ri transparency repor t 201 6...ri transparency repor t 201 6 aviva investors 1 about this report...

TRANSCRIPT

An investor initiative in partnership with UNEP Finance Initiative and UN Global Compact

RI TRANSPARENCY REPOR T

201 6

Aviva Investors

1

About this report

The PRI Reporting Framework is a key step in the journey towards building a common language and industry standard for

reporting responsible investment (RI) activities. This RI Transparency Report is one of the key outputs of this Framework.

Its primary objective is to enable signatory transparency on RI activities and facilitate dialogue between investors and their

clients, beneficiaries and other stakeholders. A copy of this report will be publicly disclosed for all reporting signatories on

the PRI website, ensuring accountability of the PRI Initiative and its signatories.

This report is an export of the individual Signatory organisation’s response to the PRI during the 2016 reporting cycle. It

includes their responses to mandatory indicators, as well as responses to voluntary indicators the signatory has agreed to

make public. The information is presented exactly as it was reported. Where an indicator offers a response option that is

multiple-choice, all options that were available to the signatory to select are presented in this report. Presenting the

information exactly as reported is a result of signatory feedback which suggested the PRI not summarise the information.

As a result, the reports can be extensive. However, to help easily locate information, there is a Principles index which

highlights where the information can be found and summarises the indicators that signatories complete and disclose.

Understanding the Principles Index

The Principles Index summarises the response status for the individual indicators and modules and shows how these

relate to the six Principles for Responsible Investment. It can be used by stakeholders as an ‘at-a-glance’ summary of

reported information and to identify particular themes or areas of interest.

Indicators can refer to one or more Principles. Some indicators are not specific to any Principle. These are highlighted in

the ‘General’ column. When multiple Principles are covered across numerous indicators, in order to avoid repetition, only

the main Principle covered is highlighted.

All indicators within a module are presented below. The status of indicators is shown with the following symbols:

Symbol Status

The signatory has completed all mandatory parts of this indicator

The signatory has completed some parts of this indicator

This indicator was not relevant for this signatory

- The signatory did not complete any part of this indicator

The signatory has flagged this indicator for internal review

Within the table, indicators marked in blue are mandatory to complete. Indicators marked in grey are voluntary to complete.

2

Principles Index Organisational Overview Principle General

Indicator Short description Status Disclosure 1 2 3 4 5 6

OO 01 Signatory category and services Public

OO 02 Headquarters and operational countries Public

OO 03 Subsidiaries that are separate PRI signatories

Public

OO 04 Reporting year and AUM Public

OO 05 Breakdown of AUM by asset class

Asset mix

disclosed in

OO 06

OO 06 How would you like to disclose your asset class mix

Public

OO 07 Fixed income AUM breakdown Public

OO 08 Segregated mandates or pooled funds Public

OO 09 Breakdown of AUM by market Public

OO 10 Additional information about organisation Public

OO 11 RI activities for listed equities Public

OO 12 RI activities in other asset classes Public

OO 13 Modules and sections required to complete

Public

3

Strategy and Governance Principle General

Indicator Short description Status Disclosure 1 2 3 4 5 6

SG 01 RI policy and coverage Public

SG 02 Publicly available RI policy or guidance documents

Public

SG 03 Conflicts of interest Public

SG 04 RI goals and objectives Public

SG 05 Main goals/objectives this year - n/a

SG 06 RI roles and responsibilities Public

SG 07 RI in performance management, reward and/or personal development

Public

SG 08 Collaborative organisations / initiatives Public

SG 09 Promoting RI independently Public

SG 10 Dialogue with public policy makers or standard setters

Public

SG 11 ESG issues in strategic asset allocation Private

SG 12 Long term investment risks and opportunity

Public

SG 13 Allocation of assets to environmental and social themed areas

Public

SG 14 ESG issues for internally managed assets not reported in framework

n/a

SG 15 ESG issues for externally managed assets not reported in framework

n/a

SG 16 RI/ESG in execution and/or advisory services

n/a

SG 17 Innovative features of approach to RI Public

SG 18 Internal and external review and assurance of responses

Public

4

Indirect – Manager Selection, Appointment and Monitoring Principle General

Indicator Short description Status Disclosure 1 2 3 4 5 6

SAM 01 Role of investment consultants/fiduciary managers

Public

SAM 02 RI factors in selection, appointment and monitoring across asset classes

Public

SAM 03 Breakdown by passive, quantitative, fundamental and other active strategies

Public

SAM 04 ESG incorporation strategies Public

SAM 05 Selection processes (LE and FI) Public

SAM 06 Appointment considerations (LE and FI) n/a

SAM 07 Monitoring processes (LE and FI) Public

SAM 08 Percentage of (proxy) votes cast Public

SAM 09 Selection processes (PE, PR and INF) n/a

SAM 10 Appointment considerations (PE, PR and INF)

n/a

SAM 11 Monitoring processes (PE, PR and INF) n/a

SAM 12 Percentage of externally managed assets managed by PRI signatories

Private

SAM 13 Examples of ESG issues in selection, appointment and monitoring processes

Public

SAM 14 Disclosure of RI considerations Public

5

Direct - Listed Equity Incorporation Principle General

Indicator Short description Status Disclosure 1 2 3 4 5 6

LEI 01 Breakdown by passive, quantitative, fundamental and other active strategies

Public

LEI 02 Reporting on strategies that are <10% of actively managed listed equities

n/a

LEI 03 Percentage of each incorporation strategy

Public

LEI 04 Type of ESG information used in investment decision

Public

LEI 05 Information from engagement and/or voting used in investment decision-making

Public

LEI 06 Types of screening applied n/a

LEI 07 Processes to ensure screening is based on robust analysis

n/a

LEI 08 Processes to ensure fund criteria are not breached

n/a

LEI 09 Types of sustainability thematic funds/mandates

n/a

LEI 10 Review ESG issues while researching companies/sectors

Public

LEI 11 Processes to ensure integration is based on robust analysis

Public

LEI 12 Aspects of analysis ESG information is integrated into

Public

LEI 13 ESG issues in index construction Public

LEI 14 How ESG incorporation has influenced portfolio composition

Public

LEI 15 Measurement of financial and ESG outcomes of ESG incorporation

Public

LEI 16 Examples of ESG issues that affected your investment view / performance

Public

LEI 17 Disclosure of approach to ESG incorporation

Public

6

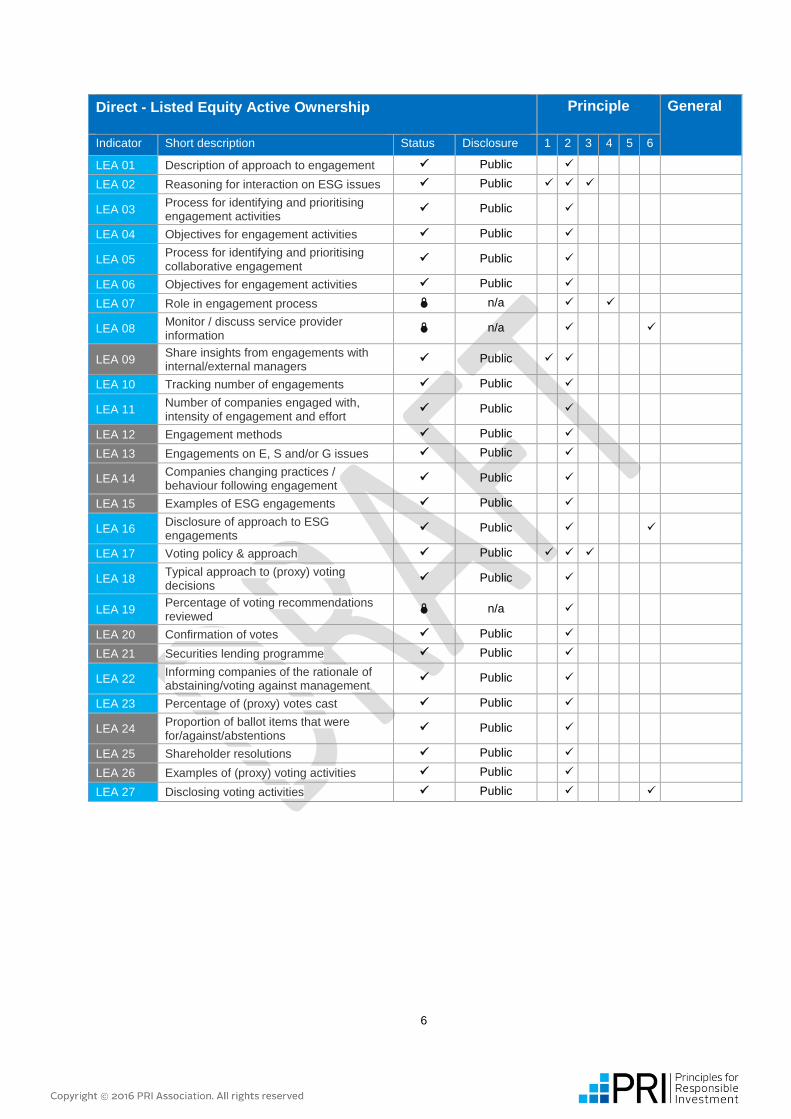

Direct - Listed Equity Active Ownership Principle General

Indicator Short description Status Disclosure 1 2 3 4 5 6

LEA 01 Description of approach to engagement Public

LEA 02 Reasoning for interaction on ESG issues Public

LEA 03 Process for identifying and prioritising engagement activities

Public

LEA 04 Objectives for engagement activities Public

LEA 05 Process for identifying and prioritising collaborative engagement

Public

LEA 06 Objectives for engagement activities Public

LEA 07 Role in engagement process n/a

LEA 08 Monitor / discuss service provider information

n/a

LEA 09 Share insights from engagements with internal/external managers

Public

LEA 10 Tracking number of engagements Public

LEA 11 Number of companies engaged with, intensity of engagement and effort

Public

LEA 12 Engagement methods Public

LEA 13 Engagements on E, S and/or G issues Public

LEA 14 Companies changing practices / behaviour following engagement

Public

LEA 15 Examples of ESG engagements Public

LEA 16 Disclosure of approach to ESG engagements

Public

LEA 17 Voting policy & approach Public

LEA 18 Typical approach to (proxy) voting decisions

Public

LEA 19 Percentage of voting recommendations reviewed

n/a

LEA 20 Confirmation of votes Public

LEA 21 Securities lending programme Public

LEA 22 Informing companies of the rationale of abstaining/voting against management

Public

LEA 23 Percentage of (proxy) votes cast Public

LEA 24 Proportion of ballot items that were for/against/abstentions

Public

LEA 25 Shareholder resolutions Public

LEA 26 Examples of (proxy) voting activities Public

LEA 27 Disclosing voting activities Public

7

Direct - Fixed Income Principle General

Indicator Short description Status Disclosure 1 2 3 4 5 6

FI 01 Breakdown by passive,active strategies Public

FI 02 Option to report on <10% assets n/a

FI 03 Breakdown by market and credit quality Public

FI 04 Incorporation strategies applied Public

FI 05 ESG issues and issuer research Public

FI 06 Processes to ensure analysis is robust Public

FI 07 Types of screening applied n/a

FI 08 Negative screening - overview and rationale

- n/a

FI 09 Examples of ESG factors in screening process

- n/a

FI 10 Screening - ensuring criteria are met - n/a

FI 11 Thematic investing - overview n/a

FI 12 Thematic investing - themed bond processes

n/a

FI 13 Thematic investing - assessing impact n/a

FI 14 Integration overview Public

FI 15 Integration - ESG information in investment processes

Public

FI 16 Integration - E,S and G issues reviewed Public

FI 17 ESG incorporation in passive funds Public

FI 18 Engagement overview and coverage Public

FI 19 Engagement method Public

FI 20 Engagement policy disclosure Public

FI 21 Financial/ESG performance Public

FI 22 Examples - ESG incorporation or engagement

Public

FI 23 Communications Public

8

Direct - Property Principle General

Indicator Short description Status Disclosure 1 2 3 4 5 6

PR 01 Breakdown of investments Private

PR 02 Breakdown of assets by management Public

PR 03 Largest property types Private

PR 04 Description of approach to RI Private

PR 05 Responsible Property Investment (RPI) policy

Public

PR 06 Fund placement documents and RI Public

PR 07 Formal commitments to RI Private

PR 08 Incorporating ESG issues when selecting investments

Public

PR 09 ESG advice and research when selecting investments

Private

PR 10 Examples of ESG issues in investment selection process

Public

PR 11 Types of ESG information considered in investment selection

Private

PR 12 ESG issues impact in selection process Public

PR 13 ESG issues in selection, appointment and monitoring of third-party property managers

Public

PR 14 ESG issues in post-investment activities Public

PR 15 Proportion of assets with ESG targets that were set and monitored

Public

PR 16 Certification schemes, ratings and benchmarks

Private

PR 17 Proportion of developments and refurbishments where ESG issues were considered

Public

PR 18 Proportion of property occupiers that were engaged with

Public

PR 19 Proportion of green leases or MOUs referencing ESG issues

Public

PR 20 Proportion of assets engaged with on community issues

Public

PR 21 ESG issues affected financial/ESG performance

Public

PR 22 Examples of ESG issues that affected your property investments

Public

PR 23 Disclosure of ESG information to public and clients/beneficiaries

Public

9

Aviva Investors

Reported Information

Public version

Organisational Overview

PRI disclaimer

This document presents information reported directly by signatories. This information has not been audited by the PRI

Secretariat or any other party acting on their behalf. While this information is believed to be reliable, no representations or

warranties are made as to the accuracy of the information presented, and no responsibility or liability can be accepted for

any error or omission.

10

Basic Information

OO 01 Mandatory Gateway/Peering General

OO 01.1 Select the services you offer.

Fund management

% of assets under management (AUM) in ranges

<10%

10-50%

>50%

Fund of funds, manager of managers, sub-advised products

% of assets under management (AUM) in ranges

<10%

10-50%

>50%

Other, specify

Execution and advisory services

OO 02 Mandatory Peering General

OO 02.1 Select the location of your organisation’s headquarters.

United Kingdom

OO 02.2 Indicate the number of countries in which you have offices (including your headquarters).

1

2-5

6-10

>10

OO 02.3 Indicate the approximate number of staff in your organisation in full-time equivalents (FTE).

FTE

1393

11

OO 02.4 Additional information. [Optional]

Investment management and distribution of Aviva Investors' products takes place in the UK, France, Poland, Singapore, Canada and the United States. We have offices covering distribution only in Australia, Ireland, the Netherlands, Sweden, Switzerland, Taiwan and UAE. Our office in Germany has an investment team and our Luxembourg office manages fund administration.

OO 03 Mandatory Descriptive General

OO 03.1 Indicate whether you have subsidiaries within your organisation that are also PRI signatories in their own right.

Yes

No

OO 04 Mandatory Gateway/Peering General

OO 04.1 Indicate the year end date for your reporting year.

31/12/2015

OO 04.2 Indicate your total AUM at the end of your reporting year, excluding subsidiaries you have chosen not to report on, and advisory/execution only assets.

trillions billions millions thousands hundreds

Total AUM 289 910 000 000

Currency GBP

Assets in USD 438 230 608 036

OO 06 Mandatory Descriptive General

OO 06.1 To contextualise your responses to the public, indicate how you would like to disclose your asset class mix.

Publish our asset class mix as percentage breakdown

Publish our asset class mix as broad ranges

Internally managed (%) Externally managed (%)

Listed equity 10-50% <10%

Fixed income >50% <10%

Private equity 0 0

12

Property 10-50% 0

Infrastructure 0 0

Commodities 0 0

Hedge funds 0 0

Forestry 0 0

Farmland 0 0

Inclusive finance 0 0

Cash 0 0

Other (1), specify <10% 0

Other (2), specify 0 0

'Other (1)' specified

Other mixed assets, balanced funds and structured products managed by Aviva Investors which cannot be allocated to a specific asset class

OO 06.2 Publish our asset class mix as per attached image [Optional].

OO 07 Mandatory to Report Voluntary to Disclose Gateway General

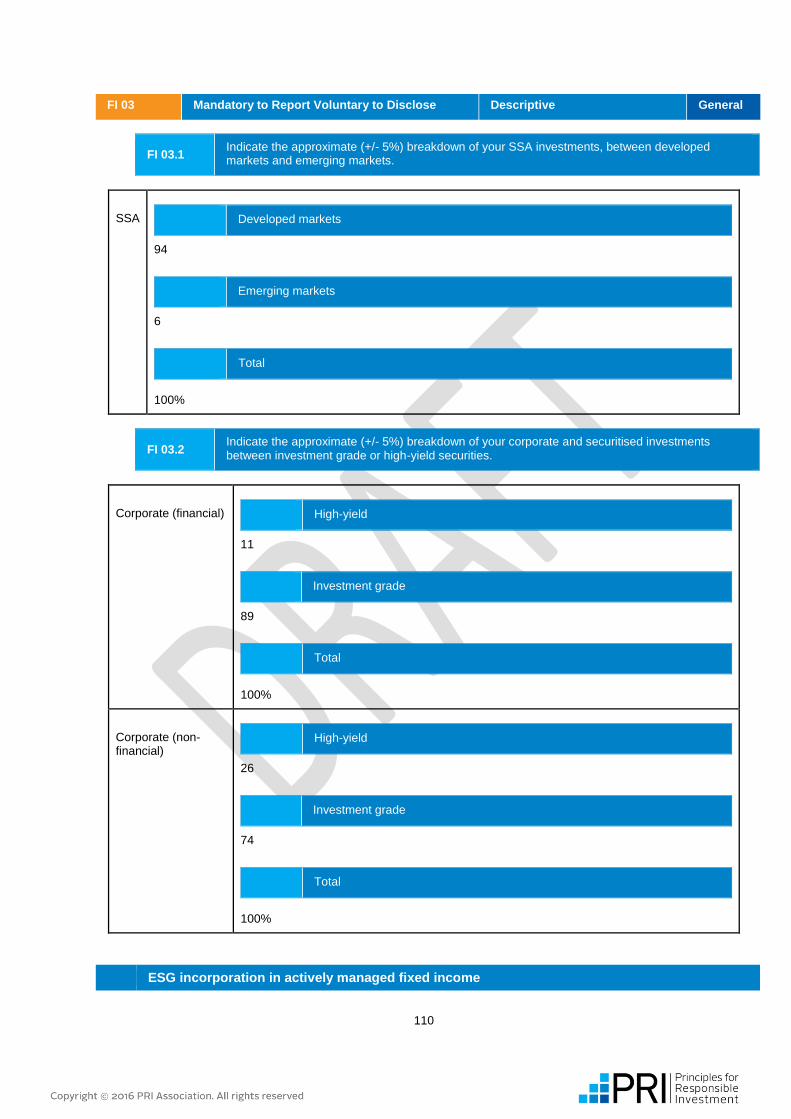

OO 07.1 Provide to the nearest 5% the percentage breakdown of your Fixed Income AUM at the end of your reporting year, using the following categories.

13

Internally managed

SSA

10

Corporate (financial)

50

Corporate (non-financial)

40

Securitised

0

Total

100%

Externally managed

SSA

10

Corporate (financial)

50

Corporate (non-financial)

30

Securitised

10

Total

100%

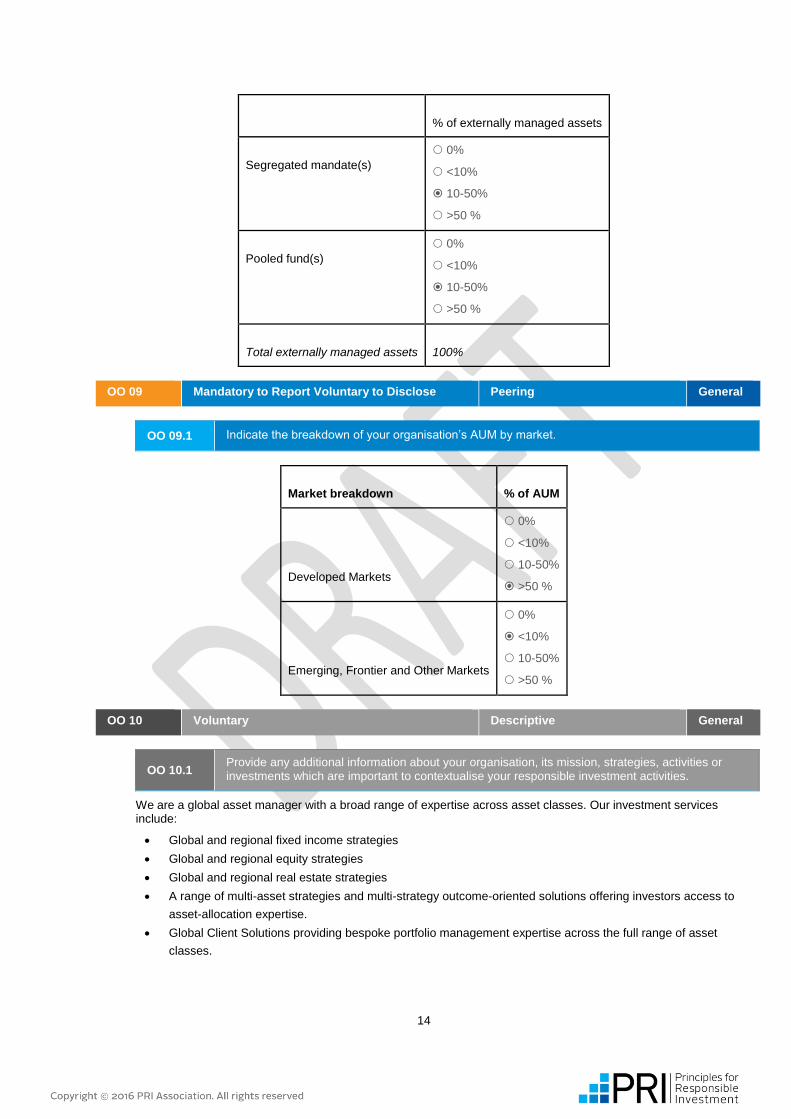

OO 08 Mandatory to Report Voluntary to Disclose Peering General

OO 08.1 Provide a breakdown of your organisation’s externally managed assets between segregated mandates and pooled funds.

14

% of externally managed assets

Segregated mandate(s)

0%

<10%

10-50%

>50 %

Pooled fund(s)

0%

<10%

10-50%

>50 %

Total externally managed assets

100%

OO 09 Mandatory to Report Voluntary to Disclose Peering General

OO 09.1 Indicate the breakdown of your organisation’s AUM by market.

Market breakdown

% of AUM

Developed Markets

0%

<10%

10-50%

>50 %

Emerging, Frontier and Other Markets

0%

<10%

10-50%

>50 %

OO 10 Voluntary Descriptive General

OO 10.1 Provide any additional information about your organisation, its mission, strategies, activities or investments which are important to contextualise your responsible investment activities.

We are a global asset manager with a broad range of expertise across asset classes. Our investment services include:

Global and regional fixed income strategies

Global and regional equity strategies

Global and regional real estate strategies

A range of multi-asset strategies and multi-strategy outcome-oriented solutions offering investors access to

asset-allocation expertise.

Global Client Solutions providing bespoke portfolio management expertise across the full range of asset

classes.

15

Our overarching strategy is to offer investment propositions that deliver those outcomes that are central to the success or wellbeing of our customers. We focus on what we do best, and on capabilities and propositions that build on our heritage in managing long-term savings.

Gateway asset class implementation indicators

OO 11 Mandatory Gateway General

OO 11.1 Select your direct or indirect ESG incorporation activities your organisation implemented, for listed equities in the reporting year.

We incorporate ESG in our investment decisions on our internally managed assets

We address ESG incorporation in our external manager selection, appointment and/or monitoring processes

We do not incorporate ESG in our directly managed listed equity and/or we do not address ESG incorporation in our external manager selection, appointment and/or monitoring processes.

OO 11.2 Select your direct or indirect engagement activities your organisation implemented for listed equity in the reporting year.

We engage with companies on ESG issues via our staff, collaborations or service providers

We require our external managers to engage with companies on ESG issues on our behalf

We do not engage directly and do not require external managers to engage with companies on ESG factors.

OO 11.3 Select your direct or indirect voting activities your organisation implemented for listed equity in the reporting year

We cast our (proxy) votes directly or via dedicated voting providers

We require our external managers to vote on our behalf

We do not cast our (proxy) votes directly and do not require external managers to vote on our behalf

OO 12 Mandatory Gateway General

OO 12.1 Select internally managed asset classes where you implemented responsible investment into your investment decisions and/or your active ownership practices (during the reporting year)

Fixed income – SSA

Fixed income – corporate (financial)

Fixed income – corporate (non-financial)

Property

Other (1)

None of the above

'Other (1)' [as defined in OO 05]

Other mixed assets, balanced funds and structured products managed by Aviva Investors which cannot be allocated to a specific asset class

16

OO 12.2

Select externally managed assets classes where you addressed ESG incorporation and/or active ownership in your external manager selection, appointment and/or monitoring processes (during the reporting year)

Fixed income – SSA

Fixed income – corporate (financial)

Fixed income – corporate (non-financial)

Fixed income – securitised

None of the above

OO 13 Mandatory Gateway General

You will need to make a selection in OO 13.1onlyif you have any voluntary modules that you can choose to report on.

OO 13.1 You are only required to report on asset classes that represent 10% or more of your AUM. You may report voluntarily on any applicable modules or sections by selecting them from the list below.

Core modules

Organisational Overview

Strategy and Governance

RI implementation directly or via service providers

Direct - Listed Equity incorporation

Listed Equity incorporation

Direct - Listed Equity active ownership

Engagements

(Proxy) voting

Direct - Fixed Income

Fixed income - SSA

Fixed income - Corporate (financial)

Fixed income - Corporate (non-financial)

Direct - Other asset classes with dedicated modules

Property

RI implementation via external managers

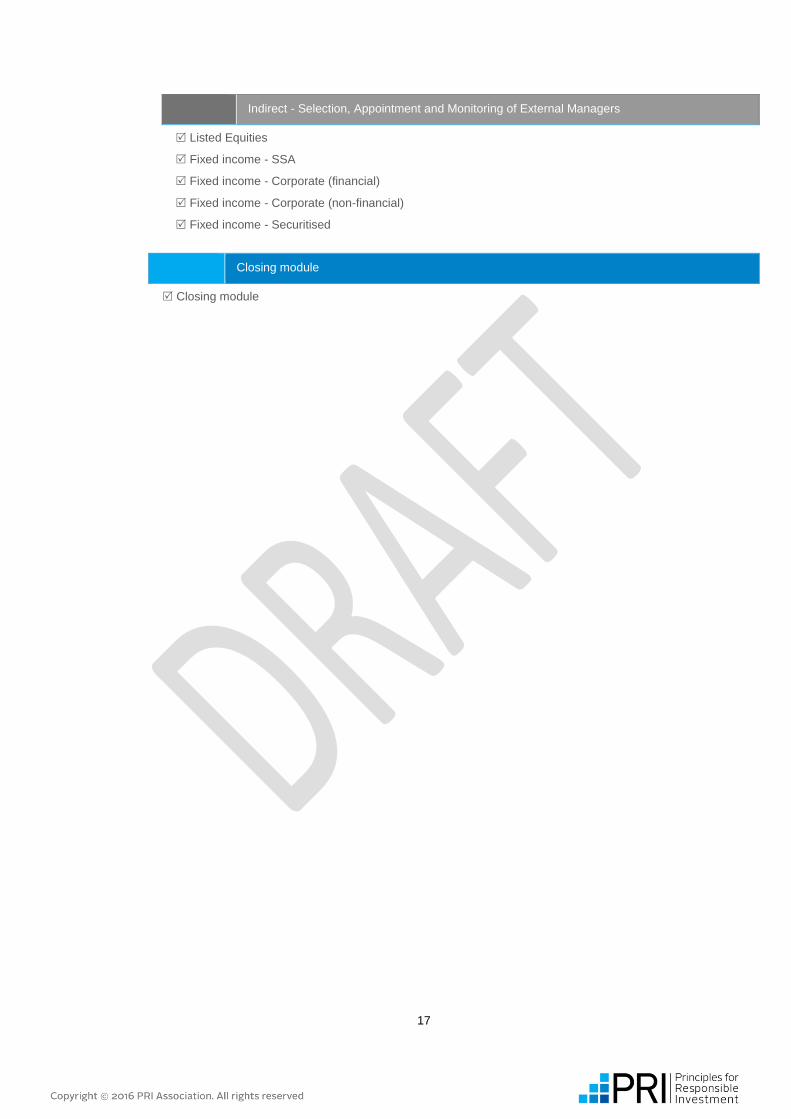

17

Indirect - Selection, Appointment and Monitoring of External Managers

Listed Equities

Fixed income - SSA

Fixed income - Corporate (financial)

Fixed income - Corporate (non-financial)

Fixed income - Securitised

Closing module

Closing module

18

Aviva Investors

Reported Information

Public version

Strategy and Governance

PRI disclaimer

This document presents information reported directly by signatories. This information has not been audited by the PRI

Secretariat or any other party acting on their behalf. While this information is believed to be reliable, no representations or

warranties are made as to the accuracy of the information presented, and no responsibility or liability can be accepted for

any error or omission.

19

Responsible investment policy

SG 01 Mandatory Core Assessed General

SG 01.1 Indicate if you have an investment policy that covers your responsible investment approach.

Yes

SG 01.2 Indicate the components/types and coverage of your policy.

Select all that apply

Policy components/types

Coverage by AUM

Policy setting out your overall approach

Formalised guidelines on environmental factors

Formalised guidelines on social factors

Formalised guidelines on corporate governance factors

Asset class-specific guidelines

Sector specific RI guidelines

Screening / exclusions policy

Engagement policy

(Proxy) voting policy

Other, specify (1)

Other, specify(2)

Applicable policies cover all AUM

Applicable policies cover a majority of AUM

Applicable policies cover a minority of AUM

SG 01.3 Indicate what norms have you used to develop your RI policy.

UN Global Compact Principles

UN Guiding Principles on Business and Human Rights

Universal Declaration of Human Rights

International Bill of Human Rights

International Labour Organization Conventions

United Nations Convention Against Corruption

OECD Guidelines for Multinational Enterprises

Other, specify (1)

other (1) description

UK Stewardship Code, UK Corporate Governance Code and International Corporate Governance Network (ICGN) Global Corporate Governance Principles

Other, specify (2)

20

other (2) description

Oslo Convention on Cluster Munitions and Ottawa Convention on Anti-Personnel Mines

Other, specify (3)

None of the above

SG 01.4 Provide a brief description of the key elements of your investment policy that covers your responsible investment approach [Optional].

Aviva Investor's overarching investment philosophy forms five pillars, three of which directly draw on our approach to responsible investment.

1. We believe in informed risk, effectively managed: by combining our extensive experience and unique

insights, we reach an informed view on every decision throughout the whole investment process.

2. We are actively responsible investors: we promote sustainable business practices in global markets,

encouraging greater transparency and better corporate governance. This helps us to reduce risk and

strive to enhance the long-term value of our clients' investments

3. We invest with conviction for the long term: everything we do is driven by our long-term perspective and

our focus on building strategies and funds that are built to last.

https://uk.avivainvestors.com/gb/en/institutional/about-us/investment-philosophy.html

No

SG 01.5 Additional information [Optional].

At Aviva Investors, we seek to deliver the specific and meaningful outcomes that matter most to today's investor. Our commitment to responsible investment is fundamental to delivering this goal. We focus on integration, active stewardship and market advocacy to deliver our view of responsible investment.

THE THREE STRATEGIC PILLARS OF OUR APPROACH ARE:

1. Integration of environmental, social& governance (ESG) considerations into investment decisions - we work together with fund managers and analysts, customising ESG integration for each investment process, to deliver improved investment outcomes for clients

2. Active ownership& stewardship through engagement and voting - we use our influence to promote good practice among those companies in which we invest, and to gain insight and reduce investment risk on ESG issues for our clients. We focus on generating outcomes that benefit our clients and in many cases society, the environment and the broader economy as well.

3. Shaping markets for sustainability - we advocate policy measures that support longer term, more sustainable capital markets. We aim to correct market failures such as a lack of corporate disclosure on ESG risks and climate change - at a national, EU, OECD and UN level to improve long-term policy outcomes.

KEY POLICIES

For 93% of assets under management we have developed a tailored responsible investment approach. The key policies that guide our approach to responsible investment are:

The Aviva Investors Stewardship Statement sets out our commitment to the UK Stewardship Code and the Principles for Responsible Investment. It also outlines the philosophy, beliefs and practices that drive Aviva Investors' behaviours as a major responsible institutional investor.

Our Corporate Governance and Corporate Responsibility Voting Policy sets out the standards of good corporate governance and corporate responsibility we expect from the companies in which we invest and outlines how this is translated into our voting policy.

We have also developed specific policies for different asset classes as we regard the consideration of ESG issues and their impact on investment as an essential part of our fiduciary duty to clients. For example, as one of Europe's largest real estate investment manager we have a Responsible Property Policy that applies to all Aviva Investors Real Estate's global activities.

21

SG 02 Mandatory Core Assessed PRI 6

SG 02.1 Indicate which of your investment policy documents (if any) are publicly available. Provide URL and an attachment of the document.

Policy setting out your overall approach

URL

https://uk.avivainvestors.com/gb/en/institutional/about-us/responsible-investment.html

Formalised guidelines on corporate governance factors

Asset class-specific guidelines

URL

http://www.avivainvestors.co.uk/pension_schemes/cs/groups/internet/documents/webattachment/zgzf/mdmw/~edisp/pdf_030468.pdf

Engagement policy

URL

https://uk.avivainvestors.com/content/dam/aviva/aviva-investors/united-kingdom/documents/institutional/ai-stewardship-statement.pdf

(Proxy) voting policy

URL

https://uk.avivainvestors.com/content/dam/aviva/aviva-investors/united-kingdom/documents/institutional/uk-corporate-governance-and-corporate-responsibility-voting-policy-rebranded.pdf

We do not publicly disclose our investment policy documents

SG 03 Mandatory Core Assessed General

SG 03.1 Indicate if your organisation has a policy on managing potential conflicts of interest in the investment process.

Yes

22

SG 03.2 Describe your policy on managing potential conflicts of interest in the investment process.

Our approach to managing conflicts of interest is publicly disclosed within our Stewardship Statement, which we update on an annual basis.

No

Objectives and strategies

SG 04 Mandatory Gateway/Core Assessed General

SG 04.1 Indicate if and how frequently your organisation sets and reviews objectives for its responsible investment activities.

Quarterly or more frequently

Biannually

Annually

Less frequently than annually

Ad-hoc basis

It is not reviewed

SG 04.2 Additional information. [Optional]

The Global Responsible Investment team reports annually to the Aviva Investors Executive Committee and the Aviva Board Governance Committee on performance against responsible investment objectives. We hold a quarterly planning meeting on our annual overarching objectives as well as review our engagement targets. Progress is reviewed on a quarterly basis by the Global Responsible Investment Advisory Committee comprising four experts in governance and sustainability issues.

Governance and human resources

SG 06 Mandatory Core Assessed General

SG 06.1 Indicate the roles present in your organisation and for each, indicate whether they have oversight and/or implementation responsibilities for responsible investment.

23

Roles present in your organisation

Board members or trustees

Oversight/accountability for responsible investment

Implementation of responsible investment

No oversight/accountability or implementation responsibility for responsible investment

Chief Executive Officer (CEO), Chief Investment Officer (CIO), Investment Committee

Oversight/accountability for responsible investment

Implementation of responsible investment

No oversight/accountability or implementation responsibility for responsible investment

Other Chief-level staff or head of department, specify

Portfolio managers

Oversight/accountability for responsible investment

Implementation of responsible investment

No oversight/accountability or implementation responsibility for responsible investment

Investment analysts

Oversight/accountability for responsible investment

Implementation of responsible investment

No oversight/accountability or implementation responsibility for responsible investment

Dedicated responsible investment staff

Oversight/accountability for responsible investment

Implementation of responsible investment

No oversight/accountability or implementation responsibility for responsible investment

External managers or service providers

Investor relations

Other role, specify

Other role, specify

SG 06.3 Indicate the number of dedicated responsible investment staff your organisation has.

Number

7

SG 06.4 Additional information. [Optional]

The Global Responsible Investment (GRI) team comprises seven corporate governance and responsible investment professionals. We have plans to expand our team and will be recruiting for two new roles in 2016. Our responsible investment work is supported by a network of over 30 Responsible Investment Officers distributed across all asset classes, front and middle office functions as well as different geographic regions.

SG 07 Voluntary Additional Assessed General

24

SG 07.1 Indicate if your organisation’s performance management, reward and/or personal development processes have a responsible investment element.

Board members/Board of trustees

Responsible investment included in personal development and/or training plan

None of the above

Chief Executive Officer (CEO), Chief Investment Officer (CIO), Investment Committee

Responsible investment KPIs and/or goals included in objectives

Responsible investment included in appraisal process

Variable pay linked to responsible investment performance

Responsible investment included in personal development and/or training plan

None of the above

Portfolio managers

Responsible investment KPIs and/or goals included in objectives

Responsible investment included in appraisal process

Variable pay linked to responsible investment performance

Responsible investment included in personal development and/or training plan

None of the above

Investment analysts

Responsible investment KPIs and/or goals included in objectives

Responsible investment included in appraisal process

Variable pay linked to responsible investment performance

Responsible investment included in personal development and/or training plan

None of the above

Dedicated responsible investment staff

Responsible investment KPIs and/or goals included in objectives

Responsible investment included in appraisal process

Variable pay linked to responsible investment performance

Responsible investment included in personal development and/or training plan

None of the above

25

SG 07.3 Provide any additional information on your organisation’s performance management, reward and/or personal development processes in relation to responsible investment.

Aviva Investors was one of the first large mainstream asset managers to make the integration of environmental, social and governance (ESG) factors into investment decisions part of the pay criteria of its main investment desk heads. We have a network of Responsible Investment Officers (RIO)s that play an active role in embedding ESG data and analysis fully into each desk's investment process. This network of over 30 fund managers, analysts and support functions is the first point of contact for ESG integration within each investment desk and region. Responsible Investment objectives are now incorporated into the appraisal and compensation of a number of our RIO network, with a modest but meaningful part of their annual compensation linked to ESG issues.

Promoting responsible investment

SG 08 Mandatory Core Assessed PRI 4,5

New selection options have been added to this indicator. Please review your prefilled responses carefully.

SG 08.1 Select the collaborative organisation and/or initiatives of which your organisation is a member or in which it participated during the reporting year, and the role you played.

Select all that apply

Principles for Responsible Investment

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

Aviva Investors is proud to be a founding signatory and a strong supporter of the Principles for Responsible Investment (PRI). We previously played a formal role in the PRI (Steve Waygood, Chief Responsible Investment Officer, was a Partner of the PRI Academic Network). Our current involvement is being active participants in leading and supporting engagements through the PRI Clearing House.

AFIC – La Commission ESG

Asian Corporate Governance Association

Australian Council of Superannuation Investors

BVCA – Responsible Investment Advisory Board

CDP Climate Change

26

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

Having supported CDP since before its inception in 2001, Aviva provided seed funding to the Carbon Action Initiative and participated in the investor steering group along with CCLA, Robeco and Scottish Widows Investment Partnership (SWIP) in its development. We continue to work closely with them on their focus on non-disclosure of risks relating to carbon, water and forest commodities. Aviva Investors continues to be an active spokesperson on carbon risks and the CDP, contributing to a promotional video in 2015.

CDP Forests

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

Please see CDP response above

CDP Water

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

Please see CDP response above

CFA Institute Centre for Financial Market Integrity

27

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Code for Responsible Investment in SA (CRISA)

Council of Institutional Investors (CII)

ESG Research Australia

Eumedion

EVCA – Responsible Investment Roundtable

Extractive Industries Transparency Initiative (EITI)

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Global Investors Governance Network (GIGN)

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

Aviva Investors is a founding member of GIGN and held the positon of Chair for 10 years until 2014 when our tenure ended. We continue to be active members of the organisation.

Global Impact Investing Network (GIIN)

Global Real Estate Sustainability Benchmark (GRESB)

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

Aviva Investors joined GRESB in 2010. Both our European Direct Real Estate team and Global Indirect Real Estate (GIRE) team are currently members. Kathleen Jowett of our GIRE team sits on GRESB's Advisory Board.

GIRE requires all its underlying managers to participate in GRESB. From an indirect investing perspective, the GRESB survey allows us to both monitor existing practices and promote best practice. This is something we have done since 2005.

28

Since 2014 Aviva Investors has co-chaired an investor-led initiative to create a global standard and benchmarking tool for measuring sustainability in infrastructure investments in order to allow investors to better assess ESG performance and risk across infrastructure investments. This working group entered into a partnership with GRESB and will form the Infrastructure Advisory Board and commit to the development of the initiative for the next 3 years. In 2015 we hosted the European launch of the GRESB Infrastructure initiative in London.

John Gellatly, Head of UK and Europe in our Global Indirect Real Estate (GIRE) team, presented at GRESB's 2015 results event in London on how Aviva Investors participates in GRESB and uses the results to monitor and encourage best practice.

Institutional Investors Group on Climate Change (IIGCC)

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

We are active participants in IIGCC, our Head of Responsible Investment Strategy& Research chairs the Corporate Working Group which shapes IIGCC engagement priorities with carbon and energy intensive companies on carbon risk. Part of this role has involved the development of sector specific engagement guides for investors.

Interfaith Center on Corporate Responsibility (ICCR)

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

We are supportive of the organisations efforts and have followed their work on ESG shareholder resolutions closely. We have been supportive of the shareholder proposals when they have been in line with our voting policy.

International Corporate Governance Network (ICGN)

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

29

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

We are longstanding members of ICGN and previously served on the Board of Governors. We currently Chair the Nomination Committee.

Investor Group on Climate Change, Australia/New Zealand (IGCC)

International Integrated Reporting Council (IIRC)

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

We were formerly members of the investor working group and continue to follow their work, contributing where relevant.

Investor Network on Climate Risk (INCR)/CERES

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

Aviva Investors is signatory to the Ceres Carbon Asset Risk initiative and we are actively engaging with target companies. We also collaborate via the Global Investor Coalition on climate change, which includes IIGCC, ICGG and AIGCC.

Local Authority Pension Fund Forum

Principles for Financial Action for the 21st Century

Regional or National Social Investment Forums (e.g. UKSIF, Eurosif, ASRIA, RIAA), specify

UKSIF, Eurosif

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

30

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

Aviva Investors is a long standing member of UKSIF. In addition, although serving in a personal capacity, our Head of Responsible Investment Strategy and Research is on the Board of UKSIF and our Head of Responsible Investment Engagement is on the Leadership Committee. We support flagship initiatives such as Ownership Day co-hosted events on several ESG topics including Sustainable Fisheries.

Shareholder Association for Research and Education (Share)

United Nations Environmental Program Finance Initiative (UNEP FI)

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

United Nations Global Compact

Your organisation’s role in the initiative during the reporting period (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

Our parent company, Aviva is a longstanding signatory to the UN Global Compact Principles. In 2010, we were invited to be one of approximately 50 companies forming the Global Compact LEAD, to set a best practice example to others. As well as reporting annually against these principles we support the UN Global Compact principles through our Corporate Governance and Corporate Responsibility Voting Policy and targeted engagement (including leading a collaborative engagement on the PRI Clearing House).

We also consider the UN Global Compact to be a strategic partner in the Sustainable Stock Exchange Initiative and work closely on a range of other initiatives.

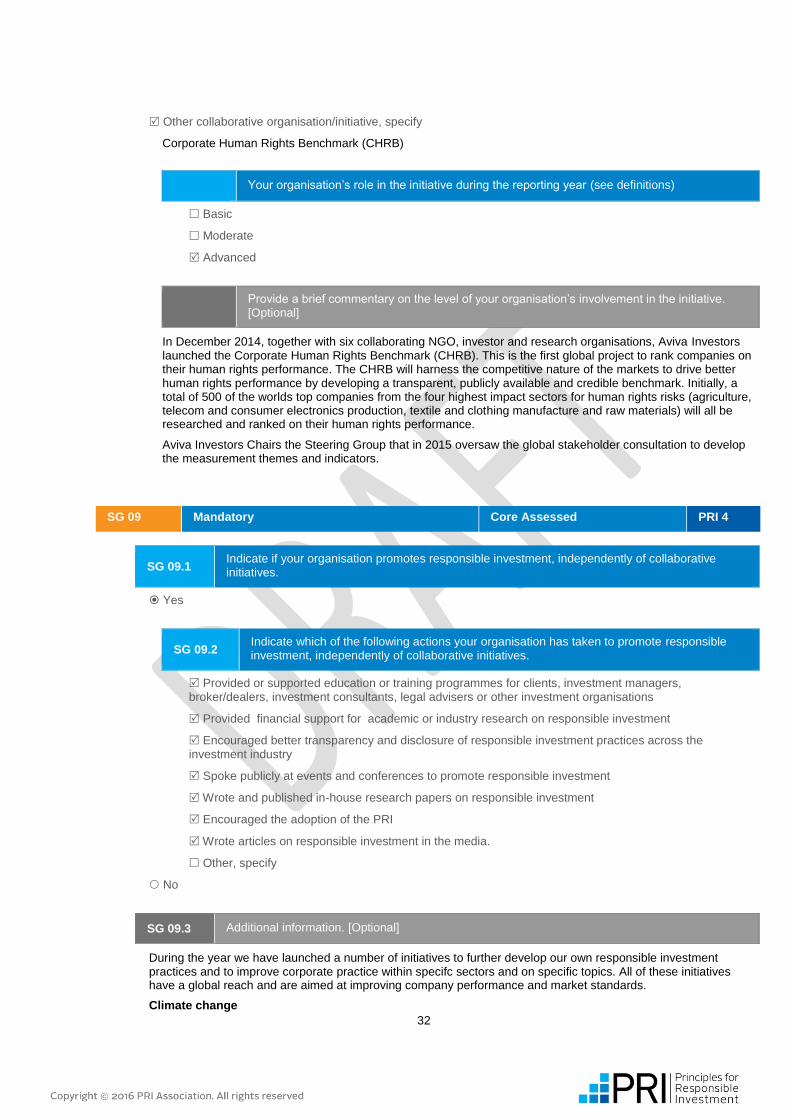

Other collaborative organisation/initiative, specify

Sustainable Stock Exchange Initiative - a partnership between investors, the UN Global Compact, the PRI, UNEP-FI and UNCTAD.

Your organisation’s role in the initiative during the reporting year (see definitions)

Basic

Moderate

Advanced

31

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

Aviva Investors played a prominent role in helping to establish the Sustainable Stock Exchange (SSE) in 2009, which is now run by PRI, UNEP, UNGC and UNCTAD. The SSE initiative is a peer-to-peer learning platform for exploring how exchanges, in collaboration with investors, regulators, and companies, can enhance corporate transparency - and ultimately performance - on ESG issues and encourage sustainable investment as well as promoting sustainable capital markets encouraging long term approaches to investment.

In 2015 30 stock exchanges joined the initiative, whilst stock exchanges from Kazakhstan, Mexico, Morocco, Norway and Spain announced their public commitment to produce a guidance on ESG disclosure by the end of 2016. These five exchanges join eight others that announced their commitment at the launch of the United Nations SSE initiative's Campaign to Close the ESG Guidance Gap, hosted at the London Stock Exchange in September 2015.

Other collaborative organisation/initiative, specify

2020 Stewardship Working Party

Your organisation’s role in the initiative during the reporting year (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

We are founding members of the 2020 Stewardship Working Party a group whose outputs include:

development of the stewardship framework of the PLSA (formerly NAPF)

publication, with the ICSA, of 'Enhancing Stewardship Dialogue'

research collaboration of the Investment Association, PLSA, ICSA and Investor Relations Society to

assess the progress of stewardship since the introduction of the Stewardship Code.

Other collaborative organisation/initiative, specify

Investment Association (IA)

Your organisation’s role in the initiative during the reporting year (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

We are active memebrs of the Investment Association participating in various ways including:

members of the Corporate Governance and Stewardship Committee

Directorship on the Board of the Investor Forum, the IAs body for collective investor engagement

members of the Productivity Steering Group that is producing an Action Plan for improved productivity for

UK companies.

32

Other collaborative organisation/initiative, specify

Corporate Human Rights Benchmark (CHRB)

Your organisation’s role in the initiative during the reporting year (see definitions)

Basic

Moderate

Advanced

Provide a brief commentary on the level of your organisation’s involvement in the initiative. [Optional]

In December 2014, together with six collaborating NGO, investor and research organisations, Aviva Investors launched the Corporate Human Rights Benchmark (CHRB). This is the first global project to rank companies on their human rights performance. The CHRB will harness the competitive nature of the markets to drive better human rights performance by developing a transparent, publicly available and credible benchmark. Initially, a total of 500 of the worlds top companies from the four highest impact sectors for human rights risks (agriculture, telecom and consumer electronics production, textile and clothing manufacture and raw materials) will all be researched and ranked on their human rights performance.

Aviva Investors Chairs the Steering Group that in 2015 oversaw the global stakeholder consultation to develop the measurement themes and indicators.

SG 09 Mandatory Core Assessed PRI 4

SG 09.1 Indicate if your organisation promotes responsible investment, independently of collaborative initiatives.

Yes

SG 09.2 Indicate which of the following actions your organisation has taken to promote responsible investment, independently of collaborative initiatives.

Provided or supported education or training programmes for clients, investment managers, broker/dealers, investment consultants, legal advisers or other investment organisations

Provided financial support for academic or industry research on responsible investment

Encouraged better transparency and disclosure of responsible investment practices across the investment industry

Spoke publicly at events and conferences to promote responsible investment

Wrote and published in-house research papers on responsible investment

Encouraged the adoption of the PRI

Wrote articles on responsible investment in the media.

Other, specify

No

SG 09.3 Additional information. [Optional]

During the year we have launched a number of initiatives to further develop our own responsible investment practices and to improve corporate practice within specifc sectors and on specific topics. All of these initiatives have a global reach and are aimed at improving company performance and market standards.

Climate change

33

As part of our proactive response to understanding climate risk and the economic implications to our customers, business and society as a whole, Aviva commissioned research from the Economist Intelligence Unit on the value at risk from climate change to the global asset base, including investment, pensions and long-term savings. We have been active in sharing this publicly available research amongst the industry.

In July 2015 we set out our Strategic Response to Climate Change, which identified five areas where we will focus our attention as part of our contribution to tackling climate change. The response is based on five carbon pillars, which all have an associated work stream. These are: further integrating climate risk into investment considerations; investment in lower carbon infrastructure; supporting policy action on climate change; active stewardship on climate risk; and divesting where necessary.

World Heritage Sites

Together with Investec Asset Management and WWF we launched a report on protecting World Heritage Sites (WHS) from extractive activites. Together we produced research on the scale of the problem, producing guidance and recommendations for investors as well as establishing a collaborative engagement group via the PRI Clearing House. We consider launching projects to address emerging issues an important part of our responsibility as investors.

Human rights

Along with 6 partners, Aviva Investors launched the Corporate Human Rights Benchmark (CHRB). This is the first global project to rank companies on their human rights performance. The CHRB will harness the competitive nature of the markets to drive better human rights performance by developing a transparent, publicly available and credible benchmark. Initially, a total of 500 of the worlds top companies from the four highest impact sectors for human rights risks (agriculture, telecom and consumer electronics production, textile and clothing manufacture and raw materials) will all be researched and ranked on their human rights performance.

SG 10 Voluntary Additional Assessed PRI 4,5,6

SG 10.1 Indicate if your organisation - individually or in collaboration with others - conducted dialogue with public policy makers or regulators in support of responsible investment in the reporting year.

Yes

Yes, individually

Yes, in collaboration with others

SG 10.2 Select the methods you have used.

Endorsed written submissions to governments, regulators or public policy developed by others

Drafted your own written submissions to governments, regulators or public policy markers

Participated in face-to-face meetings with government members or officials to discuss policy

Other, specify

SG 10.3 Where you have made written submissions (individually or collaboratively) to governments and regulatory authorities, indicate if these are publicly available.

Yes, publicly available

No

No

Implementation not in other modules

SG 12 Mandatory to Report Voluntary to Disclose Descriptive PRI 1

34

SG 12.1 Some investment risks and opportunities arise as a result of long term trends. Indicate which of the following you consider.

Changing demographics

Climate change

SG 12.2 Indicate which of the following activities you have undertaken to respond to climate change risk and opportunity

Established a climate change sensitive or climate change integrated asset allocation strategy

Targeted low carbon or climate resilient investments

Reduced portfolio exposure to emissions intensive or fossil fuel holdings

Used emissions data or analysis to inform investment decision making

Sought climate change integration by companies

Sought climate supportive policy from governments

Other, specify

None of the above

SG 12.3 Indicate which of the following tools you use to manage emissions risks and opportunities

Carbon footprinting

Scenario testing

Disclosure on emissions risk to clients/trustees/management/beneficiaries

Target setting for emissions risk reduction

Encourage internal and/or external portfolio managers to monitor emissions risk

Emissions risk monitoring and reporting are formalised into contracts when appointing managers

Other, specify

None of the above

Resource scarcity

Technology developments

Other, specify(1)

Other, specify(2)

None of the above

SG 12.5 Additional information [Optional]

Our Strategic Response to Climate Change identified five areas where we will focus our attention as part of our contribution to tackling climate change. The response is based on five carbon pillars, which all have an associated work stream. These are:

4. Further integrating climate risk into investment considerations - we will continue to explore ways to

integrate carbon risk, alongside other material environmental, social and governance issues (ESG) , and

actively seek to collaborate to publish new research and insights. We remain deeply committed to ensuring

ESG issues are included in our investment analysis and decision making.

5. Investment in lower carbon infrastructure - we will target a £500 million annual investment in low-carbon

infrastructure for the next five years. This means more money invested into renewable energy and energy

efficiency. We will also target 'carbon returns' alongside financial returns on our investment and are setting an

35

associated carbon savings target for this investment of 100,000 tonnes of CO2 annually. The transition to a

low-carbon economy requires capital. A large proportion of this will need to be directed towards infrastructure.

6. Supporting strong policy action on climate change - we supported policymakers in negotiating a credible

long-term greenhouse gas reduction goal at the upcoming UNFCCC negotiations in Paris in December 2015

and beyond that at a national and regional level. It is in all our interests to see a smooth transition to a lower

carbon economy. We consider climate change a market failure that requires government action to correct.

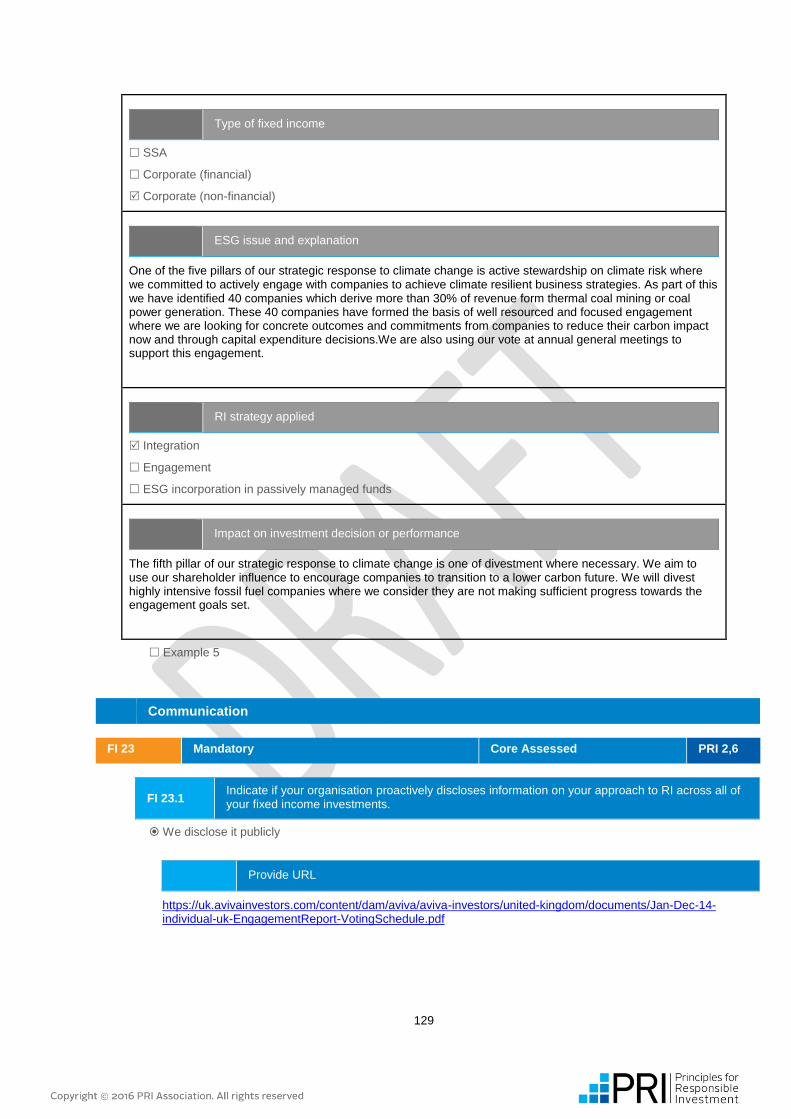

7. Active stewardship on climate risk - we have been actively engaging with 40 coal companies to achieve

climate-resilient business strategies. We have a fiduciary duty to protect and enhance the value of client

assets. Acting as responsible stewards - engaging and voting with the companies where we are shareholders

- is central to delivering this.

8. Divesting where necessary - we have committed to divest highly carbon-intensive fossil fuel companies

where we consider they are not making sufficient progress towards the engagement goals set. This decision

will not be taken lightly and only where we believe that divestment is a balanced and proportionate response.

Further information can be found here: http://www.aviva.com/media/thought-leadership/climate-change-value-risk-investment-and-avivas-strategic-response/

SG 13 Mandatory to Report Voluntary to Disclose Descriptive PRI 1

SG 13.1 Indicate if your organisation allocates assets to, or manages, funds based on specific environmental and social themed areas.

Yes

No

SG 13.4 Additional information [Optional].

We run a limited number of bespoke mandates with specific environmental or social criteria.

Innovation

SG 17 Voluntary Descriptive General

SG 17.1 Indicate whether any specific features of your approach to responsible investment are particularly innovative.

Yes

36

SG 17.2 Describe any specific features of your approach to responsible investment that you believe are particularly innovative.

A key innovation to facilitate our integration of ESG issues into investment analysis and decision-making is our Responsible Investment Officer (RIO) network. This network of 30 fund managers, analysts and support functions is the first point of contact for ESG integration within each investment desk and region. The RIOs play an active role in embedding ESG data and analysis fully into each desk's investment process. This includes working with the Global Responsible Investment team on the most appropriate use of ESG data and the development of tools.

No

Assurance of responses

SG 18 Voluntary Additional Assessed General

SG 18.1 Indicate whether your reported information has been reviewed, validated and/or assured by internal and/or external parties.

Yes

SG 18.2 Indicate who has reviewed, validated and/or assured your reported information.

Reviewed by Board, CEO, CIO or Investment Committee

Validated by internal audit or compliance function

Assured by an external independent provider, specify name

Other, specify

SG 18.3 Describe the steps you have taken to review, validate and/or assure the content of your reported information.

This report was prepared by the Head of Responsible Investment Strategy and Research with support from the RIO network at Aviva Investors and has been reviewed and signed-off by the relevant desk heads for each asset class and the Chief Responsible Investment Officer.

In December 2014, we were pleased to receive independent assurance on our Stewardship Code statement under the AAF 01/06 Stewardship Supplement by PwC. One of less than ten per cent of signatories to the UK Stewardship Code to do so. It is our intention to have our Stewardship Code Statement externally audited periodically.

No

37

Aviva Investors

Reported Information

Public version

Indirect – Manager Selection, Appointment and Monitoring

PRI disclaimer

This document presents information reported directly by signatories. This information has not been audited by the PRI

Secretariat or any other party acting on their behalf. While this information is believed to be reliable, no representations or

warranties are made as to the accuracy of the information presented, and no responsibility or liability can be accepted for

any error or omission.

38

Overview

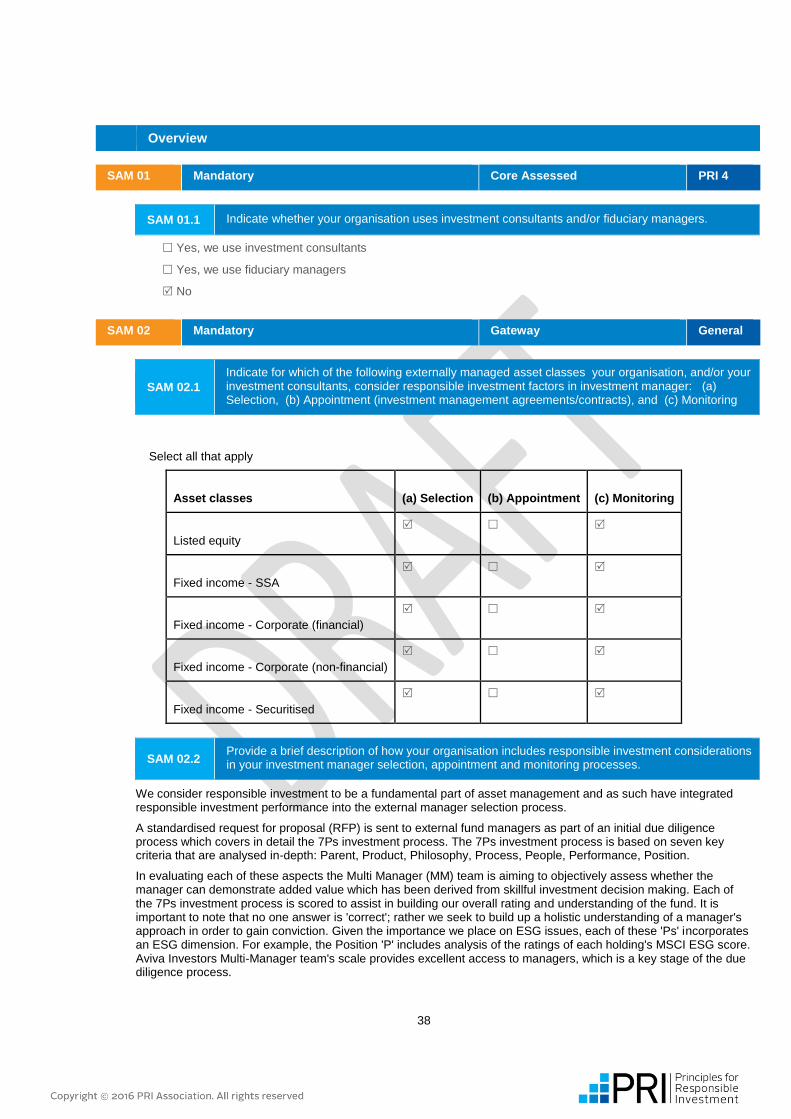

SAM 01 Mandatory Core Assessed PRI 4

SAM 01.1 Indicate whether your organisation uses investment consultants and/or fiduciary managers.

Yes, we use investment consultants

Yes, we use fiduciary managers

No

SAM 02 Mandatory Gateway General

SAM 02.1

Indicate for which of the following externally managed asset classes your organisation, and/or your investment consultants, consider responsible investment factors in investment manager: (a) Selection, (b) Appointment (investment management agreements/contracts), and (c) Monitoring

Select all that apply

Asset classes

(a) Selection

(b) Appointment

(c) Monitoring

Listed equity

Fixed income - SSA

Fixed income - Corporate (financial)

Fixed income - Corporate (non-financial)

Fixed income - Securitised

SAM 02.2 Provide a brief description of how your organisation includes responsible investment considerations in your investment manager selection, appointment and monitoring processes.

We consider responsible investment to be a fundamental part of asset management and as such have integrated responsible investment performance into the external manager selection process.

A standardised request for proposal (RFP) is sent to external fund managers as part of an initial due diligence process which covers in detail the 7Ps investment process. The 7Ps investment process is based on seven key criteria that are analysed in-depth: Parent, Product, Philosophy, Process, People, Performance, Position.

In evaluating each of these aspects the Multi Manager (MM) team is aiming to objectively assess whether the manager can demonstrate added value which has been derived from skillful investment decision making. Each of the 7Ps investment process is scored to assist in building our overall rating and understanding of the fund. It is important to note that no one answer is 'correct'; rather we seek to build up a holistic understanding of a manager's approach in order to gain conviction. Given the importance we place on ESG issues, each of these 'Ps' incorporates an ESG dimension. For example, the Position 'P' includes analysis of the ratings of each holding's MSCI ESG score. Aviva Investors Multi-Manager team's scale provides excellent access to managers, which is a key stage of the due diligence process.

39

The RFP incorporates a number of questions relating to ESG, both at the firm level and in the investment process.These are focused on assessing external fund managers' commitment but also evidence of their ESG integration strategy.

The MM team seeks to understand how managers consider and incorporate ESG factors into their investment processes. For instance, although a number of the asset managers that the MM team invests with are signatories to the PRI (as at end 2015, just over 79% of our managers are PRI signatories, up from 55% in 2014), the MM team also seeks evidence through the due diligence process that these values feed into the individual strategy level.

It is indeed not just about potential robust corporate ESG policies, the team requires external fund managers to evidence ESG integration and ownership (where relevant) in their investment processes.

Once appointed, ESG features in the monitoring process and is covered during the review meetings we regularly host with managers.

Listed equity (LE) and Fixed income (FI)

Overview

SAM 03 Mandatory to Report Voluntary to Disclose Gateway General

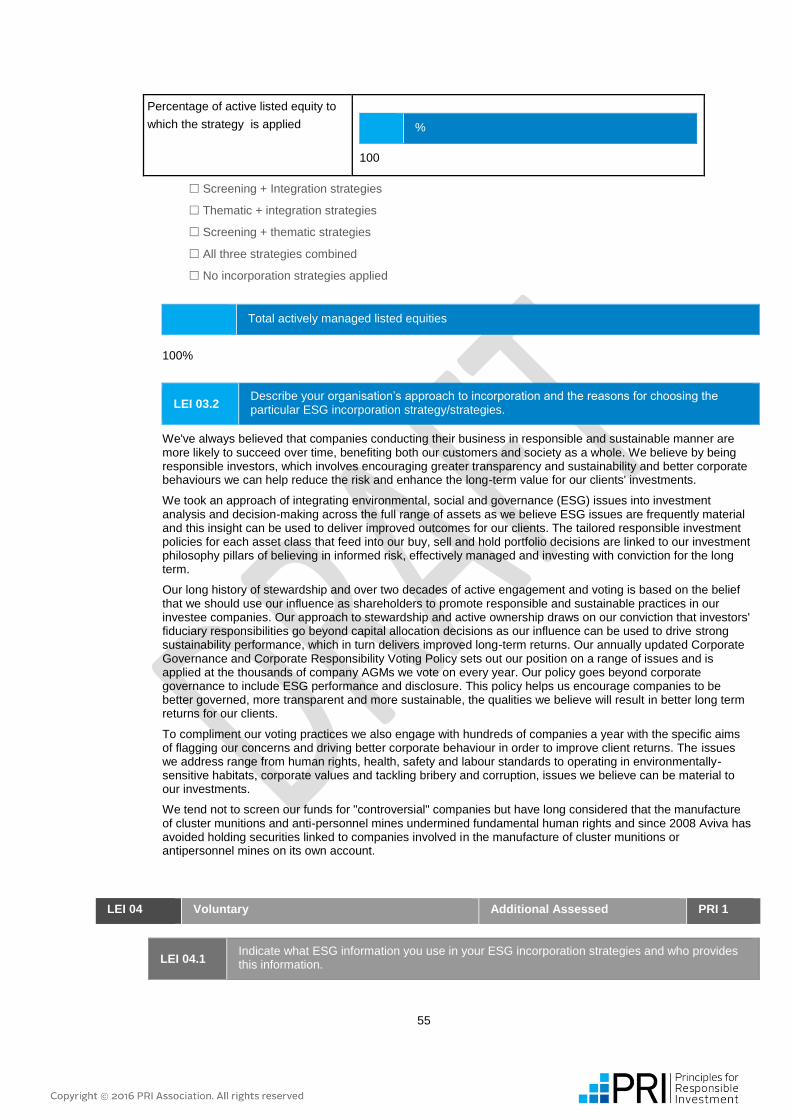

SAM 03.1 Provide a breakdown of your externally managed listed equities and fixed income by passive, active quant and, active fundamental and other active strategies.

40

Listed equity (LE)

Passive strategies

0

Active - quantitative (quant) strategies

10

Active - fundamental and active - other

90

100%

Fixed income - SSA (SSA)

Passive strategies

0

Active - quantitative (quant) strategies

0

Active - fundamental and active - other

100

100%

Fixed income - Corporate

(financial)

Passive strategies

0

Active - quantitative (quant) strategies

0

Active - fundamental and active - other

100

100%

Fixed income - Corporate

(non-financial)

Passive strategies

0

Active - quantitative (quant) strategies

0

41

Active - fundamental and active - other

100

100%

Fixed income - Securitised

Passive strategies

0

Active - quantitative (quant) strategies

0

Active - fundamental and active - other

100

100%

SAM 04 Mandatory Gateway PRI 1,2

Appeal approved for this indicator

SAM 04.1 Indicate which of the following ESG incorporation strategies you require your external manager(s) to implement on your behalf:

Active investment strategies

Active investment strategies

LE

SSA

Corporate (financial)

Corporate (non-financial)

Securitised

Screening

Thematic

Integration

None of the above

Selection

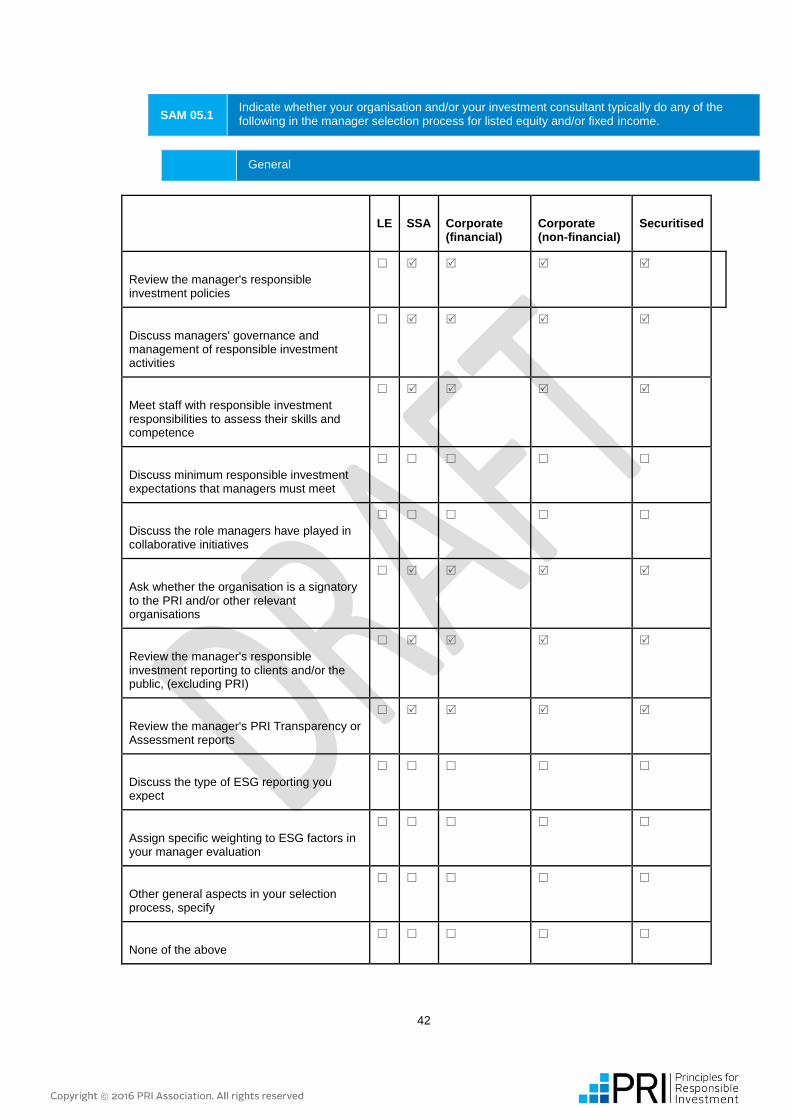

SAM 05 Mandatory Core Assessed PRI 1-6

42

SAM 05.1 Indicate whether your organisation and/or your investment consultant typically do any of the following in the manager selection process for listed equity and/or fixed income.

General

LE

SSA

Corporate (financial)

Corporate (non-financial)

Securitised

Review the manager's responsible investment policies

Discuss managers' governance and management of responsible investment activities

Meet staff with responsible investment responsibilities to assess their skills and competence

Discuss minimum responsible investment expectations that managers must meet

Discuss the role managers have played in collaborative initiatives

Ask whether the organisation is a signatory to the PRI and/or other relevant organisations

Review the manager's responsible investment reporting to clients and/or the public, (excluding PRI)

Review the manager's PRI Transparency or Assessment reports

Discuss the type of ESG reporting you expect

Assign specific weighting to ESG factors in your manager evaluation

Other general aspects in your selection process, specify

None of the above

43

ESG incorporation

SSA

Corporate (financial)

Corporate (non-financial)

Securitised

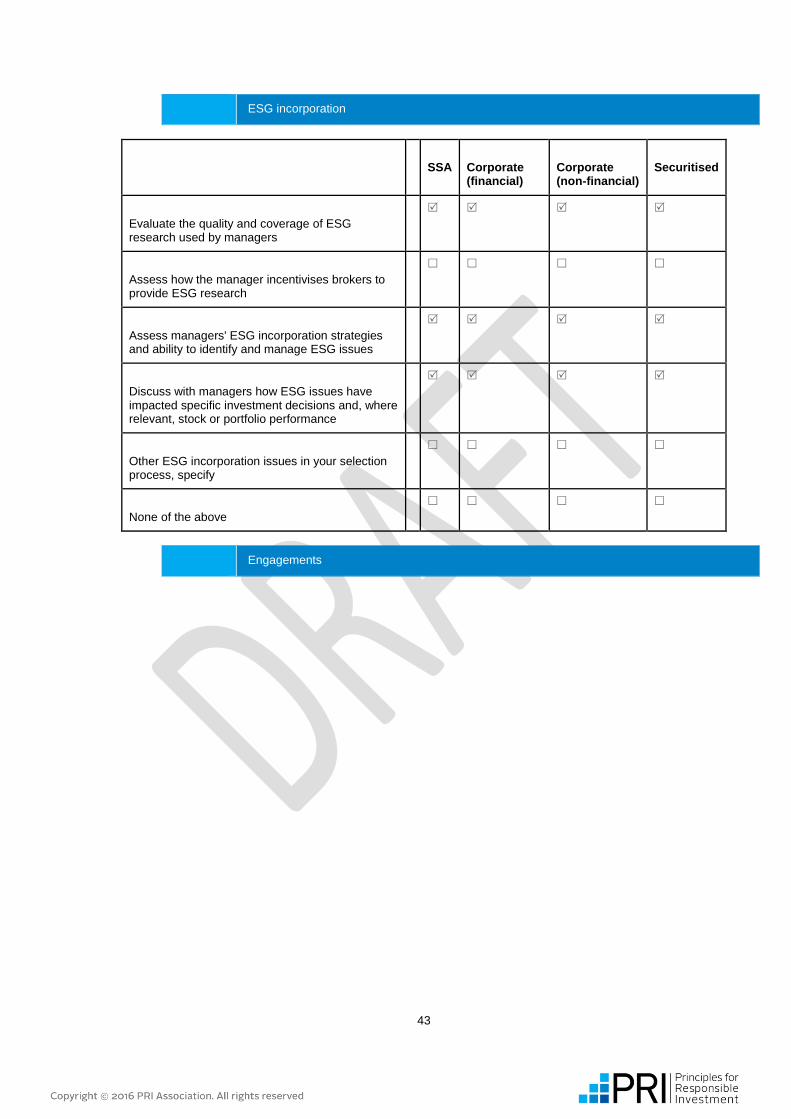

Evaluate the quality and coverage of ESG research used by managers

Assess how the manager incentivises brokers to provide ESG research

Assess managers' ESG incorporation strategies and ability to identify and manage ESG issues

Discuss with managers how ESG issues have impacted specific investment decisions and, where relevant, stock or portfolio performance

Other ESG incorporation issues in your selection process, specify

None of the above

Engagements

44

SSA

Corporate (financial)

Corporate (non-financial)

Securitised

Discuss with the manager the historic interactions they have had with the investee entities

Discuss the comprehensiveness of managers' engagement processes

Discuss the role managers have played in influencing investee entities' ESG practices and performance

Discuss the escalation strategies the manager deploys in case of insufficient ESG performance

Discuss how information gained through engagement is incorporated into investment decision-making

Other engagement issues in your selection process,specify

None of the above

(Proxy) voting

LE

Discuss the managers' voting processes

Discuss how information gained through research for (proxy) voting is used in investment-decision making

Discuss whether the manager is able to deploy the asset owner's proprietary voting policy or aligning its voting policy with the asset owner's investment beliefs and strategy

Other (proxy) voting issues in your selection process, specify

None of the above

45

SAM 05.2 Please describe the level of experience board members/trustees/chief-level staff have with incorporating ESG factors into investment decision-making processes.

This question is not applicable.

Monitoring

SAM 07 Mandatory Core Assessed PRI 1

SAM 07.1 Indicate whether your organisation and/or your investment consultant in the dialogue and monitoring of your external manager typically do any of the following.

General

46

LE

SSA

Corporate (financial)

Corporate (non-financial)

Securitised

Include responsible investment as a standard agenda item at performance review meetings

Highlight examples of good responsible investment practice by other managers

Discuss if the manager has acted in accordance with your overall investment beliefs on responsible investment and ESG issues

Discuss if the manager has acted in accordance with your organisation's overall strategy on responsible investment and ESG issues

Discuss if the manager has acted in accordance with your organisation's overall policy on responsible investment and ESG issues

Review the manager's responsible investment reporting (excluding PRI)

Review the manager's PRI Transparency or Assessment reports

Review ESG characteristics of the portfolio

Review the impact of ESG issues on financial performance

Encourage your managers to consider joining responsible investment initiatives/organisations or participate in collaborative projects with other investors

Include responsible investment criteria as a formal component of overall manager performance evaluation

Other general aspects of your monitoring, specify

None of the above

ESG incorporation

47

SSA

Corporate (financial)

Corporate (non-financial)

Securitised

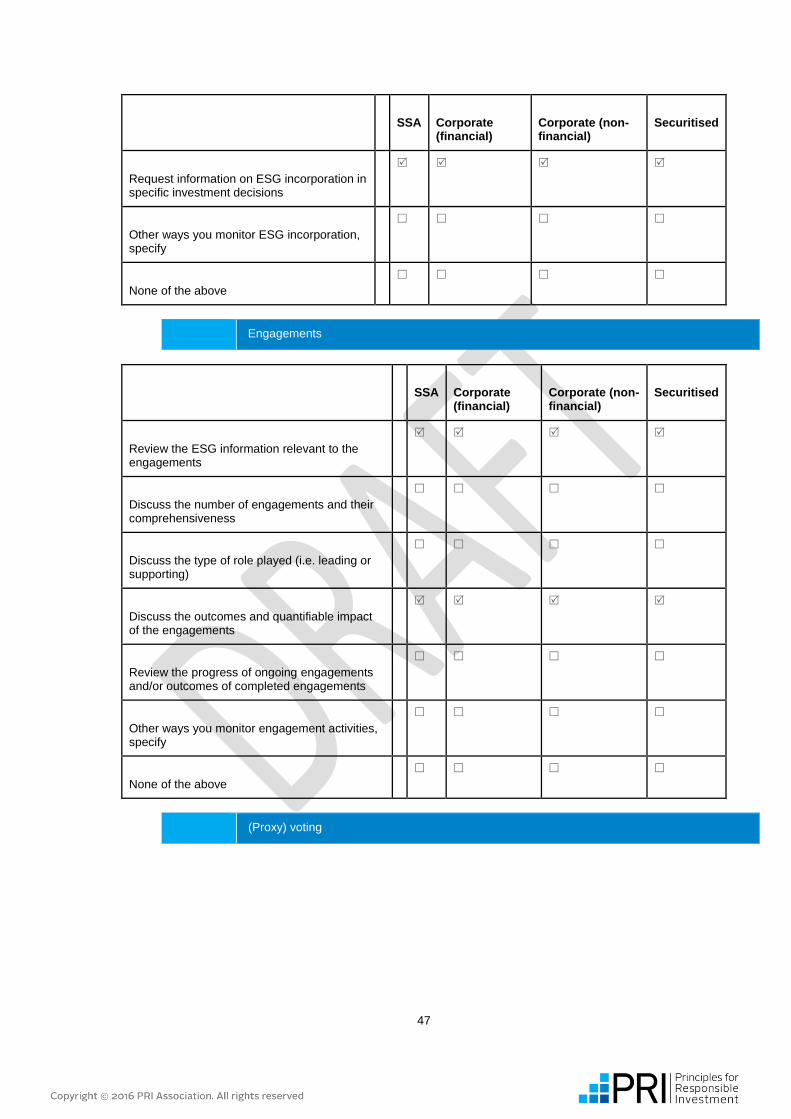

Request information on ESG incorporation in specific investment decisions

Other ways you monitor ESG incorporation, specify

None of the above

Engagements

SSA

Corporate (financial)

Corporate (non-financial)

Securitised

Review the ESG information relevant to the engagements

Discuss the number of engagements and their comprehensiveness

Discuss the type of role played (i.e. leading or supporting)

Discuss the outcomes and quantifiable impact of the engagements

Review the progress of ongoing engagements and/or outcomes of completed engagements

Other ways you monitor engagement activities, specify

None of the above

(Proxy) voting

48

LE

Review the number or percentage of votes cast

Request an explanation of reasons for votes cast

Discuss whether companies were informed of the reasons for votes against management recommendations or abstentions/withheld votes

Review the number of resolutions on ESG issues filed or co-filed

Discuss the changes in company practice (outcomes) that have been achieved from voting activities

Other ways you monitor (proxy) voting activities, specify

None of the above

If you select any 'Other' option(s), specify

Our sub investment managers apply their own voting policies to our mandates, however our Investment Management Agreements (IMA) require that they provide us with their proxy voting records. We publish these proxy voting records on our website alongside the votes cast by Aviva Investors using our Corporate Governance and Corporate Responsibility Voting Policy.

SAM 08 Mandatory Core Assessed PRI 2

SAM 08.1 For the listed equities where you have given your external managers a (proxy) voting mandate, indicate the approximate percentage (+/- 5%) of votes that were cast during the reporting year.

We track or collect this information

Votes cast (to the nearest 5%)

%

80

Specify the basis on which this percentage is calculated

Of the total number of ballot items on which they could have issued instructions

Of the total number of company meetings at which they could have voted

Of the total value of your listed equity holdings on which they could have voted

We do not track or collect this information

49

SAM 08.2 Additional information. [Optional]

A small number of our managers do not have the resources to proxy vote on our behalf. We are currently looking into voting these holdings ourselves applying our Corporate Governance and Corporate Responsibility Voting Policy.

Outputs and outcomes

SAM 13 Voluntary Descriptive PRI 2

SAM 13.1 Provide examples of how ESG issues have been addressed in the manager selection, appointment and/or monitoring process for your organisation during the reporting year.

Add Example 1

Topic or

issue Integration

Conducted

by Internal staff

Asset class All asset classes

Listed Equity

Fixed income – SSA

Fixed income – corporate (financial)

Fixed income – corporate (financial)

Fixed income – securitised

Scope and

process In a recent monitoring meeting with an equity manager with a focus on Asian equities, the manager gave us a specific example of a stock they chose not to invest in following interaction with their dedicated ESG team. The ESG team highlighted a case of child labour at an affiliate of the company in question and the manager decided not to invest.

Outcomes This demonstrated that their ESG process actively impacts portfolio management decisions, confirming our conviction in the responsible investment performance of the manager.

Add Example 2

50

Topic or

issue ESG scoring

Conducted

by Internal staff

Asset class All asset classes

Listed Equity

Fixed income – SSA

Fixed income – corporate (financial)

Fixed income – corporate (financial)

Fixed income – securitised

Scope and

process A manager of a short-dated corporate bond fund described how ESG scores feed into analyst reports. If the scores are low the team are required to carry out a further assessment prior to investing. If the score is low due to poor governance or poor accounting standards it is highly unlikely the team would invest.

Outcomes We consider a fully integrated ESG research function as best in class. This is a strong positive and a contributory factor as to why we have strong conviction in this manager.

Add Example 3

51

Topic or

issue Screening for CCC holdings

Conducted

by Internal staff

Asset class All asset classes

Listed Equity

Fixed income – SSA

Fixed income – corporate (financial)

Fixed income – corporate (financial)

Fixed income – securitised

Scope and

process As part of our active monitoring process we recently reviewed our Asian managers, specifically, we use the MSCI ESG screen to see how many CCC rated holdings our managers are exposed to. We have one manager in this area who is very conscious of ESG in their process and they were not exposed to any CCC rated holdings. Where our managers are exposed to CCC holdings we question our managers at our bi-annual meetings on these holdings.

Outcomes These reviews are used to understand how well ESG is integrated into their approach and hold managers to account on their communicated processes.

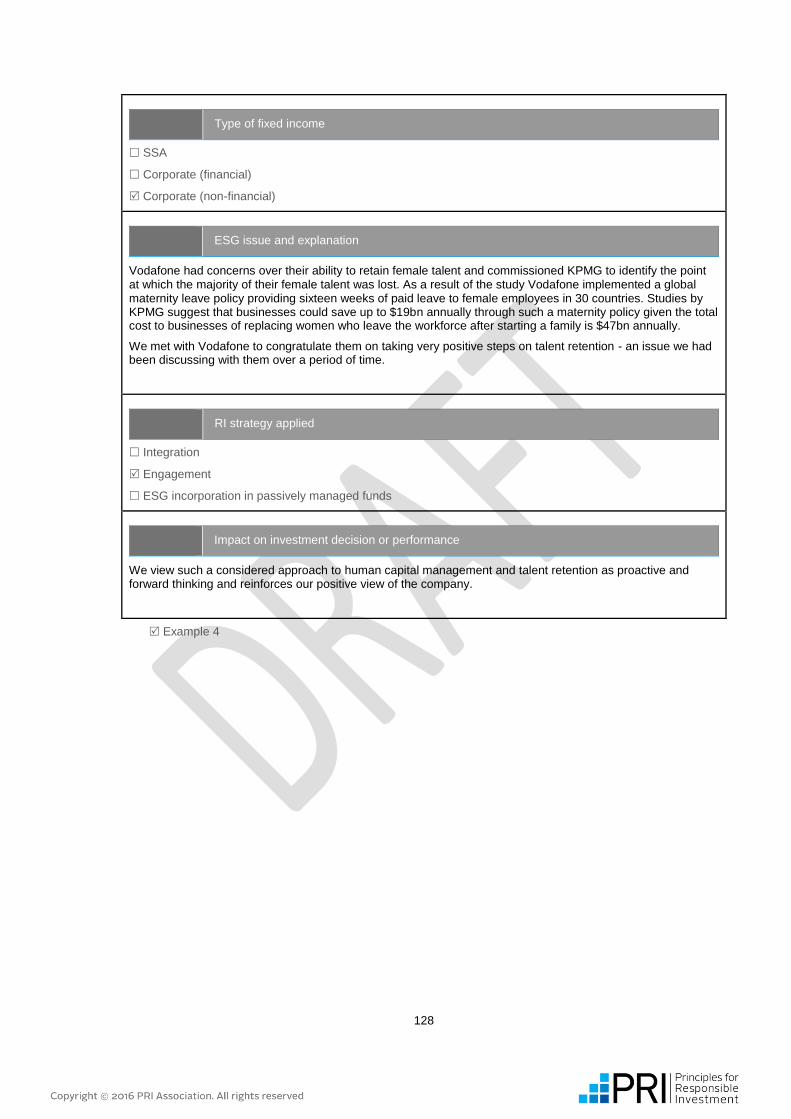

Add Example 4

Add Example 5

Communication

SAM 14 Mandatory Core Assessed PRI 6

SAM 14.1 Indicate if your organisation proactively discloses any information about responsible investment considerations in your indirect investments.

Yes, we disclose information publicly

provide URL

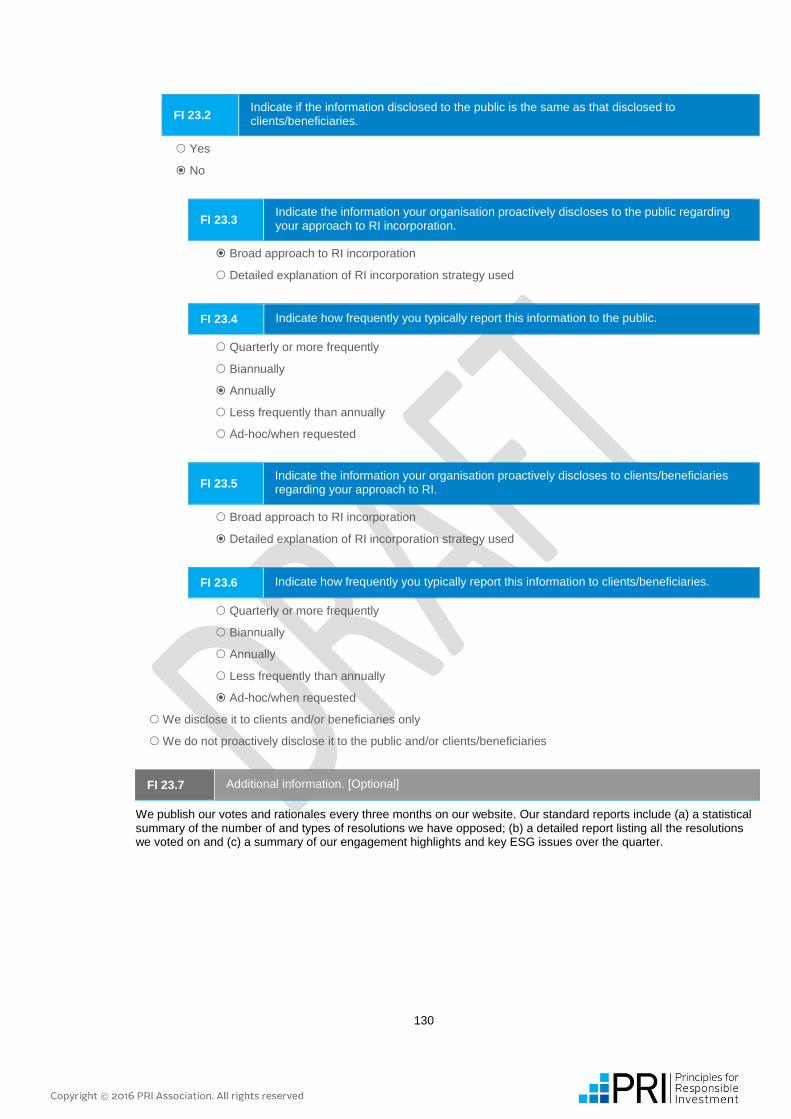

https://uk.avivainvestors.com/content/dam/aviva/aviva-investors/united-kingdom/documents/Jan-Dec-14-individual-uk-EngagementReport-VotingSchedule.pdf

SAM 14.2 Indicate if the level of information you disclose to the public is the same as that disclosed to clients and/or beneficiaries.

Yes

No

52

SAM 14.3 Indicate what type of information your organisation proactively discloses to the public and clients and/or beneficiaries about your indirect investments.

Information

Public

Clients/beneficiaries

How responsible investment considerations are included in manager selection, appointment and monitoring processes

Details of the responsible investment activities carried out by managers on your behalf

E, S and/or G impacts and outcomes that have resulted from your managers' investments and active ownership

Other, specify below

Yes, we disclose information to clients/beneficiaries only

We do not proactively disclose information to the public and/or clients/beneficiaries

SAM 14.4 Additional information. [Optional]

ESG is part of both the Multi Manager (MM) team's RFP process as well as part of its in-depth investment process.We now report on the voting of our underlying external managers on the Aviva Investors website. Upon client request, we could also provide details of the responsible investment activities carried out by managers on our behalf as well as specific E, S and/or G impacts from some of the MM team's investments and active ownership .

53

Aviva Investors

Reported Information

Public version

Direct - Listed Equity Incorporation

PRI disclaimer

This document presents information reported directly by signatories. This information has not been audited by the PRI

Secretariat or any other party acting on their behalf. While this information is believed to be reliable, no representations or

warranties are made as to the accuracy of the information presented, and no responsibility or liability can be accepted for

any error or omission.

54

Overview

LEI 01 Mandatory to Report Voluntary to Disclose Gateway General