reverse mortgage: pros and cons

TRANSCRIPT

Getting a reverse mortgage is as much alifestyle decision as it is a financialdecision. As in almost all major decisionsthat one must make in life, opting for areverse mortgage has pros and cons toconsider.

BLOWNMORTGAGE.COM

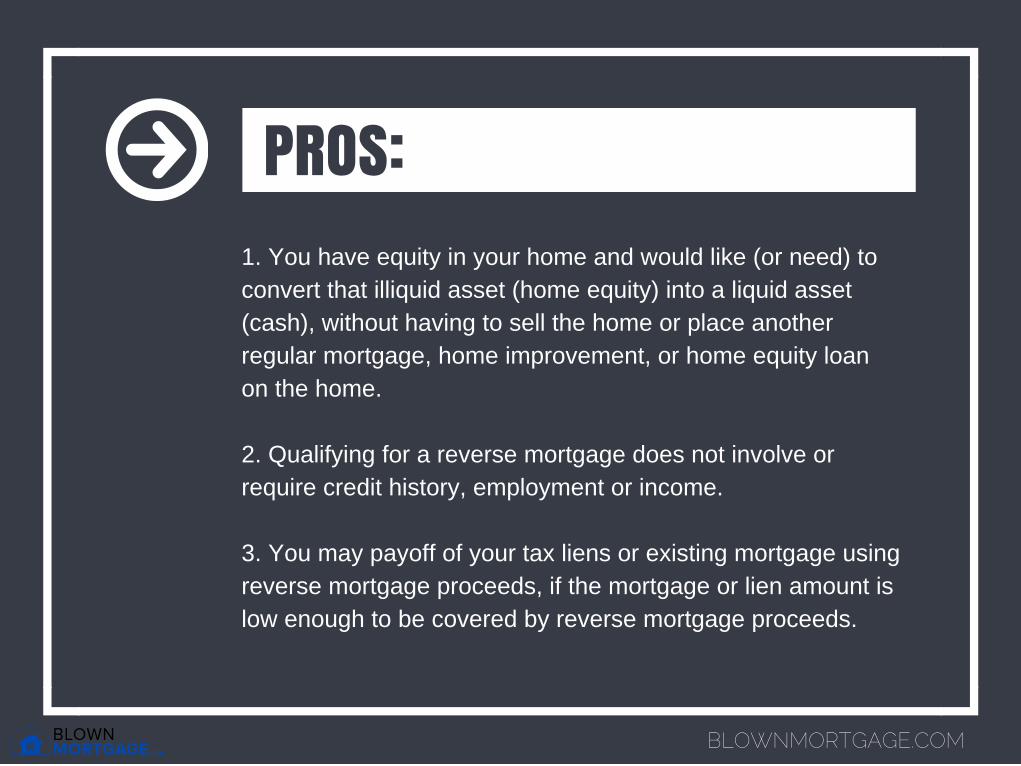

PROS:1. You have equity in your home and would like (or need) toconvert that illiquid asset (home equity) into a liquid asset(cash), without having to sell the home or place anotherregular mortgage, home improvement, or home equity loanon the home.

2. Qualifying for a reverse mortgage does not involve orrequire credit history, employment or income.

3. You may payoff of your tax liens or existing mortgage usingreverse mortgage proceeds, if the mortgage or lien amount islow enough to be covered by reverse mortgage proceeds.

BLOWNMORTGAGE.COM

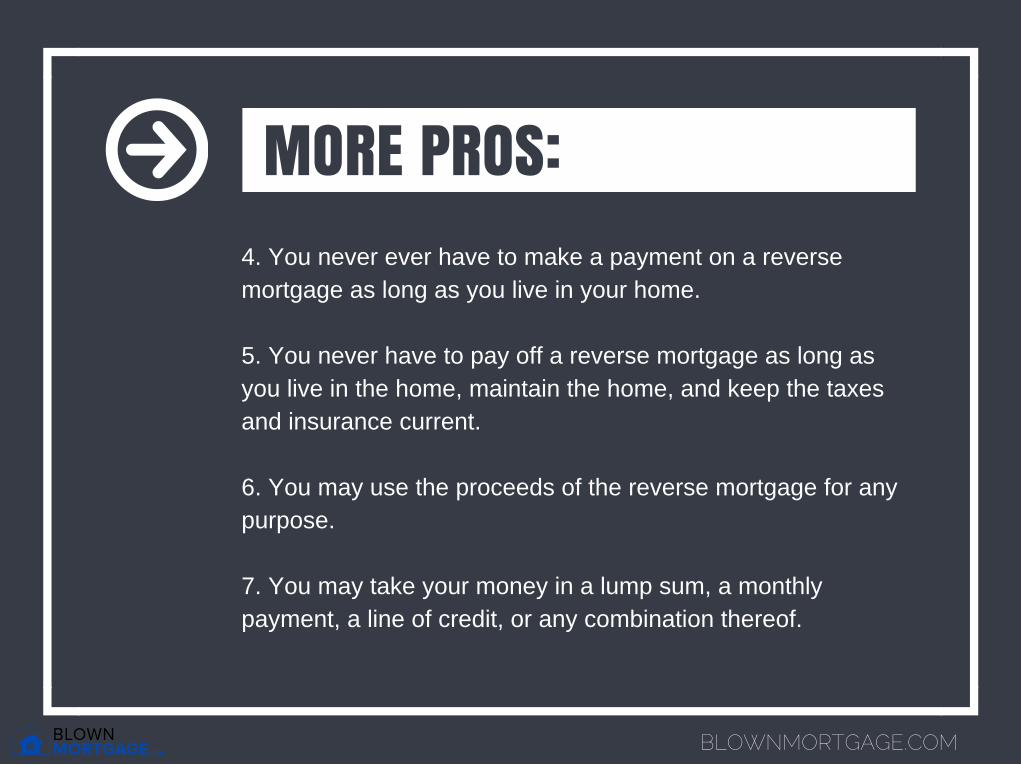

MORE PROS:4. You never ever have to make a payment on a reversemortgage as long as you live in your home.

5. You never have to pay off a reverse mortgage as long asyou live in the home, maintain the home, and keep the taxesand insurance current.

6. You may use the proceeds of the reverse mortgage for anypurpose.

7. You may take your money in a lump sum, a monthlypayment, a line of credit, or any combination thereof.

BLOWNMORTGAGE.COM

MORE PROS:8. Your line of credit can grow. If you choose a HECM reversemortgage with a line of credit payment option, the size of theline of credit will increase annually.

9. Your heirs only have to pay back the loan to the extent thesale of your home covers the debt. If the debt exceeds thesales price of the home, FHA pays the difference, not yourheirs. They never have to come out-of-pocket to pay off yourreverse mortgage.

10. Funds you receive from a reverse mortgage are tax freeand do not affect your social security or Medicare benefits.

BLOWNMORTGAGE.COM

MORE PROS:11. You still have equity in your home following the funding ofa reverse mortgage.

12. The bank does not own your home; you do, and will for aslong as you live.

BLOWNMORTGAGE.COM

CONS:1. You must have significant equity in your home, or have itpaid for in full, in order to secure a reverse mortgage. If youhave a high loan to value on your home, a reverse mortgagemay not be right for you.

2. The amount of money you are entitled to, under reversemortgage guidelines, is dependent on the age of the youngestborrower in the home and the value of the home; and, thepercent of value you receive varies with your age at the timeof the closing of the loan.

BLOWNMORTGAGE.COM

MORE CONS:3. Failure to maintain the home to minimum FHA standards,to keep taxes paid and keep homeowner’s insurance in forceon the home, are elements of default on a reverse mortgage.If you cannot, or will not meet those minimum requirements, areverse mortgage may not be right for you.

4. A reverse mortgage, like any mortgage, has closing costs(including FHA Mortgage Insurance Premiums) which arepaid at the closing of the loan out of loan proceeds. Thisamount, while usually comparable to costs incurred in anymortgage transaction, can amount to several thousand dollarsand that amount is deducted from the funds you will beeligible to receive from the reverse mortgage loan.

BLOWNMORTGAGE.COM

MORE CONS:5. Reverse mortgage proceeds do not affect social security orMedicare eligibility, but may affect other programs such asSSI, or State run programs such as Medicaid. Before optingfor a reverse mortgage, check with program advisors oradministrators to see what effect, if any, a reverse mortgagemay have on your eligibility for those programs.

6. A reverse mortgage must be paid off if you move from thehome on which a reverse mortgage is placed. If you leave thehome for more than one year, or switch to another home asyour primary residence, this event is triggered.

BLOWNMORTGAGE.COM

MORE CONS:7. Normally heirs sell your house to pay off your reversemortgage after you pass away. If your heirs elect to keep yourhome after you pass away the reverse mortgage loan mustbe paid from insurance proceeds, refinance proceeds, thepersonal assets of the heirs, or from other resources. Thebottom line is the reverse mortgage must then be paid in full.

8. Equity in your home may be “used up” over time, leavinglittle or no equity for your heirs. This may, or may not be aproblem for your heirs. Simply ask them if they are expectingto get money from the equity you have in your home whenyou die. Most will want you to enjoy the money you haveinvested in your home over time and will say “no,” but thequestion probably should be asked anyway.

BLOWNMORTGAGE.COM

As with anything in life, it is good toweigh the pros and cons of getting areverse mortgage – and be sure tospeak with a loan officer who specializesin Reverse Mortgages. They will be ableto help you see what is right for you inyour particular situation.

BLOWNMORTGAGE.COM

CLICK HERETO LEARN MORE:

BLOWNMORTGAGE.COM LENDER HOTLINE: 888-581-5008

INFORMATION PROVIDED BY:

Justin McHood

Mortgage Commentator

Information Originally Published: 4/22/15

Justin McHood is Americas Mortgage Commentator and has been providing Mortgage commentary for over 10 years.

http://www.blownmortgage.com/reverse-mortgage-pros-and-cons/

BLOWNMORTGAGE.COM

MORTGAGECOMMENTATOR.COM

@MORTGAGECOM_

FACEBOOK.COM/MORTGAGECOMMENTATOR

LEARN MORE ABOUT MORTGAGE COMMENTATOR: