rewarding risk: the russian insurance market in 2013 · rewarding risk: the russian insurance...

TRANSCRIPT

Rewarding risk: The Russian

insurance market in 2013

June 2013

kpmg.ru

KPMG in Russia and the CIS

2 | Rewarding risk

The continued strong insurance premium growth in Russia appears lucrative compared with the global average. The

insurance industry is forecast to grow to RUB930bn (ex OMI) in 2013 which reaffirms Russia’s place among the world’s leading

insurance markets. Ensuing expansion of credit lending, albeit at a reduced pace than in 2012, is cited as the prime growth driver.

Despite prevailing growth, pressure on profit margins remains stubbornly intact and companies have confirmed to be diversifying

focus away from solely managing premium growth towards improving profitability through mostly monitoring expenses and quantifying risk.

Insurers can no longer afford to be spread across the entire market and will increasingly operate in only the segments where they have a

marked competitive advantage. Client centricity, service efficiency and continuous streamlining of the cost-base are emerging as the more prominent

competitive differentiators in this regard.

The Russian insurance market has experienced a number of significant regulatory changes in recent years, such an increase in statutory capital,

mandatory transition to IFRS and introduction of new compulsory segments, while the formation of a single financial mega regulator is underway. Despite

these developments, a majority of insurance executives highlight that insurance regulation in Russia is still a factor requiring further sustained attention, particularly

in the area of supervision of intermediaries and financial reporting.

Continued market growth coupled with the recent relaxation in the foreign capital quota presents a window of opportunity for entry of new foreign players. Though market

participants believe that M&A activity in the Russian insurance sector will pick up over 2013–2014, against recent periods, the feeling is that transactions will predominantly be

among the larger domestic players.

We invite you to explore these keynotes in greater detail in our fourth annual survey of the insurance industry in Russia. We also take this opportunity to thank our colleagues who

provided input and made this survey possible.

Enjoy, Adrian Quinton

Partner, CIS Head of Insurance and Actuarial Services

Adrian Quinton Partner, CIS Head of Insurance and Actuarial Services

Introduction

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Russian insurance market in 2013 | 3

Top line growth 07

Bottom line management 13

Market regulation 17

M&A activity 18

Executive summary 04

Contents

Stage of the insurance maturity cycle and key priorities 06

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

4 | Rewarding risk

KEY DEVELOPMENT PRIORITIES FOR INSURERSThe Russian insurance industry remains attractive as the market is likely to remain in the growth and development phase for another 3–5 years. That said, insurers ought to keep a close eye on maintaining distinct competitive advantage through the following key elements becoming evident in our survey:

● Defining and targeting market segments and associated distribution channels where they have a distinct competitive advantage.

● Strengthening client centricity alongside improving service efficiency and quality.

● Optimising the cost base including enhancing risk management to enable a more tangible view on the size and nature of accepted risks.

GROWTH PROSPECTS ● Our respondents predict that the combined insurance

market will grow by 10–15% in 2013, propelling it to between RUB890bn–RUB930bn, which is just short of the pivotal RUB1trn milestone. Economic growth which was headlined as the main growth factor in last year’s survey was not marked as the prominent contributor to growth in 2013, which is perhaps linked to a dampened forecast on GDP growth for Russia.

Insurers feel that overall market growth in 2013 will for the most part be supported by the continuing boom in retail credit lending (which is forecast to increase by 30%*) and regulatory factors (such as the recently introduced mandatory insurance of Passenger Carrier’s Liability).

● In 2013, Casco will be the dominant contributor to expansion of the non-life market. As in previous years, growth is primarily supported by the increase in consumer lending.

● Life insurance is the fastest growing segment today. Gross premiums grew by an impressive CAGR of 63% translating to a RUB23bn to RUB53bn leap in market size from 2010 to 2012, which has led to an improved share of life insurance in the total voluntary insurance market of 8% from 5%. It is expected that the double digit growth of 30-50% will prevail, fuelled by the increase in the volume of mortgage lending forecasted at 15-20% for 2013**.

● Banks continue to be the fastest growing insurance distribution channel in 2013. Market players participating in the Casco, Life and Accident lines will have the opportunity to boost premiums in these segments, albeit at the expense of reduced profit due to upscale commissions demanded by the banking groups.

IMPROVING EFFICIENCY ● Corporate property insurance maintains its status as the

industry’s profit centre while other mass-market lines such as Casco, Osago and Voluntary Medical Insurance (‘VMI’), will generate only marginal profits in view of intense competition in these segments.

● As in 2012, optimisaton of administration and acquisition expenditure remains an area of key importance for most insurers, though some of the focus has diversified towards reducing claims costs.

● The preferred methods of keeping the cost of claims under control in 2013 are fostering improved relationships with business partners (car dealerships, health care clinics, etc), enhancement of the process for monitoring and settlement of court-originated claims as well as improving the processing of subrogation claims.

Executive summary

** Forecast of the household mortgage agency.* Forecast of the Central Bank of Russia.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Russian insurance market in 2013 | 5

MARKET REGULATION ● Senior executives maintain the view that the market

is in need of progressive regulatory and legal reform. In their view, the areas that require the most intervention are regulation and supervision of financial reporting and enhanced monitoring of brokers and intermediaries. With reference to the latter, the specific items pointed out in our survey are oversight of commission levels, client-intermediary-provider linkages and broker licensing.

● In the near future, market participants foresee a decline in profitability of OSAGO due to the anticipated adverse impact of legislative reforms under discussion, such as the extension of the law on consumer protection and the uncertainty around lifting tariffs to compensate for the corresponding expected increase in OSAGO limits.

M&A ACTIVITY ● Market participants believe that the Top 10 segment will

improve its market share by more than 2% in 2013. It is expected that the speeding up of consolidation will be supported by a rise in M&A activity among large domestic players.

● The assessment of premium multiples, expressed as the ratio of the company’s price to gross premium, has softened since 2012, which is suggestive of a more cautious outlook on future market growth and the economy in general.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

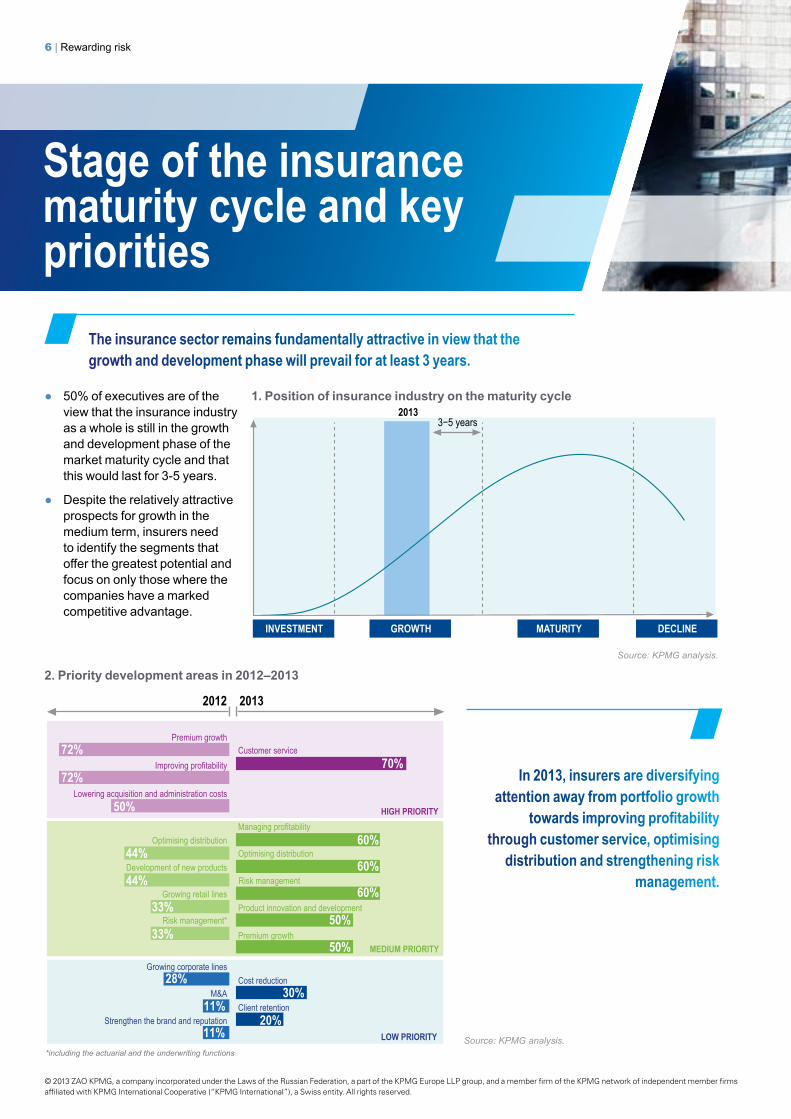

6 | Rewarding risk

20133−5 years

INVESTMENT GROWTH MATURITY DECLINE

The insurance sector remains fundamentally attractive in view that the growth and development phase will prevail for at least 3 years.

● 50% of executives are of the view that the insurance industry as a whole is still in the growth and development phase of the market maturity cycle and that this would last for 3-5 years.

● Despite the relatively attractive prospects for growth in the medium term, insurers need to identify the segments that offer the greatest potential and focus on only those where the companies have a marked competitive advantage.

Source: KPMG analysis.

Stage of the insurance maturity cycle and key priorities

In 2013, insurers are diversifying attention away from portfolio growth

towards improving profitability through customer service, optimising

distribution and strengthening risk management.

2. Priority development areas in 2012–2013

72%

72%

50%

44%

44%

33%

33%

28%

11%

11%

Premium growth

Improving profitability

Lowering acquisition and administration costs

Optimising distribution

Development of new products

Growing retail lines

Risk management*

Growing corporate lines

M&A

Strengthen the brand and reputation

70%

60%

60%

60%

50%

50%

30%

20%

Customer service

*including the actuarial and the underwriting functions

Client retention

Cost reduction

Premium growth

Product innovation and development

Risk management

Optimising distribution

Managing profitabilityHIGH PRIORITY

MEDIUM PRIORITY

LOW PRIORITY

2012 2013

Source: KPMG analysis.

1. Position of insurance industry on the maturity cycle

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

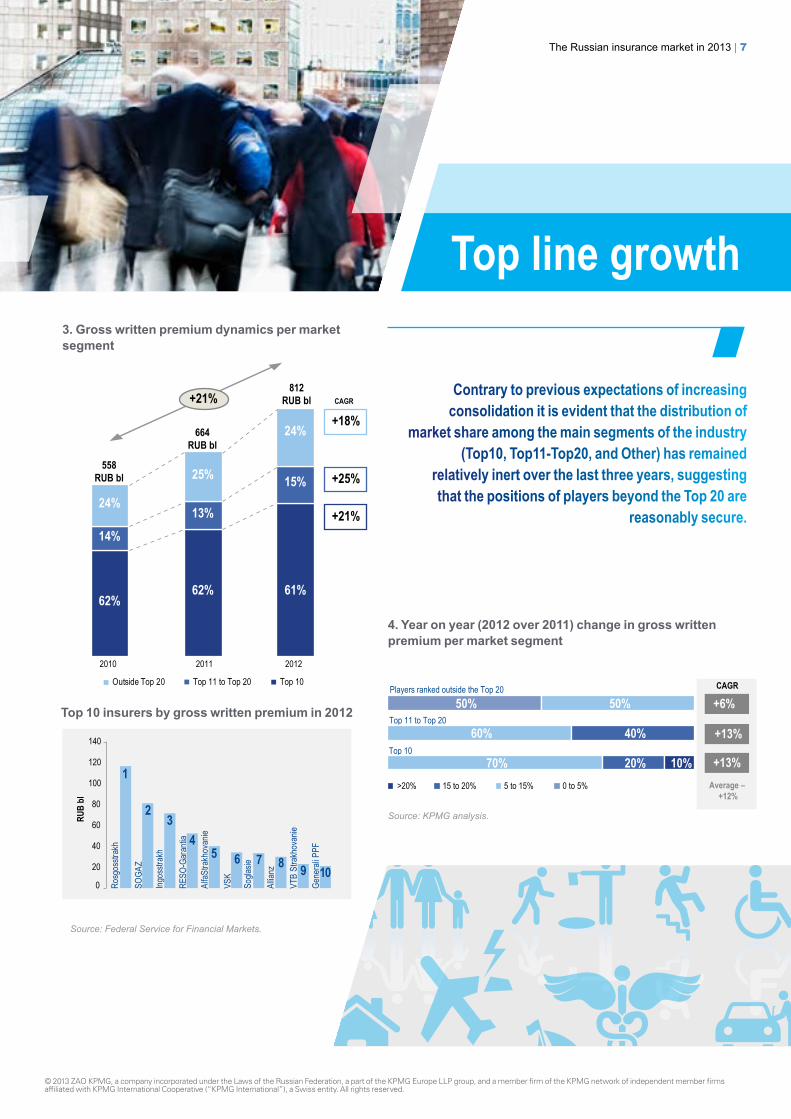

The Russian insurance market in 2013 | 7

3. Gross written premium dynamics per market segment

4. Year on year (2012 over 2011) change in gross written premium per market segment

Source: Federal Service for Financial Markets.

Top line growth

Contrary to previous expectations of increasing consolidation it is evident that the distribution of

market share among the main segments of the industry (Top10, Top11-Top20, and Other) has remained

relatively inert over the last three years, suggesting that the positions of players beyond the Top 20 are

reasonably secure.

Outside Top 20 Top 11 to Top 20 Top 10

Players ranked outside the Top 20

Top 11 to Top 20

Top 10

>20% 15 to 20% 5 to 15% 0 to 5%

+6%

+13%

+13%Average –

+12%

CAGR

50%

70%

60%

50%

20%

40%

10%

2010 2011 2012

62%62%

14%13%

24%

25%558

RUB bl

664RUB bl

+18%

+25%

+21%

CAGR

61%

15%

24%

812RUB bl+21%

0

20

40

60

80

100

RUB

bl

VSK

Ingos

strak

h

SOGA

Z

Rosg

osstr

akh

Gene

rali P

PF

VTB

Stra

khov

anie

Allia

nz

RESO

-Gar

antia

Sogla

sie

AlfaS

trakh

ovan

ie

1

23

45 6 7 8 9 10

120

140

Outside Top 20 Top 11 to Top 20 Top 10

Players ranked outside the Top 20

Top 11 to Top 20

Top 10

>20% 15 to 20% 5 to 15% 0 to 5%

+6%

+13%

+13%Average –

+12%

CAGR

50%

70%

60%

50%

20%

40%

10%

2010 2011 2012

62%62%

14%13%

24%

25%558

RUB bl

664RUB bl

+18%

+25%

+21%

CAGR

61%

15%

24%

812RUB bl+21%

0

20

40

60

80

100

RUB

bl

VSK

Ingos

strak

h

SOGA

Z

Rosg

osstr

akh

Gene

rali P

PF

VTB

Stra

khov

anie

Allia

nz

RESO

-Gar

antia

Sogla

sie

AlfaS

trakh

ovan

ie1

23

45 6 7 8 9 10

120

140

Top 10 insurers by gross written premium in 2012

Source: KPMG analysis.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

8 | Rewarding risk

5. Premium growth drivers in 2013

HIGH PRIORITY

MEDIUM PRIORITY

LOW PRIORITY

70%

70%

50%

50%

40%

40%

40%

30%

10%Infrastructure growth and development

Intermediaries

Competition

Business partners

Compulsory classes of insurance

Improvement in the culture and awareness of insurance

Economic growth

Regulation and legislation

Volume of bank lending

Source: KPMG analysis.

● In 2013, the market expects a slowing in pace of growth of credit finance relative to 2012 figures. For example, the volume of loans to individuals is forecast to increase by 30%* compared with 40% in 2012 while the growth rate in corporate lending is expected to remain at the 2012 level of 15%.

● The deceleration of the pace of credit lending in the retail sector may slow growth in the auto, life and accident insurance segments. Despite this, credit finance is still marked as the primary growth driver in 2013.

● The slowdown in the Russian economy in 2013 (GDP is set to reach 2.4%**) has reduced the importance of GDP relative to last year when 78% of managers reported economic growth as the main driver of insurance market growth.

Life insurance and accident insurance grew remarkably from 2010 to 2012 which caused this segment to significantly increase its share in the voluntary insurance market

Source: KPMG analysis.

31% 31% 30%

31% 31% 28%

19% 18% 17%

8% 9% 12%

6% 5% 5% 5% 6% 8%

Доля основных сегментов добровольного страхования по размеру страховой премии с 2010 по 2012

2010 2011 2012

Liability

Accident

VMI

Property

Casco

Life +3%−1%+4%

−2%

−3%

−1%

CAGR

6. Premium share by key segment in 2010–2012

The growth of the insurance market will be primarily upheld by an increase in credit lending and legislative reform

* Forecast of the Central Bank of Russia. ** Forecast of the Ministry of Economic Development.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Russian insurance market in 2013 | 9

9. Expected premium growth in 2013 over 2012 per segment

>20% 15 to 20% 5 to 15% 0 to 5%

+12%

+11%

+11%

CAGR 2013

10%

20%

30%

50%

90%

80%

40%

40%

10%

10%

20%

30%

20%

10%

Liability

Accident

VMI

Property

Casco

5)Expected premium growth in 2013 over 2012 per segment

30%

10%

+16%

+18%

+19%

+13%

+13%

CAGR 2010−2012

+43%

+6%

7. Gross written premium growth dynamics per line

196

75

30

53

139

3727 23

165

49

28 35

2010 20112012

CASCO Casualty Liability Life

RUBb

l

+19%

10986

97

VMI

+13%

180

140

169

Property

+13%

+43%

+6%+63%

The dominant segments of non-life insurance will continue to prosper at double digit rates in 2013, though the pace of growth

has slowed. As before, Casco and Property insurance will be the largest contributors to growth of the market

Source: KPMG analysis.

8. Outlook of the pace of growth of non-life insurance in the near-term

33%

67%

Growth will be slowerthan in recent years,

but will remain attractive

Continue to grow at a relatively high growth rate

Source: KPMG analysis.

Sources: RBC, Federal Service for Financial Markets, KPMG analysis.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

10 | Rewarding risk

In the short term, the life market has a good chance to maintain the pace of growth achieved in 2010–2012 (63% CAGR)

10. Outlook of the pace of growth of life insurance in the near-term

Source: KPMG analysis.

10%

Moderate growth rates

Continue to grow at a relatively high growth rate

Growth will be slower thanin recent years, but will remain attractive

40%

50%

● One half of respondents note that the pace of growth of the life insurance market may be supressed against the impressive growth levels experienced in 2010-2012 but will remain at a generous range of 30% to 50%.

11. Life insurance growth drivers in the near term

HIGH PRIORITY

MEDIUM PRIORITY

LOW PRIORITY

60%

60%

50%

40%

30%

20%

The volume of mortgage lending

Improved tax benefits

Improving opportunities in investment activity

The pace of economic growth

Entrance of major banking groups into the insurance sector (eg, Sberbank)

Introduction of state guarantees on benefits

Source: KPMG analysis.

● The rise in mortgage lending by 15-20%* in 2013 will be the principal driver of growth in the life insurance market in 2013.

● As in 2012, the majority of executives (60%) are certain that improvement in the tax regime may significantly expand life insurance particularly in the corporate segment.

*Forecast of the household mortgage agency

In 2013 the level of market premium rates for the main classes of insurance will not change relative to the previous year

12. Change in the level of market premium rates in 2013 relative to 2012 per segment

33%

11%

12%

12%

22%

11%

33%

12%

12%

56%

33%

44%

44%

33%

22%

44%

11%

33%

11%

11%

Liability

Accident

VMI

Property

Casco

6) Market premium rates in 2013 relative to 2012

<90% 95% 100% 105% >110%

+1%

–3%

+1%

CAGR

–1%

–4%

Source: KPMG analysis.

● The higher losses in Casco and VMI will deter further price dumping on the part of insurers. For this reason, most executives believe that insurance rates will remain either at the level of 2012 or increase only slighty.

● The comparatively attractive profitability of property insurance will not entice price cuts in 2013. If rates do decrease it would be by not more than 1-3% against the previous year.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Russian insurance market in 2013 | 11

11. Life insurance growth drivers in the near term

10%30%

40%40%

50%50%

70%

50%50%30%

40%50%50%

20%

20%30%

20%

10%

Independent agents

Tied agents

Own points of sale (offices and branches)

Brokers

Direct

Car dealers and other business partners

Banks

Year on year change (2013 over 2012) in gross written premium by distribution channel

20%Increase Stay the same Decrease Increase Stay the same Decrease

20%

10%

40%

70%

100%

80%

90%

50% 10%

Independent agents

Tied agents

Broker

Car dealers and other business partners

Banks

10%

20%

The banking channel remains the fastest-growing insurance sales channel in 2013

The rising influence of the banking channel will spur increases in commission. The level of commissions

will generally remain at last year’s level among other key channels

● The expansion of the banking channel will drive sales of life and accident insurance where the dominant share of premium income in these segments (50% *) is collected through banks.

● The share of motor insurance sales will continue to increase at the already familiar dealership channel while a growing portion of sales is derived via the the online channel, which is still in its early stages of development.

13. Year on year change (2013 over 2012) in gross written premium by distribution channel

14. Year on year change (2013 over 2012) in commission rates by distribution channels

*Expert RA

Source: KPMG analysis. Source: KPMG analysis.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

12 | Rewarding risk

Changes in the relative importance of purchasing criteria differ between the retail and the corporate segment: with reference to the former, price and speed of claims settlement have become more important in 2013 whereas service quality and financial stability are now preferred more in respect of corporate insurance

15. Change in the relative importance of the purchasing criteria in 2013 (from 2012) from the perspective of retail clients

50%

30%

60%

70%

40%

60%

50%

60%

40%

30%

50%

40%

10%

10%

Positive prior experience with the Company

Brand

Quality of client service (excluding speed of claims settlement)

Speed of claims settlement

Financial stability

Price

22) Change in the relative importance of the purchasing criteria in 2013 (from 2012) from the perspective of retail clients

Increase Stay the same Decrease

16. Change in the relative importance of the purchasing criteria in 2013 (from 2012) from the perspective of corporate clients

50%

10%

60%

30%

70%

30%

50%

80%

40%

70%

20%

60%

10%

10%

10%

Positive prior experience with the Company

Brand

Quality of client service (excluding speed of claims settlement)

Speed of claims settlement

Financial stability

Price

Increase Stay the same Decrease

Source: KPMG analysis. Source: KPMG analysis.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Russian insurance market in 2013 | 13

Casco, OSAGO and VMI continue to be the least profitable lines

17. Ranges of estimates of the IFRS loss ratio per segment in 2012–2013

2012 2013

29%

14%

57%

43%

100%

43%

14%

14%

43%

29%

57%

86%

71%

Liability

Accident

VMI

Osago

Property

Casco

10) Ranges of estimates of the IFRS loss ratio per segment in 2013

>90% [70%; 90%] [50%; 70%] < 50%

37%

6% 50%

88%

63%

44%

12%

82%Liability

Accident

VMI

Osago

Property

Casco25% 69% 6%

75% 19% 6%

18%

Bottom line management

● This year the respondents’ expectations on the loss ratio for Casco are more concentrated than in 2012 as 100% of participants predict the loss ratio will be in the interval [70%-90%], whereas in 2012 a quarter of respondents predicted a more favourable range [50%-70%].

● More than half of executives anticipate that the loss ratio for OSAGO will be above 70% in 2013 though it is difficult to predict the ultimate result with reasonable certainty in view of the ensuing industry debate on lifting of OSAGO limits and tariffs.

● Based on responses, our colleagues anticipate that the underwriting performance of VMI will improve in 2013 over 2012. Despite this, VMI remains the least profitable segment and almost a third of respondents cite that the loss ratio will be above 90% this year.

Source: KPMG analysis.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

14 | Rewarding risk

18. Ranges of estimates of the IFRS combined loss ratio per segment in 2012–2013

57%

29%

43%

14%

29%

57%

43%

86%

100%

14%

14%

100%

14%

>100% [90%; 100%] < 90%

Liability

Accident

VMI

Osago

Property

Casco

6%

19%

12%

50%

56%

50%

100%

18%

44%

25%

100%

38%

82%

2012 2013

Liability

Accident

VMI

Osago

Property

Casco

● The overall market perception is a trend to declining profitability in Casco with 43% of the respondents expecting a combined ratio of over 100% in 2013.

Despite the low profitability, Casco generates cash, facilitates cross-sales and supports

the brand which suggests that only a few players would actually withdraw from this line altogether.

● Property insurance is set to remain the most attractive segment in terms of own profit margin and contribution to overall profit.

Developing the asset management function is not a priority for insurers as immediate opportunities for improving investment income are not obvious

10%

30%

60%

Yes, we see a goodopportunity in this

Yes, we have plans for this, but the scope for improving

investment returns is not clear

No, we do not see the rationale for this

19. Companies' views on improvement of the asset management function in the near term (2013–2014)

Source: KPMG analysis.

Source: KPMG analysis.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Russian insurance market in 2013 | 15

Optimisation of administration and acquisition expenses will remain a priority for insurance companies in 2013, though the importance of these

areas has decreased due to a shift of attention towards reducing claims costs. In particular, insurers are planning to pay increased attention to

subrogation and court-originated claims

20. Components of the bottom line to be optimised in 2012–2013

2012 2013

10) Ranges of estimates of the IFRS loss ratio per segment in 2013

40%

50%

70%

60%

50%

30%

Claims management costs

Acquisition costs

Administration costs

Greater degree Lesser degree

72%

33%

11%

28%

67%

89%

Claims management costs

Acquisition costs

Administration costs

Insurance companies intend to limit administration costs through reducing staff costs, improving organisational design and advancing operating models

HIGH PRIORITY

MEDIUM PRIORITY

LOW PRIORITY

50%

50%

50%

40%

30%

10%Reduction of rental costs

Not planning to significantly change the management of the above costs

Implement shared services

Improve operational models, including IT

Improve organisational design

Reduce employee costs without outsourcing

Source: KPMG analysis.

● Compared with 2012, the number of companies who do not plan to curtail administrative costs increased from 11% to 30%. This serves to underline that companies intend to diversify focus away from administration expenditure towards monitoring claims costs.

21. Methods aimed at reducing administration costs (2013–2014)

Source: KPMG analysis.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

16 | Rewarding risk

Optimisation of contractual relationships with intermediaries is a lower priority in 2013, though it remains an important avenue for managing acquisition costs

22. Preferred methods of containing acquisition costs in 2013

Source: KPMG analysis.

HIGH PRIORITY

MEDIUM PRIORITY

60%

60%

50%

30%Growth of the tied agent network

Improvement of direct channels

Development of internet sales

Optimisation of contractual relationships with intermediaries and business partners (e.g. banks, car dealers)

15) Preferred methods of containing acquisition costs in 2013

● Continued strengthening of the influence of banks and car dealers* in the market compels insurers to search for alternative methods of containing acquisition costs such as pursuing ways to improve direct distribution.

● The relative appeal of digitally-supported distribution via internet and telephone among companies has grown: in 2013 60% of executives replied that they intend to develop ‘digitial’ sales further compared to only 44% in 2012.

*Expert RA

Improving relationships with business partners (car dealers, clinics, etc) and enhancing the process for settling court-originated claims are the preferred methods aimed at reducing the cost of claims in 2013

HIGH PRIORITY

MEDIUM PRIORITY

LOW PRIORITY

67%

67%

56%

33%

33%

11%Exchange of claims data with other insurers

Segmentation of pricing using additional risk factors

Tougher anti-fraud management

Increasing application of deductibles and co-payments

Enhancing litigation processes

Improving relationships with business partners

13) Preferred methods for reduction of claims costs in 2013

Source: KPMG analysis.

23. Preferred methods for reduction of claims costs in 2013

Insurers intend to increase expenditure on internet marketing in 2013 to accommodate a growing online audience

24. Changes in marketing costs in 2013 relative to 2012

increase stay the same decrease

11%

11%

22%

78%

78%

89%

78%

22%

TV/Radio advertising

Street advertising

Telephone calls

Internet

16) Changes in marketing costs in 2013 relative to 2012

11%

Source: KPMG analysis.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Russian insurance market in 2013 | 17

Market regulation

Insurers maintain the view that the majority of areas of insurance regulation and legislation require

comprehensive reform

25. Areas of regulation and legislation that require progressive improvement in 2013–2014

HIGH PRIORITY

MEDIUM PRIORITY

60%

50%

50%

40%

70%

40%

30%

20%

10%

10% LOW PRIORITY Claims reporting/assessment

Fraud/Anti-money laundering

Competitive activity

Internet/telephone policy issuance

Tax benefits (centered on Life and VMI)

Investment policy

Pricing policy

Independent actuarial review

Risk Management and Governance

Capital Adequacy and Risk Based Capital

Supervision of brokers/intermediaries

Financial reporting

17) Areas of regulation and legislation that require progressive improvement in 2013 - 2014

40%

40%

Source: KPMG analysis.

● At the end of 2012, the activities for the creation of a single financial mega regulator in Russia were set in motion when the government agreed to integrate the Federal Financial Markets Service (‘FFMS’) with the Central Bank. It is expected that this measure will help improve transparency and effectivess of regulatory oversight of the entire financial services market, which will have a positive effect on the insurance industry. The majority of surveyed executives (70%) believe that in the first instance the new regulator ought to focus on improving the process for submission and review of financial statements of insurers.

● Agents and intermediaries remain the lifeblood of insurance distribution in Russia yet regulation and supervision of intermediaries remains relatively low key. Because of this, almost two-thirds of respondents (60%) would like to see improvements in regulation and legislation in this area, and, in particular, in the areas of oversight of commission levels, client-intermediary-insurer linkages and broker licensing.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

18 | Rewarding risk

M&A activity

Executives feel that the market share of the Top 10 segment will increase in 2013

Increase in market share of the Top 10 in 2013

>5%

30%

50%

20%

2% to 5%

0% to 2%

Source: KPMG analysis.

26. Increase in market share of the Top 10 in 2013

Under the assumption that the ongoing consolidation of the market will be primarily driven by M&A in 2013: 80% of executives expect that deals will largely be between leading Russian players

27. Likely M&A activity in 2013–2014

● The attractiveness of the Russian insurance sector in view of its high growth potential coupled with the recent relaxation of foreign capital quota (from 25% to 50%) presents a solid ground for the entry of new foreign players. Despite this only 10% of survey respondents feel that new foreign players will enter in 2013–2014, which is partly explained by the fact that many global insurers are still preoccupied with maintaining performance in their core markets.

30%

10%

10%

10%

20) M&A activity in 2013-2014

80%

40%

Entry of new foreign players

Exit of foreign players

Expansion of major Russian players in neighbouring markets (eg CIS,CEE,Asia)

Sale of one or more leading Russian insurers

Suspension or withdrawal of the insurance license of one or more leading players

Mergers and acquisitions among major Russian players

Source: KPMG analysis.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Russian insurance market in 2013 | 19

In 2013, pricing multiples expressed as “company market price/gross written premium” have declined in comparison with 2012 for all of the leading 30 players

28. Assessment of multiples per market segment in 2012–2013

2012 2013

80% 20%0−0.75 0.75−1 1−1.5 1.5−20−1 1−1.5 1.5−2

Top 31 to Top 50

Top 11 to Top 30

Top 1010% 20%30% 40%

40% 10%30% 20%Top 31 to Top 50

Top 11 to Top 30

Top 10

>2 >2

44%

6%

11%89%

50%

17% 33%44%

6%

● The decline in multiples is the prime reason for the wait-and-see attitude among market players. Sellers are not keen to give up their prize assets at relatively reduced prices and prefer to wait over the period of subdued economic conditions while the buyers are not willing to offer a premium over the local market price and over European multiples and are playing a wait and see game.

● Ultimately the market offers a golden chalice of sub 100% loss ratios and double digit growth coupled with a favourable economic climate supported by the government which suggests that deals will be done.

Source: KPMG analysis.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2013 ZAO KPMG, a company incorporated under the Laws of the Russian Federation, a part of the KPMG Europe LLP group, and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Russia.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

kpmg.ru

Adrian Quinton Head of Insurance and Actuarial services Partner T: +7 (495) 937 4477 E: [email protected]

Alexey NazarovManagement Consulting Director T: +7 (495) 937 4477 E: [email protected]

Julia TemkinaTransactions and RestructuringDirector T: +7 (495) 937 4477 E: [email protected]

Mikhail KlementievTax and LegalPartner T: +7 (495) 937 4477 E: [email protected]

Philip SementsovActuarial ServicesSenior Manager T: +7 (495) 937 4477 E: [email protected]

Contacts

KPMG Thought Leadership app