risk solutions user forum jeff bottari, vp risk solutions group checkfree october 24, 2007

Post on 18-Dec-2015

220 views

TRANSCRIPT

Risk Solutions User Forum

Jeff Bottari, VP Risk Solutions GroupCheckFree

October 24, 2007

2

Welcome!!

3

User Conference Objectives

Very few CheckFree commercials

Shared experiences using CheckFree products

Shared industry concerns

A time to talk with other banks about issues

Advise CheckFree on what you like, don’t like, and would like to see

A feeling of community

An opportunity to advance best practices

It should be fun!

Jeff Bottari

Compton Harry

Debb Gordon

Don Crosby

Robert McCannMichael Bunyard

Karen Taylor

Pete Sullivan

Jeff S-S-Sargent

Dee Millard

Mark Steeber

Angela Bardowell

Rich Rosner

Dan Barta

Roger Snell

7

Whatever happened to Carreker?

8

CheckFree / Carreker

Acquisition completed on April 1st, 2007

CheckFree is a $1 billion company with 4,400 employees world-wide, located in more than 20 different cities

Carreker’s current solutions are being integrated into CheckFree’s current product structure

The combination of the two predecessor companies makes CheckFree an industry leader in software applications that cross the traditional check-based & ACH payments arena

We are uniquely qualified to help banks balance customer needs with needs for greater efficiency and profitability, as an already diverse payments environment continues to evolve and change

9

CheckFree Snapshot

Premier provider of financial electronic commerce services and software products

Founded by current Chairman & CEO Pete Kight in 1981

Became a publicly traded company in 1995

26 years in operation

2006 in Review:

Revenue of $972.6 million

Nearly 1.3 billion transactions processed

Nearly 226 million electronic bills delivered

Nearly 2.7 million portfolios under management at year end

10

Whatever happened to CheckFree?

Soon to be a part of…

11

Carreker/CheckFree’s Risk Management Solutions

We are the premier supplier of Enterprise Risk and Fraud Mitigation Solutions.

Our Pragmatic Convergence approach provides financial institutions with maximum protection via multi-channel transaction monitoring and customer behavior modeling.

12

Pragmatic Approach Defined

The destiny: An enterprise risk mitigation platform which correlates fraud across access points and channels by customer

Allows you to leverage your existing investments to create an achievable strategic plan

Stay ahead of the fraudsters while gradually adding functionality

Each step provides a return on investment in months not years

prag·mat·ic [prag-mat-ik] -adjective: Concerned with practical matters; “a matter-of-fact approach to the problem”

— Webster

13

Weaknesses of Current Risk Management Models

Largely a Day 2 Process… Limited Day 1 and Day 0 Analytics

Day 0: Real time instantaneous transaction monitoring at Customer Access Point — Proactive

Day 1: Same-day analysis of transactions before posting (near real time or multiple batch runs) — Reactive

Day 2: Batch analysis after Posting — Reactive

Different capabilities in different silos

No ability to correlate transactions in multiple customer access points in multiple timeframes

Multiple analysts working same accounts in different channels

14

Example of Fraud Detection in Individual Silos

Sophisticated Fraudsters Will Find The Weakest Link

• Duplication of solution investments• High/unnecessary IT overhead• Duplication of data and resource expenses• No leverage of cross-silo alerts

Results in:

Alert MgmtSystem

Shared Data

Scoring Engines, Models, Rules

On-Us / Deposit

Alert MgmtSystem

Shared Data

Scoring Engines, Models, Rules

ACH

Alert MgmtSystem

Shared Data

Scoring Engines, Models, Rules

Wires

Alert MgmtSystem

Shared Data

Scoring Engines, Models, Rules

Internet /ATM

15

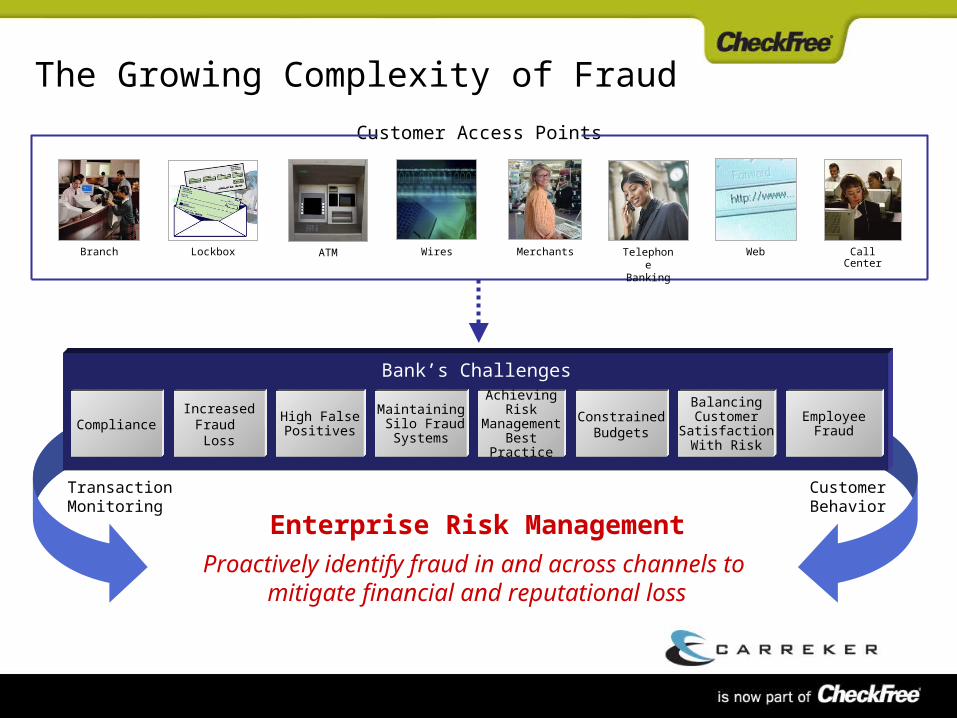

Customer Access Points

Enterprise Risk ManagementProactively identify fraud in and across channels to

mitigate financial and reputational loss

IncreasedFraud Loss

High FalsePositives

Achieving Risk

Management Best

Practice

Bank’s Challenges

Constrained Budgets

Balancing Customer

Satisfaction With Risk

Maintaining Silo Fraud Systems

The Growing Complexity of Fraud

Transaction Monitoring

Customer Behavior

Branch Lockbox WebMerchantsATM Telephone Banking

Call CenterWires

Employee FraudCompliance

16

Industry Best Practice:Enterprise Risk Management

Holistic View of transactions, accounts, and relationships

Monitor all transactions for suspicious behavior

Analyze monetary and non-monetary data

Enable creating rules containing cross-channel variables

Manage potential fraud cases effectively, from detection through law enforcement reporting

Move to Proactive vs. Reactive

17

Carreker/CheckFree Enterprise Risk Management

DetectionManagement

AlertManagement

CaseManagement

Other Detection

Investment Accounts

Credit Accounts

Other Detection

Other Detection

Liability Accounts

InvestigationInvestigation

Link Link AnalysisAnalysis

ReportingReporting

AcquireAcquire

ResearchResearch

DecisionDecision

AnalyzeAnalyze

Day 0, Day 1 or Day 2 Capabilities

Alerts

On-UsDeposit

WiresACH Fraud

ManagerFraud

Manager

Fraud

Workflow ManagerWorkflow Manager

Syfact Investigator

Syfact Investigator

18

Data Acquisition Detection

Data Staging

Workflow Manager Disposition

Data

Acq

uis

ition

En

gin

e

External Data

Sources

All Trans-actions File

Internal Data

Sources

FraudLink On-Us

Mainframe

FraudLink Deposit

Mainframe

Su

spect D

ata

base

Case Management

Ale

rt Packag

er

On-Us Real Time

DepositReal Time

On-Us Day 1 & 2

DepositDay 1 & 2

ACH

ATM

InternetBanking

Wires

Other

Modeling

Segments

Profiles

User Defined Rules

Filter

Lists

Alert Management

Research

Decisioning/ Fraud Analyst Workstation

Reporting

Queries / Dashboard

WorkDistribution

Credit LRM ATM/Cards Treasury Mgmt

Enterprise Risk Management

19

Frauds

Dashboard Example

On-Us Deposit ACH Wires OnlineLoans Internal

Enterprise Region Customer

Total Customers Alerted(000)’s

Total Fraud Volume YTD Number of Alerts Process per FTE

per Hour

Regions # Alerted % Increase from last Qtr

Region 12 7,245 15Region 14 5,895 10Region 5 5,432 7Region 8 5,236 3Region 11 2,529 0

Top 5 Customer AlertedRegions in 4Q 2005

Regions $ Alerted % Increase from last Qtr

Region 12 3,796,380 15Region 14 2,528,955 10Region 8 2,371,908 7Region 5 2,297,736 3Region 11 1,044,477 0

Top 5 Alerted AmountsRegions in 4Q 2005

20

Benefits of Enterprise Risk Management

Efficiency

Automated processes

Review fraud-rich pool of suspects with no addition to staff

Single platform for all fraud mitigation

Effectiveness

Improved fraud detection

Lower false positives, reduce false negatives

Improved analyst job satisfaction

Flexibility

Dynamic creation of rules

Image-based workflow

Champion vs. Challenger

21

Agenda Day One

Welcome and Introductions Jeff Bottari, VP Risk Solutions Group, CheckFree

Enterprise Alert Management: Managing Alerts More Effectively

Silvia Sarra, AVP Loss Prevention & Security, Sovereign Bank

Dan Barta, Service Delivery Manager, CheckFree

Citibank and CheckFree Fraud Manager Deposit Case Study

Debb Gordon, Director Business Architecture and Analysis, CheckFree

Reducing False Positives: Effectively using Account Types and Period Parameters

Lisa Zarzycki, Vice President and Risk Manager Fraud Services, Comerica Bank

22

Agenda Day One, continued

Internet Banking Fraud Trends Carly Boardman, Manager Cheque Compliance & Fraud Detection, ANZ

Peter Casey, Manager Fraud Detection, ANZ

Understanding Your Bank’s “Fraud Profile”: A Risk-Based Approach to Re-calibration

Mark Steeber, Risk Advisory Consultant, CheckFree

Closing Remarks Jeff Bottari

Cocktail Happy Hour

Client Conference Event

Tapas Bar and Drinks ReceptionTerrace Bay Lobby, Lower Level

San Diego Zoo

23

Agenda Day Two

Emerging Fraud Trends:What trends are you seeing?

Angela Bardowell, Director Risk Consulting Group, CheckFree

Product Roadmap

Product Roadmap Session with Customer Input

Michael Bunyard, Director Product Management, CheckFreeGroup Discussion

Group Discussion

Meeting Wrap-Up Jeff Bottari, VP Risk Solutions Group, CheckFree

Questions?

Enterprise Alert Management:Managing Alerts More Effectively

Silvia Sarra, Sovereign Bank

Dan Barta, CheckFree

October 24, 2007

26

What is Enterprise Alert Management?

en·ter·prise [en'-ter-prahyz] −noun:

1) a project or undertaking that is especially difficult, complicated, or risky

2) readiness to engage in daring or difficult action: initiative <showed great enterprise in dealing with the crisis>

3) a unit of economic organization or activity; especially: a) a business organization b) a systematic purposeful activity <agriculture is the main economic enterprise among these people>

— Webster

27

What “Enterprise” will we be Discussing Today?

Enterprise Definition and Scope

Focus on transaction accounts (DDA & SAV)

Focus on payment transactions and account opening

Limited inclusion of money laundering analysis

Focus on fraud and loss prevention activities

Other areas that could be included

Mortgage and other lending transactions

Investment accounts (brokerage, mutual funds, etc.)

Insurance

Other Industries

28

Payment ChannelsPayment Channels

Enterprise Alert Management

FraudLinkACHeCK

Falcon Fraud MgrWires Other ToolsFalcon

FraudLinkOn-Us/Deposit

Detection ToolsDetection Tools

SuspectReport

SuspectReport

SuspectReport

SuspectReport

SuspectReport

SuspectReport

ACH Debit Wires ATMCreditCheck

29

Payment ChannelsPayment Channels

Enterprise Alert Management

FraudLinkACHeCK

Falcon Fraud MgrWires Other ToolsFalcon

FraudLinkOn-Us/Deposit

Detection ToolsDetection Tools

ACH Debit Wires ATMCreditCheck

Workflow ToolWorkflow Tool

SuspectReport

SuspectReport

SuspectReport

SuspectReport

SuspectReport

SuspectReport

30

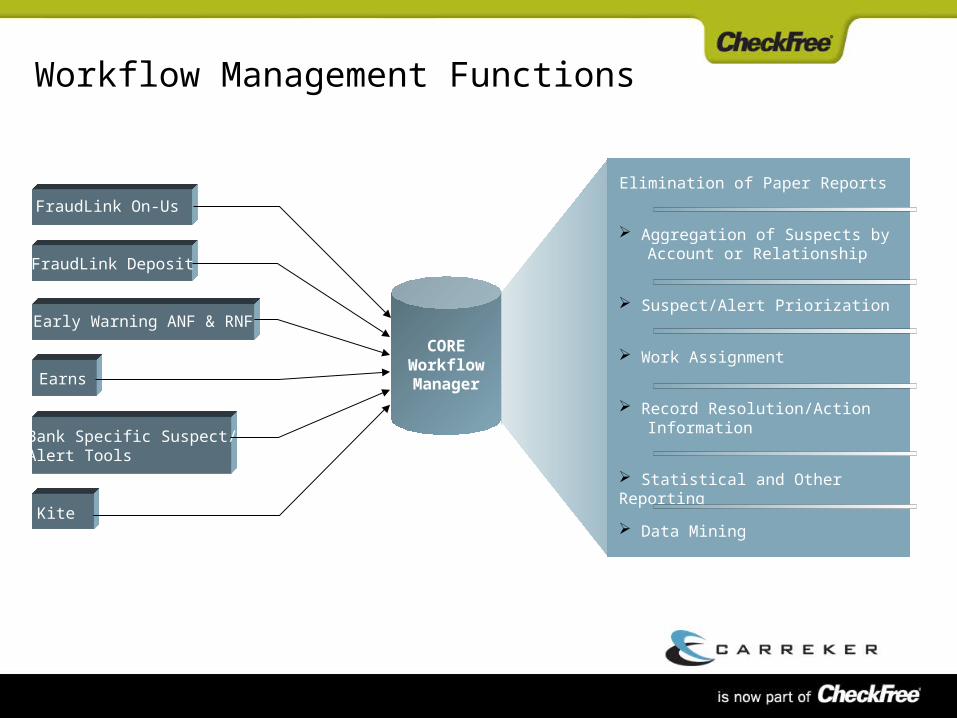

CORE Workflow Manager

Elimination of Paper Reports

FraudLink Deposit

Early Warning ANF & RNF

Earns

Bank Specific Suspect/Alert Tools

Kite

Aggregation of Suspects by Account or Relationship

Suspect/Alert Priorization

Work Assignment

Record Resolution/Action Information

Statistical and Other Reporting

Data Mining

FraudLink On-Us

Workflow Management Functions

31

CORE Workflow Manager

Elimination of Paper Reports

FraudLink Deposit

Early Warning ANF & RNF

Earns

Bank Specific Suspect/Alert Tools

Kite

Aggregation of Suspects by Account or Relationship

Suspect/Alert Priorization

Work Assignment

Record Resolution/Action Information

Statistical and Other Reporting

Data Mining

FraudLink On-Us

DocumentGeneration

Mainframe Communication

Workflow Management Functions

32

Benefits of Enterprise Alerts Management

Utilization of Database software

More complete view of risk at the account/customer level

Better Prioritization of Suspect/transaction Activity

Elimination of Redundant Effort

Smarter/Faster Decisions

Historical Picture of Suspect/Alert Activity

Research capability

Elimination of Paper Reports

33

Sovereign Bank – Company Overview

Sovereign’s headquarters in Wyomissing, PA

$82 billion financial institution

Markets primarily in the Northeast United States

750 Community Banking Offices (CBOs) & 2,250 ATMs

18th largest banking institution in the United States

Successfully completed two dozen acquisitions since the late 1980s

34

Loss Prevention – Operational Overview

Centralized Loss Prevention Unit

Team of 44

Check fraud prevention (Deposit & On-Us)

Case Management case input

Centralized check fraud claims

Debit card (signature and pinned)

Fraud claims

Single point of contact for ID Theft

CBOs, customers, and other Sovereign units’ support via a toll free response line

Elderly Abuse

35

Business Drivers to Implement Enterprise Alert Management

Mergers and Acquisitions

Standardize staff training

Establish a suspect/victim model

Inability to prioritize highest risk alerts

Analysts working in silos i.e. same suspects in multiple reports

Manual processes

Customer notifications (Reg CC)

Re-keying same info in several applications

Unable to identify new trends

Lack of audit trails

Paper driven

36

Staff Efficiency & Operational Gains

Prioritization of highest risk accounts

Elimination of manual processes

Customer notifications

Connection to host system eliminating re-keying of same date

Audit trail (tracks every keystroke)

On average it takes 5 minutes vs. 10 minutes to make a decision to pay/return/hold/freeze

Holistic review of suspects

At a glance history of suspect transactions

Detection rate of alerts reviewed year to date averages 90%

Return on investment (ROI) year to date averages 22:1

4 FTE reduction

37

Customer Service Impacts

Standardize notification to customers

Info populating by pulling from host systems hence less chance for typos

Any Analyst can assist customer that calls inquiring about a notification they received, less time spent on the phone

Questions?

Citibank and CheckFreeFraud Manager Deposit: A Case Study

Gail O’Brien, Citibank

David Fapohunda, Citibank

Debb Gordon, CheckFree

October 24, 2007

40

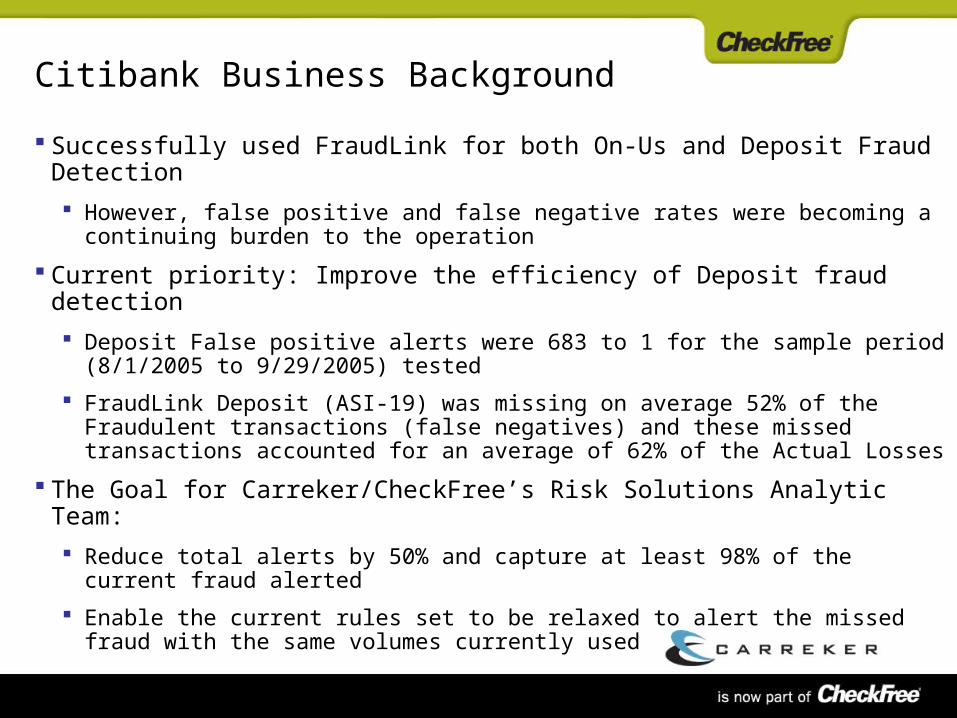

Citibank Business Background

Successfully used FraudLink for both On-Us and Deposit Fraud Detection

However, false positive and false negative rates were becoming a continuing burden to the operation

Current priority: Improve the efficiency of Deposit fraud detection

Deposit False positive alerts were 683 to 1 for the sample period (8/1/2005 to 9/29/2005) tested

FraudLink Deposit (ASI-19) was missing on average 52% of the Fraudulent transactions (false negatives) and these missed transactions accounted for an average of 62% of the Actual Losses

The Goal for Carreker/CheckFree’s Risk Solutions Analytic Team:

Reduce total alerts by 50% and capture at least 98% of the current fraud alerted

Enable the current rules set to be relaxed to alert the missed fraud with the same volumes currently used

41

Analytic Project Background

Early 2006, Carreker/CheckFree approached Citibank to perform a validation of the statistical models created from pooled bank data

Citibank initially provided FraudLink Deposit Transaction alert data from 8/1/2005 thru 9/29/2005

The Risk Solutions Analytic Team scored the transactions on the Generic model and developed a Custom Model for Citibank

Following the Development process, Citibank provided three months of blind data (11/1/2005 thru 1/31/2006) to be scored and returned to their analysts

The model was successfully able to meet the project criteria of a total alert reduction of 50% while maintaining a fraud detection rate of at least 98%

21 months later, the validation was repeated and replicated the results

42

Advanced Analytics

System Capabilities

Modeling

Statistical fraud models designed and tailored to fit behavior in each institution

Rules

Custom defined rules written and published by the operation

Lists

Can be imported from an outside source, or created by the operation

Segmentation

Create segments that can be serviced with different logic

Filters

Filters limit what you want to alert

43

Advanced Analytics

The Score

Each transaction is scored based on good customer profiles

Scores range from Zero to 1,000, the higher the score the more likely it’s fraud

Scores are presented in a distribution, you pick the cut-off score that best fits you

Use the score to prioritize workflow, or use a combination of score and any other information you use today

44

Analytic Study Results

Deposit Model and Blind Testing

False Positives were reduced by 51%

Fraud Capture with existing FraudLink alerts was 98%

21 Months later

False Positives were still showing a reduction on average of 45%

Fraud Dollar Capture with existing FraudLink alerts was 98.3%

The reduction in total alerts allows for relaxing existing FraudLink rule sets to allow for more of the false negative frauds to be scored

45

Citibank’s Business Application

Scored transactions

Defined rules

Prioritization in Workflow

Combining different information for better decisioning

46

Conclusion

Based on these Model Validation studies, Citi expects a significant reduction in alert volume

Combining the use of the score with other user written rules can improve these results even more.

Citi is looking forward to greater operational efficiency in Day 2 Batch

Future releases will bring the detection to Day 0 Real Time, allowing for automated holds and returns at the point of Deposit

Questions?

Comerica’s Experience with FraudLink DepositReducing False Positives:Effectively using Account Types and Period Parameters

Lisa M. Zarzycki, Comerica

October 24, 2007

49

Comerica Overview*

$58.6 Billion in total assets

401 Banking Centers in 5 States

Michigan,

California,

Texas,

Florida, and

Arizona

Select businesses operating in several other states, as well as Canada, Mexico, and China

Among the 20 largest U.S. banking companies

*As of July 18, 2007

50

FraudLink Deposit History

Comerica installed FraudLink Deposit v2.0 in October 2003.

With the exception of “home grown” ATM deposit fraud reports, Comerica had no deposit fraud prevention tool.

Comerica estimated $375,000 in loss avoidance in the first year.

Actual Loss Avoidance: $1.8 M

Total At Risk: $1.9 M

230 Cases

Average Prevention: $7,800

51

FraudLink Deposit Rules at Inception

5 of the 7 available rules (excluding 3 & 5) 3 Account Periods 3 Separate Markets 13 account types

Type A – Access & Value Ckg *Free Retail Type C – Correspondent Banks Type E – Employee Accounts Type H – High End Retail Ckg Type I – Interest Retail Type L – Large Business Type M – Interest & MMIA Bus Type O – Other Business *Professional (Drs., IOLTA, etc.) Type R – Regular Chg Type S – Small Business *Free Business Type 1 – Retail Savings Type 2 – Business Savings DFLT – Default Accounts *Deposit is made in market other than home market

52

FraudLink Deposit Inception

Average suspects per day – 2,137

4 FTE reviewed 994 or 46% on average

To manage volumes, analysts review “high risk” account types and high risk markets.

53

Upgrade to FraudLink v3.0

August 2006, Comerica Upgrades to FraudLink v3.0

Charge off analysis reveals that 80% of deposit fraud losses occur in the first 90 days and 63% of deposit fraud losses occur in the first 10 days of account opening

Move to 6 Account Periods:

0 to 10 days

11 to 90 days

91 to 180 days

181 to 365 days

366 to 1095 days

Greater than 1095 days

Update Parameters Based on Account Periods

Enable Rule 3 (36% reduction in suspects)

54

Additional Filters

January 2007, filter added to work flow management system

If the count of the number of times an account has suspected is greater than X times (Y or more) the alert will not be passed into the system to be worked by an analyst.

The filter is not applied to the FLK system but rather to the output from the system.

This allows the group to identify in a charge off analysis if the filter caused the account not to suspect and there was subsequent fraud.

The filter reduced suspects by an additional 16%.

55

FraudLink Today

Average: 1533 suspects per day

Staffing: 5 FTE

Results: 1080 suspects reviewed or 73%

Focus on “high risk” account types as defined by loss analysis

High Risk Account Types:

70% of Suspects

82% of Deposit Fraud at Fisk

79% of Deposit Fraud New Losses

Continuous charge off analysis to identify high risk account types and markets and manage false positives

Questions?

Contact Lisa M. Zarzycki

248-371-6742

Australia and New Zealand Banking Group Limited

Carly BoardmanManager

Fraud Detection &Cheque Compliance

Peter CaseyManager

Fraud Detection

ANZ Banking Group Limited

• One of the 5 largest and most successful companies in Australia and the number one bank in New Zealand

• Represented in our primary markets of Australia and New Zealand, as well as Asia, the Pacific, the UK, Europe and USA

• 781 branches in Australia and 1,265 other worldwide points of representation

• 6 million customers worldwide – personal, private banking, small business, corporate, institutional & asset finance

• USD$298 billion in assets

• Employ more than 30,000 staff worldwide

Financial Intelligence Operations

Cheque Fraud

Detection

Internet & Phone Banking Fraud Detection

Cheque Compliance

Denied Payments

AML / CTF

Education of ANZ branch staff, detection of on us and deposit fraud by way of: Fraudlink ASI16 & ASI19, Fraudlink Cheque Order Report, Fraudlink Kite ANZ Visual Image Archive Data exchange with other Fraudlink enabled banks Physical examination of large amount cheques

Detection of internet and phone banking fraud by way of: Fraudlink Billpay Eunexus Internet Intelligence System

Assist with the design, approval and production of ‘special print’ cheques for ANZ business customers.

Represent ANZ on the Australian banking industry Printing Standards Committee.

Filter inward and outward messages against lists, looking for Sanctioned Parties, Countries, Assets (Commodities), Currencies by way of Metavante’s Prime Compliance Suite of products.

Team currently ‘under construction’.

ANZ AML Program looking to introduce new technology and processes to meet revised Australian legislation that will ensure compliance with international standards (FATF).

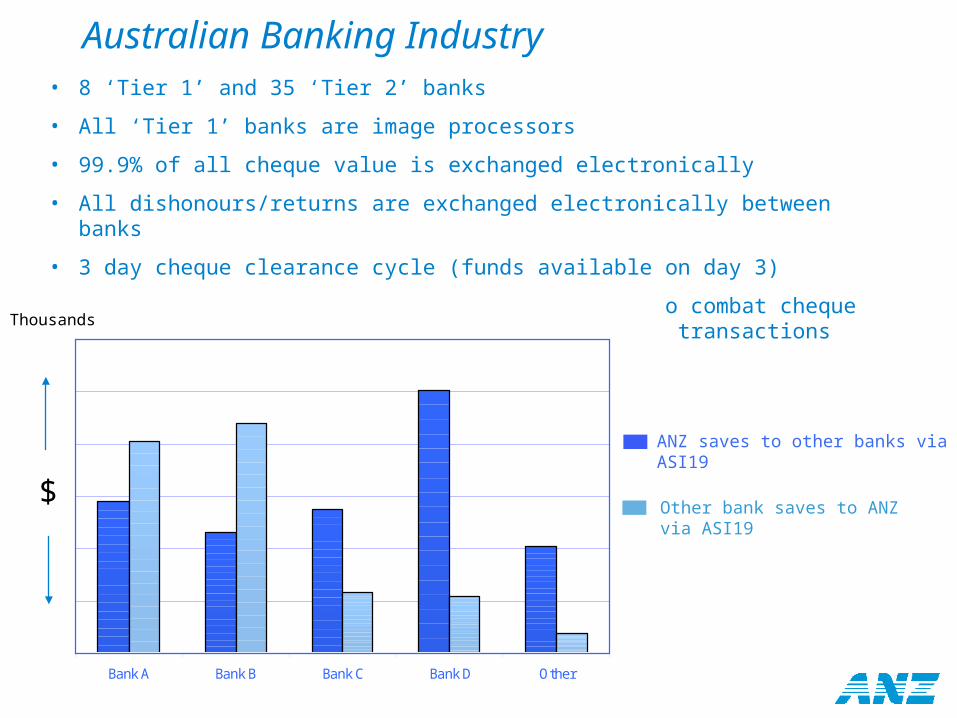

Australian Banking Industry• 8 ‘Tier 1’ and 35 ‘Tier 2’ banks

• All ‘Tier 1’ banks are image processors

• 99.9% of all cheque value is exchanged electronically

• All dishonours/returns are exchanged electronically between banks

• 3 day cheque clearance cycle (funds available on day 3)

• FraudLink enabled banks work collaboratively to combat cheque fraud, i.e. daily exchange of ‘suspect’ cheque transactions

12 month period

Bank A Bank B Bank C Bank D Other

$

ANZ saves to other banks via ASI19

Other bank saves to ANZ via ASI19

Thousands

Australian Domestic Payment Streams

Figures obtained via the Australian Payments Clearing Association (APCA) Ltd

Avg. transaction volume per month

Cheque Online Debit

Online Credit ATM

EFTPOS Credit Card

$120

$100

$80

$60

$40

$20

Million

1997 200320022001200019991998 2007200620052004

10% 20% 30% 40% 50%

Breach of Mandate

Third Party Conversion

Counterfeit

Theft / Forgery

Alteration

Valueless / Kite Flying

% of Value

% of Value

Figures obtained via the Australian Payments Clearing Association (APCA) Ltd

Australian Cheque Fraud Experience $148M in attempts, $32M in losses Losses represent 0.0005% of cheque transaction volume Losses represent 0.0019% of cheque transaction value

In 2006

ANZ Internet Banking Functionality

Balance and Transaction Enquiries Pay Bills to over 10,000 registered billers, e.g. utility companies Receive, view and pay bills online Transfer between connected accounts Transfer funds to accounts held with other Australian banks Transfer funds overseas Multi Payments, e.g. company payroll Purchase a Bank Cheque or International Draft Secure Mail

Security

128-bit SSL Encryption

Firewalls to prevent access to the ANZ network

Automatic time-outs

Fraud Detection (FraudLink)

Limited use of Two Factor Authentication

ANZ Internet Banking

What We Plan To Do?

Migration to CheckFree’s Fraud Manager Platform (Business Case in progress)

Move to real time detection (as opposed to intra day batch)

Login Session Monitoring – Stop the fraud before it happens

Continue Consumer Education & Awareness Campaigns

What Have We Done?

Implemented Fraudlink Billpay (2004)

Integration of Eunexus Internet Intelligence System to enrich Fraudlink

Billpay

Real-time sharing of IP intelligence with other Eunexus enabled banks in

Australia

Consumer Education & Awareness Campaigns

ANZ won Financial Insights Innovation Award in the category of security

& fraud management

Decreased losses by 40% increased detection by 80%

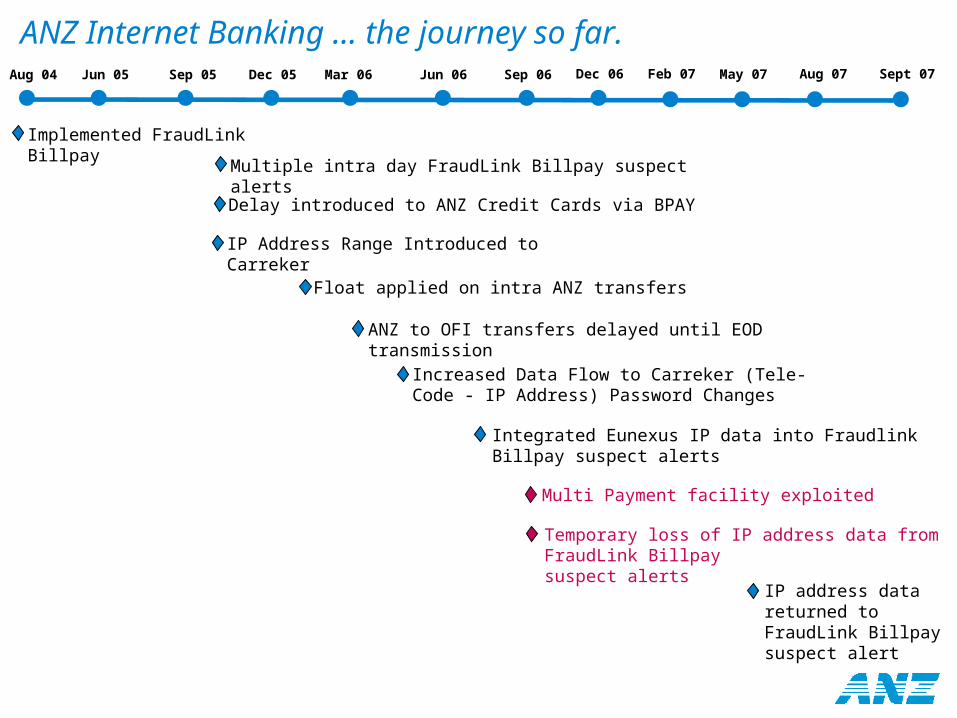

ANZ Internet Banking … the journey so far.Aug 04 Sep 05 Jun 06 Sep 06 Dec 06Mar 06Dec 05Jun 05 May 07 Sept 07Feb 07 Aug 07

Multi Payment facility exploited

Temporary loss of IP address data from FraudLink Billpay suspect alerts

Implemented FraudLink Billpay

Multiple intra day FraudLink Billpay suspect alerts

Delay introduced to ANZ Credit Cards via BPAY

IP Address Range Introduced to Carreker

Float applied on intra ANZ transfers

ANZ to OFI transfers delayed until EOD transmission

Increased Data Flow to Carreker (Tele-Code - IP Address) Password Changes

Integrated Eunexus IP data into Fraudlink Billpay suspect alerts

IP address data returned to FraudLink Billpay suspect alert

ANZ Internet Banking

Billion

How we are tracking against increased transaction volume …

Tra

nsa

ction V

alu

e

Some Fraud Alert Triggers Payee or Recipient is not in previous account history

Dollar Value is “Greater Than Average”

IP Address originates from an overseas destination

IP address has been marked as ‘fraud’ by another Eunexus enabled bank

IP address identified as either ‘malicious or ‘proxy’ by the Eunexus Internet Intelligence System

IP Address has never been used previously by customer

Payment message or reference entered at the time of transaction, considered suspicious

Payments to ‘high risk’ billers (gambling institutions or money transfer agents)

Telecode/Password resets (for telephone banking channel)

Weight of a suspect alert (10 – 20 – 30 – 40)

IP Sharing & ReportingIP Sharing

75% of all Australian banks, are using IP data provided by Eunexus

‘Eunexus’ enabled banks are actively sharing IP intelligence, thereby effecting an industry approach to internet fraud, e.g. blacklisting IP addresses

Reporting to Government

Australian banks report all cases of online fraud to the Australian High Tech Crime Centre (AHTCC)

The AHTCC is a collaboration between the government and private industry to enable a national and coordinated approach to combating serious, multi-jurisdictional technology enabled crimes.

Questions?

Understanding Your Banks “Fraud Profile”: A Risk-Based Approach to FraudLink Re-Calibration

Mark Steeber, CheckFree

October 24, 2007

Agenda

Overview: Check and Deposit Fraud – How Has It Changed? How Does It Remain the Same?

Determining Your “False Positive Rate” & “Fraud Detection Rate”

FraudLink System Reports: Data Collection & Analysis

Fraud Detection/Fraud Losses: Data Collection & Analysis

“Fraud Profile”: Identifying Current & Emerging Fraud Activity

Risk-Based Re-Calibration: Targeting Your “Fraud Profile”

Overview: Check and Deposit Fraud – How has it changed? How does it remain the same?

Back in the “old days,” remember when…

A $1000 fraud loss was catastrophic

No automated way to detect in-clearing check fraud

Two types of deposit fraud; new account fraud and kiting

The fraudster had to come into the bank to commit fraud

Depended on new account reps. and tellers to detect fraud

Fraud today…

A $10,000 fraud loss might be catastrophic?????

FraudLink On-Us in-clearing check fraud detection

FraudLink Deposit & Kite detecting deposit fraud schemes

Fraudster doesn’t have to enter bank to commit fraud

Depend on new account reps and tellers to sell, sell, sell…

Overview: Check and Deposit Fraud – How has it changed? How does it remain the same?

Fundamentally check fraud has not changed

Checks are still…

Lost or stolen

Forged

Counterfeited

Purchases

Deposit fraud schemes

Teller cashed

Paid in-clearing

The playing field has just gotten bigger

Professionals

Amateurs

Victim Customers

Electronic Transaction – ACH & Debit Card

Overview: Check and Deposit Fraud – How has it changed? How does it remains the same?

Challenges

Check Losses Highest Among All Payments Channels

< Check Volume = > Check Fraud?????

Federal Reserve Payments Study -

Check Volume: 2000 – 41.9B & 2003 – 36.7B = ↓12.4%

Electronic Payments: 2000 – 30.6B & 2003 – 44.5B = ↑44.5%

ABA Fraud Survey

Fraud Cases: 1999 – 447G; 2001 – 600G & 2003 – 616G

Attempted Check Fraud: 1999 - $2.2B; 2001 - $4.3B & 2003 - $5.5B

Losses: 1999 - $679M; 2001 - $698M & 2003 - $677M

Overview: Check and Deposit Fraud – How has it changed? How does it remains the same?

Challenges FinCEN SAR Reporting - (Check Fraud, Kiting & Counterfeit Checks

Only)

1999 – 27,682; 2001 – 43,501; 2003 – 61,611; 2006 – 124,905

Association of Financial Professionals (AFP) 2007 Payments Fraud Survey

Check fraud is increasing despite check volume decline Check Fraud 93%

ACH Debit Fraud 35%

Consumer Credit Card Fraud 17%

Corporate Purchasing Card14%

Consumer Debit Card Fraud 5%

ACH Credit Fraud 4%

Wire Transfer Fraud 3%

Determining Your “False Positive Rate” & “Fraud Detection Rate”

FraudLink On-Us “False Positive Rate”

FraudLink On-Us Suspects Deemed Good ÷ Total FraudLink On-Us Suspects = False Positive Rate

1,068,000 Suspect Items - 1,360 Fraud Items = 1,066,640 Good Suspects

1,066,640 Goods ÷ 1,068,000 Total Suspects = 99.8% False Positive Rate

Loss Avoidance Total: $4.4M – Charge Off Total : $400K

Daily Average Suspect Volume: 4,240/5 FTE = 850 Items/FTE

Determining Your “False Positive Rate” & “Fraud Detection Rate”

FraudLink On-Us “False Positive Ratio”

FraudLink On-Us Suspect Items ÷ FraudLink On-Us Items Detected = False Positive Ratio

1,068,000 Suspect Items ÷ 1,360 Fraud Items = 785:1 Ratio

One Fraud Item for Every 785 Suspects

Determining Your “False Positive Rate” & “Fraud Detection Rate”

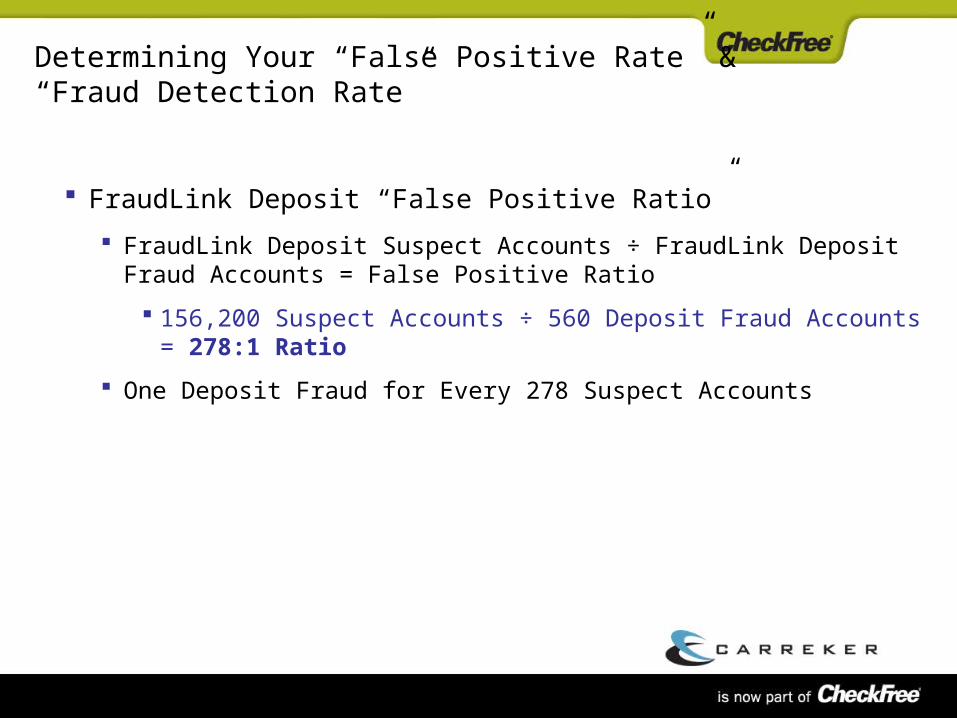

FraudLink Deposit “False Positive Rate”

FraudLink Deposit Suspects Deemed Good ÷ Total FraudLink Deposit Frauds = False Positive Rate

156,200 Suspect Accounts - 560 Deposit Frauds = 155,640 Good Accounts

155,640 Goods ÷ 156,200 Total Suspects = 99.7% False Positive Rate

Loss Avoidance Total: $19M – Charge Off Total: $2.2M

Daily Average Suspect Volume:620/5 FTE = 125 Accounts/FTE

Determining Your “False Positive Rate” & “Fraud Detection Rate”

FraudLink Deposit “False Positive Ratio”

FraudLink Deposit Suspect Accounts ÷ FraudLink Deposit Fraud Accounts = False Positive Ratio

156,200 Suspect Accounts ÷ 560 Deposit Fraud Accounts = 278:1 Ratio

One Deposit Fraud for Every 278 Suspect Accounts

Determining Your “False Positive Rate” & “Fraud Detection Rate”

FraudLink On-Us “Fraud Detection Rate” Dollars

On-Us Fraud Dollars Charged Off + FraudLink On-Us Fraud Dollars Detected = Total On-Us Check Fraud Dollars Exposure

$400K Charged Off + $4.4 Detected = $4.8M Total Fraud Exposure

FraudLink On-Us Fraud Dollars Detected ÷ Total Dollars Exposure = Fraud Dollars Detection Rate

$4.4M Detected ÷ $4.8 Exposure = 92% Fraud Dollars Detection Rate

Determining Your “False Positive Rate” & “Fraud Detection Rate”

FraudLink On-Us “Fraud Detection Rate” Items

On-Us Fraud Items Charged Off + FraudLink On-Us Fraud items Detected = Total On-Us Check Fraud Items Exposure

670 items Charged Off + 1,360 items Detected = 2,030 Total Items Exposure

FraudLink On-Us Items Detected ÷ Total Items Exposure = Fraud Items Detection Rate

1,360 Detected ÷ 2,030 Exposure = 70% Fraud Items Detection Rate

Determining Your “False Positive Rate” & “Fraud Detection Rate”

FraudLink Deposit “Fraud Detection Rate” Dollars

Deposit Fraud Dollars Charged Off + FraudLink Deposit Dollars Detected = Total Deposit Fraud Dollars Exposure

$2.2M Charged Off + $19M Detected = $21.2M Total Fraud Exposure

FraudLink Deposit Dollars Detected ÷ Total Dollars Exposure = Fraud Detection Rate

$19M Detected ÷ $21.2 Exposure = 90% Fraud Detection Rate

Determining Your “False Positive Rate” & “Fraud Detection Rate”

FraudLink Deposit “Fraud Detection Rate” Accounts

Deposit Fraud Accounts Charged Off + FraudLink Deposit Accounts Detected = Total Deposit Fraud Accounts Exposure

250 Accounts Charged Off + 560 Accounts Detected = 810 Total Accounts Exposure

FraudLink Deposit Accounts Detected ÷ Total Accounts Exposure = Fraud Detection Rate

560 Detected ÷ 810 Exposure = 69% Fraud Account Detection Rate

Determining Your “False Positive Rate” & “Fraud Detection Rate”

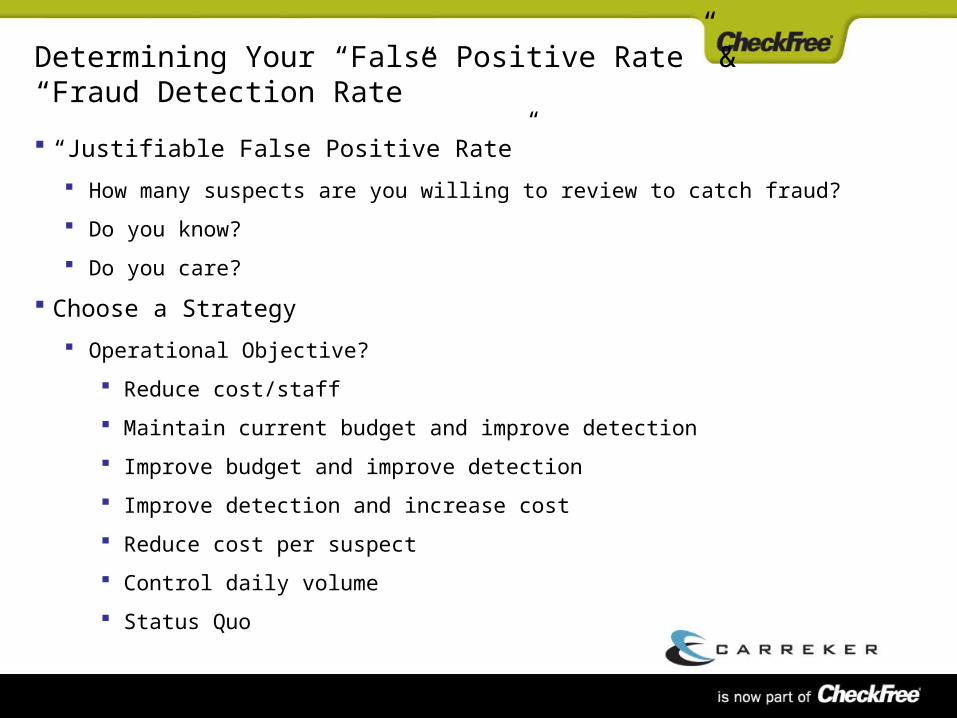

“Justifiable False Positive Rate”

How many suspects are you willing to review to catch fraud?

Do you know?

Do you care?

Choose a Strategy

Operational Objective?

Reduce cost/staff

Maintain current budget and improve detection

Improve budget and improve detection

Improve detection and increase cost

Reduce cost per suspect

Control daily volume

Status Quo

Determining Your “False Positive Rate” & “Fraud Detection Rate”

Baseline measurements?

Average number of suspects per day

Average number of false positives

Average number of frauds observed per period

Average number of “false negatives” observed per period

“False negative” losses that failed to appear on Suspect Report

Detection rate observed per period

No “One Size Fits All” Solution

Decision up to each individual bank

FraudLink System Reports: Data Collection & Analysis

Understanding FraudLink Suspect Distribution

FraudLink On-Us Back Office Summary Report

Produces Daily Reports

Bank

Group

Account Type

Reason/Rule

Number Checks/Accounts

Grand Total

Average Suspect Activity

Observe the distribution of Suspects across all Account Types and Reason/Rule

FraudLink System Reports: Data Collection & Analysis

DATE: 01/16/2002 08:37 CARREKER FRAUDLINK ON-US FRAUD DETECTION SYSTEM A16RPT04POSTED DATE : 01/15/2002 BACK OFFICE SUMMARY REPORT CONTAINING ITEMS FROM ALL SOURCES PAGE 12

GRAND TOTALS REASON CHECKS ACCOUNTS AMOUNT

DUPLICATE SERIAL NUMBER 14 8 $18,302.02SERIAL NUMBER OUT OF RANGE 102 65 $371,305.26AMOUNT GREATER THAN AVERAGE 34 29 $1,976,687.96AMOUNT EXCEEDS LARGEST ON FILE 21 19 $412,938.72NO HISTORY FOR ACCOUNT 4 4 $3,528.50NO HISTORY FOR NEW ACCOUNT 2 1 $4,326.42MISSING SERIAL NUMBER 17 9 $31,177.61LOW DOLLAR CHECK PULL 148 148 $384,295.54LOWEST CHECK NUMBER ON FILE 9 8 $12,200.17VELOCITY BACK OFFICE 4 2 $1,540.80BRANCH VELOCITY 0 0 $0.00BRANCH DUPLICATE SERIAL 10 3 $8,339.44DUPLICATE AMOUNT 24 8 $14,765.21SERIAL NUMBER IN NEW CHECK RANGE 0 0 $0.00HIGH DOLLAR 98 69 $3,463,688.35DUPLICATE SERIAL AND AMOUNT 0 0 $0.00EXCEEDED DOLLAR THRESHOLD 0 0 $0.00PAYEE VELOCITY 0 0 $0.00SUSPECT ONLY ITEMS 204 117 $3,315,609.02COMPANION ONLY ITEMS 108 108 $29,477.99SUSPECT COMPANION ITEMS 40 40 $354,817.55

FRAUD ANALYSIS HAS FLAGGED 352 CHECKS FOR 153 ACCOUNTS WITH A TOTAL VALUE OF 3,699,904.56 FOR THIS DAYS WORK

DATE: 01/16/2002 08:37 CARREKER FRAUDLINK ON-US FRAUD DETECTION SYSTEM A16RPT04POSTED DATE : 01/15/2002 BACK OFFICE SUMMARY REPORT CONTAINING ITEMS FROM ALL SOURCES PAGE 12

GRAND TOTALS REASON CHECKS ACCOUNTS AMOUNT

DUPLICATE SERIAL NUMBER 14 8 $18,302.02SERIAL NUMBER OUT OF RANGE 102 65 $371,305.26AMOUNT GREATER THAN AVERAGE 34 29 $1,976,687.96AMOUNT EXCEEDS LARGEST ON FILE 21 19 $412,938.72NO HISTORY FOR ACCOUNT 4 4 $3,528.50NO HISTORY FOR NEW ACCOUNT 2 1 $4,326.42MISSING SERIAL NUMBER 17 9 $31,177.61LOW DOLLAR CHECK PULL 148 148 $384,295.54LOWEST CHECK NUMBER ON FILE 9 8 $12,200.17VELOCITY BACK OFFICE 4 2 $1,540.80BRANCH VELOCITY 0 0 $0.00BRANCH DUPLICATE SERIAL 10 3 $8,339.44DUPLICATE AMOUNT 24 8 $14,765.21SERIAL NUMBER IN NEW CHECK RANGE 0 0 $0.00HIGH DOLLAR 98 69 $3,463,688.35DUPLICATE SERIAL AND AMOUNT 0 0 $0.00EXCEEDED DOLLAR THRESHOLD 0 0 $0.00PAYEE VELOCITY 0 0 $0.00SUSPECT ONLY ITEMS 204 117 $3,315,609.02COMPANION ONLY ITEMS 108 108 $29,477.99SUSPECT COMPANION ITEMS 40 40 $354,817.55

FRAUD ANALYSIS HAS FLAGGED 352 CHECKS FOR 153 ACCOUNTS WITH A TOTAL VALUE OF 3,699,904.56 FOR THIS DAYS WORK

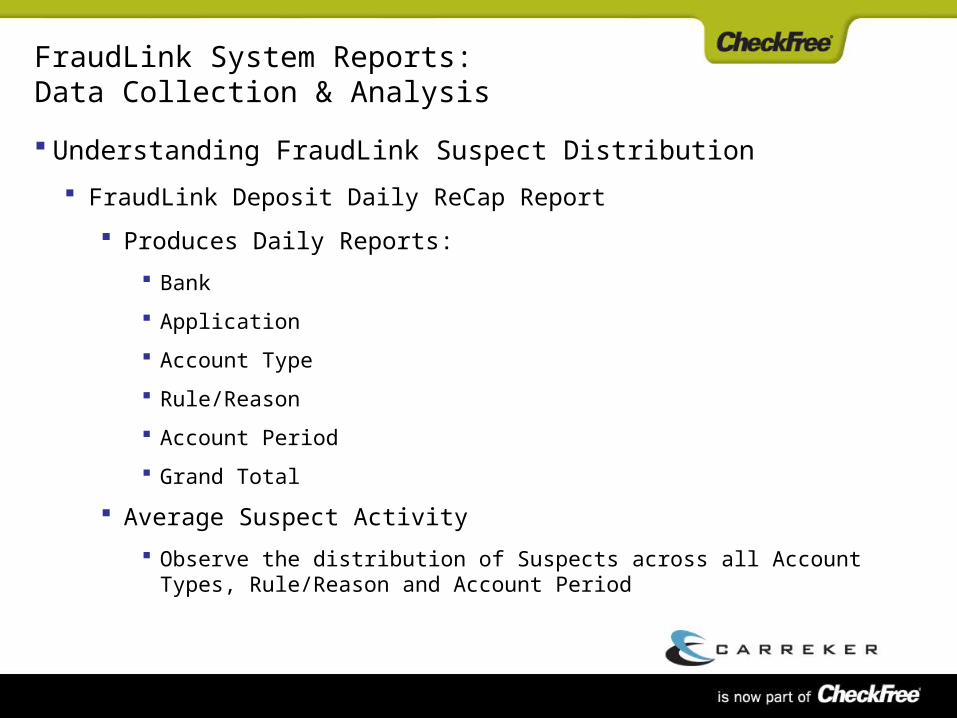

FraudLink System Reports: Data Collection & Analysis

Understanding FraudLink Suspect Distribution

FraudLink Deposit Daily ReCap Report

Produces Daily Reports:

Bank

Application

Account Type

Rule/Reason

Account Period

Grand Total

Average Suspect Activity

Observe the distribution of Suspects across all Account Types, Rule/Reason and Account Period

FraudLink System Reports: Data Collection & Analysis

Fraud Detection/Fraud Losses: Data Collection & Analysis

Collect, Sort and Stratify Your On-Us Detection and Loss Data

On-Us Fraud Analysis

Geographical Risk

Product Risk

FraudLink Suspect Rule

Loss Avoidance Amount

Loss Amount – FraudLink Suspect Y/N

Return Reason

Understand Your Entire Risk Exposure

What’s working

What’s not working

Where changes are needed

Fraud Detection/Fraud Losses: Data Collection & Analysis

Collect, Sort and Stratify Your Deposit Detection and Loss Data

Deposit Fraud Analysis

Geographical Risk

Product Risk

Age of Account Risk – FraudLink Account Periods

FraudLink Suspect Rule

Deposit Amount

Loss Avoidance Amount

Loss Amount – FraudLink Suspect Y/N

RDI Reason

Understand Your Entire Risk Exposure

What’s working

What’s not working

Where changes are needed

“Fraud Profile”: Identifying Current & Emerging Fraud Activity “Fraud Profile”

Current Trends – Commonality

Common Fraud Amounts

Common Bank Products

Common Geographic's

Common Account Age

Common Detection & Failures

In-clearing vs. Teller Cashed

Emerging Fraud – Un-Commonality

New Fraud Amounts

Fraud Below Current FraudLink System Settings

New Bank Products

New Geographic’s

New Account Ages

Fraud Moving From Paper to other Delivery Channels

Risk-Based Re-Calibration: Targeting Your “Fraud Profile”

Where is the Fraud Risk?

FraudLink On-Us

Product – Commercial DDA

Amounts - $375.00 - $998.00 & $4,800 - $9,900

Detection – Rule 2 Serial Number Out of Range-83% & Rule 1 Duplicate Serial Number-12%

Determine “False Negatives”

Where isn’t the Fraud Risk?

FraudLink On-Us

Product – Senior 50+ DDA & MMDDA

Amounts < $374.00

Detection – Rule 3 Amount Greater Than Average & Rule 13 Duplicate Check Amounts

Determine “False Negatives”

Risk-Based Re-Calibration: Targeting Your “Fraud Profile”

Where is the Fraud Risk?

FraudLink Deposit

Product – Free Personal DDA & Internet Free Personal DDA

Amounts – Account Period 1: $2,000 - $5,500 Account Period 3: $35,000 - $425,000

Detection – Rule 1 Daily Total Above Average-88% & Rule 5 Invalid Routing & Transit Number-9%

Region – 1 & 2

Where isn’t the Fraud Risk?

FraudLink Deposit

Product – Commercial DDA & Public Funds Accounts

Amounts < $1,000

Detection – Rule 8 Deposit Velocity Exceeds Average & Rule 6 Duplicate Items Amounts

Region – 6 & 8

Risk-Based Re-Calibration: Targeting Your “Fraud Profile”

What Have We Learned?

False Positive Rate

False Negative Rate

Fraud Detection Rate

“Justifiable False Positive”

FraudLink Suspect Volume Distribution

Fraud Exposure Distribution

Fraud Profile

Common Fraud Trends

Emerging Fraud Trends

Where Your Fraud Is

Risk-Based Re-Calibration: Targeting Your “Fraud Profile”

Re-Calibration Set and balance Rules and Parameters

Target highest Fraud Risk activity

Generate More Suspects that Provide the Greatest Value

Generate Less Suspects Where Fraud is Least Likely

Results

More Fraud Detection

Less False Negatives

Less False Positives

Happier Employees

What You Might Find…

A need to generate more Suspects than current staff can handle

Business case for added staff with significant payback

Need for full-time Business Analyst to collect and analyze data and conduct re-calibration testing

Questions?

Q: I don’t have the staff to do all of this, is there an automated way to collect this data?

A: Yes, CORE Workflow Manager & Syfact Case Management System

Q: Can Carreker/CheckFree help?

A: Yes, we provide consulting and re-calibration services, check with your Account Representative.

Now Your Questions!

Closing Remarks

Jeff Botari, CheckFree