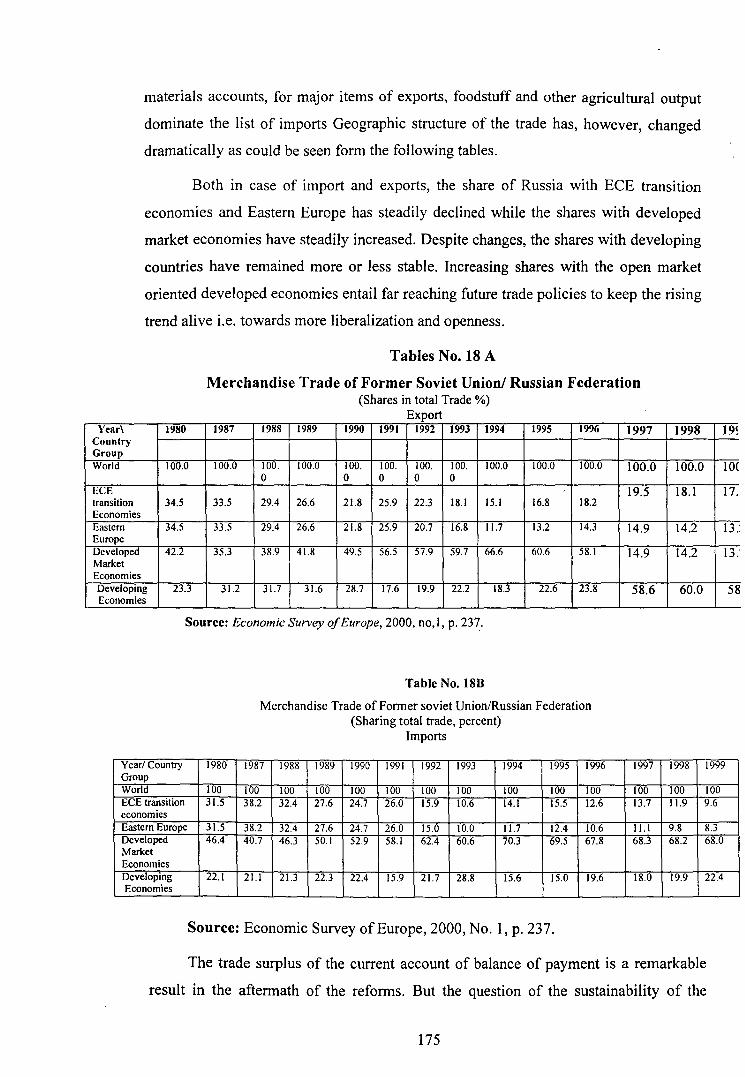

russian foreign trade in post-reform...

TRANSCRIPT

CHAPTER-4

RUSSIAN FOREIGN TRADE IN POST- REFORM ERA

In the process of transformation to a market system in Russia is inseparably

linked with the question of foreign trade. As the country's foreign trade regime

represents an integral component of the institutional and economic order now under

going renewal. The form it takes must be determined by the same principles and

objectives, which include contractual freedom, price liberalistion, competition and

privatisation. The fundamental feature of the transformation is stipulated that Russian

economy should be opened up to the world market. This is a sine quo non for the

desired change of system while at the same time acting as a source of new impulses

and, to a certain extent, as a guarantor for the success of the entire transformation

process.

Importance and Functions of Foreign Trade

The Russian economy's closer links in future with the world market ought

primarily to be regarded as a significant opportunity for economic and technological

progress. This is true even though this great country. with its huge domestic market is

less dependent upon foreign trade than smaller economi~s.

Fundamentally, foreign trade has a number of important functions to fulfill in the

stabilization of the economy as a whole. These derive first and foremost from the price

effects induced by foreign trade on the goods and factors markets alike, which can be

regarded as introducing international value standards into the economy. Ultimately,

more significant one the allocation effects induced on the basis of those price changes

leading to a transformation of the sectoral structures of production. This requires

fulfillment of certain prerequisite conditions which include removal of monopolistic

structures greater mobility of factors of production and the like. In future, however,

exploitation of the potential productivity impulses generated by foreign trade certainly

could be capable of setting welfare enhancing effects in motion, particularly when this

challenge is deliberately met head-on. After all, foreign trade guarantees a supply of

goods which would never be possible under conditions of autarky opening up

completely new opportunities for Russia's business enterprises and consumers. For

129

Russia too increasing real incomes and a rising demand for goods can be achieved with

the help of foreign trade, even if these improvements are intrinsically confined to those

areas closely associated with such trade.

Foreign Trade in Pre-reform Era

Russia is not only the most important successor states to the USSR with regard

to foreign trade but has also inherited the greater proportion of its economic potential.

Russia, today accounts for 76 per cent of Soviet Union's territory, 51 per cent of the

population, 59 per cent of the Gross National Product, 66 per cent of industrial

production and 46 per cent of agricultural production. 1 The largest reserv.es of oil, gas,

coal, gold, diamonds, timber and other natural resources identified in the USSR are

located in Russian territory. As om.: would therefore, expect Russia used to achieve

more than two-thirds of the former Soviet Union's foreign trade turn over, or more

specifically 78.9 per cent of export and 57.8 per cent ofimports.2

The foreign trade of Russia in the past is almost the foreign trade of the Soviet

Union as a whole and therefore the past performance of foreign trade of USSR is

reflection of the trade performance of Russian federation. A brief review of the USSR's

trade regime prior to reforms will invariable shed light on the trade performance etc. of

Russia for the above reasons. Further, the position taken up by Russia in the past

explains why all of the problems stemming from the planned economy past of the

Soviet Union have affected primarily Russia's Present foreign trade situation. Before

giving to the teething troubles of pre-reform era and underlining the new economic

order in the post-reform era, it is very essential to highlight the trade situation of USSR

vis-a-vis that of Eastern Europe & rest of world in the pre-reform era.

1 Klaus Werner, "Russia's Foreign Trade and the Economic Refonns," Intereconomics, vol. 28, no. 3 (May- June 1993), p.l46 2 'b'd I I ., p.l46.

130

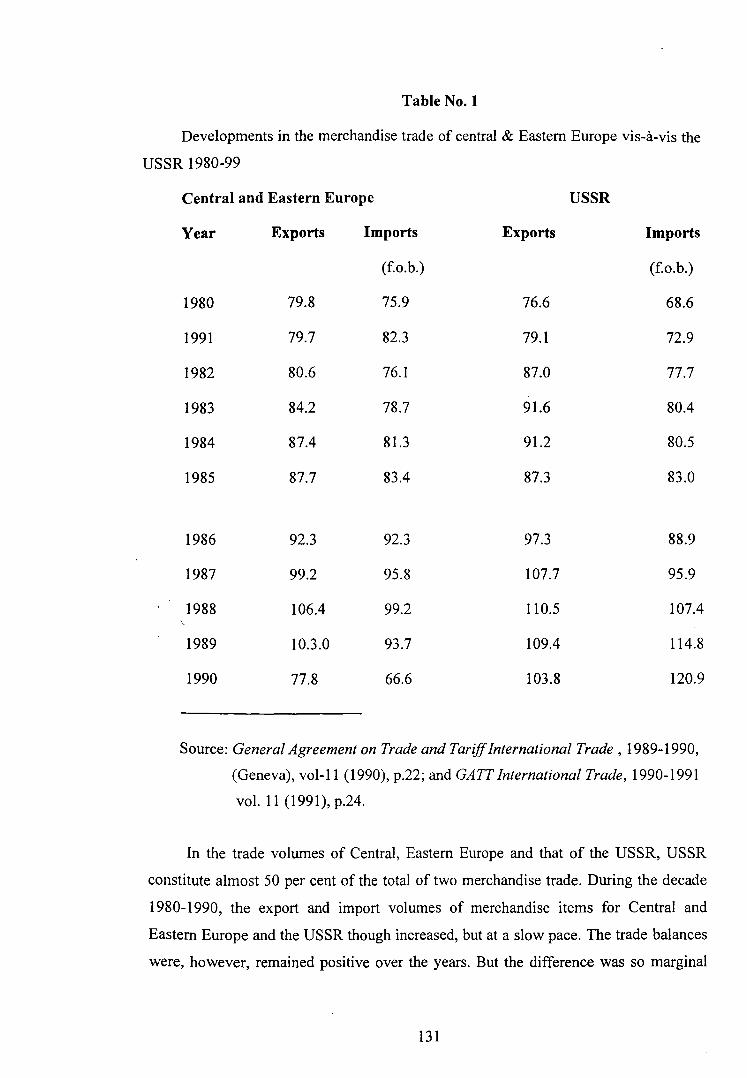

Table No.1

Developments in the merchandise trade of central & Eastern Europe vis-a-vis the

USSR 1980-99

Central and Eastern Europe

Year

1980

1991

1982

1983

1984

1985

1986

1987

1988

1989

1990

Exports

79.8

79.7

80.6

84.2

87.4

87.7

92.3

99.2

106.4

10.3.0

77.8

Imports

(f.o.b.)

75.9

82.3

76.1

78.7

81.3

83.4

92.3

95.8

99.2

93.7

66.6

Exports

76.6

79.1

87.0

91.6

91.2

87.3

97.3

107.7

110.5

109.4

103.8

USSR

Imports

(f.o.b.)

68.6

72.9

77.7

80.4

80.5

83.0

88.9

95.9

107.4

114.8

120.9

Source: General Agreement on Trade and Tariff International Trade , 1989-1990,

(Geneva), vol-11 (1990), p.22; and GATT International Trade, 1990-1991

vol. 11 (1991), p.24.

In the trade volumes of Central, Eastern Europe and that of the USSR, USSR

constitute almost 50 per cent of the total of two merchandise trade. During the decade

1980-1990, the export and import volumes of merchandise items for Central and

Eastern Europe and the USSR though increased, but at a slow pace. The trade balances

were, however, remained positive over the years. But the difference was so marginal

131

that it won't be wrong to describe the situation as passing on sword's edge. Thus,

everywhere they were creeping into stage from stage zero or negative balances and

moving thereby towards a phase of trade crisis.

The value of exports and imports though went on rising due to the exchange

rate variations, the share of trade declined considerably and continuously during the

mid eighties and late eighties which is clear from the following Table No.2. The value

of export for the whole region though started increasing from $178 bn to in 1985 to $

212 bn in 1989. It fell to$ 182 bn in 1990.

Between 1973-1985, the combined trade of Eastern Europe and the USSR

expanded in volume terms, more rapidly than the world trade. Both exports from and

imports into this region grew at an annual average rate of some 4 'l2 per cent as

compared with 3 per cent for world trade. Moreover, neither of the two recessions in

world trade (1975& 1982) significantly affected the trade of Eastern Europe and the

USSR. Not until 1985 did the volume of exports from the region decline, and then only

it started declining.

In value terms, the rate of growth of both exports and imports of Eastern Europe

and the USSR as a whole had slowed down to 1 'l2 per cent in 1984. Mainly due to

substantial reductions in shipments from Poland and the USSR, aggregate exports from

the area declined by some 2 'l2 per cent in 1935.3 Whereas imports into Eastern Europe

and the USSR recovered somewhat (up 3 ·per cent) under the combined effect of

accelerating imports into Bulgaria and a reversal of the declines in imports into

Hungary and the USSR.

With regard to trade data expressed in dollars, it should be kept in mind that

dollar unit values of both imports and exports of Eastern Europe and the USSR

increased less rapidly between 1973 and 1985 than those of world trade. This is due to

the areas trade structure and the pricing system used in intra-area exchanges and intra

area trade between Eastern Europe and the USSR, which did not change much in value

terms during the period under review, represented nearly 55 per cent of the area's

exports in 1985. more importantly the share of fuels in the area's intra-trade has

increased from 8 per cent in 1973 to about 25% in 1985. Although based on world

prices, fuel prices for intra-trade are calculated using a five year moving average. As a

3 GATT, International Trade, 1985-86 (Geneva, 1986), p.105.

132

result, when there is any change in world prices, there is a lag in the effect on intra-area

prices, (GATT, International Trade, 1985-86, pp.l05-106).

Table No.2

Share of Eastern Europe and USSR Trade in the World Trade

Year Trade value in bn $ Share in world trade (%)

Export Import Export Import

1985 178 171 9\12 8\12

1987 215 200 8\12 7\12

1988 226 214 8 7

1989 212 208 7 6\12

1990 182 187 5 5

Source: GATT, International Trade, 1985-86 (Geneva, 1986), p. 104; GATT,

International Trade, 1987-88, (1988), p. 57; GATT, International Trade, 1989-

90, (1990); and GATT, International Trade, 1990-91, (1991), p.23;

Volume of import also showed a rising trend and remained below the export

value amounting to positive trade balance except for the year 1990 where a deficit to

the tune of $ 65 was noticed. The share of export for the Eastern Europe and USSR

though was 9 \12% in 1985, it declined to 5% within a span of 5 years.

After intra-Central and Eastern Europe and USSR, it is the Western Europe

which accounts for 26 \12 per cent of the total exports of USSR and Eastern Europe

countries. The average annual change on the export during 19980-1988 to the Western

Europe found to be only 1\12 per cent and 11 per cent during 1989 over 1980-88. The

merchandise exports of the Eastern Europe and the USSR as on 1989 by destination is

summarised in the following table

133

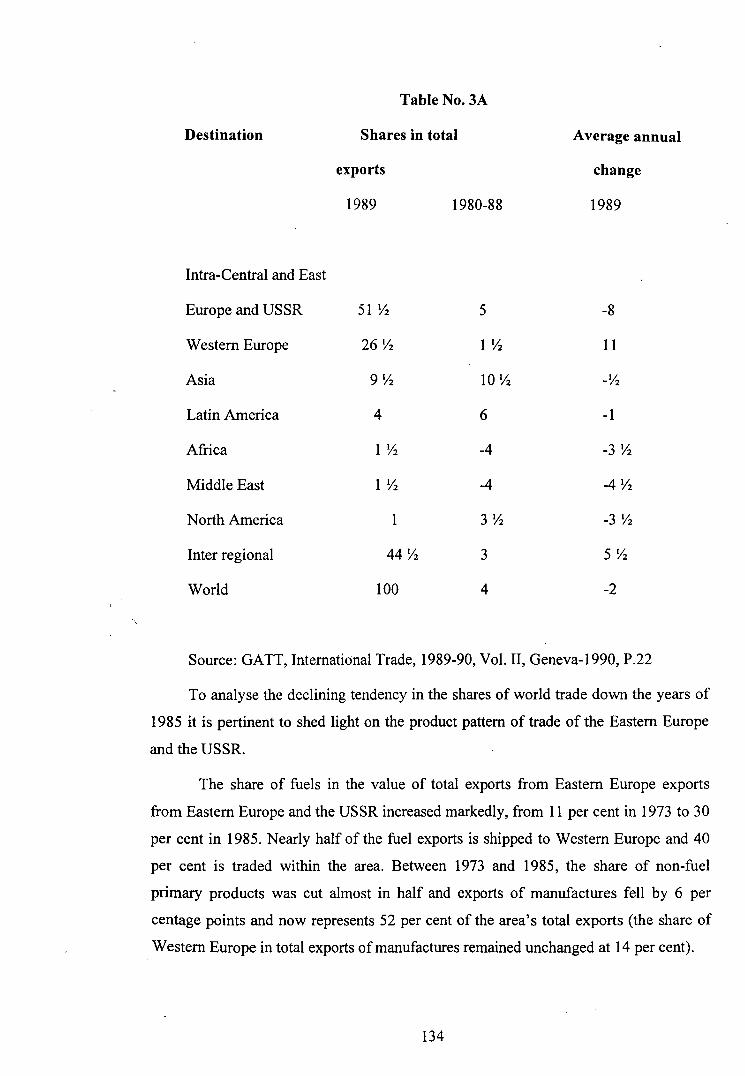

Table No. 3A

Destination Shares in total

exports

1989 1980-88

Intra-Central and East

Europe and USSR 51 'li 5

Western Europe 26 'li 1 'li

Asia 9'li IO'li

Latin America 4 6

Africa 1 'li -4

Middle East 1 'li -4

North America 1 3'li

Inter regional 44 'li 3

World 100 4

Average annual

change

1989

-8

11

-'li

-1

-3 'li

-4 'li

-3 'li

S'li

-2

Source: GATT, International Trade, 1989-90, Vol. II, Geneva-1990, P.22

To analyse the declining tendency in the shares of world trade down the years of

1985 it is pertinent to shed light on the product pattern of trade of the Eastern Europe

and the USSR.

The share of fuels in the value of total exports from Eastern Europe exports

from Eastern Europe and the USSR increased markedly, from 11 per cent in 1973 to 30

per cent in 1985. Nearly half of the fuel exports is shipped to Western Europe and 40

per cent is traded within the area. Between 1973 and 1985, the share of non-fuel

primary products was cut almost in half and exports of manufactures fell by 6 per

centage points and now represents 52 per cent of the area's total exports (the share of

Western Europe in total exports of manufactures remained unchanged at 14 per cent).

134

The decline in the share of non-fuel primary products was less pronounced due

to sustained imports of food stuffs between 1973-85, the value of non-fuel primary

product imports increased by $22 bn, of which $17bn, or 80 per cent of the total

increase was accounted for by food. 4

Table No-3 B*

Merchandise Exports and Imports of Eastern Europe and the USSR by broad

product categories- Billion dollars and percentage shows.

Export Import

1973 1980 1984 1985 1973 1980 1984 1985

52 158 183 178 Total 52 157 166 171

100 100 100 100 Shares 100 100 100 100

22 15 14 13 Non-fuel 25 25 24 22

primary products

11 27 31 30 Fuels 6 14 19 19

58 53 50 52 Manufactures 67 60 56 57

95 5 5 Unspecified 2 1 1 1

Source: GATT, International Trade, 1985-86, vol. II (1986), p.107.

The major suppliers of food outside the area were Latin America, North America

and Western Europe. Their respective shares in total food imports into Eastern Europe

and the USSR in 1985 were estimated at 33, 20 and 12 per cent respectively.5 Oil sector

dominates in the overall trade of the Western Europe with the Europe with the Eastern

Europe and the USSR in 1989, a year closer to beginning of the crisis period in those

region.

4 GATT, International Trade, 1985-86, (1986), p. 107. 5 ibid, p. 107.

135

Table No.3 B

Product composition of Western Europe's in merchandise trade with Central and

Eastern Europe and the USSR, 1989.

Per Centage Share.

Exports to

Central /USSR

Eastern

Europe

17 ~ 12 ~

10 9~

4 1 ~

1 ~

1 ~

y2 y2

Primary products

Food

Raw Materials

Ores and Minerals

Fuels

Non-ferrous metal

Imports from

Central I

Eastern I

Europe

USSR

41 ~ 83 ~

14 ~ 1 ~

5~ 9

2~ 2~

14 ~ 63

4~ 7~

Source: Trade GATT, International, 1989-90, Vol. I, Geneva,1990, P.l3.

Fuel is the dominant product in Western Europe's imports from USSR, by virtue

of important import markets such as Italy, the Federal Republic of Germany and

Finland. Food and fuels are important items in imports from Eastern Europe and

Central Europe. The latter is primarily due to products refined in those countries from

imported crude petroleum. Important products in exports of Western Europe to Central

and Eastern Europe and the USSR include various items of non-electric machinery,

chemical and iron and steel.

Thus, as could be found from the table No.3A, exports to all other regions, except

to Weston Europe, fell by and to the world as a whole. The export fell by 2% per

annum over the preceding period, 1980-88.

136

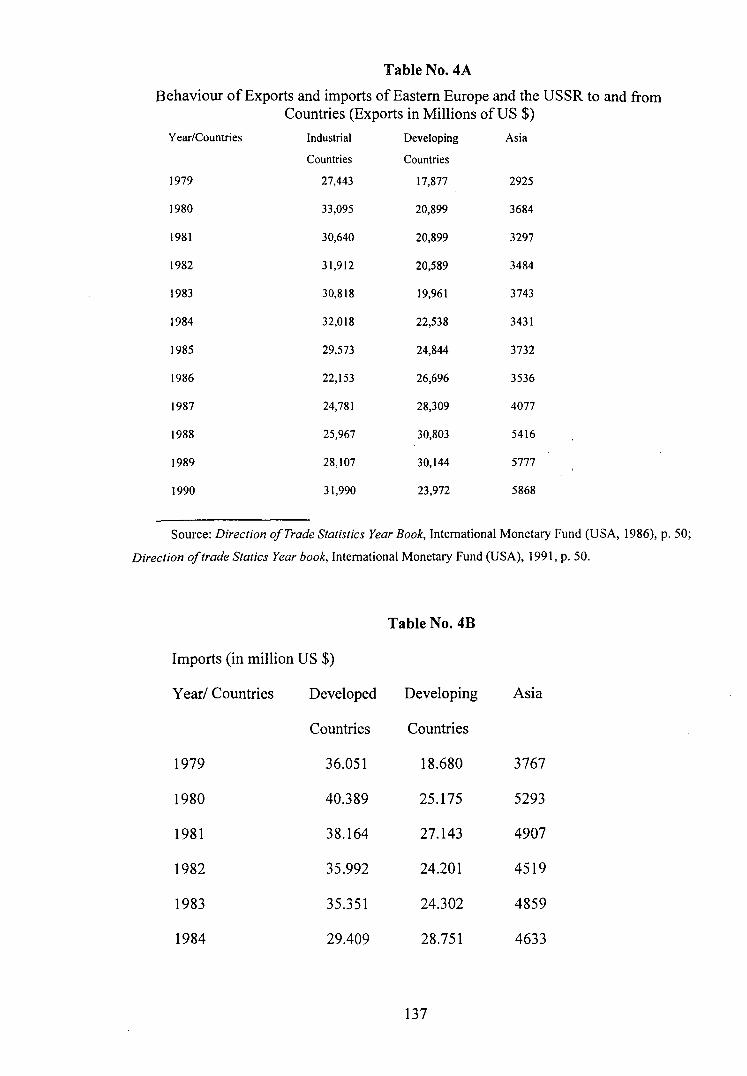

Table No. 4A

Behaviour ofExports and imports of Eastern Europe and the USSR to and from Countries (Exports in Millions of US $)

Year/Countries Industrial Developing Asia

Countries Countries

1979 27,443 17,877 2925

1980 33,095 20,899 3684

1981 30,640 20,899 3297

1982 31,912 20,589 3484

1983 30,818 19,961 3743

1984 32,018 22,538 3431

1985 29,573 24,844 3732

1986 22,153 26,696 3536

1987 24,781 28,309 4077

1988 25,967 30,803 5416

1989 28,107 30,144 5777

1990 31,990 23,972 5868

Source: Direction ofTrade Statistics Year Book, International Monetary Fund (USA, 1986), p. 50;

Direction of trade Statics Year book, International Monetary Fund (USA), 1991, p. 50.

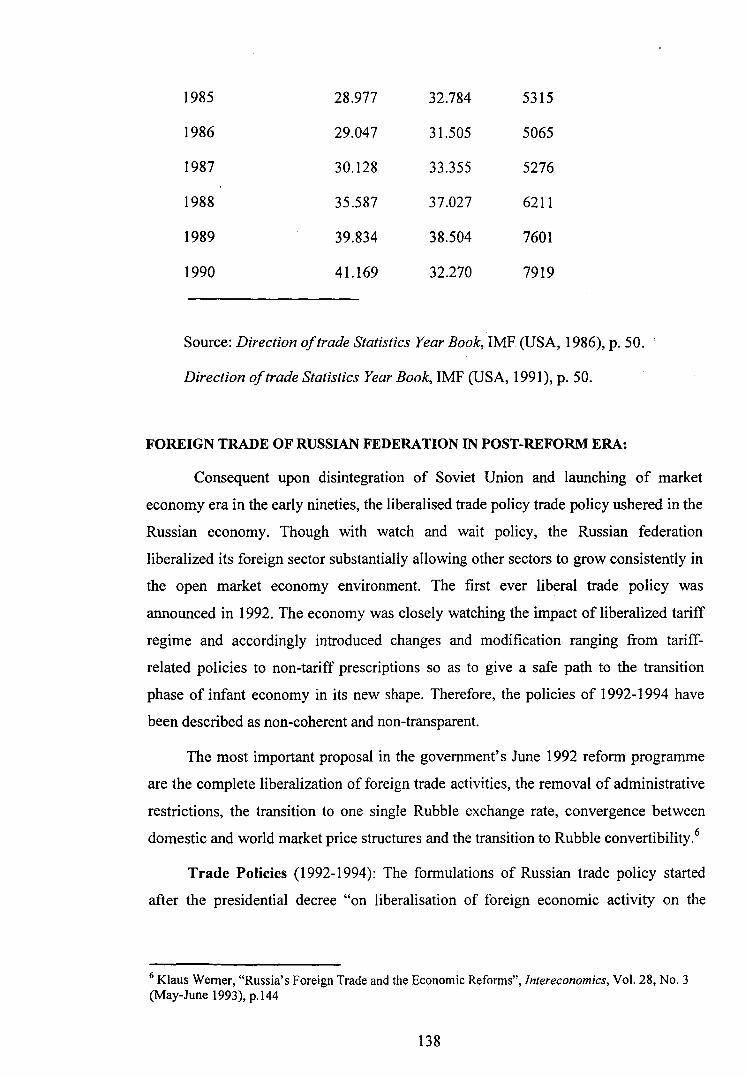

Table No. 4B

Imports (in million US $)

Year/ Countries Developed Developing Asia

Countries Countries

1979 36.051 18.680 3767

1980 40.389 25.175 5293

1981 38.164 27.143 4907

1982 35.992 24.201 4519

1983 35.351 24.302 4859

1984 29.409 28.751 4633

137

1985 28.977 32.784 5315

1986 29.047 31.505 5065

1987 30.128 33.355 5276

1988 35.587 37.027 6211

1989 39.834 38.504 7601

1990 41.169 32.270 7919

Source: Direction oftrade Statistics Year Book, IMF (USA, 1986), p. 50.

Direction oftrade Statistics Year Book, IMF (USA, 1991), p. 50.

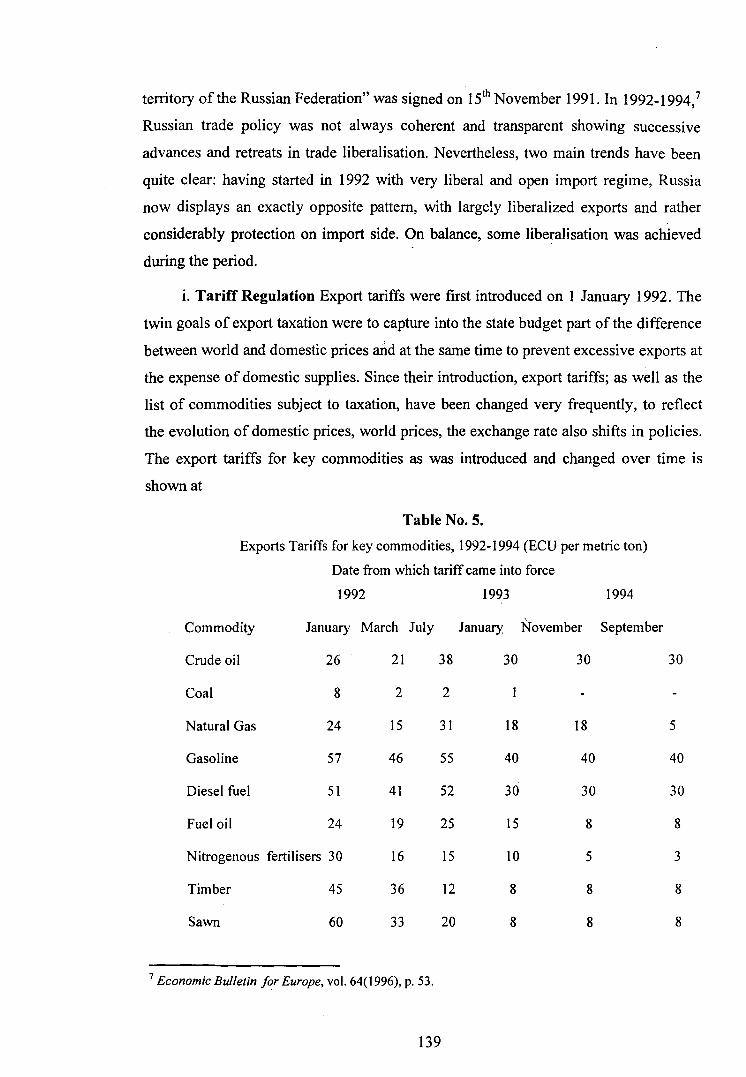

FOREIGN TRADE OF RUSSIAN FEDERATION IN POST-REFORM ERA:

Consequent upon disintegration of Soviet Union and launching of market

economy era in the early nineties, the liberalised trade policy trade policy ushered in the

Russian economy. Though with watch and wait policy, the Russian federation

liberalized its foreign sector substantially allowing other sectors to grow consistently in

the open market economy environment. The first ever liberal trade policy was

announced in 1992. The economy was closely watching the impact of liberalized tariff

regime and accordingly introduced changes and modification ranging from tariff

related policies to non-tariff prescriptions so as to give a safe path to the transition

phase of infant economy in its new shape. Therefore, the policies of 1992-1994 have

been described as non-coherent and non-transparent.

The most important proposal in the government's June 1992 reform programme

are the complete liberalization of foreign trade activities, the removal of administrative

restrictions, the transition to one single Rubble exchange rate, convergence between

domestic and world market price structures and the transition to Rubble convertibility.6

Trade Policies (1992-1994): The formulations of Russian trade policy started

after the presidential decree "on liberalisation of foreign economic activity on the

6 Klaus Werner, "Russia's Foreign Trade and the Economic Reforms", Intereconomics, Vol. 28, No.3 (May-June 1993), p.l44

138

territory ofthe Russian Federation" was signed on 15th November 1991. In 1992-1994/

Russian trade policy was not always coherent and transparent showing successive

advances and retreats in trade liberalisation. Nevertheless, two main trends have been

quite clear: having started in 1992 with very liberal and open import regime, Russia

now displays an exactly opposite pattern, with largely liberalized exports and rather

considerably protection on import side. On balance, some liberalisation was achieved

during the period.

i. Tariff Regulation Export tariffs were first introduced on 1 January 1992. The

twin goals of export taxation were to capture into the state budget part of the difference

between world and domestic prices al1d at the same time to prevent excessive exports at

the expense of domestic supplies. Since their introduction, export tariffs; as well as the

list of commodities subject to taxation, have been changed very frequently, to reflect

the evolution of domestic prices, world prices, the exchange rate also shifts in policies.

The export tariffs for key commodities as was introduced and changed over time is

shown at

Table No.5.

Exports Tariffs for key commodities, 1992-1994 (ECU per metric ton)

Date from which tariff came into force

1992 1993. 1994

Commodity January March July January November September

Crude oil 26 21 38 30 30 30

Coal 8 2 2

Natural Gas 24 15 31 18 18 5

Gasoline 57 46 55 40 40 40

Diesel fuel 51 41 52 30 30 30

Fuel oil 24 19 25 15 8 8

Nitrogenous fertilisers 30 16 15 10 5 3

Timber 45 36 12 8 8 8

Sawn 60 33 20 8 8 8

7 Economic Bulletin for Europe, vol. 64(1996), p. 53.

139

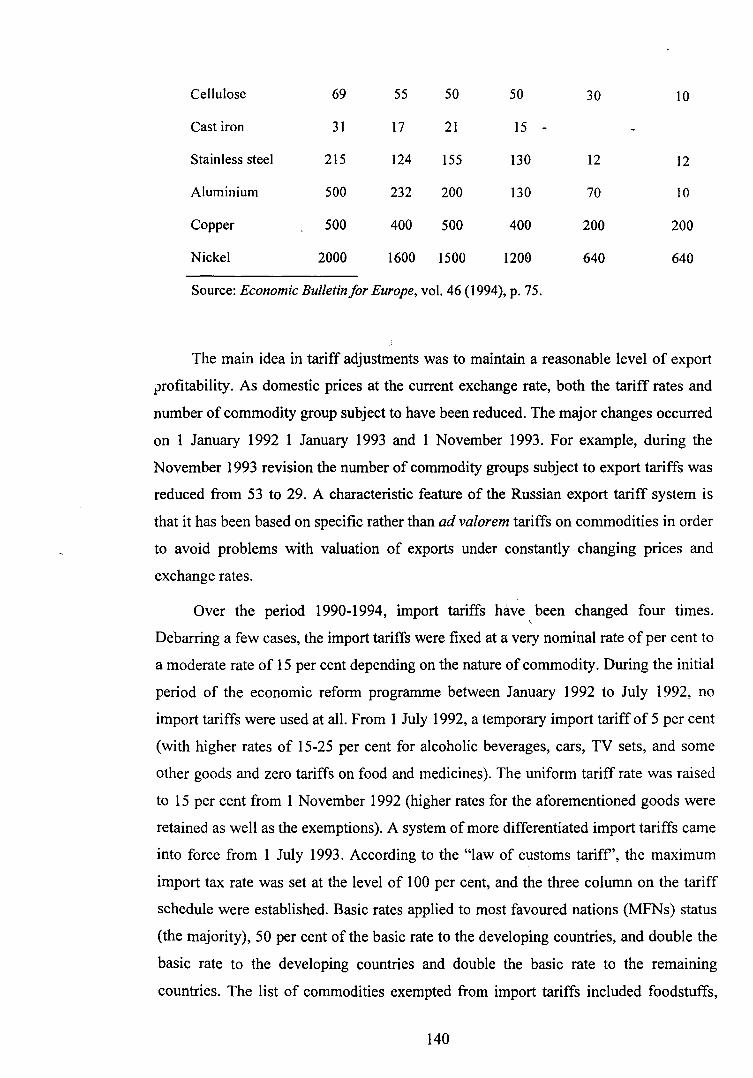

Cellulose 69 55 50 50 30 10

Cast iron 31 17 21 15 -

Stainless steel 215 124 155 130 12 12

Aluminium 500 232 200 130 70 10

Copper 500 400 500 400 200 200

Nickel 2000 1600 1500 1200 640 640

Source: Economic Bulletin for Europe, vol. 46 (1994), p. 75.

The main idea in tariff adjustments was to maintain a reasonable level of export

_profitability. As domestic prices at the current exchange rate, both the tariff rates and

number of commodity group subject to have been reduced. The major changes occurred

on 1 January 1992 1 January 1993 and 1 November 1993. For example, during the

November 1993 revision the number of commodity groups subject to export tariffs was

reduced from 53 to 29. A characteristic feature of the Russian export tariff system is

that it has been based on specific rather than ad valorem tariffs on commodities in order

to avoid problems with valuation of exports under constantly changing prices and

exchange rates.

Over the period 1990-1994, import tariffs have·, been changed four times.

Debarring a few cases, the import tariffs were fixed at a very nominal rate of per cent to

a moderate rate of 15 per cent depending on the nature of commodity. During the initial

period of the economic reform programme between January 1992 to July 1992, no

import tariffs were used at all. From 1 July 1992, a temporary import tariff of 5 per cent

(with higher rates of 15-25 per cent for alcoholic beverages, cars, TV sets, and some

other goods and zero tariffs on food and medicines). The uniform tariff rate was raised

to 15 per cent from 1 November 1992 (higher rates for the aforementioned goods were

retained as well as the exemptions). A system of more differentiated import tariffs came

into force from 1 July 1993. According to the "law of customs tariff', the maximum

import tax rate was set at the level of 100 per cent, and the three column on the tariff

schedule were established. Basic rates applied to most favoured nations (MFNs) status

(the majority), 50 per cent of the basic rate to the developing countries, and double the

basic rate to the developing countries and double the basic rate to the remaining

countries. The list of commodities exempted from import tariffs included foodstuffs,

140

medicines, medical equipments, children's clothes, and other socially significant goods.

For other goods, the basic tax rate varied form 5 per cent (intermediate goods, metals,

transport equipment) to 15 per cent (capital goods, consumer durables). The highest

rate applied to strong alcoholic drinks (1 00 per cent). [Data: Economic Bulletin for

Europe, vol. 46 (1994), p. 75.]

In March 1994, under growing pressure form the agrarian and industrial sectors, a

new system of import tariffs was approved by the Government. The average rate of

import tariffs was increased by some 60 per cent, and the number of goods subject to

tax was enlarged. The most pronounced income was in the case of foodstuffs.

From 1 February 1993 certain imported goods were exposed to excise taxation

(mainly strong alcoholic beverages, tobacco, cars, furs, (lathers articles and some other

consumer goods) and Value Added tax (VAT) of20 per cent.

ii. Non-tariff Regulations: Instruments of non-tariff regulation in the form of

licensing and quotas were introduced from the beginning of 1992. However, in 1992

licensing was applied in a very limited way for specific commodities, and the

regulation of exports was implemented in the form of quotas for 23 commodity groups

(all fuels, ferrous and non-ferrous metals, basic chemicals and others). A more

elaborate mechanism of quotas and licensees was announced in November 1992 and

came into force on 1 January 1993.8 The new system concentrated mainly on export

regulations, as quotas were not applied to imports and only a small number of specific

imported goods were subject to licensing. The list of export commodities to be

controlled by quotas and licenses included all fuels, ferrous metals, timber, fertilizers,

chemicals (17 commodity groups or about 50-60 per cent of total exports).

In addition to three types of export quotas which were allocated to individual

regions, individual producers and sold at auctions, special quotas for state's needs were

established (to secure foreign exchange revenues for budget through centralised

exports). Regional and producers' quotas were could also be traded on secondary

market, although they were issued without charge to regions and enterprises.

During 1992 and 1993, the number of commodities on the export quota list was

continuously reduced as the gap between domestic and world prices was narrowing.

From 1 January 1994, the quota list was reduced to 12 commodity groups, including oil

8 Economic Bulletin for Europe, vol. 46 (1994), p. 76.

141

and oil products, gas, electric energy, some ferrous metals and food products. From I

July 1994 all export quotas and licenses were to be abolished, but later it was classified

that quotas and licenses would be retained to the end of 1994 for crude oil and

petroleum products as well as for a number of commodities agreed between Russia and

European Union (these are mainly aluminium, fabrics and textile articles). From I

January 1995 quotas and licenses for exports of crude oil and petroleum products are

also to be eliminated.9

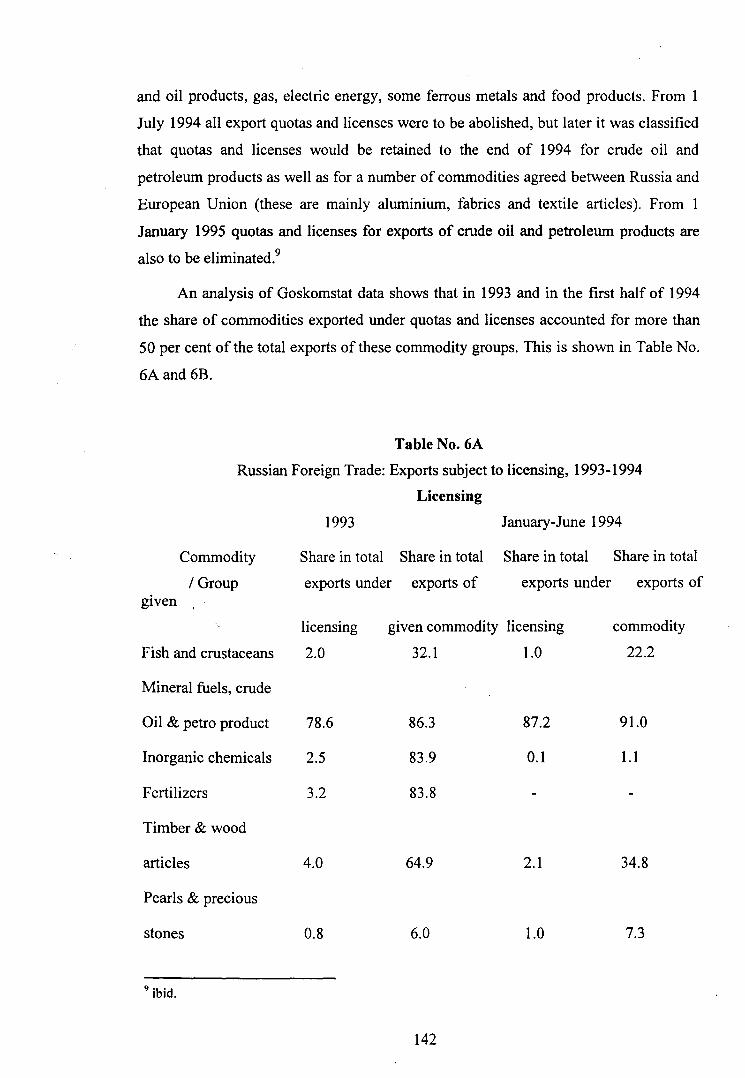

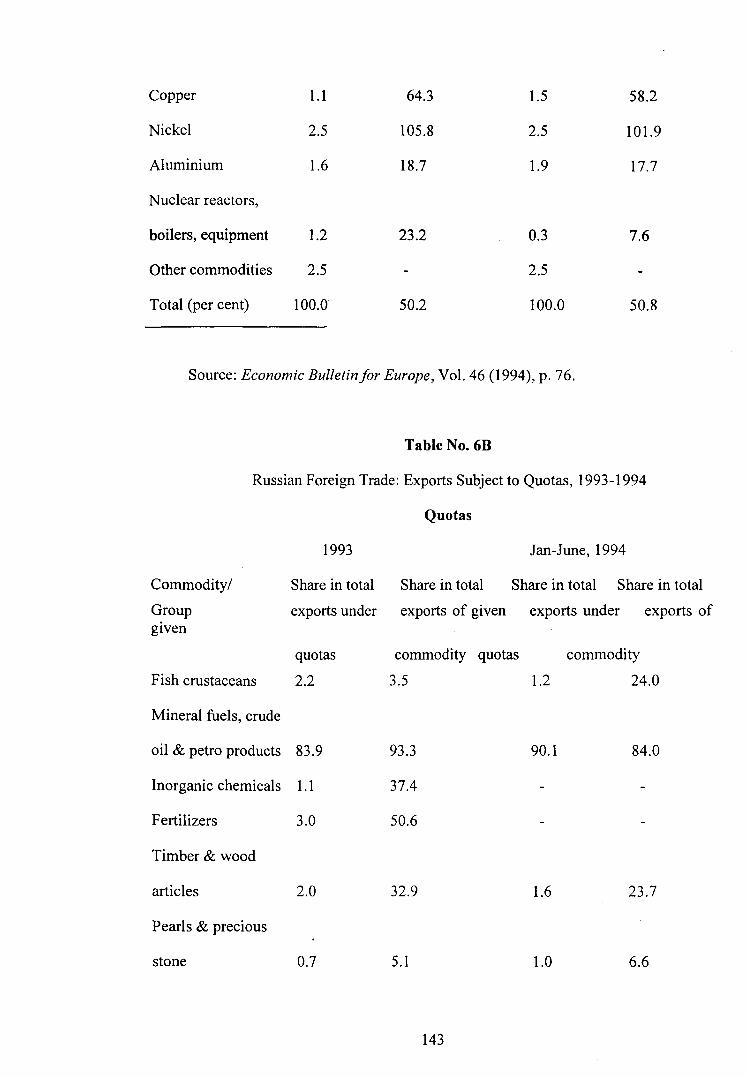

An analysis of Goskomstat data shows that in 1993 and in the first half of 1994

the share of commodities exported under quotas and licenses accounted for more than

50 per cent ofthe total exports of these commodity groups. This is shown in Table No.

6Aand 6B.

Table No. 6A

Russian Foreign Trade: Exports subject to licensing, 1993-1994

Licensing

1993 January-June 1994

Commodity Share in total Share in total Share in total Share in total

I Group exports under exports of exports under exports of gtven

'

licensing given commodity licensing commodity

Fish and crustaceans 2.0 32.1 1.0 22.2

Mineral fuels, crude

Oil & petro product 78.6 86.3 87.2 91.0

Inorganic chemicals 2.5 83.9 0.1 1.1

Fertilizers 3.2 83.8

Timber & wood

articles 4.0 64.9 2.1 34.8

Pearls & precious

stones 0.8 6.0 1.0 7.3

9 ibid.

142

Copper 1.1 64.3 1.5 58.2

Nickel 2.5 105.8 2.5 101.9

Aluminium 1.6 18.7 1.9 17.7

Nuclear reactors,

boilers, equipment 1.2 23.2 0.3 7.6

Other commodities 2.5 2.5

Total (per cent) 100.0 50.2 100.0 50.8

Source: Economic Bulletin/or Europe, Vol. 46 (1994), p. 76.

Table No. 6B

Russian Foreign Trade: Exports Subject to Quotas, 1993-1994

Quotas

1993 Jan-June, 1994

Commodity/

Group

Share in total Share in total Share in total Share in total

exports under exports of given exports under exports of given

Fish crustaceans

Mineral fuels, crude

quotas

2.2

oil & petro products 83.9

Inorganic chemicals 1.1

Fertilizers 3.0

Timber & wood

articles 2.0

Pearls & precious

stone 0.7

commodity quotas

3.5

93.3

37.4

50.6

32.9

5.1

143

1.2

90.1

1.6

1.0

commodity

24.0

84.0

23.7

6.6

Copper 1.1 62.5 1.3 44.5

Nickel 2.4 101.1 2.5 90.3

Aluminium 1.4 16.7 0.2 2.0

Nuclear reactors,

boilers, equipment

Other commodities 2.2 2.1

Total (per cent) 100.0 50.9 100.0 45.3

Source: Economic Bulletin of Europe, Vol. 46 (1994), p. 76.

iii. Strategically Important Commodities (SIC), and Special Exporters

provision: In order to protect state revenues and avoid income losses from non

equivalent exchange and secure the repatriation of export earnings, a list of

"strategically important commodities- (SIC)" was introduced from the second half of

1992, as well as a category of " special exporters", which were the only trade

orgnisations authorized to export these commodities. "The SIC list was identical with

the list of goods subject to quotas and licensing. The special exporters were registered

by the Ministry for Foreign Economic Relations, where continuously changed the 26

register both as to the number and the participants on the basis of their performance. At

the end of 1993, there were about 800 special exporters in 1994 their number was

reduced to 497. After elimination of quota in 1994, special exporters had to register

their contracts at the Ministry of Foreign Economic Relations and get a special

certificate for this. Thus, the abolition of one form of none-tariff regulation (quotas and

licenses) was replaced by another one (registration of contracts). However, from 1

January 1995the category of special exporters was abolished. 10

Besides the above policy measures, the State itself actively participated in trade

through 'centralised' exports and the system centralised won designed to acquire hard

currency for the govt. For debt servicing centralised imports and other purposes. The

Government centralized imports for debt servicing and other purposes. The system of

10 ibid.

144

centralized imports was used to provide domestic consumers with imported goods at a

price lower than the world market price, with the difference (subsidiary) paid by the

government. Centralised imports included both consumer goods (mainly food stuffs and

medicines) and investment goods and industrial inputs. Centralized exports accounted

for 33 per cent of total exports in 1992, 30 per cent in 1993 and 15 per cent in the first

half of 1994. The centralised imports are also continuously shrinking continuously. At

the end of 1993, all State subsidies for imports were abolished the government's direct

involvement in foreign trade was gradually reduced between 1992-1994. 11

iv. Measures to prevent capital flight: Tax controls over foreign exchange operations

and repatriation of foreign exchange earnings are perhaps the most acute problems

confronted by Russian trade policy markers. Trying to cut capital flight from Russia,

the authorities introduced a system of foreign exchange control over exporters' proceed

from January 1, 1994. The system tries to detect and gauge any difference between the

announced value of the contract and actual revenues obtained by exporters. Every

export transactions must be recorded in a special "passport", including all details of the

contracts. On the basis of this document, and also of bank information on payments

made out of enterprises' accounts. The customs committees compares export earnings

with the value of goods delivered and thus has a chance to uncover hidden revenues and

capital flight. As a result of this measure, the estimated amount 0f capital flight

diminished sharply in 1994 as compared with 1993.

v. Foreign exchange Policy: At the beginning of 1992, a certain liberalization of the

foreign exchange market was implemented. However, till that period, multiple

exchange rates continue along with a complicated system of foreign exchange

allocation for imports through weekly auctions and direct rationing. In addition the

principle of compulsory surrender of exports earnings was maintained. From January to

June 1992, exporters had a legal right to retain 50 per cent of hard currency revenues,

40 per cent was to be sold at a Republican hard currency reserve at a fixed rate and 1 0

per cent to the central bank of Russia at the official rate.

The rudiments of a foreign exchange market were established when the Moscow

Inter Bank Currency Exchange (MICEX) started weekly auctions, with the current

II ibid., p. 77.

145

exchange rate fixed on the basis of supply and demand. The operations of the MICEX

were performed under the control of the Central Bank, which used its hard currency

reserves to influence the exchange rate through a mechanism of interventions. from

July 1, 1992, a new set of measures was introduced to better regulate the foreign

exchange market. The most important was the unification of exchange rates for current

account transactions. The rate was floating and was determined twice a week on the

basis of quotations at the auctions of the MICEX. Exporters still had to sell 50 per cent

of their hard currency earnings, not to the government as before, but rather directly to

foreign exchange market through authorized banks where their hard currency accounts

were kept. Exporters' profits were sharply boosted as the rate used for these

transactions was the market rate.

However, in spite of the proclaimed exchange rate unification a concealed system

of multiple rates continued to be applied in the system of centralized imports. The

system though was far from perfect, it is perhaps one of the few examples in Russia

where a market is doing its job. But it remains highly volatile and its performance some

times is dismal.

The precipitate fall of Rouble in September 1994 and its dramatic collapse by

22 per cent on 11 October 1994 demonstrates the deficiencies of the thin and unstable

market. The primary causes for large exchange rate fluctuations ,Tie deeply rooted in

erratic macro-economic policies and institutional rigidities charact~ristic of the Russian

economy.

TRADE PERFORMANCE OF RUSSIAN ECONOMY DURING 1992 AND BEYOND:

To analyse the trade performance of the newly emerging Russian economy, data

problem is very severe due to its very infancy of the new form. These problems need

prior discussion to avoid and adjust certain anomalies.

Statistical and Data Problem Statistics on Russian foreign trade only started with the

emergence of Russia as an independent state, as Soviet Foreign trade statistics were

compiled only for the USSR as a whole, without break up by Republics Hence, all data

on Russian trade for the years before 1992 are estimates derived from USSR statistics,

the accuracy of which diminishes as one moves backward from 1992.

146

From the very beginning, the Russian Goshmostat faced a great number of

problem in the collection of foreign trade data: absence of customs boarders between

Russia and other Soviet Republics, transition to the new trade classification based on

the harmonized commodity description and coding system, the rapidly growing number

of firms involved in international trade and the appearance of new types to trade

activity such as exports and imports by private individuals. Under such conditions, the

first estimates of trade flows in 1992-1993 were invariably not very reliable and subject

to frequent revisions.

In 1992-1993, the methodlogy applied by Goskomstat to collect and process trade

data was stile largely based on the old principles existing under the state monopoly of

foreign trade. The system was based on reports from all economic units conducting

trade activities, which had registered with the regional statistical offices. The core of

this unit was formed by a limited number of large foreign trade organization inherited

from the Soviet period. On the basis of those reports, Gusokmstat made first estimates

of trade flow broken up by commodities and countries.

Usually these estimates severely underestimated the actual trade levels, especially

in the case of imports because not all trading entities registered with statistical offices

and the disciplines of reporting was rather poor. The preliminary Gusokmstat estimates

were then adjusted in lin~ with a special procedure elaborated by Gusokmstat together

with the ministry for foreign economic relations (MFER). This procedure takes into

account customs information mirror statistics of Russia's trade partner and the reports

of MFER representatives abroad. 12 The discrepancy between the initial trade data and

the adjusted trade values is in some cases, quite substantial which may be seen from the

following Table.

12 Ibid, p. 68.

147

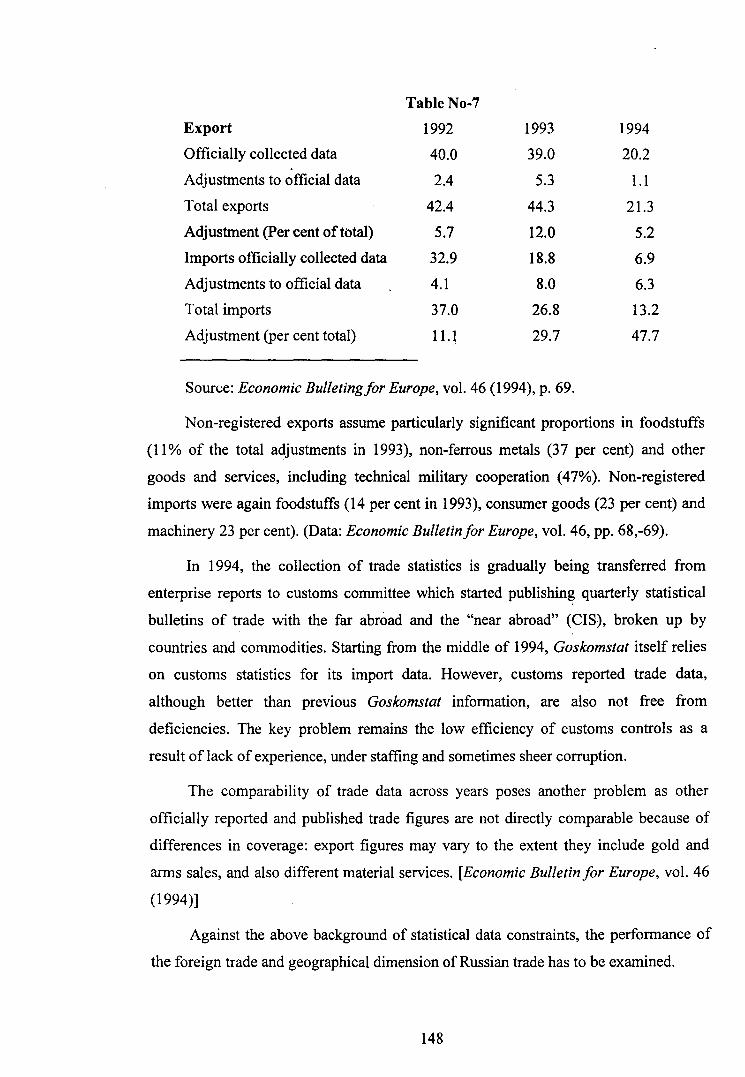

Table No-7

Export 1992 1993 1994

Officially collected data 40.0 39.0 20.2

Adjustments to official data 2.4 5.3 1.1

Total exports 42.4 44.3 21.3

Adjustment (Percent of total) 5.7 12.0 5.2

Imports officially collected data 32.9 18.8 6.9

Adjustments to official data 4.1 8.0 6.3

Total imports 37.0 26.8 13.2

Adjustment (per cent total) 11.1 29.7 47.7

Sour"e: Economic Bulletingfor Europe, vol. 46 (1994), p. 69.

Non-registered exports assume particularly significant proportions in foodstuffs

(11% of the total adjustments in 1993), non-ferrous metals (37 per cent) and other

goods and services, including technical military cooperation (47%). Non-registered

imports were again foodstuffs (14 per cent in 1993), consumer goods (23 per cent) and

machinery 23 per cent). (Data: Economic Bulletin for Europe, vol. 46, pp. 68,-69).

In 1994, the collection of trade statistics is gradually being transferred from

enterprise reports to customs committee which started publishing quarterly statistical

bulletins of trade with the far abroad and the "near abroad" (CIS), broken up by

countries and commodities. Starting from the middle of 1994, Goskomstat itself relies

on customs statistics for its import data. However, customs reported trade data,

although better than previous Goskomstat information, are also not free from

deficiencies. The key problem remains the low efficiency of customs controls as a

result of lack of experience, under staffing and sometimes sheer corruption.

The comparability of trade data across years poses another problem as other

officially reported and published trade figures are not directly comparable because of

differences in coverage: export figures may vary to the extent they include gold and

arms sales, and also different material services. [Economic Bulletin for Europe, vol. 46

(1994)]

Against the above background of statistical data constraints, the performance of

the foreign trade and geographical dimension of Russian trade has to be examined.

148

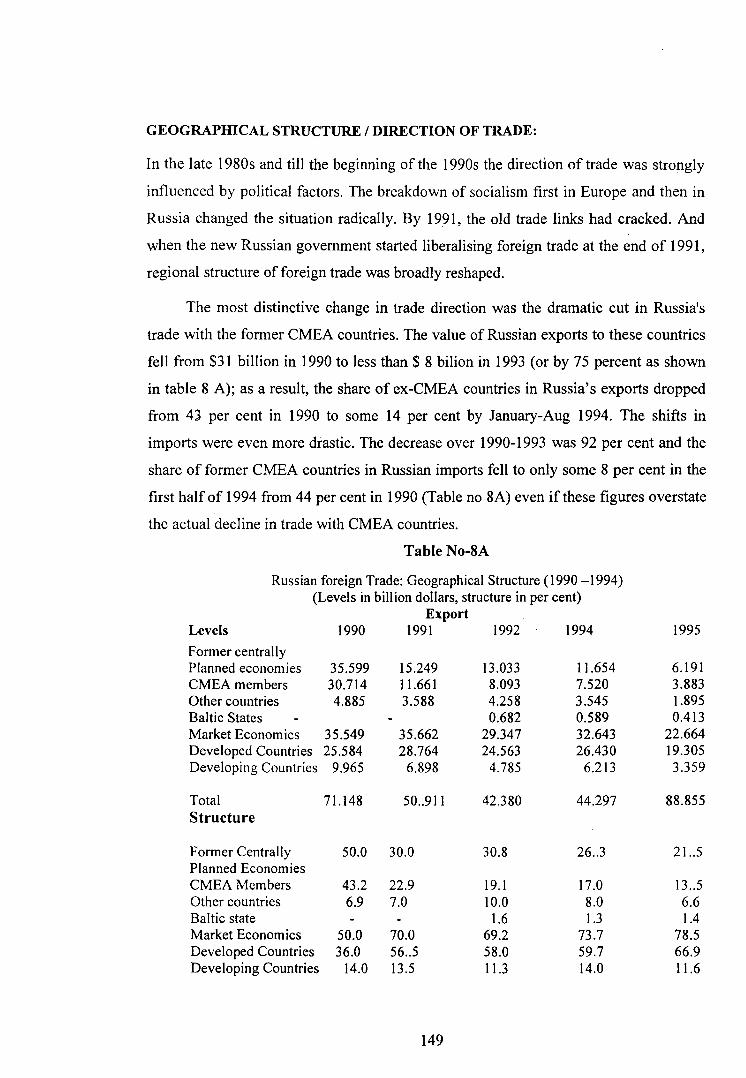

GEOGRAPHICAL STRUCTURE I DIRECTION OF TRADE:

In the late 1980s and till the beginning of the 1990s the direction of trade was strongly

influenced by political factors. The breakdown of socialism first in Europe and then in

Russia changed the situation radically. By 1991, the old trade links had cracked. And

when the new Russian government started liberalising foreign trade at the end of 1991,

regional structure of foreign trade was broadly reshaped.

The most distinctive change in trade direction was the dramatic cut in Russia's

trade with the former CMEA countries. The value of Russian exports to these countries

fell from $31 billion in 1990 to less than $ 8 bilion in 1993 (or by 75 percent as shown

in table 8 A); as a result, the share of ex-CMEA countries in Russia's exports dropped

from 43 per cent in 1990 to some 14 per cent by January-Aug 1994. The shifts in

imports were even more drastic. The decrease over 1990-1993 was 92 per cent and the

share of former CMEA countries in Russian imports fell to only some 8 per cent in the

first half of 1994 from 44 per cent in 1990 (Table no 8A) even if these figures overstate

the actual decline in trade with CMEA countries.

Table No-8A

Russian foreign Trade: Geographical Structure ( 1990 -1994) (Levels in billion dollars, structure in per cent)

Export Levels 1990 1991 1992 1994 1995

Former centrally Planned economies 35.599 15.249 13.033 11.654 6.191 CMEA members 30.714 11.661 8.093 7.520 3.883 Other countries 4.885 3.588 4.258 3.545 1.895 Baltic States 0.682 0.589 0.413 Market Economics 35.549 35.662 29.347 32.643 22.664 Developed Countries 25.584 28.764 24.563 26.430 19.305 Developing Countries 9.965 6.898 4.785 6.213 3.359

Total 71.148 50 .. 911 42.380 44.297 88.855 Structure

Former Centrally 50.0 30.0 30.8 26 .. 3 21 .. 5 Planned Economies CMEA Members 43.2 22.9 19.1 17.0 13 .. 5 Other countries 6.9 7.0 10.0 8.0 6.6 Baltic state 1.6 1.3 1.4 Market Economics 50.0 70.0 69.2 73.7 78.5 Developed Countries 36.0 56 .. 5 58.0 59.7 66.9 Developing Countries 14.0 13.5 11.3 14.0 11.6

149

Total 100.0 100.0 100.0 100.0 100.0

Source: Economic Bulletin/or Europe, vol. 46 (1994), p.70

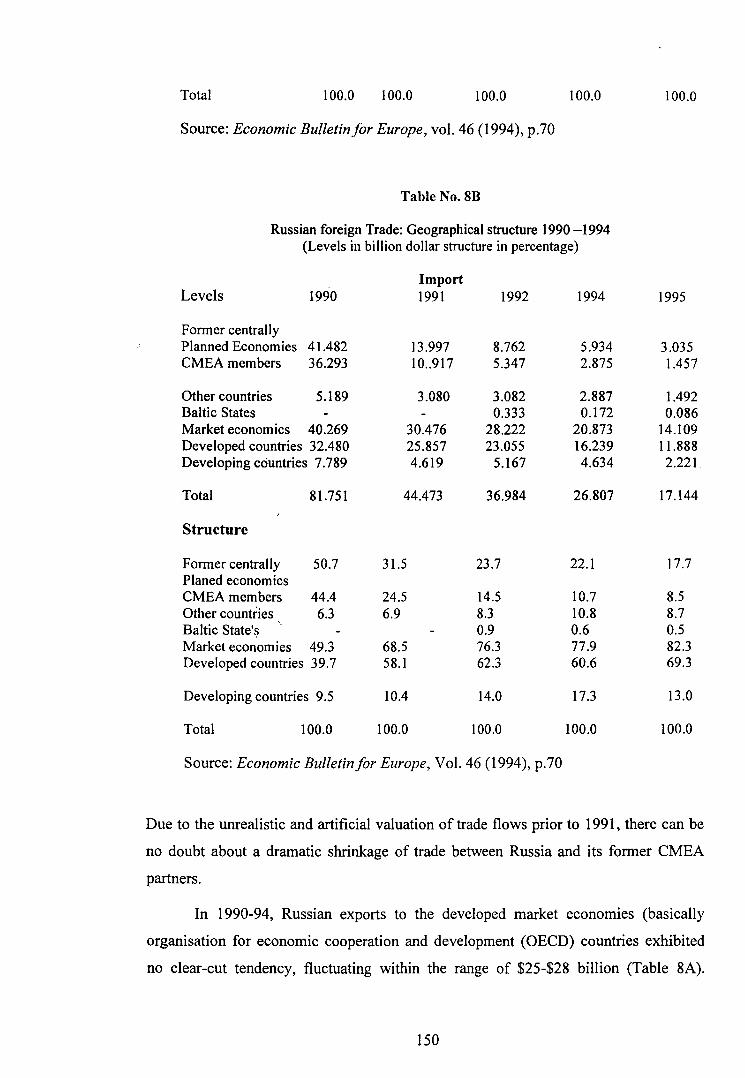

Table No. 8B

Russian foreign Trade: Geographical structure 1990 -1994 (Levels in billion dollar structure in percentage)

Import Levels 1990 1991 1992 1994 1995

Former centrally Planned Economies 41.482 13.997 8.762 5.934 3.035 CMEA members 36.293 10 .. 917 5.347 2.875 1.457

Other countries 5.189 3.080 3.082 2.887 1.492 Baltic States 0.333 0.172 0.086 Market economics 40.269 30.476 28.222 20.873 14.109 Developed countries 32.480 25.857 23.055 16.239 11.888 Developing countries 7. 789 4.619 5.167 4.634 2.221

Total 81.751 44.473 36.984 26.807 17.144

Structure

Former centrally 50.7 31.5 23.7 22.1 17.7 Planed economics CMEA members 44.4 24.5 14.5 10.7 8.5 Other countries 6.3 6.9 8.3 10.8 8.7 Baltic State's 0.9 0.6 0.5 Market economies 49.3 68.5 76.3 77.9 82.3 Developed countries 39.7 58.1 62.3 60.6 69.3

Developing countries 9.5 10.4 14.0 17.3 13.0

Total 100.0 100.0 100.0 100.0 100.0

Source: Economic Bulletin/or Europe, Vol. 46 (1994), p.70

Due to the unrealistic and artificial valuation of trade flows prior to 1991, there can be

no doubt about a dramatic shrinkage of trade between Russia and its former CMEA

partners.

In 1990-94, Russian exports to the developed market economies (basically

organisation for economic cooperation and development (OECD) countries exhibited

no clear-cut tendency, fluctuating within the range of $25-$28 billion (Table 8A).

150

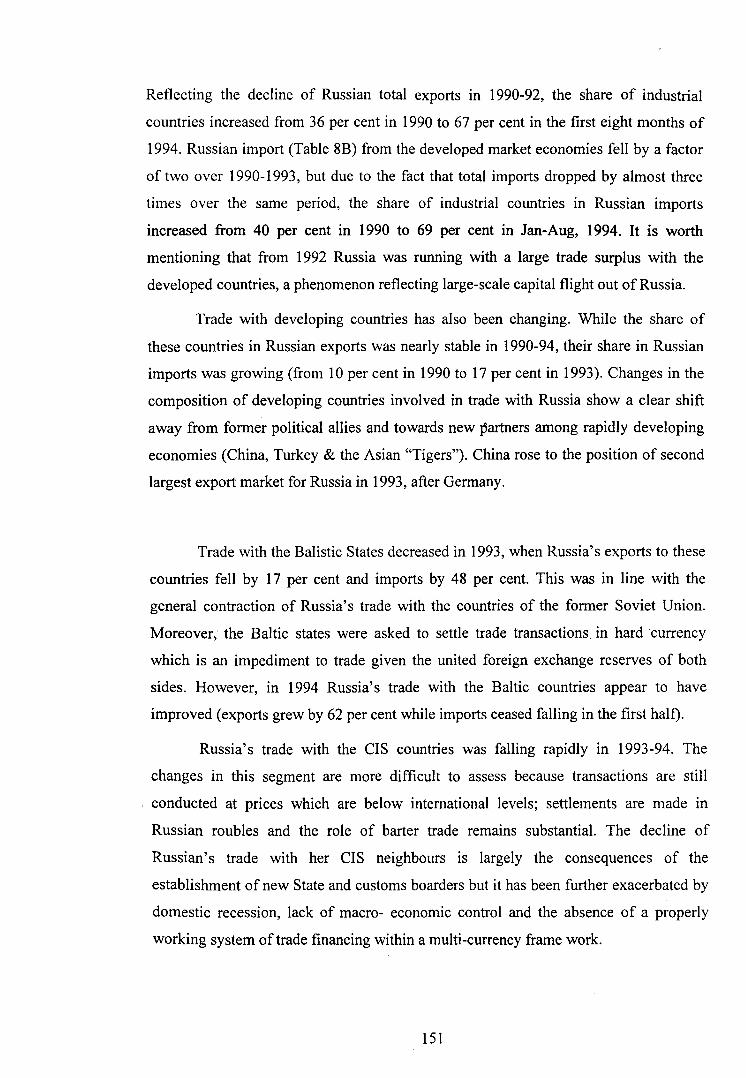

Reflecting the decline of Russian total exports in 1990-92, the share of industrial

countries increased from 36 per cent in 1990 to 67 per cent in the first eight months of

1994. Russian import (Table 8B) from the developed market economies fell by a factor

of two over 1990-1993, but due to the fact that total imports dropped by almost three

times over the same period, the share of industrial countries in Russian imports

increased from 40 per cent in 1990 to 69 per cent in Jan-Aug, 1994. It is worth

mentioning that from 1992 Russia was running with a large trade surplus with the

developed countries, a phenomenon reflecting large-scale capital flight out of Russia.

Trade with developing countries has also been changing. While the share of

these countries in Russian exports was nearly stable in 1990-94, their share in Russian

imports was growing (from 10 per cent in 1990 to 17 per cent in 1993). Changes in the

composition of developing countries involved in trade with Russia show a clear shift

away from former political allies and towards new {lartners among rapidly developing

economies (China, Turkey & the Asian "Tigers"). China rose to the position of second

largest export market for Russia in 1993, after Germany.

Trade with the Balistic States decreased in 1993, when Russia's exports to these

countries fell by 17 per cent and imports by 48 per cent. This was in line with the

general contraction of Russia's trade with the countries of the former Soviet Union.

Moreover, the Baltic states were asked to settle trade transactions in hard currency

which is an impediment to trade given the united foreign exchange reserves of both

sides. However, in 1994 Russia's trade with the Baltic countries appear to have

improved (exports grew by 62 per cent while imports ceased falling in the first half).

Russia's trade with the CIS countries was falling rapidly in 1993-94. The

changes in this segment are more difficult to assess because transactions are still

conducted at prices which are below international levels; settlements are made in

Russian roubles and the role of barter trade remains substantial. The decline of

Russian's trade with her CIS neighbours is largely the consequences of the

establishment of new State and customs boarders but it has been further exacerbated by

domestic recession, lack of macro- economic control and the absence of a properly

working system of trade financing within a multi-currency frame work.

151

During 1995, the large increase in exports to developing countries was notable. In

the same period, exports to the developing countries doubled and those to the East

European countries grew at a faster pace than exports to the Western market

economies. Significant growth in trade with the East European countries particularly

for exports (up by 43 per cent), suggests a possible revival of intra-regional cooperation

following the strong recovery of these economies, especially those in CIET A.

Maintaining its rising trend, the Russian trade with Balistic States grew rapidly.

Russian trade surpluses increased substantially with all trade-partner groups in 1995.

The largest surplus was trade with developing countries. However exports to the

developing countries declined in 1996, but imports rose rapidly. During the same

period, exports to the East European countries stagnated Russian's. imports from the

transition economies, however, declined by & per cent in the first half of 1996, the

biggest fall being with the Baltic States on Russian data.

Till end of first half of 1998, Russia's foreign trade saw a shift from the

developed economies to developing and transition economies it continued with trade

surpluses with almost all trading partners. 13

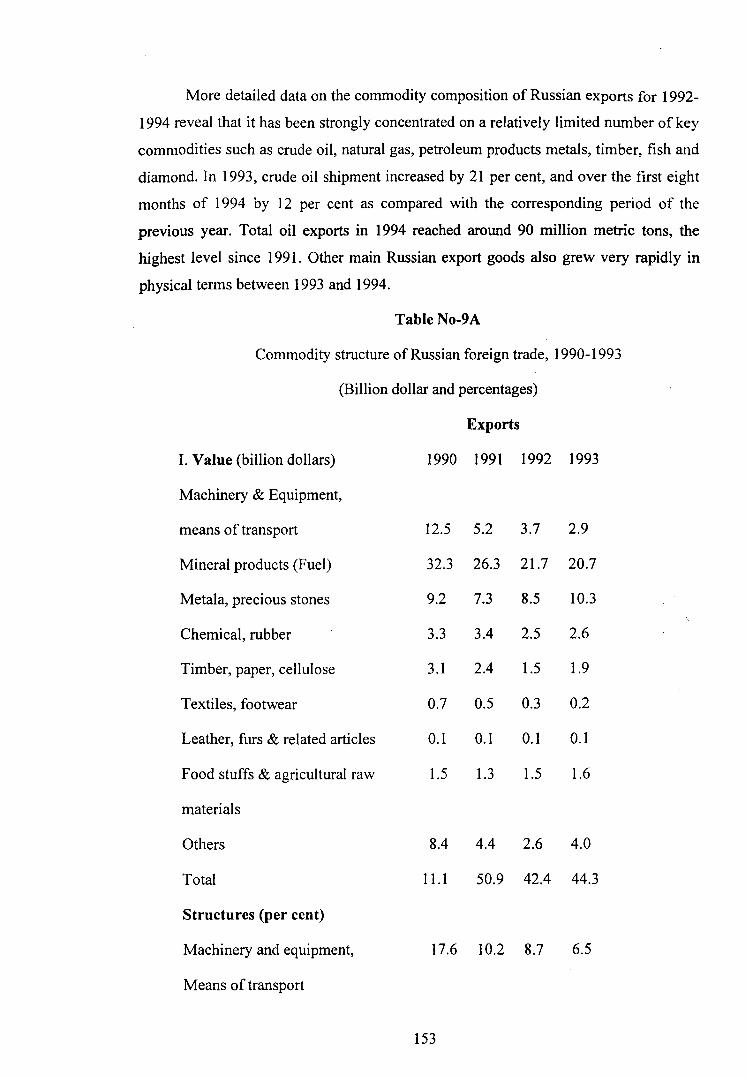

COMPOSITION OF TRADE (COMMODITY): The commodity break up of Russia's

exports in 1990-93 by nine aggregated commodity groups show that (Table 9A & 9B)

mineral fuels continue to dominate exports, although their share fell to less than 50 per

cent in 1993 because of falling world prices14. An interesting development has been an

increase of foodstuff exports, mainly fish (80-85 per cent of the total). Exports of

metals and raw diamonds also increased in 1993 as compared to 1990. All other

commodity groups, including semi-manufactures like timber and basic chemicals, were

on a downward trend with especially pronounced drops in manufactures. Exports of

textiles and foot wear fell by 71 per cent 1990 to 1993, while machinery and equipment

exports were down by 77per cent over the same period of time. In general, the share of

machinery dropped from 17.6 per cent of total exports in 1990 to 6.5 per cent in 1993,

and to less than 5 per cent in the first eight months of 1994.

13 Economic Survey of Europe, No. 3 (1998), p. 98. 14 Economic Bulletin for Europe, vol. 46, 1994. p. 72.

152

More detailed data on the commodity composition of Russian exports for 1992-

1994 reveal that it has been strongly concentrated on a relatively limited number of key

commodities such as crude oil, natural gas, petroleum products metals, timber, fish and

diamond. In 1993, crude oil shipment increased by 21 per cent, and over the first eight

months of 1994 by 12 per cent as compared with the corresponding period of the

previous year. Total oil exports in 1994 reached around 90 million metric tons, the

highest level since 1991. Other main Russian export goods also grew very rapidly in

physical terms between 1993 and 1994.

Table No-9A

Commodity structure of Russian foreign trade, 1990-1993

(Billion dollar and percentages)

Exports

I. Value (billion dollars)

Machinery & Equipment,

means of transport

Mineral products (Fuel)

Metala, precious stones

Chemical, rubber

Timber, paper, cellulose

Textiles, footwear

Leather, furs & related articles

Food stuffs & agricultural raw

materials

Others

Total

Structures (per cent)

Machinery and equipment,

Means of transport

1990 1991 1992 1993

12.5

32.3

9.2

3.3

3.1

0.7

0.1

1.5

8.4

11.1

5.2 3.7 2.9

26.3 21.7 20.7

7.3 8.5 10.3

3.4 2.5 2.6

2.4 1.5 1.9

0.5 0.3 0.2

0.1 0.1 0.1

1.3 1.5 1.6

4.4 2.6 4.0

50.9 42.4 44.3

17.6 10.2 8.7 6.5

153

Mineral products 45.4 51.7 51.2 46.7

Metala, precious stones 12.9 14.3 20.0 23.3

Chemical, rubber 4.6 6.7 5.9 5.9

Timber, paper, cellulose 4.4 4.7 3.5 4.3

Textiles, footwear 1.0 1.0 0.7 0.5

Leather, furs & related articles 0.1 0.2 0.2 0.2

Food stuffs & agricultural raw

materials 2.1 2.6 3.5 3.6

Others 11.8 8.6 6.1 9.0

Total 100.0 100.0 100.0 100.0

Source: Economic Bulletin/or Europe, vol. 46 (1994), p. 72.

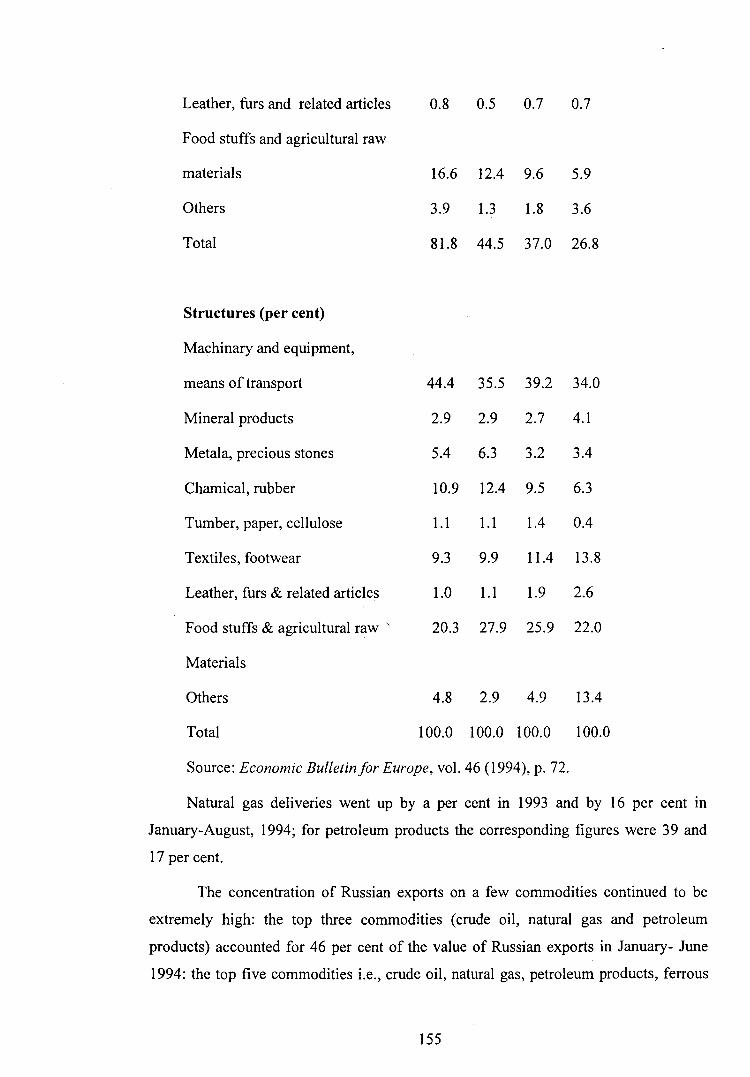

Table No. 9B

Commodity structure of Russian foreign trade, 1990-1994

(Billion dollars and percentages)

Imports

Value (billion dollars) 1990 1991 1992 1993 1994 1995 1996

Machinary and Equipment, 36.3 15.8 14.5 9.1

Means of transport

Mineral products 2.4 1.3 1.0 1.1

Metala, precious stones 4.4 2.8 1.2 0.9

Chamical, rubber 8.9 5.5 3.5 1.7

Tumber, paper, cellulose 0.9 0.5 0.5 0.1

Textiles, footwear 7.6 4.4 4.2 3.7

154

Leather, furs and related articles

Food stuffs and agricultural raw

materials

Others

Total

Structures (per cent)

Machinary and equipment,

means of transport

Mineral products

Metala, precious stones

Chamical, rubber

Tumber, paper, cellulose

Textiles, footwear

Leather, furs & related articles

Food stuffs & agricultural raw '

Materials

Others

Total

0.8 0.5 0.7 0.7

16.6 12.4 9.6 5.9

3.9 1.3 1.8 3.6

81.8 44.5 37.0 26.8

44.4 35.5 39.2 34.0

2.9 2.9 2.7 4.1

5.4 6.3 3.2 3.4

10.9 12.4 9.5 6.3

1.1 1.1 1.4 0.4

9.3 9.9 11.4 13.8

1.0 1.1 1.9 2.6

20.3 27.9 25.9 22.0

4.8 2.9 4.9 13.4

100.0 100.0 100.0 100.0

Source: Economic Bulletin/or Europe, vol. 46 (1994), p. 72.

Natural gas deliveries went up by a per cent in 1993 and by 16 per cent in

January-August, 1994; for petroleum products the corresponding figures were 39 and

17 per cent.

The concentration of Russian exports on a few commodities continued to be

extremely high: the top three commodities (crude oil, natural gas and petroleum

products) accounted for 46 per cent of the value of Russian exports in January- June

1994: the top five commodities i.e., crude oil, natural gas, petroleum products, ferrous

155

metals and diamonds account for 60 per cent. In addition to the above five

commodities, taking aluminum, timber, fish, fertilizers and cars into account, the top

ten account for three quarter of Russian exports.

The other tendency found in case of export of civilian machines & equipment is

that, they have been losing weight within total exports; their share in 1994 is expected

to fall below 5 per cent level15•

However, exports of military equipment came to around $ 3 billion in 1993 97

per cent of total exports of 1993) and will probably reach 4 billion in 1994, the decline

in civilian machinery exports seems to be a structural tendency rather than a temporary

phenomenon. Both demand supply factors play their role.

On the supply side, the domestic output of machinery and equipment registered

the highest contraction among all industrial branches. Russian machinery exports

(consisting mainly of heavy material - and energy intensive machinery) were

traditionally channeled to the CMEA and developing countries. The ex-CMEA market

is now practically lost for Russian machinery shipments, while the developing countries

are also reducing their purchases as Russian exporters are no longer in a position to

offer their products on favourable credit conditions. The main advantage to Russian

machinery export was their cheapness, which offset the low quality and generfllly poor

technical standard of goods. But the strong tendency towards appreciation of the

Rouble in real terms, a considerable increase of domestic energy prices and the

discontinuation of subsidized state credits have wiped out this advantage.

On the import side, the analysis of structural changes at the level of aggregated

commodity group shows three main tendencies, a reduction of machinery imports, a

rising share of consumer gods; and some growth of food imports. Thus the general

trend in import adjustment is that they are becoming more consumer oriented than

producer oriented.

Till late 1994 and the first half of 1995, there was no marked change in the

composition of trade. It remained largely a supplier of raw materials and energy

15 Ibid., p. 73.

156

products. Similarly, according to the custom data, the growth of imports for western

countries was concentrated in the first half of 1995. 16

In the first half of 1996, the combined share of mineral products including fuel

in the total Russian exports was 70 per cent as against 62 per cent at close of 1994. In

terms of value, in the first of 1996, there was growth of 39 per cent in the base

metals/minerals like crude oil, natural gas etc. Exports of precious stones, metals, ores

which accounted for 13 per cent in 1994, fell down to 7.5 percentage points. The most

probable reasons for this fall were high supply prices dictated by the state monopoly on

the domestic market reinforced by high taxes on domestic producers, and a dispute in

the uncut diamond sales deal with De Beers, which temporarily interrupted sales. The

share of machinery and equipment in Russian's exports remained under 3 per cent in

the first half of 1996 which is very close to 1994 figure. (Data: Economic Survey of

Europe, no. 3 (1998), p. 94).

However, in value terms, these commodities were fastest growing commodity

group. Imports of machinery and equipment fell by 15 per cent in value, and their share

in total import by 3 percentage points in the first half of 1996 as compared with the

same period of 1995. Falling imports from the West of some industrial consumer goods

and foodstuffs, including agricultural products, seem to have been partially offset by

increased imports from the CIS region.

During the first half of 1997 as compared with the same periods, the two

outstanding sectoral performers bucking the trend were the mineral products sector and

opticals, precision and medical equipment, which increased in value terms by 12 and

72 per cent, respectively.

In 1998, however, a remarkable departure in the trading of mineral products was

noticed. There was a significant fall of 28 per cent in the value of exports of such

products, which is due to the decline in crude oil process, while the fall in exports of

metal largely reflects weak import demand and lower prices for ferrous metals, nickel

and copper. Exports of precious metals and stones doubled, probably reflecting the

1998 liberalistion of gold exports that allowed Russian banks to exports precious metals

and the 1997 supply agreement between Alrosa, Russia's main diamond producer, and

worlds diamond cartel. (Data Economic Survey of Europe, No.3, 1998, p. 1994-1995).

16 Economic Bulletin for Europe, vol. 47 (1995), p. 67.

157

In 1998, the value of Russia's imports of food rose by almost robust 50 per cent

reflecting increased volumes and continued stagnation of domestic agricultural

production. Imports of machinery and equipment as well as chemicals slowed down

reflecting stagnant aggregate industrial production in Russia in the first half of 1998 as

compared to the period a year back.

OVERALL TRADE PERFORMANCE OF RUSSIAN FEDERATION (1992-1998):

After the break up of the USSR, the Russian Federation found its foreign trade

sector substantially expanded as what had been inter-republic trade within the Soviet

Union, now became external trade. The levels of Russian foreign trade in 1989-90 fell

sharply in the following years suffering from a battery of external and internal shocks

such as the collapse of CMEA in 1991, the disintegration of the Soviet Union and the

break up of the centralized controls over the economy in the absence of an efficient

market mechanism. In 1992, both exports and 'imports fell by 17 per cent. In that year,

the trade performance was affected, above all, by the frequent changes of regulations,

but also by general economic recession that followed price liberalization Exports were

mainly limited by various supply constraints while imports demand fell because of very

high process of important goods in rouble terms. During the second year of economic

reform (1993), exports increased by 4.5 per cent, but imports fell by almost 28 per

cent, mainly because cf sharp cut in cenrtralised imports, which were subsidized from

the state budget.

In the first half of 1994, exports grew even faster than in the previous year.

Moreover imports also started to improve, showing an increase of almost 4 per cent

over the corresponding period of the previous year. 17

During the first half of 1995, as compared with the same period of previous

year, the dollar value of the Russian Federations trade with non-CIS countries grew

very rapidly. The value of Russian exports increased by 39 per cent, growing for the

third consecutive year, while imports grew by 17 per cent, following an increase of 5

per cent in 1994. 18 There was significant value growth in trade with all major partner

17

18 Ibid, p. 62. Ibid, p. 62.

158

groups, including, for the first time since the collapse of the CMAEA, former CMEA

member countries.

However, a significant part of the rise in these dollar trade values reflects the

substantial depreciation of the dollar against other major currencies; hence, in the

absence of aggregate price and volume indices, the interpretations of this apparent

acceleration of trade growth must remain rather uncertain. On a rather tentative

assessment it would appear that export growth indeed accelerated some what in volume

terms, expanding at some 10-12 per cent, where as most of the value growth in imports

probably reflects price changes, volume remaining stagnant.

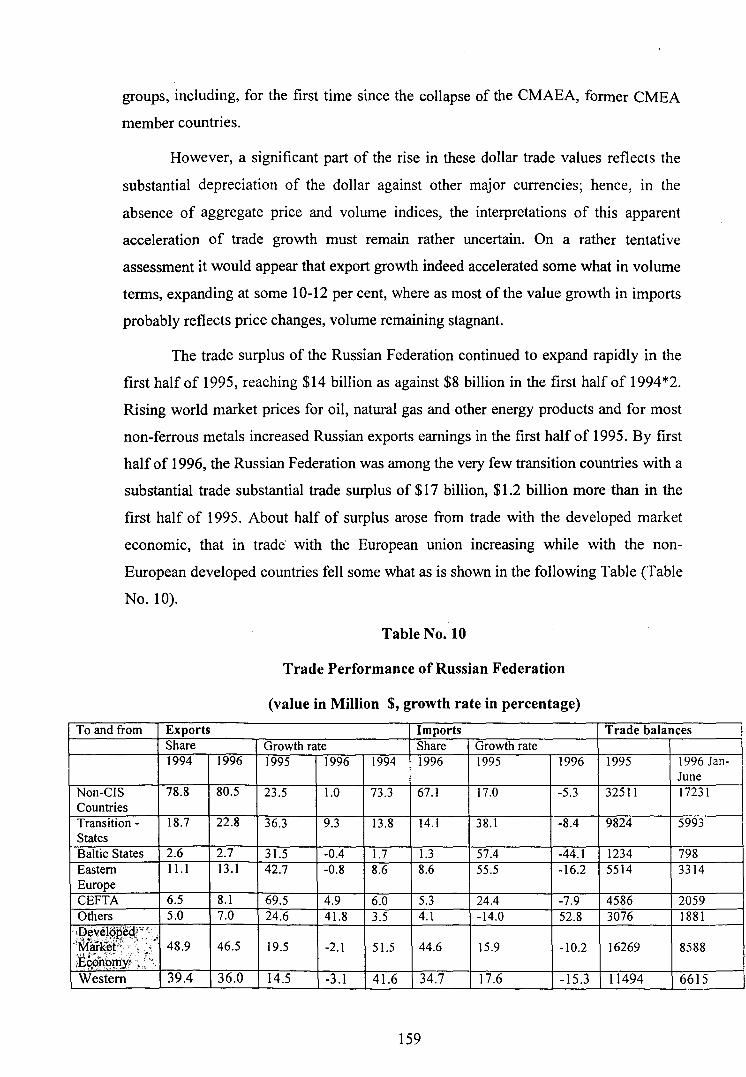

The trade surplus of the Russian Federation continued to expand rapidly in the

first half of 1995, reaching $14 billion as against $8 billion in the first half of 1994*2.

Rising world market prices for oil, natural gas and other energy products and for most

non-ferrous metals increased Russian exports earnings in the first half of 1995. By first

half of 1996, the Russian Federation was among the very few transition countries with a

substantial trade substantial trade surplus of $17 billion, $1.2 billion more than in the

first half of 1995. About half of surplus arose from trade with the developed market

economic, that in trade· with the European union increasing while with the non

European developed countries fell some what as is shown in the following Table (Table

No. 10).

Table No. 10

Trade Performance of Russian Federation

(value in Million $, growth rate in percentage)

To and from Exports Imports Trade balances Share Growth rate Share Growth rate 1994 1996 1995 1996 1994 1996 1995 1996 1995 1996 Jan-

June Non-CIS 78.8 80.5 23.5 1.0 73.3 67.1 17.0 -5.3 32511 17231 Countries Transition - 18.7 22.8 36.3 9.3 13.8 14.1 38.1 -8.4 9824 5993 States Baltic States 2.6 2.7 31.5 -0.4 1.7 1.3 57.4 -44.1 1234 798 Eastern 11.1 13.1 42.7 -0.8 8.6 8.6 55.5 -16.2 5514 3314 Europe CEFTA 6.5 8.1 69.5 4.9 6.0 5.3 24.4 -7.9 4586 2059 Others 5.0 7.0 24.6 41.8 3.5 4.1 -14.0 52.8 3076 1881

·,Deveio~ooY''-:·

·:mgl{~f~~ ~: '; , ·· 48.9 46.5 19.5 -2.1 51.5 44.6 15.9 -10.2 16269 8588 !E9,<>N~¢y! ,,; : Western 39.4 36.0 14.5 -3 .I 41.6 34.7 17.6 -15.3 11494 6615

159

Europe European 33.2 31.0 17.2 -4.6 32.2 33.2 44.5 -15.2 8241 4916 union Germany 8.1 7.5 10.5 7.0 14.7 10.8 15.1 -28.0 -496 543 Others 9.5 10.5 40.1 .}.3 10.0 10.0 8.9 13.6 4775 1973 Developing 11.3 11.3 20.1 -1.0 8.0 8.4 8.4 13.6 6417 2651 countries CIS 21.2 19.5 -0.1 20.6 26.7 32.9 31.3 49.7 720 323 World Total 100.0 100.0 18.5 4.3 100.0 100.0 10.8 7.8 33230 17554

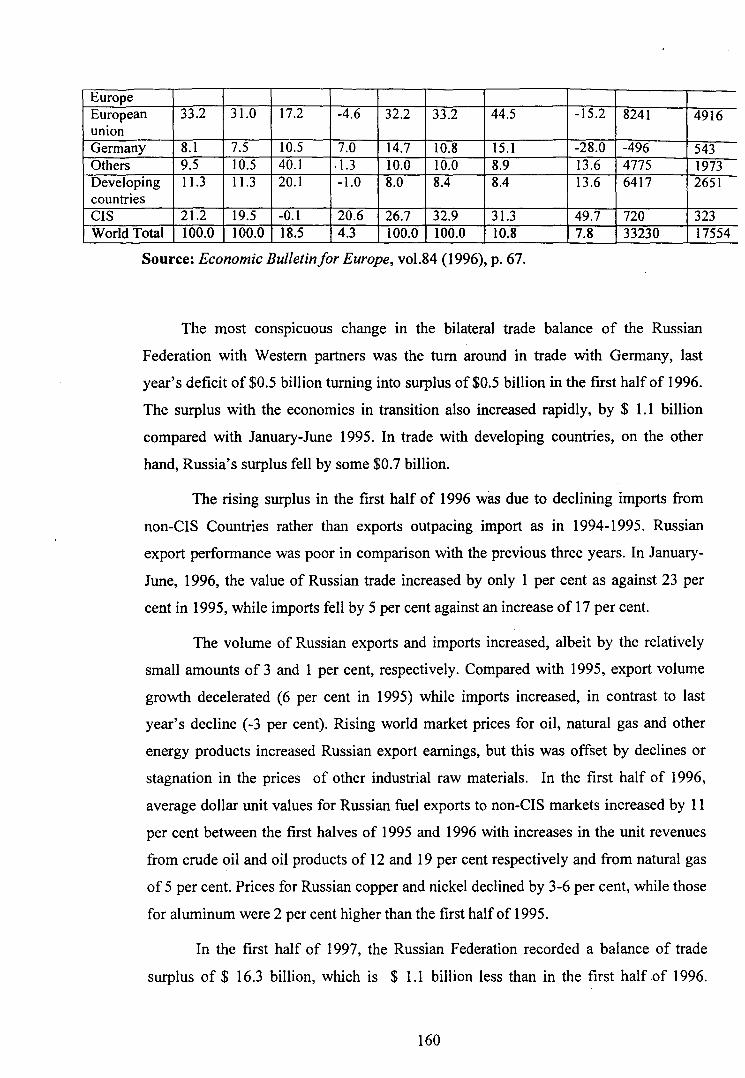

Source: Economic Bulletin/or Europe, vol.84 (1996), p. 67.

The most conspicuous change in the bilateral trade balance of the Russian

Federation with Western partners was the turn around in trade with Germany, last

year's deficit of $0.5 billion turning into surplus of $0.5 billion in the first half of 1996.

The surplus with the economies in transition also increased rapidly, by $ 1.1 billion

compared with January-June 1995. In trade with developing countries, on the other

hand, Russia's surplus fell by some $0.7 billion.

The rising surplus in the first half of 1996 was due to declining imports from

non-CIS Countries rather than exports outpacing import as in 1994-199 5. Russian

export performance was poor in comparison with the previous three years. In January

June, 1996, the value of Russian trade increased by only 1 per cent as against 23 per

cent in 1995, while imports fell by 5 per cent against an increase of 17 per cent.

The volume of Russian exports and imports increased, albeit by the relatively

small amounts of 3 and 1 per cent, respectively. Compared with 1995, export volume

growth decelerated (6 per cent in 1995) while imports increased, in contrast to last

year's decline ( -3 per cent). Rising world market prices for oil, natural gas and other

energy products increased Russian export earnings, but this was offset by declines or

stagnation in the prices of other industrial raw materials. In the first half of 1996,

average dollar unit values for Russian fuel exports to non-CIS markets increased by 11

per cent between the first halves of 1995 and 1996 with increases in the unit revenues

from crude oil and oil products of 12 and 19 per cent respectively and from natural gas

of 5 per cent. Prices for Russian copper and nickel declined by 3-6 per cent, while those

for aluminum were 2 per cent higher than the first half of 1995.

In the first half of 1997, the Russian Federation recorded a balance of trade

surplus of $ 16.3 billion, which is $ 1.1 billion less than in the first half of 1996.

160

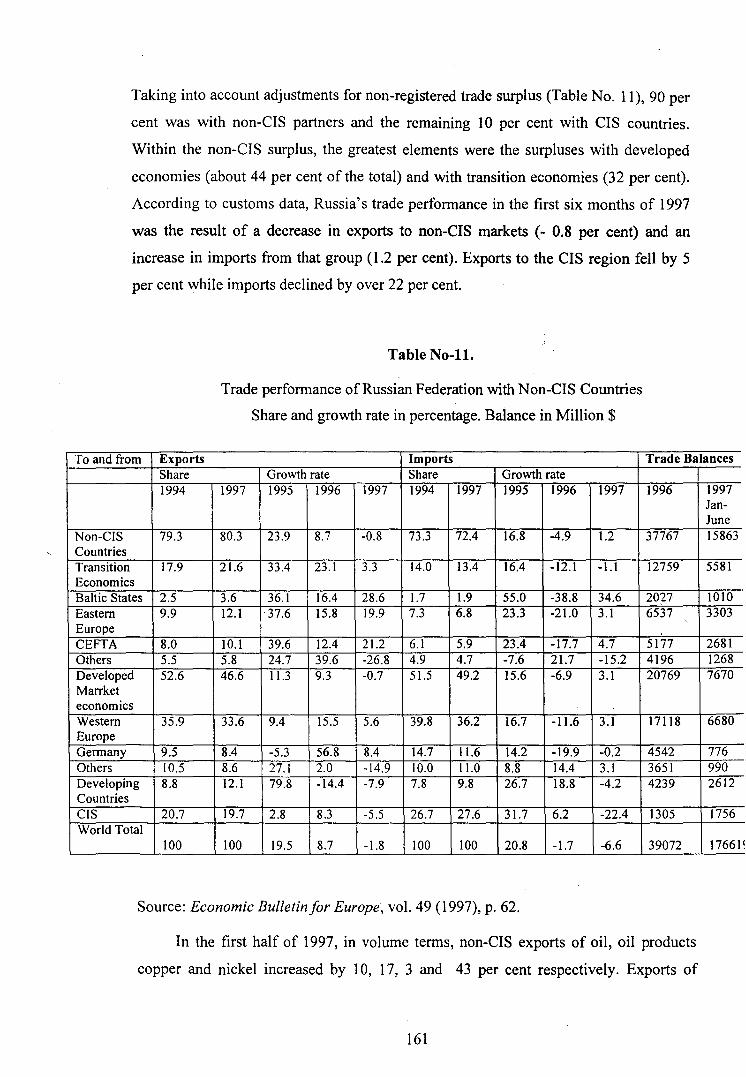

Taking into account adjustments for non-registered trade surplus (Table No. 11 ), 90 per

cent was with non-CIS partners and the remaining 10 per cent with CIS countries.

Within the non-CIS surplus, the greatest elements were the surpluses with developed

economies (about 44 per cent of the total) and with transition economies (32 per cent).

According to customs data, Russia's trade performance in the first six months of 1997

was the result of a decrease in exports to non-CIS markets (- 0.8 per cent) and an

increase in imports from that group (1.2 per cent). Exports to the CIS region fell by 5

per cent while imports declined by over 22 per cent.

Table No-11.

Trade performance of Russian Federation with Non-CIS Countries

Share and growth rate in percentage. Balance in Million $

To and from Exports Imports Trade Balances Share Growth rate Share Growth rate 1994 1997 1995 1996 1997 1994 1997 1995 1996 1997 1996

Non-CIS 79.3 80.3 23.9 8.7 -0.8 73.3 72.4 16.8 -4.9 1.2 37767 Countries Transition 17.9 21.6 33.4 23.1 3.3 14.0 13.4 16.4 -12.1 -1.1 12759 Economics Baltic States 2.5 3.6 36.1 16.4 28.6 1.7 1.9 55.0 -38.8 34.6 20f7 Eastern 9.9 12.1 37.6 15.8 19.9 7.3 6.8 23.3 -21.0 3.1 6537 Europe CEFTA 8.0 10.1 39.6 12.4 21.2 6.1 5.9 23.4 -17.7 4.7 5177 Others 5.5 5.8 24.7 39.6 -26.8 4.9 4.7 -7.6 21.7 -15.2 4196 Developed 52.6 46.6 11.3 9.3 -0.7 51.5 49.2 15.6 -6.9 3.1 20769 Marrket economics Western 35.9 33.6 9.4 15.5 5.6 39.8 36.2 16.7 -11.6 3.1 17118 Europe Germany 9.5 8.4 -5.3 56.8 8.4 14.7 11.6 14.2 -19.9 -0.2 4542 Others 10.5 8.6 27.1 2.0 -14.9 10.0 11.0 8.8 14.4 3.1 3651 Developing 8.8 12.1 79.8 -14.4 -7.9 7.8 9.8 26.7 18.8 -4.2 4239 Countries CIS 20.7 19.7 2.8 8.3 -5.5 26.7 27.6 31.7 6.2 -22.4 1305 World Total

100 100 19.5 8.7 -1.8 100 100 20.8 -1.7 -6.6 39072

Source: Economic Bulletin for Europe, vol. 49 (1997), p. 62.

In the first half of 1997, in volume terms, non-CIS exports of oil, oil products

copper and nickel increased by 10, 17, 3 and 43 per cent respectively. Exports of

161

1997 Jan-June 15863

5581

1010 3303

2681 1268 7670

6680

776 990 2612

1756

17661 ~

natural gas, coal, aluminum decreased by 7, 20 and 0.7 per cent respectively. In the first

half of 1997, Russia's average exports prices for energy products such as coal, oil and

oil products did not change much relative to 1996. In contrast, the natural gas export

price increased by over 50 per cent. Interestingly, the price increases for coal and

natural gas were offset by the export volume declines noted above. With respect to

metals, which are Russian's second most important source of export earnings, average

export prices were lower than the first half of 1996, Iron, copper, nickel and aluminum·

prices were 12.7, 12, 9.3 and 9.2 per cent lower respectively, in the first six months of

1997.

In the first half of 1998, in value terms, Russia's exports to non-CIS markets fell

by 15 per cent. Virtually all ofthe decline can be attributed to lower prices for Russia's

key exports as the overall volume of non-CIS exports was only slightly lower. On the

import side, thevalue of Russia's non-CIS purchases continued to grow albeit at a

lower rate than in 1997. Average import prices fell by 5 and 12 per cent respectively,

compared with the same periods of 1997, stimulating increased import demand. The

increased volume of imports from Non-CIS markets, while very high in the first quarter

-32 per cent slowed down to 17 per cent in the second quarter. Merchandise trade

surplus with non-CIS countries was roughly half of what it was in first half of 1997.

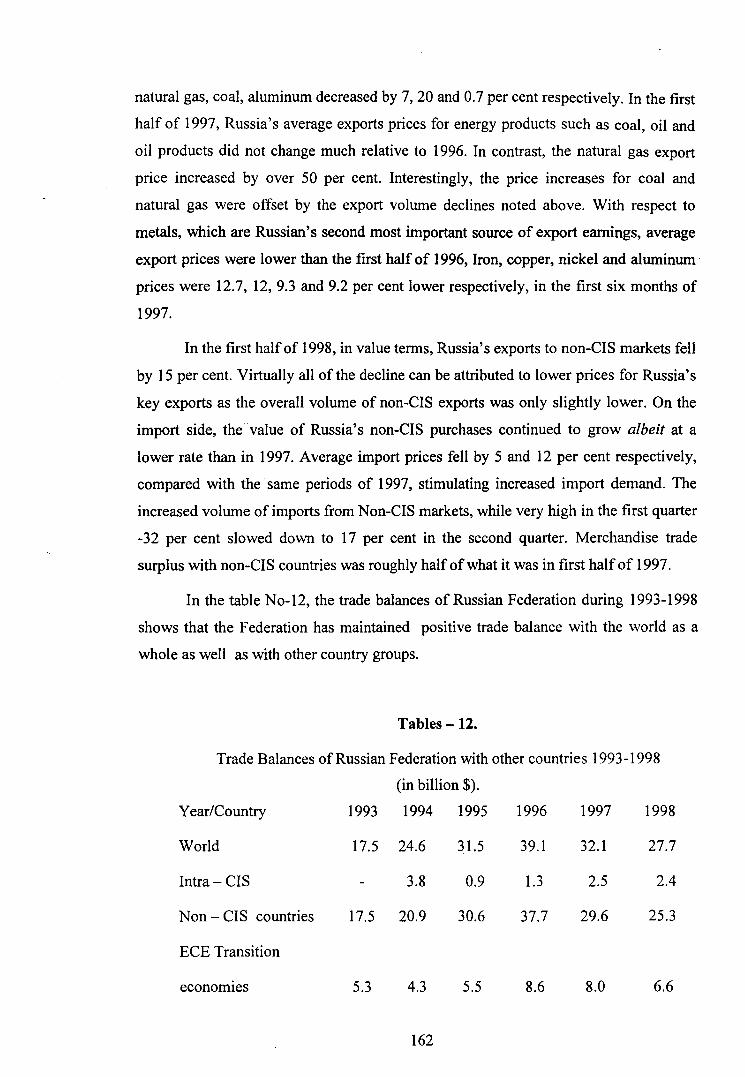

In the table No-12, the trade balances of Russian Federation during 1993-1998

shows that the Federation has maintained positive trade balance with the world as a

whole as well as with other country groups.

Tables -12.

Trade Balances of Russian Federation with other countries 1993-1998

(in billion$).

Year/Country 1993 1994 1995 1996 1997 1998

World 17.5 24.6 31.5 39.1 32.1 27.7

Intra- CIS 3.8 0.9 1.3 2.5 2.4

Non- CIS countries 17.5 20.9 30.6 37.7 29.6 25.3

ECE Transition

economies 5.3 4.3 5.5 8.6 8.0 6.6

162

Eastern Europe 4.6 3.3 4.3 6.6 5.9 5.0

Developed market

economies 10.2 12.8 15.6 18.8 13.6 12.6

Euporian Union 8.4 6.9 8.4 11.5 8.4 7.5

Developing Countries 2.0 3.8 9.4 10.3 8.0 6.2

Source: Economic Survey of Europe, No.3 (1998), P. 73

Even though, there were ups and down in the trade with certain region or among

the commodities, the overall trade performance has shown a marked improvement

following the reforms.

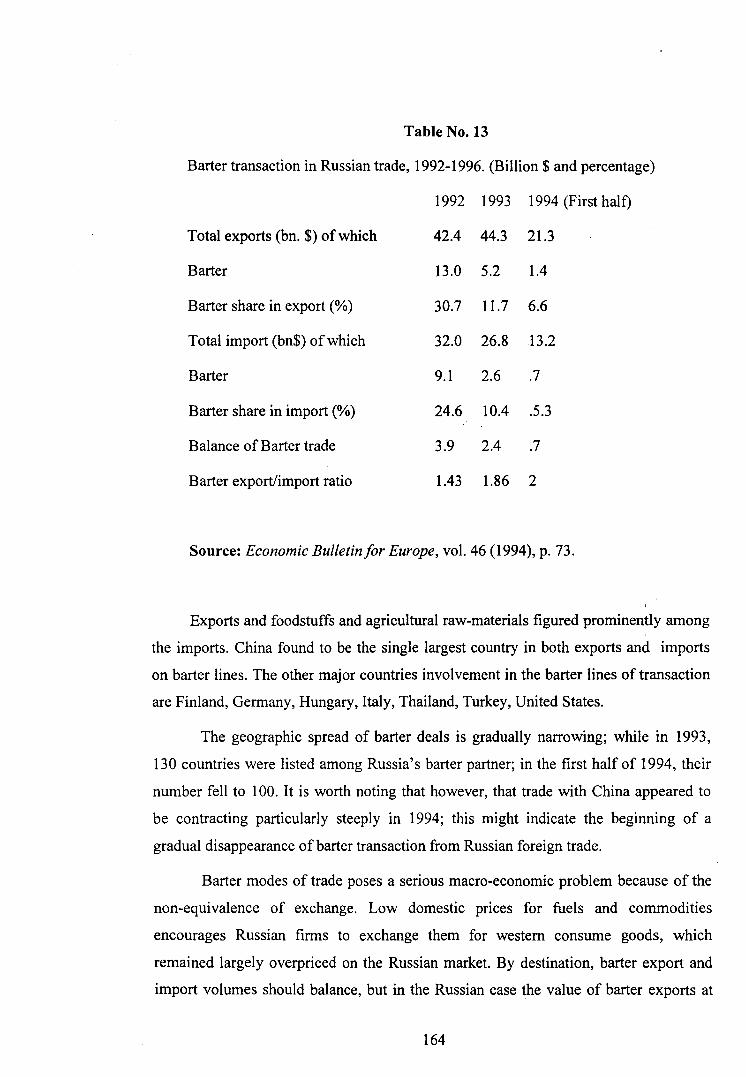

ROLE OF BARTER TRANSACTIONS IN RUSSIA'S FOREIGN TRADE: .

Barter transactions have played a significant role in Russia's trade since 1991,

when state control over foreign tra,de was eased and the initial stabilization and first

reform attempts resulted in an acute financial squeeze on Russian enterprises. Barter

trade offered possibilities to circumvent foreign exchange constraints and the

advantage of huge differentials between domestic and international prices. In addition,

the attractiveness of barter in 1992 was boosted, in the case of barter exports, by the

exemption from the compulsory surrender of foreign exchange at a below-market rate

(55 R/$), but this privilege lost its attraction when a single floating rate was introduced

in July 1992. (Economic Bulletin/or Europe, Vol.46 (1994), P.73)

Barter export constituted only 30 per cent of the total exports of the commodity

group in 1992 while barter import accounted for only 9.1 per cent. Among the

commodity group's, it is the mineral products including fuel, which constituted 25 per

cent of the total.

163

Table No.13

Barter transaction in Russian trade, 1992-1996. (Billion $ and percentage)

1992 1993 1994 (First half)

Total exports (bn. $)of which 42.4 44.3 21.3

Barter 13.0 5.2 1.4

Barter share in export (%) 30.7 11.7 6.6

Total import (bn$) of which 32.0 26.8 13.2

Barter 9.1 2.6 .7

Barter share in import (%) 24.6 10.4 .5.3

Balance of Barter trade 3.9 2.4 .7

Barter export/import ratio 1.43 1.86 2

Source: Economic Bulletin/or Europe, vol. 46 (1994), p. 73.

Exports and foodstuffs and agricultural raw-materials figured prominently among

the imports. China found to be the single largest country in both exports and imports

on barter lines. The other major countries involvement in the barter lines of transaction

are Finland, Germany, Hungary, Italy, Thailand, Turkey, United States.

The geographic spread of barter deals is gradually narrowing; while in 1993,

130 countries were listed among Russia's barter partner; in the first half of 1994, their

number fell to 100. It is worth noting that however, that trade with China appeared to

be contracting particularly steeply in 1994; this might indicate the beginning of a

gradual disappearance of barter transaction from Russian foreign trade.

Barter modes of trade poses a serious macro-economic problem because of the

non-equivalence of exchange. Low domestic prices for fuels and commodities

encourages Russian firms to exchange them for western consume goods, which

remained largely overpriced on the Russian market. By destination, barter export and

import volumes should balance, but in the Russian case the value of barter exports at

164

world market prices usually exceeded the value of imports by a large margin. the

resulting losses for the national income are important. The government tried to reduce

the scope of barter transactions by exposing them to higher export taxation: in 1992,

were 15 per cent and later 30 per cent, higher than for regular transactions. From 1st

January 1993, the tax margin was raised to 50 per cent. However, from 1 November

1993, the separate export tariff for barter transactions was abolished under the law on

customs Tariffs which established uniform tariff rates partly as a result of these

measures, but also because of the gradual convergence of relative prices in Russia and

in international markets, the share of barter deals in over all trade flows has been

decreasing as could be seen on Table No-13.

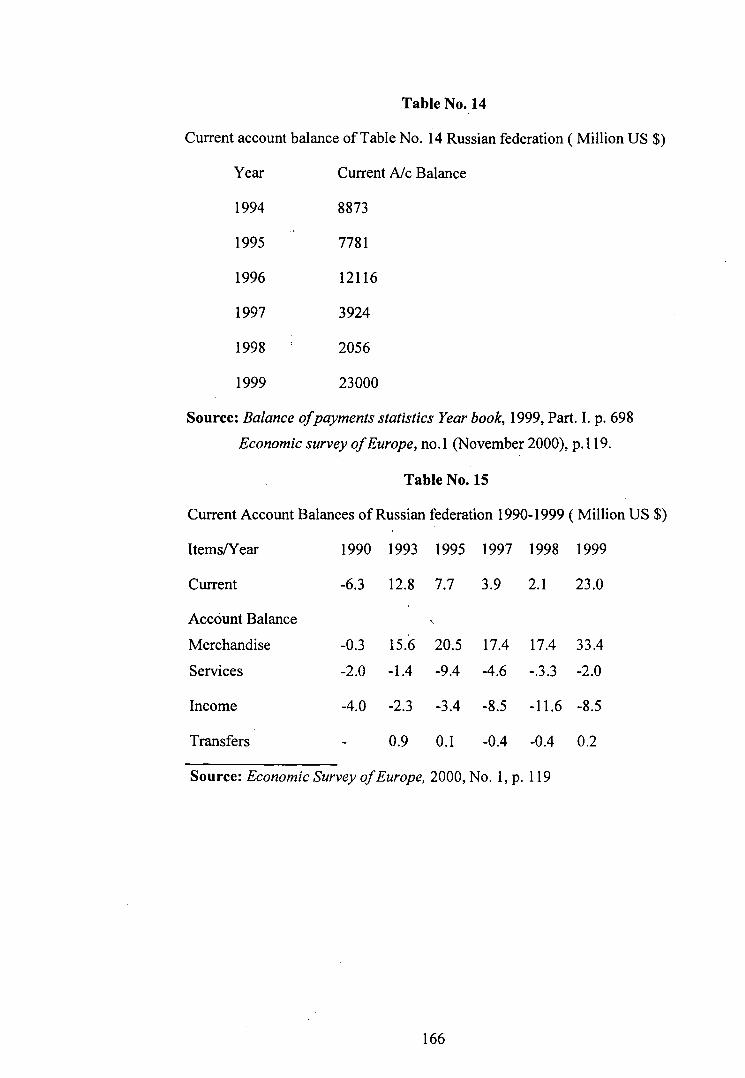

BALANCE OF PAYMENT POSITION OF RUSSIAN FEDERATION:

During the post reform period i.e., during 1992 and beyond, almost all transition

economies record negative current account balance or deficit in their overall balance of

payment statement, where as Russian federation maintained positive current account

balance through out. During 1990, it recorded $ - 6.3 million trade deficit which rose to

$ 12.8 million in 1993 showing an upward movement by about $ 16 million. During

1994, however, it maintained a trade current account balance of about $ 8.8 million

though there was corresponding increase in exports, but there was depreciation in the

value of Rouble. Starting from 1993 to 1999, the currant account balances, though

remained positive, it could not maintain a definite trend which is adjustable to

fluctuating Rouble dollar exchange rate. The trend of the current account balance

starting from 1994 to 1999 is presented in table no- 14 where as the table no-2 shows

the break up of the balances under the different items of current account. An interesting

feature could be seen from the table no-15 which shows that throughout 1993-1999, all

other balances were negative except the merchandised trade balance.

On capital account front, except the year 1994, during 1994-1999, the capital

account balance ran negative through out. The balance of payment position during the

above noted period in shown in tables no-14.

165

Table No. 14

Current account balance ofTable No. 14 Russian federation (Million US$)

Year Current Nc Balance

1994 8873

1995 7781

1996 12116

1997 3924

1998 2056

1999 23000

Source: Balance ofpayments statistics Year book, 1999, Part. I. p. 698

Economic survey of Europe, no.1 (November 2000), p.119.

Table No.15

Current Account Balances of Russian federation 1990-1999 ( Million US $)

Items/Year 1990 1993 1995 1997 1998 1999

Current -6.3 12.8 7.7 3.9 2.1 23.0

Account Balance ',

Merchandise -0.3 15.6 20.5 17.4 17.4 33.4

Services -2.0 -1.4 -9.4 -4.6 -.3.3 -2.0

Income -4.0 -2.3 -3.4 -8.5 -11.6 -8.5

Transfers 0.9 0.1 -0.4 -0.4 0.2

Source: Economic Survey of Europe, 2000, No. I, p. 119

166

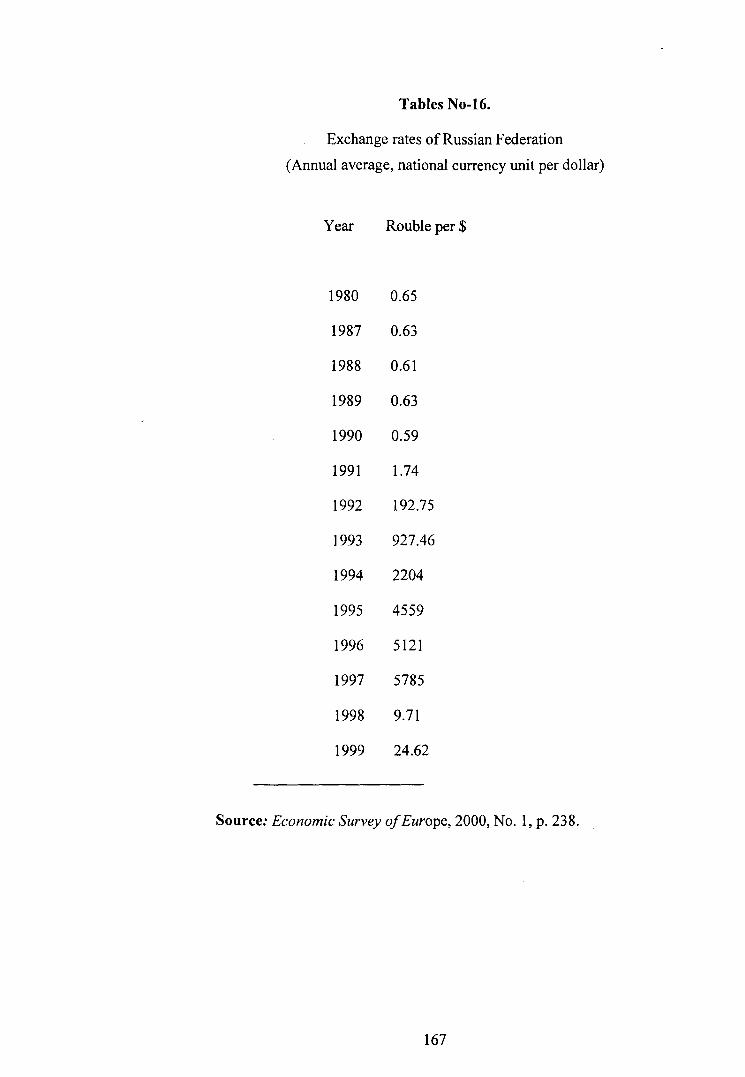

Tables No-16.

Exchange rates of Russian Federation

(Annual average, national currency unit per dollar)

Year Rouble per $

1980 0.65

1987 0.63

1988 0.61

1989 0.63

1990 0.59

1991 1.74

1992 192.75

1993 927.46

1994 2204

1995 4559

1996 5121

1997 5785

1998 9.71

1999 24.62

Source: Economic Survey of Europe, 2000, No. 1, p. 238.

167

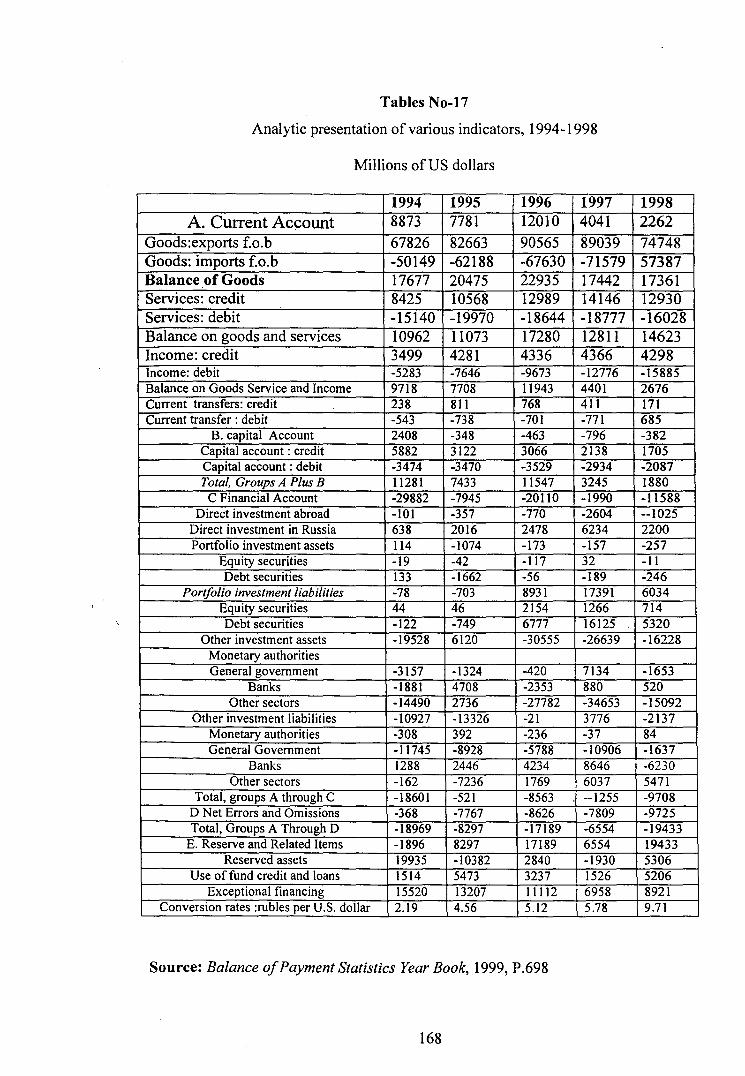

Tables No-17

Analytic presentation of various indicators, 1994-1998

Millions of US dollars

1994 1995 1996 1997 1998 A. Current Account 8873 7781 12010 4041 2262

Goods:exports f.o.b 67826 82663 90565 89039 74748 Goods: imports f.o.b -50149 -62188 -67630 -71579 57387 Balance of Goods 17677 20475 22935 17442 17361 Services: credit 8425 10568 12989 14146 12930 Services: debit -15140 -19970 -18644 -18777 -16028 Balance on goods and services 10962 11073 17280 12811 14623 Income: credit 3499 4281 4336 4366 4298 Income: debit -5283 -7646 -9673 -12776 -15885 Balance on Goods Service and Income 9718 7708 11943 4401 2676 Current transfers: credit 238 811 768 411 171 Current transfer : debit -543 -738 -701 -771 685

B. capital Account 2408 -348 -463 -796 -382 Capital account : credit 5882 3122 3066 2138 1705 Capital account : debit -3474 -3470 -3529 -2934 -2087 Total, Groups A Plus B 11281 7433 11547 3245 1880

C Financial Account -29882 -7945 -20110 -1990 -11588 Direct investment abroad -101 -357 -770 -2604 --1025

Direct investment in Russia 638 2016 2478 6234 2200 Portfolio investment assets 114 -1074 -173 -157 -257

Equity securities -19 -42 -117 32 -11 Debt securities 133 -1662 -56 -189 -246

Portfolio investment liabilities -78 -703 8931 17391 6034 Equity securities 44 46 2154 1266 714 Debt securities -122 -749 6777 16125 5320

Other investment assets -19528 6120 -30555 -26639 -16228 Monetary authorities General government -3157 -1324 -420 7134 -1653

Banks -1881 4708 -2353 880 520 Other sectors -14490 2736 -27782 -34653 -15092

Other investment liabilities -10927 -13326 -21 3776 -2137 Monetary authorities -308 392 -236 -37 84 General Government -11745 -8928 -5788 -10906 -1637

Banks 1288 2446 4234 8646 -6230 Other sectors -162 -7236 1769 6037 5471

Total, groups A through C -18601 -521 -8563 --1255 -9708 D Net Errors and Omissions -368 -7767 -8626 -7809 -9725 Total, Groups A Through D -18969 -8297 -17189 -6554 -19433

E. Reserve and Related Items -1896 8297 17189 6554 19433 Reserved assets 19935 -10382 2840 -1930 5306

Use offund credit and loans 1514 5473 3237 1526 5206 Exceptional financing 15520 13207 11112 6958 8921

Conversion rates :rubles per U.S. dollar 2.19 4.56 5.12 5.78 9.71

Source: Balance of Payment Statistics Year Book, 1999, P.698

168

EXCHANGE RATE PROBLEM: FIXED V/S FLEXIBLE RATE:

Having shed light on current account trade balances of the last few years, the

most important segment of balance of payment statement, the next pertinent question

that needs to be answered is the sustainability of the current account balance (surplus)

given the pace and parameters of trade reforms. Exchange rate volatility has attributed

inter alia other factors, towards the fluctuations of current account surplus (CAS).

Therefore, a special care needs to be attached to the exchange rate problems to even out

any abnormal volatility of roubles in order to allow smooth trade operation.

On August 17, 1998 the Russian government announced the widening of the

exchange rate band vis-a vis the US$, which in fact meant the giving up of the

exchange rate target and the introduction of flexi~le exchange rates. 19 At the same time

a moratorium of external debts and the imposition of capital account controls were

decided. The failure of monetary system and the insolvency of the government have

been the result of a deep crisis of the financial sector which had long been apparent, but

nevertheless surprised investors by its severity. The dramatic flight of the rouble might

immediately lead to a new era of hyper inflation. This ominous situation provides the

background for the revising discussion about what would constitute an adequate

exchange rate system.

In the countries with a weak financial sector, there is a fatal trade-off between the

possible import of macro-economic stabilisation via a nominal exchange rate peg and

the vulnerability to speculative attacks that can only be excluded in a region with

flexible exchange rates. Past proposals that aimed at mitigating this trade-off have been

ignored by politicians because they seemed to be too complicated or simply because the

underlying monetary system was unpopular at the time. On trade and international

economy sector front, to break the vicious circle of lack of credibility, inflationary