review of australia’s automotive industry...the review confirmed the importance of the automotive...

TRANSCRIPT

Review of AustrAliA’s Automotive industry

FinAl report22 july 2008

© Commonwealth of Australia 2008

This work is copyright. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission from the Commonwealth. Requests and inquiries concerning reproduction and rights should be addressed to the Commonwealth Copyright Administration, Attorney General’s Department, Robert Garran offices, National Circuit, Canberra ACT 2600 or posted at http://www.ag.gov.au/cca.

iSBN 0 642 72601 9

Note: The dollar amounts in this report are in Australian dollars, unless otherwise indicated.

Disclaimer

The material contained within this document has been developed by the Review of Australia’s Automotive industry. The views and opinions expressed in the materials do not necessarily reflect those of the Australian Government or the Minister for innovation, industry, Science and Research. The Australian Government and the Review of Australia’s Automotive industry accept no responsibility for the accuracy or completeness of the contents, and shall not be liable (in negligence or otherwise) for any loss or damage (financial or otherwise) that may be occasioned directly or indirectly through the use of, or reliance, on the materials.

furthermore, the Australian Government and the Review of Australia’s Automotive industry, their members, employees, agents and officers accept no responsibility for any loss or liability (including reasonable legal costs and expenses) or liability incurred or suffered where such loss or liability was caused by the infringement of intellectual property rights, including moral rights, of any third person.

22 July 2008

Senator the Hon Kim CarrMinister for innovation, industry, Science and ResearchParliament HouseCANBeRRA ACT 2600

Automotive Review Secretariat

industry House, 10 Binara StreetCANBeRRA CiTY ACT 2601

GPo Box 9839Canberra ACT 2601 Australia

email: [email protected]: www.innovation.gov.au/automotivereview

dear minister

i am pleased to submit my report on the Review of Australia’s Automotive industry.

This Review, commissioned by you on behalf of your Government, comes at a crucial time for automotive production in Australia.

A time when the industry is under considerable pressure due to a combination of externalities including the appreciation of the Australian dollar, higher fuel costs, cleaner emission requirements and intense worldwide competition.

Despite these challenges, the industry has been transforming into a more globally integrated and competitive one. This Review, therefore, recommends that the process of transformation continues through a new transition phase with the ultimate aim of achieving economic and environmental sustainability by 2020.

in particular, the Review recommends considerable new opportunities for Australia’s automotive industry in new cleaner-emissions technology.

To that end, one of the key recommendations of this Review is the bringing forward and doubling of the Green Car innovation fund combined with the inclusion of transportation in any new emissions trading scheme.

These two initiatives should result in Australia’s automotive industry changing vehicle production capacity to become more fuel-efficient, lower Co2-emitting and more internationally focused.

Additionally, this Review recommends considerable change to the existing transitional arrangements, while continuing with a lower tariff regime.

in particular, the Review recommends that the existing Automotive Competitiveness and investment Scheme be reformed into a new Global Automotive Transition Scheme, which supports greater innovation through enhanced research, development and design.

The new scheme also provides a mechanism to support structural adjustment in the Australian automotive supply chain in order to move towards supply arrangements that are more reliable and consolidated. This should, in appropriate circumstances, include fair and reasonable structural adjustment assistance for displaced automotive employees.

The emphasis on exports of assembled vehicles and component parts is also reinforced, noting that the Australian automotive industry is crucial to our worldwide trading position.

The Review confirmed the importance of the automotive industry to Australia’s economy. for example, automotive product exports in 2007 were $4.7 billion—establishing the industry amongst Australia’s top 10 export earners and the largest exporter of elaborately transformed manufactures. The industry earns more export income than more traditional industries such as wine, wheat and wool.

| v

The automotive industry is also a major investor in innovation, accounting for nearly 17 percent of all manufacturing business expenditure on research and development (R&D). in addition, the R&D intensity of the industry is around three times higher than for manufacturing as a whole and around nine times higher than for the economy. This is a key element to sustaining an internationally competitive industry based on high skills and high-wage jobs.

Australia is one of only 15 countries with the capability to take a car from concept all the way to full production. This capability encompasses strong skill sets in R&D, design, engineering, product and process development, and advanced manufacturing. The industry is also well placed to take advantage of its proximity to Asia, particularly China and india, which are expected to be major contributors to the growth in light vehicle production and sales.

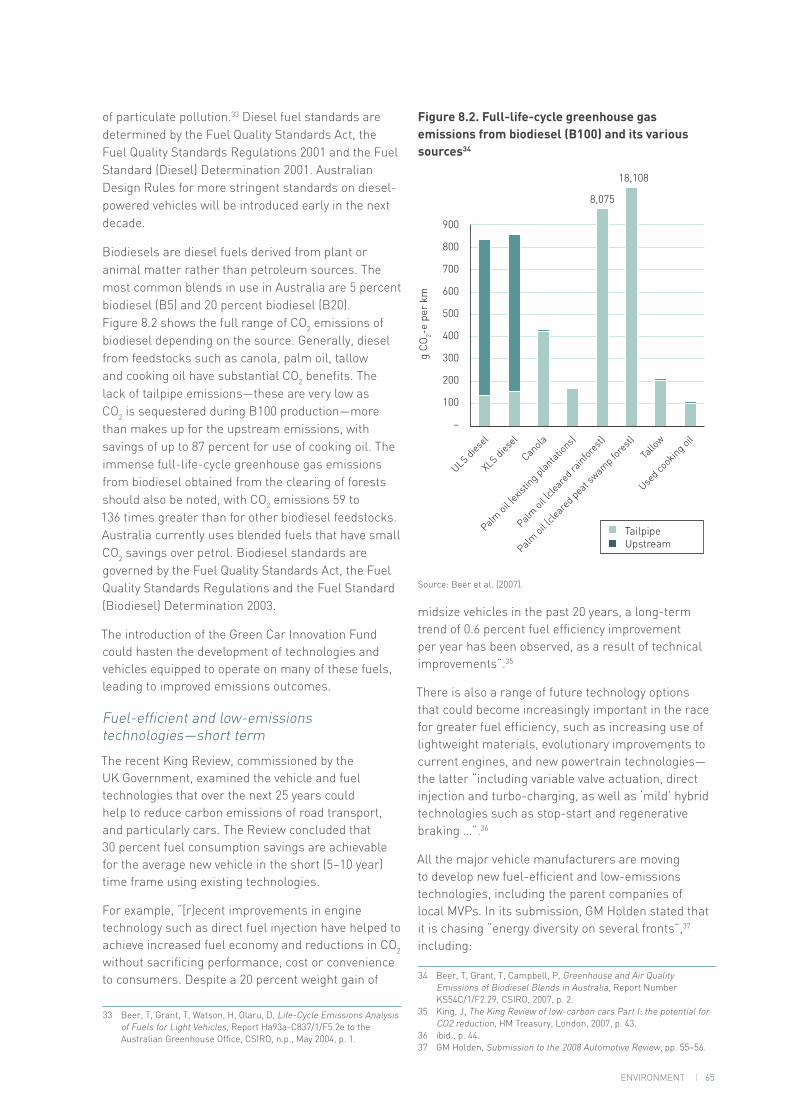

The industry has important links to the rest of the economy, and supports Australia’s capabilities in designing and manufacturing elaborately transformed goods. for example, the advanced manufacturing sector relies on the capital investment by the vehicle manufacturers and major Tier 1 companies, while other manufacturers are heavily reliant on the skills and expertise of the automotive component sector. without this skills base, industries such as the truck industry would struggle to manufacture locally. This could be to the detriment of other important sectors such as transport and resources.

The Review benefited from consultations with stakeholders and with the leaders of other concurrent reviews. The latter included Dr Terry Cutler, Professor Ross Garnaut, Professor Roy Green and Mr David Mortimer Ao.

in concluding, i would like to thank the Review’s expert Panel members—Mr Tim Harcourt, Mr Peter Upton, Dr elizabeth webster and Mr Nixon Apple—for their important contribution and assistance in preparing this report. The support provided by the innovation Department’s secretariat was also invaluable. furthermore, i would like to thank all those individuals, organisations and companies that made submissions to the Review, as well as the Productivity Commission which modelled the economy-wide effects of future assistance arrangements. These proved very helpful to the Panel in assessing the merits of various policy options.

yours sincerely

Hon steve Bracksleaderreview of Australia’s Automotive industry

| v

TeRMS of RefeReNCe vii

Review leADeR’S SUMMARY 1

RePoRT STRUCTURe AND SUMMARY of ReCoMMeNDATioNS 3

1. THe AUSTRAliAN AUToMoTive iNDUSTRY 9

2. oUTlooK foR THe AUSTRAliAN AUToMoTive iNDUSTRY 19

3. THe GloBAl AUToMoTive iNDUSTRY 25

4. CURReNT AUSTRAliAN AUToMoTive PoliCY ARRANGeMeNTS 31

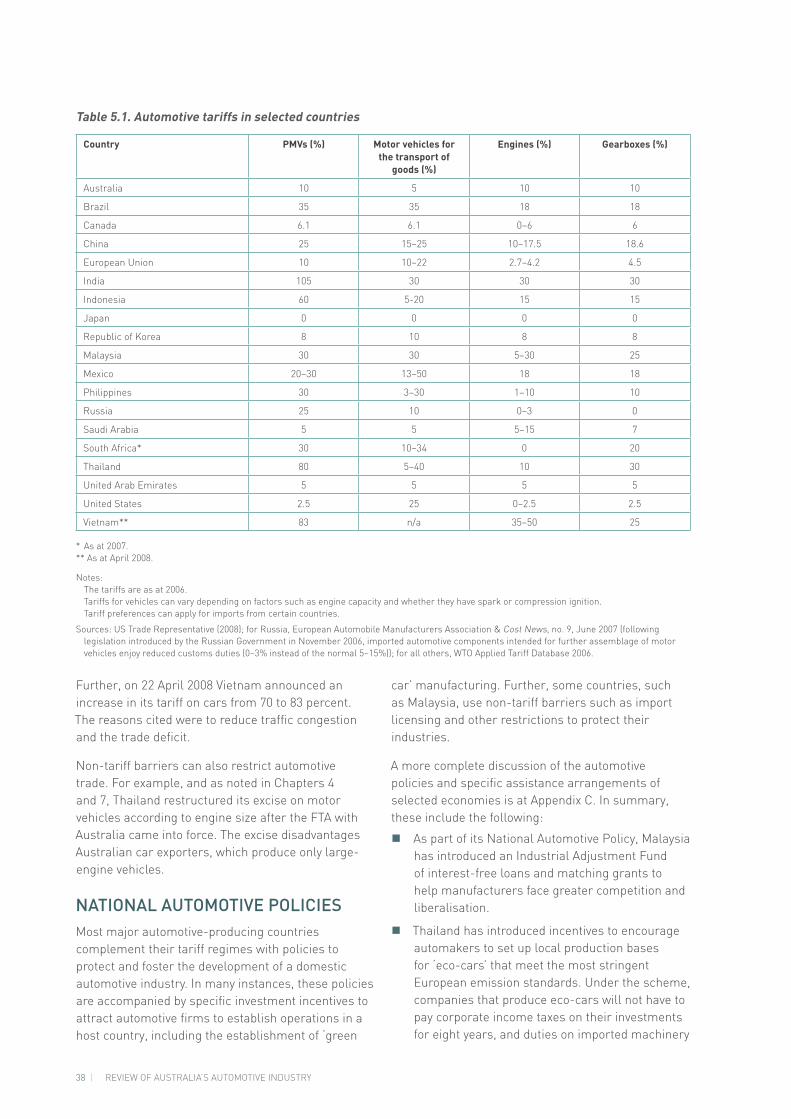

5. iNTeRNATioNAl AUToMoTive PoliCieS AND ASSiSTANCe ARRANGeMeNTS 37

6. iNNovATioN 41

7. MARKeT ACCeSS 49

8. eNviRoNMeNT 59

9. ReSTRUCTURiNG THe AUSTRAliAN AUToMoTive iNDUSTRY 75

10. veHiCle SAfeTY 87

11. fUTURe AUToMoTive ASSiSTANCe ARRANGeMeNTS 91

APPeNDixeS A–N CoNTeNTS 101

ABBReviATioNS AND DefiNiTioNS 183

RefeReNCeS 185

Contents

|vii

1. TheAustralianautomotiveindustryplaysanimportantroleinemployment,exportsandinnovationintheAustralianeconomy.inparticular,innovationintheautomotiveindustryresultsinsignificantspillovereffectsacrosstheeconomy,andparticularlythemanufacturingsector.inthiscontext,theAustralianGovernmenthascommissionedahighlevelreviewpaneltoconductareviewoftheautomotivesector,inconsultationwithabroadrangeofindustrystakeholders.Thisreviewistotakeplaceconcurrentlywithawide-rangingreviewofAustralia’snationalinnovationsystemandshouldhaveregardtotheissuesraisedinthatreview.

2. TheReviewwillbearinmindtheGovernment’sdesire:

a. foraninternationallycompetitiveandgloballyintegratedautomotivemanufacturingsector;and

b. tooptimisetheoveralleconomicperformanceoftheAustralianeconomy,includinglimitingpriceimpactsonAustralianconsumersandbusinesses.

3. TheReviewistoreportonkeyoutcomesofthecurrentpolicysettingsfortheautomotivemanufacturingsector,including:

a. anevaluationofthekeyoutcomesoftheAutomotiveCompetitivenessandinvestmentScheme(includinganassessmentoftheimpactsoneachofthefourcategoriesofparticipantsintheScheme);

b. anassessmentofthelegislatedpassengermotorvehicletariffreductions,takingintoaccounttheglobalautomotivesectorandgeneraltradeenvironment;and

c. anassessmentofcurrentandprospectivetradeobligationsarisingfromAustralia’smultilateral,regionalandbilateralcommitments.

4. TheReviewwillevaluatetheappropriatenessoftheAutomotiveCompetitivenessandinvestmentScheme(ACiS)inthecurrentcompetitiveenvironmentinrelationto:

a. thepossibleretargetingofassistancewithinACiS;and

b. investigating,identifyingandevaluatingpossiblealternativeassistancemechanisms,consistentwithAustralia’sinternationaltradeobligations.

5. TheReviewwillalsomakeanassessmentofthechallengesandopportunitiescurrentlyfacingthesector,includinghowthosechallengesandopportunitiesmightimpactonthelong-termviabilityandsustainabilityofthesector.inmakingthisassessment,theReviewshouldtakeaccountoffactorssuchas:

a. thestrengthsandweaknessesofthesector;

terms of reference for the review of australia’s automotive industry

viii| REviEWofAUSTRALiA’SAUToMoTivEiNDUSTRY

b. recentdevelopmentsandexpectedfuturedevelopmentsandconditionsintheglobalautomotivesector,including:

i. opportunitiesfor,andbarriersto,enhancedglobalintegration;

ii. competitionforinvestmentintheglobalsector;and

iii. progressontradeliberalisation(includingfreetradeagreements)intheautomotivesectorinbothexistingandprospectiveexportmarketsforAustralia.

c. theimpactofclimatechangeandchangingconsumerpreferencestowardslowemissionsandfuelefficientvehicles;and

d. otherpossiblehindrancestotheviabilityofthesectoronboththedemandandsupplysides,suchasexchangerates,petrolprices,skillshortagesandotherenvironmentalissues.

6. TheReviewwillmakerecommendationsonanyoftheissuesidentified,including:

a. measurestoboostinnovationinthesectorandtotakeadvantageofthehighlyinnovativenatureoftheautomotiveindustry;

b. measurestoensurethatsuitablyskilledpeopleareavailableandthatfairworkingpracticesareguaranteed;

c. theimpactofclimatechangepolicyontheautomotiveindustry;

d. thedeliveryoftheAustralianGovernment’sGreenCarinnovationfundfrom2011;

e. facilitatingleadershipamongAustralianautomotiveproducersandcomponentsuppliersindevelopingandadaptingfuelefficienttechnologiesandknow-howintheproductionofmotorvehiclesinAustralia;and

f. improvingAustraliancompanies’accesstoglobalsupplychainsandexportmarkets.

7. TheReviewistoprovideaninterimreporttotheGovernmentby31March2008andafinalreportby31July2008.

|1

TheAustralianAutomotiveReviewispredicatedonprovidingadvicetotheFederalGovernmentonmeasuresrequiredtoachieveaneconomicallyandenvironmentallysustainableAustralianautomotiveindustry.

TheAustralianautomotiveindustryhasbeentransformedtoamoregloballyintegratedandcompetitiveindustry.

ThistransitionneedstobeenhancedandadvancedsothattheAustralianautomotiveindustryachieveseconomicandenvironmentalsustainabilityby2020.Indoingso,theindustrywillcontinuetoprovideAustralia’slargestnon-resourceexportproduct.

Toachievetheseaims,theReviewcontinuesthepolicysettingsoverthelasttwodecadesofphasingdowntariffsupport,encouragingincreasedexportsandenhancinginnovationthroughmoreeffectiveresearch,developmentanddesign.TheReviewalsotakesaccountofthesignificantlychangedconditionssince2002duetotheappreciationoftheAustraliandollar,higherfuelcosts,cleaneremissionrequirementsandnewfreetradeagreements.

Thenewrecommendationsacknowledgethesechangesand,asaconsequence,proposenewtransitionalarrangementstoenabletheAustralianautomotiveindustrytobeworld-competitiveandviable,including:

replacingtheAutomotiveCompetitivenessandInvestmentScheme’sproductionvolumesubsidywitha�newGlobalAutomotiveTransitionSchemedesignedtosupportresearch,development,designandexportwhileassistingintherestructureoftheAustraliansupplychaintobemorecompetitiveandreliable;

bringingforward,anddoublingto$1billionifsuccessful,theGreenCarInnovationFundand�recommendingguidelinesforthetotalsupplychain(nationallyandinternationally)andresearchinstitutionstodevelopgreencarinnovationtechnologies;

encouragingtheAustralianGovernmenttoincludetransportation(includingfuel)inanemissionstrading�scheme,furtherenhancinggreencartechnologies;

reducingthepassengermotorvehicletariffto5percentby2010,makingAustraliancartariffsthethird-�lowestamongstmajorautomotive-producingeconomiesintheworld(andwithanimport-weightedtariffrateofbetween3and4percent);

encouragingexpandedfreetradeagreements,particularlywiththeGulfStates,theAssociationof�SoutheastAsianNationsandSouthAfrica;

expandingoverseasmarketsthrougha‘TeamAustralia’approachusingeminentautomotiveambassadors;�

review leader’s summary—review of australia’s automotive industry

2| REVIEWoFAUSTRALIA’SAUToMoTIVEINDUSTRY |3

harmonising,andinsomecasesreducing,passengermotorvehicletaxes,includingstatestampdutyand�vehicleregistrations,whileencouraginggovernmentstosupportanenvironmentallysustainableAustralianindustry;and

establishinganewAutomotiveIndustryInnovationCounciltoprovideadviceandoversightinrelationto�thenewtransitionalarrangementsandincludingareferencegroupprovidingadviceonautomotiveskillsmatterstoManufacturingSkillsAustralia.

TheReview’srecommendationsarepredicatedonchangingthebehaviourofautomotivefirmsandtheindustrytomakethemmorecompetitiveandbetterabletomeetglobalchallenges,includingthemovetoalowercarbonenvironment,overthelongterm.

2| REVIEWoFAUSTRALIA’SAUToMoTIVEINDUSTRY |3

report structure and summary of recommendations

Structure of thiS reportThisAustralianAutomotiveReviewreportisstructuredasfollows:

Chapters1to6examinetheexistingAustralianandglobalautomotiveindustries,includingcurrent�industryassistancearrangementsandsupportforinnovation.ThesechapterscontainfindingsbytheReviewbutnorecommendations.

Chapters7to11addressproposedfuturearrangementstoassisttheAustralianautomotiveindustry.�Thesechaptersalsoaddresscurrentandproposedmarketaccess,environmentalissues,industryrestructuringandvehiclesafetyarrangements.Theycontainbothfindingsandrecommendations(exceptChapter11,whichcontainsrecommendationsonly).

TheReview’srecommendationsaresummarisedbelow.Tofacilitateanunderstandingofthemasa�comprehensivepackageoffutureautomotiveassistancemeasures,theyaregroupedunderthematicheadingsandnotnecessarilybychapter.

AppendixesAtoNsupplementinformationcontainedinthemainbodyofthereport.�

thematic Summary of recommendationS

AnewGlobalAutomotiveTransitionScheme(Chapter11)

Anew,retargetedtransitionalprogramtitledtheGlobalAutomotiveTransitionSchemeshouldbe�legislatedin2009andcommencein2010.TheGlobalAutomotiveTransitionSchemewouldcomplement,andbeadditionalto,theAustralianGovernment’sGreenCarInnovationFund.

TherearethreeoptionsforfundingtheGlobalAutomotiveTransitionSchemeandothermeasures�recommendedinthisreport.Theseare:

option1:� FundingfortheGlobalAutomotiveTransitionSchemeoverthefiveyearsto2015(inclusive)shouldbe$1.5billionincappedassistance.Anadditionaltrancheoffundingof$1billionincappedassistanceshouldbeprovidedfrom2016to2020,withthisfront-loadedandreducingtozero.

Thefundingalsocoverstheindustryrestructuringfund,TeamAustraliaAutomotive,the–AutomotiveAmbassadors,theAutomotiveIndustryInnovationCouncilandthechangedLPGVehicleSchemearrangements.Theseinitiativesshouldcommencein2009.

TheGreenCarInnovationFund,worth$500million,shouldbebroughtforwardto2009.–

4| REVIEWoFAUSTRALIA’SAUToMoTIVEINDUSTRY |5REPoRTSTRUCTUREANDSUMMARYoFRECoMMENDATIoNS

option2� :FundingfortheGlobalAutomotiveTransitionSchemeoverthefiveyearsto2015(inclusive)shouldbe$1.5billionincappedassistance.Anadditionaltrancheoffundingof$1billionincappedassistanceshouldbeprovidedfrom2016to2020,withthisfront-loadedandreducingtozero.

Thefundingalsocoverstheindustryrestructuringfund,TeamAustraliaAutomotive,theAutomotive–Ambassadors,theAutomotiveIndustryInnovationCouncilandthechangedLPGVehicleSchemearrangements.Theseinitiativesshouldcommencein2009.

FundingfortheGreenCarInnovationFundshouldbebroughtforwardto2009and,ifsuccessful,the–Fundshouldbedoubledfrom$500millionto$1billionandextendedbeyonditsinitialfiveyears.

option3� :FundingfortheGlobalAutomotiveTransitionSchemeoverthefiveyearsto2015(inclusive)shouldbe$1.5billionincappedassistance.Anadditionaltrancheoffundingof$1billionincappedassistanceshouldbeprovidedfrom2016to2020,withthisfront-loadedandreducingtozero.

Afurthertrancheoffundsshouldbemadeavailabletocovertheindustryrestructuringfund,Team–AustraliaAutomotive,theAutomotiveAmbassadors,theAutomotiveIndustryInnovationCouncilandthechangedLPGVehicleSchemearrangements.Theseinitiativesshouldcommencein2009.

FundingfortheGreenCarInnovationFundshouldbebroughtforwardto2009and,ifsuccessful,the–Fundshouldbedoubledfrom$500millionto$1billionandextendedbeyonditsinitialfiveyears.

the review recommends option 3.

otherrecommendedcomponentsoftheGlobalAutomotiveTransitionSchemeare:�

Fundingforboththemotorvehicleproducersandthesupplychainshouldbesplit55percent�(tovehicleproducers)and45percent(tothesupplychain)aftermoniesfortheadditionalprogramsareeitherdeductedfromthecappedpoolorallocatedseparatefunding.

Assistanceshouldbeintheformofgrantsandnotdutycredits.�

Creditsfortheproductionofvehiclesfordifferentmarketsshouldbetreatedthesame,bypartially�uncappingallproductioncredits.

Thedependencythresholdforthecomponentsuppliersshouldberaisedto$2milliontofacilitatethe�rationalisationoftheindustry.Automotiveserviceprovidersandautomotivemachinetoolproducersshouldcontinuetomeetthelowerthresholdof$500,000.

TheloadingsapplyingunderthepreviousAutomotiveCompetitivenessandInvestmentSchemefor�supplychaininvestmentshouldbeabolished.

Thelistofeligibleresearchanddevelopment(R&D)activitiesshouldbestreamlinedandexclude�paymentsforrecruitmentandmanagement.

TherateforclaimsforinvestmentineligibleR&Dshouldbeincreasedfrom45to50percent.�

Therateforclaimsforinvestmentinplantandequipmentshouldbereducedfrom25to15percent.�

Firmsthathavenotparticipatedinasupply-chaincapabilitydevelopmentprogramshouldparticipate�insuchaschemeinreturnforreceivinggovernmentassistance.FundingfortheprogramshouldbeprovidedbytheAustralianGovernmentwithcontributingpaymentsfromthefirmsthemselves.ThesuppliercapabilityprogramshouldnotbelimitedtoparticipationinAutomotiveSupplierExcellenceAustralia,butalsoincludeotherserviceproviderssuchasEnterpriseConnect,C21andthemotorvehicleproducers’suppliercapabilityprograms.

AnAutomotiveIndustryInnovationCouncilshouldbeestablished,withhighlevelrepresentationfrom�themotorvehicleproducers,componentsuppliers,unions,researchandacademicorganisations,andgovernment.

TheAutomotiveIndustryInnovationCouncilshouldprovideadviceandoversightinrelationtothenew�transitionalarrangementsapplyingtotheindustry.

4| REVIEWoFAUSTRALIA’SAUToMoTIVEINDUSTRY |5REPoRTSTRUCTUREANDSUMMARYoFRECoMMENDATIoNS

AdministrativeexpensesandsecretariatsupporttotheAutomotiveIndustryInnovationCouncilshould�befundedundertheGlobalAutomotiveTransitionScheme.

TheAutomotiveIndustryInnovationCouncilshouldincludeareferencegroupthatprovidesadviceon�automotiveskillsissuestoManufacturingSkillsAustralia(theIndustrySkillsCouncilhavingprimarycarriageformanufacturingindustryskillsdevelopment).

Australia’sfutureautomotivetariffs(Chapter11)

Thepassengermotorvehiclesandpartsthereoftariffsshouldbereducedfrom10to5percenton�1January2010.This,combinedwithassistanceundertheGlobalAutomotiveTransitionScheme,willhelpdeliverbenefitstotheeconomyaswellascontinuingtoprovidetransitionalsupportfortheindustry.

RestructuringtheAustralianautomotiveindustry(Chapter9)

TheAustralianGovernmentshouldcontributetoashort-termautomotiveindustryrestructurefundthat�aimstoassisttheAustralianautomotivesupplychainimproveeconomiesofscale,enhancemanagementcapabilities,internationaliseproductiontobuildcapacityanddemand,andenhancelong-termsustainability.

FundingfortheindustryrestructurefundshouldbepartofthenewGlobalAutomotive�TransitionScheme.

Paymentsundertheindustryrestructurefundshouldbedeterminedonacase-by-casebasisby�theresponsibleMinister,onadvicefromhisorherdepartment,takingintoaccount‘transmissionofbusiness’issuesincludingfacilitatingmergersandacquisitionsinthesector;addressing,whereappropriate,contingentliabilityorotherissuesthatmightactasbarrierstoeffectiveandsuccessfulsectoralconsolidation;consolidationofplantandequipment;andco-locationofproduction.Whereappropriate,fairandreasonableassistanceshouldalsobemadeavailabletoemployeesmaderedundantthroughautomotiverestructuring.

TheindustryrestructurefundshouldincludesupportfordevelopingtheAustralianautomotivesupply�chain’smanagementandoperationalcapabilitiesandprocesses(similartoAutomotiveSupplierExcellenceAustralia,C21andotherexistinginitiatives).

Governmentfundingfortheindustryrestructurefundshouldbeofalimitedamountandduration(for�example,$60to$80millionovertwoyears)tocovertheimmediaterestructuringandconsolidationneedsoftheautomotiveindustry.

Theautomotiveindustryshouldcontributefinanciallytotheactivitiessupportedbytheindustry�restructurefund.

Theautomotiveindustry,unions,employeesandgovernmentsshouldengageinanongoingdialogueso�thattherestructuringandconsolidationprocessiseffectiveinhelpingwithanorderlytransitiontoamorecompetitiveandsustainablefuturefortheindustry.

Amemorandumofunderstandingshouldbenegotiatedbymotorvehicleproducers,component�suppliersandunions,andbefacilitatedbygovernmentswhereappropriate.Thememorandumofunderstandingshould:

acknowledgethatrestructuringandconsolidationareanecessarypartofassuringavitalAustralian�automotiveindustryintothefuture;and

assistwithassuringcontinuityofsupplyinanindustrycharacterisedbyjust-in-timedeliveryandhigh�levelsofinternationalcompetition.

Theleadershipdialoguebetweenthecomponentsectorandunionsshouldcontinue.�

Whetherthistranslatesintoaframeworkagreementisamatterfortheparticipants.However,there�arebenefitstobegainedfromasharedunderstandingofthechallengesthatlieaheadandtheneedforimprovementsincompetitivenessandproductivity.

Theissueofemployeeentitlementsisalsoamatterwherealeadershipdialoguecanassistthe�participantstomoreeffectivelymanagetherestructuringprocess.

6| REVIEWoFAUSTRALIA’SAUToMoTIVEINDUSTRY |7REPoRTSTRUCTUREANDSUMMARYoFRECoMMENDATIoNS

Toassistwithresolvingskillsissuescommonacrosstheautomotiveandothermanufacturingindustries,�theAustralianGovernmentshouldestablishareferencegrouptoprovideadviceonautomotiveskillsissuestoManufacturingSkillsAustralia.

ThereferencegroupshouldcomeundertheAutomotiveIndustryInnovationCouncil.�

TheGreenCarInnovationFund(Chapter8)

TheGreenCarInnovationFundshouldassisttheAustralianautomotiveindustrywithdevelopingand�commercialisingtechnologiesaimedatimprovingvehiclefuelefficiencyandemissions.ThecombinationoftheFundwithanemissionstradingschemewilldrivepositiveinnovationandenvironmentaloutcomesfortheeconomyandtheindustry.

Inpreparationforanemissionstradingscheme,thestartdateoftheFundshouldbebroughtforward�to2009.

IftheFundprovessuccessfulinitsfirsttwoyearsofoperation,itsfundingshouldbedoubledfrom$500�millionto$1billionandtheschemeextendedbeyonditsinitialfiveyears.

BenefitsfromtheFundshouldbepaidascashgrants,followingacompetitiveselectionprocessbased�onbroadcriteriathatassesstheinnovation,technological,commercialandenvironmentalmeritsofapplications.

Sinceautomotiveindustryinvestmentisoften‘lumpy’thereshouldbescopeundertheFundtovarythe�amountofFundpaymentsbetweenyears.

Thereshouldbescopetovarytheone-to-threedollarfundingratiowithinarange(forexample,one-to-two�dollarstoone-to-fourdollars)totakeaccountofvaryingriskprofiles.

Thereshouldbeamaximumlimitsetontheamountofsupportavailabletoanyonefundingrecipient.This�limitshouldbesetatahighlevelinordernottorestrictsignificantprojects.

Mandatoryanddiscretionarycriteriashouldbedesignedtoassessproposalsagainstamixofquantitative�andqualitativeaspects.Commercialapplicationoftechnologyshouldbeamandatorycriterion.

Allorganisationsandindividualsshouldbeeligible,includingparticipantsintheautomotivesupplychain,�researchorganisations,andinternationalfirmswhereeligibleactivitiesareperformedinAustralia.

Fundeligibilityshouldnotberestrictedtoanyparticularrangeofautomotivetechnologies.�

Emissionstradingandtheenvironment(Chapter8)

Roadtransport(includingfuel)shouldbeincludedintheemissionstradingschemeasitallowsthe�industrytodeterminethelowest-costformofemissionsabatement.Inthisrespect,futureconsiderationofmandatoryemissionstargetsfornewvehiclesshouldhaveregardtodevelopmentoftheemissionstradingscheme.

Iftheemissionstradingschemeexcludesroadtransport,thenamandatorygreenhousegasemissions�targetshouldbeintroducedasa‘secondbest’policy.

Thegrantforliquefiedpetroleumgas(LPG)unitsfittedatthetimeofmanufactureofavehicleunderthe�LPGVehicleSchemeshouldberaisedfrom$1,000to$2,000,provideditfacilitatestheuptakeofnewtechnologiesthatprovidesignificantlybettergreenhousegasemissionsoutcomesthancurrentlyfittedLPGtechnologies.

Improvingaccesstoglobalmarkets(Chapter7)

ThesuccessfulconclusionoftheWorldTradeorganizationDohaDevelopmentAgendashouldcontinueto�beaprincipalfocusofAustralia’stradenegotiations.

TheReviewofAustralia’sExportPoliciesandProgramsshouldgiveconsiderationtowaysofaddressing�beyond-the-borderissuessuchasnon-tariffbarriersaspartoffuturefreetradeagreementnegotiations.

6| REVIEWoFAUSTRALIA’SAUToMoTIVEINDUSTRY |7REPoRTSTRUCTUREANDSUMMARYoFRECoMMENDATIoNS

Australiashouldcontinuetoenterintofreetradeagreementnegotiations.However,fromanautomotive�perspective,theseshouldbefocusedoncountrieswithwhichAustraliacandevelopitscompetitiveadvantageoroncountrieswhereveryhighbarrierstotradeexist.EconomiesuponwhichAustraliashouldfocusitsfreetradeagreementnegotiationsincludetheGulfCooperationCouncil,theAssociationofSoutheastAsianNationsandSouthAfrica.

Traderules,suchasrulesoforigin,should,whereverpracticable,beharmonisedacrossfreetrade�agreementstoreducecompliancecoststoindustry.

Awell-knownandrespectedindustryfigureorfiguresshouldundertakeanambassadorialrolefor�theindustry.

Thisshouldbecomplementedbymedium-termfundingfortheextensionofTeamAustraliaAutomotive�tonewandemergingmarkets,aspartoftheGlobalAutomotiveTransitionScheme.

DeliveryoftheTeamAustraliaAutomotiveinitiativeshouldbethroughacontestablegrantprocess,and�presentaunitedAustralianautomotivecapability(encompassingstategovernmentsupplychainandexportpromotionprograms)tointernationalmarkets.

Vehiclesafety(Chapter10)

VehiclesafetystandardsshouldadheretotheAustralianDesignRulesandbeuniformacrossallstates�andterritories.

AnychangestovehiclesafetystandardsshouldalsobeconsistentwithAustralia’sinternationalobligations�andnotimpactonmutualrecognitionmatters(andhenceriskmarketaccessrestrictionsforAustralian-madevehicles).

othermatters

AustraliangovernmentsshouldcontinuetoincludeAustralian-madevehiclesasamajorpartoftheir�purchasingpolicies,andshouldreinforcethisthroughathresholdagreementattheCouncilofAustralianGovernments.Thisshouldbesubjecttothelocalindustrycontinuingtoimprovegreenhousegasemissionsoutcomesthroughtheuptakeofvariousemissionsabatementtechnologies.(Chapter8)

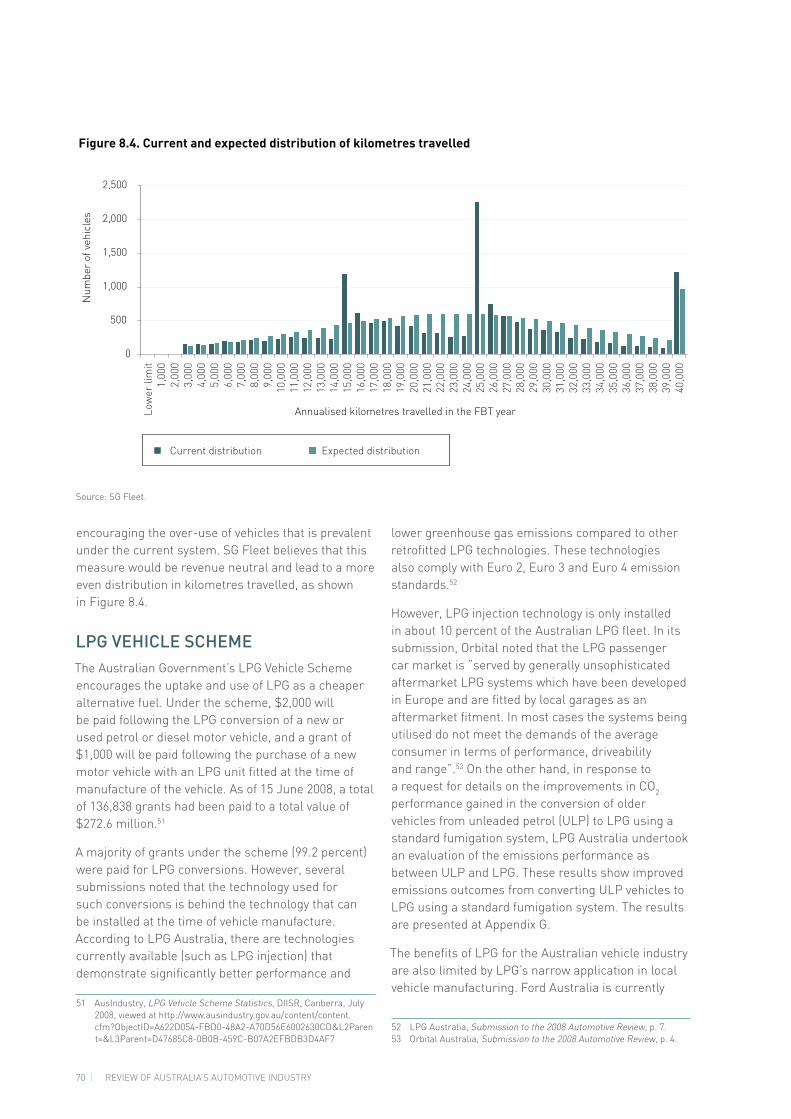

TheHenryReviewoftaxationshouldconsidertheadoptionofanewfringebenefitstaxstatutoryratetable�thatismoreevenlyspreadacrosstherangeofkilometrestravelled.Thenewratetablewouldencouragedriverstousetheirvehiclesonlyasnecessary.(Chapter8)

AdialoguebetweentheAustralianandaffectedstateandterritorygovernmentsshouldoccurtoensure�thatinvestmentincentivesarenotoverlygenerousandthatthebenefitsexceedthecostsofprovidingsuchassistance.(Chapter11)

Statesandterritoriesshouldconsidertheharmonisationandreductionofstampduties,vehicle�registrationandcompulsorythird-partyinsurancetofacilitatethepurchaseofnew(ornewersecond-hand)vehiclestohelptoreducetheaverageageoftheAustralianvehiclefleet.ThiscouldbethroughforumssuchastheCouncilofAustralianGovernmentsortheCouncilfortheAustralianFederation.(Chapter11)

|9

IntroductIonTheAustralianautomotiveindustryhasundergoneextensivereform,especiallysincetheButtonPlanin1985,whentheindustrywasprotectedbyquotasandatariffof57.5percent.Theremovalofquotasandtheloweringofprotectionledtosomerationalisationoftheindustryandmadeimportsmoreaccessibletoconsumers.Thesereformshavealsomadetheindustrymoreinternationallycompetitiveandexportfocused.Forexample,exportsofautomotiveproductswerearound$4.7billionin2007,makingautomotiveoneofAustralia’stop10exportearners(andthelargestmanufacturingexportearner).Italsoplacestheautomotivesectoraheadofmoretraditionalexportssuchaswine,wheatandwool.

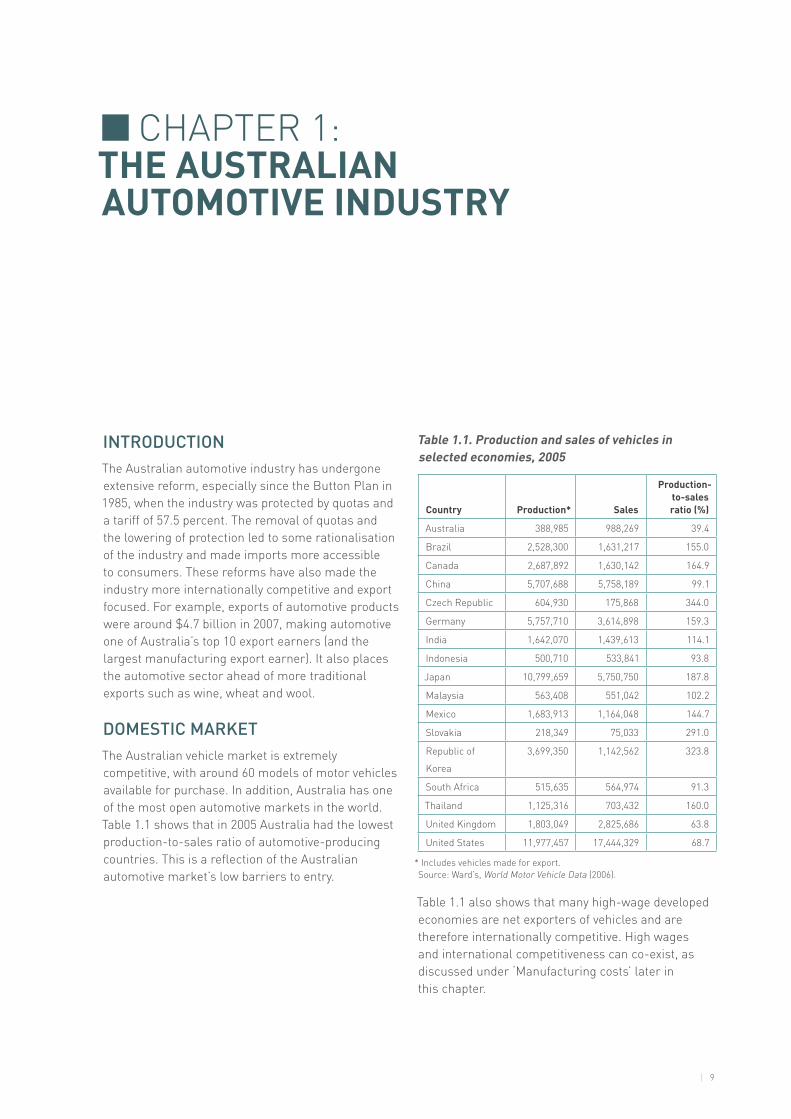

domestIc marketTheAustralianvehiclemarketisextremelycompetitive,witharound60modelsofmotorvehiclesavailableforpurchase.Inaddition,Australiahasoneofthemostopenautomotivemarketsintheworld.Table1.1showsthatin2005Australiahadthelowestproduction-to-salesratioofautomotive-producingcountries.ThisisareflectionoftheAustralianautomotivemarket’slowbarrierstoentry.

Table 1.1. Production and sales of vehicles in selected economies, 2005

Country Production* Sales

Production-to-sales ratio (%)

Australia 388,985 988,269 39.4

Brazil 2,528,300 1,631,217 155.0

Canada 2,687,892 1,630,142 164.9

China 5,707,688 5,758,189 99.1

CzechRepublic 604,930 175,868 344.0

Germany 5,757,710 3,614,898 159.3

India 1,642,070 1,439,613 114.1

Indonesia 500,710 533,841 93.8

Japan 10,799,659 5,750,750 187.8

Malaysia 563,408 551,042 102.2

Mexico 1,683,913 1,164,048 144.7

Slovakia 218,349 75,033 291.0

Republicof

Korea

3,699,350 1,142,562 323.8

SouthAfrica 515,635 564,974 91.3

Thailand 1,125,316 703,432 160.0

UnitedKingdom 1,803,049 2,825,686 63.8

UnitedStates 11,977,457 17,444,329 68.7

*Includesvehiclesmadeforexport.Source:Ward’s,WorldMotorVehicleData(2006).

Table1.1alsoshowsthatmanyhigh-wagedevelopedeconomiesarenetexportersofvehiclesandarethereforeinternationallycompetitive.Highwagesandinternationalcompetitivenesscanco-exist,asdiscussedunder‘Manufacturingcosts’laterinthischapter.

CHAPTeR1:The auSTralian auTomoTive induSTry

10| ReVIeWoFAUSTRALIA’SAUToMoTIVeINDUSTRY |11THeAUSTRALIANAUToMoTIVeINDUSTRY

In2007,theAustralianmarketrecordedsalesofoveronemillionvehiclesforthefirsttime.Thiswasa45percentincreaseinvehiclesalescomparedto1997anda27percentincreasecomparedto2002,1andcoincidedwiththeincreasingaffordabilityofvehicles.Sincethemid-1990s,realearningshaveincreasedatasignificantlyhigherratethanvehicleprices.2Thishasmeantthatsince1995theaffordabilityindexformotorvehicles(averageweeklyearningsdividedbytheconsumerpriceindexformotorvehicles)hasincreasedby84.8points.3Anothermeasureofincreasingaffordabilityisthat‘family6cars’(HoldenandFordsix-cylinderbasemodels)nowtake31.9averageweeks’earningstopayoff,comparedto41.6weeksin1995.4

Althoughvehicleaffordabilityhasrisen,theoperatingcostsofpassengervehicleshaveincreaseddramaticallyinthepastfewyears.Since2002therehasbeena400percentincreaseinthepriceofoil,fromUS$25perbarreltoUS$100perbarrel.5Thishascontributedtoa33percentincreaseinthepriceofpetrolinAustraliasince2004.6In2003–04,fuelaccountedfor24percentofanAustralianhousehold’stransportcosts,behindmotorvehiclepurchases(36percent),butaheadofregistration/insurance(17percent),othercharges(13percent),spareparts(5percent),publictransport(3percent)andfaresandfreight(2percent).7Itwouldbeexpectedthattheproportionofahousehold’stransportcostsaccountedforbyfuelwouldhaveincreased,asthepriceofpetrolhasincreasedatafargreaterratethanhouseholdincome.However,theriseinthepriceoffuelhasbeencushionedbytheappreciationintheAustraliandollar.

Shiftinconsumerpreferences

Therehasbeenasignificantchangeinthetypeofvehiclesdemandedbyconsumers.8Traditionally,theAustralianvehiclemarkethasbeendominatedbylargepassengercarsandvariants(forexample,HoldenCommodoreandFordFalcon)andlargemediumvehicles(suchastheToyotaAurionandCamry).Therehasbeenarecenttrendtowardssmaller,lowerfuelconsumptionvehicles(suchastheToyotaYarisandCorolla),luxurycars(suchasMercedesBenzandBMW)andsportsutilityvehicles

1 FederalChamberofAutomotiveIndustries,VFacts,FCAI,2007.2 AustralianAutomotiveIntelligence,AustralianAutomotive

IntelligenceYearbook2008,7thedn,RichardJohns,2008,p.55.3 ibid.,p.56.4 ibid.5 Fromthemid-1980sthroughto2002,theinflation-adjustedpriceof

oilwasgenerallyunderUS$25abarrel.6 FCAI,Submissiontothe2008AutomotiveReview,p.21.7 AustralianBureauofStatistics,HouseholdexpenditureSurvey,

Australia,DetailedexpenditureItems,2003–04,cat.no.6535.0ABS,Canberra,2006.

8 FederalChamberofAutomotiveIndustries,op.cit.

(SUVs)(whichrangeinsizefromtheSuzukiVitaraandToyotaRAV4throughtotheHummer).TherehasbeenasignificantsalessubstitutionfromlargeAustralian-madevehiclestoSUVs,eventhoughSUVsaregenerallylessfuelefficient.Thesetrendshaveimpactedonlocalvehicleproducers—themarketshareofAustralianmotorvehicleproducers(MVPs)fellfrom30percentin2002to19percentin2007.Thisfallcontinuedthroughthefirstseveralmonthsof2008,andwas17percentinMay2008.

Inaddition,whiletheAustralianautomotiveindustrycontinuestodominatesalesinthelargeandmediumcarmarket,thedomesticmanufacturers’shareofthismarkethasfallen—from95percentin2002to88percentin2007.ThesetrendsareshowninFigures1.1and1.2.

SalesofAustralian-madevehiclesarelargelydependentonprivateandgovernmentfleetsales.Lessthanone-quarterofAustralian-madevehiclesalesin2007weretoprivatebuyers.Thereisalsoagrowinglevelofsalestothebusinesssector.In2007,salestothissectoramountedto113,807,ornearly56percentoftotalAustralian-madevehiclepurchases(Figure1.3).Inthesameyear,governmentsacrossvarioustierspurchased37,073(or19percent)ofAustralian-madevehicles(Figure1.4).

Source:FederalChamberofAutomotiveIndustries,VFacts.

10| ReVIeWoFAUSTRALIA’SAUToMoTIVeINDUSTRY |11THeAUSTRALIANAUToMoTIVeINDUSTRY

Source:FederalChamberofAutomotiveIndustries,VFacts.

Source:FederalChamberofAutomotiveIndustries,VFacts.

Source:FederalChamberofAutomotiveIndustries,VFacts.

domestIc productIonTheAustralianautomotiveindustryencompassesawiderangeofactivitiesincludingvehicleproduction,componentproduction,toolinganddesignandengineering.ItisanimportantpartoftheAustralianeconomy,employingover64,000people9andaccountingforalmost6percentofmanufacturingemployment.Valueaddedtothesectortotalsmorethan$5.6billion,10representing5.6percentofthemanufacturingsector’sindustryvalueaddedand0.6percentofnationalgrossdomesticproduct(GDP).InitssubmissiontotheReview,FordAustralianotedthatAustraliaisoneofonly15countriesthatcantakeacarfromconceptallthewaytofullproduction.11

TherearethreeMVPsinAustralia—GMHolden,FordMotorCompanyofAustraliaandToyotaMotorCorporationAustralia.Allthreecompaniesarefullyownedsubsidiariesofmajoroverseasproducers.MitsubishiMotorsAustraliaceaseditsAustralianproductioninMarch2008,althoughitremainsinthemarketasanimporterofafullrangeofvehicles.

MotorvehicleproductiontakesplaceinVictoriaandSouthAustralia.FordhasanassemblyplantinBroadmeadows(Melbourne)andacomponentandengineplantinGeelong.GMHoldenmanufacturesvehiclesinelizabeth(Adelaide),andproducesV6enginesatitsFishermansBend(Melbourne)facility.TheV6engineissuppliedtoboththedomestic

9 AustralianBureauofStatistics,LabourForce,Australia,Detailed,Quarterly,cat.no.6291.0.55.003,ABS,Canberra,2008.

10 AustralianBureauofStatistics, ManufacturingIndustry,Australia,2005–06,cat.no.8221.0,ABS,Canberra,2008.

11 FordAustralia,Submissiontothe2008AutomotiveReview,2008,p.3.

12| ReVIeWoFAUSTRALIA’SAUToMoTIVeINDUSTRY |13THeAUSTRALIANAUToMoTIVeINDUSTRY

market,forinclusioninGMHolden’srangeoflocallymanufacturedvehicles,andtoanumberofexportmarkets.Toyotamanufacturesvehiclesandfour-cylinderenginesinAltona(Melbourne).

AllthreeMVPshaveR&DcapabilitywithinAustralia.GMHoldenhasaregionaldesignandengineeringcentreinAustraliathatemploysaround1,000staffandisinvolvedinGM’sglobalproductdevelopment.Toyota’sregionaltechnicalcentreemploysaround100staffandalsocontributestoToyota’sglobalplatforms.FordAustraliahasestablishedadesignandengineering‘Centreofexcellence’whichisresponsibleforseveralprojects,includingaglobalpick-uptruckplatform.FordAustralia’sproductdevelopmentprogramemploysover1,300staff.

Inaddition,thereareover200firms—predominantlybasedinMelbourneandAdelaide—producingautomotivecomponentsforthevehiclemanufacturers.TheAustralianautomotiveindustryalsohasaccesstospecialisedtoolingservicesfromaround500firms.

In2007,productionofAustralianvehiclesnumbered327,984,adropof5percentfrom2000.12Inglobalterms,thislevelofproductionisrelativelysmall,accountingforlessthan0.5percentofworldproduction.Competingagainstcountrieswithmajorproduction-scaleadvantagespresentsadifficultchallengefortheindustry.ontheotherhand,Australia’srelativelysmallscaleofproductionmeansthattheindustryisgenerallymoreflexibleinrespectofchangesindemand,moreefficientinservicingnichemarkets,andmorecost-effectiveinsmallerproductionruns.

ThequalityofAustralian-producedvehiclescanbemeasuredbythenumberoffaultspervehicle.AustralianvehiclessuchastheHoldenCommodore(1.2faultspervehicle)andtheFordFalcon(1.0faultpervehicle)wereslightlyabovetheaverageforlargecars(0.8faultpervehicle)in2006.Bothcarsrecordedareducingincidenceoffaultsoverthelastfewyears.TheToyotaAurionhadanaverageofonly0.7faultpervehicle,whichisbelowtheindustryaverage.13

AustralianMVPsareheavilyreliantonAustralianinputs.In2006,MVPssourced75percentoftheircomponents—worth$4.6billion—fromAustraliancomponentproducers.14Similarly,Australiancomponentproducersareheavilyreliantondomesticsales—81percentoftotalsalesaremadedomestically.15

12 FCAI,2008,http://www.fcai.com.au/volumes13 DepartmentofInnovation,Industry,ScienceandResearch,Key

AutomotiveStatistics2007,DIISR,Canberra,2008,p.22.14 ibid.15 ibid.

TrendsthathavedevelopedinthelastfewyearshavechallengedthelinkbetweendomesticMVPsandcomponentproducers.First,duetotheriseofglobalplatformsMVPsaremorecommonlysourcingcomponentsfromoverseas.Theseglobalsupplychainsarebecomingincreasinglyintegrated,andsince1994Australiancomponentimportshaveincreasedby74percent.16Second,MVPsaregenerallyonlyawardingshort-termcomponentscontracts,therebyunderminingthefinancialsecurityofmanycomponentproducers.17Asaresult,manycomponentproducersaremovingtheiroperationsoverseasorreducingtheirrelianceondomesticsales.Forexample,in1994,90percentofcomponentproducers’saleswerederivedfromthedomesticmarket.Thishadfallento81percentofsalesby2007.

Truckandbussector

TherearecurrentlythreeassemblersoftrucksinAustralia:Iveco(Wacol,Queensland),Kenworth(Bayswater,Victoria)andVolvoCommercialVehicles(whichassemblesbothMackandVolvotrucksinDandenong,Victoria).Thesethreeplantsproduceover50percentofheavy-dutytruckchassissoldinAustralia.18Thereisalsoasecondarymanufacturingprocesswhichinvolvesfittingequipmenttotruckchassisasrequiredbythefinaloperator.Therearemanymanufacturers,rangingfromsmallfirmstothetruckchassisassemblers,involvedinthissecondarymanufacturingprocess.ThesemanufacturersandassemblersareheavilyreliantontheskillsandexpertiseoftheAustralianautomotivecomponentsector.Withoutthisskillbase,thetruckmanufacturingindustrywouldstruggletomanufacturelocally,whichcouldbedetrimentaltootherimportantsectorssuchastransportandresources.

Itisestimatedthatthetruckmanufacturingindustryemploysabout2,350peopleinchassismanufacturingandabout7,600in‘secondary’manufacturing.19

Likethecarindustry,theAustralianheavycommercialvehicleindustrywasrationalisedinthe1980sand1990sasgovernmentprotectionwasreduced.Thegeneraltariffof5percentnowappliestoallheavycommercialvehicleimports.

16 DepartmentofInnovation,Industry,ScienceandResearch,op.cit.17 HouseofRepresentativesStandingCommitteeonemployment,

WorkplaceRelationsandWorkforceParticipation,ShiftingGears:employmentintheAutomotiveComponentsManufacturingIndustry,HRSCeWR,Canberra,2006,p.13.

18 TruckIndustryCouncil,Submissiontothe2008AutomotiveReview,p.1.

19 ibid.,p.2.

12| ReVIeWoFAUSTRALIA’SAUToMoTIVeINDUSTRY |13THeAUSTRALIANAUToMoTIVeINDUSTRY

Aftermarketmanufacturingsector

Thissectormanufacturesarangeofautomotivepartsandaccessoriesfortheindependentautomotiveaftermarket(partsandaccessoriesdistributedthroughnetworksexternaltoMVPnetworks)andtheoriginalequipmentautomotiveaftermarket(partsandaccessoriesdistributedthroughMVPsandtheirdealers’networks).20

Theautomotiveaftermarketmanufacturingsectorisasignificantcontributortotheautomotivesector,employingaround30,000people.21Thesectorisalsoasignificantexporter—around170manufacturersarenowinvolvedindirectexport,technologylicensingandinternationaljointventuresworthanestimated$600millionperannum.22

Retail,serviceandrepairsectors

Althoughnotdirectlyinvolvedinmanufacturing,theautomotiveretailsectorplaysthesignificantroleofselling,distributingandservicingbothimportedandAustralian-manufacturedmotorvehicles.Understandingtheimportanceofthisrole,MVPsalsoundertakesignificantcapitalinvestmentsintheirdealernetworks.AtDecember2006,therewereover1,299dealersinAustraliawithover52,000employees.23

TheautomotiverepairandservicesectorisalsoamajorpartoftheAustralianautomotiveindustry.Morethan25,596businesseswereregisteredattheendofthe2007–08financialyear,24andasatFebruary2008thesectoremployedatotalof135,335people.25

Advancedmanufacturingindustry

Theadvancedmanufacturingindustryprovidesdesign,tooling,manufacturingtechnologyandequipmenttotheautomotivesectoraswellastothebroadermanufacturingsector.Assuch,itisseentoplayan‘enablingrole’withintheAustralianeconomy.In2004,theindustrywasworth$2.84billionannuallyanddirectlyemployed12,000people.26

20 AustralianAutomotiveAftermarketAssociation,Submissiontothe2008AutomotiveReview,p.6.Notethat45percentofAAAAmembersproducefortheaftermarketandtheoriginalequipmentmarketwhiletheremaining55percentofmemberssupplyonlytotheaftermarket.

21 BasedontotalAAAAmembership.22 AAAA,loc.cit.,p.5.23 MotorTradesAssociationofAustralia,MotorData©,MTAA,Canberra,

2008.24 AustralianBureauofStatistics,CountsofAustralianBusinesses,

includingentriesandexits,cat.no.8165.0,ABS,Canberra,2008.Thisfigureincorporatesthe‘AutomotiveRepairandServicesn.e.c.’industrysubdivision.

25 AustralianBureauofStatistics,LabourForce,Australia,Detailed,Quarterly,catno.6291.0,ABS,Canberra,2008.

26 AdvancedManufacturingAustralia,Submissiontothe2008

profItabIlIty27

In2007,tradinglossesinvehiclemanufacturingfortheMVPstotalled$722million,oran8.6percentlossonsales.ThiswassomewhatoffsetbyMVPs’salesofcomponentsandotherbusiness,withnetlossesonallMVPactivitiestotalling$449million.Thissituationcanbecomparedtothatofadecadeearlier,whennettradingprofitsfortheMVPstotalled$518million,including$344millioninprofitsonvehiclemanufacturing.JustifyingdomesticproductionwithsuchlargetradinglossespresentsamajorchallengetotheAustralianMVPs.However,the2007figuresalsoincludethelossesofMitsubishi,whichhassinceexitedthemarket,aswellascostsassociatedwiththedevelopmentofnewmodelsbytheremainingthreeproducers.Itshouldbenotedthatprofitsarealsofallinginanumberofotherautomotive-producingeconomies,includingsomeofthemajorones.TheglobaldownwardtrendinprofitsisdiscussedinmoredetailinChapter3.

Thereisalsoevidencethatcomponentproducersarehavingtheirprofitmarginsreducedasthecompetitivenessofimportsincreases.Thisisdue,inpart,tothestrongAustraliandollarandtothestandardglobalplatformsthatallowMVPstoincreaseimportsubstitutionofcomponents.Cost-downpressuresfromtheMVPs,aswellasrisinginputcosts,havealsoservedtoreducemargins.

manufacturIng costsThecostofmanufacturinginAustraliaisrisingandisamajorconcernformanyautomotivemanufacturingfirms.Productioninputssuchaslabour,materials,energy,waterandlogisticsfeedintothecoststructuresofallmanufacturers.ComponentproducerDensoconductedastudyofthe‘on-costs’ofoperatinginAustraliacomparedtoitsequivalentoperationsinThailand.ThestudyfoundthatoperatinginAustralia(asopposedtoThailand)amountedtoacostpenaltyofaround48percent.Afterfactoringinanelectricitypricerise,thepenaltyincreasedto69percent.28Boschnotesthatlogisticsisamajorincreasingcostforitsbusiness,especiallysincelogisticsamountstoabout3to4percentoftotalcosts.29

AutomotiveReview,p.5.27 DepartmentofInnovation,Industry,ScienceandResearch,op.cit.28 Denso,Submissiontothe2008AutomotiveReview,pp.7–8.29 RobertBosch,Submissiontothe2008AutomotiveReview,p.11.

14| ReVIeWoFAUSTRALIA’SAUToMoTIVeINDUSTRY |15THeAUSTRALIANAUToMoTIVeINDUSTRY

Intermsofinternationalcomparativelabourcosts(viewedinisolationfromtechnologicalcapacityandtotalfactorproductivity),theAustralianautomotiveindustry’slabourcostsarebelowthoseindevelopedeconomiesbutabovethoseindevelopingeconomiesthathavemajorautomotiveinvestments.AsshowninTable1.2,wagecostsinAustraliaaremuchlessthaninGermanyandtheUnitedStates,butsimilartolevelsinJapan.Labourcostsinautomotive-producingcountriessuchastheRepublicofKorea,TaiwanandMexicoweresignificantlylowerthaninAustralia.

Table 1.2. hourly compensation costs for motor vehicle and parts production workers (in uS dollars)

1999 2002 2005

Germany* $34.28 $32.21 $44.95

UnitedStates $26.98 $32.49 $35.57

UnitedKingdom $20.35 $21.23 $29.27

Japan* $26.06 $24.23 $27.12

Australia $16.59 $15.96 $25.96

RepublicofKorea* $9.57 $12.33 $16.61

Taiwan $7.71 $7.05 $7.75

Mexico* $2.46 $3.46 $3.52

*Denotesnetexporters.Source:USDepartmentofLabor,BureauofLaborStatistics(12May2008).

ofcourse,withregardtolabourcostsatleast,thecomparativedatapresentedinTable1.2donottakeintoaccountAustralia’stechnologicalandskilladvantages,aswellasadvanceddesignandengineeringcapabilities,vis-à-visitslow-wagecompetitors.Inaddition,AustraliaimportsvehiclesandcomponentsfromhigherwagecountriessuchasGermany,theUnitedStatesandJapan.

Still,countriessuchasChinaandIndiaareseekingto‘moveupthevaluechain’byupgradingtheirtechnologicalandresearchinfrastructure.TheimplicationisthattheAustralianindustrymustcontinuetoimproveitsinternationalbenchmarkperformanceinregardtomanufacturingcosts.Inaddition,initssubmissiontotheReview,GMHoldennotedthat,“InthekeyareaofsupportforR&D,Australiaislaggingbehindotherdevelopedcountries”.30Giventhatinnovationandproductivitygrowtharekeystoacompetitiveandsustainableindustryinthefuture,Australia-basedMVPsandthesupplychainshouldstrivetoimprovetheirperformanceagainstbothemergingandestablishedcompetitors.LabourproductivitytrendsarediscussedinChapter9.

30 GMHolden,Submissiontothe2008AutomotiveReview,p.36.

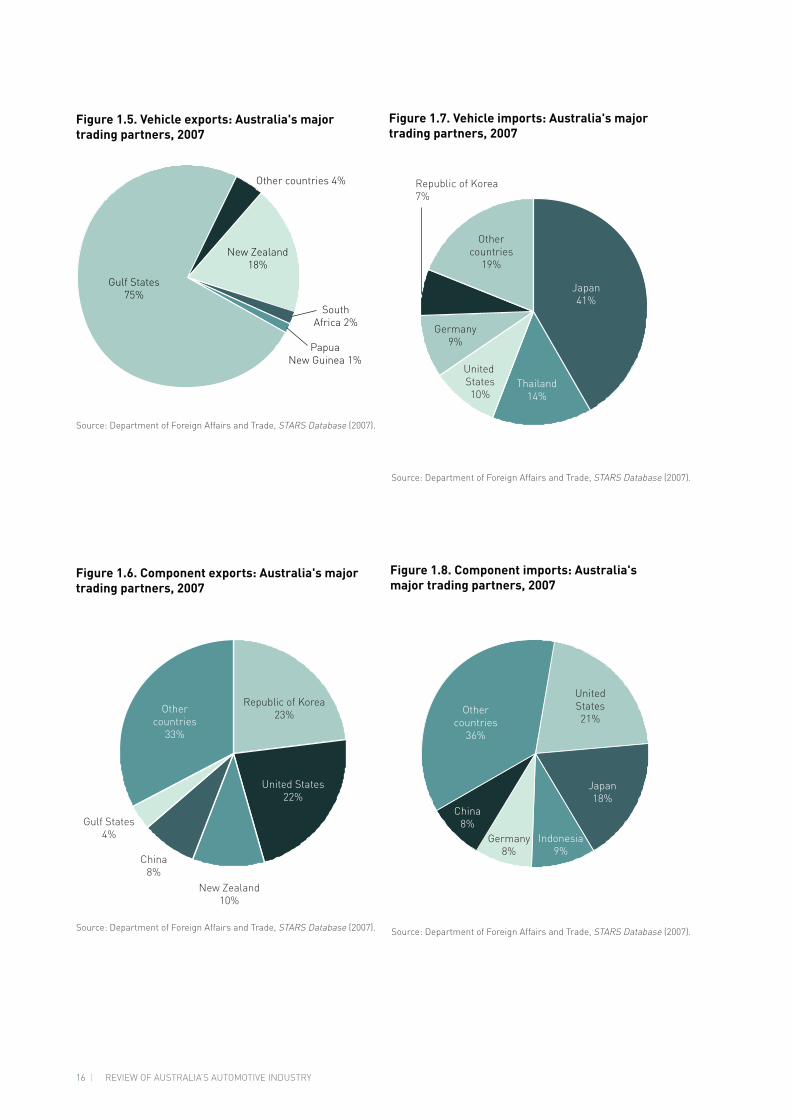

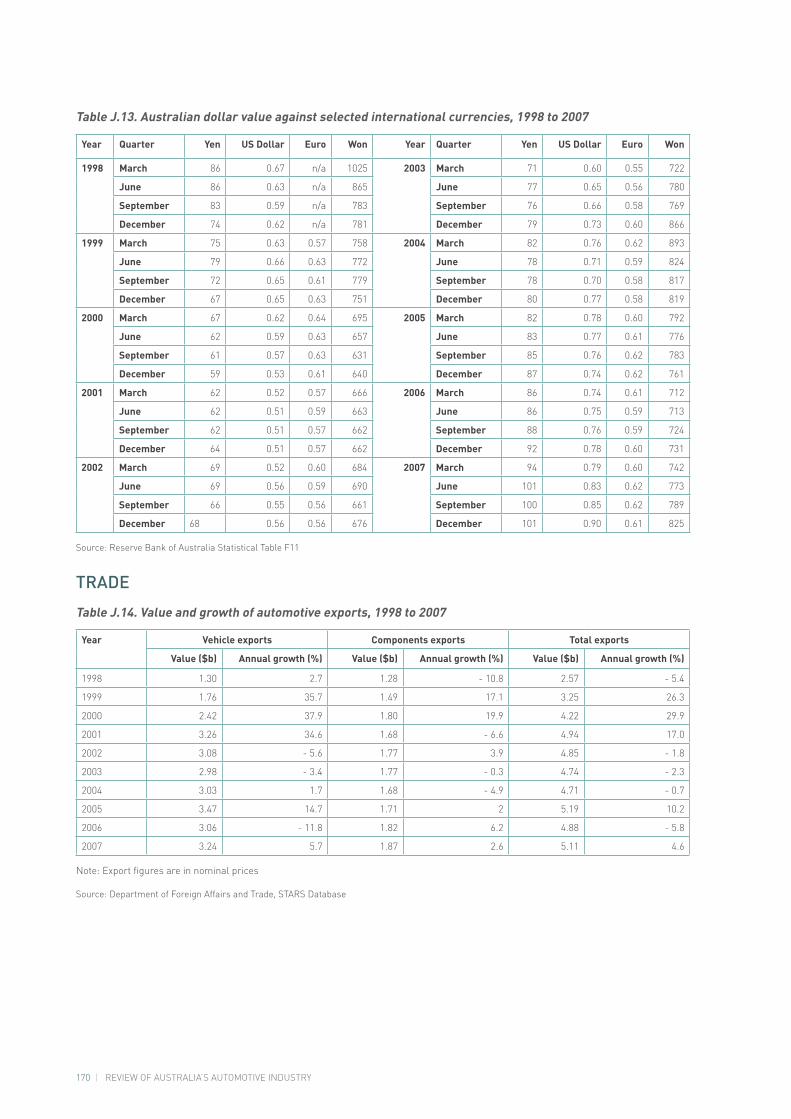

tradeTheexportofautomotiveproductsisofgrowingsignificancetotheAustralianeconomy—amountingto$4.7billionin2007.31ThismakestheautomotivesectoroneofAustralia’stop10exportearnersandthelargestmanufacturingexportearner(with10.7percentoftotalmanufacturingexportsin2007).Italsoplacestheautomotivesectoraheadofmoretraditionalexportssuchaswine,wheatandwool.ThegrowthinAustralia’sautomotiveexportshasoccurreddespitethelargereductionsindomesticautomotivetariffssincethe1980s.

Theimportanceofimprovingaccesstomarketsandtheimpactofinvestmentandlocationdecisionsonexportperformancearediscussedelsewhereinthisreport.Asnoted,thesefactorscanbeinfluencedbyheadofficedecisionsoverexportandimportstrategies,co-locationtoachieveproximitytomajorassemblersandtradebarriers.

Inaddition,currenttradedataarebasedongrossvaluesanddonotreflecttheAustralian-onlyvalueofcomponentsandpartsinautomotivegoods.Assuch,thetradedataincludeexportsofimportedcomponentsandpartsthathavegoneintothemanufactureofautomotivegoods.

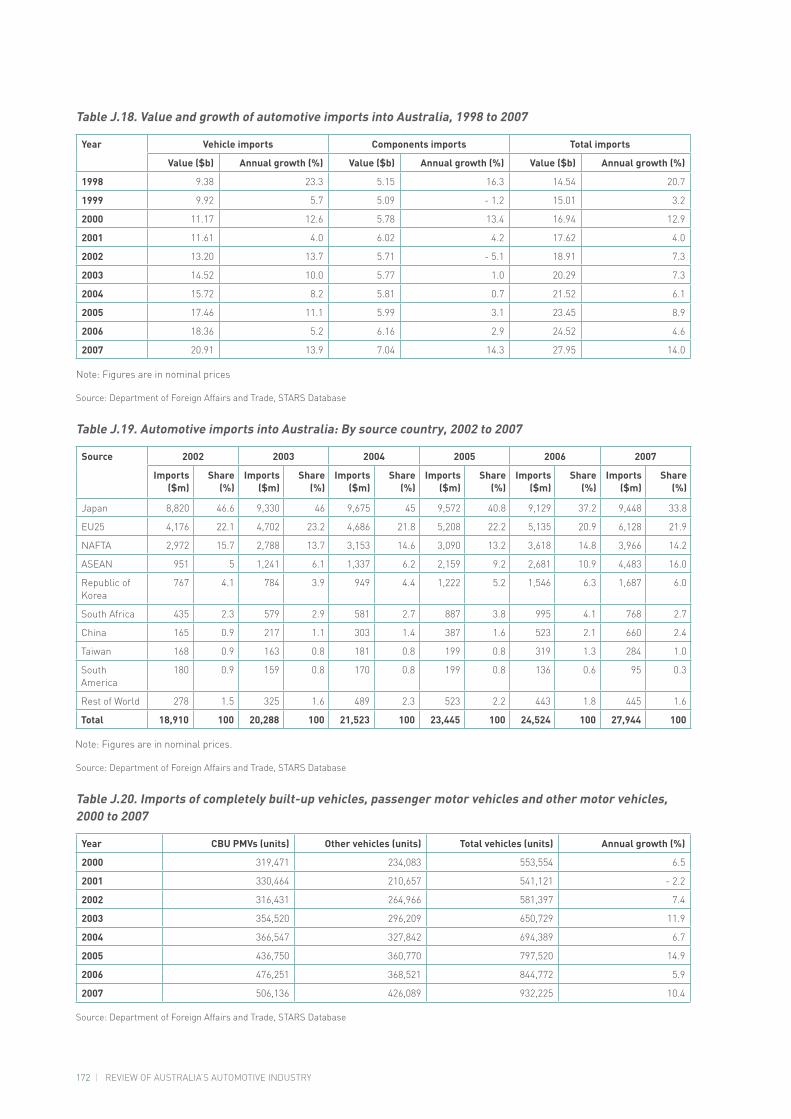

Imports

TheAustralianautomotiveindustryoperatesinanincreasinglycompetitiveglobalenvironment.ItfacescompetitionfromtraditionalautomotiveproducerssuchasJapan,theeuropeanUnionandtheUnitedStates,andfromAsianeconomiessuchasThailand,ChinaandtheRepublicofKorea.Australiaisalsooneofthemostopenautomotivemarketsintheworld.ofthemajorautomotive-producingcountries,onlytheUnitedStates,Canada,JapanandtheRepublicofKoreahavemoreopenmarketsintermsofthelevelofappliedtariffsonautomotiveproducts(seeTable5.1inChapter5).TheeuropeanUnionappliesa10percenttariffonautomotiveimports.

Importshaveincreasedsignificantlyoverthelastfewyearsfrom$18billionin2002to$27billionin2007,anincreaseof47percent.Thisincreasecamelargelyfroma61percentincreaseinvehicleimportsbetween2002and2007.

Australia’smajorsourceofimportsremainsJapan(36percentofvehicleandpartsimports),followedbyThailand(12percent),theUnitedStates(12percent),

31 DepartmentofForeignAffairsandTrade,STARSDatabase,DFAT,Canberra,2008.

14| ReVIeWoFAUSTRALIA’SAUToMoTIVeINDUSTRY |15THeAUSTRALIANAUToMoTIVeINDUSTRY

Germany(9percent)andtheRepublicofKorea(6percent).ThelargestimportgrowthhasbeenfromThailand,whichincreasedby$2.1billionbetween2002and2007.SomeofthiscanbeattributedtotheThailand–Australiafreetradeagreement,whichallowsduty-freeentryofThai-manufacturedvehiclesintoAustralia.

exports

In2007,totalautomotiveexportsfromAustraliaamountedto$4.7billion,whichplacestheindustryinthetop10exportearnersandaheadofmoretraditionalexportssuchaswheatandwool.ofthis,over$2.9billioncamefromtheexportofmotorvehicles,and$1.7billioncamefromthedirectexportofautomotivecomponents,32thatis,componentsnotincorporatedintocompletevehicleexports.

AustralianMVPshavebecomeincreasinglyfocusedonexportmarkets.TheAustralianmotorvehiclemarketisrelativelysmall,andMVPsarefacingdifficultyinachievingscaleeconomiessolelyonthestrengthofdomesticsales.In1997,only16percentoflocalproductionofAustralianmotorvehicleswassoldoverseas.By2007,thisfigurehadincreasedto42percent.33

Since2002,automotiveexportshavefallenby$79millionto$4.7billion.ThiscanbepartlyexplainedbytheappreciationoftheAustraliandollar,whichhaslessenedtheAustraliandollarvalueofexportswherecontractsaredenominatedinUSdollars.However,thisexchangerateeffecthasbeenpartlyoffsetbyincreasesinefficienciesintheautomotiveindustry.Thiscanbeseenbythefactthat,whiletheAustraliandollarhasappreciatedby53percentsince2002,automotiveexportshavefallenbyonly4.6percentoverthesameperiod.

Giventhehigh—but,forsomemodels,declining—localcontentinAustralian-madecars,andthedependenceofcomponentproducersonsalestodomesticMVPs,exportsofvehiclesareveryimportanttothecomponentsector.

Inthepastfewyears,theMiddleeasthasemergedasAustralia’smainexportmarket.Thereissignificantpotentialforgrowthinthisregion,givenitshighlevelofdemandforlargecarssuchastheToyotaCamryandHoldenCommodore(badgedastheChevroletLumina).Australianvehiclesarealsogrowinginpopularityintermsoffleetsales.TaxifleetsintheregionhaveapreferencefortheAustralian-producedToyotaCamry,andtheSaudiArabianpoliceforcehasapreferenceforHoldenCommodores.The

32 ibid.33 DepartmentofInnovation,Industry,ScienceandResearch,op.cit.,

p.21.

demographicsintheregionalsosuggestthatthemarketwillcontinuetogrow—themedianageinSaudiArabiaisaround21years.Itisalsoexpectedthatwomenwillbegrantedtherighttodrivebytheendof2008,whichwillpotentiallyincreasethesizeoftheautomotivemarket.

exportstoSaudiArabia,theUnitedArabemirates,Kuwait,oman,QatarandBahrainamountedto$2.2billionin2007,or46percentoftotalautomotiveexports(and75percentofvehicleexports),anincreaseof19percentsince2002.Australia’slargestsingletradingpartnerisSaudiArabia,withautomotivesalesof$1.2billionin2007.ThisdependenceontheMiddleeastmarketisaconcernfortheindustry,especiallywithgrowingcompetitionfromnationsthatenjoyscaleandgeographicadvantagesoverAustralia.Inaddition,US-sourcedvehiclesentertheGulfStatesduty-freeduetofreetradeagreementprovisions.

othermajorautomotiveexportmarketsincludeNewZealand(16percent),theRepublicofKorea(9percent)andtheUnitedStates(9percent).AutomotiveexportstotheUnitedStatesdecreasedby64.6percentfrom2002to2007,fallingfrom$1.1billionto$394million.ThiscouldbepartlyduetotherisingAustraliandollarandthefallintheUSmarketshareoftheUS-ownedand-basedautomotivecompanies.However,earlysalesoftheAustralianHoldenG8vehicletotheUnitedStateshavebeenstrong,andGMHoldenforecastsavolumeofaround30,000unitstobeproducedfortheUSmarketin2008.34

TheexportofdesignandengineeringservicesisbecomingincreasinglyimportantfortheAustralianindustry.WhilesubmissionstotheReviewdidnotreportontheincomeearnedfromsuchactivities,Australia-basedGMHoldenisresponsibleforthedesignandengineeringofrear-wheel-driveproductsforAustraliaandGMbrandsglobally,FordAustraliaisthedesignandengineeringcentreofexcellencefortheAsia–PacificandAfricaregionsforitsparentcompany,whileToyotaAustraliaisoneoftwotechnicalcentresforToyotaMotorCorporationintheAsia–Pacificregionandoneofitsfivetechnicalcentresglobally.Inaddition,firmsinthesupplychainarealsoearningexportrevenuethroughdesign,engineering,andreturnsonintellectualproperty,aswellasrepatriatingprofitsfromoverseasoperations.

Figures1.5to1.8below,andAppendixA,providefurtherdetailonAustralia’stradeinautomotiveproducts.

34 GMHolden,op.cit.,p.24.

16| ReVIeWoFAUSTRALIA’SAUToMoTIVeINDUSTRY |17THeAUSTRALIANAUToMoTIVeINDUSTRY

Source:DepartmentofForeignAffairsandTrade,STARSDatabase(2007).

Source:DepartmentofForeignAffairsandTrade,STARSDatabase(2007).

Source:DepartmentofForeignAffairsandTrade,STARSDatabase(2007).

Source:DepartmentofForeignAffairsandTrade,STARSDatabase(2007).

16| ReVIeWoFAUSTRALIA’SAUToMoTIVeINDUSTRY |17THeAUSTRALIANAUToMoTIVeINDUSTRY

summary of fIndIngsAustraliahasoneofthemostopenautomotive�marketsintheworld.

Australianmotorvehicleandcomponent�producershavebecomeincreasinglyfocusedonexportmarkets.TheautomotiveindustryisamongAustralia’stop10exporters,aheadoftraditionalindustriessuchaswine,wheatandwool.

Therehasbeenashiftinconsumerpreference�towardssmaller,lowerfuelconsumptionvehiclesandSUVs(whichareseenasasubstituteforthefamilycar).Thishasadverselyaffectedthelocalvehicleassemblers,whichproduceinthelargecarsegment,despitethefactthatSUVsaregenerallynotasfuelefficientastheAustralian-madelargevehicles.

Theautomotiveindustryisanimportantpartof�theAustralianeconomy,employingover64,000peopleandaccountingforalmost6percentofmanufacturingemployment.Valueaddedforthesectortotalsmorethan$5.6billion,representing5.6percentofthemanufacturingsector’sindustryvalueaddedand0.6percentofnationalgrossdomesticproduct.

FallingprofitabilitylevelsofthelocalMVPs�presentsamajorchallengetothelocalindustry.In2007,tradinglossesinvehiclemanufacturingforMVPswere$722million,oran8.6percentlossonsales.

|19

IntroductIonThecompetitiveenvironmentfacingtheAustralianautomotiveindustryhaschangedsubstantiallysincethecompletionofthepreviousvehicleindustryreviewinDecember2002.TheindustrynowfacesastrongandrisingAustraliandollar,risinginputcosts(particularlyforrawmaterials),anincreasinglycompetitiveglobalautomotivemarket,environmentalconcerns,risingoilprices,andchangingconsumerpreferencesinamovementawayfromlargeAustralian-producedvehicles.Thelocalindustryneedstotakeadvantageofarangeofopportunities,includingtheconsumershifttowardnewfuelanddrivetraintechnologiesandthedramaticgrowthinemerginginternationalvehiclemarkets.

Theindustryalsohasopportunitiestocompeteinvarioussegmentsoftheautomotivedesignandmanufacturingprocess,notonlyinrelationtotheexportofautomotivegoodsbutalsoinrelationtotheexportofR&Danddesign,licensingofIP,relocation,andtherepatriationofprofitsfromforeigndirectinvestment.

opportunItIes for the AustrAlIAn AutomotIve Industry

Exportopportunitiesinestablishedandemergingmarkets

Thelocalmarketisrelativelysmallandexpansionintooverseasmarketsisimportantforincreasedsalesandproductionandscaleeconomies.Thisexpansionalsohelpsunderpintheindustry’ssustainability.

EmergingmarketssuchasChina,RussiaandIndiapresentmajoropportunitiesformotorvehicleproducers(MVPs)andcomponentsuppliers.TheautomotiveindustriesintheseeconomiesarestilldevelopingandthispresentsanopportunityfortheAustralianautomotiveindustry,whichincludesestablishedcomponentproducersandhasadvanceddesignandtoolingcapabilities.However,FuturisandarangeofothercompaniesnotedintheirAutomotiveReview2008submissionsthattariffandnon-tariffbarrierspresentamajorobstacleinmanyofthesecountries(thisisdiscussedfurtherinChapter7).

TradetoestablishedmarketssuchastheUnitedStatesandtheMiddleEaststillpresentsMVPsandcomponentproducerswithopportunitiesforgrowth.ToyotahasestablishedastrongmarketintheMiddleEast,particularlyinSaudiArabia.Toyotaexportsaround95,000vehiclesayearandsalestofleet,taxiandgovernmentbodiesinthesecountriesareparticularlystrong.Inaddition,GMHoldenhasopenedupanentirelynewmarketsegment,andwillbeginexportingtheHoldenutilitytotheUnitedStatesfrom2009.

ThereisalsopotentialtoexporttoemergingmarketsintheMiddleEastandNorthAfrica,includingLibya.ThegrowthintourisminLibyapresentsopportunitiesforAustraliatosupplytothetaxifleetmarketintheregion.

Increasingglobalsupplychainintegration

TheAustralianautomotiveindustryiscompetinginanincreasinglyintegratedglobalmarket.Costpressureshavemeantthatglobalplatforms,thatis

CHAPTER2:outlook for the australian automotive industry

20| REVIEWoFAUSTRALIA’SAUToMoTIVEINDUSTRY |21oUTLookFoRTHEAUSTRALIANAUToMoTIVEINDUSTRY

theuseofcommonvehicledesignsacrossdifferentproductionlocations,havebecometheindustrystandard.Thisphenomenonpresentsopportunitiesforcomponentsupplierstobecomemoreintegratedintoglobalsupplychainsandtodiversifyandinvestinforeignmarkets.Itcanalsobeathreat,inthatthelocalsupplychainfacesincreasingcompetitionfromimportsusedtomanufacturelocalvehiclesandmajorcomponents.

Acompleteindustry

Australiaisoneofonly15countrieswiththecapabilitytotakeacarfromconceptallthewaytofullproduction.ThiscapabilityencompassesstrongskillsetsinR&D,design,engineering,productandprocessdevelopmentandadvancedmanufacturing.Thismeansthatforasmallcountry,Australiacanproducevehiclesandcomponents,andforaworldmarketprovidedesignandengineeringservices(andaworldmarketcanproduceautomotivegoodsandservicesforAustralia).

ThisalsoprovidesAustralianfirmswithanadvantagewhencompetingagainstcountrieswhichmaylackacompleteindustryandwhichthereforemustfindanicheroleinglobalautomotiveproduction.ontheotherhand,opportunitiesavailabletotheindustryareunderpressurefromemergingeconomiessuchasChinaandIndia,whicharemovingupthevaluechainandareactivelydevelopingthefullspectrumofcapabilitiesneededtohostacompleteindustry.

ProximitytoAsia

Asiancountries,particularlyChinaandIndia,areexpectedtobemajorcontributorstogrowthingloballightvehicleproduction.Australiaiswelllocatedtobeabletotakeadvantageofthis,especiallyiftradebarriersareremovedorreduced.ontheotherhand,thegrowthinautomotivecapacityintheseeconomiesislikelytobeathreatintheAustralianmarketandinmarketsinwhichAustraliacompetes.

Creatingamarketnicheinemergingalternativefuelanddrivetraintechnologies

TheshiftofconsumerpreferencestowardsvehicleswithlowfuelconsumptionpresentsanopportunityforAustralia’sMVPstofindanichemarketforsuchproductsinthemediumtolargecarsegment.ForMVPsandthesupplychain,theopportunitiesrangefromtheproductionofhybridsandalternativefuelvehicles(suchasliquefiedpetroleumgas(LPG)andcleandiesel)throughtothedevelopment,adoptionanduptakeofcurrentdrivetraintechnologiessuch

ascylinderdeactivation,variablevalvetimingandactuation,sparkignitiondirectinjection,regulatedvoltagecontrol,variabledisplacement,air-conditioningcompressorandelectricpowersteering.

chAllenges

MaintainingandexpandingtheMiddleEastmarket

TheAustralianautomotiveindustryisheavilydependentonexportsalestotheMiddleEast,whichaccountforthree-quartersofvehicleexportsandnearlyhalfofthevalueofallautomotiveexports.ThreatstothismarketincludecompetitionfromimportsfromeconomiessuchasChina,IndiaandThailand.Thereisalsoarealdangerthatthismarketmayshifttowardssmallcarsashasoccurreddomestically.However,theMiddleEastmarketalsoconstitutesapotentialgrowthopportunityforAustralian-madevehicles.ThemaintenanceandexpansionofthismarketaredependentupontheexportstrategiesoftheparentsofAustralianMVPs.TheseandothermarketaccessissuesarediscussedinChapter7.

Changingconsumerpreferences

TherehasbeenasignificantchangeinthetypeofvehiclesdemandedbyAustralianconsumers.1Traditionally,theAustralianvehiclemarkethasbeendominatedbylargepassengercarsandtheirvariants.TherehasbeenatrendinAustraliaandinternationallytowardssmaller,lowerfuelconsumptionvehicles,sportsutilityvehicles(SUVs)andluxurycars.Thistrendhasrecentlyaccelerated,andimpactedonlocalvehicleproducers,withthemarketshareofAustralianMVPsfallingfrom30percentin2002to19percentin2007.

Morespecifically,since2002,domesticsalesofnewAustralian-madevehicleshavedecreasedforGMHolden(by33percent),Ford(by10.5percent),andMitsubishi(by53percent).onlysalesofAustralian-madeToyotavehicleshaveincreasedsince2002—by22percentto2007.Thistrendhascontinuedintothefirsttwomonthsof2008,withsalesofAustralian-madevehiclescontinuingtofall.

Nonetheless,thereareearlyencouragingsignsthatAustralianMVPsarerespondingtothechangingmarketcircumstances.Forexample,Fordhasannouncedplanstomanufacturethefour-cylinderFocusinAustraliafrom2011,andToyotaplanstobuildtheCamryhybridlocallyfrom2010.

1 FederalChamberofAutomotiveIndustries,VFacts,FCAI,2007.

20| REVIEWoFAUSTRALIA’SAUToMoTIVEINDUSTRY |21oUTLookFoRTHEAUSTRALIANAUToMoTIVEINDUSTRY

Greenhouseemissions

Theautomotiveindustryisconsideringwaystoimprovefuelconsumptionandreducegreenhouseemissions.Theseplansarecloselyintertwinedwitheffortstodevelopnewfuelefficienttechnologiesandvehicles,suchastheCamryhybridduein2010.TheMVPsnotethatimplementingthesechangestoincreasefuelefficiencyandreducingemissionsisextremelycostlyandrequireslargecapitalinvestments.

TheGarnautClimateChangeReview’sdraftreportrecommendedthatadomesticemissionstradingschemeshouldincluderoadtransport.2Thiswouldincreasethepricepaidbyconsumersforfuelssuchaspetrolanddiesel,andbeachallengefortheAustralianindustry,whichcurrentlyproduceslargecarswithrelativelylargeenginecapacities.

on16July2008,theAustralianGovernmentreleaseditsgreenpaperontheCarbonPollutionReductionScheme,whichisintendedtobeimplementedin2010.Attheheartoftheschemeisemissionstrading.Theschemewillcovertransport.To“offsettheinitialpriceimpactonfuelassociatedwiththeintroductionoftheCarbonPollutionReductionScheme,theGovernmentwillcutfueltaxesonacentforcentbasis”.TheGovernmentalsointendstoprovidetransitionalassistanceintheformofashareoffreepermitstothemostemissions-intensive,trade-exposedindustries.3

Profitability

AsdiscussedinChapter1,theprofitabilitylevelsofthelocalMVPsarefalling.Thereisalsoevidencecomponentproducers’profitmarginsaredeclining,whichcouldsignalfurtherrationalisationsintheindustry.

TherisingAustraliandollar

ThestrengthoftheAustraliandollar,especiallyinrelationtotheUSdollarandtheJapaneseyen,hashadamajornegativeeffectonthecompetitivenessoftheAustralianautomotiveindustry.Fortheexportsector,thekeyexchangerateistheUSdollar,bothbecausemostcontractsaredenominatedinthiscurrencyandbecausemajormarketsfortheindustry,suchastheUSandGulfCooperationCouncil,are

2 Garnaut,R,GarnautClimateChangeReview.DraftReport,CommonwealthofAustralia,Canberra,2008,p.368.

3 Wong,P(MinisterforClimateChange),GreenPaperonCarbonPollutionReductionSchemeReleased,mediarelease,PW117/08,16July2008.

linkedtotheUSdollar.4Forautomotiveimports,thevalueoftheJapaneseyenisparticularlyimportant,sincemostvehiclesareimportedfromJapanandarepaidforwithyen.

FromJanuary2002toJanuary2008,thevalueoftheAustraliandollarappreciated77percentagainsttheUSdollar,40percentagainsttheJapaneseyen,27percentagainstthekoreanwonand36percentonatrade-weightedbasis.5

ThishasledtoAustralianvehiclesbecomingrelativelymoreexpensivecomparedtotheirimportcompetition.Thenewcarpriceindex,whichmeasurestheaverageretailpricesofvehicles,hasincreasedby9percentsince2001forAustralianautomobiles.6However,overthesameperiod,thepriceindexofallimportedvehiclesdroppedby2percent,andforJapanesevehiclesfellby4percent.TherisingAustraliandollaralsoimpactsonexporters,asmanycontractsuseUSdollars.

ontheotherhand,MVPsandsomecomponentproducershaveanaturalhedgeagainsttherisingAustraliandollar,astheyimportinputstoproduction.Inaddition,theappreciationoftheAustraliandollarhasreducedthecostofimportedcapitalequipmentrequiredforupgradingandexpandingcapacity.

TheProductivityCommission’seconomicmodellingshowsthattheeffectsofchangesinautomotiveassistanceontheindustry,andindeedtheeconomy,wouldbeverysmallrelativetootherinfluencesontheindustry,inparticularexchangeratemovements.Forexample,afurtherappreciationoftheAustraliandollar,inducedbyanongoingcommodityboom,isprojectedtoleadtoasignificantcontractionintheautomotiveindustry.Thiscontradictionwouldbefargreaterthanoneresultingfromreducingtariffs,andwouldalsoleadtoacontractioninseveralotherindustries.Moreover,afuturedecreaseintheexchangerateofcomparablemagnitude—resulting,forexample,fromareductionincommodityprices—wouldseeanexpansionthatwouldmorethanoffsetthemodelledeffectsofreductionsinassistance.7Thisassumes,ofcourse,thatasignificantcontractionintheautomotivesectordoesnotleadtodiseconomiesofscaleandtheexitofmanyfirmsthatwouldnotre-entertheAustralianmanufacturingsector.

4 DFAT,Submissiontothe2008AutomotiveReview,p.13.5 ReserveBankofAustralia,HistoricalExchangeRates,2008,

www.rba.gov.au/statistics/historicalexchangerates6 AustralianAutomotiveIntelligence,AustralianAutomotive

IntelligenceYearbook2008,7thedn,RichardJohns,2008.7 ProductivityCommission,ModellingEconomy-wideEffectsofFuture

AutomotiveAssistance.ResearchReport,PC,Canberra,2008,p.61.

22| REVIEWoFAUSTRALIA’SAUToMoTIVEINDUSTRY |23oUTLookFoRTHEAUSTRALIANAUToMoTIVEINDUSTRY

Smallscale

Anumberofnewglobalautomotiveassemblyplantshaverecentlyopened,eachwithaminimumproductioncapacityof300,000unitsperannum.ThisfigureisclosetotheentireAustralianannualproduction.Itisgenerallyacceptedthataminimumplantcapacityof300,000to400,000unitsperannumisnecessarytohelpensureprofitabilityforsomesmallandmediumsizecarproductionwheremarginsarelow.Australiadoesnothavethedomesticmarketsizetojustifysuchascaleofproduction.Thisfurtherhighlightstheimportanceofexportsinhelpingboostproductionandeconomiesofscale.

ontheotherhand,therelativelysmallscaleofproductioninAustraliaallowssignificantflexibilitybasedonnicheproductionandsignificantscopetorampuporreduceproductioninlinewithmarketdemand.Forexample,thesmallscalecanenablefirmstorespondmoreflexiblytochangingcircumstances,suchasrisingdemandformorefuel-efficientvehicles.Itismuchharderforlargercapacityplantstoretoolforsmallvolumes.

Fragmentedcomponentsector

TheAustraliancomponentmanufacturingsectorisfragmented,withmanysmallfirmsoperatingintheindustry.Afragmentedcomponentindustrydoesnotproduceonasufficientscaletobegloballycompetitive.Furthermore,smallerfirmsdonothaveaccesstotheglobaltechnologiesavailabletothelargermultinationalTier1firms,arenotascompetitiveaslargerTier1firms,andlackskillsparticularlyintermsofmanagementandmanufacturingquality.8TheseinefficienciesimpactontheentireautomotiveindustryandarediscussedfurtherinChapter9.

Discontinuityofsupply

Arangeoffactors,includingthoselistedabove,haveimpactedheavilyonAustraliancomponentmanufacturers,especiallysmallerfirmsoperatingatthemargin.Asaresult,anumberofsmallercomponentproducershaveclosedinthepastfewyears,anditisestimatedthat7,135jobshavebeenlostintheautomotivecomponentsectorbetween2002and2006.9Thisdiscontinuityincomponentsupplyaffectstheentireautomotiveindustryproductionchain,giventheimportanceofjust-in-timeproduction.AsdiscussedinChapter9,thisimposesanumberofcosts,includingsupplybreakdowns.Italso

8 AustralianAutomotiveIntelligence,op.cit.,p.45.9 FAPM,Submissiontothe2008AutomotiveReview,p.53.

hascostsassociatedwithMVPsandTier1companieshavingtofindalternativesuppliers,coststoworkers,andcoststothereputationoftheAustralianindustry,includinginexportmarkets.Furthermore,itflowsthroughtoandimpactsonthereputationoftheAustralianmanufacturingsectorasawhole.AnactualorperceivedinabilityoftheautomotiveindustrysupplychaintoprovidecontinuityofsupplyhasthepotentialtodiminishtheattractivenessofAustraliaasaninvestmentlocation.

Competitionforinvestment

ManyoftheAustralianMVPsandTier1componentmanufacturersarepartofglobalorganisationsandcompeteforinvestmentfundswithotherforeignsubsidiaries.ManyofthesefirmsnotedintheirsubmissionstotheReviewthatitisbecomingincreasinglydifficulttoattractinvestmentfundshavingcompetingsubsidiariesfromnationswithlowercoststructures(intermsofoverheadsandlabour),moregovernmentsupportprograms,greatertradeprotectionandgreateradvantagesofscale.Inpart,thesedevelopmentsreflectthechangeintheAustraliandollarexchangerateoverthelastseveralyears.

Thishasimplicationsforthesupplychain,whichisreliantondomesticproductionofvehiclesandwhichsuppliesTier1companies.Forexample,theAustraliantoolingindustryisheavilyreliantoncapitalinvestmentbyMVPsandthecomponentssectorinplantandequipment,suchasassemblyandsubassemblylines.Thisinvestmentis‘lumpy’innatureandcentredaroundnewmodellaunches.Thetoolingindustryisalsofacingincreasedcompetitionfromimportsofbasictools,particularlyfromChinaandIndia.

SeveralMVPsandTier1componentmanufacturersnotedtheimportanceoftheAutomotiveCompetitivenessandInvestmentScheme(ACIS)inattractinginvestmentintheirReviewsubmissions.Forexample,GMHoldenreportedthat“ACIScombinedwithothergovernmentincentiveschemeshasprovidedsupportforlarge-scalecapitalinvestmentinAustraliaincludingtheHigh-FeatureV6EngineplantatFisherman’sBend,andthenewVECommodore”.10

RelianceofthecomponentproducersandthetoolingindustryondomesticMVPs

ThecomponentproducersandthetoolingindustryareveryreliantondomesticMVPsforsales.ThecomponentproducersrelyontheMVPstoassemble

10 GMHolden,Submissiontothe2008AutomotiveReview,p.40.

22| REVIEWoFAUSTRALIA’SAUToMoTIVEINDUSTRY |23oUTLookFoRTHEAUSTRALIANAUToMoTIVEINDUSTRY

completevehicles,eveniftheysupplytoothercomponentproducers.ThetoolingindustryreliesoncapitalinvestmentbyMVPsasnotedabove.

Thisreliancecanhaveadverseeffectsonthesupplychain.Forexample,theHouseofRepresentativesStandingCommitteeonEmployment,WorkplaceRelationsandWorkforceParticipationreportedthattheglobalpricematchingpracticesoftheMVPs,includingtherequirementthatlocalsuppliersmatchdevelopingcountries‘exworks’prices(thatis,pricesofgoodsleavingthefactory)withoutincludingtransportationandstoragecosts,combinedwiththecontractmanagementprocess,hadledtoaninsecuretradingenvironment.11SuchpracticescanseriouslyaffectthosefirmsreliantontheMVPsandmilitateagainstsufficientgrowthininternalcashflowfromretainedearningstofinanceproductivity-enhancingautomationorinvestmentinR&D.TheresultingfinancialstressandlackofcompetitivenessputstheviabilityoflocalsuppliersatriskandcanactasadisincentivetocontinuedinvestmentinAustralia.

Componentsectorbenchmarkedperformance

TheAutomotiveSupplierExcellenceAustraliaStage2initiativefoundthatthecapabilitiesintheautomotivecomponentproducersectorrequiringthemostattentionweremanagementandleadership,followedbymanufacturingandquality,supplychainintegrationandmanagement,globalsourcingandmarketingstrategiesandfinancialsystemsandpractices.ThisisdiscussedmorefullyinChapter9.

summAry of fIndIngsTheAustralianautomotiveindustryneedsto�continueexpandingitsexportstoattainthescalenecessarytobegloballycompetitive.

MVPsandTier1componentmanufacturers�arefacingincreasingcompetitionforscarceinvestmentfundsfromother-country-basedsubsidiarieswithintheirglobalorganisation.Nevertheless,theAustralianautomotiveindustrycontinuestobegloballycompetitive,maintainingastrongexportbaseeveninthecontextofanappreciatingAustraliandollar.

TheAustralianMiddleEastmarketisvulnerable�toimportcompetitionfromChina,IndiaandThailandandalsoapossibleshifttoapreferenceforsmallervehicles.ontheotherhand,thereis

11 HouseofRepresentativesStandingCommitteeonEmployment,WorkplaceRelationsandWorkforceParticipation,ShiftingGears:EmploymentintheAutomotiveComponentsManufacturingIndustry,HRSCEWR,Canberra,2006,p.13.

alsotheopportunitytoexpandAustralia’smarketintheMiddleEastandNorthAfrica,includinginLibya.

Thetrendtowardssmaller,lowerfuel-�consumptionvehiclesimpactsonlocalvehicleproducersandthesupplychain,withthedomesticmarketshareofAustralianMVPsfalling.Nonetheless,thereareencouragingsignsthatAustralianproducersarerespondingtothesechangingcircumstances,suchasplanstolocallyproducetheFordFocusandToyotaCamryhybrid.

Consistentwithtrendsinothermajorautomotive-�producingcountries,andwithlargetradinglossesoccurring,justifyingdomesticproductionpresentsamajorchallengetoAustralianMVPs.

ThestrengthoftheAustraliandollarishavinga�majornegativeimpactonthecompetitivenessoftheAustralianautomotiveindustry.

TheAustraliancomponentmanufacturingsector�isfragmented,withmanyfinanciallystressedsmallfirmsoperatingintheindustry.Thishasledtoarangeofinefficiencieswithinthecomponentindustryassociatedwithlackofscale,andunderdevelopmentofthemanagementsystemsandorganisationalcapabilitiesrequiredtocompeteeffectively.

Componentproducersmustnowcompeteagainst�productionfromdevelopingcountrieswithlowercoststructuresthanAustraliaandincreasinglycompetitiveproductquality.

Thecapabilitiesand,insomecases,thescale�ofsmallercomponentmanufacturersneedtoberaisedclosertointernationalbestpracticeiftheyaretosurviveandbeviableintheindustry.Thisincludesmanagementandleadershipimprovements.

|25

IntroductIonTheproductionofmotorvehiclesrepresentsthelargestmanufacturingsectorintheworld:ifitwereacountry,theindustrywouldhaveanoutputequivalenttothatoftheworld’ssixth-largesteconomy.1Whileitisakeyactivityinadvancedindustrialnations,theindustryisalsoofincreasingsignificanceintheemergingeconomiesofNorthandEastAsia,SouthAmericaandEasternEurope.Itdrawsonawiderangeofsupplierindustries,fromrawmaterials(suchassteel,aluminium,plasticsandchemicals)throughtosophisticatedcomponentassemblies,tooling,designandengineeringservices.TheindustryisalsooneofthelargestinvestorsinR&D,playingakeyroleinsociety-widetechnologicaldevelopment.Withitsskillbaseandinnovativepractices,theautomotivesectorisseenasprovidinganeffectivenationaltraininggroundformanymanufacturingandengineeringemployeesacrossverydiverseindustries.

GeoGraphIcal dIversIfIcatIon and GlobalIsatIon of productIon

Globalproductionandsales

Onaglobalscale,theproductionofmotorvehicleshasexpandedsignificantlysincethelate1990s.Globalproductionofpassengermotorvehiclesgrewbyaround25percentbetween1999and2006,fromjustunder40millionunitstoalmost50millionunits.Globalproductionofcommercialvehiclesincreasedfromnearly16.5millionunitsin1999

1 OrganisationInternationaledesConstructeursd’Automobiles(OICA),2008,http://oica.net/category/economic-contributions/

toover19millionunitsin2006,anincreaseofaround16.6percent.

Globalvehiclesaleshavealsobeenincreasingsteadily,withsalesrisinginbothmatureandemergingmarkets.Motorvehicleproducers(MPVs)sold65.2millionunitsin2006,thefifthconsecutiveyearofrecordsales.Moreover,industrysaleshaveincreasedbymorethan30percentinthelastdecade,oratabouttwicethepaceofexpansionintheprevioustwodecades.2

Nonetheless,salesgrowthhassignificantlylaggedbehindthegrowthofproductionvolumes(with65.2millionsalesversusnearly70millionunitsproduced).Indeed,significantexcesscapacitycontinuestoexistintheindustry.AccordingtoCSMWorldwide,theindustrybeganthecurrentdecadeatonly68percentofcapacityutilisation—wellbelowthe80percentconsiderednecessaryforsustainedprofitability.Whilethatlevelrosetoabout76percentbytheendof2005,CSMforecastssignificantover-capacitytocontinueatanannualaverageofsome18.4millionunitsinthe2008–2014period.3Asaresult,alargenumberofMVPs,particularlyinthematureeconomies,haveundertakencostlyrestructuringsandrationalisationsinordertoreducecapacityandrealignboththeirproductionvolumesandemployeenumberswithoftenstagnantorevennegativedomesticsalesgrowth.TherecentslowdownintheUSautomotiveindustryisexacerbatingthistrend.

2 PriceWaterhouseCoopers,GlobalAutomotiveFinancialReview:AnOverviewofIndustryDataTrendsandFinancialReportingPractices,PWC,n.p.,2007,p.8.

3 Cather,C,NavigatingtheAutoIndustry’sVolatileWaters,CSMWorldwide,n.p.,2008,viewedathttp://www.automotivedigest.com/WhitePapers/CSM_FFS_NavigatingAutoIndustry.pdf

ChAPTER3:The global auTomoTive indusTry

26| REVIEWOFAUSTRALIA’SAUTOMOTIVEINDUSTRY |27ThEGLObALAUTOMOTIVEINDUSTRY

Riseofemergingmarketsandgeographicaldispersionofproduction

Demandforvehicleshasgrownrapidlyindevelopingcountries,providinganincentiveforthemajorglobalvehicleandcomponentmanufacturerstosetupproductionfacilitiesinthesemarkets.Inits2002reviewofthevehicleindustry,theProductivityCommissionnotedtherewereseveralfactorsthatreinforcedthisincentive,allofwhichareofcontinuingrelevancetoday:

localindustrysupportmeasuresthathaveboth�encouragedinvestmentinproductionfacilitiesanddiscouragedservicingthesemarketsviaexports;

improvedautomotiveinfrastructure,production�skillsandtoolingcapacityinmanyemergingvehicle-producingcountries(towhichonecouldaddstrengtheningR&Dcapabilities);and

logisticalconsiderationsthatencouragethe�locationofcomponentproducersclosetotheircustomers,includingjust-in-timeand/orsequencedvehicleproduction.4

Whiledevelopedcountriesstillaccountforthebulkofglobalvehicle,component,andrelateddevelopmentanddesignactivities,thegeographicaldiversificationofproductionhasresultedinashiftinthebalanceofoutputtowardsdevelopingeconomies.CountriessuchasChina,theRepublicofKorea,brazil,India,Russia,ThailandandMexicopossessthrivingautomotivesectors,asbothlocalandforeigninvestmentflowintonewandalreadyestablishedmanufacturingplants.AnumberofcountriesinEasternEurope(particularlytheCzechRepublicandSlovakia)havealsobeenrecipientsofmajorinvestmentsinnewvehiclemanufacturingplants.