revised elaa proposal - european...

TRANSCRIPT

1

Revised ELAA Proposal

16 June 2006

Executive Summary

In the event that the Council decides to abolish the current Block Exemption for liner conferences as contained in Regulation 4056/86, the ELAA is submitting this Revised Proposal for the forthcoming Commission Guidelines.1

At the core of the Revised ELAA Proposal is a desire to create an environment of shared knowledge and improved communication embracing both service provider and end-user. Although we feel that conferences have proved their worth to world trade, we recognise the need to change. We want to propel ourselves into an age of shared knowledge, which will assist the functioning of a highly efficient, modern and transparent liner shipping industry.

The principles of the Revised Proposal are:

• A port-to-port aggregated volume database, based on aggregated figures provided by the carriers to an independent data service, with safety mechanisms to ensure that individual carrier figures cannot be identified. Practical delays in producing data mean that data can be published immediately when available without influencing competition, although it is conceivable that carriers will come up with a better system whereby the delay could be reduced and the ELAA firmly believes that the IDS should be allowed to publish data as it becomes available. This kind of information will not influence pricing negotiations and cannot be used as a tool for collusion;

• An industry supply and demand forecast produced with the help of an independent expert, based on accurate aggregated supply figures provided by the carriers to the independent data service, as well as demand figures and other information available in the public domain;

• A system of industry-wide consultation organised by a Liner Shipping Association, with an integrated system of carrier consultations as well as consultations with all other industry stakeholders to interpret, discuss and improve the forecast and better predict supply and demand developments as well as other issues relevant to the efficient management of a complex logistics chain;

• A simple aggregated price index by trade direction;

• Publication of information from the public domain to increase transparency of cost elements related to liner shipping such as bunkering, canal dues and port charges;

• Publication of information related to carrier currency costs; and

• All information generated will be made available to the general public.

The ELAA maintains that all these elements, which are explained in detail below, are absolutely necessary to maintain the stability of supply and regular liner shipping services to and from Europe when Regulation 4056/86 no longer applies. The ELAA Proposal does not allow any form of discussion between service providers on price, limitation of capacity or individual lines’ strategies.

Liner shipping is the engine room of globalization and a prerequisite for the maintenance and development of the European economy. Stability of supply and regularity of liner shipping

1 The ELAA submits this Revised ELAA Proposal without prejudice to its position, (as articulated during the

Commission’s review process) that DG Comp has not received or produced sufficient evidence that Regulation 4056/86 fails to satisfy the conditions of Article 81(3) EC and should be abolished.

2

services are the critical beneficial features of the current system that must be preserved in the new system, because they are crucial to almost every European business. The ELAA Proposal constitutes the least restrictive way to achieve those benefits in a fiercely competitive market.

But the ELAA is concerned about the potential implications of the Commission’s stated policy goal of abolishing the current Block Exemption for liner conferences as contained in Regulation 4056/86, not least on the international scene. Whilst agreeing on the need to create openness and transparency, the industry is faced with a regulatory world which is becoming more complex and more non-convergent by the day. This poses considerable threat to stability and unnecessary and unhelpful complication to the liner shipping industry. Regulatory authorities have to prevent this from happening.

The conference system has created stability in an otherwise volatile market. A comparison with the bulk market shows a large discrepancy; the bulk market has been significantly more volatile over the years. Abolition without an appropriate replacement would put the liner shipping industry at risk of becoming as volatile as the bulk market, an effect that will be further reinforced assuming the abolition of conference THCs. This would not only result in highly volatile freight rates but also in instability of supply. Rate fluctuations will result in uncertainty of the viability of future investment, and a risk of significant under-investment – putting efficient global trade in jeopardy. The first signs are already there with fear of insufficient supply in 2009. Regulation 4056/86 will be abolished, but the ELAA requests that the safeguards for stability as contained in this Proposal are provided. Global trade cannot afford to gamble with the stability of supply of liner shipping services.

The experience of liberalization and deregulation in other industries shows that the most diligent approach is one of caution. Unleashing uncontrolled competition in important network industries has led to damaging results in the past; as an example, the US is currently struggling with its major air carriers moving in and out of bankruptcy. The ELAA hopes that the European Commission, as in air transport (we refer to Annex 9 where the differences between liner shipping and aviation is described in detail), will take a more careful and sensitive approach than its US counter-parts did when deregulating the air carrier industry.

Information is a tool of competition. By making all information public, the Revised Proposal creates a level playing field with equally well-informed carriers, transport users and other industry stakeholders. Thus, the Revised ELAA Proposal is pro-competitive, as, in the words of Commissioner Reding, “only a well-informed consumer is a well-armed consumer”.2

2 Commission Press Release IP/05/1217, 4 October 2005 (regarding the Commission programme to publish

mobile roaming tariffs).

3

1. Introduction

1. On 6 August 2004, the European Liner Affairs Association (ELAA)3 submitted a Proposal for a new regulatory structure for the liner shipping industry (the Original ELAA Proposal). The Original ELAA Proposal was complemented by an in-depth assessment under Article 81 EC, submitted on 10 March 2005 (ELAA Article 81 EC Assessment). The Original ELAA Proposal represented, as does this Revised ELAA Proposal, a bona fide effort by the liner shipping industry to produce an alternative to the current Regulation 4056/86 regime, compatible with the Lisbon Agenda, which would enable the industry to continue delivering consumer welfare benefits in a post-conference world, whilst minimizing restrictions of competition. Since the submission of the Original ELAA Proposal, the consultation process has enabled the ELAA to consider its position and refine its suggestions to take into account comments that have been made. Extensive dialogue between DG Comp, DG Tren, shippers, freight forwarders and the ELAA has made this possible, and the ELAA is particularly grateful for DG Comp’s willingness to devote considerable resources and provide its comments in an open and transparent manner, which has enabled us to explain in detail why this Revised ELAA Proposal is necessary for the industry, and to make refinements in response to concerns raised by DG Comp. The ELAA explains the key elements of this Revised Proposal and their rationale in Annex 1.

2. The ELAA welcomes the Commission’s statement in its Explanatory Memorandum to the 14 December 2005 Proposal to repeal Regulation 4056/86 to issue Commission Guidelines on the application of competition rules to the maritime sector and in particular its commitment to include each item of the ELAA Proposal in those Guidelines.4

3. The ELAA’s position (as in all its previous submissions) is based on three pillars which characterize the liner shipping industry:

• The non-collusive market structure (whereto we note that the liner shipping market will become even more competitive after Regulation 4056/86 is abolished, and conferences, conference surcharges and ancillary charges will disappear);

• Its unique blend of characteristics; and

• The importance of stability of supply.

4. As misconceptions appear to remain – we refer to the DG Comp impact assessment based on the GI Study, published on the 14 December 2005 – the ELAA finds it necessary to reiterate the main aspects of these three pillars in Annex 2.

5. In particular, we note that stability of supply and reliability of liner shipping services is crucial for world trade. The industry characteristics have an inherent tendency to result in instability because of the high fixed costs needed for the provision of regular scheduled international services, rate fluctuations and fluctuating demand which the industry cannot control without an appropriate instrument to accurately forecast demand and supply. The

3 The world’s main liner shipping companies are comprised in the ELAA’s Members and their subsidiaries:

A.P. Møller/Maersk Sealand, Atlantic Container Line AB (Grimaldi), China Shipping (Group) Company, CMA-CGM Group, COSCO, CSAV (Compaňia Sud-Americana de Vapores S.A.), Evergreen Marine Corp. (Taiwan) Ltd., Hamburg Südamerikansiche Dampfschiffahrtsgesellschaft KG, Hapag Lloyd, Hanjin Shipping Co. Ltd., Hyundai Merchant Marine Co., Ltd., Kawasaki Kisen Kaisha, Ltd., Malaysia International Shipping Corporation (MISC), Mediterranean Shipping Co. S.A. (MSC), Mitsui OSK Lines, APL Co. Pte. Ltd., NYK Line (Nippon Yusen Kaisha Line), Orient Overseas Container Line Ltd., United Arab Shipping Co. (SAG), Yang Ming Marine Transport Corp., and Zim Integrated Shipping Services Ltd.

4 Proposal for a Council Regulation repealing Regulation (EEC) 4056/86 and amending Council Regulation (EC) 1/2003, COM(2005) 651 final, 14 December 2005, Explanatory Memorandum at 43. Therefore, the ELAA, having taken the comments made by DG Comp and other stakeholders into account, submits this Revised Proposal for review. The ELAA would like to stress that this is not a new Proposal, but a compilation of clarifications and modifications resulting from the consultation process; it contains no fundamental changes that would render the previously submitted ELAA Article 81 EC Assessment invalid, but rather less restrictive elements that would ensure compatibility with Article 81 EC.

4

essential welfare benefit generated by the current regime is stability of supply, defined as the matching of supply to demand, which seeks to ensure a relatively stable environment for an inherently unstable industry, as per the main objective of Regulation 4056/86.

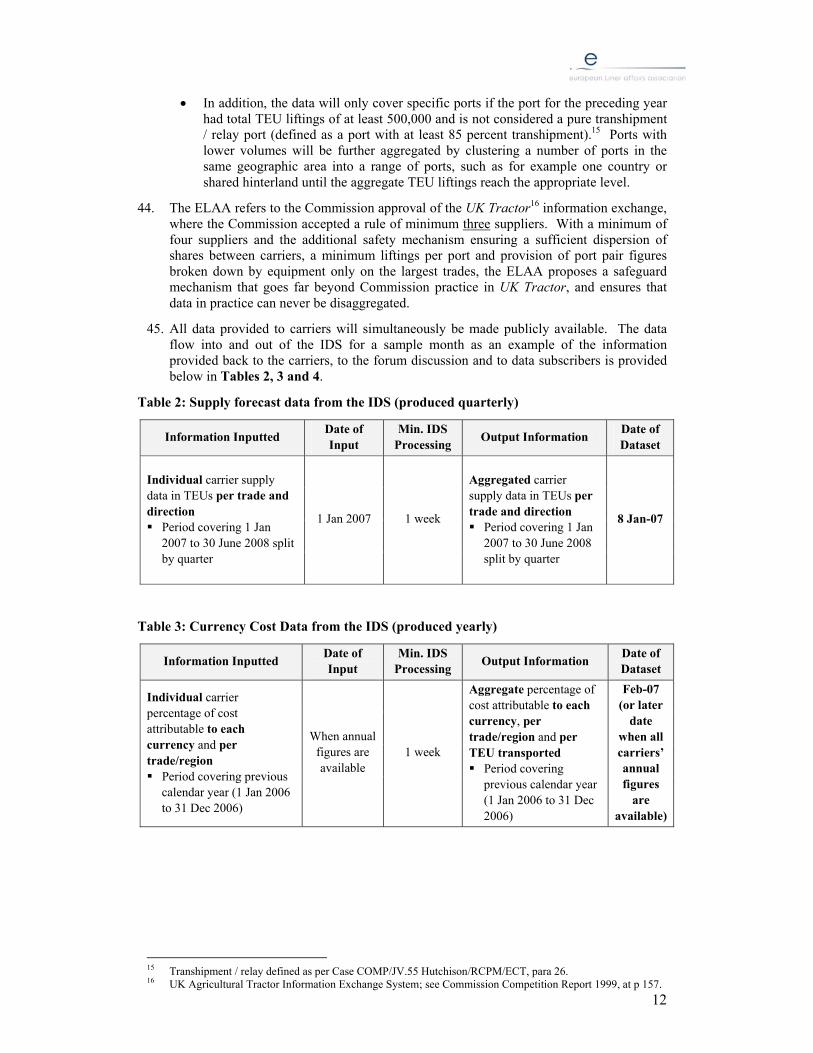

6. Overall, the ELAA believes the Revised Proposal achieves this benefit while remaining fully in line with Article 81 EC, and clearly much less restrictive than the existing system. In particular, the ELAA would like to stress the following crucial differences with the current system as contained in Regulation 4056/86. The Revised Proposal:

• Contains no provision for discussion on price or capacity management;

• Contains no provision for jointly agreed surcharges and ancillary charges and no joint discussions on the topic;

• Contains no provision for carriers to be able to take uniform decisions or strategies on commercial issues whatsoever;

• Contains no provision for exchange of individual sensitive carrier information, either through data exchange or discussions, but only aggregated and general information; and

• Explicitly ties the other industry stakeholders into the information exchange and discussions to ensure that true consultation emerges and all market participants can benefit.

7. DG Comp has stated that the Revised ELAA Proposal aims for “more than what is available today”. Although the ELAA agrees that the envisaged data would be of higher quality and have wider market coverage than today, it is not true that we are asking for more than what is currently available. Carriers today are allowed to discuss rates, regulate capacity and exchange individualised data and set surcharge and ancillary charges. The JoC data published on US trades, resulting from the need to file cargo information under OSRA, is significantly more detailed and recent than what the ELAA is proposing. A comparative overview of the differences between the current system and the Revised Proposal is presented in Annex 3.

8. The ELAA has during the consultation process made significant refinements to comply with DG Comp’s requirements, as outlined below in Table 1, by abandoning Trade Committees and the jointly agreed surcharges and ancillary charges, further delaying and aggregating data and by increasing transparency and the influence of other industry stakeholders.

5

Table 1: Comparison between the Original and the Revised ELAA Proposal

Original ELAA Proposal Changes in the Revised ELAA Proposal

Exchange and discussion between carriers of aggregated capacity utilization and market size data by trade and on a region/zone to region/zone basis (historic data with a month delay).

The exchange will be further aggregated at carrier level and the discussion will take place between carriers as well as with all industry stakeholders and regulators in a forum; data will be split by trade and port pairs or a range of ports in a trade zone); data which can be disaggregated will not be provided and solid safety mechanisms against disaggregation have been imposed; all information would be made publicly available. The data will remain sufficiently delayed, and the current delay will be a minimum of eight weeks.

Exchange, discussion and evaluation of commodity developments by trade (based on data aggregated with a month delay).

There will be no exchange of data split by commodity, but merely split by 20’ dry, 40’ dry and reefer containers (in the case of North-South trades provided only on a trade basis); the exchange will be further aggregated at carrier level; commodity developments will be discussed based on data from other sources, such as specific trade associations; all information would be made publicly available.

Discussion and evaluation of aggregate supply and demand data by trade/commodity. Forecasts of demand by trade and commodity would be published.

The industry forecast report will be produced with the help of an independent, external consultant, and then discussed and improved by the consultation process; there will be no commodity forecast; all information would be made publicly available.

Carriers will obtain their own market share by trade, by region and by port (data aggregated with a month delay).

No market share data of cargo carried will be provided.

Price index differentiated by type of equipment (reefer, dry) and trade direction (data aggregated with a quarterly delay). This information would be made publicly available.

The price index will not be differentiated by equipment type, but will be one index figure for the whole trade direction, which will continue to be publicly available. The index would continue to be provided monthly with a quarterly delay, but cover a whole quarter period.

Surcharges and ancillary charges based on publicly available and transparent formulae; the details of which would be discussed with shippers.

The Liner Shipping Association would publish the cost factors which constitute the stevedoring charge (THC) and publicly available information regarding other cost factors such as details of purchase price of fuel at various locations around the world, average fuel consumption, canal dues and port charges.

Based on the average aggregated cost structure of carriers, the Liner Shipping Association would publish the fluctuation of the US dollar compared to the average percentage attributed to each currency per TEU on a trade.

The envisaged system of information exchange would be based upon one or more industry body(ies) or agreements and committees per trade.

The trade committees have been replaced by an integrated system of industry-wide consultation, including carrier consultation and trade forums open to all stakeholders, split by trade; all information would be made publicly available.

6

9. Similarly significant are the differences between the Commission’s stated policy goal of abolition of Regulation 4056/86 and what the regulatory regimes of EU’s major trading partners allow. In fact, many of these seem to be on a different path from the EU. In particular:

• Japan is continuing to support the conference system and carrier consultation in general;

• The US has secured consultation through the Ocean Shipping Reform Act (“OSRA”) and very detailed statistics through the Journal of Commerce (JoC);

• Singapore has recently announced its intention to introduce a block exemption for conferences and other liner agreements5; and

• India is currently contemplating a system of significant transparency of data, even individualised, and will most likely accept liner conferences.

10. In Annex 4, the ELAA describes the importance of international comity and how this Revised ELAA Proposal can help overcome the problems created by the abolition of Regulation 4056/86 envisaged by the Commission.

11. In sum, the Revised Proposal signifies the end of commercial cooperation and transparency of carrier strategies, and introduces a new system that, in the ELAA’s view, significantly improves the information available to the market; a necessity in today’s knowledge based economy. It eliminates the facilitators of collusion but maintains, to the greatest extent possible, the means to provide stable and reliable liner shipping services in a fiercely competitive market. Without the Revised ELAA Proposal, there will be no regime to replace the information generated by conferences today; the industry stakeholders would have to act blind-folded.

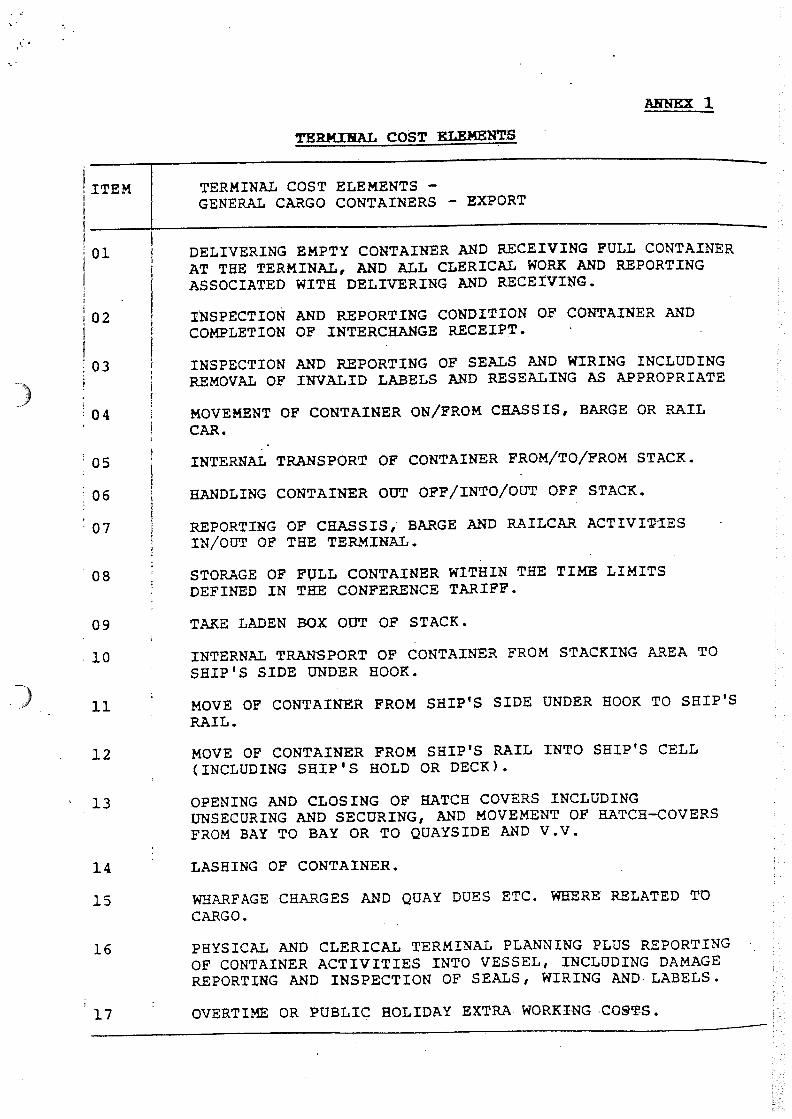

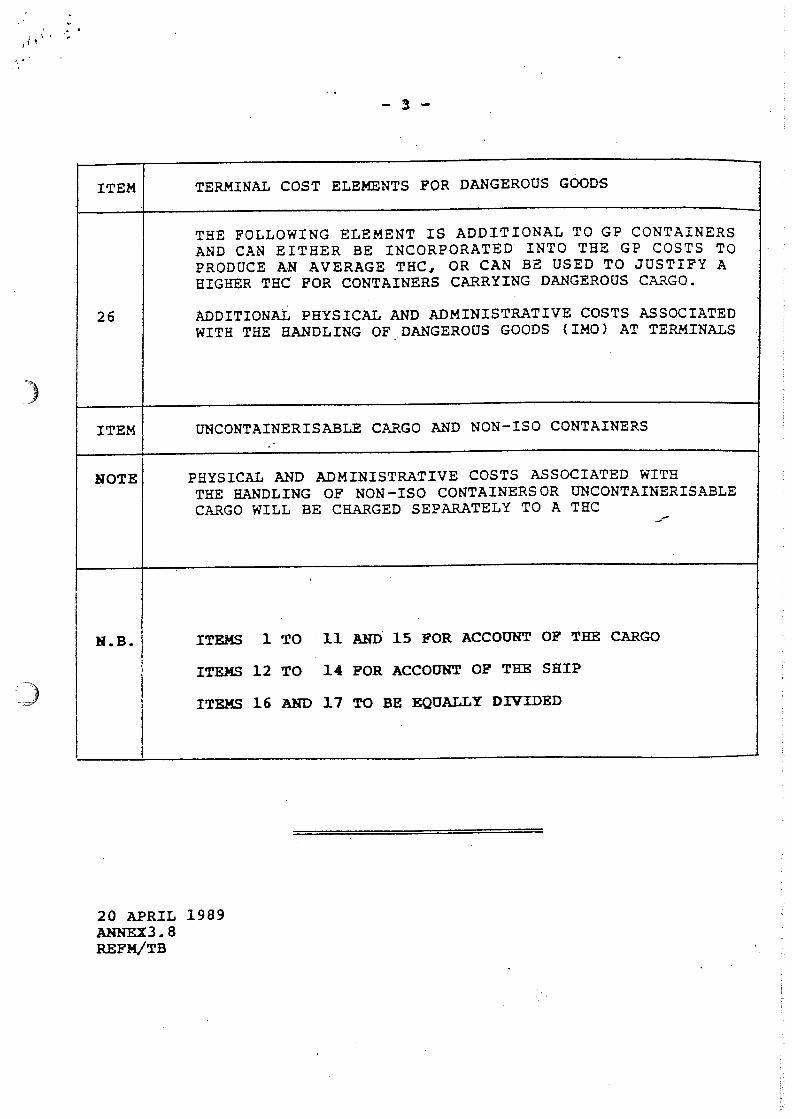

12. Almost all useful trade volume statistics (except for on US trades) are generated by the conference secretariats. Without conferences, there will be no reliable data available to industry stakeholders unless an appropriate replacement regime is put in place. This crucial factor has been overlooked in the impact assessments carried out by the Commission services and their consultants.

2. Why Are Guidelines Appropriate?

13. Article 81 EC incorporates a sliding scale. The more significant the restrictions of competition, the more significant the efficiencies and the consumer benefits generated must be.6 The assessment of the Revised Proposal under EC competition law is in essence an evaluation of the increased risk for collusion, if any, measured against the increased stability of supply. Although the Revised Proposal should not be salami-sliced but rather looked at as a whole (as also recognised by DG Comp), we will describe the key elements and the functioning of the envisaged system, and prove how for each element the benefits clearly outweigh any restrictions on competition. As a whole, the Revised Proposal as it now stands is clearly compatible with Article 81 EC.

14. The benefits of the ELAA Proposal cannot be fully appreciated by isolating and analyzing each element separately and out of context. Below, we first describe the benefits of the system as a whole. The benefits of each element will then be described in turn.

5 See Media Release of the Competition Commission Singapore, Competition Commission Consults on

Proposed Block Exemption Order (BEO) for Liner Shipping Agreements in the Maritime Industry, 6 April 2006, and Proposed Competition Act Order of the same date.

6 Commission Notice, Guidelines on the application of Article 81(3) of the Treaty, [2004] OJ C 101/97, at 90.

7

Short-Term Needs

15. Carriers, and all other service providers in the liner shipping industry, are committed to further improving the efficiency of the already successful global transportation and logistics system.7

16. Clearly, this entails a need to listen to market demands. Our customers’ profitability relies on keeping stock at a minimum level, but at the same time never being short of supply:

• Liner shipping ensures just-in-time delivery and stability of supply, both well-recognized efficiencies;8

• Actions by any one carrier have positive “network externalities”, conferring benefits on customers generally, and not just those customers that use their own service (for example, extra capacity allows for adjustment of existing schedules); and

• Also, customers can reduce their stock, which is a crucial cost saving to allow for “just-in-time” delivery.

17. Current trade data and trends are needed for effective planning of ocean carrier service capabilities. This is a challenging task, which cannot be performed without sufficient knowledge to ensure that all components of the supply chain work effectively together, and to be flexible and find fast solutions in case they do not:

• Liner carriers need to know where the demand is, and where it is likely to be;

• Liner carriers need to know the trades that suffer from over or under capacity in order to deploy their vessels where they are most needed to ensure constantly stable and reliable services across the globe;

• Liner carriers need to know where port and terminal congestion can be expected and need to discuss with all stakeholders how to overcome the problems we face; and

• It is also a benefit to customers to be able to plan in advance, which in turn gives rise to market demand for scheduled services at pre-determined prices.

18. The result would be an efficient adjustment of capacities resulting from efficient independent decisions taken by each carrier. Prices could be affected in so far as the capacity adjustments prevent a capacity shortage and, hence, steeply rising prices in light of a growing demand. This ultimately benefits the shippers and guarantees that vessels are allocated efficiently between different routes. If demand falls, there is no risk that carriers would jointly withdraw capacity, as capacity management falls outside the ELAA Proposal and is explicitly prohibited.

19. The concept of stability of supply and reliability of services is also closely interlinked with environmental issues. Apart from the fact that vessels operating at low utilisation

7 The Commission agrees in its Proposal to repeal Regulation 4056/86: “Maritime transport services are key to

the development of the EU economy”; Proposal for a Council Regulation repealing Regulation (EEC) 4056/86 and amending Council Regulation (EC) 1/2003, COM(2005) 651 final, 14 December 2005, Explanatory Memorandum, at 1. The success of the industry in ensuring sufficient capacity is made available to meet increasing demand whilst investing in innovation and reducing costs is recognised at para 828 of the GI report: “The industry is healthy, and growing; Global Insight, ISL and TU Berlin, The Application of Competition Rules to Liner Shipping, Final Report to DG Comp, 26 October 2005, at 828.

8 See e.g. Regulation 4056/86, [1986] OJ L 378/4, recital 8. For full references of the recognition of benefits of stability in the maritime sector, see ELAA Technical Paper: Precedents Drawn from Case Law Regarding the Concept of Stability, submitted for the Oral Hearing, December 2003. See also Article 81 EC Guidelines, at 68 and 82; and Case 26/76 Metro SB-Grossmärkte v Commission, [1977] ECR 1875; as well as EC Commission Decisions Sicosav [1999] OJ L 004/27; and Whitbread [1999] OJ L 88/26.

8

levels are a waste of resources, in particular port congestion is highly detrimental to the environment for the following reasons:

• Having vessels waiting to call outside a port seriously increases port pollution;

• As a result of port congestion, vessels will have to go at higher speed to keep up with the schedule, again increasing pollution and risk of accidents; and

• As counter-measure to avoid congestion, vessels will call at fewer ports, thereby increasing the need for overland transport, which is drastically less environmentally friendly than sea transport.

20. The system envisaged by the ELAA Proposal should ensure more and better information is available to avoid or at least alleviate such issues.

Long-Term Needs

21. To enable individual carriers to make sound investment decisions, data needs to be put into its market context and inferences for the prediction of future market developments have to be made. Although the task of obtaining and processing accurate and complete data is significant, this forecasting exercise is perhaps the most crucial, and certainly the most challenging, of the whole investment exercise. Many factors need to be taken into account, and these considerations require a complete knowledge of the industry. Allowing experts from liner shipping companies, with additional input from all other stakeholders of the industry within the forums, to engage in discussions on general topics (i.e. discussions of common issues which do not relate to the individual behaviour of carriers) that may influence future supply and demand would enable all participants to develop an accurate and informed view of trade developments. It would also generate substantial savings of cost and time in terms of research, etc. A better understanding of where capacity is needed most – i.e. based on a more accurate forecast of demand – brings significant benefits to carriers, shippers and ultimately consumers in this essentially cyclical industry.

22. The GI Report confirmed what the ELAA has constantly held, that chartering vessels is not an option in times of high demand as in those market circumstances “virtually no vessels are available.”9 The availability of reliable information is critical in order to enable carriers to make sound and efficient individual deployment and investment decisions. The best, and in fact only, source of relevant and useful data must come from carriers, which today happens through the conference secretariats. Should in the future these data providers not have information currently generated by the conferences under Regulation 4056/86, their basis for data analysis would be removed and they would be left with almost nothing (except for volume data on US trades). That would not constitute a useful basis for investment decisions.

Overall Position

23. In sum, all the elements of the Revised ELAA Proposal are needed for carriers in order to provide stability of supply, in particular to:

• Ensure the smooth running of a complex logistics chain;

• Fulfil the service requirements of our customers;

• Improve vessel and container deployment; and

• Make as accurate forecasts as possible of future supply and demand in order to make sound investment decisions (in particular given the size of the investments concerned).

9 Global Insight, ISL and TU Berlin, The Application of Competition Rules to Liner Shipping, Final Report to

DG Comp, 26 October 2005, at 117.

9

24. Our customers – shippers, freight forwarders – have recognized the importance of this type of data gathering and industry consultation, and we believe that the time has finally come for effective participation of all stakeholders in the way the industry is run (a theoretical possibility that was already contained in the old conference system through “consultation”, which works well with many of our major trade partners, e.g. Australia, Japan, South Africa, etc.).

25. The ELAA believes its Revised ELAA Proposal responds to what all stakeholders ultimately demand from a new framework for the liner shipping industry.

26. To achieve the benefits of the envisaged system, it is important that as many carriers as possible join the system contained in the ELAA Proposal. This has also been recognized in shipper responses to the Commission’s White Paper.10

27. A diagram in Annex 5 summarizes the key elements of the proposed system of effective industry-wide consultation. Data exchange and bilateral contacts between carriers, customers, ports, stevedores, etc, go a long way in achieving a market-oriented system of industry-consultation, but they do not go the whole way. Hence, the Revised ELAA Proposal introduces forums for discussions involving all stakeholders, with everyone able to participate: carriers, customers, ports, stevedores, governments, regulators, etc.

3. The Revised ELAA Proposal – Industry-Wide Consultation

28. The Revised ELAA Proposal is set up as an integrated system of industry-wide data exchange and consultation, organized around major regional trading areas and by direction (e.g. Africa, Asia, North and South America, Oceania).

29. Divided into distinct steps, the Revised ELAA Proposal would amount to the following; a detailed description of all steps is contained in Annex 6.

3.1. Step 1 – Carrier Submission to the Independent Data Service (IDS)

Volume Data

30. Figures inputted: The ELAA foresees structuring the submission of data to the IDS in the following way: individual carriers submit a monthly summary of volumes (TEU loadings) per port pair and equipment type to the Independent Data Service (IDS). The “monthly summary of volume” is an aggregation of volumes on a bill of lading port/port basis that were carried by a line during the previous calendar month for all cargo by 20’ dry, 40’ dry and reefer containers carried on a trade in the previous calendar month by direction and port-pair.

31. Timing of input: The data will be inputted to the IDS from individual carriers’ financial databases once a month will cover all completed shipments for a calendar month. However, given the pre-shipment logistics, the length of the voyage and the time required to complete the voyage accounts, the data will naturally be delayed by at least seven weeks before it is even received by the IDS although for most trades, the delay will be one to two weeks longer as a result of the lengthier voyages.

32. The Revised Proposal results in carriers aggregating data to the largest extent possible before submitting to the IDS, so that in effect the only thing the IDS does is aggregate the selected data from all carriers and apply the safety mechanisms against disaggregation (see below at Step 2).

10 Michelin, Comment on the EC Commission White Paper, at p 6.

10

Capacity Data

33. Carriers would enter in a separate spreadsheet their current and forecast capacity per trade and submit to the IDS. The forecast input will only be made quarterly, for quarterly periods over the next 18 months. This data is derived by each carrier on the basis of which vessels are going to be deployed by that carrier on a trade. The capacity figure would come from the nominal quarterly capacity of the vessels to be deployed.

34. The ELAA would like to stress that the envisaged supply forecast and data from the past will only be provided in terms of slots to be provided / that were provided on a trade direction and not by port-pair. The carrier submission of planned future trade capacity to be further aggregated by the Independent Data Service was not specified in the Original ELAA Proposal. There is an increasing demand for accurate information. As is generally accepted, container tonnage is expensive to build and to ensure that the correct amount of space is put on a trade, one needs to look at both supply and likely demand. Otherwise valuable assets in terms of container space might go underused in one trade when they are needed in another, or even worse, there may be undersupply generally or in a particular trade. This goes to the very purpose of the ELAA Proposal, i.e. to ensure the continued stability of supply.

35. The ELAA notes that the Commission has previously allowed for similar supply forecast schemes11 and most trade associations engage in information exchange in some form.

Currency Cost Information

36. The carriers would input, at yearend, the percentage of currencies used for their costs per trade. Example: Carrier X’s would, as soon as the annual figures are available, submit to the IDS the percentage of costs attributable to the Euro, the Great Britain Pound, the Yen, the US Dollar, the Australian Dollar, etc, for each trade. This figure would be updated once a year.

3.2. Step 2 – IDS Processing of Data

37. Based on the carrier input, the IDS will produce two kind of reports:

• A monthly report of aggregated volume and utilisation figures with at least 8 weeks’ delay and a price index (see below at Step 5) covering a quarter with at least 3 months’ delay;

• A quarterly report on aggregated estimated supply figures per trade over the forthcoming 18 months split by quarter. The IDS will not produce a demand forecast; and

• A yearly report on aggregated percentage of cost attributable per currency, per trade or region and per TEU transported. The IDS would aggregate these figures and give them weighting according to the volumes of each carrier on the trade or region in the same time period. The IDS would then produce a “currency basket” which would show the average percentage of each currency attributable for the cost per TEU of the services in the trade or region in question. We refer to Table 3 below, as well as Step 7, where the methodology of currency cost information is further described.

11 For example, see Commission Notice pursuant to Article 19(3) of Council Regulation 17/62 Cartonboard

[1996] OJ C 310/3, at 12, and Commission Notice pursuant to Article 19(3) of Council Regulation 17/62 European Wastepaper Information Service [1987] OJ C 399/7, at 5 and 9. For a detailed discussion on the cases, see Annex 6.

11

38. The IDS – envisaged as a fully independent group of data analysts – would be a separate undertaking contracted by the Liner Shipping Association, which will provide the appropriate software and maintain the database.12

39. The IDS would aggregate the data according to a coherent standard, based on information available in the public domain. ‘Coherent standard’ means that each line would submit information using a template to ensure consistency, i.e. the ‘coherent standard’ will be applied already at the carrier input level. As pointed out by Dynamar in their response to the Commission, there is currently no such ‘coherent standard’ applied worldwide.13

40. The IDS would produce a monthly report for each trade, showing TEU volume and capacity split by 20’ dry, 40’ dry and reefer containers per trade and origin-destination port pair or a range of ports in the same geographic area and a price index per trade leg split by dry and reefer. In terms of methodology of aggregation, supply data will be provided only by trade direction and volume data by trade and port, unless an additional safety mechanism to prevent disaggregation of data as outlined below at para 43 is triggered. In that case, data will be further aggregated by the IDS, by clustering a number of ports in the same geographic area on either or both sides of the trade into a range of ports, such as for example one country or shared hinterland.

41. Splitting data by 20’ and 40’ containers would enable carriers to identify most of their equipment needs without the knowledge of certain commodity volumes and at the same time ensure a high level of aggregation. For reefer containers, 20 foot containers are scarce and on their way out of the market. As a response to DG Comp concerns that a split between 20’ and 40’ reefer containers could help identifying figures of individual carriers or customers, all reefer containers will be aggregated.

42. The IDS would not collect commodity data.

43. The IDS must ensure that the data cannot be disaggregated. Each data point from the IDS will only be provided if the following data aggregation safety mechanisms are fulfilled:

• There are at least four independent operators14 serving the segment which the data point in question relates to;

• The three largest independent operators’ combined share of the segment the data point relates to does not exceed 80 percent;

• Equipment-specific information on North-South trades would only be made available on a total trade (per direction) basis and not on a port pair basis, so as to ensure that individual shipper identities cannot be traced;

• On very thin trades (defined as trades with a total annual volume below 150,000 TEUs in both trade directions), data will not be provided at all or be grouped with a neighbouring trade so that data cannot be disaggregated. The same applies on other trades if data aggregated up to trade level still trigger one of the safety mechanisms; and

12 The IDS will be a small entity, and as requested in the GI Report, “an institution with the highest possible

level of independence”. Its only role will be to aggregate the data in a database, to double-check data which appears to be incorrect (both automatically and manually), to apply the safety mechanisms to ensure sufficient aggregation, etc.

13 Dynamar response to Commission White Paper, at p 3. 14 For the purpose of applying the safety mechanisms only, a carrier participating (in the trade in question) in a

cooperation agreement such as a consortium allowing for information exchange of volumes and capacity would not be considered an “independent operator”. In other words, for those trades where such a cooperation agreement exists, the parties to the cooperation agreement will on the trade in question be viewed as one carrier for the purposes of the application of the safety mechanisms. For that reason, each participating carrier must notify the IDS of all cooperation agreements it has entered into with other carriers that allow for information exchange of volumes and capacity. This is without prejudice to the position that the ELAA strongly maintains that there is significant internal competition between consortium members, and that the internal competition will increase even further with the repeal of Regulation 4056/86.

12

• In addition, the data will only cover specific ports if the port for the preceding year had total TEU liftings of at least 500,000 and is not considered a pure transhipment / relay port (defined as a port with at least 85 percent transhipment).15 Ports with lower volumes will be further aggregated by clustering a number of ports in the same geographic area into a range of ports, such as for example one country or shared hinterland until the aggregate TEU liftings reach the appropriate level.

44. The ELAA refers to the Commission approval of the UK Tractor16 information exchange, where the Commission accepted a rule of minimum three suppliers. With a minimum of four suppliers and the additional safety mechanism ensuring a sufficient dispersion of shares between carriers, a minimum liftings per port and provision of port pair figures broken down by equipment only on the largest trades, the ELAA proposes a safeguard mechanism that goes far beyond Commission practice in UK Tractor, and ensures that data in practice can never be disaggregated.

45. All data provided to carriers will simultaneously be made publicly available. The data flow into and out of the IDS for a sample month as an example of the information provided back to the carriers, to the forum discussion and to data subscribers is provided below in Tables 2, 3 and 4.

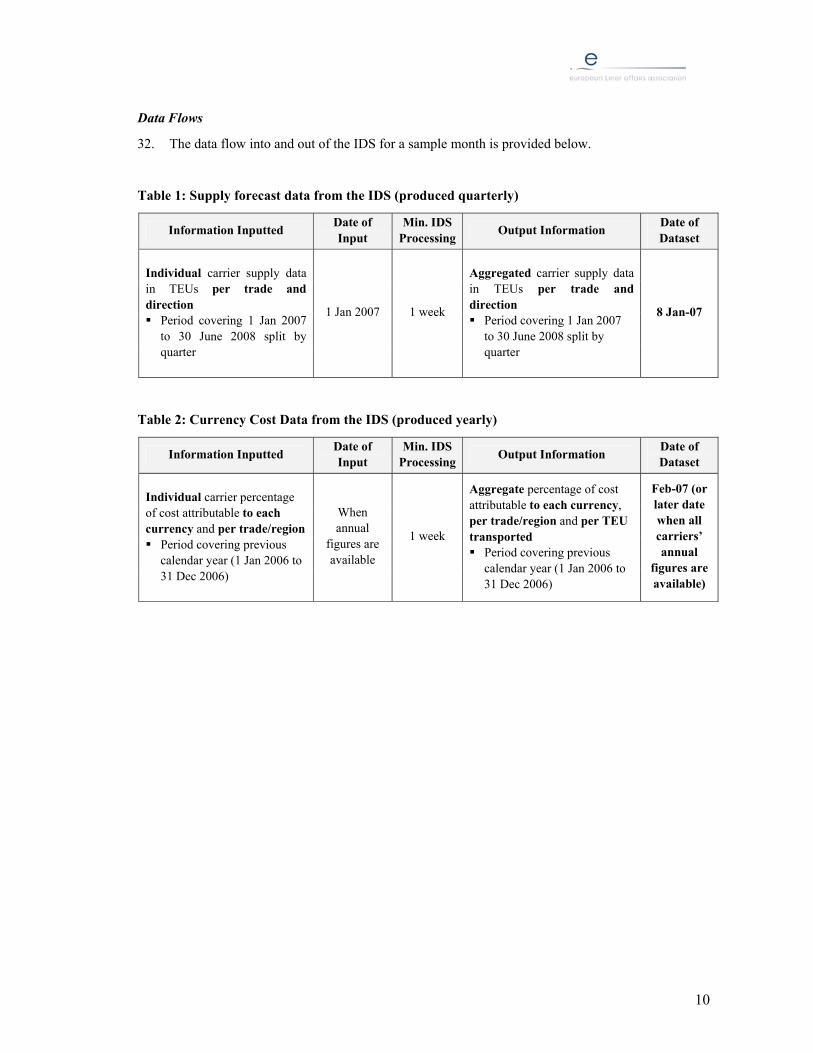

Table 2: Supply forecast data from the IDS (produced quarterly)

Information Inputted Date of Input

Min. IDS Processing Output Information Date of

Dataset

Individual carrier supply data in TEUs per trade and direction Period covering 1 Jan

2007 to 30 June 2008 split by quarter

1 Jan 2007 1 week

Aggregated carrier supply data in TEUs per trade and direction Period covering 1 Jan

2007 to 30 June 2008 split by quarter

8 Jan-07

Table 3: Currency Cost Data from the IDS (produced yearly)

Information Inputted Date of Input

Min. IDS Processing Output Information Date of

Dataset

Individual carrier percentage of cost attributable to each currency and per trade/region Period covering previous

calendar year (1 Jan 2006 to 31 Dec 2006)

When annual figures are available

1 week

Aggregate percentage of cost attributable to each currency, per trade/region and per TEU transported Period covering

previous calendar year (1 Jan 2006 to 31 Dec 2006)

Feb-07 (or later

date when all carriers’ annual figures

are available)

15 Transhipment / relay defined as per Case COMP/JV.55 Hutchison/RCPM/ECT, para 26. 16 UK Agricultural Tractor Information Exchange System; see Commission Competition Report 1999, at p 157.

13

Table 4: Actual data of the past from the IDS (Produced monthly)

Trade Latest Date of

Contract

Min. Pre-shipment

Period

Min. Voyage Period

Min. Post-shipment

Period Information Inputted Min. IDS

Processing

Voyage Completion

Period

Output Information

Date of Dataset

Min. delay

N. Europe – Far East 22 Oct-06 4 weeks 10 weeks

N. Europe – India 22 Oct-06 4 weeks 10 weeks

N. Europe – W. Africa 1 Nov-06 3 weeks 9 weeks

Transatlantic19 8 Nov-06

1 week

2 weeks

4 weeks

Individual carrier port-port volumes from financial data bases in TEUs per port-pair and direction 20’ dry17 40’ dry Reefer

1 week Nov 2006

Aggregated port-port18 volumes in TEUs per port-pair and direction 20’ dry 40’ dry Reefer

8 Jan-07

8 weeks

N. Europe – Far East NA NA NA NA NA NA

N. Europe – India NA NA NA NA NA NA

N. Europe – W. Africa NA NA NA NA NA NA

Transatlantic NA NA NA NA

Individual carrier supply data In TEUs per trade and direction

NA

4th quarter 2006

Aggregated supply data (average per month in the quarter) In TEUs per trade and direction

8 Jan-07

NA

N. Europe – Far East 22 Sep-06 4 weeks 3 weeks 22 Dec-06 3 months

N. Europe – India 22 Sep-06 4 weeks 3 weeks 22 Dec-06 3 months

N. Europe – W. Africa 1 Oct-06 3 weeks 4 weeks 1 Jan-07 3 months

Transatlantic 8 Oct-06

1 week

2 weeks

4 weeks

Average individual carrier $/TEU ocean rate including surcharges and ancillaries, irrespective of ports and equipment, inland excluded 5 weeks

Aug-Oct 2006

Rolling Quarterly Price Index (one index figure per trade direction for whole quarter)

8 Jan-07 3 months

17 For North-South trades, input as well as output per equipment type would be provided on a trade basis only. 18 Or, alternatively, a range of ports in one geographic area, should the port volumes not meet the safeguards against disaggregation (see above at 43 et seq). At present, port-port volumes are

taken from the lines’ financial information. This is the most accurate information currently available, but it is only produced at the end of each voyage, or in some cases round voyages. The projected 10 weeks for the East/West trades, for example, are in line with what we have at the moment.

19 For Transatlantic volumes a faster system is available through the Journal of Commerce statistics.

14

Competition Law Assessment of Steps 1 & 2

46. Steps 1 & 2 amount to the envisaged system of information exchange, on the basis of which carriers can make their individual decisions. As explained in great detail in the ELAA Article 81 EC Assessment, accurate data from the past is a crucial element for capacity planning.20 ELAA Members have identified a need to obtain this information by trade and by port pair. Such a level of detail is required to enable carriers to optimally adjust their capacities to important regional differences in infrastructure (e.g. facilities, feeder operations, access to ports). The carriers need to carefully monitor shifts in demand in different ports, as for example the relocation of a manufacturing plant will need careful planning in advance in respect of carrying capacity, slots, container type, etc. Accurate data is also necessary to match segments of the supply chain – to the benefit of all stakeholders in the industry. The GI Report in the assessment of the Original Proposal found that “[t]he information exchange concept by itself would appear to have possible benefits in terms of efficiency.”21

47. All the data provided would be sufficiently aggregated and delayed, although it is conceivable that carriers will come up with a better system whereby the delay could be reduced to 4 or 5 weeks and the ELAA firmly believes that the IDS should be allowed to publish data as it becomes available, as this kind of information will not influence pricing negotiations and cannot be used as a tool for collusion. The ELAA has previously explained in detail how contracting works in the liner shipping industry.22 What happened in the past is of little relevance for the pricing negotiations, but is crucial for the lines’ management of their business in order to ensure a reliable and efficient service around the globe, with a well-balanced supply and demand situation. The ELAA believes that the Revised ELAA Proposal is sufficiently flexible to deal with market developments.

48. The efficiencies envisaged are created in a manner that will not restrict competition. In order to have all relevant information gathered in an efficient way, one functional data service must have sole responsibility. The use of several data centres naturally leads to incompleteness, or at the very least to inefficient duplication of work. Moreover, as recognized in the GI Report, the publication of data “avoids” or has the capability of “perhaps dulling any collusive utility”.23 The ELAA therefore suggests the creation of a single Independent Data Service to gather the data:24

• The liner shipping market is a knowledge economy and at the moment it is running with insufficient, inaccurate information. Global trade is too important to be left to chance. The shipping industry has a real opportunity to conduct a proper analysis of container cargo moving to and from Europe, with the ability to accumulate timely and accurate port-to-port information for the first time;

• The supply and demand figures are must-haves for carriers in order to provide the services their customers’ demand, i.e. stable supply and reliable, efficient and cheap liner services across the globe. The restrictions of competition, if any, are very limited and definitely not appreciable, as no data will enable the identification of individual carrier strategies; and

20 See in particular paras 595-599. 21 Global Insight, ISL and TU Berlin, The Application of Competition Rules to Liner Shipping, Final Report to

DG Comp, 26 October 2005, at 825. 22 ELAA Article 81 EC Assessment, at 264-307 and in Annex 2 to this submission. 23 Global Insight, ISL and TU Berlin, The Application of Competition Rules to Liner Shipping, Final Report to

DG Comp, 26 October 2005, at 73 and 772. 24 See ELAA Article 81 EC Assessment, at 594.

15

• In addition, the information generated will make the logistic planning of shippers easier, as concluded in the GI Report.25 Shippers will have access to data from the immediate past that will enable them to plan their just-in-time business with the lowest possible inventory without ever being short of supply, which in turn will lead to cost-reductions that are passed on to the end-consumer. The users of liner shipping have a major interest in ensuring that there is better data in the liner shipping market. Several comments on the Commission White Paper confirm that.26

49. As far as currency cost information is concerned, we refer to Step 7 below.

3.3. Step 3 – Industry Specialist Analysis

50. Simultaneously with the carriers and other subscribers, the IDS reports (the monthly volumes and utilisation figures as well as the quarterly supply forecast) will be passed on to an independent group of experts for analysis. The demand data provided to the forecaster by the IDS will amount to the sufficiently delayed volume figures as they become publicly available. The forecaster group could be a university or a consultancy group with industry specialization, which could be selected by an open tender to operate on a time-limited retainer. On a quarterly basis and in advance of the carrier and industry wide consultations, the experts will:

• Compare the data with other statistics available, such as data compiled by industry consultants and others, US FMC data as published by JoC, trade statistics from various industries, etc.;

• Keep track of industry news such as public announcements of capacity increases or withdrawals, regulatory restrictions such as import bans, etc;

• Contact individual carriers and customers with follow-up questions; and

• Based on all the collected information, produce a quarterly report including a supply and demand forecast per quarter over the next 18 months.

51. Both supply and demand would be calculated by trade direction, i.e. not on port level. The final trade definition is yet to be determined, but as a working assumption, trades will be defined in line with EC case law. The main task of the forecaster is to analyze the demand situation in comparison to the supply forecast provided by the IDS, as well as non-member supply. The report will be provided to all members of the Liner Shipping Association for the trades to which they have inputted data, and to whomever subscribes to it. Non-subscribers attending the forum discussions will receive sufficient data for a fruitful discussion; all data will be provided simultaneously to subscribers (from a pick-and-choose menu) on fair, reasonable and non-discriminatory terms.

52. The forecaster is independent, which means naturally its view cannot be ascribed to the carriers. Rather, it is an outsider’s view, which will form the basis for the next step of the Proposal, i.e. the industry-wide consultation, where carriers and transport users will get the opportunity to comment on and improve the independent forecast report, and produce an industry view.

25 Loc cit., at 809, “Additionally, it might provide valuable information for shippers and other interested

parties”. 26 See ELAA Article 81 EC Assessment, at 618 and the responses of Höganäs (at p 5), VA Tech Hydro (at pp 3-

5) and Volkswagen (at p 6).

16

3.4. Step 4 – Consultation

53. The ELAA envisages two integrated forms of consultation in order to improve the prospects for stability of supply in the liner shipping market:

• Meetings between carriers active in a trade; and

• Meetings between carriers and other industry stakeholders in industry-wide trade forums.

54. The carrier consultations are a necessary preparation and a prelude to the industry-wide forums. The carrier consultations as well as the industry wide consultations are envisaged to be quarterly (save for exceptional circumstances such as war risks, major strikes, etc) on big trades and bi-annual on smaller trades. The purpose of both of them is to improve the knowledge of the carriers, the transport users and the other industry stakeholders on the issues facing the industry and the likely development of supply and demand.

Carrier Consultation – Structure and Scope

55. Member carriers will meet quarterly to discuss supply and demand per trade, within the framework of the Liner Shipping Association. Carriers will convene to discuss and interpret the forecast report in preparation for the industry-wide forums.27

56. The consultations would be organised by the Liner Shipping Association and governed by the Liner Shipping Association’s statutes. There could be different consultations per, for example, Europe / Asia, Transatlantic, etc.

57. It is important to state that neither the Liner Shipping Association nor the consultation participants will in any way be involved in the collection of carrier data, and discussions will not touch upon issues such as individual data or strategies, pricing or capacity management. In preparation of the industry-wide consultations, the clear focus of the discussions would be expected demand developments. The carrier consultations are envisaged to:

• Deal with trade-specific and technical issues;

• Security on vessels;

• Major events such as war, strikes, major port congestions and natural disasters;

• Government decisions on above matters to be applied in certain areas; and

• Discuss supply/demand developments.

58. The Liner Shipping Association will publish after each consultation a report on the discussion of the above matters, including comments of the independent forecast report and other industry expert views which normally collect information from carriers but not necessarily deliver correct information. This report will form the basis for the industry-wide forum discussions.

59. The consultations will be facilitated by a representative from the Liner Shipping Association to ensure compliance with its statutes and legal provisions (such as antitrust compliance), and a lawyer will be present at all times. DG Comp will be notified in

27 The GI Report’s main criticism against what were the Trade Committees in the Original Proposal was that

they would act as a “club” and that the only “police” against collusion would be club’s own lawyers. The issue that gave rise to this fear is removed in the Revised ELAA Proposal, as interested industry stakeholders will get access to data and be invited to participate in industry-wide consultation (see below at 60 et seq.) Likewise, there are no discussion on surcharges and ancillary charges, no carrier votes on a forecast report which the GI Report (inaccurately) described as “agreements on common business goals”; Global Insight, ISL and TU Berlin, The Application of Competition Rules to Liner Shipping, Final Report to DG Comp, 26 October 2005, at 709, 793 and 799.

17

advance and on reasonable notice of consultations, and a written report would be submitted to DG Comp after the meeting (DG Comp has declined the ELAA’s suggestion to be invited to attend the meetings).

Industry-Wide Forum Discussions – Structure and Scope

60. Consultation between carriers and other industry stakeholders are envisaged to follow the carrier meetings and provide the necessary customer input to finalise the conclusions of the supply and demand developments. Given the number of participants envisaged, the discussions would be more general, and give shippers and other stakeholders the opportunity to comment on and discuss the forecast reports and the carrier consultation reports. In particular, this would give an opportunity for smaller shippers to hear the industry view and to be heard.

61. The industry acknowledges that consultation with shipper organizations in Europe has not been particularly successful in the recent past, whereas it has been successful in other jurisdictions such as, for example, Australia, Japan, and South Africa. But there is fresh thinking in the industry, and the ELAA submits that the envisaged system of industry-wide consultation is designed to be useful and effective. Recent statements by the ESC and FTA show signs of a new attitude and commitment to make consultation work.28 The ELAA Members are equally committed, and have recently started to engage in extensive consultation with customers to identify the needs and wishes of transport users. That is why the forums together with the carrier consultations have replaced the envisaged Trade Committees in the Original ELAA Proposal. The forums differ significantly from the Trade Committees as they are based on open participation of all industry stakeholders. Obviously, the industry cannot oblige anyone, carriers or other stakeholders, to participate, but the broader the participation, the better for the industry as a whole. The ELAA has during the course of the review of Regulation 4056/86 urged shippers, freight forwarders and their representatives to come forward and explain how they would like consultation to work for the future. Below, we outline how such forums could operate, but this is, of course, also subject to agreement with other industry stakeholders.

Carrier Meetings and Industry-Wide Forums – What Would Not Be Discussed?

62. Neither carrier meetings nor forum discussions would include any of the following items:

• Prices (current, past or future) or discussion on what the price index translates into;

• Individual carrier or shipper future demand;

• Relationship between demand forecasts and individual expectation of the aggregate supply position;

• Any form of capacity management on a trade;

• Current individual carrier capacity utilization;

• Shipper auctions, tenders, individual contracts, etc.;

• Industry views of trade rate development; or

• Surcharges and ancillary charges.

Article 81 EC Assessment of Carrier Consultations

63. The main object of carrier consultation is to refine the independent expert forecast and to achieve better know-how to understand the supply and demand figures in order to

28 Messrs. Filip Beckers, ESC, and Andrew Traill, FTA, Shipper Forum 2005, Hamburg, see Lloyd’s List of 7

October 2005.

18

improve carriers’ knowledge as a better basis for individual decision-taking and crucially in order to improve the prospects for a fruitful industry-wide forum discussion.

64. There will be no discussion of individual data. Hence, the influence on market behaviour resulting from the meetings, once the consultation process including the forum discussions is completed, will be that individual decisions by shippers and carriers are taken on a better informed basis and thus reduce the risk of misinterpretation, which ultimately could lead to disruptions in service and cost increases. All actions will be individual; there will be no joint action.

65. It has been argued that the carrier discussions are unnecessary if there are effective industry-wide consultations. The carrier meetings will be regulated by strict antitrust compliance rules, which will be monitored by a lawyer and DG Comp will be invited to attend. As the carriers will not exchange business sensitive information, there will be no secrecy of the meetings at all. The reason why the ELAA believes that industry-wide consultations must include carrier meetings is three-fold:

• First, as preparation for the industry-wide forums. Shippers at the industry-wide forums will ask for a common industry position. This may not be possible, but at least carrier meetings in advance of the forums may serve to avoid confusing messages because of different industry forecasts. The problem with analyst reports is that even if carriers and analysts have the same data, analysts tend to come up with different results.29 Carriers need to discuss why there is such a difference. Carriers will also have different views internally, but will make an effort to come up with a consensus.

• Secondly, there are limits to how many people can join a discussion before it loses its focus. The ELAA does not believe that a fruitful meeting to interpret a forecast report is possible in an open-to-all meeting; and

• Thirdly, there is a clear risk that a forum discussion on the forecast could break down into discussions between individual carriers and individual customers when both carriers and customers are participating. This must be avoided as it is not the purpose of the meeting, and would risk distracting from the main point of the meeting, which is a discussion on what has happened and might happen on a trade.

66. Narrowing down the inherently speculative element of investment by providing carriers with a proper foundation to forecast supply and demand is an efficiency which is difficult to quantify. However, one can only imagine the cost for society in the case of insufficient liner shipping capacity in the world.30

• Carriers would not be able to satisfy all shippers’ needs for transportation, leading to high rates and the exclusion of customers that could otherwise be served;

• Cargo would not move, or would move very slowly and at a very high rate;

• Moreover, manufacturers would need to consider moving manufacturing facilities to otherwise less cost-efficient locations, if that were at all possible; and

• Undertakings would not be able to sustain “just-in-time” or similar type manufacturing and distribution models which depend on the availability of regular and predictable logistics services, of which liner shipping is a key component.31

29 The FEFC predictions of demand developments have over time been significantly more accurate than other

information providers’ forecasts. Illustrative examples can be found when comparing the FEFC forecasts to Drewry in May 2005, the GI and the FEFC predictions for 2005.

30 The reverse situation would also be very serious. The continuation of globalization would be seriously impeded with irreparable damages to developing countries and overall trade.

31 See ELAA Response to the DG Comp consultation paper of 18 June 2003, at 9.

19

67. Another objection against the need for carrier consultation has been that given the improved data exchange envisaged by the ELAA Proposal, there would be no need to further interpret the data. Nothing could be more wrong. The information provided by the IDS for the first time provides a clear view of the recent past of the industry, on which the forecaster will base its predictions. But it does not mean that the crystal ball for the future is clear. There are still significant uncertainties about the future.

68. The carrier consultations are therefore creating additional efficiencies to the industry which are indispensable to the attainment of stable liner shipping service in all European trades.

Article 81 EC Assessment of Forum Discussions

69. Various participants in the wider transport community require accurate, regular, and reliable information to assist them in the development and management of transport infrastructure and planning. Within the context of expanding world trade, increasing transportation infrastructure capacity challenges and complex supply chains, it is in the future incumbent on the liner industry to provide a forum in which these matters can be discussed and understood and in which accurate assessments shared with interested parties.

70. The demand for and use of accurate trade data is increasingly important as international shipping and logistics grows and becomes more complex, as the efficient flow of international trade becomes even more important to the European economy, and as transportation infrastructure challenges to the effective and efficient management of supply chains proliferate. Accurate and reliable trade information requires the collective input, analysis and understanding of the wider industry.

71. Shippers, freight forwarders, government, Commission, ports – all stakeholders collect useful information that determine supply & demand for liner shipping – which (if appropriately aggregated) adds further knowledge to the platform; normally the meeting would not be open to the public.

3.5. Step 5 – Price Index

72. Furthermore, the ELAA understands that shippers, freight forwarders and carriers alike, as well as Governments and research institutions, wish to have a historical benchmark of how prices have been developing. The ELAA believes that the envisaged price index (as contained in the Original ELAA Proposal) could fulfil that need if provided directly from the IDS to the industry stakeholders participating in the trade forum.

73. Carriers will submit their average revenue per TEU (i.e. there will be no port-specific pricing data), defined as all charges on the carriers’ bills of lading (including surcharges and ancillary charges) except charges for inland haulage), per trade to the IDS. The average revenue will be calculated using a template and the information will stem directly from carriers’ individual financial data bases. The IDS will collect all the prices and calculate a simple index per trade direction. The index would be published monthly but with a minimum delay of three months. An important change compared to the Original ELAA Proposal is that the price index will not be split by dry and reefer. Moreover, the index will cover a whole quarter rather than a month only, which means that the index will be based on figures between three and six months old, as suggested by the Commission consultants in the GI report.32 Such an index, which does not show any specific prices at all and hence does not enable carriers to identify even past strategies of

32 Global Insight, ISL and TU Berlin, The Application of Competition Rules to Liner Shipping, Final Report to

DG Comp, 26 October 2005, at 774.

20

competitors, cannot be anything other than compatible with EC competition law. The main reasons for this are the following33:

• The data is sufficiently delayed. How prices moved a quarter ago will not influence either spot or contract pricing negotiations – as recognised by DG Comp’s consultants;34

• The data is aggregated from at least three independent operators but in the vast majority of cases from numerous independent operators;

• The index produced by the IDS will not refer to any amount in currency (i.e. no US$ amounts, etc.), and it will not be split up by equipment type, commodity, region or port. It will be the summary of numerous pricing points of a carrier on each port pair, multiplied by the number of port pairs served and the number of carriers. It will include all elements of the rates apart from the inland leg(s), i.e. ocean freight rates, surcharges and ancillary charges;

• The only split that will be made is by trade direction (westbound/eastbound or northbound/southbound). Given significant imbalances of trades, such a split is necessary to provide relevant aggregate information; and

• The price index would also be made available to shippers and the wider public.

74. A price index constructed in this way cannot be used to facilitate collusion. The GI Report found that “it is doubtful whether a price index can be used as a good monitoring variable”, and that “consumers (shippers) may to some extent benefit, in this instance, perhaps dulling any collusive utility to some extent”.35 In the Revised TACA decision,36 the Commission held that the exchange of commercially sensitive information concerning prevailing prices is compatible with Article 81 EC if there is a sufficient level of aggregation of data and the individual data is disclosed neither to other members of the agreement nor to the secretariat, but only to an independent third party.37

3.6. Step 6 – Public Information Regarding Cost Elements Related to Liner Shipping

75. The Original ELAA Proposal suggested that carriers after discussion with shippers should agree on joint formulae for surcharges and ancillary charges. Despite what the ELAA conceives are significant benefits of such formulae through operational and administrative efficiencies and order in the terminals, DG Comp has consistently held during the discussions with the ELAA that such formulae would amount to price recommendations and would not be acceptable under EC competition law. Although the ELAA contests this finding, it has substantially changed its proposal and abandoned the envisaged formulae concerning cost elements related to liner shipping. This Revised Proposal merely envisages the following Liner Shipping Association activity in relation to cost elements related to liner shipping:

• The publication of the general terminal cost elements, for transparency and reference for shippers and carriers alike in individual negotiations of Terminal Handling Charges (THCs);

• The publication of the bunker cost and consumption that is already publicly available; and

33 See further ELAA Article 81 EC Assessment, at 49, 165 et seq. and 604-605. 34 Global Insight, ISL and TU Berlin, The Application of Competition Rules to Liner Shipping, Final Report to

DG Comp, 26 October 2005, at 68. 35 Global Insight, ISL and TU Berlin, The Application of Competition Rules to Liner Shipping, Final Report to

DG Comp, 26 October 2005, at 762 and 772. 36 Revised TACA [2003] OJ L 26/53, Commission Decision of 14 November 2002. 37 Loc cit., at para 71.

21

• Port charges and canal dues on trades to and from Europe, i.e. publicly available information on the charges due to carriers, for transparency and reference for shippers and carriers alike in individual negotiations of appropriate pass-on of these charges.

76. There will be no more agreement or even discussion between carriers on cost elements related to liner shipping under the ELAA Proposal. They will not form part of the carrier consultations or the forum discussions. The ELAA believes this may have unsettling effects on business, some of which can be overcome by at least ensuring transparent information of the cost elements behind this charges, so that shippers will understand what the charges are based on and negotiation of the charges will be founded on knowledge and not on speculation. In the following, the ELAA outlines the risks of total abolition of THCs and BAFs and how these to some extent could be overcome by increased transparency of cost factors.

THCs

77. THCs reflect a pure cost element. Conference THCs in Europe have in fact remained unchanged in Europe for the last 6-7 years, despite an increase in average terminal handling costs levied on the carriers. Today conference carriers only charge the shippers 80 percent of their terminal handling costs38 by way of THC and pay the remaining 20 percent out of the ocean freight revenue that they earn.

78. The idea behind a rule like the 80/20 rule is to make a fair split between the land and the sea part of the charge. The 80/20 split is based on the agreement between conferences and shipper association of 1989 (the CENSA agreement, see Annex 7), where the elements of the terminal costs were listed and defined as 24 items (plus some extra items for special containers and dangerous goods), out of which three items were attributed to the carrier39 and two split equally between carriers and shippers.40

79. The advantages of publishing the general terminal cost elements are significant:

• It is the perception of the industry that customers do not wish to negotiate and pay this charge individually to the stevedore, and the THC pass-on has therefore been seen as a negotiation service from the carriers, in particular to smaller customers against a consolidated and congested stevedore market with significant bargaining power.41 For this reason, the Commission did not object to joint fixing of the charges. In addition, carriers pay the full terminal handling cost upfront and give shippers a credit period of approximately 60 days; and

• By abolishing the 80/20 split carriers will have to negotiate individually with each shipper and there may be different rules applying to different shippers, resulting in a much more cumbersome procedure in the terminals and less control of the location of containers in the terminals. Some carriers may decide that it is not worthwhile to provide this service and credit period to shippers, and let each shipper deal with the terminals individually. This will potentially create chaos in the terminals, where each shipper will need to track its container from gate to vessel.

38 A charge per TEU corresponding to 80 percent of the average TEU cost of the conference members in that

port and on that trade. 39 Move of container from ship’s rail into ship’s cell (including ship’s hold or deck), opening and closing of the

hatch covers including unsecuring and securing, and movement of hatch-covers from bay to bay or to quayside and v.v as well as the lashing of the container.

40 Physical and clerical terminal planning, etc, as well as overtime or public holiday extra working costs. 41 Even in 2002, when the stevedores were less concentrated, the Commission recognized in its Revised TACA

decision that “[t]ransport users, particularly those with only small volumes to be shipped, may benefit from this situation as carriers will generally have greater bargaining power vis-à-vis terminal operators and will be able to negotiate a price that is substantially lower than that which might have been obtained by the shipper”; Revised TACA, [2003] OJ L 26/53, Commission Decision of 14 November 2002, at para 96.

22

80. In sum, abolition of the conference THC risks to create uncertainty in ports and significant bargaining power for the large shippers and terminal operators to the detriment of smaller players. This will likely lead to less efficient terminal handling, a more complex security clearance, higher risk of dislocation of cargo, higher and more volatile THCs and foreclosure of smaller actors. Admittedly, the solution in this Revised ELAA Proposal does not cover all these risks, but at least it will provide greater clarity and transparency of the charges currently levied upon carriers by the terminal operators. This will hopefully lead to a smoother negotiation of the level of the THCs or integration of THCs in the freight rate, and hence better chances for a continuation of efficient handling of goods port terminals.

Cost of Bunkering Vessels

81. Under the terminology used today, the cost of bunkering vessels is generally regulated in contracts by Bunker Adjustment Factors (BAFs). BAFs are adjustment factors for bunker costs. The purpose of BAFs is to hedge the risks for sharp fluctuations in bunker cost for carriers as well as transport users, which will serve to mitigate fluctuations in the overall freight rate. Today, the conference BAFs are a calculation of the increase or decrease in fuel cost per TEU on the trade in question, calculated on a formula based on a start date, average fuel price and average consumption per carried TEU. Based on this, the increase or decrease in the fuel price is calculated. Hence, the BAF is not always a positive charge, but an adjustment factor (that can be a negative charge) to take into account the fluctuation in fuel price.

82. There is no BAF equivalent in the ELAA Proposal. However, the ELAA anticipates a need for shippers and carriers alike of transparency in the calculation of costs of bunkering vessels. The ELAA therefore anticipates to publish regularly the price of fuel over time (IFO 180 and 380) in the most common locations for bunkering (essentially Rotterdam in Europe and key bunkering locations on the other leg of the European trades), as well as publicly available information on average fuel consumption for different standard vessel types so that an average cost per TEU can be calculated. This will increase transparency as to the cost of fuel, and facilitate individual negotiations of compensation for fluctuating bunkering costs.

3.7. Step 7 – Cost of Currency

83. Under the terminology used today, the currency risks of liner shipping are generally regulated in contracts by Currency Adjustment Factors (CAFs). CAFs are adjustment factors for currency costs. The purpose of CAFs is to hedge the risks for sharp fluctuations in currency costs for carriers as well as transport users, which will serve to mitigate fluctuations in the overall freight rate. For the convenience of transport users, carriers traditionally charge their customers in US dollars. However, the cost basis of carriers is generally more influenced by other currencies. Naturally, the spread of costs would be different on different trades and regions. This means that carriers need to hedge against the considerable currency risks they are facing due to the fluctuation of the US dollar. Just like the BAF, the CAF is not always a positive charge, but an adjustment factor (that can be a negative charge) to take into account the fluctuation of the US dollar in a more transparent and fair way than merely building the currency risk into the freight rate.

84. There is no CAF equivalent in the ELAA Proposal. However, the ELAA anticipates a need for shippers and carriers alike of transparency in the calculation of currency costs. The ELAA therefore envisages publishing the fluctuation of the US dollar compared to the average percentage attributed to each currency per TEU on a trade or region. The system would work in the following way (see also Table 3 above):

23

• Carriers input to the IDS the average percentage of costs in the trade or region in question attributable to each currency for the previous year;

• The IDS aggregates the percentage figures as soon as they become available (usually when all carriers have completed their annual accounting), and gives them a weighting corresponding to the volumes carried in the trade or region by each carrier in the previous year (usually the volume figures will since long be made public before the closing of each participating carrier’s annual accounts);

• Based on this information, the IDS can calculate an average attribution per currency and TEU on a trade or region. This information, a “currency basket”, will be produced annually and be placed in the public domain by the Liner Shipping Association without delay;

• The Liner Shipping Association would then continuously monitor the fluctuation between the US dollar and the “currency basket”, provided as a percentage of the revaluation or devaluation of the US dollar in relation to the “currency basket”, as a plus or minus figure compared to a historic reference point;

• The percentage figure would provide transport users and carriers alike better knowledge of the importance of currency fluctuations in future individual contract negotiations.