san francisco market overview - f.datasrvr.com

TRANSCRIPT

San Francisco Market OverviewFourth Quarter 2018

U.S. Market

Comparisons

Cushman & Wakefield

0 2 4 6 8 10 12

1945-48

1949-53

1954-57

1958-60

1961-69

1970-73

1975-80

1980-81

1982-90

1991-01

2001-07

2009-18

Years

9.8 Years –2nd longest

10.1 Years - longest

8.8 Years – 3rd longest

It’s tracking to become the longest U.S. economic expansion

Cushman & Wakefield

Office Market Comparison – Vacancy Rate and Average Asking Rent – Q4 2018 San Francisco has the lowest major market vacancy rate and highest asking rent

Source: Cushman & Wakefield; PRELIMINARY STATS

Seattle

8.0% / $34.68

San Francisco

6.4% / $75.57

Silicon Valley

10.3% / $54.12

Austin

10.6% / $36.26

Boston

9.7% / $36.97

NYC (Manhattan)

9.2% / $72.28

Washington, DC

14.1% / $54.34

Portland

11.8% / $29.85

United States

13.2% / $31.54

Chicago

18.5% / $29.97

Denver

15.2% / $28.21

Los Angeles

13.9% / $39.75Phoenix

15.6% / $25.83

Salt Lake City

12.4% / $24.30

Atlanta

16.2% / $26.64San Diego

14.2% / $36.84

Oakland (CBD)

7.9% / $55.22

Dallas/Fort Worth

18.6% / $26.58

Charlotte

7.6% / $26.25

Sacramento

9.2% / $22.68

Cushman & Wakefield

Economic / Demographic Comparison – Select MarketsCost of living (housing) is the key issue for the Bay Area

City Cost of Living Index % Millennials Avg Hourly Wage Educational AttainmentOverall Avg Office

Asking Rent

Silicon Valley 173.0 21.9% $43.01 50.1% $54.12

San Francisco 172.8 22.0% $39.01 48.5% $75.57

Oakland 172.8 22.0% $39.01 48.5% $55.22*

Seattle 137.3 22.8% $37.26 42.0% $34.68

Los Angeles 128.8 22.7% $29.10 33.5% $39.75

San Diego 128.4 24.3% $29.43 37.4% $36.84

New York City 119.7 21.3% $32.25 39.0% $72.28

Portland 113.4 21.3% $28.13 38.9% $29.85

Austin 114.7 24.5% $28.94 42.8% $36.26

Denver 112.7 22.4% $30.01 42.5% $28.21

Dallas-Fort Worth 111.7 21.3% $27.21 33.9% $26.58

Sacramento 110.0 21.1% $27.75 32.6% $22.68

Salt Lake City 109.2 23.2% $26.89 33.0% $24.30

Phoenix 93.8 20.9% $26.86 30.8% $25.83

U.S. 100 20.7% $26.84 31.3% $31.54

Cost of Living Index – Moody’s metro level; U.S. = 100

Millennial Population (Ages 20 to 34) – Moody’s

Hourly Wage – U.S. Bureau of Labor Statistics

Educational Attainment – Moody’s; Population with a Bachelor’s Degree or Higher

Overall Office Asking Rent – Cushman & Wakefield (Preliminary) Fourth Quarter 2018; *Oakland Rent is Central Business District

Cushman & Wakefield

NorCal– Solid Economic FundamentalsJob Growth in Major Markets

Healthy job growth levels across

the major MSAs including San

Francisco-Oakland-San Mateo,

San Jose and Sacramento.

Majority of job growth in San

Francisco has been within the

office-using sector.

Sacramento office-using sector

year-over-year in negative

territory though forecast to move

back into the black over the next

year.

Key Takeaways

102,640 101,490

87,160

67,710

60,610

52,892

47,76045,400

39,800 38,91036,400 35,780 34,820

29,860

12,970

1.1%

2.8%

2.9%

1.1%

3.0%

1.5%

1.8%1.9%

3.6%

1.5%

1.3%

2.5%

1.2%

0.6%

1.3%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

0

20,000

40,000

60,000

80,000

100,000

120,000

Ne

w Y

ork

Da

llas

Ho

usto

n

Los A

ng

ele

s

Se

attle

Wash

ingto

n,

DC

Atla

nta

Sa

n F

ran

cis

co

Sa

n J

ose

Mia

mi

Bo

sto

n

De

nve

r

Ph

ilade

lph

ia

Ch

ica

go

Sa

cra

me

nto

Non Office-Using Office-Using % Growth YOY

Source: Moody’s/BLS; Metropolitan Statistical Area level data

Cushman & Wakefield

Office Jobs versus Total Jobs

Source: Moody’s/BLS; All markets are MSA level except metropolitan division (MD) where noted

Of all the major U.S. markets,

San Francisco and San Jose

have the largest percentage of

office to total jobs.

NYC has, by far, the most office

jobs of any market.

Key Takeaways

39.4%

32.2%30.7% 30.1%

28.7% 28.5% 28.2% 27.6% 27.0%26.1% 25.6% 25.4%

23.9% 23.3% 23.3% 22.8%

19.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

Percentage Private Sector Office Jobs to Total Jobs Total Office Jobs (millions)

Cushman & Wakefield

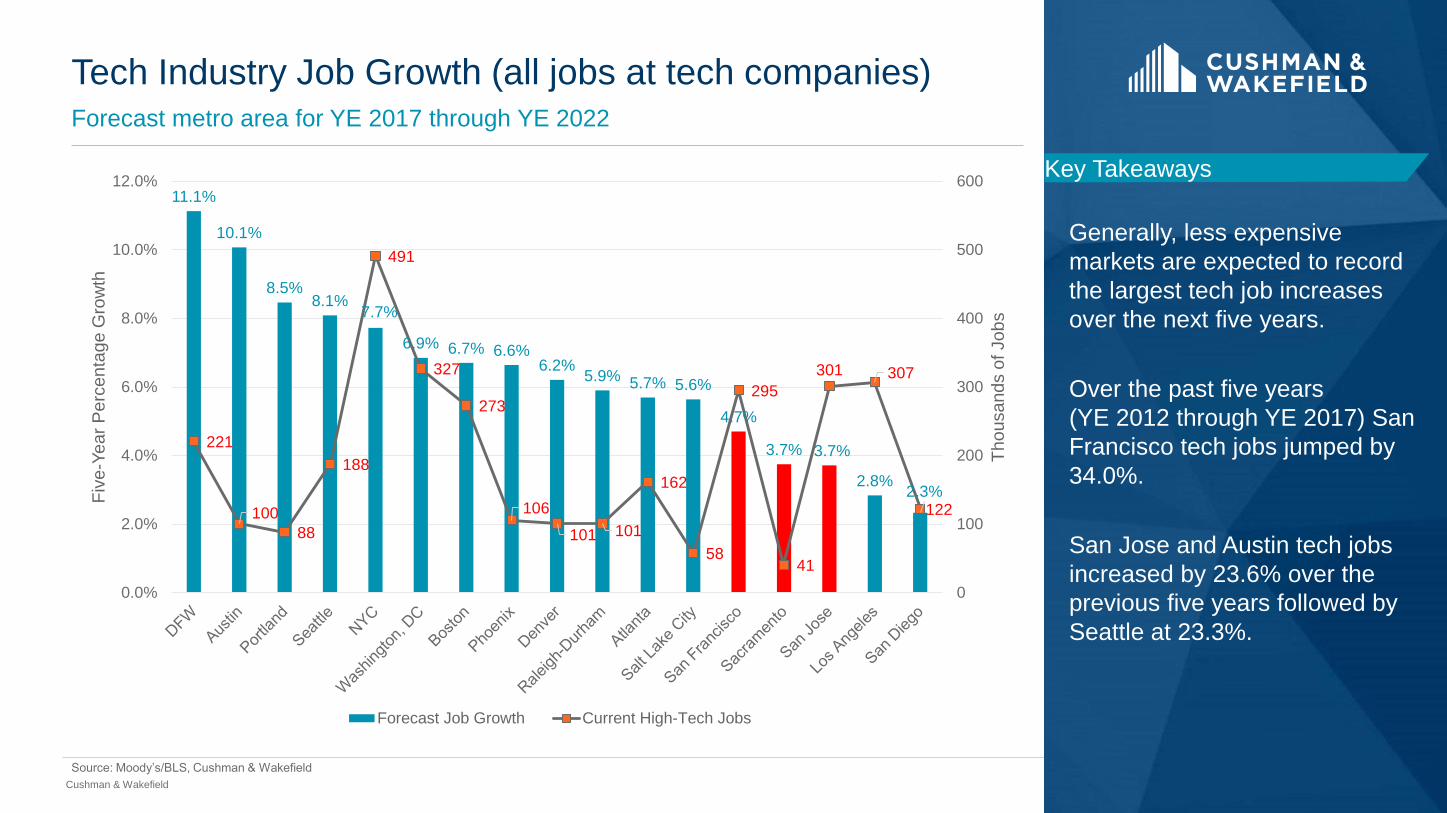

Tech Industry Job Growth (all jobs at tech companies)Forecast metro area for YE 2017 through YE 2022

Source: Moody’s/BLS, Cushman & Wakefield

Generally, less expensive

markets are expected to record

the largest tech job increases

over the next five years.

Over the past five years

(YE 2012 through YE 2017) San

Francisco tech jobs jumped by

34.0%.

San Jose and Austin tech jobs

increased by 23.6% over the

previous five years followed by

Seattle at 23.3%.

Key Takeaways11.1%

10.1%

8.5%8.1%

7.7%

6.9% 6.7% 6.6%6.2%

5.9% 5.7% 5.6%

4.7%

3.7% 3.7%

2.8%2.3%

221

100

88

188

491

327

273

106

101 101

162

58

295

41

301 307

122

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

100

200

300

400

500

600

Fiv

e-Y

ea

r P

erc

en

tag

e G

row

th

Tho

usands o

f Job

s

Forecast Job Growth Current High-Tech Jobs

San Francisco

Cushman & Wakefield

2013 2018

WHERE HAVE WE BEEN?

CITYWIDE OVERALL ASKING RENTS VS VACANCY RATES

SAN FRANCISCO

41% INCREASE IN

RENTAL RATE

340 BPS

DECLINE IN VACANCY

WHERE ARE WE NOW?

FULL SERVICE

ASKING RENTCHANGE/YEAR VACANCY RATE CHANGE/YEAR

Q4 13 $53.46 9.8%

Q4 14 $60.87 +13.9% 7.4% -240 BPS

Q4 15 $68.14 +11.9% 5.9% -150 BPS

Q4 16 $69.77 +2.4% 8.0% +210 BPS

Q4 17 $71.02 +1.8% 8.6% +60 BPS

Q4 18 $75.57 +6.4% 6.4% -220 BPS

BPS = Basis Points

Q4 2013 OVERALL

INVENTORY – 73,919,488 SF Q4 2018 OVERALL

INVENTORY – 82,280,598 SF

Cushman & Wakefield

2013 2018

WHERE HAVE WE BEEN?

CBD CLASS A DIRECT ASKING RENTS VS VACANCY RATES

SAN FRANCISCO

42% INCREASE IN

RENTAL RATE

260 BPS

DECLINE IN VACANCY

WHERE ARE WE NOW?

FULL SERVICE

ASKING RENTCHANGE/YEAR VACANCY RATE CHANGE/YEAR

Q4 13 $57.98 8.0%

Q4 14 $65.34 +12.7% 7.7% -30 BPS

Q4 15 $72.96 +11.7% 6.1% -160 BPS

Q4 16 $74.13 +1.6% 7.2% +110 BPS

Q4 17 $76.05 +2.6% 8.0% +80 BPS

Q4 18 $82.12 +8.0% 5.4% -260 BPS

BPS = Basis Points

Q4 2013 CBD CLASS A

INVENTORY – 39,888,644 SF Q4 2018 CBD CLASS A

INVENTORY – 44,538,857 SF

Cushman & Wakefield

San Francisco Citywide Overall Asking Rent vs NASDAQAs NASDAQ goes so goes the San Francisco real estate market; close eye on the financial markets in first half of 2019

0.00

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

7,000.00

8,000.00

9,000.00

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

Q1

19

93

Q3

19

93

Q1

19

94

Q3

19

94

Q1

19

95

Q3

19

95

Q1

19

96

Q3

19

96

Q1

19

97

Q3

19

97

Q1

19

98

Q3

19

98

Q1

19

99

Q3

19

99

Q1

20

00

Q3

20

00

Q1

20

01

Q3

20

01

Q1

20

02

Q3

20

02

Q1

20

03

Q3

20

03

Q1

20

04

Q3

20

04

Q1

20

05

Q3

20

05

Q1

20

06

Q3

20

06

Q1

20

07

Q3

20

07

Q1

20

08

Q3

20

08

Q1

20

09

Q3

20

09

Q1

20

10

Q3

20

10

Q1

20

11

Q3

20

11

Q1

20

12

Q3

20

12

Q1

20

13

Q3

20

13

Q1

20

14

Q3

20

14

Q1

20

15

Q3

20

15

Q1

20

16

Q3

20

16

Q1

20

17

Q3

20

17

Q1

20

18

Q3

20

18

NA

SD

AQ

Qu

art

erly C

lose

SF

Cityw

ide O

ve

rall

Askin

g R

ent

SF Overall Asking Rent NASDAQ

2 Quarter Lag

3 Quarter Lag

Source: NASDAQ, Cushman & Wakefield

Cushman & Wakefield

San Francisco Citywide Overall Asking Rent vs VC Spending• Not tracking as closely as in the past; wild swings in major late-stage funding rounds

• For full-year 2018, capital invested reached a record $24.9B with 1,214 deals (previous peak of $18.0B in 2000).

• Major VC deals in Q4 2018 included Instacart ($871M), Lime ($335M), Coinbase ($300M) and Plaid ($250M) – all late stage rounds.

$0.00

$1,000.00

$2,000.00

$3,000.00

$4,000.00

$5,000.00

$6,000.00

$7,000.00

$8,000.00

$9,000.00

$10,000.00

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Q3 2

011

Q4 2

011

Q1 2

012

Q2 2

012

Q3 2

012

Q4 2

012

Q1 2

013

Q2 2

013

Q3 2

013

Q4 2

013

Q1 2

014

Q2 2

014

Q3 2

014

Q4 2

014

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Q1 2

016

Q2 2

016

Q3 2

016

Q4 2

016

Q1 2

017

Q2 2

017

Q3 2

017

Q4 2

017

Q1 2

018

Q2 2

018

Q3 2

018

Q4 2

018

SF

VC

Investm

ent (b

illio

ns)

SF

Cityw

ide O

vera

ll A

skin

g R

ent

San Francisco Overall Asking Rent San Francisco VC Investment (Billions)

Source: PitchBook, Cushman & Wakefield

Cushman & Wakefield

San Francisco Overall Asking Rent vs (Pre to Early Stage) VC Spending• Juul with a $1.235B round in Q3 pushes 2018 to a record level within the early stage category ($7.1B for the year)

• By industry, biotech and financial software drove the San Francisco market during the year

$0.00

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

$3,000.00

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Q3 2

011

Q4 2

011

Q1 2

012

Q2 2

012

Q3 2

012

Q4 2

012

Q1 2

013

Q2 2

013

Q3 2

013

Q4 2

013

Q1 2

014

Q2 2

014

Q3 2

014

Q4 2

014

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Q1 2

016

Q2 2

016

Q3 2

016

Q4 2

016

Q1 2

017

Q2 2

017

Q3 2

017

Q4 2

017

Q1 2

018

Q2 2

018

Q3 2

018

Q4 2

018

SF

VC

Investm

ent (b

illio

ns)

SF

Cityw

ide O

vera

ll A

skin

g R

ent

San Francisco Overall Asking Rent San Francisco VC Investment (Billions)

Source: PitchBook, Cushman & Wakefield

Cushman & Wakefield

Likely IPOs in 2019The year of the mega-deals?

Source: PitchBook, Cushman & Wakefield

Public markets have seen only 6 VC-backed exits

over $10B since 2007 though 5 of the 7 San

Francisco companies listed here have valuations

above that figure

But public markets have been struggling in late 2018

and early 2019; nevertheless many companies are

expected to push through during this volatile period

(as opposed to total downturn)

Heavily weighted to San Francisco-based companies

Company Valuation Primary Industry Year Founded Employees

Uber $72.0B Automotive 2009 17,000

Airbnb $31.0B Hotel/Leisure 2008 4,000

Stripe $20.3B Financial Software 2010 1,300

Lyft $15.1B Automotive 2007 3,000

Pinterest $12.3B Social Content 2008 1,500

Slack $7.1B Communications 2009 1,000

Postmates $1.1B Social/Platform 2011 680

50 San Francisco-based VC-backed companies

currently with $1B+ valuation (unicorns)

Cushman & Wakefield

San FranciscoProp C Commercial Rent Tax for Childcare and Early Education (June 2018)

What is it?

A commercial rent tax approved on June 5, 2018; expected to bring in $146 million a year with 85 percent designated for childcare and educations and 15 percent for general city

purposes.

This is an additional tax on “individuals and businesses that receive income from the lease or sublease of commercial space, primarily offices” with annual gross receipts greater

than $1 million.

In addition to the existing gross receipts tax (which ranges from 0.285 percent to 0.3 percent) this measure will impose a new tax of:

1% on the amounts a business receives from the lease of warehouse space in the City; and

3.5% on the amounts a business receives from the lease of other commercial spaces in the City.

“Effectively, this measure would increase the tax rate for commercial rent income to 3.785 percent or 3.8 percent for most types of commercial space.”

Proposition C exempts commercial landlords with less than $1 million in gross receipts, along with rents for nonprofit, government, arts, industrial, and non-formula retail uses,

among other state exemptions.

Impact:

Cost of doing business in SF just became even more expensive

Landlord cost to own commercial RE in SF increased

Tenant rent will go up.

NNN leases more attractive to Landlords

Bifurcates rent from expenses (LLs may claim only rent should be subject to gross receipts)

Pushes costs onto tenants

When does it go into effect?

January 1, 2019 NOTE: Prop C can be amended or repealed by the Board of Supervisors by ordinance without going back to voters.

Source: City of San Francisco, Spur, Cushman & Wakefield

Cushman & Wakefield

San FranciscoProp C Gross Receipts Tax for Homelessness Services (November 2018)

What is it?

A business tax approved on November 6, 2018

Increases gross receipts tax on a sliding scale for businesses with over $50M in gross receipts OR

Certain businesses with administrative offices in San Francisco, at least $1 billion in gross receipts and at least 1,000 employees nationwide would be required to pay an annual

homelessness administrative office tax (rather than the gross receipts tax) at a rate of 1.5 percent of payroll expenses.

Expected to bring in $300 million a year with 50 percent to permanent housing, 25 percent to mental health services, 15 percent to homelessness prevention and 10 percent to short-

term shelters.

Impact:

Cost of doing business in SF will become even more expensive

Preliminary count of businesses affected: 174 businesses occupying 25.6 MSF (31% of San Francisco inventory) with the average size of 147,000 SF

When does it go into effect?

Funds will be collected beginning January 1, 2020 but frozen due to legal dispute regarding whether simple majority or two-thirds majority threshold was required for passage.

Source: City of San Francisco, Ballotpedia, Spur, Cushman & Wakefield

Business Activity Set Tax Increase

Retail/Wholesale Trade 0.175%

Biotech, Clean Tech, Information, Food Services, Manufacturing, Transport 0.500%

Accomodations, Utilities, Arts/Entertainment/Recreation 0.425%

Admininstrative/Support, Private Education, Health Services 0.690%

Construction 0.475%

Financial Services, Insurance, Professional/Scientific/Technical Services 0.600%

Real Estate/Rental/Leasing Services 0.325%

18Cushman & Wakefield

San Francisco – Prop M8.9 MSF in the pending phase (large cap projects over 50,000 SF); potential to add 1.6 MSF to the allocation from prior residential and hotel conversions.

PROJECT DEVELOPER STATUS ENTITLEMENT (SF) REMAINING (SF)

ALLOCATION FOR 2017

(occurred 17 October 2016)

875,000 1,318,869

633 Folsom St Swig Entitled (90,102) 1,228,767

ALLOCATION FOR 2018

(Occurred 17 October 2017)

875,000 2,103,767

552 Berry St/1 De Haro St SKS Entitled (86,301) 2,017,466

ALLOCATION FOR 2019

(Occurred 17 October 2018)

875,000 2,892,466

*Pier 70 Forest City Pending (1,810,000)

*Mission Rock Giants Pending (1,300,000)

542-550 Howard St -Transbay F Hines Pending (288,677)

2 Henry Adams RREEF Pending (245,697)

1800 Mission St - Armory AJ Capital Pending (119,599)

610-698 Brannan St/Flower Mart - Central SoMa Kilroy Pending (2,030,560)

598 Brannan St – Central SoMa Tishman Speyer Pending (922,291)

88 Bluxome Street - Central SoMa TMG/Alexandria Pending (833,040)

725-735 Harrison Street –

Central SoMa

Boston Properties Pending (770,301)

400 2nd St – Central SoMa Cresleigh Pending (421,000)

505 Brannan Street – Central SoMa TMG Pending (165,000)

* Office allocation will be provided automatically on a per-permit basis, at the time of issuance of each building permit.

Availability as of

January 2019

19Cushman & Wakefield

20Cushman & Wakefield

San Francisco Remaining Big Blocks Moving Fast

ADDRESS SUBMARKET TOTAL

BUILDING SQ

FT

AVAILABLE SQ

FT

OCCUPANCY DATE STATUS COMMENTS

50 First Street

(Oceanwide Center)

South Financial 1,050,000 1,050,000 2022 Under Construction Mixed-Use Complex

1455 Market Street Mid-Market 1,026,000 326,000 2020 Built Uber relocating to Mission

Bay

50 Beale Street South Financial 662,000 321,000 2019 Built; Renovation

planned

BlueShield moving out

45 Fremont Street South Financial 596,000 280,000 2019 Built Wells Fargo and others

633 Folsom Street South Financial 269,000 269,000 2020 Built; adding floors and

renovation

Will be delivered vacant

555 Market Street South Financial 281,000 242,000 2020 Built Uber relocating to Mission

Bay

215 Fremont Street South Financial 373,000 187,000 Immediate – Sublease

Five-Year Term

Built Fitbit

Mega block availabilities (150K and larger) through end of decade are sparse; several below have leases pending

21Cushman & Wakefield

1.7 1.8 1.7

0.61.4 1.4

2.31.5

2.3 2.21.5

2.0 1.9

1.51.7

1.1

0.7

1.51.9

2.3

1.8

3.5

1.8

2.0

2.23.0

1.41.5

1.1

1.0

1.5

1.8

1.4

1.9

2.4

1.4

1.4

2.1

2.01.7

1.6

0.7

1.1

1.0

1.4

2.5

2.0

1.6

0.81.3

2.41.9

0.0

2.0

4.0

6.0

8.0

10.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

MS

F

Q1 Q2 Q3 Q4

6.2

8.78.9

6.36.6

4.6

3.4

5.4

6.5

8.5

7.2

9.8

6.3

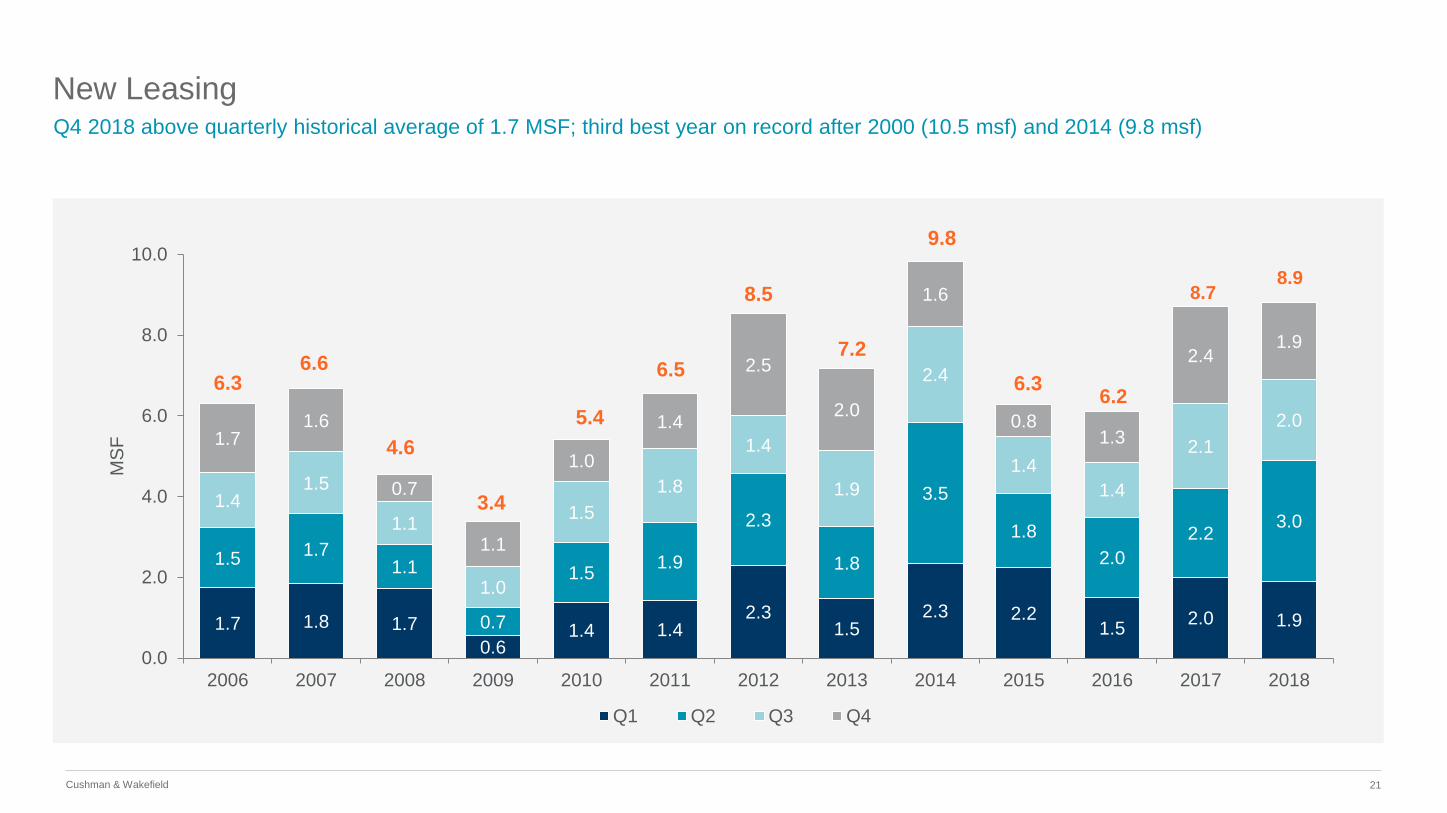

New LeasingQ4 2018 above quarterly historical average of 1.7 MSF; third best year on record after 2000 (10.5 msf) and 2014 (9.8 msf)

22Cushman & Wakefield

1.6 1.6

(1.1)

(2.3)

(0.8)

2.3

0.8

0.4

3.2

0.9 0.6

(0.3)

4.8

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.02006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Net AbsorptionA record-setting year in 2018 for positive absorption with various buildings delivering at 100 percent occupied

23Cushman & Wakefield

Totals are down after strong 2018 leasing but still significant number of tenants in the market121 active tenant requirements totaling 5.2 msf

17%

20%

14%

21%

28%

0% 10% 20% 30%

<10,000 SF

10,000-14,999 SF

15,000-24,999 SF

25,000-49,999 SF

>50,000 SF

Requirements

59.8%

9.2%

6.1%

9.6%

13.0%

0.6% 1.3% 0.5%Software/Tech

FIRE

Legal

Professional Services

Consumer Products/Services

Government/Education

Medical/Health Care

Non-Profit

24Cushman & Wakefield

San Francisco

Market is very tight….

• Much deeper / more sustained expansion compared to the first dot-

com boom with $70.00 / RSF and greater rents for 14 quarters and

counting today vs 5 quarters previously.

• Class A CBD direct rent and Citywide overall rents at all-time highs

- $82.12 / RSF and $75.57 / RSF, respectively.

• 30+ leases signed in 2018 at $90 or higher effective rent - View

space premiums are back!

• Overall vacancy down to 6.4% - minimal big block options.

• Still robust demand – currently tracking 5.2 MSF of tenants in the

market.

• 8.9 MSF of new leasing activity in 2018, third best on record but will

be hard to beat without mega pre-leasing activity in 2019.

• Sublease vacancy = 1.8% or 1.2 MSF total. Good subleases

moving fast.

• San Francisco VC spending is far and away highest in the US.

• VCs sitting on approximately $77B in dry powder and expect much

of that to flow local companies.

….And there are headwinds

• Construction pricing has increased by 25%+ over past 2 years.

• $100+ TI packages increasingly common.

• Limited new supply and rents driving tenants to expand outside of

SF.

• Increasingly difficult / expensive to hire the right talent with office

sector unemployment effectively at 0%.

• Cost of housing, congestion, taxes, homelessness, open drug use.

• Tax increases for child care and education effective 1/1/2019;

business tax to pay for homeless issues effective 1/1/2020.

• Prop M Allocation – less than 3.0 MSF available with 8.9 MSF in

the pending phase.

• Central SoMa passes but timeline of project delivery is long.

• Further tightening of the market expected in the near-term with a

slowdown by 2020.

25Cushman & Wakefield

cushmanwakefield.com

©2018 Cushman & Wakefield. All rights reserved. The material in this presentation

has been prepared solely for information purposes, and is strictly confidential. Any

disclosure, use, copying or circulation of this presentation (or the information

contained within it) is strictly prohibited, unless you have obtained Cushman &

Wakefield’s prior written consent. The views expressed in this presentation are the

views of the author and do not necessarily reflect the views of Cushman &

Wakefield. Neither this presentation nor any part of it shall form the basis of, or be

relied upon in connection with any offer, or act as an inducement to enter into any

contract or commitment whatsoever. NO REPRESENTATION OR WARRANTY IS

GIVEN, EXPRESS OR IMPLIED, AS TO THE ACCURACY OF THE

INFORMATION CONTAINED WITHIN THIS PRESENTATION, AND CUSHMAN &

WAKEFIELD IS UNDER NO OBLIGATION TO SUBSEQUENTLY CORRECT IT

IN THE EVENT OF ERRORS.