riskminds - did basel & iosco put the final nail in the coffin of csa-discounting?

TRANSCRIPT

Did Basel & IOSCO put the final nail in the

coffin of CSA-Discounting ?

Amsterdam – December 10th, 2014

Alexandre Bon, Murex

FVA in presence of imperfect collateralisation, IMs and variable funding spreads

Copyright © 2014 Murex S.A.S. All rights reserved 2

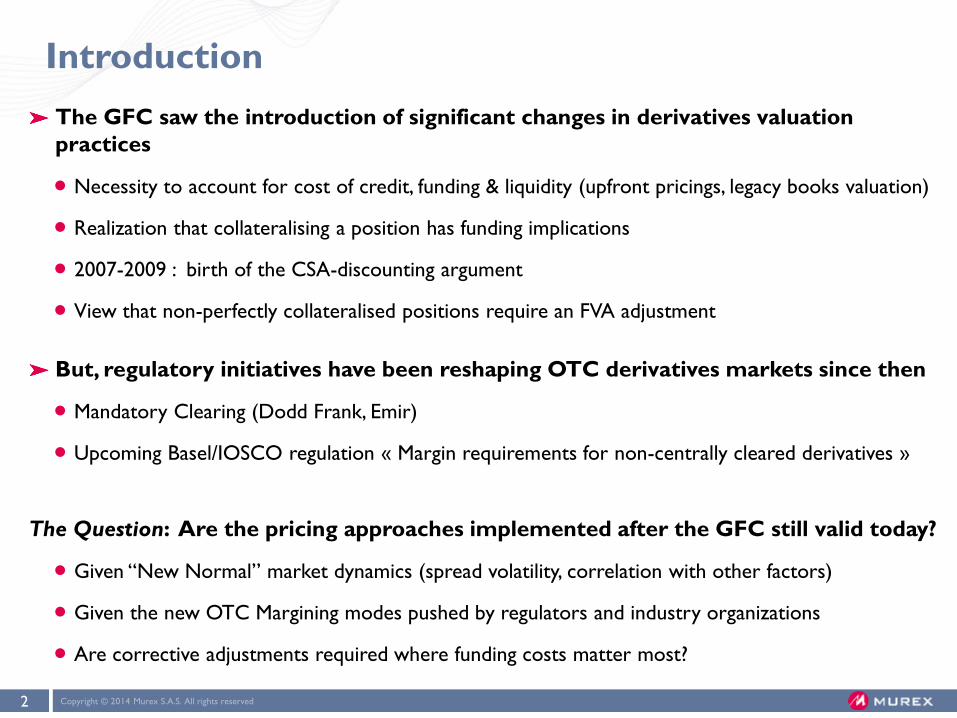

Introduction

The GFC saw the introduction of significant changes in derivatives valuation

practices

Necessity to account for cost of credit, funding & liquidity (upfront pricings, legacy books valuation)

Realization that collateralising a position has funding implications

2007-2009 : birth of the CSA-discounting argument

View that non-perfectly collateralised positions require an FVA adjustment

But, regulatory initiatives have been reshaping OTC derivatives markets since then

Mandatory Clearing (Dodd Frank, Emir)

Upcoming Basel/IOSCO regulation « Margin requirements for non-centrally cleared derivatives »

The Question: Are the pricing approaches implemented after the GFC still valid today?

Given “New Normal” market dynamics (spread volatility, correlation with other factors)

Given the new OTC Margining modes pushed by regulators and industry organizations

Are corrective adjustments required where funding costs matter most?

Agenda

1. PRICING FUNDING COSTS AFTER THE CRISIS

2. COMPETING FVA MODELS : CSA-DISCOUNTING & EXPOSURE SIMULATION

3. WHICH FVA MODELS ARE STILL VALID NOW?

CONSIDERING POST-CRISIS SPREADS DYNAMICS

GIVEN THE IMPACT NEW REGULATORY DEVELOPMENTS (EMIR, BASEL/IOSCO…) ON

COLLATERALISATION REGIMES

4. ONE POSSIBLE FVA OPERATING MODEL

Copyright © 2014 Murex S.A.S. All rights reserved 4

Justification for a funding adjustment

Unsecured derivatives positions

Future cash flow assets (liabilities) are term-funded by borrowing on an unsecured

basis and investing (borrowing) in a “risk-free” money market account that will pay

back the required amount at maturity.

i.e. the value of this derivative can be obtained by :

Discounting future cash-flows on our own unsecured funding curve (term-funding).

Equivalently, the integral of future MtMs discounted with our unsecured funding spread gives

the valuation adjustment that can be subtracted from the “risk-free” price to derive our

economic value for this transaction

Other argument : the unsecured derivatives is hedged by a collateralised one

Copyright © 2014 Murex S.A.S. All rights reserved 5

Justification for a funding adjustment

Collateralised derivatives positions

When the value of the position 𝑉(𝑡) is positive we effectively borrow the collateral

amount 𝐶(𝑡) at the collateral rate 𝑟𝑖𝑠𝑘 𝑓𝑟𝑒𝑒 + 𝑆𝑐𝑜𝑙𝑙𝑎𝑡 and fund the remaining shortfall

excess 𝑉 𝑡 − 𝐶 𝑡 at our cost of funds (and vice versa).

The collateral rate is the interest rate specified in the agreement, when exchanging

cash collateral, the funding cost/benefit is thus the combination of:

𝐶(𝑡) at the collateral spread 𝑆𝑐𝑜𝑙𝑙𝑎𝑡

𝑉 𝑡 − 𝐶 𝑡 + at the unsecured borrowing spread 𝑆𝑏𝑜𝑟𝑟𝑜𝑤

𝐶 𝑡 − 𝑉 𝑡 − at the unsecured lending spread 𝑆𝑙𝑒𝑛𝑑

Assuming continuous collateralisation 𝑉 𝑡 = 𝐶(𝑡) : cash flows can be discounted on

the collateral rate (CSA-discounting)

Usually the collateral rate is an OIS index which is also the benchmark for repos and

our “risk-free” money market account.

Under these ideal hypotheses : FVA = 0

Copyright © 2014 Murex S.A.S. All rights reserved 6

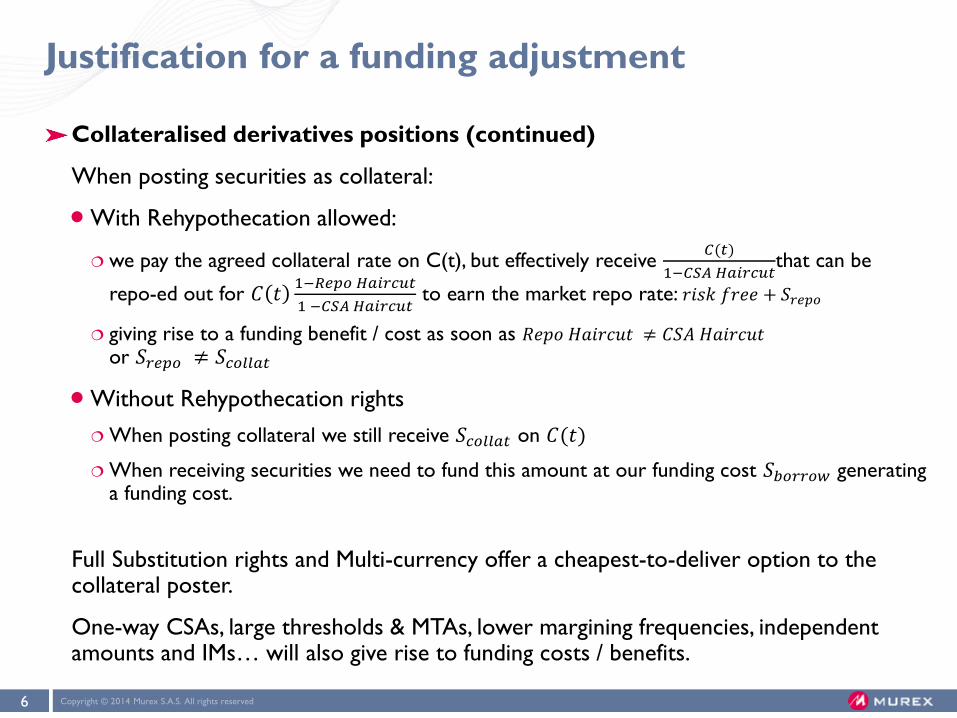

Justification for a funding adjustment

Collateralised derivatives positions (continued)

When posting securities as collateral:

With Rehypothecation allowed:

we pay the agreed collateral rate on C(t), but effectively receive 𝐶(𝑡)

1−𝐶𝑆𝐴 𝐻𝑎𝑖𝑟𝑐𝑢𝑡that can be

repo-ed out for 𝐶 𝑡1−𝑅𝑒𝑝𝑜 𝐻𝑎𝑖𝑟𝑐𝑢𝑡

1 −𝐶𝑆𝐴 𝐻𝑎𝑖𝑟𝑐𝑢𝑡 to earn the market repo rate: 𝑟𝑖𝑠𝑘 𝑓𝑟𝑒𝑒 + 𝑆𝑟𝑒𝑝𝑜

giving rise to a funding benefit / cost as soon as 𝑅𝑒𝑝𝑜 𝐻𝑎𝑖𝑟𝑐𝑢𝑡 ≠ 𝐶𝑆𝐴 𝐻𝑎𝑖𝑟𝑐𝑢𝑡 or 𝑆𝑟𝑒𝑝𝑜 ≠ 𝑆𝑐𝑜𝑙𝑙𝑎𝑡

Without Rehypothecation rights

When posting collateral we still receive 𝑆𝑐𝑜𝑙𝑙𝑎𝑡 on 𝐶(𝑡)

When receiving securities we need to fund this amount at our funding cost 𝑆𝑏𝑜𝑟𝑟𝑜𝑤 generating a funding cost.

Full Substitution rights and Multi-currency offer a cheapest-to-deliver option to the collateral poster.

One-way CSAs, large thresholds & MTAs, lower margining frequencies, independent amounts and IMs… will also give rise to funding costs / benefits.

Agenda

1. PRICING FUNDING COSTS AFTER THE CRISIS

2. COMPETING FVA MODELS : CSA-DISCOUNTING & EXPOSURE SIMULATION

3. WHICH FVA MODELS ARE STILL VALID NOW?

CONSIDERING POST-CRISIS SPREADS DYNAMICS

GIVEN THE IMPACT NEW REGULATORY DEVELOPMENTS (EMIR, BASEL/IOSCO…)

ON COLLATERALISATION REGIMES

4. ONE POSSIBLE FVA OPERATING MODEL

Copyright © 2014 Murex S.A.S. All rights reserved 8

The CSA-discounting argument & assumptions

Uncollateralised trades are priced by discounting Cash Flows on a curve representing

our cost of fund (usually Libor + spread).

Collateralised trades are priced by discounting Cash Flows on a curve representing

the collateral rate (usually OIS rate of a specified currency).

Implicit assumptions:

Transactions are held to maturity and term-funded

For each 𝑡 there is a single funded amount 𝑉(𝑡) and a single funding rate 𝑆𝑏𝑜𝑟𝑟𝑜𝑤 or 𝑆𝑐𝑜𝑙𝑙𝑎𝑡

Following hypotheses regarding the margining process and market dynamics:

1. Strong “ideal CSA” assumptions :

Bilateral & continuous margining

Cash equivalent collateral

0-thresholds

No MTAs, Rounding, IAs and … No IMs

Full substitution and re-hypothecation rights

2. Funding spreads are :

Symmetrical (lending = borrowing)

Fixed (and obviously independent from

exposure drivers)

Copyright © 2014 Murex S.A.S. All rights reserved 9

CSA-discounting has become market practice

Intuitive trade-level method, now widely used as the pricing approach on FO desks.

Usual consensus that, so far, the “ideal CSA” assumption has worked for the bulk

of interbank portfolios on “classical” CSAs and for uncollateralised positions as

well.

ISDA Margin Survey 2014 [17]

This year, 66% of participants indicated they were referencing terms contained within their

underlying CSAs when pricing derivatives transactions for collateral margining (CSA-discounting).

Copyright © 2014 Murex S.A.S. All rights reserved 10

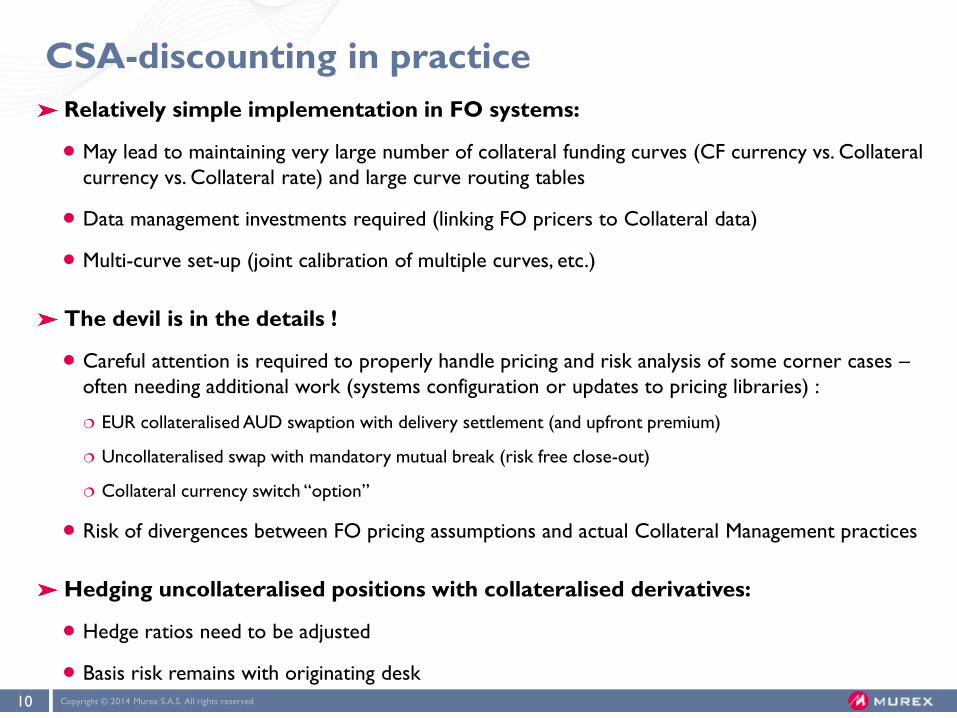

CSA-discounting in practice

Relatively simple implementation in FO systems:

May lead to maintaining very large number of collateral funding curves (CF currency vs. Collateral

currency vs. Collateral rate) and large curve routing tables

Data management investments required (linking FO pricers to Collateral data)

Multi-curve set-up (joint calibration of multiple curves, etc.)

The devil is in the details !

Careful attention is required to properly handle pricing and risk analysis of some corner cases –

often needing additional work (systems configuration or updates to pricing libraries) :

EUR collateralised AUD swaption with delivery settlement (and upfront premium)

Uncollateralised swap with mandatory mutual break (risk free close-out)

Collateral currency switch “option”

Risk of divergences between FO pricing assumptions and actual Collateral Management practices

Hedging uncollateralised positions with collateralised derivatives:

Hedge ratios need to be adjusted

Basis risk remains with originating desk

Copyright © 2014 Murex S.A.S. All rights reserved 11

Reminder: CVA & FVA definition

CVA & DVA

CVA is the market value of counterparty credit risk for OTC derivatives (or the difference

between the risk-free price and the mid-market price of the portfolio).

Expectation over time of discounted future exposures weighted by default probabilities and

recoveries.

FVA

Similarly FVA aims to capture the funding costs (FCA) and benefits (FBA) incurred on derivatives

transactions due to timing mismatches between inflows and outflows that would be financed at

unsecured rates.

Integral over time of Funded Amounts weighted by the corresponding Funding Spreads.

Under the CSA-discounting assumptions, FVA is the difference in value obtained by discounting

cash flows on their relevant funding curves vs. a reference “risk-free” curve (OIS).

As funding spreads contain a credit risk element and funded amounts can correspond (not

always) to discounted exposure, there are definite overlaps between bilateral CVA and FVA (esp.

FBA and DVA).

Copyright © 2014 Murex S.A.S. All rights reserved 12

FVA via Exposure Simulation

The second approach consists in extending the CVA simulation framework to

price FVA at the portfolio level:

All trades are discounted on their relevant “risk-free” OIS benchmark for pricing, regardless of the

collateral agreement details

Exposures and Collateral balances are simulated explicitly taking into account the full details of the

collateral agreement (coverage, thresholds, collateral currency, haircuts, IMs, etc.)

FVA is measured by taking the integral of discounted exposures/liabilities weighted by the

appropriate funding spreads (if desired, different rates can be applied for the lending & borrowing

cases).

This approach offers improved modeling flexibility but at the cost of added

computational complexity (akin to the simulation model for CVA/DVA).

By isolating the “funding component” of the price, this method:

lends itself well to centralised management and internal transfer pricing (FVA desk)

preserves hedge ratios between collateralised and uncollateralised positions.

Copyright © 2014 Murex S.A.S. All rights reserved 13

FVA Simulation Principles

Funding spreads are measured between the effective Collateral rate and the chosen

reference risk-free funding rate

Similar to the CSA-discounting case, with the option of also evolving spreads as a stochastic risk

factor

Behavioural assumptions can be made regarding the :

Counterparty's choice of collateral assets (currency switch option, cash/securities mix).

Assumed funding lifetime of the positions.

Effective rehypothecation ratio / repo haircuts of illiquid securities (RMBS, corporate / municipal

bonds, etc.) and counterparty’s own bonds on stressed scenarios.

FVA can be simply split into sub-components:

FBA vs. FVA

FVA, LVA, CollVA, IMVA… (e.g. separating CDS-Bond basis liquidity spread from the credit spread, or

isolating the funding component due to collateral excesses/shortfalls).

P&L attribution elements

Copyright © 2014 Murex S.A.S. All rights reserved 14

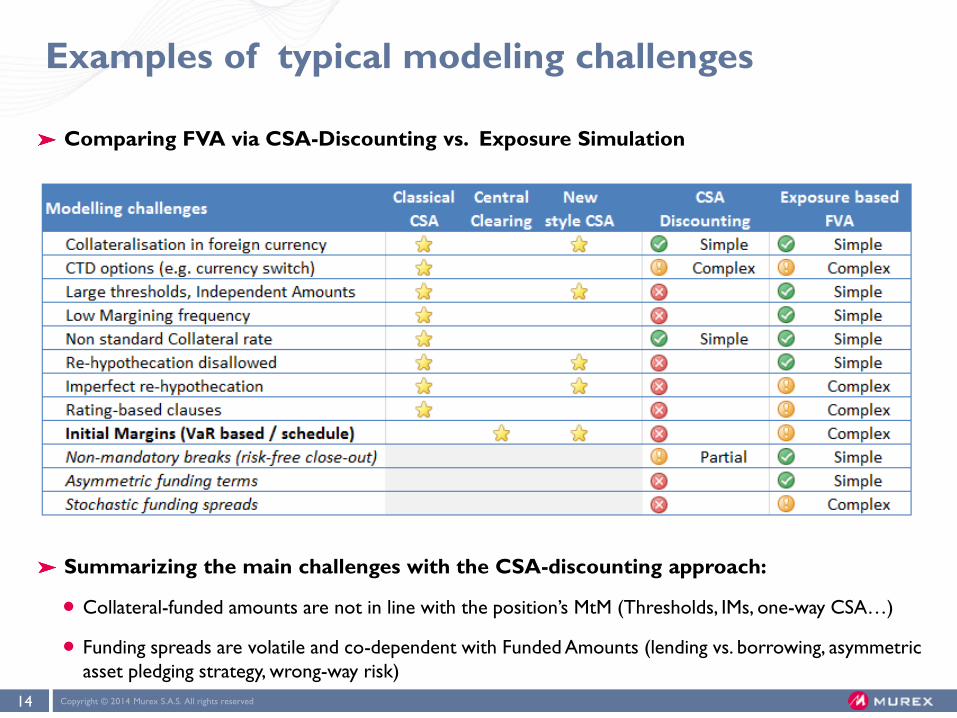

Examples of typical modeling challenges

Comparing FVA via CSA-Discounting vs. Exposure Simulation

Summarizing the main challenges with the CSA-discounting approach:

Collateral-funded amounts are not in line with the position’s MtM (Thresholds, IMs, one-way CSA…)

Funding spreads are volatile and co-dependent with Funded Amounts (lending vs. borrowing, asymmetric

asset pledging strategy, wrong-way risk)

Copyright © 2014 Murex S.A.S. All rights reserved 15

Is CSA-discounting still a valid pricing method ?

The question is whether a CSA-discounting approach alone can be used to

price incrementally without the risk of providing distorted incentives:

Depends on the portfolio in place (transactions and agreements) and magnitude of the

impacts.

E.g. if clearing of a given product can happen only on a single CCP.

Option to fix some of the CSA-discounting shortfalls by fiddling with the pricing and

curve libraries.

Strong intuition that aggregation-dependent effects (VaR-based IMs, one-way CSAs)

should be modeled upfront

Whether the volatility of spreads and their correlation with exposure factors can have

a material impact is less clear (apart from obvious pathological cases)

Agenda

1. PRICING FUNDING COSTS AFTER THE CRISIS

2. COMPETING FVA MODELS : CSA-DISCOUNTING & EXPOSURE SIMULATION

3. WHICH FVA MODELS ARE STILL VALID NOW?

CONSIDERING POST-CRISIS SPREADS DYNAMICS

GIVEN THE IMPACT NEW REGULATORY DEVELOPMENTS (EMIR, BASEL/IOSCO…)

ON COLLATERALISATION REGIMES

4. ONE POSSIBLE FVA OPERATING MODEL

Copyright © 2014 Murex S.A.S. All rights reserved 17

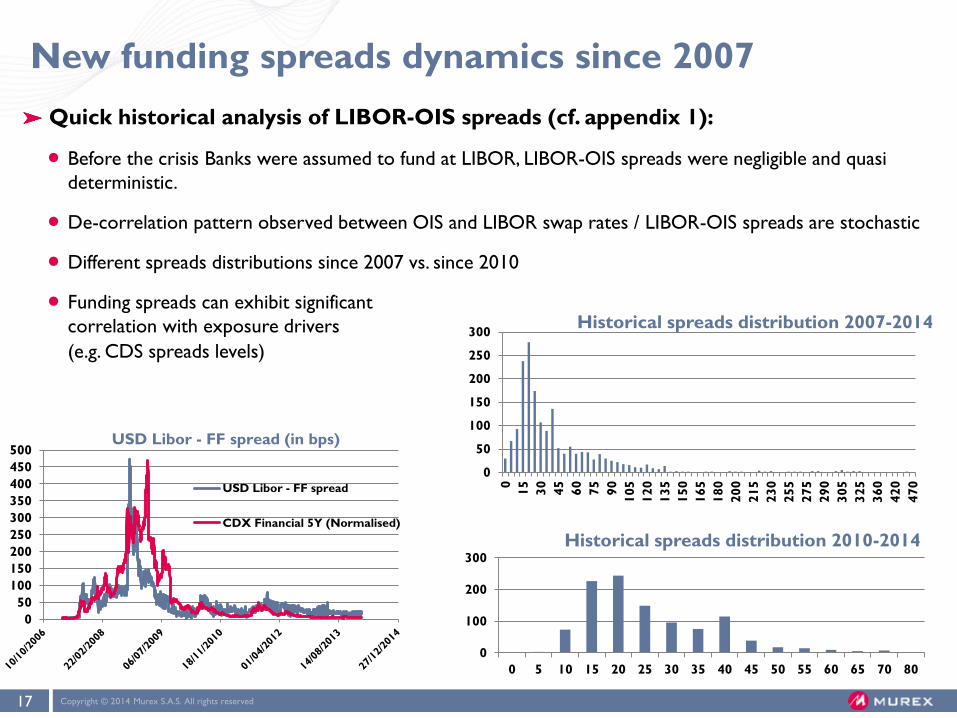

New funding spreads dynamics since 2007

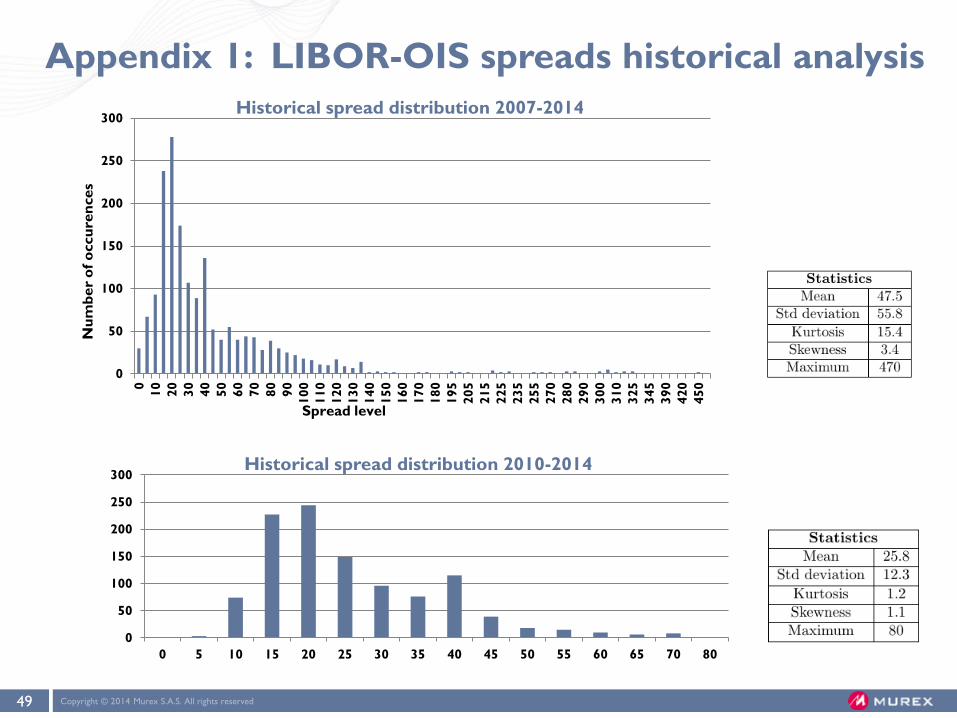

Quick historical analysis of LIBOR-OIS spreads (cf. appendix 1):

Before the crisis Banks were assumed to fund at LIBOR, LIBOR-OIS spreads were negligible and quasi

deterministic.

De-correlation pattern observed between OIS and LIBOR swap rates / LIBOR-OIS spreads are stochastic

Different spreads distributions since 2007 vs. since 2010

Funding spreads can exhibit significant

correlation with exposure drivers

(e.g. CDS spreads levels)

0

50

100

150

200

250

300

350

400

450

500

USD Libor - FF spread

CDX Financial 5Y (Normalised)

USD Libor - FF spread (in bps)

0

50

100

150

200

250

300

0

15

30

45

60

75

90

105

120

135

150

165

180

200

215

230

255

275

290

305

325

360

420

470

Historical spreads distribution 2007-2014

0

100

200

300

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 80

Historical spreads distribution 2010-2014

Copyright © 2014 Murex S.A.S. All rights reserved 18

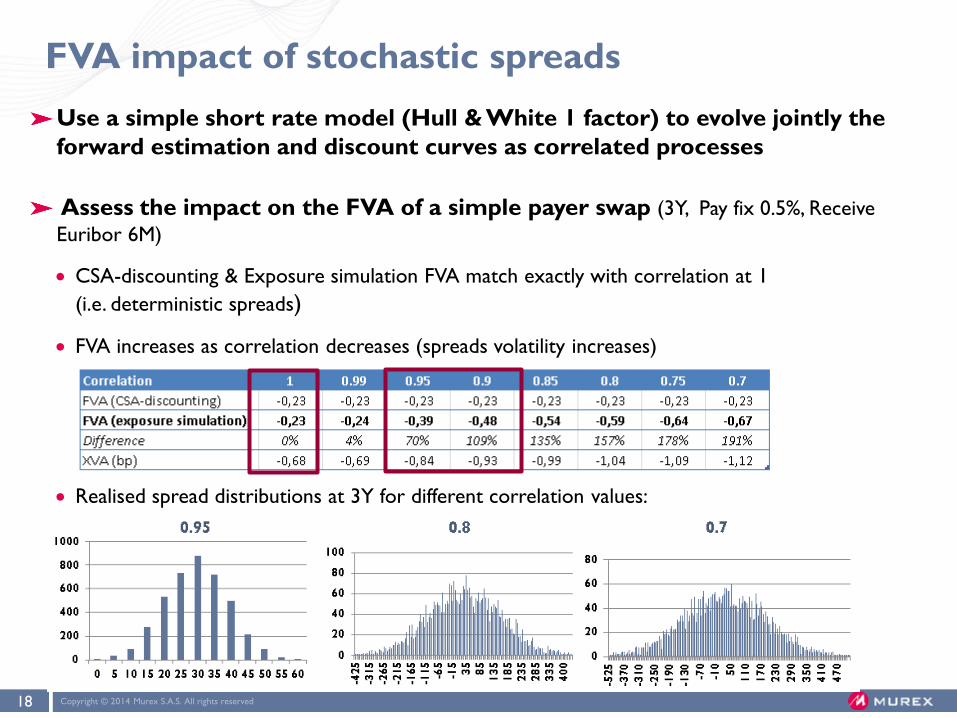

FVA impact of stochastic spreads

Use a simple short rate model (Hull & White 1 factor) to evolve jointly the

forward estimation and discount curves as correlated processes

Assess the impact on the FVA of a simple payer swap (3Y, Pay fix 0.5%, Receive

Euribor 6M)

CSA-discounting & Exposure simulation FVA match exactly with correlation at 1

(i.e. deterministic spreads)

FVA increases as correlation decreases (spreads volatility increases)

Realised spread distributions at 3Y for different correlation values:

Copyright © 2014 Murex S.A.S. All rights reserved 19

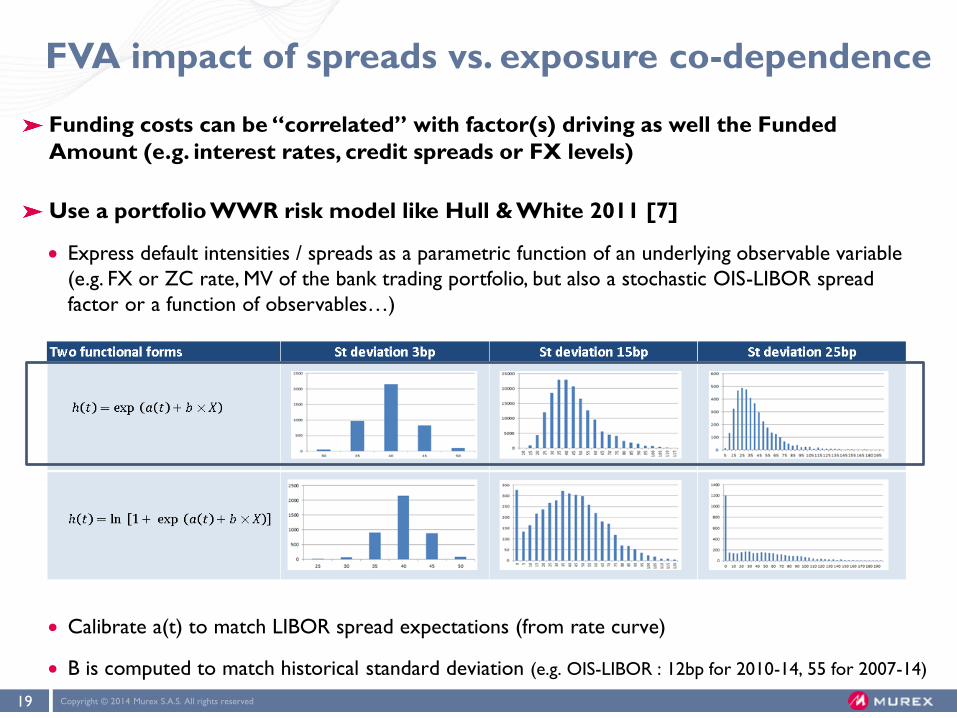

FVA impact of spreads vs. exposure co-dependence

Funding costs can be “correlated” with factor(s) driving as well the Funded

Amount (e.g. interest rates, credit spreads or FX levels)

Use a portfolio WWR risk model like Hull & White 2011 [7]

Express default intensities / spreads as a parametric function of an underlying observable variable

(e.g. FX or ZC rate, MV of the bank trading portfolio, but also a stochastic OIS-LIBOR spread

factor or a function of observables…)

Calibrate a(t) to match LIBOR spread expectations (from rate curve)

B is computed to match historical standard deviation (e.g. OIS-LIBOR : 12bp for 2010-14, 55 for 2007-14)

Copyright © 2014 Murex S.A.S. All rights reserved 20

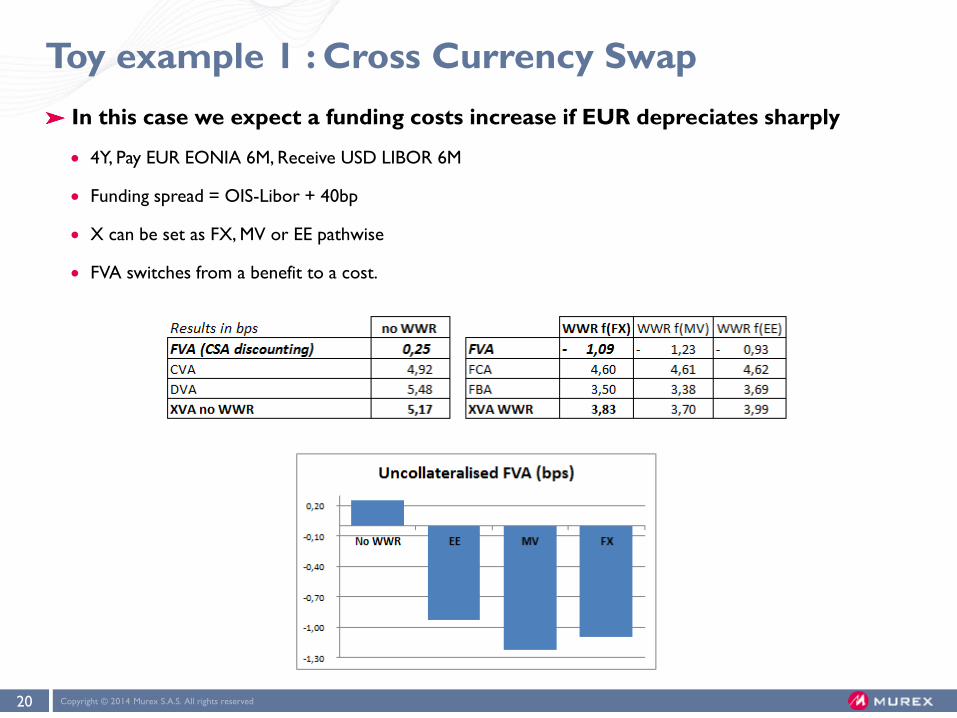

Toy example 1 : Cross Currency Swap

In this case we expect a funding costs increase if EUR depreciates sharply

4Y, Pay EUR EONIA 6M, Receive USD LIBOR 6M

Funding spread = OIS-Libor + 40bp

X can be set as FX, MV or EE pathwise

FVA switches from a benefit to a cost.

Copyright © 2014 Murex S.A.S. All rights reserved 21

Real-life examples of FVA WWR/RWR

SSAs hedging bonds issuances:

Long-Term IRD positions with One-way CSAs

Alternatively the Counterparty posts their Own Bond as Collateral : no reduction of CVA.

Recover funding benefit in normal market conditions, but funding benefit may vanish in stressed market (inability to

repo large positions, rising haircuts…)

Selling structured products hedges to Corporates

Local bank selling structure back-to-back : uncollateralised with corporate, collateralised with hedge counterparty

(e.g. TARFS, TARNS, Accumulators, PRDCs…)

Hedging products, hence often believed to carry no CVA WWR, or even be Right Way positions

Often packaged as 0-premium notes:

Attractive rate for customer (e.g; carry trade, ITM options), but with limited upside (target redemption or KO)

Reverse position for the bank knocking in at OTM level, often with gearing

Competitive markets (very popular products can turn into crowded trades)

Very asymmetric pay-offs : potential for high funding requirements, and specific WWR (gearing and one-way market)

Local banks funding spreads can be strongly correlated to large moves in the underlying asset price

Copyright © 2014 Murex S.A.S. All rights reserved 22

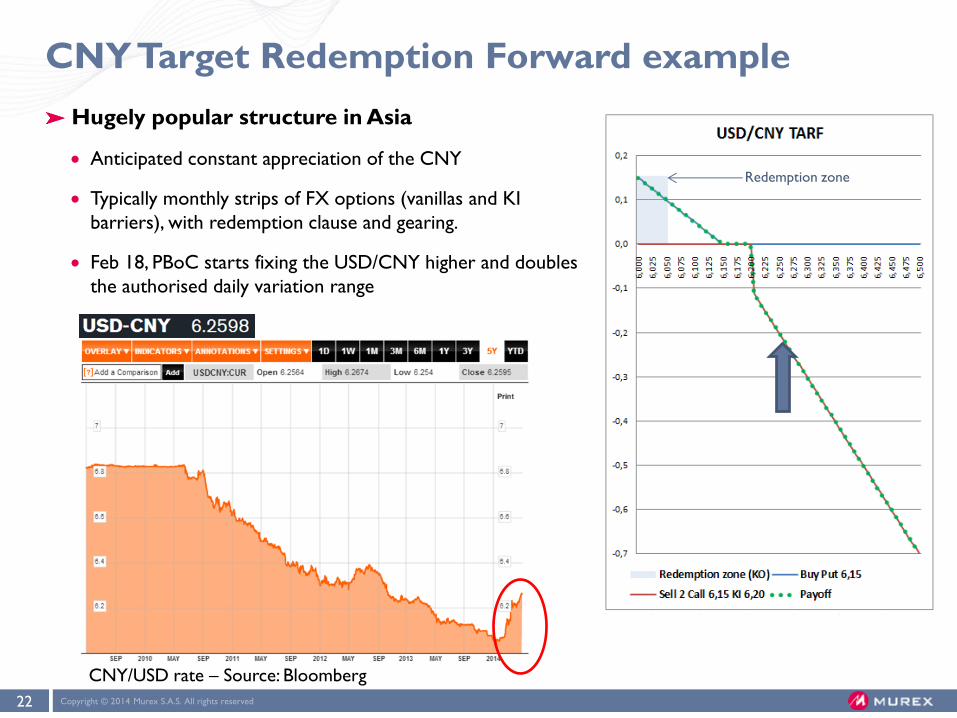

CNY Target Redemption Forward example

CNY/USD rate – Source: Bloomberg

Hugely popular structure in Asia

Anticipated constant appreciation of the CNY

Typically monthly strips of FX options (vanillas and KI

barriers), with redemption clause and gearing.

Feb 18, PBoC starts fixing the USD/CNY higher and doubles

the authorised daily variation range

Redemption zone

Copyright © 2014 Murex S.A.S. All rights reserved 23

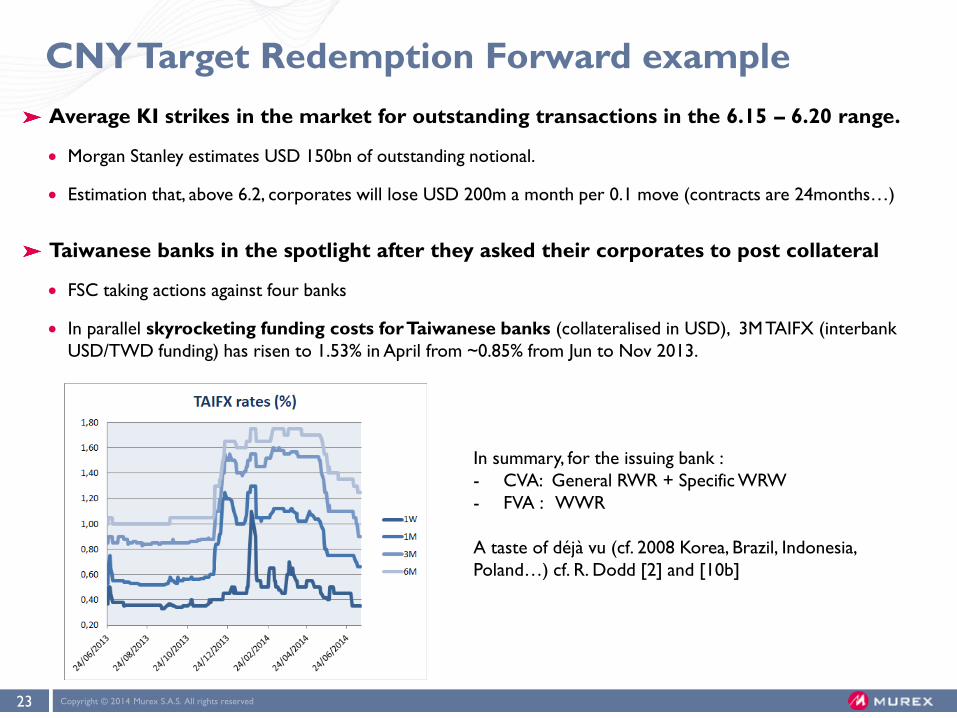

CNY Target Redemption Forward example

Average KI strikes in the market for outstanding transactions in the 6.15 – 6.20 range.

Morgan Stanley estimates USD 150bn of outstanding notional.

Estimation that, above 6.2, corporates will lose USD 200m a month per 0.1 move (contracts are 24months…)

Taiwanese banks in the spotlight after they asked their corporates to post collateral

FSC taking actions against four banks

In parallel skyrocketing funding costs for Taiwanese banks (collateralised in USD), 3M TAIFX (interbank

USD/TWD funding) has risen to 1.53% in April from ~0.85% from Jun to Nov 2013.

In summary, for the issuing bank :

- CVA: General RWR + Specific WRW

- FVA : WWR

A taste of déjà vu (cf. 2008 Korea, Brazil, Indonesia,

Poland…) cf. R. Dodd [2] and [10b]

Copyright © 2014 Murex S.A.S. All rights reserved 24

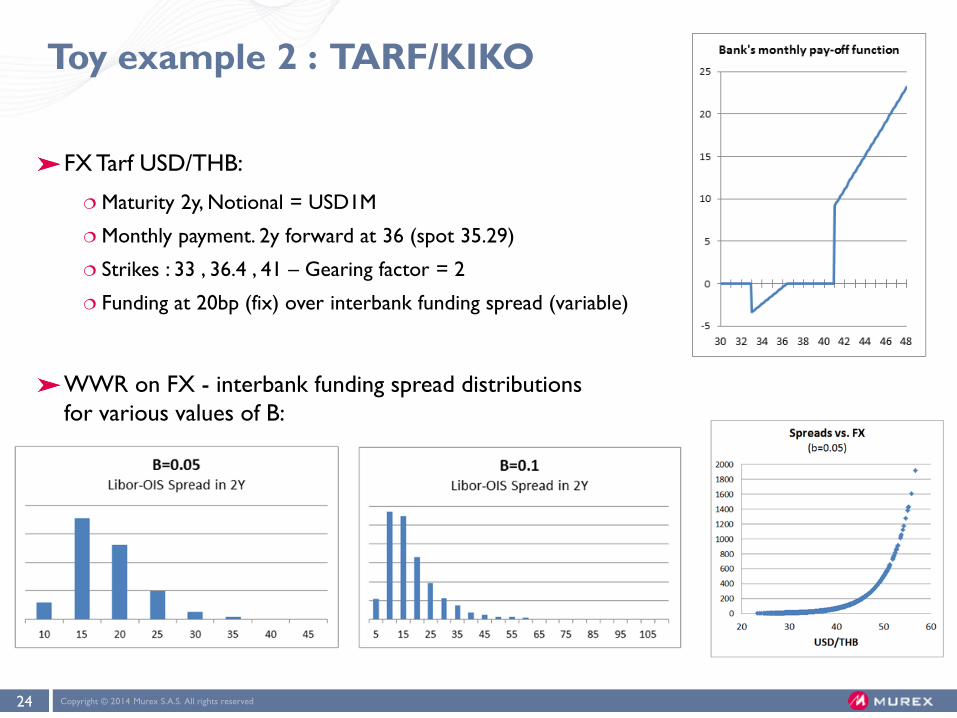

Toy example 2 : TARF/KIKO

FX Tarf USD/THB:

Maturity 2y, Notional = USD1M

Monthly payment. 2y forward at 36 (spot 35.29)

Strikes : 33 , 36.4 , 41 – Gearing factor = 2

Funding at 20bp (fix) over interbank funding spread (variable)

WWR on FX - interbank funding spread distributions

for various values of B:

Copyright © 2014 Murex S.A.S. All rights reserved 25

Toy example 2 : TARF/KIKO

Taking the funding B(FX) as 0.1, we get a 65% increase in FVA

Adding similar dynamics for CVA :

General RWR on FX (the corporate is hedging against THB appreciation)

Specific WWR on the structure’s MtM (due to gearing, default probabilities rise

sharply once the MtM rises beyond certain levels)

We get the following results with a 78% XVA increase due to combined

WWR effects on funding costs and credit risk.

Agenda

1. PRICING FUNDING COSTS AFTER THE CRISIS

2. COMPETING FVA MODELS : CSA-DISCOUNTING & EXPOSURE SIMULATION

3. WHICH FVA MODELS ARE STILL VALID NOW?

CONSIDERING POST-CRISIS SPREADS DYNAMICS

GIVEN THE IMPACT NEW REGULATORY DEVELOPMENTS

(EMIR, BASEL/IOSCO…) ON COLLATERALISATION REGIMES

4. ONE POSSIBLE FVA OPERATING MODEL

Copyright © 2014 Murex S.A.S. All rights reserved 27

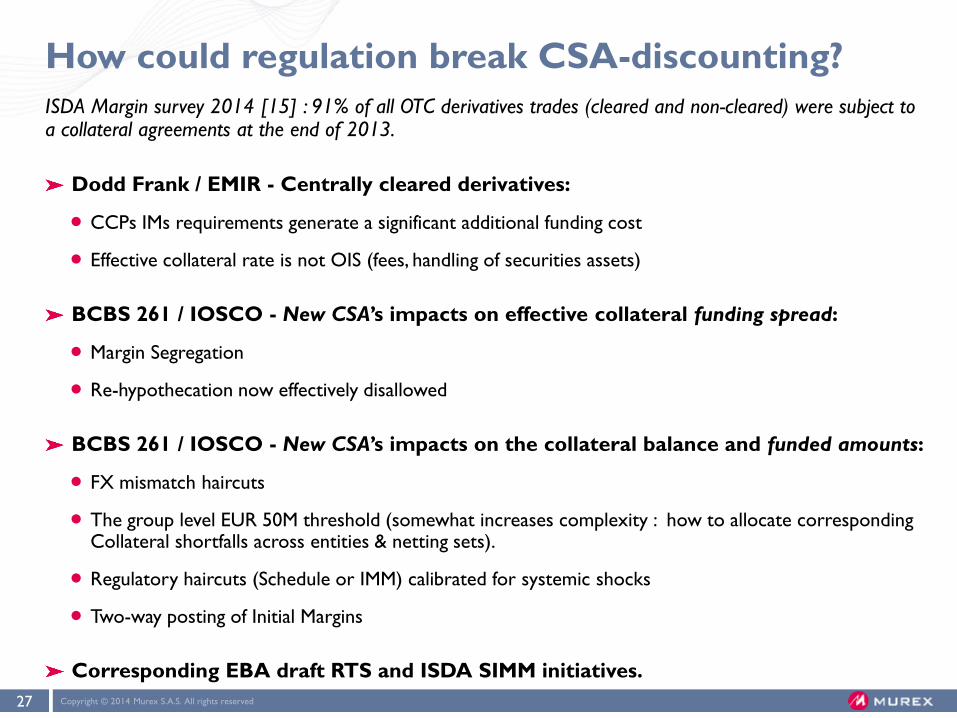

How could regulation break CSA-discounting?

ISDA Margin survey 2014 [15] : 91% of all OTC derivatives trades (cleared and non-cleared) were subject to a collateral agreements at the end of 2013.

Dodd Frank / EMIR - Centrally cleared derivatives:

CCPs IMs requirements generate a significant additional funding cost

Effective collateral rate is not OIS (fees, handling of securities assets)

BCBS 261 / IOSCO - New CSA’s impacts on effective collateral funding spread:

Margin Segregation

Re-hypothecation now effectively disallowed

BCBS 261 / IOSCO - New CSA’s impacts on the collateral balance and funded amounts:

FX mismatch haircuts

The group level EUR 50M threshold (somewhat increases complexity : how to allocate corresponding Collateral shortfalls across entities & netting sets).

Regulatory haircuts (Schedule or IMM) calibrated for systemic shocks

Two-way posting of Initial Margins

Corresponding EBA draft RTS and ISDA SIMM initiatives.

Copyright © 2014 Murex S.A.S. All rights reserved 28

Computation of Initial Margins (IMs)

Listed products usually SPAN-based methods

Centrally cleared products use VaR-based methods; CCPs methodologies vary

VaR or Expected Shortfall (99,7%), 5d/10d liquidity horizon, 10y history, EWMA decay or scaling

Credit & liquidity multipliers

CCP pays back OIS rate – spread on cash Collateral received, not necessarily on securities.

Future CSA for uncleared products (cf. appendix 2):

Mandatory exchange of “two-way initial margins”

Simple and prohibitively expensive standardised Schedule method (40/60 NGR)

Internal model : 99% 10d VaR, split in 4 asset classes buckets, 3y history incl. period of stress

FX mismatch haircut and Group-level threshold (max €50m) across entities & agreements

ISDA SIMM proposals:

V1: Sensitivities-based VaR (Taylor expansion) on risk factor buckets

V2: SBA-M, scaled down version of the SBA-C method for FRTB, risk weight applied by sensitivities buckets – under discussion.

Copyright © 2014 Murex S.A.S. All rights reserved 29

Should IMs be considered in trade-level FVAs?

a. Simplistic example :

Assume a portfolio’s value is normally distributed (IID)

Compare the daily IMs with the portfolio average MtM,

depending on the average “age” of the positions

b. Margin replication benchmark exercise on

IRD portfolios:

Are IM amounts material enough ?

Obviously extremely variable and a function of the leverage and directionality of the portfolio being

cleared/collateralised.

Copyright © 2014 Murex S.A.S. All rights reserved 30

Modeling VaR-based IMs for FVA

Copyright © 2014 Murex S.A.S. All rights reserved 31

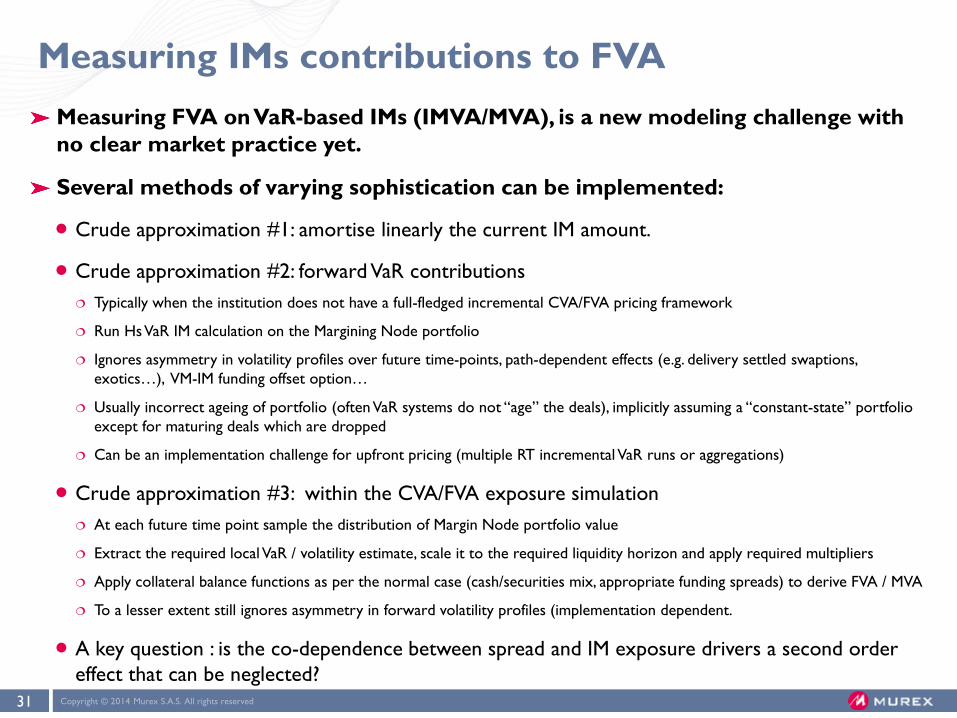

Measuring IMs contributions to FVA

Measuring FVA on VaR-based IMs (IMVA/MVA), is a new modeling challenge with

no clear market practice yet.

Several methods of varying sophistication can be implemented:

Crude approximation #1: amortise linearly the current IM amount.

Crude approximation #2: forward VaR contributions

Typically when the institution does not have a full-fledged incremental CVA/FVA pricing framework

Run Hs VaR IM calculation on the Margining Node portfolio

Ignores asymmetry in volatility profiles over future time-points, path-dependent effects (e.g. delivery settled swaptions,

exotics…), VM-IM funding offset option…

Usually incorrect ageing of portfolio (often VaR systems do not “age” the deals), implicitly assuming a “constant-state” portfolio

except for maturing deals which are dropped

Can be an implementation challenge for upfront pricing (multiple RT incremental VaR runs or aggregations)

Crude approximation #3: within the CVA/FVA exposure simulation

At each future time point sample the distribution of Margin Node portfolio value

Extract the required local VaR / volatility estimate, scale it to the required liquidity horizon and apply required multipliers

Apply collateral balance functions as per the normal case (cash/securities mix, appropriate funding spreads) to derive FVA / MVA

To a lesser extent still ignores asymmetry in forward volatility profiles (implementation dependent.

A key question : is the co-dependence between spread and IM exposure drivers a second order

effect that can be neglected?

Copyright © 2014 Murex S.A.S. All rights reserved 32

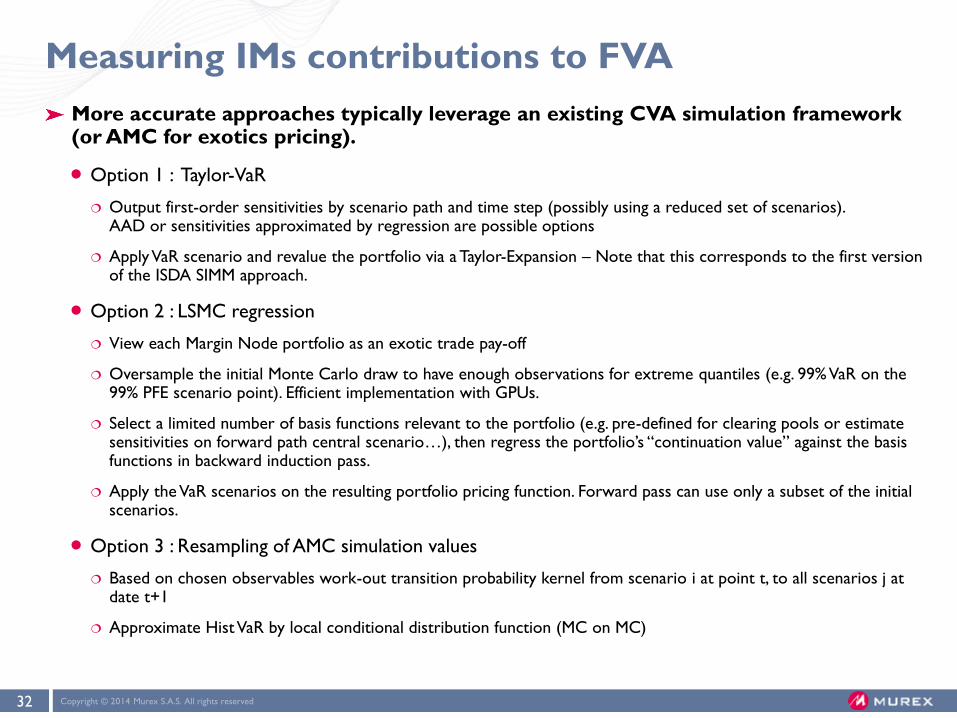

Measuring IMs contributions to FVA

More accurate approaches typically leverage an existing CVA simulation framework (or AMC for exotics pricing).

Option 1 : Taylor-VaR

Output first-order sensitivities by scenario path and time step (possibly using a reduced set of scenarios). AAD or sensitivities approximated by regression are possible options

Apply VaR scenario and revalue the portfolio via a Taylor-Expansion – Note that this corresponds to the first version of the ISDA SIMM approach.

Option 2 : LSMC regression

View each Margin Node portfolio as an exotic trade pay-off

Oversample the initial Monte Carlo draw to have enough observations for extreme quantiles (e.g. 99% VaR on the 99% PFE scenario point). Efficient implementation with GPUs.

Select a limited number of basis functions relevant to the portfolio (e.g. pre-defined for clearing pools or estimate sensitivities on forward path central scenario…), then regress the portfolio’s “continuation value” against the basis functions in backward induction pass.

Apply the VaR scenarios on the resulting portfolio pricing function. Forward pass can use only a subset of the initial scenarios.

Option 3 : Resampling of AMC simulation values

Based on chosen observables work-out transition probability kernel from scenario i at point t, to all scenarios j at date t+1

Approximate Hist VaR by local conditional distribution function (MC on MC)

Copyright © 2014 Murex S.A.S. All rights reserved 33

Local regression for LSMC-based IM simulation

In low dimensions (e.g. clearing), local regression methods (LOWESS) can be an

interesting alternative to the usual parametric forms (e.g. polynomials).

Significant accuracy improvement on high “PFE” quantiles for exotic pay-offs

LSMC PFE accuracy w.r.t closed-form pricing (cf. Morali [12])

Parametric

regression

Local

regression

Copyright © 2014 Murex S.A.S. All rights reserved 34

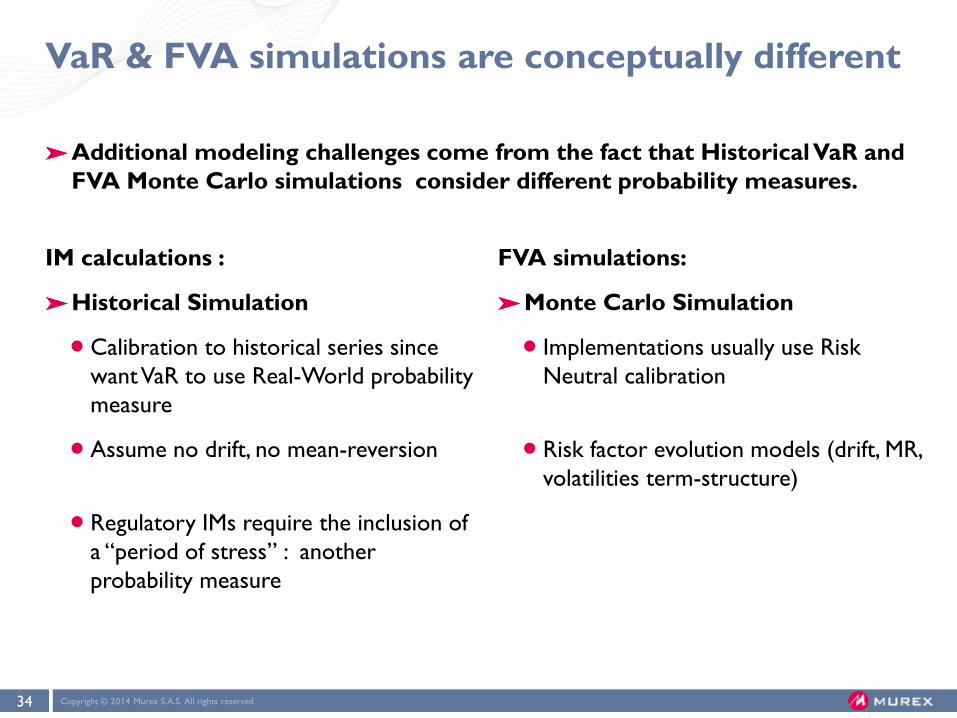

VaR & FVA simulations are conceptually different

IM calculations :

Historical Simulation

Calibration to historical series since

want VaR to use Real-World probability

measure

Assume no drift, no mean-reversion

Regulatory IMs require the inclusion of

a “period of stress” : another

probability measure

FVA simulations:

Monte Carlo Simulation

Implementations usually use Risk

Neutral calibration

Risk factor evolution models (drift, MR,

volatilities term-structure)

Additional modeling challenges come from the fact that Historical VaR and

FVA Monte Carlo simulations consider different probability measures.

Copyright © 2014 Murex S.A.S. All rights reserved 35

FVA for VaR-based IMs: methodology challenges

Is FVA estimated in the Risk-Neutral or Real World measure?

Approximations will have to be used, esp. for translating VaR scenarios in the

forward simulation

Initialization of path-wise calibration time series should be avoided :

Potentially complex (e.g. filtering or vol rescaling)

Undesirable “change of volatility regime” from today onwards, impact of mean-reversion over

long-horizons

Can we assume equivalence between:

Historical and Monte Carlo VaR?

Risk Neutral – Real World equivalence by a change of measure and use RN calibration for VaR

For regulatory IM, apply a change of measure or a simple volatilities scale-up (Stressed

Measure for Real-World Measure)?

Handling of VaR scenarios on risk factors not captured in the FVA simulation /

Margining node pricing function

Copyright © 2014 Murex S.A.S. All rights reserved 36

Modeling challenges with the “SBA-M” proposal

ISDA’s tentative proposal : SBA for Margin (SBA-M)

Purpose: offer a risk-sensitive approach that will support simplicity and speed of computations as well as facilitate the reconciliation process

Aligned on Standardised method for market risk capital (bcbs 265 : Fundamental Review of the Trading Book), with some simplifications and adjustments:

First-order sensitivities (without disallowance factor ignoring curvature/basis risk)

Recalibration of risk weights (10d liquidity period), and single correlation set. No JTD, No vega-margin in phase 1

Collateral FX risk directly included & Bucketing by risk factors rather than asset classes

Etc.

The computation of the corresponding IM FVA thus requires producing Deltas on all scenario paths and time points within the simulation, before applying the SBA algorithm !

No simple approximations as sensitivities are not stable through time and space

Full computation too heavy for incremental pricing needs

One option: estimate sensitivities in the American Monte Carlo by regressing incremental changes in values vs. incremental values of the risk driver and applying a correction for correlations (cf. Cesari [1]].

Agenda

1. PRICING FUNDING COSTS AFTER THE CRISIS

2. COMPETING FVA MODELS : CSA-DISCOUNTING & EXPOSURE SIMULATION

3. WHICH FVA MODELS ARE STILL VALID NOW?

CONSIDERING POST-CRISIS SPREADS DYNAMICS

GIVEN THE IMPACT NEW REGULATORY DEVELOPMENTS (EMIR, BASEL/IOSCO…)

ON COLLATERALISATION REGIMES

4. ONE POSSIBLE FVA OPERATING MODEL

Copyright © 2014 Murex S.A.S. All rights reserved 38

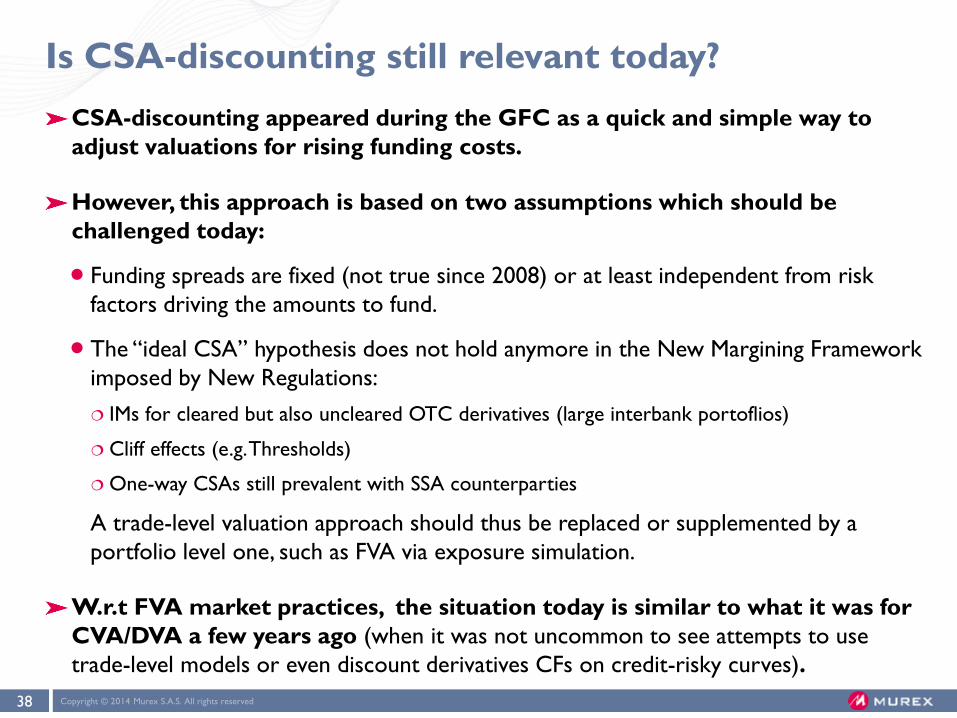

Is CSA-discounting still relevant today?

CSA-discounting appeared during the GFC as a quick and simple way to

adjust valuations for rising funding costs.

However, this approach is based on two assumptions which should be

challenged today:

Funding spreads are fixed (not true since 2008) or at least independent from risk

factors driving the amounts to fund.

The “ideal CSA” hypothesis does not hold anymore in the New Margining Framework

imposed by New Regulations:

IMs for cleared but also uncleared OTC derivatives (large interbank portoflios)

Cliff effects (e.g. Thresholds)

One-way CSAs still prevalent with SSA counterparties

A trade-level valuation approach should thus be replaced or supplemented by a

portfolio level one, such as FVA via exposure simulation.

W.r.t FVA market practices, the situation today is similar to what it was for

CVA/DVA a few years ago (when it was not uncommon to see attempts to use

trade-level models or even discount derivatives CFs on credit-risky curves).

Copyright © 2014 Murex S.A.S. All rights reserved 39

Summary of possible valuation approaches

Nonetheless, can CSA-discounting still be used in an economic value perspective

(e.g. for pricing incremental operations) in some cases ?

Copyright © 2014 Murex S.A.S. All rights reserved 40

Economic value optimisation: the accounting analogy

Why compute valuation adjustments?

Initial motivation: incentivize risk takers by valuing all economic costs/benefits to the BU ignored

in the theoretical price (credit, funding, capital…).

Later on: recognize that market prices deviate from their theoretical levels (since institutions

adjust their quotes for CVA/FVA…) to present an accurate picture of assets values in financial

statements.

Cost Accounting: aims at presenting detailed costs information to feed in internal

managerial decisions and control current operations by optimally allocating resources to the

most efficient and profitable business areas.

Financial Accounting: produces formalized financial statements (P&L account and Balance

Sheet) that are used by external stakeholders to get a “true and fair” picture of transactions,

and analyze the results and financial position of the firm on a given date.

Copyright © 2014 Murex S.A.S. All rights reserved 41

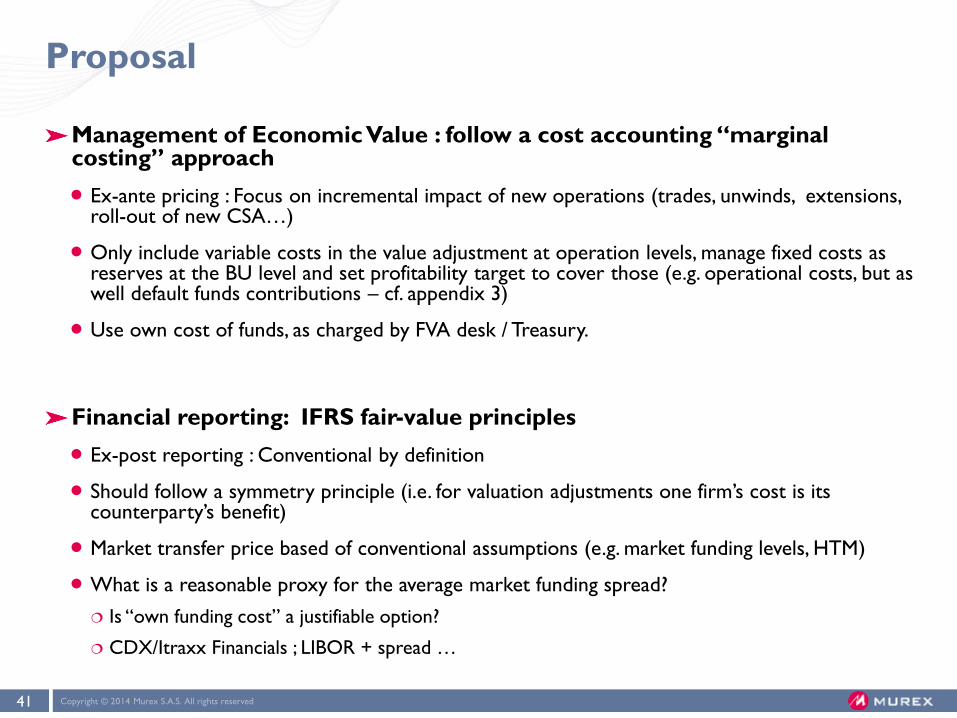

Proposal

Management of Economic Value : follow a cost accounting “marginal costing” approach

Ex-ante pricing : Focus on incremental impact of new operations (trades, unwinds, extensions, roll-out of new CSA…)

Only include variable costs in the value adjustment at operation levels, manage fixed costs as reserves at the BU level and set profitability target to cover those (e.g. operational costs, but as well default funds contributions – cf. appendix 3)

Use own cost of funds, as charged by FVA desk / Treasury.

Financial reporting: IFRS fair-value principles

Ex-post reporting : Conventional by definition

Should follow a symmetry principle (i.e. for valuation adjustments one firm’s cost is its counterparty’s benefit)

Market transfer price based of conventional assumptions (e.g. market funding levels, HTM)

What is a reasonable proxy for the average market funding spread?

Is “own funding cost” a justifiable option?

CDX/Itraxx Financials ; LIBOR + spread …

Copyright © 2014 Murex S.A.S. All rights reserved 42

One possible FVA operational model (1/2)

All trades are priced with OIS discounting and FVA adjustment:

Funding costs are priced via FVA adjustment(s), like credit is priced via CVA

FVA fees and positions are transferred to a FVA desk (can be part of Treasury or CVA desk),

leaving limited IR basis risks in the trading portfolio. Hedge ratios are identical for collateralised /

uncollateralised positions in the trader’s book.

A dedicated desk, reports and manages the Funding P&L (analysis, hedging / reserving for basis

effects, etc.)

As a default rule, assume that all trades are held to maturity (i.e. full lifetime

term-funding)

Some exceptions can be granted for specific counterparties (hedge funds) in order to price

competitively, they are managed through ad hoc processes.

Transaction extensions / roll-overs (or cash settled swaptions, exercised in delivery mode) incur

an incremental FVA charge – consistent with CVA.

Conversely early-terminations/unwinds can get back a FVA benefit fee.

Copyright © 2014 Murex S.A.S. All rights reserved 43

One possible FVA operational model (1/2)

Regarding the funding curve, an arrangement can be made with the FVA/Treasury desk:

Treasury agrees to apply a single FTP/funding rate (lend & borrow) based for a year on an industry benchmark (e.g. Libor + Xbp) - cf. Smirnov [9]

This rate is guaranteed for as long as the trading desk maintains positions within pre-agreed limits (gaps, CF ladders, PV01s…). Otherwise punitive rates are applied.

A reserve is passed at the BU level to cover for the risk of higher reset of the funding at year end (period cost)

Additional costs

Contribution to Liquidity buffer is not included in transaction prices as Treasury/ALM takes the responsibility to optimize the funding strategy (this premium is already included in the internal funding rate)

LCR/NSFR contributions can be incorporated in a KVA adjustment (being mindful of potential overlaps with liquidity buffers)

The CVA/FVA desk, Treasury and the Collateral Management function need to collaborate closely

Continuous alignment of pricing assumptions with Collateral Management practices (substitutions, re-hypothecation…)

Securities assets optimization (collateral & regulator capital)

Data management, implementation of new CSAs…

Copyright © 2014 Murex S.A.S. All rights reserved 44

Conclusion

Computing FVA for Economic Value assessment or Fair Value Accounting purpose may warrant using different modeling approaches, both in terms of methodology and inputs (e.g. choice of funding curves)

In the near future, the bulk of OTC derivatives positions will be split across:

Centrally cleared position (largest portion), where IMs, multipliers and default fund contributions generate additional funding requirements

New style CSAs (with two-ways IMs, re-hypothecation and haircuts)

Some old-style CSAs with buy-side institutions, corporates & SSAs – sometimes with the usual twists (one-way, thresholds…)

Exotics and uncollateralised transactions with corporates, SSAs (often structured trns), that can be quite sensitive to stochastic funding spreads and WWR effects.

In order to price incremental operations in a way that recognizes the economic benefits/costs of funding, a plain CSA-discounting valuation approach will not suffice anymore.

It may even provide distorted incentives by missing some important effects.

Current CSA-discounting implementations, will need to be complemented by additional computations (e.g. IMVA) or replaced by comprehensive exposure simulations.

Copyright © 2014 Murex S.A.S. All rights reserved 45

Acknowledgments

Sincere thanks to my colleagues, and in particular:

Gil Guillaumey

Guillaume Juge

Adrien Taÿ-Pamart

Copyright © 2014 Murex S.A.S. All rights reserved 46

References Industry papers

[1] G. Cesari & a. - 2009

« modeling, Pricing, and Hedging Counterparty Credit Exposure. A Technical Guide »

[2] R. Dodd, IMF paper – July 2009

« Exotic Derivatives Losses in Emerging Markets: Questions of Suitability, Concerns for Stability »

[3] C. Fries – February 2011

« Funded replication: Valuing with stochastic funding »

[4] A. Green, C. Kenyon, and C. R. Dennis – February 2014

« KVA: Capital Valuation Adjustment »

[5] J. Gregory – 2009

« Counterparty credit risk – The new challenge for global financial markets. »

[6] J. Hull & A. White – March 1998

« Incorporating volatility updating into the historical simulation for value at risk »

[7] J. Hull & A. White – June 2011

« CVA & Wrong Way Risk »

[8] M. Morini, WBS Fixed income conference – October 2012

« Model risk in today’s approaches to funding and collateral »

[9] I. Smirnov, WBS Fixed income conference – October 2013

« Liquidity & Capital in derivatives pricing »

Copyright © 2014 Murex S.A.S. All rights reserved 47

References Murex documents

[10] A. Bon, WBS CVA conference – March 2012 « OTC Collateralisation : Implementation Issues in CVA & FVA frameworks »

[10b] A. Bon – September 2010 « Specific WWR examples – case 3 : from right way to wrong way »

[11] D. Loiseau, MathFinance conference, March 2012 « Introducing Stochastic Spreads in a Multi-Curves Framework »

[12] A. Morali, HPCFinance Conference – May 2013 « American Monte Carlo for Portfolio CVA & PFE »

[13] InteDelta & Murex – May 2014 « CVA & Counterparty Risk Management : a survey of management, measurement and systems »

Regulation & institutional documents

[14] BCBS-IOSCO – September 2013 « Margin requirements for non-centrally cleared derivatives »

[15] ESMA-EBA – April 2014 « Draft RTS on risk-mitigation techniques for OTC-derivative contracts not cleared by a CCP »

[16] ISDA – December 2013 « Standard Initial Margin Model for Non-Cleared Derivatives »

[17] ISDA – April 2014 « Margin Survey 2014 »

[18] ISDA – 2014 « SIMM Methodology – SBA-Margin »

Copyright © 2014 Murex S.A.S. All rights reserved 48

Appendix 1: LIBOR-OIS spreads historical analysis

0

20

40

60

80

100

120

140

160

180

200EUR Libor - EONIA spread (in bps)

Sp

read

0

20

40

60

80

100

120

140

160

180

200

EURIBOR - EONIA SpreadItraxx Senior Financial (Normalised)

EUR EONIA spreads Vs Credit spreads

0

50

100

150

200

250

300

350

400

450

500 USD Libor - FF spread (in bps)

Sp

read

0

50

100

150

200

250

300

350

400

450

500

USD Libor - FF spread

CDX Financial 5Y (Normalised)

USD Libor - FF spread (in bps)

Copyright © 2014 Murex S.A.S. All rights reserved 49

0

50

100

150

200

250

300

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

180

195

205

215

225

235

255

270

280

290

300

310

325

345

390

420

450

Historical spread distribution 2007-2014 N

um

ber

of

occu

ren

ces

Spread level

0

50

100

150

200

250

300

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 80

Historical spread distribution 2010-2014

Appendix 1: LIBOR-OIS spreads historical analysis

Copyright © 2014 Murex S.A.S. All rights reserved 50

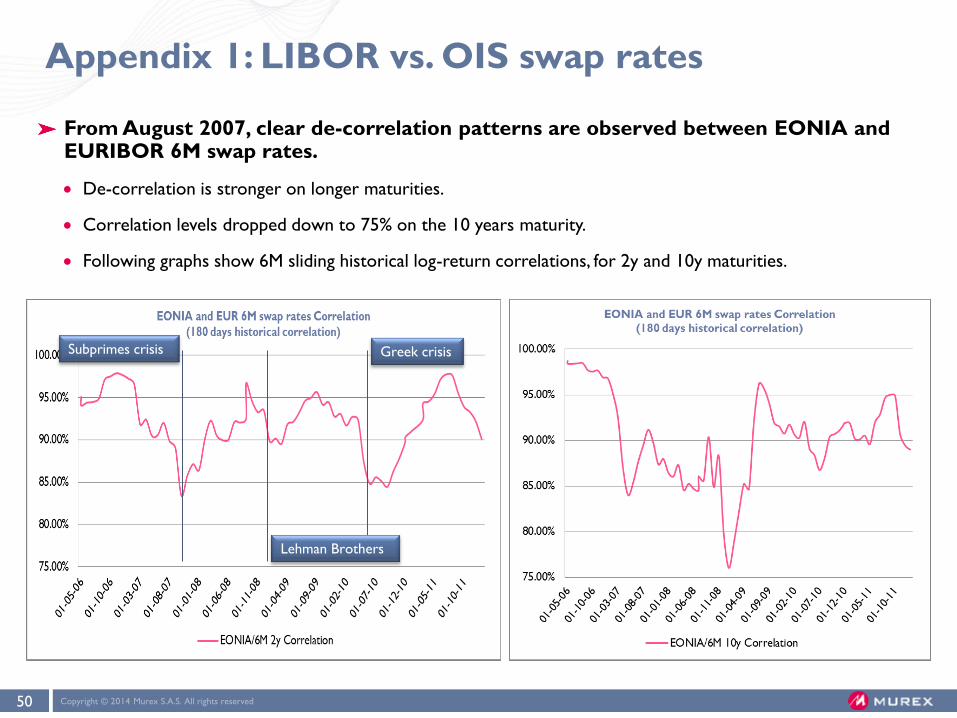

From August 2007, clear de-correlation patterns are observed between EONIA and EURIBOR 6M swap rates.

De-correlation is stronger on longer maturities.

Correlation levels dropped down to 75% on the 10 years maturity.

Following graphs show 6M sliding historical log-return correlations, for 2y and 10y maturities.

Subprimes crisis

Lehman Brothers

Greek crisis

Appendix 1: LIBOR vs. OIS swap rates

Copyright © 2014 Murex S.A.S. All rights reserved 51

Appendix 2: the new CSAs

New regulation aiming at “reducing systemic risk and promoting central clearing”

BCBS-IOSCO “Margin requirements for non-centrally cleared derivatives”, bcbs 261, Sep 2013 [14]

ESMA-EBA “Draft RTS on risk-mitigation techniques for OTC-derivative contracts not cleared by a CCP”, Apr 2014 , on-going consultation [15]

Applicable to Financial Institutions (interbank) with over €8bn notional of non-centrally cleared derivatives - gradual roll-out from Dec 2015 to Dec 2019

Key provisions in a FVA context

Mandatory exchange of “two-way initial margins”

Margin segregations and no re-hypothecation / re-use rights

Internal models or Standardised schedule methods for determining IMs and collateral haircuts

FX mismatch haircut

Group-level threshold (max €50m) across legal entities and netting agreements

De facto killed the S-CSA initiative

Dec 2013 : ISDA SIMM proposal for an internal model Initial [16]

On-going : second SIMM version aligning with market risk regulatory capital practices

Copyright © 2014 Murex S.A.S. All rights reserved 52

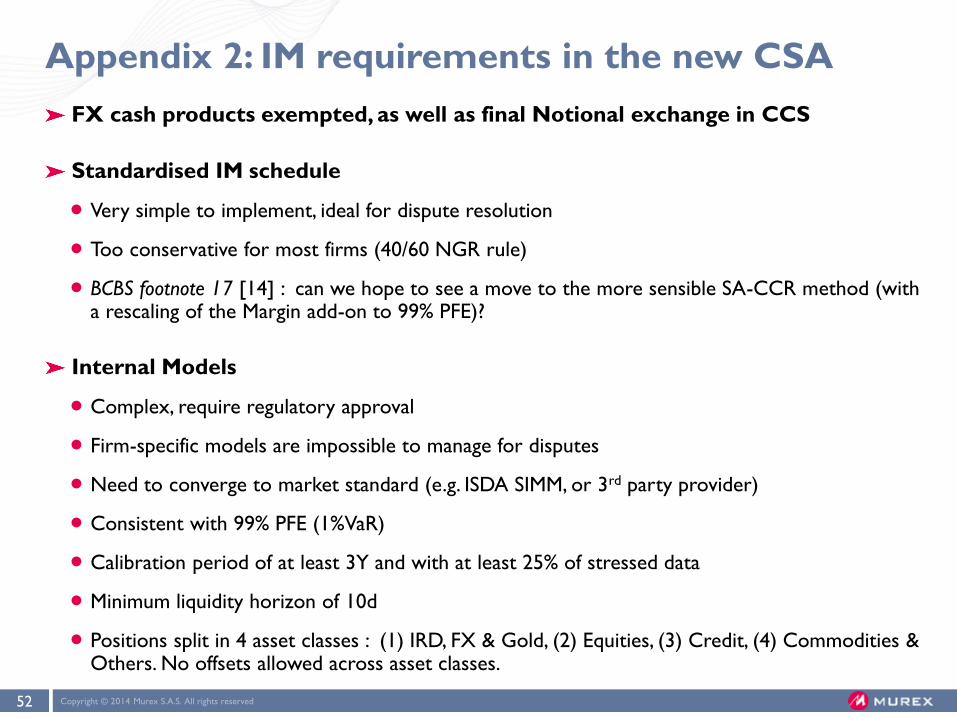

Appendix 2: IM requirements in the new CSA

FX cash products exempted, as well as final Notional exchange in CCS

Standardised IM schedule

Very simple to implement, ideal for dispute resolution

Too conservative for most firms (40/60 NGR rule)

BCBS footnote 17 [14] : can we hope to see a move to the more sensible SA-CCR method (with a rescaling of the Margin add-on to 99% PFE)?

Internal Models

Complex, require regulatory approval

Firm-specific models are impossible to manage for disputes

Need to converge to market standard (e.g. ISDA SIMM, or 3rd party provider)

Consistent with 99% PFE (1%VaR)

Calibration period of at least 3Y and with at least 25% of stressed data

Minimum liquidity horizon of 10d

Positions split in 4 asset classes : (1) IRD, FX & Gold, (2) Equities, (3) Credit, (4) Commodities & Others. No offsets allowed across asset classes.

Copyright © 2014 Murex S.A.S. All rights reserved 53

Appendix 2: computation of IMs at CCPs

Different CCPs can apply different methodogies

Listed products usually SPAN-based methods

OTC derivatives usually VaR-based:

10 years historical series with EWMA decay (e.g. LCH SwapClear) or EWMA vol re-

scaling (cf. Hull & White [6]).

5d/10d risk factor shocks are applied (with overlapping sampling)

High percentile VaR or Expected Shortfall (e.g. 99.7%)

CCP-specific pricing conventions (e.g. OIS discounting)

Credit & Liquidity Multipliers:

Can be material too

Can show some cliff effects

Copyright © 2014 Murex S.A.S. All rights reserved 54

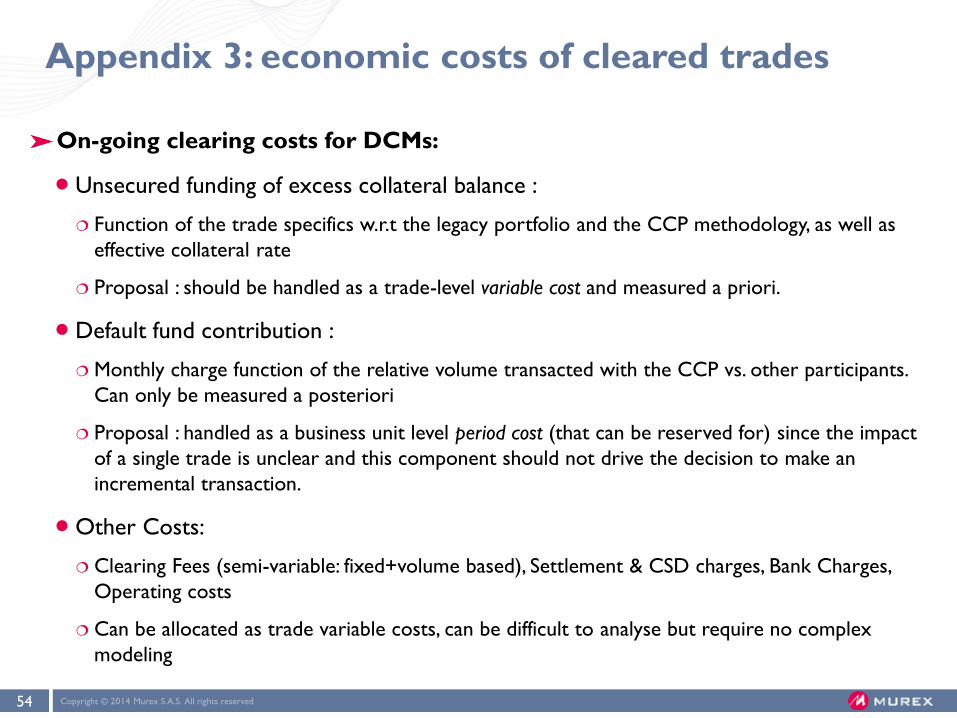

Appendix 3: economic costs of cleared trades

On-going clearing costs for DCMs:

Unsecured funding of excess collateral balance :

Function of the trade specifics w.r.t the legacy portfolio and the CCP methodology, as well as

effective collateral rate

Proposal : should be handled as a trade-level variable cost and measured a priori.

Default fund contribution :

Monthly charge function of the relative volume transacted with the CCP vs. other participants.

Can only be measured a posteriori

Proposal : handled as a business unit level period cost (that can be reserved for) since the impact

of a single trade is unclear and this component should not drive the decision to make an

incremental transaction.

Other Costs:

Clearing Fees (semi-variable: fixed+volume based), Settlement & CSD charges, Bank Charges,

Operating costs

Can be allocated as trade variable costs, can be difficult to analyse but require no complex

modeling

Copyright © 2014 Murex S.A.S. All rights reserved 55

Appendix 3: economic costs of cleared trades

Proposal : unsecured funding of excess collateral balance : should be

handled as a trade-level variable cost and measured a priori.

Additional on-going clearing costs for DCMs:

Default fund contribution :

Monthly charge function of the relative volume transacted with the CCP vs. other participants.

Can only be measured a posteriori

Proposal : handled as a business unit level period cost (that can be reserved for) since the impact

of a single trade is unclear and this component should not drive the decision to make an

incremental transaction.

Other Costs:

Clearing Fees (semi-variable: fixed + volume based), Settlement & CSD charges, Bank Charges,

Operating costs

Can be allocated as trade variable costs, can be difficult to analyse but require no complex

modeling

THANK YOU