respondent franchise tax board's exhibitsrespondent franchise tax board's exhibits for...

TRANSCRIPT

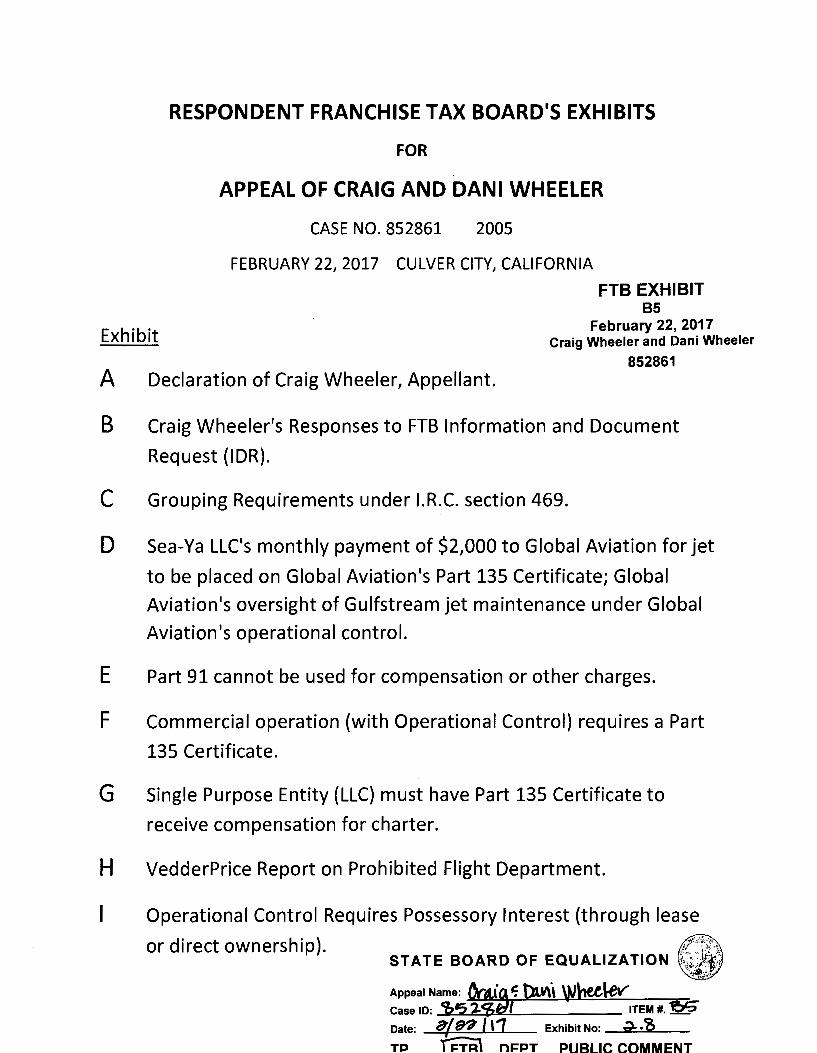

RESPONDENT FRANCHISE TAX BOARD'S EXHIBITS

FOR

APPEAL OF CRAIG AND DANI WHEELER

CASE NO. 852861 2005

FEBRUARY 22, 2017 CULVER CITY, CALIFORNIA

FTB EXHIBIT 85

February 22, 2017 Craig Wheeler and Dani Wheeler

852861

Exhibit

A Declaration of Craig Wheeler, Appellant.

B Craig Wheeler's Responses to FTB Information and Document

Request (IDR).

C Grouping Requirements under I.R.C. section 469.

D Sea-Ya LLC's monthly payment of $2,000 to Global Aviation for jet

to be placed on Global Aviation's Part 135 Certificate; Global

Aviation's oversight of Gulfstream jet maintenance under Global

Aviation's operational control.

E Part 91 cannot be used for compensation or other charges.

F Commercial operation (with Operational Control) requires a Part

135 Certificate.

G Single Purpose Entity (LLC) must have Part 135 Certificate to

receive compensation for charter.

H VedderPrice Report on Prohibited Flight Department.

Operational Control Requires Possessory Interest (through lease

or direct ownership). i(~··:·~~{" ;;...,\ STATE BOARD OF EQUALIZATION \{ ~;

Appeal Name: ~~,; tlu\1 Wh¢~v Case ID: Cf,'5 _ __ ( ITEM#.~

Date: 8/9'3° / 11 Exhibit No: i). ,?, TP TFi1:i\ DEPT PUBLIC COMMENT

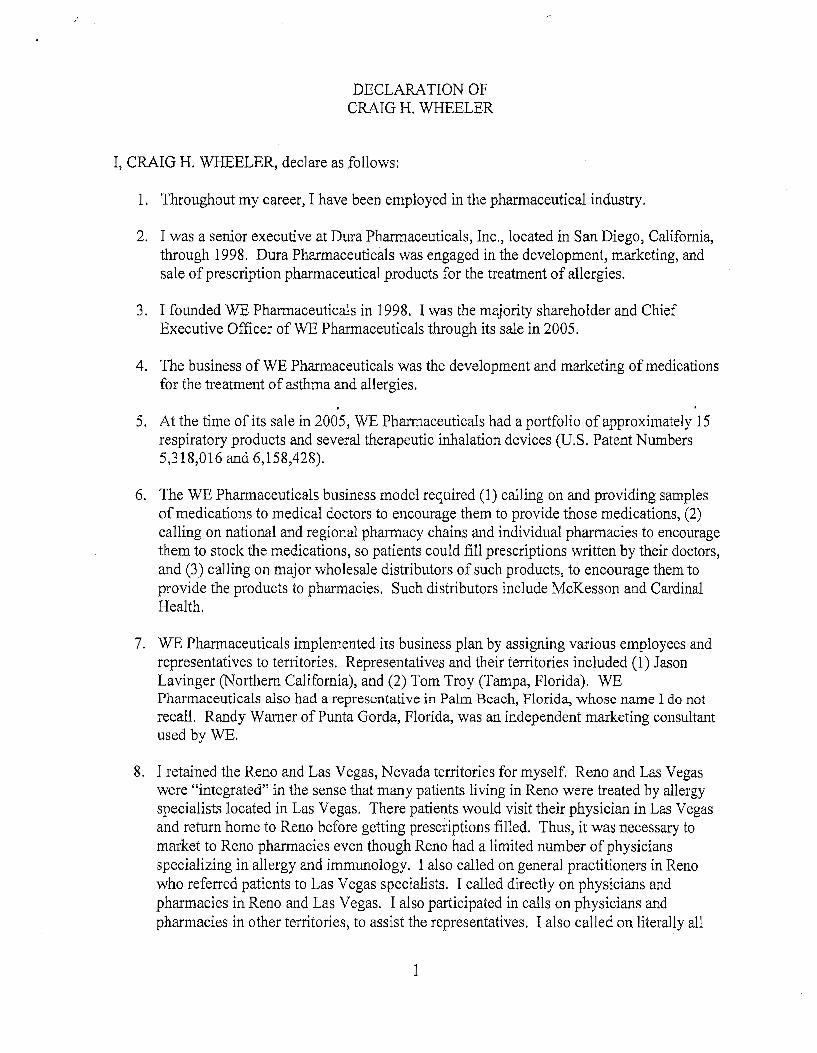

DECLARATION OF CRAIG H. WHEELER

I, CRAIG H. WHEELER, declare as follows:

1. Throughout my career, I have been employed in the pharmaceutical industry.

2. I was a senior executive at Dura Pharmaceuticals, Inc., located in San Diego, California, through 1998. Dura Pharmaceuticals was engaged in the development, marketing, and sale of prescription pharmaceutical products for the treatment of allergies.

3. I founded WE Pharmaceuticals in 1998. I was the majority shareholder and Chief Executive Officer of WE Pharmaceuticals through its sale in 2005.

4. The business of WE Pharmaceuticals was the development and marketing of medications for the treatment of asthma and allergies.

5. At the time of its sale in 2005, WE Pharmaceuticals had a portfolio of approximately 15 respiratory products and several therapeutic inhalation devices (U.S. Patent Numbers 5,318,016 and 6,158,428).

6. The WE Pharmaceuticals business model required (1) calling on and providing samples of medications to medical doctors to encourage them to provide those medications, (2) calling on national and regional pharmacy chains and individual. pharmacies to encourage them to stock the medications, so patients could fill prescriptions written by their doctors, and (3) calling on major wholesale distributors of such products, to encourage them to provide the products to pharmacies. Such distributors include McKesson and Cardinal Health.

7. WE Pharmaceuticals implemented its business plan by assigning various employees and representatives to territories. Representatives and their territories included (1) Jason Lavinger (Northern California), and (2) Tom Troy (Tampa, Florida). WE Pharmaceuticals also had a representative in Palm Beach, Florida, whose name I do not recall. Randy Warner of Punta Gorda, Florida, was an independent marketing consultant used by WE.

8. I retained the Reno and Las Vegas, Nevada territories for myself. Reno and Las Vegas were "integrated" in the sense that many patients living in Reno were treated by allergy specialists located in Las Vegas. There patients would visit their physician in Las Vegas and return home to Reno before getting prescriptions filled. Thus, it was necessary to market to Reno pharmacies even though Reno had a limited number of physicians specializing in allergy and immunology. I also called on general practitioners in Reno who referred patients to Las Vegas specialists. I cal.led directly on physicians and pharmacies in Reno and Las Vegas. I also participated in cal.ls on physicians and pharmacies in other territories, to assist the representatives. I also called on literally all

1

physicians in San Diego specializing in allergy and immunology, including Dr. James P. Kemp, M.D. and Eli 0. Meltzer, M.D.

9. Part of the WE Pharmaceuticals business plan was for me, the Chief Executive Officer of the Company, to make personal sales calls. The presence of the Chief Executive Officer seemed to impress physicians and pharmacy chain executives. This approach was an attempt to compete with similar, but much larger companies, such as Eli Lilly. While Eli Lilly had sales representatives, calling on physicians and pharmacy chain executives, senior management did not do so. Another part of our business plan was to call on physicians and pharmacy representatives on Saturdays, when competing representatives were not working.

10. In 2003, I purchased an airplane to use in my marketing efforts for WE Pharmaceuticals. Title was taken in Sea-Ya Enterprises, LLC, a Delaware limited liability company. I was the sole member.

11. In 2005, the aircraft was managed by Global Executive Aviation, LLC, under an Aircraft Management Agreement.

12. In 2005, Global Executive Aviation arranged for numerous flights by unrelated individuals or companies.

13. Also in 2005, Global Executive Aviation also arranged for at least 13 flights by WE Pharmaceuticals.

14. I was physically present on the aircraft for 11 of these 13 flights.

15. From February 11 through February 15, 2005, the aircraft flew from San Diego, to Colorado, to New Jersey, and back to San Diego. I was not physically present on this flight. WE and Global made the aircraft available for this flight to an outside attorney, who had provided litigation services to WE. WE paid Global for this :flight, and all other flights arranged by Global in 2005.

16. On Wednesday, February 23, 2005, I flew to Reno to call on physicians and pharmacy representatives. The pilots for that flight were Ramon Manriquez and Jim White. ---.

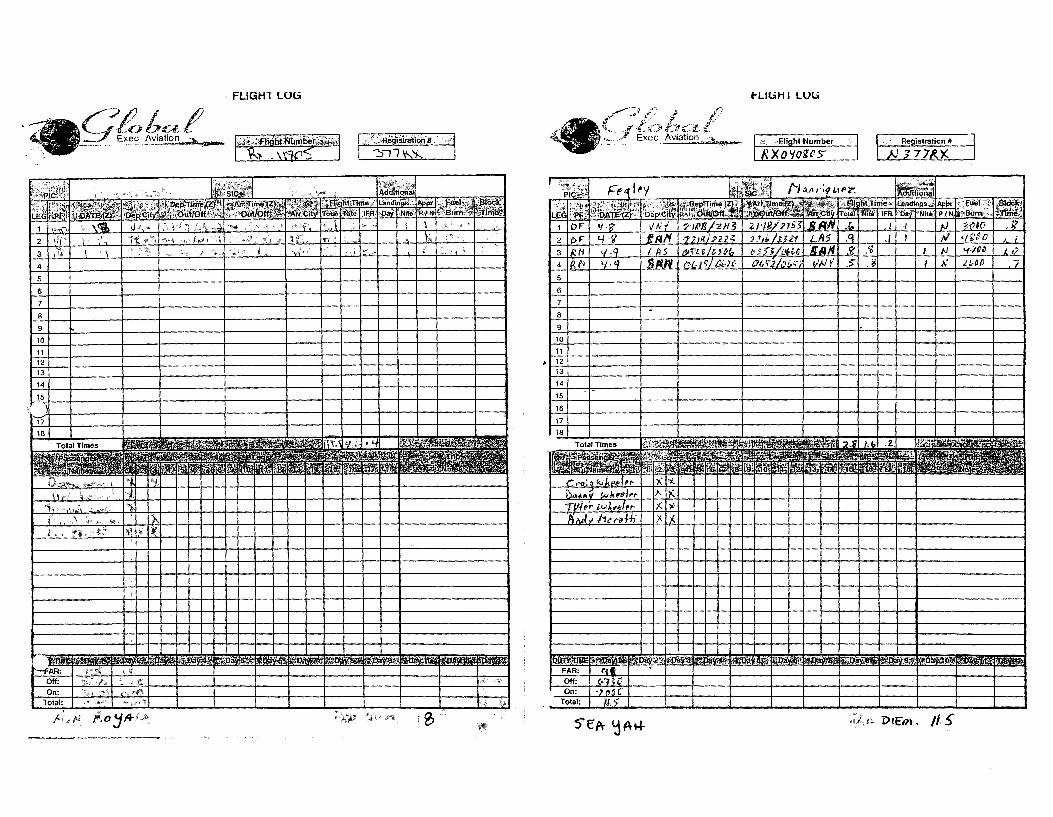

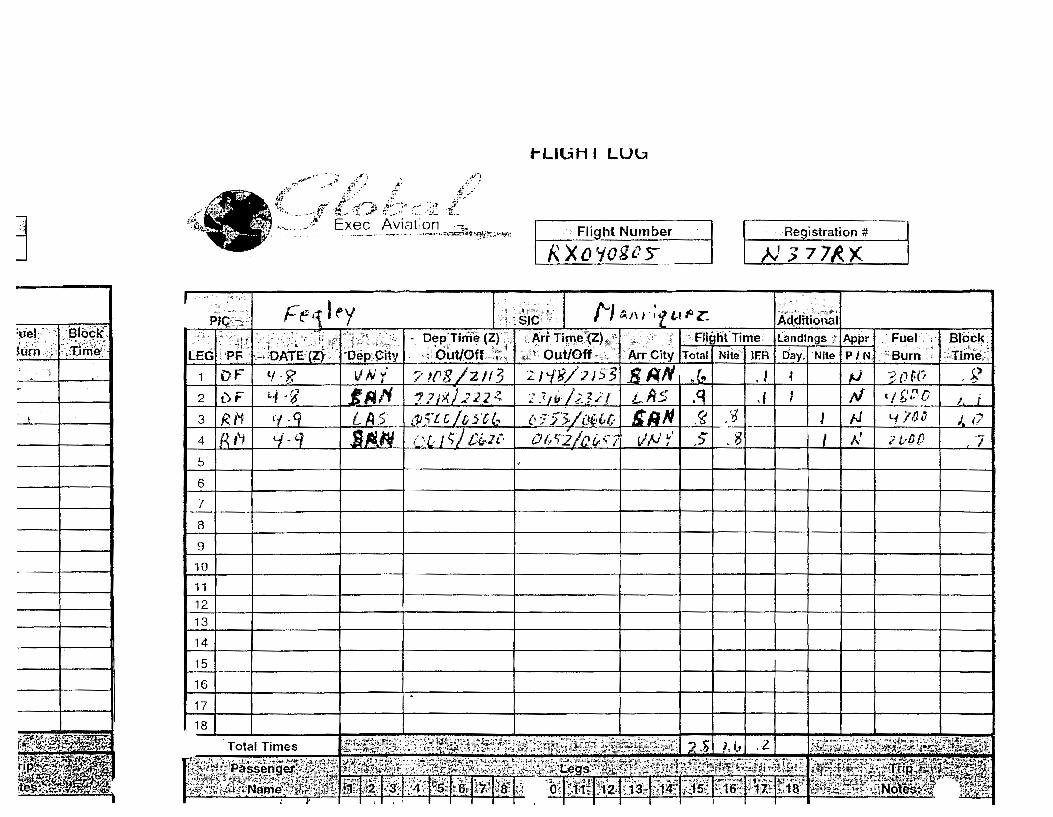

17. On Friday, April 8, 2005, I flew to Las Vegas to meet with Dr. Victor E. Cohen, M.D., Allergy and Asthma Specialist. I discussed WE products with Dr. Cohen and left him samples of products. On Saturday, April 9, I met with a pharmacy representative, and then flew back to San Diego. The pilots for that flight were Ramon Manriquez and Jim White. ~

18. On Tuesday, April 26, 2005, I flew to Las Vegas to meet with Dr. Jim Christensen of Allergy Asthma & Immunology, a Division of Pulmonary Associates, and then on to Reno, to meet with physicians and pharmacy representatives, returning on Friday, April 29. The pilots for that flight were Ramon Manriquez and Jim White.

2

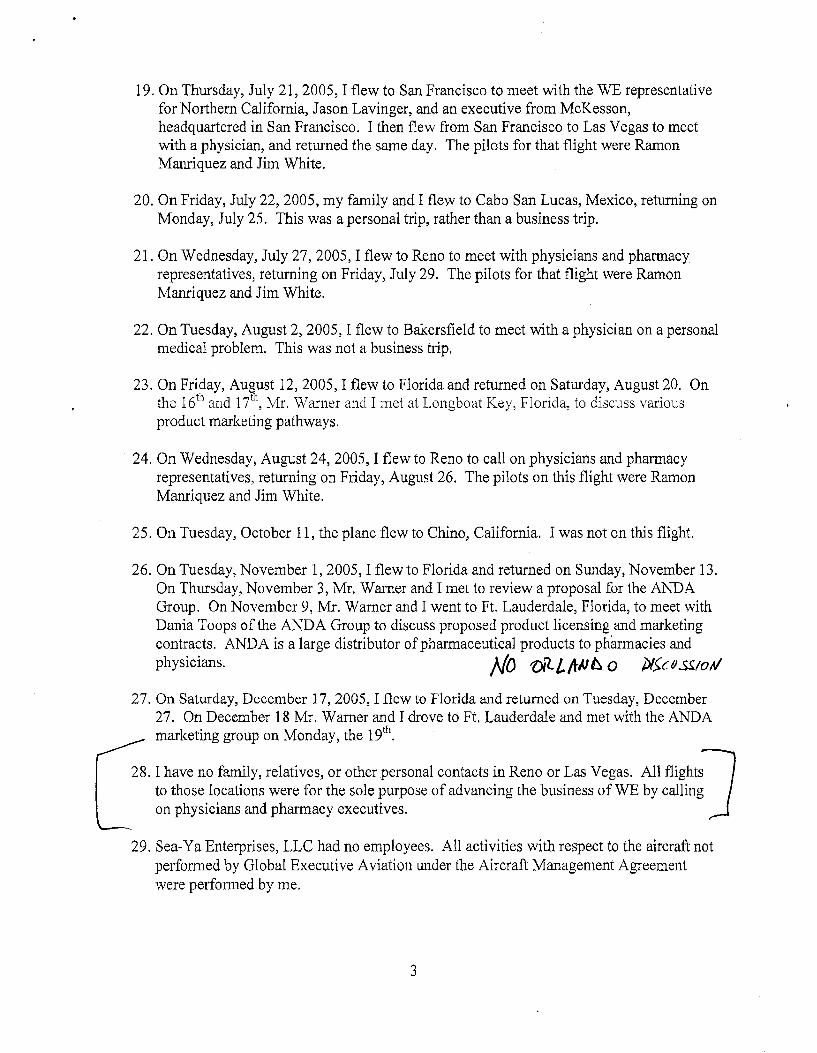

19. On Thursday, July 21, 2005, I flew to San Francisco to meet with the WE representative for Northern California, Jason Lavinger, and an executive from McKesson, headquartered in San Francisco. I then flew from San Francisco to Las Vegas to meet with a physician, and returned the same day. The pilots for that flight were Ramon Manriquez and Jim White.

20. On Friday, July 22, 2005, my family and I flew to Cabe San Lucas, Mexico, returning on Monday, July 25. This was a personal trip, rather than a business trip.

21. On Wednesday, July 27, 2005, I flew to Reno to meet with physicians and pharmacy representatives, returning on Friday, July 29. The pilots for that flight were Ramon Manriquez and Jim White.

22. On Tuesday, August 2, 2005, I flew to Bakersfield to meet with a physician on a personal medical problem. This was not a business trip.

23. On Friday, August 12, 2005, I flew to Florida and returned on Saturday, August 20. On the 16th and 17th

, Mr. Warner and I met at Longboat Key, Florida, to discuss various product marketing pathways.

24. On Wednesday, August 24, 2005, I flew to Reno to call on physicians and pharmacy representatives, returning on Friday, August 26. The pilots on this flight were Ramon Manriquez and Jim White.

25. On Tuesday, October 11, the plane flew to Chino, California. I was not on this flight.

26. On Tuesday, November 1, 2005, I flew to Florida and returned on Sunday, November 13. On Thursday, November 3, Mr. Warner and I met to review a proposal for the ANDA Group. On November 9, Mr. Warner and I went to Ft. Lauderdale, Florida, to meet with Dania Toops of the ANDA Group to discuss proposed product licensing and marketing contracts. ANDA is a large distributor of pharmaceutical products to pharmacies and

physicians. }lo Vt'll/rlJb O µ/~cu.ss..10/tl

27. On Saturday, December 17, 2005, I flew to Florida and returned on Tuesday, December 27. On December 18 Mr. Warner and I drove to Ft. Lauderdale and met with the ANDA marketing group on Monday, the 19th

.

28. I have no family, relatives, or other personal contacts in Reno or Las Vegas. All flights] to those locations were for the sole purpose of advancing the business of WE by calling on physicians and pharmacy executives.

29. Sea-Ya Enterprises, LLC had no employees. All activities with respect to the aircraft not performed by Global Executive Aviation under the Aircraft Management Agreement were performed by me.

3

30, I have reviewed the Statement of Facts in the Protest and believe the facts stated are true and coITect to the best of my knowledge.

I declare the foregoing is true and correct to the best ofmy knowledge,

Dated this .J day of July, 2012.

4

FLIGHT LOG t-Lll>HI LUl:i

/7{) / ..(')

-~;I {if:f~fr!n t,: :- . t'.~sf!i_9\i!i@ii9ii II ..

.(j ~ .. '"~· ~:;i .l~.: .i· .. ;.:.··

( .. ff t' cl') f.:'$ ;:;::.t ( ,. ..ff E~e(;. Aviation _;;t,_.

-Flight Number Registration #

-::,-n 'rs: KXO'f()lC'> ''377/<X

_ _J .i

4 4 IKP I '1 · '"I I .!l/'<lr9 I Ct, P/ '·'"". I V& >,f.11:,'I,;' IL VfV T_J_.-'_l ~, I I t 1 N I 21,00

5 5

6 6

7 7

8 8

9 9

10 10

11

12

13

14 14

1.s 15

16

l!fJ>lly,,, ®!:

½ ,"-),? #,Jt-i,1 ~ -· 5'ef't 4.jA+-l-- n Diem. //.!

t-LluH I LUll

./.,,, .. ... f(·.~:/l~> l;' ,, l" ,i~ . ~ • .

--u,,... i, . ,,1 ,-...... --- Ex~~-A~,~~~9~ ..•. ~t-.-.... -~;_,~..,, w .~J. Flight Number Reqistration #

RX O '10g CS ';77P.,X_

~

!:.- '. ,_-i31o~1( n:./ :'::ii'rllii.

Pie,:-:

·. ~~~ t LEGl:·pf> -----OF -

Fe•{ I ey I • "- r ,~-··· -t

i. S_IC ('J tJ.. IH. ; i_ l,.1 f-' Z: ic1c1ttionai ,·: - -:- --71: < I . :: . -:, 1 · Pep"Time (Z) - Arr Time'(Z) Landings. Appr _·Fuel. :·l Block_

,_::.;'..bir'ii,-{z(10 Dep,~i!v· _ ·fQut/Off .. ( , Out/Off- - [)ay Nite P, N - Burn : 1--Tirrie;; t/·?~ I YNr· I 2JPR/z113 I 21':f~/:ns:&,BA'NI .t~I I .11 ~ I l>J [3__0~Q I .!?

2 I i)F

~ 'i ...... , 1.1·'i 1i:,-.!'I -12><'.2222,, 2.7 ..u-t:~.u LA5 ,q ., 1 ;v (1 i;.~o ,_

l/ -q LA .S tP;.TJ,_LJ_& :i·c & J,~:fj,/~1~·{,C- If }if . '!5 J /J '"f /,0 J J. c if-<-] i.s11.~lc&,1r;/1 .. "'i-it-[Q~ii1~'l_(f~·A vNr'I SI .81 I I 111./ I 21.,-Do L __ ,L

5 -6

7 -8 -9 -10 -11 -12 -13 -14 -15

16

17

18

Total Times

1~1~;.m~t1~Ji~~i~1111'.

j

=_u'etur

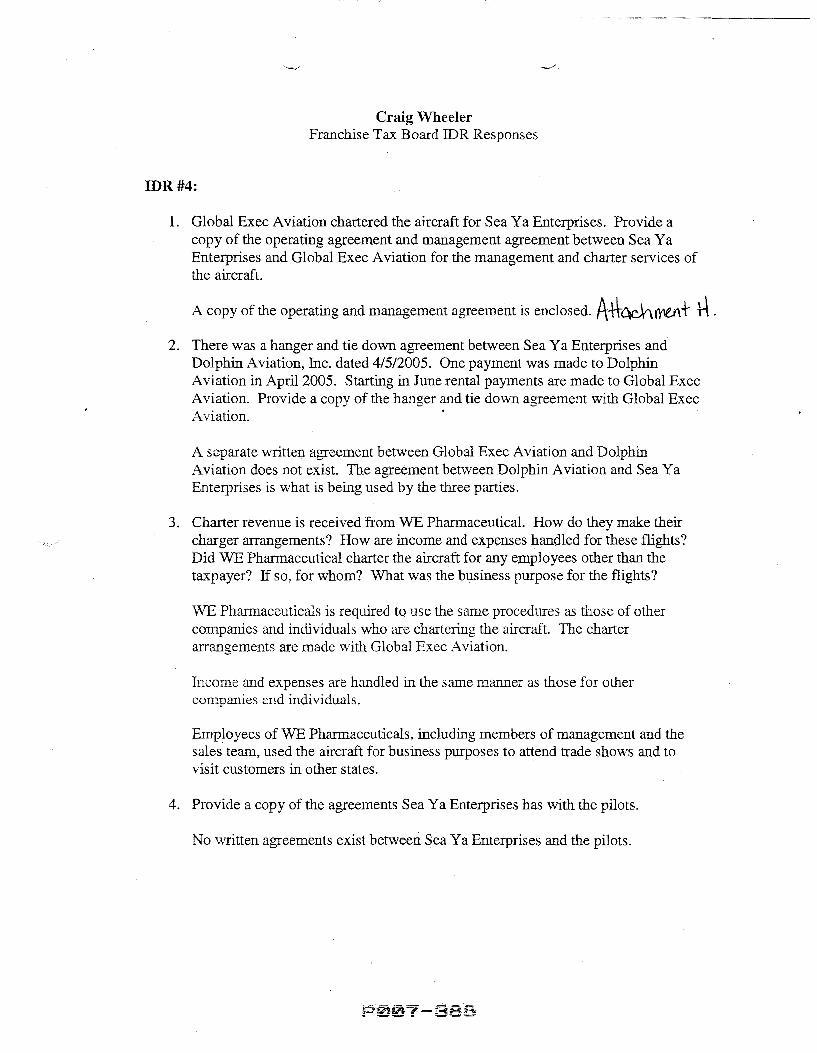

Craig Wheeler Franchise Tax Board IDR Responses

IDR#4:

I. Global Exec Aviation chartered the aircraft for Sea Ya Enterprises. Provide a copy of the operating agreement and management agreement between Sea Ya Enterprises and Global Exec Aviation for the management and charter services of the aircraft.

A copy of the operating and management agreement is enclosed. A+\-~i'Y'lfl+ H . 2. There was a hanger and tie down agreement between Sea Ya Enterprises and

Dolphin Aviation, fuc. dated 4/5/2005. One payment was made to Dolphin Aviation in April 2005. Starting in June rental payments are made to Global Exec Aviation. Provide a copy of the hanger and tie down agreement with Global Exec Aviation.

A separate written agreement between Global Exec Aviation and Dolphin Aviation does not exist The agreement between Dolphin Aviation and Sea Ya Enterprises is what is being used by the three parties.

3. Charter revenue is received from WE Pharmaceutical. How do they make their charger arrangements? How are income and expenses handled for these flights? Did WE Pharmaceutical charter the aircraft for any employees other than the taxpayer? If so, for whom? What was the business purpose for the flights?

WE Pharmaceuticals is required to use the same procedures as those of other companies and individuals who are chartering the aircraft. The charter arrangements are made with Global Exec Aviation.

Income and expenses are handled in the same manner as those for other companies and individuals.

Employees of WE Pharmaceuticals, including members of management and the sales team, used the aircraft for business purposes to attend trade shows and to visit customers in other states.

4. Provide a copy of the agreements Sea Ya Enterprises has with the pilots.

No vvritten agreements exist between Sea Ya Enterprises and the pilots.

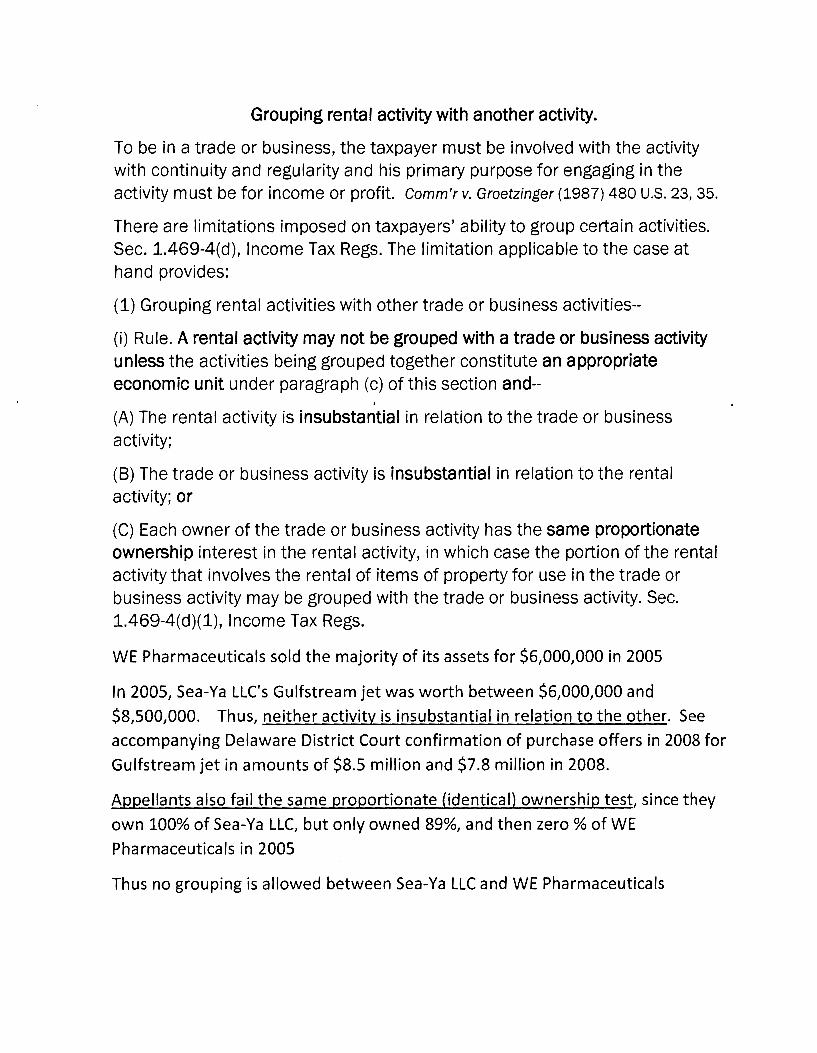

Grouping rental activity with another activity.

To be in a trade or business, the taxpayer must be involved with the activity with continuity and regularity and his primary purpose for engaging in the activity must be for income or profit. Comm'r v. Groetzinger (1987) 480 U.S. 23, 35.

There are limitations imposed on taxpayers' ability to group certain activities. Sec. 1.469-4(d), Income Tax Regs. The limitation applicable to the case at hand provides:

(1) Grouping rental activities with other trade or business activities--

(i) Rule. A rental activity may not be grouped with a trade or business activity unless the activities being grouped together constitute an appropriate economic unit under paragraph (c) of this section and--

(A) The rental activity is insubstantial in relation to the trade or business activity;

(B) The trade or business activity is insubstantial in relation to the rental activity; or

(C) Each owner of the trade or business activity has the same proportionate ownership interest in the rental activity, in which case the portion of the rental activity that involves the rental of items of property for use in the trade or business activity may be grouped with the trade or business activity. Sec. 1.469-4(d)(1), Income Tax Regs.

WE Pharmaceuticals sold the majority of its assets for $6,000,000 in 2005

In 2005, Sea-Ya LLC's Gulfstream jet was worth between $6,000,000 and

$8,500,000. Thus, neither activity is insubstantial in relation to the other. See

accompanying Delaware District Court confirmation of purchase offers in 2008 for

Gulfstream jet in amounts of $8.5 million and $7.8 million in 2008.

Appellants also fail the same proportionate (identical) ownership test, since they

own 100% of Sea-Ya LLC, but only owned 89%, and then zero% of WE

Pharmaceuticals in 2005

Thus no grouping is allowed between Sea-Ya LLC and WE Pharmaceuticals

IN THE UNITED ST ATES DISTRICT COURT FOR THE DISTRICT OF DELAWARE

BANK OF AMERICA, N.A.,

Plaintiff,

v.

SEA-YA ENTERPRISES, LLC, CRAIG H. WHEELER, and DANI D. WHEELER,

Defendant.

C.A. 11-445-RGA

MEMORANDUM OPINION

David B. Stratton, Esq., Wilmington, Delaware; James G. McMillan, Esq., Wilmington, Delaware; James H.S. Levine, Esq., Wilmington, Delaware; Attorneys for Plaintiff Bank of America N.A.

Kevin S. Mann, Esq., Wilmington, Delaware; Dennis R. Haber, Esq., Miami, Florida; Attorneys for Defendants Sea-Ya Enterprises, LLC, Craig H. Wheeler, and Dani D. Wheeler

July3, 2012

Wilmington, Delaware

1

��

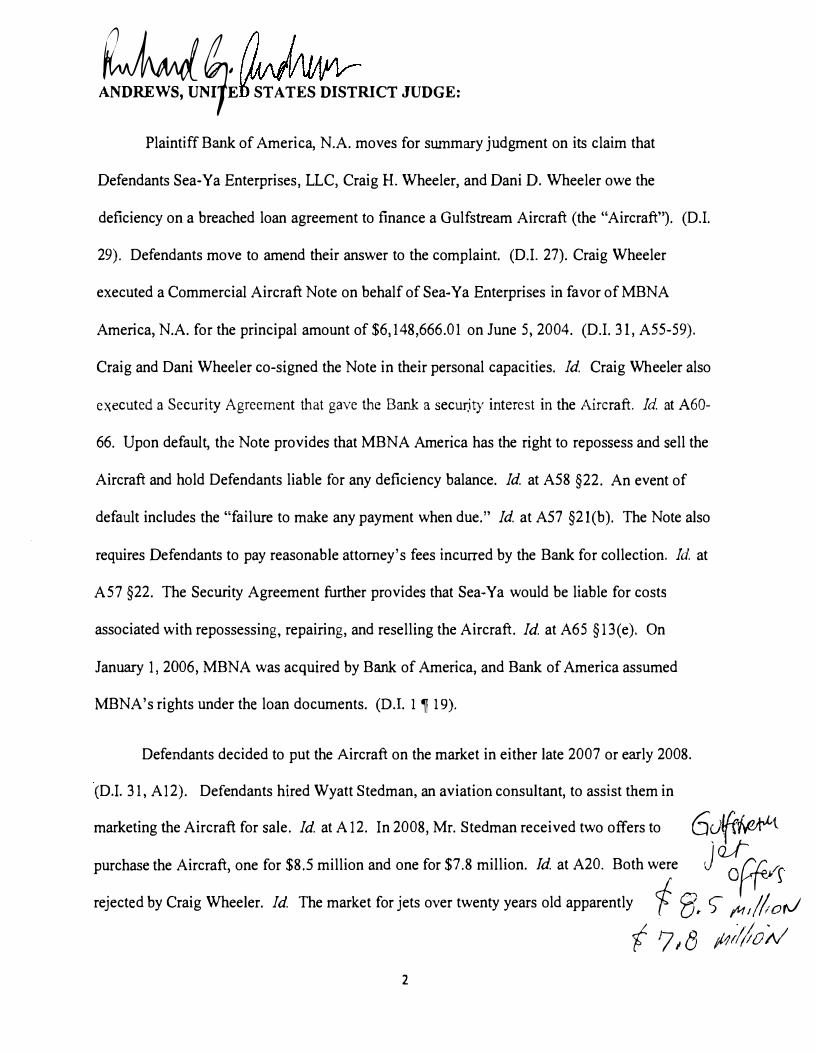

� STATES DISTRICT JUDGE:

Plaintiff Bank of America, N.A. moves for swnmary judgment on its claim that

Defendants Sea-Ya Enterprises, LLC, Craig H. Wheeler, and Dani D. Wheeler owe the

deficiency on a breached loan agreement to finance a Gulfstream Aircraft (the "Aircraft"). (DJ.

29). Defendants move to amend their answer to the complaint. (DJ. 27). Craig Wheeler

executed a Commercial Aircraft Note on behalf of Sea-Ya Enterprises in favor of MBNA

America, N.A. for the principal amount of $6,148,666.01 on June 5, 2004. (DJ. 31, A55-59).

Craig and Dani Wheeler co-signed the Note in their personal capacities. Id. Craig Wheeler also

executed a Security Agreement that gave the Blliik a securjty interest in the Aircraft. Id at A60-

66. Upon default, the Note provides that MBNA America has the rightto repossess and sell the

Aircraft and hold Defendants liable for any deficiency balance. Id. at A58 §22. An event of

default includes the "failure to make any payment when due." Id. at A57 §2l(b). The Note also

requires Defendants to pay reasonable attorney's fees incurred by the Bank for collection. Id. at

A57 §22. The Security Agreement further provides that Sea-Ya would be liable for costs

associated with repossessing, repairing, and reselling the Aircraft. Id. at A65 §13(e). On

January 1, 2006, MBNA was acquired by Bank of America, and Bank of America assumed

MBNA's rights under the loan documents. (DJ. 1 i 19).

Defendants decided to put the Aircraft on the market in either late 2007 or early 2008.

(D.I. 31, A 12). Defendants hired Wyatt Stedman, an aviation consultant, to assist them in

marketing the Aircraft for sale. Id. at A 12. In 2008, Mr. Stedman received two offers t

purchase the Aircraft, one for $8.5 million and one for $7.8 million. Id. at A20. Both were

rejected by Craig Wheeler. Id. The market for jets over twenty years old apparently

2

6ulfr(ve,rlt ,J:t

J offv"\ 1 ca .. ) f"u//rorJ

f 17,8 ;1Jrli)oAI

o

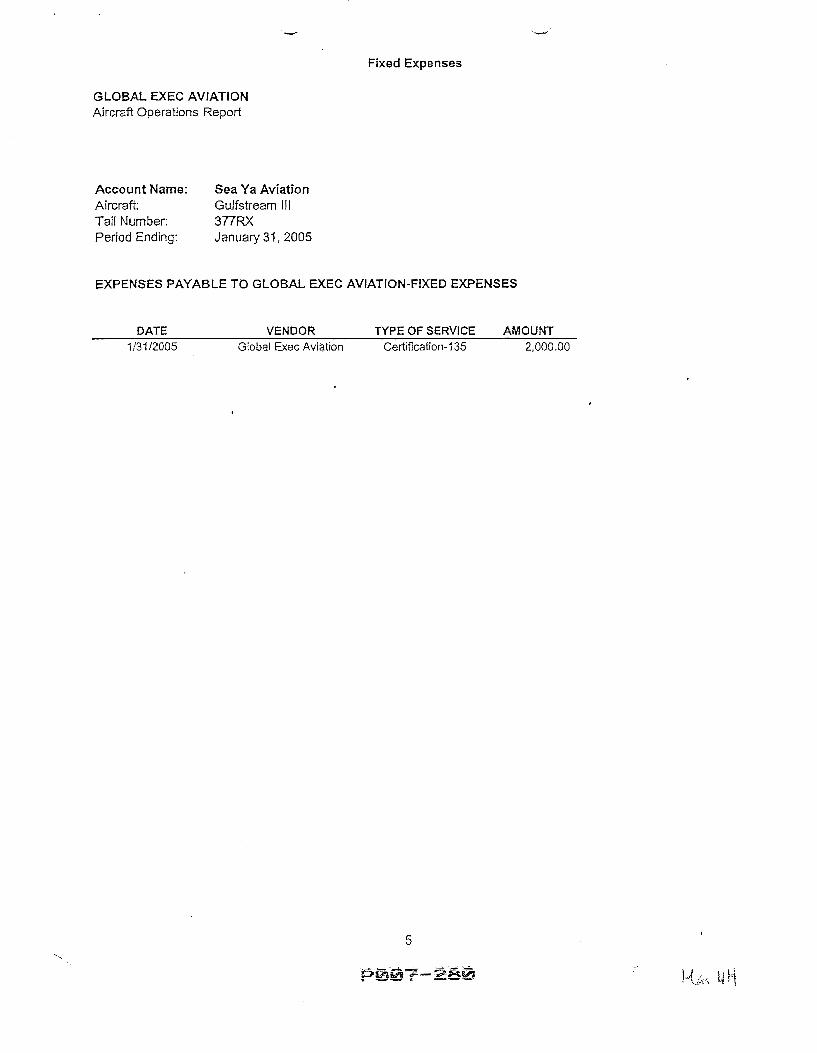

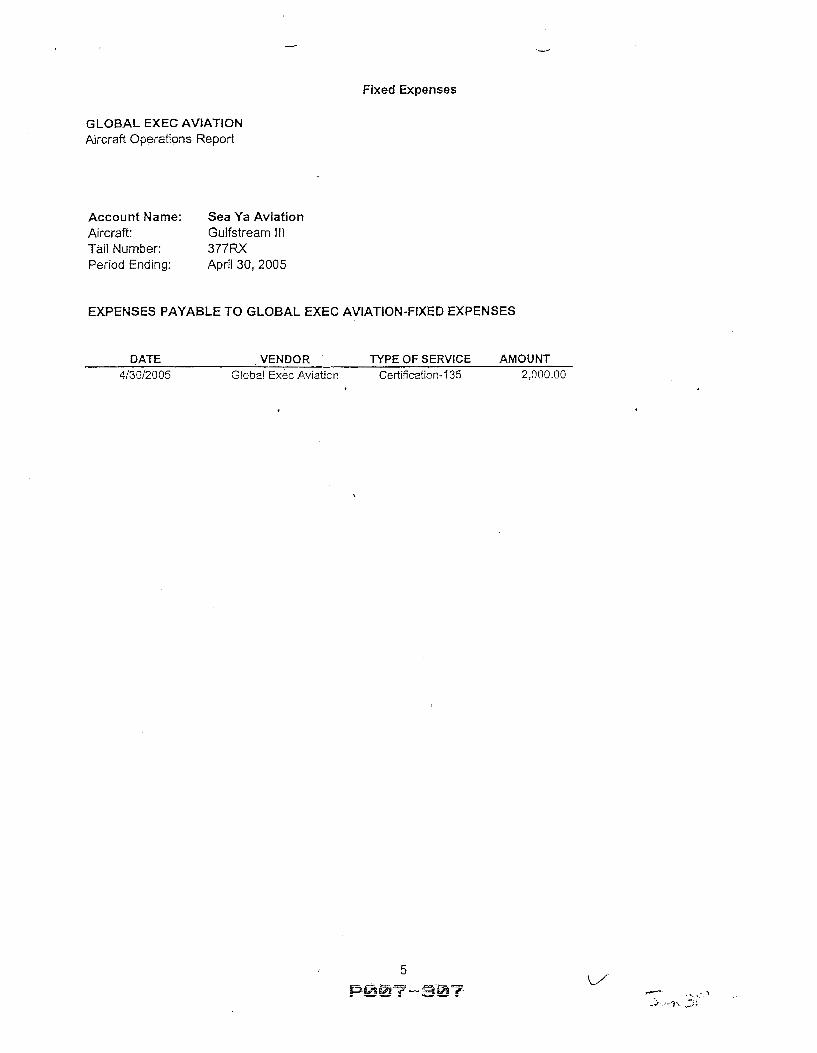

Fixed Expenses

GLOBAL EXEC AVIATION Aircraft Operations Report

Account Name: Sea Ya Aviation Aircraft: Gulfstream Ill Tail Number: 377RX Period Ending: January 31, 2005

EXPENSES PAYABLE TO GLOBAL EXEC AVIATION-FIXED EXPENSES

DATE VENDOR TYPE OF SERVICE AMOUNT 1/31/2005 Global Exec Aviation Certification-135 2,000.00

5

Fixed Expenses

5 V

GLOBAL EXEC AVIATION Aircraft Operations Report

Account Name: Sea Ya Aviation Aircraft: Gulfstream Ill Tail Number: 377RX Period Ending: April 30, 2005

EXPENSES PAYABLE TO GLOBAL EXEC AVIATION-FIXED EXPENSES

DATE VENDOR TYPE OF SERVICE AMOUNT

4/30/2005 Globa! Exec Aviation Certification-135 2,000.00

Fixed Expenses

. ___ .,

• . .);:

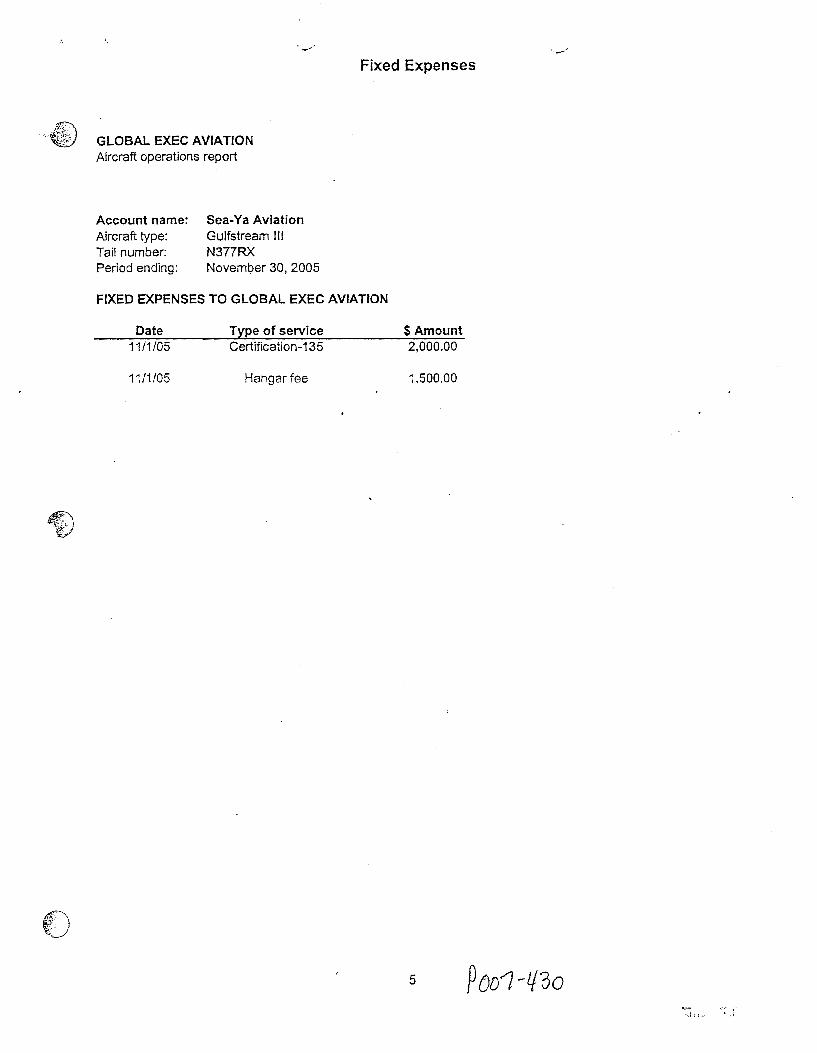

GLOBAL EXEC AVIATION Aircraft operations report

Account name: Sea-Ya Aviation Aircraft type: Gulfstream Ill Tail number: N377RX Period ending: November 30, 2005

FIXED EXPENSES TO GLOBAL EXEC AVIATION

Date Type of service $ Amount 11/1/05 Certification-135 2,000.00

11/1/05 Hangar fee 1,500.00

C\.) ~k j

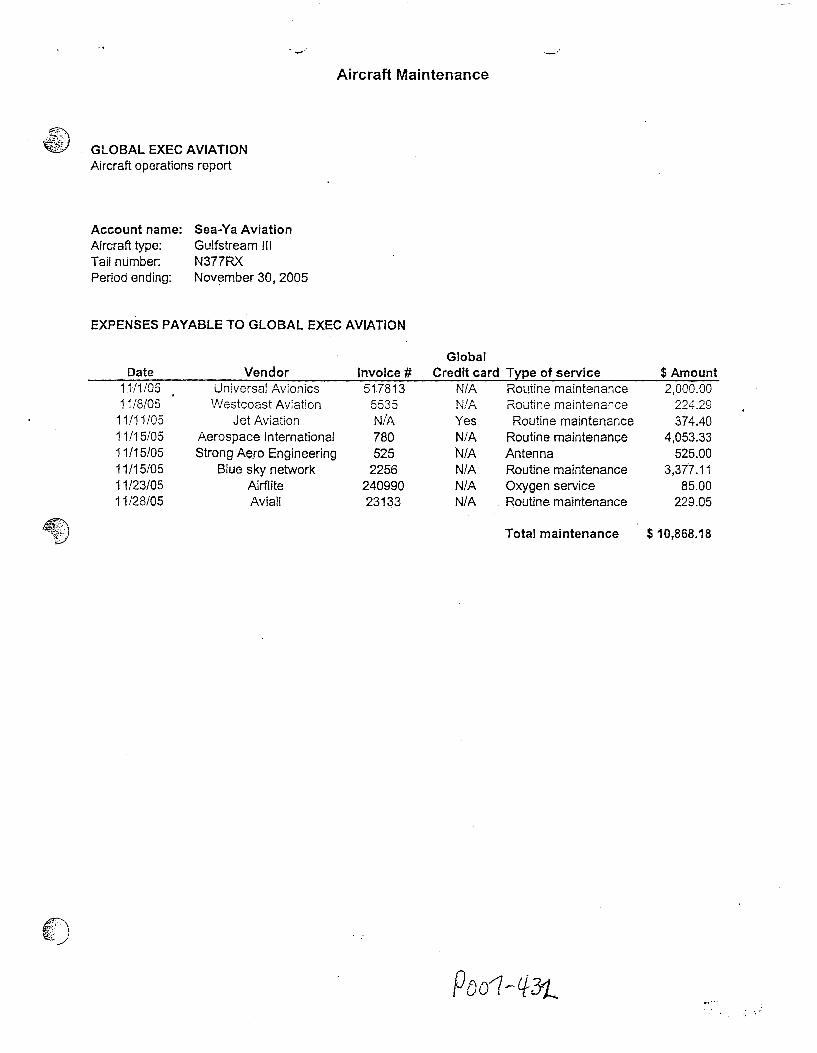

Aircraft Maintenance

GLOBAL EXEC AVIATION Aircraft operations report

Account name: Sea-Ya Aviation Aircraft type: Gulfstream Ill Tail number: N377RX Period ending: November 30, 2005

EXPENSES PAYABLE TO GLOBAL EXEC AVIATION

Global Date Vendor Invoice# Credit card· Type of service $ Amount

11/1/05 Universal Avionics 517813 N/A Routine maintenance 2,000.00 11/8/05 Westcoast Aviation 5535 N/A Routine maintenance 224.29

11/11/05 Jet Aviation NiA Yes Routine maintsnance 374.40 11/15/05 Aerospace International 780 NIA Routine maintenance 4,053.33 11/15/05 Strong Aero Engineering 525 N/A Antenna 525.00 i 1/15/05 Blue sky network 2256 NIA Routine maintenance 3,377.11 11/23/05 Airflite 240990 N/A Oxygen service 85.00 11/28/05 Aviall 23133 NIA . Routine maintenance 229.05

Total maintenance $10,868.18

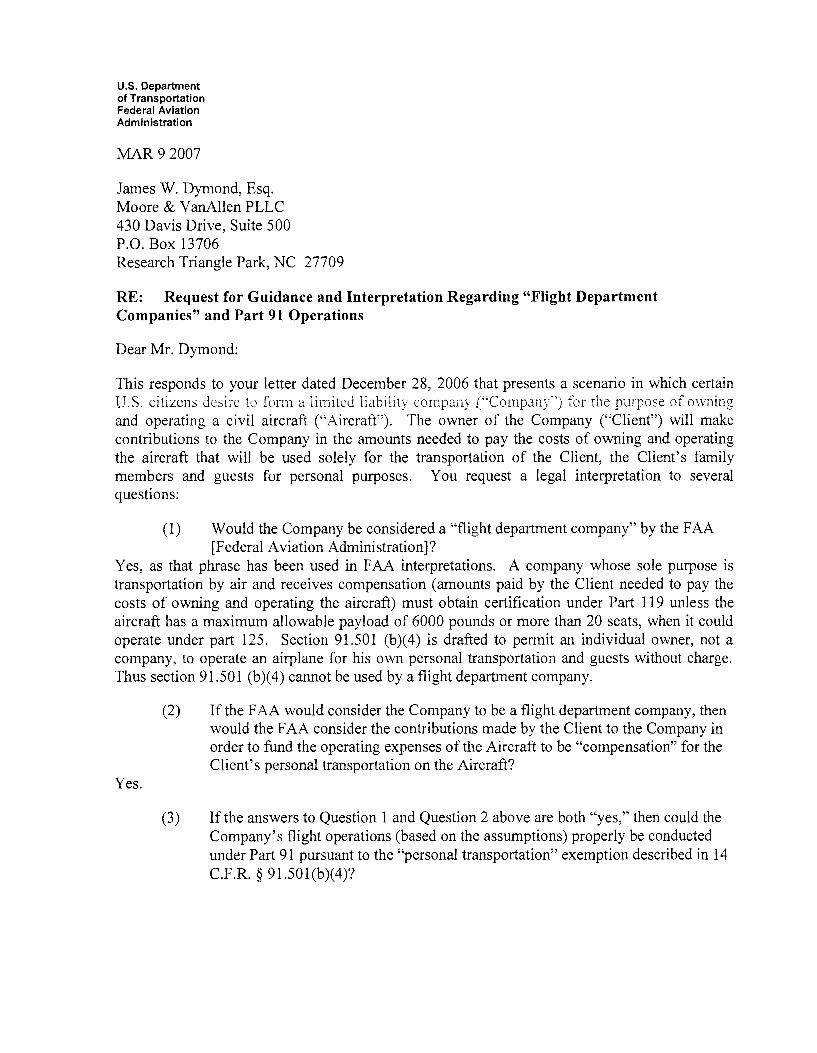

U.S. Department of Transportation Federal Aviation Administration

MAR92007

James W. Dymond, Esq. Moore & VanAllen PLLC 430 Davis Drive, Suite 500 P.O. Box 13706 Research Triangle Park, NC 27709

RE: Request for Guidance and Interpretation Regarding "Flight Department Companies" and Part 91 Operations

Dear Mr. Dymond:

This responds to your letter dated December 28, 2006 that presents a scenario in which certain U.S. citizens desire to form a limited liability company ("Company'") for the purpose of o\vning and operating a civil aircraft ('"Aircraft"). The owner of the Company ("Client") will make contributions to the Company in the amounts needed to pay the costs of owning and operating the aircraft that will be used solely for the transportation of the Client, the Client's family members and guests for personal purposes. You request a legal interpretation to several questions:

( 1) Would the Company be considered a "flight department company" by the FAA [Federal Aviation Administration]?

Yes, as that phrase has been used in FAA interpretations. A company whose sole purpose is transportation by air and receives compensation (amounts paid by the Client needed to pay the costs of owning and operating the aircraft) must obtain certification under Part 119 unless the aircraft has a maximum allowable payload of 6000 pounds or more than 20 seats, when it could operate under part 125. Section 91.501 (b)(4) is drafted to permit an individual owner, not a company, to operate an airplane for his own personal transportation and guests without charge. Thus section 91.501 (b)(4) cannot be used by a flight department company.

(2) If the FAA would consider the Company to be a flight department company, then would the FAA consider the contributions made by the Client to the Company in order to fund the operating expenses of the Aircraft to be "compensation" for the Client's personal transportation on the Aircraft?

Yes.

(3) If the answers to Question 1 and Question 2 above are both "yes," then could the Company's flight operations (based on the assumptions) properly be conducted under Part 91 pursuant to the "personal transportation" exemption described in 14 C.F.R. § 91.501(b)(4)?

2

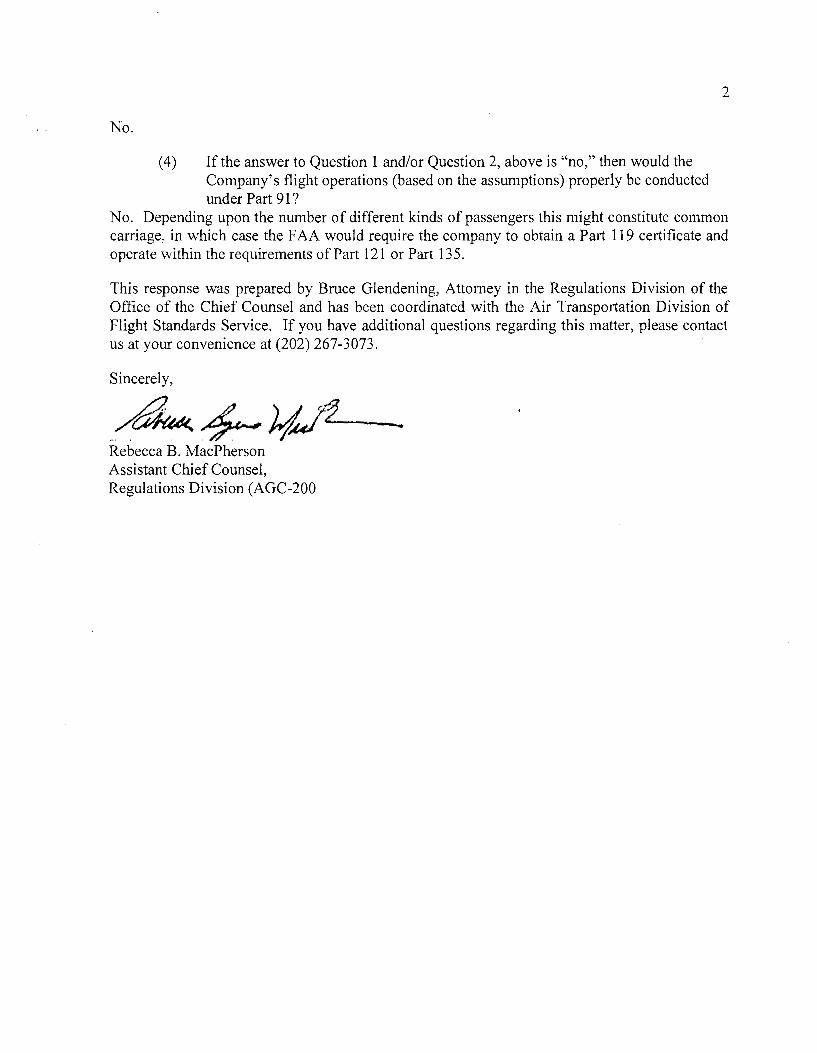

No.

(4) If the answer to Question 1 and/or Question 2, above is "no," then would the Company's flight operations (based on the assumptions) properly be conducted under Part 91?

No. Depending upon the number of different kinds of passengers this might constitute common carriage, in which case the FAA would require the company to obtain a Part 119 certificate and operate within the requirements of Part 121 or Part 135.

This response was prepared by Bruce Glendening, Attorney in the Regulations Division of the Office of the Chief Counsel and has been coordinated with the Air Transportation Division of Flight Standards Service. If you have additional questions regarding this matter, please contact us at your convenience at (202) 267-3073.

Sincerely,

-~4-1/fl-Rebecca B. MacPherson Assistant Chief Counsel, Regulations Division (AGC-200

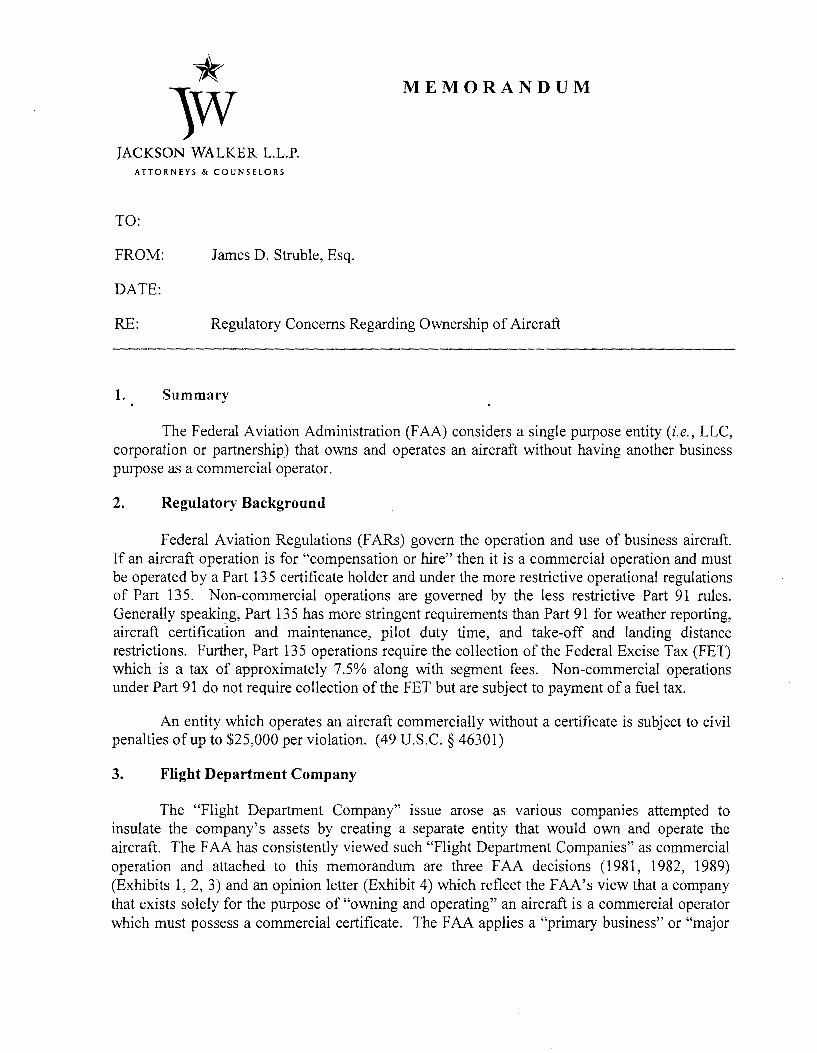

* )W JACKSON WALKER L.L.P.

ATTORNEYS & COUNSELORS

MEMORANDUM

TO:

FROM: James D. Struble, Esq.

DATE:

RE: Regulatory Concerns Regarding Ownership of Aircraft

1. Summary

The Federal Aviation Administration (FAA) considers a single purpose entity (i.e., LLC, corporation or partnership) that owns and operates an aircraft without having another business purpose as a commercial operator.

2. Regulatory Background

Federal Aviation Regulations (F ARs) govern the operation and use of business aircraft. If an aircraft operation is for "compensation or hire" then it is a commercial operation and must be operated by a Part 135 certificate holder and under the more restrictive operational regulations of Part 135. Non-commercial operations are governed by the less restrictive Part 91 rules. Generally speaking, Part 135 has more stringent requirements than Part 91 for weather reporting, aircraft certification and maintenance, pilot duty time, and take-off and landing distance restrictions. Further, Part 135 operations require the collection of the Federal Excise Tax (FET) which is a tax of approximately 7.5% along with segment fees. Non-commercial operations under Part 91 do not require collection of the FET but are subject to payment of a fuel tax.

An entity which operates an aircraft commercially without a certificate is subject to civil penalties of up to $25,000 per violation. (49 U.S.C. § 46301)

3. Flight Department Company

The "Flight Department Company" issue arose as various companies attempted to insulate the company's assets by creating a separate entity that would own and operate the aircraft. The FAA has consistently viewed such "Flight Department Companies" as commercial operation and attached to this memorandum are three FAA decisions (1981, 1982, 1989) (Exhibits 1, 2, 3) and an opinion letter (Exhibit 4) which reflect the FAA's view that a company that exists solely for the purpose of "owning and operating" an aircraft is a commercial operator which must possess a commercial certificate. The FAA applies a "primary business" or "major

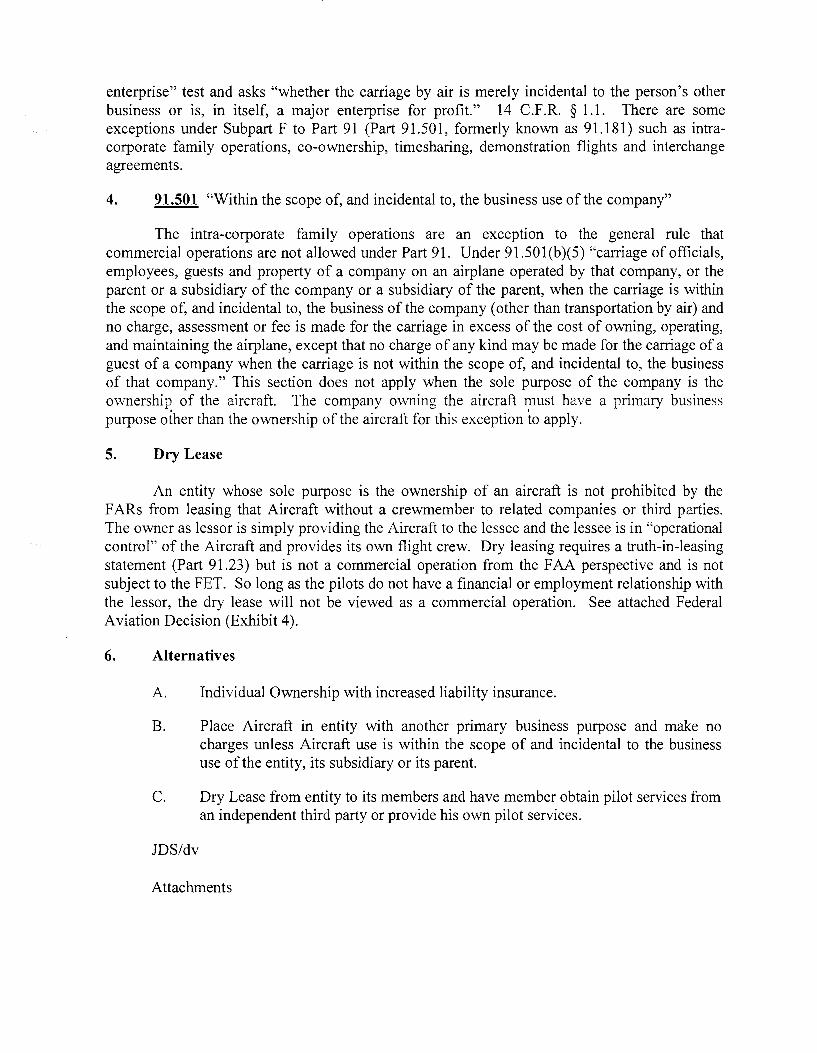

enterprise" test and asks "whether the carriage by air is merely incidental to the person's other business or is, in itself, a major enterprise for profit." 14 C.F.R. § 1.1. There are some exceptions under Subpart F to Part 91 (Part 91.501, formerly known as 91.181) such as intracorporate family operations, co-ownership, timesharing, demonstration flights and interchange agreements.

4. 91.501 "Within the scope of, and incidental to, the business use of the company"

The intra-corporate family operations are an exception to the general rule that commercial operations are not allowed under Part 91. Under 91.501(b)(5) "carriage of officials, employees, guests and property of a company on an airplane operated by that company, or the parent or a subsidiary of the company or a subsidiary of the parent, when the carriage is within the scope of, and incidental to, the business of the company ( other than transportation by air) and no charge, assessment or fee is made for the carriage in excess of the cost of owning, operating, and maintaining the airplane, except that no charge of any kind may be made for the carriage of a guest of a company when the carriage is not within the scope of, and incidental to, the business of that company." This section does not apply when the sole purpose of the company is the ownership of the aircraft. The company owning the aircraft must have a primary business purpose other than the ownership of the aircraft for this exception to apply.

5. Dry Lease

An entity whose sole purpose is the ownership of an aircraft is not prohibited by the F ARs from leasing that Aircraft without a crewmember to related companies or third parties. The owner as lessor is simply providing the Aircraft to the lessee and the lessee is in "operational control" of the Aircraft and provides its own flight crew. Dry leasing requires a truth-in-leasing statement (Part 91.23) but is not a commercial operation from the FAA perspective and is not subject to the FET. So long as the pilots do not have a financial or employment relationship with the lessor, the dry lease will not be viewed as a commercial operation. See attached Federal Aviation Decision (Exhibit 4).

6. Alternatives

A. Individual Ownership with increased liability insurance.

B. Place Aircraft in entity with another primary business purpose and make no charges unless Aircraft use is within the scope of and incidental to the business use of the entity, its subsidiary or its parent.

C. Dry Lease from entity to its members and have member obtain pilot services from an independent third party or provide his own pilot services.

JDS/dv

Attachments

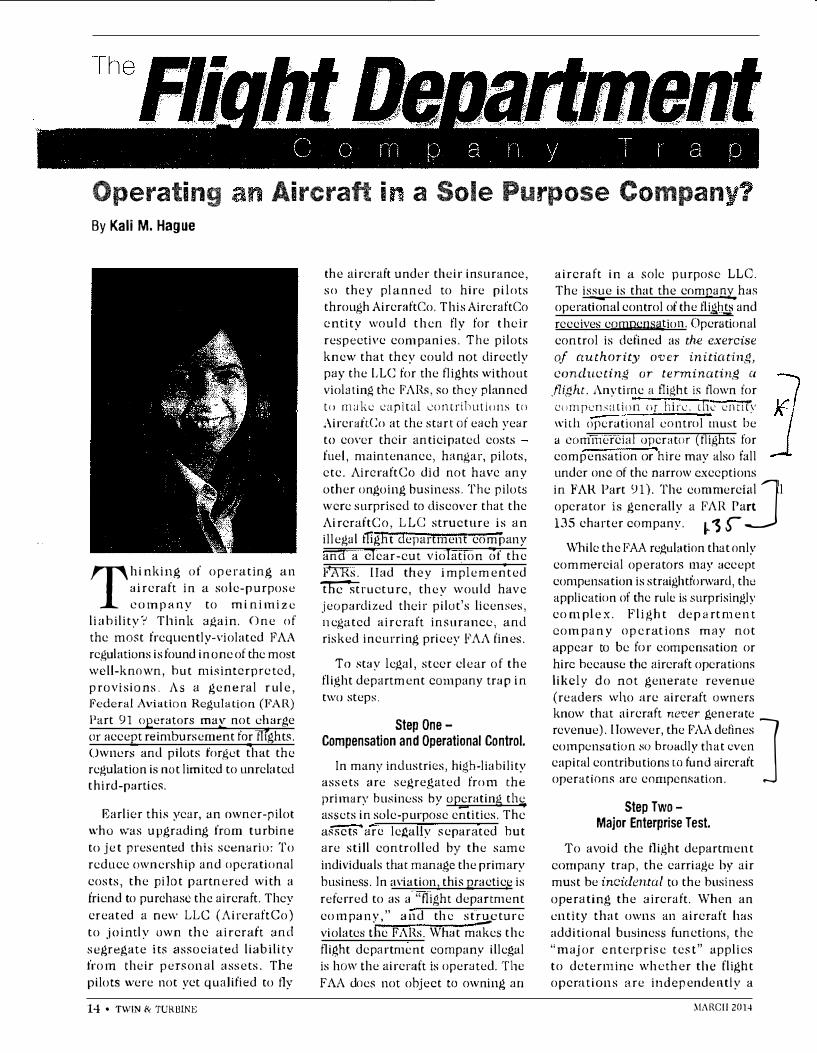

Operating Aircraft i a Sole Purpose Compan Ill

By Kali M. Hague

Thinking of operating an aircraft in a sole-purpose

.company to mi nimize liahility':' Think again. One of the most frequently-violated FAA regulations is found in one of the most well-known, hut misinterpreted, provLsions. As a general r ule, Federal Aviation Regulation (I?AR) Part 91 operators may not charge or accept reimbursement for tl(ghts. Owners an<l pilots forget that the regulation is not limited to unrelated third-parties.

Earlier this year, an owner-pilot who was upgrading from turbine to jet presented this scenario: To reduce ownership and operational costs, the pilot partnered with a friend to purchase the aircraft. They created a new LLC (AircraftCo) to jointly own the aircraft and segregate its associated liability from their personal assets. The pilots were not yet qualified to fly

the aircraft under their insurance, so they planned to hire pilots through AircraftCo. This AireraftCo entity would then fly for their respective companies. The pilots knew that they could not directly pay the LLC for the flights without viol:.Jting the r'ARs, so they planned to make t.:apital t.:ontril)Utions to ,--\ircraftCo at the st.ire of each year to cover their anticipated costs fuel, maintenance, hangar, pilots, etc. AircraftCo did not have any other ongoing business. The pilots were surprised to discover that the AircraftCo, LLC structure is an illegal flight department company and a clear-cut v iolation 6f the h\Ks. liad

J t they implemented

�<:;tructurc, they would have jeopardized their pilot's licenses, negated aircraft insurance, and risked incurring pricey FAA fines.

To stay legal, steer clear of the fli,i=:ht department company trap in two steps.

Step OneCompensation and Operational Control.

In many industries, high-liability assets are segre,11,ated from the primary business by operating th� assets in sole-purpose eii"tities. The assets 'arc legally separated hut are still controlled by the same individuals that mana,ge the primary business. Jn aviation, this practic,e is referred to as a "t1ight department company," and the st!:.l\.eturc violates tfic FARs. What makes the flight department company ille,gal is how the aircraft is operated. The FAA does not object to owning an

aircraft in a sole purpose LLO. The i8..::.!:1e is that the comparu:.. has operational control of the tligh� and receives compcnsi.!Jion. Operational control is defined as the exercise of authority o'Ver initiatin,g, concluctin,g or terminatin,g a jli,[Jht. Anytime a fli,ght is flown tor compcn:,ation or hir-:. lbL' c:nt'it\ with operational control must be a commercial operator (flights for compensation or hire may also fall under one of the narrow exceptions in FAR Part 91). The eommerci ,toperator is generally a FAR Part :J135 charter company. �'Sr

While the FAA regulation that only commercial operators may accept compensation is straightforward, the application of the rule is surprisingly complex. Flight department company operations may not appear to be for compensation or hire hecausc the aircraft operations likely do not generate revenue (readers who are aircraft owners know that aircraft ne<t•er generate revenue). !Iowever, the FAA defines compensation so broadly that c.:ven J capital contributions to fun� aircraft

.operatwns are compcm:at10n.

Step TwoMajor Enterprise Test.

To avoid the flight department company trap, the carriage by air must be incidental to the business operating the aircraft. When an entity that owns an aircraft !ms additional business functions, the "major enterprise test" applies to determine whether the flight operations are independently a

14 • TWlN & TURl3lNE �!ARCH 2014

l

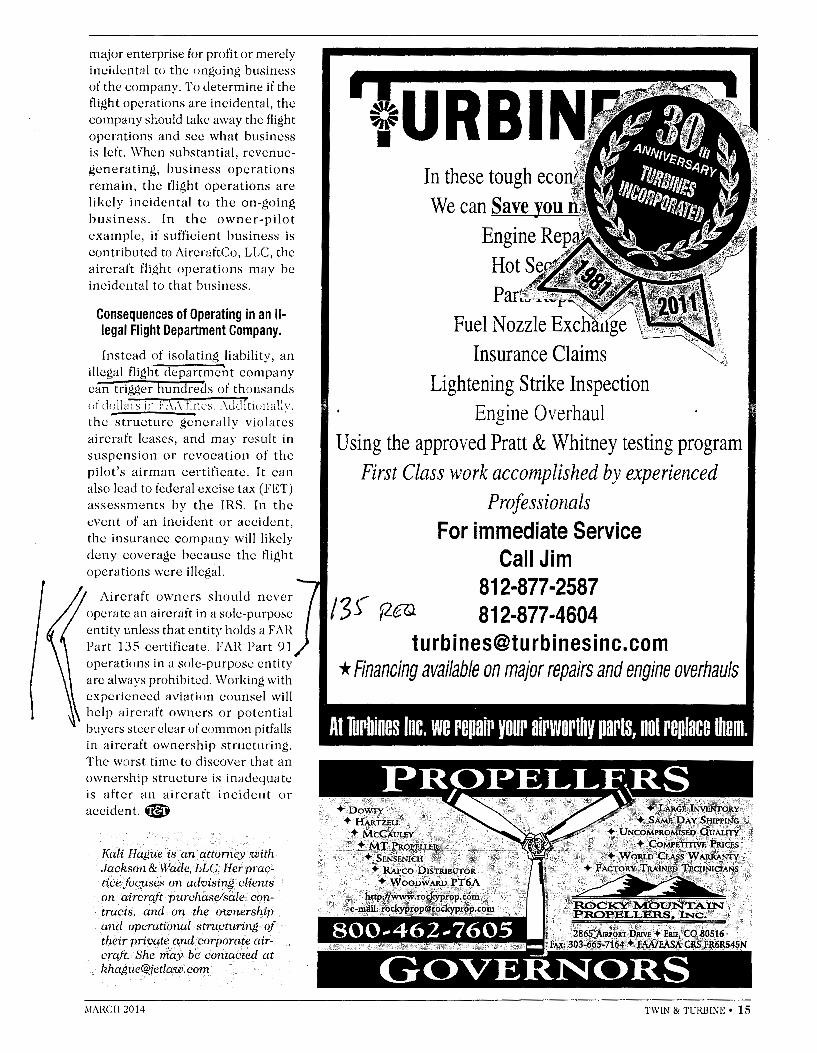

major enterprise for profit or merely indt.kmtal to the ongoing business of the company. To determine if the flight operations are incidental, the company should take away the flight operations and sec what business is left. When substantial, rcvcnucgenerating, business operations remain, the flight operations are likely incidental to the on-going business. In the owner-pilot example, if sufficknt business is contributed to i\ircraftCo, LLC, the aircraft flight operations may he incidental to that business.

Consequences of Operating in an Illegal Flight Department Company.

Instead of isolating liability, an illegal flight department company can trigger hundreds of thousands (Jf dollars in FA.\ tinc:s .. \dditio11ally, the structure generally violates aircraft leases, and may result in suspension or revocation of the pilot's airman certificate. It can also lead to federal excise tax (FET) assessments by the IRS. In the event of an inddcnt or accident, the insurance company will likely deny coverage because the flight operations were illegal.

Aircraft owners should never operate an aircraft in a sole-purpose entity unless that entity holds a FAR Part 135 certificate. FAR Part 91 operations in a sole-purpose entity arc always prohibited. Working with experienced aviation counsel will help aircraft owners or potential buyers steer clear of common pitfalls in aircraft ownership structuring. The worst time to discover that an ownership structure is inadequate is after an aircraft incident or accident.®

Kali Hague is an attorney with Jackson & Wade, LLC. Herpmctice .focuses on advising clients on aircrqft purchase/sale contracts, and on the ownership and operational structuring of their 7nivate and corporate aircraft. She may be contacted at khague@,ietla·w.com

i\lARCII 2014

yURBIN In these tough eco We can Save you llti~

Engine Rep 1 ·

Hot Seoi ~ Par:t~;:~~,

Fuel Nozzle Ex~Bif{1ge Insurance Claims

Lightening Strike Inspection Engine Overhaul

Using the approved Pratt & Whitney testing program First Class work accomplished by experienced

Professionals For immediate Service

Call Jim 812-877-2587

/3f r;zca 812-877-4604 [email protected]

* Financing available on major repairs and engine overhauls

At Turbines Inc. we repair your airworthy parts, not replace them.

}~ ~cI~!ri6kv · . + S~DAYSHil'P[NG

·•···.· .+(~(1'f¾~fl~i~; ·.·... +·Woru.o CLASS W J\RR.AN!'Y

···~:~ . ROc~MOUN'rAIN .. · .•.PROPELLERS.:INCP·

... 2s6sAr1iP~a;p~f1:~,'?0Josi6 ..•... FAx, 303-.665,7}64};, .FAA,ZMSA.G~Jill.fi~45N

TWIN & TURBIXE • lS

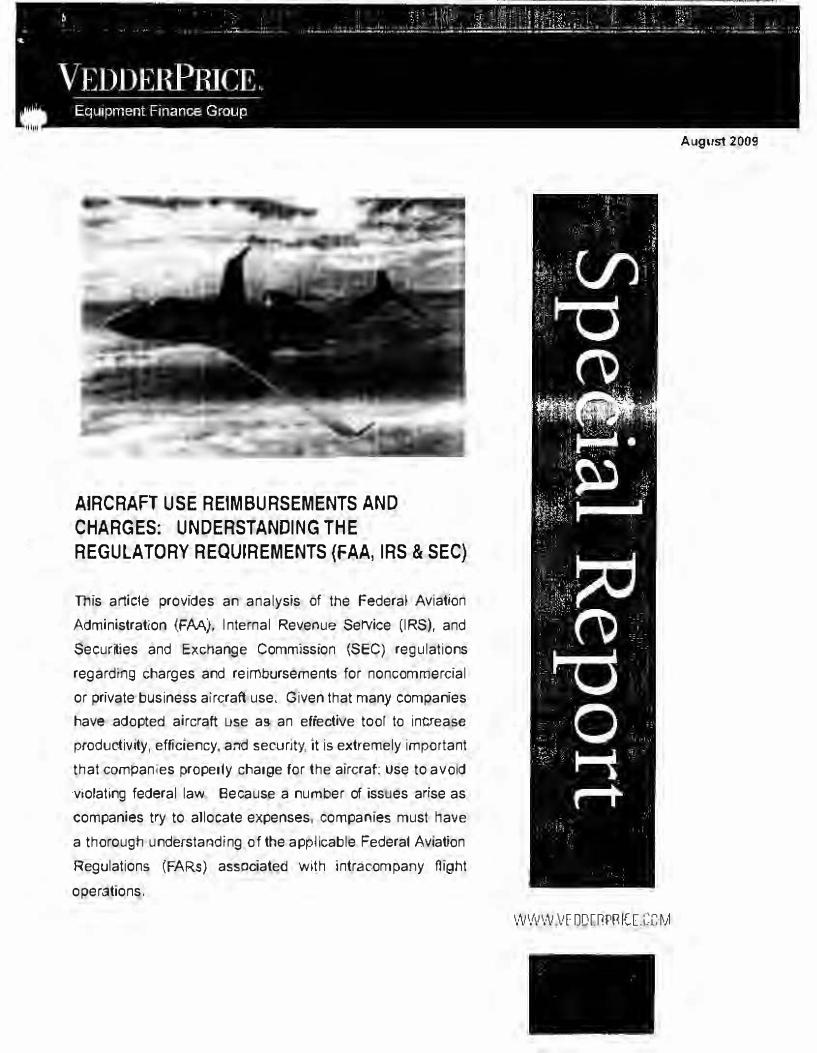

August 2009

AIRCRAFT USE REIMBURSEMENTS AND

CHARGES: UNDERSTANDING THE REGULA TORY REQUIREMENTS (FAA, IRS & SEC)

This article provides an analysis of the Federal Aviation

Administration (FAA)., Internal Revenue Service (IRS), and

Secur ties and Exchange Commissioh (SEC) regulations iregardlf'\9 charges and reimbursements for noncommercial

or private business aircraft use, Given that many companies

have adopted aircraft use as an effectiVe tool to increase

productivity, efficiency, -and security, lt is extremely important

that companies properly charge for the aircraft Use to avo d iviolating federal law Because a number of issues arise as

companies try to allocate expenses, companies must have

a thorough understar:iding of the applicable Federal Aviation

Regulations (FARS) assc;iciated with intracompany flight

operations.

vvwvv.\J[ D D(l1P111CE f;DM

Special llf•porf • ,fog11sf 2009

that such advice has in terms of the increased costs and reduced operating capabilities associated with operating under Part 135 as opposed to Part 91. More importantly, no reason exists for a company to obtain an expensive Part 121 or 135 air carrier certificate when a company's flight operations fall exclusively within the ambit of Section 501.

A. I1ighl Deparlmenl r'c1mprmies

In an effort to limit liability, many companies often make the mistake of creating a separate flight department special purpose entity (SPE) whose sole business function is the ownership and operation of aircraft. Typically, the SPE owns the aircraft, employs pilots, leases the aircraft with crew (a wet lease) to other members of the corporate family, and then seeks reimbursement. However, a SPE flight department is problematic because the SPE's flights are not incidental to the business of the company. Rather, the flights are the SPE's major enterprise or primary business purpose11 for which it receives compensation.12 According to the FAA, such an operation falls squarely within the definition of a commercial operator.

The prohibition against flight department SPEs also extends to individuals who own aircraft solely for personal use and then set up a flight department company. A good example would be an executive of a company who owns an aircraft for his personal use, who is then solicited by the company to use the aircraft for company business and is then reimbursed. The executive would have to create an SPE because individuals are prohibited from receiving reimbursement and, in doing so, the executive would have created a flight department SPE, in violation of the FARs. 13

Little doubt exists that the FAA would view such an entity as operating as an entity for compensation or hire for which an appropriate operating certificate would be required. One solution would be to establish a flight department division within a parent or subsidiary, thus avoiding the creation of an SPE.

As a practical matter, any potential reduced liability sought by the creation of the flight department SPE must be weighed against the likelihood of whether

[

\

an insurance company would honor a policy in the event of an accident, since the policyholder is likely operating in violation of the FARs.

B. •· 1f7thin tlw Scope of awl lncitfontal to ..

Before a company may seek reimbursement for expenses associated with a given flight, the company must determine whether the transportation is within the scope of, and incidental to, the business of that company or its parent or subsidiary, or its parent's subsidiary.14 Specifically, Section 501 (b)(5) provides that a company may charge for the carriage of a company's officials, employees, guests, or property on a company aircraft only when carriage is within the scope of, and incidental to, the busine,ss of the aircraft owner/operator, its parent or its subsidiary, or its parent's subsidiary. 15 If the transportation is not within the scope of, and incidental to, the business of that company, a company may still perform the flight under Part 91, but it may not seek reimbursement for expenses.

The determination of whether a company's carriage of persons or property is within the scope of, and incidental to, the company's business must be made on a case-by-case basis after the facts have been evaluated in the context of the company's business. 16 Clearly, for purposes of Section 501 (b)(5), not all of a company's transportation is within the scope of, and incidental to, a company's business. While the FAA has provided little guidance on the subject, some guidance may be gleaned from a few FAA Chief Counsel Interpretations, preambles to the Notice of Proposed Rufemaking (NPRM) and the Final Rule (FR), as well as subsequent amendments.

1. Vacation, Pleasure, or Similar Carriage

The FAA's policy is that vacation, pleasure, or similar carriage is not within the scope of, and incidental to, the business of a company. Specifically, in a Chief Counsel Interpretation, the FAA concluded that an executive was prohibited from reimbursing the company for the carriage for vacation, pleasure, or similar purposes.17 The company claimed that

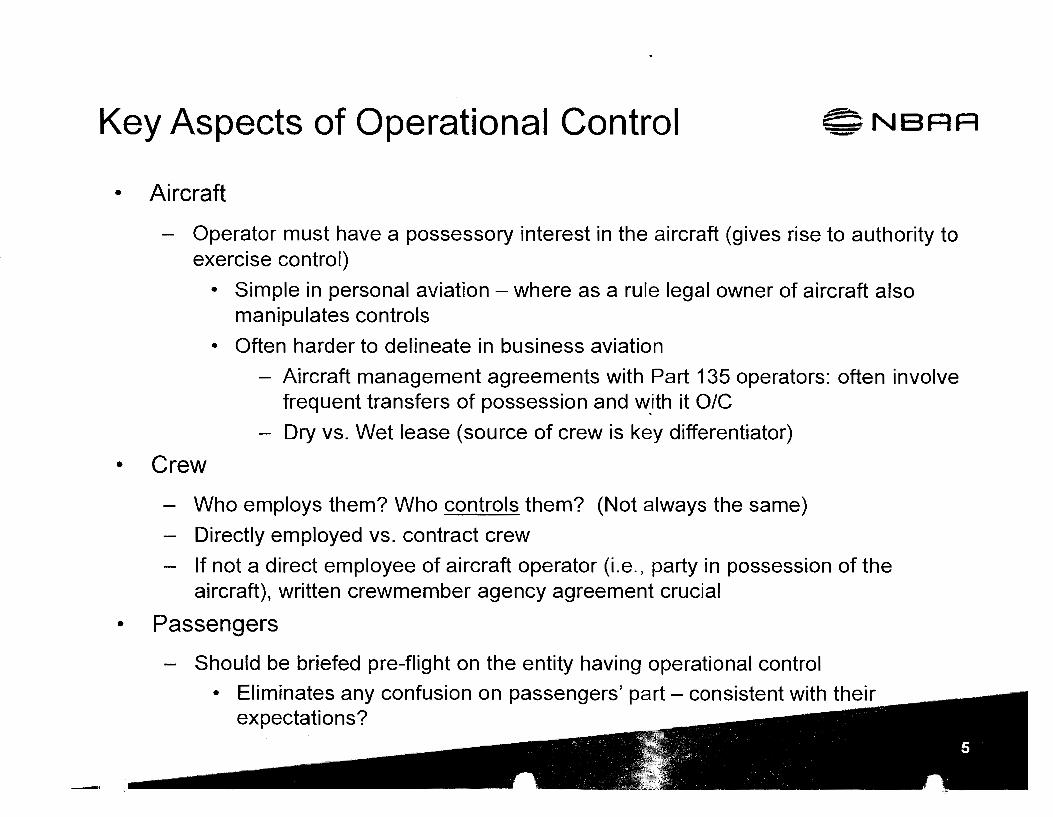

Key Aspects of Operational Control ~NBRA -• Aircraft

- Operator must have a possessory interest in the aircraft (gives rise to authority to exercise control)

• Simple in personal aviation - where as a rule legal owner of aircraft also manipulates controls

• Often harder to delineate in business aviation

- Aircraft management agreements with Part 135 operators: often involve frequent transfers of possession and w_ith it 0/C

- Dry vs. Wet lease (source of crew is key differentiator)

• Crew

Who employs them? Who controls them? (Not always the same)

- Directly employed vs. contract crew

- If not a direct employee of aircraft operator (i.e., party in possession of the aircraft), written crewmember agency agreement crucial

• Passengers

- Should be briefed pre-flight on the entity having operational control

• Eliminates any confusion on passengers' part - consistent with their expectations?

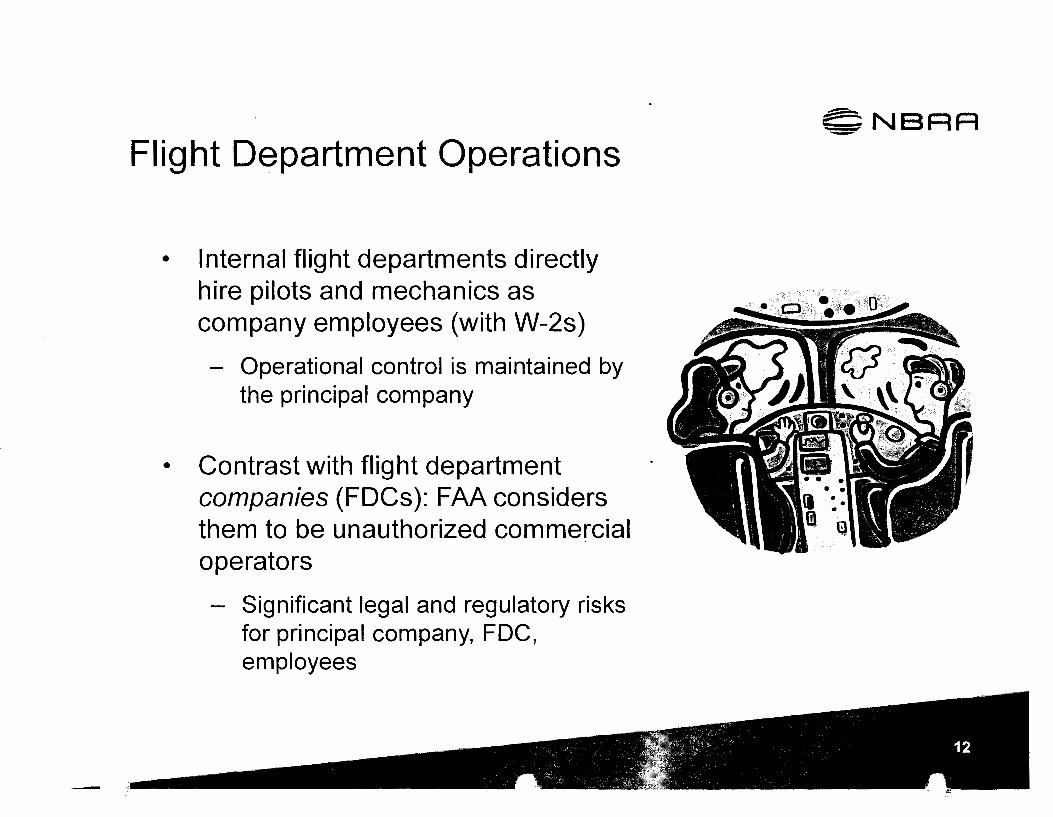

Flight Department Operations

• Internal flight departments directly hire pilots and mechanics as company employees (with W-2s)

- Operational control is maintained by the principal company

• Contrast with flight department companies (FDCs): FAA considers them to be unauthorized commercial operators

- Significant legal and regulatory risks for principal company, FDC, employees

~NBAR -

!(()) z m

] ]