retail research template - altech chemicals limited dj carmichael...distinguishing feature of...

TRANSCRIPT

D J Carmichael Pty Limited ABN 26 003 058 857 AFSL 232571

Telephone: 08 9263 5200 Facsimile: 08 9263 5283 Email: [email protected] Webpage: http://www.djcarmichael.com.au

RESEARCH

Industrials

Altech Chemicals Ltd (ATC-AU)

Analyst

Paul Adams

Director, Head of Natural Resources

+61 89 263 5200

2 19 February 2016

RESEARCH

Industrials

Table of Contents

1. Front Page-Key Points

2. Corporate Summary

3. Valuation and Recommendation

3.1. Valuation Summary

3.2. WACC Analysis

3.3. Comparable Analysis

Summary

Orbite Technologies Inc

Recent transactions

Sensitivity Analysis

4. Summary Financials Sheet

5. Share Price Catalysts

6. SWOT Analysis

7. Risks and Mitigating Actions

8. Progress on project financing

8.1. Mandate executed with Kfw-IPEX Bank

8.2. What is ECA Cover and how does ATC benefit?

9. ATC Sales & Marketing Strategy

9.1. Agreement with Mitsubishi, Japan

9.2. Marketing Manager, China

10. Bankable Feasibility Study outcomes

10.1. Summary conclusions

10.2. Major Assumptions

10.3. Production ramp-up schedule

10.4. Capital cost estimates

10.5. Operating costs

10.6. Selling price assumptions

10.7. Discount rate and NPV

11. Corporate Summary

11.1. Corporate Structure

11.2. Capital Structure & Shareholders

12. Upstream Items

12.1. Meckering Aluminous Clay Resources

12.2. Approvals

12.3. Second kaolin deposit at Kerrigan

12.4. Mining Rights to Dana

19 February 2016 3

RESEARCH

Industrials

13. Downstream Items

13.1. HPA Plant Site, Tanjung Landsat Industrial Park, Johor

13.2. Major consumables from sister industrial Park

13.3. ATC’s HPA processing facility

13.4. Design philosophy

13.5. Patented process steps

13.6. Optimisation study

13.7. Major Processing Steps

13.8. Process Plant Flow Diagram

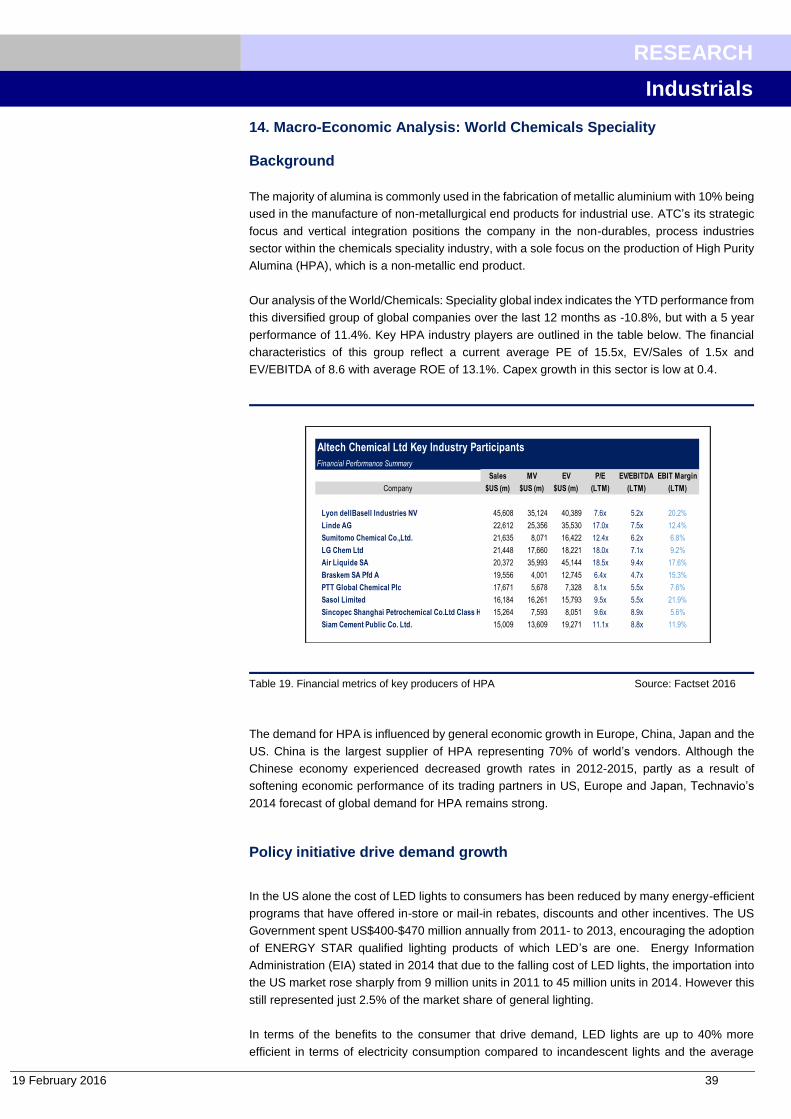

14. Macro-economic Considerations for HPA

14.1. Background

14.2. Policy initiatives to drive growth

14.3. HPA Demand

14.4. HPA Supply

14.5. Sapphire glass market

14.6. Potential influence of Apple Inc.

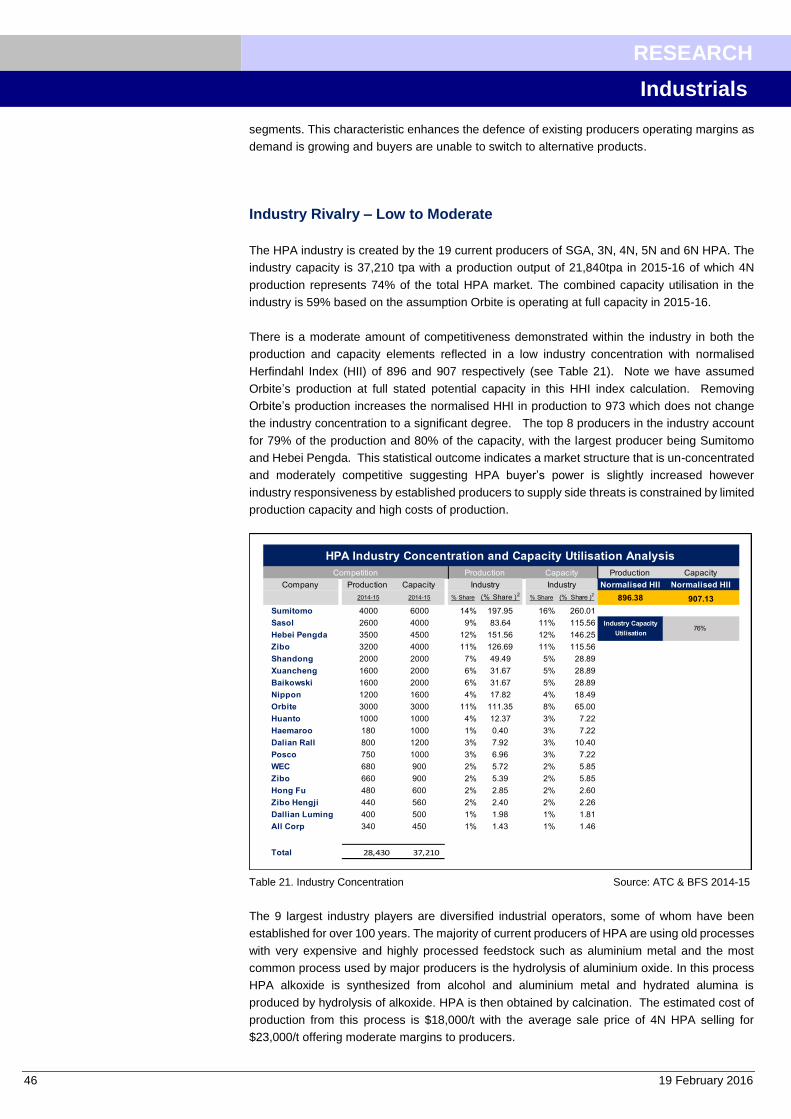

15. HPA Industry Analysis

15.1. Industry attractiveness

15.2. Bargaining power of buyers

15.3. Bargaining power of sellers

15.4. Threat of new entrants

15.5. Threat of substitutes

15.6. Industry rivalry

15.7. ATC’s sustainable competitive advantage

16. Project Schedule

17. Board and Management

4 19 February 2016

RESEARCH

Industrials

Altech Chemicals Ltd (ATC) Speculative Buy

Unique opportunity in high-tech chemicals

Altech Chemicals Ltd (ATC. ASX) is a speciality chemicals company developing a

vertically integrated High Purity Alumina (HPA) project. ATC is unique in that it uses a

process to convert aluminous clay, sourced from its own quarry in Western Australia

(WA), to HPA in a simple, highly cost effective process with operating costs a fraction of

its larger, more established peers. ATC follow a conservative development strategy,

using management’s extensive experience in building chemical plants, with the aim to

be one of the world’s largest producers of HPA. HPA is being used in a growing number

of high tech applications and is set to have a CAGR of 19.7% to 2021.

Key Points

HPA. What is it and what is it used for? HPA (99.99% Al2O3) is sold as a white powder and

is the base material for the manufacture of sapphire substrates, scratch proof sapphire glass

and as a coating on separators used in lithium-ion batteries. Most HPA is used in the

manufacture of LED’s, alumina semi-conductors and phosphor TV screens but it is

experiencing a wider and growing use in smartphones and Li-ion battery applications amongst

others (aerospace, medical, defence). Government Policy and public awareness on energy

saving is, in part, driving the increased usage of these products. ATC is developing a large

HPA project with its own source of feedstock from a quarry in WA and its own HPA plant based

in Malaysia. The Asia–Pacific region is expected to see the highest growth in use of HPA over

the coming years.

Most competitors are using old processes: Most existing producers of HPA exist as small

business units in very large industrial conglomerates, using processing routes that re-refine

aluminium metal that was produced from bauxite via the Bayer Process, to produce HPA. This

is expensive and very energy intensive. High labour costs also add to operating costs. More

recently, aluminium waste products are being used as a feedstock, but ATC has a sustainable

competitive advantage in that it will use an inexpensive, white, very pure aluminous clay as a

feed source.

Project financing: ATC executed an exclusive mandate with Kfw IPEX-Bank GmbH for the

provision of services relating to project financing of its HPA project. The mandate contemplates

the arrangement of senior debt project financing aimed at utilising, to the maximum extent, an

Export Credit Agency (ECA) insurance cover under German-backed project finance export

guarantees. ATC estimate that approximately US$40m of the estimated total US$77m project

capital cost will qualify for ECA cover. An additional $15m of senior debt financing will be

required.

Very robust financial metrics: The current macroeconomic environment in the medium term

favour ATC’s strategic intent. Global 4N HPA demand is set to increase significantly with a

forecast CAGR of 19.7%. This fact and new market developments support ATC’s projected

operating margins. ATC’s planned production facility operates with an attractive contribution

margin generating sustainable gross operating margins of between 60-80% and EBIT margins

of 50%. Unlevered free cash flows are robust with the HPA project generating an IRR of 29%

with a payback period of 5 years.

Recommendation and Valuation: We place a Speculative Buy recommendation and our

risked valuation of $0.41 a share.

12 Month Performance

Source: FactSet

ATC-AU

Current Share Price 0.09$

Current Market Cap $m 14$

Base Case Valuation ($Mcap m) 302.8$

Base Case Valuation ($/sh) 0.81$

Project Stage Risk Discount 50%

Target Price Current Stage ($/sh) 0.41$

Altech Chemicals Ltd

19 February 2016 5

RESEARCH

Industrials

2. Corporate Summary

ATC is a specialty chemicals company, focused on the development of a processing plant that

has the capacity to produce up to 4,000 tonnes of high purity alumina (HPA) per annum for

delivery into the high tech manufacturing industries. Under full capacity, ATC would rank in the

top 3 producers of HPA globally, but more importantly, one of the lowest cost producers. The

distinguishing feature of ATC’s operations is the one-step processing route from aluminous clay

to HPA using hydrochloric acid, rather than having to derive HPA by re-refining aluminium metal

that has been produced from bauxite via the Bayer process.

HPA is an essential component for the manufacture of LED lighting – currently providing 55%

of global HPA demand – and a number of other applications in the high tech space including

the manufacture of sapphire glass, the glass currently employed for high quality watch faces

and mobile phone camera lenses and home button, and soon, the facing glass for new mobile

phone releases. Other applications lie in phosphors (16%) and semi-conductors (22%). Lithium-

ion battery separators could also be a large, growing market for products derived from HPA.

ATC has two upstream sources of high grade aluminous clay from its 100% owned JORC

complaint deposits in WA. Current resources would supply many decades of feedstock at

anticipated mining rates. ATC has also secured a ~4Ha plot of land in a major industrial park in

Johor, Malaysia, where it will build its HPA processing plant. Total capital costs are anticipated

to be ~US$77m.

ATC has already completed a Bankable Feasibility Study (BFS) for the project. Approximately

50% of the plant and equipment is of German or European origin, and consequently ATC has

received an LOI from Euler Hermes Aktiengesellschaft (“Hermes”) in Hamburg, Germany

confirming in-principle support under the export credit insurance guarantee scheme (ECA) from

the Federal Republic of Germany (subject to due diligence), potentially covering 73% of the total

project debt financing. ATC has also executed a mandate with German bank Kfw IPEX-Bank in

relation to securing senior debt project financing.

ATC expect to close project financing by Q4 2016 and begin construction early 2017.

ATC is a specialty chemicals company aimed at providing high purity alumina (HPA) to high tech manufacturing industries

6 19 February 2016

RESEARCH

Industrials

3. Valuation and Recommendation

The financial analysis and valuation of ATC was undertaken after the completion of a thorough

economic and strategic evaluation of the HPA market and ATC’s strategic position. We

completed a Porters Five Forces strategic analysis to review ATC’s sustainable competitive

advantage and developed a level of subjective confidence in relation to ATC’s operating

margins and determined them to be defendable for purposes of the valuation process. We

believe that we have applied a level of risk adjustment to the valuation model to accommodate

the short to medium term economic forces in the HPA industry.

Valuation Summary

The valuation process involved a combination of techniques involving the review of comparable

companies and precedent transactions in order to determine the most appropriate

benchmarked exit multiple for ATC within the Specialist Chemical industry sector.

With the appropriate exit multiple established a WACC analysis was completed initially using a

number of variables from the BFS to establish managements predicted valuation. DJC then

developed a list of comparable companies, de-levered then re-levered the WACC then applied

a series of adjustments to de-risk the financing elements of the HPA project making allowance

for the enterprise size and its position within its life cycle.

The number of industry participants involved in the HPA market is relatively small, yet the

industry concentration is not strong. ATC are unique in terms of their focused strategy and as

a result identifying comparable companies was challenging. Most HPA producers are

established diversified groups. The closest comparable we identified was Orbite Technologies

Inc, in Canada. However it does not have an operating financial history for comparison

purposes and so it was evaluated against ATC as outlined below in Table 6.

The DCF analysis was performed with a downside, upside and base case scenario analysis.

Furthermore, a thorough sensitivity analysis was complete on key outputs as outlined in Table

8 & 9. In our base case analysis we applied a significant discount to current HPA prices being

achieved by Sasol (≈ €36/kg). Note that prices vary according to the product quality.

An exchange rate of AU$0.70 is maintained throughout the model. The future operating

margins are diminished by escalating costs at a faster rate than price rises (negative jaws). For

the debt assumptions we ignored any financing benefits that may be derived from the potential

financing deal from Kfw IPEX-Bank GmbH Germany utilising ECA cover.

In terms of future potential dilution, new equity issues were assumed on the basis of a rising

share price with the first tranche of shares will be issued at AU$0.10, March/April 2016 and the

second tranche issued at AU$0.20 October/November 2016.

The Malaysian corporate tax rate is 25% and there is no withholding tax on dividends back to

Australia. In addition no allowance has been given in this model for the 60% uplift on total

Capex value for calculating depreciation deductions in Malaysia which can be offset against

70% of the operating profits for the first five (5) years of operations. Management have

indicated that this depreciation allowance may possibly extend for another five (5) years

suggesting a very low corporate tax rate in at least the first five years, and possibly ten years,

of operations.

19 February 2016 7

RESEARCH

Industrials

Table 1. Valuation scenario table Source: DJC research

Recommendation and Valuation: We place a Speculative Buy recommendation and our

risked valuation of $0.41 a share.

Variables Management Downside Base Upside

Currency $AU $AU $AU $AU

Exchange Rate 0.90$ 1.00$ 0.70$ 0.70$

Price Inflator 0% 0% 2% 5%

Cost Inflator 0% 3% 5% 2.5%

Prices

Price Change Assumptions 0% -15% 0% 20%

HPA SGA Price 0.44$ 0.37$ 0.44$ 0.53$

HPA 3N Price 10.00$ 8.50$ 10.00$ 12.00$

HPA 4N Price 25.56$ 21.73$ 25.56$ 30.67$

Cost of Capital

WACC (After Tax) 7.4% 12% 10% 6.5%

Percentage Debt Funded by KfW 80% 0 0% 80%

Debt to Equity 70% 70% 70% 70%

Cost of Debt After Tax 3.4% 10% 7.2% 3%

Size Premium 5% 7% 6% 3%

Levered Beta 1.85 1.85 1.85 1.85

Risk Free Rate 3% 3% 3% 3%

Market Risk Premium 5% 5% 5% 5%

Capital Structure

Shares on issue (undiluted) 152,612,782 152,612,782 152,612,782 152,612,782

First Tranche Issue Price 0.10$ 0.08$ 0.10$ 0.15$

Second Tranch Issue Price 0.45$ 0.10$ 0.20$ 0.50$

New Issues & Options

First Tranche Shares Issued 40,000,000 50,000,000 40,000,000 26,666,667

Second Tranche Shares Issued 68,888,889 310,000,000 155,000,000 62,000,000

Options 25,350,000 25,350,000 25,350,000 25,350,000

Total Shares on Issue Fully Diluted 286,851,671 537,965,782 372,965,782 279,965,782

Valuation

EV/EBITDA Exit Multiple 9 5 7 11

IRR 28% 24% 28% 34%

Payback Period (Years) 5 7 5 5

Terminal Value/EV % 56% 46% 49% 62%

Enterprise Value ($m) 521,246$ 168,069$ 379,359$ 882,454$

Implied Equity Value ($m) 444,212$ 91,036$ 302,325$ 805,420$

Indicative Share Price ($/sh) 1.55$ 0.17$ 0.81$ 2.88$

Assumptions

Managements cost of debt asssumes KfW funding at Libor +2%.

Median/ Mean Median/Mean

LTM EV/EBITDA ($10m EV) 6.1/ 11.6 15$ $92/$174 0.25$ 0.46$

2016E EV/EBITDA ($50M EV) 6.7/10.1 50$ $333/506 0.89$ 1.36$

2017E EV/EBITDA ($100 EM) 7.9/8.0 100$ $794/$797 2.14$ 2.13$

Median/ Mean 15$ Median/Mean

2015-2016 LTM EV/EBITDA 10.1/10 15$ $101/$100 0.41$ 0.40$

Precedent Transactions Specialist Chemicals Sector Inidicative Pricing

EV/EBITDA Exit

Multiple

EV (estimated

$m)

Ent Value

(estimated $m)

Indicative

Share Price

($/Sh)

Indicative

Share Price

($/Sh)

EV/EBITDA Exit

Multiple

EV (estimated

$m)

Ent Value

(estimated $m)

Public Company Comparables Specialist Chemicals Sector Indicative Pricing

Altech Chemicals Ltd Valuation Scenarios and Comparisons for HPA

Project Meckering & Johor Summary

DJC Modeling Assumptions

Discounted Cash Flow Input Variables

ATC

8 19 February 2016

RESEARCH

Industrials

DJC applied a number of discount factors to capture a risk adjusted indicative share price as

outlined below.

Table 2. Risk Adjusted Valuation table Source: DJC research

Further risk adjustments were made with a higher discount rate of 10% with an average post-tax

cost of debt of 7.2%, An exchange rate of AU/USD:0.70 and an average 4N HPA price of

AU$25.56/kg were applied. The base case pricing reflects a 45%-56% discount on current prices

paid by European buyers for 4N HPA. The indicative share price is based an enterprise value

of AU$345.6m with an implied equity value of AU$302.3m and a fully diluted share capital of

372,965,782 shares.

Based upon these assumptions, ATC’s HPA project generated an IRR of 29% with a payback of

6 years (full year analysis only) with a reasonable exit EV/EBITDA multiple of 7. Given the long

term nature of this project we considered a terminal value of 52% reasonable.

3.2 WACC Analysis

ATC intend to fund 80% of its debt via Kfw IPEX-Bank GmbH facility with the remainder from

alternative commercial sources. Indications from potential funders is that debt supported by ECA

cover will be offered at around LIBOR plus 2% and the terms and conditions of these potential

loans offer greater flexibility to ATC in terms of future repayment schedules. For the purposes of

the WACC calculation we applied general commercial rates of between 9-12% to all components

of the debt and added a significant size premium to account for current stage of development of

the project.

As the debt will be issued to fund the Malaysian plant development, a 25% tax rate was applied.

In terms of the beta we developed a list of comparable entities unlevered the beta then re-levered

to establish a levered beta of 1.85.

The risk free rate was interpolated from a 10 year AUD Treasury Bond as this rate more than

covers the period of time of the debt funding as outlined in the project. In this process we applied

a WACC of 10%.

Variable Risk Adjusted Impact Comments

4N HPA Sales Included in model 45% HPA price reduction built into DCF

Depreciation Included in model 15% share price inflation from Capex uplift disallow ed

Financing Risk 10% Additional Risk Factor

Execution Risk 25% Additional Risk Factor

Operation Risk 15% Additional Risk Factor

50%

Current Indicative Price 0.81$

Less Risk Discount 0.41$

Target Price 0.41$

Total Added Risk

Discount

Altech Chemicals Ltd: Risk Adjusted Implied Valuation

19 February 2016 9

RESEARCH

Industrials

Table 3. WACC calculation summary Source: DJC research

3.3 Comparable Analysis

Summary

A universe of comparable companies to ATC acts as the foundation of the trading comparisons

valuation methodology. This was developed in order to identify companies with similar business

strategies and financial characteristics to that of ATC.

Orbite Technologies Inc, is a comparable technical competitor listed on the TSX-listed which is

intending to move into production this quarter. As it has not yet generated sustainable earnings

it was not included in the comparable list, instead it was evaluated on a stand-alone basis as

outlined below.

This universe of comparables was interesting as no particular entity mirrored ATC in size, sector

positioning nor strategic focus. Furthermore, a significant number of the identified market

participants are private and non-reporting companies based in China. Outlined below are the list

of selected companies.

Altech Chemicals Ltd Weighted Average Cost of Capital Analysis

($ in millions)

Target Capital Structure Predicted Market Market Debt/ Marginal Unlevered

Debt-to-Total Capitalization 70.0% Company Levered Beta(4) Value of Debt Value of Equity Equity Tax Rate Beta

Equity-to-Total Capitalization 30.0% Mersen SA 0.51 265.70$ 455.20$ 58.4% 30.0% 0.36

Toyo Tanso Co., Ltd. 0.87 5,046.96$ 59,179.60$ 8.5% 30.0% 0.82

Norsk Hydro ASA 0.94 11,167.00$ 74,030.00$ 15.1% 30.0% 0.85

Cost of Debt SEC Carbon Ltd. 0.53 1,626.00$ 34,784.00$ 4.7% 30.0% 0.52

Cost of Debt 9.55% Alcoa Inc. 1.23 9,103.00$ 12,244.00$ 74.3% 30.0% 0.81

Tax Rate 25.0%

After-tax Cost of Debt 7.2% Mean 0.82 32.2% 0.67

Median 0.87 15.1% 0.81

Cost of Equity

Risk-free Rate(1) 2.72% Mean Target Target

Market Risk Premium(2) 4.8% Unlevered Debt/ Marginal Relevered

Levered Beta 1.85 Beta Equity Tax Rate Beta

Size Premium(3) 6.00% Relevered Beta 0.67 233.3% 25.0% 1.85

Cost of Equity 17.6%

WACC 10% 10.3% 8.6% 9.1% 9.6% 10.1% 10.6%

50.0% 10.4% 10.6% 10.8% 10.9% 11.1%

60.0% 10.1% 10.3% 10.5% 10.7% 11.0%

70.0% 9.8% 10.0% 10.3% 10.6% 10.8%

80.0% 9.5% 9.8% 10.1% 10.4% 10.7%

90.0% 9.1% 9.5% 9.8% 10.2% 10.5%

(1) Interpolated y ield on 10-year AUD Treasury Bond Issued Jan 2015

(2) Obtained from www.Market-Risk-Premia.com-Dec 2015

(3) Micro-Cap size premium based on market capitalization Brand.

(4) Sourced from Factset

(5) Libor plus 2% as issued by German bank KFW and approved by ECA (Germany)

(6) Libor 1 month USD 0.42 _Factset

Deb

t-to

-To

tal

Cap

ital

izat

ion

WACC Calculation Comparable Companies Unlevered Beta

WACC Sensitivity Analysis

Pre-tax Cost of Debt

10 19 February 2016

RESEARCH

Industrials

Table 4. Comparable companies operating in Speciality Chemicals Source: DJC research

In terms of the analysis, each companies five (5) year historic financial data and key financial

metrics were reviewed. Growth rate assumptions of each entity were derived and projected

forecasts were applied two (2) years ahead based upon collected data.

Each entities general information, reported and adjusted income statements, balance sheet,

cash flow statement, trading multiples, selected market data, issued capital, LTM return on

investment ratios, and LTM credit statistics were analysed.

Based upon the analysis of the historic financial data 1 year, 2 year and 5 year CAGR’s were

determined where possible and estimated forward looking growth rates for 1 and 2 year out.

The list of companies was summarised into two benchmarking worksheets, comparing market

valuation, LTM statistics, profitability margins, growth rates, ROI, LTM leverage and coverage

ratios. This information was tiered into large cap, mid cap and small cap companies.

Two key output worksheets were derived from this information comparing historic LTM EV, price

and exit multiple analysis.

The final step was to establish industry sector minimum, maximum, median and mean values for

key financial metric outputs. This analysis allowed us to determine the most reasonable

EV/EBITDA exit multiples that would be applied to the DCF model.

The results, outlined in the table below, indicate the mean and median exit multiple for 2016E is

5.9-7.9x EV/EBITDA.

Equity Enterprise LTM

Value ($m) Value ($m) Sales ($m)

Altech Chemicals Limited Prov ides mineral ex ploration serv ices 15$ 14$ -$

Sasol Limited Manufactures industrial chemicals 17,127$ 16,368$ 2,802-$

Alcoa Inc. Manufactures aluminum products, fabricated aluminum and other alloy s 9,551$ 18,819$ 21,442$

Sumitomo Chemical Co., Ltd. Manufactures and distributes basic chemicals, petrochemicals, fine and agrichemicals 8,245$ 17,373$ 29,860-$

Norsk Hydro ASA Manufactures aluminum products and produces renew able energy 6,799$ 7,037$ 14,251$

United Co. RUSAL Plc Produces aluminum, alloy and related products 4,334$ 12,724$ 6,227$

Aluminum Corporation of China Limited Class H Engages in the manufacturing and distribution of alumina, primary aluminum and aluminum fabricated products 1,181$ 7,336$ 15,268$

Shenzhen Desay Battery Technology Co., Ltd. Class A Manufactures alkaline manganese, alkaline and lithium batteries; produces battery chargers and adapters 1,142$ 983$ 1,494$

Vedanta Resources plc Engages in mining of copper, zinc, aluminum and iron ore metals 933$ 27,120$ 12,793$

Nippon Light Metal Holdings Co., Ltd. Manufactures aluminum products 928$ 1,706$ 11,080$

Blue Solutions SA Engages in the production and marketing of electricity storage components and solutions 536$ 558$ 146$

Mersen SA Manufactures and distributes materials and electrical components for the industrial sector 300$ 546$ 1,004$

Toyo Tanso Co., Ltd. Engages in the production and sale of isotropic graphite and other specialized carbon products 286$ 220$ 790$

Tokai Carbon Korea Co., Ltd. Manufactures carbon fibers including silicon w afers and semiconductor materials 263$ 257$ 6,380$

SEC Carbon Ltd. Manufactures and sells graphite and steel products 96$ 98$ 740-$

Ultralife Corporation Produces and sells dry cell batteries 86$ 68$ 70$

Company Business Description

Altech Chemicals List of Comparable Companies ($US m)

19 February 2016 11

RESEARCH

Industrials

Table 5. Comparable company analysis Source: FactSet / DJC research

Alt

ech

Ch

em

icals

Ltd

C

om

pa

rab

le C

om

pa

nie

s A

na

lys

is($

in m

illions,

except

per

share

data

)

Alte

ch

Ch

em

ica

ls

Cu

rre

nt

% o

f2016

LT

ML

TM

LT

Sh

are

52-w

k.

Eq

uit

y

En

terp

rise

EB

ITD

AD

eb

t /

Int

Ex

p /

EP

SD

iv

Co

mp

an

yT

icke

rP

rice

Hig

hV

alu

eV

alu

e2016E

2017E

Ma

rgin

EB

ITD

AE

BIT

DA

2016E

2017E

Gro

wth

Yie

ld

2016E

2017E

Alt

ech

Ch

em

ica

ls L

imit

ed

AT

C-A

U$0.0

7

$0.7

5

$10.5

8

$10.1

4

N

AN

AN

A-

($19.7

2)

N

AN

AN

/AN

AN

AN

A

Sasol Lim

ited

SO

L-Z

A$25.4

5

61%

16,5

80.9

4$

15,8

22.2

3$

5.7

x4.5

x32%

1.6

.x20.2

12.0

.x10.1

.x-1

.3%

25.4

%-1

7.4

%-1

7.3

%

Alc

oa Inc.

AA

-US

7.9

0$

49%

10,3

50.2

6$

19,6

18.2

6$

7.0

x5.9

x14%

1.6

.x4.0

22.7

.x13.3

.x9.6

%6.1

%1%

7%

Sum

itom

o C

hem

ical C

o.,

Ltd

.4005-J

P4.7

9$

75%

7,9

35.2

6$

17,0

62.8

8$

6.4

x6.1

x17%

1.6

.x0.0

11.1

.x9.2

.x30.0

%6.8

%N

AN

A

Nors

k H

ydro

AS

AN

HY

-NO

3.3

8$

54%

6,9

98.7

4$

7,2

36.9

5$

4.5

x5.7

x13%

1.6

.x19.0

11.2

.x16.7

.x8.0

%18.8

%14%

3%

United C

o.

RU

SA

L P

lc486-H

K0.3

0$

38%

4,4

86.2

6$

12,8

76.2

6$

5.5

x8.9

x25%

1.6

.x2.8

3.7

.x5.9

.x44.2

%0.0

%27%

10%

0.0

Me

an

5.8

x6.2

x19%

11.1

13.8

x11.8

x10.8

x18%

11%

Me

dia

n5.8

x5.6

x14%

12.5

13.8

x11.5

x10.0

x10%

7%

Alu

min

um

Corp

ora

tion o

f C

hin

a L

imited C

lass H2600-H

K0.3

2$

46%

1,2

70.9

2$

7,4

26.6

6$

6.6

x8.0

x2%

1.6

.x2.8

.x-1

0.6

x-9

.5x

-76%

0%

NA

NA

Shenzhen D

esay B

att

ery

Technolo

gy C

o.,

Ltd

. C

lass A

000049-C

N5.7

8$

54%

1,1

85.9

4$

1,0

27.6

0$

N

AN

A5%

1.6

.x0.0

.x25.9

x18.7

xN

/A2%

NA

NA

Vedanta

Resourc

es p

lcV

ED

-GB

3.5

1$

33%

944.7

3$

27,1

32.5

3$

10.4

x8.8

x23%

1.6

.x1.9

.x-3

.5x

-5.8

x-6

3%

75%

66%

18%

Nip

pon L

ight

Meta

l H

old

ings C

o.,

Ltd

.5703-J

P1.6

0$

86%

872.5

8$

1,6

51.3

3$

N

AN

A12%

1.6

.x0.0

.xN

AN

AN

/A11%

NA

NA

Blu

e S

olu

tions S

AB

LU

E-F

R18.0

6$

56%

520.7

9$

543.1

1$

29.5

x13.2

x9%

1.6

.x22.9

.x-1

20.9

x46.5

xN

/A0%

NA

NA

Me

an

15.4

x10.6

x11%

5.5

x5.5

x-2

8.2

x13.4

x-3

3%

18%

Me

dia

n12.4

x10.3

x8%

4.2

x1.9

x-6

.8x

6.5

x-3

3%

2%

Tokai C

arb

on K

ore

a C

o.,

Ltd

.064760-K

R25.8

9$

100%

302.2

5$

296.0

6$

17.5

x10.2

x33%

1.6

.x0.0

.x31.3

x14.8

x74%

1.7

6%

NA

NA

Toyo T

anso C

o.,

Ltd

.5310-J

P14.5

0$

72%

300.9

1$

235.0

3$

NA

NA

13%

1.6

.x137.2

.x51.6

x19.9

x36%

6%

NA

NA

Mers

en S

AM

RN

-FR

13.7

1$

48%

283.4

4$

529.0

8$

5.2

x4.9

x13%

1.6

.x9.9

.x15.4

x7.9

x5%

19%

3%

16%

SE

C C

arb

on L

td.

5304-J

P2.2

8$

72%

94.5

4$

96.8

0$

N

AN

A14%

1.6

.x777.0

.xN

AN

AN

/A16%

NA

NA

Ultra

life

Corp

ora

tion

ULB

I-U

S5.0

7$

68%

77.1

7$

59.1

9$

N

AN

A8%

1.6

.x22.4

.xN

AN

AN

/A0%

NA

NA

Me

an

7.9

x7.0

x16%

1.8

x189.3

.x30.4

x13.7

x38%

9%

Me

dia

n5.9

x7.0

x13%

1.7

x22.4

.x25.8

x12.8

x34%

6%

Me

an

10.1

x8.0

x16%

6.1

x68.0

x3.1

x12.4

x14%

13%

Me

dia

n6.7

x7.9

x13%

2.5

x4.0

x11.9

x11.2

x10%

6%

Hig

h30.3

x14.0

x33%

21.8

x777.0

x49.1

x49.3

x75%

75%

Lo

w4.3

x4.6

x2%

0.0

x0.0

x-1

24.4

x-8

.8x

-76%

0%

So

urc

e: C

om

pa

ny f

ilin

gs

, Fa

cs

et,

Co

ns

en

su

s E

sti

ma

tes

No

te: L

as

t tw

elv

e m

on

ths

da

ta b

as

ed

on

De

ce

mb

er

20

15

. E

sti

ma

ted

an

nu

al fi

na

nc

ial d

ata

ba

se

d o

n a

fin

an

cia

l ye

ar.

Tie

r I:

La

rge

-Ca

p D

ive

rsif

ied

Sp

ecia

lia

lity

Ch

em

ica

l C

om

pa

nie

s

Tie

r II

: M

id-C

ap

Div

ers

ifie

d S

pe

cia

lia

lity

Ch

em

ica

ls

Tie

r II

I: S

ma

ll-C

ap

-D

ive

risif

ied

Sp

ecia

lia

lity

Ch

em

ica

ls

Ove

rall

EV

/EB

ITD

AP

/EF

CF

Yie

ld

12 19 February 2016

RESEARCH

Industrials

3.4 Orbite Technologies Inc is ATC’s closest technical competitor

Orbite Technologies Inc. (ORT.TSX) is a Canadian company whose processes are expected to

produce alumina and other high-value products, such as rare earth and rare metal oxides, at one

of the lowest costs in the industry, using feedstocks that include aluminous clay, kaolin,

nepheline, bauxite, red mud, fly ash as well as serpentine residues from chrysotile processing

sites. Orbite is currently in the process of finalising its first commercial high-purity alumina (HPA)

production plant in Cap-Chat, Quebec and has completed the basic engineering for a proposed

smelter-grade alumina (SGA) production plant, which would use clay mined from its Grande-

Vallee deposit (Source: Orbite Technologies Inc website).

Therefore, ORT intend to recover a number of products from a variety of feedstocks, which in

our view, adds a level of complexity to recovery operations. The kaolin feed into the ORT plant

also has a high iron content of around 8% which therefore needs to be removed during the

process.

Existing producers, apart from ORT, commonly use a very expensive and highly processed

feedstock material such as aluminium metal to produce HPA product. Although ORT announced

they would produce product in 2015 a dispute with a contractor on site resulted in a delay in

construction. ORT now expect to start production in 1Q 2016.

ORT intend commissioning a plant with a capacity of 3 tonnes per day, or 1,095 tonnes per year.

The company intended to make an expansion decision to 5 tpd, or 1,825 tpa, in 2016. However,

given the delay in construction completion, we believe this timetable may be pushed back into

2017.

Capital costs for the plant is estimated at US$117m. ORT has a market capitalisation of $152.8m

and in 4Q ORT completed a US$22m debt facility with MidCap Financial at Libor plus 6.5%.

The reason that we believe ATC capital is considerably less than ORT is the simple one-step

process for the manufacture of HPA that ATC will adopt, and the low cost environment afforded

by Malaysia, compared to Canada.

Table 6. Comparison between ORT.TSX and ATC. ASX Source: DJC research, Factset

Shares on Issue (m)

Share Price $

Market Cap ($m)

Cash + Investments ($m)

Debt ($m)

Enterprise value ($m)

Feedstock

By-products

Anticipated HPA production (tpa)

Product range

Year in production (FY)

CAPEX costs (A$m)

Capital intensity ($/t)

Altech Chemical Ltd: Comparitive Evaluation to Orbite Technologies Inc

Orbite Technologies Inc

(ORT.CA)

Altech Chemicals Ltd

(ATC.AU) Metric

Fly ash, kaolin, waste Al, red

mud, SGA

haematite, Mg oxides, REO,

silica

White aluminous clay (kaolin)

Silica

377.51

0.28

105.7

28.5

35.6

112.8

152.6

0.10

15.3

0.5

0

14.8

1825

4N, 5N, 6N

4000

4N

2019

110

27,500

2016

117

64,110

19 February 2016 13

RESEARCH

Industrials

ORT has provided samples to potential purchasers of 5N HPA product (99.999%) for testing

together with other products, such as gamma HPA, which may provide additional opportunities

to include a higher volume customer base.

Figure 1. Price and volume chart for Orbite Technologies Inc (ORT-TSE) Source: FactSet

3.5 Precedent Transactions

A world review of the recent precedent transactions identified a small but meaningful sample of

merger and acquisition transactions. This list of precedent transactions was created by

identifying transaction type, consideration paid, and acquirer in the specialist chemicals sector.

We then spread out the financial metric of each transaction and compared the LTM sales,

EBITDA, EBIT and LTM EBITDA margins. Lastly, we analysed the equity value to LTM net

income. The range of exit multiples was calculated for this sample.

The transactions identified as relevant date back to 2004. The calculated mean and median

EV/EBITDA multiple from the last twelve months (LTM) is 10.1x-10.0x.

Table 7. Precedent transactions Source: FactSet / DJC Research

Altech Chemicals Ltd Precedent Transactions Analysis($ in millions)

E16 E12 E7 E18 E19 E30 E37 E40 E42 E44 O41 E46 ##

Enterprise Value / LTM Equity Value / Premiums Paid

Date Transaction Purchase Equity Enterprise LTM LTM LTM EBITDA LTM Days Prior to Unaffected

Announced Acquirer Target Type Consideration Value Value Sales EBITDA EBIT Margin Net Income

511733MM

20090430 Platinum Equity LLC Alcoa, Inc. /Wire Harness & Electrical Distribution Bus/Acquisition / Merger Combo 175 175 0.2x

465198MM

20080318 Nippon Oil Corp. Kyushu Oil Co., Ltd. Acquisition /

Merger

Cash 152 1,538 0.2x 15.1x 15.1x 1% 26.7x

452402MM

20071223 Rank Group Holdings Ltd. Alcoa, Inc. /Packaging &

Consumer Division/

Acquisition /

Merger

Cash 2,700 2,700 0.8x 28.4x

428675MM

20070521 Ineos Group Holdings Plc Kerling ASA Acquisition /

Merger

908 908 0.8x 10.1x 10.1x 8% 13.6x

409498MM

20070202 Tanabe Seiyaku Co., Ltd. Mitsubishi Pharma Corp. Acquisition /

Merger

Stock 4,357 4,357 2.2x 25.4x

329410MM

20050228 Orkla ASA Elkem AS Acquisition /

Merger

Cash 899 2,537 0.8x 6.1x 10.1x 13% 20.2x

320835MM

20041125 Dainippon Sumitomo Pharma

Co., Ltd.

Sumitomo Pharmaceuticals

Co., Ltd.

Acquisition /

Merger

Stock 2,207 2,207 1.7x 11.1x 11.1x 15% 18.8x

317839MM

20041027 Ryerson Tull, Inc. Integris Metals Corp. Acquisition /

Merger

Cash 410 653 0.4x 7.6x 9.4x 5% 16.9x

Mean 0.9x 10.0x 11.2x 8% 21.4x

Median 0.8x 10.1x 10.1x 8% 20.2x

High 2.2x 15.1x 15.1x 15% 28.4x

Low 0.2x 6.1x 9.4x 1% 13.6x

14 19 February 2016

RESEARCH

Industrials

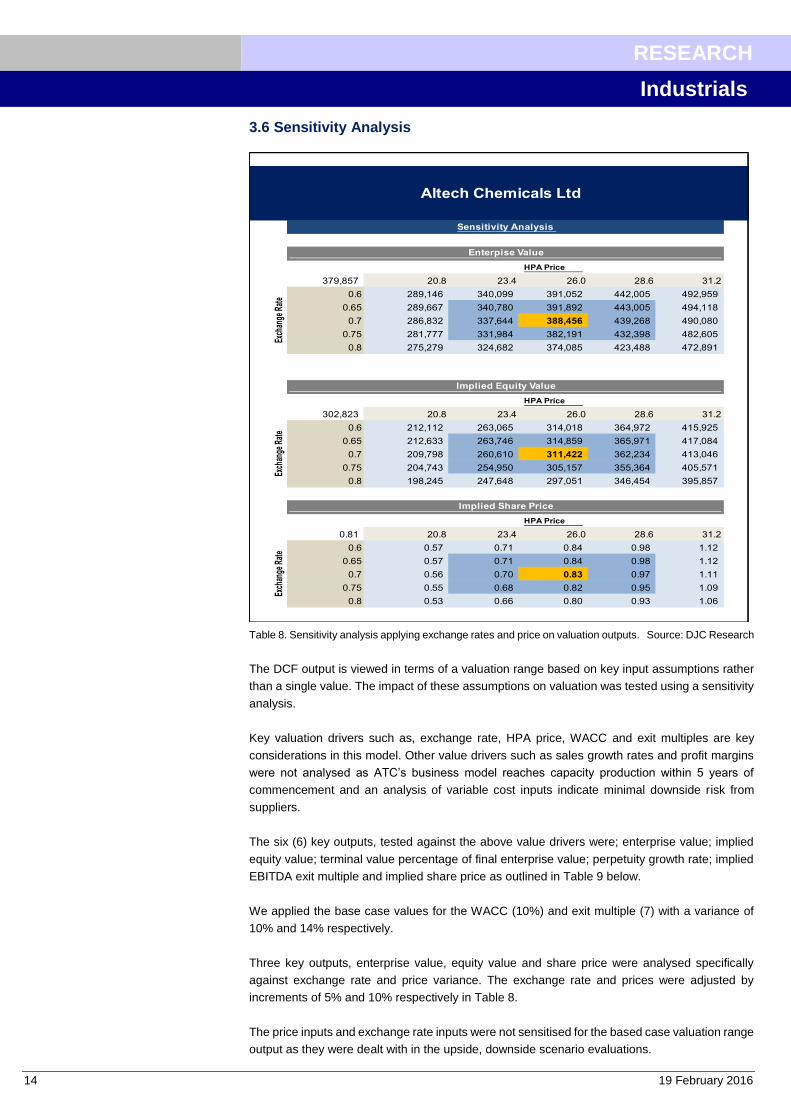

3.6 Sensitivity Analysis

Table 8. Sensitivity analysis applying exchange rates and price on valuation outputs. Source: DJC Research

The DCF output is viewed in terms of a valuation range based on key input assumptions rather

than a single value. The impact of these assumptions on valuation was tested using a sensitivity

analysis.

Key valuation drivers such as, exchange rate, HPA price, WACC and exit multiples are key

considerations in this model. Other value drivers such as sales growth rates and profit margins

were not analysed as ATC’s business model reaches capacity production within 5 years of

commencement and an analysis of variable cost inputs indicate minimal downside risk from

suppliers.

The six (6) key outputs, tested against the above value drivers were; enterprise value; implied

equity value; terminal value percentage of final enterprise value; perpetuity growth rate; implied

EBITDA exit multiple and implied share price as outlined in Table 9 below.

We applied the base case values for the WACC (10%) and exit multiple (7) with a variance of

10% and 14% respectively.

Three key outputs, enterprise value, equity value and share price were analysed specifically

against exchange rate and price variance. The exchange rate and prices were adjusted by

increments of 5% and 10% respectively in Table 8.

The price inputs and exchange rate inputs were not sensitised for the based case valuation range

output as they were dealt with in the upside, downside scenario evaluations.

HPA Price

379,857 20.8 23.4 26.0 28.6 31.2

0.6 289,146 340,099 391,052 442,005 492,959

0.65 289,667 340,780 391,892 443,005 494,118

0.7 286,832 337,644 388,456 439,268 490,080

0.75 281,777 331,984 382,191 432,398 482,605

0.8 275,279 324,682 374,085 423,488 472,891

HPA Price

302,823 20.8 23.4 26.0 28.6 31.2

0.6 212,112 263,065 314,018 364,972 415,925

0.65 212,633 263,746 314,859 365,971 417,084

0.7 209,798 260,610 311,422 362,234 413,046

0.75 204,743 254,950 305,157 355,364 405,571

0.8 198,245 247,648 297,051 346,454 395,857

HPA Price

0.81 20.8 23.4 26.0 28.6 31.2

0.6 0.57 0.71 0.84 0.98 1.12

0.65 0.57 0.71 0.84 0.98 1.12

0.7 0.56 0.70 0.83 0.97 1.11

0.75 0.55 0.68 0.82 0.95 1.09

0.8 0.53 0.66 0.80 0.93 1.06

Sensitivity Analysis

Enterpise Value

Exch

ange

Rat

e

Implied Equity Value

Exch

ange

Rat

e

Implied Share Price

Exch

ange

Rat

e

Altech Chemicals Ltd

19 February 2016 15

RESEARCH

Industrials

Table 9. Sensitivity analysis using WACC and exit multiple on various financial metrics Source: DJC Research

Exit Multiple Exit Multiple

379,857 6.0 6.5 7.0 7.5 8.0 -8% 6.0 6.5 7.0 7.5 8.0

9.0% 390,075 405,858 421,641 437,425 453,208 9.0% -9.34% -8.69% -8.12% -7.62% -7.17%

9.5% 370,335 385,274 400,214 415,154 430,094 9.5% -9.30% -8.65% -8.08% -7.58% -7.14%

10.0% 351,567 365,712 379,857 394,002 408,147 10.0% -9.26% -8.61% -8.05% -7.55% -7.11%

10.5% 333,718 347,113 360,509 373,905 387,300 10.5% -9.23% -8.58% -8.01% -7.52% -7.08%

11.0% 316,734 329,424 342,113 354,802 367,492 11.0% -9.19% -8.54% -7.98% -7.49% -7.05%

Exit Multiple Exit Multiple

302,823 6.0 6.5 7.0 7.5 8.0 4 6.0 6.5 7.0 7.5 8.0

9.0% 313,041 328,824 344,608 360,391 376,174 9.0% 4.5 4.7 4.8 5.0 5.2

9.5% 293,301 308,241 323,180 338,120 353,060 9.5% 4.3 4.4 4.6 4.8 4.9

10.0% 274,533 288,678 302,823 316,968 331,113 10.0% 4.0 4.2 4.4 4.5 4.7

10.5% 256,684 270,079 283,475 296,871 310,267 10.5% 3.8 4.0 4.1 4.3 4.4

11.0% 239,701 252,390 265,079 277,768 290,458 11.0% 3.6 3.8 3.9 4.1 4.2

Exit Multiple Exit Multiple

52% 6.0 6.5 7.0 7.5 8.0 0.81$ 6.0 6.5 7.0 7.5 8.0

9.0% 48.6% 50.6% 52.4% 54.1% 55.7% 9.0% 0.84 0.88 0.92 0.97 1.01

9.5% 48.4% 50.4% 52.3% 54.0% 55.6% 9.5% 0.79 0.83 0.87 0.91 0.95

10.0% 48.3% 50.3% 52.1% 53.9% 55.5% 10.0% 0.74 0.77 0.81 0.85 0.89

10.5% 48.2% 50.2% 52.0% 53.7% 55.3% 10.5% 0.69 0.72 0.76 0.80 0.83

11.0% 48.1% 50.1% 51.9% 53.6% 55.2% 11.0% 0.64 0.68 0.71 0.74 0.78

WA

CC

WA

CC

Implied Perpetuity Growth Rate Enterprise Value

Sensitivity Analysis

WA

CC

WA

CC

Implied Equity Value Implied Enterprise Value/EBITDA (Yr 5)

WA

CC

WA

CC

PV of Terminal Value % of Enterprise Value Implied Share Price

Altech Chemicals Ltd

16 19 February 2016

RESEARCH

Industrials

4. Financial Summary Sheets

Altech Chemicals Ltd Balance Sheet

2015a 2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e

Cash 575 3,300 821 315 431 3,512 7,886 13,135 63,996

Current Assets 1,549 3,320 841 335 8,233 14,372 22,014 31,350 84,460

Total Assets 3,780 9,159 61,342 120,514 109,750 104,303 102,640 124,752 173,137

Debt 815 0 20,297 76,635 70,481 48,917 14,574 0 0

Other Liabilities 228 228 0 0 0 0 0 0 0

Total Liabilities 1,043 1,215 20,697 79,873 92,920 83,123 62,751 26,111 12,430

Total Shareholders' Equity 2,736 7,944 40,645 40,641 23,730 28,310 47,543 107,168 160,678

Full Year Summary (A$m)

Altech Chemicals Ltd Income Statement

2015a 2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e

Sales Revenue 0 0 0 0 38,911 54,200 70,538 90,978 102,222

EBITDA (1,293) 0 65 3 15,844 31,099 45,631 65,215 76,650

Depreciation & Amortisation (8) 0 0 0 (17,955) (10,928) (9,713) (8,866) (7,895)

EBIT (1,301) 0 59 (4) (11,066) 10,283 25,328 45,773 58,191

Net Interest Expense (66) 0 0 0 (5,845) (5,451) (4,101) (1,829) (197)

Profit Before Tax (1,367) 0 59 (4) (5,220) 15,735 29,429 47,602 58,389

Income Tax Expense 0 0 0 0 0 (252) (1,995) (3,553) (4,485)

Underlying NPAT (1,392) 0 59 (4) (16,911) 4,581 19,233 59,625 53,510

Abnormal Items 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Minority Interests 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Reported NPAT (1,392) 0 59 (4) (16,911) 4,581 19,233 59,625 53,510

Normalised Earnings (1,392) 0 59 (4) (16,911) 4,581 19,233 59,625 53,510

Full Year Summary (A$m)

Altech Chemicals Ltd Cash Flows

2015a 2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e

Cash Flow Operations

Sales 0 0 0 0 38,911 54,200 70,538 90,978 102,222

Other Items 8 (1,629) 500 0 (13,329) (7,238) (11,906) (17,366) (13,219)

Operating Cash Flow 8.40 (1,629.00) 500.00 0.00 25,582.29 46,961.85 58,632.17 73,611.47 89,003.26

Cash Flow Investing

Capital Expenditure (49,195.02) (49,400.96) (999.97) (1,999.96) (2,999.96) (3,999.96) (3,999.96) (4,999.95) (4,999.95)

Free Cash Flow (49,186.62) (51,029.96) (499.97) (1,999.96) 22,582.34 42,961.89 54,632.20 68,611.52 84,003.31

Cash From Financing

Equity Raised 0 5,450 31,250 0 0 0 0 0 0

Dividends Paid 0 0 0 0 0 0 0 0 0

Inc/(Dec) in Borrowings 0 20,297 58,938 0 0 0 0 0 0

Less Debt Repayment 0 0 0 (2,600) (12,000) (27,300) (41,500) (15,100) 0

Financing Cash Flow 0 25,747 90,188 (2,600) (12,000) (27,300) (41,500) (15,100) 0

Movement in Net Cash (49,187) 464 179,877 (7,200) (1,418) (11,638) (28,368) 38,412 84,003

Full Year Summary (A$m)

19 February 2016 17

RESEARCH

Industrials

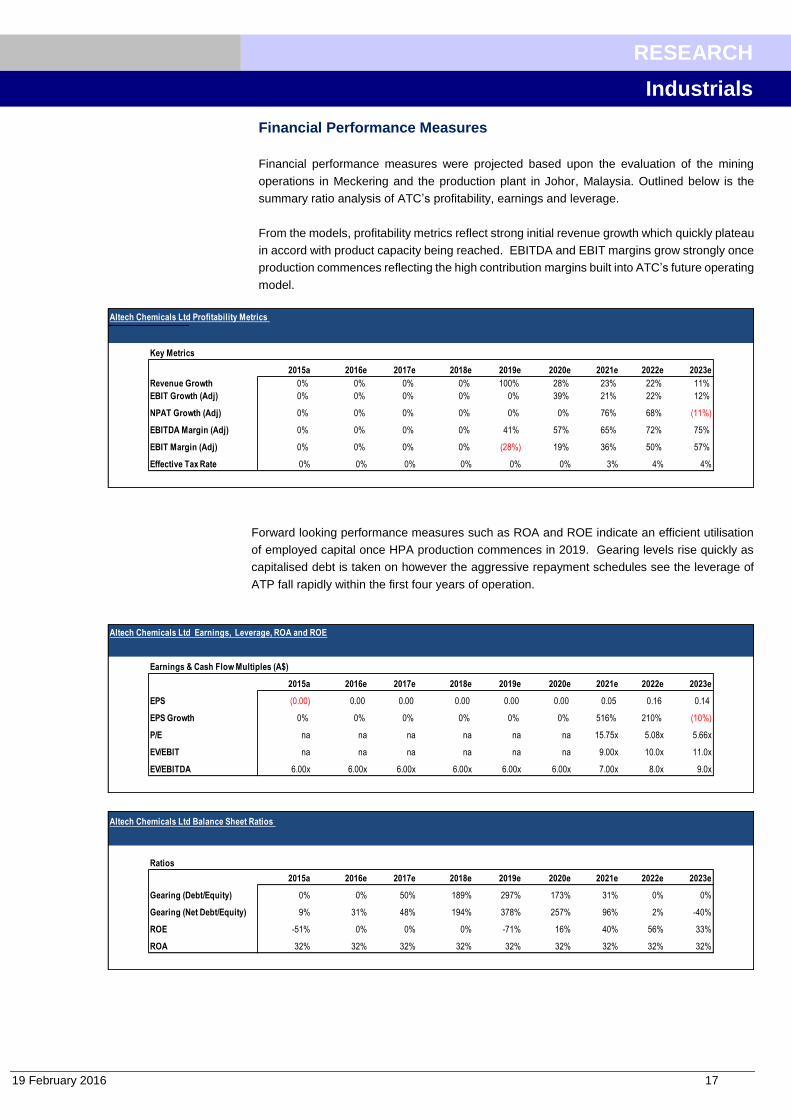

Financial Performance Measures

Financial performance measures were projected based upon the evaluation of the mining

operations in Meckering and the production plant in Johor, Malaysia. Outlined below is the

summary ratio analysis of ATC’s profitability, earnings and leverage.

From the models, profitability metrics reflect strong initial revenue growth which quickly plateau

in accord with product capacity being reached. EBITDA and EBIT margins grow strongly once

production commences reflecting the high contribution margins built into ATC’s future operating

model.

Forward looking performance measures such as ROA and ROE indicate an efficient utilisation

of employed capital once HPA production commences in 2019. Gearing levels rise quickly as

capitalised debt is taken on however the aggressive repayment schedules see the leverage of

ATP fall rapidly within the first four years of operation.

Altech Chemicals Ltd Profitability Metrics

Key Metrics

2015a 2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e

Revenue Growth 0% 0% 0% 0% 100% 28% 23% 22% 11%

EBIT Growth (Adj) 0% 0% 0% 0% 0% 39% 21% 22% 12%

NPAT Growth (Adj) 0% 0% 0% 0% 0% 0% 76% 68% (11%)

EBITDA Margin (Adj) 0% 0% 0% 0% 41% 57% 65% 72% 75%

EBIT Margin (Adj) 0% 0% 0% 0% (28%) 19% 36% 50% 57%

Effective Tax Rate 0% 0% 0% 0% 0% 0% 3% 4% 4%

Altech Chemicals Ltd Earnings, Leverage, ROA and ROE

Earnings & Cash Flow Multiples (A$)

2015a 2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e

EPS (0.00) 0.00 0.00 0.00 0.00 0.00 0.05 0.16 0.14

EPS Growth 0% 0% 0% 0% 0% 0% 516% 210% (10%)

P/E na na na na na na 15.75x 5.08x 5.66x

EV/EBIT na na na na na na 9.00x 10.0x 11.0x

EV/EBITDA 6.00x 6.00x 6.00x 6.00x 6.00x 6.00x 7.00x 8.0x 9.0x

Ratios

2015a 2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e

Gearing (Debt/Equity) 0% 0% 50% 189% 297% 173% 31% 0% 0%

Gearing (Net Debt/Equity) 9% 31% 48% 194% 378% 257% 96% 2% -40%

ROE -51% 0% 0% 0% -71% 16% 40% 56% 33%

ROA 32% 32% 32% 32% 32% 32% 32% 32% 32%

Altech Chemicals Ltd Balance Sheet Ratios

18 19 February 2016

RESEARCH

Industrials

Table 10. Revenue, Cash Flow, Margin and Tax Analysis Source: DJC Research

Supporting the financial statements above are the graphs for revenue, cash flow, EBITDA, EBIT

and Tax. Note the tax rate applied does not include the capex allowance and hence the graphs

potentially overestimate the tax paid.

The gradual increase in revenues is reflective of the staged plant development and the shift from

SGC, 3N & 4N production in 2019 to entirely 4N production by 2022. Once full production

capacity is reached revenues plateau.

Cash flow charting show traditional project financing cash flow impacts which will be funded by

the debt and equity raises proposed in FY2016 and FY2017.

Altech Chemicals Ltd Financial Analysis Graphs

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e 2024e 2025e 2026e 2027e 2028e 2029e 2030e

Rev

enue

s A

U$(

m)

Production Year

HPA Revenues

Series1

Linear (Series1)

-20,000

-10,000

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e 2024e 2025e 2026e 2027e 2028e 2029e 2030e

$AU

(m

)

Production Year

EBITDA, EBIT and EFFECTIVE TAX

EBITDA EBIT Tax

-60000

-40000

-20000

0

20000

40000

60000

80000

2016e 2017e 2018e 2019e 2020e 2021e 2022e 2023e 2024e 2025e 2026e 2027e 2028e 2029e 2030e

Cas

h Fl

ow $

AU(m

)

Production Year

Cash Flows

Cash Flows

19 February 2016 19

RESEARCH

Industrials

5. Share Price Catalysts

Successful grant of ECA cover: Positive conclusion of Export Credit Agency cover will mitigate

risk for German-based debt providers and will mean that financing terms for the project debt

component will be very favourable. This in turn reduces the financing costs and WACC.

Successful financial due diligence: Kfw IPEX-Bank are currently mandated to source primary

debt funding for the project. As part of this process Kfw IPEX Bank are making extensive Due

Diligence enquiries. Successful DD paves the way for project financing negotiations with debt

providers.

Further off-take or distribution agreements: Similar to the Mitsubishi Agreement for Japan,

where Mitsubishi will act as exclusive seller and distributor of HPA to the Japanese markets, we

would expect to see further off-take and/or distribution MOU’s or Agreements for other Asian

countries. ATC recently appointed an experienced Chinese-based Sales and Marketing Manager

to establish off-take agreements in that jurisdiction.

Meckering and Malaysian approvals: Mining approval for Meckering and Malaysia

environmental and construction approvals will also be an important risk mitigation step but

unlikely to be major price catalysts in themselves.

Completion of project debt funding: Arrangements for project debt (execution of a financing

terms sheet) through Kfw IPEX-Bank or another lender. We see a successful conclusion to debt

funding as a major milestone for the project, which will effectively mitigate much of the financing

risk. We envisage successful debt funding to be the precursor to an equity issue to obtain the

remainder of the project financing. We have assumed a debt:equity ratio of 70:30.

Commissioning of process plant: Commissioning of the process plant is likely to take at least

6 months. First 4N product will be used as samples to establish permanent supply contracts as

buyers will have to be satisfied with the quality of the product and the consistency of supply.

Satisfactory specifications on sample 4N product should be another major operational milestone

and confirm that the plant is operating as expected.

First commercial HPA production: First production and ramp up in sales will provide cash flow

and establish ATC as a major player in the global HPA market. This will be a major price catalyst

as they will be the only company globally to provide a focused exposure to the HPA market with

one of the lowest production costs in the world.

Potential corporate activity: We believe that ATC, once in full scale operation, could be a prime

takeover target for a larger company. Suitors would likely to come from established, large-scale

specialist chemical providers who already have an exposure to HPA production. The more

established industrial HPA producers will likely have older, higher cost operations and would

seek to get further down the cost curve and gain market share in this fast growing sector.

20 19 February 2016

RESEARCH

Industrials

6. SWOT Analysis

Focused on HPA production only Currency exposure

Patented process Reliance on HPA sales agreements

Low operating costs Project Execution Risk

Established Japanese distribution New entrant to established market

Upstream kaolin supply

Located close to markets in Asia

Growing demand for HPA Global competition

Exposed to Li Fe battery sector Variation in feedstock impurities

Policy drivers Changes to Malaysian business conditions

Industry consolidation Project financing

New technologies

Future Takeover taget

S W

O T

Significant Malaysian

shareholder already on register

Access to cheap project

financing at attractive terms

19 February 2016 21

RESEARCH

Industrials

7. Risks and Mitigating Actions

Lower grade kaolin feed

There is a risk that kaolin of lower grade will be fed into the plant, thereby effecting the

ability of the processing plant to produce 4N quality product as a result of high

contaminants. ATC will now construct the kaolin beneficiation plant to Malaysia. Initially

we thought this could present a grade control issue in Malaysia.

Mitigation step: However, mining over the 2 month period will produce enough raw

product for 3 years of supply. The kaolin will be grade controlled at site and stored in a

number of grade fingers where grade is significantly different. Ongoing sampling on site

will ensure that grades are blended (if required) and managed to produce the right

balance of kaolin grade and contaminants.

Not achieving 4000tpa of 4N production or meeting 4N specification

There is a risk that ATC will not be able to ramp up production to 4,000t of 4N HPA

(design capacity). This would potentially affect revenues, operating costs and payback.

Mitigation step: ATC has built in a relatively slow ramp up in their BFS financial model,

assuming that full design capacity will only be reached in Year 5. This allows time for

fine tuning the process if required and takes a measured approach to delivery of 4N

product into a market commensurate with increasing demand. ATC has assumed that

initial sales will consist of a variety of products, from a lower value SGA (Smelter Grade

Alumina) through 3N HPA and, increasingly, 4N HPA until an envisaged 4,000 tonnes

per annum of 4N HPA is produced.

Price war on too much supply

The CAGR on the value of the HPA market is anticipated to be 16.3% from 2015 to

2021. In volume terms the global HPA market is expected to expand at a CAGR of

19.7%. A supply response from existing producers, and potentially new entrants, is

expected. Downward pressure on prices could be exerted if new supply is excess to

demand.

Mitigation step: ATC are likely to be operating in the lower third of the cost curve for

production of HPA. This is due to their process using kaolin as a feedstock and the use

of HCl in a closed recovery circuit reducing reagent costs. It would be unlikely that a

price war by largely, higher cost producers would affect ATC production as competitor

margins and capacity are constrained by old production facilities.

Lack of future capital raising to achieve detailed design

Just like any other listed company in a development phase ATC are required to find

funds for the completion of studies. ATC need to find enough funds to complete

outstanding work and to fund working capital prior to project funding completion.

Mitigation step: ATC has already completed its bankable feasibility Study and has

embarked on the detailed design phase prior to construction. Even so, optimisation

work post BFS completion has identified at least one change to the process design

which will have operational benefits. Other requirements involve continuing permitting

activity, none of which will make large draws on cash. Support from its major Malaysian

domiciled shareholder – Melewar International Investment Company should likely be

available.

22 19 February 2016

RESEARCH

Industrials

Plant utilisation, HPA recovery and bottle-necks

With any new plant, there are likely to be some issues identified during the

commissioning process. Bottle-necks and design faults could reduce plant utilisation,

recoveries and affect production levels.

Mitigation steps: ATC has designed its plant to use off-the-shelf components as much

as possible, with no new technology employed in the processing route. Additionally,

ATC has built in conservative estimates for utilisation and recovery into its financial

model in anticipation of these issues. Recoveries are conservatively assumed at 80%

and plant utilisation has been assumed at 77% in the model, including planned

maintenance.

Project financing

ATC need to secure debt and equity financing during 2016. In uncertain capital markets,

this could be challenging.

Mitigation Step: The recent financing proposals from Kfw-IPEX Bank in Germany and

a successful application to access the ECA cover will mitigate some financial risk. The

guarantee under the scheme will mean financing for that portion covered under the

scheme will be at very attractive rates and be of low risk to lenders. Kfw-IPEX Bank has

arranged project finance for a number of similar speciality chemical projects in the

region and is well placed to arrange project financing. Debt is to be held at the project

level.

19 February 2016 23

RESEARCH

Industrials

8. Progress on Project Financing

Mandate executed with Kfw IPEX-Bank

Following several meetings late last year, ATC received a Letter of Interest (LOI) from Kfw IPEX-

Bank and on 2 December 2015, executed an exclusive mandate with the bank for the provision

of services relating to project financing of the Company’s HPA project.

Kfw IPEX-Bank is a wholly owned subsidiary of the promotional bank Kfw and will provide

advisory and structuring services to ATC. The subsidiary is a leading German export and project

finance group with significant experience in mining and chemicals projects globally, including in

Asia, where the bank has advised on projects similar to ATC’s HPA plant.

The mandate contemplates the arrangement of senior debt project financing that is aimed at

utilising, to the maximum extent, an Export Credit Agency (ECA) insurance cover under German-

backed project finance export guarantees.

The Kfw IPEX-Bank is the largest subsidiary of the Kfw Banking Group and unlike the parent

bank, competes directly with commercial banks and is therefore legally and financially

independent of its parent. Kfw-IPEX Bank’s balance sheet amounted to €26.3 billion in 2014.

What is ECA cover and why would ATC qualify for its use?

ECA cover is an instrument for the promotion of German exports. Essentially it is a cover facility

to bank lenders to insure against risk of an export loan and is administered by Euler Hermes, the

German Export Credit Agency. As a result of the insurance cover for lenders, the interest rate on

that part of the project financing covered by the ECA is at very attractive rates, given that the risk

on that portion is mitigated for the lender. The term of debt covered is also long term.

On 10 December 2015, ATC received an LOI for German export credit cover. Whilst still subject

to due diligence, the receipt of the letter is a major step in advancing ATC’s project financing, as

Hermes would have already undertaken its preliminary evaluation of the HPA project. ATC need

to now submit a detailed application with supporting documentation to obtain the ECA cover.

ATC estimate that approximately US$40m of the total US$77m project capital cost will qualify for

ECA cover. An additional $15m of senior debt financing will be required to total around US$55m

of project debt.

ATC qualify under the German ECA scheme as the majority of the plant componentry and the

EPC contractor, M+W Group, originate from Germany or other EU countries. This goes back to

the design philosophy behind the plant which would utilise as much as possible, top quality, off-

the-shelf components. Many of the component suppliers chosen by ATC happen to be German,

or EU based and it is for this reason that ATC qualify for ECA cover.

Kfw IPEX-Bank has an operational base in Singapore as do ATC’s EPC contractor, M+W.

Remainder of Project financing likely through equity

Much of the remaining project finance for the HPA project would likely come from equity

representing an approximate 70:30 debt:equity split.

Kfw is a German government-owned development bank that supports and promotes German manufacturing and innovation in export projects globally

ECA insurance cover significantly reduces the risk to lenders and therefore secures very low interest rates for borrowers

24 19 February 2016

RESEARCH

Industrials

9. Altech’s HPA Sales and Marketing Strategy Sales and Distribution Agreement with Mitsubishi

On 24 September 2015, ATC announced the execution of a Sales and Distribution Agreement

with Mitsubishi Australia Ltd (“Mitsubishi”), a corporate subsidiary of Mitsubishi Corporation,

Japan. In 2014, Japan was estimated to represent 21% of the estimated global demand for HPA,

equivalent to approximately 4,000 tonnes of demand, or coincidently, ATC’s annual output at full

capacity.

The agreement appoints Mitsubishi as exclusive seller and distributer of ATC’s HPA product into

the Japanese market. ATC would benefit from the extensive industrial reach of Mitsubishi which

operates across a variety of industries, including the chemicals industry. Mitsubishi has agreed

not to purchase or resell any HPA from a third party supplier. Mitsubishi will only buy and resell

ATC’s HPA within Japan.

ATC appoints Sales and Marketing Manager, China

On 14 January 2016, ATC announced the appointment of a Sales and Marketing Manager, Mr

Martin Ma, for China. Given ATC’s strategy to focus on the Asia-Pacific Region, the appointment

of a Sales and Marketing Manager for China will complement the Mitsubishi Agreement for Japan

and will facilitate ATC to gain market share in both these important jurisdictions, where HPA is

already in use for the manufacture of high tech items.

The incumbent has extensive experience in sales management of high purity feedstock to

Chinese industries such as lithium battery and electrical vehicle industries. There is growing

demand for HPA to be incorporated in batteries as coatings on battery separators as it increases

discharge rates, lowers self-discharge and lengthens battery life cycles. The increasing

deployment of electric vehicles in China and rapid growth in battery manufacture and increasing

use of LED’s makes China an important market for HPA.

Mr Ma has previously been involved in sales and marketing of lithium carbonate into north and

central China with Galaxy Lithium.

We expect to see other appointments in the Asia-Pacific Region as ATC gets closer to HPA

production.

The strategic agreement brings one of the most influential Japanese industrial giants to act as ATC’s exclusive seller in japan, which represents over 20% of the global market for HPA

19 February 2016 25

RESEARCH

Industrials

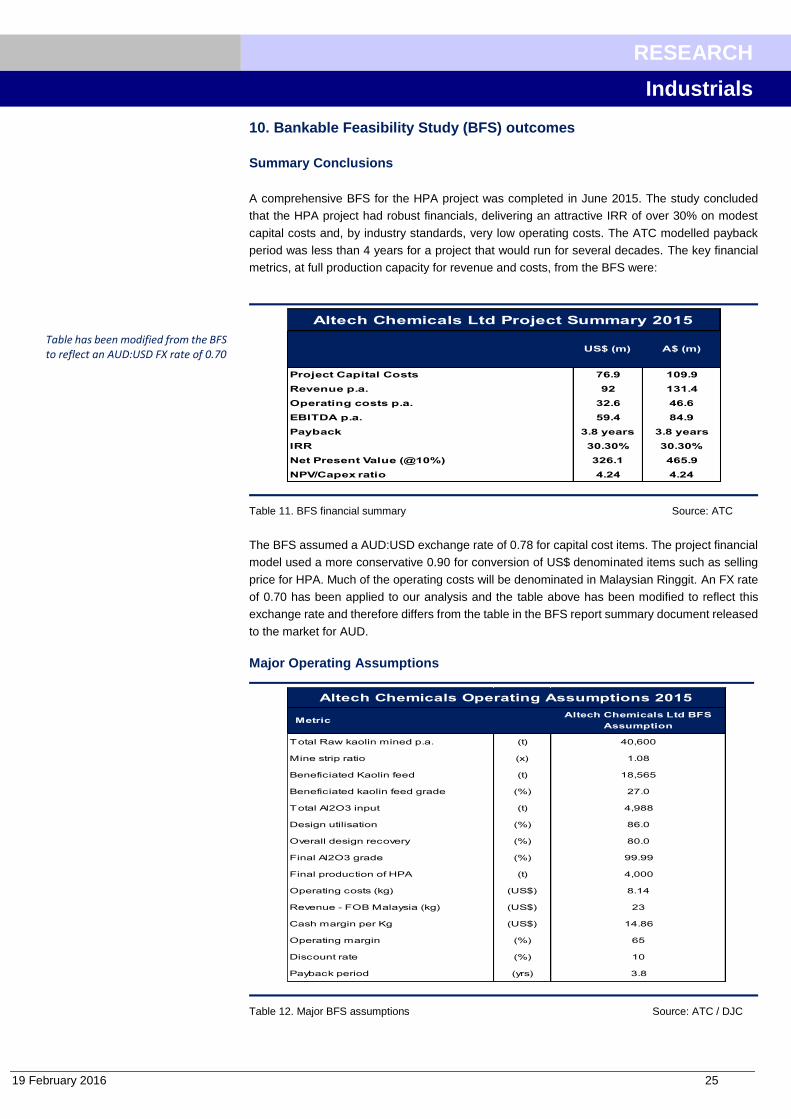

10. Bankable Feasibility Study (BFS) outcomes

Summary Conclusions

A comprehensive BFS for the HPA project was completed in June 2015. The study concluded

that the HPA project had robust financials, delivering an attractive IRR of over 30% on modest

capital costs and, by industry standards, very low operating costs. The ATC modelled payback

period was less than 4 years for a project that would run for several decades. The key financial

metrics, at full production capacity for revenue and costs, from the BFS were:

Table 11. BFS financial summary Source: ATC

The BFS assumed a AUD:USD exchange rate of 0.78 for capital cost items. The project financial

model used a more conservative 0.90 for conversion of US$ denominated items such as selling

price for HPA. Much of the operating costs will be denominated in Malaysian Ringgit. An FX rate

of 0.70 has been applied to our analysis and the table above has been modified to reflect this

exchange rate and therefore differs from the table in the BFS report summary document released

to the market for AUD.

Major Operating Assumptions

Table 12. Major BFS assumptions Source: ATC / DJC

Project Capital Costs 76.9 109.9

Revenue p.a. 92 131.4

Operating costs p.a. 32.6 46.6

EBITDA p.a. 59.4 84.9

Payback 3.8 years 3.8 years

IRR 30.30% 30.30%

Net Present Value (@10%) 326.1 465.9

NPV/Capex ratio 4.24 4.24

Altech Chemicals Ltd Project Summary 2015

US$ (m) A$ (m)

Total Raw kaolin mined p.a. (t) 40,600

Mine strip ratio (x) 1.08

Beneficiated Kaolin feed (t) 18,565

Beneficiated kaolin feed grade (%) 27.0

Total Al2O3 input (t) 4,988

Design utilisation (%) 86.0

Overall design recovery (%) 80.0

Final Al2O3 grade (%) 99.99

Final production of HPA (t) 4,000

Operating costs (kg) (US$) 8.14

Revenue - FOB Malaysia (kg) (US$) 23

Cash margin per Kg (US$) 14.86

Operating margin (%) 65

Discount rate (%) 10

Payback period (yrs) 3.8

MetricAltech Chemicals Ltd BFS

Assumption

Altech Chemicals Operating Assumptions 2015

Table has been modified from the BFS to reflect an AUD:USD FX rate of 0.70

26 19 February 2016

RESEARCH

Industrials

Measured approach to production ramp up

The HPA plant will have a design capacity of 4,000tpa but the BFS has assumed a conservative

approach to the commissioning and ramp up phase. During the first 12 months, ATC has assumed

an output of 2,000 tonnes (50% of design capacity) and only 70% of that output will be HPA. The

remaining 30% will be 3N alumina (99.9% alumina) and SGA (smelter grade alumina).

The above product mix reflects the likelihood that on commission and start up some of the product

will not meet 4N specification. The slow ramp up allows for this but maintains a product line that

can be marketed and sold to lower specification customers.

Table 13. Production tonnage ramp up Source: ATC

Full production capacity has been assumed from Year 5 onwards. The latent capacity allows for

an increase in production above the assumed ramp up rate, should the demand be there. The

ramp up also incorporates a 6 month period of product qualification and acceptance by major

customers and has been reflected in the BFS financial model.

Capital cost estimates

Capital cost estimates in the BFS were undertaken by Simulus Group, one of Australia’s leading

boutique hydrometallurgy and mineral processing service groups with experience in process plant

engineering and design similar to the HPA plant. Capital costs have been estimated to a precision

of around ±15%.

Capital cost estimates in the BFS were chunked into Meckering and Johor. In the BFS, the

beneficiation plant was to be constructed at the Meckering site with an estimated total capital of

US$16.047m with an additional US$1.145m in contingency. This now equates to A$22.9m plus

contingency at current FX rates.

However, the optimised design, with the beneficiation plant being in Malaysia, has the potential

to save capital costs from installation of a smaller plant, as it will be operated 24 hours per day

rather than day shift only if in Australia.

Capex in Malaysia was estimated at US$54.6m, or A$70m at an FX rate of 0.78. At current FX

rates, this has climbed to A$78m. An additional US$3.848m was placed in contingency.

19 February 2016 27

RESEARCH

Industrials

* at current AUD:USD exchange rate of 0.7

Table 14. Capex allocation in BFS Source: ATC

Operating costs

ATC has estimated that the sighting of the HPA plant in Malaysia may save up to 40% on

operating costs compared with a similar plant located in Australia.

The BFS operating costs are based on actual quotation from suppliers in every aspect of the

process route, from mining through to final production of 4N HPA. Labour rates, where large

savings can be made, are based on recent market survey data, with overhead costs based on

experience.

Total operating costs were estimated at US$32.6m per annum or US$8,140 of finished HPA

product, at full design capacity. This is now equivalent to A$11,600 per tonne at current FX rates.

In US$ terms, ATC estimated a gross operating margin of approximately 65% at the time of writing

(June 2015).

* at current AUD:USD exchange rate of 0.7

Table 15. Opex allocation in BFS Source: ATC

Selling price assumptions

A long term selling price of US$23 per Kg (A$32.86 at current exchange rates) was set for the

BFS financial model, FOB Malaysia.

Meckering 16.0 22.9

HPA Plant (Tanjung Langset) 54.6 78.0

Insurances 1.3 1.8

Contingency 5.0 7.1

Total 76.9 109.9

Altech Chemicals Ltd Capex 2015

US$ (m) A$ (m) Capital Cost Area

Meckering Mining 0.11 0.16

Meckering Beneficiation 1.26 1.80

Transport (Meckering to Malaysia) 0.69 0.99

WA State Royalty 0.09 0.13

HPA Manufacturing 3.76 5.37

HPA selling Costs etc 0.76 1.09

Corporate (Aust) 0.98 1.40

Corporate (Malaysia) 0.5 0.71

Total per Kg 8.15 11.64

US$ (kg) A$ (kg)* OPEX Activity

Altech Chemicals Ltd Opex 2015

28 19 February 2016

RESEARCH

Industrials

Discount rate and NPV sensitivity

ATC employed a discount rate of 10% in the BFS. Australia and Malaysia are relatively low risk

jurisdictions and the current cost of equity and debt are favourable for project funding. We see a

10% discount rate as appropriate given that execution risk on construction and commissioning

are still present. In the BFS, ATC estimated that at an 8% discount rate, NPV increased by ~30%

to US$423m.

The NPV is most sensitive to USD:AUD exchange rates and movement in the HPA selling price,

as this is denominated in USD. In the tables above we have modified the A$ conversion to show

the equivalent amount in A$ at an FX rate of 0.7, more reflective of current rates than that used

in the BFS. This also gives a better estimate of the A$ capital expenditure requirements and

therefore capital raising requirements. The NPV is not as sensitive to capital and operating costs.

19 February 2016 29

RESEARCH

Industrials

11. Corporate and capital structure

Altech Chemicals Australia Pty Ltd is ATC’s wholly-owned subsidiary that holds the HPA

business. Under this holding company are two further wholly-owned subsidiaries - Altech

Meckering Pty Ltd, as the registered holder of the Meckering asset and tenure, and Altech

Chemicals Sdn Bhd that holds the company’s assets in Malaysia.

Figure 2. Company structure under Altech Chemicals Ltd Source: ATC

Capital structure and Shareholders

The capital structure in the table below reflects the lapse of listed 10c options (ASX:ATCO) that

were convertible up to 31 December 2015.

Table 15. Share capital of ATC Source: ATC filing

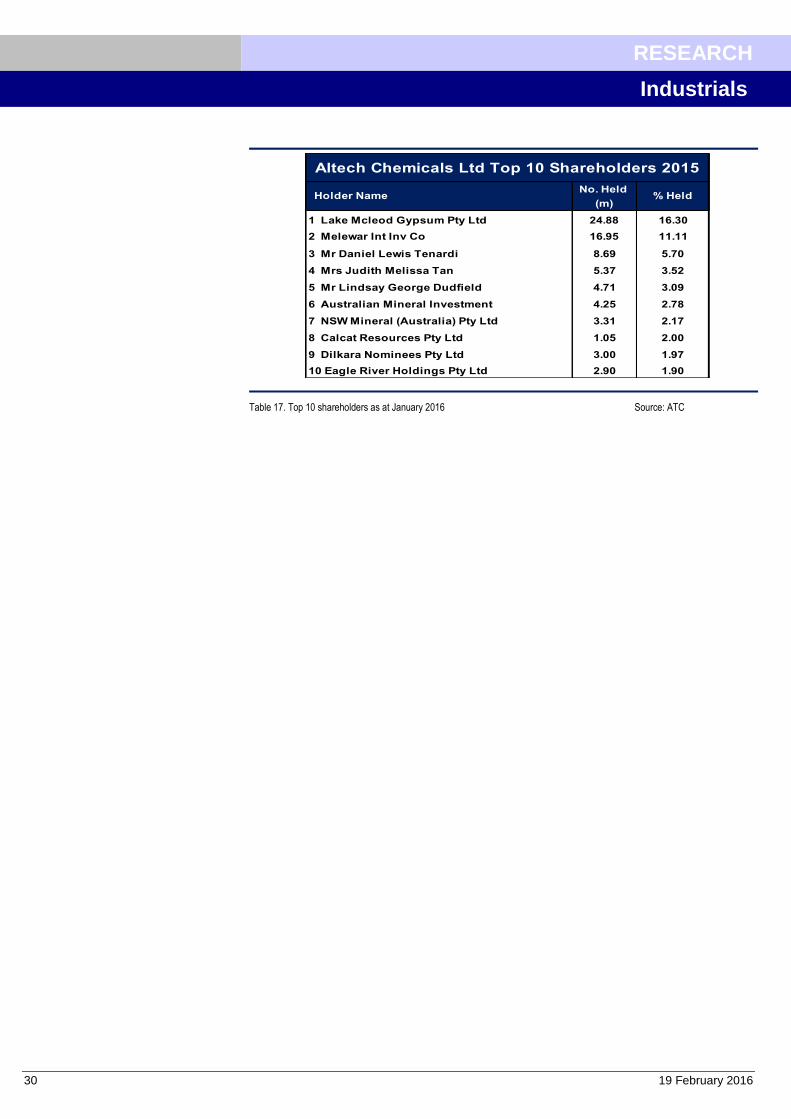

The Top 20 shareholders are tabulated below. A recent Top 20 shareholder is the Melewar Khyra

Group of Companies (Melewar), a Malaysian base diversified financial and industrial services

group. Melewar recently invested $1.0m through a two-stage share placement completed on 20

October 2015 of 16.95m shares. Melewar owns 11.98% of the undiluted issued capital of ATC.

Tunku Dato’ Ya’acob bin Tunku Tan Sri Abdullah, who is the Executive Chairman of Melewar,

was subsequently appointed to the board.

Fully Paid Ordianry Shares (ATC)

Unlisted Options

Unlisted Performance Rights

Share Capital Structure No. of Securities

152,615,782

Altech Chemicals Ltd Capital Structure 2015

6,100,000

19,050,000

30 19 February 2016

RESEARCH

Industrials

Table 17. Top 10 shareholders as at January 2016 Source: ATC

No. Held

(m)

1 Lake Mcleod Gypsum Pty Ltd 24.88 16.30

2 Melewar Int Inv Co 16.95 11.11

3 Mr Daniel Lewis Tenardi 8.69 5.70

4 Mrs Judith Melissa Tan 5.37 3.52

5 Mr Lindsay George Dudfield 4.71 3.09

6 Australian Mineral Investment 4.25 2.78

7 NSW Mineral (Australia) Pty Ltd 3.31 2.17

8 Calcat Resources Pty Ltd 1.05 2.00

9 Dilkara Nominees Pty Ltd 3.00 1.97

10 Eagle River Holdings Pty Ltd 2.90 1.90

Holder Name

Altech Chemicals Ltd Top 10 Shareholders 2015

% Held

19 February 2016 31

RESEARCH

Industrials

12. Upstream Items

The Meckering aluminous clay resource

ATC owns 100% of the Meckering aluminous clay (kaolin) resource in Western Australia, just

130km east of the port of Fremantle.

Geologically, the aluminous clay deposit, currently estimated at 65Mt at a brightness value of

85.3% (<45 micron) is a weathered granitoid, where almost all of the constituent minerals, other

than quartz, have been weathered to a white aluminous clay. Total impurities in the Meckering

deposit are a fraction of other aluminous clay deposits with an Fe2O3 content of just 0.7% and

K2O and NaO contents of just 0.1% in typical analysis. This analysis is comparable to the

composition of ceramic-grade kaolins used in tableware (ECC Grolleg)

The Meckering aluminous clay deposit is primary in nature. The nature of the parent rock will

define the level of impurities in the resultant clays, with iron, titanium and sodium content being

particularly important.

Table 18. Mineral resources for Meckering Aluminous clay deposit Source: ATC

The deposit is outcropping at surface and lies within below 2m of ‘soil’ cover. A transition or

mottled zone is present over most of the deposit to a depth of around 4m, under which lies the

white aluminous clay with residual quartz. The water table will not be intersected in mining. The

water in the photograph below is rain water accumulating in the historic trial pit.

Figure 3. Location map of the Meckering aluminous clay deposit Source: ATC

Indicated 16,770,000 42.3 83.2

Inferred 48,280,000 41.8 83.5

Total Mineral Resources 65,000,000 41.9 83.4

Note 1. The -45 micron precentage was measured by wet screening

Note 2. Brightness is the ISO brightness of the -45 micron fraction

Altech Chemicals Ltd JORC Compliant Resource Table 2015

Classification

Mineral Resources (JORC 2004)

as at 30 June 2015

Tonnes -45 micron (%) 1 Brightness 2

Definition of Brightness Brightness is defined as the ratio, expressed as a percentage, of the radiation reflected by a body to that reflected by a perfectly reflecting ISO-approved BaSO4 standard measured at an effective wavelength of 457nm with a Carl Zeiss photoelectric reflection photometer

Source: British Geological Survey

32 19 February 2016

RESEARCH

Industrials

Due to the size and density contrast between the clay and the remnant quartz grains, the quartz

can be relatively easily separated from the clay. Due to the low level of impurities, especially iron,