russia’s oil&gas development and exports trends · 2019. 2. 1. · 32,2% 31,3% 18,6% 18,4%...

TRANSCRIPT

Alexey GROMOV,PhD, Principal Director on Energy Studies

Institute for Energy and Finance

Russia’s Oil&Gas Development and Exports Trends

The Eleventh Japan-Russia Energy and Environment Dialogue (JREED)Niigata, Japan

30th January 2019

1

Oil Industry1

Gas Industry2

Global oil market context

Russian oil production and export trends up to 2023

EU Gas market trends

Russian gas production and export trends up to 2023

R1-GROMOVEleventh Japan–Russia Energy and Environment Dialogue in Niigata

©ERINA

2

20

30

40

50

60

70

80

90

01/

15

03/

15

05/

15

07/

15

09/

15

11/

15

01/

16

03/

16

05/

16

07/

16

09/

16

11/

16

01/

17

03/

17

05/

17

07/

17

09/

17

11/

17

01/

18

03/

18

05/

18

07/

18

09/

18

11/

18

$/bblBrent WTI

OPEC+ Agreement Update (December

2018)OPEC+

Agreement (December

2016)

OECD commercial stocks reduction

Decreaseduring 2015

OPEC+ Agreement Update

(June 2018)

OPEC+ Agreement has a crucial role to stabilize the global oil market

• OPEC+ Agreement (December 2016) to cut collective oil production of 1,8 MMb/d supported global oil prices and reduced price volatility in1Q2017- 1Q2018.

• The threat of US sanctions against Iranian oil exports led to OPEC+ Agreement Update in June 2018 (increase collective oil production of 1MMb/d).

• New OPEC+ Agreement Update (December 2018) to cut collective oil production of 1,2 MMb/d has to reduce the oil market volatility in 2019

OPEC+ Agreement Update in December 2018 lead to gradually balancing the global oil market in 2019

Снижение предложения/увеличение спроса Увеличение предложения/снижение спроса

0,7

-0,4

-0,4

-0,8

-0,1

+0,2+0,2 0,35

0,75

+0,4

+0,3

-0,2 +0,3

+0,40,1

0,4

+1,2

-0,1 +0,1+0,2

-0,5

+0,2

-0,0 +0,2 +0,3-0,1

-2.0

-1.6

-1.2

-0.8

-0.4

0.0

0.4

0.8

1.2

1.6

2.0

ОПЕК Не ОПЕК*

США ОПЕК Не ОПЕК*

США ОПЕК Не ОПЕК*

США ОПЕК Не ОПЕК*

США

4Q2018

Спрос Предложение 1Q2019

Спрос Предложение 2Q2019

Спрос Предложение 3Q2019

Спрос Предложение 4Q2019

Доп. ростспроса

Changes in global liquid fuels market balance

Decrease in supply /Increase in demand Increase in supply/Decrease in demand

* Not including USSource: IEF estimates bases on EIA, МЭА, ОПЕК data

3

D D D D

Notes:

D - Demand

OPEC OPEC OPEC OPECUS US US USNonOPEC

NonOPEC

NonOPEC

NonOPEC

Supply Supply Supply Supply

Mbd

R1-GROMOVEleventh Japan–Russia Energy and Environment Dialogue in Niigata

©ERINA

4

Russiaʼs Role in the OPEC+ Agreement

Russia’s share in the collective oil production cuts planned in 2017 within OPEC+ Agreement (tbd)

Level of Russian compliance with initial OPEC+ Agreement production cut target, 2017-18

Source: IHS Markit

1Q 2017 – 1Q 2018

• Russia played central role bringing aboutOPEC and non-OPEC output reduction dealsof December 2016

• Russia pledged to gradually lower output by300,000 b/d during first half of 2017compared with October 2016 level (largestnon-OPEC reduction)

• Russia with Saudi Arabia now apparently co-determining OPEC+ policy

OPEC+ Agreement Update (June 2018)

• Russia and Saudi Arabia ensured theimplementation of ‘Vienna Alliance’ members’decision to increase the collective oilproduction of 1MMbd in coming months

• Russia exceeds October 2016 baseline forproduction cuts for first time in October 2018,setting new oil output record of 11,6 MMb/d(activating most spare capacity built upduring period of output cuts)

OPEC+ Agreement Update (December 2018)

• Russia played central role to reach new Updatefor OPEC+ Agreement (restart of collective oiloutput cuts of 1,2 MMb/d from January 2019)

5

Oil Industry1

Gas Industry2

Global oil market context

Russian oil production and export trends up to 2023

EU Gas market trends

Russian gas production and export trends up to 2023

R1-GROMOVEleventh Japan–Russia Energy and Environment Dialogue in Niigata

©ERINA

Russian oil production back to growth in 2018

Russia’ crude oil production, 1989-2018 Russian oil production cuts withinOPEC+Agreement led to oil production decreasein 2017 up to 546,2 MMt (-0,3% y-o-y), for the firsttime in last 10 years

But Russian oil production back to growth in 2018and ensured new annual oil output record of 556MMt (11,35 MMb/d) due to the activation of mostspare capacity built up during period of output cuts

After 10 years of decline the Western Siberia’ oiloutput back to growth in 2018 due to increase oilproduction in Yamalo-Nenets AO

Greenfield expansion have supported the raise of oiloutput in the Eastern Siberia (Suzun and Vankor) andon Caspian onshore (Filanovsky’ field)

Russia’ crude oil production by key oil&gas regions, 2014-17

0

100

200

300

400

500

600

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

MMt CRUDE OIL LEASE CONDENSATE

Sources: Rosstat, Russian Ministry of Energy, FIEF 6

32,2% 31,3%

18,6% 18,4%

11,4% 10,5%

0

50

100

150

200

250

300

350

2014 2017 2014 2017 2014 2017 2014 2017Western Siberia Ural-Volga Eastern Siberia and

Far EastTiman-Pechora

MMtlower 1 MMt 1-2 MMt

2-5 MMt more 5 MMt

7

Gazprom Neft is the main driver of oil productionʼ increase

Oil output by Russian Oil&Gas Majors, 2008-17

Sources: Rosstat, companies’ data, FIEF estimations

Gazprom Neft is the main driver of Russian oilproduction’ increase (+9 MMt in 2015-17)

Rosneft continue to develop Vankor oil cluster: oiloutput at the Suzun field raised by 4 times up to 4,14 MMt,at the Tagul field – by 9 times up to 0,34 MMt

Sakhalin PSAs had increased oil output in 2017 as well asindependent Russian producers including JV with Japaneseinvestors (INPEX, ITOCHU, JOGMEC)

Nevertheless, oil production by Rosneft, LUKOIL andSurgutneftegas decreased during this period due toOPEC+ cuts and oil output decline at the WesternSiberia

In 2017-18 OPEX by Russian majors have stabilized atthe level of 3-4$/bbl

Russian majors have kept their costs at such a low level dueto pressure on contractors who are forced to reduce priceseven in the face of rising world oil prices and volumes ofwork performed

OPEX/bbl in upstream by Russian Oil&Gas Majors, 2014-18

113 115 116 118 121204 202 200 222 221

90 92 90 85 84 85 86 86 83 82

62 60 60 61 61 61 61 62 62 6146 47 49 49 50 49 51 54 58 60

48 51 57 62 65 61 65 69 77 76

0

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Others Gazprom Tatneft

Gazprom Neft Surgutneftegaz LUKOIL

Bashneft TNK-BP Rosneft

MMt

3.2

4.2

3.7

4.3

2

4

6

8

2014 2015 2016 2017 2018

Rosneft LUKOIL

Gazprom Neft Tatneft$/bbl

R1-GROMOVEleventh Japan–Russia Energy and Environment Dialogue in Niigata

©ERINA

8

Idling of wells was the main instrument to achieve 2017 OPEC+ production cuts

Change in Russian idle well count by company, October 2016-September 2018

Deactivation of (most likely marginal) wells waskey method for achieving production cuts in 2017

Russia’s idle well count jumped by over 5,000between October 2016 and January 2018

Idle well rate rose from 12,5% in October2016 to 15,2% in January 2018

Sharp drop in idle well count in 2018 coincidedwith main period of Russian oil productiongrowth in 2018

Russia’s idle well count has fallen over 3,000since January 2018

Idle well rate down to 13,2% in September2018

Tatneft and Rosneft have registered biggestreductions in idle well numbers in 2018, indicatingnew brownfield investment focus by thiscompanies

Sources: IHS Markit, FIEF

New field development activity up significantly in 2017 despite cuts

9

Oil production at new felds inRussia,2016-18Indexes for new oil field activity in Russia, 2016-18

Development drilling at new fields in Russia, 2016-18 New well completions at new fields in Russia, 2016-18

Sources: TEK Rossii

R1-GROMOVEleventh Japan–Russia Energy and Environment Dialogue in Niigata

©ERINA

10

Tax Reform ʻBig Maneuvreʼ is neutral for Russian upstream

Sources: Finance Ministry, IHS Markit

Starting from 2019 the export duty on oil will bemultiplied by a reduction factor

Starting from 2023, the export duty will be reset

Lower oil export duty will lead to higherdomestic oil prices (net back), and alignmentof domestic oil prices and world prices (lesslogistics costs)

To compensate budget losses due to the reductionof export duties on oil, a new component isintroduced into the MET (DM coefficient)- KMAN,which actually repeats the formula for calculatingthe export duty on oil

As a result, the overall tax burden on oilproduction will not change

Tax reform for mature oil fields: The Samotlor tax break

Russia’s current oil sector tax system, based on grossrevenues of production, particularly burdensome formature field producers

Samotlor oil field has obtained (2017) major tax reliefpackage in exchange of Rosneft promise to investmore heavily in this field redevelopment

• Finance Ministry agreed to annual METreduction for Samotlor oil field of 35 trillionrubles (around $0,6 billion) and set to last for10 years

Finance Minsitry of Russia promised to revisitquestion of comparable tax breaks for othermature fields in three years, after evaluatingimpact of Samotlor experiment on federal budget

Samotlor oil production and decline rate

Rosneft committed to drill about 2,400 new wells andproduce an incremental 50 MMt (365 MMbbd) at Samotlorfield during next 10 years

11

CAPEX in Upstream: from stagnation in 2016 to acceleration in 2017

CAPEX in upstream by Russian Oil&Gas Majors,2010-17

Sources: Rosstat, companies’ data, FIEF estimations

In 2017, investments in oil production increased by13% y-o-y, reaching 1.9 trillion rubles

Rosneft became the leader in the dynamics of capitalinvestments (+29% y-o-y)

LUKOIL significantly increased investments (+11%y-o-y)

Other majors reduced investments in oil production

The key areas of Rosneft's investments were themaintenance of production at the old fields of WesternSiberia and the development of the Vankor cluster

In 2017, LUKOIL continued to increase investments inold fields of Western Siberia (116.4 billion rubles, +28.4%y-o-y) and the Caspian sea shelf (55.9 billion rubles, +35% y-o-y)

Some (-9% y-o-y) decline in investment in GazpromNeft's production projects was due to the completion ofthe Novoportovskoye field infrastructure

CAPEX/bbl in upstream by Russian Oil&Gas Majors, 2014-18

188 240 276 330 350 456608

786119149

220 265328

292284

315

132178

239228

208

146166 173

187206

209

199

160 271

325

377 300

355

0

500

1,000

1,500

2,000

2010 2011 2012 2013 2014 2015 2016 2017

billions rubles

Others Tatneft Surgutneftegas Gazprom Neft

LUKOIL Bashneft TNK-BP Rosneft

7.5

7.1

7.4

3.3

2

4

6

8

10

12

14

2014 2015 2016 2017 2018

Rosneft LUKOIL

Gazprom Neft Tatneft

$/bbl

R1-GROMOVEleventh Japan–Russia Energy and Environment Dialogue in Niigata

©ERINA

12

CAPEX trends up to 2023: growth will continue

CAPEX in upstream (facts and forecast), 2013-23 In 2019-23, investments in oil production will grow by 39%

(+14% in real terms) due to the implementation of large-scale programs for the development of productioncapacities of Gazprom Neft and Rosneft

Rosneft plans to increase oil and gas condensate productionto 250 MMt by 2025 (+29 MMt by 2017) by introducing newfields in Eastern Siberia and increasing production at oldfields in Western Siberia (Samotlor)

In 2018, Gazprom Neft announced the postponement toachieve oil production of 100 MMt from 2020 to 2021-22(mainly due to the OPEC+ cuts), while production in Russiawill total 75-80 MMt. The main production gains will beensured by new projects in the Yamalo-Nenets AO (Taz,North Samburgskoe)

Capex/bbl for Russian majors remains significantlylower than that of the largest international oilcompanies, as in the portfolio of Russian majors' projectsare still dominated by traditional oil fields (Western Siberia,Eastern Siberia) with relatively low exploitation costs

Average CAPEX/bbl in upstream by companies, 2015-17

3.45.1

6.37.4

8.29.0

14.415.115.515.6

16.419.019.3

25.726.8

0 5 10 15 20 25 30

TatneftRosneft

Russia (2015-2017)LUKOIL

Russia (2023)Gazprom Neft

SinopecExxonMobilPetroChina

ENIPetrobras

StatoilBP

ChevronTotal

$/bbl

Sources: Rosstat, companies’ data, FIEF estimations

990

1,14

6

1,32

8

1,39

2

1,56

2

1,70

8

1,80

0

1,89

5

2,07

6

2,21

6

2,33

7

223283

329 291338

381406

433481

522559

0

500

1,000

1,500

2,000

2,500

3,000

2013

2014

2015

2016

2017

2018

*

2019

2020

2021

2022

2023

billion rubles Oil related services Upstream

13

Russian oil production outlook up to 2023

Crude oil production by Rosneft, MMt

Crude oil production by LUKOIL, MMt

Crude oil production by Gazprom Neft, MMt

Russian crude oil production (facts and forecast), 2013-23

6075

0

20

40

60

80

2017 2022

млн т

82 86

0

20

40

60

80

100

2017 2022

млн т

221 250

0

50

100

150

200

250

2017 2022

млн т

Sources: Rosstat, companies’ data, FIEF estimations

522 526 535 548 546 556 561 566 569 571 573

0

100

200

300

400

500

600

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

MMt

R1-GROMOVEleventh Japan–Russia Energy and Environment Dialogue in Niigata

©ERINA

14

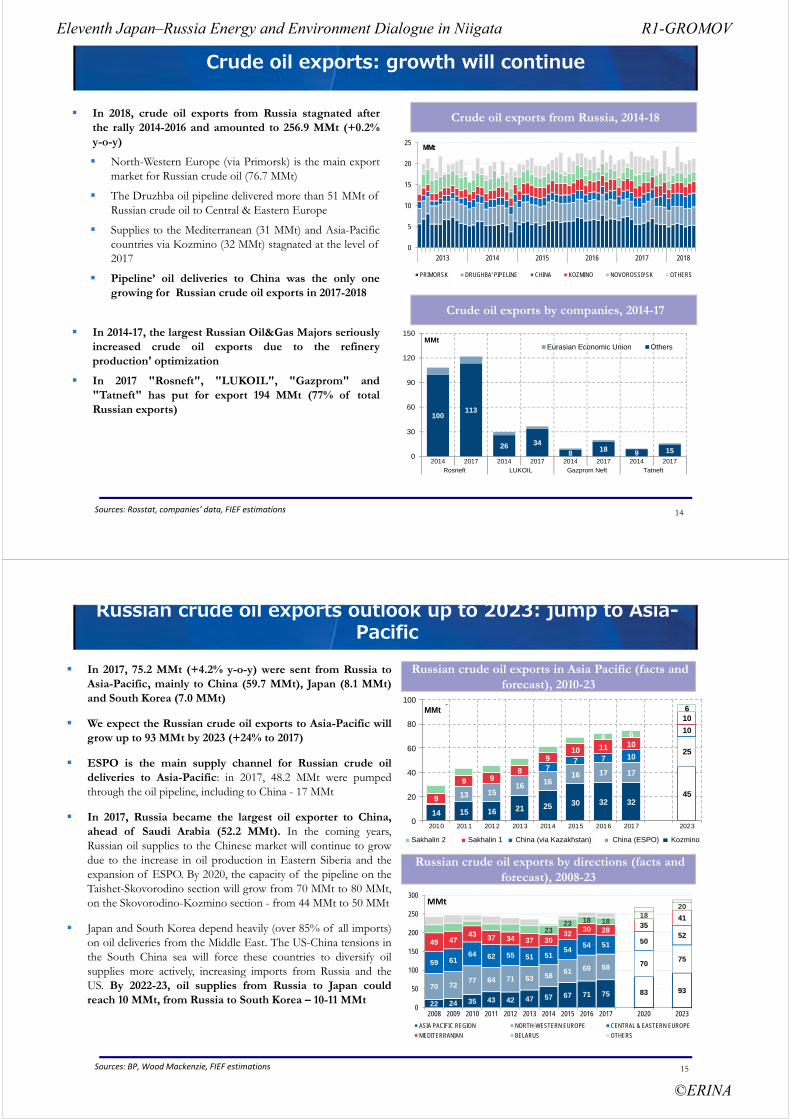

Crude oil exports: growth will continue

Crude oil exports from Russia, 2014-18 In 2018, crude oil exports from Russia stagnated afterthe rally 2014-2016 and amounted to 256.9 MMt (+0.2%y-o-y)

North-Western Europe (via Primorsk) is the main exportmarket for Russian crude oil (76.7 MMt)

The Druzhba oil pipeline delivered more than 51 MMt ofRussian crude oil to Central & Eastern Europe

Supplies to the Mediterranean (31 MMt) and Asia-Pacificcountries via Kozmino (32 MMt) stagnated at the level of2017

Pipeline’ oil deliveries to Сhina was the only onegrowing for Russian crude oil exports in 2017-2018

In 2014-17, the largest Russian Oil&Gas Majors seriouslyincreased crude oil exports due to the refineryproduction' optimization

In 2017 "Rosneft", "LUKOIL", "Gazprom" and"Tatneft" has put for export 194 MMt (77% of totalRussian exports)

Crude oil exports by companies, 2014-17

0

5

10

15

20

25

2013 2014 2015 2016 2017 2018

MMt

PRIMORSK DRUGHBA' PIPELINE CHINA KOZMINO NOVOROSSIYSK OTHERS

100113

26 34

8 18 9 150

30

60

90

120

150

2014 2017 2014 2017 2014 2017 2014 2017Rosneft LUKOIL Gazprom Neft Tatneft

MMtEurasian Economic Union Others

Sources: Rosstat, companies’ data, FIEF estimations

15

Russian crude oil exports outlook up to 2023: jump to Asia-Pacific

Russian crude oil exports in Asia Pacific (facts and forecast), 2010-23

In 2017, 75.2 MMt (+4.2% y-o-y) were sent from Russia toAsia-Pacific, mainly to China (59.7 MMt), Japan (8.1 MMt)and South Korea (7.0 MMt)

We expect the Russian crude oil exports to Asia-Pacific willgrow up to 93 MMt by 2023 (+24% to 2017)

ESPO is the main supply channel for Russian crude oildeliveries to Asia-Pacific: in 2017, 48.2 MMt were pumpedthrough the oil pipeline, including to China - 17 MMt

In 2017, Russia became the largest oil exporter to China,ahead of Saudi Arabia (52.2 MMt). In the coming years,Russian oil supplies to the Chinese market will continue to growdue to the increase in oil production in Eastern Siberia and theexpansion of ESPO. By 2020, the capacity of the pipeline on theTaishet-Skovorodino section will grow from 70 MMt to 80 MMt,on the Skovorodino-Kozmino section - from 44 MMt to 50 MMt

Japan and South Korea depend heavily (over 85% of all imports)on oil deliveries from the Middle East. The US-China tensions inthe South China sea will force these countries to diversify oilsupplies more actively, increasing imports from Russia and theUS. By 2022-23, oil supplies from Russia to Japan couldreach 10 MMt, from Russia to South Korea – 10-11 MMt

Russian crude oil exports by directions (facts and forecast), 2008-23

Sources: ВР, Wood Mackenzie, FIEF estimations

14 15 16 21 25 30 32 324513 15

16 1616 17 17

25

77 7 10

10

9

9 98

910 11 10

10

6 6

6

0

20

40

60

80

100

2010 2011 2012 2013 2014 2015 2016 2017 2023

млн т

Пригородное Де-Кастри Китай (через Казахстан) Китай (ВСТО) Козьмино

22 24 35 43 42 47 57 67 71 75 83 9370 7277 64 71 63 58

61 69 68 707559 61

64 62 55 51 5154

54 51 5052

49 4743 37 34 37 30

3230 28

3541

2323 18 18

1820

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2020 2023

MMt

ASIA PACIFIC REGION NORTH-WESTERN EUROPE CENTRAL & EASTERN EUROPE

MEDITERRANIAN BELARUS OTHERS

Sakhalin 2 Sakhalin 1 China (via Kazakhstan) China (ESPO) Kozmino

MMt

R1-GROMOVEleventh Japan–Russia Energy and Environment Dialogue in Niigata

©ERINA

16

Russian petroleum products output and exports outlook up to 2023

Russian petroleum products output (facts and forexcast), 2015-23

In 2018, Russian refinery industry shifts to growth afterthree years of decline

In 2018, the primary oil refining increased to 286.9 MMt(+2.5% y-o-y)

The return to growth was facilitated by the recovery ofworld oil prices (as a result, the oil refining marginincreased)

In 2019-20, the primary oil refining will stabilize at thelevel of 290-293 MMt, but since 2020, it will again beginto fall

The main causes are high competition with refineries fromthe Middle East and oversupply of petroleum products inthe domestic market

In 2019-20, the exports of petroleum products willstabilize at the level of 150 MMt, but since 2021, theexports of petroleum products will decline following thefall of refinery production

We expect the most significant decrease in the supply offuel oil up to 36 MMt to 2023, while the exports of dieseland gasoline will grow slightly

Russian petroleum products exports (facts and forecast), 2015-23

Sources: Rosstat, FIEF estimations

39 39 38 [ЗНАЧЕНИЕ] 41 42 43 44 45

76 76 77 77 80 82 84 86 88

72 57 51 47 44 39 36 33 30

100 113 118 124 128 129 126 122 117

0

100

200

300

2015 2016 2017 2018 2019 2020 2021 2022 2023

MMt Others Fuel Oil Gasoil/Diesel Gasoline

51 49 51 54 56 57 57 58 59

8972 63 56 52 48 44 40 36

27

3130 36 38 37 35 33 28

0

50

100

150

200

2015 2016 2017 2018 2019 2020 2021 2022 2023

MMtOthers Fuel Oil Gasoil/Diesel Gasoline

17

Oil Industry1

Gas Industry2

Global market trends

Russian oil production and export trends up to 2023

EU Gas market trends

Russian gas production and export trends up to 2023

R1-GROMOVEleventh Japan–Russia Energy and Environment Dialogue in Niigata

©ERINA

18

EU gas demand outlook: the recovery will continue up to 2023

According to preliminary estimates, in 2018, the growthof gas demand in the EU continued and amounted to 494bcm (+0.6% y-o-y)

In the next 5 years, power sector will remain the maindriver of gas demand in the EU

In the longer term, the gas demand in the Europeantransport sector also will slightly increase

However, in the long term the total EU gas demand willnot increase significantly due to the continued raise ofrenewable energy use, as well as energy efficiencyimprovements

In June 2018, the EU approved legally binding targets forthe development of RES up to 2035

The main goal is to achieve the share of RES in the EUfinal energy consumption at the level of 32% by 2030

According to the European Commission, in 2016 the shareof RES in the EU final energy consumption was 17.04%

This decision may have a negative impact on the long-termprospects of gas demand in the EU

EU gas demand (facts and forecast), 2007-30

EU power industry gas demand (facts and forecast), 2010-23

Source: European Commission

542491 494 492

217

0

100

200

300

400

500

600

2010

2011

2012

2013

2014

2015

2016

2017

2018

*

2030П

Bcm

ENTSO-G (ST scenario) WEO NPS BP Energy Outlook 2018

186171

145129 121 123

147 156 151 152 164 159 161 165

0

50

100

150

200

2010

2011

2012

2013

2014

2015

2016

2017

2018

*

2019

2020

2021

2022

2023

Bcm

19

Oil Industry1

Gas Industry2

Global market trends

Russian oil production and export trends up to 2023

EU Gas market trends

Russian gas production and export trends up to 2023

R1-GROMOVEleventh Japan–Russia Energy and Environment Dialogue in Niigata

©ERINA

20

Gazprom is the leader in Russian gas production growth in 2018

In 2018, Russian gas production reached a new all-timerecord of more than 725.2 Bcm (+34 Bcm or +4.9% y-o-y)

The main increase in production was provided by Gazprom(+30 Bcm or +6,5% y-o-y)

Independent gas producers and oil companies maintained thegas production at 2017’ level

In 2018, according to our estimates, domestic gas demand(including the needs of the gas transportation system and gasinjection into UGS) increased by 4.0% y-o-y

In 2018, Gazprom's gas supplies to the domestic marketalso increased significantly, mainly due to a reduction in gassupplies from independent gas producers

After the launch of Yamal LNG project, NOVATEKreoriented the significant part of gas deliveries from thedomestic market to LNG exports

Rosneft faced difficulties in increasing production and wasforced to conclude an agreement with Gazprom for thepurchase of gas of 5 Bcm

We expect that Russian domestic gas demand will remainstable in the range of 470-480 Bcm in the forecast perspective

Russian gas production by months, 2016-18

Russian gas production by companies, 2012-18

40

45

50

55

60

65

70

Janu

ary

Febr

uary

Mar

ch

April

May

June July

Augu

st

Sept

embe

r

Oct

ober

Nov

embe

r

Dec

embe

r

Bcm 2018 2017 2016

Historical range 2011-2017

Sources: TEK Rossii, companies’ data, FIEF estimations

482 476 432 406 406 441 470

655 669 641 636 641 691725

0

150

300

450

600

750

2012

2013

2014

2015

2016

2017

2018

Bcm

Oil companies (total) GazpromNOVATEK Other producers (incl. JVs)PSA (Sakhalin 1 & Sakhalin 2)

21

Russian gas production outlook up to 2023

In 2019-2023, Russian gas production will grow slightlyfaster than predicted before and will reach the range744-755 Bcm by 2023 (+2,6-4,1% to 2018)

In the coming years, Gazprom's production in the WesternSiberia will be supported by launching the spare capacity ofNadym-Pur-Taz fields, especially Zapolyarnoye andUrengoy fields

NOVATEK plans to develop Utrennee field which will bethe resource base for the Arctic-2 LNG Project on GydanPeninsula

Rosneft gas production is likely to be stable in 2018, while Rospan full expansion planned for 2019

After 2021-2022, the main increase in gas productionwill be ensured by Eastern Siberia and the Far Eastmainly due to the commissioning of theChayandinskoye and Kovykta fields, as well asincreasing the production of APG in the oil fields

Gazprom’ current spare capacity (~100 Bcm) willfacilitate required production growth in the near tomedium term up to 2023

Russian gas production (facts & forecast), 2008-23

Russian gas production outlook by regions, 2015-23

Sources: Ministry of Economic Development of the Russian Federation, Gazprom, companies’ data, FIEF estimations

725

755

744

600

625

650

675

700

725

750

775

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Bcm

FIEF forecast Ministry forecast (2017)

608 615 666 685 687 678 664 656 648

48 64 76 89 107

0

200

400

600

800

2015 2016 2017 2018 2019 2020 2021 2022 2023

Bcm

Western Siberia & European part of Russia Eastern Siberia & Far East

R1-GROMOVEleventh Japan–Russia Energy and Environment Dialogue in Niigata

©ERINA

22

Russian gas exports : facts & forecast

In 2018 Russian gas export increased up to 260 Bcm(+7,7% y-o-y)

Gazprom set a new record with pipeline exports to Europereaching more than 200 Bcm (+5,6% y-o-y)

LNG exports (26 Bcm) are expanding fast (+62,1% y-o-y)following the launch of two trains on Yamal LNG

Exports to former Soviet republics (CIS) stable, with noofficial supply to Ukraine (although deliveries continue toseparatist areas in east)

Pipeline exports to Europe have been rising since 2014setting records for three consecutive years,emphasizing Russia’s critical supply role with theadvantage of incumbency in contractual relations, low-cost gas and flexibility of supply

Offshore section of Turk Stream is finished, Nord Stream 2 isbeing constructed; but transit through Ukraine will still berequired, therefore solution for new transit arrangements mustbe found before end of 2019

In 2019-2021, we expect stabilization of exports volumesof Russian pipeline gas at the current level but after 2021the pipeline gas exports will grow again due to thecommissioning of Power of Siberia project oriented toChina

Russian gas exports, 2012-18

Russian gas exports by pipeline to Europe (non-CIS)

145167 154 159 179 192 201

6053

41 3429

30 321515

14 1515

1626

0255075

100125150175200225250275

2012 2013 2014 2015 2016 2017 2018

Bcm

Europe & Turkey by pipeline Former soviet republics & Baltic states LNG

Sources: Gazprom, IHS Markit, FIEF estimations

23

Russian gas shift to the East: both pipeline and LNG projects are progressing

Russia is pushing several options for gas exports to Asia-Pacific markets: total potential almost 200 Bcm/y(95 Bcm/y by pipe to China and South Korea and over 100 Bcm/y of LNG exports) by 2035

Gazprom’s Power of Siberia project (38 Bcm/y) is being built on budget and on time and expected to begin deliveries in late 2019, in line with agreement. Ramp-up period will depend on Chinese market

Active negotiation is ongoing about expansion of Power of Siberia and other routes including Power of Siberia 2 (Altay pipeline, 30 Bcm/y) and additional eastern route for Sakhalin gas from Dalnerechensk (6-8 Bcm/y)

Gazprom and KOGAS have revived negotiations on a new export gas pipeline. Russian gas could become the most competitive source of gas, depending on what pipeline route is selected; the most efficient one involves transit through North Korean territory

Yamal LNG has launched all three large-scale trains ahead of schedule

FID for Arctic LNG-2 expected in 2019

Russia perceives a significant opportunity in global LNG market: it has a potential to develop 100 MMtpa by 2030,capturing half of global incremental demand.

Long-term success of Russian LNG projects in Arctic targeting Asia-Pacific markets largely depends on commercial navigation of Northern Sea Route

R1-GROMOVEleventh Japan–Russia Energy and Environment Dialogue in Niigata

©ERINA