sample portfolio investment

DESCRIPTION

Here you can find a full portfolio investment sample.TRANSCRIPT

Assignment on

Portfolio Investment Of 20 lac BDT

Prepared For

Dr. Md. Jahangir Alam

Professor

Course Instructor

Portfolio Management

Prepared by

Mohammad Riyadul Islam (50)

Tazrian Shainam Shahid (68)

Muhammad Mazhar Hossain (96)

Wahath Shahid (111)

Institute Of Business Administration

University of Dhaka

19 November 2012

Contents Introduction .................................................................................................................................................. 3

1.1 Outline of the paper ...................................................................................................................... 4

This term paper will consist of the following ............................................................................................ 4

1. Basic concepts and methods Portfolio design .................................................................................. 4

2. Developing an investment policy statement on the basis of the concepts above ........................... 4

3. Examining current and projected financial and economic conditions ............................................. 4

4. Implementing investment policy statement by constructing the portfolio ..................................... 4

5. Establish a process for a continuous monitoring of the investors needs ......................................... 4

Basic concepts and methods Portfolio design .......................................................................................... 4

2. Basic Portfolio Design steps .................................................................................................................. 5

2.2 Determining the goals of Investment ................................................................................................ 5

2.3 Asset Allocation ................................................................................................................................... 5

2.4 Creating your Investment Policy Statement ....................................................................................... 6

2.4.1 Investment objectives .................................................................................................................. 6

2.4.4 Monitoring procedures .................................................................................................................... 6

3. The Investment Policy Statement ......................................................................................................... 7

3.1 Investor Circumstances ....................................................................................................................... 7

Objectives of the portfolio ............................................................................................................................ 7

Time Horizon ......................................................................................................................................... 7

Risk Tolerances ...................................................................................................................................... 8

Roles and Responsibilities ............................................................................................................................. 8

Constraints of investors ................................................................................................................................ 8

Liquidity Needs.......................................................................................................................................... 8

Time Horizon ............................................................................................................................................. 9

Taxes ......................................................................................................................................................... 9

Unique Circumstances .............................................................................................................................. 9

Risk Tolerance ............................................................................................................................................... 9

Investment Opportunities ............................................................................................................................. 9

4. Current Financial and Economic conditions ................................................................................... 10

4.1 Overview of the Market .................................................................................................................... 11

Risk associated with investment: ................................................................................................................ 11

4.2 Measures Taken ................................................................................................................................ 13

4.3 Examination of Market Anomalies.................................................................................................... 14

4.4 Future Directions of the Market ....................................................................................................... 14

We are investing BDT 1,000000 on Real Estate. Following are the justification behind the investment.

................................................................................................................................................................ 16

Calculation of Asset Appreciation from Real Estate Investment ............................................................ 16

Growth Rate Calculation ..................................................................................................................... 16

Conclusion: .................................................................................................................................................. 19

Reference .................................................................................................................................................... 20

Appendix ..................................................................................................................................................... 20

Introduction

This term paper will follow a systematic step by step process in order to design an investment portfolio

that is based upon a certain financial circumstance. The resulting portfolio design will help to ensure

that individual investment decisions are complimentary and supportive of the initial financial goals.

The actual design of the investment portfolio is one of the most important aspects of investing. The

individual investment decisions should be coordinated and organized according to a well-defined

portfolio design. Just like investment professionals, personal investors need to develop a customized

portfolio design to guide and coordinate their individual investment decisions. The key items they need

to focus on in this process include

their financial goals

their ability to save

their required average annual rate of return, and

assuming the least amount of investment risk as possible

With these items in focus we are asked to take the shoes of an investor with Tk. 20,00,000 that has to be

invested in a suitable portfolio to achieve certain goals. Tk. 20,00,000 may seem like a significant sum of

money but in investment terms its actually a small amount. As for most small investors, their investment

portfolio will be a collage of individual and separate investment decisions. One investment decision is

often made in isolation of previous decisions. More often than not the investment decisions are made at

the time of their savings contribution and are based upon what seems to be working at that moment.

This adhoc approach to investing can be counter-productive with previous investment decisions and can

actually work against achieving the financial goals. Hence this term paper is going to look at a systematic

approach to investing this sum.

Creating a proper portfolio design will help the invesotors achieve the following investment goals:

Defending your savings from unknowable future events

Incorporating your investing personality

Complementing your financial circumstances

Identifying your financial goals

The following section in this chapter discusses the outline of the report and the next chapter will review

the basics of portfolio design in order to create a sound portfolio for the above mentioned investor.

1.1 Outline of the paper

This term paper will consist of the following

1. Basic concepts and methods Portfolio design

2. Developing an investment policy statement on the basis of the concepts above

3. Examining current and projected financial and economic conditions

4. Implementing investment policy statement by constructing the portfolio

5. Establish a process for a continuous monitoring of the investors needs

Basic concepts and methods Portfolio design

This section is going to highlight relevant literature and pertinent studies behind the effective design of

portfolio which help rationalize the decisions in the next steps.

Developing Investment policy statement

Policy statement is the roadmap for the investor’s guide the investment process. Policy statement

includes the objectives and policies of the investors and the constraint faced by the investors. It also sets

the standards for evaluating the investment performance. Investors can evaluate the performance of

the investment by comparing with the policy statement to find out whether the investment is

appropriate for the investor.

Examining financial and economic condition

Before investing investors require to study short term and intermediate term expected financial and

economic condition and forecast their future needs. There are 3 factors, investor needs, expectation

from the financial market, and economic conditions, jointly determine the investment strategy for the

investor.

Implementing the Investment policy statement by constructing the portfolio

With the policy statement and financial forecast the investor determine how to implement the

investment plan to allocate available funds across different asset classes and securities. This involves

constructing a portfolio to minimize the investor’s risk.

Monitoring the performance of investment

Investors’ needs might change overtime so it requires continual monitoring of the investors’ needs and

conditions of the financial market. So it is very much important for the investors to monitor the portfolio

performance and compare it with the expectation and the requirement of the investors. It does not

meet the investors’ needs and requirement; investors require updating the investment portfolio. That

means investors require to drop some securities and to add some other securities in the portfolio. So

the policy statement should be modified accordingly when necessary.

2. Basic Portfolio Design steps

Any good investment design should give a clear answer on the following questions

Are the investments working together or against each other?

Is the investor over exposed or under exposed to certain investment categories?

Is the portfolio too risky or too conservative?

Is the portfolio making or losing money?

There's more to successful portfolio building than picking good investments. Putting together a portfolio

of securities is like building a wardrobe. Even if the closet is filled with top-of-the-line attire that may not

be enough: All those components need to work together as outfits. Investment portfolios are the same

way.

2.2 Determining the goals of Investment

It is important to know and realize what an investor wants out of his investment efforts. We regularly

invest -- squirreling away as much as we can -- without knowing whether we're saving enough for our

goals. That's because most of us have no idea what our goals will cost. The goals may range from

paying off student loans

saving to purchase a house

saving for your children’s education

saving to purchase a new car

saving for that special vacation

saving for an additional home

saving to start your own business

saving for retirement

saving to leave an estate for your children and grandchildren

2.3 Asset Allocation

Before the investor begins choosing individual mutual funds and stocks, he/she needs to think in broader

strokes. They need to consider your asset allocation. A portfolio’s asset allocation is the portfolio's blend

of stocks, bonds and cash. Finding the best asset mix is crucial to meeting investment goals. In fact, most

financial advisers agree that setting up the right asset mix is more important than choosing great

investments.

Before asset allocation the investor needs to answer the following questions regarding their goals of

investing

1. The number of years until your goal is reached. The deadline when you need the investment

amount as well as the returns. That's the number of years to your goal.

2. How much money you need for your goal.

3. How much money you can invest right now.

4. How much money you can contribute each month.

2.4 Creating your Investment Policy Statement

Creating an Investment Policy Statement enables the investor to put his/her investment strategy in

writing and commit to a disciplined investment plan.

Big organizations create Investment Policy Statements for their company retirement plans. Financial

advisers craft them for their clients. They require some philosophizing and number crunching. However,

an IPS isn't only for the well-heeled who love paperwork. It's a must for all investors. That's because

creating an Investment Policy Statement forces you to put your investment strategy in writing and

commit to a disciplined investment plan. It's both a blueprint and a report card.

2.4.1 Investment objectives The Investment Objectives portion of your Investment Policy Statement details what the investor is

trying to achieve and in what time frame.

It answers the following questions:

What is the investors’ financial goal?

How long will the investor be funding this goal?

How much will this goal cost every year

2.4.4 Monitoring procedures

The Monitoring Procedures portion of the Investment Policy Statement details the plan for keeping tabs

on investments. It's the blueprint for rebalancing, and for determining what investments, if any, should

be sell.

Answer the following questions:

How often will the investor monitor the portfolio?

How will the investor determine how well the individual investments are doing?

How will the investor determine how well his overall portfolio is doing?

How will the investor determine whether his portfolio is meeting his expected return?

How will the investor determine whether losses fall within his accepted range?

To determine how well individual investments and overall portfolio are doing, investors must use the

benchmarks chosen in the Investment Policy Statement. If it is found that the portfolio is not meeting

the expected return, or that losses are falling outside of an acceptable range, the investor may need to

adjust the investments.

When monitoring, the focus must not only be on performance. It also has to be seen that the reasons

these investments were chosen in the first place still apply. To do that, the status of each investment

must be checked against the Investment Selection Criteria. If a stock or fund no longer meets the

criteria, it may be a sell candidate.

3. The Investment Policy Statement

3.1 Investor Circumstances

The Trust beneficiaries are a group of 4 people ages 26-29 who are all in fair health and with stable

employment. They have accumulated BDT 20,00,000 and wish to invest the amount. They have no

immediate need liquidity and wish for this amount to grow to a more significant amount after 5 years so

that they can start their own business

The primary objective of this portfolio is to appreciate in value in real terms, while also generating a

stable continuous source of income as a secondary goal.

Objectives of the portfolio

The portfolio will have a long term investment horizon. The primary objectives are:

Generation of current income. This can be done through reinvestment of sufficient total return

and additional funds.

Capital preservation of current and future contributions

Maximize return within reasonable risk levels.

Providing opportunities to diversify across risk-return spectrum.

Time Horizon The investment guidelines are based upon an investment horizon of greater than five years. The

strategic asset allocation is also based on this long-term perspective. Short-term liquidity requirements

are anticipated to be small and to be covered by cash inflows.

Risk Tolerances It is recognized that some risk must be assumed in order to achieve the investment objectives of

In establishing the risk tolerances of the IPS, the ability to withstand short and intermediate term

variability were considered.

We have ranked, among the broad possible priorities, the following investment objectives:

Safety/ 4

Capital Preservation (Adjusted for Inflation) 5

Growth: 5

Liquidity: 3

Current Income: 3

The long-term objective for the assets under this policy is to achieve after fees and expenses, a pre-tax average annual return of 15% over the expected holding period of this portfolio.

Roles and Responsibilities

The investment will be done through the broker house Commercial Bank Securities and Investment

Limited (CSBIL). A broker will be engaged in fulfilling the objectives set here within. The total investment

amount of BDT 2,000,000 will be placed in one account. Thus the trading will be done through this single

account. All four members of this group will monitor the market and the final decisions regarding the

portfolio will be made through a joint consensus.

Constraints of investors

Liquidity Needs

Sufficient liquidity must be maintained through the choice of investment vehicles and asset allocation,

so as in cases of cash inflow deficit expenses can be met. Liquidity needs in the short term period inare

minimal.

Time Horizon

This portfolio is suitable for investors with a minimum time horizon of five years. Capital values fluctuate

over short period of time and the risk of incurring loss is high in short term period. Research suggests

that this loss can be minimized over a long period of time. The portfolio’s asset allocation is based on

this long-term perspective, since short-term liquidity needs are of less importance.

Taxes

Since the investment being made as a single investor, the returns from this portfolio will be subjected to

income tax rates in-line with the policies set by the National Board of Revenue.

Unique Circumstances

Due to insufficient funds investing in some asset classes will not be conceivable.

Risk Tolerance

Some risks must be assumed in order to achieve the investment objectives. The portfolio's long time

horizon, current financial condition and several other factors suggest collectively some interim

fluctuations in market value and rates of return may be tolerated in order to achieve the longer-term

objectives.

Investment Opportunities

For any investor these are many outlets through which they can invest their money. The following are

the list of opportunities that are available in Bangladesh. Also we have identified the opportunities are

most suitable to us based on our objectives:

4. Current Financial and Economic conditions

Multiple downside risks and growing uncertainties continued to characterized the global economy as it

entered into 2012. Double-dip depression was not unlikely, particularly in the backdrop of a slowing

pace of economic growth in the last quarter of 2011, and weak growth projections for 2012 and 2013.

Persistently high unemployment rate, low consumer and business confidence, and volatility in financial

sectors are likely to have wide ranging multiple downside risks and growing uncertainties continued to

characterize the global economy as it entered into 2012.

Double-dip depression was not unlikely, particularly in the backdrop of a slowing pace of economic

growth in the last quarter of 2011, and weak growth projections for 2012 and 2013. Persistently high

unemployment rate, low consumer and business confidence, and volatility in financial sectors are likely

to have wide ranging. The Bangladeshi economy has shown great resilience in the face of the recent

global economic crisis and recession and has continued to grow at a healthy rate. Since 1996, the

economy has grown 5% – 6% per year. Political instability, poor infrastructure, corruption, insufficient

power supplies, and slow implementation of economic reforms have not slowed down growth.

Economists agree that the country has the potential to achieve a higher growth rate if these roadblocks

are adequately addressed. More than half of GDP is generated through the service sector, but nearly

two-thirds of Bangladeshis are employed in the agriculture sector. The share of agriculture in the labor

force is 45%, in industry 30% and in services 25%. The share of the service sector in GDP is 52.6% while

industry’s share is 28.7% and agriculture’s 18.7% (Independent Review of Bangladesh’s Development

(IRBD), 2012).

The stock market in Bangladesh was characterized by an extreme see-saw motion throughout 2010 and

early 2011. Record numbers in index, turnover, market capitalization and investors were the brighter

aspects of the market until dramatic falls were experienced twice in December 2010, sparking street

protests. The benchmark key index at the DSE nearly doubled within a year, from 4535.53 points in 30

December 2009 to 8290.41 points on the last trading day of 2010. In the last two years many small

investors flocked to the market, lured by the prospect of easy profits. It is estimated that more than 1.3

million new investors entered the capital market in this period and the total stood at 3.3 million by the

end of 2010. After a slight recovery in the last days of 2010, the stock market crumbled in January 2011.

In two days in January the Bangladeshi stock market lost more than 15%, an estimated loss of wealth of

almost $7.5 billion. It was a confluence of factors, including lack of investment opportunities in the real

sector, excessive supply of money and proliferation of trading facilities that encouraged inexperienced

small investors to take a wild ride in the stock market. The banks’ reckless participation in the market

exacerbated the situation. The central bank paid very little attention to the growing bubble until it was

too late. Of particular concern is the central bank’s lack of oversight with regard to the sector’s

participation in the stock market. It allowed banks to leave their traditional business and did not enforce

rules limiting stock market participation by them.

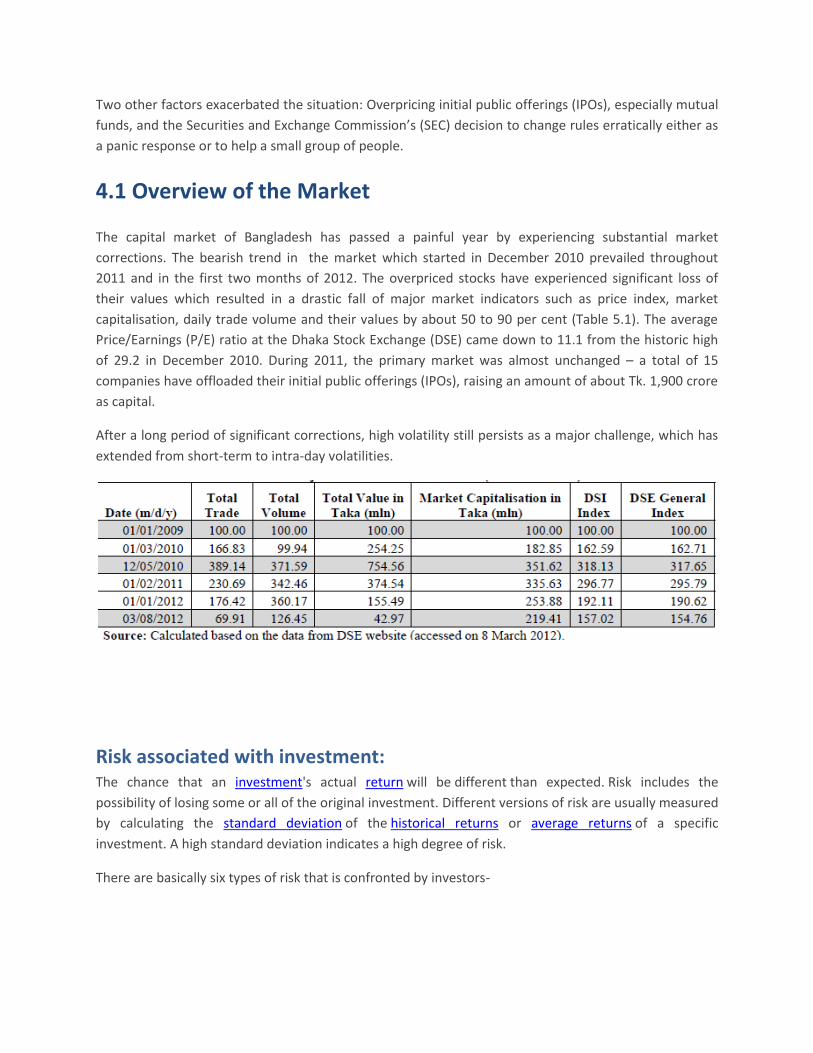

Two other factors exacerbated the situation: Overpricing initial public offerings (IPOs), especially mutual

funds, and the Securities and Exchange Commission’s (SEC) decision to change rules erratically either as

a panic response or to help a small group of people.

4.1 Overview of the Market

The capital market of Bangladesh has passed a painful year by experiencing substantial market

corrections. The bearish trend in the market which started in December 2010 prevailed throughout

2011 and in the first two months of 2012. The overpriced stocks have experienced significant loss of

their values which resulted in a drastic fall of major market indicators such as price index, market

capitalisation, daily trade volume and their values by about 50 to 90 per cent (Table 5.1). The average

Price/Earnings (P/E) ratio at the Dhaka Stock Exchange (DSE) came down to 11.1 from the historic high

of 29.2 in December 2010. During 2011, the primary market was almost unchanged – a total of 15

companies have offloaded their initial public offerings (IPOs), raising an amount of about Tk. 1,900 crore

as capital.

After a long period of significant corrections, high volatility still persists as a major challenge, which has

extended from short-term to intra-day volatilities.

Risk associated with investment: The chance that an investment's actual return will be different than expected. Risk includes the

possibility of losing some or all of the original investment. Different versions of risk are usually measured

by calculating the standard deviation of the historical returns or average returns of a specific

investment. A high standard deviation indicates a high degree of risk.

There are basically six types of risk that is confronted by investors-

I. Market risk: The risk to investors whose investment horizon is shorter than the maturity of a

financial asset that the market price of that asset will decline, resulting in capital loss when

sold. Sometimes referred to as interest rate risk.

II. Reinvestment risk: The risk to investors whose investment horizon exceeds the maturity of

financial asset that they will be forced to place earning from that maturity asset into a lower

yielding investment because interest rate has fallen.

III. Default risk: The probability that a borrower will fail to meet one or more promised principal

or interest payments on a loan or security.

IV. Inflation risk: The risk that increases in the general price level will reduce the purchasing

power of earnings from a loan, security or other investment.

V. Currency risk: The risk that adverse movements in the price of one national currency against

another currency will reduce the net rate of return from a foreign investment. Some time

referred to as exchange rate risk.

VI. Political risk: The probability that changes in government laws or regulations will reduce an

investor’s expected return from an investment.

Risk associated with financial instrument we have selected for the portfolio

We have selected following financial instrument for developing portfolio and their associated risk is

discussed below-

I. Purchasing of raw land: Risk associated with purchasing of raw land is uncertainty of prices and

low liquidity.

II. Certificate of deposit/Fixed deposit: It is the deposit of money for a specific length of time and

it pays the higher interest rate than the saving account and penalty is imposed for early

withdrawal of money from the account. Risk associated with this instrument is the liquidity risk

because penalty is imposed for withdrawal of money before the maturity period.

III. Common Stock: It is the perfect equity instrument. It represents residual ownership of a

corporation. They get residual amounts after paying to creditors and preferred shareholders.

Investors return depends on the performance of the company and the decision of the board of

directors.

Common stockholders have some rights over the preferred shareholders.

They have the right to vote at the shareholders meeting on fundamental policies of the

corporation. Fundamental policy of the firm may be the wage policy or merger and acquisition

policy, financial policy.

They have the right to elect the member of the board of directors.

To evaluate the performance of the management of the firm.

When dividends are declared by the board of directors they have the right to receive the

dividend.

They have the right to sell their shares in the secondary market without consent of the

corporation.

They are entitled to share assets in the event of the liquidation of the firm but they have the last

claim on assets after creditors and the preferred shareholders.

They have right to purchase proportionate amount of future stock offerings. These are called right

shares. There is uncertainty for unexpected price change.

4.2 Measures Taken

Since the collapse of the market in December 2010, three types of measures were announced

with a view to stabilise the market:

a) direct injection of funds and making legal provisions for attracting more funds for increasing

transactions in the secondary market (e.g. establishment of the Bangladesh Fund and the Market

Stabilization Fund with special provisions for investment by banks and other financial institutions);

b) amendment of existing rules and regulations and introduction of new rules (e.g. amendment of book

building rule, de-mutualisation of Stock Exchanges, Financial Reporting Act, and mandatory holding of

certain percentage of shares by sponsor directors and board of directors); and

c) measures against fraudulent practices and illegal activities identified till now. These measures are to

be enforced over short, medium and long-terms.

It is found that short-term measures are mostly related to direct injection of fund and facilitation of

institutional funds in the secondary market. Most of those measures were implemented as per the

timeline except for the establishment of two mutual funds (one is partially established). The medium

and long-term measures, on the other hand, are related to strengthening the legal base of the market

and taking measures against illegal activities.

Although a number of these measures have been initiated (e.g. investor advisory service, corporate

governance guideline, etc.), implementation of those and other measures would be difficult within the

stipulated timeline (i.e. March 2012). In general, the government took a ‘market-based’ approach to

address the crisis which came under criticism on a number of accounts.

It has been argued in various studies and reports (CPD 2011a; CPD 2011b; Probe Committee for the

Stock Market, 2011; Moazzem and Rahman 2012) that the crisis in the market is mainly originated in

institutional failure, particularly of the regulatory body (SEC), which failed to monitor, operate and take

actions against fraudulent and malpractices. Hence, stabilisation of the market and restoration of

investors’ confidence through the initiated and other proposed steps are likely to be a far-fetched goal

to achieve.

4.3 Examination of Market Anomalies

The nature and extent of market anomalies have often been overlooked by the regulators and

other stakeholders due to lack of proper investigation. Centre for Policy Dialogue has studied two key

issues, one concerning the primary market (i.e. use of fund raised through IPOs), and the other on the

secondary market (i.e. transaction behaviour of institutional investors vis-à-vis that of retail investors).

In case of raising fund through issuance of IPOs, a number of anomalies were identified. These include

diversion of fund to activities not stipulated in the prospectus, concealment of important and sensitive

information in company’s annual reports and cash flow statements, lack of satisfactory explanation

provided by the auditor in the audit reports, failure of DSE and SEC to identify those anomalies before

giving approval, and failure of the company board to address those issues. Most of these irregularities

are in violation of various regulations put in place by the Commission itself.

The transaction behaviour of institutional investors was examined by analysing day-to-day transaction of

a number of sample Beneficiary Owner (BO) accounts during 2009 and 2010.

Institutional investors were found to behave like noise traders in the above mentioned periods which

was reflected in the estimated withdrawal-deposit ratio of transactions in the sample BO accounts.

This kind of noise trading by the institutional investors has significantly contributed to overheating of

the market in 2009 and 2010. Transaction behaviour of institutional investors trading with brokerage

houses was even noisier (withdrawal-deposit ratio was 2.14), compared to those trading with merchant

banks (1.34). This raises the question regarding the nature of relationship maintained by institutional

investors with the brokerage houses. On the other hand, transaction behaviour of investors maintaining

omnibus accounts was found to be noisier (2.12) than those who traded through BO accounts (1.5)

Transaction through omnibus accounts appears to take place due to absence of accountability and

transparency.

4.4 Future Directions of the Market

The current state of the market is close to what was prevailing before the pre-boom phase in early 2009

(Table 5.1). The primary market is stable and eight new companies are in the process of issuance of

IPOs. However, the secondary market is still in a volatile state.

Portfolio investment has registered a 22 per cent rise in FY2012. Under the current state of market, it is

hard to find reasons for stocks to be overpriced under rational expectation. In other words, ongoing

measures should not have any significant contribution in any artificial rise of the market. Nevertheless

market is still at a dysfunctional state.

The General index at the end of September 2012 stands higher at 4544.41 compared to 4446.87 at the

end of August 2012. The monthly turnover increased significantly from BDT 5727.66 crore in August

2012 to BDT 18761.51 crore in September 2012. Thus at this stage a careful selection of stocks of low

risk companies and IPOs of stable well known companies are the way to go forwards for investors

5. Constructing the portfolio

We are investing BDT 1,000000 on Real Estate. Following are the justification behind the investment.

Calculation of Asset Appreciation from Real Estate Investment

Here is the value of land in Gazipur district for last few decades. The growth rate of land per year is also

shown.

Year Value of land (B.D.T/ katha) Value increase per Year

1990 826446.65

2000 2809917.35 24%

2010 10247933.88

26%

2011 18512396.69

81%

Growth Rate Calculation

Weight Assigned to growth rate:

50% of 2011 growth rate which is 81%

30% of 2010 growth rate which is 26%

20% of 2009 growth rate which is 24%

Calculated growth rate = (50%*81%+30%*26%+20%*24%) = 45%

Base value of the purchased land = 550,000 B.D.T

Value of Land after 5 years = 550,000 x (1+45%) 5 = 3,218,437 BDT

Percentage increase from the base value = (3,218,437 - 550,000)/ 550,000 = 544%

We choose to purchase the land on 60 installments in 5-year time rather purchasing it directly with the

amount of BDT 550000. Rest of the money will be kept in Mutual trust bank for 5 years which gives an

interest rate of 12.5% on monthly schemes.

In this case, we have to pay BDT 700000 in total within the 5-year time period. The initial down payment

(or the first installment) is 20% of the total amount which is (700000*20%) = 140000.

Rest of the money (700000-140000) = 560000 BDT will be handed over in next 59 equal installments.

Each installment is equal to (560000/59) = 9491.5 BDT per month, that is 113898 BDT per year.

At the beginning, we have BDT 1,000000 to invest on Real Estate. Now after the initial down payment of

BDT 140000, we are left with BDT 860000 which will be kept in Mutual Trust Bank that provides a 12.5%

interest on monthly schemes.

Money kept on Bank: BDT 860000

Year 1 BDT

Year 2 BDT

Year 3 BDT

Year 4 BDT

Year 5 BDT

At the end of 5 years (BDT)

Installments to be paid for the real

estate 113898 113898 113898 113898 113898

Interest from Bank on current amount 107500 106700 105800.4502 104788.2 103649.45

Additional amount

withdrawn from bank to pay the installment 6398 7198 8098 9110 10249

Net bank balance

853602 846404 838306 829196 818947

Now, value of land after 5 years: 3,218,437 BDT

Net Bank Balance after 5 years: 818947 BDT

Total Return from investment on real estate: 4037384 BDT

Percent increase on initial investment = 4037384/1000000 * 100% = 403.73%

Since the investment on real state can give an expected return of 403.73% , so we are investing half of

our amount on real state. It’s also a secured investment.

We are investing BDT 600000 on Real Estate. Following are the justification

behind the investment.

These are DSE 20 companies with the highest expected rate of return. We choose 3 companies

considering their beta and standard deviation. The 3 companies we choose are

Bata

Beta value: 124.10, St D: 37.53%

BAT

Beta value: 69.90, St D: 57.54%

Monno Ceramic

Beta value: 175.50, St D: 32.56%

The portfolio return is 33%

Portfolio Standard deviation 0.2067

As the above mentioned 3 companies have the least standard deviation they will be least risky

to invest. Also liquidation of money is available in this investment. Unlike other portfolio

investments we can liquidity the assets in case of emergency.

AVERAGE ANNUAL RETURNS.D. C.V. Beta

ACI 55.33% 105.97% 1.92 63.50

APEX Tannary 49.82% 49.59% 0.995307093 225.25 portfolio sd 0.206704122

BATA 40.72% 37.53% 0.92173755 124.10 0.2

BAT 57.74% 48.06% 0.832302499 69.90 0.2 portfolio return 33%

BD LAMP 31.91% 35.15% 1.101589784 485.25

BEX PHARMA 22.22% 48.08% 2.163636596 43.90

DHAKA BANK -18.18% 43.85% -2.411867334 370.25

GQ BALL PEN 32.10% 32.22% 1.00379314 53.20

IBBL -9.31% 48.96% -5.258359452 4,529.25

MEGHNA CEMENT 24.78% 67.87% 2.739164249 250.50

MONNO CERAMICS 32.56% 21.57% 0.662578093 175.50 0.4

NBL -19.00% 46.37% -2.440280738 739.00

PRIME -7.27% 56.87% -7.824468947 386.00

SINGER BD 48.34% 73.00% 1.51011549 742.25

SOUTHEAST BANK -0.78% 35.96% -45.84638843 353.75

SQUARE TEXTILE 17.45% 27.36% 1.56814379 64.10

SQUARE PHARMA 8.38% 28.63% 3.416340168 2,283.25

UTTARA BANK -21.38% 52.87% -2.472646187 1,813.00

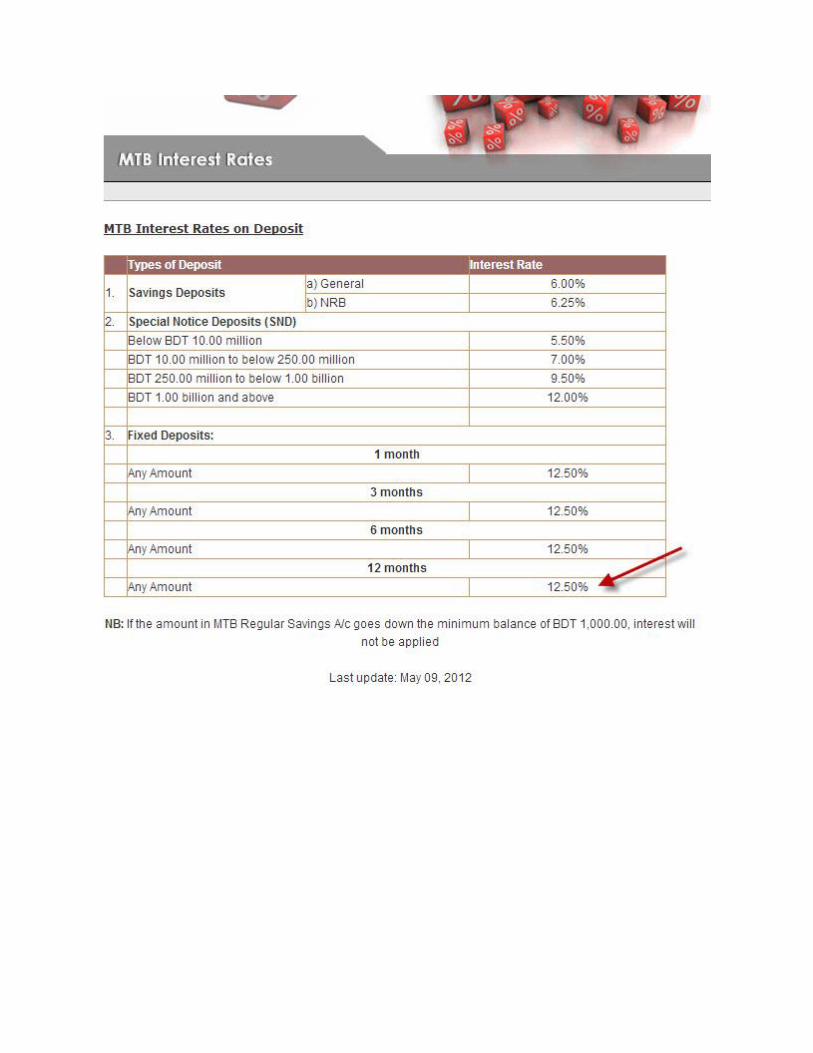

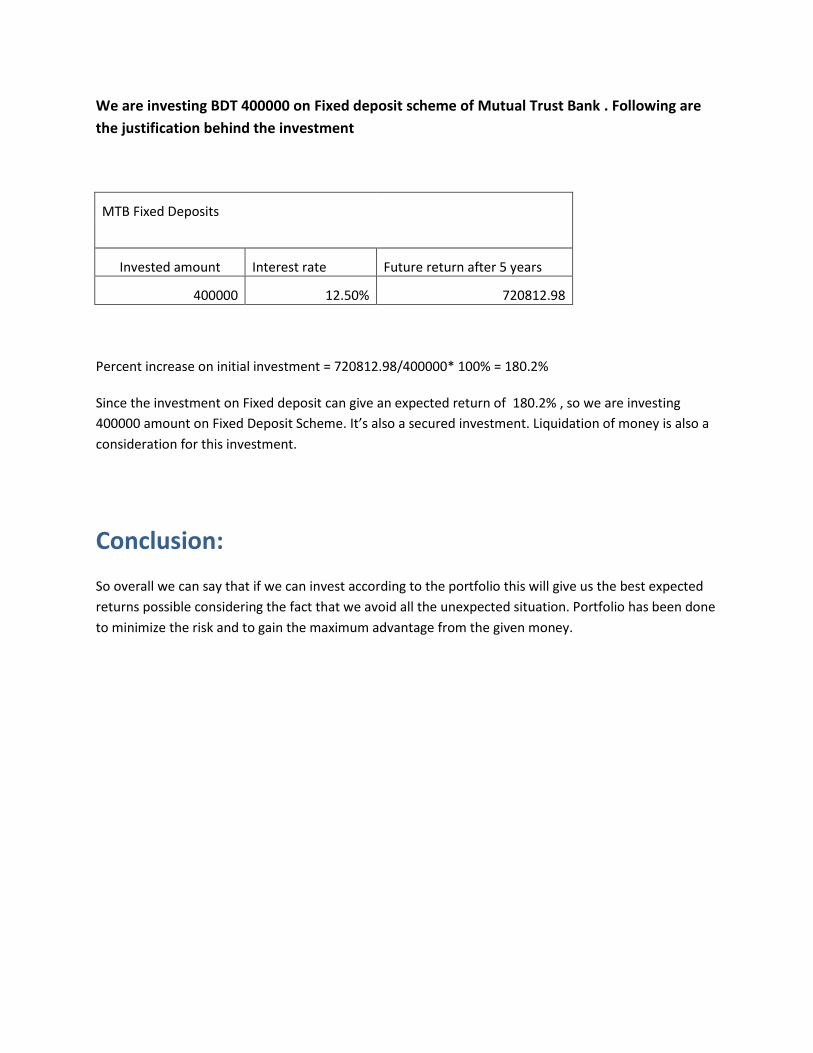

We are investing BDT 400000 on Fixed deposit scheme of Mutual Trust Bank . Following are

the justification behind the investment

MTB Fixed Deposits

Invested amount Interest rate Future return after 5 years

400000 12.50% 720812.98

Percent increase on initial investment = 720812.98/400000* 100% = 180.2%

Since the investment on Fixed deposit can give an expected return of 180.2% , so we are investing

400000 amount on Fixed Deposit Scheme. It’s also a secured investment. Liquidation of money is also a

consideration for this investment.

Conclusion:

So overall we can say that if we can invest according to the portfolio this will give us the best expected

returns possible considering the fact that we avoid all the unexpected situation. Portfolio has been done

to minimize the risk and to gain the maximum advantage from the given money.

Reference

http://www.newdhakacity.com.bd/offers.php

http://www.mutualtrustbank.com/info_interest_rate.php

http://www.dsebd.org/dse20_share.php

Appendix