· restricted report no. eap-21 this report was prepared for use within the bank and its...

TRANSCRIPT

RESTRICTED

Report No. EAP-21

This report was prepared for use within the Bank and its affiliated organizations.They do not accept responsibility for its accuracy or completeness. The report maynot be published nor may it be quoted as representing their views.

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL DEVELOPMENT ASSOCIATION

PHILIPPINES:

PROSPECTS AND PROBLEMS OF THE ECONOMY

March 31, 1971

East Asia and Pacific Department

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

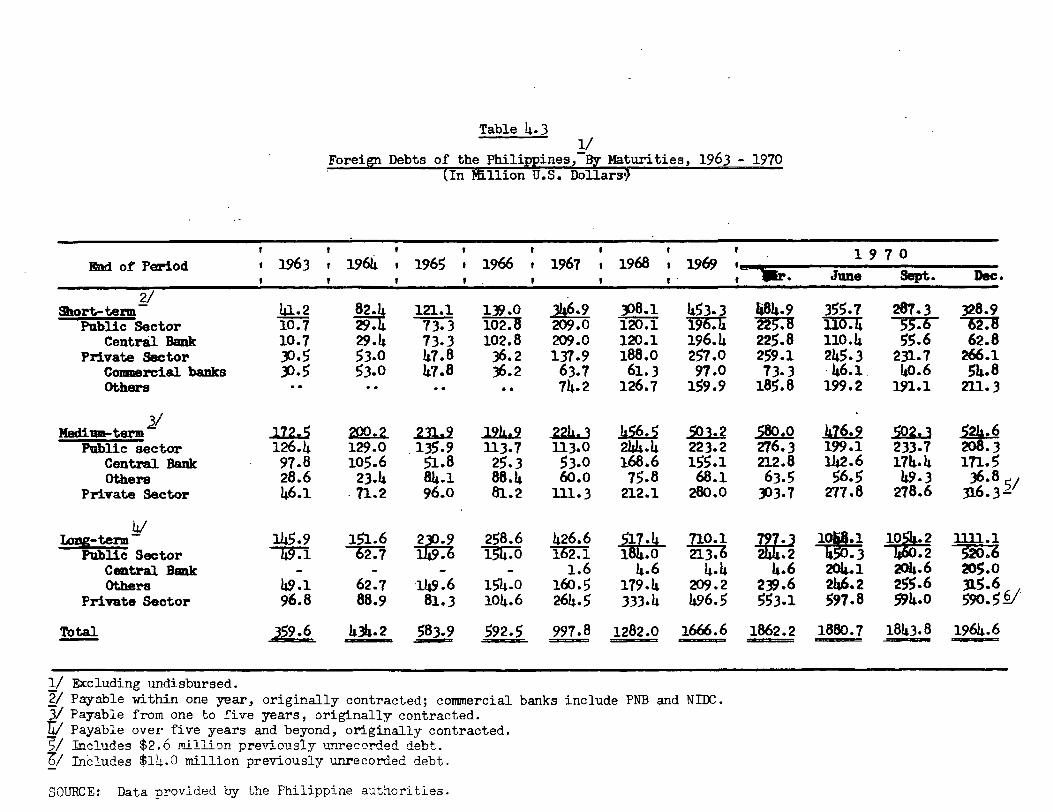

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVAIENI'S

Before Feb. 21, 1970

US$ 1.00 Pesos 3.90Pesos 1,000 US$ 256.LoPesos 1 million US$ 256,0O

After Feb. 21, 1970

US$ 1.00 Pesos 6 .435 (interbank)guiding rate sinceSept. 1970)

Pesos 1,000 US$ 155.40Pesos 1 million US$ 155,400.

FISCAL YEAR

In the Philippines the Fiscal Year covers the periodJuly 1 to June 30.

This report is based on the findings of

an Econamic Mission which visited the

Philippines from February 15 to March 5,1971. Its members were:

Parvez Hasan Chief of MissionM.ss H.J. Goris General EconomistGeorge C, Maniatis General EconomistHake M. Kamrany General Economist

TABLE OF CONTENTS

Page

BASIC DATA

SUMMARY AND CONCIUSIONS i- v

CHAPTER I - Recent Trends and Economic OutlookA. Introduction 1B. Fiscal Trends ItC. Balance of Payments 10D. Money and Credit 15E. Growth Prospects 17

CHAPTER II - Sectoral Developments and IssuesA. Agriculture 19B. Manufacturing 21C. Infrastructure Program 24D. Family Planning 27

CHAPTER III - Balance of Payments Prospects andForeign Capital Requirements

A. Introduction 29B. Exports 31C. Imports 33D. Invisibles 34E. Debt Service 35F. Financing Capital Require-

ments 36

STATISTICAL APPENDIX

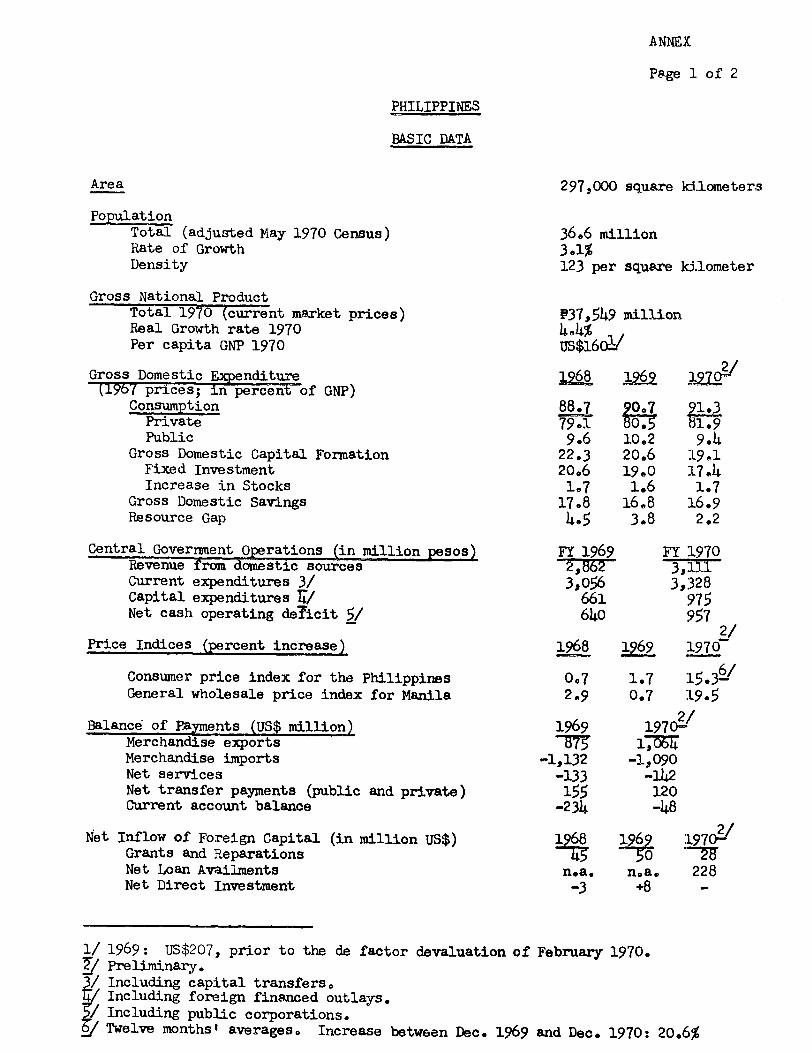

ANNEX

Page 1 of 2

PHILIPPINES

BASIC DATA

Area 297,000 square ki.lometers

PopulationTotal (adjusted May 1970 Census) 36.6 millionRate of Growth 3.1%Density 123 per square kilometer

Gross National ProductTotal 1970 (current market prices) P37,549 millionReal Growth rate 1970 4.4%Per capita GNP 1970 US$1601 /

Gross Domestic Expenditure 1268 1 6O 120(196 prices; in percent of GNP)

Consumption 807 1.3Private 79.1 0. 81.9Public 9.6 10.2 9.4

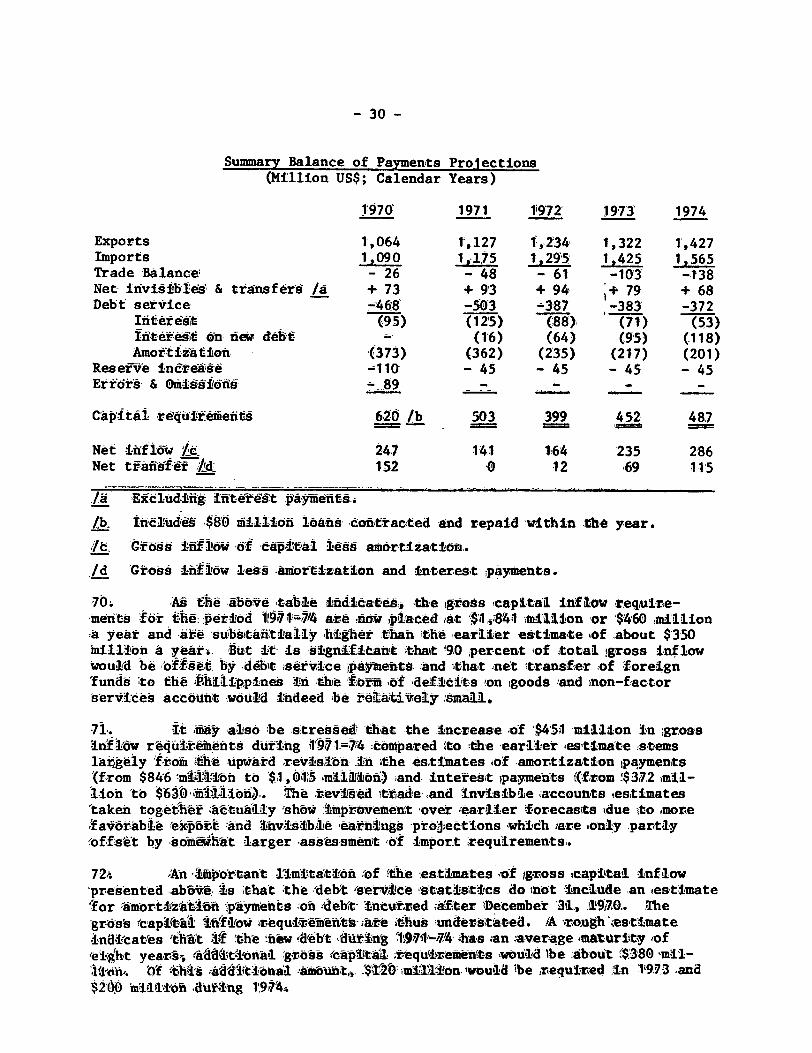

Gross Domestic Capital Formation 22.3 20,6 19.1Fixed Investment 20.6 19.0 17.4Increase in Stocks 1.7 1.6 1.7

Gross Domestic Savings 17.8 16.8 16.9Resource Gap 4.5 3.8 2.2

Central Goverment Operations (in million pesos) FY 1969 FY 1970Revenue from domestic sources 62 3,111Current expenditures 3/ 3,056 3,328Capital expenditures IT/ 661 975Net cash operating deficit 5/ 640 957

2/Price Indices (percent increase) 1968 1?69 197C7

Consumer price index for the Philippines 0.7 1.7 15.36/General wholesale price index for Manila 2.9 0.7 19.5

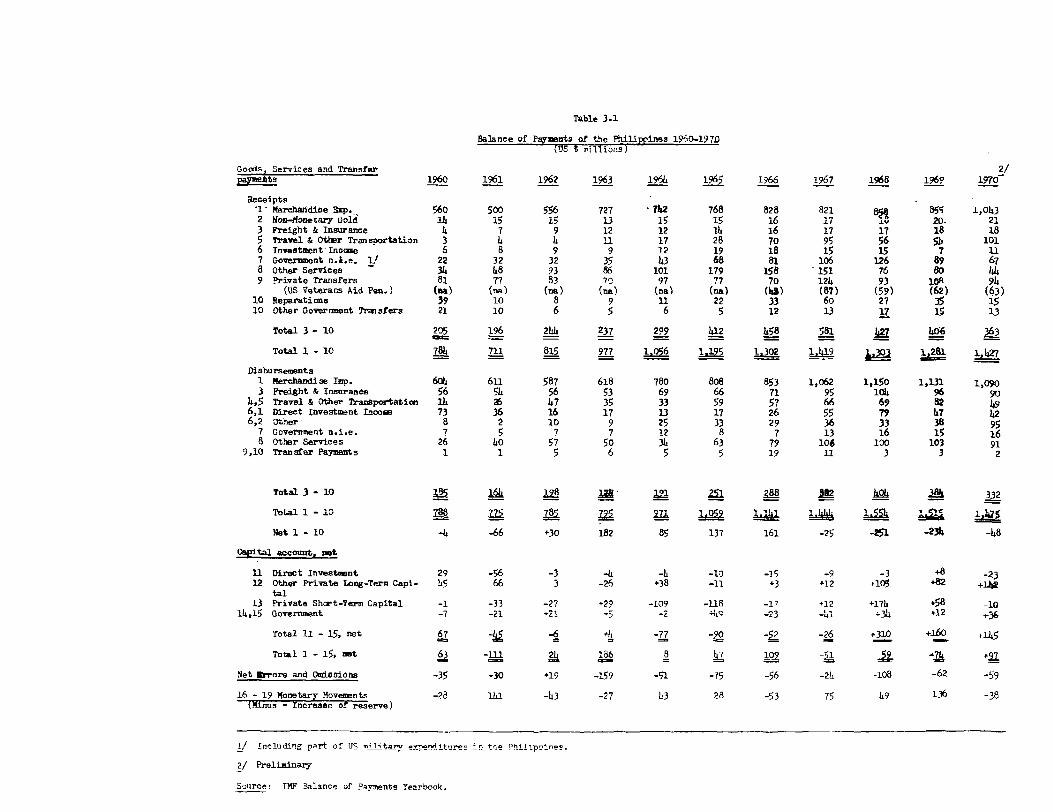

2/Balance of Payments (US$ million) 1969 19704

Merchandise exports 6F 1,6WMerchandise imports -1sl32 -1,090Net services -133 -142Net transfer payments (public and private) 155 120Current account balance -234 -48

2/Net Inflow of Foreign Capital (in million US$) 1968 196 19702Grants and Reparations M50 -WNet Loan Availments n.a. n.a. 228Net Direct Investment -3 +8 -

1/ 1969: US$207, prior to the de factor devaluation of February 1970.Preliminary.Including capital transfers,Including foreign financed outlays.Including public corporations.Twelve months' averages. Increase between Dec. 1969 and Dec. 1970: 20.6%

ANNEX

Page 2 of 2

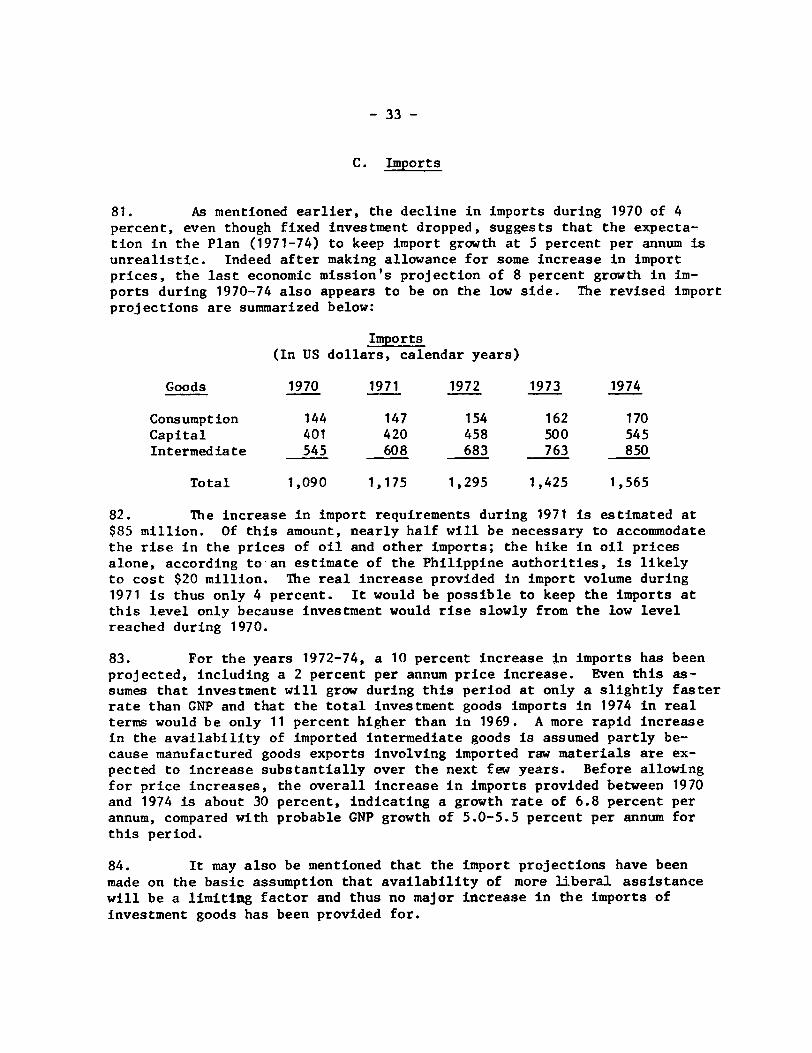

Major Exports (percent) 1969 1970Coconut products 1-9Sugar products 18 18Forest products 33 25Mineral products 19 20Others 11 15

Foreign Exchange Reserves (US$ million) Dec. 1969 June 1970 Dec. 1970Internation Reserves 1/ 126 211 237

External Public and Private Debt (US* million) Dec. 196 Dec. 1270Short term 196 63Medium term 423 417Long term 724 1,093

Total (excluding MF and revolving 1,3W4 1,573trade credits)

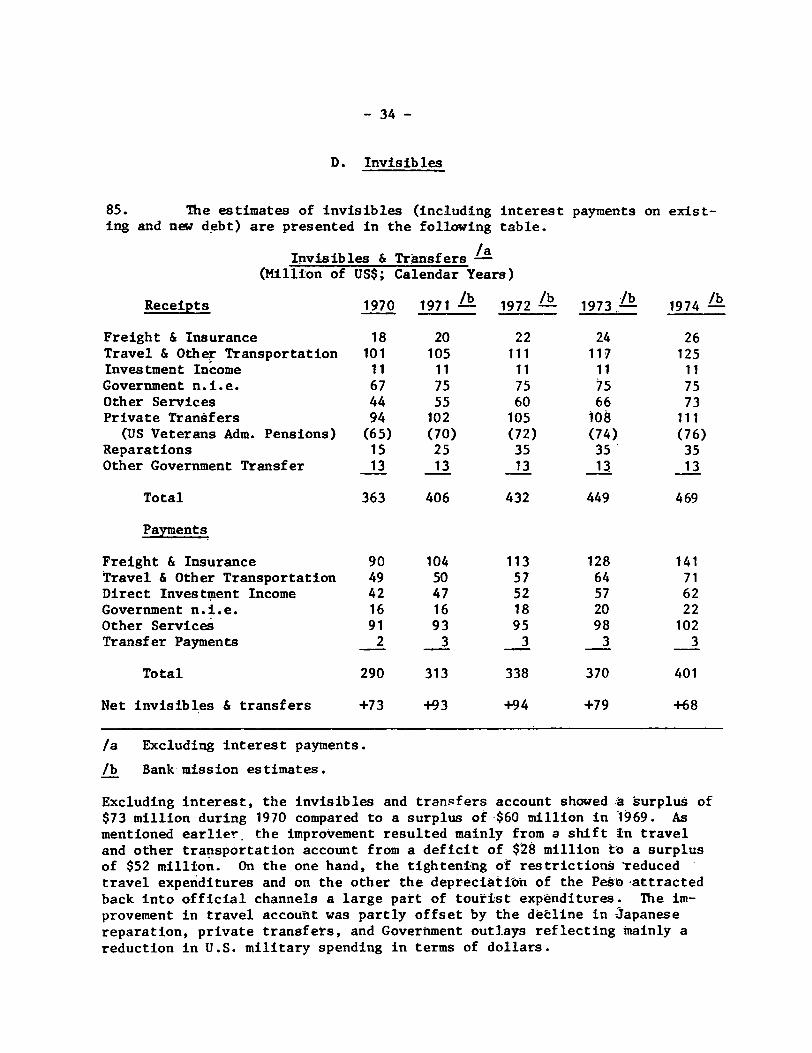

Debt Service CY 1970 CY 19712/Amortiation 373 362Interest 95 141Total 1023

Debt service ratio 3/(Total debt, publTc and private) 33% 33%

Bank operations(Dec. 31, 190)Bank loans outstanding US$ 119 millionUndisbursed amount US$ 73 million

IMF PositionQuota uS$ 155 millionDrawing outstanding (Dec. 31, 1970) k/ US$ 107.50 millionPar Value - up to Feb. 21, 1970 P3.90 per US$Floating since Feb. 21, 1970

Net reserves of commercial banks plus gross reserves of Central Bank./ Projection.

3 Basis: exports of goods and services, plus public and private tranAfers.Additional Standby of $45 million was approved in Xarch 19716

March 31, 1971

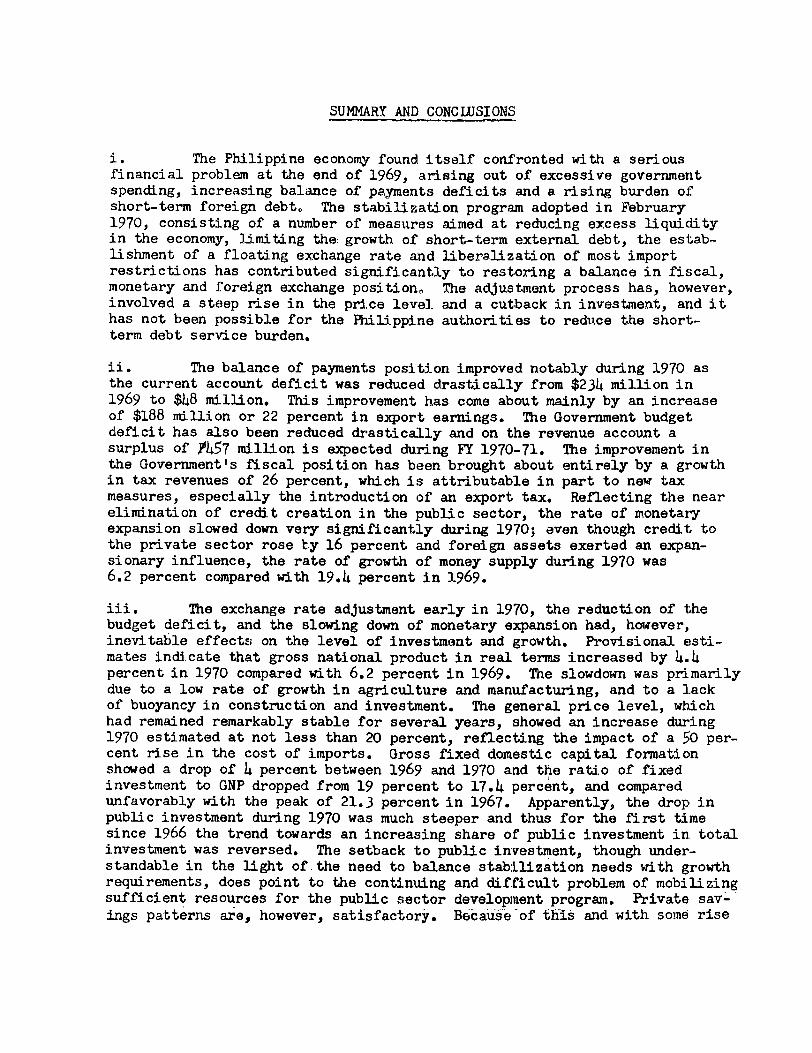

SUMMARY AND CONCLUSIONS

i. The Philippine economy found itself confronted with a seriousfinancial problem at the end of 1969, arising out of excessive governmentspending, increasing balance of payments deficits and a rising burden ofshort-term foreign debt. The stabilization program adopted in February1970, consisting of a number of measures aimed at reducing excess liquidityin the economy, limiting the:growth of short-term external debt, the estab-lishment of a floating exchange rate and liberalization of most importrestrictions has contributed significantly to restoring a balance in fiscal,monetary and foreign exchange position, The adjustment process has, however,involved a steep rise in the price level and a cutback in investment, and ithas not been possible for the Philippine authorities to reduce the short-term debt service burden.

ii. The balance of payments position improved notably during 1970 asthe current account deficit was reduced drastically from $234 million in1969 to $48 million. This improvement has come about mainly by an increaseof $188 million or 22 percent in export earnings. The Government budgetdeficit has also been reduced drastically and on the revenue account asurplus of 0457 million is expected during FY 1970-71. The improvement inthe Government's fiscal position has been brought about entirely by a growthin tax revenues of 26 percent, which is attributable in part to new taxmeasures, especially the introduction of an export tax. Reflecting the nearelimination of credit creation in the public sector, the rate of monetaryexpansion slowed down very significantly during 1970; even though credit tothe private sector rose ty 16 percent and foreign assets exerted an expan-sionary influence, the rate of growth of money supply during 1970 was6.2 percent compared with 19.4 percent in 1969.

iii. The exchange rate adjustment early in 1970, the reduction of thebudget deficit, and the slowing down of monetary expansion had, however,inevitable effects on the level of investment and growth. Provisional esti-mates indicate that gross national product in real terms increased by 4.4percent in 1970 compared with 6.2 percent in 1969. The slowdown was primarilydue to a low rate of growth in agriculture and manufacturing, and to a lackof buoyancy in construction and investment. The general price level, whichhad remained remarkably stable for several years, showed an increase during1970 estimated at not less than 20 percent, reflecting the impact of a 50 per-cent rise in the cost of imports. Gross fixed domestic capital formationshowed a drop of 4 percent between 1969 and 1970 and the ratio of fixedinvestment to GNP dropped from 19 percent to 17.4 percent, and comparedunfavorably with the peak of 21.3 percent in 1967. Apparently, the drop inpublic investment during 1970 was much steeper and thus for the first timesince 1966 the trend towards an increasing share of public investment in totalinvestment was reversed. The setback to public investment, though under-standable in the light of.the need to balance stabilization needs with growthrequirements, does point to the continuing and difficult problem of mobilizingsufficient resources for the public sector development program. Private say-ings patterns are, however, satisfactory. Becau&eof tis and with some rise

- ii -

in public savings, the overall savings rate of the Philippine economy

actually improved during 1970 and at around 17 percent of GNP does not

compare unfavorably with most developing countries.

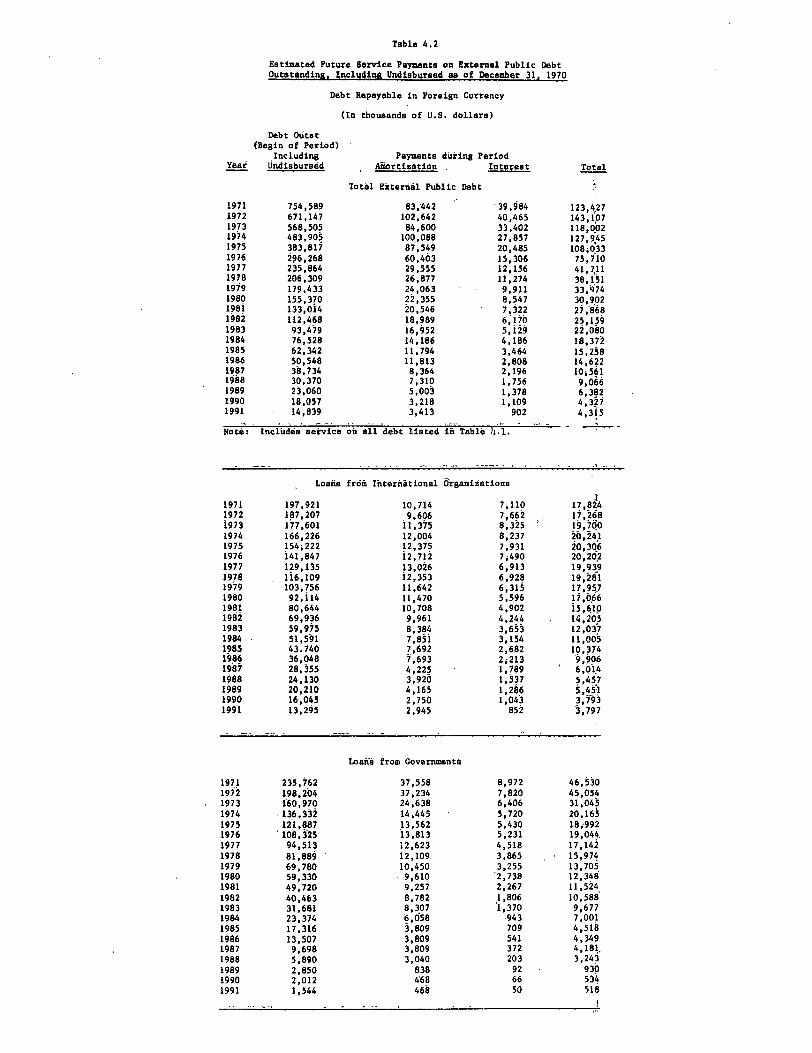

iv. Another important but less favorable feature of developments during1970 was a further increase in the foreign debt of the Philippines. Thetotal foreign debt outstanding (excluding drawings on the IMF and.short-termliabilities other than those of the Central Bank) increased by $228 millionbetween the endlof 1969 and the end of 1970. Despite a substantial increasein total debt, the short-term debt with a maturity of up to one year droppedsharply from $196.4 million from the end of 1969 to $62.8 million at the endof 1970, largely owing to the refunding of over $220 million oif Central Bankobligations by longer-term loans. Nevertheless, the structure of Philippinedebt continues to be a matter of serious concern. While the total volume ofexternal debt is not much higher than one year's gross foreign exchangeearnings, 23 percent of the debt is payable in 1971 and nearly two-thirds must,be paid within the next four years. The amortization payments of $362 millionalong with the estimated interest payments of $141 million will mean a totaldebt service of $503 million during 1971, which is larger than the debtservice of $468 million in 1970. The ratio of debt service to total foreignexchange earnings during 1971 will remain unchanged at almost 33 percent, the1970 level.

v. That the Philippines has a much more complex debt problem than wasoriginally believed is brought out by the balance of payments projections inthe report. Even disregarding principal payments on new debt which will beincurred during.the period 1971-74, the debt service during 1971-74 willaverage $410imillion annually. If it is assumed that new debt would have anaverage maturity of eight years, the debt service burden would rise from$503 million in 1971 to $564 million in 1974.and the ratio of debt serviceto gross foreign exchange earnings would drop only marginally from 33 percentto 30,percent over the period.

vi., Considering that the Philippines: is a developing country with arelatively low per capita income of $160, a reliance on net capital inflowsfrom abroad should be regarded as a normal feature of its economic develop-mentin the foreseeable future. It would be unrealistic and undesirable toexpect, therefore, a reduction in the debt service burden of the Philippinesto.come through.?a net repayment of debt from Philippine resources, that isthrough a surplus on goods and non-factor services account. As it is, thebalance of payments projections contained in the report provide for a netinflow of resources of only $50 million per year during 1971-74 or less than.one percent of GNP. This implies that investment levels will be determinedalmost entirely by the domestic savings effort. Even with the substantialdomestic saving ,effort, the ratio of fixed investment to GNP would riseslowly from the relatively low level of 17.5 percent touched in 1970. Afurther reduction in the level of net inflow cannot be undertaken withoutfurther reducing the level of investment and economic activity which wouldin turn seriously jeopardize the prospects of long-term growth of output and

- iii -

exports. Indeed, the main consideration in not suggesting a larger netinflow of capital into the Philippines has been the likely difficulty ofsecuring capital on terms which would not add materially to the already heavyburden of debt service.

vii. The improvement in the structure of the Philippine debt over aperiod of time must come, therefore, entirely from a substitution of out-standing debt by longer term capital on more favorable terms and with longergrace periods. Part of the difficulty in bringing about an improvement inthe debt structure of the Philippines arises from a heavy dependence onprivate trade credits. Over the next four years, however, the requirementsof foreign exchange loans for the public infrastructure program are projectedto increase markedly. But an increase in the absorptive capacity of thepublic sector and a sustained increase in the availability of local currencyfunds for development are necessary preconditions of a sharp rise in officialassistance, which hopefully can come on easier terms. In the near future,the Philippines will have to exercise extreme care in negotiating its new debtwith a view to minimizing the service of this additional debt in the next fewyears.

viii. The vital need in the Philippine context of raising the level oftax revenues has been discussed frequently in previous Bank reports. The total.revenues of national and local governments are currently around 14 percent ofGNP and are lower than in most developing countries. Notwithstanding the gainof 26 percent in tax revenues during 1970/71, the issue of mobilizing largertax revenues remains as alive as ever. Firstly, despite the jump in taxreceipts during the current year, the public investment effort was clearlyinadequate. Moreover, the export tax imposed last year to mop up part of thewindfall gains accruing to exporters from the devaluation was approved byCongress for four years only and at gradually decreasing rates. Thus theapparently large gain in revenue of 4WAO million from these sources is not

.permanent and would disappear entirely by FY 1975. Furthermore, and this hasparticularly great relevance for the longer run, the tax system appears to berather inelastic so that production and income increases do not often resultin proportionate increases in tax revenues. A comprehensive analysis of thecauses of the lag in revenues in recent years would help to pinpoint theweaknesses of the present system. A review of the various exemptions underincome tax and other legislation appears highly desirable.

ix. The mission was impressed with the determination of the Executiveto close tax loopholes and to improve collections generally. There remains,however, an immediate and pressing need for additicnal taxation during FY 1972.About )0100 million additional taxation would be necessary merely-to offsetthe automatic reduction in export duties under the Stabilization Tax Law,which will go into effect from July 1, 1971. The tax proposals totallingp269 million to Congress include amendment of the Stabilization Tax Law, aswell as taxes on luxury consumption, inheritance tax, tax on idle lands,revision or repeal of certain tax exemption laws, and imposition of fees andtaxes on certain forms of gambling after legalizing the activity. The tax

proposals are generally well conceived but their passage by Congresscertainly poses a problem in an election year. Nevertheless, there is areal urgency about mobilizing additional tax revenue because currently(FY 1971) public investment is lower in real terms than three years ago.

x. From the viewpoint of both equity and revenue, the maintenance ofexport taxes on most products at least at the 1970-71 level (a range of 8-10percent) deserves high priority. Considering the large windfall"gainsbecoming available to agricultural exporters through the floating exchangerate, the initial export levies did not impose a heavy burden. For most ofthe export products which were moving through official channels, the exportduties were aimed at best at mopping up about one-third of the increase inexport incomes. In fact, the depreciation of the peso through the floatingexchange rate went further than was originally envisaged and thus even asmaller portion of the total increase in export income has been capturedthrough export taxes.

xi. Despite the likely constraints arising from the insufficientavailability of foreign assistance on more liberal- terms and the inadequatemobilization of tax revenues, the growth prospects of the Philippines in theimmediate future appear good. Fortunately, the impact of a slow rise ininvestment on growth in the next few years would be cushioned by a set offavorable factors and thus it might be possible to keep the overall growthrate above 5 percent per annum during 1970-74 as against the Plan target of5.6 percent. Firstly, output will continue to benefit from the relativelyhigh rate of investment during FY 1965-69. Secondly, and closely related topast investment in key sectors such as mining, the outlook for exportsremains good. The export sector, which currently accounts for nearly 18 per-cent of GNP should grow by about 8 percent per annum after allowing for somereduction in export prices. Thirdly, the possibilities of spreading techno-logical change in agriculture are by no means exhausted. Despite the damagefrom typhoons during 1970, the current signs augur well for continued vigorousgrowth in agriculture provided a realistic policy framework is established,the right financial support and priorities are chosen and political goodwillis forthcoming from Congress. Finally, even though industrial growth continuesto suffer from excess capacity and overcrowding in many industries, theexchange rate adjustment has created a favorable climate for rationalizationefforts by opening up possibilities of exports. Meanwhile, because of thefinancial squeeze on industries, the leverage of the Development Bank of thePhilippines over the private sector has increased. The Board of-Investments,which controls and supervises all new investments, is cognizant of the short-comings of past policies and appears determined to reorient industrialpolicies, especially towards export promotion, and to this end a basic reformof the existing tariff system is planned.

xii. In sharp contrast to the slow average growth of less than 5 percentin merchandise exports during 1959-69, the export prospects for the nextseveral years appear good. The mission estimates indicate an annual growthrate of 10 percent between 1969 and 1974. The satisfactory export performance

- v -

during 1970 was attributable partly to a reduction in unrecorded exports andpartly to an improvement in export prices. However, the entire increase inearnings during the next four years is expected to come from an increase inthe volume of exports. Between 1969 and 1974, the volume of copper exportsis expected to nearly double, while sugar exports should increase by 45 per-cent, log exports by 28 percent, and nickel would be added to the export listin 1973. While prices of most export commodities are projected during 1971-74to remain at about the 1969 level, copper prices are assumed, on average, tobe 25 percent lower. But notwithstanding the downward revision of copperprice forecasts compared to last year, the latest export estimates are some-what higher than the last mission's projections and are more optimistic onthe whole than the Plan forecasts.

xiii. The mission projections assume a much higher growth rate for non-traditional exports, which comprise mainly minor agricultural products andmanufactured goods. These exports are expected to double between 1970 and1974. Their relative share in total exports would improve from 15 percent in1970 to 21 percent in 1974, reflecting mainly reduced dependence on coconutproducts and sugar.

xiv. The decline in imports during 1970 of 4 percent, even though fixedinvestment dropped, suggests that the expectation in the Plan (1971-74) tokeep import growth at 5 percent per annum is unrealistic. Indeed, aftermaking allowance for some increase in import prices, the last economicmission's projection of 8 percent growth in imports during 1970-74 alsoappears to be on the low side. Before allowing for price increases, the over-all increase in imports provided between 1970 and 1974 is about 30 percent,indicating a growth rate of 6.8 percent per annum, compared with probableGNP growth of 5.0-5.5 percent per annum for this period. These importprojections are in a sense a minimum because they will permit only an 11 per-cent growth of investment goods imports between 1969 and 1974.

xv. Even on the basis of this rather modest increase in imports and asubstantial growth in export earnings, the capital inflow requirements for1971-74 are now placed at $1,841 million or $460 million a year and aresubstantially higher than the earlier estimate of about $350 million a year.These gross inflow requirements, however, are understated to the extentthat allowance has not been made for amortization during 1971-74 of debtincurred after December 31, 1970. A rough estimate indicates that, assumingthat the average maturity of the new debt is eight years, the gross capitalrequirements would increase further by about $400 million. Most of theincrease will fall in 1973/74 and on adjusted basis, the gross capitalrequirement for 1974 would thus be substantially larger than at present.This again points attention to the fact that unless her debt burden can bealleviated by more liberal long-term assistance, the Philippines will befaced with an immense foreign exchange management problem.

CHAPTER I

Recent Trends and Economic Outlook

A'. Introduction

1. The economic performance of the Philippines during 1966-69 was inmany ways very satisfactory. The real growth rate of the economy duringthis period averaged 6.2 percent per annum, compared with less than 5 per-cent per annum during 1963-66 and the over-all price increase was limitedto 4 percent per annum. The investment level remained high; the ratio 1/of fixed investment to GNP averaging over 20 percent during 1966-69,compared with around 18.5 percent in the previous four years. What is evenmore important, previously neglected public sector investments in infra-structure rose rapidly, doubling between 1965-66 and 1968-69, and the ratioof public investment to total investment, though still very low, improved.However, savings performance, which had been such a strong feature of theover-all economic picture in,the first half of 1960's, deteriorated after1966; the national saving rate dropped-from the peak of 22 percent in 1965-66to 16 percent in 1968-69. A reflection of the savings-investments gap wasthe growing fiscal deficit which reached a record level in 1969 and thelarge increase in bank credit to the private sector. The balance of paymentsposition thus came under serious pressure during 1968 and 1969. Whileimports expanded by 35 percent between 1966 and 1968 and then levelled offduring 1969, exports increased by less than 1 percent per annum during1966-69. Consequently, the current account deficit (including transfers)reached huge proportions averaging 3.2 percent of GNP during 1968-69. Thisdeficit was largely financed with foreign credits of relatively shortmaturities.

2. The Philippine economy thus found itself confronted with a seriousfinancial problem at the end of 1969. As foreign exchange reserves declined,confidence in the peso weakened further, encouraging the diversion of ex-ports and invisible earnings into unofficial channels. In this situation,Philippine authorities decided at the beginning of 1970 basically to reorientthe economic policies to strengthen the balance of payments and to facil-itate an orderly settlement of the foreign debt. A standby agreement withthe IMF was concluded in February 1970 and a comprehensive stabilization 2/program was adopted. The program consisted of a number of measures aimedat reducing excess liquidity in the economy, limiting the growth of short-term external debt, the establishment of a floating exchange rate andliberalization of most import restrictions.

1/ All GNP, investment and saving data are in 1967 prices.

2/ For details of the stabilization program, see pages 18-23 of the lastBank report on "Current Economic Position and Prospects of thePhilippines", August 1970 (EAP-16a).

- 2-

Overall Developments During 1970

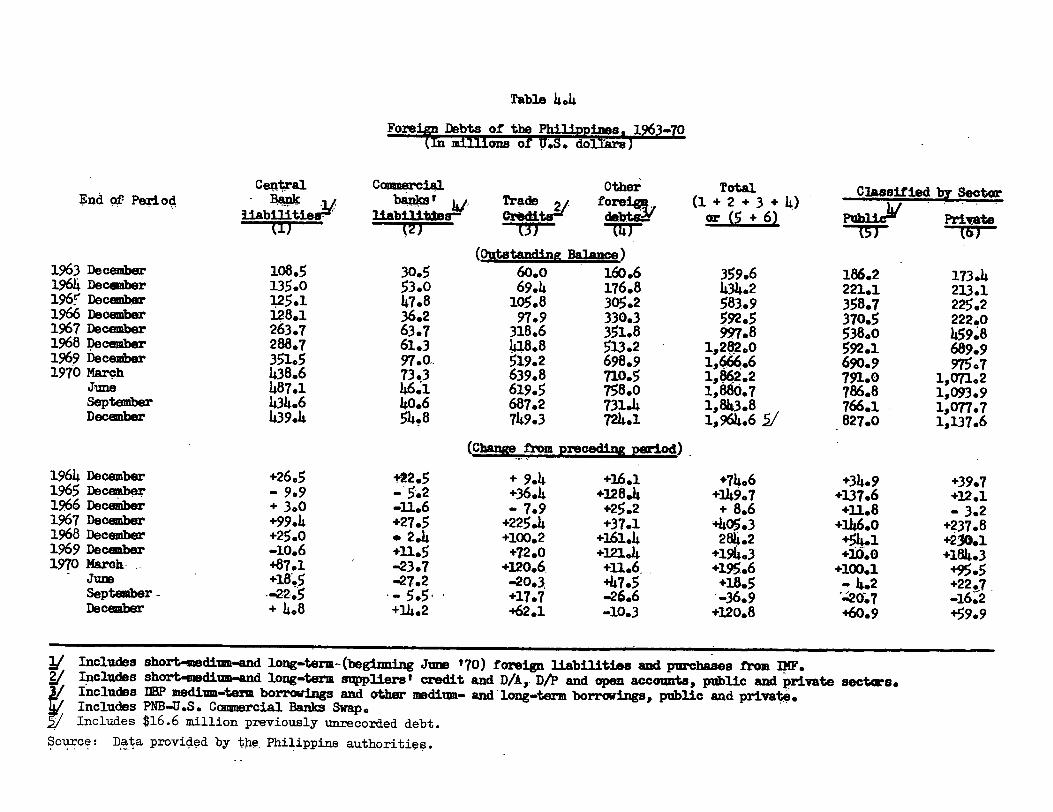

3. The stabilization program was followed by the Government with greatdetermination throughout 1970 and has contributed significantly to theimprovement in the balance of payments. Partly as a result of shiftsbrought about by the depreciation in the exchange rate from par value ofP 3.90 per US dollar to 6.43 per US dollar 1/ and partly as a result ofincreases in copper, sugar and coconut production, the current accountdeficit 2/ was reduced drastically from $234 million in 1969 to $48 millionin 1970. At the same time, international reserves increased by $111 million.The building up of foreign exchange reserves and financing of the currentaccount resulted in a further increase in external debt outstanding during1970 of $228 million.

Production Trends

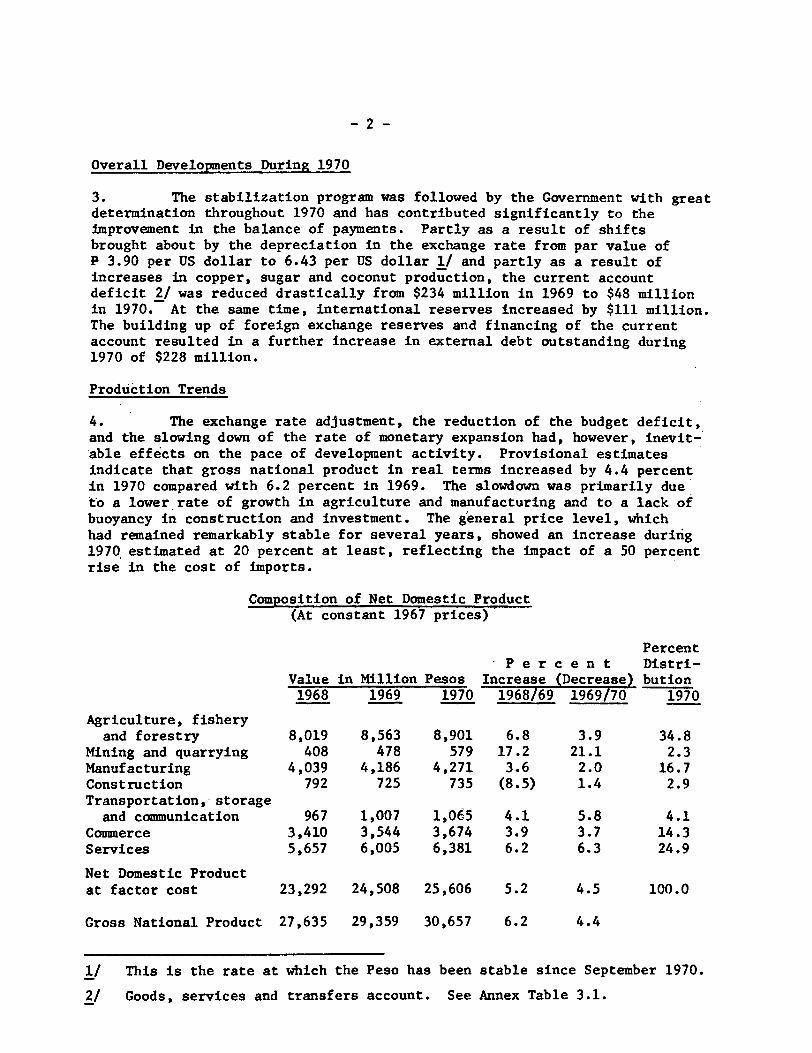

4. The exchange rate adjustment, the reduction of the budget deficit,and the slowing down of the rate of monetary expansion had, however, inevit-'able effects on the pace of development activity. Provisional estimatesindicate that gross national product in real terms increased by 4.4 percentin 1970 compared with 6.2 percent in 1969. The slowdown was primarily due*to a lower rate of growth in agriculture and manufacturing and to a lack ofbuoyancy in construction and investment. The general price level, whichhad remained remarkably stable for several years, showed an increase during1970 estimated at 20 percent at least, reflecting the impact of a 50 percentrise in the cost of imports.

Composition of Net Domestic Product(At constant 1967 prices)

PercentPercent Distri-

Value in Million Pesos Increase (Decrease) bution1968 1969 1970 1968/69 1969/70 1970

Agriculture, fisheryand forestry 8,019 8,563 8,901 6.8 3.9 34.8

Mining and quarrying 408 478 579 17.2 21.1 2.3Manufacturing 4,039 4,186 4,271 3.6 2.0 16.7Construction 792 725 735 (8.5) 1.4 2.9Transportation, storage

and communication 967 1,007 1,065 4.1 5.8 4.1Commerce 3,410 3,544 3,674 3.9 3.7 14.3Services 5,657 6,005 6,381 6.2 6.3 24.9

Net Domestic Productat factor cost 23,292 24,508 25,606 5.2 4.5 100.0

Gross National Product 27,635 29,359 30,657 6.2 4.4

1/ This is the rate at which the Peso has been stable since September 1970.

2/ Goods, services and transfers account. See Annex Table 3.1.

-3-

5. Value added in agriculture increased by 3.9 percent, compared withan increase of 6.8 percent in 1969. The main factors adversely affectingagricultural output were a series of typhoons, measures to limit log exportsfor conservation purposes, and weaker demand for forest products in localand foreign markets. Sugar and rice production increased substantially inthe crop year 1969-70. Favorable weather in sugar growing areas, increasedmilling capacity and a larger acreage under cultivation (13 percent) led toa nearly 20 percent growth in sugarcane production. Rice production con-tinued to benefit from wider use of high-yielding varieties, increasedfertilizer use and extension of irrigation facilities.

6. Available data indicate that value added in manufacturing industrieswould show only a small increase in 1970 compared with 1969. The slowdownin manufacturing activity could be attributed to a number of factors, in-cluding import restrictions during the latter part of 1969 and early 1970,the relatively tight credit conditions, the higher costs of imported rawand semi-processed materials, a shortage of liquidity in firms with a highforeign debt share in the capital structure, and to a slowdown in construc-tion which had.especially affected the cement industry. Production oflocally assembled automobiles and of certain textile products declined.The former were adversely affected by import restrictions and an excessivenumber of small-scale operations, and the latter continued to suffer fromsmuggling. The typhoons adv4rsely affected output in certain industriesin areas where electric power had been interrupted.

Gross Domestic Capital Formation(At constant 1967 prices)

PercentValue in IncreaseMillion Pesos (Decrease) Percent of GNP1968 1969 1970 1968/69 1969/70 1968 1969 1970

Construction 2,021 1,843 1,876 (8.8) 1.8 7.3 6.3 6.1

Durable Equipment 3,672 3,724 3,461 1.4 (7.1) 13.3 12.7 11.3

Increase in stocks 478 473 519 (1.0) 9.7 1.7 1.6 1.7

Gross DomesticCapitalFormation 6,171 6,040 5,856 (2.1) 3.0 22.3 20.6 19.1

Investment Level

7. As a result of stabilization policies and a sharply reduced netinflow of external resources, gross fixed domestic capital formation showeda drop of 4 percent between 1969 and 1970 and the ratio of fixed investmentto GNP dropped from 19 percent to 17.4 percent, and compared unfavorablywith the peak of 21.3 percent in 1967. Apparently, the drop in publicinvestment during 1970 was much steeper and thus for the first time since1966 the trend towards an increasing share of public investment in total

investment was reversed. The setback to public investment, though under-standable in the light,of the need to balance stabilization needs withgrowth requirements, does point to the continuing and difficult problemof mobilizing sufficient resources for the public sector development program.The overall saving rate of the Philippine economy actually improved during1970 and at around 17 percent of GNP does not compare unfavorably with mostdeveloping countries. What is needed is to bring about a better balancebetween public and private investment and to raise the investment level asa whole by increasing the net inflow of resources to the Philippines andby further increasing the level of savings. The practicability of enlargingthe current account deficit during the next few years will depend greatly,however, on the level of debt service payments as well as gross inflows.The key issues of mobilization of resources for the public sector and debtservice requirements are discussed in some detail in the subsequent sections.

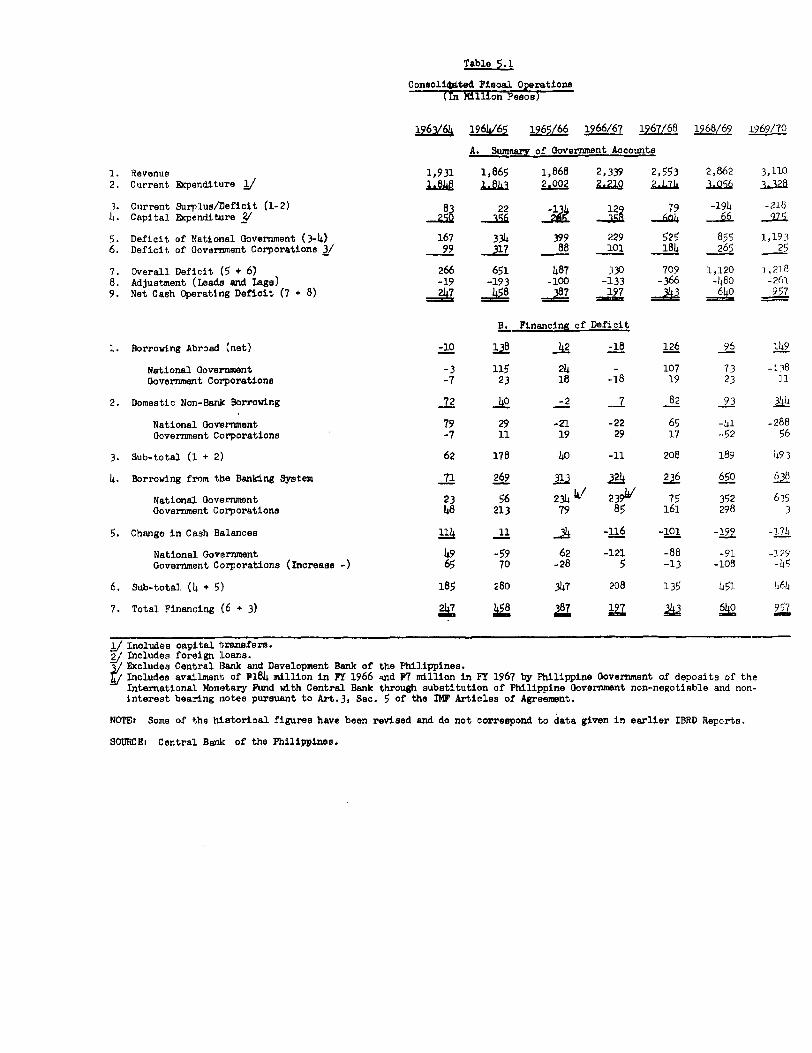

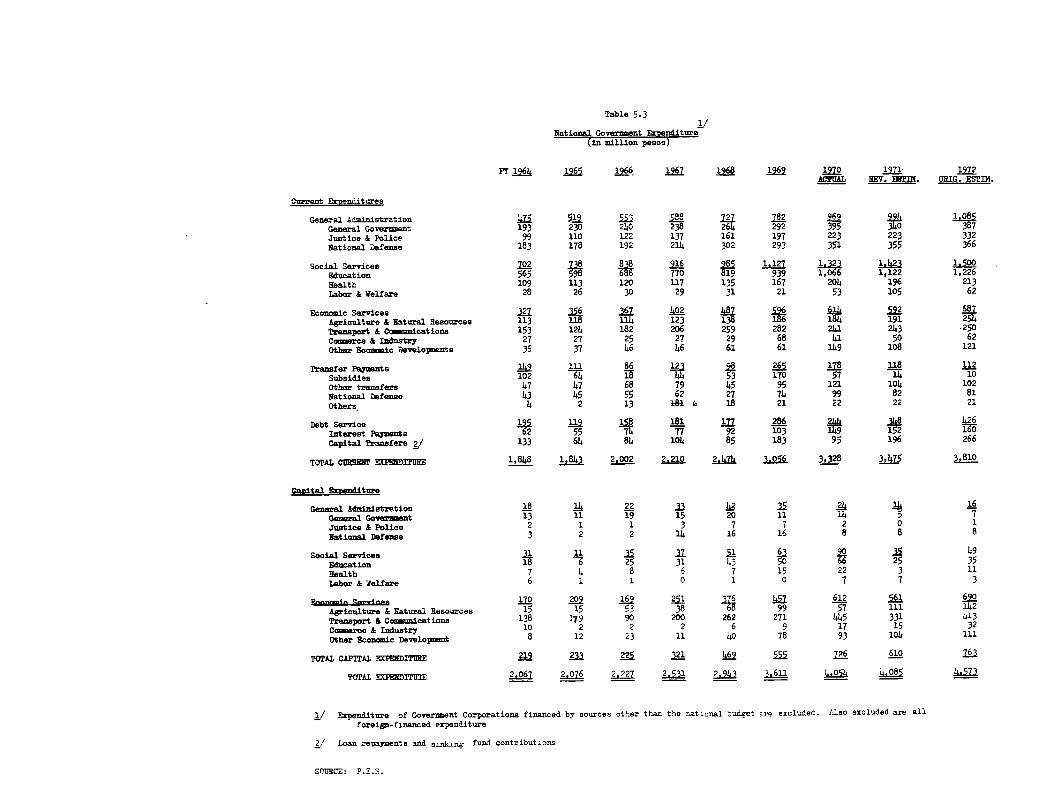

B. Fiscal Trends

8. The fiscal position of the National Government has shown aremarkable improvement during the last year. The revenue account deficit,which had grown to P 218 million in FY 1969-70, is expected to be replacedby a surplus of P 457 million during FY 1970-71. The improvement has beenbrought about entirely by a growth in tax revenues of 26 percent which isattributable in part to new tax measures, especially the introduction ofthe export tax which was expected to yield an additional revenue of P 440million. The current expenditures are expected to show an increase ofonly 4.4 percent between FY 1970 and FY 1971 which is traceable mainly toa rise in debt service. The present restraint in current government spending,notwithstanding a general rise in prices and costs, is commendable. It isnoteworthy that in the three years preceding 1970-71, current spending hadrisen by an average rate of over 16 percent per annum and had been a majorfactor responsible for the serious imbalance in the budgetary position.

- 5 -

Government Current Account, 1965/66-1971/72(In million pesos)

1965/66 1966/67 1967/68 1968/69 1969/70 1 9 7 0 / 7 1 - 1 9 7 1 / 7 2Lb-/C

Tax Revenue 1,775 2,202 2,491 2,848 3,214 4,024 4 ,7 20--

Non-Tax Revenue 306 423 395 403 399 471 477

Total 2,081 2,625 2,886 3,251 3,613 4,495 5,197

Less Transfersto LocalGovernments 213 286 333 389 502 564 637

Net CentralGovernmentRevenue 1,868 2,339 2,553 2,862 3,111 3,931 4,560

Current Expendi-ture (includingcapitaltransfers) 2,003 2,210 2,475 3,056 3,328 3,474 3,811

RevenueSurplus/Deficit -135 +129 +79 -194 -218 +457 +749

/a Rev-ised-estimates.7T Budget estimates./c Including collection from additional tax measures of P 269 million

yet to be approved by Congress.

9. Despite the impressive gain in revenues and limited rise in current

spending, the capital outlays (spending on infrastructure and non-infra-

structure capital formation) had to be cut back during 1970-71 in order to

eliminate almost entirely the reliance on the banking system for financingthe budget deficits. The sharp curtailment in credit creation for the public

sector was no doubt essential in order to relieve the pressure on the

balance of payments, but the net effect of the stabilization measures onpublic investment cannot be viewed without concern. Capital expenditure 1/

of the National Government, which had risen steadily from P 347 million in

FY 1966 to P 975 million in FY 1970, is expected to decline to P 816 million

in FY 1971. Admittedly a part of the increased spending on infrastructure

program during FY 1970 occurred under various community projects (P 163 mil-

lion) which do not rate as high priority investment. But still, allowingfor the sharp increase in the prices of investment goods which has occurred

particularly during 1970, the current levels of government capital spending

1/ Including foreign loans.

- 6 -

compare very unfavorably with the level either in FY 1968 or FY 1969. Thelost ground in public investment would have to be recovered quickly during1971-72 if the Four-Year Plan is to have even a moderate change of success.

Trends in Government Spending

1965/66 1966/67 1967/68 1968/69 1969/70 1970/71 1971/72

Percentage growth of:Total expenditure 7.2 13.7 16.3 22.7 12.3 0.8 12.0Current expenditure /a 8.6 10.3 12.0 23.5 8.9 4.4 9.7Capital expenditure 7 -3.4 42.7 46.1 18.3 30.8 -16.0 25.1Revenue /c -0.6 26.1 9.9 12.6 11.1 24.4 15.6

Capital expenditureas % of totalexpenditure /b 10.1 12.7 15.9 15.4 17.9 14.9 16.9

/a Including capital transfers (- amortization payments).7b- Excluding capital transfers.

7c National government revenue plus transfers to local governments.

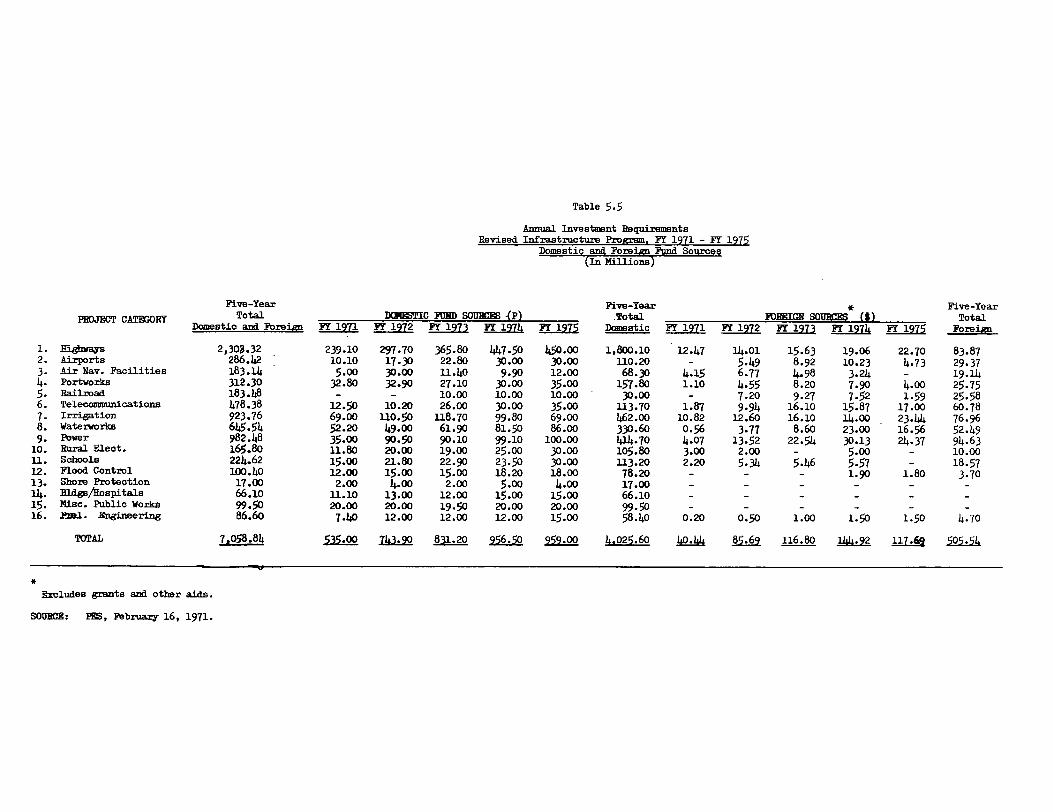

10. The Infrastructure Investment Program for FY 1971 has already been

scaled down from the Plan projections of P 976 million to P 775 million.

Moreover the price increases of capital goods have been substantially larger

than envisaged in the Plan and actual implementation during the year may fall

short of the present target of P 775 million. Thus the shortfall in infra-

structure in the first year of the Plan may be as large as one-third in real

terms.

11. The budget for FY 1972 as submitted to Congress proposes an infra-

structure investment of P 1,260 million (local currency spending of p 744

million and foreign loans or reparation of $86 million). While this level

represents a small decline of 7 percent over Plan projections, it constitutes

a most ambitious goal in the light of current !.mplementation of public develop-

ment outlays. As far as can be seen, the success of the Administration's

efforts to bring about a rapid recovery in the infrastructure investment

level would depend crucially on the additional taxation effort during FY 1972.

The President's budget message indicates a budget deficit which is to be met

from additional taxation proposals of P 269 million. In case and to the

extent that Congress does not approve the taxation proposals, the downward

adjustment would be perhaps made mainly in proposed public investment. The

current expenditures for FY 1972 which, excluding debt service, are planned

to be increased by 8.5 percent, may also bear some pruning. But considering

that salary increases of 5 percent are given automatically to public servants

- 7 -

every year and that the Administrative Reorganization 1/ proposals might notbe acted upon by Congress during the current session, prospects for majoreconomies in current spending appear limited.

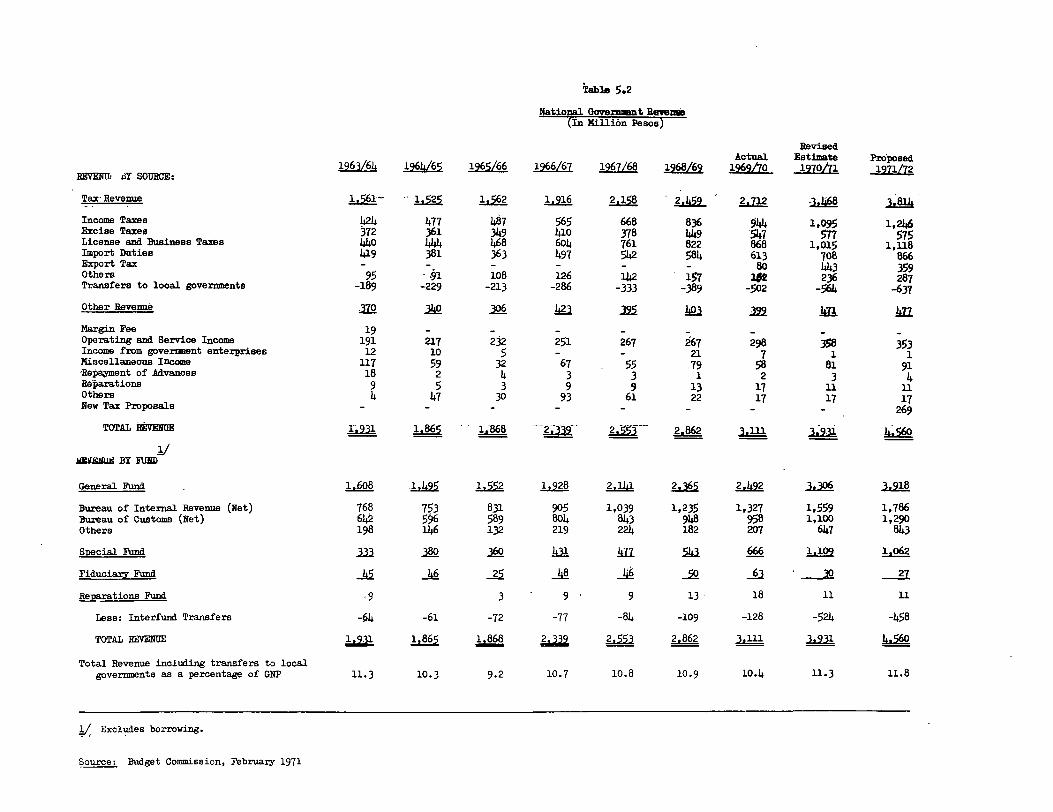

12. The absolutely vital need in the Philippine context of raising thelevel of tax revenues has been discussed frequently in previous Bank reports.Notwithstanding the impressive gain of 26 percent in tax revenues during1970-71, the issue of mobilizing larger tax revenue remains as alive as ever.Firstly, as mentioned above, despite the jump in taxation receipts during thecurrent year, the public investment effort was clearly inadequate. Moreover,the export tax imposed last year to mop up part of the windfall gains accruingto the exporters from the devaluation was approved by Congress for four yearsonly and at gradually decreasing rates. Thus the apparently large gain inrevenue of P 440 million from this source is not permanent and would dis-appear entirely by FY 1975. Furthermore, and this has particularly greatrelevance for the longer run, the tax system appears to be rather inelasticso that production and income increases do not often result in proportionateincreases in tax revenues. The tax revenues of the National Government 2/showed an increase of 60.percent between 1967-68 and 1970-71 but about halfof this increase came from additional taxation measures. The normal growthin tax revenue over this period including effects of improvement in taxcollection, estimated at 9 percent per annum compared with an annual increaseof 13 percent in GNP in current prices. Thus the ratio of tax revenues toGNP would have dropped but for the additional tax effort. As it is, the taxratio improved from 9 percent in 1967-68 to an estimated 10 percent in 1970-71.

13. In judging the total revenue effort of the government, however, itis necessary to take account of non-tax revenue of the national government,revenues of local government, and mobilization of resources through theSocial Security System (SSS) and the Government Service Insurance System(GSIS). The calculation on this basis suggests that total revenues ofnational and local governments are currently around 14 percent of GNP andare lower than in most developing countries.

I/ A Government Reorganization Commission was constituted in 1968,composed of three members from the Administration and three memberseach of the Houses of Congress, with the specific task of preparingrecommendations for economies in government expenditures and policiesfor a more efficient pursuit of economic development. The findings ofthe Commission have been finalized and would be submitted to Congressin May 1971.

2/ Before transfers to local governments.

- 8- -

Revenue Effort, FY 1966-71(In million pesos)

1966, 1967 1968, 1969 19,Q 197/1

National governmentrevenue 1,868 2,339 2,553 2,862 3,111 ,931.

Transfers to localgovernments 213 286 333 389 5Qz 564

Local governmentsrevenue 360 382 340 385 431 483

Sub-total 2,441 3,007 3,226 3,636 4,Q44 4,978

SSS 107 119 132 146 147 17QGSIS 111 130 148 254 288 319

Sub-total 218 249 280 400 435 489

Total Revenue 2,659 3,256 3,506 4,036 4,479 5,467GNP (in current prices) 22,158 24,635 26,830 29,687 34,644 39766 /a

Revenue Effort

(% of GNP) 12.0 13.2 13.1 13.6 12.9 14.0

/a Estimate.

14. But in the final analysis, it is not so much the level of taxrevenues as the outlook for growth which is relevant for Judging theadequacy of a tax system. It is in this context that the Philippines'rather inelastic tax system and dependence on a temporary source of reyeque,vix. the export tax, cause concern. A meaningful tax reform must aim at notonly tapping new sources of revenue but also improving the responsiveness ofthe tax structure to income changes. A comprehensive analysis of the causesof the lag in revenues in recent years would help to pinpQipt the weaknessesof the present system. Generally speaking, the tax program approved in FY1969, while raising additional revenue eroded the tax basis further bygranting liberal tax exemptions 'under personal income tax, lso, theseexemptions were regressive as benefits went mainly to higher income groups,The Investment Incentives Act :passed in 1967 with its imporjtant tariffexemptions 'for capital goods imports has also caused a lp_s of rgep.,In'FY .1971 'Congress approved the Export Incentives Act provding tax ;rjdits,tax exemption fon imported capital -equipment,, and exemption from lexpgrt axfor exporters. 'This 'law would further affect revenue yield. Thw appropr:iate-ness 'of special export incentives at this stage is Ves a g Lg P AeTacto fdevaluat'lon 'of the peso by 40 percent since February 1:970 in itselfhas 'ensured sufficient initial incentives for potential exporters, A xypieof the Export 1ncentives Act so soon after its app.rova ma?j y, however, be:dff.`ifcult. But ,a review of the 'Investment incent-ives Act and sexemptionsavaiL4bl;e 'under in,come tax and -other 'legislation appears highly -des:irable,.

- 9 -

15. The mission was impressed with the determination on the part ofthe Executive to close tax loopholes and to improve collections generally.A Tax Census Law passed two years ago would be enforced from this year. Itrequires all citizens with property (above P 3,000) to file an assetsreturn. These returns would be processed by the Bureau of Internal Revenue(BIR) and used for building up a tax roll. Key personnel have been re-shuffled in BIR and the names of tax delinquents are being published. AStanding Committee, consisting of members from the Joing LegislativeExecutive Tax Commissionand BIR, has been created to simplify the tax codeand to make recommendations on closing the loopholes. The test of theefficacy of these administrative measures would be in achieving the projectedgrowth of 12 percent in normal tax revenues during FY 1972.

16. The immediate and pressing need in the taxation field remains,however, for additional taxation during FY 1972. About P 100millionadditional taxation would be necessary merely to offset the automaticreduction in export duties which will go into effect from July 1, 1971.The tax proposals totalling P 269 million to Congress do include amendmentof the Stabilization Tax Law, as well as taxes on luxury consumption, inheri-tance tax, tax on idle lands, revision or repeal of certain tax exemptionlaws, and imposition of fees and taxes on certain forms of gambling afterlegalizing the activity. The tax proposals are generally well conceived butare likely to meet with considerable resistance from Congress in an electionyear.

17. From the viewpoint of both equity and revenue, the maintenance ofexport taxes on most products at least at the 1970-71 level (a range of 8-10percent) deserves a high priority. Considering the large windfall gainsbecoming available to agricultural exporters through the floating exchangerate, the initial export levies certainly did not impose a heavy burden.For most of the export products which were moving through official channels,the export duties were aimed at best at mopping up about one-third of theincrease in export incomes. In fact, the depreciation of the peso throughthe floating exchange rate went further than was perhaps originally envisagedand thus even a smaller portion of the total increase in export income hasbeen captured through export taxes. The improvement in the incomes of theagricultural exporters has probably further increased income disparitiesin the Philippines as real wages have fallen due to a steep rise in theprice level. This in itself is a strong argument for maintaining the levelof export taxation. But even more important should be the long-term con-sideration of using export taxes as a more permanent device to tax agricul-tural incomes which are difficult to tax otherwise. Furthermore, exporttaxes may be an effective instrument of siphoning off large gains resultingfrom sudden increases in international prices of primary products likecopper, logs and copra. There are certain measures other than taxationwhich would also have an important bearing on the availability of publicsector resources for development in the near future. The payments forgratuities, etc. have been rising as Congress has enacted laws increasingpension and retirement benefits while premiums were kept constant. It isimportant that these actuarial deficiencies be remedied through legislation.It may also be stressed that in the past, substantial amounts of government

- 10 -

funds have been.channelled to the private sector, thus reducing the avail-

ability for public investment. It is encouraging to note that the Govern-

ment financial institutions, notably GSIS and SSS which were engaged in

commercial and industrial lending to the private sector in.the past, will

concentrate their new loans on housing as well as on self-liquidating infra-structure projects (NWSA, NPC, etc.). GSIS and SSS together will agke p 300million available for housing purposes in FY 1972 and will take up p. 130million in Government bonds. National Government support torDevelopmentBank of the Philippines for payments, abroad on loans guaranteed by DB? hastaken place in the form of depesits witb, DBP. Thus, DP is required tq repay,eventually tothe Government the amounts made available to it through ear-marking of 25 percent of export duties.

C. Balance of Payments.

Export

18. The major factor in the favorable shift in the balance of paymeptsduring 1970 was the improvement in the trade balance resulting mainly from

a large expansion in exports. Merchandise exports, which had virtually

stagnated between 1966 and 1969, showed an increase of $188 million or 22

percent to $1,043 million in 1970. The rise in total exports, notwithstanding

a decline in logs (the largest single export), was attributable entirely tothe impressive increases in coconut products, copper concentrate, sugar,

fruits and vegetables, and other exports. Though the exchange rate adjust-ment and the rise in export prices contributed significantly to the expapsignin exports, the most important factor was the rise in production of export

products notably sugar, copper and bananas.

Merchandise Exports

UnitPrice Index(1966 = 100)

1966 1967 1968 1969 1970 1970

Copra 157 129 123 87 97 110Coconut oil 75 59 77 51 101 119Other coconut products 35 28 36 25 37 101Sugar (centrifugal) 132 142 144. 149 178 113Abaca 22 17 13 16 17 113Logs 197 207 208 215 208 112Wood products 42 42 54 44 47 98Copper concentrates 75 75 89 133 190 128Tobacco 12 11 16 17 15 74Others 81 111 97 118 153

Total 828 821 857 855 1,043 -

Annual Increase -0.9 4.4 -0.2 22.0

- 11 -

19. Exports of coconut products increased by 41 percent to $235 millionduring 1970, reflecting mainly the doubling of coconut oil exports to $101million. Coconut oil prices showed an average increase over 1969 of 14 per-cent, while copra prices improved by 8 percent. It is noteworthy that exportsof copra plus the copra equivalent of oil showed an increase of 28 percentbetween 1969 and 1970. Only a part of this increase can be explained bythe modest rise in domestic production of copra. It would appear thatperhaps as much as 150,000-200,000 tons of copra exports (valued at $30--35 million) were reverted from unofficial channels to recorded earningsfollowing the devaluation. Earlier estimates of the value of unrecordedexports appear to have been exaggerated, however.

20. Earnings from copper increased by over 40 percent due mainly toincreased volume reflecting the full effect on output of increased invest-ments in mining during the last few years. Copper prices, though very highduring the early part of 1970, continued to fall throughout the year. Theaverage unit value of copper exports during 1970 showed only a slight improve-ment over 1969.

21. The expansion in sugar exports from 980,000 tons in 1969 to1,165,000 tons in 1970 was made possible by the commissioning of nine newsugar mills - first since World War II - in 1969 and 1970 and a parallelexpansion in sugar acreage and was strongly motivated by attempts at fullerutilization of quotas under U.S. Sugar Act of 1965, in view of its renewalthis year.

22. Other exports showed an increase of 30 percent during 1970.While minor manufactured goods rose following the exchange rate adjustment,the full impact of the exchange reform and Export Incentives Act on theseexports will probably be felt in 1971 and succeeding years.

23. The export performance of forest products was somewhat disappoint-ing. The output and export of logs were adversely affected by typhoons andsubsequent power failures, and slackness of international demand. Meanwhile,the plywood and wood product exports continued to be hampered by high costs.

Imports

24. According to preliminary estimates, imports recorded a decline ofnearly 4 percent during 1970. Though the breakdown of imports given belowis not precise, it does seem that the reduction in imports was confinedmainly to capital goods and consumer goods imports, and intermediate goodsimports did!not decline.

Imports(In US dollars, calendar years)

1966 1967 1968 1969 1970

Consumption 161 204 185 172 144Capital 297 407 444 444 401Intermediate 397 450 521 515 545

Total 855 1,061 1,150 1,131 1,090

- 12 -

25. On the whole, it seems that availability of raw materials wasnot a serious constraint on industrial growth during 1970 and that importliberalization in respect of most intermediate products had proceededsmoothly. Import restrictions on certain 1/ categories of goods, however,continued and it was significant that despite some quantitative restrictions,the decline in imports of 10 percent during 1969/70 projected by the Planhad not materialized. This further confirms the belief expressed in thelast Economic Report that the Plan projection visualizing only a 5 percentannual growth in imports between 1969/70 and 1973/74 was unrealistic.

Invisibles

26. The invisibles balance on account of services and transfer pay-ments deteriorated from a surplus of $22 million in 1969 to a deficit ofthe same order in 1970. The deterioration was attributable almost entirelyto higher interest payments on foreign debt which jumped by $57 million,from $38 million in 1969 to $95 million in 1970. The receipts on accountof Japanese reparations during 1970 were also $20 million smaller than inthe previous year. On the other hand, receipts from travel improved veryconsiderably due to the exchange rate adjustment, which attracted back intoofficial channels a large part of tourist expenditures. At the same time,travel expenditures abroad were cut back sharply as restrictions.tweretightened on travel.

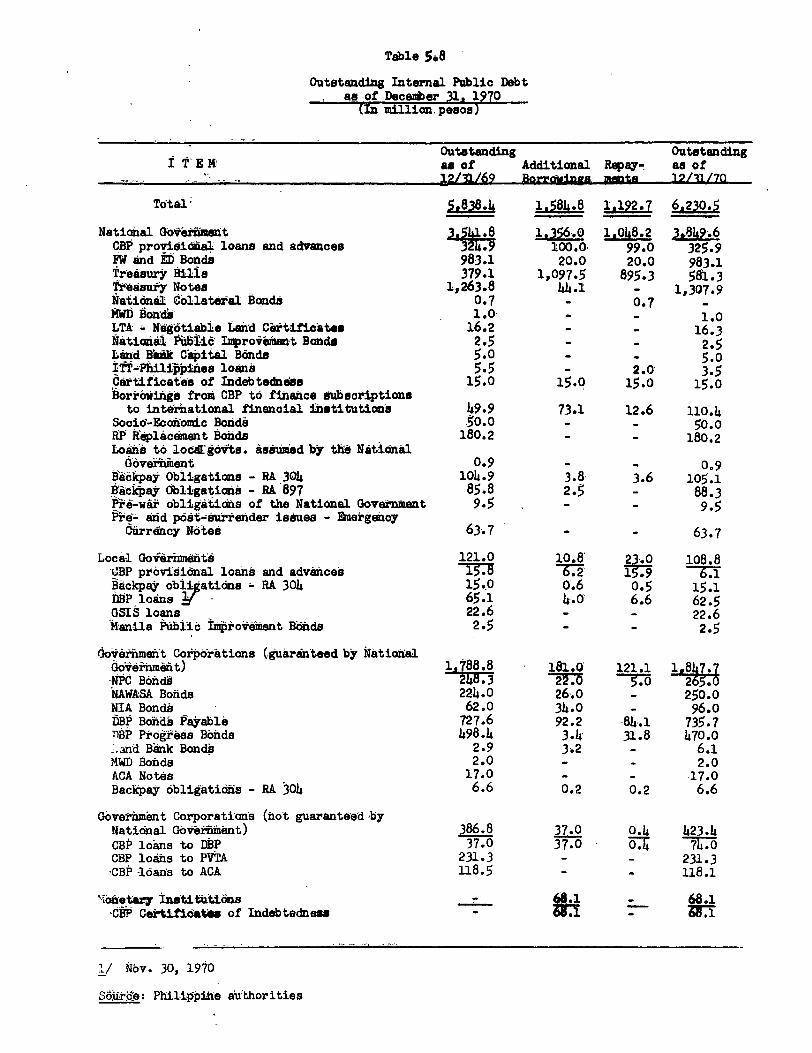

Foreign Debts

27. Despite the current account deficit, international reserves 2/increased by $111 million during 1970 to $236.6 million. The increase inforeign exchange reserves and the financing of.the current account was madepossible mainly by an estimated net increase in total foreign debt (excludingdues to IMF and short-term liabilities except those of the Central Bank) of$228 million. The first allotment of SDRs, and net IMF assistance amountedto $18 million and $14 million respectively during 1970. The overall netincrease in foreign debt during 1970 obscures the very high debt repaymentsof $373 million effected during the year. As shown by the table below,availabilities of $601 million were necessary in order to bring about the netincrease of $228 million in debt. The short-term availments of the CentralBank were largely offset by short-term repayments (excluding debt restructuring);$80 million of short-term debt was contracted and repaid within the year.But the medium- and long-term gross private borrowing at $332 million farexceeded the corresponding repayments of $187 million. Nearly three-fourthsof the net increase in outstanding debt was thus attributable to the privatesector. The details of this debt are now known, but a large part of it isin the form of suppliers' credit.

1/ The opening of letters of credit for three categories of imports is notpermitted. These categories accounted for about 5 percent of totalimports in 1068. It is not readily possible to estimate the relativeshare of other imports which are subject to restrictions.

2/ As defined by the Philippine Authorities: gross reserves of the CentralBank plus net reserves of commercial banks. The IMF definition of netreserves normally includes the foreign exchange liabilities;of CentralBank of less than 12 months' original maturity.

- 13 -

Availabilities and Repayments of/aForeign Credits and Loans in 1970--

Availabilities Repayments Net Availabilities

Short Term 140 109 31Public 140 109 31

Of which: Central Bank 140 109 31Other - - -

Medium Term 209 179 30Public 52 56 _4

Of which: Central Bank 40 13 27Other 12 43 -31

Private 157 123 34

Long Term 252 85 167Public 78 21 60

Of which: Central Bank - - -Other 78 21 60

Private 175 64 108

TOTAL 601 373 228

/a These exclude debt rescheduling in 1970: short term -- $143 millionUS bank credits (into long-term.debt) and $22 million European bankscredits (into medium-term debt); and medium term -- $58 million USbank credits (into long-term debt). The foreign debt excludes amountsdue to the IMF and short-term liabilities other than that of theCentral Bank.

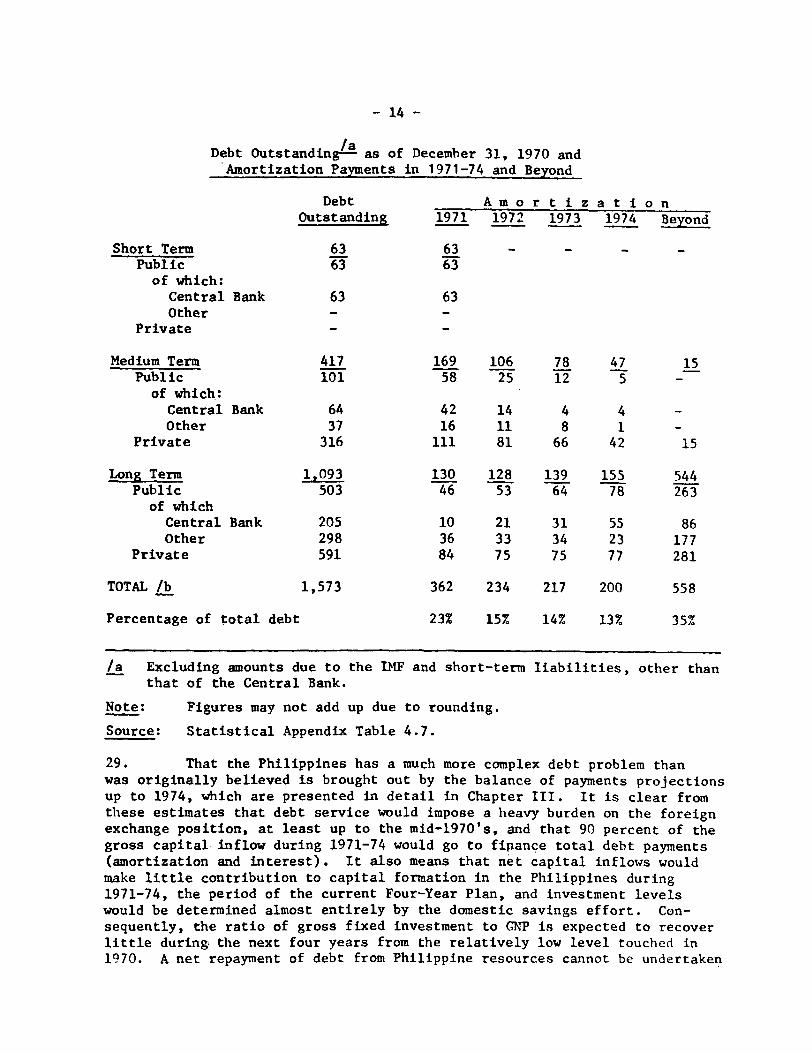

28. The total debt outstanding increased from $1,344 million at theend of 1969 to $1,573 million at the end of 1970. Despite a substantialincrease in total debt, the short-term debt with a maturity of up to oneyear dropped sharply from $196.4 million from the end of 1969 to $62.8million at the end of 1970. This reduction in short-term liabilities wasmade possible by the refunding of over $220 million of Central Bankobligations into longer-term loans. Nevertheless, the structure ofPhilippines' debt continues to be a matter of serious concern. While thetotal volume of external debt is not much higher than one year's grossforeign exchange earnings, 23 percent of the debt is payable in 1971 andnearly two-thirds must be paid within the next four years. The amortizationpayments of $362 million along with the estimated interest payments of $141million would mean a total debt service of $503 million during 1971, whichwould be larger than the debt service of $468 million in 1970. The ratioof debt service to total foreign exchange earnings during 1971 will remainunchanged at 32.8 percent, the 1970 level.

- 14 -

laDebt Outstanding- as of December 31, 1970 and

Amortization Payments in 1971-74 and Beyond

Debt Amorti zationOutstanding 1971 1972 1973 1974 Beyond

Short Term 63 63 - - - -Public 63 63of which:

Central Bank 63 63Other - -

Private - -

Medium Term 417 169 106 78 47 15Public 101 58 25 12 5 -

of which:Central Bank 64 42 14 4 4 -Other 37 16 11 8 1 -

Private 316 111 81 66 42 15

Long Term 1,093 130 128 139 155 544Public 503 46 53 64 78 263

of whichCentral Bank 205 10 21 31 55 86Other 298 36 33 34 23 177

Private 591 84 75 75 77 281

TOTAL l 1,573 362 234 217 200 558

Percentage of total debt 23% 15% 14% 13% 35%

/a Excluding amounts due to the MF and short-term liabilities, other thanthat of the Central Bank.

Note: Figures may not add up due to rounding.

Source: Statistical Appendix Table 4.7.

29. That the Philippines has a much more complex debt problem thanwas originally believed is brought out by the balance of payments projectionsup to 1974, which are presented in detail in Chapter III. It is clear fromthese estimates that debt service would impose a heavy burden on the foreignexchange position, at least up to the mid-1970's, and that 90 percent of thegross capital inflow during 1971-74 would go to fipance total debt payments(amortization and interest). It also means that net capital inflows wouldmake little contribution to capital formation in the Philippines during1971-74, the period of the current Four-Year Plan, and investment levelswould be determined almost entirely by the domestic savings effort. Con-sequently, the ratio of gross fixed investment to GNP is expected to recoverlittle during the next four years from the relatively low level touched in1970. A net repayment of debt from Philippine resources cannot be undertaken

- 15 -

without further reducing the level of investment and economic activity, whichwould in turn seriously jeopardize the prospects of long-term growth of out-put and exports. To stress the point that the large demand on resources toservice external debt may hamper the pace of development activity in thenear future, is merely to emphasize that gross capital requirements projectedby the Mission are in a sense a minimum.

30. The terms on which external capital becomes available to thePhilippines during the next four years will also be crucial. Unless thePhilippines obtains a larger inflow of longer-term capital on more favorableterms and with adequate grace periods, she will not be able to substitutelong term for medium and short term debt, and the debt service ratio willremain very high. With an average maturity of new debt of eight years butwith no grace periods, the debt service will stay close to 30 percent evenby 1974. Such a position, though not inconsistent with the creditworthinessof the Philippines, would pose an immense foreign exchange management prob-lem. It might also force the Philippine planners and financial leadershipto take a very short-term view of both balance of payments and growth. Thisunderlines the need for long term more liberal assistance to the publicsector, particularly in the form of commodity loans or quickly disbursingproject aid.

D. Money and Credit

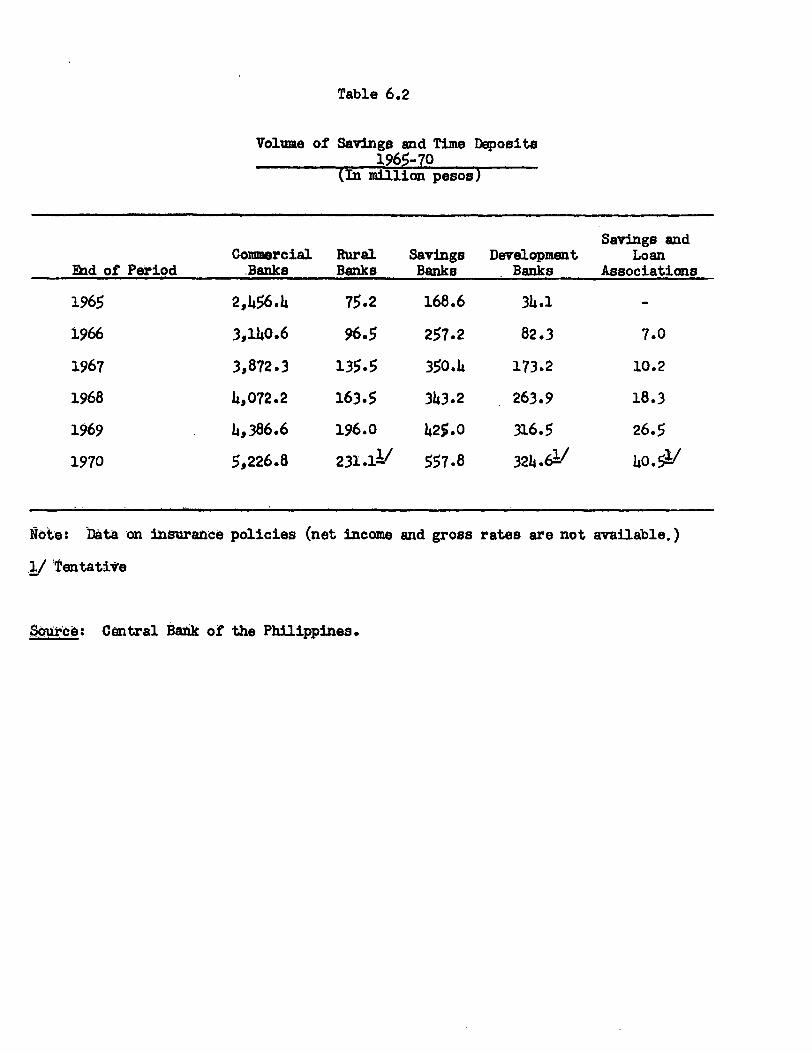

31. As a result of stringent fiscal and monetary policies, themonetary authorities managed to contain the rate of growth of money supplyin 1970 to 6.2 percent, compared with the unprecedented increase of 19.4percent in 1969. Particularly sharp was the curtailment of advances tothe public sector, which rose by a net P 46 million, or 1 percent, in greatcontrast to P 1,244 million, or 40 percent, in the preceding year. Creditto the private sector

Factors Affecting Changes in Money Supply(In million pesos)

1967 1968 1969 1970

Credit to Private Sector +904 +718 +310 +1,173

Credit to Public Sector, Net +793 +283 +1,244 + 46

Private Time and Savings Deposits -752 -690 -123 - 811

Foreign Sector -390 - 98 -497 + 321

Miscellaneous Accounts of Privateand Government Banks -145 - 13 -162 - 436

Net Change in Money Supply +410 +200 +772 + 293

In Percent 12.2 5.0 19.4 6.2

Source: Statistical Appendix, Table 6.1

- 16 -

and the transactions of the foreign sector were the main sourceh of monetaryexpansion. On the other hand, the substantial increase in time!and savingsdeposits by P'811 million, or by 18.5 percent, and in the non-d;epositliabilities of the banking ,system 1/by another P 436 million., exerted a sig-nificant ,contractive .effect, and reduced the net increase in money supplyto P 293 million.

32. Although credit to the private ,sector rose by 16 percent, theincrease in the manufacturing sector was only 3.4 percent .and was not suffi-cient to satisfy the increased needs of business firms for working capitalarising from the upward adjustment of the prices of all inputs,, includinglabor., and the higher peso requirements to service foreign obligations inforeign currencies and to meet increased margin deposits on opening importletters of cr'edit. Though exact figures are not available, most of theincrease in credit was probably directed towards financing increased pesorequirement in foreign trade sector.

33. To mobilize a greater volume of savings through the banking system,a bill has been introduced to raise maximum rates of interest.. 'The presentinterest rate structure certainly .does not reflect the relative':'scarcity ofcapital; .the real yield was actually negative during 1970. Commercial bankswere able to attract floating savings through non-deposit instruments ofindebtedness at interest rates much higher than the official deposit rates,and to relend at a premium through the method of compensating balances.Also, the sale of foreign exchange to the Central Bank by the commercialbanks under swap arrangements to improve their liquidity was an -importantcontributory factor to the sexpansion .of private credit.

34. The-Philippines entered into a new Standby arrangement with theIMF for another year and in the amount of .$45 million.. The main objectivesof the arrangement for 1971 are to continue the policy of monetary andfiscal restraint, to curb the rate of price increases and to maintain-theimprovement in the balance of payments.. In the domain of fiscal policy,cash expenditures will continue to be limited to the available resources.In the monetary sphere, the net domestic assets of the Central Bank will notbe allowed to increase by more than P 175 million through August'1971. Thismargin is subject to adjustment by,the peso equivalent of the changes inthe net foreign assets of the commercial banks. To increase the 'liquidityof the commercial banks, it is intended to reduce the reserve requirementby 2 percentage points, although by no more than 1 percent prior toAugust. The measures outlined are expected ro permit bank ,credit to expand

by 10-12 percent, which is viewed as consistent with a 5.5 percent growthof GNP and a modezt increase in prices.

1/ They include margin deposits against letters of credit, trust certi-ficates, trading accounts of the Central Bank and the Government banks,inter-bank transactions, and other accounts.

- 17 -

Prices and Wages

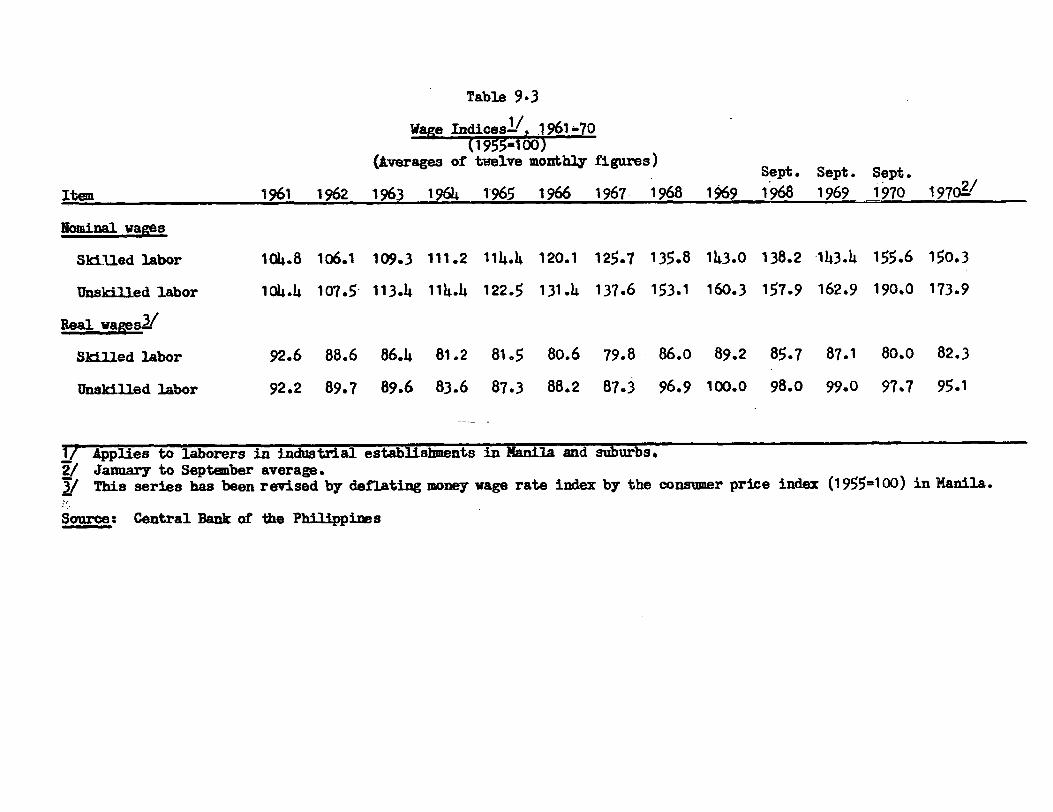

35. In the year ending December 1970, consumer and wholesale pricesrose by 21 percent. The food shortage following the damage caused by thetyphoons in the latter part of 1970 reinforced the upward price movement.A minimum wage law was enacted raising the minimum for non-agriculturalworkers from P 6 to P 8 per day, and for farm workers from P 3.50 to P 4.75.However, only a fraction of the labor force is covered by the law while inmany instances the law, cannot be enforced. As a result, real wages ofskilled and unskilled workers declined by about 9 and 6 percent, respectively,during the first 9 months of 1970.

E. Growth Prospects

36. The discussion in the preceding sections of the debt problem andshortage of resources for public sector development suggests that the majorconstraints on Philippine growth in the near future are likely to be finan-cial. The major limitations on development activity would arise from in-sufficient availability of foreign assistance on more liberal terms andinadequate mobilization of tax revenues, though lags in project preparationmight also serve to restrict,the absorptive capacity of long term assistancein the public sector.

37. Assuming that the gross capital inflow requirements of $560million per annum during 1971-74 can be met by assistance at suitable termswhich gives reasonable relief from short-term debt burden, the deficit ongoods and non-factor services account would remain during 1974 at less thanone percent of GNP, about the same level as in 1970. Assuming a marginalsaving rate of 20 percent during 1970-74, substantially higher than thepresent average of 17 percent, the investment ratio would improve onlyslightly over the period. For the period 1971-74 as a whole, fixed invest-ment as a ratio of GNP may average around 17.5 percent compared with thePlan projection of 19.5 percent.

38. This rather disappointing prospect for investment causes concernfor the long term growth of the Philippines, particularly so because theaverage growth rate of 5.5 percent per annum during 1963-70 cannot beconsidered high in the light of the country's resources and economic poten-tial. The Philippines has large resources in the form of agricultural land,mineral deposits, and above all, a level of literacy and general educationalmost unique in South East Asia, which partly accounts for, and certainlymade possible, a dynamic native enterpreneurial class. Awareness of businessopportunities and willingness to take risk for profit is widespread amongthe population, and material advancement ranks high among personal and socialvalues.

39. Fortunately the impact of slow rise in investment on growth inthe immediate future would be cushioned by a set of favorable factors andthus it might be possible to keep the overall growth rate above 5 percent

- 18 -

per annum during 1970-74 as against the Plan target of 5.6 percent. Firstly,the output trends will continue to benefit from the relatively high rate ofinvestment during FY 1965-69. Secondly, closely related'to past investmentin key sectors such as mining, the outlook for exports remains good.The export sector, which currently accounts for nearly 18 percent of GNP,should grow by about 8 percent per annum after allowing for some reductionin export prices. Thirdly, the possibilities of spreading technologicalchange in agriculture are by no means exhausted. Despite the damage fromtyphoons during 1970, the agricultural growth has averaged over 6.1 percentper annum during 1967-70, and current signs augur well for continuedvigorous growth in agriculture provided a realistic policy framework isestablished, the right financial support and priorities are chosen and poli-tical goodwill is forthcoming from Congress. Finally, even though industrialgrowth continues to suffer from excess capacity and overcrowding in manyindustries, the exchange rate adjustment has created a favorable climate forrationalization efforts by opening up possibilities of exports. Meanwhile,because of the financial squeeze on industries, the leverage of the Devel-opment Bank of the Philippines over the private sector has increased. TheBoard of Investments, which controls and supervises all new investments,is cognizant of the shortcomings of past policies and appears determinedto reorient industrial policies specially towards export promotion and tothis end a basic reform of the existing tariff system is planned. The majorproblems in agriculture, industry and other key sectors are discussed insomewhat greater detail in the next chapter. The National Economic Councilis now engaged in preparing a 20-year Perspective Plan for the Philippines.This exercise would be useful in highlighting the long term possibilities

of.growth. It .is clear, however, that if the Philippines is to achieve a

sustained growth rate of around 6 percent per annum, it cannot go on very

long with a low investment level, which is all that it is possible to

afford with resources currently available or in prospect in the near future.

Before long, -the fixed investment rate will have to be raised to 20 percent

or more as a prerequisite to a more rapid growth pattern and a larger

measure of social development, which should be possible in the second half

of the seventies. This will require a major resource effort both domestic

and foreign. The growth outlook beyond 1974 would also depend much on how

satisfactorily the approach towards the elimination in 1974 of special U.S.

privileges in the Philippines will be handled;by both parties.

- 19 -

CHAPTER II

Sectoral Developments and Issues

A. Agriculture

40. During the last few years, the agricultural sector has grown,

on average, more rapidly than the GNP. The Four-Year Development Plan

(FY 1971-74) expects this trend to continue; with an average annual agricul-ture growth rate of 6.1 percent, the share of agriculture in Net Domestic

Product would increase further to 35.1 percent by FY 1974. The present

emphasis on agricultural development is well placed since yields per hectare

are still quite low and the possibilities of spreading technological change

are by no means exhausted. It would seem, however, that in order to faci-

litate high agricultural growth rates, there is a need at this juncture to

change the emphasis of agricultural policy away from rice to other crops and

livestock enterprises. The most remarkable feature of Philippine agriculture

at this stage is the fact that the country has achieved self-sufficiency inrice ahead of the Plan despite adverse weather conditions in 1969 and

1970 1/. The very rapid expansion in high-yielding varieties of rice, the

greater use of fertilizer and irrigation water accounts for the sharp in-crease in paddy 2/ production from 4.0 million tons in 1967 to 5.3 million

tons in 1970, despite adverse weather conditions. The breakthrough in rice

has given a new impetus to the development and expansion of the agricultural

sector. The farmers have gained confidence in the efforts of the government

and have enjoyed the profits of expanded production. However, it is at

this crucial juncture that appropriate measures are needed to avoid market

disequilibrium, to maintain stable prices for rice, and shift to resources

as necessary from rice to other crops through price incentives and thus

provide new opportunities for the farmers.

41. Prima facie, it appears doubtful that further expansion of rice

production for exports would be in the best economic interest of the country.

Over-all yields per hectare are still quite low by international standardsand the quality of rice does not seem to be suitable for export. The further

increases in rice production might, thus, have to be limited to the rate of

population growth since the income elasticity of demand for rice in the

Philippines is reportedly very low. This would mean a growth rate of rice

production of 3.5-4.0 percent per annum compared with 6.5 percent growth

in the Plan.

1/ Typhoons in 1970 were the worst on record. They reduced the value of

agricultural output a hundred million pesos and the two crops hardest

hit were palay and coconuts, though the immediate production of coconut

rose due to falling of unripe nuts.

2/ Palay.

- 20 -

42. A new and young group of technocrats now heading the agriculturalsecretariat is fully aware of the need to bring about a shift in Agriculturalstrategy. The specific objectives of the agricultural program are beingreviewed and the targets and implementation plans for 197174 are likelyto undergo considerable change. While maintaining self-sufficiency in fice,priorities ate to be given to (1) expansion of livestock and poultry asimport substitution, (2) crop diversification to feedgrains, suh as yellowcorn, sotghum and soya beans, to support the production of livestock andpoultry, and (3) the development of fisheries both for meeting dodlesticdemabd and exports.

43. fho h&w prioriti6s appear to be reasonable. But the tepercussionsof a thange in Agricultural policy have not been fully worked out not aretheir implications fully understood at present. For etample the irrigatiftpolicy stillbeOs to be too tibsely tied to an expansioh i rice production.The Governielt is, heWever, cohdidering the use of some of the itrigationwater from the Upper -fpang Project for crops other thAn rice. If, Asefs probable, inrased emphasis will be give6 to sorghum and btht feedgrains in th future, thd need fot ittigAti6n for these rops it 1es@ ald amoti aggressive water development poliy to reduce the t6st of sugst Pto=duction mAy well be more televat over the nekt five years thaftih the paddyareas. At :ptebent only 5-7 percent of area undetr sugar is iftigated aid asubstantial Iiidrease it yields could be realized by further itfigati6. Thtneed for inct0asing productivity and 16V#ting dostn of sugatchr Alto aribifroi the unctainties 4bout the V8 sugar quota for the hilippii Ad itis impdrative that the sugak industry reduces its vulnerability.

44. The p,ossiblity of agridultUrai retional speciAliatih it 4ioworth exaininttg. Yor Inta&t, it hat bten 6taed that h th weni paftof the PhilipPIhes is less suscdpt-ible to typhbn as 6p-i-rd tb the tentraland Northern sketions. Thttffot, epasion of coconut pihtAtf6nM in theSouth would Veduce the risk of typban damage considerably. biftili p6ai-bilities of dgional specialization &rk worth ifooking idt6 fot 'th'd dbiAlpmeat of liittAck and feedgrains, based upon tegional compaattI# advatagsThis assumes, however, that tht6iih legislative changes or dhafes in theinterpretatod of law, it would'b6dot possible to estAblish the 1siting ofslaughterhou§es Jn a b6fe tatibha 'basis.

4. A great deal more atteltii is required in the fil- 16f exportcrops. Cotbdt produti and tfotot ptoducts, which togethef Atduit -to?heatly half of tbtal expobts, have siffteted ftm hiedglet and a laek ofclear directib in Government 'pbltis. There is no natidnal 'Pr6gram forexpansion abld Ykhibilitation bf tobOut production. The yields have beendeclining be ckuse of insufficient fertilizer use and inadequate rejuvenat1ngof old plantations (except in the South in the early sixties). Furtherm6te,the existing 'tdit is mainly short term, while coconut growerd heed mediumand long-tetm Itedit. Since the Philippines enjoys about 48 percentof the wotld's toconut market and 1i1te domestic prices of cocfut oil maycome under pt&sure due to interMtional competition from palm oIl and su'cce§-

sive increasa in rates of the U.S. bhport duty on supply f6m 'the Philip-pihes, greabtr efforts inciuding CIhd& for research are requif@4 ,t6 imp6%k

- 21 -

productivity. Also urger.t in the rationalization of the forestry and woodindustries beginning with a redefinition of the whole forestry managementpolicies of the Government in the context of a land-natural resource conser-vation and development strategy and the need to find a balance exporting logsand processed wood products. The latter should include a re-examination ofthe Government's pricing and tax policies for the use of natural resourcesin the light of the need to induce greater utilization of major and minorforest products, minimization of forest wastes and greater processing offorest materials prior to export sale.

46. The two closely related problem areas, which continue to hinderprogress in agriculture especially towards more even income distribution,are agricultural credit and land reform. The Philippines land reform whichwas initiated under the Agricultural Land Reform Code of 1963 has made verylittle headway. The intent was to replace sharecropping with a leaseholdingsystem in the first stage and to fix lease rent at 25 percent of the averagenormal harvest during the prpceding three crop years, after subtractingcosts. The second stage was to convert leaseholders into landowners bypaying the owners of the land full compensation through the Land Bank. Afterseveral years, only 30 percent of the area involved has been transferred toleaseholders as against the target of 75 percent; actual acquisition of landand transfer of ownership rights to tenants has been negligible. Even thesharecropping tenants who became leaseholders have been forced to relyheavily on the landlords for their credit needs because of inadequate alter-native facilities. Thus the effective rents may not have changed at all.Meanwhile the spread of improved technology specially in rice has greatlyincreased absolute rents and, therefore, enhanced the value of land whichthe tenants would ultimately have to pay. Indeed the interest of landlordsin increasing the productivity and thus the value of land has been reportedlyan important factor in the rapid spread of the green revolution in thePhilippines. But as a consequence, income or at least wealth disparities inagriculture have certainly increased. A large number of cases of evictionof tenants have also been reported as landlords have been able to make useof the self-cultivation clauses of the Land Reform Code. There is generalagreement that there is need to increase allocations for the land reformprogram and to simplify procedures in meaningful progress is to be made. Abill proposing amendments to the Land Reform Act is now before Congress and islikely to be passed. This provides for the elimination of the provision forevictions for self-cultivation and also proposes to reduce the ceiling oflandholdings, to be tackled on priority basis, from 75 acres to 25 acres.Also, it proposes to extend the first stage of leaseholding to the wholecountry. The financial requirements of land reform, as presently visualized,however, remain very large and, therefore, real progress is likely to beslow.

B. Manufacturing

47. A major weakness of the Philippine economy during the sixtieshas been the slow growth of the manufacturing sector; the share of manu-facturing in the NDP fell from 18.9 percent in 1960 to 16.7 percent in 1970.

- 22 -

The limited expansion of industry during the last several years is attributedto the excessive reliance on import substitution during the 1950's Histo-rically, the maintenance of an overvalued exchange rate in combinatioh witha control program which permitted cheap imports of cApitAl gbods, restrictedthe imports of finished goods and therefore ensured a shAlttred domesticmarket and high profits for Philippine manufactures. This resulted inspectacular gains in industrial output for some time, but th6 p6§§ibilite@for easy import substitution were soon exhausted. The tariff system whithreplaced direct controls in early 1960's established low rates fo machinery,moderate rates for intermediate goods and raw materials and high rates forfinished consumer goods, and thus again encouraged ftishing stage activitieswhich were heavily dependent on imported supplies. Backwad ihtegratioi addexport-oriented undertakings remained less profitable because 6f the dis-incentives the protective system set against them. Given the liiited siidof the domestic market, many industries had to operate Ata sub;6pitfad Rcalefollowing the Government's attempt to ensure competitioh &ffrfhavingestablished high tariffs, by granting incentives to sevei ptddudefiCheap capital and easy Availment of foreign exchange further promotedexcess capacity. Protection also enabled inefficient tndertakIdiia o Uft=economic size to survive. In short, the end result of the pf6tbativ6 p6lieie§of the past, reinforced by unrealistically low intetest rates, hsa boan thadevelopment of excess capacity, inefficient productiod and a dioV-doUf inindustrial growth.

48. Cognizant of the shortcomings of past polidi&sj thd 9iift@itappears determined to reorient its industrial policy. the exehdhge fateadjustment has indeed created a favorable climate fo the etksieturtig 6findustry by improving the prospects of manufactured goods 6kp6rta.

49. The Board of Investments (bOi) is f0e6ndible f6f 0-iififig thaiavailable financial resources and foreign exchange are allocated fi accord-ance with set development priorities. The Foith Investment Mdfitied ian(IPP) for the Fiscal Years 1912-75 gives distinct priority to ifidUsti#with export orientation, producing capitai godda and resu1ting iii backwardlinkages and further procesding of Orimary productsi