rome june 4 - europa

TRANSCRIPT

Pier Carlo Padoan

Deputy Secretary-General and

Chief Economist, OECD

European Parliament

Addressing macroeconomic

imbalances in Europe

20 January, 2014 - Brussels

2

Growth prospects remain strongest in the

emerging economies, weak in EU

Projected change in real GDP in 2014-15 Annual average, per cent

1. BRIICS countries comprise Brazil, China, India, Indonesia, Russia and South Africa.

Source: OECD Economic Outlook database 94.

CHN IND MEX KOR ZAF USA POL AUS SWE CAN SVK BRA IRL HUN DNK FIN FRA ITA ESP NLD-1

0

1

2

3

4

5

6

7

8

-1

0

1

2

3

4

5

6

7

8

IDN CHL TUR ISR EST NZL NOR ISL RUS CHE GBR LUX AUT DEU CZE BEL JPN PRT GRC SVN

BRIICS1

Euro area countries

Other OECD member countries

3

The current recovery is still weak by past

standards…

Note: The point labelled “t” on the horizontal axis corresponds to the pre-recession peak quarter for each cycle.

Source: OECD National Accounts database.

OECD-wide real GDP, relative to pre-recession peak Per cent

-5

0

5

10

15

20

-5

0

5

10

15

201970s; Peak at 1974Q3 1980s; Peak at 1981Q3

1990s; Peak at 1990Q4 2000s; Peak at 2008Q1

4

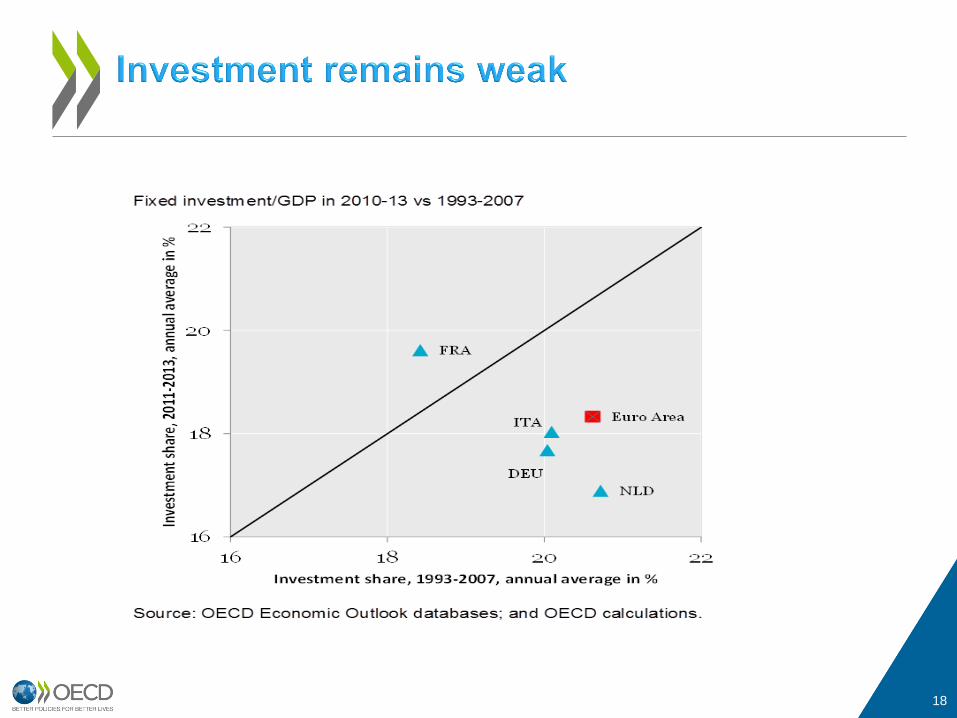

Weakness in investment…

OECD-wide fixed investment Volume, 2007 = 100

Note: Fixed investment values are the weighted average of OECD member countries, where the weights are GDP

measured at 2005 PPP USD.

Source: OECD Economic Outlook 94 database, OECD Foreign Direct Investment (FDI) Statistics.

World FDI flows Index of USD values, 2007 = 100

75

80

85

90

95

100

105

75

80

85

90

95

100

105

0

20

40

60

80

100

120

0

20

40

60

80

100

120

5

Credit lagging in EA …

Bank loans to non-financial private sector 2007 = 100

80

85

90

95

100

105

110

Euro area United States Japan

Note: Major OECD economies is calculated as the weighted average of the indices (2007 = 100) of nominal bank credit

to the non-financial private sector for the United States, the euro area and Japan, where the weights are GDP in 2007

measured at USD PPP.

Source: Datastream and European Central Bank.

80

85

90

95

100

105

110

Major OECD economies

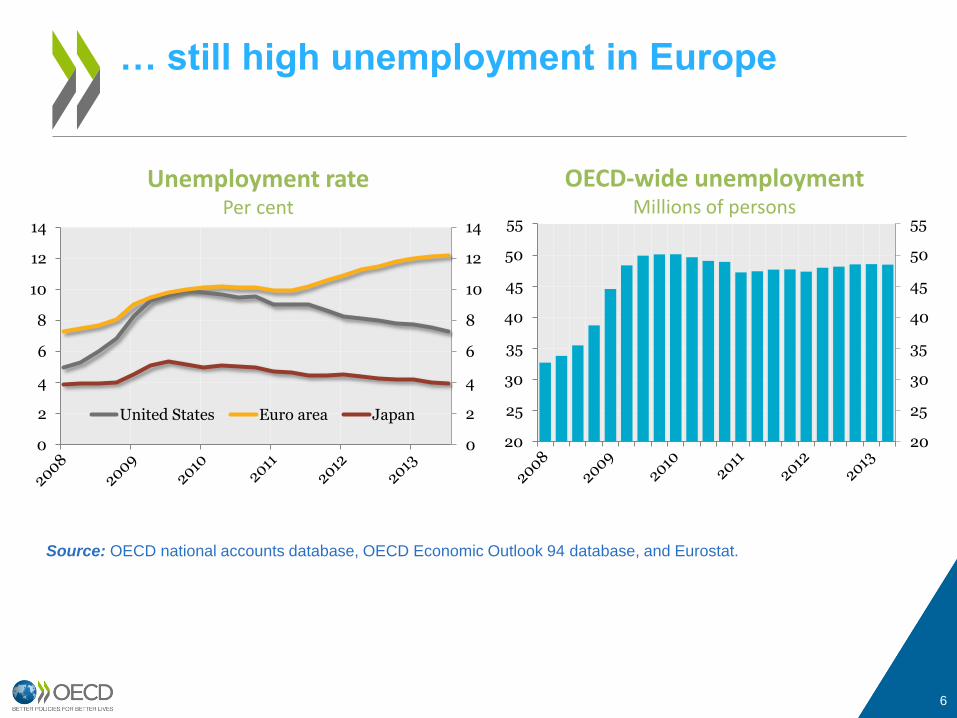

6

… still high unemployment in Europe

Unemployment rate Per cent

Source: OECD national accounts database, OECD Economic Outlook 94 database, and Eurostat.

0

2

4

6

8

10

12

14

0

2

4

6

8

10

12

14

United States Euro area Japan

OECD-wide unemployment Millions of persons

20

25

30

35

40

45

50

55

20

25

30

35

40

45

50

55

7

CA imbalances (misallocation)

Fragmentation (credit market imbalances)

Competitiveness (structural imbalances)

Adjustment, macroeconomic and structural

EA macroeconomic imbalances

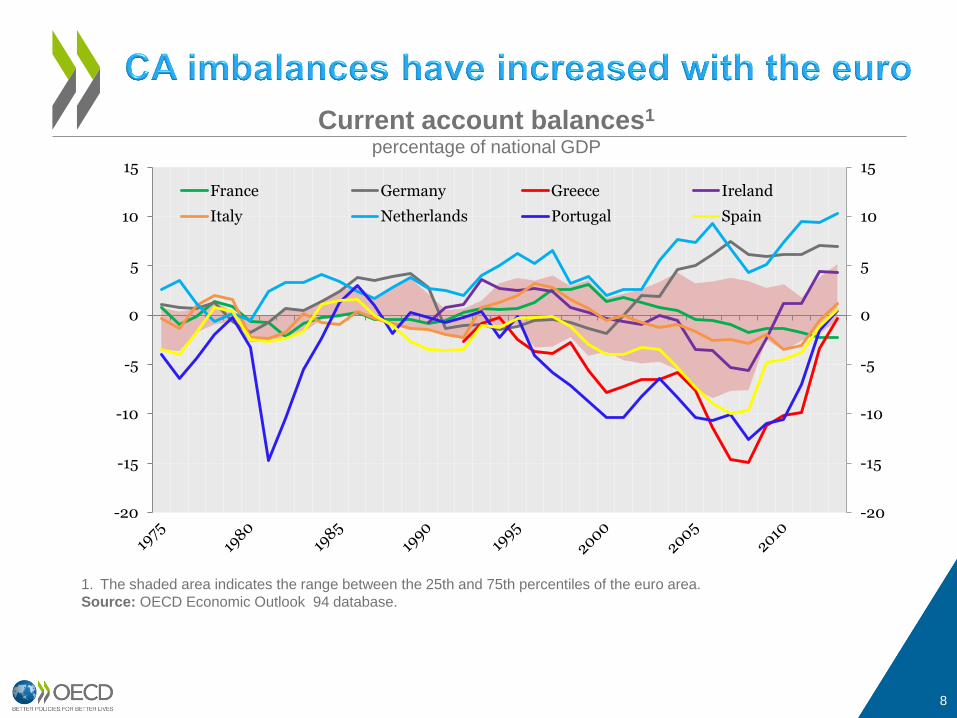

8

Current account balances1 percentage of national GDP

1. The shaded area indicates the range between the 25th and 75th percentiles of the euro area.

Source: OECD Economic Outlook 94 database.

-20

-15

-10

-5

0

5

10

15

-20

-15

-10

-5

0

5

10

15

France Germany Greece Ireland

Italy Netherlands Portugal Spain

9

In the EA, CA imbalances reflected divergence

in growth and competitiveness...

Source: OECD Economic Outlook 94database.

AUT

BEL

FIN

FRA

DEU

GRC IRL

ITA NLD PRT

SVK

SVN

ESP

0

1

2

3

4

5

6

7

-10 -5 0 5 10 15

To

tal

do

me

sti

c d

em

an

d g

ro

wth

, %

Current account balance, % of GDP

Unweighted average

Change in total domestic demand and unit labour cost in relation to

current account balance, Annual average, 2002-2007

AUT

BEL

FIN FRA

DEU

GRC

IRL

ITA

NLD

PRT

ESP

-2

-1

0

1

2

3

4

5

-10 -5 0 5 10

ch

an

ge

in

no

min

al

un

it l

ab

ou

r c

os

t, %

Current account balance, % of GDP

Eu

ro a

rea

av

era

ge

10

... in interest rates and loan accumulation

External balances, interest rate gaps and loan growth Annual average, 2002-07

1. Interest rate gap defined as the deviation of short-term interest rates from a simple Taylor rule with coefficients of 0.5 on the

output and inflation gaps, a core HICP inflation target of 1.9% and neutral real interest rate of 2.1%.

Source: OECD Economic Outlook 94 database; European Central Bank.

AUT BEL FIN

FRA

DEU

GRC

IRL

ITA NLD PRT

ESP

-3,5

-3,0

-2,5

-2,0

-1,5

-1,0

-0,5

0,0

-10 -5 0 5

Inte

re

st

ra

te g

ap

1

Current account balance, % of GDP

AUT

BEL

FIN

FRA

DEU

GRC

IRL

ITA NLD PRT

ESP

-5

0

5

10

15

20

25

-10 -5 0 5 10

Gr

ow

th o

f M

FIs

lo

an

s t

o n

on

MF

Is,

%

Current account balance, % of GDP

11

Markets assessments have increasingly

reflected CA imbalances, sovereign debt

dynamics and systemic factors

Sovereign bond yields percentage points

0

10

20

30

40

0

10

20

30

40DEU ESP FRA GRC

IRL ITA PRT

Note: Sovereign bond is 10-year benchmark government bond.

Source: Datastream.

12

Risk assessments have spilled over into private

funding conditions, aggravating divergence and

hindering rebalancing

Interest rates on loans to non-financial corporations Per cent

1

3

5

7

1

3

5

7

DEU ESP FRA IRL

ITA PRT GRC

Note: Interest rate is defined as an interest rate on new loans to non-financial corporations

(all maturities) with the exception of Greece where it refers to new loans with maturity of up

to one year.

Source: European Central Bank.

13

Sovereign spreads and yields have gone down in periphery reflecting market optimism. But credit fragmentation remains

The Asset Quality Review and stress tests must be implemented rigorously – and followed up by bank recapitalisation where needed

Further progress must be made on establishing a fully fledged banking union with an adequate joint fiscal backstop

Addressing fragmentation requires

financial repair…

14

…and real adjustment. EA countries have

made progress on structural reform…

Responsiveness to Going for Growth recommendations, 2011-12 Adjusted for the difficulty of undertaking reform¹

1. The adjusted responsiveness rate is calculated as the share of recommendations in Going for Growth 2011

for which 'significant' action has been taken, where each recommendation is weighted by the inverse of average

responsiveness to priorities in this area in non-crisis circumstances, in order to reflect the fact that some areas of

reform are more difficult than others. The euro area and OECD rates are calculated as an unweighted average;

the OECD rate is not adjusted.

Source: OECD Going for Growth 2013.

0,0

0,5

1,0

0,0

0,5

1,0

GRC IRL PRT ESP ITA Euroarea

OECD

15

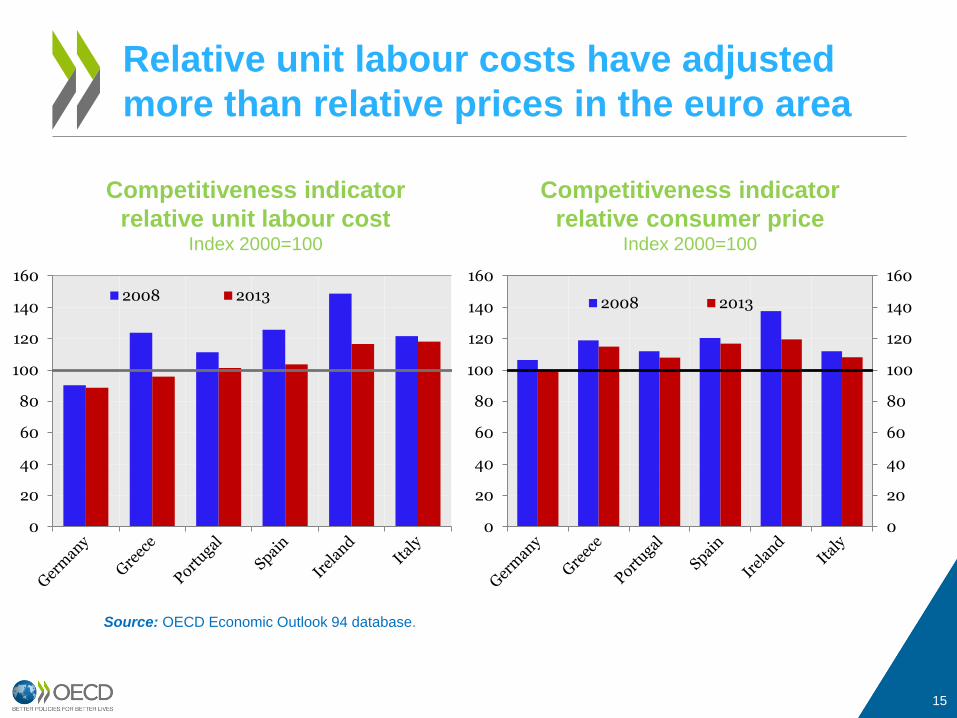

Relative unit labour costs have adjusted

more than relative prices in the euro area

Competitiveness indicator

relative unit labour cost Index 2000=100

Competitiveness indicator

relative consumer price Index 2000=100

0

20

40

60

80

100

120

140

160

2008 2013

0

20

40

60

80

100

120

140

160

0

20

40

60

80

100

120

140

160

2008 2013

Source: OECD Economic Outlook 94 database.

16

Structural reforms are assisting

internal rebalancing…

Contributions to improvement in net exports since 2007-081

In per cent of 2007-08 euro area GDP1

1. The values shown are the changes between Q4 2007 – Q3 2008 and Q3 2012 – Q2 2013.

Source: OECD Economic Outlook 94 database.

-0,5

0,0

0,5

1,0

1,5

-0,5

0,0

0,5

1,0

1,5

Greece Ireland Italy Portugal Spain

Fall in imports Rise in exports Change in net exports

17

Although adjustment must be more

symmetric

Current account balance/GDP Per cent, 4-quarter moving average

Source: OECD National Accounts database.

-20

-15

-10

-5

0

5

10

-20

-15

-10

-5

0

5

10

DEU GRC ITA PRT ESP

18

19

ADDITIONAL SLIDES

20

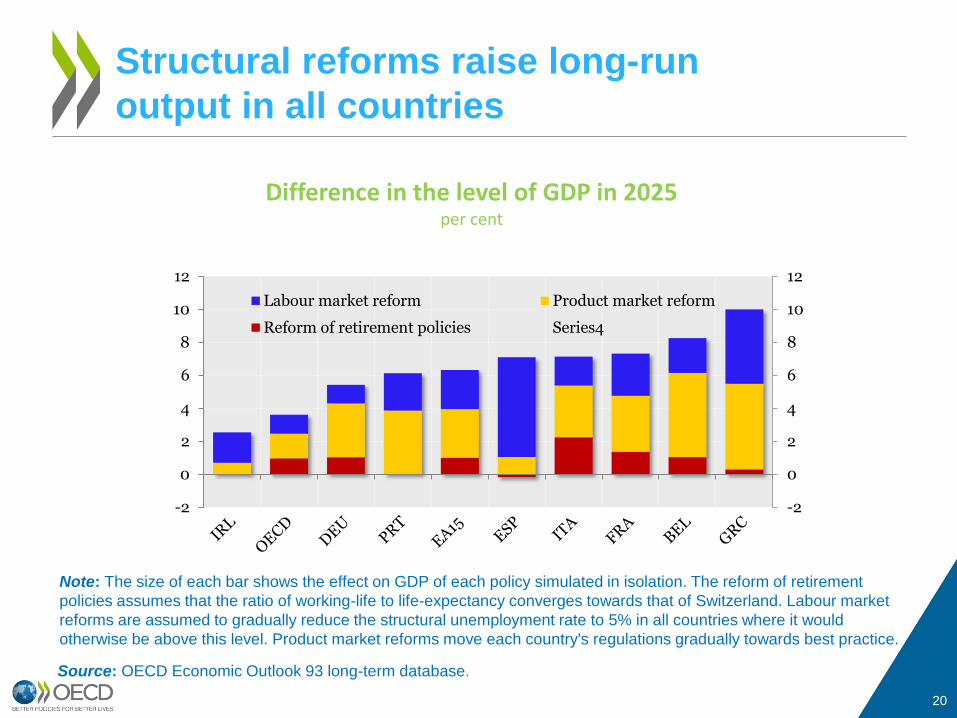

Structural reforms raise long-run

output in all countries

Source: OECD Economic Outlook 93 long-term database.

Difference in the level of GDP in 2025 per cent

Note: The size of each bar shows the effect on GDP of each policy simulated in isolation. The reform of retirement

policies assumes that the ratio of working-life to life-expectancy converges towards that of Switzerland. Labour market

reforms are assumed to gradually reduce the structural unemployment rate to 5% in all countries where it would

otherwise be above this level. Product market reforms move each country's regulations gradually towards best practice.

-2

0

2

4

6

8

10

12

-2

0

2

4

6

8

10

12

Labour market reform Product market reform

Reform of retirement policies Series4

21

SR can produce benefit (higher growth) also in the short

term but full impact takes time

SR impact requires confidence (e.g. product market

reforms increase investment opportunities through more

competition, but investment requires confidence… and

finance)

SR impact can be limited if financial markets are not

repaired

SR short term impact may be weak if activity is low

Political and economic contagion can frustrate reform

efforts if market confidence does not improve

22

SR more intense in crisis countries, but risk of

reform fatigue

SR effort limited in core surplus countries.

“excessive competitiveness” ?

Contractual agreements?

Stronger links to budget consolidation?

More Single Market pressure?

New trade agreements can accelerate the

agenda ?

Incentives for structural reforms