risk minimizing portfolio optimization and hedging with conditional value-at-risk jing li mingxin xu...

Post on 22-Dec-2015

216 views

TRANSCRIPT

Risk Minimizing Portfolio Optimization and Hedging with

Conditional Value-at-Risk

Jing Li Mingxin XuDepartment of Mathematics and StatisticsUniversity of North Carolina at Charlotte

[email protected] [email protected]

Presentation at the 3rd Western Conference in Mathematical Finance

Santa Barbara, Nov. 13th~15th, 2009

Outline

• Problem• Motivation & Literature• Solution in complete market• Application to BS model• Conclusion

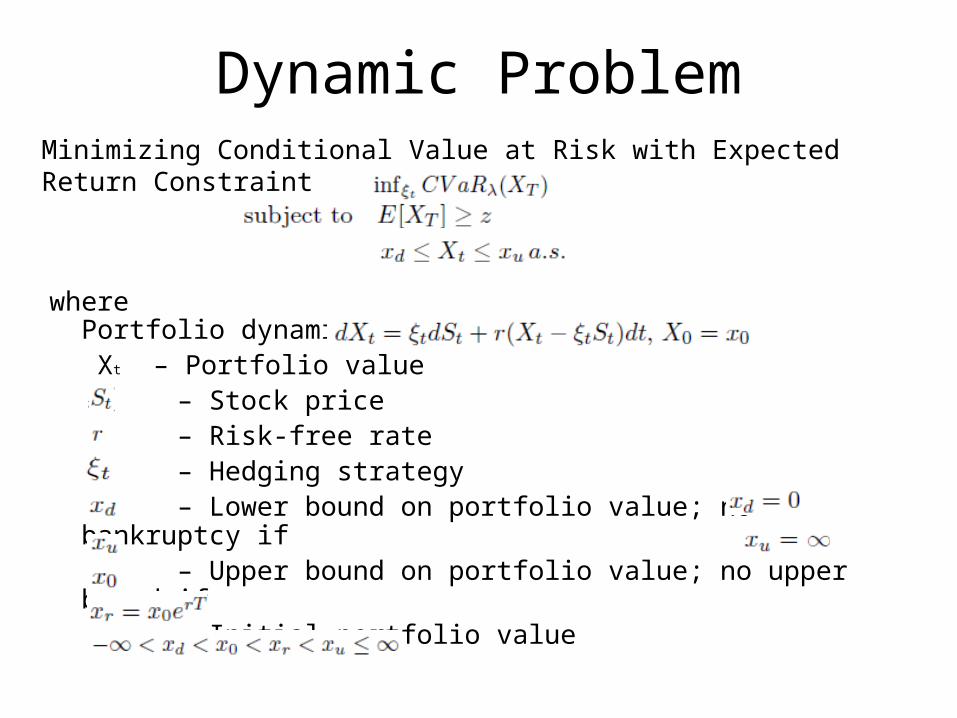

Dynamic ProblemMinimizing Conditional Value at Risk with Expected Return Constraint

wherePortfolio dynamics: Xt – Portfolio value – Stock price – Risk-free rate – Hedging strategy – Lower bound on portfolio value; no bankruptcy if – Upper bound on portfolio value; no upper bound if – Initial portfolio value

Background & MotivationEfficient Frontier and Capital Allocation Line (CAL):

• Standard deviation (variance) as risk measure • Static (single step) optimization

Risk Measures• Variance - First used by Markovitz in the classic portfolio

optimization framework (1952)

• VaR(Value-at-Risk) - The industrial standard for risk management, used by BASEL II for capital reserve calculation

• CVaR(Conditional Value-at-Risk) - A special case of Coherent Risk Measures, first proposed by Artzner, Delbaen, Eber, Heath (1997)

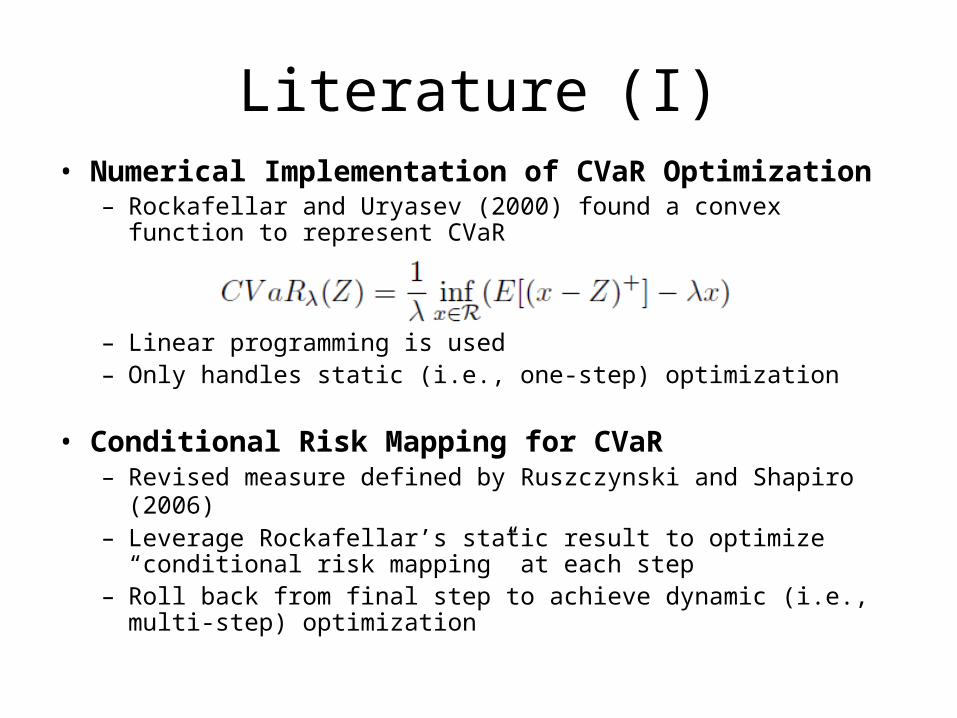

Literature (I)• Numerical Implementation of CVaR Optimization

– Rockafellar and Uryasev (2000) found a convex function to represent CVaR

– Linear programming is used– Only handles static (i.e., one-step) optimization

• Conditional Risk Mapping for CVaR– Revised measure defined by Ruszczynski and Shapiro (2006) – Leverage Rockafellar’s static result to optimize “conditional

risk mapping” at each step– Roll back from final step to achieve dynamic (i.e., multi-step)

optimization

Literature (II)• Portfolio Selection with Bankruptcy Prohibition

– Continuous-time portfolio selection solved by Zhou & Li (2000)– Continuous-time portfolio selection with bankruptcy prohibition

solved by Bielecki et al. (2005)

• Utility maximization with CVaR constraint. (Gandy, 2005; Gabih et al., 2009)– Reverse problem of CVaR minimization with utility constraint;– Impose strict convexity on utility functions, so condition on

E[X] is not a special case of E[u(X)] by taking u(X)=X.

• Risk-Neutral (Martingale) Approach to Dynamic Portfolio Optimization by Pliska (1982)– Avoids dynamic programming by using risk-neutral measure– Decompose optimization problem into 2 subproblems: use

convex optimization theory to find the optimal terminal wealth; use martingale representation theory to find trading strategy.

The Idea• Martingale approach with complete market assumption to convert the

dynamic problem into a static one:

• Convex representation of CVaR to decompose the above problem into a two step procedure:

Step 1: Minimizing Expected Shortfall

Step 2: Minimizing CVaR

Convex Function

Solution (I)• Problem without return constraint:

• Solution to Step 1: Shortfall problem– Define:– Two-Set Configuration .– is computed by capital constraint for every given level of .

• Solution to Step 2: CVaR problem – Inherits 2-set configuration from Step 1;– Need to decide optimal level for ( , ).

Solution (II)

• Solution to Step 2: CVaR problem (cont.)– “star-system” : optimal level found by

• Capital constraint:

• 1st order Euler condition .– : expected return achieved by optimal 2-set configuration.– “bar-system” :

• is at its upper bound,

• satisfies capital constraint .

– : expected return achieved by “bar-system” • Highest expected return achievable by any X that satisfies

capital constraint.

Solution (III)• Problem with return constrain:

• Solution to Step 1: Shortfall problem– Define:

– Three-Set Configuration – , are computed by capital and return constraints for every given

level of .

• Solution to Step 2: CVaR problem– Inherits 3-set configuration from Step 1;– Need to find optimal level for ( , , ); – “double-star-system” : optimal level found by

• Capital constraint:• Return constraint:

• 1st order Euler condition:

Solution (IV)• Solution:

– If , then • When , the optimal is

• When , the optimal does not exist, but the infimum of CVaR is .

– Otherwise,• If and , then “bar-system” is optimal:

• If and , then “star-system” is optimal:.

• If and , then “double-star-system” is optimal:

• If and , then optimal does not exist, but the

infimum of CVaR is

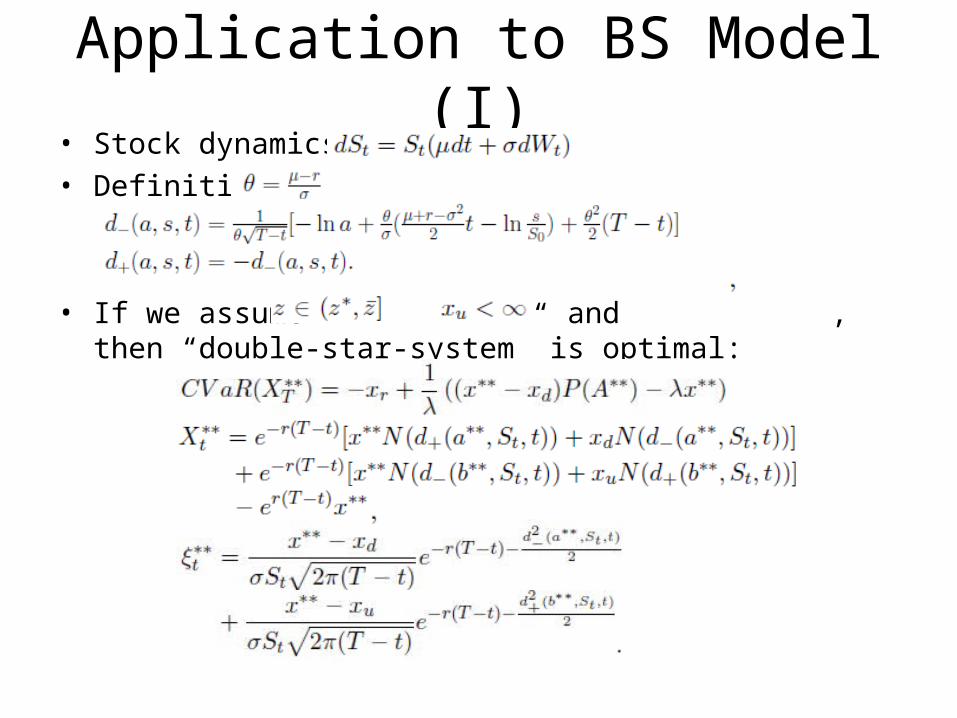

Application to BS Model (I)• Stock dynamics:

• Definition:

• If we assume and , then “double-star-system” is optimal:

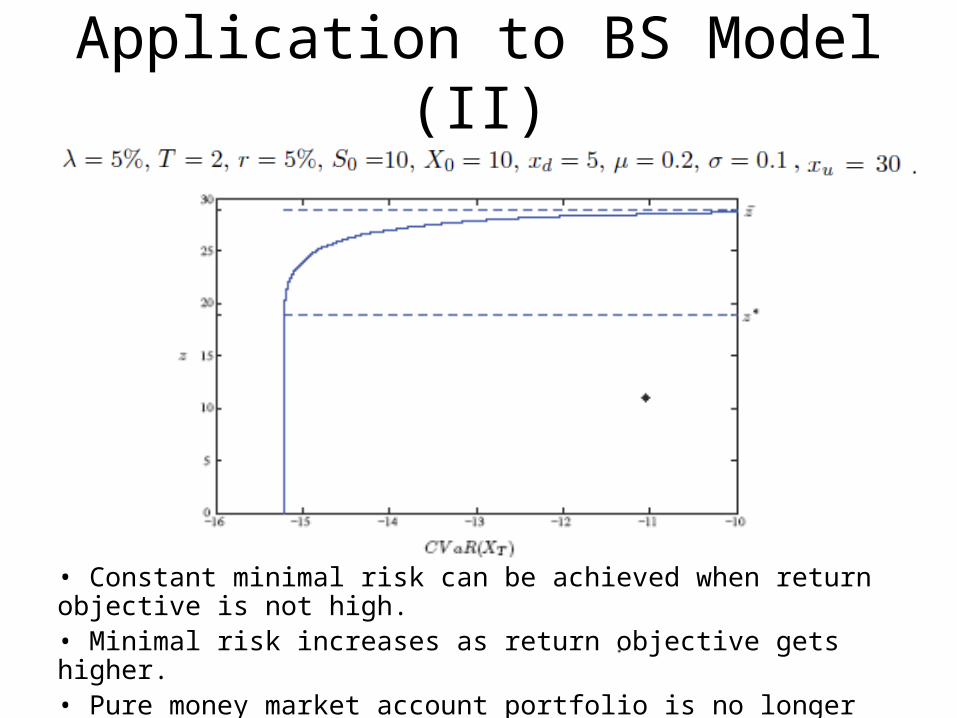

Application to BS Model (II)

• Constant minimal risk can be achieved when return objective is not high.• Minimal risk increases as return objective gets higher.• Pure money market account portfolio is no longer efficient.

Conclusion & Future Work

• Found “closed” form solution to dynamic CVaR minimization problem and the related shortfall minimization problem in complete market.

• Applications to BS model include formula of hedging strategy and mean CVaR efficient frontier.

• Like to see extension to incomplete market.

The End

Questions?

Thank you!