s&p global ratings aviation seminar

TRANSCRIPT

S&P Global Ratings Aviation Seminar

May 20, 2019Copyright © 2018 by S&P Global. All rights reserved.

Copyright © 2019 by S&P Global. All rights reserved.

U.S. Airlines

S&P Global Ratings Aviation Seminar

May 20, 2019

Philip Baggaley, CFA

Managing Director

Corporate Ratings

Copyright © 2019 by S&P Global.

All rights reserved.

Audience Poll

Private & Confidential 3

To what extent do you believe that the North American airline industry is, or is

not, fundamentally less risky than in the past?

A. Consolidation and better management have made the industry fundamentally more stable

and less cyclical

B. The industry is clearly more profitable, but whether it is less cyclical remains to be seen

C. The revenue picture has improved, but costs are increasing and upside is limited

D. Industry fundamentals have not really changed, although market conditions are currently

favorable

Private & Confidential 4

Jet Fuel Prices

Source: US Energy Information Administration. Jet fuel is Refiner Price to End User, expressed as $/barrel

$0

$20

$40

$60

$80

$100

$120

$140

Crude Oil and Jet Fuel Prices ($/bbl)

WTI Crude Jet Fuel

Revenues / ASM Correlates With Jet Fuel Prices

Private & Confidential 5

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

14.0

14.5

15.0

15.5

16.0

16.5

2013 2014 2015 2016 2017 2018

TRASM (cents) vs. Jet Fuel ($/gal.)

TRASM (left scale) Jet Fuel (right scale)

American + Delta + Southwest + United vs. U.S. Jet Fuel Prices

Source: Company Financial Reports, Energy Information Administration

Jet Fuel Prices: Recent and Forecast

Private & Confidential 6

$1.40

$1.50

$1.60

$1.70

$1.80

$1.90

$2.00

$2.10

$2.20

$2.30

$2.40

1Q2017

2Q2017

3Q2017

4Q2017

1Q2018

2Q2018

3Q2018

4Q2018

1Q2019

2Q2019F

3Q2019F

4Q2019F

1Q2020F

2Q2020F

3Q2020F

4Q2020F

Quarterly Average U.S. Jet Fuel Prices

Energy Information Administration Forecast, May 2019

S&P’s Corporate Criteria Framework

Private & Confidential 7

Assessments as of May 9, 2019

minimal modest intermediate significant aggressive highly leveraged

sati

sfa

cto

ry

excellent

strong

satisfactory

fair

weak

vu

lnera

ble

vulnerable

- investment grade * not exposed to high risk countries

Financial Risk

Bu

sin

ess R

isk o

f A

irlin

es*

fair

weak

Co

mp

etitive

Positio

n

Cash Flow / Leverage Analysis Ratios1 -- Standard Volatility

-- Core ratios---- Supplementary coverage

ratios---- Supplementary payback ratios--

FFO / debt (%)

Debt / EBITDA (x)

FFO / cashinterest (x)

EBITDA / interest (x)

OCF / debt (%)

FOCF / debt (%)

DCF / debt (%)

Minimal > 60 < 1.5 > 13 > 15 > 50 > 40 > 25

Modest 45 - 60 1.5 - 2 9 - 13 10 - 15 35 - 50 25 - 40 15 - 25

Intermediate 30 - 45 2 - 3 6 - 9 6 - 10 25 - 35 15 - 25 10 - 15

Significant 20 - 30 3 - 4 4 - 6 3 - 6 15 - 25 10 - 15 5 -10

Aggressive 12 - 20 4 - 5 2 - 4 2 - 3 10 - 15 5 - 10 2 - 5

Highly Leveraged < 12 > 5 < 2 < 2 < 10 < 5 < 2

Determining The Financial Risk Profile: Ratio Guidelines

(1) Standard & Poor’s adjusted amounts.Primary Core Ratio

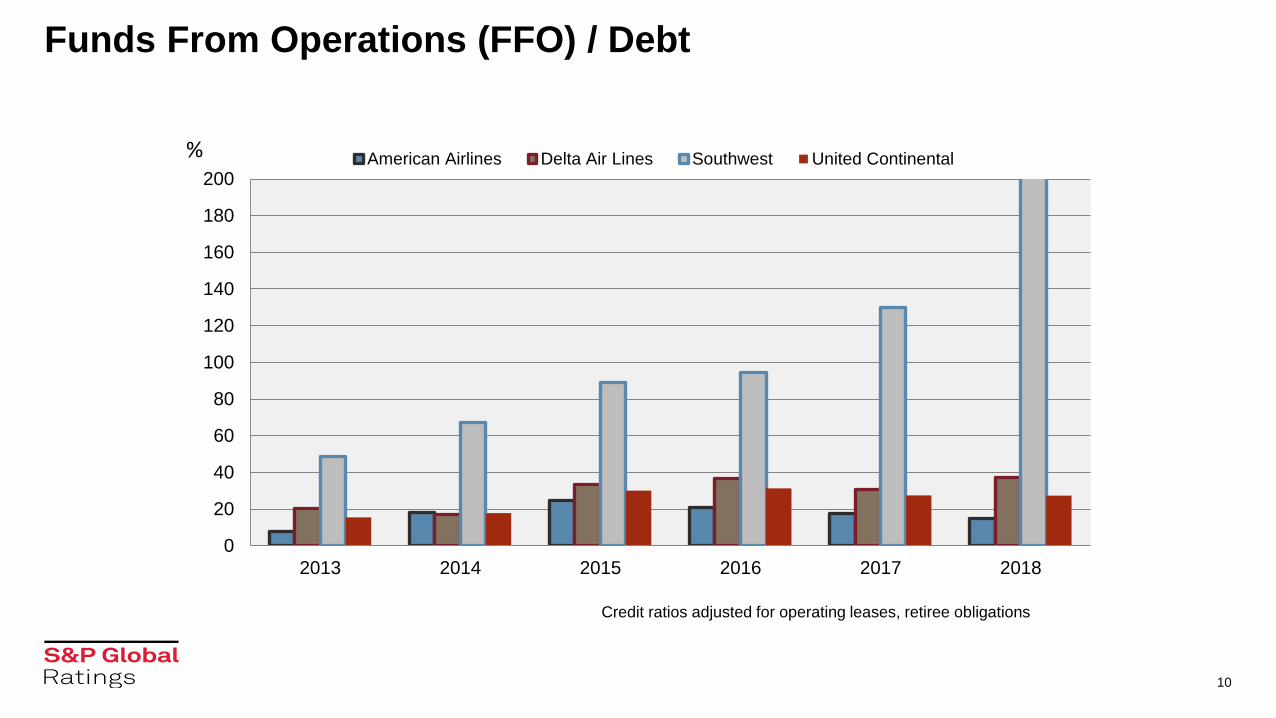

Funds From Operations (FFO) / Debt

0

20

40

60

80

100

120

140

160

180

200

2013 2014 2015 2016 2017 2018

American Airlines Delta Air Lines Southwest United Continental

10

Credit ratios adjusted for operating leases, retiree obligations

%

Funds From Operations (FFO) / Debt

0

5

10

15

20

25

30

35

40

2013 2014 2015 2016 2017 2018

American Airlines Delta Air Lines United Continental

11

Credit ratios adjusted for operating leases, retiree obligations

%

Free Operating Cash Flow (FOCF) / Debt

-50

0

50

100

150

200

2013 2014 2015 2016 2017 2018

American Airlines Delta Air Lines Southwest United Continental

12

Credit ratios adjusted for operating leases, retiree obligations

%

Free Operating Cash Flow (FOCF) / Debt

-10

-5

0

5

10

15

20

25

30

35

40

2013 2014 2015 2016 2017 2018

American Airlines Delta Air Lines United Continental

13

Credit ratios adjusted for operating leases, retiree obligations

%

Audience Poll – Our Take

Private & Confidential 14

To what extent do you believe that the North American airline industry is, or is

not, fundamentally less risky than in the past?

A. Consolidation and better management have made the industry fundamentally more stable

and less cyclical

B. The industry is clearly more profitable, but whether it is less cyclical remains to be seen

C. The revenue picture has improved, but costs are increasing and upside is limited

D. Industry fundamentals have not really changed, although market conditions are currently

favorable

When The Cycle Turns…

Private & Confidential 15

Cushions to the downside

• Oil (and jet fuel) prices would likely fall sharply

• Most airlines can dial back capacity to some extent

• Ample liquidity and generous (or absent) covenants

Some areas of concern

• Labor costs have been rising and continue upwards

• U.S. airlines have spent billions on share buybacks, foregoing debt reduction

• Vulnerability to non-economic shocks: terrorism, war, epidemic disease, cyberattacks

How Well Prepared Are U.S. Airlines?

Enhanced Equipment Trust Certificates

Private & Confidential 16

Cape Town Convention

• Avianca Brasil, continued

S&P Counterparty Criteria change

• Previously limited EETC rating to liquidity provider rating in almost all cases

• New criteria allow for greater rating elevation above “threshold rating” of liquidity

provider upgrades

Non-US$ EETC

• Risk of $ weakening Eroding collateral value

Current Developments

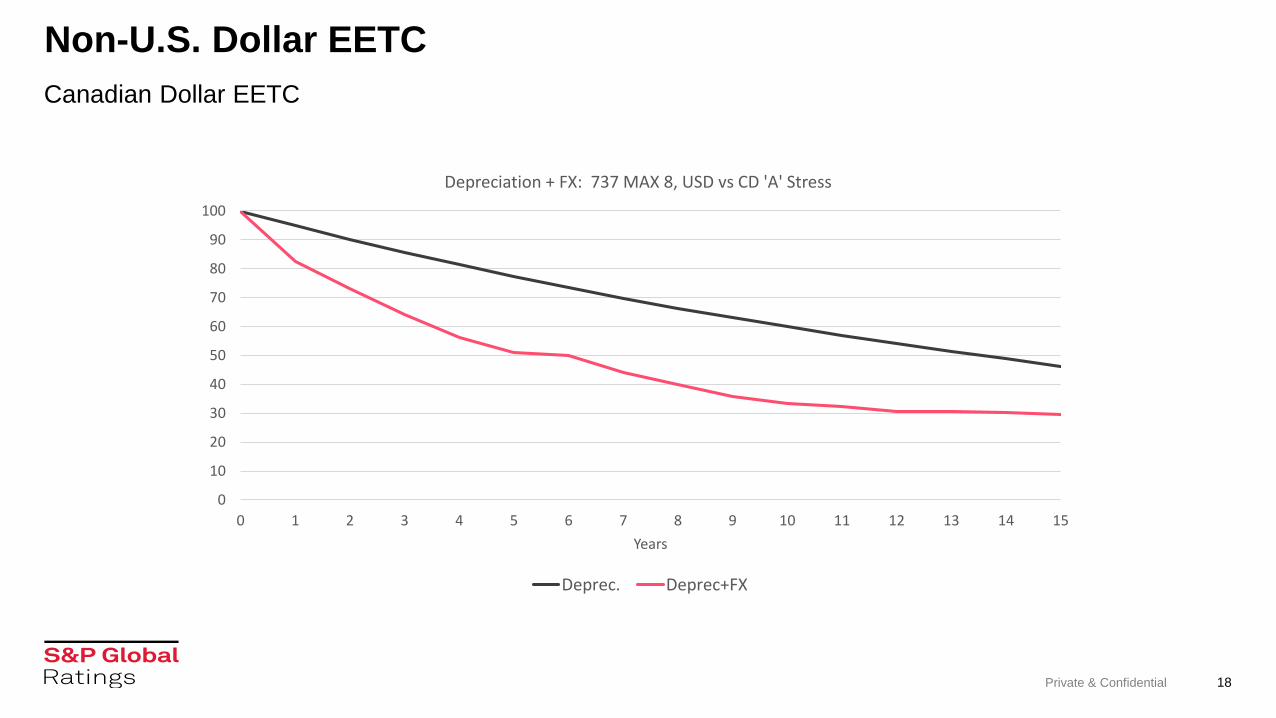

Non-U.S. Dollar EETC

Private & Confidential 17

Canadian Dollar EETC

0

10

20

30

40

50

60

70

0 4 8

12

16

20

24

28

32

36

40

44

48

52

56

60

64

68

72

76

80

84

88

92

96

10

0

10

4

10

8

11

2

11

6

12

0

12

4

12

8

13

2

13

6

14

0

14

4

14

8

15

2

15

6

16

0

16

4

16

8

17

2

17

6

18

0

Months

FX Stresses (%)

AAA AA A BBB BB B

Non-U.S. Dollar EETC

Private & Confidential 18

Canadian Dollar EETC

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Years

Depreciation + FX: 737 MAX 8, USD vs CD 'A' Stress

Deprec. Deprec+FX

Enhanced Equipment Trust Certificates

Private & Confidential 19

Bullet EETCs

• Overcollateralize to the level needed at maturity

• Increased rejection risk?

What About the 737 MAX?

• Is there a material, permanent diminution in collateral ‘quality’?

• Do the appraisers lower their base values materially?

• Might prolonged problems change an airline’s interest in keeping it?

Current Developments, continued

Canadian Airlines

S&P Global Ratings Aviation SeminarMay 20, 2019

Alessio Di Francesco, CFA

Associate Director

Corporate Ratings

Copyright © 2019 by S&P Global.

All rights reserved.

21

Air Canada vs WestJet

Credit Rating – May 20, 2019 BB+/Stable BBB-/Watch Neg

Revenue C$18.1 billion C$4.7 billion

S&P Adj. EBITDA margin 17.9% 16.8%

Available Seat Miles (ASM) 110.9 million 32.9 million

Revenue per ASM 16.3 cents 14.4 cents

CASM (excluding fuel) – CAD 11.2 cents 10.1 cents

Load Factor 83.3% 83.8%

Fleet size (as of Mar. 31, 2019) 401 182

737 MAX fleet 24 13

737 MAX % of 2019 capacity ~8% ~10%

Average age of fleet 14.8 years 8.1 years

Average Stage Lengths (miles) 1,738 860

S&P Adj. Debt-to-EBITDA 2.0x 1.7x

S&P Adj. FFO-to-Debt 42.8% 52.3%

S&P Adj. FOCF-to-Debt 16.3% 3.2%

2018 unless stated otherwise

• WestJet’s rating is one notch higher than Air Canada driven by the company’s historically stronger credit measures and profitability

• S&P placed WestJet’s ratings on Watch Negative following the recently announced acquisition by Onex.

• We believe the transaction is likely to result in more aggressive financial policies and weaker credit measures when compared to Air Canada.

• S&P upgraded Air Canada by one notch in March

• AC’s credit risk has reduced significantly from lower debt levels and improved profitability.

• We expect this trend to continue with Adj. FFO/Debt of 50%-55% in 2019 and 55%-60% in 2020

• Compared to WestJet, we believe Air Canada benefits from stronger market share, diversification, and scale.

Private & Confidential 22

Air Canada Has Closed The Profitability Gap With WestJet

0%

5%

10%

15%

20%

25%

30%

35%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

06A 07A 08A 09A 10A 11A 12A 13A 14A 15A 16A 17A 18A* Q1/19LTM*

S&P

Ad

j. E

BIT

DA

Mar

gin

(%)

S&P

Ad

j. E

BIT

DA

(C$

mil

lio

ns)

EBITDA - WJA EBITDA - AC EBITDA Margin - AC EBITDA Margin - WJA

*includes IFRS 16 impact

Private & Confidential 23

Air Canada Credit Measures Have Strengthened Considerably

0%

10%

20%

30%

40%

50%

60%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

06A 07A 08A 09A 10A 11A 12A 13A 14A 15A 16A 17A 18A* Q1/19LTM*

S&P

Ad

j. F

FO-t

o-D

eb

t (%

)

S&P

Ad

j. D

eb

t-to

-EB

ITD

A (x

)

Debt/EBITDA - WJA Debt/EBITDA - AC FFO/Debt - AC FFO/Debt - WJA

WJA BBB- BBB- BBB- BBB- BBB- BBB- BBB- BBB- BBB- BBB- BBB- BBB- BBB- BBB-

AC B B B CCC+ B- B- B- B- B B+ BB- BB- BB BB+

*includes IFRS 16 impact

24

Update On The 737 MAX Grounding

On March 13, 2019, Canada joined many other countries in grounding the 737 MAX aircraft.

Air Canada and WestJet are removing the 737 MAX from their schedules until at least July 31, 2019 and

suspended their public guidance for the year.

WestJet should be more adversely impacted as the 737 MAX represents a larger portion of its fleet

• WestJet has 13 737 MAX aircraft that represent ~10% of 2019 capacity

• Air Canada has 24 737 MAX aircraft that represent ~8% of 2019 capacity

We anticipate the grounding to have a moderate impact on 2019 results in the form of lower capacity

and fuel efficiency as well as higher costs related to flight cancelations and reschedules.

Steps to mitigate operating disruptions include:

• Redeploy underutilized aircraft from less profitable routes to fill capacity gaps

• Extend aircraft leases to meet demand in the busy summer months

• Defer certain cabin upgrades and maintenance

If regulators sign off on a return to service, we expect it would take several weeks before Air Canada and

WestJet could get all MAX’s back in the air and that their return to service should be gradual. We also

believe it could take time for passengers to regain confidence in the aircraft

IMO 2020

The Tsunami Approaches

S&P Global Platts Analytics

Lenny Rodriguez

Team Lead

Arbitrage & Latin American Oil

S&P Global Ratings Aviation Seminar

May 20, 2019

Copyright © 2019 by S&P Global.

All rights reserved.

Global bunker fuel specs will tighten in 2020 forcing

widespread disruptive changes within and beyond the oil

industry

• Around 3.5 MMB/D of high sulfur residual fuel oil will be affected

• Most will change to low sulfur blends/gasoil

• Scrubbers increasing but not enough for 2020; LNG limited to small fraction

• Spec change will occur despite counterarguments, compliance concerns

• Multiple forces will push toward higher compliance

• Non-compliance and waivers will likely have only a small impact on HS bunker demand

• Impact will drive price, trade, operations

• Refining industry will be severely stretched; trade patterns will change

• Light product prices spike, HSFO prices fall, LS-HS spreads widen

• Freight costs for all goods increase; ripple effects in other industries

Up to $1 trillion transfer from consumers & HS crude producers to refiners & LS producers**

** 5 year total, net oil price impact only

Global bunker fuel spec changes in 2020 will force ~3 MMB/D of

HSFO to switch to LSFO and distillates

0

1

2

3

4

5

6

7

8

2010 2015 2020 2025 2030

High Sulfur Residual Fuel Oil

Distillates

Dist for Blending

LS HFO

0.5%S

LSFO

and

Blends

Global Bunker Demand, MMB/D

LNG

There are multiple options for compliance with the new IMO

bunker fuels specification

● Purchase/use compliant fuels

• 0.5%S bunkers for open seas and 0.1%S in ECAs

● Invest in scrubbers

• Scrubber penetration to date somewhat limited

• Installations to date mostly ferries/cruise ships in ECAs, but spreading to larger ships

• Known/planned scrubbers will be in 2200 vessels by 1/1/2020 = 500 MB/D of Fuel Oil

● Invest in Dual Fuel engines capable of burning LNG or liquid fuels

• LNG bunker use rare (except for LNG carriers) due lack of delivery infrastructure

● Seek waivers or disregard new standard (non-compliance)

Multiple refining factors will be needed to meet 2020 demand

including higher crude runs leading to higher crude prices

Maximizing distillate

Increase distillates yield (+1% yield)

Increase HCU and Coker Utilization

Increase Crude throughput (more distillates, lightends and fuel oil)

Maximize LSFO Production

Segregation of low sulfur crudes

Maximize residue desulfurization capacity

Displace LS VGO and LSLR from FCCU runs for Fuel Oil Blend Stock

Minimize HSFO/HSLR Production

Increase fuel oil destruction through higher complex capacity utilization (i.e., coking)

Shifting fuel oil pool from viscosity-limited to sulfur-limited

Increase HSFO sales for non-Bunkers use

Decline in Fuel Oil demand due to IMO 2020 will be offset by the significant increase in Gasoil demand

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20

Other Residual Fuel Oil Distillates JK Gasoline Naphtha LPG

MM

B/D

1.491.791.59

1.26

In absence of IMO spec

change, oil demand would

slow down further in 2020

1.79

-0.38

-0.15

1.26

(500)

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Demand Runs

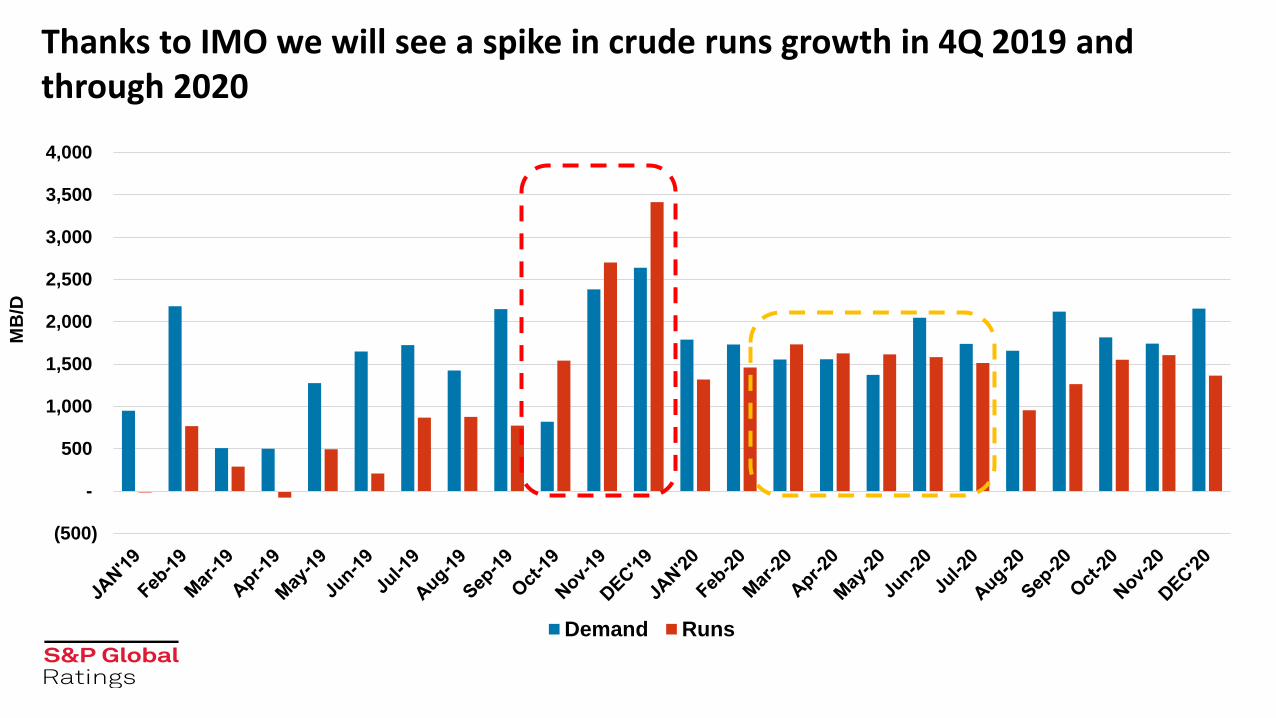

Thanks to IMO we will see a spike in crude runs growth in 4Q 2019 and through 2020

MB

/D

The IMO Tsunami Approaches…

-5

-4

-3

-2

-1

0

1

2

3

4

5

-40

-30

-20

-10

0

10

20

30

40

Jan-19 Apr-19 Jul-19 Oct-19 Jan-20 Apr-20 Jul-20 Oct-20

Th

ou

sa

nd

s

HSFO LS Residuals LS Gasoil for blends MGO

MGO

$/Bbl

HS carriage ban

HSFO arb to Asia

collapses

HSFO

Blends

Diesel vs Brent

HSFO vs Brent

Bunker Demand, MMB/D

Middle distillates ease in 1H19 but then soar late in 2019 and peak

in 1H20 with IMO 2020. Forward curve does not reflect this

5

10

15

20

25

30

35

Jan-18 Jan-19 Jan-20

ARA ULSD vs Dated Brent

ICE Forward Curve - Apr 19 Forecast - Prompt

$/Bbl

(35)

(30)

(25)

(20)

(15)

(10)

(5)

0

2000 2005 2010 2015 2020 2025 2030

0

5

10

15

20

25

30

35

2000 2005 2010 2015 2020 2025 2030

USG NWE Singapore

Diesel

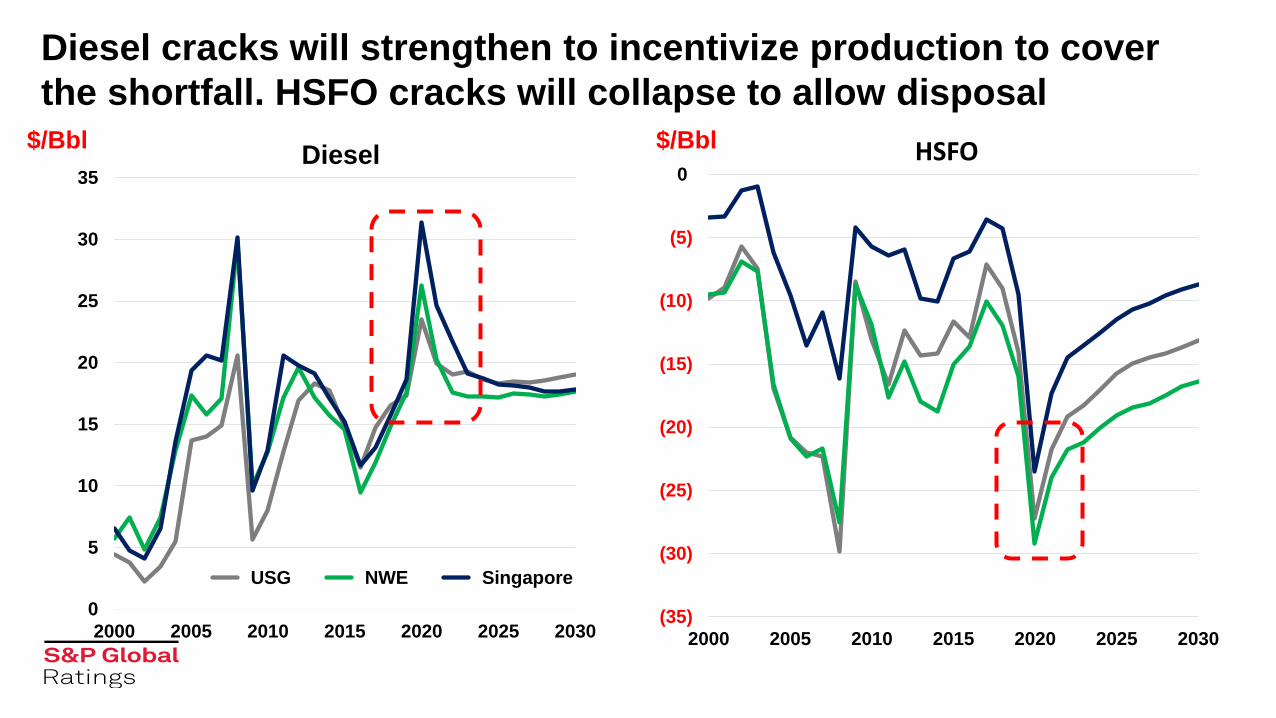

Diesel cracks will strengthen to incentivize production to cover

the shortfall. HSFO cracks will collapse to allow disposal$/Bbl HSFO$/Bbl

0

10

20

30

40

50

60

70

80

90

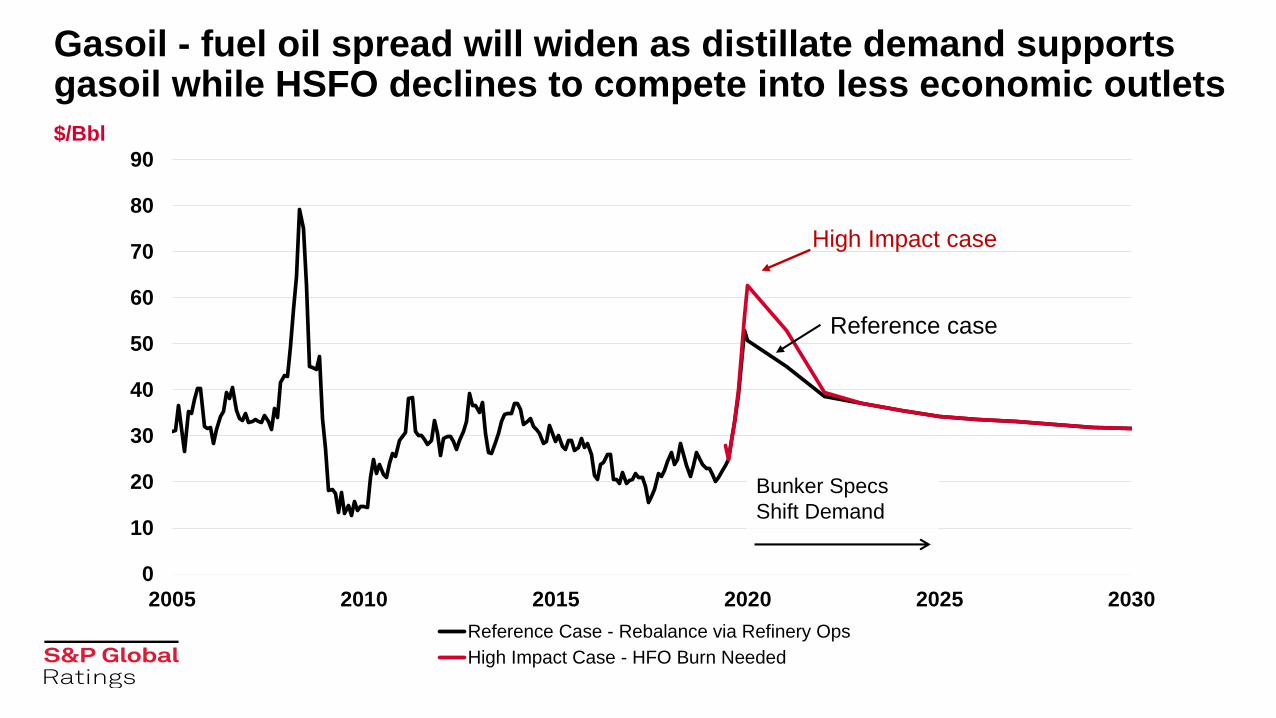

2005 2010 2015 2020 2025 2030

Reference Case - Rebalance via Refinery Ops

High Impact Case - HFO Burn Needed

Bunker Specs

Shift Demand

$/Bbl

Gasoil - fuel oil spread will widen as distillate demand supports gasoil while HSFO declines to compete into less economic outlets

Reference case

High Impact case

0

5

10

15

20

25

30

35

2000 2005 2010 2015 2020 2025 2030

USG NWE Singapore

Gasoline cracks get some support from IMO 2020 as FCC feed

tightens; jet fuel cracks soar tracking LS diesel $/Bbl Gasoline

0

5

10

15

20

25

30

35

2000 2005 2010 2015 2020 2025 2030

Jet Fuel$/Bbl

-5

0

5

10

15

20

2000 2005 2010 2015 2020 2025 2030 2035 2040

NWE Urals Cracking Singapore Dubai Cracking

Singapore Dubai Simple

Cracking

Sour crude

Hydroskimming

Conversion margins will soar with changes in product cracks &

crude differentials before quickly returning to historical trends

Europe and Asia Margins Constant $/Bbl Constant $/Bbl

0

5

10

15

20

25

2000 2005 2010 2015 2020 2025 2030 2035 2040

USG Margins

USG LLS Cracking USG Maya Coking

Cracking

Coking

Freight rates will increase with higher fuel costs, increased tonne miles and tighter availability due to scrappage & floating storage

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

VLCC-WAFR to Asia Suezmax-WAFR toUKC

MR-NWE to USAC

HSFO 0.5% @ +$200/ton0.5% @+$300/ton 0.5% @+$400/ton

Flat rates, $/MT

0

5

10

15

20

25

30

35

40

45

50

2000 2005 2010 2015 2020 2025

WAFR to Asia WAFR to UKC NWE to USAC

Transport Cost, $/Bbl

2019 Global Jet Fuel prices expected to track similar to last year

thru the Fall but supported later by the IMO 2020 diesel pull

30

40

50

60

70

80

90

100

110

120

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

USGC Jet Fuel Price Forecast

2017 2018 2019 2020

$/Bbl

IMO 2020 effectkicks in 4Q19

30

40

50

60

70

80

90

100

110

120

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

Jul-

18

Oct

-18

Jan

-19

Ap

r-1

9

Jul-

19

Oct

-19

Jan

-20

Ap

r-2

0

Jul-

20

Oct

-20

USGC Jet Fuel Price Buildup

USGC Jet Crack LLS

$/Bbl

Global jet fuel demand growth to stay healthy in 2020 despite IMO

impact

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2018 2019 2020

ME/Africa Europe/FSU Latin America China Asia (ex. China) US/CanadaMB/D

175 MB/D190 MB/D

Commercial Aerospace

Outlook

S&P Global Ratings Aviation Seminar

May 20, 2019

Christopher DeNicolo, CFA

Senior Director

Lead Aerospace & Defense Analyst

Copyright © 2019 by S&P Global.

All rights reserved.

737 MAX Grounding: Update

Oct. 29, 2018 Lion Air accident

March 10, 2019 Ethiopian Airlines accident

March 11, 2019 China grounds MAX

March 13, 2019 FAA grounds MAX, Boeing suspends deliveries

April 4, 2019 Preliminary Ethiopian findings

April 5, 2019 Boeing lowers production to 42/month from 52/month

April 29, 2019 FAA stands up global group to review MCAS software update

42

737 MAX Grounding: Boeing Impact

Sufficient liquidity and cushion in rating to survive crisis

• $7.7 billion of cash and $5.1 billion of revolver at March 31, 2019

• Put in temporary $1.5 billion revolver

• Raised $3.5 billion new debt

• Suspended share repo

1Q impact moderate, but worst yet to come as inventories build and other costs mount

Temporary production cut conserves some cash and helps preserve supply chain

China Airbus order, Garuda cancellation likely not start of more lost sales

Long term impacts

• Reputation

• Market Share

• NMA/777X

• Investigations

43

737 MAX Grounding: Supplier Impact

Impact will vary by supplier

Spirit AeroSystems and GE/CFM staying at 52/month

Could help some suppliers who were behind catch up (e.g. castings/forgings, engines)

Likely help from Boeing, tier 1 suppliers for lower tier suppliers

Cost drag as most were already prepared for jump to 57/month

Lower aftermarket provisioning

44

Audience Poll

When do you think Boeing will resume deliveries of the 737 MAX?

A. June 2019

B. September 2019

C. December 2019

D. After December 2019

45

737 MAX Grounding: Things to Watch For

• FAA certification of updated software

• Approval by other global regulatory

agencies

• Boeing resumes deliveries

• Airlines resume flying

• Restored trust of airlines, pilots,

regulators, flying public

• Final outcome of accident

investigations, investigations of

certification process

• Boeing increases production to

57/month

• Order cancellations

46

Source: Boeing website

Middle East/Africa8%

US23%

North and Central America (ex US)

6%

South America3%China

2%Asia (ex China)

23%

Europe15%

Unidentified20%

737 Backlog by Region (March 2019)

Order Cycle Has Peaked

47

Air Traffic Slowing, But Remains Strong

48

Source: IATA

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19

Global Passenger Traffic Growth

YoY Change Historical Average

Long Wait For Popular Aircraft

49

Source: Manufacturers' websites, S&P Global estimates

0 1 2 3 4 5 6 7 8 9

B737

A320

B767

A330

B787

B777

A350

B747

Years Backlog at Planned Near Term Production Rates

Some uptick in airline failures, cancellations, deferrals

Failures

• WOW Air

• Avianca Brasil

• Jet Airways (125 737 MAX, 10 787-9, 5 A330 on order)

• Germania

• Flybmi

• Flybe

Cancellations/deferrals

• Garuda (cancel 49 737 MAX)

• Emirates (cancel 39 A380)

• Etihad (cancel 42 A380, 42 A350)

• American (defer 40 737 MAX, 22 A321neo)

• Air New Zealand (defer 3 A320/A321neo, 2 widebodies)

50

Audience Poll

Where are we in the aircraft delivery cycle?

A. Near peak

B. Past peak

C. Plateauing

D. What cycle?

51

Delivery Increase in 2019 Tempered by MAX Grounding?

52

?

Supply Chain Key Risk to Higher Production

Delays of 737 MAX deliveries last year due to engine, fuselage issues

• Temporary production cut may provide some relief

Continuing delays to A320neo deliveries due to engines

Engine delays due mostly to constraints at casting/forging suppliers

Interiors also causing issues, especially for widebodies

Some suppliers straining to increase production profitably

Pricing pressures are increasing

• Boeing’s “partnering for success” program

• Spirit AeroSystems making suppliers rebid with 15%-35% lower prices

• OEMs need to balance lower costs with disrupting production

53

Boeing Redefining Supplier/OEM Relationship

Trying to capture more life cycle value of aircraft, increase control of development and

production process

Went too far with 787 outsourcing

Vertical integration (e.g. 777X wing, 737 actuators, nacelles, avionics, seats, APUs)

Expanding into aftermarket

• “All about the parts”

• Trying to keep more IP

• Component repair

Suppliers responding by consolidating, repositioning

Winners and losers will become clear on next new aircraft

54

M&A

Airbus bought C-Series (now A220) to expand product line

Boeing pursuing combination with Embraer to get access to engineers, faster development

process

Boeing bought KLX to expand parts distribution business

Supplier consolidation

• UTC bought Rockwell Collins to broaden product line in response to pressures from OEMs, now splitting up

aerospace, commercial business

• Spirit AeroSystems buying Asco to improve diversity, increase defense, fabrication work

• TransDigm bought Esterline

• More likely

55

Boeing Still Evaluating Launch of NMA

Trying to close business case to

produce aircraft airlines want, at a price

they will pay, that is still profitable

Originally ATO this year, launch next

year, and first delivery 2025 to take

advantage of 757/767 replacement cycle

Competition from A321neo at low end

and own 787 at upper end

Choice of engine?

Impact of MAX grounding

• Certification

• Resource constraints

• New narrowbody instead?

56

Source: Boeing Capital Financiers and Investors Conference, April 9, 2019

Other Markets Mostly Weak

Business jet market weak, but seeing signs of life?

• Small and mid-sized demand still weak, but improving

• Large cabin solid

• New models supporting modest production growth

Regional jets

• Some demand for larger jets

• 50-seat replacement?

Helicopters

• Significant impact from lower oil prices, especially for larger helicopters

Aftermarket

• Solid traffic growth should support demand, but uneven due to airline and distributor inventory management

• Airline profitability could drive more refurbishment demand

57

Future Competitors?

Russia and China had first flights of the MC-21 and C919 narrowbodies last year, but first

deliveries still a few years out

Possibly competitors to 737/A320, but questions about performance, reliability, and support

likely to limit customers to home country and allies in developing countries that can’t afford

Western jets

• Chinese government could force local airlines to use C919 instead of buying Airbus or Boeing jets

Russia and China formed joint venture to build larger jet

Mitsubishi Regional Jet repeatedly delayed

58

US Commercial Aerospace Outlook Distribution

59

Source: S&P Global RatingsAs of May 8, 2019

Stable68%

Positive4%

Negative28%

Credit Quality Stable to Somewhat Negative Overall

MAX grounding impact

Supplier earnings and cash flow has not benefited from solid demand the past few years due

to investments to support higher rates and operational problems resulting in some

downgrades or outlook changes

Industry changes likely to put further pressures on supplier credit quality

M&A impact on credit quality

60

Aircraft Leasing

S&P Global Ratings Aviation Seminar

May 20, 2019

Betsy Snyder, CFA

Director

Corporate Ratings

Copyright © 2019 by S&P Global.

All rights reserved.

Boeing Global Forecast 2018-2037

Source: Boeing Commercial Market Outlook

Airbus Global Forecast 2018-2037

Source: Airbus Global Market Forecast

Annual growth forecast at around 5%

Global population growth

Middle class growth with more disposable income

All age segments

Trips per capita in 2017

• U.S.: 1.9

• China: 0.4

• India: 0.1

Estimated 250 million new passengers in 2019

Global Air Traffic Growth Continues Strong And

Above Long-term Trends

Lessor Share Of Global Fleet

Source: Boeing Capital Corp.

Source: Boeing Current Aircraft Finance Market Outlook

Audience Poll

Private & Confidential 66

Do you believe there is too much liquidity available for aircraft

lessors?

A. Yes, this risks an asset bubble and eventual value declines

B. Yes, somewhat, but do not see this as a major risk currently

C. No, the amount is consistent with strong demand for air travel

D. Hard to generalize; it depends on particular sources of capital and

who they are lending to

Private & Confidential 67

Lessor Sources of Financing

Source: Boeing Current Aircraft Finance Market Outlook

Private & Confidential 68

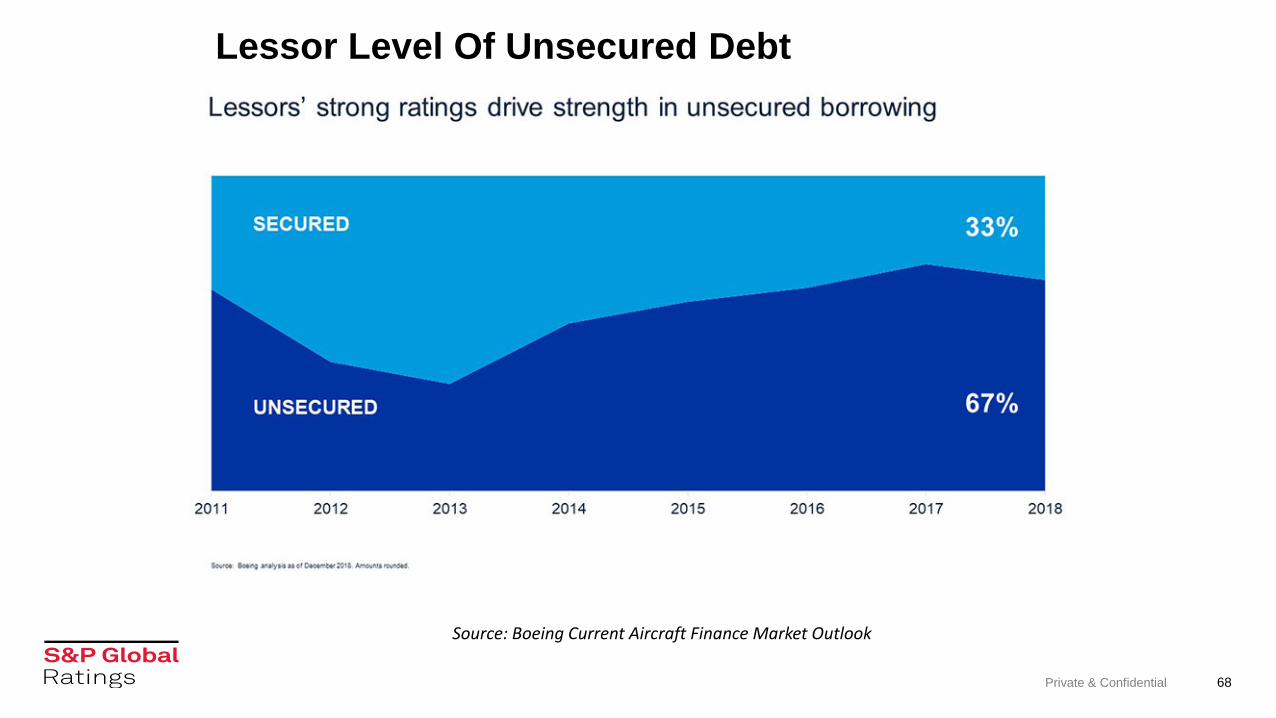

Lessor Level Of Unsecured Debt

Source: Boeing Current Aircraft Finance Market Outlook

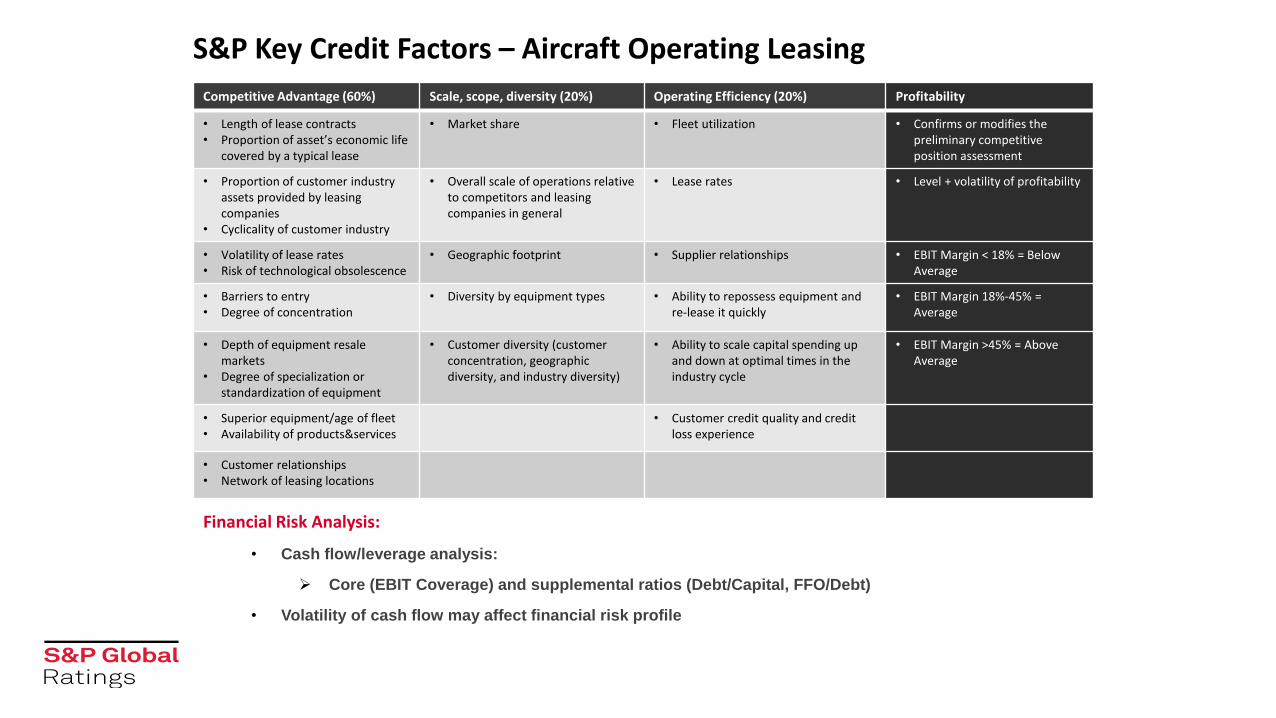

S&P Key Credit Factors – Aircraft Operating Leasing

Financial Risk Analysis:

• Cash flow/leverage analysis:

Core (EBIT Coverage) and supplemental ratios (Debt/Capital, FFO/Debt)

• Volatility of cash flow may affect financial risk profile

Competitive Advantage (60%) Scale, scope, diversity (20%) Operating Efficiency (20%) Profitability

• Length of lease contracts• Proportion of asset’s economic life

covered by a typical lease

• Market share • Fleet utilization • Confirms or modifies the preliminary competitive position assessment

• Proportion of customer industry assets provided by leasing companies

• Cyclicality of customer industry

• Overall scale of operations relative to competitors and leasing companies in general

• Lease rates • Level + volatility of profitability

• Volatility of lease rates• Risk of technological obsolescence

• Geographic footprint • Supplier relationships • EBIT Margin < 18% = BelowAverage

• Barriers to entry• Degree of concentration

• Diversity by equipment types • Ability to repossess equipment and re-lease it quickly

• EBIT Margin 18%-45% = Average

• Depth of equipment resale markets

• Degree of specialization or standardization of equipment

• Customer diversity (customer concentration, geographic diversity, and industry diversity)

• Ability to scale capital spending up and down at optimal times in the industry cycle

• EBIT Margin >45% = Above Average

• Superior equipment/age of fleet• Availability of products&services

• Customer credit quality and credit loss experience

• Customer relationships• Network of leasing locations

S&P’s Operating Leasing Criteria Framework

Private & Confidential 70

Competitive Advantage

Scale, Scope & Diversity

Operating Efficiency

Profitability: EBIT Margin,

Volatility

Core: Volatility adjusted

EBIT/Interest

Supplemental: Debt/Capital

FFO/Debt

Aircraft Lessors Issuer Credit Ratings

Business Risk Profile

Financial Risk Profile

Minimal Modest Intermediate Significant Aggressive Highly Leveraged

Excellent

Strong

Satisfactory

BOC Aviation Ltd. (A-)*

Air Lease Corp. (BBB)

Aviation Capital Group Corp. (A-)*

SMBC Aviation Capital Ltd. (A-)*

AerCap Holdings N.V. (BBB-)

Aircastle Ltd. (BBB-)

Avolon Holdings Ltd. (BBB-)

Dubai Aerospace Enterprise Ltd. (BB+)

Fair Fly Leasing Ltd. (BB-)

Weak Avation PLC (B+)Voyager (Intrepid)

(B+)

Vulnerable

As of 5/17/2019 * Incorporates three notches of parent support

Sector Outlook:

• Global air traffic growth continues strong and above long-term trends

• Demand remains strong for narrowbody (single-aisle) planes, somewhat softer for widebody

(twin-aisle)

• Oil price decline from several years ago has narrowed lease rate premium for fuel efficient

new technology planes, but demand remains strong for them

• Lessors have so far managed repossessions well

• Consolidation, aircraft portfolio sales

Credit Outlook:

• Relatively stable credit metrics forecast; all rating outlooks positive or stable

• Rising interest rates should not present a problem, so long as they are not sudden and

unexpected

• Potential Chinese tariffs on Boeing aircraft

• Potential impact of Boeing 737 MAX grounding

• Ample liquidity has driven up values and driven down lease rates; some risk of disruption

when new entrants face a downturn with limited staff and experience

Aircraft Lessors

Aircraft ABS

S&P Global Ratings Aviation Seminar

May 20, 2019

Belinda Ghetti

Analytical Leader

Structured Finance / Non-Traditional

Kate Scanlin

Senior Director

Structured Finance / Non- Traditional

2019 Themes

Observations in new issuance transactions

Considerations with maintenance cash flows

Appraisal valuation differences

Airline-owned vs. airline-leased aircraft economic life

Performance of existing book

Impact of recent credit events

74

Copyright © 2019 by Standard & Poor’s Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse

engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of Standard & Poor’s Financial Services LLC or

its affiliates (collectively, S&P). The Content shall not be used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders,

employees or agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or

omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is

provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF

MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL

BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any

direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits

and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P’s opinions,

analyses and rating acknowledgment decisions (described below) are not recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the

suitability of any security. S&P assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill,

judgment and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not act as a fiduciary or an

investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable, S&P does not perform an audit and undertakes no duty of due

diligence or independent verification of any information it receives.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P reserves the right to

assign, withdraw or suspend such acknowledgement at any time and in its sole discretion. S&P Parties disclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of

an acknowledgment as well as any liability for any damage alleged to have been suffered on account thereof.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of

S&P may have information that is not available to other S&P business units. S&P has established policies and procedures to maintain the confidentiality of certain non-public information received

in connection with each analytical process.

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P reserves the right to disseminate its opinions and

analyses. S&P's public ratings and analyses are made available on its Web sites, www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com

(subscription), and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available at

www.standardandpoors.com/usratingsfees.

Australia

Standard & Poor's (Australia) Pty. Ltd. holds Australian financial services license number 337565 under the Corporations Act 2001. Standard & Poor’s credit ratings and related research are not

intended for and must not be distributed to any person in Australia other than a wholesale client (as defined in Chapter 7 of the Corporations Act).

STANDARD & POOR’S, S&P and RATINGSDIRECT are registered trademarks of Standard & Poor’s Financial Services LLC.

75