risk & regulatory academy 2020 - deloitte.com

TRANSCRIPT

Risk & Regulatory Academy 2020

© 2020 Deloitte Central Europe 2© 2020 Deloitte

DAY 1

CREDIT RISK

2Risk & Regulatory Academy

© 2020 Deloitte Central Europe 3

Agenda

IntroductionDimitrios Goranitis, Risk & Regulatory Leader at Deloitte Central Europe

IFRS9 in COVID : Staging, provisioning and the end of the moratoriaGerrit Reher, Credit Risk Leader at Deloitte Germany

Model Implications IFRS 9 and IRB: The time has come to redevelop or recalibrate our models? Thomas Moosbrucker, Quantitative Services Leader at Deloitte Germany

Acting on measured risk – how are banks managing the risk they identify?Krisztina S-Nagy, Risk & Regulatory Leader at Deloitte Hungary

NPL prevention and managementHerve Phaure, Credit Risk Leader at Deloitte France

Implications for Audit – What has changed as a result of COVID-19?Krisztina S-Nagy, Risk & Regulatory Leader at Deloitte Hungary

PANEL DISCUSSION

Dimitrios GoranitisRisk & Regulatory Leader

at Deloitte CE

Herve Phaure Credit Risk Leader at Deloitte France

Przemyslaw SzczygielskiRisk & Regulatory Leader

at Deloitte Poland

Thomas MoosbruckerQuantitative Services Leader

at Deloitte Germany

Gerrit ReherCredit Risk Leader

at Deloitte Germany

Krisztina S-Nagy Risk & Regulatory Leader

at Deloitte Hungary

INTRODUCTION

© 2020. For information, contact Deloitte Central Europe 5

While the overall economy is coming back, the ascent will likely be long, uneven, and uncertain

• Q2 GDP outturns, on balance,delivered positive surpriseas economies reopened

• Momentum going into the fourth quarter appears to be slowing

• The policy initiatives have prevented even worse outcomes and have also helped lift sentiment

• The recovery is expected to strengthen gradually over 2021, and will be driven by persistent social distancing and by the level of mitigation measures taken by countries

• COVID vaccine breakthrough fuels broad equity rally (Europe’s Stoxx 600 closed up 4 per cent, its best day since May)

Key takeaways from the overall COVID-19 impacton major EU countries

-14 -12 -10 -8 -6 -4 -2 0 2 4 6

Belgium

Cyprus

Czech Republic

France

Germany

Greece

Italy

Netherlands

Portugal

Spain

United Kingdom

Romania

Poland

Real GDP growth (Annual percent change)

2020 2019

-14

-12

-10

-8

-6

-4

-2

0

GDP growth rate in main EU countries vs overall euro area level

2020 Euro area

Source: IMF World Economic Outlook

© 2020. For information, contact Deloitte Central Europe 6

The downturn triggered by the COVID-19 pandemic has been very different from past recessions

• In comparison with the global financial crisis, the Covid-19 crisis affected the various industry groups in a much more drastic and severe way: within only two months, between February and April 2020, the index for total industrial production dropped by 28 points

• Between January 2008 and December 2008, the index for the total production of services in the EU-27 dropped by 4.7 index points, compared with a drop of 20.4 points from February to June 2020

• In the current crisis, the public health response needed to slow transmission, together with behavioral changes, has meant that service sectors reliant on face-to-face interactions—particularly wholesale and retail trade, hospitality, and arts and entertainment—have seen larger contractions than manufacturing

Services turnover growth rates

TotalTransportation &

storageAccomodation &

foodInformation &

communicationProfessional

servicesAdministration

support

Q1 Q2 Q1 Q2 Q1 Q2 Q1 Q2 Q1 Q2 Q1 Q2

EU-27 -3.8 -16.5 -3.5 -18.1 -17.1 -55.4 -0.5 -3.1 -0.5 -10.5 -6.1 -26.3

Belgium -4.3 -8.8 -4.9 -12.5 -18.4 -43.6 -2.9 -3.4 0.2 -6.9 -3.8 -14.3

Czech Republic -4.5 -16.0 -1.4 -18.7 -12.9 -54.3 0.9 -2.3 -1.3 -6.8 -6.7 -32.3

Germany -1.7 -15.7 -0.7 -14.4 -14.1 -54.3 -2.7 -4.2 2.0 -8.8 -7.1 -29.0

Greece : : : : -14.0 : : : : : : :

Spain -7.3 -34.8 -5.7 -32.2 -18.7 -78.2 -3.9 -12.7 -4.0 -23.3 -8.1 -44.0

France -5.8 -17.8 -6.5 -19.6 -16.1 -56.9 -0.9 -5.2 -3.4 -7.7 -6.9 -20.3

Italy : : -4.4 -27.8 -24.0 -62.6 -1.1 -6.7 -0.4 -23.2 -3.3 -30.7

Cyprus -8.0 -16.1 -5.7 -10.9 -32.9 -22.3 -6.9 -5.7 -1.3 -7.7 -7.0 -28.8

Netherlands -4.4 -14.1 -1.5 -20.0 -19.9 -38.0 -0.8 -2.5 2.5 -10.9 -2.9 -29.5

Portugal -6.0 : -5.0 -40.7 -16.4 -66.4 1.5 -5.9 0.0 -21.4 -0.4 -39.5

United Kingdom -8.2 -27.9 -12.0 -40.2 -25.3 -61.8 -2.6 -6.5 -2.4 -10.3 -4.9 -23.6

© 2020. For information, contact Deloitte Central Europe 7Source: IMF World Economic Outlook

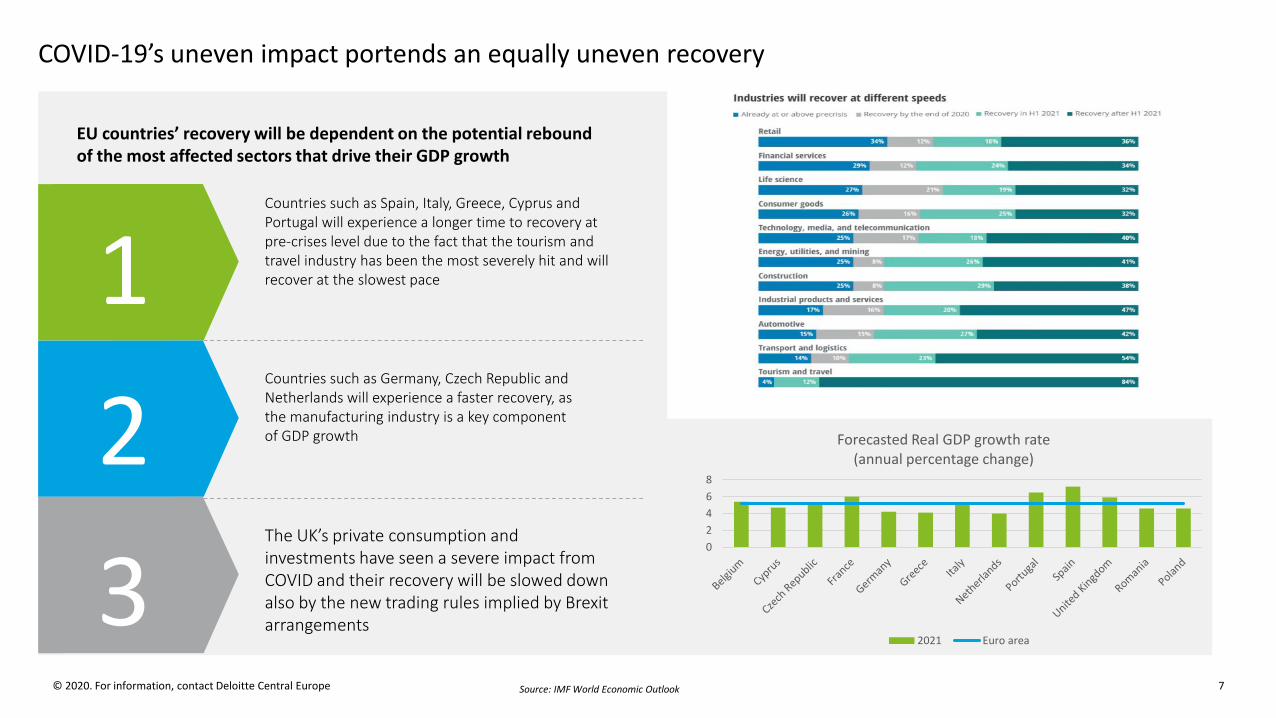

Countries such as Spain, Italy, Greece, Cyprus and Portugal will experience a longer time to recovery at pre-crises level due to the fact that the tourism and travel industry has been the most severely hit and will recover at the slowest pace

Countries such as Germany, Czech Republic and Netherlands will experience a faster recovery, as the manufacturing industry is a key component of GDP growth

The UK’s private consumption and investments have seen a severe impact from COVID and their recovery will be slowed down also by the new trading rules implied by Brexitarrangements

1

2

3

EU countries’ recovery will be dependent on the potential rebound of the most affected sectors that drive their GDP growth

0

2

4

6

8

Forecasted Real GDP growth rate (annual percentage change)

2021 Euro area

COVID-19’s uneven impact portends an equally uneven recovery

© 2020. For information, contact Deloitte Central Europe 8

EBA passed the message that moratoria will not be extendedNBR has under strict attention the moratoria and implications from postponement of payments and urged banks to present the timely assessment of debtors and provision recognition

06

05

04

03

02

01

COVID-19 IFRS 9 impact

Modification vs. derecognition

Disclosures

Credit Risk parameters(PD, LGD, EAD)

Scenario analysis

Staging criteria

Business and operations

• On 21st of September, EBA phased out the GL on Moratoria. The GL will continue to apply to all payment holidays granted under eligible payment moratoria prior to 30 September 2020. In Romania, Private moratoria is applicable until 30 Sep

• There are banks that already have clients that reached deadline on public moratoria and requested private moratoria

• EBA statement on the application of prudential framework regarding Default, Forbearance and IFRS 9 in light of COVID-19, 25 March 2020

• ECB letter IFRS 9 in the context of the coronavirus pandemic, 1 April 2020

• European Commission Spring 2020 Economic Forecast (base scenario, per country)

• ECB Alternative scenarios for the impact of the COVID-19 pandemic on economic activity in the euro area

Latest developments

Key regulatory instructions

Updated macroeconomic forecasts

© 2020. For information, contact Deloitte Central Europe 9

IASB, ECB, EBA passed clear message on timely recognition of impairment

The use of judgement is needed to correct assumptions which are no longer valid

The hypothesis needs to be frequently revisited as new information becomes available

Reasoning of the assumptions used need to be thoroughly documented

“ IFRS 9 requires the application of judgement and both requires and allows entities to adjust their approach to determining ECLs in different circumstances. Entities should not continue to apply their existing ECL methodology mechanically. […]Both the assessment of SICRs and the measurement of ECLs are required to be based on reasonable and supportable information that is available to an entity without undue cost or effort.”— IASB, IFRS 9 and covid-19, 27 March 2020

“The EBA is of the view that the public and private moratoria, as a response to COVID-19 epidemic to the extent they are not borrower specific but rather addressed to broad ranges of product classes or customers, do not have to be automatically classified as forbearance measures, as for IFRS9 and the definition of default. However, this does not remove the obligations for credit institutions to assess the credit quality of the exposures benefiting from these measures and identify any situation of unlikeness to pay of the borrowers accordingly.”— EBA, Statement regarding Default, Forbearance and IFRS9 in light of COVID19 measures, 25 March 2020

“It is likely to be difficult at this time to incorporate the specific effects of covid-19 and government support measures on a reasonable and supportable basis. However, changes in economic conditions should be reflected in macroeconomic scenarios applied by entities and in their weightings. If the effects of covid-19 cannot be reflected in models, post-model overlays or adjustments will need to be considered.— IASB, IFRS 9 and covid-19, 27 March 2020

© 2020. For information, contact Deloitte Central Europe 10

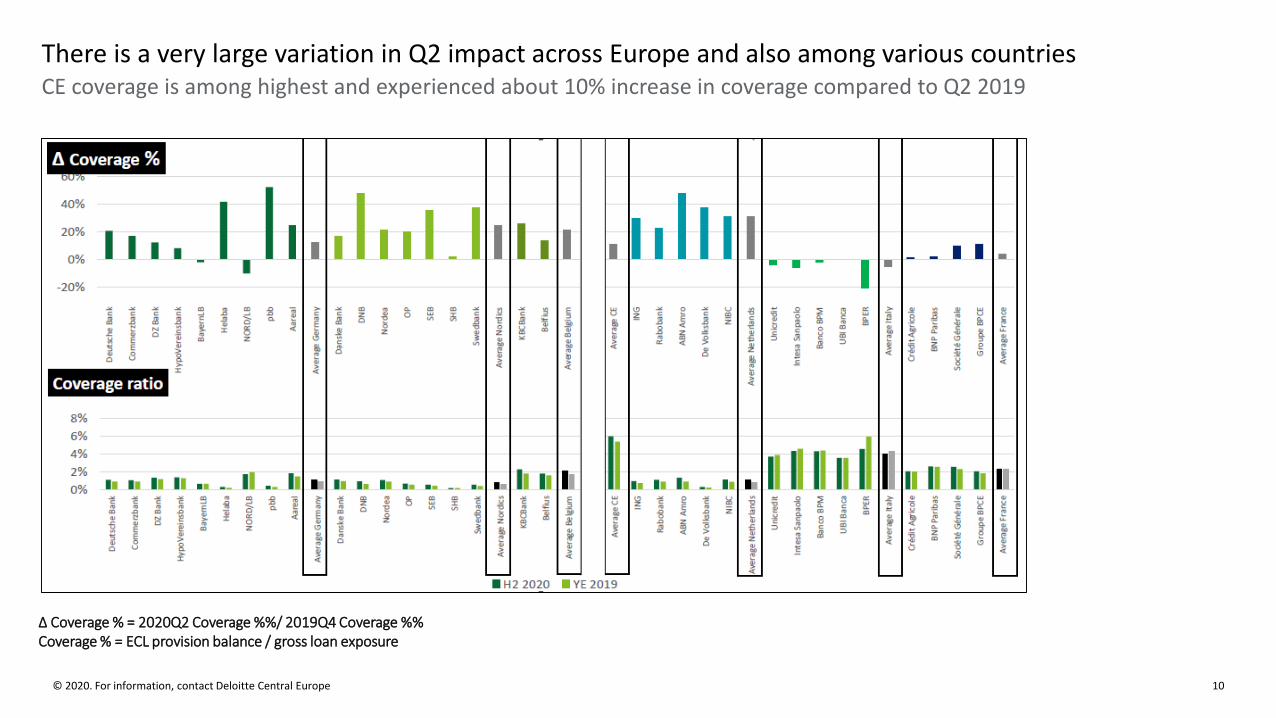

There is a very large variation in Q2 impact across Europe and also among various countriesCE coverage is among highest and experienced about 10% increase in coverage compared to Q2 2019

Δ Coverage % = 2020Q2 Coverage %%/ 2019Q4 Coverage %% Coverage % = ECL provision balance / gross loan exposure

© 2020. For information, contact Deloitte Central Europe 11

Quantitative impacts : 30.09.20Change in the cost of risk - in absolute terms

Cost of risk allocation for the first nine months of 2020 (in €M)

11

(1) Arithmetic average without taking into account balance sheet sizes or other weighting elements

-B

alan

ce s

he

etsi

ze +

3,203

2,341

1,757

2,107

1,278

1,367

723

3,383

767

769

4,118

6,491

2,734

4,789

2,617

2,074

1,540

2,938

3,430

1,631

BNPP

HSBC

GCA

Barclays

SG

BPCE

DeutscheBank

Unicredit

NatWestGroup

StandardChartered

Y-e 2019 9M2020

FX Rate : BdF average monthly exchange rate (November 2020)

FY2019 average: €1.7bn(1) Average 9M 2020: €3.2bn(1)

1,28

Cost of risk 9M 2020 as a coefficient of the total cost of risk 2019

2,12

4,5

0,86

2,12

1,5

2

2,77

1,55

2,27

2,1On average, the cost of risk over the first nine months of

2020 is already almost double that recorded for the

whole of 2019.

© 2020. For information, contact Deloitte Central Europe 12

Quantitative impacts : 30.09.20Change in the cost of risk - in absolute terms

Cost of risk allocation for the first nine months of 2020 (€M) : details of allocations by quarter

12

12

-B

alan

ce s

he

etsi

ze +

1,426

2,570

930

2,331

820

504

506

1,261

884

812

1,447

3,254

1,208

1,789

1,279

981

761

937

2,266

519

1245

667

596

670

518

589

273

741

280

300

BNPP

HSBC

GCA

Barclays

SG

BPCE

Deutsche Bank

Unicredit

NatWest Group

Standard Chartered

Q1 2020 Q2 2020 Q3 2020

FX Rate : average monthly exchange rate BdF (November 2020)

Average allocation(1) per quarter

Q1

1,2 Md€

Q2

1,44 Md€

Q3

0,6 Md€

+ 20%

- 60%

(1) Arithmetic average without taking into account balance sheet sizes or other weighting elements

© 2020. For information, contact Deloitte Central Europe 13

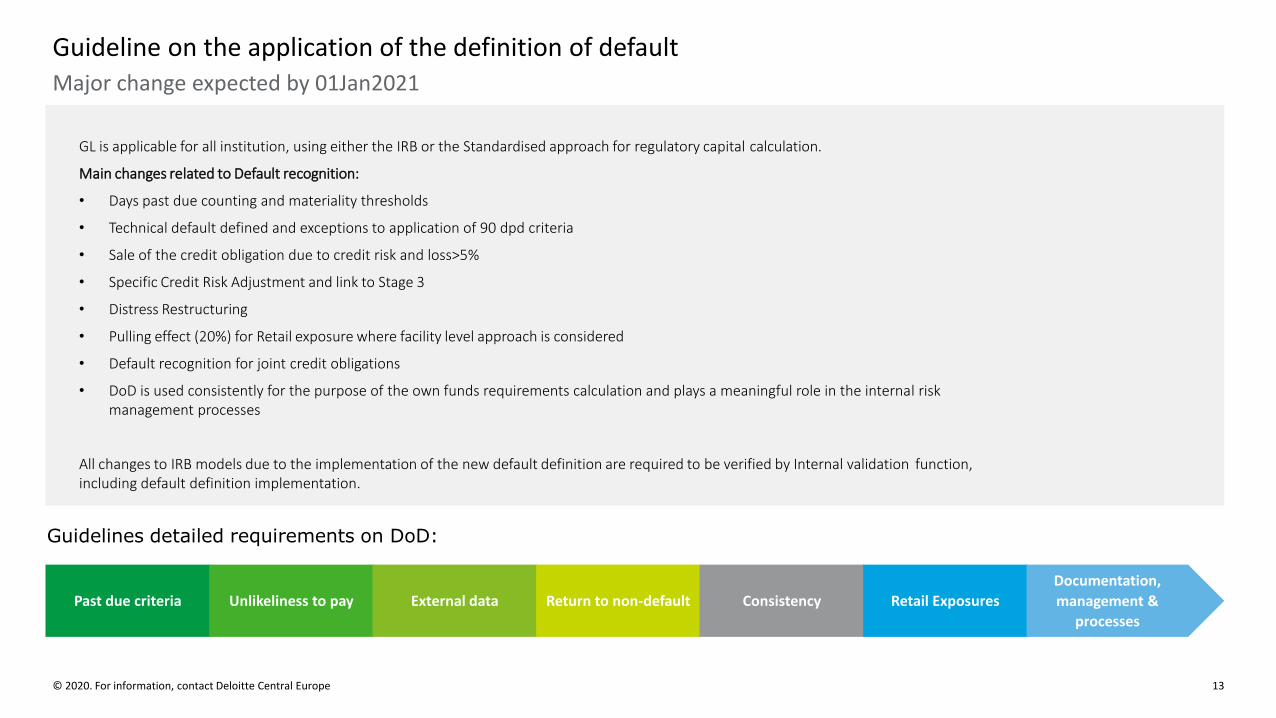

Guideline on the application of the definition of defaultMajor change expected by 01Jan2021

GL is applicable for all institution, using either the IRB or the Standardised approach for regulatory capital calculation.

Main changes related to Default recognition:

• Days past due counting and materiality thresholds

• Technical default defined and exceptions to application of 90 dpd criteria

• Sale of the credit obligation due to credit risk and loss>5%

• Specific Credit Risk Adjustment and link to Stage 3

• Distress Restructuring

• Pulling effect (20%) for Retail exposure where facility level approach is considered

• Default recognition for joint credit obligations

• DoD is used consistently for the purpose of the own funds requirements calculation and plays a meaningful role in the internal risk management processes

All changes to IRB models due to the implementation of the new default definition are required to be verified by Internal validation function, including default definition implementation.

Past due criteria Unlikeliness to pay External data Return to non-default Consistency Retail Exposures

Documentation,

management &

processes

Guidelines detailed requirements on DoD:

© 2020. For information, contact Deloitte Central Europe 14

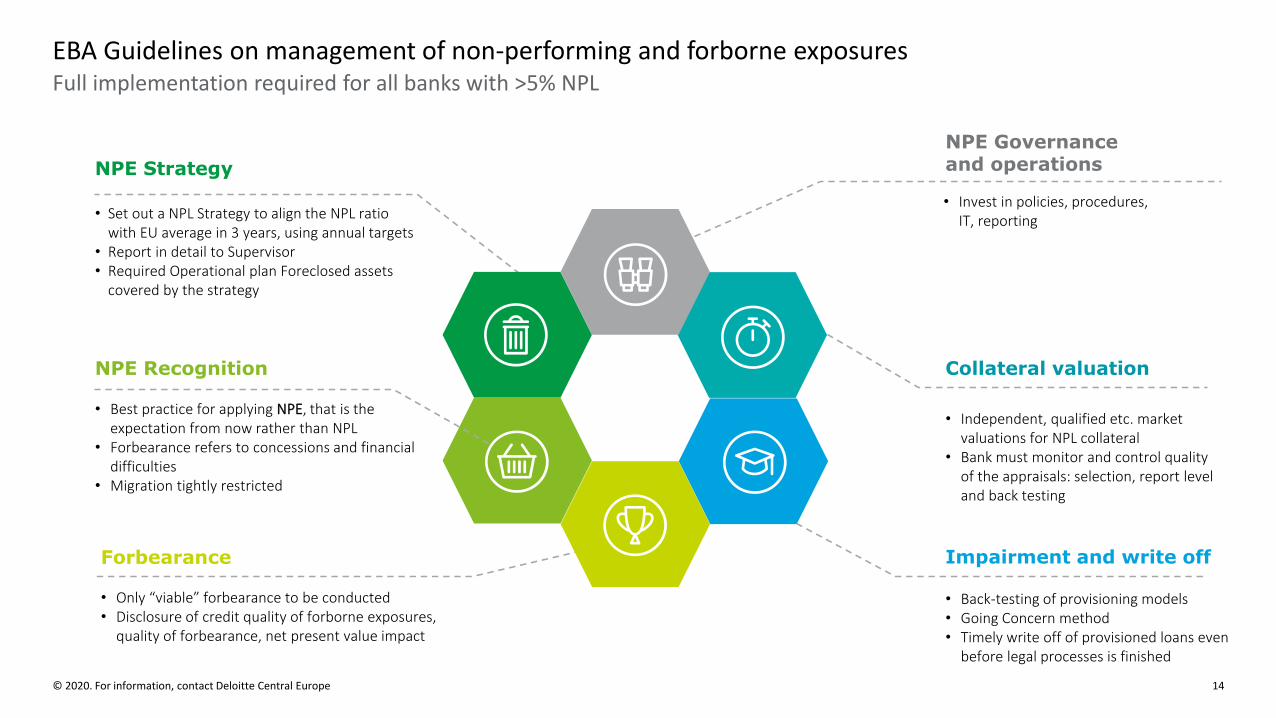

• Best practice for applying NPE, that is the expectation from now rather than NPL

• Forbearance refers to concessions and financial difficulties

• Migration tightly restricted

Impairment and write off

NPE Recognition

NPE Strategy

Collateral valuation

NPE Governance and operations

Forbearance

• Only “viable” forbearance to be conducted• Disclosure of credit quality of forborne exposures,

quality of forbearance, net present value impact

• Independent, qualified etc. market valuations for NPL collateral

• Bank must monitor and control quality of the appraisals: selection, report level and back testing

• Back-testing of provisioning models• Going Concern method• Timely write off of provisioned loans even

before legal processes is finished

• Set out a NPL Strategy to align the NPL ratio with EU average in 3 years, using annual targets

• Report in detail to Supervisor • Required Operational plan Foreclosed assets

covered by the strategy

• Invest in policies, procedures, IT, reporting

Full implementation required for all banks with >5% NPL

EBA Guidelines on management of non-performing and forborne exposures

© 2020. For information, contact Deloitte Central Europe 15

EBA GL (29 May 2020) on Loan Origination and MonitoringMonitoring framework was enhanced for a timely detection of increased credit risk

Stress testingTogether with simple sensitivity analyses, based on internal and external information

EWIsIn combination with an adequate escalation process

Watch listCredit exposures and borrowers with increased risk, including those identified though the monitoring of EWI

As part of their monitoring framework, institutions should develop, maintain and regularly evaluate relevant quantitative and qualitative EWIs that are supported by an appropriate IT and data infrastructure that would allow the timely detection of increased credit risk in their portfolio

Granular framework to identify associated credit risk with the borrower, market risk, country risk, impairments, write-offs, etc. via key risk indicators;

Strong link to the overall IT and data infrastructure, and

information collected at the point of origination;

Feedback loop to inform the setting/review of credit risk appetite, policies and limits.

Institutions should have a robust and effective monitoring framework, supported by an adequate data infrastructure, to ensure that information regarding their credit risk exposures, borrowers and collateral is relevant and up to date, and that the external reporting is reliable,

complete and up to date.

© 2020. For information, contact Deloitte Central Europe 16

Statutory backstop - Applicable for NPE exposures

NPE Provision coverage expectations

Number of years as NPE

UnsecuredSecured other than

immovable propertySecured immovable

propertySecured

Pillar 1/Pillar2 Addendum

Pillar2 StockPillar 1/Pillar2

AddendumPillar 1/Pillar2

AddendumPillar2 Stock

>1 0% 0% 0% 0% 0%

>2 35% 100% 0% 0% 0%

>3 100% 100% 25% 25% 40%

>4 100% 100% 35% 35% 55%

>5 100% 100% 55% 55% 70%

>6 100% 100% 80% 70% 85%

>7 100% 100% 100% 80% 100%

>8 100% 100% 100% 85% 100%

>9 100% 100% 100% 100% 100%

Pillar 1 Backstop:

In case the amounts set aside by a bank were below the applicable minimum level, the difference will be deducted from its own funds.

Legally, the backstop is a minimum requirement (i.e. "Pillar 1") directly applicable to all banks that are subject to the Capital Requirements Regulation.This established prudential treatment under Pillar 1 for NPEs arising from loans originated from 26 April 2019 onwards. These Pillar 1 rules are legally binding and apply to all banks established in the EU.

Pillar 2 Addendum/Stock of NPE:

From end-2020 onwards, JSTs will discuss with banks as part of the supervisory dialogue the supervisory coverage expectations, The outcome of the supervisory dialogue will be taken into account in upcoming SREP cycles, starting with SREP 2021, as part of the normal supervisory engagement.

IFRS9 in COVID : Staging, provisioning and the end of the moratoria

IFRS 9Deloitte Central Europe 18

IFRS9 in COVID: Staging, provisioning and the end of the moratoria

Dispersion in impairmentsMajor observations based on Q2/Q3 2020 results

Uncertainties in forecasts01

Structural breaks02

Scenario frameworks03

Stage transfer definitions04

Lifetime vector constructions05

Bow wave ahead?06

Model inputs such as macroeconomic outlooks are uncertain

Assumptions need to be reconsidered based on the new normal

Uncertainty in scenario definitions and scenario weights

Various different approaches in the market react differently

Assumptions about timing and size of a potential bow wave have their impact

Model assumptions in lifetime estimations influence the results

Model Implications IFRS 9 and IRB: The time has come to redevelop or recalibrate our models?

IFRS 9Deloitte Central Europe 20

Model Implications IFRS 9 and IRB: The time has come to redevelop or recalibrate our models?

Current issuesMajor aspects under consideration

Identify new risk factors that may need to be included in the models

Risk factorsReconsider customers business models under the new normal

Customers business models

Analyse trends in manual overridesManual Overrides

Start collect new types of data nowData collections

Acting on measured risk – how are banks managing the risk they identify?

22

How are banks responding to the risks they identify?

Acting on the risk measured

© 2020 Deloitte Hungary

Fight or Flight

Restructuring programmes identifying and targeting vulnerable borrowers

Refinancingdemand following rate cuts and government-supported products

New lending New opportunities under the changed competitive landscape

Change in pricing components to combat NIM squeeze

Adapting operationsMoving staff between channels and activities, engaging 3rd

parties and use of digital & automated decisioning where possible

Temporary freeze in lending and credit lines

at the onset of the 1st lockdowns

Overall slowdownin 2020 lending growth (but picking up in 2021 to

stimulate economic recovery?)

Targeted reduction in lending growth in some high risk business lines or those affected by

government/national bank pricing caps

Tightened credit standards and/or capacity constraints

slowing down credit assessmentwhile ‘caring for the customer’ prevails

NPL disposalsIs there a new wave coming?

NPL prevention and management

© 2020. For information, contact Deloitte Central Europe 24

NPL prevention and managementOn the road to client oriented NPL framework…

Identify new risk factors that may need to be included in the models

Blind" risk analysis devices

Banks are expected to control their NPL level AND play their role on the economic equation

Strong expectation from the regulator

Atypical macroeconomic contextLack of observable dataUnusual mechanism of risk propagation

Unique and never seen before situation

A NPL wall to come ?How fast will be the recovery step ?

Huge uncertainty of future development

Rely on real data and progressively build assumptions and appropriate segmentation

Need to come back to observations and understanding of client’s context

Agile device, easy to deploy, with limited impact on existing IT and adjustable to future developments

Adopt a dynamic and adjustable NPL management framework

Implications for Audit – What has changed as a result of COVID-19?

© 2020 Deloitte Central Europe 26

What has changed as a result of COVID-19?

Audit implications

Options

01Model risk

02Model adjustments

03Economic scenarios

04SICR

Model validation and recalibration dilemmas under COVID-19

Quantitative vs. qualitative analysis and documentation of model adjustments

Tactical solutions and operative constraints for running sensitivity analyses

Forward-looking indicators under COVID, treatment of moratoria and restructurings

Audit focus areas from FY19… …are back with a twist in FY20

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities (collectively, the “Deloitte organization”). DTTL (also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and independent entities, which cannot obligate or bind each other in respect of third parties. DTTL and each DTTL member firm and related entity is liable only for its own acts and omissions, and not those of each other. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte Central Europe is a regional organization of entities organized under the umbrella of Deloitte Central Europe Holdings Limited, the member firm in Central Europe of Deloitte Touche Tohmatsu Limited. Services are provided by the subsidiaries and affiliates of, and firms associated with Deloitte Central Europe Holdings Limited, which are separate and independent legal entities. The subsidiaries and affiliates of, and firms associated with Deloitte Central Europe Holdings Limited are among the region’s leading professional services firms, providing services through nearly 7,000 people in 44 offices in 18 countries.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited („DTTL“), its global network of member firms or their related entities (collectively, the “Deloitte organization”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser.

No representations, warranties or undertakings (express or implied) are given as to the accuracy or completeness of the information in this communication, and none of DTTL, its member firms, related entities, employees or agents shall be liable or responsible for any loss or damage whatsoever arising directly or indirectly in connection with any person relying on this communication. DTTL and each of its member firms, and their related entities, are legally separate and independent entities.

© 2020. For information, contact Deloitte Central Europe

Risk & Regulatory Academy