retail lending 3.0 boosting productivity and improving the customer

TRANSCRIPT

Retail Lending 3.0Boosting productivity and improving the customer experience

1 Introduction 2 A changing world 7 Emerging trends in retail lending 9 Winning strategies 12 Toward Retail Lending 3.0: The next steps

Content

AcknowledgmentsDeveloping this report was a team effort that required dedication, experience, and insight from Deloitte’s Financial Services practice in Canada. Nancy Monson, Deloitte Canada; and Joel So, Deloitte Canada, led the effort, and a number of others made significant contributions, including Bill Currie, Deloitte Canada; David Goslin, Deloitte Mexico; David Dawson, Deloitte Canada; Matthew Rossiter, Deloitte Canada; and Justin Chu, Deloitte Canada.

Retail Lending 3.0 Boosting productivity and improving the customer experience 1

Introduction

For retail lending, the Internet has opened the door to a whole new world.

In fact, it has fundamentally changed the way in which business is done

and services are delivered. Whether in a retail store, a restaurant, or a bank,

consumers’ expectations have changed. They expect businesses to provide

services that are simple to understand, tailored to their needs, and rapidly

delivered. They also expect to connect in real time and on demand through

whatever channel they prefer – in person, over the Internet, by phone, or

through a mobile device.

Financial institutions have recognized these trends and have increased their

hours of operation, enhanced their online offerings, and developed mobile

applications. Although these changes have already improved the way

banking is done, today’s retail lenders still have the opportunity to be on the

leading edge of this transformation. To be successful, lenders will need a

clear view of how these changes will be reflected in their market and how to

make the most of this new reality.

Consumers expect businesses to provide services that are simple to understand, tailored to their needs, and rapidly delivered.

2

The retail lending marketThe retail lending market is recovering from the global financial crisis and is expected to remain a profit driver for financial institutions into the foreseeable future. For example, in Canada, consumer demand for credit is steadily increasing, with Canadian mortgage debt alone valued at over US$1 trillion.[1] In the United States, consumer credit grew for three consecutive months (as of December 2010) after declining for the previous 20 months.[2]

Trends in Latin America indicate a lending boom, with impressive credit growth fuelled by increasing consumer consumption and banks offering innovative lending products.[3] Brazil’s economy has been riding a wave of consumer credit, with the major banks reporting credit growth of more than 20 percent in 2010,[4] and both Columbia and Mexico are experiencing rapid growth in the acceptance of financial products. At the end of September 2010, 62 percent of Columbians were using a financial product, an increase of 1.8 million over the previous year.[5] In Mexico, the potential for growth in retail lending is enormous, with approximately 18 million families (out of 25 million) not currently using the banking system at any level.[6]

Retail lending products have been recognized as the cornerstone of a bank’s long-term relationship with its customers. The loan transaction presents a pivotal opportunity for you, as a lender, to connect with a customer and build a relationship that will last for years. However, the loan origination experience is often less than ideal, as a result of dated technologies, cumbersome policies, and labour-intensive processes. Your organization’s ability to capture a growing share of the retail market depends on your ability to deliver a superior customer experience that takes advantage of leading-edge technologies.

Leading retail lending technologiesWith the retail lending market so attractive, what can you do to improve your market position? Three technologies have emerged as winners in the U.S. market and are potential “game changers” for the rest of the Americas: online loan origination, mobile applications, and progressive decisioning (i.e., using software to optimize borrower interview questions and preapprove a loan amount based on the applicant’s inputs and responses, in real time). Each has an impressive track record in boosting customer satisfaction and improving productivity. In short, these technologies have made originations faster and less expensive.

Online loan originationThe transition to online loan origination is inevitable – consider that 63 percent of Internet users in Canada are already banking online,[7] and this number is climbing every year. The percentage of U.S. adults who bank online rose from 51 percent in 2005 to 59 percent in 2010.[8] Customers are now using the Internet for their borrowing needs as well. In fact, the Web is the fastest-growing delivery channel for mortgage originations in the United States (increasing from 4 percent in 2010 to 13 percent in 2013)[9] and is quickly becoming the source customers turn to first. In the United States, where online loan origination is more established, over 70 percent of borrowers shop for their mortgages online.[10]

A changing world

The loan transaction presents a pivotal opportunity for you, as a lender, to connect with a customer and build a relationship that will last for years.

Retail Lending 3.0 Boosting productivity and improving the customer experience 3

The shift to online banking is not limited to North America. Approximately half of the consumers in Western Europe now bank online, and this figure continues to increase. In some banks, it has reached 60 percent or even 80 percent.[11] Online banking is even more popular in Brazil than it is in the United States, with 60 percent of Internet users in Brazil being online banking patrons.[12] The trend continues throughout Latin America. In Mexico, online banking has shown continuous growth consistent with the growth of Internet usage in the country.

Growth of internet users vs. online banking transactions40

35

30

25

20

15

10

5

0

Inte

rnet

use

rs in

Mex

ico

(MM

) Online banking transactions

in Mexico (M

M)

1,200

1,000

800

600

400

200

02011e 2012e2008 2009 2010e

Internet Online banking

Source: Datamonitor, Internet access in Mexico Banxico, Online banking transactions in Mexico

Outside of the United States, most online banking consumers use the Internet to check balances, make payments, or compare rates. But improvements in technology have made it easier to access more complex products online.[11] Today, when customers use the online channel, they want more than just easy access to today’s rates. They want to be able to compare rates and products, conduct borrowing scenario analyses, calculate monthly payments, get personalized recommendations based on their own unique circumstances, get preapproved for a loan (or at least start the application process), and track their loan status – all in real time.

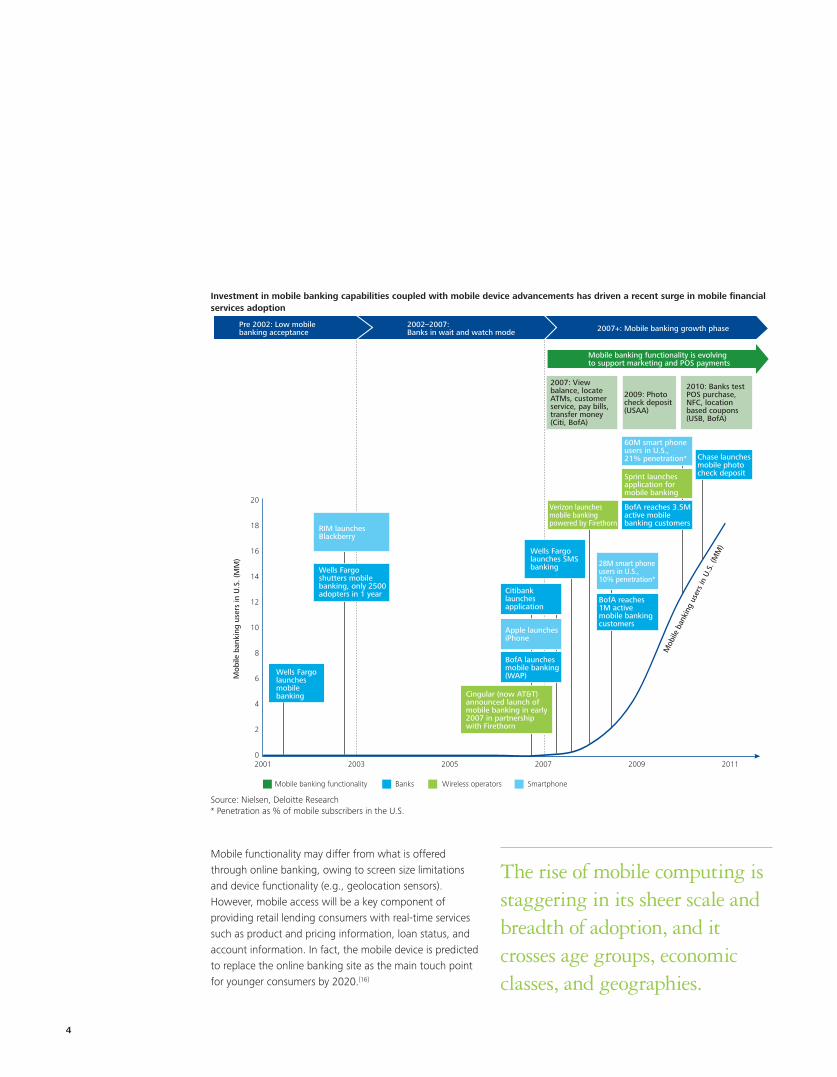

Mobile applicationsThe rise of mobile computing is staggering in its sheer scale and breadth of adoption, and it crosses age groups, economic classes, and geographies. Consumer interest in smartphones, tablets, and connected devices is growing faster than any other product segment, with a projected growth of 36 percent in the coming year,[12] and this trend shows no sign of abating.

Consider these growth forecasts for mobile devices:[6]

•The projected growth rate for use of these devices in North America between 2008 and 2012 is 27 percent.

•Smartphones are forecasted to represent 46 percent of the North American market by 2015, as well as 54 percent of the Western European market.

•Globally, more Smartphones than laptops were shipped in 2010 and are expected to outship the global PC market (including desktops) by the end of 2012.

Latin America’s mobile phone industry has a high degree of market penetration. Mobile subscriptions totaled 88.2 percent of the region’s population in 2009, compared to 55.2 percent in Asia Pacific, 90.4 percent in North America, and 50.6 percent in the Middle East and Africa.[14] The mobile phone market grew at a rate of over 10 percent in Mexico during 2009, with the number of users increasing to 79 million.[6] The adoption rate of mobile devices is even higher in some countries, such as Colombia, which has 42 million subscribers and a 92 percent mobile penetration rate. In 2010, Colombians made nearly 16 million financial transactions using their mobile devices.[15]

In countries where many consumers lack access to PC-enabled online banking, they do own mobile phones. As consumers grow accustomed to banking on these devices, mobile retail banking solutions must be able to deliver the full range of bank services that are available through other channels. By 2015, 10 percent of retail banking customers will use mobile devices to access most functions currently available via online banking.[16]

The transition to online loan origination is inevitable.

4

Investment in mobile banking capabilities coupled with mobile device advancements has driven a recent surge in mobile financial services adoption

Pre 2002: Low mobilebanking acceptance

2002–2007:Banks in wait and watch mode 2007+: Mobile banking growth phase

Wells Fargolaunches mobilebanking

RIM launchesBlackberry

Wells Fargoshutters mobilebanking, only 2500adopters in 1 year

Cingular (now AT&T) announced launch of mobile banking in early 2007 in partnership with Firethorn

BofA launches mobile banking (WAP)

Apple launchesiPhone

Citibank launches application

Wells Fargo launches SMS banking 28M smart phone

users in U.S.,10% penetration*

BofA reaches 1M active mobile banking customers

BofA reaches 3.5M active mobile banking customers

Sprint launches application for mobile banking

60M smart phone users in U.S., 21% penetration*

Verizon launches mobile banking powered by Firethorn

20010

20

18

16

14

12

10

8

6

4

2

Mobile banking functionality

Mob

ile b

anki

ng u

sers

in U

.S. (

MM

)

Mob

ile b

anki

ng u

sers

in U

.S. (

MM

)

Banks Wireless operators Smartphone

2003 2005 2007 2009 2011

Mobile banking functionality is evolving to support marketing and POS payments

2007: View balance, locate ATMs, customer service, pay bills, transfer money(Citi, BofA)

2009: Photo check deposit (USAA)

2010: Banks test POS purchase, NFC, location based coupons (USB, BofA)

Chase launches mobile photocheck deposit

Source: Nielsen, Deloitte Research* Penetration as % of mobile subscribers in the U.S.

The rise of mobile computing is staggering in its sheer scale and breadth of adoption, and it crosses age groups, economic classes, and geographies.

Mobile functionality may differ from what is offered through online banking, owing to screen size limitations and device functionality (e.g., geolocation sensors). However, mobile access will be a key component of providing retail lending consumers with real-time services such as product and pricing information, loan status, and account information. In fact, the mobile device is predicted to replace the online banking site as the main touch point for younger consumers by 2020.[16]

Retail Lending 3.0 Boosting productivity and improving the customer experience 5

Portable lending tools are also changing the lending landscape in terms of how employees are deployed. Lending leaders already have mobile advisers wielding iPads, BlackBerry devices, laptops, and other state-of-the-art mobile devices. These advisers are ready to talk about loans from anywhere – a local bank branch, a coffee shop, or even the dining room table. In emerging markets like Latin America, many alternative banking services (such as bill pay, deposits, and drafts) are offered by lottery houses, supermarkets, and drugstores. The emergence of new “bankers,” such as mobile operators and perhaps Internet portals, has led to diversification of banking services as the new players[3] use new ways to connect with their customers.

Progressive decisioningWhen customers apply for a loan, they have just one goal in mind: to receive an approval. Usually, consumers are emotionally invested in a loan request, whether they are purchasing a car or home, or starting a business. Delivering their loan decision rapidly and accurately will improve their lending experience and consequently their loyalty to your

organization. Even if you cannot approve the loan, the more quickly you can communicate that to the applicant, the better.

Loan decisions are becoming increasingly automated through the use of sophisticated decisioning technology that incorporates your unique lending guidelines. By combining this technology with “smart” application tools that tailor the loan interview to the applicant’s circumstances, you can improve efficiency and make the customer’s experience more positive. It is important to eliminate redundant information collection and delays in the approval process, as such inconveniences leave applicants frustrated and dissatisfied.

The retail lending space will be a key battleground for financial service providers. So whether you already incorporate these technologies into your lending strategy or are still evaluating their potential impact, it is important to consider how they can be used to sharpen your competitive edge by providing your customers with better service at a reduced cost – a win-win proposition for both parties.

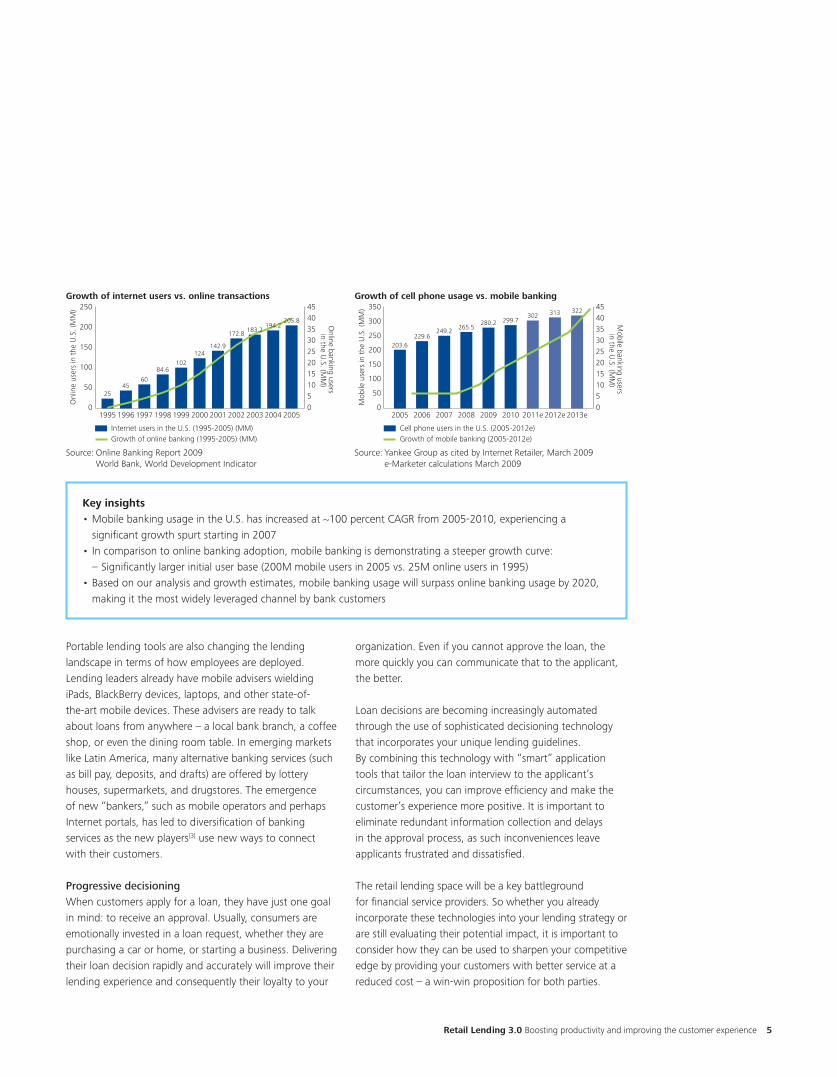

Growth of internet users vs. online transactions250

200

150

100

50

0

Onl

ine

user

s in

the

U.S

. (M

M)

Online banking users in the U

.S. (MM

)

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

45

3540

302520151050

2545

60

84.6102

124142.9

172.8 183.2194.2

205.8

Internet users in the U.S. (1995-2005) (MM)Growth of online banking (1995-2005) (MM)

Source: Online Banking Report 2009 World Bank, World Development Indicator

Growth of cell phone usage vs. mobile banking350

300

200

250

150

100

50

0Mob

ile u

sers

in t

he U

.S. (

MM

)

Mobile banking users in the U

.S. (MM

)

2005 2006 2007 2008 2009 2010 2011e 2012e 2013e

45

3540

302520151050

Cell phone users in the U.S. (2005-2012e)Growth of mobile banking (2005-2012e)

203.6229.6

249.2 265.5280.2

322

299.7302 313

Source: Yankee Group as cited by Internet Retailer, March 2009 e-Marketer calculations March 2009

Key insights•Mobile banking usage in the U.S. has increased at ~100 percent CAGR from 2005-2010, experiencing a

significant growth spurt starting in 2007•In comparison to online banking adoption, mobile banking is demonstrating a steeper growth curve:

– Significantly larger initial user base (200M mobile users in 2005 vs. 25M online users in 1995)•Based on our analysis and growth estimates, mobile banking usage will surpass online banking usage by 2020,

making it the most widely leveraged channel by bank customers

6

The customer experienceWhen it comes to banking, consumers expect quality customer service. Nearly 64 percent of Canadians plan to switch banks or have done so in the last year because of service-quality issues. In a recent survey, 34 percent of respondents said they “receive occasional or absolutely no personalized attention from their banks, making them easy targets for competitive offers.”[17] Banks looking to grow and retain their retail customers will need to make big improvements in these two key areas. In the United States, a 2010 survey of more than 48,000 retail banking customers revealed that overall satisfaction has decreased for the fourth year in a row, primarily as a result of low marks in customer service. According to the study, 37 percent of customers who changed their primary banking relationship in 2010 did so because of poor customer service at their previous bank.[18]

Globally, 36 percent of customers have changed their primary bank in the past, and 7 percent are planning to leave their current bank. The numbers are even higher in Brazil, where 40 percent of customers have changed their primary bank. Again, customer service is most often cited as the reason for choosing a new bank or financial institution. Interestingly, the study also found that Internet banking was the channel with the highest level of customer satisfaction – a resounding 83 percent.[19]

“High-touch” service is no longer defined as your borrower sitting with you in the branch. Lending is increasingly conducted outside of branches and call centers, with consumers electing to apply for loans over the Internet, by

phone, or at a third-party location. The around-the-clock convenience of the Internet has also radically altered customers’ expectations. Not only do they expect instant access to information, they expect immediate service tailored to their needs. “Needs-based” selling is having a radical effect on how financial institutions operate, and it requires better systems and processes to support it.[11]

This new reality of higher customer expectations requires more than technology; it also requires a new approach to engaging the customer.[20] Today’s borrowers expect to have real-time pricing information available at the click of a mouse. They expect an intuitive, simplified application process, whether it is delivered in person or over the Internet. They also expect results – with a streamlined approval process that delivers at least a preliminary decision quickly.

In this consumer-centric world, there are key opportunities in the lending process to enhance the borrowing experience. The area with the greatest potential for meaningful change is communication and collaboration with the applicant. For example, the transfer of documents needed to complete an application can be almost instantaneous in this age of email and handheld devices. You can offer your borrowers the option to deliver documents to you electronically, view their loan status or answer questions about their application online, and perhaps even sign their loan documents electronically. In this mobile age, the ability to engage your customers in a dialogue without requiring their physical presence may become a key differentiator.

The quality of the borrower’s experience must always be paramount. Regardless of the number of moving parts required to fulfill a loan request, the borrower will hold you, as the lender, accountable for the quality of the service provided. The more critical the experience (such as buying a home), the greater the potential impact if the service level is disrupted.

The around-the-clock convenience of the Internet has also radically altered the customer’s expectations.

Retail Lending 3.0 Boosting productivity and improving the customer experience 7

Emerging trends in retail lending

The retail lending marketplace is seeing changes, both in what consumers want and in how lenders are responding.

Trends in retail lending are driven by two prominent forces: first, applicants want a better borrowing experience, and second, lenders want to become more efficient – in terms of both productivity and cost. Combined, these forces define where the industry is going: toward “Retail Lending 3.0,” a truly positive customer experience combined with highly efficient business practices.

There are three key market trends changing the retail lending industry: increasing automation and mobility, increasing collaboration between borrowers and lenders, and improving customer centricity in lending products and marketing. These trends have different driving forces behind them (increasing business efficiency versus improving customer experience), but ultimately all three will contribute to the evolution of the retail lending process in the coming years.

Tren

d: In

crea

sing

front

-Lin

e &

back

-offi

ce a

utom

atio

n &

mob

ility

Trend: In

creasin

g collaboratio

n

between borro

wers & lenders

Trend: Improving customer centricity

& understanding customers’ needs

Target state:“Lending 3.0”

PoorCustomer experience

Low

Hig

hB

usin

ess

effic

ienc

y

Positive

Increasing frontline and back-office automation and mobilityRetail lenders are making changes to increase back-office automation while strengthening their mobile sales forces. These changes are largely driven by the need to increase operational efficiency, and to some extent, to improve the customer experience by accelerating business processes. The new technology makes it possible to integrate the origination and loan approval processes, allowing a loan application to be handed off automatically from origination to approval. Workflows are also becoming more automated, increasing the rates of auto-decisioning and preapproval. With broker-originated mortgages growing steadily in the United States and Canada (particularly among first-time home buyers and young borrowers), a mobile frontline sales force is becoming critical to reaching the growing population of prospective mortgage applicants.

In North America, the industry is also moving toward a paperless loan process that allows for increased automation and enables borrowers to receive, review, and approve documents online. In other parts of the Americas, hard-copy documents are more commonly used, although this may change over time as confidence in the technologies grows. Customer convenience will continue to drive the need to streamline and simplify the lending process.

Productivity gains are being realized by moving key functions – including credit retrieval, disclosures, and preapprovals – to the frontline point of sale. In addition, automating the business rules and processes associated with regulatory compliance increases efficiency in today’s complex and changing regulatory environment. Of course, lenders’ ability to automate and go mobile will largely be dictated by the flexibility and capabilities of their lending systems, particularly for origination and loan approval.

Customer convenience will continue to drive the need to streamline and simplify the lending process.

8

Increasing collaboration between borrowers and lendersYour borrowers want to work more effectively with you as much as you want to work more effectively with them. Because of the need to improve the customer experience and provide more personalized service, increased collaboration between applicants and lenders is an emerging trend in the marketplace. This trend includes improving communications, increasing access to advisers and services, streamlining borrower-lender interactions (e.g., needs-based interviews and selling), and accelerating lending processes and decisions.

Online or mobile technology can also be used to enhance the collaborative process. Online “smart applications” provide interactive, secure, real-time tools for customers to access their loan information, apply for loans, and monitor in-process applications 24/7. Online applications are also providing automated decisioning, including preapprovals and online disclosures. Mobile applications for smartphones and tablets further enable consumers (and brokers or agents) to access lending products on the go and communicate throughout the loan process.

Allowing applicants to transition easily and seamlessly between channels – online, mobile, telephone, branch – is equally important to increasing the level of collaboration between borrowers and lenders. This means that information must be shared across channels, in real time, providing the customer with “high-touch” service that is delivered consistently. Improving borrower-lender collaboration also requires a simplified employee experience in originating the loan. The optimum environment would include frontline adviser tools, and technologies to support needs-based interview wizards, “what-if” scenarios, and progressive decisioning support. These technologies allow you to work more closely with borrowers and move quickly toward a loan decision.

Improving customer centricity and understanding customer needsThere’s no better way to improve the customer experience than to demonstrate that you really know and understand your customers’ needs. Customer centricity (including customercentric marketing analytics) is an emerging trend in many retail markets. This is especially true in retail banking and lending. The industry is moving toward developing a single, unified view of the customer – incorporating personal, transactional, application, and product-selection data collected from all interactions with the financial institution – and using this data to perform rich analytics and needs assessments for individual borrowers.[21] Understanding your customers’ needs using their actual data lets you more effectively cross-sell other credit products (e.g., insurance, cards) at key decision points during the loan-application process, using marketing strategies specific to and optimized for each channel.

Assessing an applicant’s needs in real time during the loan application is also becoming increasingly important. Progressive decisioning during loan origination provides a customer experience that optimizes interview steps, product offerings, and cross-selling, based on the borrower’s responses. The wisdom of this approach seems obvious enough: get to know your customers better based on everything you already know about them and what you learn about them in real time. However, the approach also has drawbacks, which may be less obvious – implementing progressive decisioning often requires significant technology and business process reengineering.

There’s no better way to improve the customer experience than to demonstrate that you really know and understand your customers’ needs.

Retail Lending 3.0 Boosting productivity and improving the customer experience 9

Winning strategies

One way to improve the delivery of retail lending services and to capitalize on emerging trends in the marketplace is to examine the strategies that are transforming financial institutions into Retail Lending 3.0 operations. Origination and loan approval/decision systems are a good place to start.

Leverage the Web to gain visibility and reach new marketsIn an increasingly Web-based world, the Internet is not just the fastest-growing delivery channel – it is often the channel that consumers turn to first. If your organization does not have an effective website to capture prospects’ interest, they will quickly move on.

Common challenges with origination systems today:•Dated user interfaces with little automation

or intelligent workflow, resulting in a less than ideal experience

•Complex or redundant adjudication processes•Little or no integration among origination,

adjudication, and servicing systems

Internet-based lending can also dramatically increase your reach. You can serve borrowers entirely through the online channel, even if you do not have a branch location near them. The Internet thus offers a significant opportunity to access previously untapped markets without having to invest in infrastructure.

As you would expect, the online channel requires a specialized marketing approach. Although the Internet offers access to new prospects, it has also changed the competitive landscape, making it easier for borrowers to compare products, pricing, and service. You have only moments to satisfy customers’ needs when they visit your website, and if you don’t, you may lose them permanently.

Keep it simple – with intelligence behind itInnovators like Wikipedia, Facebook, and Google have set the standard for search, knowledge management, collaboration, and productivity.[20] You will be interacting with the same consumers who use these services when competing for their loan business, and they expect that same level of sophistication and service from you.

Consider the user experience of purchasing a book on Amazon. A powerful search engine not only displays your selection but suggests other books you might be interested in. With one click, you can check out and pay for your item. The next time you sign on, the system remembers your preferences and again offers you tailored selections. Although the process appears simple, you are responding to sophisticated software that provides you with “needs-based” recommendations based on your behavior.

Your lending process should function much the same way. Your loan application should be “smart,” meaning that the questions should change based on the borrower’s responses. Credit bureau information should automatically populate relevant data fields, and loan data should seamlessly integrate with the decisioning engine. By the end of the application process, borrowers should leave with a preapproval or some indication of whether or not they qualify for the loan.

Whether your borrowers apply online or in person, your goal should be to provide a simple and satisfying experience that delivers the level of service they have come to expect from other vendors.

Your loan application should be “smart,” meaning that the questions should change based on the borrower’s responses.

10

Think mobileThe mobile trend offers a real opportunity to offer value to your customers who use mobile devices. Most consumers use mobile applications today to perform simple banking functions like balance inquiries or payment transfers. As mobile applications expand to lending, consumers will need applications that are more targeted to specific tasks than to complicated multipurpose solutions. Navigation should be designed for single-hand or voice operation, should minimize interaction points, and should filter and pre-populate information where possible to simplify the user experience. Again, the message is “keep it simple.” The most effective mobile applications are specialized and intuitive.

Mortgage pre-approval use case[22]

Based on her location, the listing pops up, and her lender will display the estimated payment and whether she can qualify based on her existing approvals. She can request additional funds on the spot.

She gets a mortgage approval on the spot, and an appointment with the real estate agent

She walks down the street in her favorite neighborhood and starts an application. She points her device at a house with a “For Sale” sign.

Mary wants to purchase a house

Mortgagepre-approval

Today, there are iPhone, iPad, Android, and BlackBerry mobile apps available that enable consumers to access lending products on the go, compare and select programs, do quick loan applications and easily transition to other channels for a full application.

Develop a multichannel strategy that delivers a superior borrower experienceToday’s borrowers expect the same high-quality experience regardless of which channel – or channels – they use to apply. They may apply in a branch, by phone, over the Internet, or using a mobile device. In fact, they may use all of these channels over the course of their loan experience. To effectively compete in 2011 and beyond, you must be able to support borrowers through their preferred point of sale.

As part of developing your strategy, consider how you will market and deliver products differently through each channel. An effective multichannel strategy will drive greater product penetration, increased customer loyalty, and higher profitability. However, it may lead to fundamental changes in how your services are perceived and delivered. For example, there is much debate around the future role of the branch and how it fits into a multichannel model. The branch may evolve from a transactional location to more of a customer hub for providing advice, premium service, or support for more complex transactions. A change management strategy may also be needed to assist employees in adjusting to the new culture and changing their sales approach to support specific channels.

Today’s borrowers expect the same high-quality experience regardless of which channel – or channels – they use to apply.

Retail Lending 3.0 Boosting productivity and improving the customer experience 11

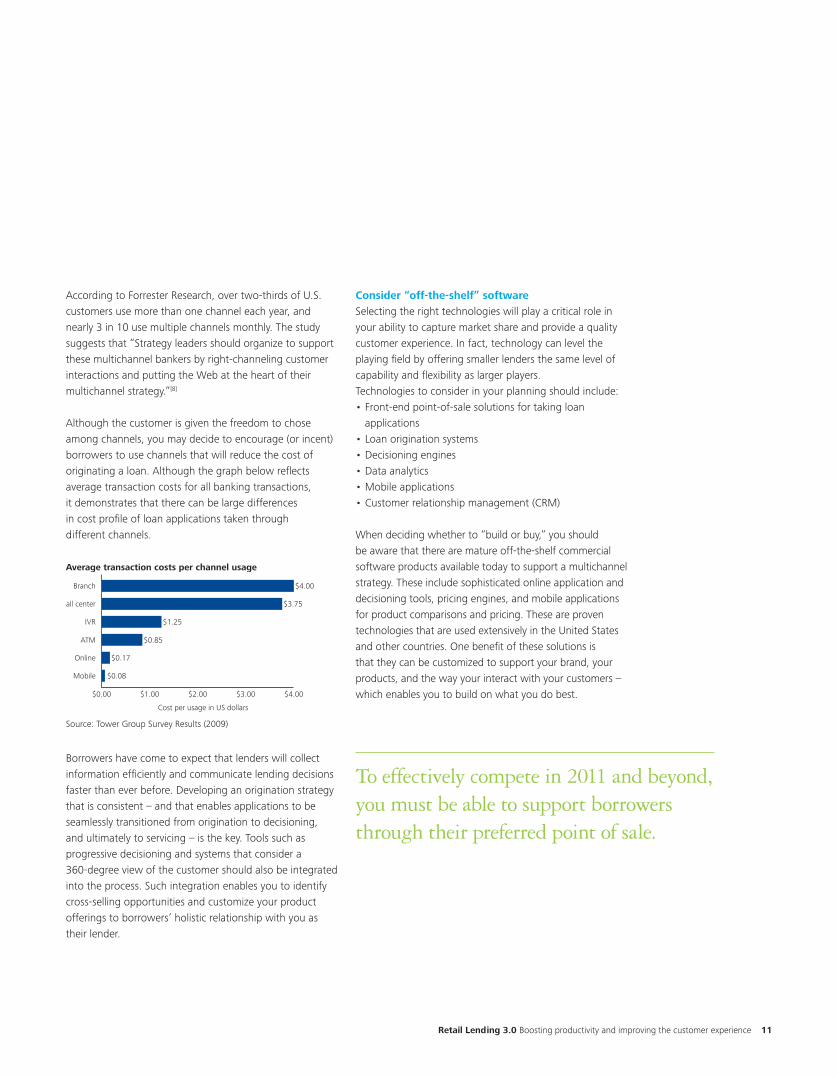

According to Forrester Research, over two-thirds of U.S. customers use more than one channel each year, and nearly 3 in 10 use multiple channels monthly. The study suggests that “Strategy leaders should organize to support these multichannel bankers by right-channeling customer interactions and putting the Web at the heart of their multichannel strategy.”[8]

Although the customer is given the freedom to chose among channels, you may decide to encourage (or incent) borrowers to use channels that will reduce the cost of originating a loan. Although the graph below reflects average transaction costs for all banking transactions, it demonstrates that there can be large differences in cost profile of loan applications taken through different channels.

Average transaction costs per channel usage

Branch

$0.00 $1.00 $2.00 $3.00 $4.00

$4.00

$3.75

Bank

cha

nnel

Cost per usage in US dollars

Call center

IVR

ATM

Online

Mobile

$0.85

$1.25

$0.17

$0.08

Source: Tower Group Survey Results (2009)

Borrowers have come to expect that lenders will collect information efficiently and communicate lending decisions faster than ever before. Developing an origination strategy that is consistent – and that enables applications to be seamlessly transitioned from origination to decisioning, and ultimately to servicing – is the key. Tools such as progressive decisioning and systems that consider a 360-degree view of the customer should also be integrated into the process. Such integration enables you to identify cross-selling opportunities and customize your product offerings to borrowers’ holistic relationship with you as their lender.

Consider “off-the-shelf” softwareSelecting the right technologies will play a critical role in your ability to capture market share and provide a quality customer experience. In fact, technology can level the playing field by offering smaller lenders the same level of capability and flexibility as larger players.Technologies to consider in your planning should include:•Front-end point-of-sale solutions for taking loan

applications•Loan origination systems•Decisioning engines•Data analytics•Mobile applications•Customer relationship management (CRM)

When deciding whether to “build or buy,” you should be aware that there are mature off-the-shelf commercial software products available today to support a multichannel strategy. These include sophisticated online application and decisioning tools, pricing engines, and mobile applications for product comparisons and pricing. These are proven technologies that are used extensively in the United States and other countries. One benefit of these solutions is that they can be customized to support your brand, your products, and the way your interact with your customers – which enables you to build on what you do best.

To effectively compete in 2011 and beyond, you must be able to support borrowers through their preferred point of sale.

12

Toward Retail Lending 3.0: The next steps

The face of lending may look quite different in the next few years as loans are delivered in new and innovative ways. A local branch might look more like a relaxing café than a traditional teller line. A loan application might be completed in the applicant’s home, at a kiosk in a grocery store, or over the Internet. In fact, rather than being impersonal, the Internet may be the way that you deliver “high-touch” service with 24/7 round-the-clock access, immediate loan decisions, and real-time “chat” opportunities with your borrowers. Technology makes it possible to treat every applicant as though he or she is in a “class of one,” with products and services personalized to that individual’s needs. These ideas may seem futuristic, but your social-media-savvy customer expects it, and your competitor is looking for a way to get there first.

Implementation challengesThe journey toward Retail Lending 3.0 is an exciting one, and arriving at the desired target state should prove highly beneficial. However, our experience indicates three common challenges that you may encounter in making the transition:•Managing cultural change within your organization as

you transition to a customercentric business model•Successfully integrating disparate systems to support

a lending experience that appears seamless to the customer

•Developing effective marketing and communication strategies that are specific to each channel and appropriate to the sales cycle

Deloitte understands the journey – and the challenges – and we have proven methodologies and experience to achieve measurable, sustainable results while mitigating risk. We work with you to develop a unified approach focused on improving the customer experience while managing your costs, to create a better experience for both your borrowers and your employees. Our objective is to help you make the right investment decisions, both for your dollars and your efforts.

We are well positioned to assist you through this journey. With global lending subject-matter expertise, cross-discipline service offerings, and insight into solution options complemented by strong vendor relationships, our Consulting, Financial Advisory, and Enterprise Risk Services teams have the necessary experience and know-how to guide you through your journey.

We look forward to the opportunity to share additional insights and experiences with you.

Technology offers the ability to treat every applicant as though he or she is in a “class of one,” with products and services personalized to the individual’s needs.

Retail Lending 3.0 Boosting productivity and improving the customer experience 13

References[1] Jason Kirby, “Awash in a Sea of Debt,” Maclean’s, 2 February 2010, http://www2.macleans.ca/2010/02/02/

awash-in-a-sea-of-debt/.[2] Trefis Team, “Consumer Credit Rebound Kicks Capital One up to $61,” Forbes, 15 February 2011, http://blogs.forbes.

com/greatspeculations/2011/02/15/consumer-credit-rebound-kicks-capital-one-up-to-61/.[3] Anuradha Mallya, “LATAM - Banking on a Brighter Outlook,” InfoSys FinacleConnect, http://www.infosys.com/finacle/

finacle-connect/Issue_18/kali2.asp.[4] Joe Leahy, “Fraga Warns on Brazilian Credit Growth,” 23 February 2011, http://www.ft.com/cms/s/0/a4ce09e2-3f89-

11e0-a1ba-00144feabdc0.html#axzz1L35nKm1d.[5] “Resume: Baking and Mobile Market in Columbia,” Deloitte, April 2011.[6] “Leveraging the Mobile Channel as a Catalyst to Improving Overall Bank Performance,” Deloitte, February 2011.[7] Megan Harman, “Canadians flock to online banking,” Investment Executive, 28 July 28 2010, http://www.

investmentexecutive.com/client/en/News/DetailNews.asp?Id=54442&IdSection=147&cat=147.[8] Emmett Higdon & Peter Wannemacher, “How US Banking Customers Use Different Channels,” Forrester Research, 26

July 2010, http://www.forrester.com/rb/Research/how_us_banking_customers_use_different_channels/q/id/56822/t/2.[9] “Online Lending: The New Reality,” Lieberman Research Group, August 2010.[10] Annette Tirabasso, “The Silver Lining in Lending: Turning Doubters into Online Believers,” Deloitte Inc., 2007, http://

www.deloitte.com/assets/Dcom-UnitedStates/Local%20Assets/Documents/us_fsi_onlinebanking_May08.pdf.[11] EFMA & Microsoft, “Transforming Retail Banking to Reflect the New Economic Environment,” 2010, http://download.

microsoft.com/download/B/8/C/B8C335B3-9316-4604-BA57-B59C88478221/Microsoft%20EFMA%20Report%20-%20Transforming%20Retail%20Banking%20to%20Reflect%20the%20New%20Ecomonic%20Environment.pdf.

[12] Byron Acohido, “Banking Trojans Infest Internet,” 22 February 2009, http://lastwatchdog.com/banking-trojans-infest-internet/.

[13] “Depth Perception: A dozen technology trends shaping business and IT in 2010,” Deloitte, 2010, http://www.deloitte.com/us/2010technologytrends.

[14] Countries and Consumers team, “Latin America Enjoys Mobile Telephone Boom,” Euromonitor Global Research Blog, 28 May 2010, http://blog.euromonitor.com/2010/05/regional-focus-latin-america-enjoys-mobile-telephone-boom.html.

[15] “Banking and Mobile Market in Columbia,” Deloitte, April 2011.[16] Richard De Lotto, Stessa Cohen, Mary Knox & David Schehr, “Predicts 2010: In Banking and Investment Services,

Business as Usual Won’t Meet New Customer Demands,” Gartner, 4 November 2009, http://www.gartner.com/DisplayDocument?doc_cd=171956.

[17] Joel McKay, “Retail Bank Customers on the Hunt for First-Rate Service: E&Y,” Business in Vancouver, 12 March 2011, http://www.bivinteractive.com/index.php?option=com_content&task=view&id=3847&Itemid=32.

[18] “2010 Retail Banking Satisfaction Study,” JD Power and Associates, http://www.jdpower.com/finance/articles/2010-Retail-Banking-Satisfaction-Study/.

[19] “Global Consumer Banking Survey 2011,” Ernst & Young, 2011, http://www.ey.com/Publication/vwLUAssets/A_new_era_of_customer_expectation:_global_consumer_banking_survey/$FILE/A%20new%20era%20of%20customer%20expectation_global%20consumer%20banking%20survey.pdf.

[20] “Tech Trends for 2011 - The Natural Convergence of Business and IT,” Deloitte Consulting LLP, 2011.[21] Vanessa Niemeyer, “Driving Sales On Banks’ Secure Sites – Global Best Practices,” Forrester Research, 20 July 2009,

http://www.forrester.com/rb/Research/driving_sales_on_banks_secure_sites_%26%238212%3B/q/id/53456/t/2.[22] Andrew Szabo, “Augmented Reality,” Deloitte Inc., February 2009.

About Deloitte

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s approximately 182,000 professionals are committed to becoming the standard of excellence.

This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this publication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication.

© 2012 Deloitte Global Services Limited

Designed and produced by The Creative Studio at Deloitte, Canada. 11-973G

About the authorsNancy MonsonDeloitte Canada+1 780 719 [email protected]

Nancy is a manager with Deloitte’s Technology Strategy practice in Edmonton. She has nearly 30 years of retail lending experience with a focus on mortgage and online origination technologies in the United States. Nancy specializes in evaluating and selecting lending software, conducting process and workflow analysis, and implementing technology to support lending initiatives. Typically, her projects involve requirements gathering, vendor selection, IT strategies, systems integration, and implementation.

Joel SoDeloitte Canada+1 416 601 [email protected]

Joel is a senior manager with Deloitte’s Technology Strategy practice in Toronto. He has over nine years of industry experience with a special focus on financial services technology – in particular, retail lending, core banking, cash management, and payments systems. His areas of specialization include business-IT alignment, strategic IT architecture and roadmap development, solution and vendor selection, and IT business casing. One of Joel’s recent projects involved assisting a Canadian bank with retail lending platform transformation, including solution selection, requirements gathering, and business case development.

Matthew RossiterDeloitte Canada+1 416 775 [email protected]

Matt is a senior consultant with Deloitte’s Strategy & Operations practice in Toronto. He focuses on corporate strategy within the financial services industry. Matt has over four years of industry experience, and during that time he has worked in retail lending and mortgages, global payments, commercial banking, and technology strategy with Canada’s largest financial services institutions. Matt’s functional experience includes mortgage process redesign, retail customer segmentation and strategy, requirements gathering and assessment, resourcing requirements modeling, and business case development.

Justin ChuDeloitte Canada+1 416 601 [email protected]

Justin is an analyst in Deloitte’s Technology Consulting practice in Toronto. He has project experience in designing and implementing technology solutions, with a focus on delivering projects to clients in the financial services industry. Justin specializes in projects related to IT service management process engineering, business-technology strategic alignment, and RFP vendor selection processes.