results presentation jan- sep 2015 - isolux corsan€¦ · document contains statements related to...

TRANSCRIPT

Results Presentation

Jan- Sep 2015 November 25th, 2015

November 25th 2015 | 2

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Disclaimer

This document has been prepared by Grupo Isolux Corsán, S.A.; therefore no part of it may be published, disclosed or distributed in any form or by any means, nor used by any other person or entity, without the prior written consent of Grupo Isolux Corsán, S.A. This document contains statements related to our future business and financial performance and future events or developments involving us that may constitute forward-looking statements. These statements may be identified by words such as “expects,” “looks forward to,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “will,” “project” or words of similar meaning. We may also make forward-looking statements in other reports, in presentations, in material delivered to shareholders and in press releases. In addition, our representatives may from time to time make oral forward-looking statements. Such forward-looking statements and information are based on the current expectations and assumptions, and are, therefore, subject to certain risks and uncertainties. A variety of factors, which are beyond our control or may be difficult to predict, affect our operations, performance, business strategy and results and could cause our actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements or anticipated on the basis of historical trends. Should one or more risks or uncertainties materialize, or should underlying assumptions prove incorrect, our actual results, performance or achievements may vary materially from those described in the relevant forward-looking statement as being expected, anticipated, intended, planned, believed, sought, estimated or projected. We neither intend, nor assume any obligation, to publicly update or revise these forward-looking statements in light of developments which differ from those anticipated. The information contained in this document has not been verified or revised by the auditors of Grupo Isolux Corsán, S.A. Certain data included in this presentation has been subject to rounding adjustments. Accordingly, in certain instances, the sum of the numbers in a column or a row in tables may not conform exactly to the total figure given for that column or row. This document does not constitute or form part of any offer for sale or subscription of or solicitation or invitation of any offer to buy or subscribe for any securities in any jurisdiction, including in the United States, nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever. Specifically, this presentation does not constitute a “prospectus” within the meaning of the Securities Act.

November 25th 2015 | 3

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Results Presentation Q3 2015 | Table of Contents

Table of Contents 1. Key Developments

2. Business and Financial Highlights

i. EPC

ii. Concessions

3. Cash flow and debt overview

4. Appendix

November 25th 2015 | 4

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

1. Key Developments

November 25th 2015 | 5

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Results Presentation Q3 2015 | Key Developments

Group

Financials

Q3 YTD 2015 consolidated Revenues reached €1,580 million.

Q3 YTD 2015 consolidated EBITDA: €115 million. EBITDA includes non-recurring losses coming from Brazil where macro environment led to a significant

slowdown in collections, resulting in project cancellations. This effect represents €34 million of negative EBITDA.

Q3 YTD 2015 Net loss of €20 million vs. a loss of €17 million in the same period last year, driven by a larger share of profit from the equity accounted business which helped offset the decline in EBITDA.

EPC

EPC backlog at €7.0 billion (5% Y-o-Y increase).

New orders in the first nine months of 2015 amounted to €1,798 million.

Main contracts awarded in Q3 2015: Transmission lines between Kenya and Ethiopia in joint venture with Siemens (€170 million). Solar plant in Chile (€124m). Transmission lines and substations in US (€48 million).

Concessions

Two new transmission line concessions awarded in Brazil, in the states of Pará and Rondônia, which are part of the package to be sold.

Japan solar plant already under construction after securing long term financing.

November 25th 2015 | 6

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Results Presentation Q3 2015 | Key Developments

Corporate

Isolux Infrastructure (IIN) break up process:

Isolux and PSP entered into an agreement dated March 31, 2015, related to the dissolution of the joint venture (Isolux Infrastructure) by splitting the company's business between them, in such manner that Isolux shall become the sole owner of electric transmission lines and solar photovoltaic assets (Energy Business) excluding WETT transmission line and PSP shall become the sole owner of toll roads and WETT.

An independent third party was appointed to determine, among others, the equity split and the adjustment payment.

Third party expert determination report was received on September 4, 2015, concluding that PSP owes

$197.5 million to Isolux (corresponding from a total amount of $302.5 million of which $105 million have already been paid) to be adjusted with post-effective date leakages.

November 25th 2015 | 7

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Results Presentation Q3 2015 | Key Developments

Corporate

Upon break up completion Isolux will become the sole owner of IIN Energy Business (ex WETT).

Different offers to acquire our transmission lines and solar business are under analysis.

CASH: $302.5 million (of which $105 million have already been paid)

88%

IIN Energy Business (Isolux 100%)

100%

50% IENNE – Interligação

100% LXTE - Xingu

100% LMTE – Macapá

CPTE - Cachoeira Paulista 100%

JTE – Jaurú 33%

Brazil

Uttar Pradesh 100%

India

161 MW 51%

Spain

7 MW 51%

Italy

44 MW 51%

Peru

Transmission Lines Solar PV

17 MW 50%

India

LTTE – Taubate 100%

LITE - Itacaiunas 100%

25 MW 100%

US

35 MW 100%

Japan

30 MW 100%

Puerto Rico

November 25th 2015 | 8

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Results Presentation Q3 2015 | Key Developments

Isolux Corsán Group Key metrics by segment (in € MM, unless otherwise stated)

Q3 YTD 2014

Q3 YTD 2015

Change

EPC 1,541 1,561 1%

Subtotal (before IFRS 11) 2,009 2,232 11%

Concessions 447 653 46%

Other and corporate 21 18 (15%)

Adjustments due to change in consolidation method(1) (460) (652) -

REVENUES

Total Consolidated 1,549 1,580 2%

Q3 YTD 2014

Q3 YTD 2015

Change

203 148 (27%)

452 491 9%

267 375 40%

(18) (32) -

(266) (376) -

EBITDA

186 115 (38%)

Q3 YTD 2014

13%

23%

60%

n.a.

n.a.

EBITDA Margin

12%

Q3 YTD 2015

9%

22%

58%

n.a.

n.a.

7%

(1) Equity method consolidation of Isolux Infrastructure and the Car park business

One off losses in Brazil, driven by country macro environment, compressed EPC EBITDA margin

November 25th 2015 | 9

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Results Presentation Q3 2015 | Key Developments

Isolux Corsán Group Debt breakdown by segment (in € MM, unless otherwise stated)

Sep 30, 2015

Dec 31, 2014

EPC 170 158

Subtotal (before IFRS 11) 1,599 1,548

Concessions 7 8

Corporate and other 1,422 1,382

Adjustments due to change in consolidation method(1) - -

Bank borrowings and Senior Notes

Total Consolidated 1,599 1,548

Sep 30, 2015

Dec 31, 2014

-

3,424

3,263

160

(3,173)

Project Finance(2)

250

Sep 30, 2015

Dec 31, 2014

177 248

480 631

296 339

7 45

(292) (325)

Cash and STFI

188 306

-

3,464

3,308

156

(3,243)

221

(1) Equity method consolidation of Isolux Infrastructure and the Car park business (2) Guarantees given from Grupo Isolux Corsán to Isolux Infrastructure to finance projects amounted to €171M as of December 31, 2014 and €124M as of September 30, 2015.

Estimated adjusted payment inflow ($197.5 million) to be received after Q3 2015

November 25th 2015 | 10

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

(93)

(57)

(18)

162

(33)

(24)

(49)

123

(-26)

(74) (59)

2013 2014 2015

Q1 Q2 Q3 Q4

Results Presentation Q3 2015 | Key Developments

Cash flow from operating activities: seasonality

Negative cash flow from operations driven by working capital outflow in line with seasonal patterns

*2015 dotted line to illustrate customary seasonal trend

*

November 25th 2015 | 11

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Results Presentation Q3 2015 | Key Developments

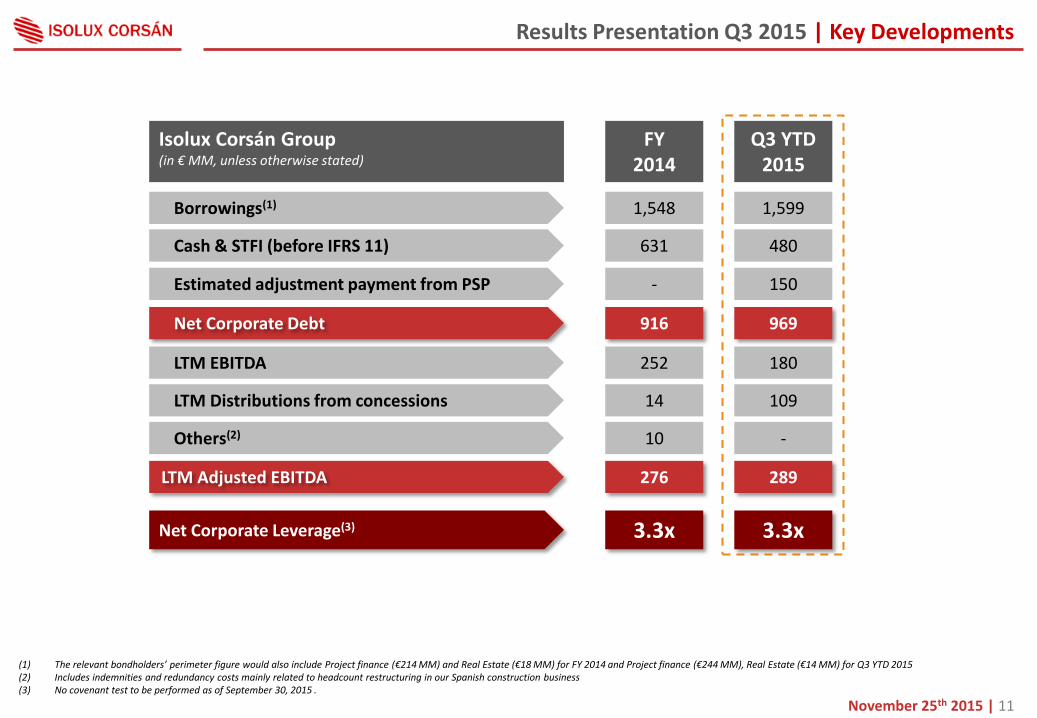

FY 2014

Q3 YTD 2015

Borrowings(1) 1,548 1,599

Cash & STFI (before IFRS 11) 631 480

Net Corporate Debt 916 969

LTM EBITDA 252 180

LTM Distributions from concessions 14 109

LTM Adjusted EBITDA 276 289

Net Corporate Leverage(3) 3.3x 3.3x

(1) The relevant bondholders’ perimeter figure would also include Project finance (€214 MM) and Real Estate (€18 MM) for FY 2014 and Project finance (€244 MM), Real Estate (€14 MM) for Q3 YTD 2015 (2) Includes indemnities and redundancy costs mainly related to headcount restructuring in our Spanish construction business (3) No covenant test to be performed as of September 30, 2015 .

Isolux Corsán Group (in € MM, unless otherwise stated)

Others(2) 10 -

Estimated adjustment payment from PSP - 150

November 25th 2015 | 12

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

2. Business and Financial Highlights

i. EPC

November 25th 2015 | 13

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

(1) Defined as New Orders / Revenue (2) From consolidated Cash Flow Statement which is a proxy to EPC & Other business segments.

EPC (in € MM, unless otherwise stated)

Q3 YTD 2014

Q3 YTD 2015

Change

New Orders

Backlog

Backlog for 3rd parties

2,223 1,798 (19%)

6,626 6,969 5%

80% 83% 3 p.p.

Revenue 1,541 1,561 1%

Book to bill ratio(1) 1.4x 1.2x (0.2x)

EBITDA 203 148 (27%)

EBITDA Margin 13% 9% (4 p.p.)

Operating Cash Flow(2) (49) (59) (20%)

Cash Flow from Investments(2) (24) 62 -

Robust backlog represents almost 3 years of activity

Results Presentation Q3 2015 | Business and Financial Highlights

November 25th 2015 | 14

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

2,223

1,798

9m 2014 9m 2015

EPC - Key Financial Highlights

Key Figures EPC Segment (in € MM) Main developments

Brazil impacted not only EBITDA, but, in terms of revenues, has almost no contribution.

Senegal road: 2 out of 3 segments have been completed and the client has issued provisional acceptance certificate.

New orders awarded in Q3 in the US which is a target market for the Group:

Contract with MidAmerican Energy for several T&D works in high voltage lines and substations in Texas (€30 million).

EPC works on high voltage lines and

substations in Arkansas, South Dakota and Florida (€18 million).

EPC Segment New Orders

y-o-y Backlog

y-o-y Revenue

y-o-y EBITDA

y-o-y

Growth (19%) 5% 2% (27%)

New Orders Backlog Revenue EBITDA

6,626 6,969

9m 2014 9m 2015

1,541 1,561

9m 2014 9m 2015

203

148

9m 2014 9m 2015

Results Presentation Q3 2015 | Business and Financial Highlights

November 25th 2015 | 15

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Spain 19%

Latam 53%

Rest of Europe

3%

Middle East and Africa

5%

North America

2% Asia 18%

Spain 15%

Latam 56%

Rest of Europe

2%

Middle East and Africa

11%

North America

3% Asia 13%

Energy 34%

T&D 26%

Infrastructure 40%

Energy 47%

T&D 21%

Infrastructure 32%

EPC Revenue by activity

Q3 YTD 2015

Q3 YTD 2014

EPC Revenue by Geographic Area

Q3 YTD 2015

Q3 YTD 2014

85% International

€1,561 MM

€1,541 MM

81% International

Results Presentation Q3 2015 | Business and Financial Highlights

November 25th 2015 | 16

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Middle East and

Africa 13%

Asia 16%

LATAM 48%

Rest of Europe

4%

Spain 13%

North America

6%

Middle East and

Africa 13%

Asia 15%

LATAM 48%

Rest of Europe

3%

Spain 16%

North America

5% >250M 14%

100M-250M 30%

50M-100M 20%

10M-50M 26%

<10M 10%

>250M 19%

100M-250M 27% 50M-

100M 22%

10M-50M 24%

<10M 8%

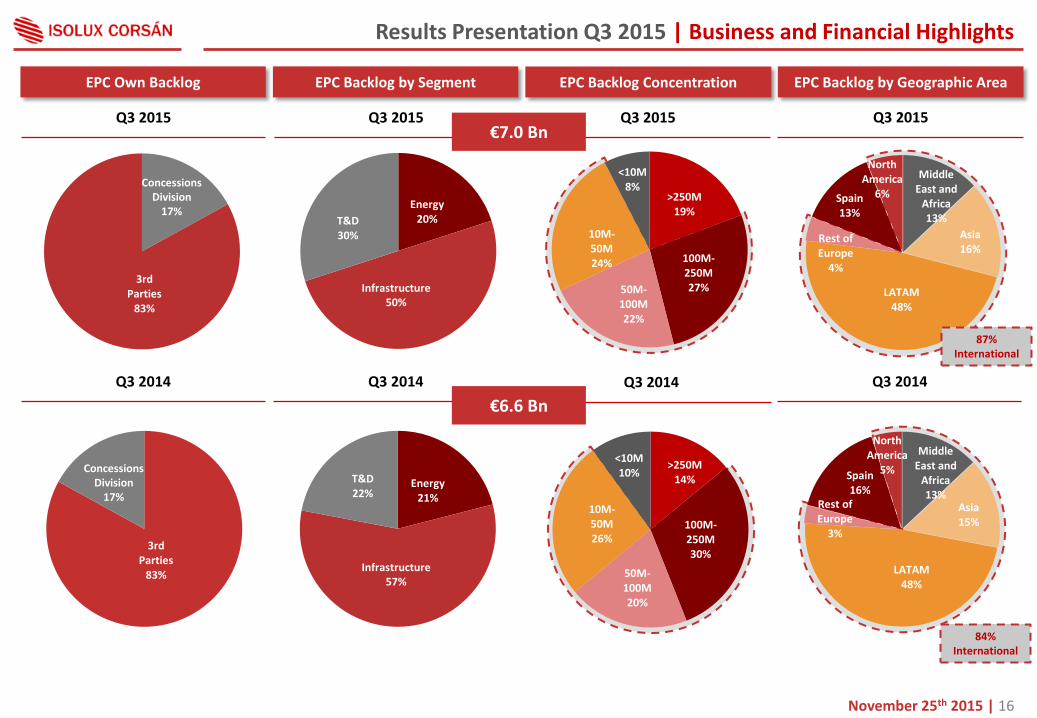

Q3 2014

Energy 20% T&D

30%

Infrastructure 50%

3rd Parties

83%

Concessions Division

17%

Energy 21%

T&D 22%

Infrastructure 57%

Q3 2015

EPC Backlog by Segment EPC Backlog by Geographic Area

Q3 2015

Q3 2014

EPC Backlog Concentration

Q3 2015

Q3 2014

87% International

84% International

EPC Own Backlog

Q3 2015

Q3 2014

€7.0 Bn

€6.6 Bn

3rd Parties

83%

Concessions Division

17%

Results Presentation Q3 2015 | Business and Financial Highlights

November 25th 2015 | 17

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

2. Business and Financial Highlights

ii. Concessions

November 25th 2015 | 18

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

447

653

Q3 YTD 2014 Q3 YTD 2015

Concessions - Key Financial Highlights

Key Figures Concessions (in € MM) Main developments

Revenue growth includes the impact related to the tariff review of the transmission lines in Brazil (already detailed in our H1 2015 presentation).

Transmission lines operating EBITDA increased by 12%.

Toll roads EBITDA has grown by 24% driven by the opening of NH6 and NH8 to traffic.

Isolux Infrastructure and car parks accounted by the equity method

(1) Construction Revenue not included

Revenue Q3 YTD 2015 (1) Revenue Q3 YTD 2014 (1)

Revenue EBITDA

267

375

Q3 YTD 2014 Q3 YTD 2015

47%

31%

19%

3% Transmission lines

Toll roads

Solar

Car parks

+46% +40%

54% 28%

15%

3%

Results Presentation Q3 2015 | Business and Financial Highlights

November 25th 2015 | 19

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Concessions Key financial metrics (in € MM, unless otherwise stated)

Q3 YTD 2014

Q3 YTD 2015

Change

Transmission lines 172 262 52%

Isolux Infrastructure 354 468 32%

Toll roads 114 136 19%

Solar photovoltaic 67 70 4%

Revenues

Total Concessions 447 653 46%

Q3 YTD 2014

Q3 YTD 2015

Change

140 226 62%

266 370 39%

71 88 24%

55 56 2%

EBITDA

267 375 40%

Q3 YTD 2014

81%

75%

62%

82%

EBITDA Margin

60%

Q3 YTD 2015

86%

79%

65%

80%

58%

Car Parks 10 15 47% 3 8 136% 31% 53%

Toll roads

97%

3%

Total kilometres: 1,644

89%

11%

100%

Total MW: 286 Total spaces: 27,329

In operation Under construction

Other( inc. Construction revenue) 83 170 - (2) (3) - n.a. n.a.

Solar PV Car Parks Transmission lines

61%

39%

Total kilometres: 5,959

Results Presentation Q3 2015 | Business and Financial Highlights

Of which, operating 87 93 7% 70 78 12% 80% 84%

November 25th 2015 | 20

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Location Asset Stake (1)

(%) Years to Maturity

Demand Risk

Revenue Mechanism(2)

Equity Invested(5) Net Debt(6)

LXTE 100% Availability Payment €122m €225m

LMTE 100% Availability Payment €133m €207m

CPTE 100% Availability Payment €15m €40m

IENNE 50% Availability Payment €37m €23m

JTE 33% Availability Payment €20m €16m

LTTE 100% Availability Payment €43m €46m

LITE 100% Availability Payment €4m €3m

UPTE 100% Availability Payment €114m €301m

WETT 50% Unlimited Availability Payment €152m €272m

BR116 90% Real Toll €103m €170m

NH1 61% Real Toll €47m €405m

NH2 (4) 50% Real Toll €17m €13m

NH6 (4) 50% Real Toll €24m €135m

NH8 (4) 50% Real Toll €28m €80m

CAMS 100% Real Toll €58m €297m

COPEXA 50% Real Toll €71m €242m

Ocaña A4 51% Shadow Toll €14m €44m

I 69 Section 5 51% Availability Payment €6m €62m

T-Solar 88% Unlimited PPA(3)/ Feed in Tariff €239m €711m

Concessions – Isolux Infrastructure’s Assets

Toll

-Ro

ads

Tran

smis

sio

n L

ine

s

(1) Stake held by Isolux Infrastructure (2) Revenues indexed to inflation. (3) PPA stands for Power Purchase agreement. (4) 50% stake owned in partnership with Morgan

Stanley Infrastructure Partners. (5) Isolux Infrastructure proportional Equity Invested

as of September 2015 (6) Isolux Infrastructure Net debt based on

Consolidation stake as of September 2015. Holdco Net debt was €80m So

lar

(Brazil)

(India)

(Mexico)

(Spain)

(USA)

(Brazil)

(India)

(USA)

2013

2004

2013

2013

2007

2009

2012

2013

2010

2009

2010

Operational & under construction

Under construction

Start of operations

2015

23

22

17

23

22

26

28

33

19

9

25

13

12

39

38

11

36

Results Presentation Q3 2015 | Business and Financial Highlights

2015

November 25th 2015 | 21

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

3. Cash flow and debt overview

November 25th 2015 | 22

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5 250

186

294

(59)

(111)

62

Cash and cash equivalentsSep 2014

Cash and cash equivalentsDec 2014

Operating Cash Flow Q3 YTD2015

Cash Flow from Investingactivities Q3 YTD 2015

Cash Flow from FinancingActivities Q3 YTD 2015

Cash and cash equivalentsSep 2015

Consolidated Cash Flow Bridge December 2014 to September 2015 (in € MM)

Cash Flow Bridge

Results Presentation Q3 2015 | Cash flow and debt overview

Cash from operations(1):

€99M Working capital:

€(159M)

(1) Cash from operations including profit for the year and after taxes paid (2) Cash and cash equivalents as of September 30, 2015, include €8.3 million of Exchange trade differences

(2)

November 25th 2015 | 23

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Corporate debt maturities as of September 30, 2015(1): breakdown by type of debt (Total €1,599 MM)

Debt Maturities

Over 83% of our corporate debt maturities are long term

(1) Adjusted for subsequent extensions that have taken place from September 30th until the date of this presentation (2) Senior Notes in accordance with IFRS, at amortized cost

2015 2016 2017 2018 2019 2020 onwards

Results Presentation Q3 2015 | Cash flow and debt overview

121 70

30

197

150 45

27

26

832(2)

3

67

13

2015 2016 2017 2018 2019 2020 and onwards

Term loans Advanced credit debts Senior notes Credit lines Finance lease liabilities

92

216

83

982

18

November 25th 2015 | 24

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

4. Appendix

November 25th 2015 | 25

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Results Presentation Q3 2015 | Appendix

Detailed Financial Statements - Consolidated Balance Sheet by segment

Consolidated Balance Sheet (in million €)

Property, plant and equipment 81 0 31 113 - 113 75 0 31 107 - 107

Investments in associates and joint ventures - (0) - (0) 974 974 - - - - 870 870

Other non-current assets 619 5,048 364 6,030 (4,963) 1,067 660 4,991 312 5,963 (4,871) 1,092

Total non current assets 700 5,048 395 6,143 (3,989) 2,154 735 4,991 343 6,070 (4,001) 2,069

Inventories 135 25 101 261 (7) 253 173 27 103 304 (5) 299

Accounts receivable 2,651 312 (774) 2,189 (341) 1,847 3,007 102 (664) 2,444 (245) 2,199

Derivative financial instruments 2 - 0 2 - 2 0 7 2 9 (7) 2

Financial assets 11 25 3 39 (25) 15 11 16 3 29 (16) 13

Cash and cash equivalents 236 314 41 592 (301) 291 167 280 4 450 (276) 174

Non-current assets held for sale - - 380 380 - 380 - - 353 353 - 353

Total current assets 3,035 676 (249) 3,462 (674) 2,788 3,358 431 (199) 3,590 (548) 3,041

Total assets 3,735 5,724 146 9,605 (4,663) 4,942 4,093 5,422 144 9,660 (4,550) 5,110

Borrowings 158 8 1,382 1,548 - 1,548 170 7 1,422 1,599 - 1,599

Project finance - 3,308 156 3,464 (3,243) 221 - 3,263 160 3,424 (3,173) 250

Liabilities held for sale - - 173 173 - 173 - - 151 151 - 151

Accounts payable 2,505 556 (294) 2,767 (412) 2,355 2,747 373 (233) 2,887 (224) 2,663

Other liabilities 196 915 51 1,162 (882) 280 232 1,060 (27) 1,265 (1,029) 236

Total liabilities 2,859 4,787 1,467 9,113 (4,536) 4,577 3,150 4,704 1,473 9,326 (4,427) 4,899

September 30, 2015

EPC ConcessionsOther and

corporateSub-Total

Change in

consolidation

method

Total

Consolidated

December 31, 2014

Sub-Total

Change in

consolidation

method

Total

ConsolidatedEPC Concessions

Other and

corporate

November 25th 2015 | 26

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Detailed Financial Statements - Consolidated Income Statement by segment

Results Presentation Q3 2015 | Appendix

Consolidated Income Statement (in million €)

Segment's ordinary revenue 1,541 447 21 2,009 (460) 1,549 1,561 653 18 2,232 (652) 1,580

Other 12 - 0 13 (8) 4 22 - (1) 22 (7) 14

Total operating income 1,553 447 21 2,021 (468) 1,553 1,584 653 17 2,254 (659) 1,595

Other operating expenses (1,350) (179) (40) (1,569) 202 (1,367) (1,436) (277) (50) (1,763) 283 (1,480)

EBITDA 203 267 (18) 452 (266) 186 148 375 (32) 491 (376) 115

Depreciation, amortization and impairment losses (15) (64) (21) (100) 65 (35) (10) (69) (24) (103) 79 (24)

Change in trade provisions (10) 0 (25) (35) - (35) (9) 0 (12) (21) - (21)

Operating results 178 203 (64) 317 (201) 116 129 306 (69) 367 (297) 70

Net financial results (17) (189) (120) (326) 169 (158) (28) (210) (113) (351) 201 (150)

Equity method - - - - 22 22 - - - - 48 48

Profit before income tax 161 14 (184) (9) (10) (20) 101 96 (181) 16 (48) (32)

Income tax - - (3) (3) 11 8 - - (27) (27) 48 21

Results for the period from continuing operations 161 14 (187) (12) 1 (11) 101 96 (208) (11) 0 (11)

Results for the period from discontinuing operations - - (8) (8) - (8) - - (11) (11) - (11)

Results for the period 161 14 (195) (20) 1 (20) 101 96 (220) (22) 0 (22)

Attributable to:

Owners of the parent - - - (17) - (17) - - - (20) - (20)

Non-controlling interests - - - (3) 1 (3) - - - (2) 0 (2)

Q3 YTD 2014

EPC ConcessionsOther and

corporateSub-Total

Change in

consolidation

method

Total

Consolidated

Q3 YTD 2015

EPC ConcessionsOther and

corporateSub-Total

Change in

consolidation

method

Total

Consolidated

November 25th 2015 | 27

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

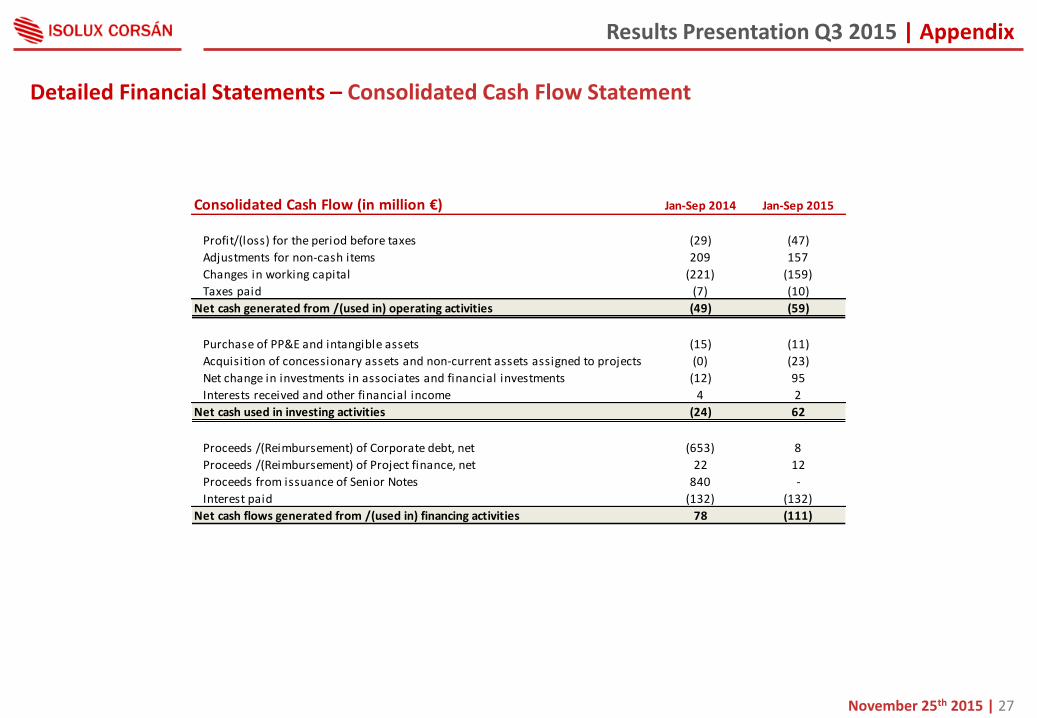

Detailed Financial Statements – Consolidated Cash Flow Statement

Results Presentation Q3 2015 | Appendix

Consolidated Cash Flow (in million €) Jan-Sep 2014 Jan-Sep 2015

Profit/(loss) for the period before taxes (29) (47)

Adjustments for non-cash items 209 157

Changes in working capital (221) (159)

Taxes paid (7) (10)

Net cash generated from /(used in) operating activities (49) (59)

Purchase of PP&E and intangible assets (15) (11)

Acquisition of concessionary assets and non-current assets assigned to projects (0) (23)

Net change in investments in associates and financial investments (12) 95

Interests received and other financial income 4 2

Net cash used in investing activities (24) 62

Proceeds /(Reimbursement) of Corporate debt, net (653) 8

Proceeds /(Reimbursement) of Project finance, net 22 12

Proceeds from issuance of Senior Notes 840 -

Interest paid (132) (132)

Net cash flows generated from /(used in) financing activities 78 (111)

March 5th 2015 | 28

225

131

131

196

48

48

178

178

178

234

234

234

243

203

0

235

138

27

129

5

5

Thank you

© Isolux Corsán 2015

Isolux Corsán Investor Relations [email protected]