retirement plan funding dynamics: how retirement plan variables affect funding outcomes

DESCRIPTION

Retirement Plan Funding Dynamics: How Retirement Plan Variables Affect Funding Outcomes. Jack Lawless, CPA, APM Pension Strategies, LLC DFW FPA Platinum Sponsor. Objectives. Identify the variables that play a roll in funding options when looking at a Qualified Retirement Plan. - PowerPoint PPT PresentationTRANSCRIPT

Retirement Plan Funding Dynamics:

How Retirement Plan Variables Affect Funding Outcomes

Jack Lawless, CPA, APMPension Strategies, LLC

DFW FPA Platinum Sponsor

Objectives

• Identify the variables that play a roll in funding options when looking at a Qualified Retirement Plan.

• Explore how those different variables affect the available funding for both Defined Contribution and Defined Benefit Plans.

• Look at strategies to optimize the future outcome by correctly managing the current variables.

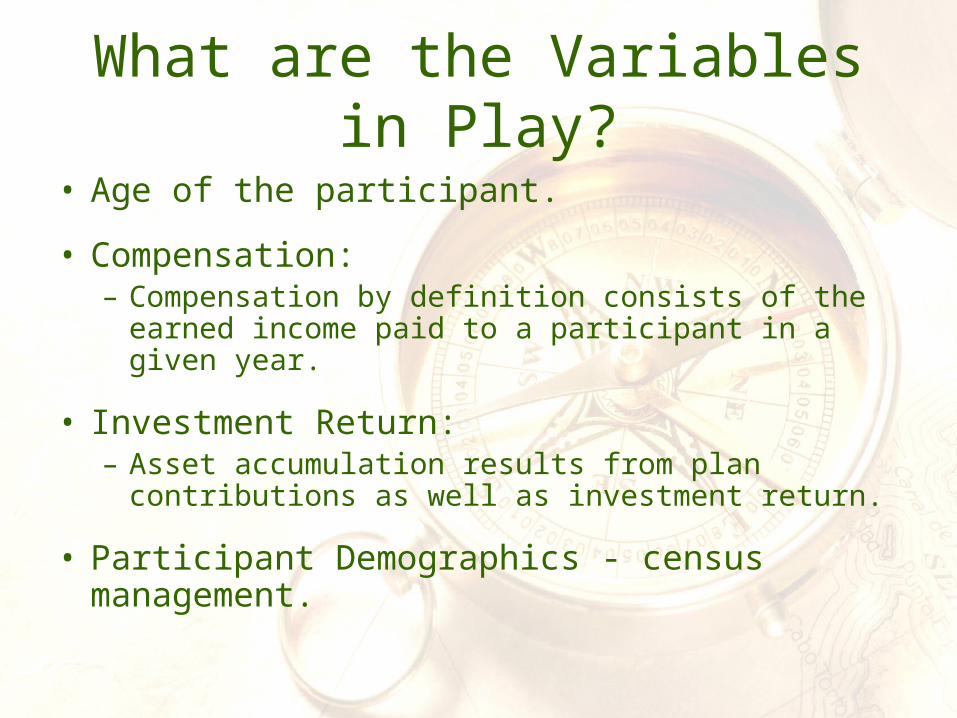

What are the Variables in Play?

• Age of the participant.

• Compensation:– Compensation by definition consists of the earned

income paid to a participant in a given year.

• Investment Return: – Asset accumulation results from plan contributions as

well as investment return.

• Participant Demographics - census management.

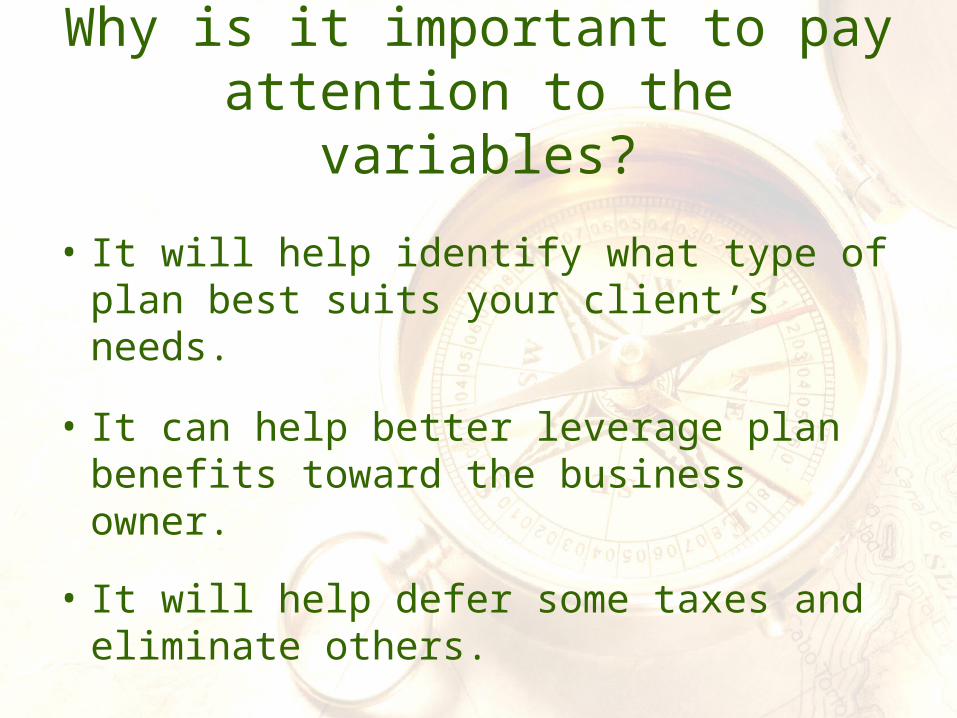

Why is it important to pay attention to the variables?

• It will help identify what type of plan best suits your client’s needs.

• It can help better leverage plan benefits toward the business owner.

• It will help defer some taxes and eliminate others.

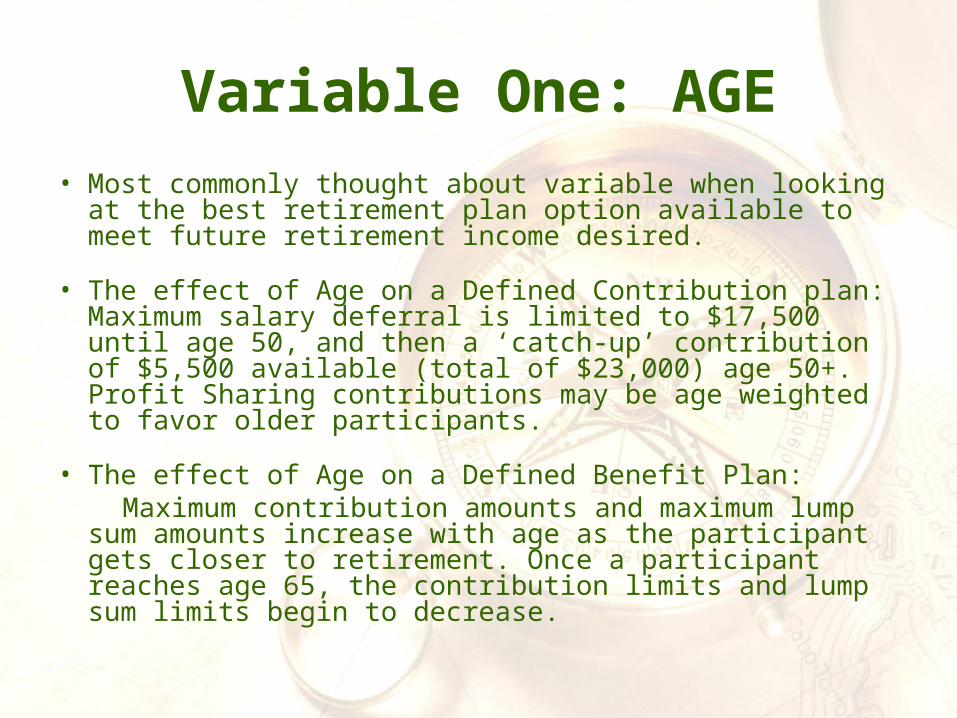

Variable One: AGE

• Most commonly thought about variable when looking at the best retirement plan option available to meet future retirement income desired.

• The effect of Age on a Defined Contribution plan: Maximum salary deferral is limited to $17,500 until age 50, and then a ‘catch-up’ contribution of $5,500 available (total of $23,000) age 50+. Profit Sharing contributions may be age weighted to favor older participants.

• The effect of Age on a Defined Benefit Plan: Maximum contribution amounts and maximum lump sum

amounts increase with age as the participant gets closer to retirement. Once a participant reaches age 65, the contribution limits and lump sum limits begin to decrease.

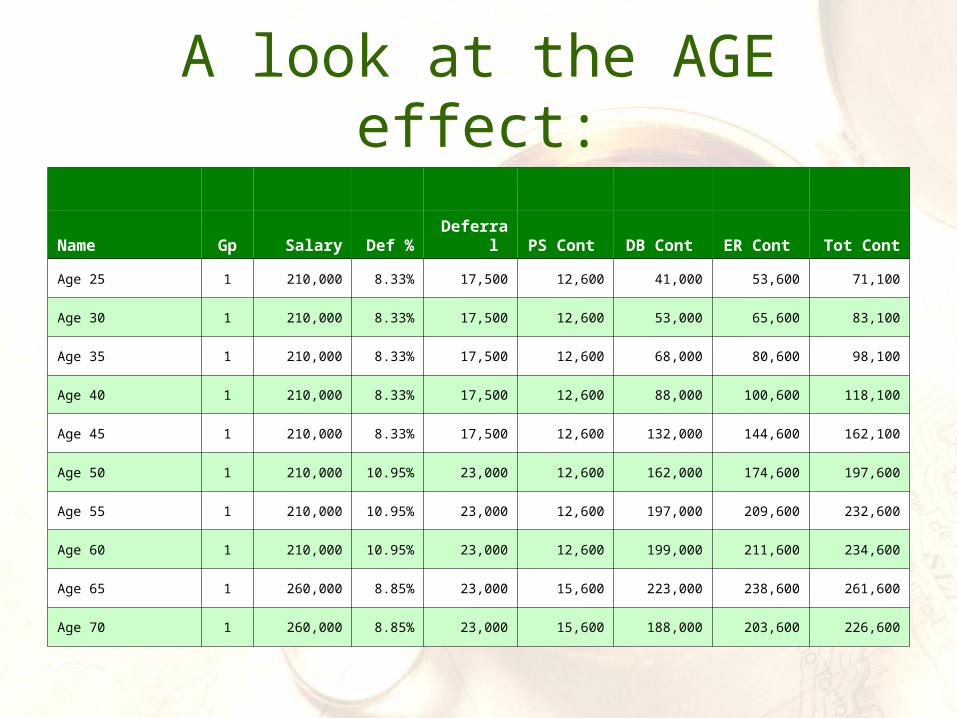

A look at the AGE effect:

Name Gp Salary Def % Deferral PS Cont DB Cont ER Cont Tot Cont

Age 25 1 210,000 8.33% 17,500 12,600 41,000 53,600 71,100

Age 30 1 210,000 8.33% 17,500 12,600 53,000 65,600 83,100

Age 35 1 210,000 8.33% 17,500 12,600 68,000 80,600 98,100

Age 40 1 210,000 8.33% 17,500 12,600 88,000 100,600 118,100

Age 45 1 210,000 8.33% 17,500 12,600 132,000 144,600 162,100

Age 50 1 210,000 10.95% 23,000 12,600 162,000 174,600 197,600

Age 55 1 210,000 10.95% 23,000 12,600 197,000 209,600 232,600

Age 60 1 210,000 10.95% 23,000 12,600 199,000 211,600 234,600

Age 65 1 260,000 8.85% 23,000 15,600 223,000 238,600 261,600

Age 70 1 260,000 8.85% 23,000 15,600 188,000 203,600 226,600

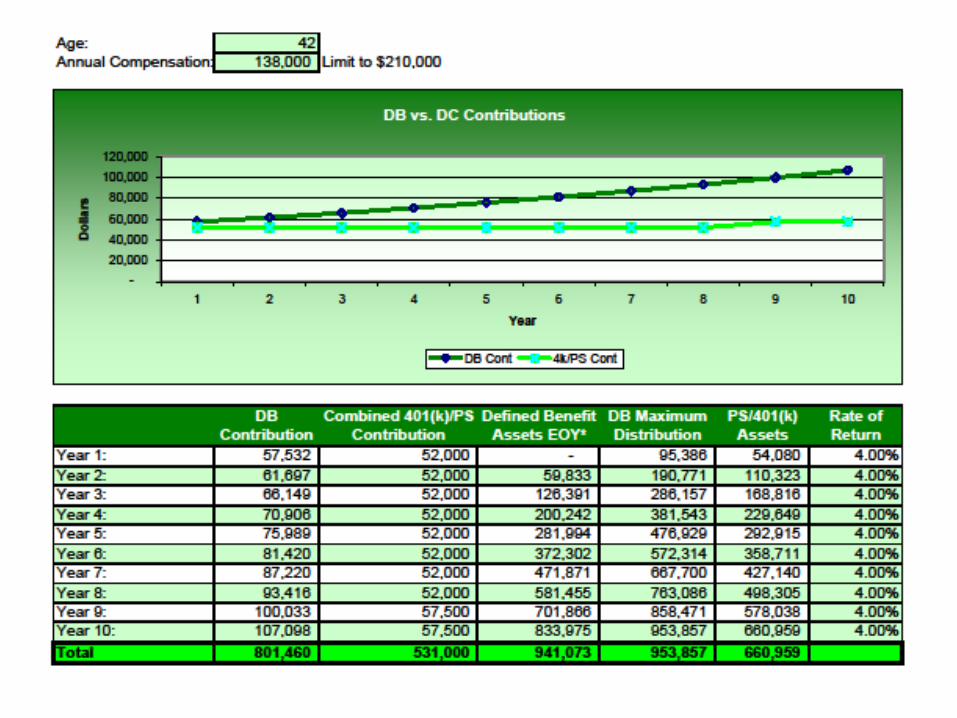

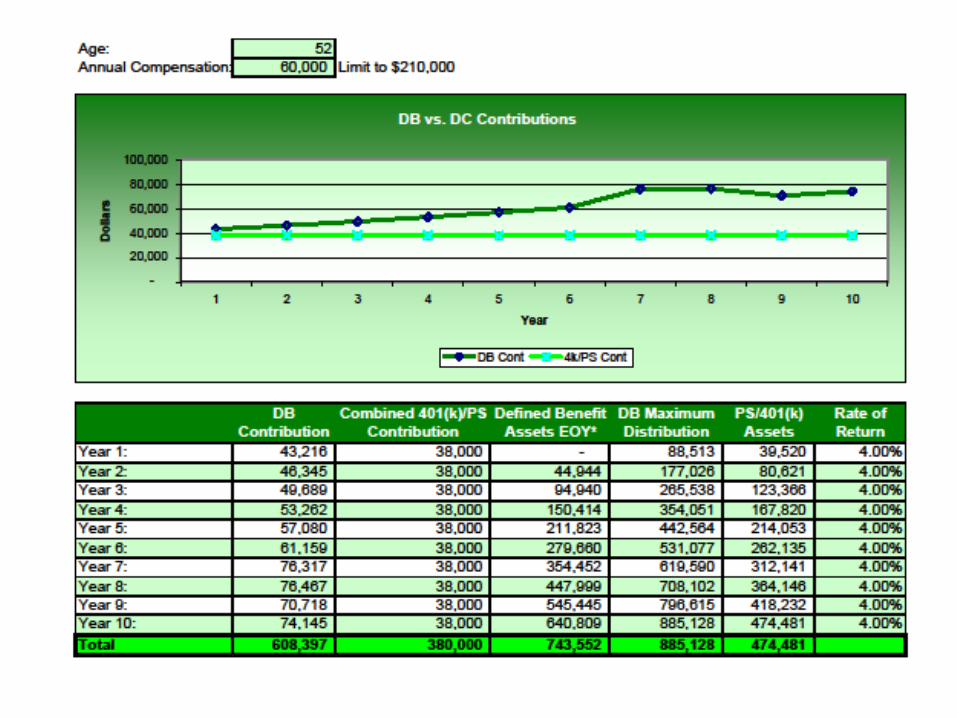

Variable Two: Compensation

• Current maximum compensation allowed: $260,000

• How compensation affects available funding in a Defined Contribution Plan:– Profit Sharing Contribution is based off of 25% of compensation, up

to a total DC contribution allowed of $52,000.– Once Compensation is above $138,000, participant has reached

maximum contribution limit of $52,000 (or $57,500 if over age 50), between the maximum deferral and profit sharing contributions.

• How compensation affects available funding in a Defined Benefit Plan:– Defined Benefit Plans use current, high average, or final average

compensation. – Defined Benefit compensation maximum when calculating a lump

sum is $210,000 at retirement age 62.

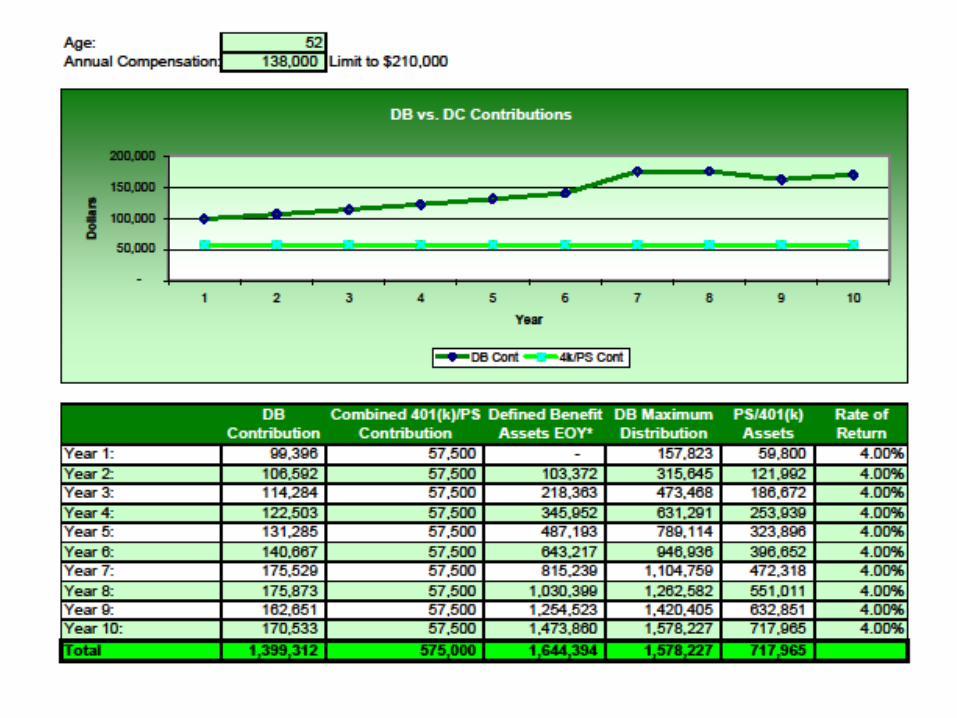

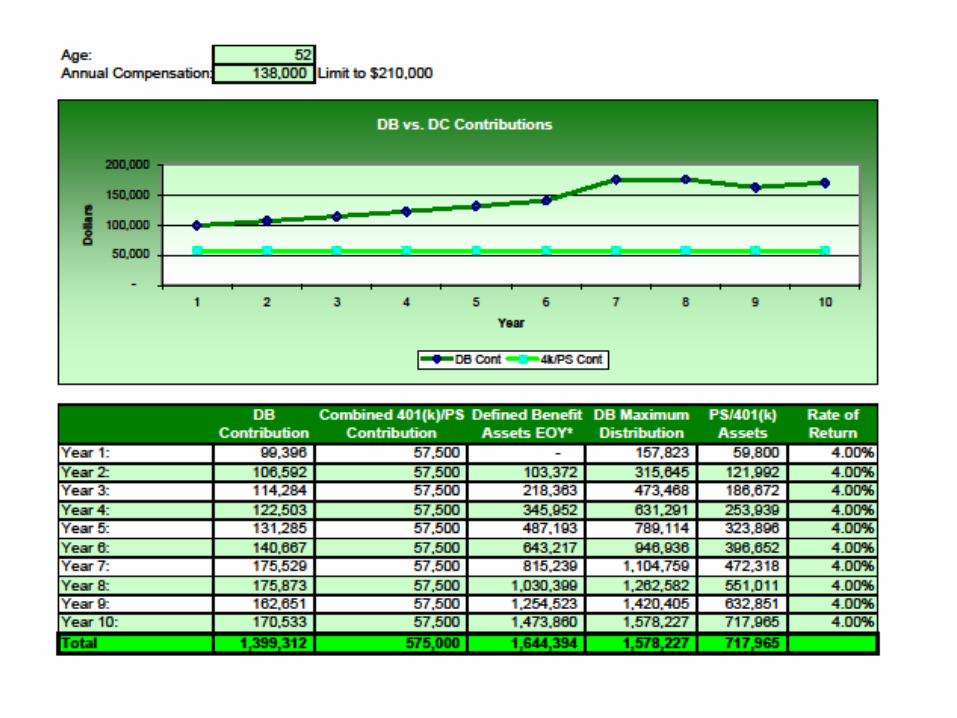

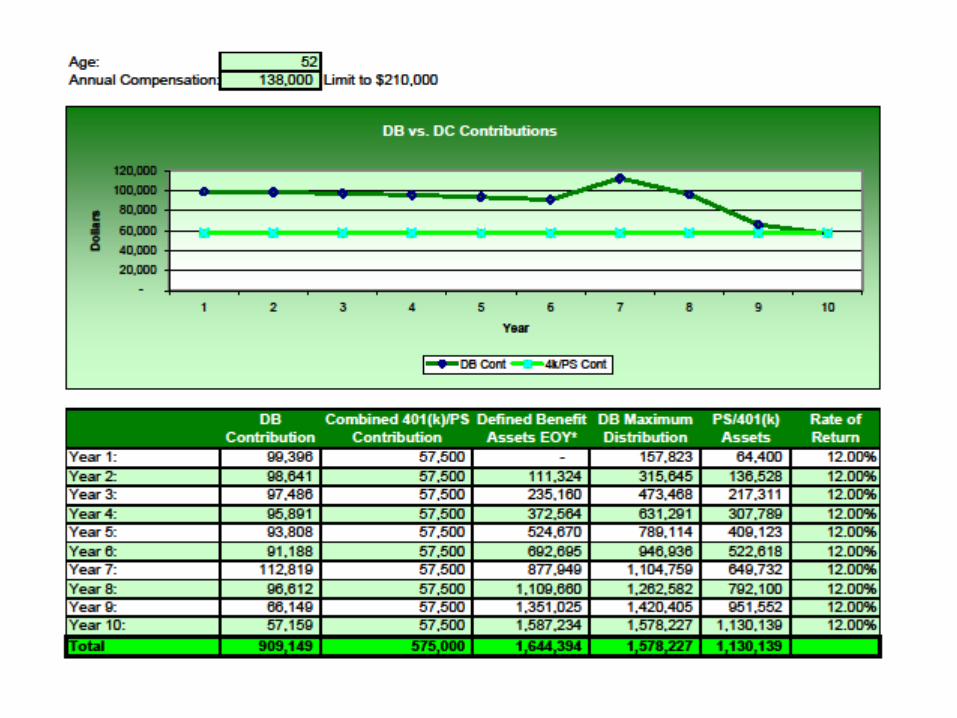

Variable Three: Return

• Asset accumulation results from two sources:– Contributions made into the plan.– Rate of Return on investments.

• In a Defined Contribution Plan, the rate of return on investments plays no part in the calculation of the contributions allowed. – High growth rate investments do better in a Defined Contribution Plan.

• In a Defined Benefit Plan, these two sources work hand in hand: As the rate of return increases, the contribution requirements will decrease. Likewise, if there is a negative rate of return (loss), the contribution for the next year will increase, in order to make up a portion of the investment loss.– Very conservative investments work best in a Defined Benefit Plan.

Variable FOUR: Company Demographics

• There are different allocation methods available in Defined Contribution plans, which are chosen depending on age and salary history of the employees at a company.

• Depending on company demographics, an employer may chose to have a cross-tested Defined Benefit Plan or go with a Cash Balance option.

• Also, part-time (otherwise excludable) employees, may be used to help balance testing requirements in either a Defined Benefit or Defined Contribution plan.

Design with Owner and Employee

Employee Name Salary 401(k)

Contribution Safe Harbor Contribution

Profit Sharing Contribution

Defined Benefit

Contribution Total Contribution Owner- Age 53 150,000 23,000 - 1,000 94,594 118,594 Employee- Age 48 65,000 - 1,950 9,845 9,107 20,902 Totals 215,000 23,000 1,950 10,845 103,701 139,496

Design with Owner, Employee, and Stepson:

Employee Name Salary 401(k)

Contribution Safe Harbor Contribution

Profit Sharing Contribution

Defined Benefit

Contribution Total Contribution Owner- Age 53 150,000 23,000 - 1,000 94,594 118,594 Employee- Age 48 65,000 - 1,950 2,080 2,277 6,307 Stepson- Age 19 8,000 - 240 256 48 544 Totals 223,000 23,000 2,190 3,336 96,919 125,445

Total Contribution 139,496 125,445

% to Owner and family 85% 95%

% to Others 15% 5%

Rewards of a little investigative work:

Let’s take a look….

Pension Strategies, LLCMallory YoungSenior Pension Consultant(214) 221-9800 Ext. [email protected]

www.pensionstrategies.com Request for proposalRetirement plan limitsSign up for Newsletter