revitalization: the success of new postal...

TRANSCRIPT

Revitalization:

The Success Of New Postal ModelsAchieving High Performance in the Postal Industry

Accenture Research and Insights 2014

2

High-performing postal organization research

While the industry remains in transition, we are seeing successful

strategies emerge that prove postal organizations can thrive.

Copyright © 2014 Accenture All rights reserved.

2009 2010 2011 2012 20132006

3

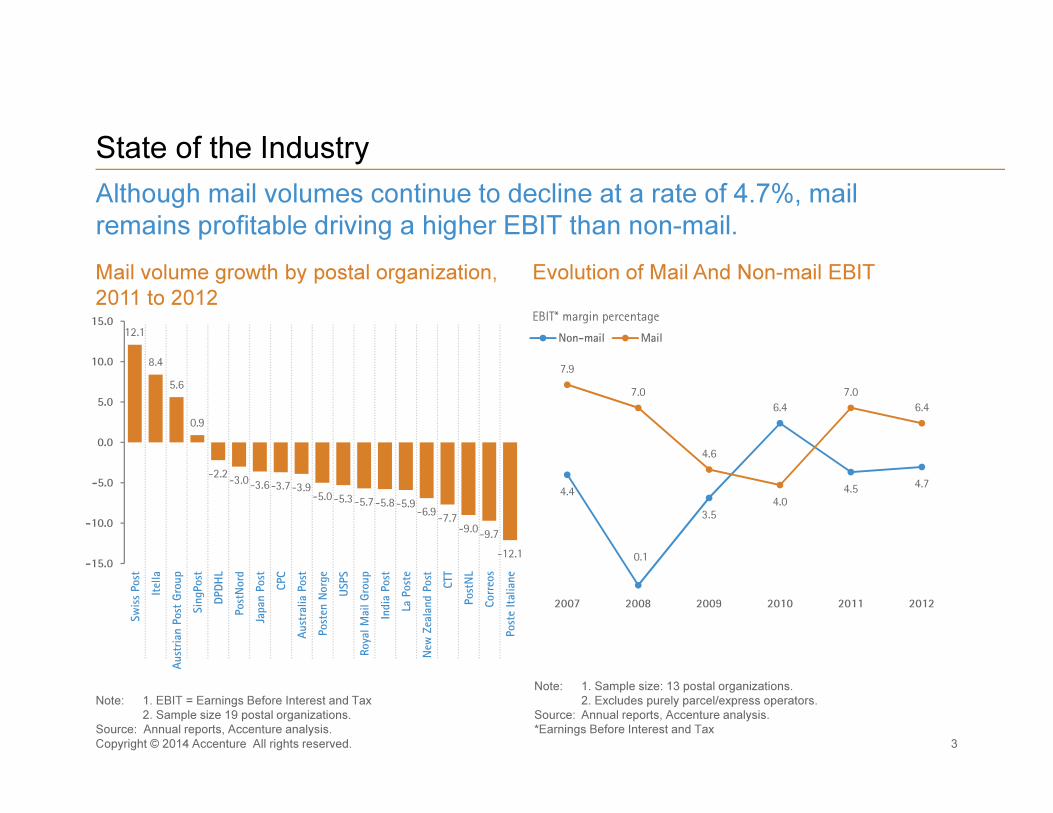

State of the Industry

Although mail volumes continue to decline at a rate of 4.7%, mail

remains profitable driving a higher EBIT than non-mail.

Copyright © 2014 Accenture All rights reserved.

Note: 1. EBIT = Earnings Before Interest and Tax

2. Sample size 19 postal organizations.

Source: Annual reports, Accenture analysis.

Mail volume growth by postal organization,

2011 to 2012

Evolution of Mail And Non-mail EBIT

12.1

8.4

5.6

0.9

-2.2-3.0-3.6-3.7-3.9

-5.0-5.3-5.7-5.8-5.9-6.9

-7.7-9.0-9.7

-12.1-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

Sw

iss

Post

Itel

la

Aust

rian P

ost

Gro

up

Sin

gPost

DPD

HL

Post

Nord

Japan P

ost

CPC

Aust

ralia P

ost

Post

en N

org

e

USPS

Roya

l M

ail G

roup

India

Post

La P

ost

e

New

Zea

land P

ost

CTT

Post

NL

Corr

eos

Post

e It

alia

ne

4.4

0.1

3.5

6.4

4.5 4.7

7.9

7.0

4.6

4.0

7.0

6.4

2007 2008 2009 2010 2011 2012

Non-mail Mail

EBIT* margin percentage

Note: 1. Sample size: 13 postal organizations.

2. Excludes purely parcel/express operators.

Source: Annual reports, Accenture analysis.

*Earnings Before Interest and Tax

For the first time, revenue from non-mail activities (parcels, retail,

financial services and logistics) exceeded mail revenue, 52% to 48%.

Diversification success

Copyright © 2014 Accenture All rights reserved. 4

Note: Revenue diversification is based on business unit breakdown and numbers reported in the company annual reports. Accenture categorizes revenue into

the above groups based on its understanding of activities which represent an approximation of diversification.

Source: Annual reports, Accenture analysis

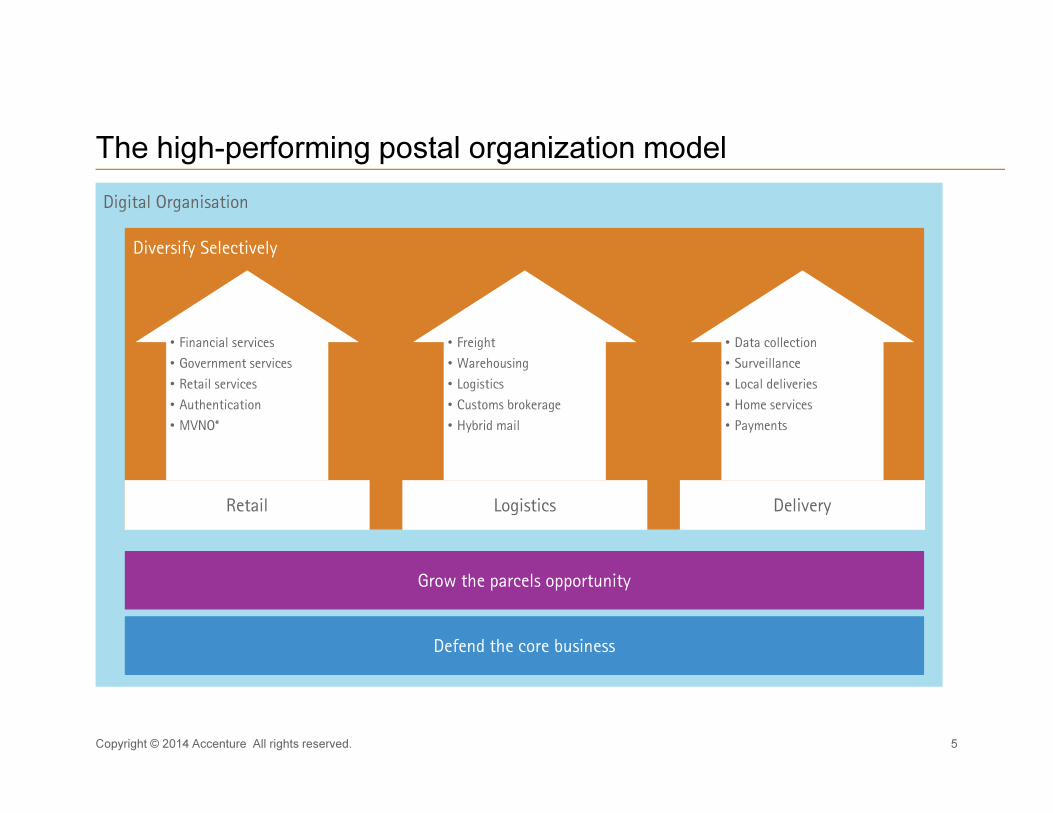

The high-performing postal organization model

Digital Organisation

Diversify Selectively

Grow the parcels opportunity

Defend the core business

Retail Logistics Delivery

• Financial services

• Government services

• Retail services

• Authentication

• MVNO*

• Freight

• Warehousing

• Logistics

• Customs brokerage

• Hybrid mail

• Data collection

• Surveillance

• Local deliveries

• Home services

• Payments

Copyright © 2014 Accenture All rights reserved. 5

2014 Key insights

and Implications

6Copyright © 2014 Accenture All rights reserved.

Finding 1: High performers achieve core business excellence

with diversification at scale

7

Revenue Growth by Performer

Group

Mail Volume, Revenue and EBIT

by Performer Group

13.9

-1.8-2.6

4.0

1.3

-5.4

4.9

-1.7

0.5

-3.5

-5.4-5.9

-3.1

-5.9

-10

-5

0

5

10

15

-2.4

Mail Rev.

Growth 2011-12

Mail Vol.

Growth 2011-12

Mail EBIT

% in 2012

Note: CAGR = compound annual growth rate

Source: Accenture analysis

Copyright © 2014 Accenture All rights reserved.

Success in the mail business is driven both by cost control as well as

adding value to mail through innovation.

Top 5 Bottom 5Lagging 5Middle 10Next 5

3.23.23.8

0.9

2.63.3

0.60.6

3.3

-1.6

-3.8

-1.7 -1.7-1.7-2.4

-10

-5

0

5

10

15

Revenue growth

2011-2012

5 year revenue

CAGR

3 year revenue

CAGR

Middle 10Next 5 Lagging 5 Bottom 5Top 5

High performers have achieved scale and market dominance in two

diversified market areas.

Finding 1: High performers achieve core business excellence

with diversification at scale

Copyright © 2014 Accenture All rights reserved. 8

Note: 1) Excluding Correios Brasileiros, Japan Post, TNT, FedEx, UPS because of non availability of data for 2009/2012; Dominant Area is defined as a number one or two

in terms of market position or a market share above 25%.

Sources: Accenture High Performance Post research; Operators’ annual reports; IPC website; Accenture analysis

Evolution of Mail and Non-Mail

Revenue, 2009-2012, B Euros

Diversification Areas by Performer

Group

21018

19791

106

Revenue

Growth

’09-’12

-4

Total

Revenue

’09

Non-Mail

Revenue

Growth

’09-’12

Total

Revenue

’12

Non-Mail

Revenue

’09

Revenue

’09

6.09% growth in

CAGR came from

non-mail revenue

-1.36% decline in

CAGR came from

Mail revenue

2.4

11.6

2.4

6.4

2.0

8.1

1.2

6.6

1.2

7.0

0

5

10

15

Dominant Areas of

Diversification(1)

Total Areas of Diversification

Bottom 5Next 5 Lagging 5Middle 10Top 5

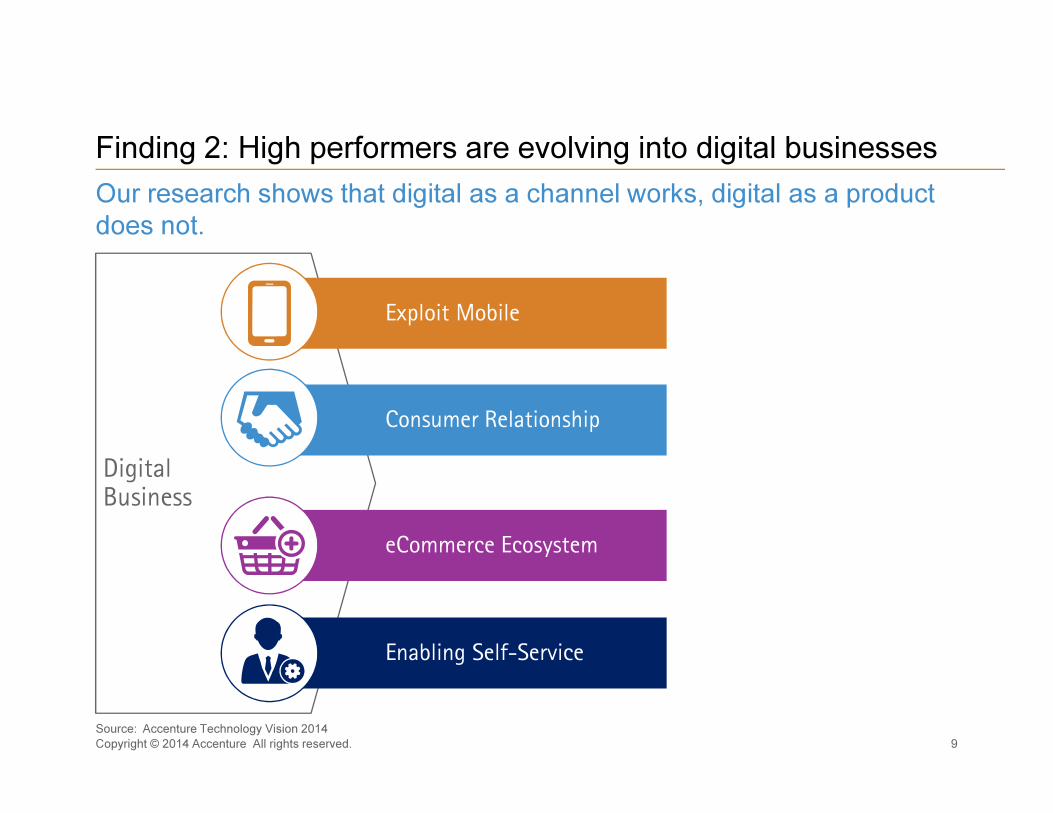

Our research shows that digital as a channel works, digital as a product

does not.

Finding 2: High performers are evolving into digital businesses

Copyright © 2014 Accenture All rights reserved. 9

Digital Business

Exploit Mobile

Consumer Relationship

eCommerce Ecosystem

Enabling Self-Service

Source: Accenture Technology Vision 2014

Tracking

Notifications

Deliveryscheduling

Accelerateddelivery

DeliveryinstructionsSecure delivery/

retrieval

Manage returns

Releaseauthorization

Alternate recipient authorization

Redirect

40%

50%

60%

70%

80%

90%

10% 20% 30% 40% 50% 60% 70% 80%

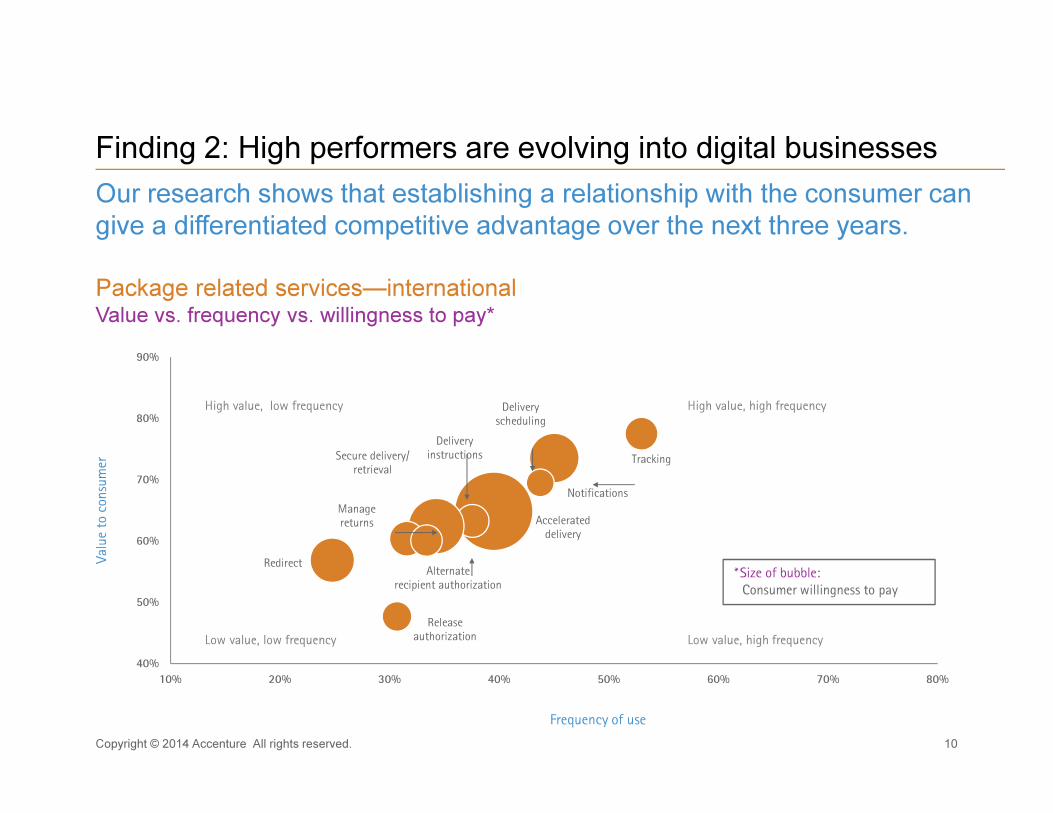

Our research shows that establishing a relationship with the consumer can

give a differentiated competitive advantage over the next three years.

Finding 2: High performers are evolving into digital businesses

High value, low frequency

Low value, high frequencyLow value, low frequency

Valu

e to

consu

mer

Frequency of use

* Size of bubble:

Consumer willingness to pay

High value, high frequency

Package related services—internationalValue vs. frequency vs. willingness to pay*

10Copyright © 2014 Accenture All rights reserved.

High performers are able to operate using a commercial versus a political

decision-making process.

Finding 3:

High performers operate with a strong commercial focus

Copyright © 2014 Accenture All rights reserved.

Note: Degree of liberalization calculated based on the following point scale: 0 = Reserved Area still intact; not liberalized; 0.5 = liberalized less than 3 years ago;

1 = Never liberalized or liberalized over 3 years ago

Source: Postal websites; Accenture Analysis

Commercial Focus Social Focus

Government intervention Limited government

intervention in postal

activities or decisions –

government outlines

commercial mandate.

Political considerations and

intervention in operations

favor a specific policy

or social mandate.

Strategic decision making Driven by Board and

executive committee.

Driven by department

and regulator.

Strategic focus Achieve profitability and

long-term financial

sustainability.

Focused on revenues and

delivering public service.

Mergers and acquisitions Conduct mergers and

acquisitions to grow

inorganically and seize

opportunities.

Limited ability to conduct

mergers and acquisitions –

require department or

regulator approval.

Talent management Able to hire at market rates

and attract talent from other

sectors of interest and build

and maintain centers

of excellence.

Government salary and

banding policies apply to the

postal operator and limit the

ability to attract and retain

talent.

Performer groups 2014

0.0

0.2

0.4

0.6

0.8

1.0

0.0 0.2 0.4 0.6 0.8 1.0

Deg

ree

of

liber

aliza

tion

Degree of private ownership

Bottom 10

Middle 10

Top 10

11

Parcel volumes continue to climb and are a strong driver of growth.

Finding 4: High performers are transforming their parcel

networks to seize market share

Copyright © 2014 Accenture All rights reserved.

Note: Parcel revenue is based on annual report data and may not include all express and courier volume.

Source: Accenture Analysis, Annual Reports

42.1

9.8

7.5

5.6 5.6 5.54.7

4.33.7 3.7 3.4 3.2 3.2

2.5 2.5

-2.3 -2.5-3.1

-4.8-6

-4

-2

0

2

4

6

8

10

12

14

India

Post

DPD

HL

USPS

Post

NL

Yam

ato

La P

ost

e

bpost

Roya

l M

ail G

roup

Post

e It

aliane

Sw

iss

Post

Itel

la

Aust

rian P

ost

Gro

up

UPS

Fed

Ex

CPC

Japan P

ost

CTT

Post

en N

org

e

Corr

eos

43

12

13

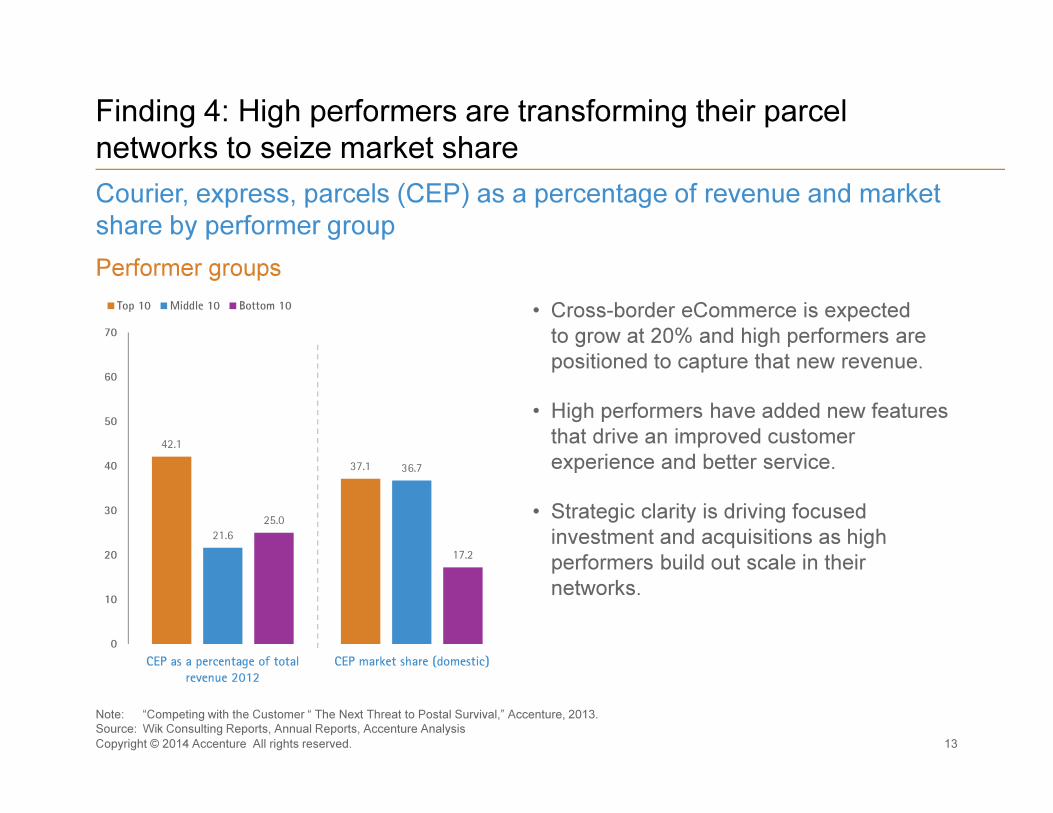

Finding 4: High performers are transforming their parcel

networks to seize market share

Courier, express, parcels (CEP) as a percentage of revenue and market

share by performer group

• Cross-border eCommerce is expected

to grow at 20% and high performers are

positioned to capture that new revenue.

• High performers have added new features

that drive an improved customer

experience and better service.

• Strategic clarity is driving focused

investment and acquisitions as high

performers build out scale in their

networks.

Copyright © 2014 Accenture All rights reserved.

Note: “Competing with the Customer “ The Next Threat to Postal Survival,” Accenture, 2013.

Source: Wik Consulting Reports, Annual Reports, Accenture Analysis

42.1

37.1

21.6

36.7

25.0

17.2

0

10

20

30

40

50

60

70

CEP as a percentage of total

revenue 2012

CEP market share (domestic)

Top 10 Middle 10 Bottom 10

Performer groups

14Copyright © 2014 Accenture All rights reserved.

On the horizon

While B2C eCommerce is growing at 17% globally, parcel volumes in our

study have been growing at less than 5%. Competitors are taking

significant volumes.

On the horizon

Copyright © 2014 Accenture All rights reserved. 15

Global Integrators

Domestic Competitors

eTailers/Retailers

• Expanding network to add new lanes• Leveraging domestic carriers for extended last mile• Negotiating global terms which simplifies integration

• New domestic or regional carriers growing quickly• Experimenting with last mile solutions• Range from full-service solutions to niche services (ie same day)

• Experimenting with click-and-collect/ship-to-store solutions• Intend to own delivery in key markets• Aggressively pursuing alternatives (eBay buys Shutl, Amazon

drones)

16

On the horizon

Digital economy

Identity services

As eCommerce becomes more integrated

into our daily lives and we become a more

“digital society,” identity management and

authentication will become far more

important.

Mobile commerce

Mobile commerce will grow significantly over

the next 5 years and will require a new type

of shipping interaction that involves

eliminating keystrokes and creating single-

click convenience.

Analytics

Postal organizations have a wealth of data

around customers and operations they can

use to capture a competitive edge.

Emerging technology

Drones

Drone solutions will be effective not just for

rural, hard to reach places but also in the

center of mega-cities as congestion drives

up the cost of delivery.

3D printing

Expanded production capabilities and more

readily accessible designs are creating new

consumer focused solutions that could be

accessed through postal retail outlets.

Robotics

From warehouse automation to driverless

vehicles, the possibility to replace labor and

become 24/7.

Copyright © 2014 Accenture All rights reserved.

What does it take to be a high performer?

Talent

Transformation

• Less in mail, more in new business lines

• New knowledge workers and digital talent

• Additional flexibility

Customer Focus

• Customer segmentation and CRM

• Relationships with senders and recipients

• Better cross-channel experience

Manage by Data

• Customer and operational analytics

• Predictive solutions

• Big data

Governance

• Commercial focused decision making

• Over-diversification

• Challenging the USO

Investment

Strategy

• Balanced investment for growth and

efficiency

• Drive to scale in new areas

• Mergers and acquisitions

17Copyright © 2014 Accenture All rights reserved.

To discover more about how postal organizations can achieve high

performance, please contact:

Andre Pharand

Brody Buhler

Contact us

Copyright © 2014 Accenture All rights reserved. 18