riverside county california cost allocation plan overview and applications august 27, 2008 eric...

TRANSCRIPT

Riverside County CaliforniaCost Allocation Plan Overview and Applications

August 27, 2008

Eric Parish & Sara BeemerPRM, a Subsidiary of MGT of America, Inc.

Purpose of Presentation

1. Explain the cost allocation project including preparation, applications and benefits.

2. Gain feedback and input from County personnel.

3. Answer questions.

PRM / MGT Introduction Consulting firm focused on local government cost

issues Cost allocation plans Indirect cost rate proposals User fee studies Rate studies State mandated reimbursement (SB90)

26 consultants 140+ clients in 20 states 5th year providing cost allocation work for the

County

Cost Allocation Presentation Outline

What is cost allocation Benefits of cost allocation Preparing a cost allocation plan Continuous improvement process Example results of a cost allocation plan OMB A-87 cost plan vs. Full Cost plan Applications of cost allocation Questions throughout

What is Cost Allocation (Theory)

Method to identify and distribute County indirect costs Direct costs (specific) Indirect costs (shared)

Administrative Support Overhead

What is Cost Allocation (Theory)

Direct vs. Indirect

Direct costs

Costs that can be assigned, or directed, to a specific task, activity or program

What is Cost Allocation (Theory)

Direct vs. IndirectIndirect costs.Costs that cannot be assigned, or directed, to a specific task, activity or program.

Costs incurred for a common or joint purpose benefiting more than one task, activity or program.

Indirect costs cannot be directly assigned without making an effort disproportionate to the results achieved.

What is Cost Allocation (Theory)

Accomplished through an annual cost allocation plan Concept recognizing operating programs should

pay for the general fund County support received

Document identifying and distributing County indirect (administrative, support, overhead) costs to benefiting departments/divisions/programs

Benefits of Cost Allocation

Recover allowable indirect costs from federal and state programs

Allocate appropriate indirect costs to other funds, programs or activities

Critical component of SB90 claims Fee calculation Subsidy decisions Resource allocation

Preparing a Cost Allocation Plan

Collect financial and operational data Prior year actual expenditures

Communicate with department representatives Identify department functions Identify and request allocation data Match expenditures and allocations Process cost allocation plan Review, correct, re-process

Continuous Improvement

Annually present overview of cost plan Identify annual area(s) of emphasis Annual department meetings

Three ways to ask the same question

Management Report Variance Analysis Unit Costs

Communicate year-round with cost plan stakeholders

Reviewing a Cost Allocation Plan15001 County Counsel

6 Legal Services Direct Hours per dept/agency County Counsel 11301 Human Resources

7 HR Services Direct Cost per Dept Id 73001 Purchasing

8 Purchasing Services # of Purchase Orders per dept8 Support Services Direct Cost of Svcs

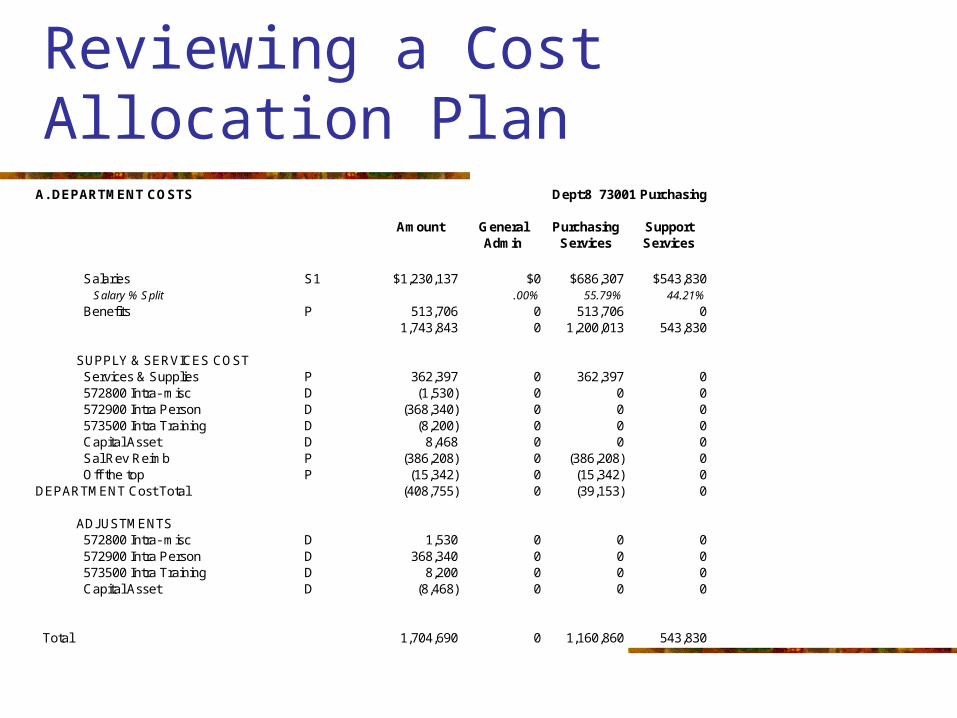

Reviewing a Cost Allocation PlanA. DEPARTMENT COSTS Dept:8 73001 Purchasing

Amount General Admin

Purchasing Services

Support Services

Salaries S1 $1,230,137 $0 $686,307 $543,830 Salary % Split .00% 55.79% 44.21% Benefits P 513,706 0 513,706 0

1,743,843 0 1,200,013 543,830

SUPPLY & SERVICES COST Services & Supplies P 362,397 0 362,397 0 572800 Intra- misc D (1,530) 0 0 0 572900 Intra Person D (368,340) 0 0 0 573500 Intra Training D (8,200) 0 0 0 Capital Asset D 8,468 0 0 0 Sal Rev Reimb P (386,208) 0 (386,208) 0 Off the top P (15,342) 0 (15,342) 0

DEPARTMENT Cost Total (408,755) 0 (39,153) 0

ADJ USTMENTS 572800 Intra- misc D 1,530 0 0 0 572900 Intra Person D 368,340 0 0 0 573500 Intra Training D 8,200 0 0 0 Capital Asset D (8,468) 0 0 0

Total 1,704,690 0 1,160,860 543,830

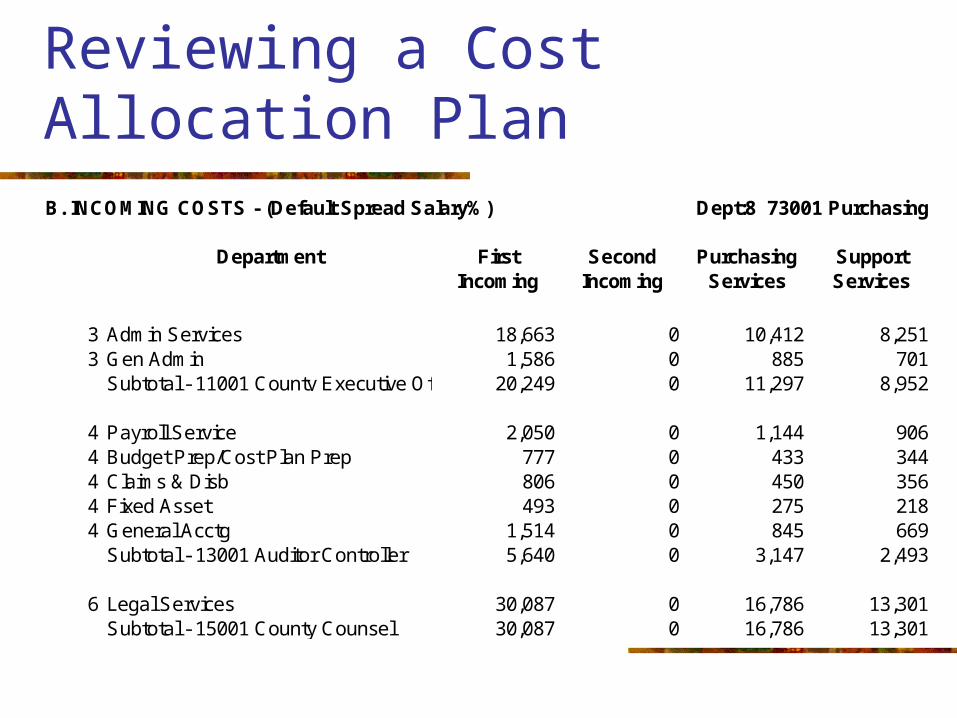

Reviewing a Cost Allocation PlanB. INCOMING COSTS - (Default Spread Salary%) Dept:8 73001 Purchasing

Department First Incoming

Second Incoming

Purchasing Services

Support Services

3 Admin Services 18,663 0 10,412 8,2513 Gen Admin 1,586 0 885 701

Subtotal - 11001 County Executive Office 20,249 0 11,297 8,952

4 Payroll Service 2,050 0 1,144 9064 Budget Prep/Cost Plan Prep 777 0 433 3444 Claims & Disb 806 0 450 3564 Fixed Asset 493 0 275 2184 General Acctg 1,514 0 845 669

Subtotal - 13001 Auditor Controller 5,640 0 3,147 2,493

6 Legal Services 30,087 0 16,786 13,301Subtotal - 15001 County Counsel 30,087 0 16,786 13,301

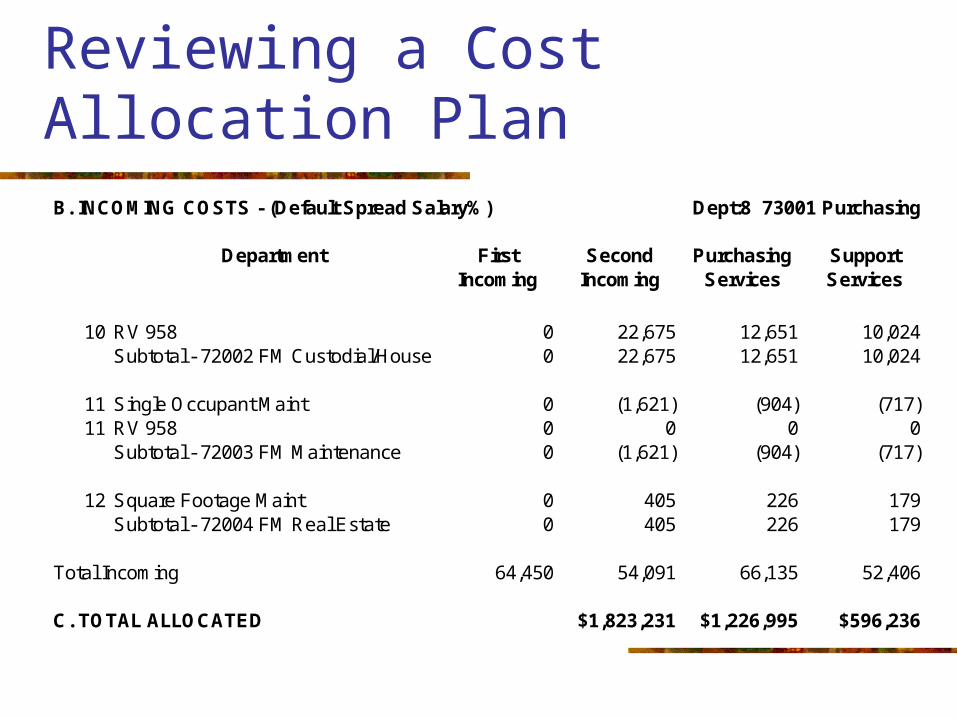

Reviewing a Cost Allocation PlanB. INCOMING COSTS - (Default Spread Salary%) Dept:8 73001 Purchasing

Department First Incoming

Second Incoming

Purchasing Services

Support Services

10 RV 958 0 22,675 12,651 10,024Subtotal - 72002 FM Custodial/Housekeeping 0 22,675 12,651 10,024

11 Single Occupant Maint 0 (1,621) (904) (717)11 RV 958 0 0 0 0

Subtotal - 72003 FM Maintenance 0 (1,621) (904) (717)

12 Square Footage Maint 0 405 226 179Subtotal - 72004 FM Real Estate 0 405 226 179

Total Incoming 64,450 54,091 66,135 52,406

C. TOTAL ALLOCATED $1,823,231 $1,226,995 $596,236

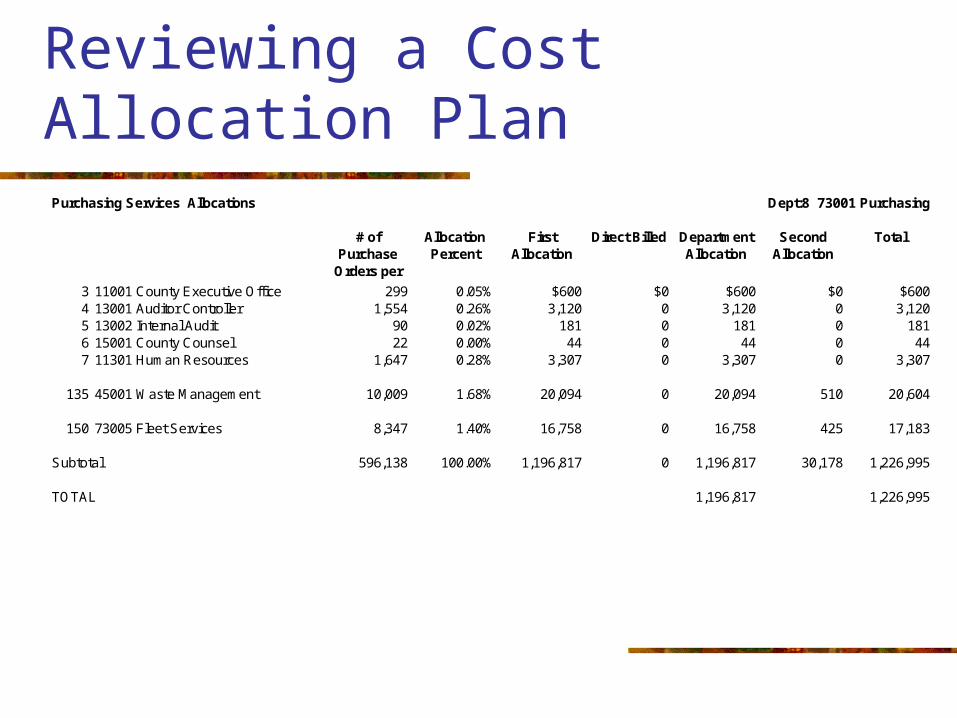

Reviewing a Cost Allocation PlanPurchasing Services Allocations Dept:8 73001 Purchasing

# of Purchase Orders per

dept

Allocation Percent

First Allocation

Direct Billed Department Allocation

Second Allocation

Total

3 11001 County Executive Office 299 0.05% $600 $0 $600 $0 $6004 13001 Auditor Controller 1,554 0.26% 3,120 0 3,120 0 3,1205 13002 Internal Audit 90 0.02% 181 0 181 0 1816 15001 County Counsel 22 0.00% 44 0 44 0 447 11301 Human Resources 1,647 0.28% 3,307 0 3,307 0 3,307

135 45001 Waste Management 10,009 1.68% 20,094 0 20,094 510 20,604

150 73005 Fleet Services 8,347 1.40% 16,758 0 16,758 425 17,183

Subtotal 596,138 100.00% 1,196,817 0 1,196,817 30,178 1,226,995

TOTAL 1,196,817 1,226,995

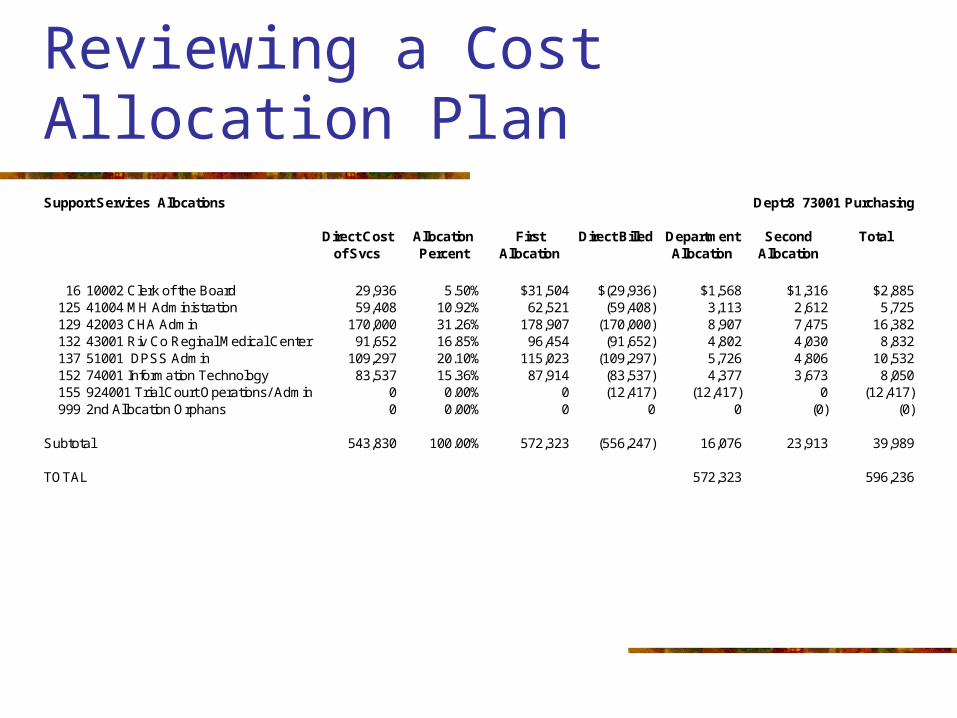

Reviewing a Cost Allocation PlanSupport Services Allocations Dept:8 73001 Purchasing

Direct Cost of Svcs

Allocation Percent

First Allocation

Direct Billed Department Allocation

Second Allocation

Total

16 10002 Clerk of the Board 29,936 5.50% $31,504 $(29,936) $1,568 $1,316 $2,885125 41004 MH Administration 59,408 10.92% 62,521 (59,408) 3,113 2,612 5,725129 42003 CHA Admin 170,000 31.26% 178,907 (170,000) 8,907 7,475 16,382132 43001 Riv Co Reginal Medical Center 91,652 16.85% 96,454 (91,652) 4,802 4,030 8,832137 51001 DPSS Admin 109,297 20.10% 115,023 (109,297) 5,726 4,806 10,532152 74001 Information Technology 83,537 15.36% 87,914 (83,537) 4,377 3,673 8,050155 924001 Trial Court Operations/ Admin 0 0.00% 0 (12,417) (12,417) 0 (12,417)999 2nd Allocation Orphans 0 0.00% 0 0 0 (0) (0)

Subtotal 543,830 100.00% 572,323 (556,247) 16,076 23,913 39,989

TOTAL 572,323 596,236

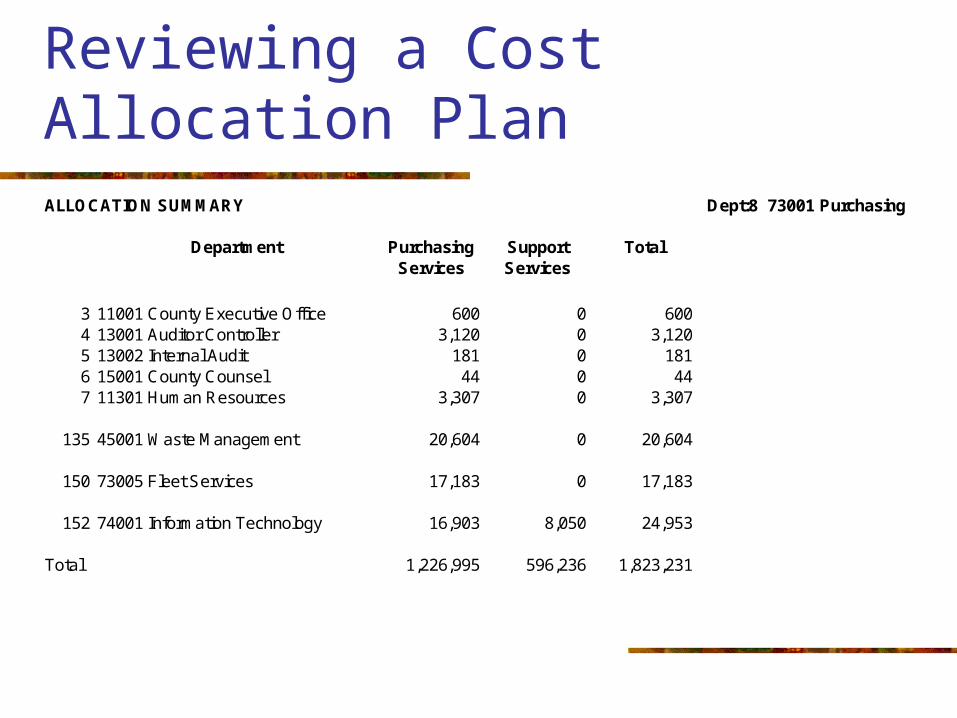

Reviewing a Cost Allocation PlanALLOCATION SUMMARY Dept:8 73001 Purchasing

Department Purchasing Services

Support Services

Total

3 11001 County Executive Office 600 0 6004 13001 Auditor Controller 3,120 0 3,1205 13002 Internal Audit 181 0 1816 15001 County Counsel 44 0 447 11301 Human Resources 3,307 0 3,307

135 45001 Waste Management 20,604 0 20,604

150 73005 Fleet Services 17,183 0 17,183

152 74001 Information Technology 16,903 8,050 24,953

Total 1,226,995 596,236 1,823,231

Results of Cost Allocation Plans

Identify annual dollar amount of general fund support (indirect, administrative, overhead) allocated to benefiting departments, divisions or programs.

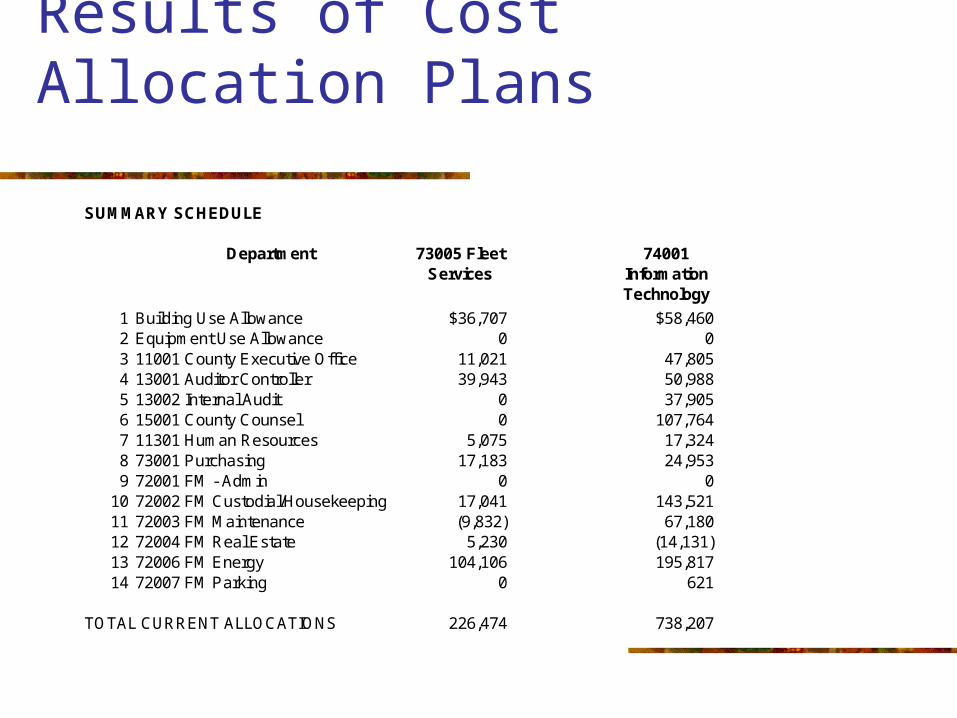

Results of Cost Allocation Plans

SUMMARY SCHEDULE

Department 73005 Fleet Services

74001 Information Technology

1 Building Use Allowance $36,707 $58,4602 Equipment Use Allowance 0 03 11001 County Executive Office 11,021 47,8054 13001 Auditor Controller 39,943 50,9885 13002 Internal Audit 0 37,9056 15001 County Counsel 0 107,7647 11301 Human Resources 5,075 17,3248 73001 Purchasing 17,183 24,9539 72001 FM - Admin 0 0

10 72002 FM Custodial/Housekeeping 17,041 143,52111 72003 FM Maintenance (9,832) 67,18012 72004 FM Real Estate 5,230 (14,131)13 72006 FM Energy 104,106 195,81714 72007 FM Parking 0 621

TOTAL CURRENT ALLOCATIONS 226,474 738,207

Applications of Cost Allocation

Request reimbursement from Federal and State grants Transfer dollars from non-general funds to general

fund Understand true or full cost of providing services

Subsidy decisions Resource allocation Performance measures

Integrate into user fee calculations Integrate into SB90 claims

OMB A-87 vs. Full Cost

Two types of cost allocation plans:

1. OMB A-87 Cost Allocation Plan

2. Full Cost Allocation Plan

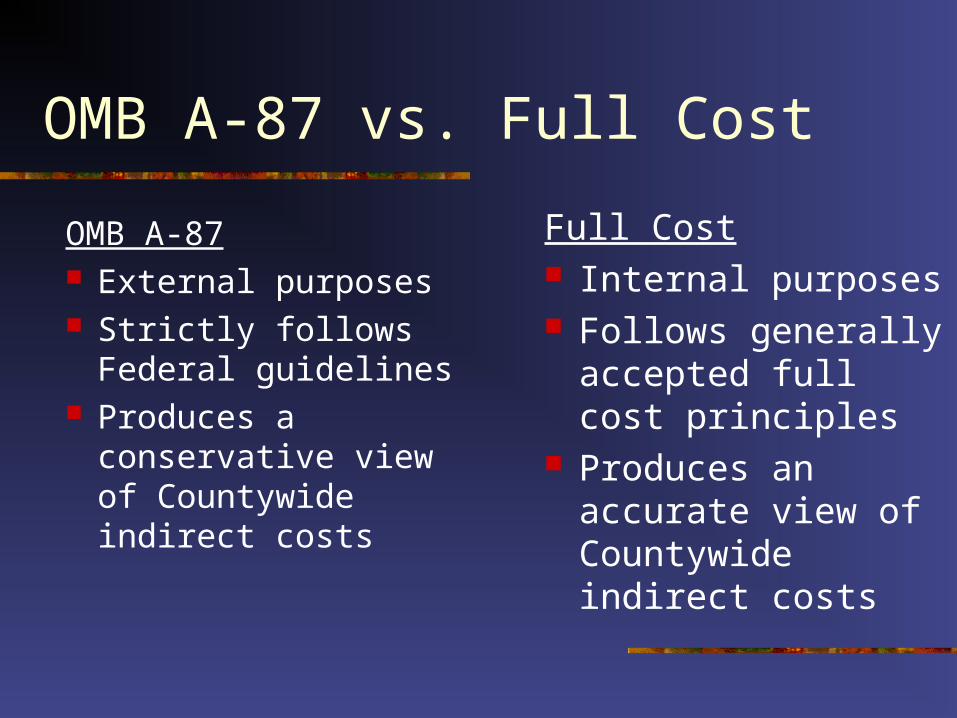

OMB A-87 vs. Full Cost

OMB A-87 External purposes Strictly follows Federal

guidelines Produces a conservative

view of Countywide indirect costs

Full Cost Internal purposes Follows generally

accepted full cost principles

Produces an accurate view of Countywide indirect costs

OMB A-87 vs. Full Cost

OMB Excludes Auditors Office Treasurers Office Board of Supervisors County Executive

~ Amount Excluded 15% 100% 100% 31%

Full Cost ~ 15% less than OMB

Cost Allocation Quiz

The cost allocation plan identifies and distributes ____________ costs.

Cost Allocation Quiz

The cost allocation plan identifies and distributes indirect costs.

Cost Allocation Quiz

Indirect costs are also referred to as _____________, _____________, and/or ___________________ costs.

Cost Allocation Quiz

Indirect costs are also referred to as administrative, support, and/or overhead costs.

Cost Allocation Quiz

What is a department that typically has indirect costs?

Cost Allocation Quiz

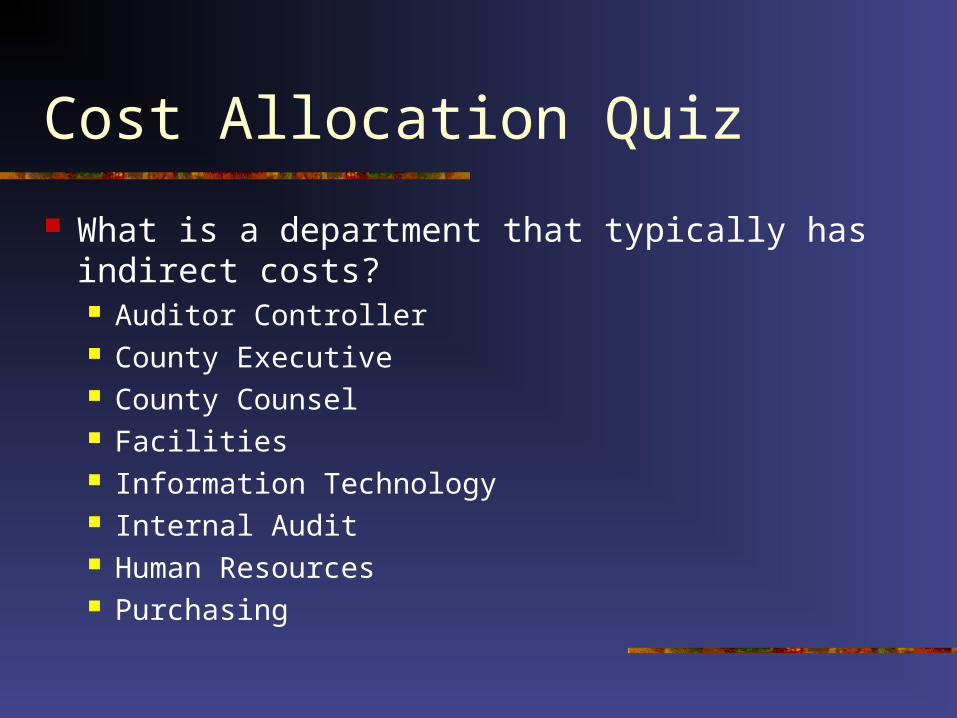

What is a department that typically has indirect costs? Auditor Controller County Executive County Counsel Facilities Information Technology Internal Audit Human Resources Purchasing

Cost Allocation Quiz

What are the reasons for preparing an annual cost allocation plan?

Cost Allocation Quiz

What are the reasons for preparing an annual cost allocation plan? Request reimbursement from Federal and State grants Transfer dollars from non-general funds to general fund

Understand true or full cost of providing services Subsidy decisions Resource allocation Performance measures

Integrate into user fee calculations Integrate into SB90 claims

Cost Allocation Quiz

Who at the County can you contact with questions or to review the cost allocation plan?

Cost Allocation Quiz

Who at the County can you contact with questions or to review the cost allocation plan? Teresita Soriano