sample - global water intelligence...sample a global water intelligence publication global water...

TRANSCRIPT

Water for PowerOpportunities in water and wastewater treatment for tomorrow’s energy needs

www.globalwaterintel.comA Global Water Intelligence publicationSam

ple

GlobalWater Intelligence

6 Regional

snapshots4 C

ountry chapter: C

hina

Table of contents

References

2 Global

trends

2Global trendsSa

mpl

e

13

Future Fuel use and power plant construction

© Global Water Intelligence, 2013. Contact [email protected] for permissions.

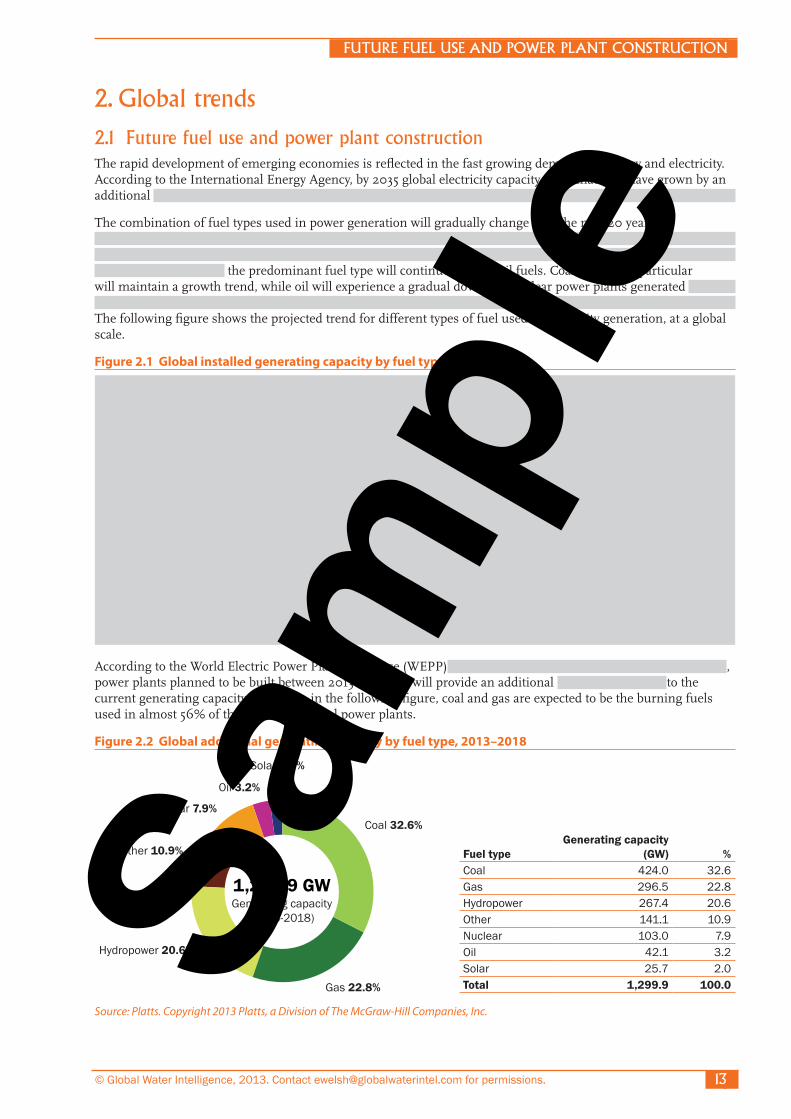

2. Global trends

2.1 Future fuel use and power plant constructionThe rapid development of emerging economies is reflected in the fast growing demand for energy and electricity. According to the International Energy Agency, by 2035 global electricity capacity is estimated to have grown by an additional

The combination of fuel types used in power generation will gradually change over the next 20 years. the predominant fuel type will continue to be fossil fuels. Coal and gas in particular will maintain a growth trend, while oil will experience a gradual downfall. Nuclear power plants generated The following figure shows the projected trend for different types of fuel used in electricity generation, at a global scale.

Figure 2.1 Global installed generating capacity by fuel type, 2005–2035

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2035203020252020201520102005

Coal

Oil

Gas

Nuclear

Renewable

GW

Source: IEA, 2012

According to the World Electric Power Plants Database (WEPP) , power plants planned to be built between 2013 and 2018 will provide an additional to the current generating capacity. As shown in the following figure, coal and gas are expected to be the burning fuels used in almost 56% of the future additional power plants.

Figure 2.2 Global additional generating capacity by fuel type, 2013–2018

Fuel typeGenerating capacity

(GW) %Coal 424.0 32.6Gas 296.5 22.8Hydropower 267.4 20.6Other 141.1 10.9Nuclear 103.0 7.9Oil 42.1 3.2Solar 25.7 2.0Total 1,299.9 100.0

Coal 32.6%

1,299.9 GWGenerating capacity

(2013-2018)

Gas 22.8%

Hydropower 20.6%

Nuclear 7.9%

Oil 3.2%

Other 10.9%

Solar 2.0%

Source: Platts. Copyright 2013 Platts, a Division of The McGraw-Hill Companies, Inc.

Sam

ple

35

© Global Water Intelligence, 2013. Contact [email protected] for permissions.

MARKET FORECAST

The fastest growth is expected in , estimated to be %. This segment will be focused in the U.S. and China. The equipment that we have considered as part of these systems is described below:

• Pretreatment – All equipment for removing suspended solids from the boiler and cooling system makeup streams. This includes screening and pumping equipment at the intake, clarification and settling tanks, chemical feed systems, internal pipework, valves and fittings, and all associated monitoring and control systems. This does not include ion exchange and membrane systems for treatment of boiler feedwater.

• Boiler feedwater – All equipment for treating boiler makeup water to the required purity. This includes ion exchange systems, high pressure membrane systems, membrane and multimedia pretreatment systems, chemical dosing systems, associated internal pipework, valves and fittings, monitoring and control systems. This also includes equipment required to maintain water purity within the boiler, including chemical feed systems, deaerators, monitoring and control systems. This does not include steam pipes and associated fittings in the boiler system

• Condensate polishing – All equipment for treating water from the condenser before it re-enters the boiler, including full-flow and sidestream polishing. This includes ion exchange and high pressure membrane systems used as a polisher. This does not include steam pipes and associated fittings in the boiler system.

• Conventional wastewater treatment – All equipment for treating cooling cycle blowdown and FGD wastewater using physical and chemical methods. This includes clarification and settling tanks, chemical feed systems, pipework, valves and fittings, monitoring and control systems. This does not include evaporation ponds or wastewater treatment that takes place off-site. This category also includes wastewater treatment systems for treating coal pile runoff, leachate from ash landifllls, and the treatment of coolant in the primary cycle of nuclear power plants.

• High recovery wastewater treatment – All equipment for treating wastewater before internal reuse and to meet more stringent discharge regulations. This includes advanced physical and chemical processes for precipitating metals, biological treatment methods for removal of selenium, membrane technologies, and thermal treatment systems.

The following figure summarises our forecast of capital expenditure on each of these systems in the global power industry.

Figure 2.31 Worldwide capital expenditure on water and wastewater treatment by system, 2011–2018

$ m

illio

n

High recovery wastewater treatment

Conventional wastewater treatment

Condensate polishing systems

Boiler feedwater systems

Pretreatment systems0

500

1,000

1,500

2,000

2,500

3,000

20182017201620152014201320122011

System ($m) 2011 2012 2013 2014 2015 2016 2017 2018Pretreatment systems Boiler feedwater systems Condensate polishing systems Conventional wastewater treatment High recovery wastewater treatment Total

Source: GWI Sam

ple

39

© Global Water Intelligence, 2013. Contact [email protected] for permissions.

MARKET PLAYERS

2.6.3 EPC contractorsEPC contractors that deliver turnkey solutions are very important market players because the construction of new power plants is most often procured on an EPC basis. Besides EPC contractors, the biggest EPC contractors in the international market are . Other relevant players that don’t make the top 20 list but are highlighted by industry experts are

EPC contractors dominate the Middle East and Asia Pacific markets, which are largely driven by cost.

Figure 2.35 Top 20 EPC contractors in the power industry by capacity, worldwide Rank Company Country Capacity (MW)

Source: Platts. Copyright 2013 Platts, a Division of The McGraw-Hill Companies, Inc.

2.6.4 Water technology companiesThe key players among water technology companies in the power industry are

These companies provide whole engineered solutions and water treatment systems. Considering the wide range of their services in the power sector – equipment, chemicals, mobile water and outsourcing capabilities – is the market leader in the power industry with estimated of the market share. The second biggest player is whose share in the power sector’s water and wastewater segment is around .

Besides these few large global players, the rest of the market consists of Sa

mpl

e

GlobalWater Intelligence

35 C

ountry chapter: India

Executive sum

mary

7

Country

chapter: U.S.

Services

1 Introduction

3Country chapter:United StatesSa

mpl

e

45

Regulations

© Global Water Intelligence, 2013. Contact [email protected] for permissions.

Figure 3.3 Techniques used to mitigate the emission of sulphur dioxide from coal-fired plants, 2013

System type Generating capacity (MW) %Wet Other Dry Unknown Total

Wet 55.1%

332,142 MWGenerating capacity

(2013)

Dry 9.0%

Other 34.8%

Unknown 1.1%

Note: “Other” category includes alternative boiler and low sulphur fuel to achieve compliance. Source: Platts. Copyright 2013 Platts, a Division of The McGraw-Hill Companies, Inc.

3.3 Regulations There are three main regulations that affect the type of water and wastewater technologies adopted at power plants:

• Steam electric power generating effluent guidelines (Steam Electric ELGs) – 40CFR Part 423

• Cooling water intake structures – CWA 316b

• Impaired waters and Total Maximum Daily Load (TMDL) regulations – CWA 303d

3.3.1 steam electric power generating effluent guidelines (steam electric elgs) – 40CFR Part 423The steam electric power industry currently contributes more than half of the toxic pollutants discharged to water bodies. The EPA has decided to act on this and on 7 June, 2013 proposed a revision to the Steam Electric ELGs that were last updated in 1982.

The proposed regulations will strengthen limits for metals such as mercury, arsenic, lead and selenium as well as for nutrients. The regulations will mainly affect the following wastewater streams generated at coal-fired power plants:

• Flue gas desulphurisation (FGD) wastewater

• Fly ash and bottom ash wastewater

• Leachate from ash/FGD ponds and landfills

• Flue gas mercury control waste

• Gasification of fuels such as coal and petroleum coke – Gasification process discharges

• Non-chemical metal cleaning wastes

Gas, nuclear and other thermoelectric power plants are also covered by the regulation, but due to the nature of the wastewater generated at these plants, the impact of the regulations on them will be much smaller. The key issue for these plants will be compliance with non-chemical metal cleaning waste limits. These are small volume streams, but still important as they are currently being discharged without appropriate treatment. Sa

mpl

e

GlobalWater Intelligence

6 Regional

snapshots4 C

ountry chapter: C

hina

Table of contents

References

2 Global

trends

4Country chapter:China

Sam

ple

63

Technology Trends

© Global Water Intelligence, 2013. Contact [email protected] for permissions.

4.3 Technology trendsWater treatment for boiler feedwater in power plants in China follows technological treatment trains and trends found elsewhere in the world (see Chapter 2, Section 2.4).

The general trend in China is to reuse wastewater from municipal wastewater treatment plants and to treat it for use as boiler feedwater. This implies the increased use of . According to industry experts,

Although water reuse within power plants used to be very limited, increasingly much higher water reuse rates have been imposed in recent years. This is driving the use of for wastewater treatment as an emerging trend in China.

The reuse of cooling tower blowdown is the most common initiative to reuse water within power plants. Often, cooling tower blowdown is mixed with wastewater which can be reused in cooling tower systems after . However, it is anticipated that more and more plants will

FGD systems are mandatory in all existing and future power plants in China. The majority of the currently installed FGD systems use . Currently, FGD wastewater is treated with

At the moment, the use of ZLD technologies i

4.4 Procurement processThe most common form of procurement for new power plants including water and wastewater treatment systems is engineering, procurement and construction (EPC). Tendering practices can vary from awarding the entire project to an EPC contractor who then subcontracts the water and wastewater treatment systems to power plant operators directly procuring the water and wastewater treatment systems. The top power generation companies

Water and wastewater systems are generally tendered separately from other power plant components. The water and wastewater treatment package can

. They have the most influential role in determining design specifications which typically contain a detailed Even in the cases when plant operators have enough experience in dealing with the tender specifications, they are advised by . are involved in the entire process from the pre-tender phase to the procurement process. End users need to work with them to obtain the licenses which are required for the construction of a new power plant.

Although in theory, tenders are open, EPC contractors and equipment suppliers To be successful in the backroom negotiations, it is essential to

Sam

ple

GlobalWater Intelligence

6 Regional

snapshots4 C

ountry chapter: C

hina

Table of contents

References

2 Global

trends

6Regional snapshotsSa

mpl

e

121

© Global Water Intelligence, 2013. Contact [email protected] for permissions.

REST OF ASIA

The capacity of new coal-fired power plants is projected to peak in will be added to the Rest of Asia region. According to Platts’ database, the highest growth in gas power is expected in the year Nuclear power plants, The following figure presents the trend in the development of new thermal power plants in the Rest of Asia region from 2005 to 2018.

Figure 6.58 Annual additional generating capacity of thermal power plants by fuel type, 2005–2018

0

5,000

10,000

15,000

20,000

25,000

2017201520132011200920072005

Coal

Gas

Nuclear

Oil

MW

Source: Platts. Copyright: 2013 Platts, a Division of The McGraw-Hill Companies, Inc.

6.4.1.1 Coal-fired power plants

During 2013–2018, the construction of new coal-fired generating units will produce an additional generating capacity of In the Rest of Asia region, offers the greatest opportunity in the water for power market, as 36% of the future additional generating capacity of coal-fired power plants will be located there. Other countries, like will be particularly active in the construction of new coal-fired power plants. The following figure presents the additional generating capacities of coal-fired power plants by country between 2013 and 2018.

Figure 6.59 Additional coal-fired generating capacity in the Rest of Asia region by country, 2013–2018

CountryAdditional

generating unitsAdditional generating

capacity (MW)% of total additional generating capacity

Vietnam Republic of Korea Indonesia Taiwan Philippines Thailand Malaysia Other Total

Source: Platts. Copyright: 2013 Platts, a Division of The McGraw-Hill Companies, Inc.Sam

ple

GlobalWater Intelligence

35 C

ountry chapter: India

Executive sum

mary

7

Country

chapter: U.S.

Services

1 Introduction

Services

7Sample

155

© Global Water Intelligence, 2013. Contact [email protected] for permissions.

CHEMICALS

We anticipate that will be the biggest market for chemical suppliers in the power industry, with an estimated value of in 2013. We estimate that in 2013, the market for chemical addition in treatment processes is worth , and the market for internal boiler treatment is worth . Our forecast for expenditure on chemicals for these systems is presented in the following figure.

Figure 7.12 Global expenditure on chemical treatment by system, 2011–2018

$ m

illio

n

0

500

1,000

1,500

2,000

2,500

3,000

3,500

20182017201620152014201320122011

Process water andwastewater treatment

Wet cooling systems

Boiler and steamsystems

System ($m) 2011 2012 2013 2014 2015 2016 2017 2018Boiler and steam systems Wet cooling systems Process water and wastewater treatment

Total

Source: GWI

We estimate that will represent the largest share of this market, The following figure summarises our forecast of expenditure for water treatment chemicals in the global power industry.

Figure 7.13 Global expenditure on chemical treatment by product category, 2011–2018

$ m

illio

n

0

500

1,000

1,500

2,000

2,500

3,000

3,500

20182017201620152014201320122011

Commodity acid /alkali

Corrosion inhibitors

Scale inhibitors

Biocides

Coagulants /flocculants

Product line ($m) 2011 2012 2013 2014 2015 2016 2017 2018Coagulants / flocculants Biocides Commodity acid / alkali Corrosion inhibitors Scale inhibitors Total

Source: GWI

Sam

ple