sales tax brief 2015 - shekha & muftishekhamufti.com/managed/pdf/sales tax brief 2015.pdf ·...

TRANSCRIPT

Sales Tax Brief 2015

Covering SROs issued after enactment of Finance Bills 2015 Under Sales Tax Act 1990, Federal Excise Act 2005 & Sindh

Sales Tax on Services Act 2011

Shekha & Mufti is an independent member firm of Moore Stephens

International Limited, members in principal cities throughout the world.

Shekha& Mufti Chartered Accountants

2 | P a g e

Preface

This sales tax brief summarizes crucial changes made through SROs issued under Federal & Provincial Sales Tax Laws 0n 01 July 2015. This document contains our comments, which represent our interpretation of the legislation. We, therefore, recommend that while considering their application to any particular case, reference be made to the specific wordings of the relevant statute(s). The memorandum can also be accessed on our website www.shekhamufti.com July 4, 2015

Shekha& Mufti Chartered Accountants

3 | P a g e

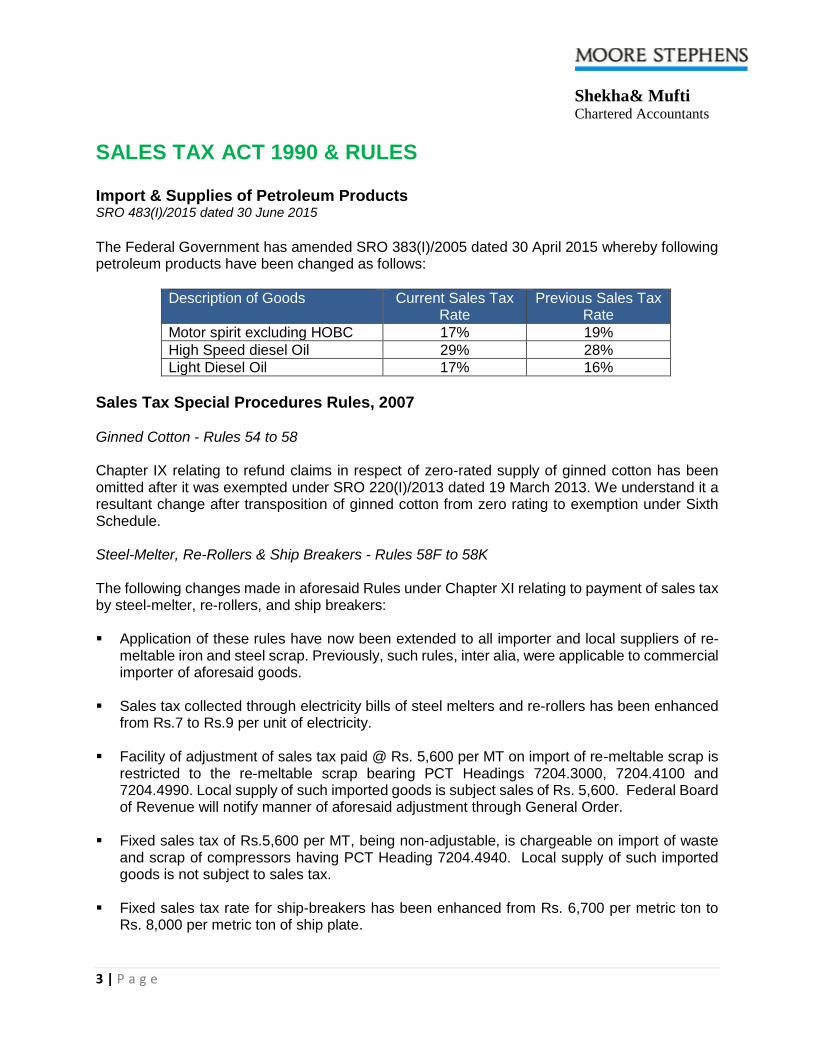

SALES TAX ACT 1990 & RULES Import & Supplies of Petroleum Products SRO 483(I)/2015 dated 30 June 2015

The Federal Government has amended SRO 383(I)/2005 dated 30 April 2015 whereby following petroleum products have been changed as follows:

Description of Goods Current Sales Tax Rate

Previous Sales Tax Rate

Motor spirit excluding HOBC 17% 19%

High Speed diesel Oil 29% 28%

Light Diesel Oil 17% 16%

Sales Tax Special Procedures Rules, 2007 Ginned Cotton - Rules 54 to 58 Chapter IX relating to refund claims in respect of zero-rated supply of ginned cotton has been omitted after it was exempted under SRO 220(I)/2013 dated 19 March 2013. We understand it a resultant change after transposition of ginned cotton from zero rating to exemption under Sixth Schedule. Steel-Melter, Re-Rollers & Ship Breakers - Rules 58F to 58K The following changes made in aforesaid Rules under Chapter XI relating to payment of sales tax by steel-melter, re-rollers, and ship breakers:

Application of these rules have now been extended to all importer and local suppliers of re-

meltable iron and steel scrap. Previously, such rules, inter alia, were applicable to commercial importer of aforesaid goods.

Sales tax collected through electricity bills of steel melters and re-rollers has been enhanced

from Rs.7 to Rs.9 per unit of electricity.

Facility of adjustment of sales tax paid @ Rs. 5,600 per MT on import of re-meltable scrap is restricted to the re-meltable scrap bearing PCT Headings 7204.3000, 7204.4100 and 7204.4990. Local supply of such imported goods is subject sales of Rs. 5,600. Federal Board of Revenue will notify manner of aforesaid adjustment through General Order.

Fixed sales tax of Rs.5,600 per MT, being non-adjustable, is chargeable on import of waste and scrap of compressors having PCT Heading 7204.4940. Local supply of such imported goods is not subject to sales tax.

Fixed sales tax rate for ship-breakers has been enhanced from Rs. 6,700 per metric ton to

Rs. 8,000 per metric ton of ship plate.

Shekha& Mufti Chartered Accountants

4 | P a g e

Fixed value of Re-rollable scrap supplied by ship breakers is enhanced from Rs. 39,412 per metric ton to Rs. 47,059 per metric ton for the purpose of charging sales tax for ship-breakers of ship plate.

Sales tax rates proportionately enhanced relating to melters and re-rollers using gas generators for generation of electricity.

After the amendments, the following sum of sales tax will be charged by the registered persons:

Rule Ref #

Invoice issued by and for or to

Previous Amount of Sales Tax

Current Amount of Sales Tax

1

By steel melters or composite units of melting, re-rolling and MS cold drawing to registered re-rollers

Rs. 6,447 per MT

Rs. 8,047 per MT

2

By Steel re-rollers, using ingots and billets of steel melter or composite units of melting re-rolling and MS cold drawing, to registered persons

Rs. 7,357 per MT

Rs. 9,217 per MT

4

By re-rollers, using ship-plates and re-rollable scrap as raw material, to registered persons

Rs. 7,610 per MT

Rs. 9,170 per MT

5 By re-rollers, to unregistered persons

Rs. 910 per MT Rs. 1,170 per MT

7 By persons supplying imported MS products, to unregistered persons.

Rs. 910 per MT Rs. 1,170 per MT

Wholesaler-cum-Retailer - Rule 58RA Beneficial amendments have been made in Chapter XII relating chains of wholesale-cum-retail outlets. Such outlets can now issue sales tax invoices tax to registered person for the purpose of claiming input tax against supplies of specified goods fall under Chapter XIII which are subject to extra tax. By virtue of Rule 58T(5), such outlets could not issue sales tax invoice since supply of specified goods, exposed to extra tax, were exempt subsequent to import and manufacturing stages. Now, such outlets and their subsequent supplies chain will charge sales tax @ 17% on subsequent sales. Further, provisions of Section 73 will not apply where such outlets receives consideration in cash against the supplies made by them. Earlier, such waiver was withdrawn through SRO 608(I)/2014 dated 02 July 2014.

Shekha& Mufti Chartered Accountants

5 | P a g e

Adjustment of Extra Tax - Rule 58T Extra tax has been made non-adjustable in the hands of the supplier. Consequently, extra tax charged by supplier will be payable to the government exchequer without being part of output tax and adjusted against gross input tax. Similar amendment was brought in Section 7 of the Act through Finance Act, 2014 in respect of ‘further tax’. The buyer of goods exposed to extra tax is already barred from claiming adjustment of extra tax under Section 8(1)(c) of the Act. Cottonseed Oil - Rule 58X An anomaly existed in Rule 58X of Chapter XIV-A relating to sales tax on supply of cottonseed oil has retrospectively been removed with effect from 5 March 2015. Such an anomaly occurred when such rule was notified through SRO 188(I)/2015 dated 5 March 2015 after superseding SRO 213(I)/2013 dated 15 March 2013. Sales Tax Special Procedure (Withholding) Rules, 2007 SRO 485(I)/2015 dated 30 June 2015 Rules 2(5) & 2(6) Withholding tax agents are now required to deposit withholding sales tax at the time of purchases instead at the time of payment of tax invoice. In other words, sales tax withholding regime has been transformed from cash basis to accrual basis. We understand this measure is against the spirit of withholding tax regime and would hurt the business community both in terms of liquidity as well as compliance purposes. This measure would effectively restrict the benefit of input tax which is claimed on accrual basis. We understand applicability of withholding tax rules on unpaid purchase bills as on 01 July 2015 needs to be clarified by FBR. Rule 5 The following changes have been made in the scope of withholding of sales tax:

Motor spirit and high speed diesel purchased from dealer has been exempted. However, other purchases from other dealers are subject withholding of sales tax @10%.

Steel Melters, Re-Rollers and Ship Breakers who pay fixed sales tax amount under Chapter XI of the Sales Tax Special Procedure Rules 2007 have been exempted. However, purchases from registered person against standard tax rate have now been made subject of withholding of sales tax. Earlier, payments to supplier of mild steel product were not subject to sales tax withholding.

Exclusions under Rules 5(v) to 5(vii) from sales tax withholding have been removed. Accordingly, purchases of following products are now subject to withholding sales tax:

Shekha& Mufti Chartered Accountants

6 | P a g e

Products made sheets of iron or non-steel alloy, stainless, steel or other allow steel, such

as pipes, almirahs, trunks etc.

Papers, in roll or sheet

Plastic products

Reduced Sales Tax Regime of Five Sectors SRO 1125(I)/2011 dated 31 December 2011 SRO 486(I)/2015dated 30 June 2015 The following amendments have been made: Maize (corn) starch is now subject sales tax @ 17%. Previously, it was subject to reduced

rates as provided under conditions to SRO 1125. Sales Tax Rate is enchased to 3% from 2% as specified under Table II. Conditions (iii) to (ixa) to SRO 1125 have now been transformed into Table II. Despite transformation of conditions into Table II, we understand overlapping exists between entries 2 and 4 of SRO 1125. Earlier, condition (viia) relating to fabric was a ‘non abstante’ condition which overrided other conditions mentioned in SRO 1125. Accordingly, tax authorities may now demand sales tax @ 5% instead of 3% considering fabric as finished article of textile. Exclusion from Section 8B SRO 491(I)/2015 dated 30 June 2015 The Government has extended facility of 100% input tax adjustment to reduced rates supplies covered under SRO 1125. Previously, input tax to the extent of 90% of output tax could have been adjusted against such supplies under Section 8B of the Act. This beneficial amendment in SRO 647 dated 27 June 2007 was backed by long outstanding demand of textile sector since transposition of sales tax regime from zero rating to reduced rate occurred in March 2013 through SRO 154(I)/2013 dated 28 February 2013. Monthly Refund of Excess Input Tax SRO 494(I)/2015 dated 30 June 2015 Rule 34 of the Sales Tax Rules, 2006 has been amendment whereby reduced rate sectors including textile can now claim refund on monthly basis. Previously, refund against local supplies was allowed through SRO 898(I)/2013 dated 4 October 2013 subject to certain conditions.

Shekha& Mufti Chartered Accountants

7 | P a g e

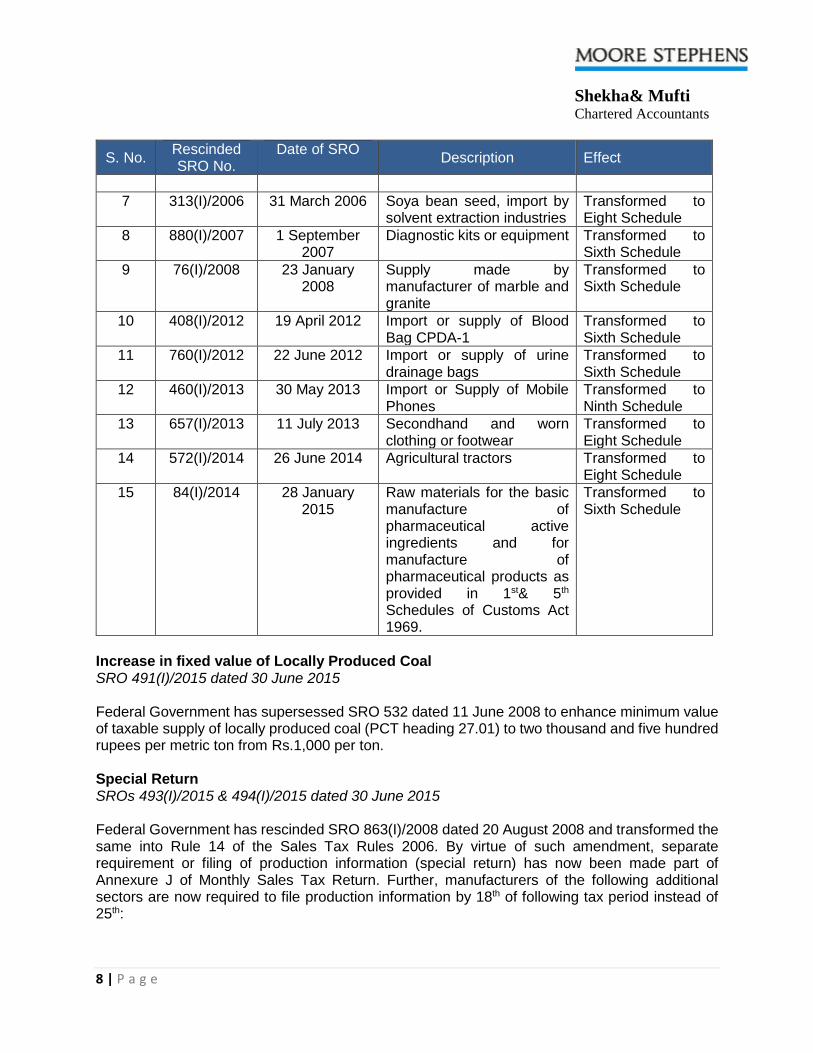

Changes in dates of ST Payment & Filing for Exploration & Production Co. SRO 487(I)/2015 dated 30 June 2015 SRO 88 dated 11 February 2002 has been supersessed with this SRO whereby petroleum exploration and production companies are now required to make payment of sales tax on 18th and file its sales tax return on 21st of the following tax period instead of 25th of the following tax period. Notifications Rescinded SRO 488(I)/2015 dated 30 June 2015 Federal Government rescinded the following notifications:

S. No. Rescinded SRO No.

Date of SRO Description Effect

1 208(I)/1998 31 March 1998 Excess amount of Sales Tax on Sugar under SRO 207/98 dated 31 March 1998

Exemption withdrawn

2 397(I)/2001 18 June 2001 Specification of Plant and Machinery for the purpose of zero-rated supply to manufacturer in the Export Processing Zone

Transformed to Fifth Schedule

3 77(I)/2004 28 January 2004

Sugar purchased and exported by Trading Corporation of Pakistan (TCP) shall be charged to tax at the rate of zero percent subject to certain conditions

Zero Rating Withdrawn.

4 433(I)/2005 14 May 2005 Facility of zero rating to one hundred completely built buses model and engine and chasis number manufactured by Hino Pak Motors Limited

Zero Rating Withdrawn.

5 1007(I)/2005 26 September 2005

Import and supply of ingredients of poultry and cattle feed.

Exemption withdrawn and now such imports and supplies are subject to reduced sales tax rate of 5% under Eight Schedule

6 69(I)/2006 28 January 2006

Rapeseed, sunflower seed and canola seed, import by solvent extraction industries

Transformed to Eight Schedule

Shekha& Mufti Chartered Accountants

8 | P a g e

S. No. Rescinded SRO No.

Date of SRO Description Effect

7 313(I)/2006 31 March 2006 Soya bean seed, import by solvent extraction industries

Transformed to Eight Schedule

8 880(I)/2007 1 September 2007

Diagnostic kits or equipment Transformed to Sixth Schedule

9 76(I)/2008 23 January 2008

Supply made by manufacturer of marble and granite

Transformed to Sixth Schedule

10 408(I)/2012 19 April 2012 Import or supply of Blood Bag CPDA-1

Transformed to Sixth Schedule

11 760(I)/2012 22 June 2012 Import or supply of urine drainage bags

Transformed to Sixth Schedule

12 460(I)/2013 30 May 2013 Import or Supply of Mobile Phones

Transformed to Ninth Schedule

13 657(I)/2013 11 July 2013 Secondhand and worn clothing or footwear

Transformed to Eight Schedule

14 572(I)/2014 26 June 2014 Agricultural tractors Transformed to Eight Schedule

15 84(I)/2014 28 January 2015

Raw materials for the basic manufacture of pharmaceutical active ingredients and for manufacture of pharmaceutical products as provided in 1st& 5th Schedules of Customs Act 1969.

Transformed to Sixth Schedule

Increase in fixed value of Locally Produced Coal SRO 491(I)/2015 dated 30 June 2015 Federal Government has supersessed SRO 532 dated 11 June 2008 to enhance minimum value of taxable supply of locally produced coal (PCT heading 27.01) to two thousand and five hundred rupees per metric ton from Rs.1,000 per ton. Special Return SROs 493(I)/2015 & 494(I)/2015 dated 30 June 2015 Federal Government has rescinded SRO 863(I)/2008 dated 20 August 2008 and transformed the same into Rule 14 of the Sales Tax Rules 2006. By virtue of such amendment, separate requirement or filing of production information (special return) has now been made part of Annexure J of Monthly Sales Tax Return. Further, manufacturers of the following additional sectors are now required to file production information by 18th of following tax period instead of 25th:

Shekha& Mufti Chartered Accountants

9 | P a g e

MS Pipes Yarns (all Kinds) Iron & Steel products including stainless steel products Storage Batteries (all Kinds) Processed Fabrics Pesticides and insecticides Liquid Glucose Fertilizers Footwear Power Transformers Filter Rod Amendments in Sales Tax Rules, 2006 SRO 494(I)/2015 dated 30 June 2015 Registration – Rule 5 Registration rules have been amended. By virtue these amendment, the following additional formalities are required to be fulfilled at time of registration: Additional information is notified for the purpose of Sales Tax Registration. Accordingly, the

applicant is now required to submit, inter alia, the following additional information (as the case may be):

Distribution certificate from the principal showing distributorship or dealership, in case of

distributor or dealer; Balance sheet / statement of affairs / equity of the business; Particulars of all branches in case of multiple branches at various locations; and Particulars of all franchise holders in case of national or international franchise.

In case of submitting manual application, the applicant is required to submit biometric

verification along with all required documents . Now all applicants including wholesalers are required to submit GPS-tagged photographs of

business premises, office equipment, electricity meter and gas meter. Previously, only manufacturers were required to furnish GPS-tagged photographs.

In case of any omission or wrong statement is discovered by the applicant, revised registration form can now be submitted during the registration process. Previously, the entire process of registration was required to be started from the beginning for changing any particular of registration before sales tax registration.

The applicant is required to furnish evidences of demarcation and installation of sub-meter where a premise is being shared.

Shekha& Mufti Chartered Accountants

10 | P a g e

Temporary Registration - New Rule 5A FBR has introduced the concept temporary registration in Finance Act 2015. The following are its salient features: Temporary sales tax registration will be allowed within 72 Hours of filing complete application

to manufacturer who has not yet imported/ installed any machinery.

Such registration will be allowed for the only period of 60 days for the purpose of import of machinery.

The applicant will also be allowed to imports machinery as well as raw material after fulfilling the following requirements: Submission of Post Dated Cheque to Customs Authorities Submission of List of machinery and their Good Declarations Filling of sales tax returns without taking any input tax adjustment Fulfilling registration requirements within 60 days of temporary registration

The applicant will not be allowed to issue sales tax invoices till his registration is confirmed by

FBR. Suspension & Blacklisting - Rule 12 FBR has now notified the procedures for suspending or blacklisting the registration in Sales Tax Rules, 2006 which are currently also prescribed in Sales Tax General Order [STGO] 3 dated 20 June 2004. Non Active Taxpayer - Rule 12A Finance Act 2015 has already brought the provisions relating to non-active taxpayer in the Act which were already part of SGTO 34 dated 16 September 2010. The detailed procedures have now been notified in Sales Tax Rules, 2006. The salient rules are as follows: Non Active Taxpayer shall not entitled to:

file Good Declarations for import and export Issue Sales Tax Invoices Claim input tax or refund Avail any concession under the Act or rules

Registered persons including government authorities are not allowed to procure any taxable supplies from Non Active Taxpayer.

Registered persons are also not allowed to claim input tax against invoice issued by Non Active Taxpayer even prior to become Non Active.

Shekha& Mufti Chartered Accountants

11 | P a g e

Restoration as Active Taxpayer will be made in the following sequential steps:

Such Non Active Taxpayer files sales tax returns alongwith payment of tax due under Sales Tax Act, 1990 or Income Tax Ordinance 2001

Concerned RTO / LTU recommends to FBR, and FBR will pass the order for restoration as Active Taxpayer

Filing sales tax return after six months - New Rule 14(2) Now onward, a registered person will only be allowed to file his sales tax return after obtaining approval of Commissioner Inland Revenue, provided that 6 months were lapsed before he filed his last tax return. New Rules FBR has also issued the following SROs: Import or Supply of exempt goods to Organization or Agencies under Grants-in-Aid

Rules 57A to 57B under Chapter VIII-A Monitoring or Tracking of Certain Registered Persons by Electronic or other Means (for

monitoring or tracking business activities of registered restaurants, cafes, coffee shops, eateries, snack bars and hotels) Rules 150ZA to 150ZE under Chapter XIV-A

Electronic Monitoring and Tracking of Specified Goods (for monitoring and tracking by affixing

or printing a tax stamp, banderole, sticker, label barcode, etc. on every package of Aerated Waters, Cigarettes, Fertilizer, Cement, Sugar) Rules 150ZF to 150ZQ under Chapter XIV-B

Shekha& Mufti Chartered Accountants

12 | P a g e

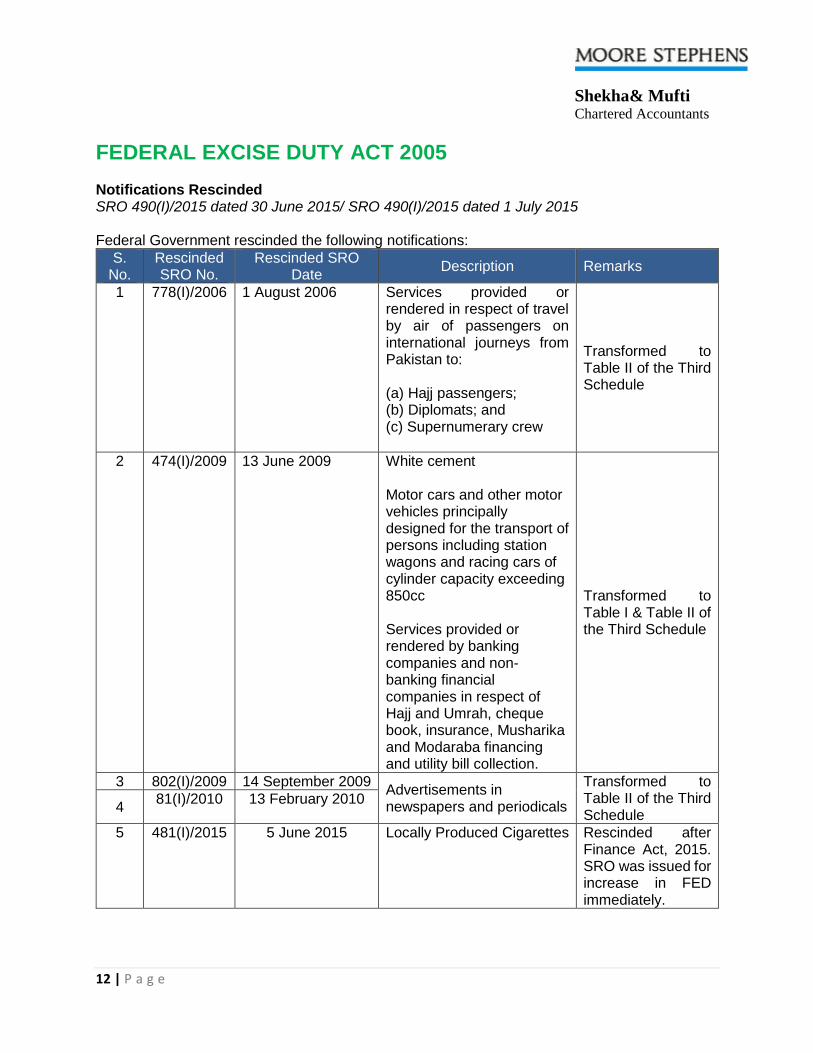

FEDERAL EXCISE DUTY ACT 2005 Notifications Rescinded SRO 490(I)/2015 dated 30 June 2015/ SRO 490(I)/2015 dated 1 July 2015 Federal Government rescinded the following notifications:

S. No.

Rescinded SRO No.

Rescinded SRO Date

Description Remarks

1 778(I)/2006 1 August 2006 Services provided or rendered in respect of travel by air of passengers on international journeys from Pakistan to: (a) Hajj passengers; (b) Diplomats; and (c) Supernumerary crew

Transformed to Table II of the Third Schedule

2 474(I)/2009 13 June 2009 White cement

Motor cars and other motor vehicles principally designed for the transport of persons including station wagons and racing cars of cylinder capacity exceeding 850cc

Services provided or rendered by banking companies and non-banking financial companies in respect of Hajj and Umrah, cheque book, insurance, Musharika and Modaraba financing and utility bill collection.

Transformed to Table I & Table II of the Third Schedule

3 802(I)/2009 14 September 2009 Advertisements in newspapers and periodicals

Transformed to Table II of the Third Schedule

4 81(I)/2010 13 February 2010

5 481(I)/2015 5 June 2015 Locally Produced Cigarettes Rescinded after Finance Act, 2015. SRO was issued for increase in FED immediately.

Shekha& Mufti Chartered Accountants

13 | P a g e

Amendment in SRO 550(I)/2006 dated 5 June 2006 SRO 489(I)/2015 dated 30 June 2015 Services of local travel by air of passengers and carriage of goods by air has been excluded from FED in Sales Tax Mode. By virtue these amendments, input tax adjustment on receipt of such services are now debarred.

Shekha& Mufti Chartered Accountants

14 | P a g e

SINDH SALES TAX ON SERVICES ACT 2011 Reduced Rate Services Notification No.SRB-3-4/8/2013 dated 1 July 2013 read with SRB-3-4/3/2015 dated 1 July 2015 The following amendments have been brought into regime of reduced sales tax: Following services, previously exposed to sales tax @ 5%, will now carry an incidence of

6%: Legal practitioners and consultants Accountants and auditors Tax consultants Construction services Corporate Law Consultants

The following services have brought to tax net at following reduced rate:

Tariff Heading Description of services Rate of tax

9805.5000 Travel Agents 10%

9806.3000 Renting of immovable property services 6%

9806.4000 Car or automobile dealers 10%

9819.9100 Auctioneers 10%

9822.4000 Dredging or desilting services 10%

No input tax adjustment against aforesaid reduced rate services is allowed to either service provider or service recipient under Sindh Sales Tax on Services Act, 2011 and Sales Tax Act, 1990.

Sales tax on services provided by programme producers and production houses has been

reduced to 6% from 10%.

Sales tax on telecommunication services has been reduced to 18% from 19.5% subject to condition of passing on full benefit of the reduced sales tax rate to service recipient.

Input tax adjustment on the following services is allowed to such registered persons who opt

to pay sales tax @ 14% instead of reduced rate:

Franchise Services Construction Services Transport Services Ready mix concrete services Intellectual property services

Shekha& Mufti Chartered Accountants

15 | P a g e

Tax Exemption Notification No.SRB-3-4/7/2013 dated 18 July 2013 read with SRB-3-4/2/2015 dated 1 July 2015 Exemption on Advertisements financed out of funds under grant-in-aid agreements has been

restricted to Government. Exemption on Renting of immovable property services which are rendered or provided to

individual person who is not liable to pay any income tax on rental income under Income Tax Ordinance, 2001.

Exemption on utility bill collection services provided or rendered by NADRA Technologies Ltd

(NTL) and banking companies or other financial institutions has been withdrawn. Now, such services are subject to sales tax @ 14%.

Exemption on Laundries and dry cleaners services has been granted to following new

categories:

turnover exceeds Rs.3.6 Million in a financial year total utility bills does not exceed Rs.40,000 in a financial year

Conditional exemption has been granted on services provided or rendered by persons

engaged in inter-city transportation or carriage of goods by road for the tax periods from July 2014 to June 2015, if such persons; Deposit charged or collected sales tax by 15 July 2015 with SRB Obtain sales tax registration by 25 July 2015

Sindh Sales Tax Special Procedure (Withholding) Rules, 2014 Notification No.SRB-3-4/7/2013 dated 18 July 2013 read with SRB-3-4/4/2015 dated 1 July 2015 The following amendments have been made: FBR Registered or SRB Registered person who receive the following services have become

withholding agents and are required to withhold 100% sales tax @ applicable rate: Renting of immovable property services Services of Auctioneers Service of inter-city transportation or carriage of goods by road Advertising agent who issue release orders or book advertisement space

Tax fraction formula has been introduced through Sindh Finance Act, 2015 in Section 2(93A)

of the Sindh Sales Tax on Services Act, 2011 for working out value of taxable services to compute amount of sales tax withholding. Previously, gross value of taxable services was used for working out value for withholding sales.

Shekha& Mufti Chartered Accountants

16 | P a g e

Withholding agents specified under Rules 1(2)(a) to 1(2)(d) are now electronically required to file withholding statements. Previously, such withholding returns were manually submitted.

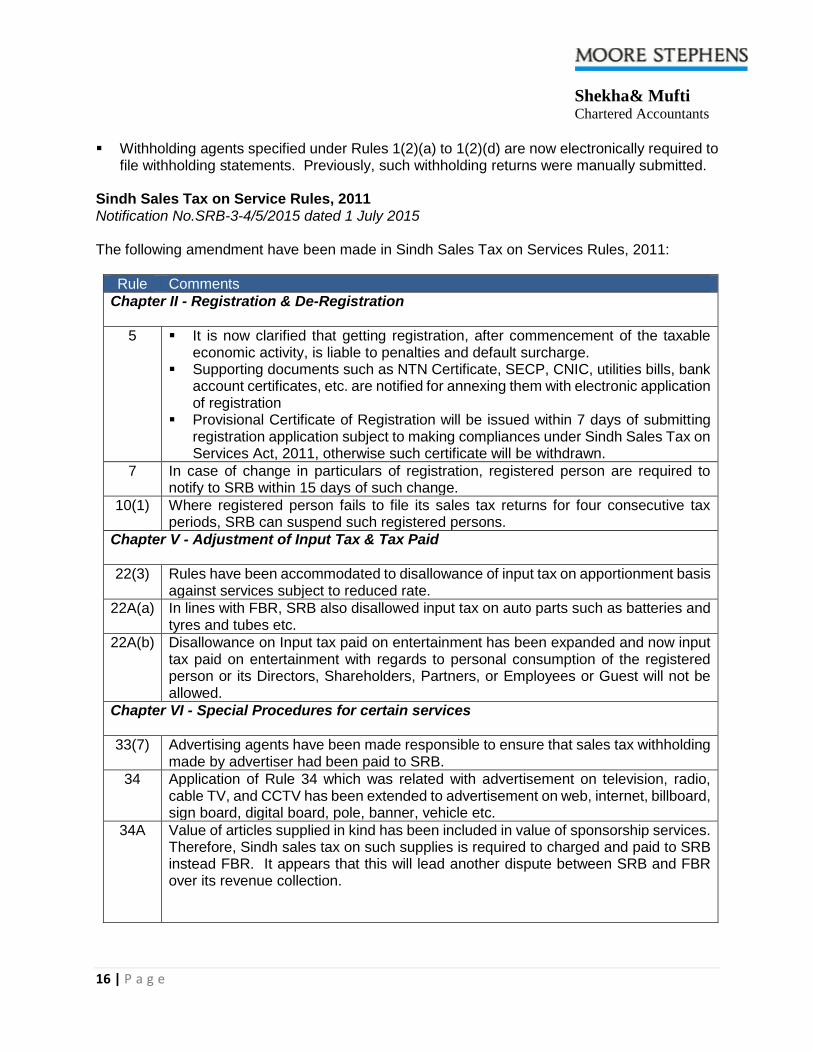

Sindh Sales Tax on Service Rules, 2011 Notification No.SRB-3-4/5/2015 dated 1 July 2015 The following amendment have been made in Sindh Sales Tax on Services Rules, 2011:

Rule Comments

Chapter II - Registration & De-Registration

5 It is now clarified that getting registration, after commencement of the taxable economic activity, is liable to penalties and default surcharge.

Supporting documents such as NTN Certificate, SECP, CNIC, utilities bills, bank account certificates, etc. are notified for annexing them with electronic application of registration

Provisional Certificate of Registration will be issued within 7 days of submitting registration application subject to making compliances under Sindh Sales Tax on Services Act, 2011, otherwise such certificate will be withdrawn.

7 In case of change in particulars of registration, registered person are required to notify to SRB within 15 days of such change.

10(1) Where registered person fails to file its sales tax returns for four consecutive tax periods, SRB can suspend such registered persons.

Chapter V - Adjustment of Input Tax & Tax Paid

22(3) Rules have been accommodated to disallowance of input tax on apportionment basis against services subject to reduced rate.

22A(a) In lines with FBR, SRB also disallowed input tax on auto parts such as batteries and tyres and tubes etc.

22A(b) Disallowance on Input tax paid on entertainment has been expanded and now input tax paid on entertainment with regards to personal consumption of the registered person or its Directors, Shareholders, Partners, or Employees or Guest will not be allowed.

Chapter VI - Special Procedures for certain services

33(7) Advertising agents have been made responsible to ensure that sales tax withholding made by advertiser had been paid to SRB.

34 Application of Rule 34 which was related with advertisement on television, radio, cable TV, and CCTV has been extended to advertisement on web, internet, billboard, sign board, digital board, pole, banner, vehicle etc.

34A Value of articles supplied in kind has been included in value of sponsorship services. Therefore, Sindh sales tax on such supplies is required to charged and paid to SRB instead FBR. It appears that this will lead another dispute between SRB and FBR over its revenue collection.

Shekha& Mufti Chartered Accountants

17 | P a g e

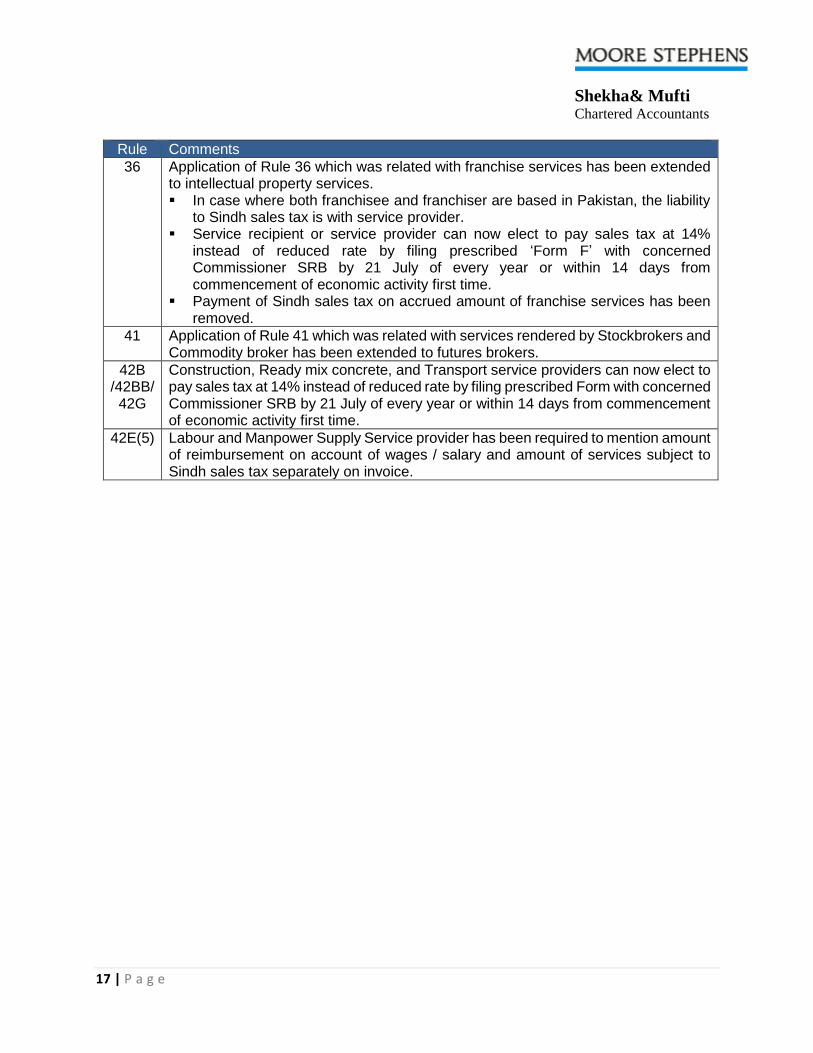

Rule Comments

36 Application of Rule 36 which was related with franchise services has been extended to intellectual property services. In case where both franchisee and franchiser are based in Pakistan, the liability

to Sindh sales tax is with service provider. Service recipient or service provider can now elect to pay sales tax at 14%

instead of reduced rate by filing prescribed ‘Form F’ with concerned Commissioner SRB by 21 July of every year or within 14 days from commencement of economic activity first time.

Payment of Sindh sales tax on accrued amount of franchise services has been removed.

41 Application of Rule 41 which was related with services rendered by Stockbrokers and Commodity broker has been extended to futures brokers.

42B /42BB/ 42G

Construction, Ready mix concrete, and Transport service providers can now elect to pay sales tax at 14% instead of reduced rate by filing prescribed Form with concerned Commissioner SRB by 21 July of every year or within 14 days from commencement of economic activity first time.

42E(5) Labour and Manpower Supply Service provider has been required to mention amount of reimbursement on account of wages / salary and amount of services subject to Sindh sales tax separately on invoice.