revision of the spa3 risk management and ... - beyond charts revision of s… · the spa3 risk and...

TRANSCRIPT

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 1 of 239

Revision of the SPA3 Risk Management and Money Management Rules

Contents 1 Executive Summary ................................................................................................................... 4

2 Transitioning to the SPA3 Revised Position Sizing ....................................................................... 5

2.1 Global Portfolio System (GPS) ............................................................................................ 5

2.1.1 SPA3 Parameters ........................................................................................................ 5

2.1.2 SPA3 Scan ................................................................................................................... 5

2.1.3 Actions to take ........................................................................................................... 6

2.2 SPA3 TradeMaster.............................................................................................................. 6

2.2.1 Actions to take ........................................................................................................... 6

2.3 SPA3 Public Portfolios ...................................................................................................... 11

3 Objectives of the SPA3 Revision Project ................................................................................... 12

4 It all starts at the Trading Plan ................................................................................................. 12

5 Catch 22 – the major problem all investors face ....................................................................... 13

6 Where to start the revision process? ....................................................................................... 14

7 Research Environment ............................................................................................................. 15

8 Revised Risk Management and Money Management Rules in SPA3 ......................................... 17

8.1 Position Sizing calculation ................................................................................................ 17

8.2 Portfolio Risk as a Master Control .................................................................................... 18

9 Portfolio Limits and Boundaries ............................................................................................... 19

9.1 Different SIROC parameters ............................................................................................. 19

9.2 An introduction to Box Plots ............................................................................................. 20

9.3 Portfolio Limits using SIROC 21 8 ...................................................................................... 21

9.3.1 $25,000 Portfolios .................................................................................................... 21

9.3.1.1 Comments ............................................................................................................ 21

9.3.2 $100,000 Portfolios .................................................................................................. 22

9.3.2.1 Comments ............................................................................................................ 22

9.3.3 $400,000 Portfolios .................................................................................................. 23

9.3.3.1 Comments ............................................................................................................ 23

9.4 Portfolio Limits using SIROC 13 5 5 – Close immediately ................................................... 23

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 2 of 239

9.4.1 $25,000 Portfolios .................................................................................................... 23

9.4.1.1 Comments ............................................................................................................ 24

9.4.2 $100,000 Portfolios .................................................................................................. 24

9.4.2.1 Comments ............................................................................................................ 24

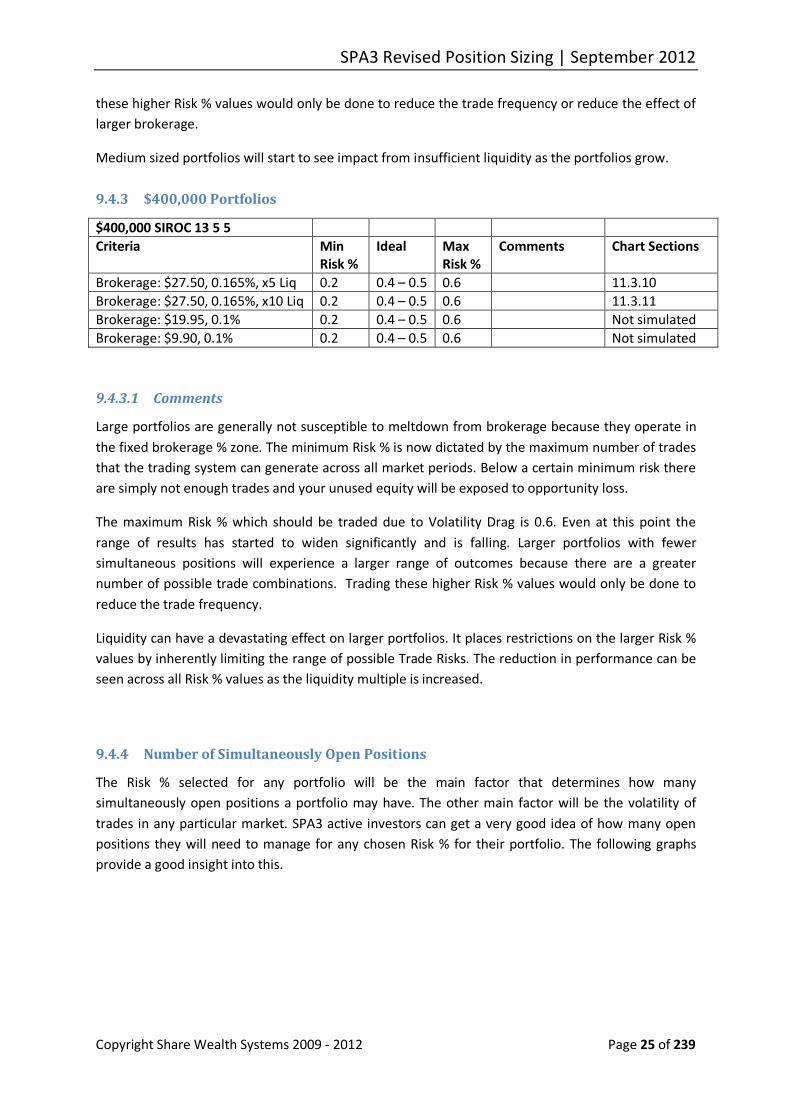

9.4.3 $400,000 Portfolios .................................................................................................. 25

9.4.3.1 Comments ............................................................................................................ 25

9.4.4 Number of Simultaneously Open Positions ............................................................... 25

10 Exploratory Simulation ......................................................................................................... 27

10.1 Introduction ..................................................................................................................... 27

10.2 Extent of exploratory simulation research ........................................................................ 29

10.3 Research period ............................................................................................................... 30

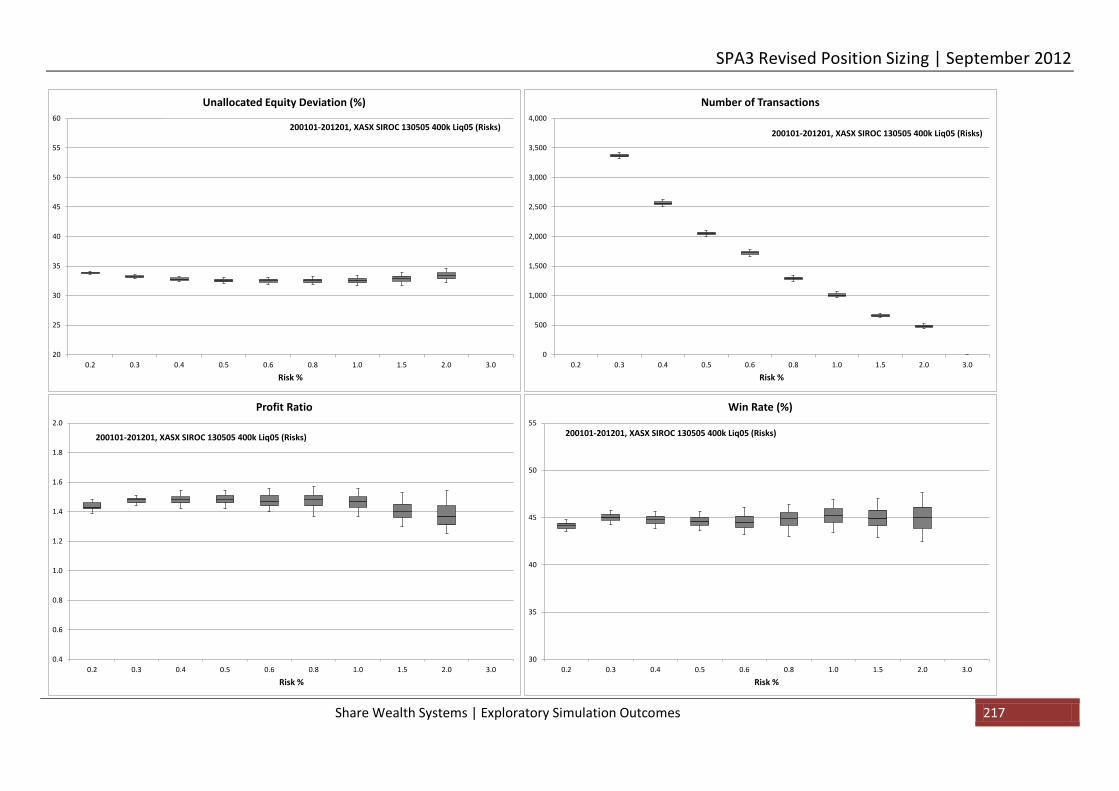

11 Exploratory Simulation Outcomes ........................................................................................ 31

11.1 Introduction ..................................................................................................................... 31

11.2 Portfolio Simulated Equity Curves and Box Plots for SIROC 21 8 ....................................... 35

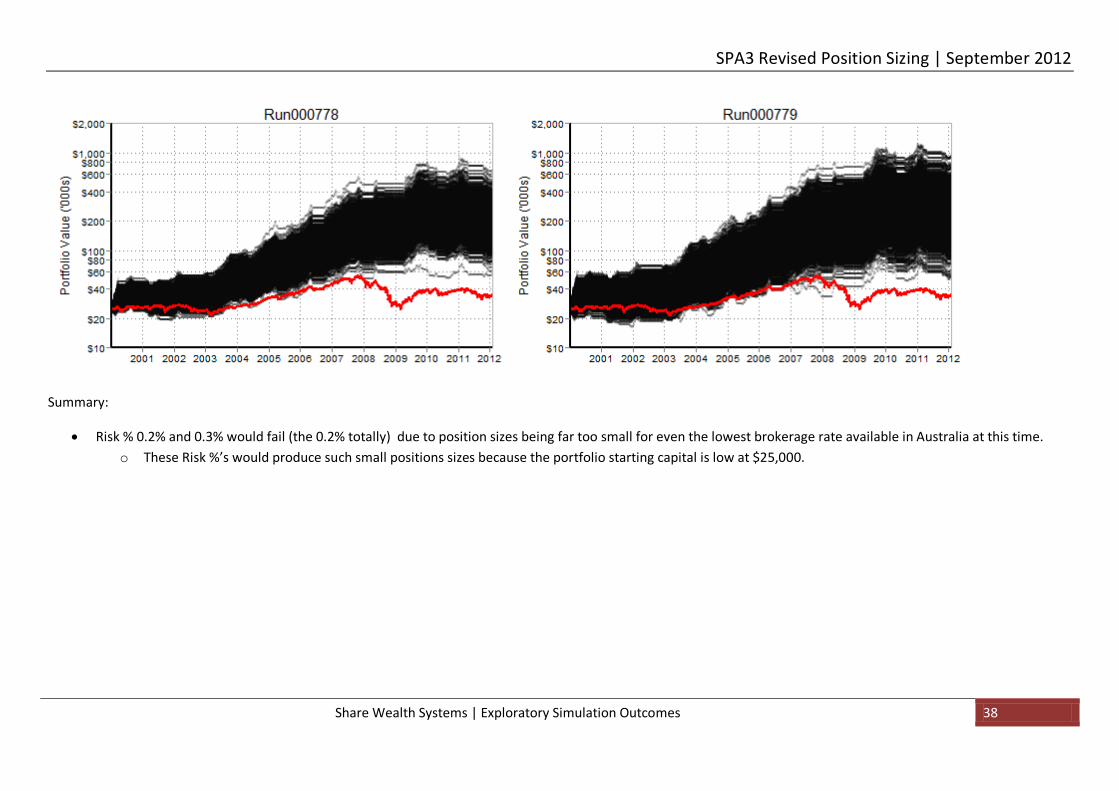

11.2.1 25k Charts: SIROC 2108, No Liquidity Check, $9.90 or 0.1% Brokerage ...................... 35

11.2.2 25k Charts: SIROC 2108, x5 Liquidity Check, $9.90 or 0.1% Brokerage ....................... 41

11.2.3 25k Charts: SIROC 2108, x10 Liquidity Check, $9.90 or 0.1% Brokerage ..................... 47

11.2.3.1 Individual Equity Curves & Underwater Equity Curves ....................................... 53

11.2.4 100k Charts: SIROC 2108, No Liquidity Check, $27.50 or 0.165% Brokerage .............. 61

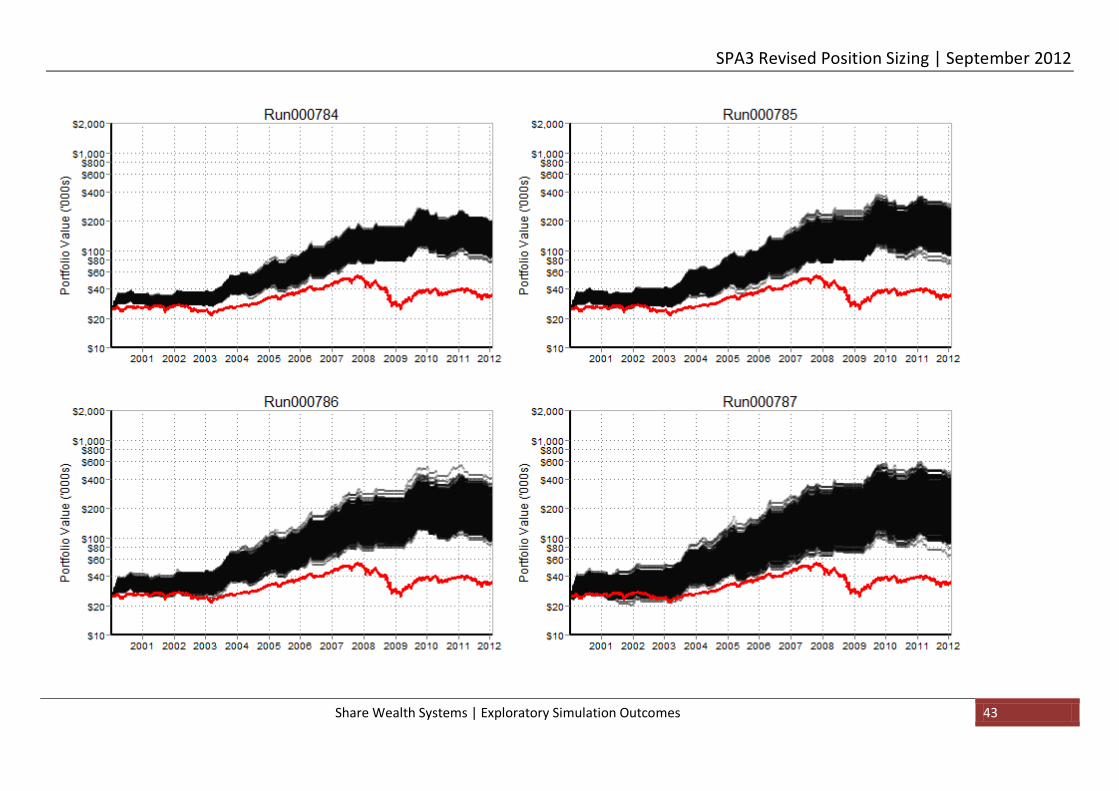

11.2.5 100k Charts: SIROC 2108, x5 Liquidity Check, $9.90 or 0.1% Brokerage ..................... 67

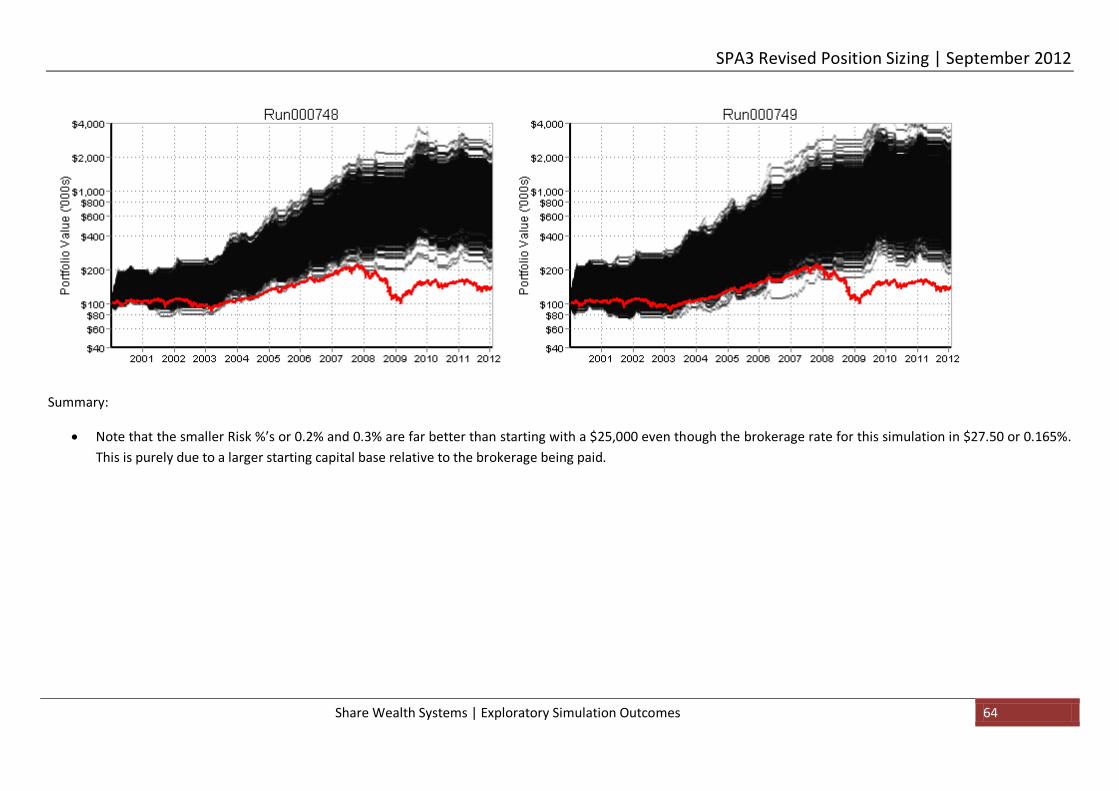

11.2.6 100k Charts: SIROC 2108, x5 Liquidity Check, $27.50 or 0.165% Brokerage ............... 74

11.2.6.1 Individual Equity Curves & Underwater Equity Curves ....................................... 80

11.2.7 400k Charts: SIROC 2108, x5 Liquidity Check, $27.50 or 0.165% Brokerage ............... 90

11.2.7.1 Individual Equity Curves & Underwater Equity Curves ....................................... 96

11.3 Portfolio Simulated Equity Curves and Box Plots for SIROC 13 5 5 – Close immediately .. 100

11.3.1 25k Charts: SIROC 130505, No Liquidity Check, $9.90 or 0.1% Brokerage ................ 100

11.3.2 25k Charts: SIROC 130505, x10 Liquidity Check, $27.50 or 0.165% Brokerage ......... 106

11.3.3 25k Charts: SIROC 130505, x10 Liquidity Check, $19.95 or 0.1% Brokerage ............. 112

11.3.4 25k Charts: SIROC 130505, x10 Liquidity Check, $9.90 or 0.1% Brokerage ............... 118

11.3.4.1 Individual Equity Curves & Underwater Equity Curves ..................................... 124

11.3.5 100k Charts: SIROC 130505, No Liquidity Check, $27.50 or 0.165% Brokerage ........ 129

11.3.6 100k Charts: SIROC 130505, x5 Liquidity Check, $27.50 or 0.165% Brokerage ......... 132

11.3.7 100k Charts: SIROC 130505, x10 Liquidity Check, $27.50 or 0.165% Brokerage ....... 138

11.3.8 100k Charts: SIROC 130505, x5 Liquidity Check, $9.90 or 0.1% Brokerage ............... 144

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 3 of 239

11.3.9 100k Charts: SIROC 130505, x10 Liquidity Check, $9.90 or 0.1% Brokerage ............. 150

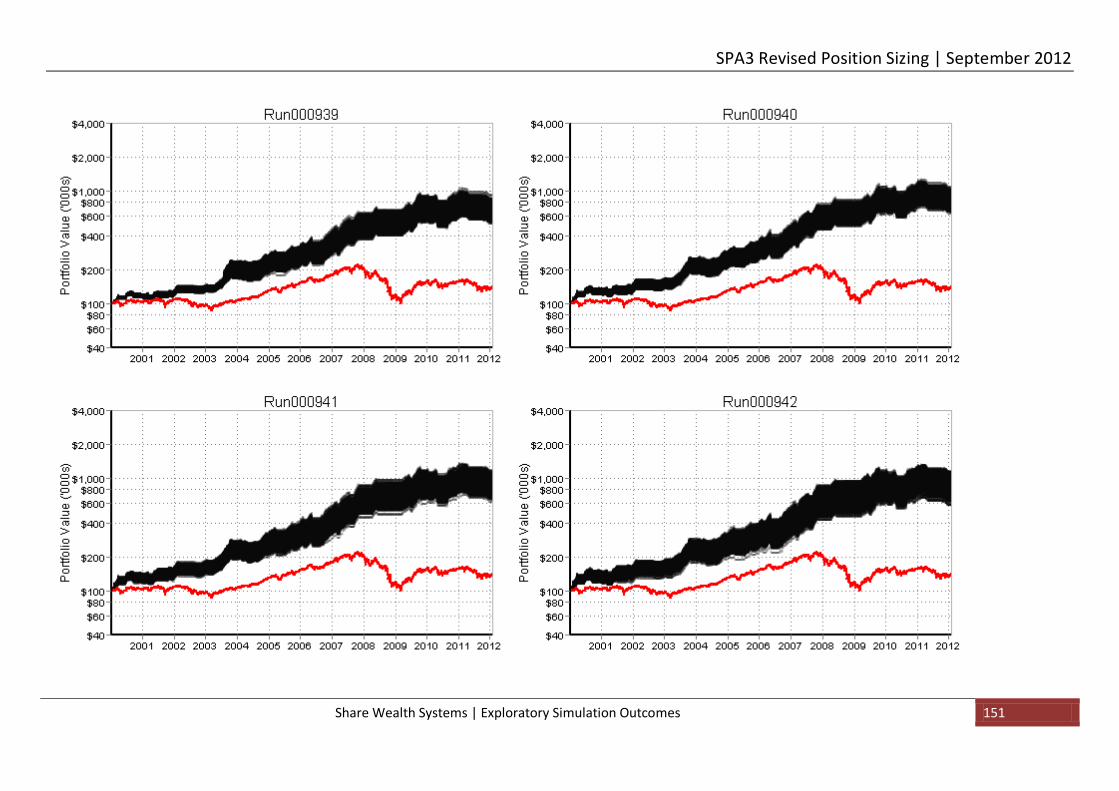

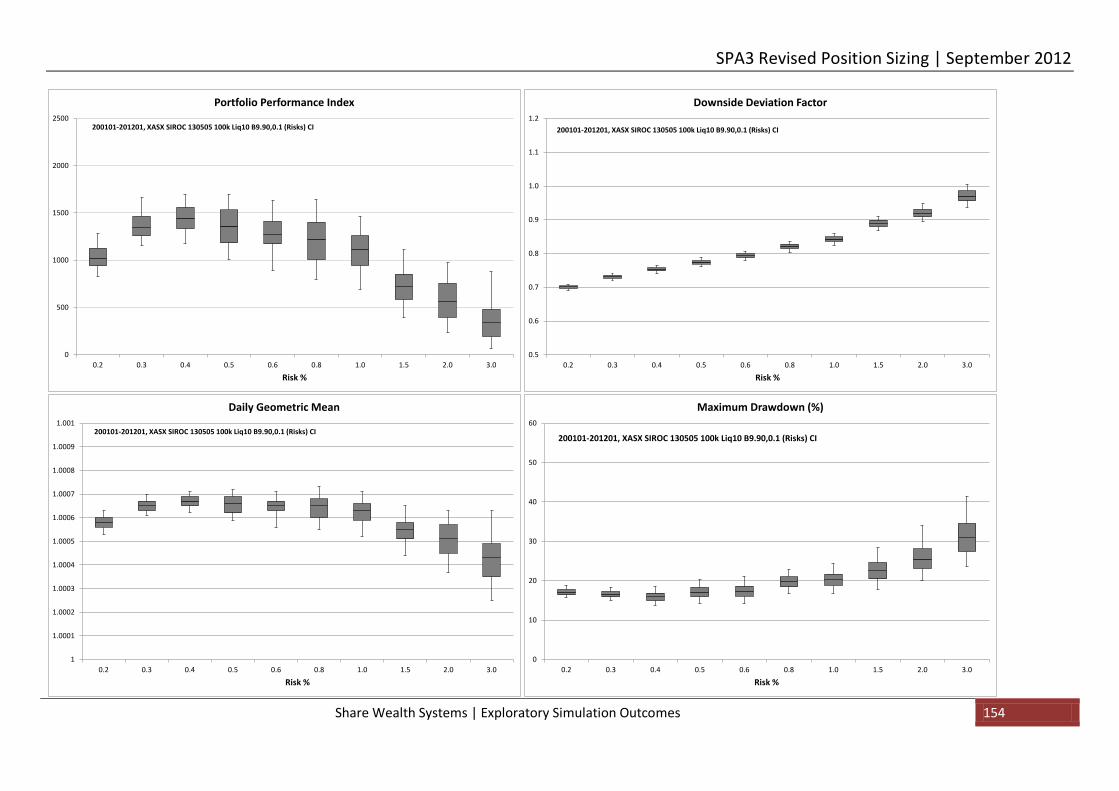

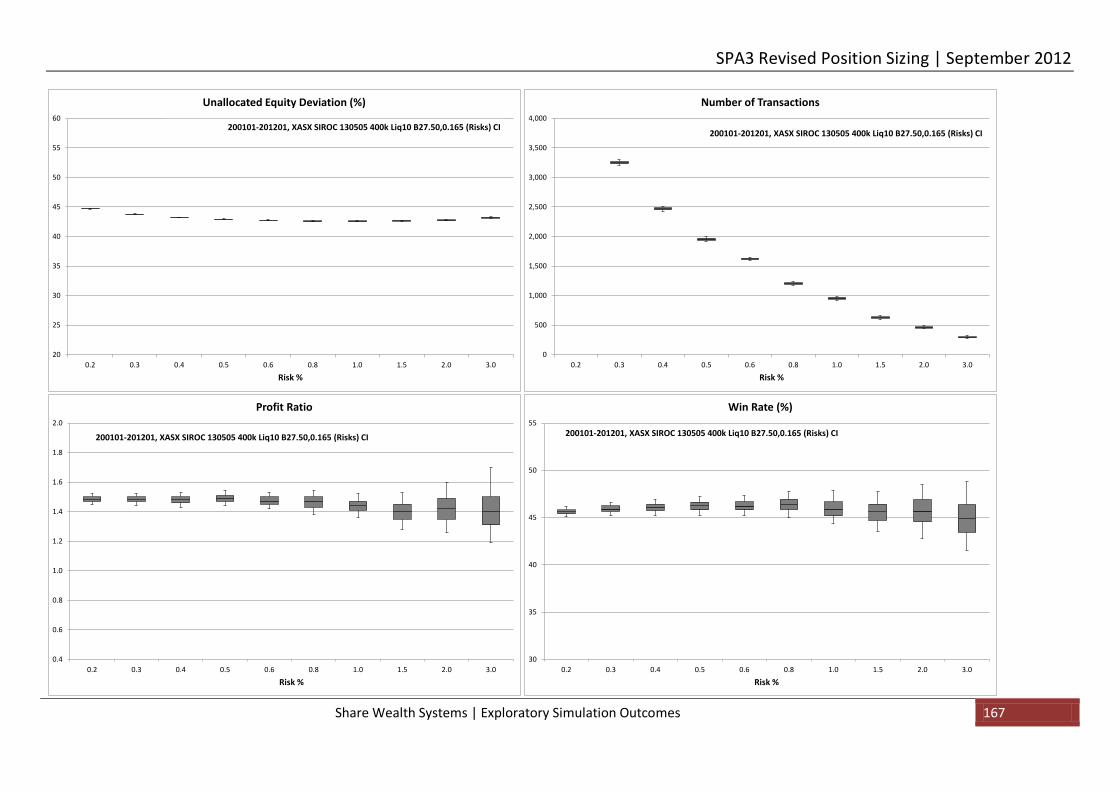

11.3.10 400k Charts: SIROC 130505, x5 Liquidity Check, $27.50 or 0.165% Brokerage ..... 156

11.3.11 400k Charts: SIROC 130505, x10 Liquidity Check, $27.50 or 0.165% Brokerage ... 162

11.4 Portfolio Simulated Equity Curves and Box Plots for SIROC 13 5 5 – Leave trades open .. 168

11.4.1 25k Charts: SIROC 130505, x10 Liquidity Check, $27.50 or 0.165% Brokerage ......... 168

11.4.2 25k Charts: SIROC 130505, x10 Liquidity Check, $19.95 or 0.1% Brokerage ............. 173

11.4.3 25k Charts: SIROC 130505, x10 Liquidity Check, $9.90 or 0.1% Brokerage ............... 178

11.4.3.1 Individual Equity Curves & Underwater Equity Curves ..................................... 184

11.4.4 100k Charts: SIROC 130505, x5 Liquidity Check, $27.50 or 0.165% Brokerage ......... 188

11.4.5 100k Charts: SIROC 130505, x10 Liquidity Check, $27.50 or 0.165% Brokerage ....... 194

11.4.6 100k Charts: SIROC 130505, x5 Liquidity Check, $9.90 or 0.1% Brokerage ............... 200

11.4.7 100k Charts: SIROC 130505, x10 Liquidity Check, $9.90 or 0.1% Brokerage ............. 206

11.4.8 400k Charts: SIROC 130505, x5 Liquidity Check, $27.50 or 0.165% Brokerage ......... 212

11.4.9 400k Charts: SIROC 130505, x10 Liquidity Check, $27.50 or 0.165% Brokerage ....... 218

12 Exploratory Simulation Summary ....................................................................................... 224

13 White Paper Summary ....................................................................................................... 225

14 Acknowledgements............................................................................................................ 227

15 References ......................................................................................................................... 227

16 Appendix A - Single Profit Stop ........................................................................................... 228

17 Appendix B - Volatility Drag................................................................................................ 231

17.1 A real world example ..................................................................................................... 231

17.2 Why is the actual return different to the average return?............................................... 231

17.3 Sorry to tell you but it gets worse ................................................................................... 233

17.4 The effect at a trade level ............................................................................................... 234

17.5 The effect at a portfolio level ......................................................................................... 235

18 ADDENDUM 1 - Position Sizing Formula Example ............................................................... 237

18.1 Determining the Trade Risk % ........................................................................................ 237

18.2 Different trades, same risk ............................................................................................. 238

18.3 Smaller Portfolio Risk, less loss. ...................................................................................... 239

18.4 Conclusion ..................................................................................................................... 239

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 4 of 239

1 Executive Summary This paper provides an update to the SPA3 methodology. It contains the details of a major revision to the SPA3 risk and money management rules. These risk and money management changes follow on from the changes released in the SPA3 Revised Edge White Paper in December 2011.

This paper will be best put into context by first reading the SPA3 Revised Edge White Paper published in December 2011, if that paper has not yet been read. Most of the research information provided in the December 2011 White Paper is not repeated here, but where relevant for emphasis, some has been.

This paper provides detail on:

1. The processes conducted in the research project for revising the SPA3 risk and money management rules.

2. The outcomes of the risk and money management research. 3. Suggested position size boundaries for trading small ($25K), medium ($100K) and large

($400K) portfolio sizes with SPA3. 4. One minor change to the Revised SPA3 Edge Profit Stop which now displays only one Profit

Stop following two or more consecutive SPA3 signals instead of multiple Profit Stop signals in these scenarios.

Much evidence is provided to show the improvements in the SPA3 risk and money management rules. This is demonstrated by providing graphical and statistical outputs for a number of different portfolio scenarios.

Some of the information may be too detailed for some. For those you need go no further than section 9 on page 19 where the suggested position sizes boundaries are provided. And then read the summary sections, 12 and 13, at the conclusion of the paper.

For those that wish to delve deeper we have provided plenty of detail. View the detail in this paper almost as a ‘database’ of simulation results. Ultimately we believe that all active investors should grasp the type of material provided in this paper to instil the necessary belief with which to execute a chosen method in an uncertain and probabilistic environment such as the financial markets. By this we mean any method, not just SPA3.

In the December 2011 White Paper on the SPA3 Revised Edge, SWS introduced the concept of exploratory simulation to our customers. Exploratory simulation is the backbone of the research conducted to produce this White Paper and to conclude the necessary improvements to the SPA3 position sizing rules.

We believe that the type of and level of research provided in this paper is unprecedented in the arena of equities trading for private investors the world over, let alone Australia. And thus, with the release of this research, we hope to raise the standard of research that any systems provider or money manager the world over provides for their products.

We commend this White Paper and its contents to our customers.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 5 of 239

2 Transitioning to the SPA3 Revised Position Sizing Before getting into the research aspects of the paper itself, we provide upfront what the SPA3 user must do to implement the SPA3 revised risk and money management rules. The transition to the revised rules is a choice and therefore some manual actions are required by you.

2.1 Global Portfolio System (GPS)

2.1.1 SPA3 Parameters

Within GPS you will notice two high level changes in the Parameters panel to support the revised SPA3 risk and money management rules. These changes are:

1. The default parameter profiles have been renamed: a. ‘Default ASX Profile’ is now ‘Default XASX SIROC 21:08’. b. ‘Default JSE Profile’ is now ‘Default XJSE SIROC 21:08’.

Any Scan or chart that used the old names will be automatically updated. No manual action is required.

2. Several new SPA3 default parameter profiles have been added: a. Default XASX SIROC 19:07 b. Default XASX SIROC 17:07 c. Default XASX SIROC 13:05

Only the profiles relevant to your SPA3 product will be shown. For example, XASX only customers won’t see the XJSE profile, and vice versa.

All these default profiles correspond with the new Risk tables in TradeMaster.

2.1.2 SPA3 Scan

It is important to note:

1. There have been no changes to any Parameter profiles or Scan profiles that you created, and 2. That no changes are required to your daily SPA3 scan process.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 6 of 239

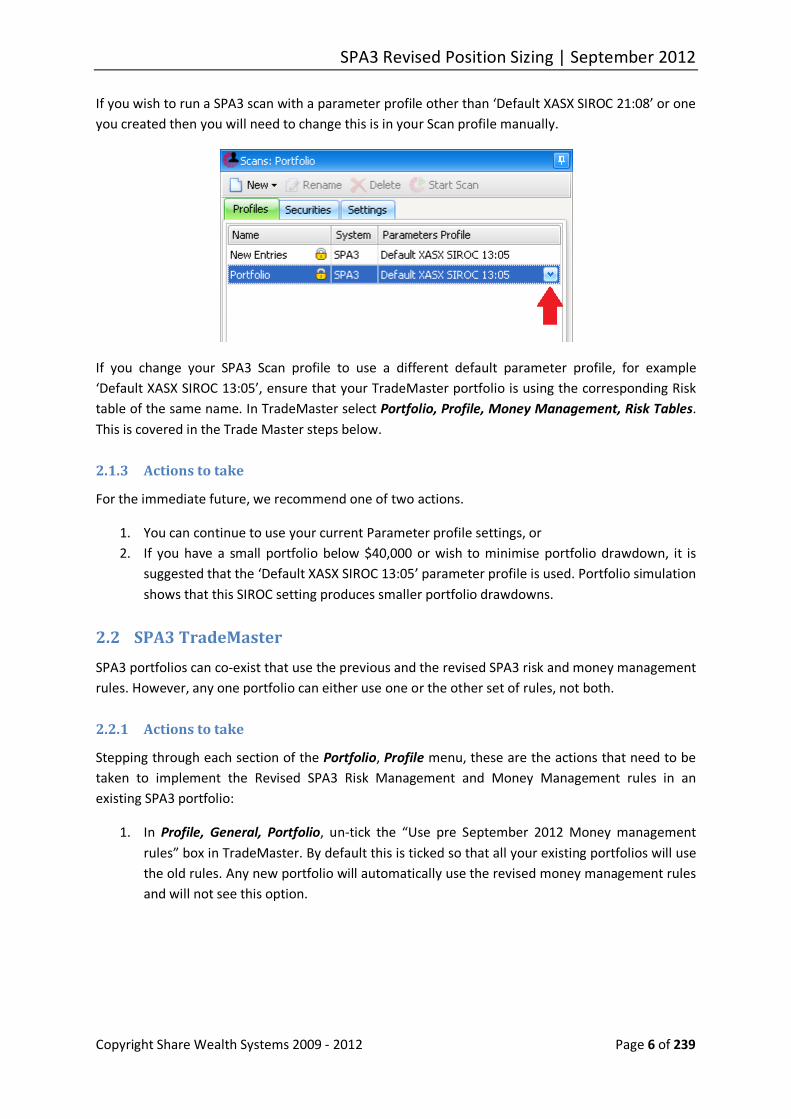

If you wish to run a SPA3 scan with a parameter profile other than ‘Default XASX SIROC 21:08’ or one you created then you will need to change this is in your Scan profile manually.

If you change your SPA3 Scan profile to use a different default parameter profile, for example ‘Default XASX SIROC 13:05’, ensure that your TradeMaster portfolio is using the corresponding Risk table of the same name. In TradeMaster select Portfolio, Profile, Money Management, Risk Tables. This is covered in the Trade Master steps below.

2.1.3 Actions to take

For the immediate future, we recommend one of two actions.

1. You can continue to use your current Parameter profile settings, or 2. If you have a small portfolio below $40,000 or wish to minimise portfolio drawdown, it is

suggested that the ‘Default XASX SIROC 13:05’ parameter profile is used. Portfolio simulation shows that this SIROC setting produces smaller portfolio drawdowns.

2.2 SPA3 TradeMaster

SPA3 portfolios can co-exist that use the previous and the revised SPA3 risk and money management rules. However, any one portfolio can either use one or the other set of rules, not both.

2.2.1 Actions to take

Stepping through each section of the Portfolio, Profile menu, these are the actions that need to be taken to implement the Revised SPA3 Risk Management and Money Management rules in an existing SPA3 portfolio:

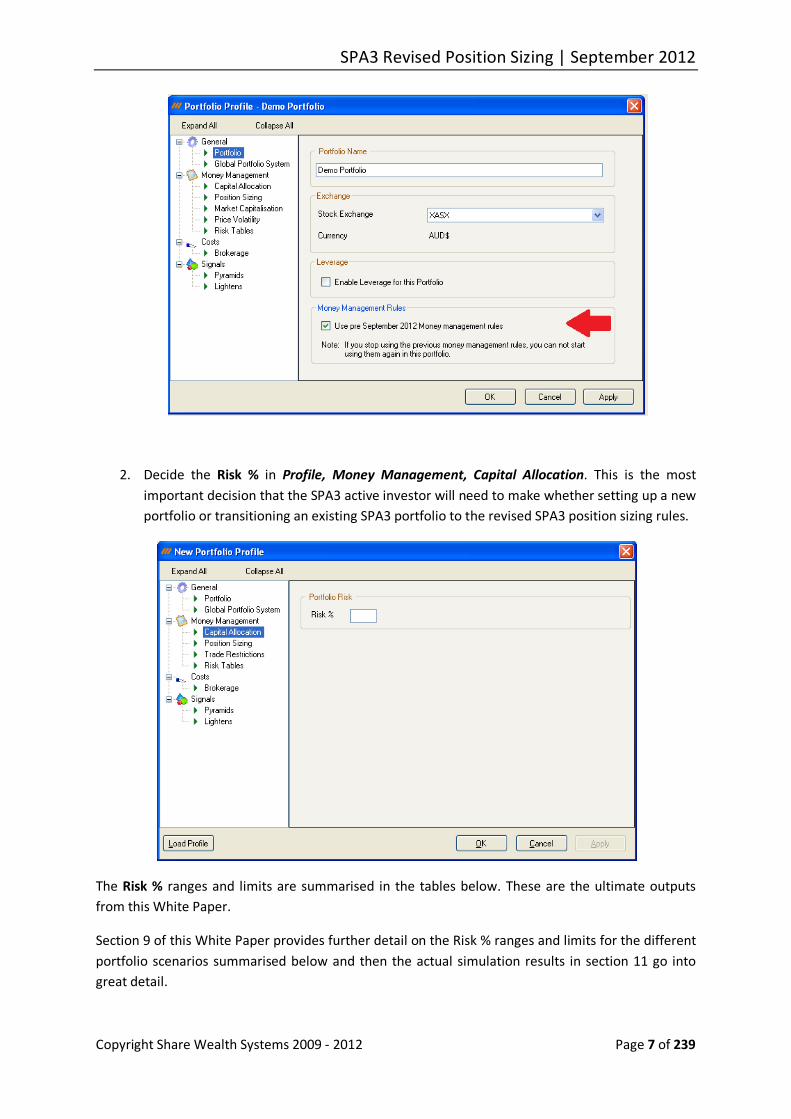

1. In Profile, General, Portfolio, un-tick the “Use pre September 2012 Money management rules” box in TradeMaster. By default this is ticked so that all your existing portfolios will use the old rules. Any new portfolio will automatically use the revised money management rules and will not see this option.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 7 of 239

2. Decide the Risk % in Profile, Money Management, Capital Allocation. This is the most important decision that the SPA3 active investor will need to make whether setting up a new portfolio or transitioning an existing SPA3 portfolio to the revised SPA3 position sizing rules.

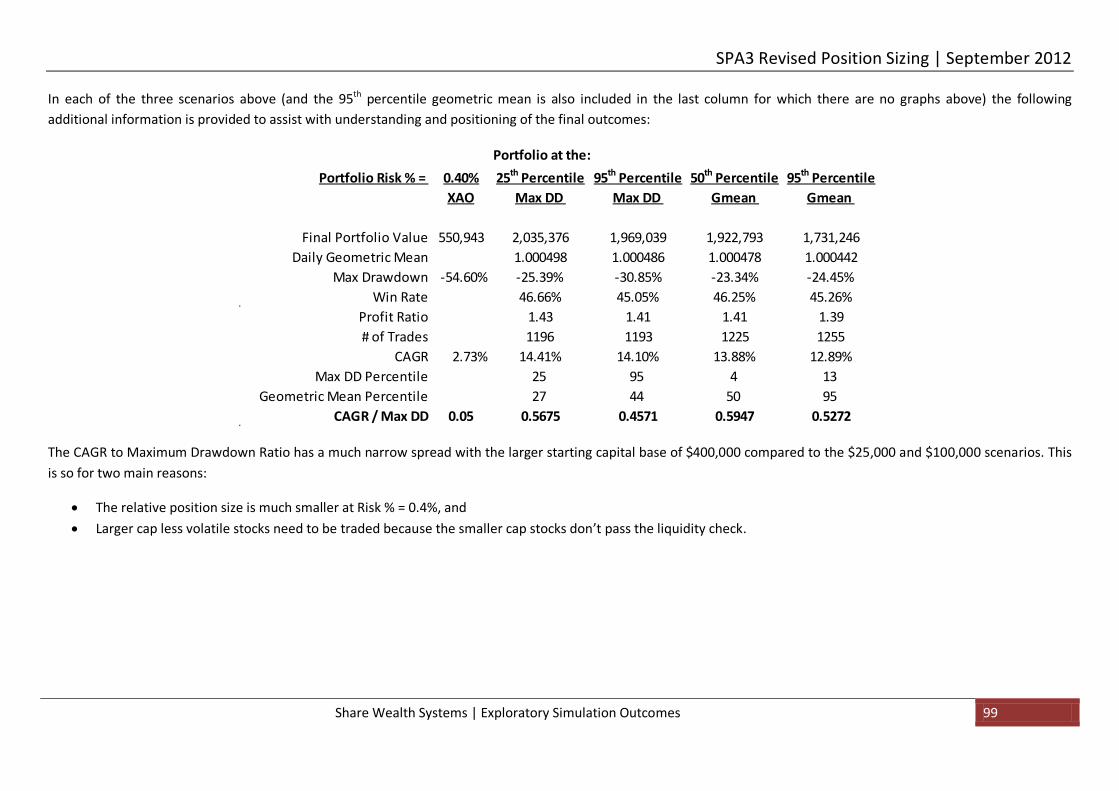

The Risk % ranges and limits are summarised in the tables below. These are the ultimate outputs from this White Paper.

Section 9 of this White Paper provides further detail on the Risk % ranges and limits for the different portfolio scenarios summarised below and then the actual simulation results in section 11 go into great detail.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 8 of 239

It is recommended that a Risk % is selected in the range provided in the [Ideal] column. The start and end of the Ideal range are inclusive.

Portfolios using SIROC 21 8

$25,000 SIROC 21 8 8 Criteria Min

Risk % Ideal Max

Risk % Comments Chart Sections

Brokerage: $9.90, 0.1%, x5 Liq 0.5 0.6 – 1.5 1.5 11.2.2 Brokerage: $9.90, 0.1%, x10 Liq 0.5 0.8 – 1.2 1.5 11.2.3

$100,000 SIROC 21 8 8 Criteria Min

Risk % Ideal Max

Risk % Comments Chart Sections

Brokerage: $9.90, 0.1%, x5 Liq 0.3 0.5 – 0.8 1.0 11.2.5 Brokerage: $19.95, 0.1% 0.4 0.5 – 0.8 1.0 Not Simulated Brokerage: $27.50, 0.165%, x5 Liq 0.4 0.5 – 0.8 1.0 11.2.6

$400,000 SIROC 21 8 8 Criteria Min

Risk % Ideal Max

Risk % Comments Chart Sections

Brokerage: $27.50, 0.165%, x5 Liq 0.2 0.4 - 0.5 0.6 11.2.7 Brokerage: $19.95, 0.11% 0.2 0.4 - 0.5 0.6 Not simulated Brokerage: $9.90, 0.1% 0.2 0.4 – 0.5 0.7 Not simulated

Portfolios using SIROC 13 5 5

$25,000 SIROC 13 5 5 Criteria Min

Risk % Ideal Max

Risk % Comments Chart

Sections Brokerage: $27.50, 0.165% None None None Not recommended 11.3.2 Brokerage: $19.95, 0.1% 0.8 0.8 – 1.0 1.5 11.3.3 Brokerage: $9.90, 0.1% 0.4 0.8 – 1.2 1.5 11.3.4

$100,000 SIROC 13 5 5 Criteria Min

Risk % Ideal Max

Risk % Comments Chart Sections

Brokerage: $27.50, 0.165%, x5 Liq 0.3 0.4 – 0.8 1.0 11.3.6 Brokerage: $27.50, 0.165%, x10 Liq 0.3 0.4 – 0.8 1.0 11.3.7 Brokerage: $19.95, 0.1% 0.3 0.4 – 0.8 1.0 Not simulated Brokerage: $9.90, 0.1%, x5 Liq 0.2 0.3 – 0.5 1.0 11.3.8 Brokerage: $9.90, 0.1%, x10 Liq 0.2 0.4 – 0.6 1.0 11.3.9

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 9 of 239

$$400,000 SIROC 13 5 5 Criteria Min

Risk % Ideal Max

Risk % Comments Chart Sections

Brokerage: $27.50, 0.165%, x5 Liq 0.2 0.4 – 0.5 0.6 11.3.10 Brokerage: $27.50, 0.165%, x10 Liq 0.2 0.4 – 0.5 0.6 11.3.11 Brokerage: $19.95, 0.1% 0.2 0.4 – 0.5 0.6 Not simulated Brokerage: $9.90, 0.1% 0.2 0.4 – 0.5 0.6 Not simulated

There is no wrong answer if a Risk % is selected in the ranges in the Ideal column above. If you wish to be far more specific then the portfolio simulation outcomes in section 11 should be consulted but initially this is not mandatory.

As a rule of thumb, if you wish to minimise drawdown then choose at the lower end, if you wish to maximise growth then choose at the higher end of the Ideal range but understand that larger position sizes are more sensitive to trading errors and to randomly selecting trades with poorer outcomes.

It is likely that you have a portfolio that is between the three starting values of $25,000, $100,000 and $400,000 chosen for simulation. A dose of common sense and erring towards a lower rather higher Risk % within the Ideal range should keep the SPA3 active investor on the straight and narrow. The Risk % can be changed at any time during the life of a portfolio.

3. Decide Market and Sector Risk settings in Profile, Money Management, Position Sizing.

The settings above will reflect the following risk management approach:

a. Risk Profile 1 - “When Market Risk is HIGH” reduces position sizes by 100%, i.e. no trade, for High and Low sector risk trades.

b. High Sector Risk trades will get a full position size because they are reduced by 0%. This is the setting that was used during all the simulations in this White Paper.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 10 of 239

Other settings can be selected. For example, if you wished to reduce the position size of a trade that has high sector risk, the bottom left quadrant should be changed to 33.33% of 50%, which ever you wish to reduce the position size by.

4. Decide the ATRVE volatility levels and minimum liquidity multiple that will be traded in Profile, Money Management, Trade Restrictions.

a. The default ATRVE levels of 1 to 12 that were used for the portfolio simulations in this paper are shown below.

b. To reduce portfolio equity curve volatility and hence potentially reduce drawdown the ATRVE levels could be narrowed down to, say, 1.5 – 2 for the minimum value and 4.5 – 5 for the maximum value. Refer to the December 2011 White Paper entitled “SPA3 Revived Edge” (which can be accessed from the GPS Help menu) for a detailed breakdown of the SPA3 raw edge by ATRVE volatility level.

c. The portfolio simulations used liquidity multiples or 5 and 10. A multiple in between can be used. A rule of thumb is that the smaller the portfolio value the higher liquidity multiple that can be used and the larger the portfolio the smaller the liquidity multiple should be but remember that the lower the multiple the bigger the liquidity risk that the active investor takes.

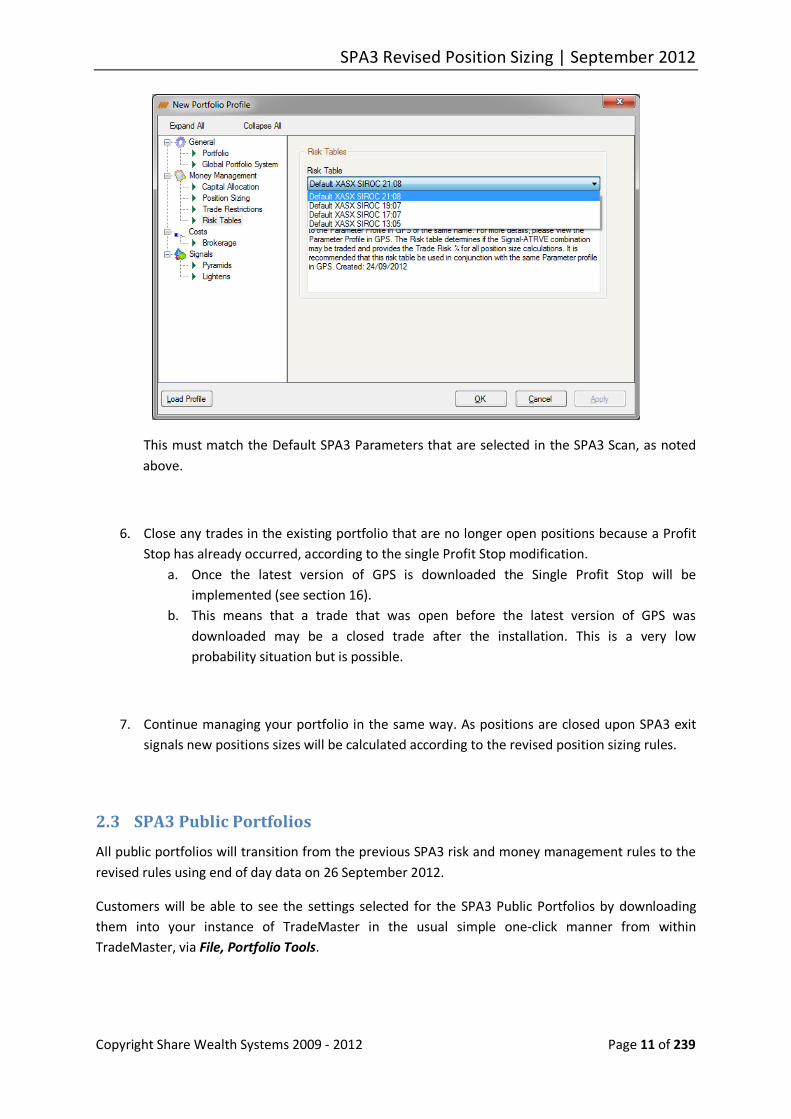

5. Select the SIROC default profile for your portfolio in Profile, Money Management, Risk Tables. Note the instructions in the Description box.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 11 of 239

This must match the Default SPA3 Parameters that are selected in the SPA3 Scan, as noted above.

6. Close any trades in the existing portfolio that are no longer open positions because a Profit Stop has already occurred, according to the single Profit Stop modification.

a. Once the latest version of GPS is downloaded the Single Profit Stop will be implemented (see section 16).

b. This means that a trade that was open before the latest version of GPS was downloaded may be a closed trade after the installation. This is a very low probability situation but is possible.

7. Continue managing your portfolio in the same way. As positions are closed upon SPA3 exit signals new positions sizes will be calculated according to the revised position sizing rules.

2.3 SPA3 Public Portfolios

All public portfolios will transition from the previous SPA3 risk and money management rules to the revised rules using end of day data on 26 September 2012.

Customers will be able to see the settings selected for the SPA3 Public Portfolios by downloading them into your instance of TradeMaster in the usual simple one-click manner from within TradeMaster, via File, Portfolio Tools.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 12 of 239

3 Objectives of the SPA3 Revision Project As SPA3 is an existing methodology, objectives had to be set for the revision project. These were set back in March 2011 and communicated to our customers in May 2011 via an eUGM, in the December 2011 White Paper and are repeated here.

The first and main objective was to improve performance. Improving performance has a number of inter-related objectives. In fact, all the objectives stated below, including the second and third objectives, lead to achieving this objective. The obvious performance measurements are:

• Increased returns, and

• Reduced drawdown.

These are achieved by improved timing, particularly exit signals, and by improved risk and money management.

The second objective was to improve the flexibility of SPA3 risk management and money management. This included:

• being able to start trading with the SPA3 methodology with starting capital as low as $10,000, and

• having a range of portfolio level risk management rules and associated money management rules that could support many and varied customised trader risk profiles from the very risk averse to the risky.

The third objective was to improve tradability. The aim is that it would become easier psychologically to trade with SPA3 regardless of previous trading experience or of the trader’s risk profile. This would be achieved through more sensitive exit signals and through greater flexibility with the risk management rules at the portfolio level, especially when first starting a portfolio.

We believe that all these objectives have been met, bar one that is met partially. Due to the mandatory cost of minimum brokerage we believe that actively trading a medium term methodology with as little as $10,000 with an unleveraged equities only strategy is not advisable. Whilst $20,000 or even $15,000 may just be OK for unleveraged equities trading with the position sizing model we have put forward in the paper with the minimum possible brokerage rate, as little as $10,000 may have to be left to the domain of leveraged trading to be able to make some headway without paying all the profits to a broker.

4 It all starts at the Trading Plan The content of a SPA3 trader’s Trading Plan is well documented in the SPA3 Getting Started Manual, the Education Centre in the SWS Members Zone and in the SPA3 Reference Manual.

The section of the Trading Plan that states the trader’s objectives is the Goals and Objectives Statement. This is the “what” section of the Trading Plan, what returns the active investor would like to achieve and within what risk constraints she / he would like to achieve these returns. There are three key areas of objectives:

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 13 of 239

• Reward objectives. These are the periodic returns that a trader would like to achieve. Whilst actual returns achieved will depend on the performance of the market being traded, setting reward objectives helps determine the risk and money management rules that will be deployed. Also, if more than one methodology is being traded then setting reward objectives helps determine what instruments and markets should be traded and whether leverage should be used or not.

Your objective is more achievable if stated in terms of the market you are trading; for example, X% outperformance.

• Risk objectives. This is the maximum drawdown that one is prepared to endure in any single trading period. This could set parameters for when to reduce position sizes so as to remain within this drawdown objective or set a “shut-off” valve as to when to cease trading until the market returns to Low Risk or is once again in sync with your systems(s), as measured by a set of pre-determined researched criteria.

You may think that risk is related to the maximum amount of money you wish to lose. And it can be. You may put this in % terms.

But your benchmark should be your base reference. You are at the mercy of the market you are trading. For example, the All Ordinaries or the ASX200 or the ASX300; the

S&P500; the Nasdaq Composite or the Nasdaq 100.

You outperform the market by rising by more and by not falling as much.

• Skills objectives. This is a set of objectives to achieve skills-based targets with respect to mindset, trade execution, market environment understanding, trading understanding, journaling, practicing of trading and any other that you may wish to set. A schedule could be included here (or the next section of your Trading Plan) that details the books to be read, courses to attend, DVD’s to watch, Blogs to follow, internet research to be done, etc to achieve your skills objectives.

The inclusion of a risk objective is a key part of the SPA3 Trading Plan as this objective will be strongly tied to each individual’s choice and deployment of particular risk and money management rules in live trading.

5 Catch 22 – the major problem all investors face What position sizing approach a trader uses to trade is directly linked to the trader’s risk objective and reward objective that they state in their Trading Plan.

The Catch 22: how does a trader know in advance what position sizing approach to use to remain within their risk objective while also have a high probability of achieving their reward objective?

Answer: they don’t. Well, nearly every trader doesn’t.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 14 of 239

Stating a risk objective is easy enough, just state a number, like 20% maximum drawdown. Now what? Too large a position size will probably rush the trader to a maximum drawdown limit very quickly thereby taking the trader out of the opportunity flow that the market offers. Too small a position size might ensure that the maximum drawdown limit is never reached but also ensure that the reward objective is also never met.

How is this Catch 22 resolved? Using exploratory simulation. Let’s get into it.

6 Where to start the revision process? As discussed above in the Trading Plan section, ultimately the two main outcomes that a trader would like to control is the degree of risk (drawdown) and the degree of reward that they would like to achieve in their portfolio within the constraints of:

• How much capital they have to trade with. • How much time they have to devote to the trading process. • What their risk profile is, measured mainly by how much drawdown they can tolerate. • Their trading methodology (includes trading system, risk management and money

management). • The brokerage paid for each transaction relative to the individual position and potential

reward on offer, i.e. average return per trade. • The liquidity of the market that they trade relative to their trading capital. • The level of their trading psychology and skill.

We know that in any decent sized sample of active investors there will be a diverse range of maximum drawdown tolerance ranging from < 10% to as much as 60%. However, most of this same sample would use similar position sizes and risk management criteria in their trading, despite having very different methodologies and very different drawdown tolerance levels. This is so for two main reasons, because:

• most books contain similar suggestions about money management, e.g. the 2% and 6% rule, and

• there are very few sufficiently functional portfolio level risk and money management tools available and those few are priced above the range that the great majority would be prepared to pay for such functionality. Also, most retail investors wouldn’t have the knowledge to research to this level because it simply is not discussed in popular main stream books, i.e. we don’t know what we don’t know.

So if the two main outcomes that a trader needs to control is their level of portfolio drawdown and their portfolio returns, what is the main determinant that controls these two outcomes? The answer is: the risk and money management controls that are used for each individual trade and for their overall portfolio. The position size is THE biggest determinant of size of outcomes, both positively and negatively.

To be able to achieve one’s reward objectives whilst remaining within one’s risk objective constraints becomes the main balancing act that a trader needs to manage on an ongoing basis.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 15 of 239

This means that a trader requires as much flexibility as possible with their risk and money management rules to have the confidence to increase and reduce position sizes (even to $0) as required to increase returns without overstepping their stated risk objective, found in their Trading Plan Objectives Statement.

The degree of flexibility that a trader can have with their risk and money management rules is determined by the variation of individual trade outcomes. When combined with risk and money management rules, this leads to the degree of variation of potential portfolio equity curve outcomes, in terms of return AND drawdown. This is a key, possibly THE key statement in this paper. Due to its importance it is repeated here from the SWS December 2011 White Paper. Ensure that you grasp it. If not now, then return here when you have read the entire paper.

This means that the more similar each trade is to another the more flexibility a trader will have with their risk and position sizing rules which leads to a higher confidence level of achieving their anticipated portfolio outcome, as stated in their Trading Plan Objectives Statement.

Therefore, making each trade as similar as possible to each other becomes a trading system design objective, in order to reduce the variation of possible trade outcomes.

This was achieved with the SPA3 Revised Edge, as published and released in December 2011. The next major step in the research process is to conduct detailed historical portfolio exploratory simulation with different risk and money management criteria to determine which criteria work the best at the portfolio level with the particular edge, given a set of portfolio execution constraints such as portfolio capital, brokerage rates and market liquidity.

It is important to note that no one position size works well within all the constraints mentioned above, meaning that the best position size will be different for each set of constraints.

In seminars that I have delivered over the years it is amazing that traders’ with different trading approaches, trading different instruments with different amounts of leverage and different starting capitals mostly trade with the same position size, the 2% risk per trade model. Why? Probably because the ‘2% rule’ is regurgitated in book after book without the necessary research having been completed. This paper will make a mockery of this regurgitation.

Getting back to the degree of variation of potential portfolio equity curve outcomes, in terms of return AND drawdown, you should use this as one of the main criteria in determining how well the risk and money management rules fit the trading system, or edge, and how well the methodology (edge, risk management and money management) suit the given environment in which it executes.

Using this measurement will help you know when you can put a stake in the ground with your research and then move to executing in a live trading environment.

7 Research Environment The SWS December 2011 White Paper provided the outcomes from revising the SPA3 Edge. This White Paper now deals with the research process of matching risk and money management rules to

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 16 of 239

the SPA3 Revised Edge and uses the universe of all trades that are generated from the SPA3 Revised Edge trading system entry and exit rules.

The SPA3 Revised Edge trades’ database is used as input to a portfolio level risk and money management engine that chronologically merges the following to create unique simulated equity curve values on a day by day basis:

1. Historical daily share price data. 2. Randomly chosen (other selection methods can be used) trades from the trades’ database

on any given trading day from all the trades signalled on that day, when a new trade is required to fill a portfolio position.

3. Portfolio risk rules and parameters to determine how much capital to expose to the chosen market.

4. Position sizes for individual new trades depending on risk rules. 5. Brokerage rates for entry and exit transactions. 6. Liquidity checks to ensure that illiquid trades relative to portfolio size are excluded from

execution.

Multiple hundreds or even multiple thousands of simulated equity curve numeric data are fed into a statistical programming environment (SWS uses R) which generates a number of equity curve statistics and portfolio straw-broom graphs.

Equity curve analysis is then conducted to determine a number of outcomes including:

• Variation of equity curves, the more similar the better.

Excel

Trades Database

Portfolio level Risk & Money Mgt

Engine

Stats Programming

e.g. ‘R’

Portfolio Equity Curve Analysis

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 17 of 239

• Equity curve percentiles, e.g. 5, 25, 50 (median), 75 & 95 percentiles, of: o geometric mean, o maximum drawdown, o Win Rate & Profit Ratio, o number of trades, o unallocated equity (~ portfolio exposure), o Portfolio Performance Index (explained below), and o Downside Deviation Factor (explained below).

From this equity curve analysis other statistical metrics can be determined like the Geometric mean 5 percentile divided by the 95 percentile maximum drawdown. Depending on the values of these metrics the risk and position sizing rules can be changed and the process re-iterated. In fact, if the metrics are deemed substandard the entire process can be re-started going all the way back to the trading system concepts and rules.

8 Revised Risk Management and Money Management Rules in SPA3

8.1 Position Sizing calculation

In the prior SPA3 position sizing calculation the market capitalization, ATRVE (Volatility) at two levels - above and below 5% - and the SPA3 signal were used to determine whether a SPA3 trade was Low, Medium or High Risk. Effectively there were just three different position sizes for any given trade but there were also three sub-portfolios of capital.

If two SPA3 users had exactly the same portfolio value with the same number of open positions then their position size for a particular trade would have been exactly the same.

The previous portfolio construction rules required that a set number of open positions be selected prior to starting to trade. With the revised position sizing rules the number of simultaneously open positions is open-ended but limited by total portfolio capital and the position size.

Under the revised position sizing calculation, the Portfolio Risk % is the only input that a SPA3 user needs to decide on.

Position Size =Portfolio Value × Portfolio Risk %

Trade Risk %

Portfolio Risk %: Percentage of the Portfolio Value you are willing to risk (lose) on a trade.

Trade Risk %: Amount of risk (loss) that may occur in this trade. This is the ‘expected loss’ but can also be the distance to a trailing stop for each particular trade.

To determine the Trade Risk % for any trade we use the volatility level (ATRVE) and the SPA3 signal. From quantitative analysis of thousands of historical trades, we found that the combination of these two characteristics provide the primary determinates of the ‘expected loss’ of a trade. This combination replaces the previous SPA3 Risk Tables. Notable changes are:

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 18 of 239

• The new Trade Risk % has no discrete levels. A change in the ATRVE value will result in a smooth and relative change in the Trade Risk %.

• There are ranges of ATRVE values for each SPA3 signal that will be designated as a ‘No Trade’.

The expected Trade Risk %’s are stored in TradeMaster and used in the position size calculation

For example, assume a portfolio of $100,000 that has chosen to risk 1% on the next trade that TradeMaster says has an expected Trade Risk% of 10%.

Portfolio Value: $100,000. Portfolio Risk % = 1% Trade Risk = 10% Position Size = ($100,000 x 1%) / 10% = $1000 / 10% = $10,000

If the entry price was $4.00, the quantity would be 2,500 shares with a Trade Risk $ of $0.40, being 10% of $4.00.

See the Addendum is section 18 on page 237 for a detailed example.

8.2 Portfolio Risk as a Master Control

There are many ways to determine how large a position size should be but every one of them has something in common. In the end, every one of them puts some of your equity at risk. A losing trade actually sees this risk eventuate and solidifies the result as a loss in your portfolio. In this regard, it therefore makes considerable sense to first determine how much risk (loss) per trade your portfolio can endure. More appropriately how much risk can you personally tolerate?

Specifying this as an absolute value, say $1000, is not appropriate because this represents something different to different size portfolios. A single loss of $1000 from a $1 million dollar portfolio is a negligible 0.1%. However, it’s a 10% loss to a $10,000 portfolio and a few of these would very quickly decimate the portfolio. So we will define risk as a percentage of the portfolio. For example, you are willing to risk 1% of your portfolio in the next trade that has an expected maximum loss. This doesn’t mean that the position size will be 1% of your portfolio. It means that if the trade results in the expected loss then you will experience a loss of 1% to your portfolio at that time.

We now have a mechanism to shape the risk that our entire portfolio experiences for every trade. By setting the portfolio risk percentage to which we are prepared to expose our portfolio, we can dial up or down the effect of every trade and therefore the eventual combined effect on the portfolio, including the drawdown, the day to day changes in equity value and the final equity value. Consider this your master volume control; consider this your master objective control for risk and reward.

The portfolio risk percentage you select will out rightly determine if you are successful in achieving your objectives, or if you are destined to fail. Don’t expect that by risking more that you will be more successful. Likewise, don’t expect that by risking less that you will be actually taking less risk. Each degree of risk percentage generates new risks, most of them interrelated and none of them have a

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 19 of 239

perfect solution. The best possible solution we can aim for is one that minimises all risks to an acceptable level. This is no easy task. Every trader has a different risk tolerance, every portfolio has a different value, and market conditions will continue to vary.

Therefore, the only variable in the above position sizing calculation that the SPA3 trader needs to decide is the Portfolio Risk %, or % Risk per Trade as it is also known. How does one know what the correct Portfolio Risk % or % Risk per Trade is for their set of trading circumstances taking into account portfolio size, brokerage rates, personal risk profile, drawdown risk objective, reward risk objective etc? Should it be 1%, or 2% as most books regurgitate, or 0.5% or 3% or 0.87%?

Rather than trading blindly with a guessed % Risk Per Trade and then letting one’s live trading results tell you over a large sample of trades whether you are taking too much or too little risk (which may take many months or even years), we use exploratory simulation to get the answers before we start trading.

9 Portfolio Limits and Boundaries This section provides the range of SWS suggested position sizes based on the analysis of the exploratory simulation research. The ‘Default XASX Profile’ SPA3 parameters were used to generate the trades’ database that was used for the respective simulations.

9.1 Different SIROC parameters

From a SPA3 Revised Edge perspective, the following SIROC parameters were re-researched since the December 2011 White Paper with the single Profit Stop (see Section 16 below), where the third parameter is the daily SIROC EMA setting:

• SIROC 5 3 5 • SIROC 8 3 5 • SIROC 13 5 5 • SIROC 17 7 8 • SIROC 19 7 8 • SIROC 21 8 8 • SIROC 26 9 8 • SIROC 30 10 8 • SIROC 34 13 8 • SIROC 55 21 8

Fig 9.1 shows the Expectancy and SQN (System Quality Number – see the December 2011 White Paper) for all trades with each of the SIROC settings above on the horizontal axis. The distribution curve shows that, using the SQN, the SIROC 17 7 8 is a tiny bit better than the other SIROC settings as it is at the top of the curve. SIROC 19 7 then SIROC 13 5 5 then SIROC 21 8 are close behind.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 20 of 239

Fig 9.1

Only two sets of SIROC parameter settings were researched using exploratory simulation, the SIROC 21 8 8 and SIROC 13 5 5. However SPA3 users can quite safely use SIROC 17 7 8 and SIROC 19 7 8 as well, as can any other either SIROC settings, but any of these four are recommended. The Trade Risk % risk tables are programmed into TradeMaster for all four SIROC settings.

For each of the two SIROC settings, SIROC 21 8 8 and SIROC 13 5 5, that were simulated, three portfolio starting capital amounts were researched, $25,000, $100,000 and $400,000. Three different brokerage rates were also researched and different liquidity settings. A number of different Portfolio Risk % settings were researched to calculate position size, ranging from 0.2% to 3%.

9.2 An introduction to Box Plots

The simplicity of the box plot makes it ideal as a means of visually comparing large sets of data. Box plots of a group of portfolio tests can be lined up side by side and the various attributes of the portfolios compared at a glance. Obvious changes in values and ranges are immediately apparent.

The box segment represents the range of values produced by the central 50% of portfolios. That is 25% of portfolios produced values below the box and 25% of portfolios produced values above the box. The vertical ‘T’ lines are known as whiskers. Throughout this paper, the upper whisker, labelled ‘MAXIMUM’ represents the values at the 5th percentile of portfolios. That is, there were another 5% of portfolios that produced values greater than the top whisker. The lower whisker, labelled

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 21 of 239

‘MINIMUM’ represents the values at the 95th percentile of portfolios. That is, there were another 5% of portfolios that produced values less than the lower whisker.

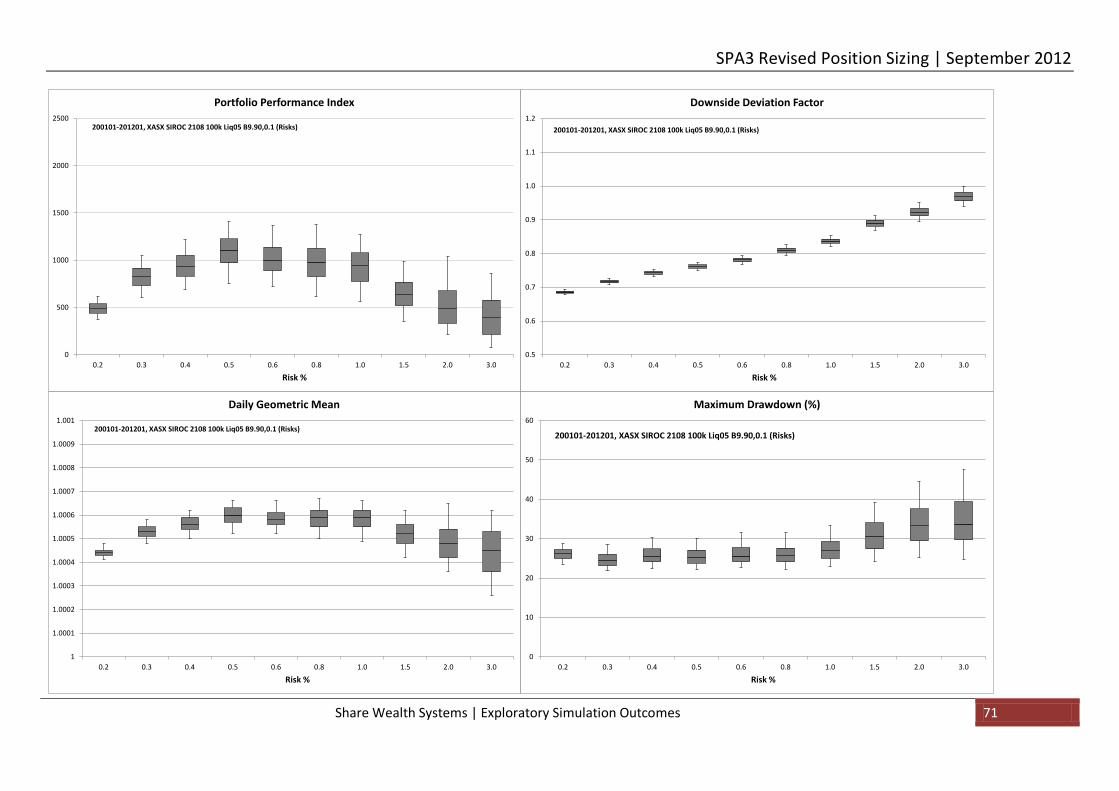

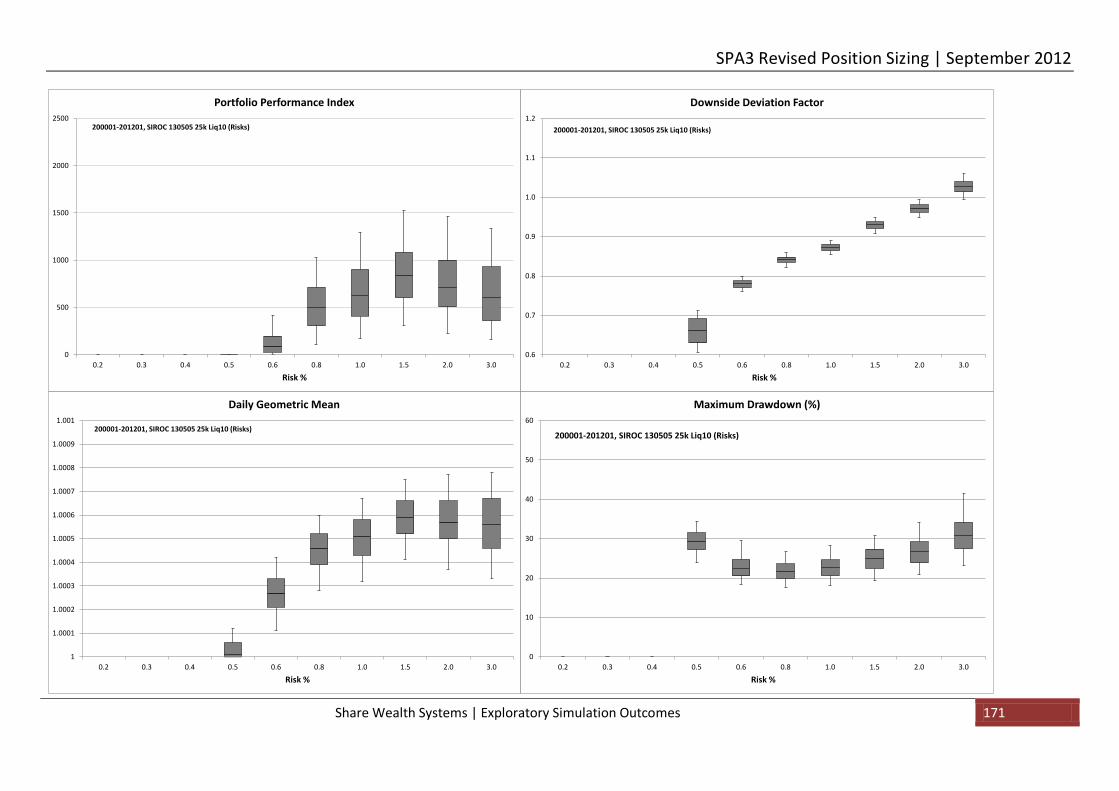

9.3 Portfolio Limits using SIROC 21 8

This section provides Portfolio Risk % boundaries for portfolios that use the SIROC 21 8 8 parameter settings, all other SPA3 settings being as per the SPA3 Revised Edge for the ASX with a single Profit Stop.

HINT: View the ‘box charts’ and simulated portfolio equity curves alongside each of the tables below, so as to compare and follow the reasoning behind the

suggested limits and boundaries. The commentary below will also make more sense.

9.3.1 $25,000 Portfolios

$25,000 SIROC 21 8 8 Criteria Min

Risk % Ideal Max

Risk % Comments Chart Sections

No Liquidity Check, $9.90, 0.1% 0.4 2.5 Not recommended 11.2.1 Brokerage: $9.90, 0.1%, x5 Liq 0.5 0.6 – 1.5 1.5 11.2.2 Brokerage: $9.90, 0.1%, x10 Liq 0.5 0.8 – 1.2 1.5 11.2.3

9.3.1.1 Comments

Whilst it makes good sense to minimise brokerage rates with any active investment strategy, with small starting capital bases of $20,000 to $40,000 it is mandatory. Hence we have simulated just the $9.90 or 0.1%, whichever is the larger, brokerage rate for the SIROC 21 8 setting on a $25,000 portfolio. Using a larger brokerage rate would have similar effects with the SIROC 21 8 as it has with the SIROC 13 5 5 settings shown above. Brokerage rates of $27.50 or 0.165% and %19.95 or 0.1% are

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 22 of 239

simulated with the SIROC 13 5 5 parameter settings to show that the $27.50 / 0.165% combination should NOT be used with a small portfolio.

The higher liquidity requirement of x10 compared to x5 does curtail performance a little in that the potential to perform better with a larger position size is reduced. Notice in sections 11.2.2 and 11.2.3 how using 1.5% Risk %, the Portfolio Performance Index (PPI) box plot starts falling for the x10 liquidity at 1.5% and the upper quartile of the box plot of the Geometric Mean is lower compared to the x5 liquidity.

Which position size to use in the ‘ideal’ ranges provided above will depend on what the Objectives are that have been set in your Trading Plan Goals & Objectives Statement.

For example, for a 1.5% Risk % with x5 liquidity the PPI and Geometric Mean 5% and 25% percentiles at the top of the box plots are higher than for position sizes with Risk % of 0.8% - approx. 0.12%. However, the 95% and 75% are lower meaning that the worse portfolio outcomes for a 1.5% Risk % will be worse than for the 0.8% - 1.2% Risk % portfolios.

The simulated portfolio outcomes have selected SPA3 trades on a random basis. Therefore if you trust yourself that will not make trading errors and that your trade selection will be better than the average of a random trade selection process then using the larger position size in the range of 0.8% - 1.2% can provide you with a better return that a smaller position size.

If you trade with a higher brokerage rate than $9.90 or 0.1% then you will have to err towards the lower end of the [Ideal] range of Risk % choice. Refer to the SIROC 13 5 5 simulated results below for further insight.

9.3.2 $100,000 Portfolios

$100,000 SIROC 21 8 8 Criteria Min

Risk % Ideal Max

Risk % Comments Chart Sections

No Liquidity Check, $27.50, 0.165% 0.3 2.0 Not recommended 11.2.4 Brokerage: $9.90, 0.1%, x5 Liq 0.3 0.5 – 0.8 1.0 11.2.5 Brokerage: $19.95, 0.1% 0.4 0.5 – 0.8 1.0 Not Simulated Brokerage: $27.50, 0.165%, x5 Liq 0.4 0.5 – 0.8 1.0 11.2.6

9.3.2.1 Comments

$100,000 portfolios are still affected by the higher $27.50 / 0.165% brokerage rate but nowhere near as much as a smaller portfolio i the $20,000 - $40,000 range.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 23 of 239

9.3.3 $400,000 Portfolios

$400,000 SIROC 21 8 8 Criteria Min

Risk % Ideal Max

Risk % Comments Chart Sections

Brokerage: $27.50, 0.165%, x5 Liq 0.2 0.4 - 0.5 0.6 11.2.7 Brokerage: $19.95, 0.11% 0.2 0.4- 0.5 0.6 Not simulated Brokerage: $9.90, 0.1% 0.2 0.4 – 0.5 0.7 Not simulated

9.3.3.1 Comments

Larger portfolios can sustain higher brokerage levels much better than smaller portfolios.

However, larger portfolios suffer lower comparative growth, as measured by geometric mean in the simulations results in this paper, due mainly to the lack of liquidity in the overall Australian equities market. However, outperformance of the All Ordinaries index is still quite spectacular over the sample research period.

Hence Risk % has to be smaller in larger portfolios due to this liquidity issue. Whilst a small 0.2% Risk % wouldn’t be too affected by the higher brokerage level the issue becomes the absolute number of trades that SPA3 traders would need to complete. Positively though, SPA3 continues to provide sufficient opportunity to trade if traders are happy to be that active. Simultaneously open position charts are provided in the detailed sections of the paper.

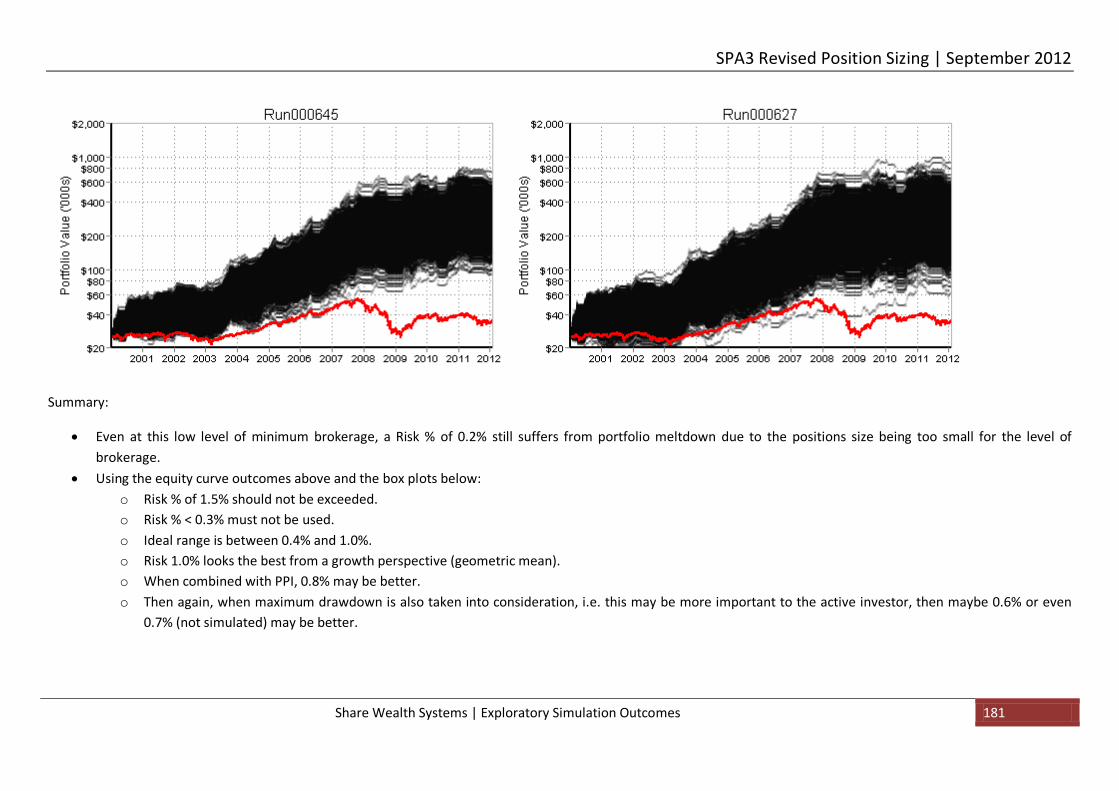

9.4 Portfolio Limits using SIROC 13 5 5 – Close immediately

This section provides Portfolio Risk % boundaries for portfolios that use the SIROC 13 5 5 parameter settings, all other SPA3 settings being as per the SPA3 Revised Edge for the ASX with a single Profit Stop. Trades are closed immediately when the Market Risk turns to High Risk.

HINT: View the ‘box charts’ and simulated portfolio equity curves alongside each of the tables below, so as to compare and follow the reasoning behind the

suggested limits and boundaries.

9.4.1 $25,000 Portfolios

$25,000 SIROC 13 5 5 Criteria Min

Risk % Ideal Max

Risk % Comments Chart

Sections No Liquidity Check None Not recommended 11.3.1 Brokerage: $27.50, 0.165% None None None Not recommended 11.3.2 Brokerage: $19.95, 0.1% 0.8 0.8 – 1.0 1.5 11.3.3 Brokerage: $9.90, 0.1% 0.4 0.8 – 1.2 1.5 11.3.4

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 24 of 239

9.4.1.1 Comments

Whilst the Max Risk % in the table above shows 1.5%, the maximum Risk % which should be traded is 2, due to Volatility Drag (this is explained in the Appendix). Beyond a Risk % of 2 the variation of portfolio outcomes starts to widen and fall quickly.

A small portfolio is highly susceptible to meltdown from high brokerage rates. As the brokerage rate increases the minimum Risk % with which to calculate position sizes needs to rise accordingly. For lower brokerage rates, the range of [Ideal] Risk % with which to calculate position sizes widens thereby increasing the trader’s position size flexibility and the probability of outperformance whilst reducing the risk of underperformance.

This is primarily due to:

1. Less capital being directed towards the broker and more capital being put to work in the market for the active investor.

2. The increased number of trades that flow through the portfolio which contributes directly to compounding. The additional trades include those with greater Trade Risk, from increased volatility, which typically come with greater reward, provided risk is managed by sticking to the SPA3 rules.

The availability of trades is not an issue.

Liquidity has a minor effect on smaller portfolios because the absolute size of positions is small.

9.4.2 $100,000 Portfolios

$100,000 SIROC 13 5 5 Criteria Min

Risk % Ideal Max

Risk % Comments Chart Sections

No Liquidity Check None Not recommended 11.3.5 Brokerage: $27.50, 0.165%, x5 Liq 0.3 0.4 – 0.8 1.0 11.3.6 Brokerage: $27.50, 0.165%, x10 Liq 0.3 0.4 – 0.8 1.0 11.3.7 Brokerage: $19.95, 0.1%, x10 Liq 0.3 0.4 – 0.8 1.0 Not simulated Brokerage: $9.90, 0.1%, x5 Liq 0.2 0.3 – 0.5 1.0 11.3.8 Brokerage: $9.90, 0.1%, x10 Liq 0.2 0.4 – 0.6 1.0 11.3.9

9.4.2.1 Comments

A medium sized portfolio is starting to see significant easing of the meltdown from brokerage issues. The smaller brokerages still restrict the minimum Risk % possible but increasing the brokerage does not increase the minimum Risk % accordingly. The ideal Risk % values are now considerably lower.

The reason that the [Ideal] range narrows for the lower brokerage level of $9.90 / 0.1% is that these Risk % selections stand out as far better when the brokerage level is reduced. At the higher brokerage level there is not as much difference between the Risk %

The maximum Risk % which should be traded due to Volatility Drag is 1. Even at this point the range of portfolio equity curves has started to widen and fall quickly to unnecessarily low levels. Trading

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 25 of 239

these higher Risk % values would only be done to reduce the trade frequency or reduce the effect of larger brokerage.

Medium sized portfolios will start to see impact from insufficient liquidity as the portfolios grow.

9.4.3 $400,000 Portfolios

$400,000 SIROC 13 5 5 Criteria Min

Risk % Ideal Max

Risk % Comments Chart Sections

Brokerage: $27.50, 0.165%, x5 Liq 0.2 0.4 – 0.5 0.6 11.3.10 Brokerage: $27.50, 0.165%, x10 Liq 0.2 0.4 – 0.5 0.6 11.3.11 Brokerage: $19.95, 0.1% 0.2 0.4 – 0.5 0.6 Not simulated Brokerage: $9.90, 0.1% 0.2 0.4 – 0.5 0.6 Not simulated

9.4.3.1 Comments

Large portfolios are generally not susceptible to meltdown from brokerage because they operate in the fixed brokerage % zone. The minimum Risk % is now dictated by the maximum number of trades that the trading system can generate across all market periods. Below a certain minimum risk there are simply not enough trades and your unused equity will be exposed to opportunity loss.

The maximum Risk % which should be traded due to Volatility Drag is 0.6. Even at this point the range of results has started to widen significantly and is falling. Larger portfolios with fewer simultaneous positions will experience a larger range of outcomes because there are a greater number of possible trade combinations. Trading these higher Risk % values would only be done to reduce the trade frequency.

Liquidity can have a devastating effect on larger portfolios. It places restrictions on the larger Risk % values by inherently limiting the range of possible Trade Risks. The reduction in performance can be seen across all Risk % values as the liquidity multiple is increased.

9.4.4 Number of Simultaneously Open Positions

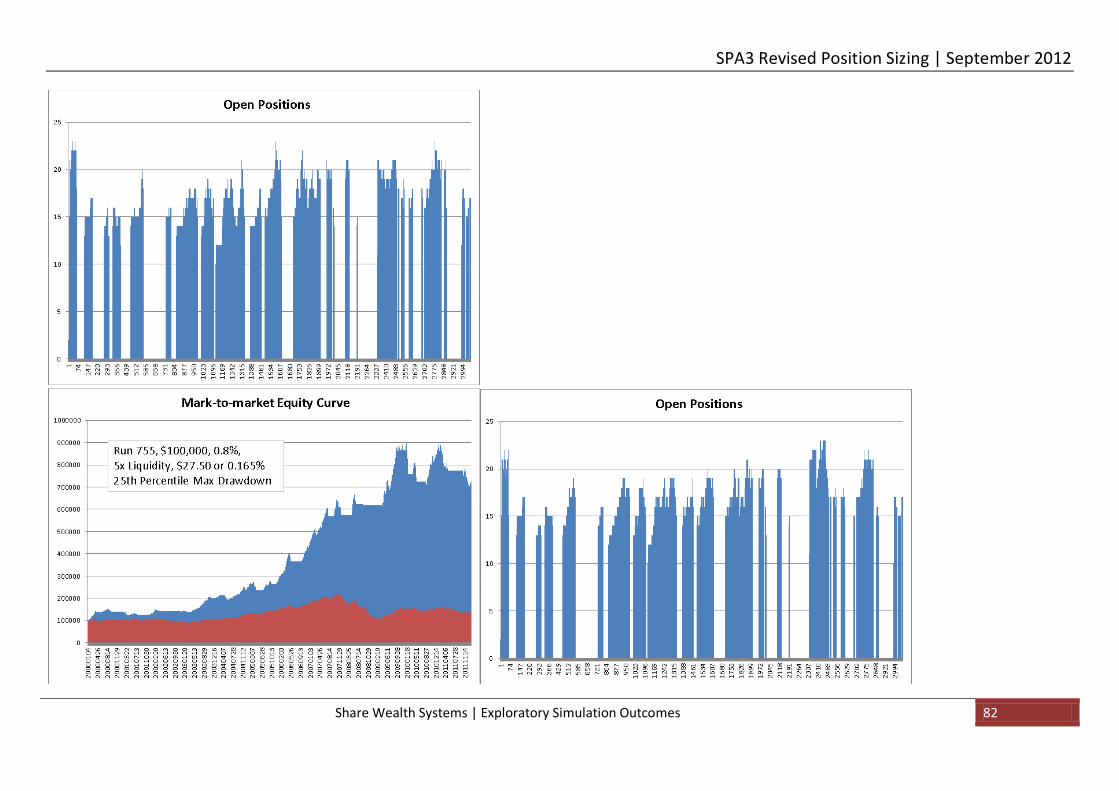

The Risk % selected for any portfolio will be the main factor that determines how many simultaneously open positions a portfolio may have. The other main factor will be the volatility of trades in any particular market. SPA3 active investors can get a very good idea of how many open positions they will need to manage for any chosen Risk % for their portfolio. The following graphs provide a good insight into this.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 26 of 239

The Open Positions charts above show the number of simultaneous open positions for a 0.2%, 0.3%, 0.4%, 0.5%, 0.6% and 0.8% Portfolio Risk % on the ASX. 0.2% and 0.3% will be a comparatively high number of positions to manage for most private active investors. 0.4% may still be a little on the high side but the risk to reward at this Risk % may make it worthwhile for some portfolio scenarios depending on starting capital and brokerage. Risk %’s of 0.5% - 0.8% should be just fine.

The following two graphs show the number of simultaneously open positions from simulating trading SPA3 on the NASDAQ with Risk % of 0.6% and 0.8%. Compare these to the corresponding Risk % for the ASX. Besides periods of volatility the number of simultaneously open positions is very similar.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 27 of 239

The following two graphs show the number of simultaneously open positions from simulating trading SPA3 on the ASX and NASDAQ, respectively, with Risk % of 1.0%.

Using a Risk% of 1.5% will reduce the number of open positions to an average of around 8 - 9 and of 2.0% to an average of 6 - 7.

This section is provided here to assist SPA3 active investors with selecting the Risk % for their portfolio.

10 Exploratory Simulation

10.1 Introduction

Please refer to the December 2011 White Paper for an introduction to exploratory simulation.

Exploratory simulation can only start once a mechanical system with an edge is established that has generated sufficient historical trades from which to compile historically simulated portfolios against past stock data.

Our main purpose here is to determine a suitable position size for a given set of trading circumstances and ultimately determine the chances of a trader achieving their reward and risk objectives in their Trading Plan.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 28 of 239

To achieve this, a back test needs to be run that simulates the mechanical process of operating a portfolio using the exact criteria that will be used in live trading. The problem with a back test is that only a single portfolio is created using a subset of the whole universe of possible historical trades and is therefore only one unique sample of what could have happened.

The different choices that each investor makes at any decision point will set them upon a different unique path to every other investor; each will have a different outcome to their portfolio and each will have a unique mix of historical trades that would have been executed in their portfolio.

These choices include; portfolio size, trade selection, trading system settings, stock liquidity requirements, brokerage rates and money management settings. All of these will produce thousands and thousands of different permutations over an extended period of time. So you can’t just run one back test, you need to run thousands.

Traditional simulation and software simulation tools would use Monte Carlo analysis. In brief, with Monte Carlo all the trades from the entire trade period are thrown into one bucket and then randomly drawn to create an imaginary portfolio. Monte Carlo analysis jumbles time randomly and therefore ignores any dependencies between trades that might have occurred such as during strong market downturns and run-ups, i.e. during strong trending periods.

Although the Monte Carlo process has some value, in that it will simulate an ‘edge’ according to its statistical expectancy, it has one major flaw that precluded us from using it. It is effectively incapable of simulating the true effect that market sentiment has on a portfolio of multiple positions in multiple securities with dependency. Consequently, Monte Carlo underestimates the actual risks from real market events, like the 2008 ‘financial crisis’, and prevents the proper portfolio simulation of money management and its outcomes by under-simulating maximum drawdowns in such market conditions. Monte Carlo would be more useful in single position simulations, such as just a Gold portfolio or just an S&P500 futures portfolio, than for portfolios with multiple simultaneously open positions such as an equities portfolio.

What we needed was a test technique that created simulated portfolios using the exact trading conditions that were available during the test period. This includes the exact order and timing of trade signals, market conditions, trading costs and money management rules. This is the only way to know what might have happened for you and, hence, gain a very good idea of what may happen in the future. We found this in a technique called Exploratory Simulation.

The result is a range of portfolio equity curves that cover a statistically significant sample of possible outcomes over the test period. We found that 1000 simulated portfolios were needed to provide a statistically significant sample that would be representative of possible portfolio scenarios over a > 10 year period. Would this cover EVERY possible scenario? Well, no. That’s what statistical analysis does, it uses a sample that is deemed statistically significant to be representative of the entire possible universe of outcomes and then attaches probabilities to the potential for the statistical sample to repeat in the future. Perfection and dead certainties will never be achieved but such statistical analysis has major advantages over not doing the research and statistical analysis at all. Mechanical trading is the execution of a process that is heavily based on statistical probabilities, nothing more nothing less.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 29 of 239

Every exploratory simulation run produces an equity curve and trade statistics. The combined data from 1000 runs generate a powerful picture of the range of portfolio behaviour given a set of risk and money management rules. Your capability of thriving and surviving is immediately evident. The impact of your trading environment and every decision or change to a process is shown clearly.

Exploratory Simulation allows you to know if your objectives are achievable with a far higher degree of certainty than with not using exploratory simulation.

10.2 Extent of exploratory simulation research

This has been a huge project no matter which way you measure the effort and the resource that has been committed to it. At times it seemed that it would be never ending! As I have said many times before, having a loyal customer base to which a commitment such as this can be made is a major motivation to keep on keeping on and to eventually deliver.

Detailed research for this project started in June 2011. Well over 500,000 portfolio simulations have been run in this project. Well over 2,500 dedicated man hours have been invested in this revision project of SPA3 risk and money management.

The specialised software tools used in the project are complex and require a detailed level of computer skills and C++ programming skills. The peripheral tools required for statistical analysis, such as R and Excel, are also used at intricate levels. This of course excludes the pre-requisite financial markets and trading knowledge required to embark on such a project.

In the exploratory simulations conducted and the results of which are provided in this paper the following criteria were used:

• ASX only trades from 4/1/2000 (first trading day of the century) to 31/1/2012. • All listed and delisted ASX stocks during this period. This means that a stock that was

delisted after January 2000 and before December 2011 will be included in the simulations. • An open-ended number of simultaneously open positions per portfolio. • Randomly chosen trade selection from available trades whenever there was available capital

to be invested, according to Risk Profile 1. o This means that on any given day where there was more than one SPA3 trade

available to select from, the trade was chosen on a purely random basis, provided the trade was liquid enough. If not, then the next trade that was liquid enough was selected randomly.

o If there was insufficient capital available to fill a required position size then the position size was NOT reduced to fill the position. This means that there are times through the life of the simulations that portfolios were not fully invested. You may devise a set of common sense rules for your own Trading Plans

whereby you reduce the position size to appoint but no less to make the trade with a smaller position size.

• The Portfolio Risk % for new position sizes were not decreased or increased for each simulation, they remained the same, based on the position size calculation, throughout the research period.

• No pyramiding or lightening was used.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 30 of 239

• Risk Profile 1 was used in all simulations, that is portfolios were moved 100% into cash when a SPA3 High Market Risk occurred.

• During Low Market Risk, all High Sector Risk trades were allocated a full position, that is, there was no reduction in position size for Sector Risk.

• In sections 11.2 (SIROC 21 8) and 11.3 (SIROC 13 5 5) all positions were closed immediately on the trading day after a SPA3 High Market Risk signal occurred.

• In section 11.4 some equity curves for the SIROC 13 5 5 allowed trades to exit normally when a SPA3 High Market Risk occurred with no new positions taken. These are noted accordingly.

• Simulations included brokerage as shown. • No dividends or interest have been included in the equity curves. The additional returns that

would be generated from these two sources would be substantial in absolute terms and in compounding terms over a period of 12 years.

• No tax is included in the equity curves except for brokerage GST.

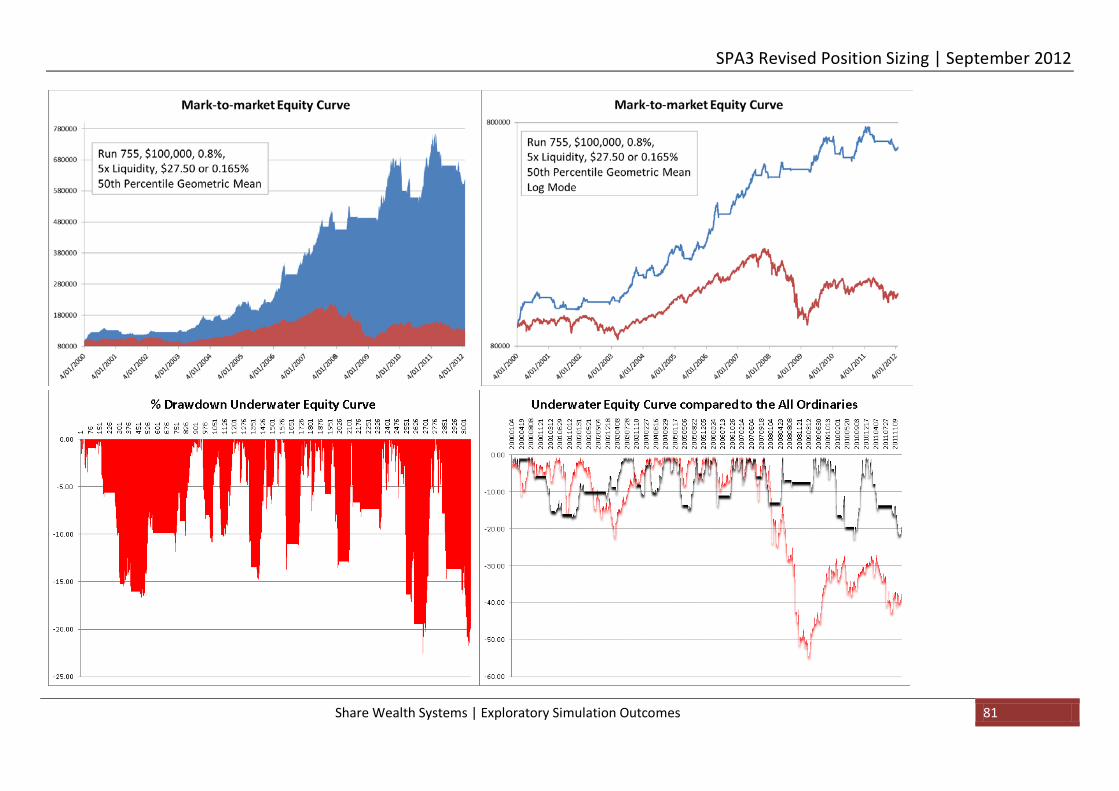

Each historical portfolio equity curve is an unrealized profit equity curve or a mark-to-market equity curve with the portfolio value being recalculated on a daily basis for the life of the portfolio.

10.3 Research period

Some comment on the research period that has been used for the portfolio simulation is required.

Big picture technical analysis will show that a secular bear market in equities started on the $DJI in January 2000 and in March 2000 on the NASDAQ Composite and S&P500. On the ASX a case might be argued against a secular bear market starting at this time as a major new high well above the March 2000 high was made in 2007. However, the period chosen has the following traits:

• Two major bear markets in the ALL ORDS of 20% and 54%. These might be termed primary bear markets within a secular bear market.

• Major geopolitical events in September 2001 in New York and July 2007 in London. • Major natural disaster events such as the tsunami in Japan in March 2011. • Primary bull markets within the secular bear market such from March 2003 and March 2009.

This is a fantastic sample research period with which to conduct exploratory simulation to demonstrate robustness of a methodology’s timing, risk management and position sizing rules.

However, the benchmark index of the market that we have researched still had an upwards bias. The ALL ORDS rose by around 30% over this period. That said the advance decline line for the ALL ORDS had a downward bias meaning that far more stocks fell than rose over this period.

In another paper due out later this year we will demonstrate SPA3 outperforming the NASDAQ Composite over the same sample period of January 2000 – January 2012. Over this period the NASDAQ Composite had a downward bias, falling 30% over this period with 2 x major primary bear markets and one major primary bull market during the secular bear market.

It is not secular bull markets such as 1982 to January 2000 that investors need worry about, it is secular bear markets such as we have experienced since 2000 and such as 1966 to 1982 that

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 31 of 239

investors must prepare themselves for. If your strategy can make positive headway during such periods then handling the secular bull market will be a fantastic ride.

As mentioned above, all the exploratory simulations conducted in this paper have been done with SPA3’s Risk Profile 1 risk management approach. This begs the question, is using Risk Profile 2 still a valid risk management approach? It is our considered view that it is, but probably only during secular bull markets. Another research project ……….

11 Exploratory Simulation Outcomes

11.1 Introduction

This section will show the graphical outcomes from this round of SPA3 research.

The main purpose of this section is to provide graphical output to support SPA3 users choosing what position size to use for their own respective investing scenarios.

Whilst there may seem to be plenty of pages, not all pages are relevant to everybody. The detail has been provided so that each SPA3 user can hone in on a portfolio scenario that is relevant to them. Of course, perusing all the material can be of great educational value. In the future we will investigate providing access to this information via a tool of sorts.

The other purposes of this section are to:

1. take the reader through a process of gaining understanding of what steps were taken to revise the SPA3 Money Management rules according to the objectives set for the research project,

2. understand why the SPA3 Revised Money Management rules are an improvement on the previous money management rules,

3. understand how extremely important it is to get one’s position sizing correct in harmony with their system and execution environment, and

4. importantly, build belief and trust in the methodology such that it is executed with consistency and confidence to be able to grow one’s trading capital to reach ones financial objectives.

Only the ASX research results are provided at this stage for unleveraged trading. JSE research results and the NASDAQ research results will be provided in future papers, as will leveraged trading with CFDs.

Each set of charts will be headed according to the following portfolio variables:

1. The amount of starting capital as at 4/1/2000, the first trading day of 2000. 2. The SIROC parameters used. 3. The liquidity check to ensure that there was sufficient liquidity to take the trade. 4. The brokerage rate used for the life of the simulation.

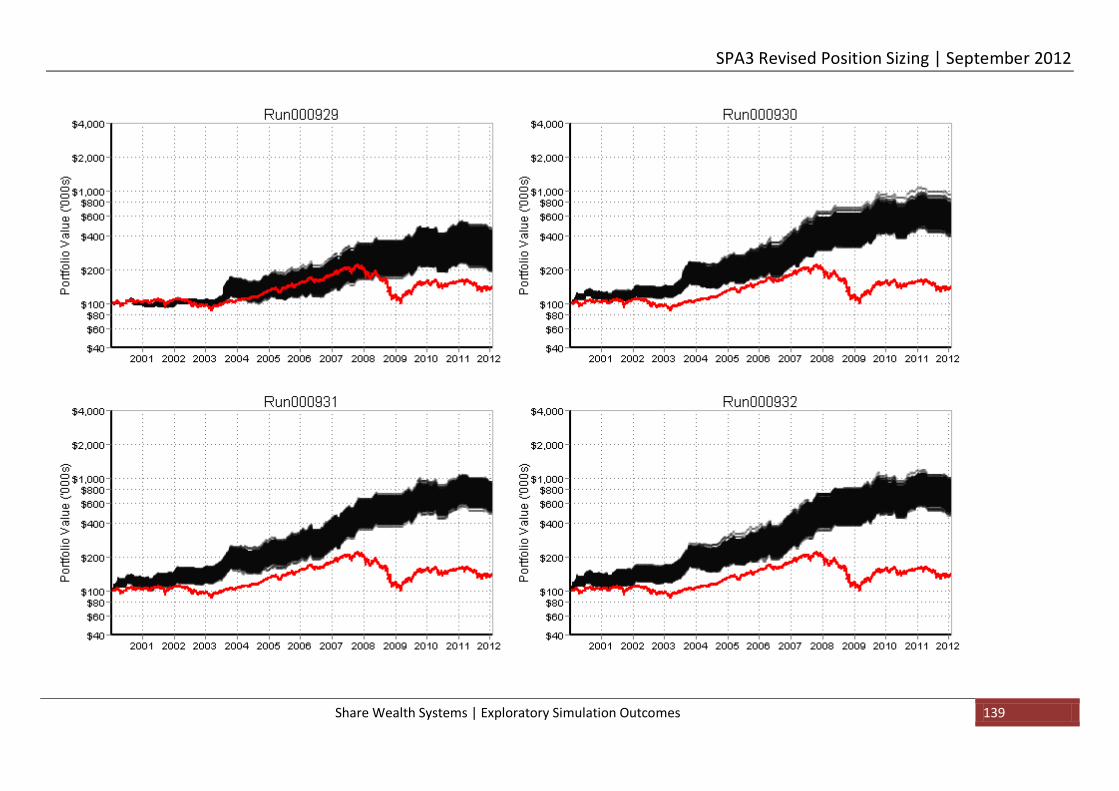

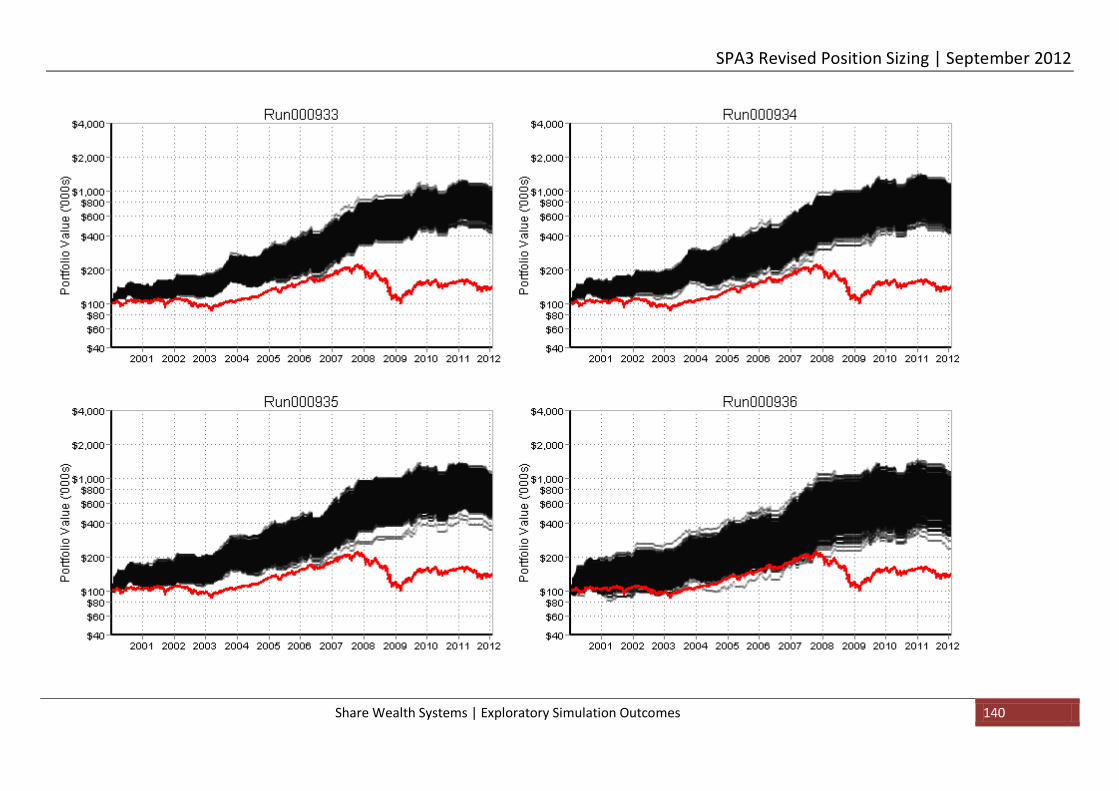

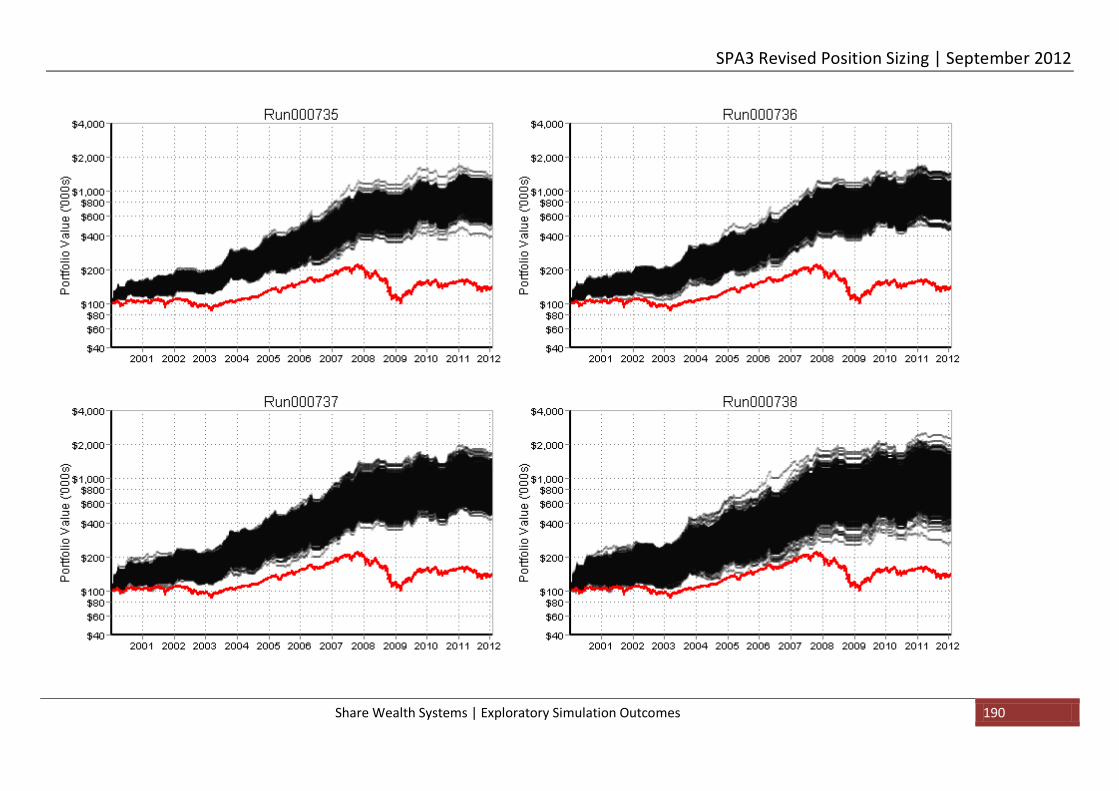

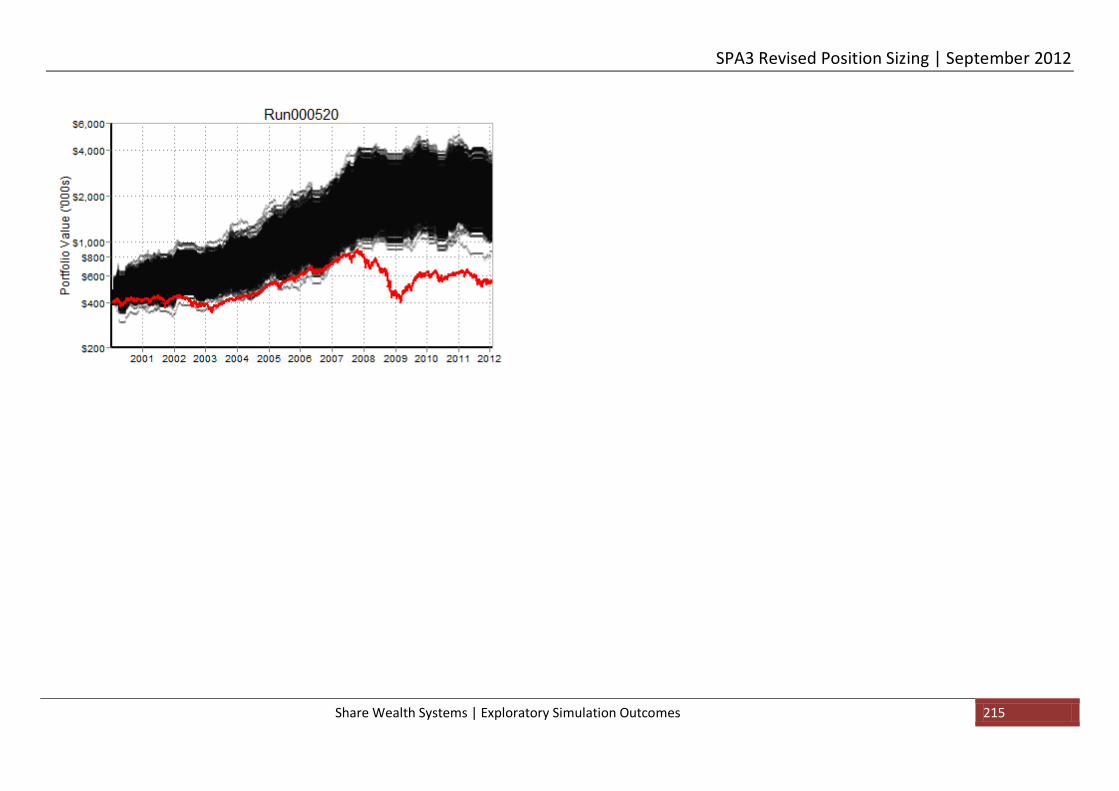

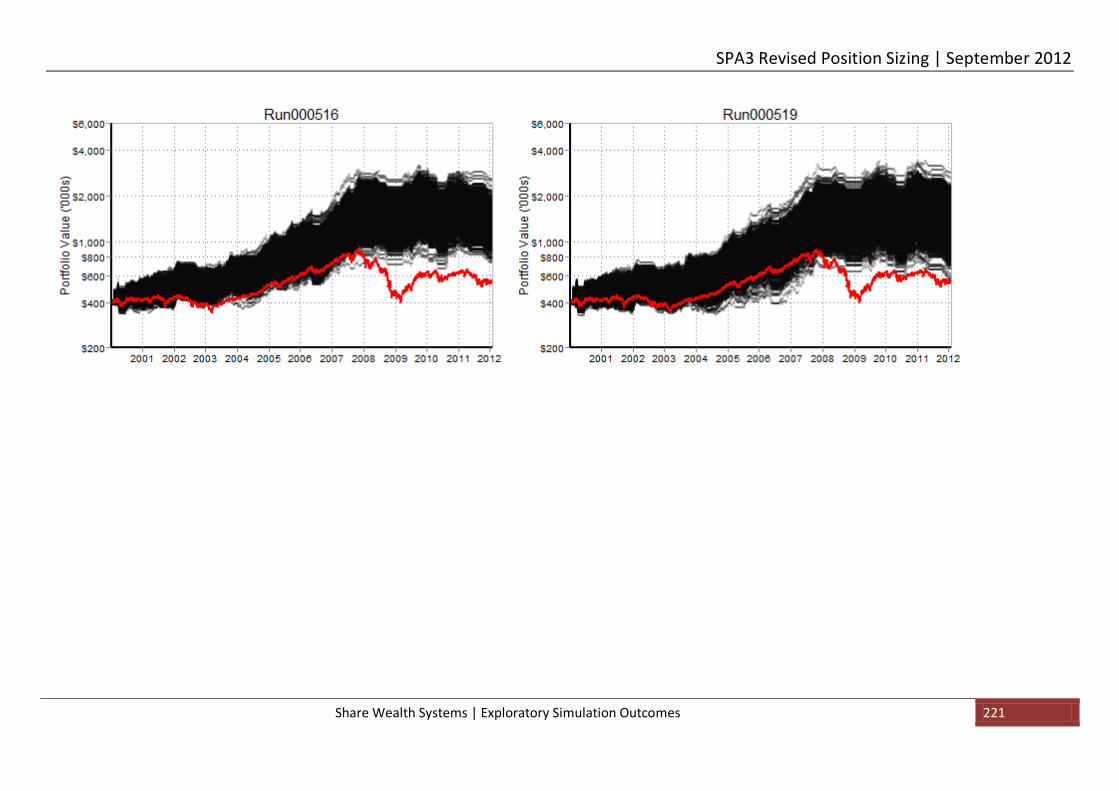

Two types of graphs will be shown for each portfolio scenario, straw-broom graphs and box plots.

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 32 of 239

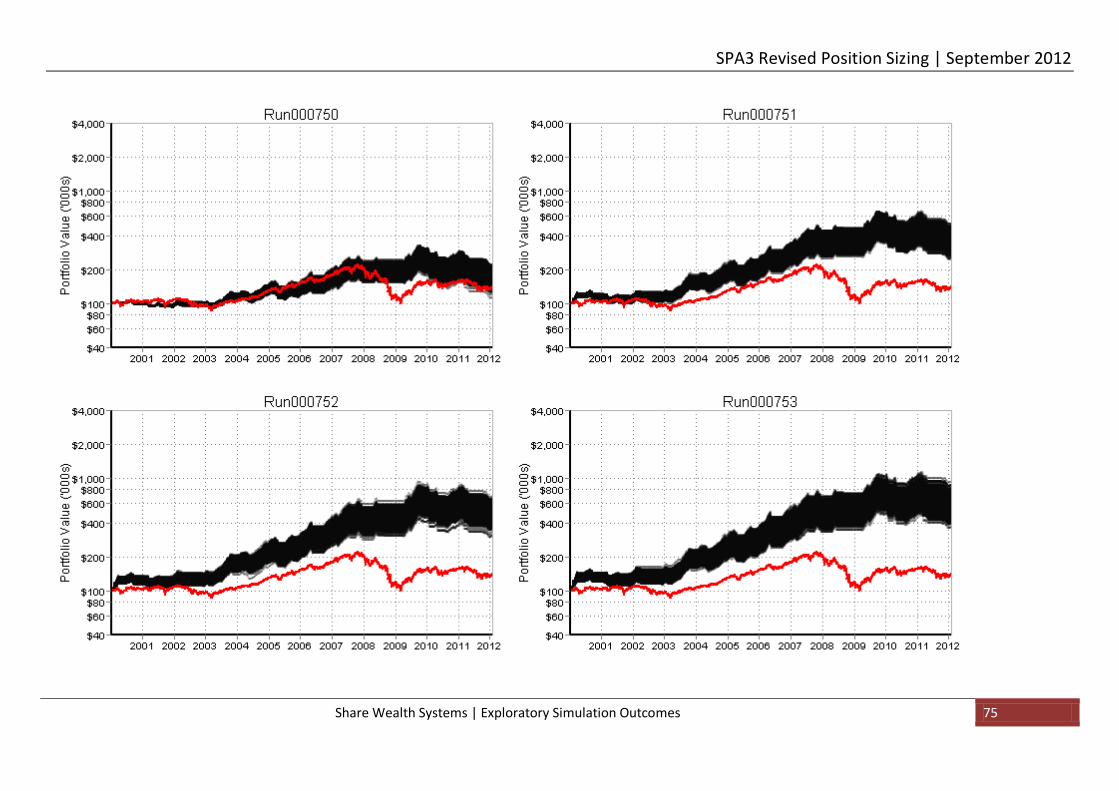

Each of the straw-broom charts show 1000 unique simulated portfolio equity curves. Each straw-broom chart has been back-tested with a different position size. Each equity curve has a unique mix of SPA3 trades that have been selected randomly based on meeting the liquidity check for the simulation. This statement applies to all the straw-broom charts that are in this White Paper.

A quick scan of the straw-broom graphs will help reveal the better Portfolio Risk %’s to use for each portfolio scenario. Notes are provided for most of the portfolio scenarios.

The box plots that are provided for each scenario show the following measurements:

1. Portfolio Performance Index.

Investors frequently associate risk with failure to attain a target return. The target is typically the return offered by a benchmark such as the relevant market index. For funds invested in the Australian stock market the common benchmark is the All Ordinaries Index ($XAO) or the S&P/ASX 200 Index ($XJO). Such benchmark comparisons are widespread in the investment industry, along with a fear of underperforming them. Benchmarks offer a fixed point of reference against which different market investments can be measured, in particular the expected return.

An investor expects that over a period of time that their portfolio will outperform the benchmark returns. As time passes the probability that a portfolio WILL outperform the benchmark is increased by having returns:

• that are more frequently greater than the benchmark, and • that are larger than the benchmark, including small losses.

“The Portfolio Performance Index (PPI) takes both of these into account to generate a number that measures a portfolios likelihood of outperforming the benchmark.”

This measurement can be used to rank several portfolios alongside each other. The benefits of this form of outperformance measurement are:

• The comparison can take place regardless of the starting capital of each portfolio. • Continuous outperformance over the period is ranked above short periods of large

outperformance, which create the false perception of overall outperformance. • The returns do not have to adhere to a normal statistical distribution, which would

typically interfere with the result.

2. Downside Deviation Factor

It would be generally agreed that when a portfolio has loss trades, it’s best if they aren’t too big and don’t occur too often. This statement suggests there should be two dimensions to any risk measurement; magnitude and probability. The common risk measurement of Average Loss % provides the dimension of magnitude but not probability. An alternative measurement is Downside Deviation (DSD) which measures the variation of returns below a

SPA3 Revised Position Sizing | September 2012

Copyright Share Wealth Systems 2009 - 2012 Page 33 of 239

target return. The result is a value that not only provides the dimension of magnitude in a statistical manner but also includes the second dimension, the probability of Loss.

An investor expects that over a period of time that the risk, in the form of loses, experienced by their portfolio will be less than that of the benchmark. The perceived risk is loosely assessed by the investor in terms of the actual magnitude and frequency experienced, against the benchmark. The Downside Deviation Factor (DDF) is a measurement that allows the risk experienced by several portfolios to be accurately compared against that presented by a benchmark.

The DDF, takes the Downside Deviation (DSD) for a portfolio and compares it directly against the DSD for the chosen benchmark.

“The DDF represents how much more or less risk, by a factor, a portfolio presents compared to the benchmark.”

The DDF ranges between 0 and 2, with a factor of 1 meaning that the portfolio offers the same risk as the benchmark. A factor below 1 means that the portfolio offers less risk, and a factor greater than 1 means that it offers more risk.

(Note, the DDF range is not linear so don’t interpret a DDF of 2 as twice as much risk. In fact it’s a lot more than that!)