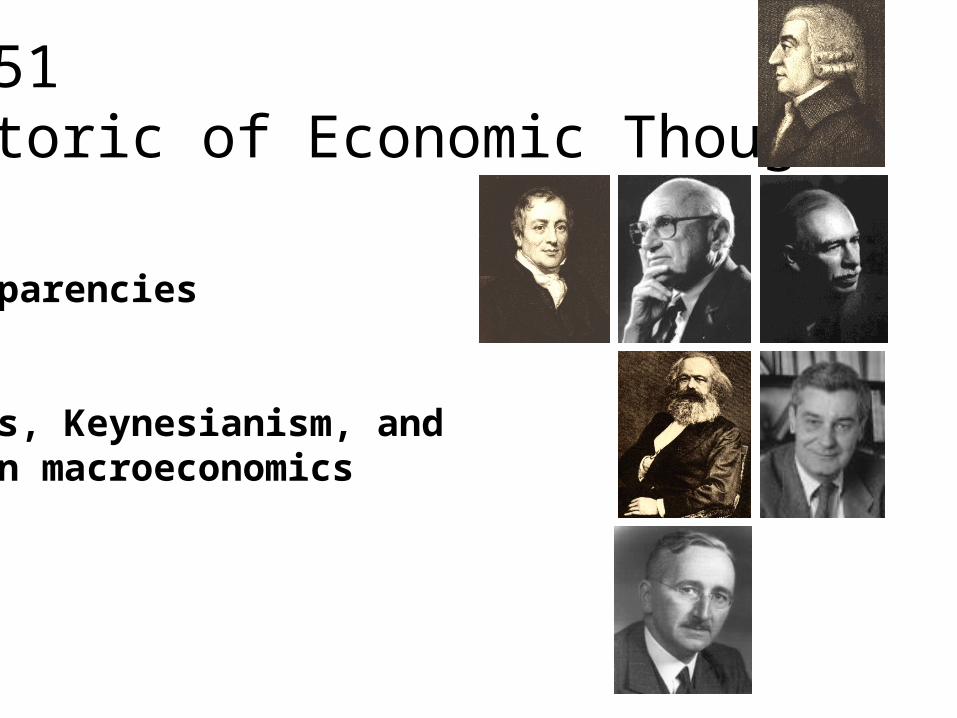

rh351 rhetoric of economic thought transparencies set 6 keynes, keynesianism, and modern...

Post on 22-Dec-2015

215 views

TRANSCRIPT

RH351Rhetoric of Economic Thought

TransparenciesSet 6

Keynes, Keynesianism, andmodern macroeconomics

Economic analysis – key contributors, 20th century

1900 2000

Joseph Schumpeter (1883 – 1950)

Thorstein Veblen (1857 – 1929)

Paul Samuelson (1915 – )

John Maynard Keynes (1883 – 1946)

Milton Friedman (1912 – )

Friedrich A. von Hayek (1899 – 1992)

Gary Becker (1930 – )

Alfred Marshall (1842 – 1924)

Lucas

Hayek

Friedman

Keynes

1950

Robert Lucas (1937 – )

Kenneth Arrow (1921 – )

Ronald Coase (1910 – )

Samuelson

John Maynard Keynes, 1883 – 1946

1883 Marx dies, Keynes born Early life Eaton / Cambridge – Studies under Marshall 1906 / 1909 British civil service / back to Cambridge 1914 – 1918 The Great War – At the Treasury, financing the war 1918 Versailles Peace Conference 1919 The Economic Consequences of the Peace 1921 Treatise on Probability 1923 Tract on Monetary Reform 1924 – 1925 Gold Standard debate in U.K. "Currency Policy and Unemployment" (1923) "Monetary Reform" (1924) "The Gold Standard Act" (1925) The Economic Consequences of Mr. Churchill (1925) 1926 The End of Laissez-Faire 1930 A Treatise on Money 1930 – 1935 Responses to “The Great Slump” 1936 General Theory of Employment, Interest, and Money 1939 – 1943 WWII, back at the Treasury 1944 Bretton Woods 1946 Keynes dies / Keynesianism is born

Biographical Details

G. E. Moore’s Principia Ethica (1903)

“… our causal knowledge is utterly insufficient to tell us

what different effects will probably result from two different actions, except within a comparatively short space of time … Our utter ignorance of the far future gives us no justification for saying that it is even probably right to choose the greater good within the region over which a probable forecast may extend … It does in fact appear to be the case that, in most cases, whatever action we now adopt, ‘it will be all the same a hundred years hence,’ … we can only hope to discover which, among a few alternatives, will generally produce the greatest balance of good in the immediate future.”

Chapter V, “Ethics in Relation to Conduct”, sections 93 and 94

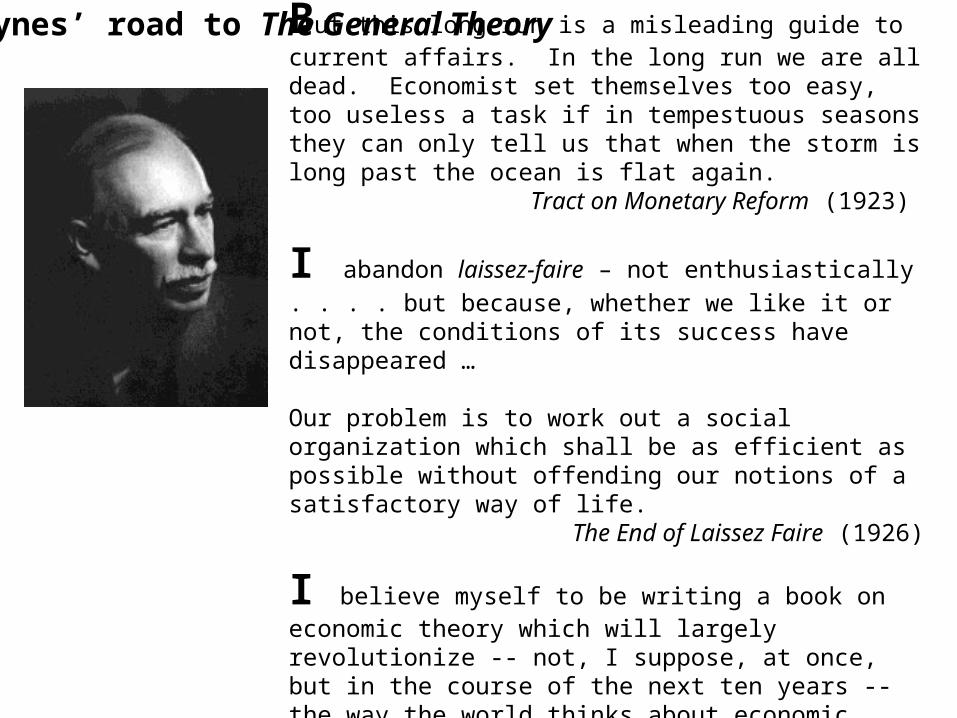

Keynes’ road to The General Theory

But this long run is a misleading guide to current affairs. In the long run we are all dead. Economist set themselves too easy, too useless a task if in tempestuous seasons they can only tell us that when the storm is long past the ocean is flat again.

Tract on Monetary Reform (1923)

I abandon laissez-faire – not enthusiastically . . . . but because,

whether we like it or not, the conditions of its success have disappeared …

Our problem is to work out a social organization which shall be as efficient as possible without offending our notions of a satisfactory way of life.

The End of Laissez Faire (1926)

I believe myself to be writing a book on economic theory which will largely revolutionize -- not, I suppose, at once, but in the course of the next ten years -- the way the world thinks about economic problems.

Letter to G.B. Shaw (1935)

The idea that we can safely neglect the aggregate demand function is fundamental to the Ricardian economics ... The celebrated optimum of traditional economic theory, which has led to economists being looked upon as Candide's ... is also to be traced, I think, to their having neglected to take account of the drag on prosperity which can be exercised by an insufficiency of effective demand ...

It may well be that the classical theory represents the way in which we should like our Economy to behave. But to assume that it actually does so is to assume our difficulties away.

Keynes, The General Theory -- Aggregate Demand

The General Theory (pp. 32 – 34)

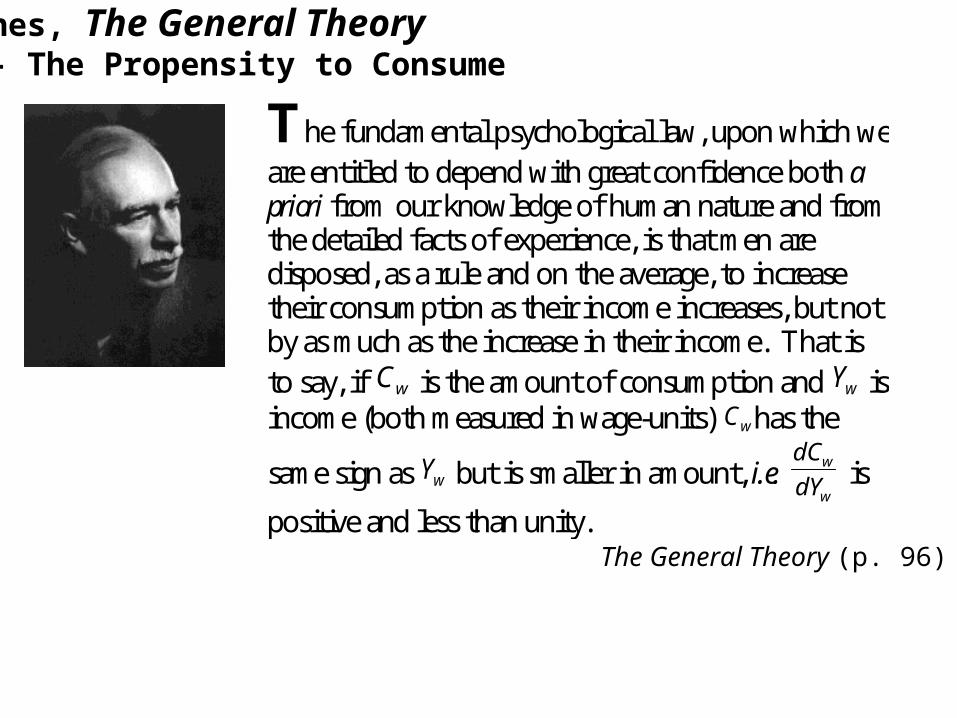

Keynes, The General Theory -- The Propensity to Consume

The General Theory (p. 96)

The fundamental psychological law, upon which we are entitled to depend with great confidence both a priori from our knowledge of human nature and from the detailed facts of experience, is that men are disposed, as a rule and on the average, to increase their consumption as their income increases, but not by as much as the increase in their income. That is to say, if wC is the amount of consumption and wY is income (both measured in wage-units) wC has the

same sign as wY but is smaller in amount, i.e. w

w

dY

dC is

positive and less than unity.

There will be an inducement to push the rate of new investment to the point which forces the supply-price of each type of capital asset to a figure which, taken in conjunction with its prospective yield, brings the marginal efficiency of capital in general to approximate equality with the rate of interest. That is to say, the physical conditions of supply in the capital goods industries, the state of confidence concerning the prospective yield, the psychological attitude to liquidity and the quantity of money ... determine, between them, the rate of new investment.

Keynes, The General Theory -- Investment

The General Theory (p. 248)

Even apart from the instability due to speculation, there is the instability due to the characteristic of human nature that a large proportion of our positive activities depend on spontaneous optimism rather than mathematical expectations, whether moral or hedonistic or economic. Most, probably, of our decisions to do something positive, the full consequences of which will be drawn out over many days to come, can only be taken as the result of animal spirits - a spontaneous urge to action rather than inaction, and not as the outcome of a weighted average of quantitative benefits multiplied by quantitative probabilities. ... if the animal spirits are dimmed and the spontaneous optimism falters, leaving us to depend on nothing but a mathematical expectation, enterprise will fade and die;

Keynes, The General Theory -- Animal Spirits

The General Theory (p. 161)

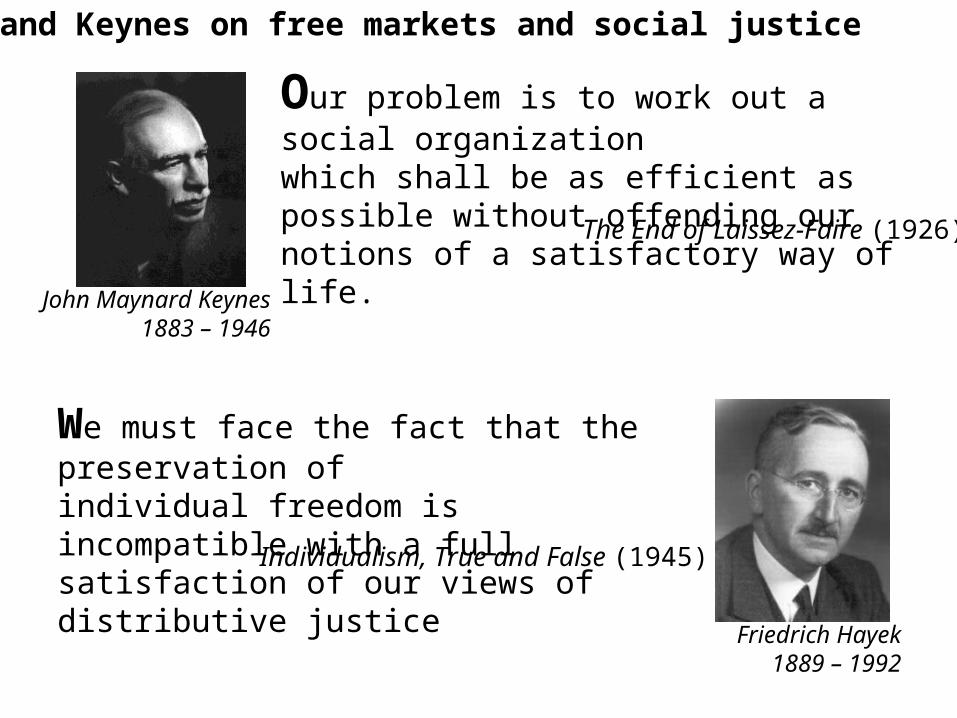

Hayek and Keynes on free markets and social justice

We must face the fact that the preservation of individual freedom is incompatible with a full satisfaction of our views of distributive justice

Individualism, True and False (1945)

Friedrich Hayek 1889 – 1992

Our problem is to work out a social organization which shall be as efficient as possible without offending our notions of a satisfactory way of life.

John Maynard Keynes 1883 – 1946

The End of Laissez-Faire (1926)

The evolution of “textbook” economics

Part 1: Basic Economic Concepts and National IncomePart 2: Determination of National Income and its FluctuationsPart 3: The Composition and Pricing of National Output

1950: EconomicsSamuelson, Economics, An Introductory Analysis (1948)

1850: Political EconomyMill, Principals of Political Economy (1848)

1900: EconomicsMarshall, Principals of Economics (1890)

Macroconomics Microconomics

Early 1800s: Political EconomyMill, The Wealth of Nations (1776)

Ricardo, Principles of Political Economy (1817)

Keynes’sGeneral Theory

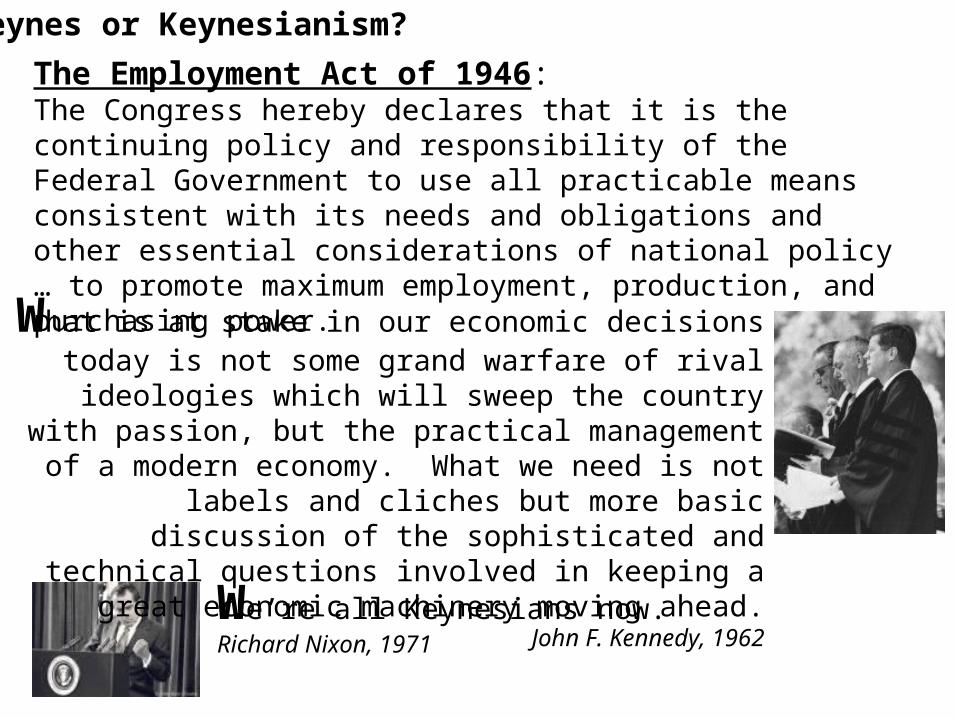

Keynes or Keynesianism?

The Employment Act of 1946:The Congress hereby declares that it is the continuing policy and responsibility of the Federal Government to use all practicable means consistent with its needs and obligations and other essential considerations of national policy … to promote maximum employment, production, and purchasing power.

What is at stake in our economic decisions today is not some grand warfare of rival ideologies which will sweep the country

with passion, but the practical management of a modern economy. What we need is not labels and cliches but more

basic discussion of the sophisticated and technical questions involved in keeping a great economic machinery moving ahead.

John F. Kennedy, 1962

We’re all Keynesians now.Richard Nixon, 1971

The Income-Expenditure Model – the “Keynesian Cross”

NNP

Samuelson, 1961 (5TH ed.)

45°

NET NATIONAL PRODUCT

TOTAL SPENDING

0

$

C

C+I

EQUILIBRIUM POINT

Hicks and the birth of IS – LM analysis

I

i

I S L

L

0

P

GNP(Y)

INTEREST RATE (R)

IS

LM

Hicks, 1937 Hall & Taylor, 1986

“Against a given quantity of money, the first equation, M = L(I,i) gives us a relation between Income (I) and the rate of interest (i). This can be drawn out as a curve (LL) which will slope upwards, since an increase in income tends to raise the demand for money, and an increase in the rate of interest tends to lower it … The curve IS can … be drawn showing the relation between Income and interest which must be maintained in order to make saving equal to investment.

“Income and the rate of interest are now determined together at P, the point of intersection of the curves LL and IS. They are determined together; just as price and output are determined together in the modern theory of demand and supply.”

J. R. Hicks, “Mr. Keynes and the ‘Classics’; A Suggested Interpretation.” Econometrica 5 (April 1937): 147 – 159.

“Hick’s graphical approach, called the IS-LM approach, is still used widely today because of its great intuitive appeal.”

Robert E. Hall and John B. Taylor, Macroeconomics: Theory, Performance, and Policy, 2nd ed. (1986).

The algebra of the basic IS-LM model

Yd

b

d

bTGcar

YbbTGcadr

GdrcbTbYaY

GdrcTYbaY

GICY

)1(

)1(

)(

1≤1

≤00<d

-b

Y

r because,

hrkYP

MrYL

P

M-=),,(=

+

e.g.,

M kYP hrP

Yh

k

P

M

hr +

1-=

0k h, because >,0>=h

k

Y

r

IS Curve(Equilibrium in the goods market)

Output = Expenditure

LM Curve(Equilibrium in the assets market)

= f(Output, Interest Rate)Demand for

“Real Balances”

Fiscal and Monetary policy with IS – LM analysis

GNP(Y)

INTEREST RATE(i)

IS

LM

GNP(Y)IS

LM

IS’

LM’

IS’

LM’

Illustrating equal magnitude Shifts of IS and LM

INTEREST RATE(i)

Typical “Monetarist” ViewIf d is “large”, IS is flat

If h is “small”, LM is steep Monetary policy is relatively strong

Typical “Keynesian” ViewIf d is “small”, IS is steepIf h is “large”, LM is flat

Fiscal policy is relatively strong

For equal magnitude changes in fiscal or monetary policy,monetary policy is relatively more effective in influencing output.

For equal magnitude changes in fiscal or monetary policy,fiscal policy is relatively more effective in influencing output.

Unemployment Rate

The Phillips Curve

w

5.5%

Phillips, A. W., “The Relationship Between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom,” Economica 25 (November 1958).

Samuelson, Paul A., and Robert M. Solow, "Analytical Aspects of Anti-Inflation Policy." American Economic Review 50:2 (1960): 177-94.

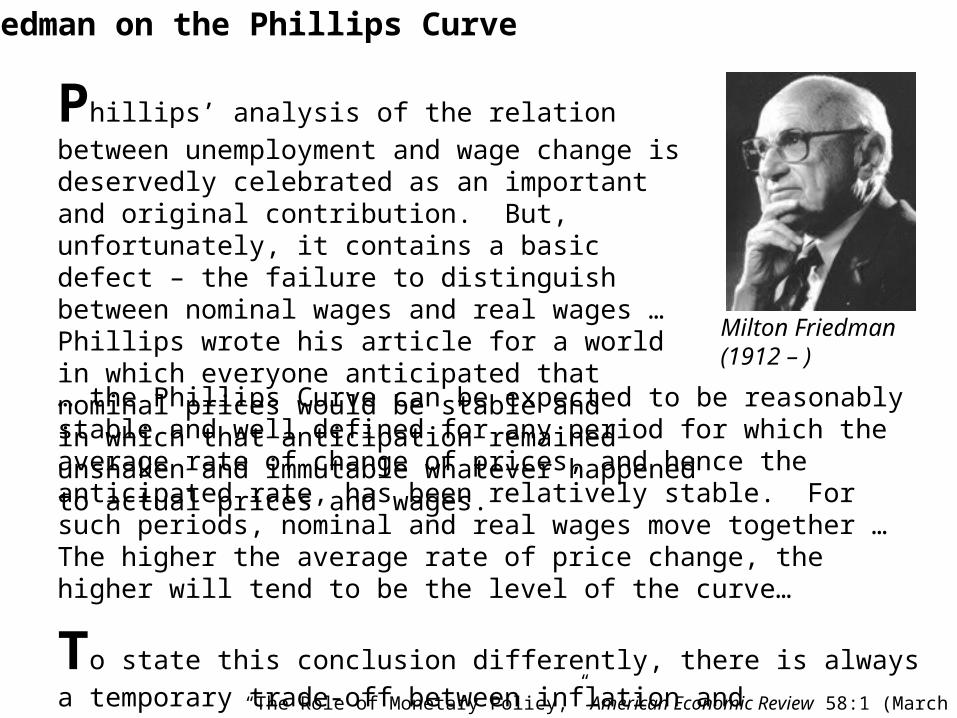

Friedman on the Phillips Curve

Phillips’ analysis of the relation between unemployment and wage change is deservedly celebrated as an important and original contribution. But, unfortunately, it contains a basic defect – the failure to distinguish between nominal wages and real wages …Phillips wrote his article for a world in which everyone anticipated that nominal prices would be stable andin which that anticipation remained unshaken and immutable whatever happened to actual prices and wages.

Milton Friedman(1912 – )

… the Phillips Curve can be expected to be reasonably stable and well defined for any period for which the average rate of change of prices, and hence the anticipated rate, has been relatively stable. For such periods, nominal and real wages move together … The higher the average rate of price change, the higher will tend to be the level of the curve…

To state this conclusion differently, there is always a temporary trade-off between inflation and unemployment; there is no permanent trade-off. The temporary trade-off comes not from inflation per se, but from unanticipated inflation.

“The Role of Monetary Policy,” American Economic Review 58:1 (March 1968), 1 – 17.

Unemployment Rate

Infl

atio

n

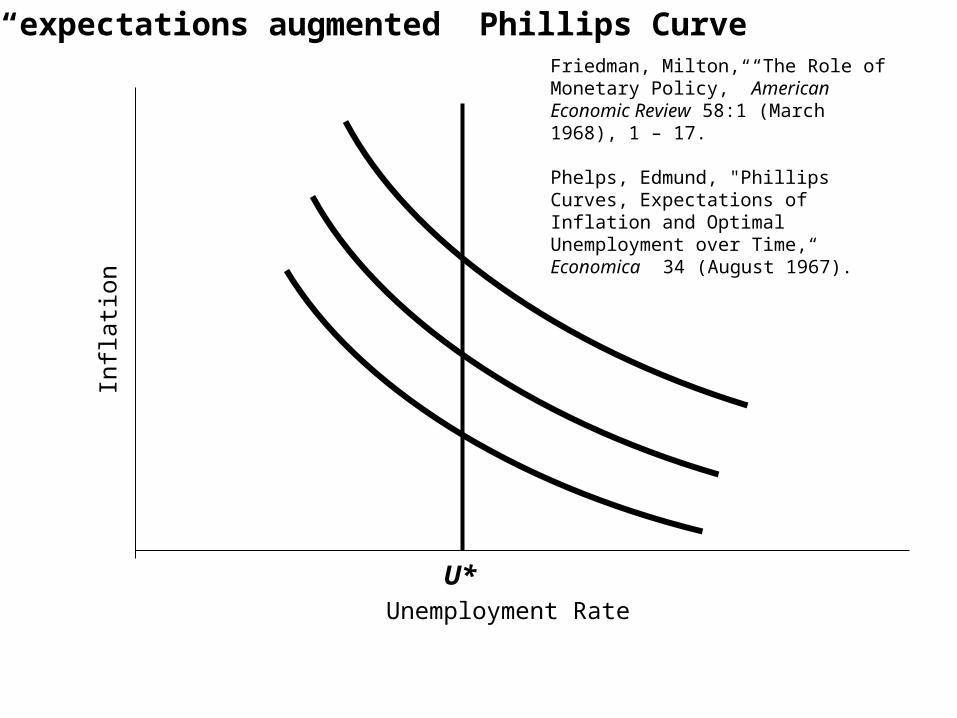

The “expectations augmented” Phillips Curve Friedman, Milton, “The Role of Monetary Policy,” American Economic Review 58:1 (March 1968), 1 – 17.

Phelps, Edmund, "Phillips Curves, Expectations of Inflation and Optimal Unemployment over Time,“ Economica 34 (August 1967).

U*

The 1970s crisis in macroeconomic policy

The present situation cannot last… it will either degenerate into hyper-inflation and radical change; or institutions will adjust to a situation of chronic inflation; or government will adopt policies that will produce a low rate of inflation and less government intervention into the fixing of prices.”

As an advice-giving profession, we’ve made a real mess of things.

Milton Friedman

Robert Lucas

Monetarism is the view that economies are inherently stable, that the quantity of money has a major influence on economic activity and the price level, and that the objectives of monetary policy are best achieved by targeting the rate of growth of the money supply. Monetarists generally express a preference for monetary policy as a stabilizing tool relative to prices only, being generally skeptical of attempts to manage output.

Keynesianism is the view that economies are inherently unstable, that they may in fact settle at less-than full employment equilibrium, that Aggregate Demand is the primary determinant of output and employment, and that authorities can intervene in an economy to stabilize it. Keynesians generally express a preference for fiscal policy as a stabilizing tool.

Friedman Greenspan Samuelson Keynes

Schools of thought in mid-20th century macroeconomics

New Classicalism is the view that economies are inherently stable, that fiscal and monetary interventions tend to be destabilizing, and that cyclical fluctuations are caused by either real shocks to the economy or unanticipated policy shocks. New classicals generally express a preference for microeconomic policies aimed at fostering aggregate supply, and a predictable monetary policy to maintain price stability.

New Keynesianism is the view that market failures and microeconomic coordination failures give rise to macroeconomic instabilities that frequently cause economies to settle at less-than full employment equilibrium, that both aggregate demand and aggregate supply are important determinants of output and employment, and that authorities can intervene with fiscal and monetary policy tools to stabilize an economy

Prescott Lucas Mankiw Bernanke

Schools of thought in late-20th century macroeconomics

Harvard / MIT•

• Yale

• Princeton• Penn

• Stanford

• Minnesota

• Chicago

Rochester•

• Carnegie - Mellon

Saltwater macroeconomicsFreshwater macroeconomics

Based on David M. Kreps, “Economics – The Current Position” (1997)

• Cal Berkeley

The Keynesian “revolution”

Beyond all this stretched the ‘Keynesian Revolution’ – the logic and practice of

managing economies so as to maintain full employment and avoid depressions like that of 1929 – 33. In the form Keynes left it, his Revolution was never wholly accepted; and the debate about its value and relevance, and its author’s place in the pantheon of thought and statesmanship, continues.

Robert Skidelsky, John Maynard Keynes, Volume III, Fighting for Freedom, 1937 – 1946 (2000)

Now, after more than three decades in the wilderness, Keynesian-style fiscal policy

seems to be staging a comeback.

“A stimulating notion,” The Economist, February 16, 2008.