review of time value of money. future value fv = p v ( 1 + r) t future value of a sum f v invested...

TRANSCRIPT

Review of Time Value of Money

FUTURE VALUE

Fv = PV ( 1 + r)t

FUTURE VALUE OF A SUM Fv INVESTED TODAY AT A

RATE r FOR A PERIOD t :

WHAT DOES « PRESENT VALUE (PV) OF AN INVESTMENT »

MEAN ?

WHAT NEEDS TO BE INVESTED TODAY IN ORDER TO REALIZE A SPECIFIC FUTURE VALUE

Suppose a pension fund manager invests $10 million in a financial instrument that promises to pay 9.2% per yearfor 6 years.

$16,956,500

Suppose a pension fund manager invests $10 million in a financial instrument that promises to pay 9.2% per yearfor 6 years with interest paid twice a year

$17,154,600

FUTURE VALUE OF AN ANNUITY

[(1+r)t – 1]FVannuity= C -------------------

r

Annuity : when the same amount of money is invested periodically

C: amount of the annuityR : risk free ratet : period of the annuity

Suppose a portfolio manager purchases $20 million par value of a15-year bond that promises to pay 10% interest per year. The issuer makes a payment once a year with the first payment a year from now. Annual interest payments are reinvested at 8% annually

What will the portfolio manager have at the end of the 15-year period ?

•$20 million when the bond matures•Interest earned by investing the anual interest payments at 8%

$20M + 48,429,840 = 68,429,840$

PRESENT VALUE OF AN ANNUITY

1 - [1/(1+r)t ]PVannuity= C -------------------

r

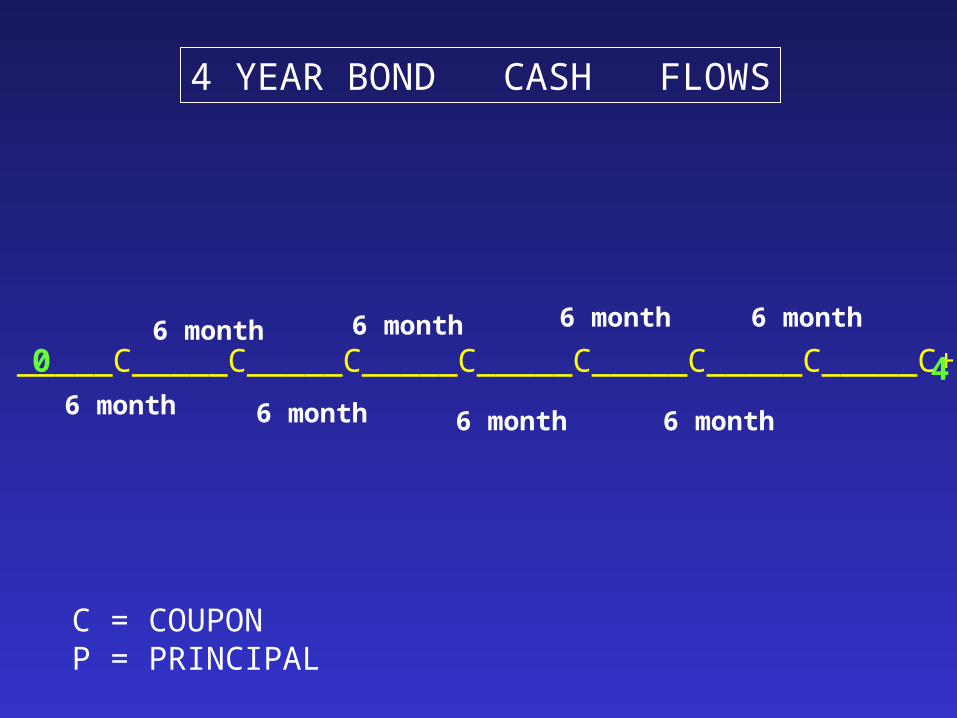

_____C_____C_____C_____C_____C_____C_____C_____C+P0 4

C = COUPONP = PRINCIPAL

6 month

6 month

6 month

6 month

6 month

6 month

6 month

6 month

THE PRICING OF A 4-YEAR BOND

PV OF ITS EXPECTED CASH FLOWS

THE PRICING OF A BOND

SUM PV OF ITS EXPECTED CASH FLOWS

SOL

VE

FO

R P

V

Fv

Σ PV = Σ ------------- ( 1 + r)t

EXAMPLE

SUPPOSE AN INVESTOR EXPECTS TO RECEIVE $1000 SEVEN YEARS FROM NOW. SUPPOSE THE INVESTOR CAN EARN 5% ANNUALLY COMPOUNDED ON ANY SUM INVESTED TODAY.

WHAT IS THE PV OF THAT SUM ?

$710.68

THE PRICE OF ANY FINANCIAL INSTRUMENT IS EQUALTO THE PRESENT VALUE OF ITS EXPECTED CASH FLOWS.

Pv = Pn/ (1+r)t

1. IDENTIFY THE EXPECTED CASH FLOWS2. ESTIMATE THE APPROPRIATE YIELD

IDENTIFY THE EXPECTED CASH FLOW:

1. COUPONS PAID EVERY 6 MONTHS

2. COUPON RATE IS FIXED

3. THE NEXT COUPON PAYMENT IS PAID EXACTLY SIX MONTHS FROM NOW.

_____C_____C_____C_____C_____C_____C_____C_____C+P0 4

C = COUPONP = PRINCIPAL

4 YEAR BOND CASH FLOWS

6 month

6 month

6 month

6 month

6 month

6 month

6 month

6 month

P= C/(1+r)t + C/(1+r)t + C/(1+r)t …+(C+P) /(1+r)t

P= C/(1+r)t + (C+P) /(1+r)t

CF of 1st CouponPrincipal+ last coupon

CF of 2nd Coupon

Sum of allCash flows

Sum of last cash flow + principal

EXERCISE

WHAT IS THE PRICE (using both methods) OF A 4-YEAR BOND (FACE VALUE $1000) WITH A 5% COUPON PAID ONCE A YEAR WHEN THE YIELD IS AT 6%?

WHAT HAPPENS TO THE BOND PRICE IF THE YIELDGOES UP TO 8%

Approx. $965

Approx. 89.90

Multi yearly payments.……

With annual coupon payments, the price of our bond would be computed as the presente value of an annuity:

+

PV of the par maturity value 1000/(1+R)t

$173

$792

$965

1 - [1/(1+r)t ]PVannuity= C -------------------

r

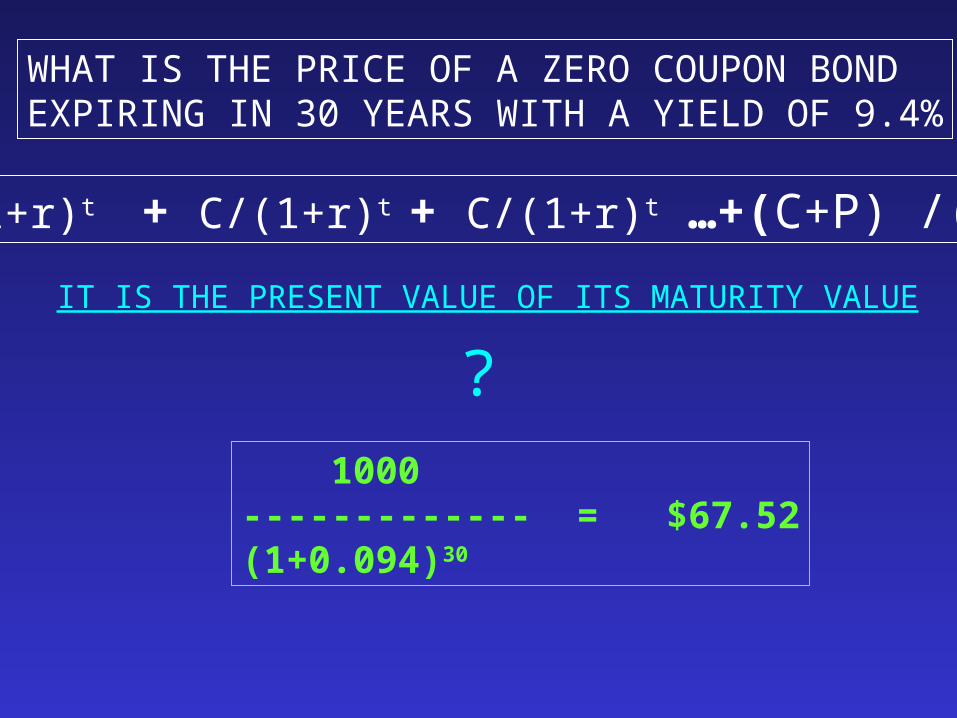

WHAT IS THE PRICE OF A ZERO COUPON BOND EXPIRING IN 30 YEARS WITH A YIELD OF 9.4%

IT IS THE PRESENT VALUE OF ITS MATURITY VALUE

? 1000------------- = $67.52(1+0.094)30

P= C/(1+r)t + C/(1+r)t + C/(1+r)t …+(C+P) /(1+r)t

WHAT ARE THE FACTORS THAT WILL AFFECT THE PRICE OF A BOND ?

•CHANGE IN RATING

•TIME LEFT TO MATURITY

•CHANGE IN INTEREST RATES

•WHETHER THE BOND TRADES AT A DISCOUNT OR AT A PREMIUM

•CREDIT RISK

PRICE QUOTE AND

ACCRUED INTEREST

•PREMIUM BOND >100•DISCOUNT BOND < 100•PAR BOND=100

WHEN QUOTING BONDS, TRADERS QUOTE THE PRICEAS A PERCENTAGE OF PAR VALUE

Cash price = Quoted price +Accrued Interest

WHEN AN INVESTOR PURCHASES A BOND BETWEEN COUPON PAYMENTS, THE INVESTOR MUST COMPENSATE THE SELLEROF THE BOND WITH THE COUPON INTEREST EARNED FROMTHE TIME OF THE LAST COUPON PAYMENT TO THE SETTLEMENT DATE OF THE BOND .

IF A BOND QUOTES 95, IT MEANS IT IS TRADING AT $950

IF A BOND QUOTES 85.5, IT MEANS IT IS TRADING AT…

$855DISCOUNT

IF A BOND QUOTES 102, IT MEANS IT IS TRADING AT…

$1020PREMIUM

GOT IT ?????

Coroporate bonds quoting system

IF A BOND QUOTES 100, IT MEANS IT IS TRADING AT…

$1000 Par

ACCRUED INTEREST

The acrrued coupon is the coupon which the seller of bond has « earned » so far by holding the bond since the last coupon date.

Consider a Treasury bond trading at 90.50 or $905Payments are made each March1 and Sept. 1Coupon rate = 8%=$80

You buy the bond on July 3…

Treasury bond : act/act basis

03/01 09/01 03/01 09/0109/01

July 3Lastcoupon date

# days since last coupon date-------------------------------------------------------------------- x coupon amount $ 365

124accrued interest = --------x 80 = $27.178

365

So, you'll pay the bond 905.0 + 27.1 = $932.1

Clean price Dirty price

Consider a corporate bond trading at 105 or maturing March 30th 2015Coupon rate = 6%=$60

You buy the bond on June 15th.

Calculate the “dirty price”.

Corp. 30/360 basis

$1050

# days since last coupon date-------------------------------------------------------------------- x annual coupon rate $ 360

75accrued interest = --------x 60 = $12.50

360

So, you'll pay the bond 1050 + 12.50 = $1062.50

Clean price Dirty price

HAVE A GOOD WEEK !