robert jahoda vupsv, v.v.i

DESCRIPTION

Model Situations of Families with Small Children Regarding Earnings When Caring Parent Enters Labour Market. Robert Jahoda VUPSV, v.v.i. Presentation Contents. Theory – Model Evaluation of Labour Market Entry Conditions Practical Examples Household 2+2; Prague Household 1+1; Prague - PowerPoint PPT PresentationTRANSCRIPT

Model Situations of Families with Small Children Regarding Earnings When

Caring Parent Enters Labour Market

Robert JahodaVUPSV, v.v.i

Presentation Contents

1. Theory – Model Evaluation of Labour Market Entry Conditions

2. Practical Examples– Household 2+2; Prague– Household 1+1; Prague– Household 2+3; Zlín– Household 1+1; Municipality up to

10,000 inhabitants

3. Conclusions and Discussion2

Maternal Employment Rates by Age of Youngest Child, 2007 (OECD; Family Database)

3

Financial Stimuli by Labour Market Entry

• Change of tax payment (social and health insurance + income tax)

• Costs of childcare (scope of services vs. price)

• Costs of commuting (?)

• Deciding about work – optimizing process how many options can they choose from?

• Loss of parental allowances (?)

• Reduction of other state social support allowances (?)

• Decreased allowances of assistance in material need (?)

• Financial stimuli are not the only factor in the family decision making

4

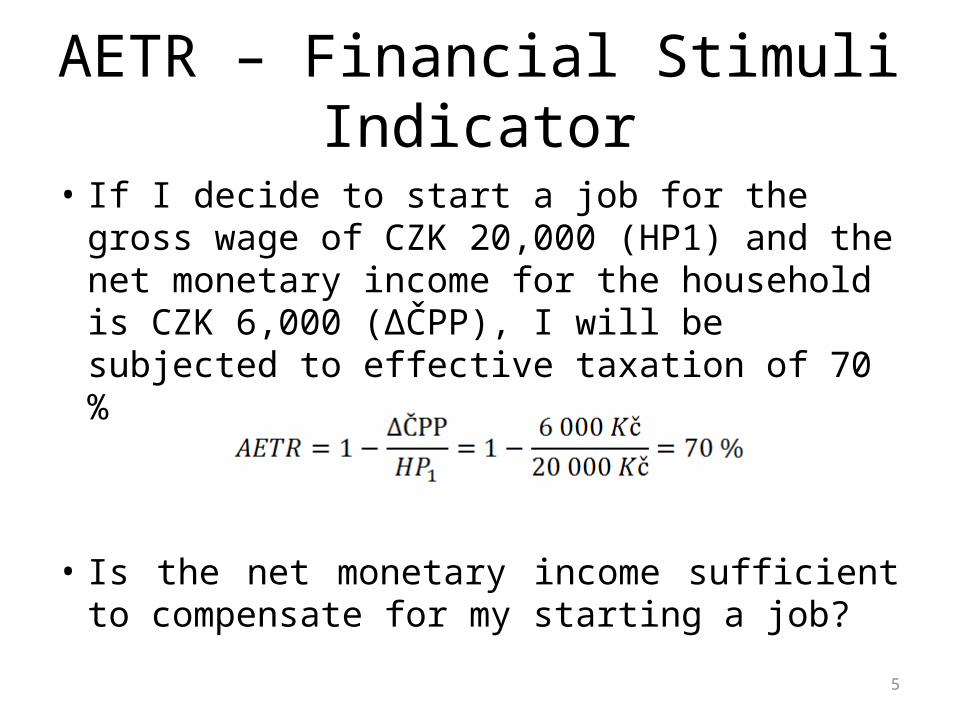

AETR – Financial Stimuli Indicator

• If I decide to start a job for the gross wage of CZK 20,000 (HP1) and the net monetary income for the household is CZK 6,000 (ΔČPP), I will be subjected to effective taxation of 70 %

• Is the net monetary income sufficient to compensate for my starting a job?

5

What do we know about households receiving family allowances?

• Structure• Education• Housing and costs• Income differentiation

6

Model Households• A household with children, one is 2 years old• The woman is deciding whether to enter the

labour market• By entering the labour market, she can expect an

income that will depend, among others, on:– Scope of employment – Abilities (education)– Regional labour market

• QUESTION: What effective taxation will the household be subjected to if its earned income is x % of the income median (CZK 20,000)

7

Effective Taxation and its Decompositionfamily 2+2; home ownership in Prague; college education;

partner's wage is 150 % of the median; higher parental allowance assessment; private childminding CZK 12,000

8

Effective Taxation for Various Levels of Partner's Income

family 2+2; home ownership in Prague; college education; higher parental allowance assessment; private childminding CZK 12,000

9

Effective Taxation for Various Levels of Partner's Income

family 2+2; home ownership in Prague; college education; higher parental allowance assessment; private childminding CZK 12,000

10

Effective Taxation for Various Levels of Partner's Income

family 2+2; home ownership in Prague; college education; higher parental allowance assessment; private childminding CZK 12,000

11

Effective Taxation for Various Levels of Partner's Income

family 2+2; home ownership in Prague; college education; higher parental allowance assessment; private childminding CZK 12,000

12

Effective Taxation and its Decomposition family 2+2; home ownership in Prague; college education; partner's wage is 0 % of the median;

higher parental allowance assessment; private childminding CZK 12,000

13

Effective Taxation and its Decompositionfamily 2+2; home ownership in Prague; college education; partner's wage is 0 % of the median;

higher parental allowance assessment; private childminding CZK 12,000

14

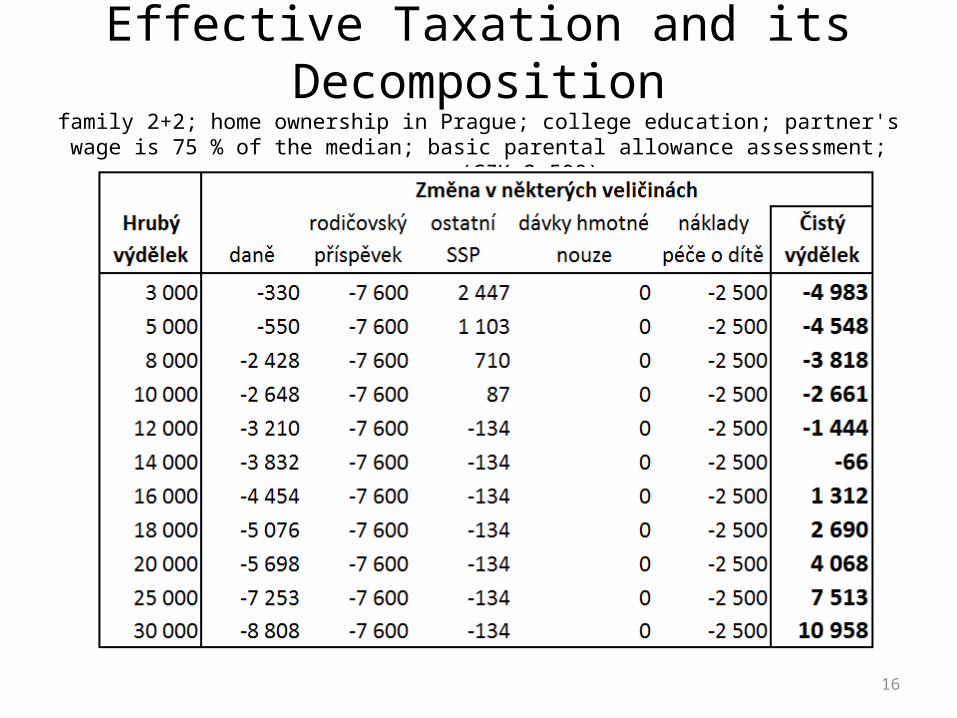

Effective Taxation and its Decompositionfamily 2+2; home ownership in Prague; college education;

partner's wage is 75 % of the median; basic parental allowance assessment; nursery (CZK 2,500)

15

Effective Taxation and its Decompositionfamily 2+2; home ownership in Prague; college education; partner's wage is 75 % of the median;

basic parental allowance assessment; nursery (CZK 2,500)

16

Effective Taxationfamily 1+1; tenement in Prague; secondary education with a graduation exam;

basic parental allowance assessment; nursery (CZK 2,500)

17

Net Income and its Decompositionfamily 1+1; tenement in Prague; secondary education with a graduation exam;

basic parental allowance assessment; nursery (CZK 2,500)

18

Effective Taxation and its Decompositionfamily 2+3+2; home ownership in Zlín (+ parents); apprentice education; partner's wage is 75 %

of the median; basic parental allowance assessment; a childminding grandmother

19

Effective Taxation and its Decompositionfamily 1+1+2; living with parents in a small town; apprentice education; basic parental allowance

assessment; a childminding grandmothercosts for commuting CZK 3,000

20

Conclusions and Discussion• The decision about entering

the labour market is influenced mainly by the costs of childcare together with the entitlement to parental allowances

• The impact of other allowances is limited – the beneficiary is rarely poverty-stricken

• The tax system "discourages" from part-time employment

TYPICAL CASE• Loss of parental allowance:

CZK 7,600• Nursery costs: CZK 2,500• Loss of tax discount for the

"partner": CZK 2,070 xxxxxxxxxxxxxxxxxxxxxxxxx• TOTAL: CZK 12,170

21

Financial Impact - State

• A woman on parental leave from the perspective of the state:– Saved costs for nurseries (carried by the

establisher)– Lower tax revenues – the model does not include

social and health insurance paid by employers (34 %)

– Duty to pay the health insurance for the woman on parental leave

22

THANK YOU FOR YOUR ATTENTION

23