retail hot buttons - consumer health products canada influencing cpg growth ... acne products ‐8%....

TRANSCRIPT

REDEFINING RETAILFACTORS INFLUENCING CPG GROWTH

WITHIN HEALTH & BEAUTY

Q2 2014

Copyrig

ht ©

2013

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

2

THE CHALLENGE FOR GROWTH

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

3

CPG STILL SPUTTERING FOR GROWTH IN NORTH AMERICA

United States

Nielsen: MarketTrack ‐ Total Tracked Sale52 wks ending June 28, 2014

Canada

+1.4 +0.0

Dollars

Nielsen: ScanTrack ‐ Total Tracked Sale52 wks ending July 5, 2014

UnitsDollars Units

+1.0 ‐0.3

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

4

5

22 2

2 20

20 0 0 0

2009 2010 2011 2012 2013 YTD 2014

$ % Chg Unit % Chg

Inflation +5 +0 +2 +2 +2 +2

2014 IS SHAPING UP TO BE MORE OF THE SAME

Source: Nielsen MarketTrack, National All Channels – YTD 28 weeks to June 28, 2014 ‐ Total Tracked Sales excluding Fresh Random Weight

Slow growth, driven only by inflation

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

5

1

0

11

3

1

00

0

‐1

2

0

National Maritimes Quebec Ontario Prairies B.C.

$ % Chg

Unit % Chg

THE PRAIRIES LEAD REGIONAL PERFORMANCE

52 week Regional CPG Performance

Source: Nielsen MarketTrack, National All Channels – 52 weeks Ending June 28 2014 ‐ Total Tracked Sales excluding Fresh Random Weight

The Prairies lead regional growth – twice the National average

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

6

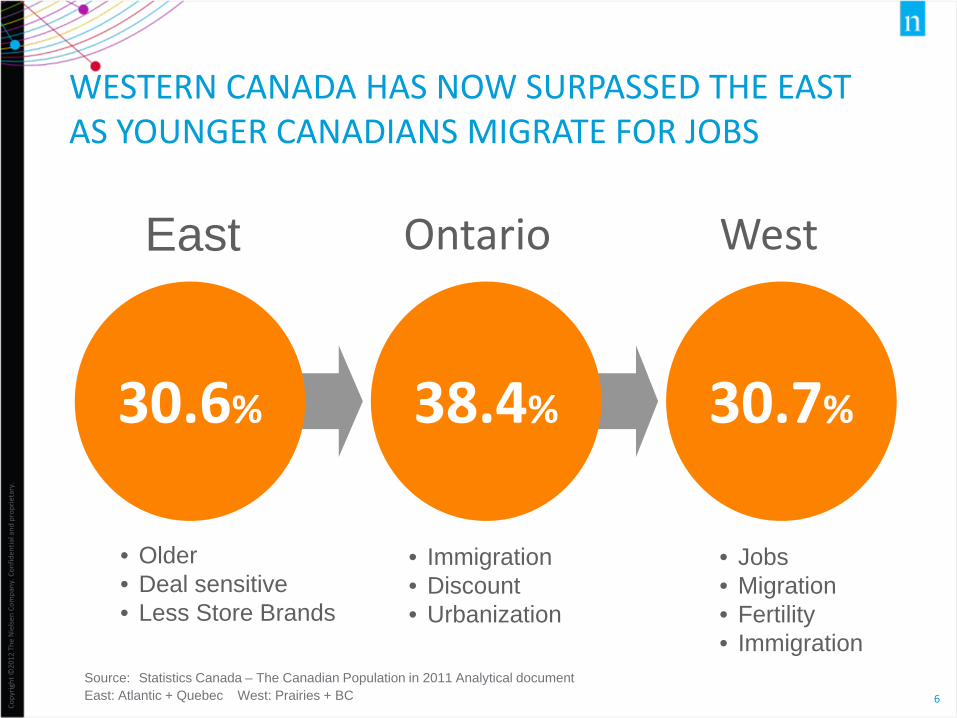

WESTERN CANADA HAS NOW SURPASSED THE EAST AS YOUNGER CANADIANS MIGRATE FOR JOBS

30.6%

East WestOntario

30.7%38.4%

• Jobs• Migration• Fertility• Immigration

• Immigration• Discount• Urbanization

Source: Statistics Canada – The Canadian Population in 2011 Analytical document East: Atlantic + Quebec West: Prairies + BC

• Older• Deal sensitive• Less Store Brands

Copyrig

ht ©

2013

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

7

71%12%

6%11%

Grocery & Mass (+1%)

Convenience & Gas (+3%)*

All Other (+2%) Total Market: $73.3 Billion (+2%)

Source: Nielsen MarketTrack, National, Dollars, 52 weeks ending June 28, 2014Excludes Fresh Random Weight and Food Service; * Includes Tobacco

Drug (+2%)

CONVENIENCE & GAS OUTPACING THE MARKET

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

8

66.6 76.4

19.6

18.1 10.5

71.2

15.3 13.0 9.6

$ Share and Growth

HABA

GroceryCategories

Non Grocery

+1

+1

+2

+1

+1

+1

+4

+1

+2

+4

+0

+6

HEALTH & BEAUTY SALES ARE OUTPERFORMING TOTAL CPG

AllChannels

Grocery + Mass

Drug Stores

Source: Nielsen MarketTrack, 52 Weeks to June 28, 2014 ‐ Excludes Random Weight Fresh

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

9

HABA CATEGORIES ARE LEADING RETAIL SALES GROWTH WITHIN GROCERY + MASS MERCHANDISERS

$ Share and Growth

66.6 76.4

19.6

18.1 10.5

71.2

15.3 13.0 9.6

HABA

GroceryCategories

Non Grocery

+1

+1

+2

+1

AllChannels

Grocery + Mass

+1

+1

+4

+1

Drug Stores

Source: Nielsen MarketTrack, 52 Weeks to June 28, 2014 ‐ Excludes Random Weight Fresh

+2

+4

+0

+6

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

10

FOOD CATEGORIES ACCOUNT FOR ALMOST 1 IN 5 DOLLARS SALES IN DRUG STORES ‐ FUELING GROWTH

$ Share and Growth

66.6 76.4

19.6

18.1 10.5

71.2

15.3 13.0 9.6

HABA

GroceryCategories

Non Grocery

+1

+1

+2

+1

AllChannels

Grocery + Mass

+1

+1

+4

+1

+2

+4

+0

+6

Drug Stores

Source: Nielsen MarketTrack, 52 Weeks to June 28, 2014 ‐ Excludes Random Weight Fresh

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

11

SDM TESTING FRESH FORMAT

Source: Nielsen photos

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

12

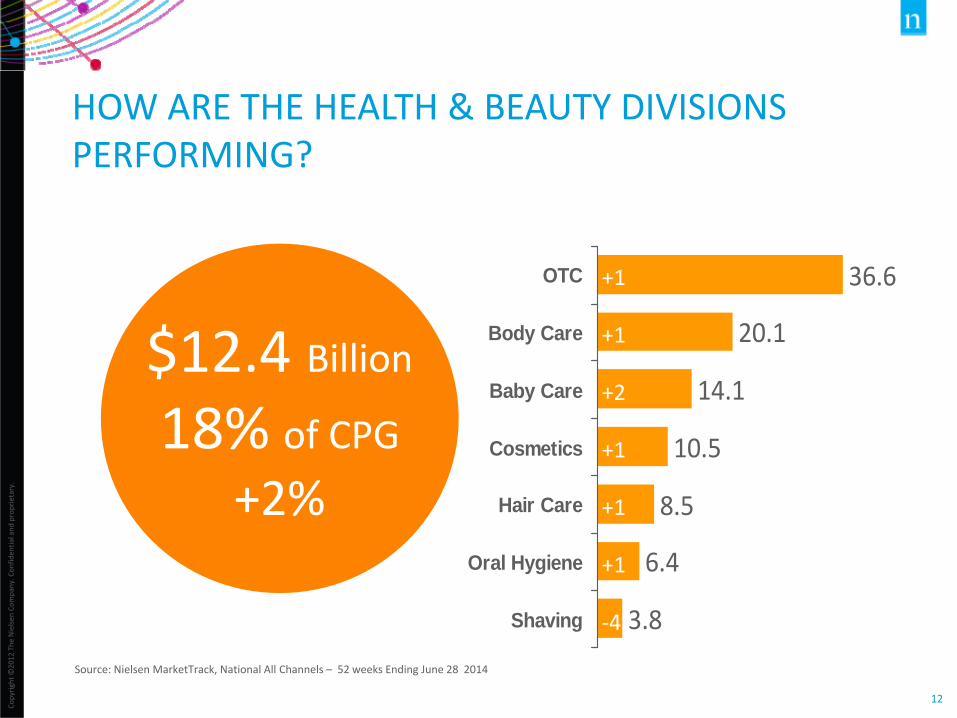

HOW ARE THE HEALTH & BEAUTY DIVISIONS PERFORMING?

Source: Nielsen MarketTrack, National All Channels – 52 weeks Ending June 28 2014

$12.4 Billion18% of CPG

+2%

36.6

20.1

14.1

10.5

8.5

6.4

3.8

OTC

Body Care

Baby Care

Cosmetics

Hair Care

Oral Hygiene

Shaving

+1

+1

+2

+1

+1

+1

‐4

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

13

MAKING THE CUT IN HABA

Source: Nielsen MarketTrack, National All Channels – 52 weeks Ending June 28 2014 > $5 million

Men’s Antifungals +17%Sleeping Aids +13%Topical Analgesics +13%Energy Nutrition +11%Athletic Supports +10%

Enemas ‐13%Tooth Polish ‐12%Acne Products ‐8%Menstrual Relief ‐8%Wart Removers ‐6%

Face Care +2%Headache Rem ‐3%Shampoo+Cond. +0%Health Suppl. +5%Diapers +0%

Top 5

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

14

DRUG STORES REMAIN THE TOP DESTINATION FOR HABA SALES – BUT LOSING SHARE

$ Share 2009 2014 Pt Chg

Drug Stores 39.6% 36.3% ‐3.4

Grocery 23.4% 22.9% ‐0.5

Mass Merch. 21.4% 21.4% +0.0

Warehouse 7.0% 9.6% +2.6

Health Food 1.9% 2.1% +0.2

Remaining 6.7% 7.7% +1.0

Source: Nielsen Homescan Channel Facts ‐ 52 Weeks Ending June 28, 2014

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

15

WHERE IS THE CONSUMER TODAY?

Do you think economics conditions are better today than a year ago?

YES NO

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

16

WHERE IS THE CONSUMER TODAY?

As a result, will you change your spending behaviours?

YES NO

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

17

WHERE DO WE FIND GROWTH IN A CHALLENGING ENVIRONMENT?

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

18

TRENDS IMPACTING GROWTH

• Economy still fragile• Cautious Consumer

Cyclical Changes

• Value Motivators• Emerging Retail Formats• Connected Consumer• Evolving Consumer

Structural Changes

Copyrig

ht ©

2013

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

19

CONSUMER SENTIMENT IN A HOLDING PATTERN

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

20

CANADIAN CONSUMER CONFIDENCE IS IN A HOLDING PATTERN SINCE THE RECESSION

Source: Nielsen Global Online Consumer Confidence Surveys – Q2 2014

110114

111 112 113

104

96

84

90

98102 101

9694

10098

100 99102

3Q05 3Q06 3Q07 3Q08 2Q09 2Q10 4Q11 4Q12 4Q13 2Q14

Recession Post‐recessionPre‐Recession

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

21

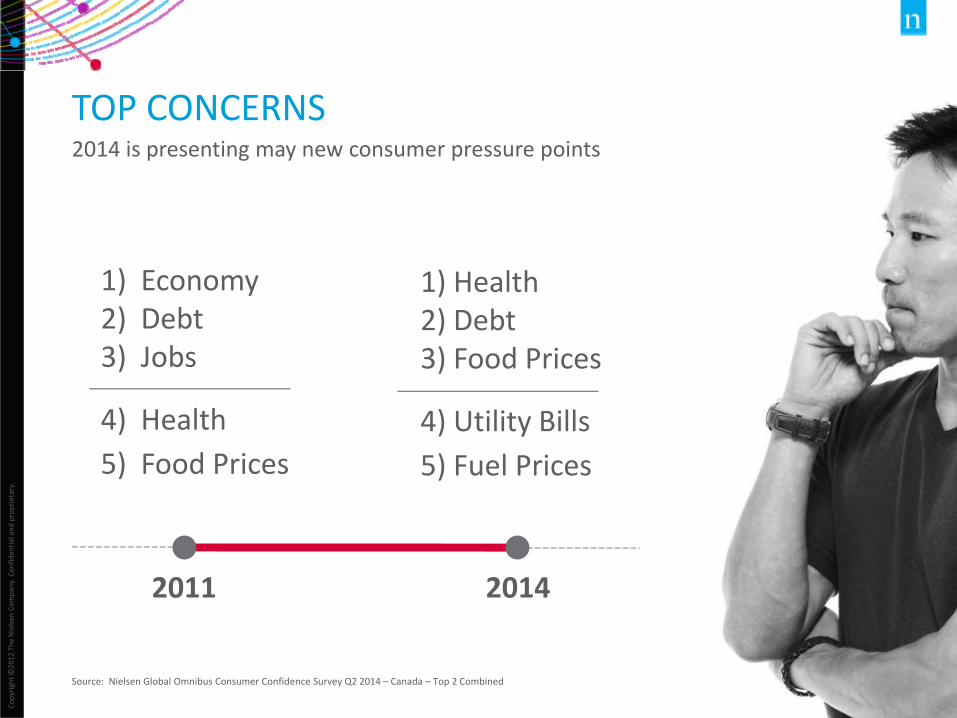

TOP CONCERNS2014 is presenting may new consumer pressure points

20142011

1) Economy2) Debt3) Jobs

4) Health5) Food Prices

1) Health2) Debt3) Food Prices

4) Utility Bills5) Fuel Prices

Source: Nielsen Global Omnibus Consumer Confidence Survey Q2 2014 – Canada – Top 2 Combined

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

22

CONSUMERS ARE STILL FOCUSED ON SPENDING RESTRAINT

$$$

54%are trying to reduce household expenses

‐3%decline in household expenditures

Source: Nielsen Homescan, Total Expenditures ‐ 52 Weeks Ending June 28, 2014 – Q2 2014 Global Omnibus Survey – Canada* Nielsen Panel Views Survey June 2014 – Canada

73%are trying to spend less on their grocery bill*

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

23

WHAT ARE CONSUMERS DOING TO SAVE?

• Stock up when on promotion 85%

• Only buy items when on sale 75%

• Use Coupons 65%

• Seek out stores with lower prices 59%

• Buy larger sizes 52%

• Buy lower priced store brands 48%

• Buy lower priced name brands 38%

• Shop at Discount Retailers 36%

Top saving activities:

$$$

Source: Nielsen PanelViews Survey ‐ Canada – June 2014

New #1

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

24

SINCE BEFORE THE RECESSION, % OF RETAIL SALES SOLD WITH A PRICE CUT HAS INCREASE 10 POINTS

% Dollars Sold on TPR

27% 27%31%

33% 34%35% 37% 37%

2007 2008 2009 2010 2011 2012 2013 2014

Quarterly PeriodsSource: Nielsen MarketTrack, National GB+MM+DG ‐ 12 week periods ending June 28, 2014

HABA 27% +4

+4

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

25

36

32

30

28

26

23

21

ORAL HYGIENE

BABY CARE

BODY CARE

HAIR CARE

SHAVING

OTC

COSMETICS

HABA DEPARTMENTS ARE LESS DEPENDENT ON PRICE CUTS BUT IS GAINING MOMENTUM

TPR* % of Total Dollar Sales ‐ $ % Chg

* TPR – Temporary Price Reduction

TPR* Total

+7 +2

+3 +2

+3 +1

‐1 +1

+3 ‐4

+5 +1

+4 +1

Source: Nielsen MarketTrack, National Grocery + Drug + Mass ‐ 52 weeks to June 28, 2014 versus Year Ago

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

26

ALMOST 6 BILLION IN GROCERY SALES HAVE SHIFTED TO DISCOUNT RETAILERS SINCE 2007

34.3%

43.7%

Discount $ Share

Yr 2007 Yr 2014

Discount Share Projections:

2014: 44.7%

2017: 50.9%

+9 share points

MORE TO COME

Source: Nielsen MarketTrack – National GB+DG+MM– 52 weeks to June 28, 2014

HABA 36%

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

27

69.5

45.7

40.3

39.7

32.7

26.8

24.9

BABY CARE

SHAVING

HAIR CARE

ORAL HYGIENE

BODY CARE

OTC

COSMETICS

DISCOUNT RETAILERS GAINING SHARE OF WALLET FOR THE MAJORITY OF HABA DEPARTMENTSDiscount Dollar Share – $ % Chg Disc

+14

‐2

+2

+3

+1

+5

+4

Conv

‐3

‐5

+0

+1

+1

+0

+0

Source: Nielsen MarketTrack, National All Channels ‐ 52 weeks to June 28, 2014 ‐ * Excludes Random Weight Fresh

Copyrig

ht ©

2013

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

28

TRADITIONAL

TRADITIONAL RETAIL UNDER ATTACK

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

29

THE LOYAL, DISLOYAL SHOPPER

Source: Nielsen Homescan: Top 10 Banners in Ontario ‐ Avg $ Share of Requirements 52 weeks to Sept 19/13

Average Loyalty to Store

14%

Need to understand what and where your shoppers are

spending the other 86%

The Opportunity

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

30

TRADITIONAL CPG CHANNELS RELATIVELY STATIC

Grocery ‐1%Drug +2%Conv & Gas +3%Warehouse +3%Mass Merch ‐5%

less Zellers +5%

Source: Nielsen Homescan Channel Watch – Canada ‐ 52 weeks to June 28, 2014*Convenience Track 52 weeks to June 28, 2014 – Drug MarketTrack

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

31

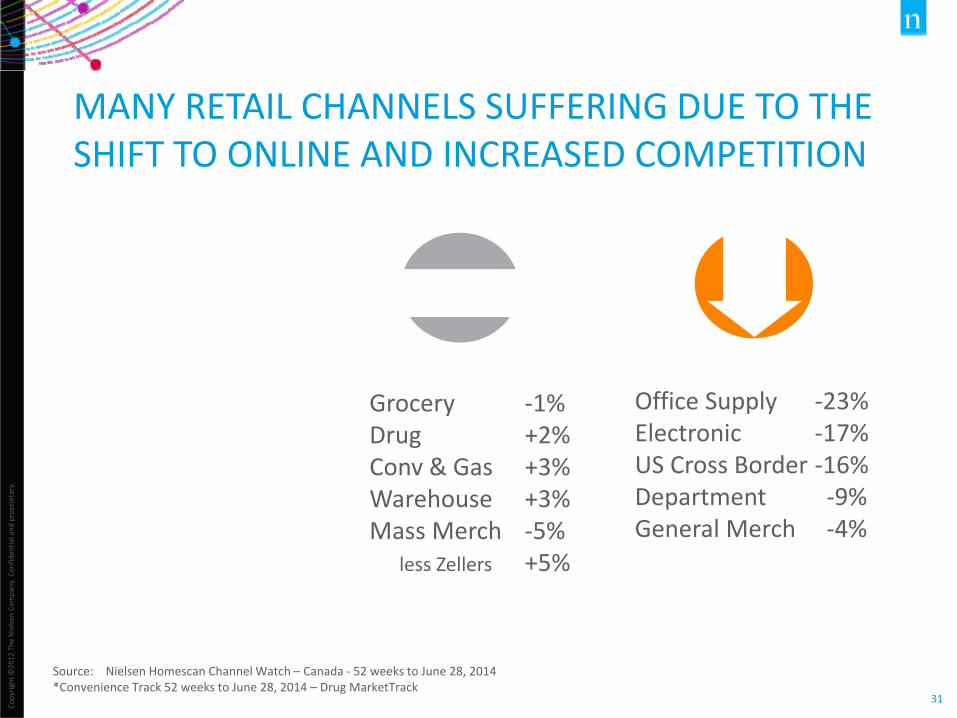

MANY RETAIL CHANNELS SUFFERING DUE TO THE SHIFT TO ONLINE AND INCREASED COMPETITION

Office Supply ‐23%Electronic ‐17%US Cross Border ‐16%Department ‐9%General Merch ‐4%

Source: Nielsen Homescan Channel Watch – Canada ‐ 52 weeks to June 28, 2014*Convenience Track 52 weeks to June 28, 2014 – Drug MarketTrack

Grocery ‐1%Drug +2%Conv & Gas +3%Warehouse +3%Mass Merch ‐5%

less Zellers +5%

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

32

E‐COMMERCE, ETHNIC , HEALTH AND DOLLAR STORES LEAD RETAIL GROWTH IN CANADA

Online +43%Ethnic Grocery +20%Health Food +8%Dollar Stores +7%

Office Supply ‐23%Electronic ‐17%US Cross Border ‐16%Department ‐9%General Merch ‐4%

Source: Nielsen Homescan Channel Watch – Canada ‐ 52 weeks to June 28, 2014*Convenience Track 52 weeks to June 28, 2014 – Drug MarketTrack

Grocery ‐1%Drug +2%Conv & Gas +3%Warehouse +3%Mass Merch ‐5%

less Zellers +5%

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

33

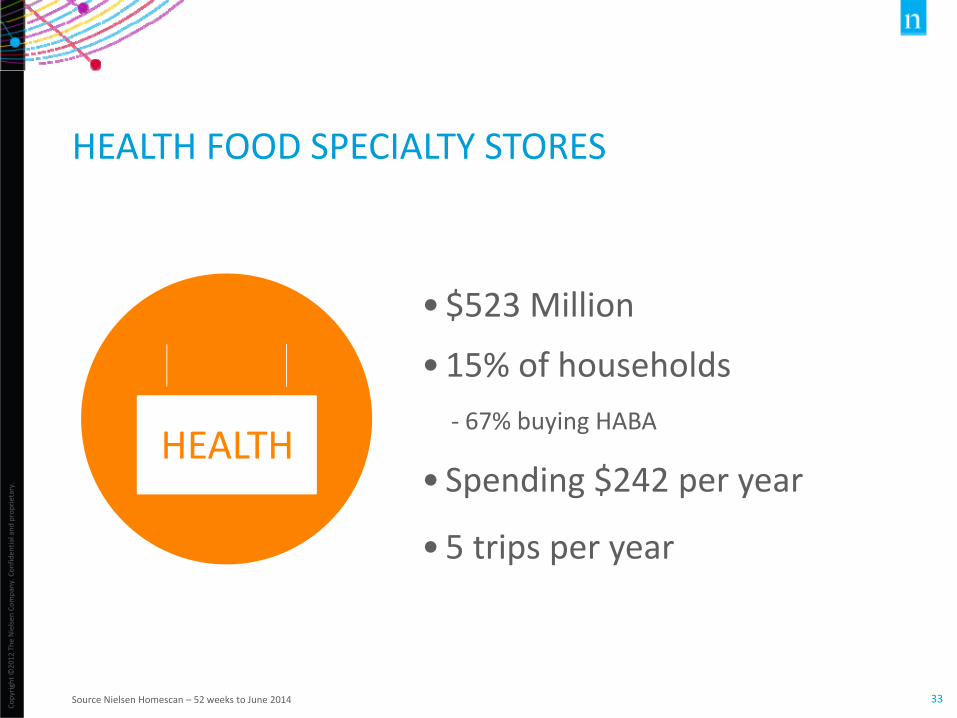

HEALTH FOOD SPECIALTY STORES

Source Nielsen Homescan – 52 weeks to June 2014

HEALTH

•$523 Million

•15% of households‐ 67% buying HABA

• Spending $242 per year

• 5 trips per year

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

34

DOLLAR STORES HAVE ROOM TO GROW IN CANADA

Source Nielsen Homescan – 52 weeks to June 2014

DOLLAR STORES

CANADA U.S

$ Share 1.2% 2.3%

% Chg +7% +1%

Penetration 75% 66%

33% of Dollar Store shoppers buy HABA in Dollar Stores

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

35

ETHNIC STORES CONTINUE TO CAPTURE A LARGER SHARE OF CANADIAN WALLETS

Source: Nielsen Homescan Retailer Watch – Ethnic Stores, 52 weeks to June 28, 2014

Ethnic Grocery

+20%•Estimate $4‐5 Billion*

•17% of households

:36% in Toronto

• Spending $328 per year

• 11 trips per year

* Perry Caico CIBC World Markets

Copyrig

ht ©

2013

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

36

ONLINE SHOPPING GAINING MOMENTUM

Online Shopping

+43%•1.9% share of Tracked Sales

‐ Grocery Composite 0.6%‐ Drug Composite 1.0%

•43% of households (+22%)

• Spending $388 /yr (+17%)$2.3 Billion

Source: Nielsen Homescan, National Total Expenditures, 52 Weeks Ending June 28, 2014

+11% YA

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

37

WHAT ARE CONSUMERS BUYING ONLINE AND WILLING TO BUY ONLINE?

Source: Canadian PanelViews Social Media Survey Oct 2013

Currently Buying Online Willing to Buy Online21% Toys16% Health & Beauty14% Cosmetics9% Paper Products7% Household Products7% Confectionery6% Pet Products6% Non Perishable Food6% Baby Products4% OTC Drugs4% Beverages3% Fresh Produce3% Perishable Food

70% Paper Products64% Household Products56% Heath & Beauty55% Toys50% Non Perishable Food49% Pet Products48% Confectionery48% Cosmetics47% OTC Drugs45% Beverages33% Baby Products20% Perishable Food18% Fresh Produce

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

38

THE FACE OF THE CANADIAN SHOPPER IS CHANGING

• Ethnicity• Downsizing• Generations

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

39

COMMON GENERATIONAL DEFINITIONS While there are many generalizations, there is no “official” definition

<19‘Gen Z’16%

19‐37‘Gen Y’27%

38‐47‘Gen X’14%

48‐67‘Boomers’28%

68+‘GI’14%

Source: Statistics Canada – Census 2011

5.7 9.4 4.7 9.8 5.0 Millions

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

40

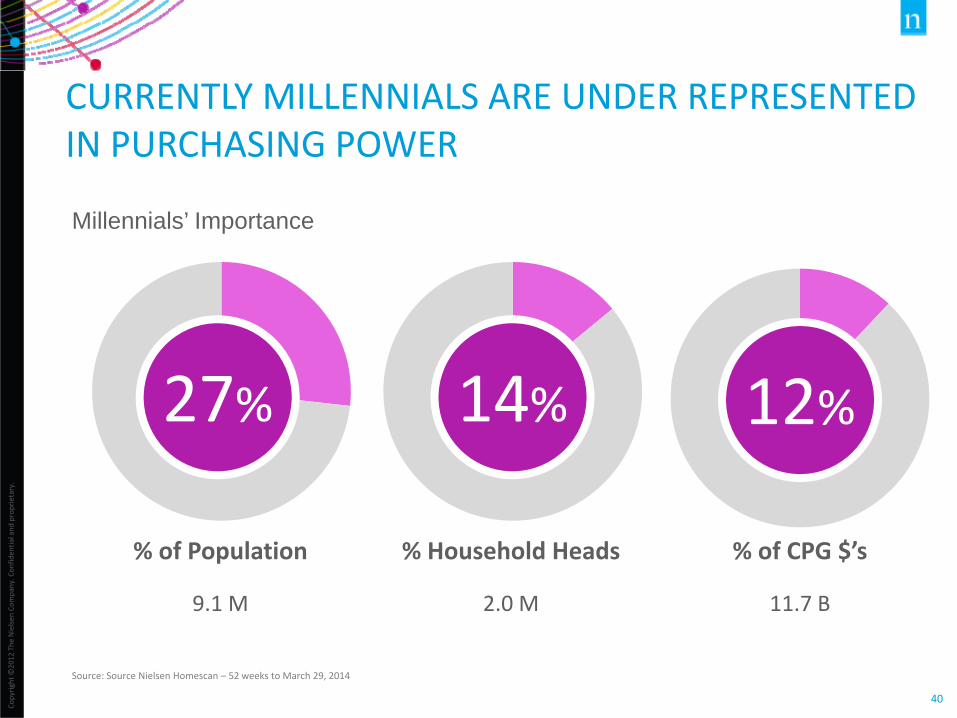

CURRENTLY MILLENNIALS ARE UNDER REPRESENTED IN PURCHASING POWER

Millennials’ Importance

27%

Source: Source Nielsen Homescan – 52 weeks to March 29, 2014

14% 12%

% of Population

9.1 M

% Household Heads

2.0 M

% of CPG $’s

11.7 B

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

41Source: Statistics Canada M: Millions

2010 2020 2030

Millennials Boomers

MILLENNIALS WILL SURPASS BOOMERS BY 2020

26%

28%

8.9 M9.7 M

26%

24%

10.0 M9.4 M

26%

20%

11.0 M8.3 M

34.2 M 38.4 M 42.1 MTotal Canada

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

42

THE CPG GROWTH ENGINE WILL SWITCH GEARS

By 2020…

Source: Nielsen Homescan 52 weeks to March 29, 2014 – HH <35 years – Based on older generation spend

MILLENNIALS BOOMERS

+$12.6 B

+207%

‐$4.3 B

‐9%

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

43

WHICH HABA DEPARTMENTS ARE MOST COMMONLY FOUND IN A MILLENNIALS’ SHOPPING BASKET?

Nielsen Homescan – Dollar Consumption Index – 52 wks to December 28, 2013 – Consumer Facts CPG Departments Relative Index (82 for total)

Relative Dollar Index <35 years

Baby Care 384Body Care 122

Hair Care 120Cosmetics 109

Oral Hygiene 97OTC 67

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

44

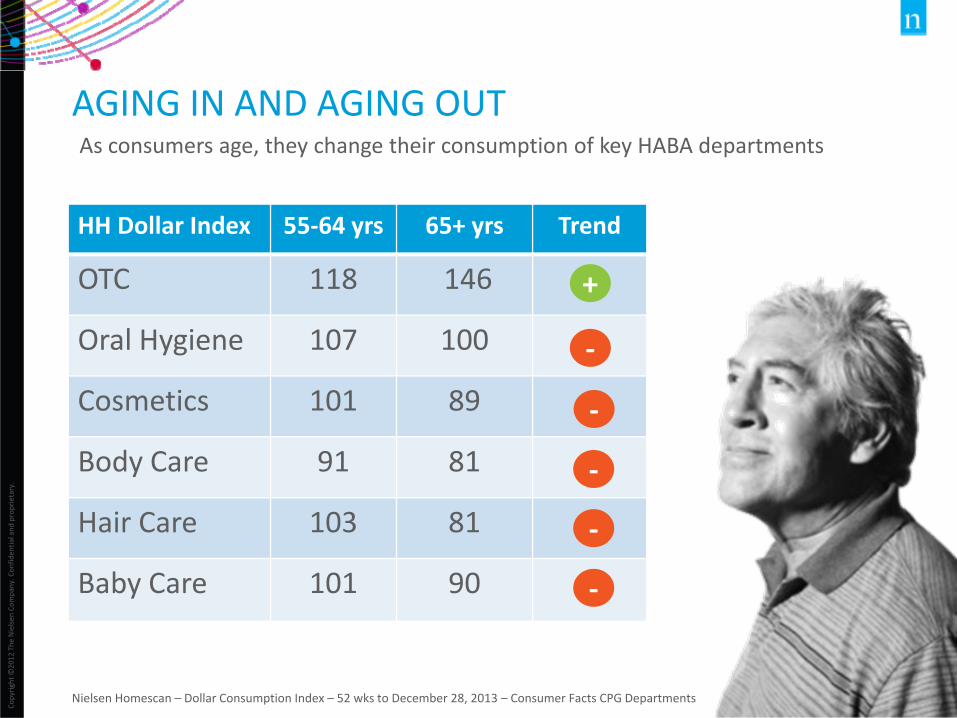

AGING IN AND AGING OUT

Nielsen Homescan – Dollar Consumption Index – 52 wks to December 28, 2013 – Consumer Facts CPG Departments

HH Dollar Index 55‐64 yrs 65+ yrs Trend

OTC 118 146

Oral Hygiene 107 100

Cosmetics 101 89

Body Care 91 81

Hair Care 103 81

Baby Care 101 90

As consumers age, they change their consumption of key HABA departments

+

‐

‐

‐

‐

‐

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

45

I want to watch what I want, when I want… and for free.

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

46

Media Usage

MEDIA HABITS DIFFER BETWEEN GENERATIONS

Source: Nielsen Spectra, PMB , January 2014

BoomersMillennial

TV

Internet

Magazines

Newspaper

Radio

LIGHT HEAVYMEDIUM

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

47Source: Nielsen Borealis; TV Data Source: BBM Canada

Millennials

Boomers

OVER THE PAST 3 YEARS, MILLENNIALS ARE WATCHING LESS TRADITIONAL TELEVISION

2012 2013 2014

22hr 48min

33hr 36min

22hr 29min

33hr 47min

20hr 52min

33hr 59min

4.9 hrs/day

3.0 hrs/day

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

48

TOP 10 TV SERIES AMONG MILLENNIALS IN 2013

Source: Nielsen Borealis; TV Data Source: BBM Canada – TV Series Excluding specials

1. Amazing Race Canada 12. Big Bang Theory 33. Masterchef 584. Stanley Cup Finals 55. Sochi 2014 66. La Voix 27. Agents of S.H.I.E.L.D 538. Under the Dome 49. Amazing Race 910.Grey’s Anatomy 22

Boomers

FEMALES:7 of 10 are reality shows

MALES:2 of 10 are reality shows

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

49

MILLENNIALS ARE CUTTING THE CORD

% with no cable or TV subscription

Millennials Boomers

26%

12%

Source: Nielsen Spectra, 2014 Mar

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

50

LESS CABLE BUT MORE ONLINE MEDIA

46% News Websites

34% Watch TV online

26% Newspapers Online

22% Radio Online

Boomers

23%

5%

14%

7%

Source: December 2013 Nielsen PanelViews Social Media Survey

Millennials

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

51

POWER AT THEIR FINGERTIPS

% Total Ownership

12% expected to buy in next year

63% potential ownership

Source: Nielsen PanelViews, Social Media Survey, 2013

51%

7% expected to buy in next year

86% potential ownership!

% Millennials Ownership

79%

Copyrig

ht ©

2012

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

52

65% have purchased or are willing to purchase via virtual store

70% have purchased from an

online store

E‐commerce M‐commerce

Nielsen, PanelViews, Social Media, survey 2013

LEADING TO ONLINE SALES

Copyrig

ht ©

2013

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

5353

KEY TAKEAWAYS

• Economic Divide: Economy remains sluggish; opportunities across the economic spectrum with polarizing growth ‐ Premium vs. Value

• Cyclical Changes: With time, the economy will improve along with consumer spending fueling growth

• Structure Changes: The face of the Canadian shopper continues to evolve changing the retail landscape. We need to align to these trends for sustainable growth.

Copyrig

ht ©

2013

The

Nielse

n Co

mpany. Con

fiden

tial and

proprietary.

54

THANK YOU!

Stay Connected to Consumer and Media Trends

For the latest insights, visit us nielsen.com

Download our app: Nielsen TOPTEN

Questions regarding the content of this presentation, contact:

Carman Allison, email [email protected]

@carman_allison