saed khalil and michel dombrecht - pma > home · saed khalil and michel dombrecht ... and when...

TRANSCRIPT

PALESTINE MONETARY AUTHORITY

PMA WORKING PAPER

WP/11/03

THE AUTOREGRESSIVE DISTRIBUTED LAG APPROACH TO CO-INTEGRATION TESTING: APPLICATION TO OPT INFLATION

Saed Khalil and Michel Dombrecht

® Palestine Monetary Authority WP/11/03

ii

PMA Working Paper

Research and Monetary Policy Department

The Autoregressive Distributed Lag Approach to Co-integration Testing: Application to OPT Inflation

Prepared by Saed Khalil* and Michel Dombrecht†

November 2011

Abstract This paper aims at estimating and forecasting the inflation rate in the OPT using the ARDL approcach to co-integration testing as an alternative to the Johansen’s co-integration testing used in the inflation report. Findings show that the results of the ARDL and the FMOLS approaches are very close. And when comparing the ARDL with the Johansen test for co-integration, the results are close and not contradicoty. Hence, ARDL and the FMOLS approches along with the Johansen testing for co-integration are suggested to be used in the inflation report for Palestine.

© November, 2011 All Rights Reserved. Suggested Citation: Palestine Monetary Authority (PMA), 2011. The Autoregressive Distributed Lag Approach to Co-integration Testing: Application to OPT Inflation. Ramallah – Palestine All Correspondence should be directed to: Palestine Monetary Authority (PMA) P. O. Box 452, Ramallah, Palestine. Tel.: 02-2409920 Fax: 02-2409922 E-mail: [email protected] www.pma.ps

JEL Classification Numbers: C18, C50, E31 Keywords: Econometric methodology, Macroeconometrics, Inflation, . Authors’ E-mail addresses: [email protected]; [email protected]

* Palestine Monetary Authority. † University of Antwerp and Hogeschool Universiteit Brussels, Belgium.

iii

Contents

I. INTRODUCTION .................................................................................................................................................................. 1

II. METHODOLOGY ................................................................................................................................................................. 1

II.1 TESTING PROCEDURE ............................................................................................................................................................ 2

II.2 MODELING PROCEDURE ....................................................................................................................................................... 3

III. APPLICATION TO OPT INFLATION ........................................................................................................................ 4

III.1 CO-INTEGRATION.................................................................................................................................................................. 4

III.2 ARDL ..................................................................................................................................................................................... 6

III.3 FMOLS .................................................................................................................................................................................. 9

IV. CONCLUSION ................................................................................................................................................................... 10

REFERENCES ........................................................................................................................................................................... 10

iv

1

I. Introduction

This technical paper aims at estimating and forecasting inflation in the Occupied

Palestinian Territory (OPT) using the Autoregressive Distributed Lag (ARDL) approach to

co-integration testing. In the inflation report produced by the Palestine Monetary Authority

(PMA) Johansen’s con-integration testing is used to find the long-run relationships between

inflation rate and its determinants and the Vector Error Correction Model (VECM) is used to

estimate the inflation rate in OPT for 2011 on a quarterly basis.

In this paper we use an alternative approach to Johansen’s co-integration to estimate

inflation rate in OPT. We will build an ARDL model to estimate inflation rate in OPT and

compare the obtained results with those in the inflation report.

In addition to estimating inflation rate for OPT we provide a detailed procedure for

testing an ARDL model, which will be useful for future uses at PMA.

This paper found that the results of the ARDL and the FMOLS approaches are very

close. And when comparing the ARDL approach with the Johansen test of co-integration

results are close and not contradictory.

The rest of the paper is organized as follows. Section II provides the methodology of

estimating the OPT CPI in 2011. Section III presents the results of the estimation based on

three alternative methodologies, Johansen’s co-integration testing, ARDL approach to co-

integration, and the fully modified ordinary least squares (FMOLS) approach. Section IV

concludes.

II. Methodology

The most popular single equation testing for co-integration between a set of I(1)

variables relied on the Engle-Granger (1987) and Phillips-Ouliaris (1990) residual based tests.

Also Hansen’s instability test (1995), Park’s added variables test (1992) and the stochastic

common trends approach of Stock and Watson (1988) are well known. System co-integration

testing is mostly based on Johansen’s (1991, 1995) system based reduced rank approach.

Saed Khalil and Michel Dombrecht

2

Recently, also the so called Autoregressive Distributed Lag (ARDL) test is found in

applied empirical papers. This test is based on Pesaran, Shin (1999) and Pesaran, Shin, Smith

(2001). This technique is reported to offer several advantages. The test is based on a single

ARDL equation, rather than on a VAR as in Johansen, thus reducing the number of

parameters to be estimated. Also unlike the Johansen approach the restrictions on the

number of lags can be applied to each variable separately. The ARDL approach also does not

require pre-testing for the order of integration (0 or 1) of the variables used in the model.

II.1 Testing Procedure

Pesaran, Shin and Smith (PSS 2001) developed a new approach to co-integration

testing which is applicable irrespective of whether the regressor variables are I(0), I(1) or

mutually co-integrated.

The starting point of their test is a data generating process represented by a general

VAR of order p which is rewritten in vector ECM form involving a vector z of variables. They

focus on the conditional modeling of the dependent scalar variable y. To that end, the vector z

is partitioned into the scalar y and vector x of dependent variables. Under the assumption

that there is no feedback from y to x, the model can be written as the following conditional

ECM model for ∆y:

∑−

=−−− +∆+∆+++=∆

1

1

''1.1

'p

ittititxyxtyyt uxzxywcy ωψππ (1)

Where,

w is a set of deterministic variables like the constant term, trend, seasonal dummies,

etc..

c is a vector of coefficients of deterministic variables

ut is the residual term.

To test the absence of a level relationship between y and x, the approach uses a Wald

or F-statistic to test for the joint hypothesis that all coefficients of all (lagged) levels in the

ECM equation are zero. PSS distinguishes five cases according to how the deterministic

ARDL Approach to Co‐integration Testing: Application to OPT Inflation

3

components are specified: no intercepts, no trends; restricted intercepts, no trends;

unrestricted intercepts, no trends; unrestricted intercepts, restricted trends, unrestricted

intercepts, unrestricted trends.

The resulting conditional ECM’s may be interpreted as autoregressive distributed

models of orders (p, p,… p), i.e. ARDL (p, p,…p) models. PSS publishes tabulated asymptotic

critical value bounds for the F-statistic for all 5 conditional ECM models. If the computed F-

statistic from exclusion of levels in the conditional EMS’s fall outside the critical value

bounds, the test allows a conclusive inference without needing to know the integration/co-

integration status of the underlying regressors. But if the F-statistic falls inside the bounds,

inference is inconclusive and knowledge of the order of integration of the underlying

variables is required before conclusive inferences can be made. If the computed F-statistic lies

below the 0.05 lower bound, the hypothesis that there is no level relationship is not rejected

at the 5 percent level. If the statistic falls within the 0.05 bounds, the test is inconclusive and

when the F-statistic lies above the 0.05 upper bound, the hypothesis of no level relationship

is conclusively rejected.

In addition to the F-test, PSS also tabulates asymptotic critical value bounds of the t-

statistic for testing the significance of the coefficient on the lagged dependent variable in the

conditional ECM. Concerning the use of the F and t-statistics, PSS suggests the following

procedure: test H0 using the bounds procedure based on the Wald or F-statistic. If H0 is not

rejected, proceed no further. If H0 is rejected test the coefficient of the lagged dependent

variables using the bounds procedure based on the t-statistic. A large value of t confirms the

existence of a level relationship between y and x;

II.2 Modeling Procedure

Testing for the existence of a level relationship as in the previous section requires that

the coefficients of the lagged changes remain unrestricted. But for the subsequent estimation

of the ECM model, a more parsimonious approach is recommended, such as the ARDL

approach to the estimation of the level relations discussed in Pesaran and Shin (1999). In

practical terms an ARDL (p, p,… p) model is selected from a broader search analysis testing

the lag orders using information criteria such as AIC or SBC. In this respect, it is interesting

that PSS note that the ARDL estimation procedure is directly comparable with the semi-

Saed Khalil and Michel Dombrecht

4

parametric Fully Modified OLS approach (FMOLS) of Phillips and Hansen (1990). From the

parsimonious ARDL specification the specification of the estimated levels relationship is then

derived, as well as the associated ECM model.

III. Application to OPT Inflation

III.1 Co-integration

In the inflation report we built a Vector Error Correction Model (VECM) which

encompasses the long run equilibrium relationship between CPI in OPT and the cost of

imports indicator (CIM, see Michel and Khalil 2011). But simultaneously it also incorporates

the short term dynamics that drive the CPI back to its long run equilibrium path after shocks

have temporarily driven CPI apart from its long run equilibrium. That a long-run co-

integrated relationship between CPI and the cost of imports exists is confirmed by the formal

Johansen co-integration test reported in table 1.

Table 1 Co-integration tests between CPI and CIM in PT (Variables expressed in logarithms)

Unrestricted Co-integration Rank Test (Trace) Sample: 1997Q4 – 2010Q3

Lags interval (in first difference): 1 to 2

Hypothesized no. of Co-integration relation(s)

Eigenvalue Trace Statistic 0.05 Critical Value Prob.**

None* 0.3415 29.8201 20.2618 0.0018

At most 1 0.1442 8.0958 9.1645 0.0795 Unrestricted Co-integration Rank Test (Max. Eigenvalue) Sample: 1997Q4 – 2010Q3

Lags interval (in first difference): 1 to 2

Hypothesized no. of Co-integration relation(s)

Eigenvalue Max-Eigen. Statistic

0.05 Critical Value Prob.**

None* 0.3415 21.7244 15.8921 0.0054 At most 1 0.1442 8.0958 9.1645 0.0795

* denotes rejection of the hypothesis at the 0.05 level. ** MacKinnon-Haug-Michelis (1999) p-values.

Besides the long run relationship between CPI and CIM, the estimated VECM also

contains the world food and beverage price index (WFOBEV) and delayed reactions of CPI to

shocks in the cost of imports (the long run effect of a change in the cost of imports is not

attained in one single quarter, but may take more time to be realized).

ARDL Approach to Co‐integration Testing: Application to OPT Inflation

5

CPI in OPT, as shown in equation 2, depends upon cost of imports, and World food and

beverages price index, but the latter is considered to be an exogenous variable in the VECM.

To estimate equation 2 VECM is used and the results are in table 2.

LCPI = f(LCIM, LWFOBEV) (2)

Where,

LCPI is the log of the consumer price index (CPI),

LCIM is the log of cost of imports (CIM), and

LWFOBEV is the log of World food and beverage price index (WFOBEV).

Table 2 VECM of CPI in PT3

Co-integrating equation: CointEq1

LCPI-1 1.0000

LCIM-1 -0.9438

[-6.4481]

C -0.2584

Error Correction: D(LCPI_PT) D(LCIM_TIM)

CointEq1 -0.1462 -0.0021

[-3.0008] [-0.0257]

∆LCPI-1 0.1671 -0.0850

[ 1.0205] [-0.3098]

∆LCPI-2 -0.4270 -0.4052

[-2.7200] [-1.5417]

∆LCPI-3 0.1841 0.45123

[ 1.2441] [ 1.8209]

∆LCIM-1 0.1615 0.1370

[ 1.5517] [ 0.7858]

∆LCIM-2 0.0317 0.1341

[ 0.2986] [ 0.7547]

∆LCIM-3 -0.1211 -0.1824

[-1.1341] [-1.0197]

C -0.1685 -0.0083

[-3.1513] [-0.0924]

LWFOBEV 0.0386 0.0032

[ 3.3232] [ 0.1628]

3 t-statistic between [ ].

Saed Khalil and Michel Dombrecht

6

Results show that there is a long run relationship between CPI in OPT and the cost of

imports in OPT. The long run coefficient in this relationship is significant and close to unity.

The results illustrate the crucial dependence of CPI in OPT on the exchange rates. Apart from

the cost of imports, the CPI is also affected by the movements of the world market prices of

food and beverages. This influence is relatively small, but can exert a pronounced influence on

CPI in times when these world prices are very volatile, as has been the case since 2007.

In the short term, inflation in OPT absorbs the shocks in import costs and world

prices mentioned above. Imported inflation shocks take time before the CPI level has fully

reacted and this drives inflation in the short run. The coefficient on the error correcting term

is negative, statistically significant and smaller than one and these conditions are an

additional confirmation of the existence of a long run equilibrium condition between CPI and

imported cost shocks.

III.2 ARDL

As an alternative we re-estimated this basic quarterly inflation model using the ARDL

technique along the lines suggested by PSS (2001).

The analysis starts from the assumption that the CPI in OPT can be modeled by a log-

linear VAR (p) model, augmented with deterministics such as a constant, seasonal dummies

and a time trend.

Let z = (LCPI, LCIM, and LWFOBEV)’. Then using proofs in PSS (2001) the following

conditional ECM was estimated:

∑−

=−

−−−

+∆+∆+∆+

+++=∆1

121

'

131211'

p

itttiti

tttt

uLWFOBEVLCIMz

LWFOBEVLCIMLCPIwcLCPI

ωωψ

πππ (3)

To determine the appropriate length of p, we estimated this conditional ECM by OLS

for p=1, 2, 3, 4, 5 over the period 1997Q1 to 2010Q4. We found the constant, time trend and the

first seasonal dummy to be insignificant for all lags and therefore decided to estimate the

ECM without these three deterministic variables. Table 3 reports the Akaike (AIC) and

Schwarz Bayesian (SBC) Information Criteria for all lags up to four.

ARDL Approach to Co‐integration Testing: Application to OPT Inflation

7

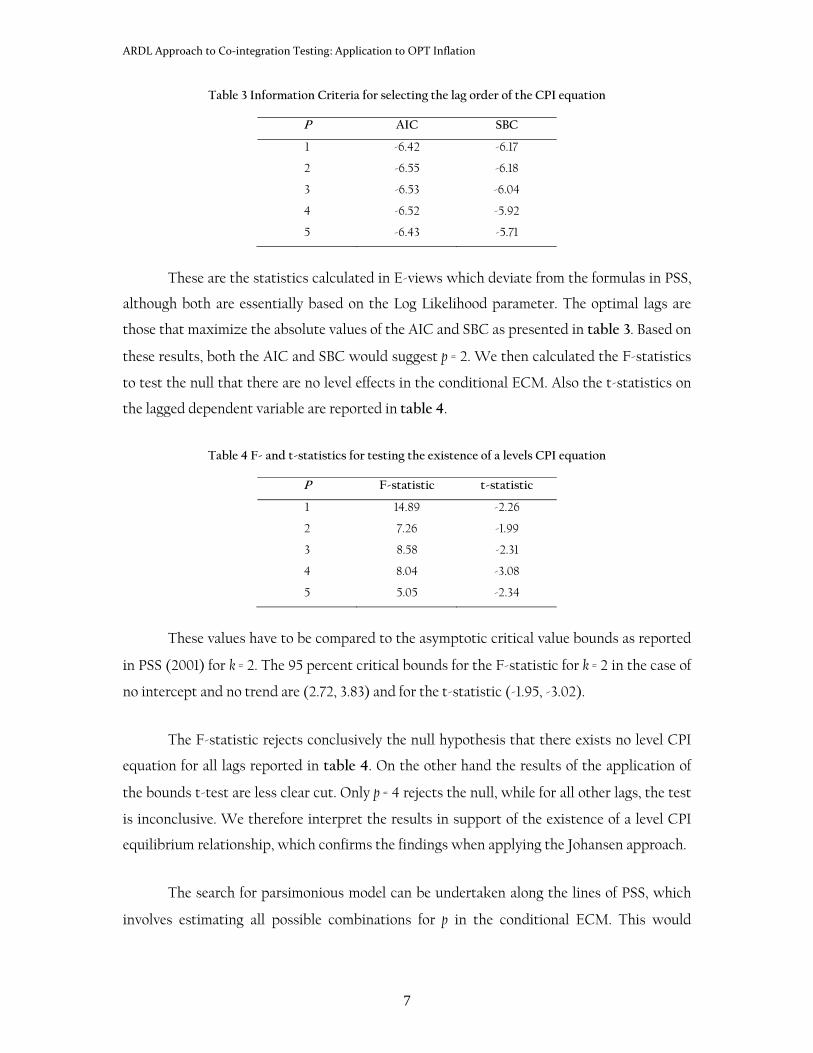

Table 3 Information Criteria for selecting the lag order of the CPI equation

P AIC SBC

1 -6.42 -6.17

2 -6.55 -6.18

3 -6.53 -6.04

4 -6.52 -5.92

5 -6.43 -5.71

These are the statistics calculated in E-views which deviate from the formulas in PSS,

although both are essentially based on the Log Likelihood parameter. The optimal lags are

those that maximize the absolute values of the AIC and SBC as presented in table 3. Based on

these results, both the AIC and SBC would suggest p = 2. We then calculated the F-statistics

to test the null that there are no level effects in the conditional ECM. Also the t-statistics on

the lagged dependent variable are reported in table 4.

Table 4 F- and t-statistics for testing the existence of a levels CPI equation

P F-statistic t-statistic

1 14.89 -2.26

2 7.26 -1.99

3 8.58 -2.31

4 8.04 -3.08

5 5.05 -2.34

These values have to be compared to the asymptotic critical value bounds as reported

in PSS (2001) for k = 2. The 95 percent critical bounds for the F-statistic for k = 2 in the case of

no intercept and no trend are (2.72, 3.83) and for the t-statistic (-1.95, -3.02).

The F-statistic rejects conclusively the null hypothesis that there exists no level CPI

equation for all lags reported in table 4. On the other hand the results of the application of

the bounds t-test are less clear cut. Only p = 4 rejects the null, while for all other lags, the test

is inconclusive. We therefore interpret the results in support of the existence of a level CPI

equilibrium relationship, which confirms the findings when applying the Johansen approach.

The search for parsimonious model can be undertaken along the lines of PSS, which

involves estimating all possible combinations for p in the conditional ECM. This would

Saed Khalil and Michel Dombrecht

8

require the estimation of (5)3 equations. A selection among those would be based on the AIC.

Our exercise would point to an underlying ARDL (1, 2, 2) model as follows:

∆LCPI = - 0.0099 SD2 - 0.0077 SD3 - 0.0549 LCPI(-1) + 0.0366 LCIM(-1)

+ 0.0202 LWFOBEV-1 + 0.3822 ∆LCIM + 0.0392 ∆LWFOBEV

+ 0.1728 ∆LCIM-1 + 0.0412 ∆LWFOBEV-1 (4)

Where,

SD2 and SD3 are seasonal dummies.

The error correction term v̂ can be written as follows:

LWFOBEVLCIMLCPIv1

2

1

2ˆππ

ππ

−−= (5)

Where, π1 = 0.0549, π2 = 0.0366, and π3 = 0.0202. The long-run relationship between LCPI and

LCIM and LWFOBEV can be written as follows:

LCPI = 0.67 LCIM + 0.37 LWFOBEV (6)

As can be seen this result implies that the sum of both cost-push factors (cost of

imports and world food and beverages index) is very close to one which conforms with

theoretical expectation. Compared to the co-integration vector that was obtained in the

VECM estimated in the 2011 inflation report, we now have a more prominent effect of the

world food and beverages price index at the expense of the more broader cost of imports

which reflects mainly CPI developments in the countries from which OPT mainly imports.

The conditional ECM is reported in table 5.

Table 5 Equilibrium correction of the ARDL (1, 2, 2) CPI equation

Regressor Coefficient Standard error p-value

1ˆ−v -0.0549 0.0090 0.0000

SD2 -0.0100 0.0029 0.0014

SD3 -0.0077 0.0028 0.0088

∆LCIM 0.3822 0.0714 0.0000

ARDL Approach to Co‐integration Testing: Application to OPT Inflation

9

∆LWFOBEV 0.0392 0.0188 0.0426

∆LCIM(-1) 0.1728 0.0737 0.0234

∆LWFOBEV(-1) 0.0412 0.0202 0.0469

2R = 0.5566 AIC = -6.6616 SBC = -6.4038

III.3 FMOLS

As an alternative, we estimated the levels CPI equation with the FMOLS (equation

7)4. The results as, shown in the equation are very close to the results obtained using ARDL.

LCPI = 0.75 LCIM + 0.24 LWFOBEV (7)

[12.934] [4.231]

The error correction term FMOLSv̂ can be written as follows:

LWFOBEVLCIMLCPIvFMOLS 24.075.0ˆ −−= (8)

As shown in table 6 using this co-integration vector in a parsimonious ECM yields

results that are again close to the final ECM of the ARDL (1, 2, 2) model.

Table 6 Equilibrium correction of the FMOLS CPI equation

Regressor Coefficient Standard error p-value

constant 0.0092 0.0019 0.0000

1ˆ −FMOLSv -0.0561 0.0265 0.0396

SD2 -0.0101 0.0031 0.0022

SD3 -0.0077 0.0030 0.0121

∆LCIM 0.3859 0.0730 0.0000

∆LWFOBEV 0.0363 0.0206 0.0838

∆LCIM(-1) 0.1696 0.0760 0.0307

∆LWFOBEV(-1) 0.0464 0.0211 0.0331 2R = 0.5357 AIC = -6.6000 SBC = -6.3054

4 T-statistics are between [ ]

Saed Khalil and Michel Dombrecht

10

IV. Conclusion

The ARDL estimation procedure is based on two basic steps. First, the existence of a

level relationship is tested using an unrestricted ARDL specification. Secondly, when the

existence of such a level relationship cannot be rejected, a more parsimonious ARDL lag

model is selected using information criteria to determine the optimal lag orders of the

independent variables in the ARDL equation. The second step involves the estimation of the

conditional ECM model from which the co-integration vector and the short term dynamics

can be obtained.

We have applied this procedure to the inflation model presented in the PMA’s 2011

inflation report. The results obtained in that report using the Johansen maximum likelihood co-

integration test and the corresponding vector error correction estimation are broadly

confirmed by the estimation of an ARDL (1, 2, 2) model.

Furthermore the results from the ARDL approach are very much in line with those

obtained using Phillips and Hansen’s Fully Modified OLS.

REFERENCES

Engle, F. and C. Granger, 1987, “Cointegration and Error Correction Representation: Estimation and Testing”, Econometrica, Vol. 55.

Hansen B., 1995, “Rethinking the univariate approach to unit root testing: using covariates to increase power”, Econometric Theory Vol. 11.

Johansen, S., 1991, “Estimation and Hypothesis Testing of Cointegrating Vectors in Gaussian Vector Autoregressive Models”, Econometrica, Vol. 59.

–––––, 1995, Likelihood-based Inference in Cointegrated Vector Autoregressive Models Oxford: Oxford University Press.

MacKinnon, J., A. Haug, and L. Michelis, "Numerical Distribution Functions of Likelihood Ratio Tests for Cointegration", Journal of Applied Econometrics, Vol. 14.

Michel, D. And S. Khalil, 2011, “Effective Exchange Rates For Palestine”, PMA.

Park, J., 1992, “Canonical Cointegrating Regressions”, Econometrica, Vol. 60.

ARDL Approach to Co‐integration Testing: Application to OPT Inflation

11

Pesaran, H. and Y. Shin, 1999, “An Autoregressive Distributed Lag Modelling Approach to Cointegration Analysis”, In S. Strom (eds.) Econometrics and Economic Theory in the 20th Century: The Ragnar Frisch Centennial Symposium Cambridge University Press.

Pesaran, H., Y. Shin, and R. Smith, 2001,“Bounds Testing Approaches to the Analysis of Level Relationships”, Journal of Applied Econometrics, special issue in honour of J. Sargan on the theme “Studies in Empirical Macroeconometrics”, (eds.) D. Hendry and M. Pesaran, Vol.16.

Phillips, P. and B. Hansen, 1990, “Statistical Inference in Instrumental Variables Regression with I(1) Processes”, Review of Economic Studies, Vol. 57.

Phillips, P. and S. Ouliaris, 1990, “Asymptotic properties of residual based tests for cointegration”, Econometrica, Vol. 58.

PMA, 2011 Inflation Report for Palestine.

Stock, J. and M. Watson, 1988, “Testing for common trends”, Journal of the American Statistical Association, Vol. 83.