rice supply and demand - coocan

TRANSCRIPT

Global Trend of

Rice Supply and Demand

Osamu Koyama

JIRCAS

需給

Contents

1. Rice as a Commodity

2. Situation of Trade

3. Price Trend

4. Demand Shift

5. Future Perspectives

Rice supplies a major part of

human energy.

World Asia

Kcal/day % Kcal/day %

Total

Food2,831 100 2,719 100

Cereals 1,410 50 1,496 55

Wheat 532 19 503 18

Rice 560 20 823 30

Source: FAOSTAT (2004)

Rice as a commodity: classification

Biological

• Indica

• Japonica

• Javanica

• Glaberrima

• Glutinous

• Non-glutinous

Commercial

• Long grain

• Medium grain

• Short grain

• Aromatic

– Basmati

– Fragrant

• Parboiled

Market share estimate

Total 26,818 100%

Indica 20,068 75%

Japonica 3,186 12%

Aromatic 3,322 12%

Glutinous 242 1%

High Quality 20,226 75%

Low Quality 6,592 25%

Paddy 1,122 4%

Husked 1,077 4%

Milled 20,639 77%

Parboiled 3,980 15%

By quality

By process

By variety

Source: C. Calpe, (FAO, 2004)

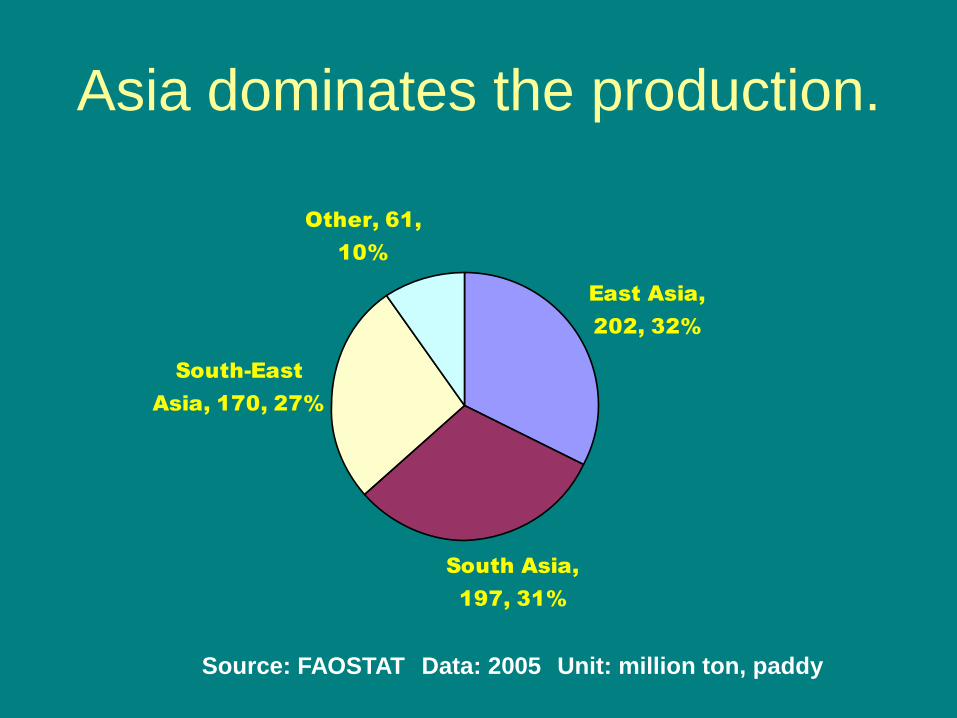

Asia dominates the production.

East Asia,

202, 32%

South Asia,

197, 31%

South-East

Asia, 170, 27%

Other, 61,

10%

Source: FAOSTAT Data: 2005 Unit: million ton, paddy

Source: IRRI

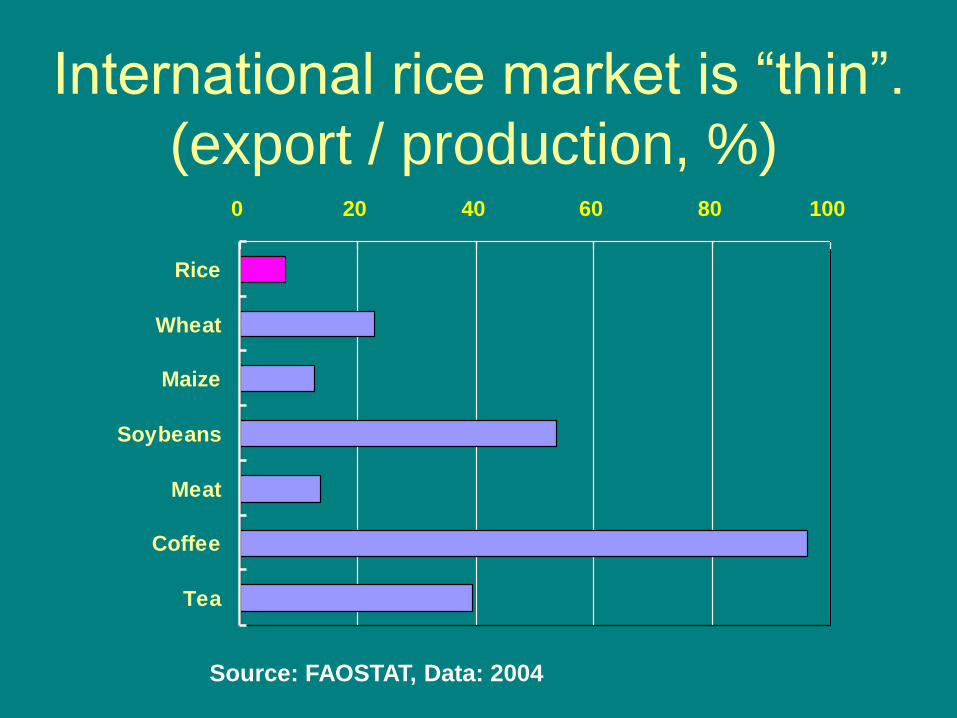

International rice market is “thin”.

(export / production, %)0 20 40 60 80 100

Rice

Wheat

Maize

Soybeans

Meat

Coffee

Tea

Source: FAOSTAT, Data: 2004

But, it becomes a global commodity.Major importing countries (2002/03-04/05)

Philippines 1,594 Brazil 667

Nigeria 1,582 Cuba 656

Saudi Arabia 1,435 Indonesia 563

EU-27 1,108 Mexico 553

Iran 1,061 United States 510

Iraq 994 Ghana 425

South Africa 877 Singapore 365

Senegal 827 Mozambique 358

Cote d'Ivoire 822 Vietnam 323

China 795 Canada 313

Malaysia 779 Cameroon 311

Japan 725 Hong Kong 311

Bangladesh 706 Guinea 257

Source: USDA, Unit: 1,000 tons

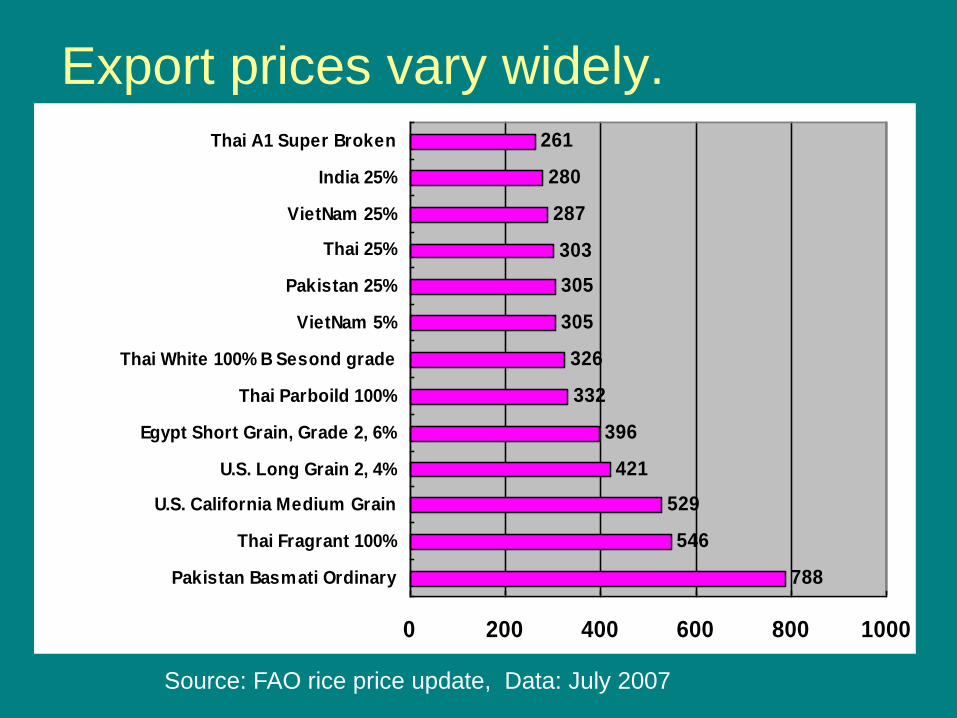

Export prices vary widely.

788

546

529

421

396

332

326

305

305

303

287

280

261

0 200 400 600 800 1000

Pakistan Basmati Ordinary

Thai Fragrant 100%

U.S. California Medium Grain

U.S. Long Grain 2, 4%

Egypt Short Grain, Grade 2, 6%

Thai Parboild 100%

Thai White 100% B Sesond grade

VietNam 5%

Pakistan 25%

Thai 25%

VietNam 25%

India 25%

Thai A1 Super Broken

Source: FAO rice price update, Data: July 2007

Rice is relatively expensive food,

But, losing ground recently.

0

50

100

150

200

250

300

350

400

4501990

1992

1994

1996

1998

2000

2002

2004

Rice, Thailand

Wheat, U.S.

Maize, U.S.

Soybeans, U.S.

Source: FAOSTAT, export unit value, US$ / ton

Because, demand is weak in Asia.

per capita food (kg/year)

0

20

40

60

80

100

120

140

1601

99

0

19

92

19

94

19

96

19

98

20

00

20

02

20

04

China

Indonesia

Malaysia

S. Korea

Japan

Source: FAOSTAT

Diversification of supply side follows.

• From quantity to quality

Japonica increases in China.

• Conversion from rice field to oil crops, feed crops, vegetable and fruits.

How to raise the value of rice.

In Africa, the situation is different.

0

5

10

15

20

25

30

1990

1993

1996

1999

2002

2005

Consumption

Production

Source: FAOSTAT, Unit: million tons

Scenery at village market in Africa

Future constraints: water resources

• Rice requires more water than other crops.

• Conflict with industrial and urban use

• New water saving technologies

• Additional investment for water

Yield growth reaches the ceiling?

0

1

2

3

4

5

6

71960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

ton

s/h

a East Asia

South Asia

Southeast Asia

Source: USDA, PS&D Views

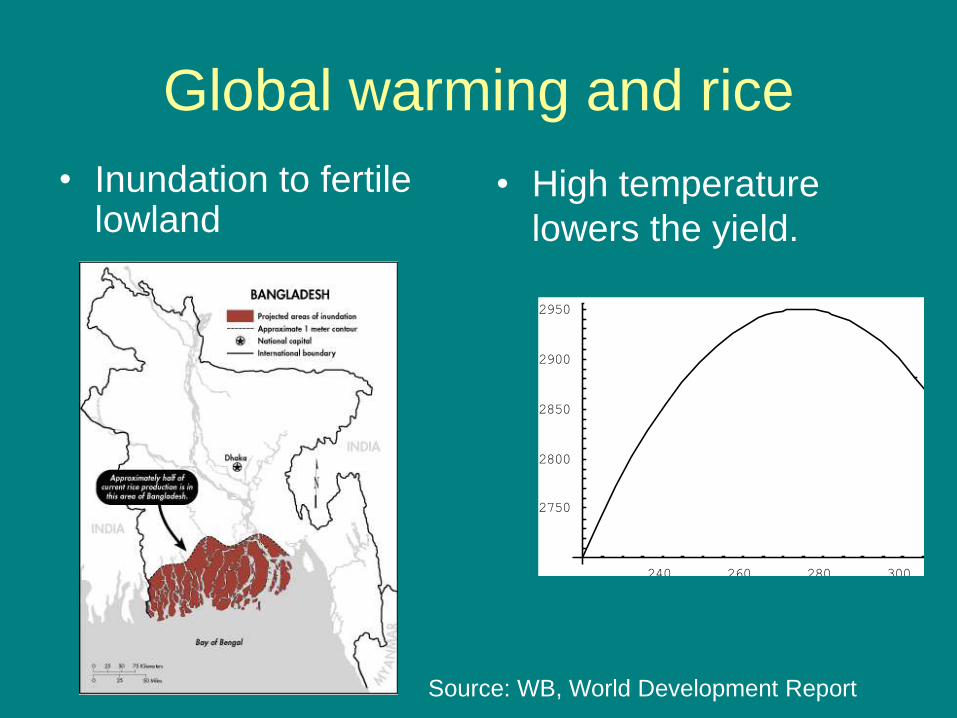

Global warming and rice

• Inundation to fertile lowland

• High temperature

lowers the yield.

240 260 280 300 320

2750

2800

2850

2900

2950

Source: WB, World Development Report

Bio-energy: risk or opportunity?

• Rice grains

– Economically not feasible

• Rice residue (straws and husks)

– Potential for thermal co-generation

• Indirect impacts

– Competition of arable land

– Additional demand Higher price

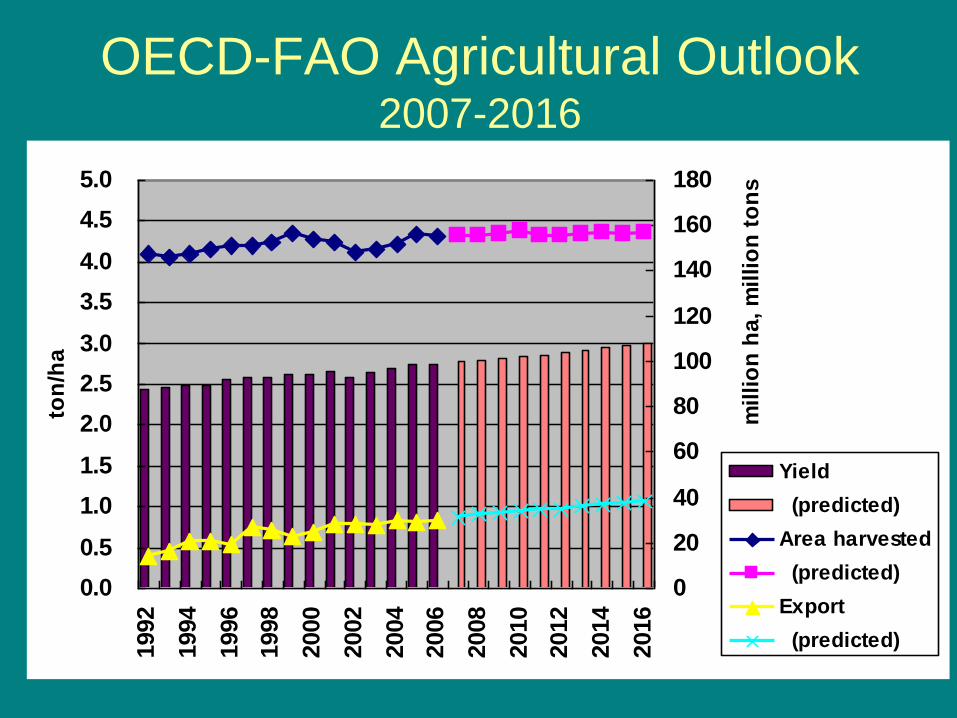

OECD-FAO Agricultural Outlook2007-2016

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

ton

/ha

0

20

40

60

80

100

120

140

160

180

mil

lio

n h

a,

mil

lio

n t

on

s

Yield

(predicted)

Area harvested

(predicted)

Export

(predicted)

Key Issues

Demand

• Diversification & market segregation

• Non-food use

Supply

• Yield potentials

• Sustainability & multi-functionality

Market

• Trade liberalization & food security

• New players (supermarkets, integration)