solar research centre, increaseinternational collaboration on technology development, strengthendomestic manufacturing capacity and increase government fundingand international support.

Current initiatives are expected to yield savings of 10,000 MW by2012. Building on the Energy Conservation Act 2001, the planrecommends:– Mandating specific energy consumption decreases in large

2. National Mission for energy-consuming industries, with a system for companies toEnhanced Energy Efficiency trade energy-savings certificates;

– Energy incentives, including reduced taxes on energy-efficientappliances;

– Financing for public-private partnerships to reduce energyconsumption through demand-side management programs inmunicipal buildings and the agricultural sector.

To promote energy efficiency as a core component of urban planning, the plan calls for:– Extending the existing Energy Conservation Building Code;– A greater emphasis on urban waste management and recycling,

3. National Mission on including power production from waste; Sustainable Habitat – Strengthening the enforcement of automotive fuel economy

standards and using pricing measures to encourage thepurchase of efficient vehicles; and

– Incentives for the use of public transportation.

Resource Guide for Indian Business: Low Carbon Investment in India 7

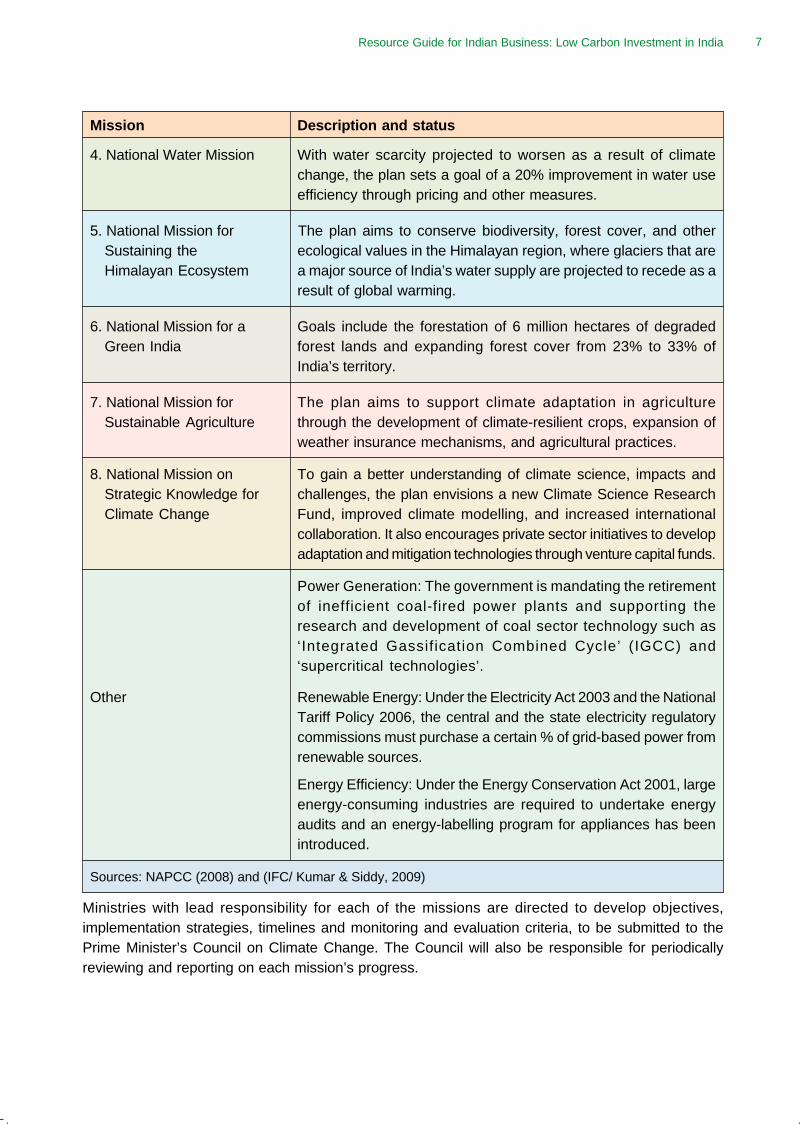

4. National Water Mission With water scarcity projected to worsen as a result of climatechange, the plan sets a goal of a 20% improvement in water useefficiency through pricing and other measures.

5. National Mission for The plan aims to conserve biodiversity, forest cover, and otherSustaining the ecological values in the Himalayan region, where glaciers that areHimalayan Ecosystem a major source of India’s water supply are projected to recede as a

result of global warming.

6. National Mission for a Goals include the forestation of 6 million hectares of degradedGreen India forest lands and expanding forest cover from 23% to 33% of

India’s territory.

7. National Mission for The plan aims to support climate adaptation in agricultureSustainable Agriculture through the development of climate-resilient crops, expansion of

weather insurance mechanisms, and agricultural practices.

8. National Mission on To gain a better understanding of climate science, impacts andStrategic Knowledge for challenges, the plan envisions a new Climate Science ResearchClimate Change Fund, improved climate modelling, and increased international

collaboration. It also encourages private sector initiatives to developadaptation and mitigation technologies through venture capital funds.

Power Generation: The government is mandating the retirementof inefficient coal-fired power plants and supporting theresearch and development of coal sector technology such as‘Integrated Gassification Combined Cycle’ (IGCC) and‘supercritical technologies’.

Other Renewable Energy: Under the Electricity Act 2003 and the NationalTariff Policy 2006, the central and the state electricity regulatorycommissions must purchase a certain % of grid-based power fromrenewable sources.

Energy Efficiency: Under the Energy Conservation Act 2001, largeenergy-consuming industries are required to undertake energyaudits and an energy-labelling program for appliances has beenintroduced.

Sources: NAPCC (2008) and (IFC/ Kumar & Siddy, 2009)

Ministries with lead responsibility for each of the missions are directed to develop objectives,implementation strategies, timelines and monitoring and evaluation criteria, to be submitted to thePrime Minister’s Council on Climate Change. The Council will also be responsible for periodicallyreviewing and reporting on each mission’s progress.

Mission Description and status

Resource Guide for Indian Business: Low Carbon Investment in India8

2. An Enabling Environment For Low Carbon Development

This chapter of the guide outlines the priority areas within the NAPCC for which laws and regulatorymechanisms have been rolled out to ensure progress and enable an environment conducive toinvestment. Individual states are taking the lead from the NAPCC and formulating state-level actionplans. Government regulations require companies to undertake adaptation and mitigation measures,which levels the playing field by making action mandatory.

The Government of India has advised the state governments to produce individual state-level plansin response to the NAPCC issued in 2008. Many states are making progress towards this objective.Renewable energy and the power sector, energy efficiency and strategic knowledge for climatechange have emerged as priority missions and are well underway. Gujarat state for example, launcheda Solar Power Policy on January 6, with an operating period up to March 31 2014, for projectsbetween 5 and 500MW and exemptions from paying the electricity duty on solar power sent to thegrid or used on site. Delhi has been the first to publish a state-level response to each of the missionswithin the NAPCC.

Acceleration of the private sector’s role in low carbon development in India requires a favourable andstable policy environment. This should be perceived as low risk and attractive to investors, both domesticand international. The priority missions within the NAPCC show a number of characteristics thatmake them attractive to investors:

• They can meet an essential demand for India’s future prosperity (i.e. energy).

• They encourage tried and tested technologies, thus investments are relatively low risk.

• The government has provided a number of incentives to investors and businesses.8

• They have the potential to attract carbon finance and generate CERs (Certified EmissionsReductions) tradable in the international market, at least until 2012.

• They can have a high impact on improving resource management within strategic industries suchas power, cement, fertilisers, metals (aluminium, iron and steel), railways, pulp and paper andtextiles. This will result in cost savings and a better reputation for these industries.

The table below shows key regulations and programmes that are in force to deliver the priority missionsrelated to energy efficiency and renewable energy. The national government has shown consistentprogress towards providing a stable platform for business growth in this area.

Energy efficiency related policies and measures

Energy Conservation (EC) Act 2001. The act was passed by the Indian Parliament in 2001.The Act created the Bureau of Energy Efficiency (BEE) to implement the provisions of this Act.The provisions of this act are reflected in the programmes of the National Mission for EnhancedEnergy Efficiency (NMEEE) as described below.

Making the EC Act operational, by strengthening the institutional capacity of StateDesignated Agencies (SDAs). The scheme seeks to build the institutional capacity of the newlycreated SDAs to perform their regulatory, enforcement and facilitative functions in the respectivestates.

8 See Chapter 3 for details of Government incentives for Renewable Energy and Energy Efficiency Sectors.

Resource Guide for Indian Business: Low Carbon Investment in India 9

Key programmes in the National Mission for Enhanced Energy Efficiency (NMEEE)implemented by the Bureau of Energy Efficiency (BEE)

1. Perform Achieve and Trade (PAT) The PAT scheme is a market-based mechanism to enhanceenergy efficiency in the ‘Designated Consumers’ (large energy-intensive industries andfacilities - power, cement, fertiliser, aluminium, iron and steel, railways, pulp and paper andtextiles). The resulting savings can be traded as Energy Savings Certificates (ESCerts),described later in this document.

For example: Enhancing the efficiency of power plants

The Electricity Regulatory Commissions9 have linked tariffs to efficiency enhancement suchas the use of more-efficient ‘super critical’ technology in coal-powered plants. This providesan incentive for renovation and modernisation.

2. Market Transformation for Energy Efficiency (MTEE)

Making energy-efficient products more affordable and mandatory in some designated sectors(mainly industrial). This target is to be achieved by Demand Side Management (DSM)10

measures, supported by carbon finance - CDM financing wherever possible. The initiativeincludes the following activities:

2.1 Programme-based (programmatic) CDM: BEE is exploring undertaking CDM Programmeof Activities within the following sectors: lighting (Bachat Lamp Yojana - replacing incandescentbulbs with energy efficient ‘Compact Fluorescent Lamps’ (CFLs), municipal DSM, agriculturalDSM, the small and medium enterprises (SME) sector, the commercial building sector and fordistribution transformers.

2.2 Standards and labelling: Step by step notification for mandatory labelling of equipment andappliance for domestic sectors, hotel equipment, office equipment, industrial products andtransport equipment.

2.3 The Energy Conservation Building Code (ECBC) 2007: Sets minimum energyperformance standards for new commercial buildings. Energy audits are mandated for largeindustrial consumers.

2.4 Public Procurement: Amendment of procurement rules to explicitly mandate procurement ofenergy efficient products for all public entities. For example, solar thermal equipment for waterheating in public buildings.

Renewable energy (RE) related policies and measures

The Government of India has set a target for at least 10% of grid-connected power to come fromrenewable sources by 2012.

Electricity Act (EA) 2003: Requirement for states to set RE targets

Section 86 of the EA 2003 promotes renewable energy by ensuring grid connectivity and sale forrenewable electricity. The section creates a demand for renewable energy by requiring StateElectricity Regulatory Commissions (SERCs) to specify a percentage of renewable energy to bepurchased within the area of a distribution licensee.

9 For more information on ‘Electricity Regulatory Commissions’ see www.cercind.gov.in10 DSM begins with an audit of the baseline energy use and delivers energy savings by applying technology, behavioural measures and

management practices.

Resource Guide for Indian Business: Low Carbon Investment in India10

National Electricity Policy (NEP) 2005: Private sector participation

Section 5.2.20 of India’s National Electricity Policy promotes private participation in renewableenergy. “Feasible potential of non-conventional energy resources, mainly small hydro, andwind and bio-mass would also need to be exploited fully to create additional power generationcapacity. With a view to increase the overall share of non-conventional energy sources in theelectricity mix, efforts will be made to encourage private sector participation through suitablepromotional measures.”

National Electricity Policy (NEP) 2005: Reducing the costs of renewable energy

Section 5.12.1 of the policy targets the reduction in capital costs of renewable energy technologiesthrough competition.

National Electricity Policy (NEP) 2005: Preferential tariffs

Section 5.12.2 of the policy states that SERCs should specify appropriate tariffs in order to promoterenewable energy (until non-conventional technologies can compete within the competitive biddingsystem), specifying percentages that progressively increase the share of electricity generatedfrom renewable sources.

Industrial policy for renewable energy

• Industrial clearances are not required to set up a company in the renewable energy industry.

• No clearance is required from the Central Electricity Authority (CEA) for power generationprojects up to Rs 100 crores.

• A ten-year tax holiday is allowed for RE generation projects.

• Soft loans are available through IREDA for RE equipment manufacturing.

• Private sector companies can set up enterprises to operate as licensee or powergenerating companies.

• A customs duty concession is available for RE spares and equipment, including those formachinery required for renovation and modernisation of power plants.

Foreign investment policy for renewable energy

• Foreign investors can enter into a joint venture with an Indian partner for financial and/or technicalcollaboration and for setting up RE-based power generation projects.

• 100% foreign investment as equity is permissible with the approval of the Foreign InvestmentPromotion Board (FIPB).

• The government allows 100% foreign direct investment (FDI) in the renewable energy sectorand has put in place conducive policies to attract foreign companies in the sector.

Solar Cities program in India

The government of India plans to develop 60 solar cities during the eleventh Five Year Plan(2007-12), to both meet the increasing electricity demand of its cities and promote the growinguse of renewable energies. Commercially viable technology, like solar thermal heating systems,will therefore play a key role in meeting this target. It will be especially useful in the “greenbuildings” that the government wants to promote on a large scale.

Resource Guide for Indian Business: Low Carbon Investment in India 11

3. Drivers for Private Sector Engagement

This chapter of the guide describes in further detail the key drivers for the private sector to becomefurther involved in and raise finance for low carbon development.

3.1 Rapid economic growth and demand for power

Indian economic growth is contributing to an ever increasing demand-supply gap in electricity production(likely to increase to 17% by 2017, despite annual power capacity growth at 10%). The current andprojected gap will drive investments in the renewable energy sector. At present, more than 90% ofIndia’s energy needs are met through coal and crude oil. Consequently, India’s carbon emissions havegrown by 65% over the past five years (the second highest growth worldwide, only behind China).

According to estimates by the Integrated Energy Policy Committee of the Planning Commission,meeting the projected GDP growth of 8% per annum by 2031-2032 will require 1,836 Mtoe (milliontonnes of oil equivalent), a four-fold increase over the requirements in 2003-04. Commercial energyrequirements are expected to be around 1,651Mtoe, a five-fold increase from 2003-04 levels11 . Primaryenergy demand in India is expected to more than double by 2030, growing by an average of 3.6% ayear. India’s rapidly growing incomes have also fuelled a demand for transport making it the fastestgrowing sector in India. This rapid increase in overall demand for energy has led to an increasingfocus on scaling-up low carbon processes (renewable energy and energy efficiency).

The Rapidly Growing Transport Sector

With climate change and peak oil becoming two of the major challenges of development today,transport and its contribution to energy consumption and carbon dioxide emissions, are takingcentre stage. According to the Inter-governmental Panel on climate change (IPCC), transportrelated carbon dioxide emissions are expected to increase 57% worldwide in the period 2005 –2030, and transport in developing countries is going to contribute about 80 % of this increase,both from passenger and freight transport. Most of the current GHG emissions in the transportsector and virtually all the expected growth in emissions come from private cars and trucks.

In India, the National Urban Transport Policy (NUTP) of 2006 clearly outlines the priority thatneeds to be given to public transport and non-motorised modes of transport. The JawaharlalNehru Urban Renewal Mission (JNNURM) takes direction from the NUTP and makes sure thatfunds are released for urban development only if the project caters to and prioritises public andnon-motorised transport (NMT) such as cycle-rickshaws.

Several initiatives have been taken by the Ministry of Urban Development to promote sustainabletransport practices in the country. The Urban Transport Planning schemes allow up to 80% ofcentral assistance to sustainable transport plans at the city level. There are plans to introduce ‘BusRapid Transit Systems’ (BRTS)12 in all the 5 million-plus cities in India. Delhi and Ahmedabadalready have operational systems and the others are following this lead. These corridors are to beintegrated with dedicated paths for non-motorised transport. The sanctioning of 15,260 modern‘Intelligent Transportation System’ (ITS) enabled buses for 61 mission cities has brought organisedpublic transport in as many as 34 cities for the first time.

With the World Bank – Global Environment Facility (GEF)’s supports demonstration projectson NMT, BRTS, Compressed Natural gas (CNG) and bio-diesel are being implemented. At thesame time several initiatives have been taken to build the capacities of the cities with workshops,guidelines and toolkits. There is 100% financial support from the central government for capacity

11 Kaur J et al. (2008) ‘Cleantech venture capital and private equity investments in India’.12 BRTS is a system based on dedicated bus lanes where other traffic is not allowed.

Resource Guide for Indian Business: Low Carbon Investment in India12

building for cities such as training and workshops. The JNNURM policy document specificallyhighlights the importance of the involvement of the private sector in the the process of urbanrenewal.

Transport-related incentives and subsidies in the 2010-2011 Union Budget:

• A nominal duty of 4% on electric cars and vehicles in order to neutralise the duty paid on theirinputs and components. Some critical parts or sub-assemblies of such vehicles are exemptedfrom basic customs duty and special additional duty. These parts will also enjoy a concessionalCountervailing Duty (CVD) of 4%.

• A concessional excise duty of 4% provided to “soleckshaw”, a product developed by the Councilfor Scientific and Industrial Research (CSIR) to replace manually-operated rickshaws. Keyparts and components will be exempted from customs duty.

• Reduction in duty on bio-fuels usage in the country.

Additionally, the Ministry of New and Renewable Energy (MNRE) provides subsidies of up to33% of the cost of the vehicle for use by institutions and other public organisation. In statessuch as Delhi, electric vehicles attract VAT refunds and exemption from registration fees. Newprojects such as the ‘Delhi Metro’ have been developed with private sector involvement andmake use of technologies that reduce carbon emissions and are also eligible for carbon finance,generating CERs.

3.2 National Action Plan on Climate Change (NAPCC)

As detailed in Chapter 1, the Government of India has planned reductions in carbon intensity of itseconomy by launching the NAPCC. Under the NAPCC, several initiatives have been planned whichwill propel low carbon investments in India as well as better management of water, natural habitatsand human settlements. There are provisions within the NAPCC that oblige Indian businesses as wellas incentivise them to be more energy-efficient and purchase or invest in renewable energy.

The NAPCC will affect a range of Indian businesses; equally, a variety of businesses can contributetowards one or more missions within the NAPCC. The diagram below presents the relationship betweensectors with the potential for low carbon development, associated national programmes and relevantnodal agencies within the government. Indian businesses need to monitor the information emergingfrom these nodal agencies at the national and state level so that they can keep track of their obligationsas well as emerging business opportunities.

TABLE 3.1: Low carbon development sectors, national missions and nodal agencies

Status

MatureMarkets

Industry SectorRenewable Energy

Low CarbonConventionalPower

Examples

a. Nuclear

Relevant Agencies

Ministry of New &Renewable Energy(MNRE).Indian RenewableEnergy DevelopmentAgency (IREDA).

Department ofAtomic Energy.

Drivers of growth

1. Carbon finance – renewableenergy.

2. Jawaharlal Nehru NationalSolar Mission (JNNSM).

3. National Renewable energytrading.

1. Nuclear fuel & technologysupply agreements betweenIndia and other worldnations.

Resource Guide for Indian Business: Low Carbon Investment in India 13

3.3 Government incentives and policies

The government is putting in place incentives, fiscal measures and preferential arrangements suchas feed-in-tariffs to attract investors and enable projects to be commercially viable. The box belowsummarises a range of incentives that are currently on offer to Indian businesses.

The government is also establishing research and innovation centres to meet the need for efficient,scalable and cost-effective technology. Three leading research institutions have been set-up recently:the Centre for Wind Energy Technology (CWET), the Solar Energy Centre (SEC) and the NationalInstitute for Renewable Energy (NIRE) for wind, solar and bio-fuels research respectively.

Status Industry Sector Examples Relevant Agencies Drivers of growth

GrowingMarkets

NascentMarkets

Energy Efficiency

Other CleanTechnologies

Waste management/ResourceEfficiency (Water)

SustainableAgriculture

Forestation/Reforestation

Climate changeinnovativetechnologies fund.

b. Coal PlantImprovements

a. Fuel Switch

a. PublicTransport/Railways

b. Electric/Hybrid/Cleanervehicles

Bureau of EnergyEfficiency (BEE).

Ministry of Power.

Bureau of EnergyEfficiency (BEE).

Ministry of UrbanDevelopment/Ministry ofRailways.

Ministry of New &Renewable Energy(MNRE)

State governments.

Ministry ofAgriculture.

State Governments.

Ministry ofEnvironment &Forests.

1. Energy Efficiency Trading.

1. New Gas Discoveries.

1. National Mission forEnhanced Energy Efficiency– NMEEE.

2. Energy Savings Certificatetrading.

3. Carbon finance – energyefficiency.

1. Jawaharlal Nehru NationalUrban Renewal Mission.

2. National Mission ofSustainable Habitat.

1. Program on BatteryOperated Vehicles, MNRE.

2. Rising fuel prices to driveconsumer towards more fuelefficient vehicles.

1. National Water Mission.2. National Mission for

Sustainable Habitat.

1. National Mission forSustainable Agriculture.

1. National Mission for aGreen India Ecosystem.

2. National Mission forSustaining the HimalayanEcosystem.

1. National Mission onStrategic Knowledge.

Interpreted from discussions and sources of information listed in Appendix 1.

Resource Guide for Indian Business: Low Carbon Investment in India14

Renewable Energy (RE): Wind, solar, bio-mass, small-hydro – government incentives13

Financial incentives for investing in renewable energy technologies

• Financial incentives from Ministry of New & Renewable Energy (MNRE), such as interest andcapital subsidy.

• Soft loans through:

1) IREDA.

2) Nationalised banks and other financial institutions for identified technologies/systems.

• Fiscal Incentives:

1) Direct taxes – 100% depreciation in the first year of the installation of the project.

a) Accelerated 80% depreciation on specified RE-based devices/projects.

b) Section 80IA – Industrial undertakings set up in any part of India for the generation orgeneration and distribution of power – 100% deduction is allowable from profits andgains for the first five years.

c) Section 115J – exemption from Minimum Alternative Tax (MAT) to industrialundertakings on profits derived from the business of generation and distribution ofelectricity.

d) Section 80JJA – 100% deduction in respect of profit and gains from business ofcollecting and processing bio-degradable wastes.

2) Exemption/reduction in excise duty.

3) Exemption from Central Sales Tax, and customs duty concessions on the import of material,components and equipment used in RE projects.

4) Generation-based incentives for solar and wind power projects.

5) Government policies covering wheeling, banking, buy-back, and third-party sale of power.

6) Other incentives for preparation of feasibility reports and detailed project reports (DPR).

7) Research and development (R&D) subsidy to the tune of 100% of project cost in governmentR&D institutions and 50% in the case of private institutions.

Other incentives

• 12 out of 29 states have implemented quotas for renewable electricity and have introducedpreferential tariffs for renewable electricity.

• Energy buy-back.

• Preferential grid connection.

• Electricity tax exemptions.

• In March 2007 the Indian Government announced a semiconductor policy under its SpecialIncentive Package Scheme (SIPS). According to this policy, the government or its agencies willprovide 20% of the capital expenditure during the first 10 years for semiconductor industries,including manufacturing activities related to solar PV technology located in Special EconomicZones (SEZ), and 25% for industries not located in an SEZ.

13 References:1) BEE http://www.bee-india.nic.in/down.php?f=actionplan.pdf2) Ministry of New & Renewable Energy www.mnes.nic.in/pdf/11th-plan-proposal.pdf3) Deutsche Research: Global Climate Change Policy Tracker: An Investor’s Assessment4) http://india-reports.in/earth-solutions/government-policies-for-renewable-energy-in-india/5) http://www.indiaenergyportal.org/viewPolicies.php?id=PO1&theme=

Resource Guide for Indian Business: Low Carbon Investment in India 15

• A specific incentive scheme for solar power was launched in 2008 and is expected to cost thegovernment Rs 90 crores and bring in private investment to the tune of Rs 1000 crores:

1) Generation based incentive of up to Rs 12 per kilowatt from solar photovoltaic cells.

2) Generation based incentive of Rs 10 per kilowatt for power generated through solar thermalpower plants.

• Specific to Wind Energy

1) 10 year income tax exemption.

2) 80% accelerated depreciation.

3) Sales tax and excise duty exemption.

4) National generation-based scheme for grid-connected power projects under 49 MW,providing an incentive of 0.7 cents per kWh.

Feed-in tariffs

“Feed-in-tariffs are a fixed price for every unit of electricity produced by a renewable source that isusually above the tariff rates of conventional power.”14 The feed-in-tariff gives investors a guaranteedprice for the power produced by them using renewable energy sources. In India, the Ministry of Newand Renewable Energy declared feed-in-tariffs first for solar and wind power projects. These feed-in-tariffs were made available for projects supported by MNRE. This in turn served as a guideline forstates to come up with a preferential tariff for renewable energy projects. This preferential tariff includesa buy back agreement from state electricity boards for the renewable power produced. The preferentialtariffs vary, mainly depending upon the renewable energy source and cost of fuel in different states.

MNRE provides a feed-in-tariff of Rs 0.50 per unit of wind power produced for a period of 10years15 . Project developers are not eligible for accelerated depreciation benefit if they opt for feed-in-tariff. Independent power producers generally prefer for feed-in-tariff whereas corporates investingin wind projects generally prefer accelerated depreciation benefits.

Under the National Solar Mission, the preferential tariff for solar PV is Rs 18.34 for projectscommissioned on or before 31st March 2012 and Rs 15.6 per unit for solar thermal projectscommissioned on or before 31st March 2013.

The preferential tariffs for various renewable energy power sources and states are made availableby state electricity regulatory commissions. These tariffs are revised periodically based on petitionssubmitted by power generators and power distributing companies. The tariffs are made availablein the “tariff orders” section of state electricity regulatory commissions’ website.

Indian Union Budget 2010-11

The 2010/11 Budget proposed additional provisions for clean technology projects in the country.Key features of initiatives planned in the latest Budget are detailed below.

• Formation of National Clean Energy Fund to fund research and innovative clean energy projectsin India. Funding will come from Rs 50/Ton levy of Coal produced and imported in India (approx450-500 Million tons/annum; hence 2500 crores/annum).

• Provision of a concessional customs duty of 5% to machinery, instruments, equipment andappliances required for the initial setting up of photovoltaic and solar thermal power generatingunits and exemption from Central Excise duty. Ground source heat pumps used to tap geo-thermal energy to be exempted from basic customs duty and special additional duty.

• Central Excise duty on LED lights reduced from 8% to 4% at par with Compact Fluorescent Lamps.

14 Handbook on Best Practices for the Successful Deployment of Grid-Connected Renewable Energy, Distributed Generation, Cogeneration,and Combined Heat and Power in India compiled by United States Energy Association.

15 Baker and McKenzie (2008)

Resource Guide for Indian Business: Low Carbon Investment in India16

3.4 Carbon emissions: market-led and voluntary reductions

India is a party to the United Nations Framework Convention for Climate Change (UNFCCC) and soClean Development Mechanism (CDM) projects can be implemented in India and the resulting CertifiedEmissions Reductions (CERs) can be traded globally. The availability of these tradable CERs increasesthe attractiveness and viability of projects for investors.

In terms of numbers of projects, India’s CDM projects are second only to China, facilitating an investmentof Rs 151,397 crores.16 The type of projects in India tend to be smaller in scale, with a low intensity ofCERs generated, and have been in the sectors of energy efficiency, renewable energy, forestry, fuelswitching, industrial processes and municipal solid waste. The potential for CER generated inflow inIndia is estimated by National Clean Development Mechanism Authority (NCDMA) at 25,500 crores[5.73 billion USD] by 2012. However, while this could provide a significant funding stream, the futureof the CDM is not clear beyond 2012, though international efforts are being made to improve the CDMprocess, its impact and secure its future beyond 2012.

Indian companies are increasingly measuring, reporting and managing their GHG emissions. In asurvey carried out as part of the Carbon Disclosure Project17 (CDP), a significant percentage of theresponding companies acknowledged the various risks and opportunities climate change presents.They reported investment into research and innovation to reduce their risks and enable them tocomply with future regulations. Many companies believe that the new regulations such as NationalMission for Enhanced Energy Efficiency (NMEEE) will drive resource efficiency and positively impacton their profit margins. Businesses are also asking how much money can be saved and made fromGHG emissions reductions and other clean development sectors.18 Many companies do not perceiverisks from current climate change related regulations, but do expect tighter regulation in the futurefor polluters and inefficient business processes. There is also a shared understanding that carbonfinance is an attractive proposition and many firms would like the process to be simplified andmade more accessible.

Internal Carbon Abatement Curve (ICAC)

Private businesses which generate significant emissions will increasingly have to decide the bestamong the options to cut, invest or pay. Companies can draw up their internal ICAC which allowsthem to consider which carbon reduction options are cheaper than simply buying allowances in themarket to comply with legislation. This will increase as national and regional programmes such asRECs and ESCerts are rolled out (see Chapter 4).

3.5 Other stimuli

Businesses in multiple sectors have voluntarily chosen to adopt low carbon development strategies.Their motivation has been perceived risk from a changing climate as well as obtaining market advantageby responding early to the growing environmental awareness among consumers and trade partners.Many Indian businesses are part of global supply chains and there is high visibility of environmentalissues among the world’s markets, civil society and consumers. Trade between markets such as EUand India will increasingly be subject to environmental and climate change screening19 .

16 National Clean Development Mechanism Authority (NCDMA).17 The Carbon Disclosure Project is an independent not-for-profit organisation holding the largest database of primary corporate climate

change information in the world. www.cdproject.net18 Carbon disclosure project report (2009).19 Screening denotes an institutional process to evaluate or regulate social, economic, environmental and mitigation outcomes of trade,

projects or programmes. Climate change and energy related directives within the EU have a high impact on how goods and services aresupplied in the EU from within or abroad.

Resource Guide for Indian Business: Low Carbon Investment in India 17

4. Finance for Low Carbon Development

This chapter provides further detail and links to the sources of finance for low carbon development.These are both international and within India. As good practice, Indian businesses should review theirbusiness practices regularly and explore opportunities to draw on investment opportunities, incentivesand the market advantages posed by reducing emissions of GHGs, energy savings and bettermanagement of waste and water. In summary, being green is good for business.

The funding requirements for mitigation, adaptation and environmental technology are enormous. Toillustrate the scale of investment required, the International Energy Agency estimates that nearly35 Trillion USD [Rs 157,500,000 crores] are required globally to finance low carbon or renewable energybetween 2010 and 2030. This investment will help maintain the global temperature rise to 2°C or less.

Current levels of global investment20 in this area are estimated to be 0.18 Trillion USD [Rs 810,000crores] per annum, just a fraction of the required annualised investment. While this is a huge gap,there is also a great deal of global political momentum to drive investment into these areas.

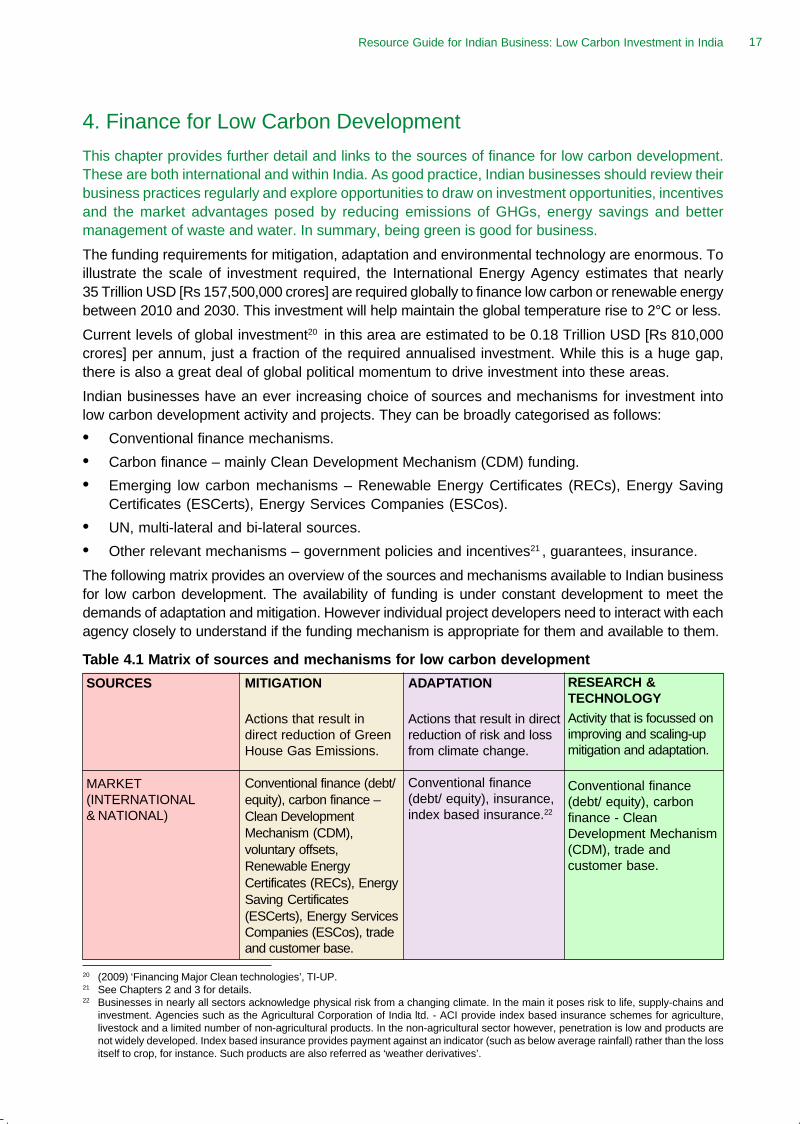

Indian businesses have an ever increasing choice of sources and mechanisms for investment intolow carbon development activity and projects. They can be broadly categorised as follows:

• Conventional finance mechanisms.

• Carbon finance – mainly Clean Development Mechanism (CDM) funding.

• Emerging low carbon mechanisms – Renewable Energy Certificates (RECs), Energy SavingCertificates (ESCerts), Energy Services Companies (ESCos).

• UN, multi-lateral and bi-lateral sources.

• Other relevant mechanisms – government policies and incentives21 , guarantees, insurance.

The following matrix provides an overview of the sources and mechanisms available to Indian businessfor low carbon development. The availability of funding is under constant development to meet thedemands of adaptation and mitigation. However individual project developers need to interact with eachagency closely to understand if the funding mechanism is appropriate for them and available to them.

Table 4.1 Matrix of sources and mechanisms for low carbon development

SOURCES

MARKET(INTERNATIONAL& NATIONAL)

MITIGATION

Actions that result indirect reduction of GreenHouse Gas Emissions.

Conventional finance (debt/equity), carbon finance –Clean DevelopmentMechanism (CDM),voluntary offsets,Renewable EnergyCertificates (RECs), EnergySaving Certificates(ESCerts), Energy ServicesCompanies (ESCos), tradeand customer base.

ADAPTATION

Actions that result in directreduction of risk and lossfrom climate change.

Conventional finance(debt/ equity), insurance,index based insurance.22

RESEARCH &TECHNOLOGY

Activity that is focussed onimproving and scaling-upmitigation and adaptation.

Conventional finance(debt/ equity), carbonfinance - CleanDevelopment Mechanism(CDM), trade andcustomer base.

20 (2009) ‘Financing Major Clean technologies’, TI-UP.21 See Chapters 2 and 3 for details.22 Businesses in nearly all sectors acknowledge physical risk from a changing climate. In the main it poses risk to life, supply-chains and

investment. Agencies such as the Agricultural Corporation of India ltd. - ACI provide index based insurance schemes for agriculture,livestock and a limited number of non-agricultural products. In the non-agricultural sector however, penetration is low and products arenot widely developed. Index based insurance provides payment against an indicator (such as below average rainfall) rather than the lossitself to crop, for instance. Such products are also referred as ‘weather derivatives’.

Resource Guide for Indian Business: Low Carbon Investment in India18

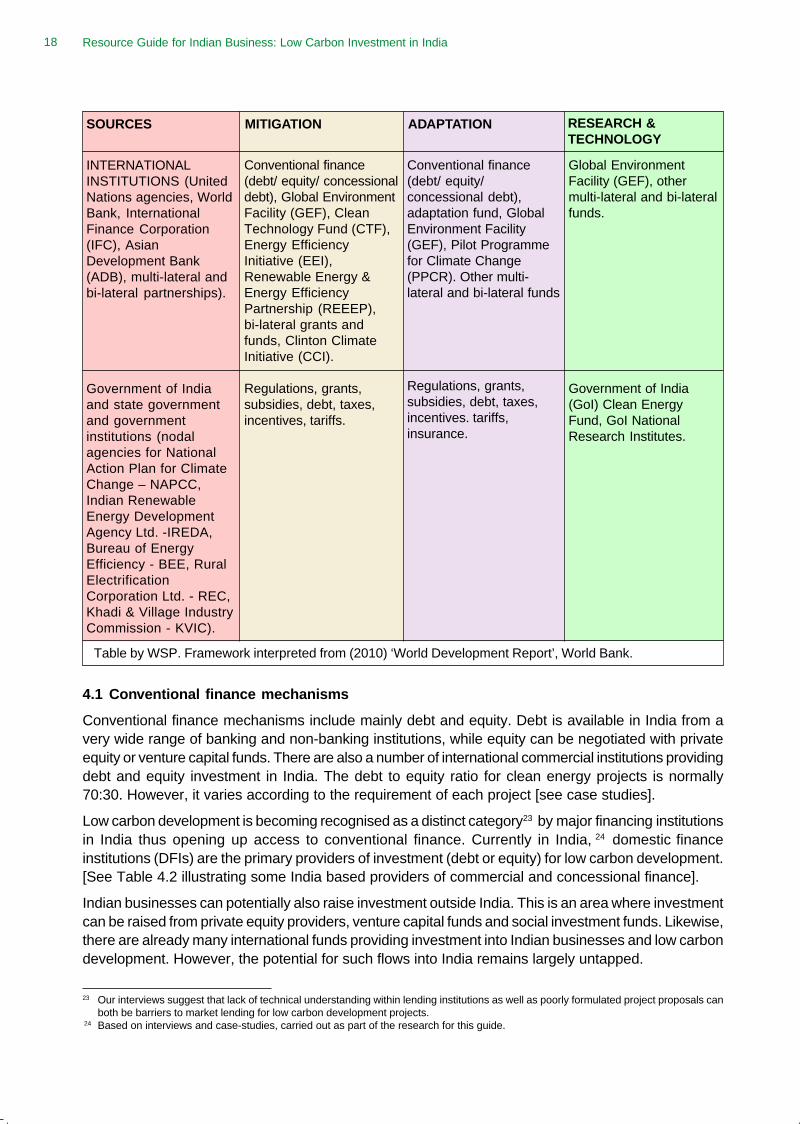

4.1 Conventional finance mechanisms

Conventional finance mechanisms include mainly debt and equity. Debt is available in India from avery wide range of banking and non-banking institutions, while equity can be negotiated with privateequity or venture capital funds. There are also a number of international commercial institutions providingdebt and equity investment in India. The debt to equity ratio for clean energy projects is normally70:30. However, it varies according to the requirement of each project [see case studies].

Low carbon development is becoming recognised as a distinct category23 by major financing institutionsin India thus opening up access to conventional finance. Currently in India, 24 domestic financeinstitutions (DFIs) are the primary providers of investment (debt or equity) for low carbon development.[See Table 4.2 illustrating some India based providers of commercial and concessional finance].

Indian businesses can potentially also raise investment outside India. This is an area where investmentcan be raised from private equity providers, venture capital funds and social investment funds. Likewise,there are already many international funds providing investment into Indian businesses and low carbondevelopment. However, the potential for such flows into India remains largely untapped.

SOURCES MITIGATION ADAPTATION RESEARCH &TECHNOLOGY

INTERNATIONALINSTITUTIONS (UnitedNations agencies, WorldBank, InternationalFinance Corporation(IFC), AsianDevelopment Bank(ADB), multi-lateral andbi-lateral partnerships).

Government of Indiaand state governmentand governmentinstitutions (nodalagencies for NationalAction Plan for ClimateChange – NAPCC,Indian RenewableEnergy DevelopmentAgency Ltd. -IREDA,Bureau of EnergyEfficiency - BEE, RuralElectrificationCorporation Ltd. - REC,Khadi & Village IndustryCommission - KVIC).

Conventional finance(debt/ equity/ concessionaldebt), Global EnvironmentFacility (GEF), CleanTechnology Fund (CTF),Energy EfficiencyInitiative (EEI),Renewable Energy &Energy EfficiencyPartnership (REEEP),bi-lateral grants andfunds, Clinton ClimateInitiative (CCI).

Regulations, grants,subsidies, debt, taxes,incentives, tariffs.

Conventional finance(debt/ equity/concessional debt),adaptation fund, GlobalEnvironment Facility(GEF), Pilot Programmefor Climate Change(PPCR). Other multi-lateral and bi-lateral funds

Regulations, grants,subsidies, debt, taxes,incentives. tariffs,insurance.

Global EnvironmentFacility (GEF), othermulti-lateral and bi-lateralfunds.

Government of India(GoI) Clean EnergyFund, GoI NationalResearch Institutes.

Table by WSP. Framework interpreted from (2010) ‘World Development Report’, World Bank.

23 Our interviews suggest that lack of technical understanding within lending institutions as well as poorly formulated project proposals canboth be barriers to market lending for low carbon development projects.

24 Based on interviews and case-studies, carried out as part of the research for this guide.

Resource Guide for Indian Business: Low Carbon Investment in India 19

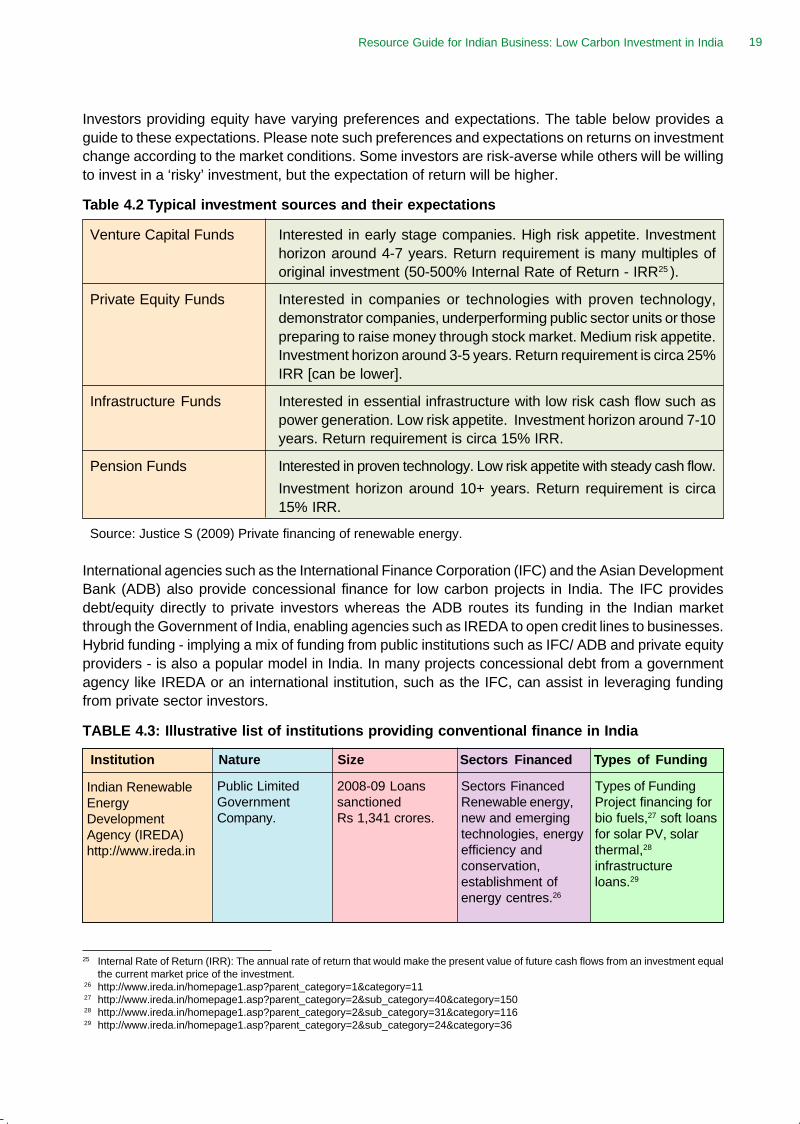

Investors providing equity have varying preferences and expectations. The table below provides aguide to these expectations. Please note such preferences and expectations on returns on investmentchange according to the market conditions. Some investors are risk-averse while others will be willingto invest in a ‘risky’ investment, but the expectation of return will be higher.

Table 4.2 Typical investment sources and their expectations

Venture Capital Funds Interested in early stage companies. High risk appetite. Investmenthorizon around 4-7 years. Return requirement is many multiples oforiginal investment (50-500% Internal Rate of Return - IRR25 ).

Private Equity Funds Interested in companies or technologies with proven technology,demonstrator companies, underperforming public sector units or thosepreparing to raise money through stock market. Medium risk appetite.Investment horizon around 3-5 years. Return requirement is circa 25%IRR [can be lower].

Infrastructure Funds Interested in essential infrastructure with low risk cash flow such aspower generation. Low risk appetite. Investment horizon around 7-10years. Return requirement is circa 15% IRR.

Pension Funds Interested in proven technology. Low risk appetite with steady cash flow.

Investment horizon around 10+ years. Return requirement is circa15% IRR.

Source: Justice S (2009) Private financing of renewable energy.

International agencies such as the International Finance Corporation (IFC) and the Asian DevelopmentBank (ADB) also provide concessional finance for low carbon projects in India. The IFC providesdebt/equity directly to private investors whereas the ADB routes its funding in the Indian marketthrough the Government of India, enabling agencies such as IREDA to open credit lines to businesses.Hybrid funding - implying a mix of funding from public institutions such as IFC/ ADB and private equityproviders - is also a popular model in India. In many projects concessional debt from a governmentagency like IREDA or an international institution, such as the IFC, can assist in leveraging fundingfrom private sector investors.

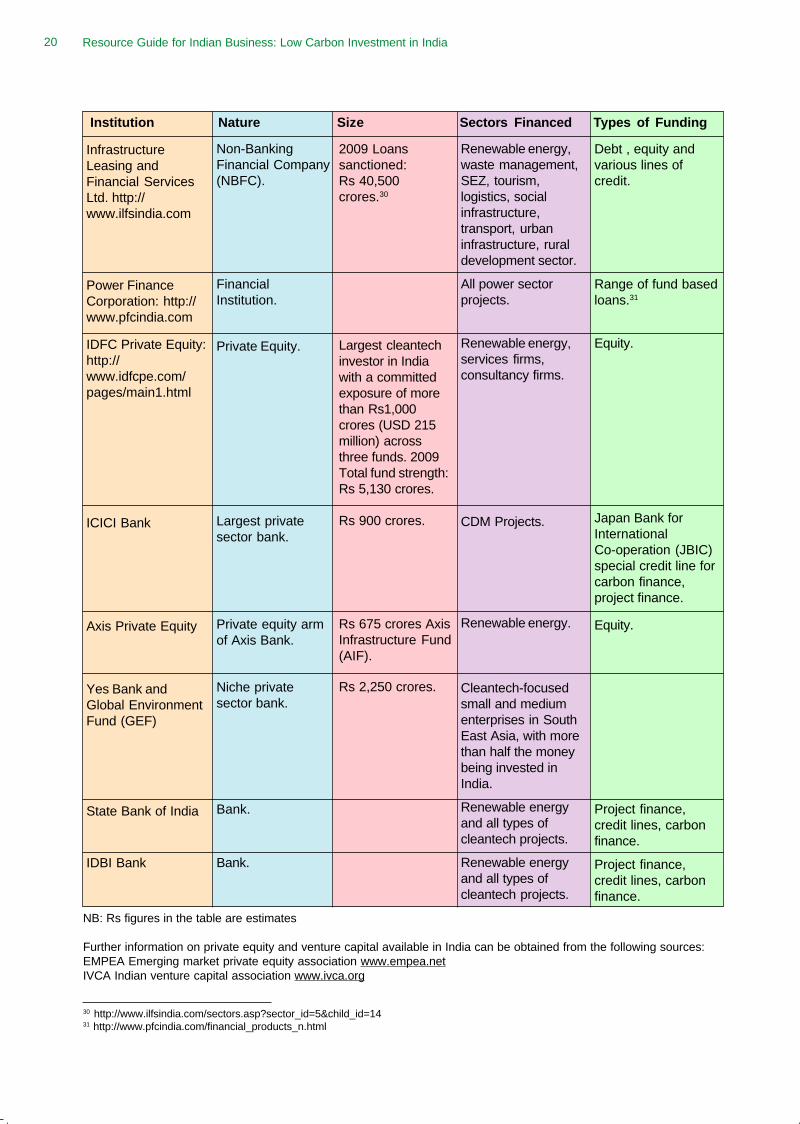

TABLE 4.3: Illustrative list of institutions providing conventional finance in India

Institution Nature Size Sectors Financed Types of Funding

Indian RenewableEnergyDevelopmentAgency (IREDA)http://www.ireda.in

Public LimitedGovernmentCompany.

2008-09 LoanssanctionedRs 1,341 crores.

Sectors FinancedRenewable energy,new and emergingtechnologies, energyefficiency andconservation,establishment ofenergy centres.26

Types of FundingProject financing forbio fuels,27 soft loansfor solar PV, solarthermal,28

infrastructureloans.29

25 Internal Rate of Return (IRR): The annual rate of return that would make the present value of future cash flows from an investment equalthe current market price of the investment.

26 http://www.ireda.in/homepage1.asp?parent_category=1&category=1127 http://www.ireda.in/homepage1.asp?parent_category=2&sub_category=40&category=15028 http://www.ireda.in/homepage1.asp?parent_category=2&sub_category=31&category=11629 http://www.ireda.in/homepage1.asp?parent_category=2&sub_category=24&category=36

Resource Guide for Indian Business: Low Carbon Investment in India20

30 http://www.ilfsindia.com/sectors.asp?sector_id=5&child_id=1431 http://www.pfcindia.com/financial_products_n.html

NB: Rs figures in the table are estimates

Further information on private equity and venture capital available in India can be obtained from the following sources:EMPEA Emerging market private equity association www.empea.netIVCA Indian venture capital association www.ivca.org

Institution Nature Size Sectors Financed Types of Funding

InfrastructureLeasing andFinancial ServicesLtd. http://www.ilfsindia.com

Power FinanceCorporation: http://www.pfcindia.com

IDFC Private Equity:http://www.idfcpe.com/pages/main1.html

ICICI Bank

Axis Private Equity

Yes Bank andGlobal EnvironmentFund (GEF)

State Bank of India

IDBI Bank

Non-BankingFinancial Company(NBFC).

FinancialInstitution.

Private Equity.

Largest privatesector bank.

Private equity armof Axis Bank.

Niche privatesector bank.

Bank.

Bank.

2009 Loanssanctioned:Rs 40,500crores.30

Largest cleantechinvestor in Indiawith a committedexposure of morethan Rs1,000crores (USD 215million) acrossthree funds. 2009Total fund strength:Rs 5,130 crores.

Rs 900 crores.

Rs 675 crores AxisInfrastructure Fund(AIF).

Rs 2,250 crores.

Renewable energy,waste management,SEZ, tourism,logistics, socialinfrastructure,transport, urbaninfrastructure, ruraldevelopment sector.

All power sectorprojects.

Renewable energy,services firms,consultancy firms.

CDM Projects.

Renewable energy.

Cleantech-focusedsmall and mediumenterprises in SouthEast Asia, with morethan half the moneybeing invested inIndia.

Renewable energyand all types ofcleantech projects.

Renewable energyand all types ofcleantech projects.

Debt , equity andvarious lines ofcredit.

Range of fund basedloans.31

Equity.

Japan Bank forInternationalCo-operation (JBIC)special credit line forcarbon finance,project finance.

Equity.

Project finance,credit lines, carbonfinance.

Project finance,credit lines, carbonfinance.

Resource Guide for Indian Business: Low Carbon Investment in India 21

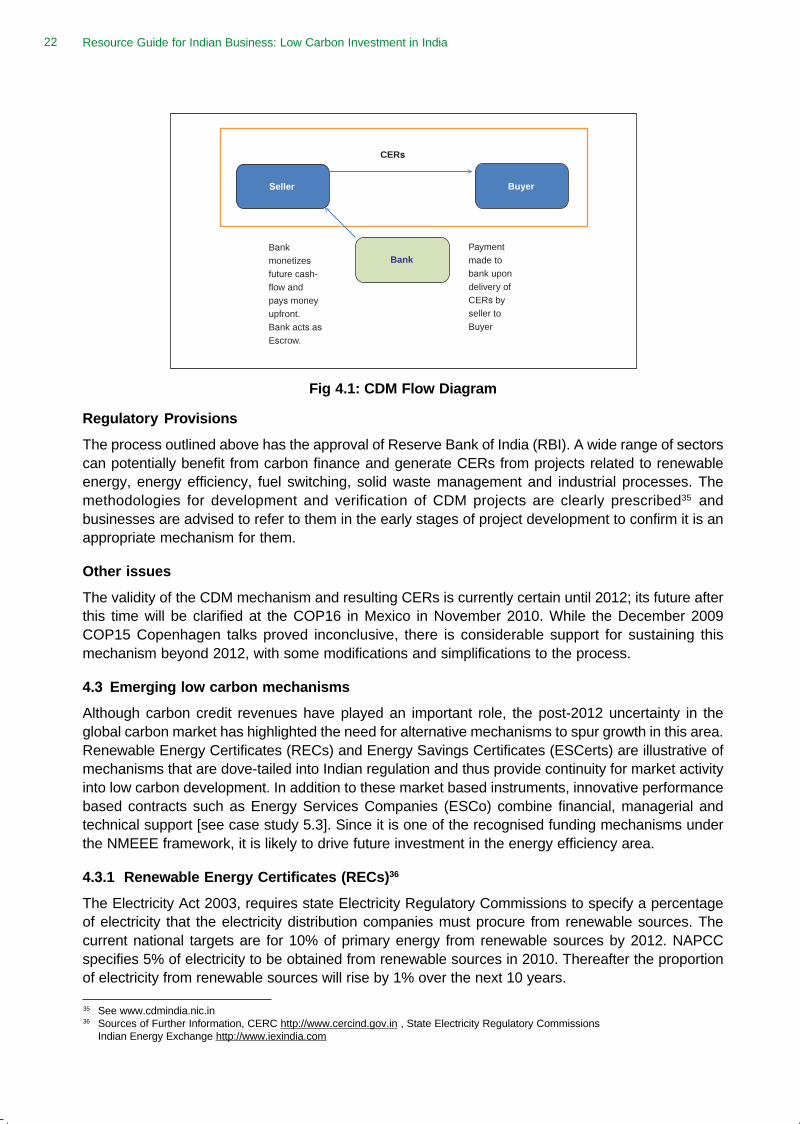

4.2 Carbon finance