risk seminar session 1 – introduction to … seminar session 1 – introduction to risk management...

TRANSCRIPT

© Oliver Wyman | LON-FSP03201-034

RISK SEMINARSESSION 1 – INTRODUCTION TO RISK MANAGEMENTNOVEMBER 2012

Stockholm, KTH

Contents

1. Introduction to risk

2. Risk Appetite

Case study: Risk Appetite engagement

3. Introduction to Economic Capital, risk types and risk measurement

Economic Capital – overview

Risk types – overview

Credit risk

Market risk

Operational risk

Introduction to riskSection 1

33© Oliver Wyman | LON-FSP03201-034

A typical bank’s balance sheet expose the institution to a number of risks (Illustrative)

Time 1 ChangeAssetsCash & balances with CB 50,073 0.1%Treasury bills 50,000 0.0%Loans to credit institutions 70,000 0.0%Loans to the public 875,518 1.3%Shares 53 17.2%Interest bearing securities 100,054 0.0%Derivatives 133 8.9%Intangible assets 2,999 0.0%Property and equipment 1,436 0.0%Other assets 60,565 0.0%Total assets 1,210,831 1.0%

LiabilitiesDeposits by credit institutions 85,000 0.0%Deposits from the public 268,912 0.8%Debt securities in issue 756,176 1.1%Derivatives ‐ N/AOther liabilities 60,000 0.0%Subordinated liabilities 15,000 0.0%Total liabilities 1,185,088 0.9%

EquityShare capital 23,000 0.0%Retained earnings 2,743 105.5%Total equity 25,743 5.8%Total liabilities and equity 1,210,831 1.0%

• Do I have enough liquid funds to sustain a closure of the funding market?

• Will my customers pay back the money they owe on time?

• How sensitive are my traded assets to market movements?

• What is the likelihood for a deposit run and how severe would it be?

• How frequently does my debt need refinancing and do I have the capacity?

• What is my re-pricing terms and what happens when IR changes?

• How likely is it that any of the above risks will deplete my equity? (See overleaf)

44© Oliver Wyman | LON-FSP03201-034

From a solvency perspective, a financial institution holds capital to protect against losses in a “worst-case” year

Assets

• Cash• Loans• Investment

securities

Liabilities

• Deposits• Borrowings• Shareholders’

equity

Available capital

Responsibility towards debt holders is “fixed” from a cash-flow perspective

• Buffer against asset value change

• Not stable: varies according to losses and retained earnings

Volatility in asset value

Economic capital indicates the amount of net financial resources required to

ensure solvency in the face of worst-case balance sheet losses

Asset value is susceptible to risk (e.g. credit losses, changes in market prices, fraud, etc.)

Typical bank balance sheet

55© Oliver Wyman | LON-FSP03201-034

The risks that a bank face are typically categorized into the following broad segments

Over and above the solvency related risks there are also a number of risks that threaten the liquidity of the institution

Major risk types relevant for Banks Description/examples

Credit Risk Will a counterparty pay back a loan (on time)?

Market Risk Will my assets lose value due to unfavourablemarket movements?

Interest Rate Risk Will my assets lose value due to unfavourableinterest rate movements?

Transfer Risk Will a foreign borrower be able to obtain the currency required to repay the debt?

Operational (Event) Risk Losses due to unforeseen events regarding people, process or system failures

Business Risk Fluctuation in consumer demand

Insurance Risk Uncertainty in number of claims and e.g. mortality assumptions

Risk appetiteSection 2

77© Oliver Wyman | LON-FSP03201-034

Risk Appetite serves as one of the most important mediums for coordinating risk-taking activities across a bank

Finance

RiskCorporate strategy

Where should we place our strategic bets?

Which risks arewe taking?

How much capital do we need?

How leveraged do we want to be?

How to optimise therisk-return trade-off?

How should we measure

value creation?

Where should we allocate

excess capital?

How should we allocate resources for

sustainable growth?

What are acceptable risks?

How volatile can results be?

• All businesses take risk to generate returns; but the types of risk taken, the absolute amounts to which the company is exposed, and how and where it is taken must be an input into strategy decisions, not a collateral by-product

• When the board and management discuss strategy, they make decisions about which risks the company will accept and take

• Risk appetite is defined as the amount of risk that the enterprise is willing to accept and risk tolerance as the degree of variance from risk appetite that the enterprise is willing to accept

8© Oliver Wyman | LON-FSP03201-034 8

Oliver Wyman supported a European bank in implementing a risk appetite framework to improve its long-term profitability

• The bank had strong risk management on transaction level, supported by a good risk culture. However, there was a need for a more integrated perspective with a focus on the portfolio view and interaction between different risk types

• Stakeholders, including regulators, debt-holders and shareholders were increasingly demanding that the Group Risk appetite was explicitly defined, monitored and actively managed

• Across the industry, financial institutions were moving towards a more structured approach to risk appetite

The overall aim of introducing the risk appetite framework was to improve the client’s risk management

and thereby long-term profitability

Case study: Risk Appetite engagement

99© Oliver Wyman | LON-FSP03201-034

The risk appetite implementation consisted of four stepsCase study: Risk Appetite engagement

Description

Identify key risk types to be managed1 Identify

appropriate metrics2 Calibration

of identified metrics3 Embed into

operational limitsin the business4

• The broad content of the risk appetite statement is outlined

• Main categories are articulated

• Detailed statements are defined in each main category

• A view on which statements to “manage by” and which to “report on” is taken (i.e. which statements are cascaded into limits and which are used as indicators of level of risk taking)

• Once statements have been identified the threshold needs to be defined (i.e. what constitutes an acceptable risk appetite)

• Analysis is based on external (peers) and internal data (current and historic values) as well as current limits and guidelines

• Where applicable, defined statements are cascaded to business units and regions to enable the business to manage based on the defined risk appetite

• Alignment of reporting will be performed as a result of this exercise

10© Oliver Wyman | LON-FSP03201-034 10

The risk appetite statements defined the outer boundaries to the client’s risk-taking activities

• The group level risk appetite consists of a number of statements on the acceptable level of risk taking covering the dimensions: Solvency, Earnings Volatility, Liquidity and Non-financial risks & reputation

• The risk appetite statements were approved by the Board of Directors and the actual risk profile in relation to each of the defined statements are regularly reported to the Risk Committee and the Board of Directors

• The statements collectively define the outer boundaries to the bank’s group-wide risk-taking activities and are translated into limits on lower organisation levels and embedded into key processes, such as strategic planning

Case study: Risk Appetite engagement

1111© Oliver Wyman | LON-FSP03201-034

Category Metric Status Comment

Credit risk Single customer concentration Green Summary of explanatory commentary

Industry concentration Amber Summary of explanatory commentary

Geographic concentration Green Summary of explanatory commentary

Expected loss Green Summary of explanatory commentary

Loan loss Green Summary of explanatory commentary

Probability of default Green Summary of explanatory commentary

Market risk Maximum reported market risk loss per quarter

Green Summary of explanatory commentary

Total economic loss from markets Red Summary of explanatory commentary

Operational risk Operational risk loss Green Summary of explanatory commentary

Reputational impact Green Summary of explanatory commentary

Solvency Tier 1 capital ratio Green Summary of explanatory commentary

Leverage ratio Green Summary of explanatory commentary

Target credit rating Green Summary of explanatory commentary

Liquidity risk Survival horizon Amber Summary of explanatory commentary

Compliance/ Non-negotiable risks

Regulatory requirements Green Summary of explanatory commentary

Internal policy and external regulatory breaches

Green Summary of explanatory commentary

Risk appetite dashboardExecutive management report

The statements consist of an overall risk appetite dashboard that enables further drill-down for additional detail

Risk dashboard

• Contains clear traffic light summary for all factors at the highest level

• Provides a clear overview and guides the reader to the key sections to focus on

• General descriptive comment for each category, focusing on recent developments

Statement reporting

• Visualises current status and development of each factor, and where relevant key drivers

• Comments are focused on explaining cause and impact of status and development

• Detailed drill down for individual drivers are available for all factors as appendix

Credit Risk (2/6) – Industry concentration

Industry concentration

Industry concentration movements

Top industry drill down

Industry Exposure EC EC% EC limit CommentReal estate management and investment

XX XX XX 20.7% Comment on development

Forest materials

XX XX XX XX Comment on development

Shipping and offshore

XX XX XX XX Comment on development

… … … …

Development of industries concentration risks– Comments on changes within considered/top industries

Comments on general structure of portfolio– E.g. Industries considered in analysis

Geographic and name-level concentrations within the largest industries

Comments on rating and economic capital limits

Comments on development efforts w.r.t. metric (as long as ongoing)

Comments

9,3% 9,9% 11,2%11,2% 9,4% 9,0%

0%

5%

10%

15%

20%

25%

2009Q4 2010Q1 2010Q2

Real estate Industry X

Real estate limit

Industry X limit

The following industry sectors should not individually be responsible for more than the stated percentage of total corporate credit risk economic capital:- Real estate management and investment : 12.0% (or up to 16% if fully explained by credit quality deterioration)

Action tracking

Previous follow-up actions agreed for metric Comments on new proposed actions

Case study: Risk Appetite engagement

1212© Oliver Wyman | LON-FSP03201-034

• Comments on the development of concentration risks– Analysis of the top 10, top 3 and top counterparties– Comments on changes within these counterparties

• General structure of portfolio– e.g. how many counterparties to consider in the

analysis

• Comments on geographic and industry concentrations within the largest single names

• Comments on rating and economic capital limits

• Comments on development efforts w.r.t. metric (as long as ongoing)

Customer concentration movements

Top single counterparties

Counterparties PDExposure (BN) Limit EC MM EC % Comment

Counterparty 1 1.22% 1,24 XX 71 0.81% Comment on development

Counterparty 2 0.88% 1.04 XX 63 0.71% Comment on development

Counterparty 3 0.03% 0.93 XX 43 0.53% Comment on development

Counterparty 4 1.14% 0.85 XX 41 0.51% Comment on development

… … … … …

The 25 largest corporate counterparties should not be responsible for more than 8% of corporate credit risk economic capital, and a single counterparty should not be responsible for more than 1% of corporate credit risk economic capital

• Previous follow-up actions agreed for metric

• Comments on new proposed actions

Top-25 limit

Top counterparty limit

Example report: Single customer concentrationCase study: Risk Appetite engagement

CommentsCustomer concentration

Action tracking

0,78% 0,92% 0,91% 0,78%

7,9% 7,4% 7,2% 7,1%

0%

2%

4%

6%

8%

10%

Q4 2010 Q1 2010 Q2 2010 Q3 2010

Top counterparty Top 25 counterparties

Introduction to Economic Capital, risk types and risk measurement

Section 3

1414© Oliver Wyman | LON-FSP03201-034

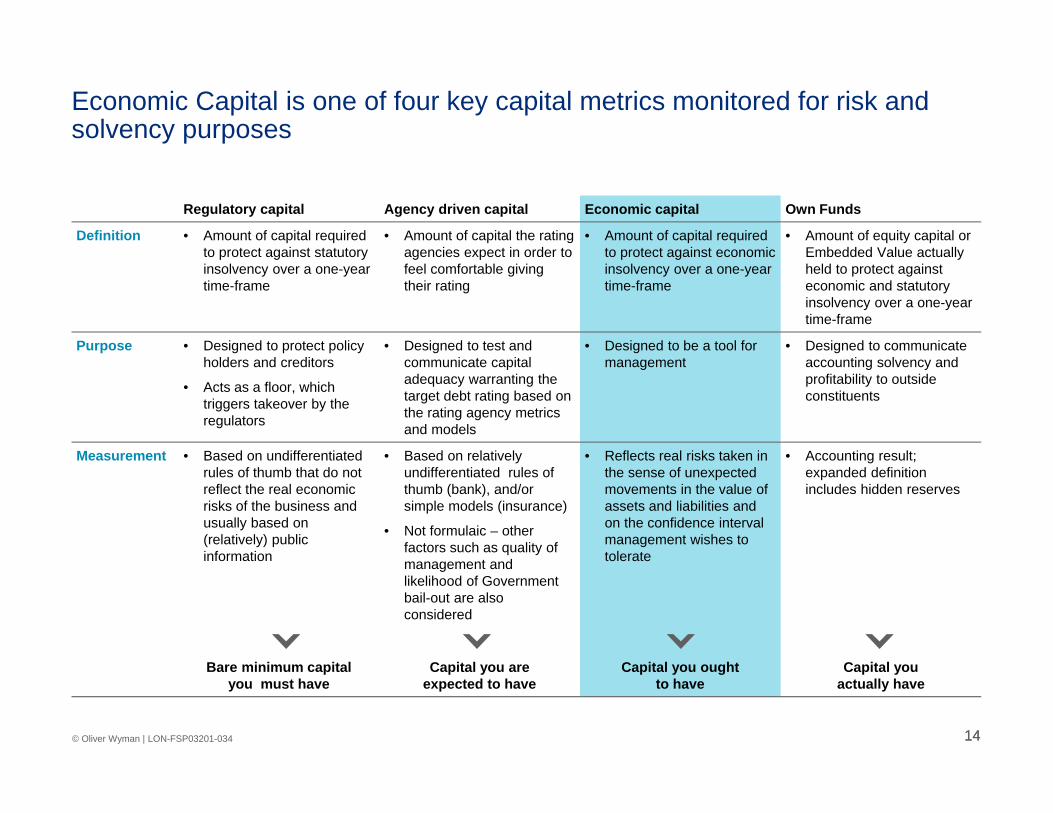

Economic Capital is one of four key capital metrics monitored for risk and solvency purposes

Regulatory capital Agency driven capital Economic capital Own Funds

Definition • Amount of capital required to protect against statutory insolvency over a one-year time-frame

• Amount of capital the rating agencies expect in order to feel comfortable giving their rating

• Amount of capital required to protect against economic insolvency over a one-year time-frame

• Amount of equity capital or Embedded Value actually held to protect against economic and statutory insolvency over a one-year time-frame

Purpose • Designed to protect policy holders and creditors

• Acts as a floor, which triggers takeover by the regulators

• Designed to test and communicate capital adequacy warranting the target debt rating based on the rating agency metrics and models

• Designed to be a tool for management

• Designed to communicate accounting solvency and profitability to outside constituents

Measurement • Based on undifferentiated rules of thumb that do not reflect the real economic risks of the business and usually based on (relatively) public information

• Based on relatively undifferentiated rules of thumb (bank), and/or simple models (insurance)

• Not formulaic – other factors such as quality of management and likelihood of Government bail-out are also considered

• Reflects real risks taken in the sense of unexpected movements in the value of assets and liabilities and on the confidence interval management wishes to tolerate

• Accounting result; expanded definition includes hidden reserves

Bare minimum capital you must have

Capital you are expected to have

Capital you oughtto have

Capital youactually have

1515© Oliver Wyman | LON-FSP03201-034

Economic Capital is based on the economic balance sheet, which considers assets and liabilities at economic value (i.e. fair or market value)

Expected

Required Economic Capital

Net assetvalue

Probability of outcome

Tail probability

AvailableEconomic

Capital

RequiredEconomic

Capital

Excess Capital

Economicvalue

of assets

Economic netasset value

Assetvolatility

Economicvalue

of liabilities

Liabilityvolatility

Economic balance sheet Distribution of economic net asset value

Available vs. required Economic Capital

• Economic value of assets includes all unrealised capital gains and excludes any amortisation, deferred acquisition costs, negative reserves, etc.

• Economic value of liabilities includes the guaranteed liabilities and value of options to policyholders for in-force business

Risk typesOverview

Section 3.1

1717© Oliver Wyman | LON-FSP03201-034

Volatility of economic earnings (including changes in balance sheet value)

Earnings volatility due to errors/omissions or changes in operating economics

Earnings volatility due to changes in market pricesor liquidity

Earnings volatility due to variation in credit losses

Economic capital

• Loans• Derivative

counterparties• Reinsurance

counterparties

• Equities• Bonds• Foreign Exchange• Real Estate• ALM risk• Liquidity risk

• Fraud• Unintentional

errors• Legal risk

• Changes in business volumes

• Changes in margins and costs

Financial institutions face three fundamental sources of risk for which they need to hold capital

Total economic risk

Credit riskIssuer/transfer/counterparty

Market riskTrading/ALM/interest rate

Operating riskBusiness/operational

1818© Oliver Wyman | LON-FSP03201-034

While different tools and methodologies are used to measure each risk…Lo

ss R

ate

Mean

Time

EL

Time

$

OperatingRisk

Capital

DM appreciation

USD appreciation

Jan 87 Jan 88 Jan 89 Jan 90 Jan 91 Jan 92 Jan 93

105104103102101100

9998979695

2 Standard deviations

Credit risk Market risk

Operating risk

OperatingRisk

Capital

1919© Oliver Wyman | LON-FSP03201-034

Prob

abili

ty

Unexpected lossesExpected losses

Manage causes Manage volatility/capitalise

…they are all based on modeling loss or value distributions

Economic capital

Economic capital is the “amount you will lose over a year with probability x%”

Illustrative loss distribution

2020© Oliver Wyman | LON-FSP03201-034

Standalone EC Diversified EC

For preciseness and ease of computation, Economic Capital is typically measured separately for each risk type…

Aggregation Engine

Inter-Risk Dependencies

…Credit Risk

ALM Risk

Market Risk

Market /ALM

Operational & Business

DiversificationBenefit

Credit

…and thereafter aggregated to a Bank-wide figure, taking into account diversification effects

OutputRisk AggregationStandalone Risk Measurement

Credit riskSection 3.2

2222© Oliver Wyman | LON-FSP03201-034

Credit Risk is expressed through the concepts of Expected Loss and Unexpected Loss

• Anticipated average annual loss rate• Foreseeable “cost” of doing business• Not “risk” as investors think of it, but rather charge

which affects anticipated yield• Equal to the mean (average) of losses over an

economic cycle

• Anticipated volatility of loss rate• Results in volatility of return over time• Unanticipated but inevitable• Requires a balance sheet cushion of “economic” capital• Defined as one standard deviation of losses

Cre

dit l

osse

s

Time (years)

EL

Expected Loss (EL)

Unexpected Loss (UL)UL

Frequency

Cre

dit l

osse

s

2323© Oliver Wyman | LON-FSP03201-034

Key risk parameters used to estimate Expected Loss and Unexpected Loss

Probability of default(PD)

Who are you lending to?

What is the % you expect to lose? Time to repayment? Expected exposure if

borrower defaults?

Loss Given Default(LGD)

Maturity (M)

Exposure at Default(EaD)

• Quantifies likelihood of borrower being unable to repay

• Rating models calibrated to long-term cycle averaged PD (central tendency)

• Quantifies the % of the exposure that is lost in the case of default, including economic costs e.g. legal costs

• Generally depends on the collateral and product type

• Quantifies the exposure at risk in the case of default

• Calculation depends upon product type

• Level of “connectedness” of individual loans in the portfolio

• Asset correlation, PD and default correlation related via Merton model

Asset/default correlation

Correlation

Credit risk

Borrower characteristics

Facility characteristics

Portfolio characteristics

2424© Oliver Wyman | LON-FSP03201-034

The economic capital calculation centers around estimating uncertainty around portfolio EL, and may be calculated via two different methods

Probability of default (PD)

Exposure at default (EaD)

Loss given default (LGD)

Expected loss (EL)

x

x

Stochastic simulation model

Closed-form aggregation model

Calculate unexpected loss (UL)

Calculate theoretical loss distribution

Run stochastic simulations

Generate simulated loss distribution

Economic capital

Economic capital calculation overview

Primary focus of economic capital build-out

2525© Oliver Wyman | LON-FSP03201-034

There are pros and cons to using a simulation vs. closed-form aggregation model for credit risk

Method Closed-form aggregation Simulation

Description Use a customised statistical approach; analytical formulae

Do a bottom-up approach covering multiple risk drivers to describe credit risk

Risk drivers

Requires at minimum: PD, LGD, EaD, associated volatilities, correlations, capital multiplier

Can be applied at loan-level or segment-level

Requires at minimum: drivers of PD, LGD, EaD, loan characteristics (maturity, amortization schedules)

Pros • Straightforward• Easily manipulate-able, can be spreadsheet-based• Easily customised

• Very powerful in describing full credit risk distribution

• Bottom-up approach can incorporate loan-level borrower behavior and product characteristics (e.g. optionality)

Cons • Accuracy of ecap estimate is highly linked to accuracy of correlations

• Does not capture borrower or management optionality well

• Complex• Requires lots of data• Difficult to parameterise especially for non-

public companies

Market riskSection 3.3

2727© Oliver Wyman | LON-FSP03201-034

Market risks affect both the asset and the liability side of the balance sheet

EquityInterest rate

Real estate

Foreign exchange

Market risks

Assets

Liabilities

Net asset value

• Movements in value of equity, fixed income and real estate investments

• Movements in value of derivatives held for hedging purposes

• Change in market value of liabilities due to

– Changes in the value of embedded options and guarantees

– Changes in market-driven policyholder behaviour

Calculating Economic Capital for market risk requires assessing asset

and liability values in stress scenarios

2828© Oliver Wyman | LON-FSP03201-034

Market Risk

Market Risk arises from two sources

• Measures market risks for liquid, actively traded positions across many markets

• Incorporates correlations across markets (e.g. interest rates, foreign exchange, commodities)– Interest Rate Risk– Equity Risk– Foreign Exchange Risk– Commodity Risk– Option Risk

• Measures structural interest rate mismatch between illiquid assets and liabilities in home currency

• Risk measured based on long time horizons and large market movements– Interest Rate Risk– Liquidity Risk– Maturity Risk

Trading Risk Asset/Liability Mismatch Risk

2929© Oliver Wyman | LON-FSP03201-034

Shareholder equity

ALM risk arises from the structural inadequacy between assets and liabilities on the balance sheet…

Assets Liabilities

“Interest sensitive assets”• Short term loans at fixed rate• Long term loans at fixed rate• Short term loans at variable

rate• Long term loans at variable

rate

“Interest bearing liabilities”• Customer deposits• Long term borrowings• Short term loans at fixed rate• Short term loans at

variable rate

-50

-40

-30

-20

-10

0

10

20

Valu

e

Liabilities Assets

• Banking is founded on the principle of leveraging a low cost of funds• The “Assets” side of the balance sheet tends to exhibit much longer duration than the “Liabilities” side

– The bulk of bank liabilities come in the form of short-term deposits, sensitive to changes in the short term interest rates– Opportunities to make money typically involve longer duration activities, sensitive to changes in the long term interest rates

• Managing the risk associated with this lopsided balance sheet is essential to keeping a bank afloat

Gap profile of a typical bank B/SBalance sheet characteristics of a typical bank

3030© Oliver Wyman | LON-FSP03201-034

…and is an aggregation of Interest rate (IRR), FX and Liquidity risks

Illustrative IR shocks

Base case

Tenor

Tenor

Tenor

Tenor

Rat

eR

ate

Rat

eR

ate

• Liquidity risk is the risk of inability to meet payout commitments due to problems raising new funds or selling assets

Liquidity risk

• FX risk is driven by the volatility of exchange rates of all currencies on the balance sheet

• Balance sheet assets and liabilities are denominated in different currencies

FX risk

• Interest rate risk is driven by the volatility of interest rates leading to changes in the yield curve i.e. shifts, twists etc.

• Balance sheet assets and liabilities have different sensitivities to interest rates in terms of economic value and generated margin

Interest rate risk

+

+

3131© Oliver Wyman | LON-FSP03201-034

For Trading Risk, Value-at-Risk is an appropriate measure of Market Risk

• Trading holding periods are short-term

• Losses are largely independent from day-to-day

• Non-linearity of options less of an issue over short time periodsValue-at-risk

• Typically daily horizon

• Two standard deviations(97.52 confidence)

Trading P&L

0

2

Adjustments are made for liquidity, time horizon and management intervention when converting to Economic Capital

Operational riskSection 3.4

3333© Oliver Wyman | LON-FSP03201-034

• Changes in volumes• Changes in margins• Changes in costs• Changes in competitive

environment• Etc.

• Systems failure• Fraud• Litigation• Processing error• Breach of regulation• Etc.

Operating Risk splits into two subcategories

Business Risk Operational/Event Risk

Operating Risk

3434© Oliver Wyman | LON-FSP03201-034

Operational risks occur from many sources

Category Symptoms typically observed Largest event observed

Intentional fraud, collusion or misrepresentation by own staff or agents

• Rogue trader

• Internal theft

• Willful misrepresentation of P&L or risk

$2,500 MMSumitomo copper trader fraud

Unintentional errors and omissions by internal staff or agents

• Incorrect accounting, modelling, pricing or risk assessment

• Programming and data input/output errors

• Settlements/reconciliation errors

$500 MMCitibank failure of controls in Australian loan approval system

Man-made shocks and disasters (external)

• Externally perpetrated fraud

• Unanticipated regulatory changes and changes in tax regimes

• Unanticipated legal disputes or change in interpretation of the law

$1,200 MMPrudential Securities suit from ING for bad advice on purchase

Unanticipated loss of resources • Loss of key systems resources

• Loss of key personnel

• Loss of key suppliers, e.g. information providers

$85 MMCitibank cancellation of software contract

Natural disasters and shocks • Acts of God, e.g. earthquake

• Accidental damage, e.g. fire

$75 MMCredit Lyonnais fire at HQ

Etc.

Appendix

3636© Oliver Wyman | LON-FSP03201-034

Risk, in a financial sense, is defined as Volatility in Earnings (or Losses)

• Risk is any deviation from expectations– e.g. 2% loss a year

• For a loan portfolio risk is any deviation from expected losses– If a bank knows that it will lose exactly

2% in write-offs every year, it does not carry any risk

– Risk arises from uncertainty around the expectation of a 2% annual loss

0 Expectedearnings

Earnings distributionLikelihood of outcome

3737© Oliver Wyman | LON-FSP03201-034

A risk appetite statement represents what risks a Group is prepared to expose itself to as part of its business

For instance• Globally leading financial group• Committed to excellence in all markets it is

active in• Financial ambitions

– Target rating– Target ROE – Maintain dividends

• What is the worst result you would accept in terms of earnings over the course of a business cycle? How frequently would you accept zero profit?

• What is the worst rating you would be willing to accept once in your career?

• In what circumstances would you actually consider cutting your dividend? How often would you expect a company to experience a dividend cut?

• When would you take drastic measures to protect solvency?

Consistency

The Risk Appetite calibration process is crucial to ensure consistency with the business model

Risk Appetite addresses the following types of questions…

…in the context of the business model

3838© Oliver Wyman | LON-FSP03201-034

The goal of defining a risk appetite is to make explicit an appropriate level and nature of risk the Group is prepared to accept in pursuit of its’ desired strategy

• Build confidence (internal and external)– Clear “field of play” for operations– Comprehensive and robust basis for

external communication

• Force explicit consideration of the risk implications of strategy choices, and vice versa– Provoke dialogue: “how much is too much?”

• Raise internal awareness of potential issues– “Plain English” description of risk

management – Facilitate debate on potential future risks

• Pre-position for future events– De-risking to bring reality in line with

expectations– Early warning measures feeding up to

senior management

• Build mechanisms for implementation– Develop risk management “levers”

• Don’t be taken by surprise…

• …and don’t take stakeholders by surprise

• Don’t allow “separation from the herd”

• Prevent inaccurate external rumours

3939© Oliver Wyman | LON-FSP03201-034

The risk appetite statement should be clearly defined and link to potential management actions that can be used to adjust the risk profile

Qua

ntita

tive

Qua

litat

ive

Metric Illustrative definition Management options Key stakeholder

Target debt rating

• We target a Moody’s rating of “XXX” on our senior debt, at all times staying above “YYY”

• Granular measurement of Economic Capital• Monitoring key metrics (e.g. AFR,

liquidity, etc.)

• Debtholders• Rating agencies

Earnings volatility

• We will not miss consensus earnings forecast by more than “X”% at a “YY”% confidence level

• We will aim to consistently target dividend of “XXX”

• Quantitative stress testing of business plans • Shareholders

Maximum loss

• We do not wish to see a loss of more than “XXX” at the “YY”% confidence interval

• Bottom up risk measurement • Management

Liquidity headroom

• Available liquidity resources to meet requirements at “XX”% confidence interval

• Liquidity model to measure and forecast requirements

• Regulator• Shareholders• Debtholders

Reputation • Ensure that the highest ethical standards are followed at all times

• Ethical policy written to be followed by all staff all the time

• Customers• Regulator

Regulation • Have no significant instances of regulatory breach

• Compliance department • Regulator• Shareholders

Governance • Ensure appropriate policies and processes are followed at all times

• Internal/external audit • Regulator• Shareholders

Growth • All new business opportunities to follow appropriate risk controls

• Strategic Planning Process• Avoid portfolio concentrations

• Shareholders

Client example

Disguised client example of range of possible Risk Tolerance statements

4040© Oliver Wyman | LON-FSP03201-034

Reporting is a key element of the risk appetite framework; it should give management a clear understanding of the bank’s risk-taking capacity

• Consistent set of figures/charts allows trend tracing

• Drill down capability– Reports covering same broad themes but at different

levels of detail- Short Board summary linked to high-level risk

strategic profile- Longer risk type summaries enabling drill down into

risk-type issues- More detailed line of business reports allowing

further drill-down

• Traffic light risk triggers and pro-active contingency plans– Early warning system to identify capital and/or earning

strains linked to a preventative actions e.g.- Green – everything on track- Yellow – consider contingency plans - Orange – put contingency plans into action and

monitor- Red – Board/Group risk intervene as last resort

• Value added commentary plus ad-hoc analysis – Comments added to put words to the graphs– Tailored analysis carried out to focus attention on key

issues e.g. relevant trends/threat scenarios

• Action point tracking (e.g. limit breaches/major risks to the bank and follow-up actions)

Risk type andBU specifics

Risk type and

BU overview

Position and exposuredrill down

Summary and aggregation by reporting units

BUmanagement

Report

Appendix

Executivesummary

Report

Appendix

Executivesummary

Report

Appendix

Enterpriseoverview

BoardExecutive managementReporting hierarchy

Recommended reporting hierarchy Reporting principles

4141© Oliver Wyman | LON-FSP03201-034

Once embedded, a structured risk appetite framework will positively influence a number of key aspects across the organisation

Optimisingrisk avoidance/risk taking

Translating overall Risk Appetite limits into limits and targets on lower organisation levels means unwanted risk taking can be avoided and areas with scope for increased risk taking can be identified

Quicker changes in risk profile

Highlight risk topics to the Risk Committee and Board in a timely manner, leading to better risk-taking

Improved governance

Clearly defined limits and more focussed reporting will support risk oversight in all three lines of defence

Support risk culture

Clear reporting, defined limits and better overall transparency on risk capacity utilisation will help highlight the importance of risk management

Day-to-day business decision

All decision makers will have a clear understanding of what is expected in terms of risk taking, and the risk appetite will influence day-to-day decision making

Board communication

Support a more structured, holistic and meaningful communication with the board on risks

4242© Oliver Wyman | LON-FSP03201-034

Three basic measurement principles are relevant to the calculation of Economic Capital

Economic Capital is the amount of resources required to protect against economic insolvency due to changes in value over a

specified time horizon and confidence interval

Economic Capital principles for today’s discussion

Definition of value

Time horizon

Confidence level

1

2

3

4343© Oliver Wyman | LON-FSP03201-034

The key choice of time horizon is between a one-year view and a multi-year view

One-year approach Multi-year approach

• Solvency is assessed over a one-year time horizon

• Expected market value of assets and liabilities in one year is compared to ‘worst case’ market value of assets and liabilities in one year

• Assumes that the portfolio can be restructured within one year in the event of adverse scenarios

• Requires ability to assess the market value of the balance sheet. The volatility of all future cash flows is implicitly captured in the volatility of the market value

• Solvency is assessed over a multi-year time period

• The value of assets and liabilities is stochastically projected over multiple years and it is checked how much capital needs to be held initially to ensure that assets exceed liabilities at the end of the projection horizon

• Typically assumes that assets and liabilities are held to maturity

• Usually cash flow-based and often used when market value assessments are not available. Requires explicit modelling of cash flows over lifetime of the asset/liability

2

Time horizon

4444© Oliver Wyman | LON-FSP03201-034

The one-year Economic Capital framework is the market standard for financial institutions

• It introduces consistency across the Group

• It is in line with capital management/ planning horizon

• One year is a relevant time horizon over which re-capitalisation would be considered

• Despite being a one-year measure, it still captures change in market value which allows it to address multi-period nature of business

• For European institutions, regulators are heading in this direction

Expected scenario

Worst case scenario (for one risk factor)

Time

Fair

valu

e

Vt+1,expected

Vt+1,worst case

Worst casevalue loss

Economic Capital

Time horizon

2

Framework Why?

4545© Oliver Wyman | LON-FSP03201-034

• Economic Capital is the amount of capital that an institution needs to hold in order to keep its probability of insolvency below a pre-specified threshold

• Solvency standard is related to likelihood of default – anchored to observable corporate bond default rates at various ratings

• For the same risk profile, an institution targeting a better credit rating will need to hold more capital

Expectedvalue

Economic required capital

ECBBB

ECA

ECAA

ECAAA

Value

AAAA AA BBB

Probabilityof outcome

Tail

prob

abili

ties

Confidence interval

Most institutions calibrate their Economic Capital models to bond probabilities of default

3

Value at risk distribution

4646© Oliver Wyman | LON-FSP03201-034

VaR is not a good way to characterise ALM Risk if the value distribution is not normal

? XVAR

ALM

“Worst case” loss relative to VAR is a function of the skewness of the distribution

• Long horizon

• Non-linearity (optionality) material

Trading

Value-at-risk2

Therefore, for ALM, one should model the annual distribution explicitly

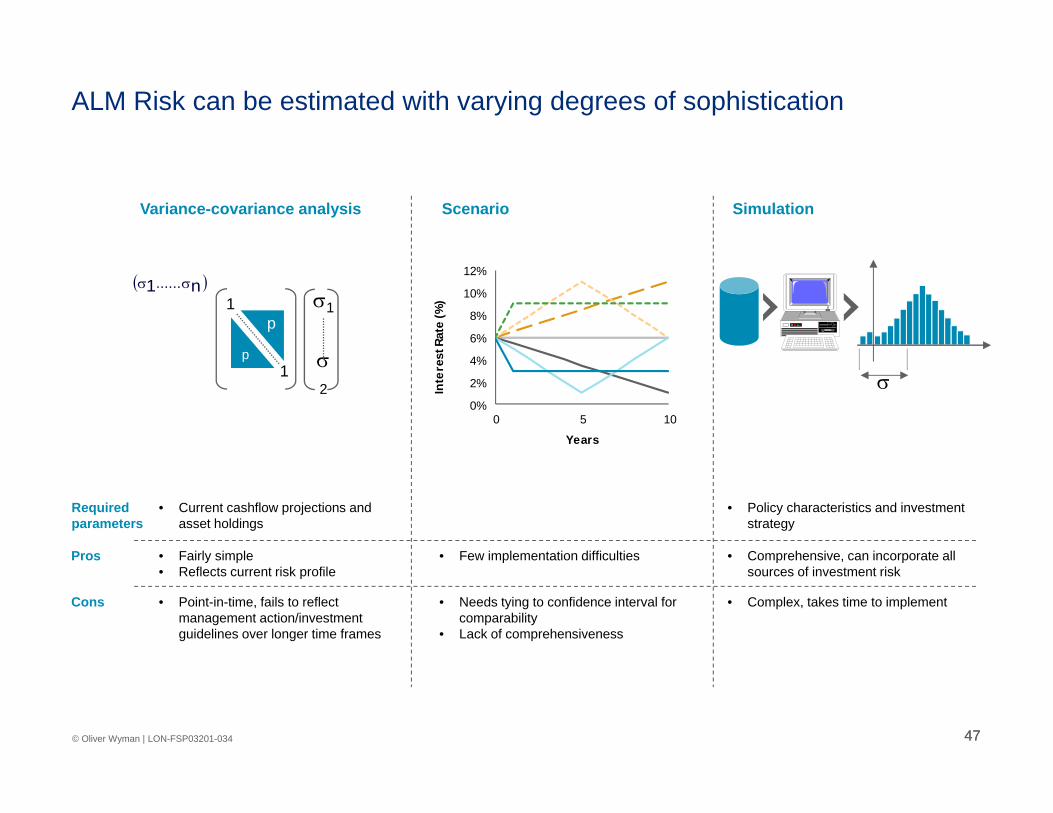

4747© Oliver Wyman | LON-FSP03201-034

Variance-covariance analysis Simulation

• Fairly simple• Reflects current risk profile

• Comprehensive, can incorporate all sources of investment risk

• Current cashflow projections and asset holdings

• Policy characteristics and investment strategy

n1 ......

p

p1

1

1

2

Scenario

0%

2%

4%

6%

8%

10%

12%

0 5 10

YearsIn

tere

st R

ate

(%)

• Few implementation difficulties

Requiredparameters

ALM Risk can be estimated with varying degrees of sophistication

• Point-in-time, fails to reflect management action/investment guidelines over longer time frames

• Complex, takes time to implement• Needs tying to confidence interval for comparability

• Lack of comprehensiveness

Pros

Cons