rising stars of asia - cpmaindia.comrising stars of asia it’s not just about china…. apic...

TRANSCRIPT

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Rising Stars of AsiaIt’s not just about China….

APIC Marketing Seminar

20 August 2018 | Kuala Lumpur, Malaysia

Tony Potter

Vice President, Specialty Chemicals, IHS Markit

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

-220

0

220

440

660

880

1,100

-10

0

10

20

30

40

50

2000 2003 2006 2009 2012 2015 2018 2021

US Ethane WEP Naphtha SEA Naphtha

Regional ethylene annual cash margins

Source: IHS Markit

Cents

Per

Pound

Dolla

rs P

er

Metr

ic T

on

© 2018 IHS Markit

Margins driving 2021+ olefin capacity additions in Asia

Strong margins

encouraged builds

Weak margins

stalled builds

Another wave

in the works?

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

Agenda

• Demographics

>Population and urbanisation

• Industry dimensions

• Olefins capacity build and trade

evolution

• Aromatics capacity build

• India

• ASEAN

3

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

Customers: India and ASEAN populations are growing faster than China

4

0

400

800

1200

1600

2000

2000 2005 2010 2015 2020 2025 2030 2035 2040

China India Japan/Korea/Taiwan ASEAN

© 2017 IHS MarkitSource: IHS Markit

Mill

ions

Population

Population 2017 Millions

Indonesia 261

Philippines 105

Vietnam 95

Thailand 68

Myanamar 55

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

Customers: India and ASEAN populations are growing faster than China

5

0

50

100

150

200

250

300

2015 2020 2025 2030 2035

Millio

ns

China India ASEAN

Source: IHS Markit © 2017 IHS Markit

Cumulative Population Growth (2015 = 0)

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

Urbanisation will sustain demand growth even as population plateaus in China

6

0

50

100

150

200

250

300

2015 2020 2025 2030 2035

Millio

ns

China India ASEAN China Urban India Urban ASEAN Urban

Source: IHS Markit © 2017 IHS Markit

Cumulative Urban Population Growth (2015 = 0)

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

7

Chemicals and polymers continue to penetrate our economies with substantial

demand growth potential

0

2

4

6

8

10PE

PP

Average Polyolefin Demand Growth 2017-2022

Source: IHS Markit © 2017 IHS Markit

Avera

ge

Dem

an

d G

row

th %

p.a

.

0 20 40 60 80 100

USA

S. Korea

Malaysia

Thailand

Japan

China

Singapore

Indonesia

India

PE + PP Consumption per Capita, 2017

Source: IHS Markit © 2017 IHS MarkitKG per Capita in 2017

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

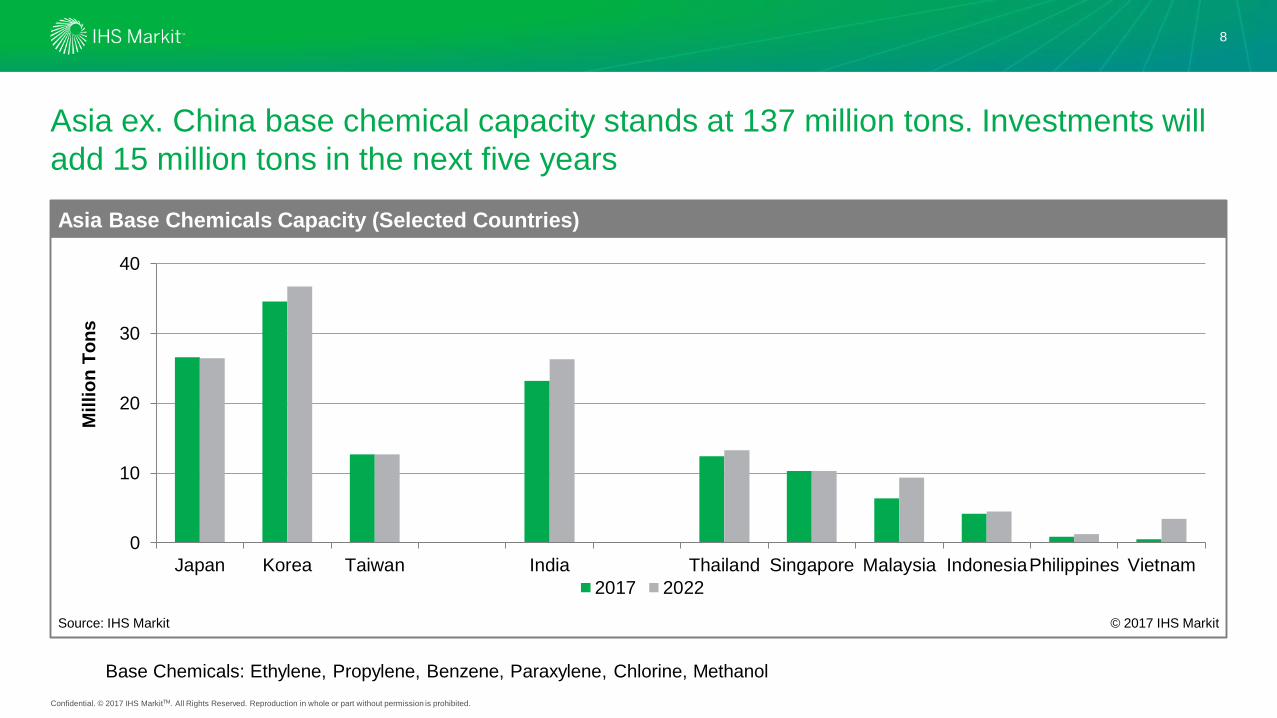

8

0

10

20

30

40

Japan Korea Taiwan India Thailand Singapore Malaysia IndonesiaPhilippines Vietnam

2017 2022

Asia Base Chemicals Capacity (Selected Countries)

© 2017 IHS Markit

Millio

n T

on

s

Source: IHS Markit

Asia ex. China base chemical capacity stands at 137 million tons. Investments will

add 15 million tons in the next five years

Base Chemicals: Ethylene, Propylene, Benzene, Paraxylene, Chlorine, Methanol

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

9

Asia is its own marginal ethylene supplier. Growing domestic deficits of ethylene

derivatives in some ASEAN countries are investment opportunities

-35.0

-25.0

-15.0

-5.0

5.0

15.0

12 13 14 15 16 17 18 19 20 21 22

Millio

n M

etr

ic T

on

s

Japan China Taiwan S. Korea Singapore Indonesia

Malaysia Phillipines Thailand Vietnam Aust/NZ Net Trade

Asia (ex India) Ethylene Net Equivalent Trade

Source: IHS Markit © 2017 IHS Markit

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

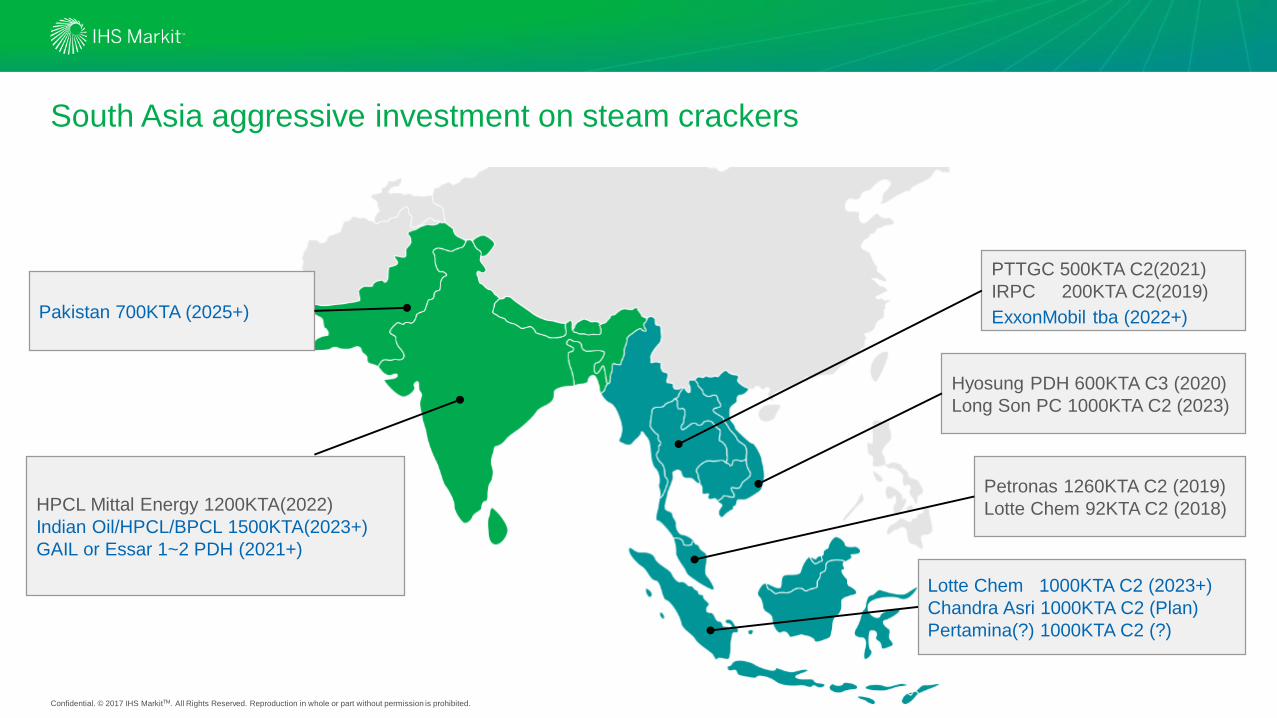

South Asia aggressive investment on steam crackers

Hyosung PDH 600KTA C3 (2020)

Long Son PC 1000KTA C2 (2023)

PTTGC 500KTA C2(2021)

IRPC 200KTA C2(2019)

Petronas 1260KTA C2 (2019)

Lotte Chem 92KTA C2 (2018)

Lotte Chem 1000KTA C2 (2023+)

Chandra Asri 1000KTA C2 (Plan)

Pertamina(?) 1000KTA C2 (?)

HPCL Mittal Energy 1200KTA(2022)

Indian Oil/HPCL/BPCL 1500KTA(2023+)

GAIL or Essar 1~2 PDH (2021+)

Pakistan 700KTA (2025+) ExxonMobil tba (2022+)

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

11

The development of aromatics “mega-complexes” in China threatens existing

exporters

0.0 5.0 10.0 15.0 20.0 25.0

India

SE Asia

Jap/Kor/Twn

China

Million Metric Tons

2012-2017 2017-2022

Asia Incremental Benzene + Paraxylene Capacity 2012-2022

Source: IHS Markit © 2017 IHS Markit

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

12

China self-sufficiency in PTA created a PX opportunity in South Korea that

threatens to be eroded post 2020

0

10

20

30

40

50

60

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

Domestic Molecule PTA Imports PX Imports

China Polyester Production

Source: IHS Markit © 2017 IHS Markit

Millio

nM

etr

ic T

on

s

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited

India

13

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

14

Investment in chemicals and polymers is not keeping up with domestic demand

growth

-9.0

-7.0

-5.0

-3.0

-1.0

1.0

12 13 14 15 16 17 18 19 20 21 22

Ethylene Vinyls Styrenics Polyethylene

Glycol Others Net Trade

Indian Subcontinent Ethylene Net Equivalent Trade

Net Exports

Net Imports

Millio

n M

etr

ic T

on

s

Source: IHS Markit © 2017 IHS Markit

• Despite the start up of new

crackers/expansions by BCPL, GAIL and

OPAL in 2016, and Reliance’s Jamnagar

cracker in 2017, India’s ethylene derivative

deficit is only in temporary respite

• Equivalent ethylene deficit will approach

seven million tons by 2022.

• New crackers under study by Indian

Oil/HPCL/BPCL and by GAIL

• Collaboration of state owned companies is

perhaps a signal of consolidation in the

refining/chemicals space. Too many public

companies created inefficiency rather than

competition

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

India thermoplastics demand will increase four-fold by 2040

15

PE35%

PP33%

PVC22%

PS2%

PET Resin6%

ABS1%

PC1%

Source: IHS Markit © 2017 IHS Markit

2016 India Thermoplastics Demand = 13.3 MM Tons

PE38%

PP38%

PVC15%

PS1%

PET Resin6%

ABS1%

PC1%

Source: IHS Markit © 2017 IHS Markit

2040 India Thermoplastics Demand = 56.3 MM Tons

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

India’s per capita thermoplastics demand will remain modest relative to the US and

China but necessitates the building of 12-15 new world scale steam crackers

16

0 10 20 30 40 50 60 70 80 90 100 110 120 130

India

Global

China

Malaysia

Indonesia

United States

2016 2040Source: IHS Markit © 2017 IHS Markit

KG/person

Thermoplastics Demand per Capita

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited

ASEAN

17

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

Singapore, Malaysia and Thailand are mature petrochemical operators that have

outgrown domestic markets

• Singapore and Thailand must compete with

lower cost Middle East and US olefin derivative

exports

• Malaysia will become exporter with RAPID

start-up

• New crackers would be export oriented with no

feedstock advantage

• But, some parts of the region eg Indonesia are

at least as accessible from these countries as

by potential domestic producers

18

-500

0

500

1000

1500

2000

2500

3000

3500

Singapore Malaysia Thailand

Thousand M

etr

ic T

ons

Ethylene Equiv Propylene Equiv Benzene Paraxylene

Net Trade 2022 Outlook

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

Substantial and growing domestic deficits of base chemicals and polymers offer

investment opportunities in Indonesia, Vietnam and the Philippines

• Refining investments to counter transportation

fuels deficits also provide feedstock platform

for petrochemical investments

• Indonesia and Vietnam studying joint venture

cracker opportunities

• Aromatics complexes being built in Vietnam

and Brunei

• NOC involvement: decision making process is

slow

19

-3000

-2500

-2000

-1500

-1000

-500

0

500

1000

Indonesia Vietnam Philippines

Thousand M

etr

ic T

ons

Ethylene Equiv Propylene Equiv Benzene Paraxylene

Net Trade 2022 Outlook

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Reproduction in whole or part without permission is prohibited.

Strategic Implications

• It’s not just about China

• APAC ex. China

> 2.5 billion potential customers driving petrochemical and polymer demand growth

> 450 million newly urbanized customers over the next 20 years deficits

• Large and growing domestic deficits of petrochemicals and polymers represent investment

opportunities, especially for olefins and derivatives, in India, Indonesia, Vietnam and The

Philippines

• India needs to build 12-15 world scale crackers by 2040 to meet domestic demand – a pace of one

project to FID every 18 months – not happening!

• Olefin margins will remain robust. Aromatics margins under threat from China Mega-units.

• Actually - it’s still a lot about China, which will remain an important export market for ASEAN

20